SECOND QUARTER REPORT

For The Six Months Ended

June 30, 2012

MANAGEMENT DISCUSSION & ANALYSIS OF FINANCIAL STATEMENTS

MINERAL PROPERTY SUMMARIES

Date of Report – August 21, 2012

S A M E X M I N I N G C O R P.

SAMEX MINING CORP. 301 - 32920 Ventura Ave. Abbotsford, BC V2S 6J3 CANADA | | TEL: (604) 870-9920 FAX: (604) 870-9930 TOLL FREE: 1-800-828-1488 EMAIL: 2samex@samex.com | | WEB: www.samex.com TRADING SYMBOLS: SXG - TSX Venture Exch. SMXMF - OTCQB |

S A M E X M I N I N G C O R P.

Second Quarter 2012

Exploration and Evaluation Asset Costs - $1,484,421 Mineral Interest Administration and Investigation Costs - $96,776 Los Zorros Property, Chile 4,440 Meters of Drilling in 9 Drill Holes

Gold and Silver Bullion Holdings Had Fair Value Of $5,990,122 At June 30, 2012

This Document Includes:

MANAGEMENT DISCUSSION & ANALYSIS OF FINANCIAL STATEMENTS,

MINERAL PROPERTY SUMMARIES

|

SAMEX is exploring in the mineral-rich country of Chile that hosts some of the world’s largest ore bodies.

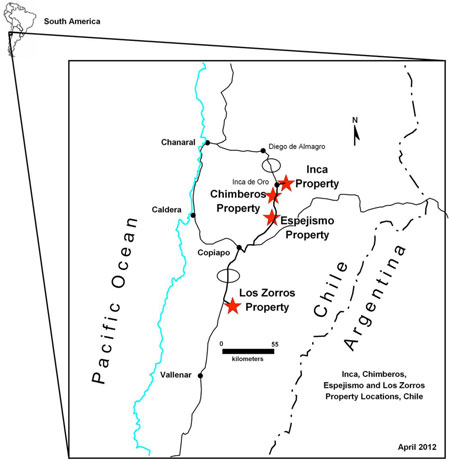

SAMEX MINERAL EXPLORATION PROPERTIES IN CHILE

LOS ZORROS PROPERTY - Gold, Silver, Copper Prospects

The Los Zorros Property covers an old mining district of small gold, silver and copper mines and showings. SAMEX is conducting exploration at a number of individual exploration project areas within this single property holding to test for multiple ore bodies:

MILAGRO PROJECT LA FLORIDA PROJECT | | NORA PROJECT LORA PROJECT | | CINCHADO PROJECT COLORINA PROJECT | | MILAGRO PAMPA PROJECT VIRGEN de CARMEN PROJECT |

The Los Zorros Property also includes other project areas yet to be systematically explored by SAMEX including:, SALVADORA, CRESTA DE GALLO and TRUENO (barite vein systems with possible deeper-seated gold and copper-gold) and GRINGO (copper-gold). |

CHIMBEROS PROPERTY - Gold, Silver, Copper Prospects |

INCA PROPERTY - Copper, Gold, Silver, Moly Prospects |

ESPEJISMO PROPERTY - Gold Prospects |

Website - www.samex.com

SAMEX trades in Canada on the TSX Venture Exchange - symbol: SXG

SAMEX is quoted in the United States on the OTCQB - symbol: SMXMF

MANAGEMENT DISCUSSION

DATE: August 21, 2012

SAMEX Mining Corp. is a junior resource company engaged in the acquisition and exploration of mineral properties in South America, particularly in the country of Chile. The Company focuses its exploration activities on the search for deposits of precious and base metals. SAMEX management is motivated by a strong conviction that gold and silver are precious, valuable “hard assets”. SAMEX has persistently maintained and declared its strong belief that gold and silver prices are significantly undervalued. Our objective is to be well-positioned to benefit from increases in the value of gold and silver and a strong demand for copper.

In Chile, the Company holds an interest in the Los Zorros district gold-copper-silver prospects, the Chimberos gold-silver prospects, the Inca copper, gold, silver and molybdenum prospects, and the Espejismo gold prospects. See the section in this report titled “Mineral Property Summaries” for individual property details. The Company also holds an interest in mineral exploration properties in Bolivia, however in 2009, the Company suspend exploration activities in Bolivia and put all of the Bolivian properties on “care and maintenance” status. We are an exploration stage company and have no mineral producing properties at this time. All of our properties are exploration projects, and we receive no revenues from production. All work presently planned by us is directed at defining mineralization and increasing our understanding of the characteristics and economics of that mineralization. There is no assurance that a commercially viable ore deposit exists in any of our properties until further exploration work is conducted and a comprehensive evaluation based upon unit cost, grade, recoveries and other factors conclude economic feasibility. The information contained herein respecting our mineral properties is based upon information prepared by, or the preparation of which was supervised by, Robert Kell, a Director and the Vice President-Exploration of SAMEX, and SAMEX geologist, Philip Southam, P.Geo. Mr. Kell and Mr. Southam are “qualified persons” pursuant to Canadian Securities National Instrument 43-101 concerning Standards Of Disclosure For Mineral Projects.

The Company carries out all normal procedures to obtain title and makes a conscientious search of mining records to confirm that the Company has satisfactory title to the properties it has acquired by staking, purchase or option, and/or that satisfactory title is held by the optionor/owner of properties the Company may acquire pursuant to an option agreement, and/or that satisfactory title is held by the owner of properties in which the Company has earned a percentage interest in the property pursuant to a joint venture or other type of agreement. However, the possibility exists that title to one or more of the concessions held by the Company, or an optionor/owner, or the owner of properties in which the Company has earned a percentage interest, might be defective for various reasons. The Company will take all reasonable steps to perfect title to any particular concession(s) found to be in question.

SAMEX is a reporting issuer in British Columbia and Alberta and trades in Canada on the TSX Venture Exchange under the symbol SXG. News releases can be viewed on the Company’s website at www.samex.com or at www.sedar.com. The Company is also quoted in the United States on the OTCQB under the symbol SMXMF.

This discussion contains forward-looking statements, the accuracy of which involves risks and uncertainties and our actual results could differ materially from those anticipated in the forward-looking statements for many reasons, including, but not limited to, those risk factors described elsewhere in this report. See note “Forward Looking Statements” at end of this report.

OVERVIEW OF RESULTS FOR THE SIX MONTHS ENDED JUNE 30, 2012

The following section contains a summary of our operating results for the six months ended June 30, 2012, which is qualified by detailed descriptions that follow elsewhere in this document. This section also contains a number of ‘forward looking statements’ which, although intended to be accurate, may be affected by a number of risks and uncertainties that may cause them to be materially different from actual outcomes. See “Forward Looking Statements” at the end of this report.

As a junior exploration company, our operations are significantly affected by a number of external factors, particularly those that affect the price of the commodities we explore for or those that affect the market for our securities. During the first six months of 2012, the global economy was still experiencing the after-shocks of the 2008-2009 financial crisis, as well as the impact of measures taken to counteract its effects. While improvements were noted, particularly in Canada and certain emerging economies, many parts of the world experienced only modest or negative growth during 2012. The United States continued to experience sluggish growth and persistent high levels unemployment along with large fiscal deficits and unprecedented levels of government debt, which reached a staggering $15.9 trillion by June 30, 2012. These and other factors gave rise to mounting concerns about the ability of the US government to manage its sovereign debt and led to the historic loss of its AAA credit rating during 2011. Conditions throughout the Euro-zone area continued to deteriorate with most member countries experiencing very low or negative growth by, and growing concern over a possible sovereign debt default in Greece and other countries, leading to widespread concern over the possible collapse of the Euro-zone as now constituted, the failure of the Euro as an international reserve currency and the possibility of contagion. In addition, new concerns began to develop over the appearance of asset bubbles in China, leading to fears of a wider slowdown.

In light of, and likely in response to these and other factors, the price of gold rose significantly during 2011 reaching over $1,900 in August, 2011 before dropping back to a $1,700 to $1,600 range where it currently trades. Silver rose to over $48 in April 2011 before dropping back to a $30-32 range by year end, and is currently trading in the $27 to $28 range. Along with the increase in precious metal prices, the market for shares of junior precious metal explorers also improved, offering greater access to capital during the first half of 2011. Since then, precious metal prices have declined somewhat but remain relatively strong with some volatility, however, the market for the shares of junior exploration companies has declined significantly, making it much more difficult for companies to raise capital for exploration. While this has not had a direct effect on the Company since we currently have sufficient funds on hand to cover our anticipated expenditures during the upcoming year, it may impact our future operations since we are dependent upon our ability to access capital markets in order to fund our programs.

