SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 2-96924

AMANA MUTUAL FUNDS TRUST

(Exact Name of Registrant as Specified in Charter)

1300 N. State Street

Bellingham, Washington 98225-4730

(Address of Principal Executive Offices, including ZIP Code)

Jane K. Carten

1300 N. State Street

Bellingham, Washington 98225-4730

(Name and Address of Agent for Service)

Registrant’s Telephone Number – (360) 734-9900 Ext. 1701

Date of fiscal year end: May 31, 2022

Date of reporting period: May 31, 2022

Item 1. Report to Shareowners

| | |

| Performance Summary | | (unaudited) |

As of May 31, 2022

| | | | | | | | | | | | | | | | | | | | | | | | |

| Average Annual Returns (before any taxes paid by shareowners) | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Expense Ratio1 | |

| | | | | | |

Amana Income Fund Investor Shares (AMANX) | | | 1.16% | | | | 13.95% | | | | 10.94% | | | | 11.54% | | | | 8.29% | | | | 1.04% | |

| | | | | | |

Amana Income Fund Institutional Shares (AMINX) | | | 1.40% | | | | 14.19% | | | | 11.19% | | | | n/a | | | | n/a | | | | 0.80% | |

| | | | | | | |

Amana Growth Fund Investor Shares (AMAGX) | | | -0.62% | | | | 18.95% | | | | 17.15% | | | | 14.98% | | | | 10.62% | | | | 0.95% | |

| | | | | | |

Amana Growth Fund Institutional Shares (AMIGX) | | | -0.40% | | | | 19.23% | | | | 17.42% | | | | n/a | | | | n/a | | | | 0.70% | |

| | | | | | | |

Amana Developing World Fund Investor Shares (AMDWX) | | | -12.47% | | | | 8.86% | | | | 3.96% | | | | 2.19% | | | | n/a | | | | 1.20% | |

| | | | | | |

Amana Developing World Fund Institutional Shares (AMIDX) | | | -12.24% | | | | 9.09% | | | | 4.18% | | | | n/a | | | | n/a | | | | 0.97% | |

| | | | | | | |

Amana Participation Fund Investor Shares (AMAPX) | | | -3.83% | | | | 1.57% | | | | 1.68% | | | | n/a | | | | n/a | | | | 0.82% | |

| | | | | | |

Amana Participation Fund Institutional Shares (AMIPX) | | | -3.58% | | | | 1.82% | | | | 1.90% | | | | n/a | | | | n/a | | | | 0.58% | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

As of June 30, 2022

| | | | | | | | | | | | | | | | | | | | | | | | |

| Average Annual Returns (before any taxes paid by shareowners) | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Expense Ratio1 | |

| | | | | | |

Amana Income Fund Investor Shares (AMANX) | | | -4.65% | | | | 10.03% | | | | 9.67% | | | | 10.76% | | | | 8.02% | | | | 1.04% | |

| | | | | | |

Amana Income Fund Institutional Shares (AMINX) | | | -4.44% | | | | 10.25% | | | | 9.91% | | | | n/a | | | | n/a | | | | 0.80% | |

| | | | | | | |

Amana Growth Fund Investor Shares (AMAGX) | | | -11.67% | | | | 13.55% | | | | 15.53% | | | | 13.82% | | | | 10.09% | | | | 0.95% | |

| | | | | | |

Amana Growth Fund Institutional Shares (AMIGX) | | | -11.46% | | | | 13.82% | | | | 15.80% | | | | n/a | | | | n/a | | | | 0.70% | |

| | | | | | | |

Amana Developing World Fund Investor Shares (AMDWX) | | | -19.09% | | | | 4.00% | | | | 2.44% | | | | 1.18% | | | | n/a | | | | 1.20% | |

| | | | | | |

Amana Developing World Fund Institutional Shares (AMIDX) | | | -18.98% | | | | 4.18% | | | | 2.62% | | | | n/a | | | | n/a | | | | 0.97% | |

| | | | | | | |

Amana Participation Fund Investor Shares (AMAPX) | | | -4.35% | | | | 1.07% | | | | 1.64% | | | | n/a | | | | n/a | | | | 0.82% | |

| | | | | | |

Amana Participation Fund Institutional Shares (AMIPX) | | | -4.19% | | | | 1.32% | | | | 1.88% | | | | n/a | | | | n/a | | | | 0.58% | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Performance data quoted in this report represents past performance, is before any taxes payable by shareowners, and is no guarantee of future results. Current performance may be higher or lower than that stated herein. Performance current to the most recent month-end is available by calling toll-free 1-888-732-6262 or visiting www.amanafunds.com. Average annual total returns are historical and include change in share value as well as reinvestment of dividends and capital gains, if any. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The Amana Funds limit the securities they purchase to those consistent with Islamic principles, which limits opportunities and may affect performance.

Institutional Shares of the Amana Income, Growth, and Developing World Funds began operations September 25, 2013.

The Amana Participation Fund began operations September 28, 2015.

A note about risk: Please see the Notes to Financial Statements beginning on page 35 for a discussion of investment risks. For a more detailed discussion of the risks associated with each Fund, please see the Funds’ prospectus or each Fund’s summary prospectus.

| 1 | By regulation, expense ratios shown in this table are as stated in the Funds’ most recent prospectus which is dated September 24, 2021, and incorporates results for the fiscal year ended May 31, 2021. Ratios presented for Amana Growth have been restated to reflect a reduction in the Advisory and Administrative Services fee, which became effective on December 1, 2020. Ratios presented in this table differ from the expense ratios shown elsewhere in this report as they represent different fiscal periods. Also by regulation, this page shows performance as of the most recent calendar quarter-end in addition to performance through the Funds’ most recent fiscal period. |

Please consider an investment’s objectives, risks, charges, and expenses carefully before investing. To obtain a free prospectus or summary prospectus that contains this and other important information on the Amana Funds, please call toll-free 1-888-732-6262 or visit www.amanafunds.com. Please read the prospectus or summary prospectus carefully before investing.

| | | | | | |

|

| | | |

| 2 | | | | Annual Report | | May 31, 2022 |

| | | | |

| Fellow Shareowners: | | July 15, 2022 | | (unaudited) |

Securities markets declined during the fiscal year ended May 31, 2022. The total return for the S&P 500 Index was -0.30% and the broader Dow Jones Islamic Market World Index fell -8.40%. Developing markets also faltered, with the MSCI Emerging Markets Index falling -18.90%. Islamic fixed-income markets suffered as well, with the FTSE IdealRatings Sukuk Index returning -5.79%. Year-to-date as of May 31, the S&P 500 Index was down -12.76%, fell even further to -19.96% as of June 30, and entered bear market territory in July.

The Amana Fund portfolios performed respectably compared to these indices. Amana Growth Investor Shares lost -0.62%, Amana Income Investor Shares gained 1.16%, Amana Developing World Investor Shares fell -12.47%, and Amana Participation Investor Shares fell -3.83% for the fiscal year. As expected, lower expenses allowed the Institutional Shares of each Fund to post slightly better returns: Amana Growth -0.40%, Amana Income 1.40%, Amana Developing World -12.24%, and Amana Participation -3.58%. More than half of the Amana Funds’ shareowner assets – 50.3% – are now in Institutional shares.

The Amana Funds’ investment philosophy follows Islamic principles, which preclude most investments in banking and finance. We favor companies with good sustainability factors, low debt levels, and strong balance sheets. In volatile and troubled times, these solid principles have repeatedly proven their value.

Bear Markets and Bare Necessities

Rising inflation became the dominant economic force during the fiscal year. Exacerbated by Russia’s invasion of Ukraine (which sparked higher oil and food prices) and Shanghai’s COVID-19 lockdown (which further roiled supply chains), inflation remains high, and the Federal Reserve has taken aggressive action to tame the beast. At fiscal year-end, the federal funds rate stood at 1.75% versus 0.25% a year ago. Regardless, more needs to be done and Fed governors are unanimous in their expectations that the rate will exceed 3% by year-end. Can rates be raised by such an amount without pushing the economy into recession? Historical precedent suggests not.

Trustee Iqbal Unus Retires

Trustee Iqbal Unus PhD retired from the Amana Mutual Funds Trust Board of Trustees in May of 2022. We express our deep gratitude for Dr. Unus’ long and dedicated service to the Trust and its shareowners, as well as to the Islamic community at large through his many endeavors, including leadership of the Islamic Society of North America. Dr. Unus served as a Trustee since 1989 and retired from the Board upon reaching the mandatory retirement age, in accordance with the bylaws of the Trust. He was appointed Emeritus Trustee in June.

Mr. Firas Barzinji was appointed to serve as an Independent Trustee following Dr. Unus’ retirement.

Stars, Globes, and Trophies

As experienced investors, we know that gains or losses over a short interval tell an incomplete story compared to performance evaluated over a lengthier time span, even during times of uncertainty. We take comfort along with our shareowners in the accolades bestowed by fund industry media watchdogs like Morningstar and Investor’s Business Daily.

Morningstar rated Amana Growth Fund and Amana Participation Fund with 5 Stars and Amana Developing World Fund with 4 Stars, all based on overall performance, as of May 31, 2022. Additionally, Amana Growth, Amana Participation, and Amana Developing World Funds each were rated 5 Stars for the three-year period ended May 31, 2022. Amana Growth Fund and Amana Participation Fund earned 5-Star ratings and Amana Developing World Fund earned a 4-Star rating for the five-year period ended May 31, 2022. Please refer to “Morningstar Ratings” on pages 6 and 7 for more details.

