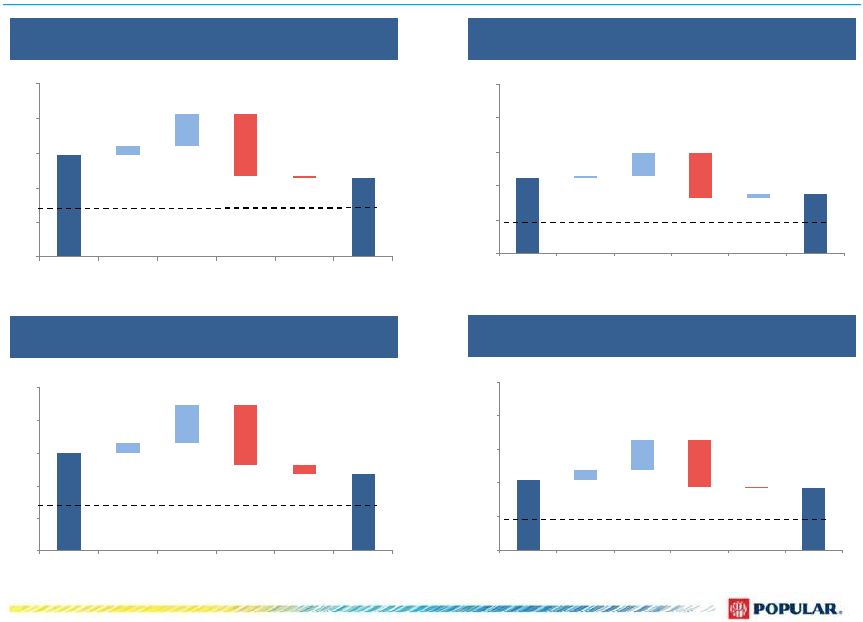

Model and Risk Components Captured in Stress Test 10 1 Risks embedded in earnings – Gains/losses on securities, Trading securities, Equity investments, OREO, HFS loans losses Purpose Estimated future impairment and/or valuation losses impacting the capital base for other assets positions (i.e., non- loan portfolio) under a specified macro-economic scenario. Methodology •Stressed OTTI write-downs due to credit losses are estimated at the security-level based on lifetime expected losses in security cash flows assuming rating downgrades based on the applicable macro-economic scenario. • Non-US Agency trading securities are modeled for potential mark-to-market (“MTM”) losses due to widening of market spreads under the Federal Reserve’s macro-economic stressed scenario of BBB corporate spreads. Quarterly projected MTM losses/gains due to stressed credit spreads are calculated based on duration approximation. •OREO balances are calculated based on average life assumptions and estimated re-valuation write-downs. Existing OREOs are modeled for future depreciation of foreclosed asset values under the stress scenario. OREO operational expense is forecasted as a ratio of the OREO balance. •SPVs and joint ventures equity loss is calculated by applying a property value depreciation percent to the assets owned by the entity. In the case of joint ventures, Popular’s capital base is impacted by its share of the underlying loss. •Strategic equity investments equity pickup forecast deterioration are mainly driven by historical stress factors and other model assumptions, taking into consideration Popular’s equity participation. Risks embedded in earnings – PPNR Purpose PPNR Model provides forecast of net interest income, non interest income and expenses by correlating macro-economic variables and interest rates with historical business activity data. Methodology • Net interest income is estimated for each scenario taking into consideration the contractual maturities and combining them with loan growth, deposit balances, and pricing forecasts based on each macro-economic scenario. • Assumptions for loan growth, pricing, deposit balances, non-interest income, and non-interest expense are determined using a bottom-up modeling framework constructed based on historical performance. This model captures critical products/categories and projects them into the future based on a correlation of macro-economic factors under the specified economic scenarios. Results are subject to review and approval by management. •The modeling approach has been implemented for the different deposit, loan, fee and expense categories considering the current size of the balance sheet or income statement item, granularity of data on specific drivers and data availability. |