The Company raised substantial private placement funding during the later part of 2010 and received significant proceeds from the exercise of warrants during 2011, which allowed us to increase our staff and expand our exploration activities and expenditures. For the three months ended June 30, 2012, "Exploration And Evaluation Assets" costs totaled $1,484,421 and "Mineral Interests Administration And Investigation" expenses totaled $96,776.

Los Zorros Property, Chile - The Los Zorros property consists of multiple project areas that have now been strategically expanded to cover more than 100 square kilometers within a district of scattered numerous small mines and prospects where there was sporadic attempts at small-scale production for gold and copper-silver in the past. SAMEX is exploring for multiple precious metal deposits that may be clustered beneath the widespread precious metal occurrences in this district of historic small mining activity. The property is situated at the convergence of important geologic and structural features and significant gold and copper-silver mineralized areas of Cinchado, Nora, Milagro, and Milagro Pampa. There are also many other mineral occurrences at Los Zorros including: La Florida and Lora (gold and copper-gold), Virgen de Carmen and Colorina (copper-silver; possible deeper-seated gold and copper-gold), and Salvadora, Cresta de Gallo, and Trueno (barite vein systems with possible deeper-seated gold and copper-gold) and Gringo (copper-gold).

The Company has 100% interest in approximately 7,774 hectares of mineral concessions acquired by staking, purchase at government auction, purchase agreement, and by two purchase option contracts. And to further expanded the Los Zorros land holdings, we signed the Aravena Option in 2011 to acquire additional mineral concessions adjacent to the Los Zorros property. The Los Zorros land holdings now cover a 15 kilometer-strike of the prospective range front/anticline along which mineralization is exposed in old-time piquenero underground workings, open cuts, trenches and pits situated in the Colorina, Nora, Virgen del Carmen, Cresta de Gallo, and Trueno project areas.

Option Payment Made On the Aravena Option - During the three months ended March 31, 2012 we made an option payment of US$95,345 on the Aravena Option. Pursuant to the option contract dated June 28, 2011, we can acquire a 100% interest in approximately 2,900 hectares of mineral concessions adjacent to the Los Zorros property by making option payments totaling the Chilean peso equivalent of U.S. $245,345 as follows: U.S. $60,000 on signing (paid); U.S. $95,345 due January 31, 2012 (paid) and U.S. $90,000 due January 31, 2013. Of particular significance, the final option payment of US$90,000 due January 31, 2013, is the only acquisition payment remaining on our extensive accumulated land holdings at Los Zorros.

Final Advance Royalty Payment Made – During the first quarter of 2012, we also made the final advance royalty payment of US$100,000 (in Chilean peso equivalent) in relation to a 209-hectare-portion of the Los Zorros property which the Company had acquired under the “Hochschild Option/Purchase”. Pursuant to the terms of the agreement, if the concessions were not in production by December 31, 2007, advance royalty payments of US$100,000 per year were required for five years: by February 29, 2008 (paid), by March 1, 2009 (paid), by March 1, 2010 (paid), by March 1, 2011 (paid), and by March 1, 2012 (paid) to a maximum of US$500,000 ($500,000 paid). The advance royalty payments are recoverable from future royalty payments.

During the first quarter of 2012, the Company continued a drilling program at Los Zorros that had commenced in July 2011. Exploration during the three months ended March 31, 2011 included 4,745 meters of drilling in 10 drill holes and bulldozer work to construct access roads, drill pads and trenches. Drilling during the first quarter of 2012 was conducted in the Nora, Milagro, Cinchado, and Lora SE project areas which are some of the multiple projects being explored within the Company's extensive landholdings that comprise the Los Zorros Property. During the first quarter, drill pads were also prepared in the Virgen del Carmen, Colorina, Milagro and Florida project areas. We also continued to further expand the Los Zorros camp facilities to accommodate the additional geologists and support workers involved in the exploration and drilling activities.

During the second quarter ended June 30, 2012 exploration continued at Los Zorros including 4,440 meters of drilling in 9 drill holes. At the time of this report, we are awaiting the continuing processing of core and the compilation of results from drilling in the Cinchado, Laura SE, Nora, Milagro, Florida, and Milagro Pampa project areas.

For details concerning exploration results and activities, see "Los Zorros Property" in the "Mineral Property Summaries" section of this MD&A report. The results and exploration activity are part of an ongoing drill program at Los Zorros, which is continuing at the time of this report. The major private placement funding we secured in the fourth quarter of 2010 along with proceeds of more than $4.6 million from exercise of warrants during 2011 has provided us with the financial resources to explore numerous project areas and prospective targets within the Los Zorros property holdings.

INCA Property, Chile - We continue to conduct meetings with parties interested in our INCA copper-gold-moly property in Chile in an effort to arrange a joint venture or sale of all or a portion of the INCA property. Our landholdings at the INCA project now consist of approximately 8,866 hectares of prospective and strategic concessions including the 45-hectare Providencia Mine concessions that we acquired in 2009 pursuant to the “Araya Option” and the 20 hectares of concessions we purchased during 2011 pursuant the Rojas Option/Purchase.

Trends and Financing - Over the past several years, we have experienced a number of important external changes in the market place that had an affect on our overall performance. In the latter part of 2008, commodity prices, particularly the price of copper, began a serious decline, eventually falling to a five year low. Shortly thereafter, we found ourselves in the middle of a global economic crisis, with its actual or threatened bank failures, major international liquidity issues, and a general slowdown leading to a global recession. These events also fed into both the decline in commodity prices and a decline in the share prices of most public companies including in particular junior resource stocks such as ours, which greatly reduced our ability to raise capital. During that time, we were able to raise additional capital by private placements, but at lower prices and less favourable terms than our private placements completed in the previous several years. While many parts of the world - particularly developing countries - had largely recovered from the financial crisis by late 2011, many countries - particularly the US and Euro-zone countries - are still experiencing slow growth, high unemployment and other economic stresses. These and other factors have led to strong prices with considerable volatility for many commodities, particularly gold and silver and copper. Along with this, after a brief improvement early in 2011, the market for the shares of junior precious metal explorers has significantly declined which may affect our future ability to access capital to fund mineral exploration projects. We anticipate that the price of gold, silver, and copper will likely be sustained at or near current levels, with continued volatility, with the possibility of significant rapid price increases due to prevailing global economic imbalances and other continuing economic conditions.

Gold and Silver Bullion Holdings - The Company has a portion of its liquid assets in gold and silver bullion to hold in lieu of cash. At June 30, 2012, the Company held 87,307 grams of gold and 49,818 ounces of silver which had a fair value of $5,990,122. Gold and silver bullion is measured at fair value through the statement of comprehensive loss. There was a loss of $301,240 on the gold and silver bullion holdings for the three months ended June 30, 2012. This amount offset a gain of $494,292 on the gold and silver bullion holdings for the three months ended March 31, 2012, resulting in a gain of $193,052 on the gold and silver bullion holdings for the six month period ended June 30, 2012.

During the three months ended June 30, 2012 there was a loss from operations of $421,165 (see consolidated statements of comprehensive loss) and a loss of $301,240 on the gold and silver bullion holdings resulting in net and comprehensive loss of $722,405 for the three month period ended June 30, 2012.

Plans and Projections – SAMEX exploration activities will continue to be focused on its high quality gold and silver projects in Chile including the Los Zorros property and the Chimberos property. The Company will also continue to conduct meetings and property tours with parties interested in our INCA copper-gold-moly property in Chile in an effort to arrange a joint venture or sale of all or a portion of the INCA property. See “Liquidity and Capital Resources” and “Anticipated Capital Requirements”. See note “Forward Looking Statements” at the end of this report.

Bolivia: Bolivian Properties Remain In “Care And Maintenance” Status – In 2009, the Company suspended exploration activities in Bolivia and put the Bolivian properties on “care and maintenance” status. In the several years leading up to this decision, we had been monitoring with concern a number of changes in the political climate in Bolivia. Over that time, the political climate for resource companies continued to deteriorate with events such as the nationalization of Bolivia’s natural gas resources, a moratorium on the grant of new mineral exploration licenses, a national referendum that resulted in constitutional changes and requirements that all mining projects be conducted only in partnership with the state mining company – on economically unfavorable terms. In light of these and other factors we decided that Bolivia carried a significant risk for development of future mineral projects. Accordingly in 2009 we minimized our activities in Bolivia by suspending exploration activities, putting all of our Bolivian projects on “care and maintenance” status, and reducing our Bolivian office, staff, and operating expenses. Each year, we continue to pay the annual patentes required to maintain the mineral concessions. Due to the inactivity on the Bolivian properties, the property interest for the Eskapa Property, the El Desierto Property and the Santa Isabel Property was each written down to a nominal value of $1,000 resulting in a combined valuation of only $3,000 for our Bolivian properties at December 31, 2011. While we hope we will be able to return to exploring our Bolivian properties at some time in the future, we do not anticipate we will be able to do so as long as current political conditions persist.