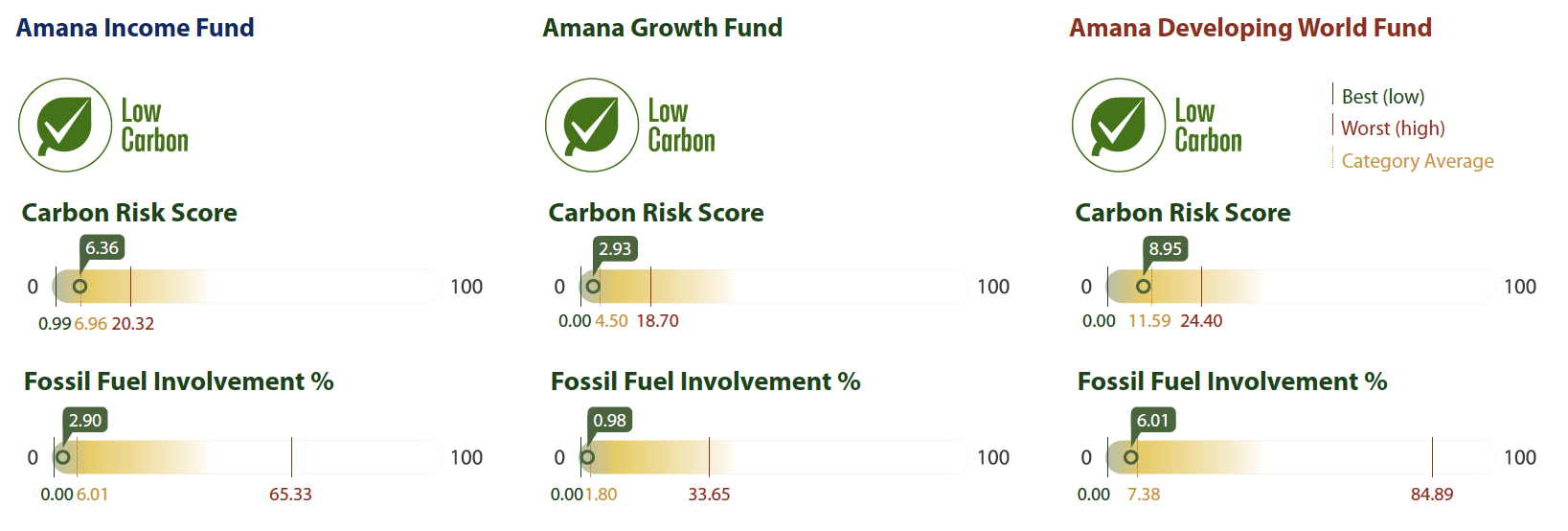

Morningstar continued to award “Low Carbon” designations to Amana Income, Growth, Developing World Funds as of March 31, 2022, which identifies them as “low-carbon” funds within the global universe (see page 7).

Amana Growth and Amana Developing World also earned “High” (5-Globe) Sustainability Ratings from Morningstar as of April 30, 2022 (see page 6).

| | | | | | |

|

| | | |

| Annual Report | | May 31, 2022 | | | | 3 |

(unaudited)

Financial news and research organization Investor’s Business Daily (IBD) recognized Amana Growth Fund among the recipients of their seventh annual Best Mutual Funds 2022 Awards for long-term performance. Amana Growth Fund placed in three categories: Best Growth Stock Mutual Funds, Best Large-Cap Stock Funds, and Best US Diversified Mutual Funds. For a fund to receive an award, it must outperform a benchmark selected by Investor’s Business Daily (in Amana Growth Fund’s case, the benchmark was the S&P 500 Index) over the 10-year period ended December 31, 2021. It was rated among 486 Growth Stock Funds, 697 Large-Cap Funds, and 1,287 US Diversified Mutual Funds.

Lower Expense Ratios

For the fiscal year ended May 31, 2022, we are again pleased to note reductions in annualized expense ratios of most Amana Funds and share classes. For the Institutional Share class of Amana Income, the expense ratio was 0.77%, for Amana Growth it was 0.64%, and for Amana Participation Fund it was 0.56%. Investor Shares expense ratios for most Funds also decreased. See page 49 for more details.

These lower expense ratios result both from greater assets to spread Fund costs, and Saturna Capital’s December 2020 reduction of Advisory and Administrative Services fee rates for the Amana equity Funds.

Going Forward

As we emerge from the current period of disruption, what sort of long-term environment can we expect on the other side? There are two competing theses. The first is that that we return to a period like the decade following the Global Financial Crisis (GFC): anemic growth, low inflation, and low interest rates. Presumably, such an easy money environment would support renewed asset price inflation with housing and stocks once again off to the races, the latter focusing on growth opportunities, be they immediate or in the future. Elements contributing to this outlook include the deflationary effect of aging demographics, stagnant-to-falling developed world populations, and continued efficiency gains from technological developments such as automation.

The second thesis is that a pullback in globalization (coupled with an end to the China-driven surge in working age population that has helped restrain prices for much of the century) will empower workers to demand higher wages, leading companies to increase prices, creating a cycle of embedded inflation and implying higher interest rates. Any sign of trouble will spur governments to act more aggressively than they did following the GFC and more closely follow their pandemic playbooks, given the apparent victory of Modern Monetary Theory and the absence of bond market vigilantes.

While it is far too early to settle upon the likely outcome, between now and then we face the highest interest rates in decades. Given our focus on strongly cash generative, low debt companies, such an environment may prove relatively beneficial for our investments. They will not be burdened by high interest payments and may be able to exploit difficulties faced by other, more heavily indebted companies, or take advantage of opportunities to invest when others cannot.

Strong Management Matters

Amana Mutual Funds embody basic principles of sound finance: good governance, transparency, fairness, and risk sharing. The Trustees are active governors, taking seriously their responsibilities to shareowners. Saturna staff work globally, based in offices in Bellingham (Washington), Henderson (Nevada), and Kuala Lumpur (Malaysia) to better serve you.

As a group, the five Amana Trustees are solidly committed to investing in Amana Mutual Funds. Including their affiliated accounts, they currently have over $34 million invested in the four mutual funds of the Trust. Dr. Mirza, Mr. Kaiser, and Mr. Fielding remain among the Trust’s largest individual shareowners.

For more information, please visit www.amanafunds.com or call 1-888/73-AMANA. We thank you for investing with us.

Respectfully,

(photo omitted)

Nicholas Kaiser,

President

(photo omitted)

M. Yaqub Mirza,

Independent Board Chairman

| | | | | | |

|

| | | |

| 4 | | | | Annual Report | | May 31, 2022 |

Portfolio Managers

| | | | | | | | | | |

| | (photo omitted) | | Scott Klimo CFA® Portfolio Manager Amana Growth Fund Deputy Portfolio Manager | | (photo omitted) | | Bryce Fegley MS, CFA®, CIPM® Deputy Portfolio Manager Amana Income Fund | | |

| | | | Amana Income Fund Amana Developing World Fund | | | | | | |

| | | | | |

| | (photo omitted) | | Monem Salam MBA Portfolio Manager Amana Income Fund | | (photo omitted) | | Christopher E. Paul MBA, CFA® Deputy Portfolio Manager Amana Growth Fund | | |

| | | | Amana Developing World Fund Deptuy Portfolio Manager Amana Growth Fund | | | | | | |

| | | | | |

| | (photo omitted) | | Patrick Drum MBA, CFA®, CFP® Portfolio Manager Amana Participation Fund | | (photo omitted) | | Elizabeth Alm CFA® Deputy Portfolio Manager Amana Participation Fund | | |

| | | | | |

| | | | | | (photo omitted) | | Levi Stewart Zurbrugg MBA, CPA® Deputy Portfolio Manager Amana Developing World Fund | | |

| | | | | | |

|

| | | |

| Annual Report | | May 31, 2022 | | | | 5 |

| | | | | | | | | | | | | | |

| Morningstar Ratings (as of May 31, 2022) | | | | | | (unaudited) |

| | | | | | | |

Morningstar™ RatingsA | | 1 Year | | 3 Year | | 5 Year | | 10 Year | | 15 Year | | Overall | | Sustainability

Rating™ B |

| | |

Amana Income Fund – “Large Blend” Category | | |

| | | | | | | |

Investor Shares (AMANX) | | n/a | | êêê | | êêê | | êê | | n/a | | êêê | | Ø Ø Ø Ø Ø |

| | | | | | | |

% Rank in Category | | 19 | | 71 | | 78 | | 86 | | 57 | | n/a | | 42 |

| | | | | | | |

Institutional Shares (AMINX) | | n/a | | êêê | | êêê | | ¶¶ | | n/a | | êêê | | Ø Ø Ø Ø Ø |

| | | | | | | |

% Rank in Category | | 17 | | 69 | | 75 | | 83 | | 51 | | n/a | | 42 |

| | | | | | | |

Number of Funds in Category | | 1,349 | | 1,221 | | 1,106 | | 807 | | 603 | | 1,221 | | 3,325 |

| |

Amana Growth Fund – “Large Growth” Category | | |

| | | | | | | |

Investor Shares (AMAGX) | | n/a | | êêêêê | | êêêêê | | êêêê | | n/a | | êêêêê | | Ø Ø Ø Ø Ø |

| | | | | | | |

% Rank in Category | | 4 | | 9 | | 6 | | 25 | | 19 | | n/a | | 4 |

| | | | | | | |

Institutional Shares (AMIGX) | | n/a | | êêêêê | | êêêêê | | ¶¶¶¶ | | n/a | | êêêêê | | Ø Ø Ø Ø Ø |

| | | | | | | |

% Rank in Category | | 3 | | 8 | | 5 | | 19 | | 15 | | n/a | | 4 |

| | | | | | | |

Number of Funds in Category | | 1,254 | | 1,142 | | 1,054 | | 777 | | 573 | | 1,142 | | 1,575 |

| |

Amana Developing World Fund – “Diversified Emerging Markets” Category | | |

| | | | | | | |

Investor Shares (AMDWX) | | n/a | | êêêêê | | êêêê | | êêê | | n/a | | êêêê | | Ø Ø Ø Ø Ø |