ANALYSIS OF FINANCIAL STATEMENTS

International Financial Reporting Standards - As result of the Accounting Standards Board of Canada’s decision to adopt International Financial Reporting Standards ("IFRS") for publicly accountable entities for financial reporting periods beginning on or after January 1, 2011, the Company adopted IFRS in its financial statements for the year ended December 31, 2011. The interim consolidated financial statements of the Company for the three months ended June 30, 2012 are also reported under IFRS. We have prepared the interim consolidated financial statements for the three months ended June 30, 2012 using the same accounting policies and critical accounting estimates we applied in our consolidated financial statement for the year ended December 31, 2011. The Company previously applied the available standards under previous Canadian Accepted Accounting Principles ("Canadian GAAP") that were issued by the Accounting Standards Board of Canada. The effects of the conversion from Canadian GAAP to IFRS were identified in Note 12 "Transition To IFRS" of our consolidated financial statements for the year ended December 31, 2011. As required by IFRS 1 “First-time Adoption of International Financial Reporting Standards”, January 1, 2010 was considered to be the date of transition to IFRS by the Company. Therefore, the comparative figures that were previously reported under previous Canadian GAAP were restated in accordance with IFRS. Our consolidated financial statements have been prepared in Canadian dollars and in accordance with IFRS which differ in significant respects from accounting principles generally accepted in Canadian GAAP and from accounting principles generally accepted in the United States ("U.S. GAAP"). As such, this discussion of our financial condition and results of operations is based on the results prepared in accordance with IFRS.

The following discussion of our operating results explains material changes in our consolidated results of operations for the three months ended June 30, 2012. In order to synchronize the difference in quarter ends, these consolidated financial statements include the accounts of the Bolivian subsidiaries for their fiscal third quarters from April 1, 2012 to June 30, 2012. The discussion should be read in conjunction with the Company's consolidated financial statements to December 31, 2011 and the related notes included in this report. Management’s discussion and analysis of our operating results in this section is qualified in its entirety by, and should be read in conjunction with, the consolidated financial statements and notes thereto. This discussion contains forward-looking statements, the accuracy of which involves risks and uncertainties and our actual results could differ materially from those anticipated in the forward-looking statements for many reasons, including, but not limited to, those risk factors described elsewhere in this report.

Overview - Our business is exploration for minerals. We do not have any properties that are in production. We have no earnings and, therefore, finance these exploration activities by the sale of our equity securities or through joint ventures with other mineral exploration companies. The key determinants of our operating results include the following:

| a) | our ability to identify and acquire quality mineral exploration properties on favorable terms; |

| b) | the cost of our exploration activities; |

| c) | our ability to finance our exploration activities and general operations; |

| d) | our ability to identify and exploit commercial deposits of mineralization; and |

| e) | the write-down and abandonment of mineral properties as exploration results provide further information relating to the underlying value of such properties. |

These determinates are affected by a number of factors, most of which are largely out of our control, including the following:

| a) | the competitive demand for quality mineral exploration properties; |

| b) | political and regulatory climate in countries where properties of interest are located; |

| c) | regulatory and other costs associated with maintaining our operations as a public company; |

| d) | the costs associated with exploration activities; and |

| e) | the cost of acquiring and maintaining our mineral properties. |

Our primary capital and liquidity requirements relate to our ability to secure funds, principally through the sale of our securities, to raise sufficient capital to maintain our operations and fund our efforts to acquire mineral properties with attractive exploration targets and conduct successful exploration programs on them. We anticipate this requirement will continue until such time as we have either discovered sufficient mineralization on one or more properties with sufficient grade, tonnage and type to support the commencement of sustained profitable mining operations and are thereafter able to place such property or properties into commercial production or until we have obtained sufficient positive exploration results on one or more of our properties to enable us to successfully negotiate a joint venture with a mining company with greater financial resources than us or some other suitable arrangement sufficient to fund our operations.

Our success in raising equity capital is dependent upon factors which are largely out of our control including:

| a) | market prices for gold, silver, copper and other metals and minerals; |

| b) | the market for our securities; and |

| c) | the results from our exploration activities. |

Significant factors affecting our operations over the past several years has been the instability in the global financial situation and the related volatility in the demand for, and in the prices of precious and base metals. However, during 2010, lingering effects of the financial crisis and government responses to it - including high levels of government debt, adoption of expansionist monetary policies, Eurozone instability, the decline of the US dollar as a reserve currency and a growing sovereign debt crisis - contributed to a significant increase in the demand for, and in the price of, gold and silver. We believe this trend is likely to continue through the next year and possibly beyond. Improvement in metal prices also brought a corresponding improvement in the market for securities of precious metal exploration companies and our ability to raise capital during 2010 and 2011. While uncertainty over global financial conditions has led to significant increases in the price of gold and silver, it has also led to significant market instability and more recently, a decline in the market for junior resource companies. While we anticipate that improved metal prices will in due course improve the market for the securities of junior gold and silver explorers and therefore our ability to secure additional equity financing, the timing and extent of such effects cannot be accurately predicted. Metal prices cannot be predicted with accuracy and our plans will be largely dependent upon the timing and outcome of metal markets, particularly the price of gold, silver and copper which is entirely outside of our control. We also anticipate that our operating results would be significantly affected by the results of our exploration activities on our existing properties. See note titled “Forward Looking Statements” at the end of this report.

Currency Risk - Currency exchange rate fluctuations could adversely affect our operations. Our functional currency is the Canadian Dollar, and we have obligations and commitments in other currencies including Chilean Pesos, United States Dollars, and Bolivian Bolivianos. Fluctuations in foreign currency exchange rates may affect our results of operations and the value of our foreign assets, which in turn may adversely affect reported financial figures and the comparability of period-to-period results of operations.

Accounting Policies - We have adopted a number of accounting policies and made a number of assumptions and estimates in preparing our financial reporting, which are described in Note 2 to our consolidated financial statements for the year ended December 31, 2011. We have prepared the interim consolidated financial statements for the three months ended June 30, 2012 using the same accounting policies and critical accounting estimates we applied in our audited annual consolidated financial statement for the year ended December 31, 2011. These policies, assumptions and estimates significantly affect how our historical financial performance is reported and also your ability to assess our future financial results. In addition, there are a number of factors which may indicate our historical financial results, but will not be predictive of anticipated future results. You should carefully review the following disclosure, together with the attached consolidated financial statements and the notes thereto, and also in conjunction with the Company's audited annual consolidated financial statements for the year ended December 31, 2011.

Going Concern Assumptions - Our consolidated financial statements have been prepared on the assumption that we will continue as a going concern, meaning that we will continue in operation for the foreseeable future and will be able to realize assets and discharge our liabilities in the ordinary course of operations. We do not have any mineral properties in production, and have not yet generated any revenues and have a history of losses. Our continuation as a going concern is uncertain and dependent on our ability to discover commercial mineral deposits on our properties and place them into profitable commercial production and our ability to sustain our operations until such time. This, in turn depends on our ability to continue to fund our operations by the sale of our securities and other factors which are largely out of our control. Although we have been successful in the past in obtaining financing, it cannot be assured that adequate financing or financing on acceptable terms can be obtained in the future. In the event we cannot obtain the necessary funds, it will be necessary to delay, curtail or cancel further exploration on our properties. Our consolidated financial statements do not reflect adjustments to the carrying values and classifications of assets and liabilities that might be necessary should we not be able to continue in our operations, and the amounts recorded for such items may be at amounts significantly different from those contained in our consolidated financial statements.