| | | | | | | |

% Rank in Category | | 23 | | 11 | | 39 | | 91 | | n/a | | n/a | | 14 |

| | | | | | | |

Institutional Shares (AMIDX) | | n/a | | êêêêê | | êêêê | | ¶¶¶ | | n/a | | êêêê | | Ø Ø Ø Ø Ø |

| | | | | | | |

% Rank in Category | | 21 | | 10 | | 34 | | 88 | | n/a | | n/a | | 14 |

| | | | | | | |

Number of Funds in Category | | 812 | | 720 | | 630 | | 364 | | 170 | | 720 | | 1,799 |

| |

Amana Participation Fund – “Emerging Markets Bond” Category | | |

| | | | | | | |

Investor Shares (AMAPX) | | n/a | | êêêêê | | êêêêê | | n/a | | n/a | | êêêêê | | n/a |

| | | | | | | |

% Rank in Category | | 2 | | 7 | | 13 | | n/a | | n/a | | n/a | | n/a |

| | | | | | | |

Institutional Shares (AMIPX) | | n/a | | êêêêê | | êêêêê | | n/a | | n/a | | êêêêê | | n/a |

| | | | | | | |

% Rank in Category | | 1 | | 7 | | 10 | | n/a | | n/a | | n/a | | n/a |

| | | | | | | |

Number of Funds in Category | | 273 | | 253 | | 214 | | 88 | | 37 | | 253 | | n/a |

The Morningstar Sustainability Rating and the Morningstar Portfolio Sustainability Score are not based on fund performance and are not equivalent to the Morningstar Rating (“Star Rating”).

© 2022 Morningstar®. All rights reserved. Morningstar, Inc. is an independent fund performance monitor. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

| A | Morningstar Ratings™ (“Star Ratings”) are as of May 31, 2022 and June 30, 2022. The Morningstar Rating™ for funds, or “star rating”, is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product’s monthly excess performance (not including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods. |

| B | Morningstar Sustainability Ratings are as of April 30, 2022. The Morningstar Sustainability Rating™ is intended to measure how well the issuing companies of the securities within a fund’s portfolio are managing their environmental, social, and governance (“ESG”) risks and opportunities relative to the fund’s Morningstar category peers. The Morningstar Sustainability Rating calculation is a two-step process. First, each fund with at least 50% of assets covered by a company-level ESG score from Sustainalytics receives a Morningstar Portfolio Sustainability Score™. The Morningstar Portfolio Sustainability Score is an asset-weighted average of normalized company-level ESG scores with deductions made for controversial incidents by the issuing companies, such as environmental accidents, fraud, or discriminatory behavior. The Morningstar Sustainability Rating is then assigned to all scored funds within Morningstar Categories in which at least ten (10) funds receive a Portfolio Sustainability Score and is determined by each fund’s rank within the following distribution: High (highest 10%), Above Average (next 22.5%), Average (next 35%), Below Average (next 22.5%), and Low (lowest 10%). The Morningstar Sustainability Rating is depicted by globe icons where High equals 5 globes and Low equals 1 globe. A Sustainability Rating is assigned to any fund that has more than half of its underlying assets rated by Sustainalytics and is within a Morningstar Category with at least 10 scored funds; therefore, the rating is not limited to funds with explicit sustainable or responsible investment mandates. Morningstar updates its Sustainability Ratings monthly. Portfolios receive a Morningstar Portfolio Sustainability Score and Sustainability Rating one month and six business days after their reported as-of date based on the most recent portfolio. As part of the evaluation process, Morningstar uses Sustainalytics’ ESG scores from the same month as the portfolio as-of date. |

The Fund’s portfolios are actively managed and subject to change, which may result in a different Morningstar Sustainability Score and Rating each month.

The Funds were rated on the following percentages of Assets Under Management:

| | | | |

| Amana Income Fund | | | 100% | |

| Amana Growth Fund | | | 100% | |

| Amana Developing World Fund | | | 98% | |

As of April 30, 2022, the Amana Participation Fund had not received a Sustainability Rating.

% Rank in Category is the fund’s percentile rank for the specified time period relative to all funds that have the same Morningstar category. The highest (or most favorable) percentile rank is 1 and the lowest (or least favorable) percentile rank is 100. The top-performing fund in a category will always receive a rank of 1. Percentile ranks within categories are most useful in those categories that have a large number of funds.

The Amana Mutual Funds offer two share classes – Investor Shares and Institutional Shares, each of which has different expense structures.

| | | | | | |

|

| | | |

| 6 | | | | Annual Report | | May 31, 2022 |

| | | | | | | | | | | | |

| Morningstar Ratings (as of June 30, 2022) | | | | | | | | (unaudited) |

| | | | | | |

Morningstar™ RatingsA | | 1 Year | | 3 Year | | 5 Year | | 10 Year | | 15 Year | | Overall |

| | | | | | | |

Amana Income Fund –“Large Blend” Category | | | | | | | | | | | | |

| | | | | | |

Investor Shares (AMANX) | | n/a | | êêêê | | êêê | | êê | | n/a | | êêê |

| | | | | | |

% Rank in Category | | 8 | | 40 | | 63 | | 81 | | 47 | | n/a |

| | | | | | |

Institutional Shares (AMINX) | | n/a | | êêêê | | êêê | | ¶¶¶ | | n/a | | êêê |

| | | | | | |

% Rank in Category | | 7 | | 34 | | 60 | | 76 | | 41 | | n/a |

| | | | | | |

Number of Funds in Category | | 1,359 | | 1,225 | | 1,107 | | 811 | | 606 | | 1,225 |

| | | | | | |

Amana Growth Fund –“Large Growth” Category | | | | | | | | | | | | |

| | | | | | |

Investor Shares (AMAGX) | | n/a | | êêêêê | | êêêêê | | êêêê | | n/a | | êêêêê |

| | | | | | |

% Rank in Category | | 7 | | 6 | | 5 | | 23 | | 17 | | n/a |

| | | | | | |

Institutional Shares (AMIGX) | | n/a | | êêêêê | | êêêêê | | ¶¶¶¶¶ | | n/a | | êêêêê |

| | | | | | |

% Rank in Category | | 6 | | 6 | | 4 | | 19 | | 14 | | n/a |

| | | | | | |

Number of Funds in Category | | 1,248 | | 1,138 | | 1,052 | | 787 | | 572 | | 1,138 |

| | | | |

Amana Developing World Fund –“Diversified Emerging Markets” Category | | | | | | | | |

| | | | | | |

Investor Shares (AMDWX) | | n/a | | êêêêê | | êêêê | | êêê | | n/a | | êêêê |

| | | | | | |

% Rank in Category | | 18 | | 10 | | 35 | | 89 | | n/a | | n/a |

| | | | | | |

Institutional Shares (AMIDX) | | n/a | | êêêêê | | êêêê | | ¶¶¶ | | n/a | | êêêê |

| | | | | | |

% Rank in Category | | 17 | | 9 | | 31 | | 85 | | n/a | | n/a |

| | | | | | |

Number of Funds in Category | | 817 | | 734 | | 635 | | 364 | | 170 | | 734 |

| | | | | | |

Amana Participation Fund –“Emerging Markets Bond” Category | | | | | | | | | | | | |

| | | | | | |

Investor Shares (AMAPX) | | n/a | | êêêêê | | êêêêê | | n/a | | n/a | | êêêêê |

| | | | | | |

% Rank in Category | | 1 | | 2 | | 5 | | n/a | | n/a | | n/a |

| | | | | | |

Institutional Shares (AMIPX) | | n/a | | êêêêê | | êêêêê | | n/a | | n/a | | êêêêê |

| | | | | | |

% Rank in Category | | 1 | | 1 | | 4 | | n/a | | n/a | | n/a |

| | | | | | |

Number of Funds in Category | | 274 | | 253 | | 215 | | 89 | | 37 | | 253 |

Morningstar Carbon Metrics (as of March 31, 2022)

Morningstar carbon metrics are asset-weighted portfolio calculations based on their Sustainalytics subsidiary’s carbon-risk research. Based on two of these metrics – Carbon Risk Score and Fossil Fund Involvement % – funds may receive the Low Carbon designation, which allows investors to easily identify low-carbon funds within the global universe.

The portfolio Carbon Risk Score is a number between 0 and 100 (a lower score is better). A portfolio’s Carbon Risk Score is the asset-weighted sum of the carbon risk scores of its holdings, averaged over the trailing 12 months. The carbon risk of a company is Sustainalytics’ evaluation of the degree to which a firm’s activities and products are aligned with the transition to a low-carbon economy. The assessment includes carbon intensity, fossil fuel involvement, stranded assets exposure, mitigation strategies, and green product solutions.

Fossil Fuel Involvement % is the portfolio’s asset-weighted percentage exposure to fossil fuels, averaged over the trailing 12 months. Companies with fossil fuel involvement are defined as those in the following subindustries: Thermal Coal Extraction, Thermal Coal Power Generation, Oil & Gas Production, Oil & Gas Power Generation, and Oil & Gas Products & Services.

To receive the Low Carbon designation a fund must have a Carbon Risk Score below 10 and a Fossil Fuel Involvement % of less than 7% of assets. For these metrics to be calculated, at least 67% of a portfolio’s assets must be covered by Sustainalytics company carbon-risk research. All Morningstar carbon metrics are calculated quarterly.

Amana Income Fund was rated on 93%, Amana Growth Fund was rated on 90%, and Amana Developing World Fund was rated on 82% of assets under management.

| | | | | | |

|

| | | |

| Annual Report | | May 31, 2022 | | | | 7 |

| | |

| Amana Income Fund: Performance Summary | | (unaudited) |

| | | | | | | | | | | | | | | | |

Average Annual Returns (as of May 31, 2022) | |

| | | | | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | Expense Ratio | |

| | | | |

Investor Shares (AMANX) | | | 1.16% | | | | 10.94% | | | | 11.54% | | | | 1.04% | |

| | | | |

Institutional Shares (AMINX)2 | | | 1.40% | | | | 11.19% | | | | n/a | | | | 0.80% | |

| | | | |

S&P 500 Index | | | -0.30% | | | | 13.38% | | | | 14.39% | | | | n/a | |

Growth of $10,000

| | |

| | Comparison of any mutual fund to a market index must be made bearing in mind that the index is unmanaged and expense-free. Conversely, the Fund will (1) be actively managed; (2) have an objective other than mirroring the index, such as limiting risk; (3) bear transaction and other operational costs; (4) stand ready to buy and sell its securities to shareowners on a daily basis; and (5) provide a wide range of services. The graph compares $10,000 invested in Investor Shares of the Fund on May 31, 2012, to an identical amount invested in the S&P 500 Index, a broad-based stock market index. The graph shows that an investment in Investor Shares of the Fund would have risen to $29,817 versus $38,377 in the Index. Investor Shares are used in this chart because they have a longer track record. Please note that investors cannot invest directly in the Index. |

Past performance does not guarantee future results. The “Growth of $10,000” graph and “Average Annual Returns” performance table assume the reinvestment of dividends and capital gains. They do not reflect the deduction of taxes that a shareowner might pay on fund distributions or the redemption of fund shares.

2 Institutional shares of the Amana Income Fund began operations September 25, 2013.

Fund Objective

The objectives of the Income Fund are current income and preservation of capital, consistent with Islamic principles; current income is its primary objective.

| | | | |

Top 10 Holdings | |

| |

| % of Total Net Assets | |

| |

Eli Lilly | | | 11.4% | |

| |

Microsoft | | | 7.1% | |

| |

Taiwan Semiconductor ADR | | | 5.1% | |

| |

Rockwell Automation | | | 4.2% | |

| |

Illinois Tool Works | | | 4.1% | |

| |

Pfizer | | | 4.0% | |

| |

Genuine Parts | | | 3.4% | |

| |

McCormick & Co | | | 3.4% | |

| |

AbbVie | | | 3.4% | |

| |

Honeywell International | | | 3.3% | |

| | | | | | | | | | | | |

Portfolio Diversification | | | | | | | | | | | | |

| | | |

| % of Total Net Assets | | | | | | | | | |

| | | |

Large Pharma | | | 26.8% | | | ∎ | | | | |

| |

Infrastructure Software | | | 7.1% | | | ∎ | | |

Household Products | | | 6.7% | | | ∎ | | |

Semiconductor Devices | | | 5.5% | | | ∎ | | |

Specialty Chemicals | | | 5.1% | | | ∎ | | |

Semiconductor Manufacturing | | | 5.1% | | | ∎ | | |

Basic & Diversified Chemicals | | | 4.5% | | | ∎ | | |

Commercial & Residential Building Equipment & Systems | | | 4.2% | | | ∎ | | |

Measurement Instruments | | | 4.2% | | | ∎ | | |

Industrial Machinery | | | 4.1% | | | ∎ | | |

Other industries < 3.5% | | | 19.3% | | | ∎ | | |

Other Assets (net of liabilities) | | | 7.4% | | | ∎ | | |

| | | | | | |

|

| | | |

| 8 | | | | Annual Report | | May 31, 2022 |

| | |

| Amana Income Fund: Discussion of Fund Performance | | (unaudited) |

Fiscal Year 2022

For the fiscal year ended May 31, 2022, Amana Income Fund Investor Shares returned 1.16%, compared to 30.87% the year before. The Institutional Shares of the Fund returned 1.40%, compared to 31.14% the year before. The S&P 500 returned -0.30% over the 2022 fiscal year.

In pursuit of its objective of current income, the Amana Income Fund distributed qualified income amounts of $0.55 per share (Investor Shares) and $0.77 per share (Institutional Shares) during the fiscal year. All shareowners received a capital gain distribution of $2.59 per share. The expense ratios for both share classes lowered over the fiscal year due to an increase in assets; the Investor Shares went from 1.04% to 1.01%, while the Institutional Shares went from 0.80% from 0.77%.

For the 10-year period ended May 31, 2022, Investor Shares of the Amana Income Fund provided an average annual return of

11.54%. Since the Fund’s inception in 1986, the Investor Shares provided an average annual compounded return of 8.97%. The Fund’s portfolio turnover rate was 5% for the fiscal year – among the lowest in the category – consistent with the overall strategy of investing in dividend-paying companies with a focus on the long-term.

Factors Affecting Past Performance

Rising inflation became the dominant economic force during the fiscal year. Supply-side issues, such as parts shortages and logistics bottlenecks in the aftermath of the COVID-19 pandemic, were compounded by demand-side forces including a strong labor market recovery and generous government stimulus measures. Because of this, higher inflation has persisted beyond the “transitory” period that policymakers estimated a year ago.

High inflation, rising interest rates, and an increasingly hawkish Federal Reserve appear to have combined to pull investors’ operative time horizons much closer to the present. Fast growth companies that had the loftiest valuations have experienced very steep share price declines as investors became less willing to wait to see if companies could meet aggressive long-term growth targets. Economically sensitive companies also fared poorly. Less cyclical companies, such as in those in the Health Care sector or companies that have the ability to pass higher costs to their customers, tended to perform better.

Five of Amana Income Fund’s top 10 performers during the fiscal year were large pharmaceutical companies, which tend to be more resilient during economic swings than other industries. The Fund’s three poorest performers, meanwhile, were Stanley Black & Decker, PPG Industries, and Johnson Controls. All three companies were negatively impacted by parts shortages, rising costs, and a weakening demand environment.

Looking Forward

In the coming fiscal year, the Fed will attempt to engineer a slowdown in inflation closer to its target of 2%, while trying to balance forces outside of its control – such as the high energy and grain prices caused by Russia’s invasion of Ukraine – and avoid causing a prolonged recession. This economic uncertainty creates a challenging environment for companies to do business. However, we also believe it creates opportunities for the types of well-managed companies with low debt in which the Amana Income Fund invests to increase market share, make timely acquisitions of weaker rivals, or negotiate better terms with suppliers as a result of their stronger footing.

| | | | | | |

|

| | | |

| Annual Report | | May 31, 2022 | | | | 9 |

| | |

| Amana Income Fund: Schedule of Investments | | As of May 31, 2022 |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | Common Stocks – 92.6% | | | | Number of Shares | | | Cost | | | Market Value | | | Percentage of Net Assets | |

| | | | | | |

| | | Consumer Discretionary | | | | | | | | | | | | | | |

| | | | | | | |

| | | Automotive Retailers | | | | | | | | | | | | | | |

| | | | | | | |

| | | Genuine Parts | | | | | 382,000 | | | | $15,016,749 | | | | $52,230,860 | | | | 3.4% | |

| | | | | | | |

| | | Home Improvement | | | | | | | | | | | | | | |

| | | | | | | |

| | | Stanley Black & Decker | | | | | 71,950 | | | | 4,850,611 | | | | 8,539,746 | | | | 0.6% | |

| | | | | | | |

| | | | | | | | | | | 19,867,360 | | | | 60,770,606 | | | | 4.0% | |

| | | | | | |

| | | Consumer Staples | | | | | | | | | | | | | | |

| | | | | | | |

| | | Household Products | | | | | | | | | | | | | | |

| | | | | | | |

| | | Colgate-Palmolive | | | | | 415,400 | | | | 15,151,572 | | | | 32,737,674 | | | | 2.1% | |

| | | | | | | |

| | | Kimberly-Clark | | | | | 230,000 | | | | 13,960,736 | | | | 30,594,600 | | | | 2.0% | |

| | | | | | | |

| | | Procter & Gamble | | | | | 135,000 | | | | 16,030,154 | | | | 19,963,800 | | | | 1.3% | |

| | | | | | | |

| | | Unilever ADR | | | | | 420,000 | | | | 14,236,893 | | | | 20,298,600 | | | | 1.3% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 59,379,355 | | | | 103,594,674 | | | | 6.7% | |

| | | | | | | |

| | | Packaged Food | | | | | | | | | | | | | | |

| | | | | | | |

| | | McCormick & Co | | | | | 559,288 | | | | 13,161,835 | | | | 51,857,183 | | | | 3.4% | |

| | | | | | | |

| | | | | | | | | | | 72,541,190 | | | | 155,451,857 | | | | 10.1% | |

| | | | | | |

| | | Health Care | | | | | | | | | | | | | | |

| | | | | | | |

| | | Large Pharma | | | | | | | | | | | | | | |

| | | | | | | |

| | | AbbVie | | | | | 350,000 | | | | 9,148,094 | | | | 51,579,500 | | | | 3.4% | |

| | | | | | | |

| | | Bristol-Myers Squibb | | | | | 650,000 | | | | 15,185,381 | | | | 49,042,500 | | | | 3.2% | |

| | | | | | | |

| | | Eli Lilly | | | | | 560,000 | | | | 20,261,156 | | | | 175,526,400 | | | | 11.4% | |

| | | | | | | |

| | | GlaxoSmithKline ADR | | | | | 610,000 | | | | 22,889,329 | | | | 26,779,000 | | | | 1.7% | |

| | | | | | | |

| | | Johnson & Johnson | | | | | 125,000 | | | | 10,460,152 | | | | 22,441,250 | | | | 1.5% | |

| | | | | | | |

| | | Novartis ADR | | | | | 275,400 | | | | 14,323,946 | | | | 25,044,876 | | | | 1.6% | |