Selected Annual Information & Summary of Quarterly Results

Selected Annual Information (1) | | IFRS Year Ended December 31, 2011 | | | IFRS Year Ended December 31, 2010 | | | Canadian GAAP Year Ended December 31, 2009 | |

| | | | | | | | | | |

| Revenue | | $ | - | | | $ | - | | | | - | |

| Loss from operations | | | 4,259,292 | | | | 1,163,026 | | | | 1,591,785 | |

| Net and comprehensive loss for the year | | | 3,845,201 | | | | 1,091,350 | | | | 4,282,770 | |

| Net loss per share | | | (0.03 | ) | | | (0.01 | ) | | | (0.05 | ) |

| Total assets | | | 23,654,987 | | | | 19,366,455 | | | | 10,154,038 | |

| Long-term liabilities | | | - | | | | - | | | | - | |

(1) Fiscal 2011 and 2010 are reported under IFRS. Fiscal 2009 is reported under Canadian GAAP. See "International Financial Reporting Standards" above.

The following summary of quarterly results for 2012, 2011 and 2010 are reported under IFRS:

Quarterly Results | | June 30, 2012 | | Mar 31, 2012 | | Dec 31, 2011 | | Sep 30, 2011 | | June 30, 2011 | | Mar 31, 2011 | | Dec 31, 2010 | | Sep 30, 2010 |

| Revenue $ | | - | | - | | - | | - | | - | | - | | - | | - |

| Net and comprehensive (earnings) loss $ | | 722,405 | | (106,600) | | 856,284 | | (74,635) | | 2,738,780 | | 324,772 | | 337,513 | | 238,480 |

| Net (earnings) loss /share $ | | (0.01) | | (0.01) | | 0.01 | | (0.01) | | 0.02 | | 0.01 | | 0.01 | | 0.01 |

The loss for the third quarter ended September 30, 2010 includes a stock-based compensation expense of $99,720 in relation to stock options granted on 430,000 shares at $0.35 per share to three employees and a consultant. The loss for the fourth quarter ended December 31, 2010 includes increased expenses incurred during the fourth quarter in the categories "Legal", "Office, Supplies, and Miscellaneous", "Regulatory Fees", "Salaries, Benefits and Stock-based Compensation", "Travel and Promotion", and "Mineral Interests Written Off". The loss for the first quarter ended March 31, 2011 includes a stock-based compensation expense of $132,130 in relation to a stock option granted to a new director on 200,000 shares at $0.70 per share. The loss for the second quarter ended June 30, 2011 includes a stock-based compensation expense of $2,494,291 in relation to stock options granted to consultants, employees, directors and officers on 1,950,000 shares at $1.50 per share. The loss for the fourth quarter ended December 31, 2011 includes year-end adjustments. In some quarters, losses are offset by gains in the fair value of gold and silver bullion held by the Company. The loss for the second quarter ended June 30, 2012 includes a loss of $301,240 on gold and silver bullion holdings.

Operating Results

The Company is continuing a drilling program at Los Zorros that commenced in July 2011. Exploration during the three months ended March 31, 2012 included 4,745 meters of drilling in 10 drill holes and bulldozer work to construct access roads, drill pads and trenches. Drilling during the first quarter of 2012 was conducted in the Nora, Milagro, Cinchado, and Lora SE project areas which are some of the multiple projects being explored within the Company's extensive landholdings that comprise the Los Zorros Property. Drill pads were also prepared in the Virgen del Carmen, Colorina, Milagro and Florida project areas. We also continued to further expand the Los Zorros camp facilities to accommodate the additional geologists and support workers involved in the exploration and drilling activities.

During the first quarter ended March 31, 2012 we made an option payment of US$ 95,345 due on the Aravena Option. Pursuant to this option, we can acquire a 100% interest in approximately 2,900 hectares of additional mineral concessions adjacent to the Los Zorros property by paying the 2011 patent payments (paid) and by making option payments totaling the Chilean peso equivalent of U.S. $245,345 as follows: U.S. $60,000 on signing (paid); U.S. $95,345 due January 31, 2012 (paid) and U.S. $90,000 due January 31, 2013. During the first quarter of 2012, the Company also made the final advance royalty payment of US$100,000 (in Chilean peso equivalent) in relation to a 209-hectare-portion of the Los Zorros property which the Company previously acquired pursuant to the “Hochschild Option/Purchase”.

During the second quarter ended June 30, 2012, exploration continued at Los Zorros including 4,440 meters of drilling in 9 drill holes. We are currently awaiting the compilation of results from drilling in the Cinchado, Laura SE, Nora, Millagro, Florida, and Milagro Pampa project areas.

For the three months ended June 30, 2012, "Exploration And Evaluation Assets" costs totaled $1,484,421 and "Mineral Interests Administration And Investigation" expenses totaled $96,776. Our assets categorized in the Consolidated Statements Of Financial Position as “Exploration And Evaluation Assets" increased to $16,775,771 at June 30, 2012 from $13,625,896 at December 31, 2011.

The amount of cash on hand at June 30, 2012 was $193,525 ($3,991,264 at December 31, 2011) and the Company's "Gold and Silver Bullion" holdings had a fair value of $5,990,122 at June 30, 2012 ($5,807,372 at December 31, 2011). The Company's total assets were $23,124,253 at June 30, 2012 ($23,654,987 at December 31, 2011). At March 31, 2012, we were debt-free, apart from accounts payable and accrued liabilities of $37,152.

The Company raised substantial private placement funding during the later part of 2010 and received significant proceeds of $4,675,500 from the exercise of warrants during 2011, which has allowed us to increase our staff and expand our exploration activities and expenditures during 2011 and 2012.

The following comments relate to certain categories in the consolidated financial statements to June 30, 2012:

Statements of Financial Position

“Gold and Silver Bullion” - During 2010 and 2011 the Company used a portion of its cash to purchase gold bullion and silver bullion to hold in lieu of cash. At June 30, 2012, the Company held 87,307 grams of gold and 49,818 ounces of silver which had a fair value of $5,990,122. Gold and silver bullion is measured at fair value through the statement of comprehensive loss. There was a loss of $301, 240 on the gold and silver bullion holdings for the three months ended June 30, 2012. Physical gold and silver bullion are highly liquid and are readily convertible to cash.

Consolidated Statements of Comprehensive Loss

"Interest and Bank Charges" - includes vault fees for storage of the Company's gold and silver bullion holdings.

“Mineral Interests Administration and Investigation Costs” - are expensed as incurred and are not capitalized to exploration and evaluation assets and include operating costs related to the Company’s activities in Chile and Bolivia that are not allocated to one of the Company’s specific mineral properties, and include generative exploration or investigating and evaluating mineral properties not acquired by the Company.

“Office and Miscellaneous” - includes rent and utilities for the Canadian corporate office, book-keeping/accounting, office supplies, telephone, postage, couriers, parking, mileage, and printing.

“Professional Fees” – includes legal fees for our corporate counsel in Canada and South America as well as fees and retainers charged by specialized legal counsel retained during the period and for other professional advisors/services.

"Salaries and Benefits" - the amount for the three months ended June 30, 2011 included regular salary payments, retroactive pay related to salary increases retroactive to January 1, 2011, and one-time bonus payments made during the second quarter of fiscal 2011.

"(Gain) Loss On Gold And Silver Bullion" - There was a loss of $301,240 on the gold and silver bullion holdings for the three months ended June 30, 2012. This amount offset a gain of $494,292 on the gold and silver bullion holdings for the three months ended March 31, 2012, resulting in a gain of $193,052 on the gold and silver bullion holdings for the six month period ended June 30, 2012.

"Net and Comprehensive Loss For The Period" - During the three months ended June 30, 2012 there was a loss from operations of $421,165 and a loss of $301,240 on the gold and silver bullion holdings resulting in net and comprehensive loss of $722,405 for the three month period ended June 30, 2012 and a net and comprehensive loss of $615,805 for the six month period ended June 30, 2012.

Statement of Changes In Shareholders' Equity

"Warrant Extension" - In fiscal 2011, during the three months ended March 31, 2011, the Company extended the term of 2,871,250 warrants at $1.00 per share by one additional year. This resulted in an incremental increase in the fair value of the warrants of $455,868 that was charged to deficit.

"Share Based Payments" - $132,130 at June 30, 2012 - During the three months ended June 30, 2012, the Company granted a stock option to an employee/geologist on a total of 100,000 shares at $0.50 per share with a fair value on the grant date of $132,130 which was capitalized to the Los Zorros Property exploration and evaluation costs as stock-based compensation.

Liquidity and Capital Resources - We are an exploration company and do not have any mineral properties in production and, therefore, did not generate any revenue from operations during the three months ended June 30, 2012. During the three months ended June 30, 2012 we realized a loss from operations of $421,165 and a loss of $301,240 on the gold and silver bullion holdings resulting in a net and comprehensive loss of $722,405 or $0.01 per share for the three month period ended June 30, 2012. This is compared to a loss from operations of $3,637,392 and a loss of $107,113 on gold and silver bullion holdings for the three months ended June 30, 2011 resulting in a net and comprehensive loss of $3,744,505 or $0.03 per share for the three month period ended June 30, 2011. The loss from operations for the three months ended June 30, 2011 included a stock-based compensation expense of $$3,101,875 (determined by the fair values on the grant dates) for stock options granted during the second quarter of 2011. Losses are a reflection of our ongoing expenditures on our mineral property exploration and evaluation assets which are all currently in the exploration stage. Since we have no source of operating revenues, no lines of credit and no current sources of external liquidity, our ability to continue as a going concern is dependent upon our ability to raise equity capital, enter into joint ventures or borrow to meet our working capital requirements. Based on the cash and gold and silver bullion on hand at the date of this report, we believe we have sufficient funds to conduct our ongoing general operations and to fund our proposed exploration programs over the next year. The Company plans to focus its exploration activities over the next year on its high quality gold and silver projects in Chile including project areas at Los Zorros. See note “Forward Looking Statements” at end of this report.

In the coming years, we will require substantial additional capital to achieve our goal of discovering significant economic mineralization on one or more of our properties. Until such time as we are able to make such a discovery and thereafter place one or more of our properties into commercial production or negotiate one or more joint venture agreements, we will be largely dependent upon our ability to raise capital from the sale of our securities to fund our operations. We do not anticipate being able to obtain revenue from commercial operations in the short term and anticipate we will be required to raise additional financing in the future to meet our working capital and on-going cash requirements. We intend to raise such financing through sales of our equity securities by way of private placements, and/or the exercise of warrants. We may also secure additional exploration funding through option or joint venture agreements on our mineral properties; or through the sale of our mineral properties, royalty interests or capital assets, or borrow to meet our working capital requirements. While we have in the past been able to raise sufficient funds to sustain our exploration programs, there is no assurance that we will continue to be able to do so. If, for any reason, we are not able to access the capital market, our resources during this period will be limited to cash and gold and silver bullion on hand and any revenues we are able to generate from joint venture or similar arrangements we may hereafter enter into. If we are unable to secure sufficient funds to pursue such proposed acquisitions and exploration to the level desired, we will adjust our proposed activities to reflect the amount of capital available to us after providing for sufficient working capital to maintain our existing operations. See note titled “Forward Looking Statements” at the end of this report.

Financing - In the past, we have relied in large part on our ability to raise capital from the sale of our securities to fund the acquisition and exploration of our mineral properties. 2010/2011 saw a significant increase in the demand for, and in the price of, gold and silver, and an improved market and price for shares of companies focused on precious metals. These trends during 2010/2011 improved our ability to raise capital at higher prices, on more favourable terms, and in greater amounts than in previous years. For example, during 2009 we raised a total of $2,586,050 through two private placements at a price of $0.10 per unit and at $0.20 per unit and from the exercise of warrants. By comparison, during fiscal 2010 we raised a total of $10,162,060 from two private placement at a price of $0.30 per unit and at $0.50 per unit and from the exercise of warrants as follows: during the first quarter ended March 31, 2010, the Company received proceeds of $177,000 from the exercise of warrants for the purchase of 885,000 shares at $0.20 per share. During the second quarter ended June 30, 2010 the Company received proceeds of $10,000 from the exercise of warrants for the purchase of 50,000 shares at $0.20 per share. During the third quarter ended September 30, 2010, the Company completed a private placement of 3,647,334 units at a price of $0.30 per unit for gross proceeds of $1,094,200 and received proceeds of $20,000 from the exercise of warrants for the purchase of 100,000 shares at $0.20 per share. During the fourth quarter ended December 31, 2010, the Company completed a private placement of 17,583,720 units at a price of $0.50 per unit for proceeds of $8,791,860 and received proceeds of $69,000 from the exercise of warrants for the purchase of 345,000 shares at $0.20 per share.

During fiscal 2011, we raised proceeds of $4,675,500 from the exercise of warrants and proceeds of $60,000 from the exercise of stock options as follows: during the first quarter ended March 31, 2011, the Company received proceeds of $1,784,550 from the exercise of warrants for the purchase of 195,000 shares at $0.20 per share, 500,000 shares at $0.30 per share, 750,000 shares at $0.70 per share, and 1,372,500 shares at $0.78 per share. During the second quarter ended June 30, 2011 the Company received proceeds of $2,800,950 from the exercise of warrants and $20,000 from the exercise of an option. During the third quarter ended September 30, 2011, the Company received proceeds of $90,000 from the exercise of warrants for 200,000 shares at $0.20 per share and 50,000 shares at $1.00 per share, and proceeds of $40,000 from the exercise of a stock option to acquire 200,000 shares at $0.20 per share.

During the three months ended March 31, 2012 we received proceeds of $5,000 from the exercise of a warrant for the purchase of 25,000 shares at $0.20 per share.

Use Of Proceeds - During the first quarter of 2009, we completed a private placement and in regulatory filings disclosed that the intended use of the $783,050 proceeds would be $400,000 for expenditures/exploration on our mineral properties and $383,050 for general working capital. This intended use of proceeds was more than fulfilled as exploration/mineral interests costs totaled $594,469 for the first quarter ended March 31, 2009. During the second quarter of 2009 we raised proceeds of $600,000 through a private placement and disclosed in regulatory filings that the intended use of proceeds would be $350,000 for expenditures/exploration on our mineral properties and $250,000 for general working capital. This intended use of proceeds was more than fulfilled as exploration/mineral interests costs totaled $243,404 for the second quarter ended June 30, 2009, $239,275 for the third quarter ended September 30, 2009, and $215,313 for the fourth quarter ended December 31, 2009.

In 2010 we completed a private placement in the third quarter and in regulatory filings disclosed that the intended use of the proceeds of $1,094,200 would be $800,000 for expenditures/exploration on our mineral properties and $294,200 for general working capital. This intended use of proceeds was more than fulfilled as exploration/mineral interests costs totaled $328,197 for the first quarter ended March 31, 2010; $194,281 for the second quarter ended June 30, 2010; $286,519 for the third quarter ended September 30, 2010; and $714,914 for the fourth quarter ended December 31, 2010 for a total of $1,523,911 exploration/mineral interests costs for the 2010 fiscal year. During the fourth quarter of 2010 we completed a private placement and in regulatory filings disclosed that the intended use of the proceeds of $8,791,860 would be $5,000,000 for expenditures/exploration on our mineral properties and $3,791,860 for general working capital. This intended use of proceeds has been fulfilled as indicated by the following exploration/mineral interests costs/expenses for 2011 and 2012.

For the year ended December 31, 2011, our exploration and evaluation assets costs totaled $3,345,249 and mineral interests administration and investigation expenses totaled $287,369.

For the three months ended March 31, 2012, our "Exploration And Evaluation Assets" costs totaled $1,668,454 and "Mineral Interests Administration And Investigation" expenses totaled $93,630. For the three months ended June 30, 2012, our "Exploration And Evaluation Assets" costs totaled $1,484,421 and "Mineral Interests Administration And Investigation" expenses totaled $96,776.

Anticipated Capital Requirements - Based on the cash and gold and silver bullion on hand at the date of this report, we believe we have sufficient funds to conduct our ongoing general operations and to fund our proposed exploration programs over the next year.

While we have in the past been able to raise sufficient funds to sustain our exploration programs, there is no assurance that we will continue to be able to do so. If, for any reason, we are not able to secure equity financings, our resources during this period will be limited to cash and gold and silver bullion on hand and any revenues we are able to generate from joint venture or similar arrangements we may hereafter enter into. If we are unable to secure sufficient funds to pursue exploration to the level desired, we will adjust our proposed activities to reflect the amount of capital available to us after providing for sufficient working capital to maintain our existing operations. Since we own our interests in the majority of our mineral properties, we do not have any significant capital obligations to third parties to maintain our property interests other than the payment of periodic patent and other government fees and the payments listed under the “Table of Contractual Obligations” (see below). Our anticipated cash requirements for the year are primarily comprised of the anticipated costs of conducting our exploration programs, our administrative overhead and the obligations listed under the “Table of Contractual Obligations” (see below) and other operating expenses in the normal course of business. See note titled “Forward Looking Statements” at end of this report.