| | | | | | | |

| | | Pfizer | | | | | 1,150,000 | | | | 19,768,443 | | | | 60,996,000 | | | | 4.0% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 112,036,501 | | | | 411,409,526 | | | | 26.8% | |

| | | | | | | |

| | | Medical Devices | | | | | | | | | | | | | | |

| | | | | | | |

| | | Abbott Laboratories | | | | | 350,000 | | | | 8,392,885 | | | | 41,111,000 | | | | 2.7% | |

| | | | | | | |

| | | | | | | | | | | 120,429,386 | | | | 452,520,526 | | | | 29.5% | |

| | | | | | |

| | | Industrials | | | | | | | | | | | | | | |

| | | | | | |

| | | Commercial & Residential Building Equipment &

Systems | | | | | | | | | | | | |

| | | | | | | |

| | | Honeywell International | | | | | 260,000 | | | | 10,768,521 | | | | 50,341,200 | | | | 3.3% | |

| | | | | | | |

| | | Johnson Controls International | | | | | 270,000 | | | | 19,152,848 | | | | 14,717,700 | | | | 0.9% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 29,921,369 | | | | 65,058,900 | | | | 4.2% | |

| | | | | | | |

| | | Courier Services | | | | | | | | | | | | | | |

| | | | | | | |

| | | United Parcel Service, Class B | | | | | 15,000 | | | | 3,325,591 | | | | 2,733,750 | | | | 0.2% | |

| | | | | | | |

| | | Flow Control Equipment | | | | | | | | | | | | | | |

| | | | | | | |

| | | Parker Hannifin | | | | | 40,000 | | | | 1,586,972 | | | | 10,886,800 | | | | 0.7% | |

| | | | | | | |

| | | Industrial Distribution & Rental | | | | | | | | | | | | | | |

| | | | | | | |

| | | W.W. Grainger | | | | | 80,000 | | | | 7,590,798 | | | | 38,965,600 | | | | 2.5% | |

| | | | | | | |

| | | Industrial Machinery | | | | | | | | | | | | | | |

| | | | | | | |

| | | Illinois Tool Works | | | | | 300,000 | | | | 14,672,460 | | | | 62,421,000 | | | | 4.1% | |

Continued on next page.

| | | | | | | | |

|

| | | | |

| 10 | | | | Annual Report | | May 31, 2022 | | The accompanying notes are an integral part of these financial statements. |

| | |

| Amana Income Fund: Schedule of Investments | | As of May 31, 2022 |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | Common Stocks – 92.6% | | | | Number of Shares | | | Cost | | | Market Value | | | Percentage of Net Assets | |

| | | | | | |

| | | Industrials (continued) | | | | | | | | | | | | | | |

| | | | | | | |

| | | Measurement Instruments | | | | | | | | | | | | | | |

| | | | | | | |

| | | Rockwell Automation | | | | | 300,000 | | | | $13,657,124 | | | | $63,960,000 | | | | 4.2% | |

| | | | | | | |

| | | Rail Freight | | | | | | | | | | | | | | |

| | | | | | | |

| | | Canadian National Railway | | | | | 384,000 | | | | 8,600,818 | | | | 43,691,520 | | | | 2.8% | |

| | | | | | | |

| | | | | | | | | | | 79,355,132 | | | | 287,717,570 | | | | 18.7% | |

| | | | | | |

| | | Materials | | | | | | | | | | | | | | |

| | | | | | | |

| | | Basic & Diversified Chemicals | | | | | | | | | | | | | | |

| | | | | | | |

| | | Air Products & Chemicals | | | | | 110,000 | | | | 6,424,723 | | | | 27,077,600 | | | | 1.8% | |

| | | | | | | |

| | | Linde | | | | | 130,000 | | | | 8,531,143 | | | | 42,208,400 | | | | 2.7% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 14,955,866 | | | | 69,286,000 | | | | 4.5% | |

| | | | | | | |

| | | Specialty Chemicals | | | | | | | | | | | | | | |

| | | | | | | |

| | | 3M | | | | | 200,000 | | | | 13,704,248 | | | | 29,858,000 | | | | 2.0% | |

| | | | | | | |

| | | PPG Industries | | | | | 379,000 | | | | 12,758,054 | | | | 47,939,710 | | | | 3.1% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 26,462,302 | | | | 77,797,710 | | | | 5.1% | |

| | | | | | | |

| | | | | | | | | | | 41,418,168 | | | | 147,083,710 | | | | 9.6% | |

| | | | | | |

| | | Technology | | | | | | | | | | | | | | |

| | | | | | | |

| | | Communications Equipment | | | | | | | | | | | | | | |

| | | | | | | |

| | | Cisco Systems | | | | | 572,000 | | | | 26,072,500 | | | | 25,768,600 | | | | 1.7% | |

| | | | | | | |

| | | Consumer Electronics | | | | | | | | | | | | | | |

| | | | | | | |

| | | Nintendo | | | | | 45,000 | | | | 23,496,950 | | | | 20,106,042 | | | | 1.3% | |

| | | | | | | |

| | | Infrastructure Software | | | | | | | | | | | | | | |

| | | | | | | |

| | | Microsoft | | | | | 400,000 | | | | 7,953,170 | | | | 108,748,000 | | | | 7.1% | |

| | | | | | | |

| | | Semiconductor Devices | | | | | | | | | | | | | | |

| | | | | | | |

| | | Intel | | | | | 900,000 | | | | 19,537,540 | | | | 39,978,000 | | | | 2.6% | |

| | | | | | | |

| | | Texas Instruments | | | | | 250,000 | | | | 38,489,292 | | | | 44,190,000 | | | | 2.9% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 58,026,832 | | | | 84,168,000 | | | | 5.5% | |

| | | | | | | |

| | | Semiconductor Manufacturing | | | | | | | | | | | | | | |

| | | | | | | |

| | | Taiwan Semiconductor ADR | | | | | 824,500 | | | | 8,249,619 | | | | 78,574,850 | | | | 5.1% | |

| | | | | | |

| | | | | | | | | | | 123,799,071 | | | | 317,365,492 | | | | 20.7% | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | Total investments | | | | | | | | | $457,410,307 | | | | $1,420,909,761 | | | | 92.6% | |

| | | | | | |

| | Other assets (net of liabilities) | | | | | | | | | | | | | 114,347,499 | | | | 7.4% | |

| | | | | | |

| | Total net assets | | | | | | | | | | | | | $1,535,257,260 | | | | 100.0% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

ADR: American Depositary Receipt

| | | | | | | | |

|

| | | | |

| The accompanying notes are an integral part of these financial statements. | | Annual Report | | May 31, 2022 | | | | 11 |

Amana Income Fund

Statement of Assets and Liabilities

| | | | |

| As of May 31, 2022 | |

| | |

| | | | |

| |

Assets | | | | |

| |

Investments in securities, at value

(Cost $457,410,307) | | | $1,420,909,761 | |

| |

Cash | | | 111,648,280 | |

| |

Dividends receivable | | | 4,278,709 | |

| |

Receivable for Fund shares sold | | | 410,385 | |

| |

Prepaid expenses | | | 36,754 | |

| |

Other assets | | | 2,528 | |

| | | | |

| |

Total assets | | | 1,537,286,417 | |

| | | | |

| |

Liabilities | | | | |

| |

Accrued advisory fees | | | 959,133 | |

| |

Payable for Fund shares redeemed | | | 839,268 | |

| |

Accrued 12b-1 distribution fees | | | 156,014 | |

| |

Accrued retirement plan custody fee | | | 23,672 | |

| |

Accrued other operating expenses | | | 14,269 | |

| |

Accrued audit expenses | | | 13,597 | |

| |

Accrued trustee expenses | | | 10,615 | |

| |

Accrued Chief Compliance Officer expenses | | | 8,092 | |

| |

Accrued legal expenses | | | 4,497 | |

| | | | |

| |

Total liabilities | | | 2,029,157 | |

| | | | |

| |

Net Assets | | | $1,535,257,260 | |

| | |

| | | | |

| | |

Analysis of Net Assets | | | | |

| |

Paid-in capital (unlimited shares authorized, without par value) | | | $520,198,071 | |

| |

Total distributable earnings | | | 1,015,059,189 | |

| | | | |

| |

Net assets applicable to Fund shares outstanding | | | $1,535,257,260 | |

| | |

| | | | |

| | |

Net asset value per Investor Share | | | AMANX | |

| |

Net assets, at value | | | $746,533,567 | |

| |

Shares outstanding | | | 12,579,554 | |

| | | | |

| |

Net asset value, offering and redemption price per share | | | $59.34 | |

| | |

| | | | |

| | |

Net asset value per Institutional Share | | | AMINX | |

| |

Net assets, at value | | | $788,723,693 | |

| |

Shares outstanding | | | 13,415,533 | |

| | | | |

| |

Net asset value, offering and redemption price per share | | | $58.79 | |

| | |

| | | | |

Statement of Operations

| | | | |

| Year ended May 31, 2022 | |

| | |

| | | | |

| |

Investment income | | | | |

| |

Dividend Income

(net of foreign tax of $711,747) | | | $30,838,387 | |

| |

Miscellaneous income | | | 7,915 | |

| | | | |

| |

Total investment income | | | 30,846,302 | |

| | | | |

| |

Expenses | | | | |

| |

Investment advisory fees | | | 11,772,305 | |

| |

12b-1 distribution fees | | | 2,006,713 | |

| |

Custodian fees | | | 68,083 | |

| |

Filing and registration fees | | | 58,600 | |

| |

Retirement plan custodial fees | | | | |

| |

Investor Shares | | | 102 | |

| |

Institutional Shares | | | 58,021 | |

| |

Printing and postage fees | | | 42,491 | |

| |

Legal fees | | | 35,091 | |

| |

Other operating expenses | | | 34,665 | |

| |

Audit fees | | | 30,631 | |

| |

Trustee fees | | | 20,879 | |

| |

Chief Compliance Officer expenses | | | 18,753 | |

| | | | |

| |

Total gross expenses | | | 14,146,334 | |

| | | | |

| |

Less custodian fee credits | | | (68,083 | ) |

| | | | |

| |

Net expenses | | | 14,078,251 | |

| | | | |

| |

Net investment income | | | $16,768,051 | |

| | |

| | | | |

| | |

| | | | |

| |

Net realized gain from investments and foreign currency | | | $86,498,012 | A |

| |

Net decrease in unrealized appreciation on investments | | | (81,975,793 | ) |

| | | | |

| |

Net gain on investments | | | $4,522,219 | |

| | |

| | | | |

| | |

Net increase in net assets resulting from operations | | | $21,290,270 | |

| | | | | |

| A | Includes $11,817,477 in net realized gains from redemptions in-kind. |

| | | | | | | | |

|

| | | | |

| 12 | | | | Annual Report | | May 31, 2022 | | The accompanying notes are an integral part of these financial statements. |

Amana Income Fund

| | | | | | | | |

Statements of Changes in Net Assets | | | Year ended May 31, 2022 | | | | Year ended May 31, 2021 | |

| | | |

Increase (decrease) in net assets from operations | | | | | | | | |

| | |

From operations | | | | | | | | |

| | |

Net investment income | | | $16,768,051 | | | | $15,901,444 | |

| | |

Net realized gain on investment | | | 86,498,012 | | | | 109,441,618 | |

| | |

Net increase (decrease) in unrealized appreciation | | | (81,975,793 | ) | | | 251,602,142 | |

| | | | | | | | |

| | |

Net increase in net assets | | | 21,290,270 | | | | 376,945,204 | |

| | | | | | | | |

| | |

Distributions to shareowners | | | | | | | | |

| | |

Net distribution to shareowners – Investor Shares | | | (39,012,483 | ) | | | (48,715,136 | ) |

| | |

Net distribution to shareowners – Institutional Shares | | | (42,119,427 | ) | | | (42,660,760 | ) |

| | | | | | | | |

| | |

Total distributions | | | (81,131,910 | ) | | | (91,375,896 | ) |

| | | | | | | | |

| | |

Capital share transactions | | | | | | | | |

| | |

Proceeds from the sale of shares | | | | | | | | |

| | |

Investor Shares | | | 63,205,053 | | | | 67,430,743 | |

| | |

Institutional Shares | | | 195,808,033 | | | | 200,977,427 | |

| | |

Value of shares issued in reinvestment of distributions | | | | | | | | |

| | |

Investor Shares | | | 37,828,390 | | | | 47,457,602 | |

| | |

Institutional Shares | | | 40,674,735 | | | | 41,065,802 | |

| | |

Cost of shares redeemed | | | | | | | | |

| | |

Investor Shares | | | (169,927,539 | ) | | | (169,718,357 | ) |

| | |

Institutional Shares | | | (117,623,925 | ) | | | (196,452,487 | ) |

| | | | | | | | |

| | |

Total capital share transactions | | | 49,964,747 | | | | (9,239,270 | ) |

| | | | | | | | |

| | |

Total increase (decrease) in net assets | | | (9,876,893 | ) | | | 276,330,038 | |

| | | |

| | | | | | | | |

| | | |

Net assets | | | | | | | | |

| | |

Beginning of year | | | 1,545,134,153 | | | | 1,268,804,115 | |

| | |

End of year | | | $1,535,257,260 | | | | $1,545,134,153 | |

| | | |

Shares of the Fund sold and redeemed | | | | | | | | |

| | |

Investor Shares (AMANX) | | | | | | | | |

| | |

Number of shares sold | | | 1,013,224 | | | | 1,197,311 | |

| | |

Number of shares issued in reinvestment of distributions | | | 584,713 | | | | 840,652 | |

| | |

Number of shares redeemed | | | (2,695,833 | ) | | | (3,062,129 | ) |

| | | | | | | | |

| | |

Net decrease in number of shares outstanding | | | (1,097,896 | ) | | | (1,024,166 | ) |

| | | | | | | | |

| | |

Institutional Shares (AMINX) | | | | | | | | |

| | |

Number of shares sold | | | 3,142,847 | | | | 3,575,035 | |

| | |

Number of shares issued in reinvestment of distributions | | | 636,014 | | | | 732,160 | |

| | |

Number of shares redeemed | | | (1,892,271 | ) | | | (3,503,470 | ) |

| | | | | | | | |

| | |

Net increase in number of shares outstanding | | | 1,886,590 | | | | 803,725 | |

| | | |

| | | | | | | | |

| | | | | | | | |

|

| | | | |

| The accompanying notes are an integral part of these financial statements. | | Annual Report | | May 31, 2022 | | | | 13 |

Amana Income Fund: Financial Highlights

| | | | | | | | | | | | | | | | | | | | |

Investor Shares (AMANX) | | | Year ended May 31, | |

| | | | | |

Selected data per share of outstanding capital stock throughout each year: | | | 2022 | | | | 2021 | | | | 2020 | | | | 2019 | | | | 2018 | |

| | | | | | |

Net asset value at beginning of year | | | $61.52 | | | | $50.03 | | | | $48.32 | | | | $48.91 | | | | $48.03 | |

| | | | | |

Income from investment operations | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net investment incomeA | | | 0.59 | | | | 0.58 | | | | 0.67 | | | | 0.61 | | | | 0.58 | |

| | | | | |

Net gains on securities (both realized & unrealized) | | | 0.37 | | | | 14.53 | | | | 5.17 | | | | 1.80 | | | | 3.28 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total from investment operations | | | 0.96 | | | | 15.11 | | | | 5.84 | | | | 2.41 | | | | 3.86 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Less distributions | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Dividends (from net investment income) | | | (0.55 | ) | | | (0.56 | ) | | | (0.66 | ) | | | (0.62 | ) | | | (0.57 | ) |

| | | | | |

Distributions (from capital gains) | | | (2.59 | ) | | | (3.06 | ) | | | (3.47 | ) | | | (2.38 | ) | | | (2.41 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total distributions | | | (3.14 | ) | | | (3.62 | ) | | | (4.13 | ) | | | (3.00 | ) | | | (2.98 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net asset value at end of year | | | $59.34 | | | | $61.52 | | | | $50.03 | | | | $48.32 | | | | $48.91 | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Total Return | | | 1.16% | | | | 30.87% | | | | 11.77% | | | | 5.35% | | | | 7.82% | |

| | | | | | |

Ratios / supplemental data | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net assets ($000), end of year | | | $746,534 | | | | $841,439 | | | | $735,565 | | | | $805,610 | | | | $882,571 | |

| | | | | |

Ratio of expenses to average net assets | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Before custodian fee credits | | | 1.01% | | | | 1.04% | | | | 1.06% | | | | 1.11% | | | | 1.13% | |

| | | | | |

After custodian fee credits | | | 1.01% | | | | 1.04% | | | | 1.06% | | | | 1.10% | | | | 1.12% | |

| | | | | |

Ratio of net investment income after custodian fee credits to average net assets | | | 0.94% | | | | 1.03% | | | | 1.31% | | | | 1.22% | | | | 1.14% | |

| | | | | |

Portfolio turnover rate | | | 5% | | | | 5% | | | | 0% | | | | 1% | | | | 1% | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Institutional Shares (AMINX) | | | Year ended May 31, | |

| | | | | |

Selected data per share of outstanding capital stock throughout each year: | | | 2022 | | | | 2021 | | | | 2020 | | | | 2019 | | | | 2018 | |

| | | | | | |

Net asset value at beginning of year | | | $61.04 | | | | $49.72 | | | | $48.12 | | | | $48.72 | | | | $47.90 | |

| | | | | |

Income from investment operations | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net investment incomeA | | | 0.74 | | | | 0.71 | | | | 0.78 | | | | 0.74 | | | | 0.70 | |

| | | | | |

Net gains on securities (both realized & unrealized) | | | 0.37 | | | | 14.42 | | | | 5.13 | | | | 1.79 | | | | 3.26 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total from investment operations | | | 1.11 | | | | 15.13 | | | | 5.91 | | | | 2.53 | | | | 3.96 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Less distributions | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Dividends (from net investment income) | | | (0.77 | ) | | | (0.75 | ) | | | (0.84 | ) | | | (0.75 | ) | | | (0.73 | ) |

| | | | | |

Distributions (from capital gains) | | | (2.59 | ) | | | (3.06 | ) | | | (3.47 | ) | | | (2.38 | ) | | | (2.41 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total distributions | | | (3.36 | ) | | | (3.81 | ) | | | (4.31 | ) | | | (3.13 | ) | | | (3.14 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net asset value at end of year | | | $58.79 | | | | $61.04 | | | | $49.72 | | | | $48.12 | | | | $48.72 | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Total Return | | | 1.40% | | | | 31.14% | | | | 11.96% | | | | 5.63% | | | | 8.05% | |

| | | | | | |

Ratios / supplemental data | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net assets ($000), end of year | | | $788,724 | | | | $703,695 | | | | $533,239 | | | | $472,724 | | | | $451,651 | |

| | | | | |

Ratio of expenses to average net assets | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Before custodian fee credits | | | 0.77% | | | | 0.80% | | | | 0.83% | | | | 0.87% | | | | 0.89% | |

| | | | | |

After custodian fee credits | | | 0.77% | | | | 0.79% | | | | 0.82% | | | | 0.86% | | | | 0.88% | |

| | | | | |

Ratio of net investment income after custodian fee credits to average net assets | | | 1.19% | | | | 1.27% | | | | 1.55% | | | | 1.47% | | | | 1.39% | |

| | | | | |

Portfolio turnover rate | | | 5% | | | | 5% | | | | 0% | | | | 1% | | | | 1% | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| A | Calculated using average shares outstanding |

| | | | | | | | |

|

| | | | |

| 14 | | | | Annual Report | | May 31, 2022 | | The accompanying notes are an integral part of these financial statements. |

| | |

| Amana Growth Fund: Performance Summary | | (unaudited) |

| | | | | | | | | | | | | | | | |

Average Annual Returns (as of May 31, 2022) | | | | | | | | | | | | | | | | |

| | | | | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | Expense Ratio1 | |

| | | | |

Investor Shares (AMAGX) | | | -0.62% | | | | 17.15% | | | | 14.98% | | | | 0.95% | |

| | | | |

Institutional Shares (AMIGX)2 | | | -0.40% | | | | 17.42% | | | | n/a | | | | 0.70% | |

| | | | |

S&P 500 Index | | | -0.30% | | | | 13.38% | | | | 14.39% | | | | n/a | |

Growth of $10,000

| | |

| | Comparison of any mutual fund to a market index must be made bearing in mind that the index is unmanaged and expense-free. Conversely, the Fund will (1) be actively managed; (2) have an objective other than mirroring the index, such as limiting risk; (3) bear transaction and other operational costs; (4) stand ready to buy and sell its securities to shareowners on a daily basis; and (5) provide a wide range of services. The graph compares $10,000 invested in Investor Shares of the Fund on May 31, 2012, to an identical amount invested in the S&P 500 Index, a broad-based stock market index. The graph shows that an investment in Investor Shares of the Fund would have risen to $40,372 versus $38,377 in the Index. Investor Shares are used in this chart because they represent the larger share class in terms of assets and have a longer track record. Please note that investors cannot invest directly in the Index. |

Past performance does not guarantee future results. The “Growth of $10,000” graph and “Average Annual Returns” performance table assume the reinvestment of dividends and capital gains. They do not reflect the deduction of taxes that a shareowner might pay on fund distributions or the redemption of fund shares.

| 1 | Expense ratios shown in this table have been restated to reflect a reduction in the Advisory and Administrative Services fee, which became effective on December 1, 2020. Ratios presented in this table differ from the expense ratios shown elsewhere in this report as they represent older fiscal periods. |

| 2 | Institutional shares of the Amana Growth Fund began operations September 25, 2013. |

Fund Objective

The objective of the Growth Fund is long-term capital growth, consistent with Islamic principles.

| | | | |

Top 10 Holdings | |

| |

| % of Total Net Assets | |

| |

Apple | | | 9.5% | |

| |

ASML Holding NY | | | 5.6% | |

| |

Intuit | | | 5.5% | |

| |

Adobe | | | 4.4% | |

| |

Estee Lauder, Class A | | | 3.7% | |

| |

Taiwan Semiconductor ADR | | | 3.7% | |

| |

Agilent Technologies | | | 3.6% | |

| |

Novo Nordisk ADR | | | 3.5% | |

| |

Eli Lilly | | | 3.5% | |

| |

Church & Dwight | | | 3.4% | |

| | | | | | | | | | | | |

Portfolio Diversification | | | | | | | | | | | | |

| | | |

| % of Total Net Assets | | | | | | | | | |

| | | |

Communications Equipment | | | 13.7% | | | ∎ | | | |

|

|

|

Large Pharma | | | 10.7% | | | ∎ | | |

Application Software | | | 9.9% | | | ∎ | | |

Semiconductor Manufacturing | | | 9.3% | | | ∎ | | |

Household Products | | | 7.1% | | | ∎ | | |

Measurement Instruments | | | 5.5% | | | ∎ | | |

Rail Freight | | | 4.0% | | | ∎ | | |

Life Science Equipment | | | 3.6% | | | ∎ | | |

Semiconductor Devices | | | 3.5% | | | ∎ | | |

Home Products Stores | | | 3.4% | | | ∎ | | |

Specialty Apparel Stores | | | 3.2% | | | ∎ | | |

Other industries < 3.0% | | | 16.7% | | | ∎ | | |

Other Assets (net of liabilities) | | | 9.4% | | | ∎ | | |

| | | | | | |

|

| | | |

| Annual Report | | May 31, 2022 | | | | 15 |

| | |

| Amana Growth Fund: Discussion of Fund Performance | | (unaudited) |

Fiscal Year 2022

For the fiscal year ended May 31, 2022, the Investor Shares of the Amana Growth Fund returned -0.62% (versus 42.16% the year before). Reflecting its lower expense structure, the Institutional Shares returned -0.40% for the year. Both slightly trailed the broad S&P 500 Index, which declined -0.30%.

While income is not an investment objective, the Amana Growth Fund paid a qualified income dividend at $0.05 per Investor Share and $0.21 per Institutional Share. All shareowners received a capital gain distribution of $0.33 per share. Higher assets helped to lower the expense ratio: 0.91% for Investor Shares and 0.64% for Institutional Shares. The Fund’s total net assets increased 4.88% during the fiscal year.

For the 15-year period ended May 31, 2022, the Investor Shares of the Amana Growth Fund provided an average annual total return of 10.62%. Since the Fund’s inception on February 3, 1994, the Investor Shares provided an average annual total return of 11.65%.

Factors Affecting Past Performance

Following a three-year stretch of remarkable equity market returns, stock indices sharply declined in the first five months of 2022 due to rapidly accelerating inflation and concurrently rising interest rates. The stock market correction, which subsequently evolved into a bear market (as measured by a 20% decline in the S&P 500 from its peak at the start of the year), followed a rational progression. As persistent inflation raised expectations for rate hikes, Technology companies with minimalist earnings and maximalist valuations based on the promise of future growth were hit especially hard. Other “long-duration” equities such as e-commerce and internet media mega-cap stocks were also sold down, dragging down Consumer Cyclical and Communication sector indices. Higher interest rates brought recession risk to the fore, leading to weakness among Industrial and Consumer Staples stocks. Eventually, war and growing geopolitical concerns pushed down the prices of defensive stocks such as Utilities and parts of Health Care. At the same time, the bond market suffered its worst start to the year in decades. Except for Energy, hiding places were few and far-between.

Several companies that led the Amana Growth Fund’s returns in calendar year 2021 have suffered the largest declines, both year-to-date and for the 2022 fiscal year. These include ASML, Johnson Controls, and Taiwan Semiconductor. Our best performers were concentrated among major pharmaceutical stocks including Eli Lilly, Novo-Nordisk, and Johnson & Johnson. Gold producer Newmont also provided positive returns as the yellow metal demonstrated its characteristic flight to quality attraction.

Our portfolio of well-established equities has more than 5% in each of the following industries: retail, pharmaceuticals, electronics, computers, semiconductors, and software.

Environmental, social, and governance (ESG) issues received increased attention with the COVID-19 pandemic, including the risks surrounding the physical and transitional risks of climate change. As climate-conscious investors, we are pleased to report that Morningstar continues to designate Amana Growth Fund a “Low Carbon” fund. Carbon, climate, and the environment constitute only one pillar of ESG. We are also concerned with social and governance issues and, as values-based investors, we are pleased that Morningstar rated the Fund in the top 4% for sustainability out of 1,575 funds in its “Large Growth” fund category for the 2022 fiscal year. See pages 6-7 for more details.

Looking Forward

Year-to-date economic statistics have settled the inflation debate. Exacerbated by Russia’s invasion of Ukraine (which sparked higher oil and food prices) and Shanghai’s COVID-19 lockdown (which further roiled supply chains), inflation remains high, and the Federal Reserve has taken aggressive action to tame the beast. At fiscal year-end, the federal funds rate stood at 1.75% versus 0.25% a year ago. Regardless, more needs to be done and Fed governors are unanimous in their expectations that the rate will exceed 3% by year-end. Can rates be raised by such an amount without pushing the economy into recession? Historical precedent suggests not. Rising rates will also provide support for a strengthening US dollar, which has already appreciated significantly against leading international currencies such as the euro and the Japanese yen. Major currency moves tend to have unanticipated ramifications. Nonetheless, we expect any potential recession to be mild as consumer leverage remains low, while we see little risk of the tremendous wealth destruction that made the Great Recession of 2008/09 so disruptive. We believe our portfolio of highly cash-generative companies with minimal debt is well-positioned to weather a period of economic weakness and emerge stronger on the other side.

| | | | | | |

|

| | | |

| 16 | | | | Annual Report | | May 31, 2022 |

| | |

| Amana Growth Fund: Schedule of Investments | | As of May 31, 2022 |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | Common Stocks – 90.6% | | | | Number of Shares | | | Cost | | | Market Value | | | Percentage of Net Assets | |

| | | | | | |

| | | Communications | | | | | | | | | | | | | | |

| | | | | | | |

| | | Internet Media | | | | | | | | | | | | | | |

| | | | | | | |

| | | Alphabet, Class A1 | | | | | 12,500 | | | | $27,109,896 | | | | $28,440,500 | | | | 0.9% | |

| | | | | | | |

| | | | | | | | | | | 27,109,896 | | | | 28,440,500 | | | | 0.9% | |

| | | | | | |

| | | Consumer Discretionary | | | | | | | | | | | | | | |

| | | | | | | |

| | | Apparel, Footwear & Accessory Design | | | | | | | | | | | | | | |

| | | | | | | |

| | | Nike, Class B | | | | | 100,000 | | | | 9,504,490 | | | | 11,885,000 | | | | 0.4% | |

| | | | | | | |

| | | Home Products Stores | | | | | | | | | | | | | | |

| | | | | | | |

| | | Home Depot | | | | | 100,000 | | | | 39,180,840 | | | | 30,275,000 | | | | 0.9% | |

| | | | | | | |

| | | Lowe’s | | | | | 400,000 | | | | 8,620,300 | | | | 78,120,000 | | | | 2.5% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 47,801,140 | | | | 108,395,000 | | | | 3.4% | |

| | | | | | | |

| | | Specialty Apparel Stores | | | | | | | | | | | | | | |

| | | | | | | |

| | | Lululemon Athletica1 | | | | | 100,000 | | | | 33,874,229 | | | | 29,269,000 | | | | 0.9% | |

| | | | | | | |

| | | TJX Companies | | | | | 1,150,000 | | | | 12,679,185 | | | | 73,105,500 | | | | 2.3% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 46,553,414 | | | | 102,374,500 | | | | 3.2% | |

| | | | | | | |

| | | | | | | | | | | 103,859,044 | | | | 222,654,500 | | | | 7.0% | |

| | | | | | |

| | | Consumer Staples | | | | | | | | | | | | | | |

| | | | | | | |

| | | Household Products | | | | | | | | | | | | | | |

| | | | | | | |

| | | Church & Dwight | | | | | 1,200,000 | | | | 21,472,365 | | | | 108,072,000 | | | | 3.4% | |

| | | | | | | |

| | | Estee Lauder, Class A | | | | | 458,594 | | | | 16,624,230 | | | | 116,780,962 | | | | 3.7% | |

| | | | | | | |

| | | | | | | | | | | 38,096,595 | | | | 224,852,962 | | | | 7.1% | |

| | | | | | |

| | | Health Care | | | | | | | | | | | | | | |

| | | | | | | |

| | | Biotech | | | | | | | | | | | | | | |

| | | | | | | |

| | | Amgen | | | | | 355,000 | | | | 18,341,782 | | | | 91,142,700 | | | | 2.9% | |

| | | | | | | |

| | | Large Pharma | | | | | | | | | | | | | | |

| | | | | | | |

| | | AstraZeneca ADR | | | | | 780,000 | | | | 53,378,052 | | | | 51,854,400 | | | | 1.6% | |

| | | | | | | |

| | | Eli Lilly | | | | | 350,000 | | | | 12,007,975 | | | | 109,704,000 | | | | 3.5% | |

| | | | | | | |

| | | Johnson & Johnson | | | | | 380,000 | | | | 23,150,478 | | | | 68,221,400 | | | | 2.1% | |

| | | | | | | |

| | | Novo Nordisk ADR | | | | | 1,002,195 | | | | 7,665,243 | | | | 110,642,328 | | | | 3.5% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 96,201,748 | | | | 340,422,128 | | | | 10.7% | |

| | | | | | | |

| | | Life Science Equipment | | | | | | | | | | | | | | |

| | | | | | | |

| | | Agilent Technologies | | | | | 900,000 | | | | 16,302,137 | | | | 114,804,000 | | | | 3.6% | |

| | | | | | | |

| | | Medical Devices | | | | | | | | | | | | | | |

| | | | | | | |

| | | Stryker | | | | | 300,000 | | | | 15,657,168 | | | | 70,350,000 | | | | 2.2% | |

| | | | | | | |

| | | | | | | | | | | 146,502,835 | | | | 616,718,828 | | | | 19.4% | |

| | | | | | |

| | | Industrials | | | | | | | | | | | | | | |

| | | | | | | |

| | | Commercial & Residential Building Equipment & Systems | | | | | | | | | | | | | | |

| | | | | | | |

| | | Johnson Controls International | | | | | 1,044,000 | | | | 48,905,901 | | | | 56,908,440 | | | | 1.8% | |

| | | | | | | |

| | | Industrial Distribution & Rental | | | | | | | | | | | | | | |

| | | | | | | |

| | | Fastenal | | | | | 633,000 | | | | 7,613,244 | | | | 33,903,480 | | | | 1.1% | |

| | | | | | | |

| | | Measurement Instruments | | | | | | | | | | | | | | |

| | | | | | | |

| | | Keysight Technologies1 | | | | | 500,000 | | | | 8,390,911 | | | | 72,800,000 | | | | 2.3% | |

| | | | | | | |

| | | Trimble1 | | | | | 1,500,000 | | | | 15,966,794 | | | | 102,075,000 | | | | 3.2% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 24,357,705 | | | | 174,875,000 | | | | 5.5% | |

Continued on next page.

| | | | | | | | |

|

| | | | |

| The accompanying notes are an integral part of these financial statements. | | Annual Report | | May 31, 2022 | | | | 17 |

| | |

| Amana Growth Fund: Schedule of Investments | | As of May 31, 2022 |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | Common Stocks – 90.6% | | | | Number of Shares | | | Cost | | | Market Value | | | Percentage of Net Assets | |

| | | | | | |

| | | Industrials (continued) | | | | | | | | | | | | | | |

| | | | | | | |

| | | Metalworking Machinery | | | | | | | | | | | | | | |

| | | | | | | |

| | | Lincoln Electric Holdings | | | | | 307,000 | | | | $6,707,264 | | | | $41,696,740 | | | | 1.3% | |

| | | | | | | |

| | | Rail Freight | | | | | | | | | | | | | | |

| | | | | | | |

| | | Norfolk Southern | | | | | 250,000 | | | | 14,370,513 | | | | 59,915,000 | | | | 1.9% | |

| | | | | | | |

| | | Union Pacific | | | | | 300,000 | | | | 16,986,610 | | | | 65,934,000 | | | | 2.1% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 31,357,123 | | | | 125,849,000 | | | | 4.0% | |

| | | | | | | |

| | | | | | | | | | | 118,941,237 | | | | 433,232,660 | | | | 13.7% | |

| | | | | | |

| | | Materials | | | | | | | | | | | | | | |

| | | | | | | |

| | | Agricultural Chemicals | | | | | | | | | | | | | | |

| | | | | | | |

| | | Corteva | | | | | 145,000 | | | | 7,702,357 | | | | 9,079,900 | | | | 0.3% | |

| | | | | | | |

| | | Precious Metal Mining | | | | | | | | | | | | | | |

| | | | | | | |

| | | Newmont | | | | | 750,000 | | | | 42,354,995 | | | | 50,887,500 | | | | 1.6% | |

| | | | | | | |

| | | | | | | | | | | 50,057,352 | | | | 59,967,400 | | | | 1.9% | |

| | | | | | |

| | | Technology | | | | | | | | | | | | | | |

| | | | | | | |

| | | Application Software | | | | | | | | | | | | | | |

| | | | | | | |

| | | Adobe1 | | | | | 329,950 | | | | 10,859,053 | | | | 137,417,576 | | | | 4.4% | |

| | | | | | | |

| | | Intuit | | | | | 422,950 | | | | 14,637,022 | | | | 175,295,857 | | | | 5.5% | |

| | | | | | | |

| | | SAP ADR | | | | | 10,050 | | | | 660,522 | | | | 1,003,392 | | | | 0.0% | 2 |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 26,156,597 | | | | 313,716,825 | | | | 9.9% | |

| | | | | | | |

| | | Communications Equipment | | | | | | | | | | | | | | |

| | | | | | | |

| | | Apple | | | | | 2,016,000 | | | | 1,526,905 | | | | 300,061,440 | | | | 9.5% | |

| | | | | | | |

| | | Cisco Systems | | | | | 1,500,000 | | | | 26,759,130 | | | | 67,575,000 | | | | 2.1% | |

| | | | | | | |

| | | Motorola Solutions | | | | | 310,000 | | | | 79,705,054 | | | | 68,119,400 | | | | 2.1% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 107,991,089 | | | | 435,755,840 | | | | 13.7% | |

| | | | | | | |

| | | Information Services | | | | | | | | | | | | | | |

| | | | | | | |

| | | Gartner1 | | | | | 179,900 | | | | 6,185,085 | | | | 47,205,760 | | | | 1.5% | |

| | | | | | | |

| | | Infrastructure Software | | | | | | | | | | | | | | |

| | | | | | | |

| | | Microsoft | | | | | 120,000 | | | | 30,150,399 | | | | 32,624,400 | | | | 1.0% | |

| | | | | | | |

| | | Oracle | | | | | 737,200 | | | | 21,467,457 | | | | 53,019,424 | | | | 1.7% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 51,617,856 | | | | 85,643,824 | | | | 2.7% | |

| | | | | | | |

| | | Semiconductor Devices | | | | | | | | | | | | | | |

| | | | | | | |

| | | Advanced Micro Devices1 | | | | | 674,194 | | | | 8,547,213 | | | | 68,673,401 | | | | 2.1% | |

| | | | | | | |

| | | Qualcomm | | | | | 304,350 | | | | 11,757,385 | | | | 43,589,007 | | | | 1.4% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 20,304,598 | | | | 112,262,408 | | | | 3.5% | |

| | | | | | | |

| | | Semiconductor Manufacturing | | | | | | | | | | | | | | |

| | | | | | | |

| | | ASML Holding NY | | | | | 308,000 | | | | 10,937,644 | | | | 177,497,320 | | | | 5.6% | |

| | | | | | | |

| | | Taiwan Semiconductor ADR | | | | | 1,222,471 | | | | 12,765,781 | | | | 116,501,486 | | | | 3.7% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | 23,703,425 | | | | 293,998,806 | | | | 9.3% | |

| | | | | | | |

| | | | | | | | | | | 235,958,650 | | | | 1,288,583,463 | | | | 40.6% | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | Total investments | | | | | | | | | $720,525,609 | | | | $2,874,450,313 | | | | 90.6% | |

| | | | | | |

| | Other assets (net of liabilities) | | | | | | | | | | | | | 299,771,646 | | | | 9.4% | |

| | | | | | |

| | Total net assets | | | | | | | | | | | | | $3,174,221,959 | | | | 100.0% | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

ADR: American Depositary Receipt

| | | | | | | | |

|

| | | | |

| 18 | | | | Annual Report | | May 31, 2022 | | The accompanying notes are an integral part of these financial statements. |

Amana Growth Fund