Table of Contractual Obligations - The following table summarizes our contractual obligations at August 21, 2012 and the effect these obligations are expected to have on our liquidity and cash flows in future periods.

| Contractual Obligations | | Payment Due By Period |

| | | Total | | Less than a year | | 1-3 Years | | 4-5 Years | | After 5 Years |

Aravena Option (1) Optional Payment | | US$90,000 | | US$90,000 | | | | | | |

Long-term Debt Obligations | | NIL | | | | | | | | |

Capital (Finances) Lease Obligations | | NIL | | | | | | | | |

Operating Lease Obligations | | NIL | | | | | | | | |

Purchase Obligations Equipment | | NIL | | | | | | | | |

Other Long-term Liabilities | | NIL | | | | | | | | |

Total Contractual Obligations and Commitments | | Option Payment US$90,000 | | Option Payment US$90,000 | | | | | | |

(1) This is the final option payment pursuant to a Unilateral Option Contract dated June 28 , 2011 between Cristian Marcelo Aravena Caullan and our subsidiary Minera Samex Chile S. A. whereby we have the option to purchase approximately 2,900 hectares of mineral concessions adjacent to the Los Zorros property. (see Note 7 “Mineral Exploration Assets” to the Consolidated Financial Statements) (see “Mineral Property Summaries” – “Los Zorros Property” for details).

Research and Development, patents and licenses, etc. - We are a mineral exploration company and we do not carry on any research and development activities.

Trend Information - We anticipate that the price of gold, silver, and copper will continue to be volatile, but will generally remain strong or increase over the next year due in large part to prevailing global economic imbalances and other continuing economic conditions. Metal prices cannot be predicted with accuracy and our plans will be largely dependent upon the timing and outcome of metal markets, particularly the price of gold, silver and copper which is entirely outside of our control. See note titled “Forward Looking Statements” at the end of this report.

The prices of precious metals and base metals fluctuate widely and are affected by numerous factors beyond our control, including expectations with respect to the rate of inflation, relative strength of the U.S. dollar, Chilean Peso and of other currencies as against the Canadian Dollar, interest rates, and global or regional political or economic crisis. The demand for and supply of precious metals and base metals may affect precious metals and base metals prices but not necessarily in the same manner as supply and demand affect the prices of other commodities. If metal prices are weak, it is more difficult to raise financing for our exploration projects. There is no assurance our attempts to attract capital will be successful. Failure to attract sufficient capital may significantly affect our ability to conduct our planned exploration activities. Conversely, when metal prices are strong, competition for possible mineral properties increases as does the corresponding prices for such prospective acquisitions and the cost of drilling and other resources required to conduct exploration activities.

We have followed the policy of, at year end, writing down to nominal value any of our mineral properties on which we have not conducted any significant exploration or acquisition activities during that fiscal year and do not plan to conduct exploration activities within the current year, regardless of our long term view of the prospects of the particular property. Since our future exploration activities are dependent upon a number of uncertainties including our ability to raise the necessary capital (which is in turn affected by external factors such the prices of precious and base metals), we may be required, by application of this accounting policy, to write down other properties now shown as an asset in our consolidated financial statements to nominal value, even though we may intend to conduct future exploration activities on them after the current fiscal period.

Off Balance Sheet Arrangements - We do not have any material off-balance sheet arrangements out of the ordinary course of business other than employment or consulting agreements with our executives.

No Exposure to Non-Recourse Loans, Derivatives or Liquidity Problems – Our working capital, excess cash, and gold and silver bullion holdings are readily redeemable and are not exposed to the liquidity problems associated with certain short-term investments such as asset-backed securities. The Company does not have any joint venture agreements on any of its mineral properties whereby the Company is exposed to non-recourse loans. SAMEX Mining Corp. is not a party to, nor bound by any agreement, document or instrument whereby the Company’s interest in mineral properties may be reduced or diluted, or whereby the Company may incur any other liabilities or obligation as a direct or indirect result of any derivative embedded in any agreement, document or instrument.

Disclosure Controls and Procedures - The Chief Executive Officer and Chief Financial Officer of the Company evaluated the effectiveness of the Company’s disclosure controls and procedures as of December 31, 2011 and concluded that as of such date, the Company’s disclosure controls and procedures were adequate and effective to ensure that material information relating to the Company and its consolidated subsidiaries would be made known to them by others within those entities. During the period covered by this report, there were no significant changes in the Company’s internal controls or in other factors that materially adversely affected, or are reasonably likely to materially adversely affect, the Company’s internal control over financial reporting.

Stock Options - Under the Company’s “rolling” Stock Option Plan approved by shareholders and accepted by the TSX Venture Exchange, the Company may reserve up to 10% of its issued and outstanding shares for issuance (less any shares already issued under existing stock options). At June 30, 2012 options were outstanding to acquire 11,655,000 shares as follows:

| Optionee | | Date of Option | | # of Shares | | Price | | Expiry Date |

| Jeffrey Dahl | | April 20, 2005 May 2, 2006 Feb 23, 2007 Sep 4, 2009 May 2, 2011 | | 350,000 300,000 270,000 625,000 375,000 | | $0.40 $0.85 $0.84 $0.20 $1.50 | | April 20, 2015 May 2, 2016 Feb 23, 2017 Sep 4, 2019 May 2, 2021 |

| Peter Dahl | | April 20, 2005 May 2, 2006 Feb 23, 2007 Sep 4, 2009 May 2, 2011 | | 350,000 150,000 150,000 400,000 225,000 | | $0.40 $0.85 $0.84 $0.20 $1.50 | | April 20, 2015 May 2, 2016 Feb 23, 2017 Sep 4, 2019 May 2, 2021 |

| Robert Kell | | April 20, 2005 May 2, 2006 Feb 23, 2007 Sep 4, 2009 May 2, 2011 | | 350,000 300,000 275,000 625,000 375,000 | | $0.40 $0.85 $0.84 $0.20 $1.50 | | April 20, 2015 May 2, 2016 Feb 23, 2017 Sep 4, 2019 May 2, 2021 |

| Larry McLean | | April 20, 2005 May 2, 2006 Feb 23, 2007 Sep 4, 2009 May 2, 2011 | | 350,000 300,000 250,000 625,000 375,000 | | $0.40 $0.85 $0.84 $0.20 $1.50 | | April 20, 2015 May 2, 2016 Feb 23, 2017 Sep 4, 2019 May 2, 2021 |

| Allen Leschert | | April 20, 2005 May 2, 2006 Feb 23, 2007 Sep 4, 2009 May 2, 2011 | | 350,000 150,000 150,000 200,000 225,000 | | $0.40 $0.85 $0.84 $0.20 $1.50 | | April 20, 2015 May 2, 2016 Feb 23, 2017 Sep 4, 2019 May 2, 2021 |

| Optionee | | Date of Option | | # of Shares | | Price | | Expiry Date |

| Malcolm Fraser | | Jan 6, 2011 May 2, 2011 | | 200,000 225,000 | | $0.70 $1.50 | | Jan 6, 2021 May 2, 2021 |

| Brenda McLean | | April 20, 2005 May 2, 2006 Feb 23, 2007 Sep 4, 2009 May 2, 2011 | | 175,000 150,000 75,000 250,000 100,000 | | $0.40 $0.85 $0.84 $0.20 $1.50 | | April 20, 2015 May 2, 2016 Feb 23, 2017 Sep 4, 2019 May 2, 2021 |

| Philip Southam | | April 20, 2005 May 2, 2006 Sep 4, 2009 Sep 16, 2010 May 2, 2011 | | 30,000 70,000 150,000 150,000 100,000 | | $0.40 $0.85 $0.20 $0.35 $1.50 | | April 20, 2015 May 2, 2016 Sep 4, 2019 Sep 16, 2015 May 2, 2021 |

| Francisco Vergara | | May 2, 2006 Sep 4, 2009 Sep 16, 2010 May 2, 2011 | | 50,000 150,000 100,000 100,000 | | $0.85 $0.20 $0.35 $1.50 | | May 2, 2016 Sep 4, 2019 Sep 16, 2015 May 2, 2021 |

| Manuel Avalos | | May 2, 2006 Sep 4, 2009 Sep 16, 2010 May 2, 2011 | | 100,000 150,000 150,000 100,000 | | $0.85 $0.20 $0.35 $1.50 | | May 2, 2016 Sep 4, 2019 Sep 16, 2015 May 2, 2021 |

| Jorge Humphreys | | May 2, 2006 | | 20,000 | | $0.85 | | May 2, 2016 |

| Jean Nicholl | | May 2, 2006 Sep 4, 2009 Sep 16, 2010 May 2, 2011 | | 20,000 50,000 30,000 25,000 | | $0.85 $0.20 $0.35 $1.50 | | May 2, 2016 Sep 4, 2019 Sep 16, 2015 May 2, 2021 |

| Jorge Espinoza | | May 2, 2006 | | 30,000 | | $0.85 | | May 2, 2016 |

| Gerald Rayner | | Sep 24, 2007 | | 50,000 | | $0.80 | | Sep 24, 2012 |

| Adrian Douglas | | Dec 20, 2007 Jan 15, 2009 Sep 4, 2009 Jan 29, 2010 May 2, 2011 | | 60,000 60,000 30,000 110,000 200,000 | | $0.70 $0.20 $0.20 $0.35 $1.50 | | Dec 20, 2012 Jan 15, 2014 Sep 4, 2019 Jan 29, 2015 May 2, 2021 |

| Justin Milliard | | Sep 6, 2011 | | 100,000 | | $1.40 | | Sep 6, 2016 |

| Lauren Foiles | | Dec 7, 2011 | | 100,000 | | $0.70 | | Dec 7, 2016 |

| Gabriela Malebran | | Jun 5, 2012 | | 100,000 | | $0.50 | | Jun 5, 2017 |

Audit Committee & Compensation Committee - The Audit Committee is governed by the Company’s Audit Committee Charter. The Audit Committee is composed of director, Larry McLean, Vice President, Operations and Chief Financial Officer of the Company who is not independent, and independent directors, Allen Leschert and Malcolm Fraser, who the Board of Directors have determined to be independent in accordance with the requirements of our Audit Committee Charter. Larry McLean and Allen Leschert have been directors of the Company since 1995 and Malcolm Fraser was appointed to the Board on January 6, 2011, and all three have, in the course of their duties, engaged in the review and analysis of - and/or have actively supervised persons engaged in the preparation, auditing and analysis of - numerous interim and annual financial statements for the Company, as well as for other public companies for which they have served as directors or officers. Allen Leschert, who serves as committee chairman, also has more than 25 years experience as a securities lawyer. In addition to holding a law degree, he also holds a B. Comm. (with distinction), specializing in Corporate Finance and Accounting. All three of the Audit Committee members are “financially literate”. The Audit Committee’s primary function is to review the annual audited financial statements with the Company’s auditor prior to presentation to the Board. The audit committee also reviews the Company’s interim un-audited quarterly financial statements prior to finalization and publication.

Our Compensation Committee is composed of independent directors of the Company, Allen Leschert and Malcolm Fraser, and executive director, Larry McLean. The Compensation Committee was established to assist and advise the Board of Directors with respect to any and all matters relating to the compensation of the executive officers of the Company or other such persons as the Board may request from time to time.

Employees, Related Party Salaries and Payments – During the three months ended June 30, 2012 we had 27 employees, the majority of which were involved in activities related to our mineral exploration properties in Chile (compared to 21 employees during the second quarter of 2011). During the three months ended June 30, 2012, salaries for employees who are also directors or officers of the Company totalled $130,950 a $40,500 portion of which was capitalized to exploration and evaluation assets (second quarter 2011 - $141,700 a $36,700 portion of which was capitalized).

Allen D. Leschert, one of our directors, provides legal services to us through Leschert & Company Law Corporation. Leschert & Company charged $38,552 for legal services during the three months ended June 30, 2012. Malcolm Fraser, one of our directors, charged the Company $6,000 during the second quarter for conducting research and consulting on behalf of the Board of Directors.

ADDITIONAL INFORMATION FOR SECOND QUARTER ENDED JUNE 30, 2012

Directors And Officers Of The Company During The Second Quarter Ended June 30, 2012: Jeffrey P. Dahl – President, CEO & Director; Peter J. Dahl - Chairman & Director; Robert E. Kell - Vice President Exploration & Director; Allen D. Leschert - Director; Larry D. McLean - Vice President Operations, CFO & Director; Malcolm B. Fraser - Director; Brenda L. McLean - Corporate Secretary.

Investor Relations – Investor relations activities during the second quarter of 2012 were handled by management and included telephone contacts and “Glance” desk-top-sharing presentations and in-person meetings with shareholders, brokers and investors.

Stock Options – During the second quarter ended June 30, 2012, the Company granted an employee/geologist a stock option on 100,000 shares at $0.50 per share with a fair value on the grant date of $132,130 which was capitalized to the Los Zorros Property exploration and evaluation costs as stock-based compensation.

Warrants – No warrants were issued or exercised during the second quarter ended June 30, 2012.

Extension Of Warrant Term - During the second quarter, the Company applied to the TSX Venture Exchange to extend the term of warrants for the purchase of 1,823,668 shares at $0.35 per share. These warrants were originally issued with a two-year term expiring July 8, 2012, and the Company made application to extend the term of these warrants for two additional years until July 8, 2014. The exercise price of the warrants will remain at $0.35 per share. A Control Person/Insider of SAMEX, Sasan Sadeghpour holds 861,834 of these warrants. Subsequent to the second quarter, the TSX Venture Exchange consented to the extension of the expiry date of these warrants. The extension of the expiry date will result in an incremental increase in the fair value of the warrants of $196,397 which will be charged to deficit in the third quarter ending September 30, 2012.

Securities Issued During The Second Quarter Ended June 30, 2012 - No securities were issued during the second quarter ended June 30, 2012.

Outstanding shares at June 30, 2012 - 126,733,719 |

Outstanding shares at the date of this report - August 21, 2012 - 126,733,719 |

MINERAL PROPERTY SUMMARIES

LOS ZORROS PROPERTY, Chile

The Los Zorros Property in the Atacama region of northern Chile is located approximately 60 kilometers south of the city of Copiapo, Chile. The property is accessed by vehicle by driving approximately 60 kilometers south of the city of Copiapo on the paved, four-lane Pan American Highway (Highway 5) then traveling 5.5 kilometers east on a government maintained dirt road to the western boundary of the property and a further 4 kilometers to the Company’s exploration camp. Although gold is the primary focus of SAMEX’s exploration at Los Zorros, important values of silver and copper are also present in certain target areas.

The Los Zorros property consists of multiple project areas that have now been strategically expanded to cover more than 100 square kilometers within a district of scattered numerous small mines and prospects where there was sporadic attempts at small-scale production for gold and copper-silver in the past. What has been revealed geologically at Los Zorros has provided SAMEX with strong impetus to explore for multiple precious metal deposits that may be clustered beneath the widespread precious metal occurrences in this district of historic small mining activity. The property is situated at the convergence of important geologic and structural features and significant gold and copper-silver mineralization in the Cinchado, Nora, Milagro, and Milagro Pampa. Project areas. The Los Zorros Property also includes other project areas including: La Florida and Lora (gold and copper-gold), Virgen de Carmen and Colorina (copper-silver; possible deeper-seated gold and copper-gold), Salvadora, Cresta de Gallo, and Trueno (barite vein systems with possible deeper-seated gold and copper-gold) and Gringo (copper-gold).

The Company has 100% interest in approximately 7,774 hectares of mineral concessions acquired by staking, purchase at government auction, purchase/option contracts, and we further expanded the Los Zorros land holdings during 2011 by signing the Aravena Option to acquire a 100% interest in approximately 2,900 hectares of additional mineral concessions adjacent to the Los Zorros property. The Los Zorros land holdings now cover a 15 kilometer-strike of the prospective range front/anticline along which mineralization is exposed in old-time piquenero underground workings, open cuts, trenches and pits situated in the Colorina, Nora, Virgen del Carmen, Cresta de Gallo, and Trueno project areas. Of particular significance, at April 2012, the only acquisition payment remaining on our extensive accumulated land holdings at Los Zorros is the final Aravena Option payment of US$90,000 due by January 31, 2013.

During 2004, we completed 8,617 meters of diamond core drilling in 26 holes, 10,800 meters of bulldozer trenching in 65 trenches and more than 3,100 trench and surface samples/assays; and an additional 1,865 meters of trenching (10 trenches/559 samples) during 2005. Our Phase I exploration yielded significant results including: Nora - DDH-N-04-05 with 15.96 g/mt gold over 7.66 meters, Trench TN-9 with 0.757 g/mt gold over 131 meters, and Trench TN-3 with 0.558 g/mt gold over 117 meters; Milagro - DDH-ML-04-01 with 2.579 g/mt gold over 4.4 meters true width; West Florida - trench TMW-10 with .405 g/mt gold over 138 meters; Cinchado - values ranging from 0.05 to 9.5 g/mt gold in 151 rock-chip samples of breccia in the open-cut of the old San Pedro mine. Phase I exploration work was conducted on only a portion of the target/project areas that we have identified to-date at Los Zorros. We resumed exploration at the Los Zorros Property in 2009 and work is continuing to the present time in 2012.

During the first quarter of 2011, the Company continued a drilling program at Los Zorros that had commenced during 2010. In late January 2011 we started a substantial geophysical survey (at a cost of US$280,000) over portions of the Los Zorros district. During the second quarter ended June 30, 2011, the information gained from the drilling, assaying and the geophysical survey was evaluated and complied in preparation for more drilling which commenced early in the third quarter, and is still in progress at the date of this report (April 2012). During the later part of 2011 the Company engaged a consulting geophysicist to assist in the interpretation and correlation of geophysical data and we expanded the exploration program at Los Zorros by adding a second drill rig, three more geologists, and additional support staff at the camp. We also commenced expansion of the Los Zorros camp and support facilities to accommodate the additional geologists and support workers and adding additional core logging, sampling, and core-saw equipment to facilitate increased exploration and drilling activities. Exploration at Los Zorros during 2011 included drilling 13 core drill holes for a total of 6,335 meters drilled. Exploration activity and results at Loz Zorros during and subsequent to 2011 are summarized below.

Cinchado Gold Project - Exploration core drilling was designed to test both beneath and the westward down-dip projected continuation of a prospective zone of strong jasperoid-barite vein/mantos alterations features. Such features at the south end of Cerro Cinchado can be traced down into the gold-mineralized breccia (3 grams/tonne gold average grade) at the San Pedro mine. The iron-oxide character of the matrix to the mined breccia suggests that the clasts were cemented by considerable copper- and iron-sulfide. The three drill holes, DDH-CC-10-01, -02, & -03, did not intersect the target, but instead found that a +250-meter thick diorite sill had been emplaced, post-mineralization/alteration, cutting through the target interval.

Titan 24 DC-IP & MT Geophysical Survey – The Titan-24 survey identified 47 interpreted geophysical anomalies, of which 19 anomalies are considered first priority anomalous zones for follow up with potential for sulphide and gold mineralization from near surface to >500m depth. The remaining 28 anomalies are second priority targets that represent small area anomalies, generally with weak to moderate responses near surface.

Approximately 14 of the 47 anomalies coincide with known areas of mineralization determined by surface workings, surface sampling or drilling, including 7 first priority anomalous zones and 7 second priority targets. The known target areas which have coincident anomalies are: (Cinchado, Cinchado East, Nora North – L100N), (Nora Central, Lora Southeast - L200N), (Milagro Pampa - L300N) and (Milagro Mine - L400N).

Milagro Gold Project – Two drill holes (DDH-MM-10-01 and -02) were completed as a follow up to test the eastward, down-dip projected continuation of a highly prospective gold-mineralized mantos intercepted in the 2004 program (DDH-MM-04-01 encountered 97.3 meters averaging 0.302 g/t gold, including 2.579 g/t gold over 4.7 meters and previously reported January 21, 2005).

The first hole DDH-MM-10-01 was sited 140 meters east of DDH-ML-04-01 and aimed inclined westward with the intention of making a relatively shallow intercept of the gold-mineralized mantos layer and underlying altered volcanic debris-flow breccia which too was found to be highly anomalous in gold averaging 0.167 g/t over 71 meters (from 31.7 to 102.7 meters). The target interval was found, in the vicinity of the new drill site, to be displaced by a steeply westward dipping normal fault intersected between depths of 37 to 53 meters. As a result, the hole penetrated through the fault gap and beneath the target interval intended to be drill tested. However, the footwall (54 – 60 meters) to the fault zone was a strongly pyritized/silicified volcaniclastic debris flow breccia with high anomalous gold content (averaging 0.364 g/t). Strongly altered quartz-sericite-pyrite altered volcaniclastic sediments and interlayered debris flow breccia intervals continued to a depth of 369 meters where the hole was stopped after penetrating well into weakly altered porphyritic diorite sill (354 – 369 meters). This entire long interval (53 to 369 meters) continuously contains elevated detectible gold values (>0.010 to <0.100 g/t) with numerous subintervals of anomalous gold (0.108 to 0.807 g/t). One interval (268.0 to 270.0 meters) comprised of strong pyritization and silicification associated with a narrow fault zone contains 11.8 g/t gold.

The second drill hole (DDH-MM-10-02) was sited 900 meters east-southeast of DDH-ML-04-01. This long step-out and location were chosen to test again the projected southeastward down-dip continuation of the gold-mineralized mantos layer and within a structural block that is largely intact without significant fault disruptions. This hole was aimed inclined northwestward and, below an altered mafic sill, entered into a thick interval (from 228 to 517 meters) of prospective-looking, quartz-sericite-pyrite altered volcaniclastic debris-flow breccia units. Geochemical analyses show that the interval from 261.5 to 373.0 meters continuously contains elevated detectible (<0.010 to <0.100 g/t) amounts of gold. Within this interval, three prominent intervals of significantly anomalous gold (>0.100 to 2.14 g/t) were intersected: 261.5 to 278.0 meters, 313.0 to 332.0 meters, and 350.0 to 373.0 meters. The hole was stopped at a depth of 517.0 meters within a silicified/pyritized carbonaceous black shale sedimentary unit where subsequent assaying shows low-level anomalous gold values (0.105 to 0.151 g/t) begin to reappear.

The results of the Milagro project reconnaissance drilling are encouraging and show widespread low-level to anomalous values of gold spread over great thicknesses of quartz-sericite-pyrite altered volcaniclastic sedimentary rock. The extent and style of alteration, and anomalous gold are indicative of large-scale mineralizing processes, and possibly comprise a halo to areas of significant gold mineralization. Titan-24 Line 4, which runs through the Milagro project area and in close vicinity to the drill holes, shows that DDH-MM-10-02 was drilling down into, but not through, a very strong IP chargeability anomaly; and over top of, thus missing, a strong resistivity anomaly. The latter resistivity anomaly outlines a target highly prospective for a gold-mineralized, silicified body positioned along the range front. This resistivity anomaly was also observed on Titan-24 Line 3, so, is known to extend for at least 700 meters from the Milagro project area northward across the east part of the Milagro Pampa project area (open-ended to the north and south).

Further west and south of the Milagro drilling, 46 samples were collected on shallow, exposed barite veins, fault zones, narrow breccias and minor jasperoid occurrences observed during prospecting traverses over a 1,300 x 800 meter area. The 46 samples range from <0.005 to 20.2 g/t gold including 10 samples returning >1.0 g/t gold, with four of these ranging from 4.26 to 5.56 g/t gold. Underlying this sampled area, a second sizeable IP anomaly characterized by high chargeability and high resistivity at relatively shallow depth, was identified by Titan-24 Line 4. The character of this anomaly is that of a thick/extensive, strongly silicified/pyritiferous mantos interval and which is known to be positioned adjacent/proximal to a shallow concealed altered porphyry intrusion (gravity low).

Milagro Pampa Project – One exploration core hole (DDH-MP-10-01) was drilled westward inclined to a depth of 869.4 meters. This hole tested down across anhydrite and quartz stock work veinlets and sheeted vein swarm within a sericite-quartz-pyrite altered porphyritic intrusion. These bedrock features are concealed beneath 12 meters of gravel cover. The hole proceeded downward through intense veinleting and pyritiferous sericite-altered porphyritic intrusion, which appears to comprise an extensive phyllic alteration halo. The west margin of the intrusion was intersected at 657 meters depth where pyritized hornfelsed and calc-silicate skarnoid metasedimentary rocks were intersected.

Geochemical results on continuous sampling show, from 150 to 500 meters depth, overall increasing levels of variably anomalous copper (>100 to 905 ppm) copper and elevated detectible to anomalous gold (>0.050 to 0.332 g/t). Below approximately 500 meters, the hole encountered a series of prominent vein and brecciated intervals from 0.3 to 1.2 meters thickness with >1% copper, and 0.475 to 6.08 g/t gold. A 1.9-meter (true width) vein/fault interval assayed 13.0 g/t gold including 0.75 meters (true width) at 29.4 g/t gold. The interval, 692.0 to 738.6 meters (23.3 meters true width), averaged 1.51 g/t Au, 2.15 g/t Ag and 0.27% Cu with strongly anomalous mercury and arsenic. The dominant orientation of veins and veinlets intersected in core indicated that the drill hole was cutting down at an acute angle to the vein dip direction and that perhaps was also drilling westward and away from the “heart” of the mineralizing system.

In late 2011, we accelerated the exploration program at the Los Zorros gold property in Chile by adding a second drill rig and three more geologists. Program highlights include: