QuickLinks -- Click here to rapidly navigate through this document

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

| Filed by the Registranto | ||

| Filed by a Party other than the Registranto | ||

Check the appropriate box: | ||

| o | Preliminary Proxy Statement | |

| o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ý | Definitive Proxy Statement | |

| o | Definitive Additional Materials | |

| o | Soliciting Material Pursuant to §240.14a-12 | |

Reebok International LTD. | ||||

(Name of Registrant as Specified In Its Charter) | ||||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

| ý | No fee required | |||

| o | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11 | |||

| (1) | Title of each class of securities to which transaction applies: | |||

| (2) | Aggregate number of securities to which transaction applies: | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| (4) | Proposed maximum aggregate value of transaction: | |||

| (5) | Total fee paid: | |||

| o | Fee paid previously with preliminary materials. | |||

| o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid: | |||

| (2) | Form, Schedule or Registration Statement No.: | |||

| (3) | Filing Party: | |||

| (4) | Date Filed: | |||

![]()

REEBOK INTERNATIONAL LTD.

1895 J.W. Foster Boulevard

Canton, Massachusetts 02021

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS

May 7, 2002

Notice is hereby given that the Annual Meeting of Shareholders of Reebok International Ltd. will be held at Reebok's Corporate Headquarters, located at the above address, at 10:00 A.M. local time on Tuesday, May 7, 2002 for the following purposes:

- 1.

- To elect three (3) Class III members of the Board of Directors.

- 2.

- To vote on a shareholder proposal that all members of the Board of Directors be elected annually.

- 3.

- To transact any other business that may properly come before the Meeting or any adjournment thereof.

Stockholders of record at the close of business on March 8, 2002 are entitled to notice of and to vote at the Meeting and any adjournment thereof. Whether or not you intend to be present in person at the meeting, please sign and date the enclosed proxy card and return it promptly in the enclosed envelope.

By Order of the Board of Directors

DAVID A. PACE

Clerk

March 25, 2002

ANNUAL MEETING OF SHAREHOLDERS

May 7, 2002

The enclosed proxy is solicited on behalf of the Board of Directors of Reebok International Ltd. ("Reebok" or the "Company") to be voted at the Annual Meeting of Shareholders to be held at the Company's principal executive offices, located at 1895 J.W. Foster Boulevard, Canton, Massachusetts 02021, on Tuesday, May 7, 2002 or at any adjournment thereof (the "Meeting"). The cost of solicitation of proxies will be borne by Reebok. Directors, officers and employees of Reebok may also solicit proxies by telephone, telegraph, electronic mail or personal interview. Reebok will reimburse banks, brokerage firms and other custodians, nominees and fiduciaries for reasonable expenses incurred by them in sending proxy materials on behalf of Reebok's management to the beneficial owners of shares. Reebok expects to mail this Proxy Statement and the enclosed proxy to shareholders on March 25, 2002.

Only shareholders of record at the close of business on March 8, 2002 (the "Record Date") are entitled to notice of and to vote at the Meeting. There were 58,700,027 shares of the Company's common stock, $.01 par value per share ("Common Stock"), outstanding on the Record Date, each of which is entitled to one vote. Under the bylaws of the Company, a majority of the shares of Common Stock issued and outstanding and entitled to vote will constitute a quorum for the Meeting. If a quorum is present, the three nominees for directors in Class III who receive the greatest number of votes properly cast (or a plurality of the votes) will be elected directors. With respect to proposal 2, if a quorum is present, a majority of the votes cast on the proposal is required. Shareholders should be aware, however, that adoption of this proposal would not eliminate board classification and institute the annual election of directors, but would constitute merely a recommendation by the stockholders voting on the proposal that the Board consider enacting such a change. The affirmative vote of two-thirds of the outstanding shares or a vote of the directors is required to opt out of the Massachusetts law and declassify the board. Votes cast by proxy or in person at the Meeting will be counted by persons selected by the Company to act as election inspectors for the Meeting (the "Election Inspectors").

The Election Inspectors will count shares represented by proxies that withhold authority to vote for a nominee for election as a director or that reflect abstentions and "broker non-votes" (i.e., shares represented at the Meeting held by brokers or nominees as to which (i) instructions have not been received from the beneficial owners or persons entitled to vote, and (ii) the broker or nominee does not have the discretionary voting power on a particular matter) only as shares that are present and entitled to vote on the matters for purposes of determining the presence of a quorum; but neither proxies that withhold authority to vote for any nominee (without naming an alternative nominee), abstentions nor broker non-votes will be counted as votes cast at the Meeting. Such proxies therefore will not be a factor for the election of directors at the Meeting.

Shares represented by proxies in the form enclosed, if properly executed and returned and not revoked, will be voted at the Meeting. To be voted, proxies must be filed with the Clerk prior to voting. Proxies may be revoked at any time before exercise by filing a notice of such revocation with the Clerk. Proxies will be voted as specified by the shareholders. Where specific choices are not indicated, proxies will be voted FOR the election of each nominee for director identified below, AGAINST the shareholder proposal that all members of the Board of Directors be elected annually, and in the discretion of the named proxies as to any other matter that may come before the Meeting or any adjournments of the Meeting.

Reebok's Annual Report on Form 10-K for fiscal year ended December 31, 2001 has been mailed with this Proxy Statement.

1

PROPOSAL 1: ELECTION OF DIRECTORS

Pursuant to the provisions of Section 50A of Chapter 156B of the Massachusetts General Laws, the Board of Directors is divided into three classes, having staggered terms of three years each. Under Section 50A and the bylaws of the Company, the Board of Directors may determine the total number of directors and the number of directors to be elected at any annual meeting of shareholders or special meeting in lieu thereof.

Of the current directors, three (3) Class III directors have terms expiring at the Meeting, three (3) Class I directors have terms expiring at the 2003 Annual Meeting and four (4) Class II directors have terms expiring at the 2004 Annual Meeting. All three (3) Class III directors whose terms expire at the Meeting have been nominated by the Board of Directors for reelection at the Meeting. Each Class III director elected at the Meeting will serve until the 2005 Annual Meeting of Shareholders, and until each such director's successor is elected and qualified.

The Board of Directors has fixed at three (3) the number of Class III directors to be elected by the Company's shareholders at the Meeting. If these three (3) nominees are elected at the Meeting, the Board of Directors will have a total of ten (10) members, including three (3) Class III directors, three (3) Class I directors, and four (4) Class II directors.

Information with Respect to Directors and Nominees for Director

Unless authority is withheld, proxies in the accompanying form will be voted FOR the election of Paul B. Fireman, Dorothy E. Puhy and Thomas M. Ryan as Class III directors, to hold office until the 2005 Annual Meeting of Shareholders, and until their respective successors are elected and qualified. If a proxy is executed in such a manner as to withhold authority to vote for one or more nominees for director, such instructions will be followed by the persons named as proxies.

All three of the nominees for director are now Class III members of the Board of Directors. The Company has no reason to believe that any of the nominees will be unable to serve. In the event that any nominee should not be available, the persons named in the proxy will vote for the others and may vote for a substitute for such nominee.

2

Listed below are the nominees for Class III director, with information showing the business experience and current public directorships, if any, of each, the age of each and the year each was first elected a director of the Company, where applicable.

| Name | Business Experience and Current Directorships | Age | Director Since | |||

|---|---|---|---|---|---|---|

| Paul B. Fireman | Chief Executive Officer and Chairman of the Board of Directors of the Company; President of the Company (from 1979 to March 1987 and from December 1989 through December 2001); and Director of Abiomed, Inc., a manufacturer of medical devices. | 58 | 1979 | |||

Dorothy E. Puhy | Chief Financial Officer and Assistant Treasurer, Dana-Farber Cancer Institute (since 1994), a leading health care provider and research concern; Chief Financial Officer, New England Medical Center Hospitals, Inc. (from 1989 to 1994), a major health care provider. | 50 | 2000 | |||

Thomas M. Ryan | President and Chief Executive Officer (since May 1998) and Chairman of the Board (since April 1999) of CVS Corporation ("CVS"), a company in the chain drug store industry; President and Chief Executive Officer of CVS Pharmacy, Inc. (since 1994); Director of FleetBoston Financial Corporation, a financial services company; and Director, Tricon Global Restaurants, Inc., the world's largest quick-serve restaurant company. | 49 | 1998 |

3

Current Class I members of the Board of Directors, whose terms of office expire at the 2003 Annual Meeting of Shareholders, are as follows:

| Name | Business Experience and Current Directorships | Age | Director Since | |||

|---|---|---|---|---|---|---|

| Mannie L. Jackson | Chairman, Chief Executive Officer and majority owner of Harlem Globetrotters International, Inc., a sports and entertainment entity (since August 1992); retired Senior Vice President-Corporate Marketing and Administration of Honeywell, Inc., a manufacturer of Control Systems, and prior to that, served in various executive capacities for Honeywell, Inc. beginning in 1968; Director of Ashland Inc., a vertically integrated petroleum and chemical company; and Director of The Stanley Works, a commercial, consumer and specialty tools company. | 62 | 1996 | |||

Jay Margolis | President and Chief Operating Officer of the Company (since December 2001); Executive Vice President and President of the Specialty Business Groups of the Company (from December 2000 to December 2001); Chairman and CEO of E7th.com, a business-to-business supply solution for the footwear industry linking wholesalers with retailers (from August 2000 to November 2000); Chairman and CEO of Esprit de Corporation (from June 1995 to January 1999); President and Vice Chairman of the Board of Tommy Hilfiger (January 1992 to June 1995); Vice Chairman of the Board of Liz Claiborne (January 1982 to January 1992). | 53 | 2002 | |||

Geoffrey Nunes | Retired Senior Vice President and General Counsel for Millipore Corporation, a leader in the field of separation technology. | 71 | 1986 |

4

Current Class II members of the Board of Directors, whose terms of office expire at the 2004 Annual Meeting of Shareholders, are as follows:

| Name | Business Experience and Current Directorships | Age | Director Since | |||

|---|---|---|---|---|---|---|

| Norman Axelrod | Chief Executive Officer of Linens "N Things, Inc. ("LNT"), a national retailer of home textiles, housewares and home accessories (since 1988); Chairman of the Board of Directors for LNT (since 1996); President and CEO of LNT, a division of Melville Corp. (from 1988 to 1996); held various senior management positions at Bloomingdale's, a national department store (from 1976 to 1988); and Director of Jaclyn, Inc., a handbags and apparel company. | 49 | 2001 | |||

Paul R. Duncan | Retired Executive Vice President of the Company (served from February 1990 until December 1998; and from January 2000 until January 2001), with various executive responsibilities including President of the Company's Specialty Business Groups (from October 1995 to November 1996 and from January 2000 until January 2001); Chief Financial Officer of the Company (from 1985 to June 1995); and Director of Enterasys Networks, successor to Cabletron Systems, Inc., a computer networking company. | 61 | 1989 | |||

Richard G. Lesser | Senior Corporate Advisor (since February 2002) and Director (since 1994) of TJX Companies, Inc. ("TJX Companies"), an off-price apparel and home furnishings retailer; Chief Operating Officer of TJX Companies (from November 1994 to February 2000) and Executive Vice President (February 1991 through December 2001); Chairman, The Marmaxx Group, a division of TJX Companies that operates TJ Maxx and Marshalls (from February 2001 to December 2001); President, The Marmaxx Group (February 1996 through February 2001); Director of A.C. Moore Arts & Crafts, Inc., an operator of arts and crafts stores; and Director of Dollar Tree Stores, Inc., a national chain of variety stores selling merchandise at one dollar. | 67 | 1988 | |||

Deval L. Patrick | Executive Vice President and General Counsel, The Coca-Cola Company, a beverage sales company (since April 2001); Vice President and General Counsel, Texaco Inc., an energy company (from 1999 to March 2001); Partner, Day, Berry & Howard (from 1997 to 1999), a law firm; Assistant Attorney General, Civil Rights Division of the U.S. Department of Justice (from 1994 to 1997); and Director, Coca-Cola Enterprises, Inc., which markets, distributes and produces bottled and canned beverages. | 45 | 2001 |

5

Meetings of the Board of Directors and Committees

During 2001, the Board of Directors held six meetings. All of the directors attended at least 75% of the Board and relevant committee meetings during 2001; except for Mr. Ryan who attended 63% of the meetings. For information on the compensation of directors, see "Compensation of Directors" below.

The Audit Committee, composed of Ms. Puhy (Chair), Mr. Lesser, and Mr. Nunes, held three meetings during 2001. The Audit Committee recommends to the Board of Directors the independent public auditors to be engaged by the Company; reviews with such auditors and management the Company's internal accounting procedures and controls; and reviews with such auditors the audit scope and results of their audit of the consolidated financial statements of the Company.

The Compensation Committee, composed of Mr. Nunes (Chair), Mr. Ryan and Mr. Axelrod (starting on May 1, 2001), held four meetings during 2001, and acted once by unanimous written consent. The Compensation Committee administers the Company's stock option and compensation plans, sets compensation for the Chief Executive Officer, reviews the compensation of the other executive officers and provides recommendations to the Board regarding compensation matters.

The Board Affairs Committee, composed of Mr. Lesser (Chair), Messrs. Jackson, Ryan, Nunes (until May 1, 2001) and Patrick (starting on May 1, 2001), held two meetings during 2001. The Board Affairs Committee is responsible for considering Board governance issues. The Board Affairs Committee also recommends individuals to serve as directors of the Company and will consider nominees recommended by shareholders. Recommendations by shareholders should be submitted in writing to the Board Affairs Committee, in care of the President of the Company.

The Executive Committee, composed of Mr. Fireman (Chair), Messrs. Duncan and Nunes, did not meet during 2001. The Executive Committee may take certain action permitted by law and the bylaws in the intervals between meetings of the full Board, and in fact, did take action once by unanimous written consent during 2001.

Compensation of Directors

During 2001, each director who was not an officer or employee of the Company received an annual retainer of $25,000, plus $2,000 for each committee chairmanship held and $2,000 for each directors' meeting and $1,000 for each committee meeting attended, plus expenses. As part of a policy adopted by the Board of Directors in 1998 that requires each director to own Reebok's Common Stock with a market value of at least four times the amount of the annual retainer within five years after the director's first election to the Board, a minimum of forty percent of the annual retainer was paid to the directors in Reebok's Common Stock.

The Company's Equity and Deferred Compensation Plan for Directors provides for the issuance of stock options to directors and provides a means by which directors may defer all or a portion of their director fees. In addition, the shareholders of Reebok approved the 2001 Equity Incentive and Director Deferred Compensation Plan at the 2001 Annual Meeting. These two plans shall be referred to as the "Directors' Plan" for purposes of this section.

6

The deferred compensation portion of the Directors' Plan permits directors who are not employees of the Company to defer all or a portion of their director compensation and to invest such deferred compensation in Reebok's Common Stock or in cash, which earns interest at the Merrill Lynch Corporate Bond Rate (the "Bond Rate"). Compensation deferred into Common Stock is converted into stock based on the price of the stock on the first day of the calendar quarter following the quarter in which the fees were deferred. Dividends paid on the Common Stock are also credited to the director's deferred compensation account.

Directors who elect to defer their compensation will receive a distribution of their deferred compensation in either a lump sum or in annual installments (at the director's election) beginning on a date specified by the director or on the date on which the director is no longer a member of the Board of Directors, whichever occurs first. If the deferred compensation is invested at the Bond Rate, the distribution will be in cash in an amount equal to the deferred compensation plus interest accrued. If the compensation is deferred into Common Stock, the distribution will be in the form of shares of Common Stock.

Under the stock option portion of the Directors' Plan, each newly elected (or re-elected) Eligible Director (as defined below) is granted an option on the date of such election (or re-election) to purchase shares of Common Stock having an aggregate market value on such date equal to six times the average cash compensation received by all directors in the immediately prior calendar year (the "Election Year Grant"). On April 28 of each year after the Election Year Grant, each Eligible Director is granted an option to purchase shares of Common Stock having a fair market value on the date of such grant equal to three times the average annual cash compensation received by all directors in the immediately prior calendar year (or a pro-rata portion based on the date of his or her election). The exercise price for all options granted under the Directors' Plan is the fair market value of Common Stock on the date of the grant.

On April 28, 1999, all Eligible Directors were granted an option equal to an Election Year Grant, even those Eligible Directors for whom 1999 was not an election year. The options granted under the Directors' Plan in 2000 were adjusted pro-rata for these 1999 grants so that the nominees and the directors whose terms expired at the 2000 Annual Meeting of Shareholders received one-third of the Election Year Grant in 2000. The options granted under the Directors' Plan in 2001 were also adjusted pro-rata for the 1999 grants such that directors whose terms expired at the 2001 Annual Meeting received two-thirds of the Election Year Grant in 2001. On April 28, 2001, Messrs. Nunes, Ryan, Lesser, Duncan, and Jackson, and Ms. Puhy, each were granted an option to purchase 5,226 shares of Common Stock. On April 28, 2001, Messrs. Lesser and Duncan each were granted an additional option to purchase 6,968 shares of Common Stock. Upon their appointment to the Board of Directors on May 1, 2001, Messrs. Patrick and Axelrod were granted an option to purchase 10,022 shares of Common Stock.

An "Eligible Director" is any director who is not an officer or employee of the Company and is not a holder of more than five percent (5%) of the outstanding shares of the Company's Common Stock or a person who is in control of such holder. In 2001, all the directors were Eligible Directors, except for Mr. Fireman.

7

Beneficial Ownership of Shares

The following table shows certain information about the shares of Common Stock owned as of the Record Date by persons owning of record or, to the knowledge of the Company, beneficially five percent (5%) or more of the outstanding shares of Common Stock. It also shows ownership by each director and nominee for director, by each executive officer named in the Summary Compensation Table below and by all directors and executive officers of the Company as a group. The address for Paul and Phyllis Fireman is c/o Reebok International Ltd., 1895 J.W. Foster Boulevard, Canton, Massachusetts 02021.

| Name | Common Stock Beneficially Owned(1) | Percent of Class(2) | |||

|---|---|---|---|---|---|

| Paul B. Fireman(3)(8) | 8,298,377 | 14.0 | % | ||

| Phyllis Fireman(4) | 6,412,002 | 10.9 | % | ||

| Norman Axelrod(5)(8) | 3,340 | * | |||

| Paul R. Duncan(5)(8) | 215,244 | * | |||

| Mannie L. Jackson(5)(8) | 49,099 | * | |||

| Richard G. Lesser(5)(6)(8) | 53,800 | * | |||

| Geoffrey Nunes(5)(8) | 65,605 | * | |||

| Deval L. Patrick(5)(8) | 3,340 | * | |||

| Dorothy E. Puhy(5)(8) | 5,226 | * | |||

| Thomas M. Ryan(5)(8) | 37,845 | * | |||

| James R. Jones(8) | 88,429 | * | |||

| Jay Margolis(8) | 137,888 | * | |||

| David A. Perdue(8) | 133,281 | * | |||

| Kenneth I. Watchmaker(8) | 304,021 | * | |||

| Directors and Executive Officers listed above and other Executive Officers as a group (16 persons)(7)(8) | 9,486,863 | 5.6 | % | ||

| Investors Group Trust Co., Ltd.(9) | 3,354,000 | 5.7 | % |

- *

- Less than 1%.

- (1)

- Except as otherwise noted, all persons and entities have sole voting and investment power over their shares. All amounts shown in this column include shares obtainable upon exercise of stock options exercisable within 60 days of the Record Date.

- (2)

- Computed on the basis of 58,700,027 shares outstanding as of the Record Date and the number of options exercisable within 60 days of the Record Date for each beneficial owner whose ownership is being reported.

- (3)

- This number includes Mr. Fireman's indirect beneficial ownership of 2,279,267 shares held in two trusts established in 1999. Excludes 3,862,931 shares that are beneficially owned by Phyllis Fireman, Paul Fireman's wife. Mr. Fireman disclaims beneficial ownership of these shares.

- (4)

- This number includes Mrs. Fireman's indirect beneficial ownership of 1,184,071 shares held in a trust established in 1999. Excludes 5,749,036 shares that are beneficially owned by Paul Fireman, Phyllis Fireman's husband. Mrs. Fireman disclaims beneficial ownership of these shares.

- (5)

- Excludes for the following persons, the following shares, which represent shares deferred pursuant to the Directors' Plan: Norman Axelrod, 1,102 shares; Paul R. Duncan, 4,241 shares; Mannie L. Jackson, 11,810 shares; Richard G. Lesser, 6,062 shares; Geoffrey Nunes, 5,838 shares; Deval L. Patrick, 964 shares; Dorothy E. Puhy, 1,759 shares; and Thomas M. Ryan, 8,368 shares.

8

- (6)

- Excludes 3,576 shares held by Mr. Lesser's wife and child. Mr. Lesser disclaims beneficial ownership of these shares.

- (7)

- Excludes the 3,862,931 shares described in note (3) above and the 3,576 shares described in note (6). Includes shares subject to options held by directors and executive officers that are exercisable within 60 days of the Record Date (see note (8) below).

- (8)

- Includes for the following persons, the following shares which are subject to stock options exercisable within 60 days of the Record Date: Paul B. Fireman, 611,150 shares; Norman Axelrod, 3,340 shares; Paul R. Duncan, 147,030 shares; Mannie L. Jackson, 48,099 shares; Richard G. Lesser, 53,800 shares; Geoffrey Nunes, 54,605 shares; Deval L. Patrick 3,340 shares; Dorothy E. Puhy, 5,226 shares; Thomas M. Ryan, 37,845 shares; James R. Jones, 73,875 shares; Jay Margolis, 37,500 shares; David A. Perdue, 75,400 shares; Kenneth I. Watchmaker, 244,000 shares; and all directors and executive officers listed above and other executive officers as a group, 1,457,175 shares.

- (9)

- Information based on a Schedule 13G dated February 14, 2002, filed with the SEC by Investors Group Trust Co. Ltd., Investors Group Trustco, Inc., Investors Group Inc., Investors Group Trust Inc., I.G. Investment Management, Ltd., Investors U.S. Large Cap Value Fund, Investors Global Fund, Investors Canadian Small Cap Fund II, Investors U.S. Opportunities Fund and Investors Canadian Equity Fund as a group (collectively, "IGT Holders"), a diversified financial services holding company, which reported the beneficial ownership of 3,354,000 shares, of which the IGT Holders have both shared voting and dispositive power with respect to all shares. The address of the IGT Holders is One Canada Centre, 447 Portage Avenue, Winnipeg, Manitoba R3C 3B6.

9

Executive Compensation

The following table shows the aggregate compensation paid or accrued by the Company for services rendered during the years that ended December 1999, 2000 and 2001 (when applicable) for (i) the Chief Executive Officer; and (ii) each of the four other most highly compensated executive officers (those falling within either clause (i) or (ii) shall be referred to herein as the "named executive officers"):

| | | | | Long Term Compensation Awards | | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | Annual Compensation | | ||||||||||

| Name | | Restricted Stock Awards($) | Securities Underlying Options(#)(2) | All Other Compensation($) | |||||||||

| Year | Salary($) | Bonus($)(1) | |||||||||||

| Paul B. Fireman Chairman and Chief Executive Officer | 2001 2000 1999 | 1,000,012 1,000,012 1,000,012 | 2,075,000 2,075,000 None | None None None | None 2,000,000 500,000 | 55,254 55,254 81,539 | (3) (3) (3) | ||||||

Jay Margolis President and Chief Operating Officer | 2001 2000 | 600,002 23,077 | 474,000 200,000 | 2,400,000 None | (4) | 400,000 150,000 | 86,325 None | (5) | |||||

Kenneth I. Watchmaker Executive Vice President; Chief Financial Officer | 2001 2000 1999 | 600,002 592,310 542,308 | 976,310 980,866 457,542 | None 393,750 None | (8) | 198,000 100,000 101,000 | (6) | 57,743 44,858 44,062 | (7) (7) (7) | ||||

David A. Perdue Executive Vice President; President and CEO, Reebok Division | 2001 2000 1999 | 600,002 434,624 350,012 | 694,310 604,597 215,250 | None 393,750 None | (8) | 228,400 100,000 None | (6) | 37,744 9,962 274,291 | (9) (9) (10) | ||||

James R. Jones, III Senior Vice President; Chief Human Resources Officer | 2001 2000 1999 | 329,992 328,456 316,928 | 238,014 229,919 145,333 | None 196,875 None | (12) | 90,500 75,000 70,000 | (6) | 30,906 25,596 13,077 | (11) (11) (11) | ||||

- (1)

- Includes any amounts deferred by the individual pursuant to the Company's Savings and Profit-Sharing Retirement Plan (the "Savings and Profit-Sharing Plan") and the Reebok Executive Deferred Compensation Plan.

- (2)

- Unless otherwise indicated, these options were granted under the 1994 Equity Incentive Plan. For more details, see the "Stock Option Grants" section.

- (3)

- Includes contributions by the Company on behalf of Mr. Fireman as follows: for 2001, $13,750 to the Savings and Profit-Sharing Plan and $41,501 in credits allocated to Mr. Fireman's account under the Company's Excess Benefits Plan; for 2000, $13,250 to the Savings and Profit-Sharing Plan and $42,001 in credits allocated to Mr. Fireman's account under the Company's Excess Benefits Plan; and for 1999, $13,000 to the Savings and Profit-Sharing Plan and $68,539 in credits allocated to Mr. Fireman's account under the Company's Excess Benefits Plan. Mr. Fireman is 100% vested in these contributions and allocations.

- (4)

- The value of the 100,000 shares of restricted stock held by Mr. Margolis as of December 31, 2001, assuming a sale price of $26.50 per share, would be $2,650,000. The Company awarded him 100,000 shares of restricted stock on December 5, 2001 at the per share price of $24.00, subject to restrictions and other conditions as discussed below in "Employee Agreements." None of these shares have vested.

- (5)

- This amount represents reimbursement of expenses incurred by Mr. Margolis in connection with his relocation to Massachusetts.

- (6)

- This number reflects the occurrence of two annual grants of stock options during 2001. The first annual grant occurred in January 2001 (related to Fiscal Year 2001) and the second annual grant in December 2001

10

(related to Fiscal Year 2002). In the future, Reebok anticipates that the annual grant of stock options will occur in December of each year.

- (7)

- Includes contributions by the Company on behalf of Mr. Watchmaker as follows: for 2001, $13,750 to the Savings and Profit-Sharing Plan and $43,993 in credits allocated to Mr. Watchmaker's account under the Excess Benefits Plan; for 2000, $13,250 to the Savings and Profit-Sharing Plan and $31,615 in credits allocated to Mr. Watchmaker's account under the Excess Benefits Plan; and for 1999, $13,000 to the Savings and Profit-Sharing Plan and $31,062 in credits allocated to Mr. Watchmaker's account under the Excess Benefits Plan. Mr. Watchmaker is 100% vested in these contributions and allocations.

- (8)

- The value of the 50,000 shares of restricted stock held by each of Mr. Watchmaker and Mr. Perdue as of December 31, 2001, assuming a sale price of $26.50 per share, would be $1,325,000. The Company awarded each of them 50,000 shares of restricted stock on January 24, 2000 at the per share price of $7.875, subject to restrictions and other conditions as discussed below in "Employee Agreements." 16,667 shares vested on July 26, 2000, after the Company met its first performance objective, and an additional 16,667 shares vested on February 6, 2001, after the Company met its second performance objective.

- (9)

- Represents contributions by the Company on behalf of Mr. Perdue as follows: for 2001, $13,750 to the Savings and Profit-Sharing Plan and $23,994 in credits allocated to Mr. Perdue's account under the Excess Benefits Plan; for 2000, $9,962 to the Savings and Profit-Sharing Plan. Mr. Perdue is 60% vested in these contributions.

- (10)

- These amounts represent reimbursements of expenses incurred by Mr. Perdue in connection with his relocation to Massachusetts.

- (11)

- Represents contributions by the Company on behalf of Mr. Jones as follows: for 2001, $13,750 to the Savings and Profit-Sharing Plan and $17,156 in credits allocated to Mr. Jones' account under the Excess Benefits Plan; for 2000, $13,250 to the Savings and Profit-Sharing Plan and $12,346 in credit allocated to his account under the Excess Benefits Plan; and for 1999, $13,000 to the Savings and Profit-Sharing Plan and $77 in credits allocated to his account under the Excess Benefits Plan. Mr. Jones is 80% vested in these contributions.

- (12)

- The value of the 9,000 shares of restricted stock held by Mr. Jones as of December 31, 2001, assuming a sale price of $26.50 per share, would be $238,500. The Company awarded him 25,000 shares of restricted stock on January 24, 2000 at the per share price of $7.875, subject to restrictions and other conditions as discussed below in "Employee Agreements." 8,333 shares vested on July 26, 2000, after the Company met its first performance objective, and an additional 8,333 shares vested on February 6, 2001, after the Company met its second performance objective.

11

Stock Option Grants

The following table shows information concerning individual grants of stock options made during 2001 to each of the named executive officers:

| | Individual Grants | | | | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | % of Total Options Granted to Employees in 2001 | | | Potential Realizable Value at Assumed Annual Rates of Stock Price Appreciation for Option Term(2) | |||||||||

| Name | Number of Options Granted(#)(1) | Exercise or Base Price ($/SH) | Expiration Date | |||||||||||

| 0%($) | 5%($) | 10%($) | ||||||||||||

| Paul B. Fireman | 0 | 0 | n/a | n/a | n/a | n/a | n/a | |||||||

| Jay Margolis | 400,000 | (3)(4) | 12.18 | 24.00 | 12/5/11 | n/a | 6,048,000 | 15,264,000 | ||||||

| Kenneth I. Watchmaker | 73,000 | 2.22 | 24.30 | 1/26/11 | n/a | 1,117,557 | 2,820,501 | |||||||

| 125,000 | (3) | 3.81 | 24.00 | 12/5/11 | n/a | 1,890,000 | 4,770,000 | |||||||

| David A. Perdue | 46,000 | 1.40 | 25.89 | 1/2/11 | n/a | 750,292 | 1,893,595 | |||||||

| 54,000 | 1.64 | 24.30 | 1/26/11 | n/a | 826,686 | 2,086,398 | ||||||||

| 28,400 | .86 | 10.25 | (5) | 4/24/11 | 347,616 | 750,007 | 1,363,174 | |||||||

| 100,000 | (3) | 3.05 | 24.00 | 12/5/11 | n/a | 1,512,000 | 3,816,000 | |||||||

| James R. Jones | 40,500 | 1.23 | 24.30 | 1/26/11 | n/a | 620,015 | 1,564,799 | |||||||

| 50,000 | (3) | 1.52 | 24.00 | 12/5/11 | n/a | 756,000 | 1,908,000 | |||||||

- (1)

- These options were granted to Messrs. Margolis, Watchmaker, Perdue and Jones under the 1994 Equity Incentive Plan. These options have a four-year vesting schedule under which twenty-five percent (25%) of the shares granted become exercisable on the first four anniversaries of the date of the grant. The options will also become exercisable upon the death or permanent disability of the optionee and may become exercisable upon certain circumstances in the event of a merger, consolidation, sale of substantially all of the Company's assets or other transaction or series of transactions that result in a change of control of the Company's Common Stock.

- (2)

- The assumed annual rates of stock price appreciation of 5% and 10% per annum are established by the SEC and are not to be construed as a forecast of future appreciation. The actual realized value of such options will depend on the market value of the Common Stock on the date of exercise; no gain will be realized by the optionees unless there is an increase in the stock price from the price on the date of grant except as noted for Mr. Perdue.

- (3)

- The Company granted these options as part of the annual grant process for Fiscal Year 2002 in December 2001 rather than in January 2002. In the future, Reebok anticipates that the annual grant of stock options will now take place in December of each year.

- (4)

- The Company intends that this mega-grant option to Mr. Margolis be in lieu of regular annual grants for his current position during the initial term of his Employment Agreement, which is discussed in the "Employee Agreements" section.

- (5)

- The market price on April 24, 2001, which was the date of grant for this option, was $22.49.

12

Aggregated Option Exercises and Values

The following table sets forth aggregated option exercises in 2001 and option values as of December 31, 2001 for each of the named executive officers:

AGGREGATED OPTION EXERCISES IN 2001

AND OPTION VALUES AS OF DECEMBER 31, 2001

| Name | Shares Acquired on Exercise(#) | Value Realized($) | Number of Unexercised Options at 12/31/01(#) Exercisable/Unexercisable | Value of Unexercised In-the-Money Options at 12/31/01($)(1) Exercisable/Unexercisable | ||||

|---|---|---|---|---|---|---|---|---|

| Paul B. Fireman | — | — | 611,150/2,000,000 | 4,245,000/17,250,000 | ||||

| Jay Margolis | — | — | 37,50/512,500 | 137,250/1,000,000 | ||||

| Kenneth I. Watchmaker | 80,000 | 1,460,374 | 175,500/383,500 | 2,430,938/3,264,663 | ||||

| David A. Perdue | 30,000 | 756,450 | 25,400/294,600 | 411,888/2,075,973 | ||||

| James R. Jones | — | — | 66,250/174,250 | 963,047/1,586,366 |

- (1)

- Based on a fair market value as of December 31, 2001 of $26.50 per share. Values are stated on a pre-tax basis.

Supplemental Executive Retirement Plan

The Board of Directors, on February 15, 1996, adopted a Supplemental Executive Retirement Plan (the "SERP") for certain key executive officers, including Mr. Fireman and Mr. Watchmaker. The SERP provides that a participant, upon attaining age 60, will receive an annual retirement benefit equal to (a) twenty-five percent (25%) of his or her average total compensation for the three calendar years out of the five consecutive calendar years ending with the year in which the participant retires ("Final Average Compensation"), in which he or she had the highest total compensation multiplied by (b) the number of years of such executive's service with the Company (not to exceed 15) divided by 15. The SERP also provides for reduced benefits for participants who retire after age 55, but before age 60, and have completed at least five full years of continuous service with the Company, or who retire before age 55, and have completed at least ten full years of continuous service.

In February 1999, the SERP was amended to provide that participants who voluntarily terminate their employment with the Company will forfeit their eligibility and further benefits if, prior to age 65, they work on a full-time basis (excluding service on a board of directors, government or public service or teaching) after leaving the Company, or if at any time they perform any services for a competitor of the Company. The SERP was further amended in December 2001 to provide that the Final Average Compensation would be calculated as the average total compensation for the three calendar years out of the ten consecutive calendar years immediately prior to the year in which the executive retires, in which the executive had the highest total compensation.

13

The following table sets forth estimated annual benefits payable under the SERP upon a participant's retirement, assuming attainment of age 60 while in the employment of the Company, for the following compensation levels and years of service:

| | Years of Service | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Final Average Total Compensation | |||||||||

| 5 | 10 | 15 and above | |||||||

| $ 450,000 | $ | 37,500 | $ | 75,000 | $ | 112,500 | |||

| 550,000 | 41,667 | 83,333 | 125,000 | ||||||

| 750,000 | 62,500 | 125,000 | 187,500 | ||||||

| 1,000,000 | 83,333 | 166,667 | 250,000 | ||||||

| 1,250,000 | 104,164 | 208,333 | 312,500 | ||||||

| 1,500,000 | 125,000 | 250,000 | 375,000 | ||||||

| 1,750,000 | 145,833 | 291,667 | 437,500 | ||||||

| 2,000,000 | 166,667 | 333,333 | 500,000 | ||||||

| 2,250,000 | 187,500 | 375,000 | 562,500 | ||||||

The compensation covered by the SERP for any calendar year is the participant's base compensation and annual incentive bonus earned for such year (which are reflected in the Salary and Bonus columns of the Summary Compensation Table), plus any amount that would have been paid to the participant but for a salary reduction agreement in effect during such year pursuant to Sections 125 or 401(k) of the Internal Revenue Code of 1986, as amended (the "Code"). The benefit payment under the SERP is not subject to any deductions for Social Security benefits or other offset amounts. Years of service credited under the SERP for the executive officers named in the Summary Compensation Table above who are participants in the SERP are as follows: Paul B. Fireman, 22 years; and Kenneth I. Watchmaker, 9 years.

Employee Agreements

The Company entered into a split-dollar insurance agreement as of September 25, 1991 with a trust established by Mr. Fireman, pursuant to which the Company and that trust will share in the premium costs of a whole life insurance policy that pays a death benefit of not less than $50,000,000 upon the death of Mr. Fireman, age 58, or Phyllis Fireman, age 57 (whichever occurs later). Under the agreement, the Company paid that portion of each annual policy premium that, in general terms, was equal to the annual increase in the cash value of the policy. The Company's obligation to make such premium payments terminated in 1996 upon the payment of the sixth annual premium due under the policy. In 1999, the Company restructured the related key man policy of which the Company is the beneficiary and which is designed to work in conjunction with the split-dollar insurance policy to insure the repayment to the Company of the aggregate amount of the premiums paid by the Company. Pursuant to this restructuring, the Company applied its cash value to the full premium of the restructured policy resulting in no premium payment obligations in 1999 or thereafter. The Company may cause the agreement to be terminated and the policy to be surrendered at any time upon 60 days' prior notice. Upon surrender of the policy or payment of the death benefit under the policy, the Company is entitled to repayment of an amount equal to the cumulative premiums previously paid by the Company, with all remaining payments to be made to the Paul Fireman Irrevocable Trust—1991.

In connection with the February 1999 amendment to the SERP, as described above in the section entitled "Supplemental Executive Retirement Plan", Mr. Fireman and Mr. Watchmaker executed Consents, each dated April 19, 1999, in which they agreed to forfeit their eligibility and further benefits under the SERP if, prior to age 65, they work on a full-time basis (excluding service on a board of directors, government or public service or teaching) after leaving the Company, or if at any time they perform any services for a competitor of the Company. In consideration of these Consents, the Company (i) granted Mr. Fireman an option to purchase 1,000 shares of Common Stock expiring on

14

April 19, 2009, at an exercise price of $18.01; and (ii) granted Mr. Watchmaker an option to purchase 1,000 shares of Common Stock, expiring on April 19, 2009, at an exercise price of $17.75.

The Company has change of control agreements with Mr. Watchmaker, Mr. Margolis, Mr. Perdue and Mr. Jones providing for certain compensation and benefits in the event of the termination of their employment with the Company following a "change in control" of the Company (as defined in the respective agreements). A "change in control" includes one which is initiated by Company management except in the case of a leveraged buy-out or recapitalization of the Company in which the executive participates as an equity investor. In each agreement, if the executive's employment with the Company were to terminate (other than as a result of the death, total disability or retirement of the executive at or after his normal retirement date) within 24 months following a change in control and the termination is (a) by the Company for a reason other than as a result of a conviction of the executive for a felony or a crime involving moral turpitude or (b) by the executive if the Company fails to maintain the executive in the positions, with the titles, that he held immediately prior to the change of control, following a downgrading of his responsibilities or authority or if the Company makes certain other changes or reductions in the executive's compensation as specified in the agreement, then the Company will pay to the executive a lump-sum cash payment equal to 300% of the aggregate of his (i) then-current annual base salary, (ii) his target bonus for the then-current year, or, if higher, his bonus for the most recent calendar year ended before the change of control, (iii) the amount of his then-current annual personal expense allowance and (iv) the annual cost of life insurance then furnished to him by the Company. In addition, all of the executive's outstanding stock options, restricted shares and other similar incentive rights and interests will become immediately and fully vested and exercisable. The executive will be treated for purposes of the SERP as having three additional years of continuous service and the Company will pay to him in a single lump-sum cash payment the present value of his benefit under the SERP. The Company will pay to the executive, in a single lump-sum cash payment, an amount equal to the difference, if any, between (i) the total distribution that he receives following his termination under the Company's Savings and Profit-Sharing Retirement Plan and its Excess Benefits Plan and (ii) the total distribution that he would have received under such plans had he accumulated three additional years of service for vesting prior to termination. The executive and his dependents will also continue to participate fully at the expense of the Company in all accident and health plans provided by the Company immediately prior to the change in control, or receive substantially equivalent coverage, until the third anniversary of his termination of employment. In addition, the agreements provide that the executive will be reimbursed by the Company for any legal fees and expenses incurred by him as a result of the termination of his employment. Each agreement provides that if it is determined that any payment or benefit provided by the Company to or on behalf of the executive, either under the executive's change of control agreement or otherwise, is subject to the excise tax imposed by Section 4999 of the Code, the Company will make an additional lump-sum payment to the executive which will be sufficient to make the executive whole for all taxes and any associated interest and penalties imposed under or as a result of Section 4999. Messrs. Watchmaker, Margolis, Perdue and Jones are required under the agreements not to leave voluntarily the employ of the Company in the event that any person or entity initiates a change of control until such time as the effort terminates or the change of control is completed. The Company amended Mr. Watchmaker's and Mr. Jones' change of control agreements in February 2000, such that if Mr. Fireman is no longer Chief Executive Officer of the Company it will be deemed a "change of control" under the Agreement.

The Company has non-competition agreements with Mr. Watchmaker, Mr. Margolis, Mr. Perdue and Mr. Jones under which each executive has agreed not to compete, directly or indirectly, with the Company during his employment and pursuant to which the Company has the right to extend the non-competition requirement for a period of up to one year after his termination of employment with the Company (the "Non-Competition Period"). During the Non-Competition Period, the Company will pay the executive an amount equal to one-half of his base salary as in effect on his termination date

15

and will continue certain medical coverage benefits, except that for Mr. Watchmaker, if the Company terminates his employment without "cause" (as defined in the agreement), he would be entitled to 100% of his base salary as of the date of termination, which amount shall be reduced by the amount of any severance payments received from the Company.

As a retention tool for certain key executives, the Board of Directors approved the grant of shares of restricted stock in January 2000 and an annual supplemental bonus program. This bonus will be in addition to any bonus payable under the Company's Bonus Plan (as defined below), or any similar program then in effect. The program will last for four years. The objectives of the restricted stock grant were to: (1) maintain the focus on shareholder returns and align senior management's interest more closely with shareholders, (2) retain certain key executives, and (3) deliver a significant increase in compensation for exceptional Company performance. Mr. Watchmaker, Mr. Perdue and Mr. Jones each received a grant of shares of Reebok Common Stock as of January 24, 2000 at a price of $7.875. The shares are "restricted," which means that they are not transferable and cannot be sold until they vest. The restricted stock will fully vest on January 24, 2004 subject to earlier vesting if the Company achieves certain established goals. Specifically: (a) one-third of the Restricted Shares will vest prior to that date if the Company's earnings per share ("EPS") at year end is $1.50 or more, or if the stock price for Reebok closes at $18.00 per share or more for any five trading days in any ten trading day period; (b) an additional one-third of the Restricted Shares will vest if the Company's EPS at year end is $2.25 or more, or if the stock price for Reebok closes at $27.00 or more for five trading days in a ten trading day period; and (c) the remaining one-third of the Restricted Shares will vest if the Company's EPS at year end is $3.00 or more, or if the stock price for Reebok closes at $36.00 or more for five trading days in a ten trading day period. As of the Record Date, two-thirds of the Restricted Shares have vested.

At the same time, Reebok adopted an Executive Loan Program. The loan may be called and required to be paid in full if: (i) the employee fails to make payments when due, or (ii) if the employment with Reebok is terminated for any reason. Each of Mr. Watchmaker and Mr. Perdue, both of whom are executive officers, became indebted individually to the Company during 2000 in the amount of $184,078 through the execution of a promissory note payable over four years (with interest accruing at 6.21% per year). As of the Record Date, $92,039 remains outstanding on the loan for each of Mr. Watchmaker and Mr. Perdue. Mr. Jones, who is also an executive officer, became indebted individually to the Company during 2000 in the amount of $92,039 through the execution of a promissory note payable over four years (with interest accruing at 6.21% per year). As of the Record Date, $46,021 remains outstanding on the loan for Mr. Jones.

The Company entered into an employment agreement with Jay Margolis, President and Chief Operating Officer of Reebok International Ltd. effective December 5, 2001 (the "Margolis Agreement"), which has an initial term of three years. This initial term will be automatically extended for up to two additional one-year terms unless terminated earlier pursuant to the terms of the Margolis Agreement. Pursuant to the Margolis Agreement, he receives an initial base salary of $1,000,000 per year with a guaranteed increase on January 1, 2003. He is entitled to receive an annual bonus of up to 100% of his base salary based on his achievement of certain financial and management performance goals on the same basis as other senior executives of the Company. As part of the Margolis Agreement, the Company also granted him 100,000 shares of restricted stock, which will vest in its entirety on December 31, 2004, but may be accelerated and become immediately vested in certain early termination circumstances. In addition, the Company granted him 400,000 non-qualified stock options. The Company intends that this mega-grant option to Mr. Margolis, which shall vest over four years, be in lieu of regular annual grants for his current position during the initial term of his Employment Agreement.

The Company also entered into an employment agreement with David Perdue, President of the Reebok Brand effective January 1, 2002 (the "Perdue Agreement"), which has an initial term of three

16

years. This initial term will be automatically extended for up to two additional one-year terms unless terminated earlier pursuant to the terms of the Perdue Agreement. Pursuant to the Perdue Agreement, Mr. Perdue receives a base salary of $600,000 per year, which may be adjusted upwards. He is also entitled to receive an annual bonus of up to 100% of his base salary based on his achievement of certain financial and management performance goals on the same basis as other senior executives of the Company.

Both the Margolis Agreement and the Perdue Agreement (the "Employment Agreements") may be terminated prior to the end of its term by the executive without good reason upon ninety days prior written notice or with good reason (defined therein) upon fourteen days prior written notice. The Company may terminate either of the Employment Agreements upon written notice for cause (defined therein), death or for any other reasons. In the event of the executive's voluntary termination without good reason, termination by Reebok for cause, or termination as a result of his death or incapacity, the executive would be entitled to payment of his base salary and medical coverage only until the last day of his active employment. If his employment is terminated as the result of his voluntary termination with good reason or involuntary termination for reasons other than cause, death or incapacity, he is entitled to continuation of his base salary and medical coverage and certain other benefits for up to a maximum of eighteen (18) months.

The above description is only a summary of the agreements which the Company has with its various executive officers and is qualified in its entirety by the actual agreements, copies of which have been filed as Exhibits to the Company's Annual Report on Form 10-K.

17

Report of Compensation Committee On Executive Compensation

The Compensation Committee has submitted the following report:

The Committee in 2001 consisted of Geoffrey Nunes, Chair, Thomas M. Ryan and Norman Axelrod (starting on May 1, 2001). The Compensation Committee's responsibilities include setting both the cash and equity compensation level for the Chief Executive Officer and reviewing the cash and equity compensation levels for all other executive officers as well as other highly compensated employees of the Company. Compensation for these other individuals is established by the Chief Executive Officer. The Committee also functions as the stock option committee, and in that capacity administers the 1994 Equity Incentive Plan and the 2001 Equity Incentive and Director Deferred Compensation Plan and approves all stock option grants to executive officers.

The Committee held four meetings during 2001 and acted once by unanimous consent. Specifically, it held meetings in February, July, October, and December. In its review of executive officer compensation for 2001, the Committee considered the results of "Competitive Assessment of Executive Compensation," a report prepared by an outside compensation consulting firm at the Committee's request. An analysis of the report showed that compensation payable to executives of the Company was largely consistent with the Company's philosophy that executives' base salary should be at the median and the total annual target compensation should be in the seventy-fifth percentile of its peer group of companies in the shoe and apparel industries as well as other leading consumer product organizations. The Committee approved the compensation for the executive officers for 2001 and modified the target bonus levels for certain of these executives based upon the results of the report.

The Committee elected to continue Mr. Fireman's cash compensation for 2001 at $1,000,000 per year and established a 2001 bonus for Mr. Fireman based on objective criteria of pre-tax operating profit and operating cash flow of the Company as a whole. In addition, the Committee increased Mr. Fireman's potential bonus target from 100% to 125% of his annual base salary, partially in recognition of his declining to accept a base pay raise in over ten years.

In February 2001, the Committee reviewed the Company's proposed Performance Incentive Plan (the "Bonus Plan") for 2001, pursuant to the terms of an Omnibus Executive Performance Incentive Plan previously approved by shareholders in 1996 (and subsequently approved again by Shareholders in May 2001), and the bonus award calculations under the Bonus Plan. The Bonus Plan permits bonuses to be paid to certain named executives only if specific financial criteria established by the Committee are met. Thus, bonuses paid under the Bonus Plan qualify for a tax deduction pursuant to Section 162(m) of the Code. The financial criteria are based on pre-tax operating profit, and other factors including cash flow from operations and increase in sales or year-end sales backlog, as appropriate. For some executives, these criteria are assessed against the results of a particular operating unit for which the executive is responsible, while for others they are assessed against the Company's overall financial results or a combination of both.

The Committee also determined the amount of the target award that would be paid if the financial criteria were satisfied. For 2001, participants had the ability to earn (i) a portion of their target award only if at least 87.5% of the financial criteria were met, (ii) 100% of their target award if all of the financial criteria were met, and (iii) could earn more than 100% of the target award (up to a maximum of 200% of the award) if the criteria were exceeded. Under the Bonus Plan, any award in excess of 125% of the target award may be deferred and paid in two equal installments on the first and second anniversary of the bonus award payment date. Target awards were fixed as a percentage of base salary and ranged from 50% to 100%. Under the Bonus Plan, the Committee has reserved the ability to reduce any award or eliminate any award based on the overall financial performance of the Company, as well as certain other factors.

18

Bonuses for the executive officers for 2001 were determined in accordance with the Bonus Plan and the Company's actual 2001 financial results. In February 2002, the Committee met to review the Company's actual financial results for 2001 and to determine whether such results satisfied the financial criteria established under the Bonus Plan. The Corporate groups essentially met their pre-tax operating profit target and exceeded the operating cash flow target in 2001. The Reebok Brand essentially met its pre-tax operating profit and exceeded its operating cash flow target, but did not achieve its target to increase sales or its target on increasing the year-end Reebok Brand backlog target. Rockport, Greg Norman Collection, and Ralph Lauren Footwear each did not achieve their targets. Based on these financial results, the Bonus Plan provided for funding of the target bonuses that were calculated based on the satisfied financial targets, and maximum payout of the target bonuses that were calculated based on the Company's cash flow. In addition, if an executive failed to manage departmental expenses consistent with his budget, the bonus was subject to reduction. In the case of Mr. Fireman, he received a bonus of $1,825,000 under the Bonus Plan. In recognition of his accomplishments in 2001 and the fact that he exceeded all of the stated objectives, the Committee granted in its discretion an additional bonus, outside of the Bonus Plan, of $250,000.

The Committee amended the Supplemental Executive Retirement Plan in December 2001 such that the final average total compensation will now be calculated as the average total compensation for the three calendar years out of the ten consecutive calendar years immediately prior to the year in which the executive retires, in which the executive had the highest total compensation. In addition, the Committee agreed that under certain limited circumstances it would permit executives to receive a discounted lump sum payment in lieu of payment through an annual benefit.

The Committee generally grants stock options to executive officers to provide long-term performance related incentives that link rewards directly to shareholder gains over a multi-year period. Under the Company's current program, the stock options for officers of the Company generally vest over a four-year period in equal installments. The stock options awarded to executive officers have an exercise price equal to the fair market value of the Company's Common Stock on the date of grant. As part of the annual process, the Company granted stock options to executive officers in both January 2001 (related to Fiscal Year 2001) and December 2001 (related to Fiscal Year 2002). In the future, Reebok anticipates that the annual grant of stock options will take place in December of each year starting in December 2002.

In adopting and administering executive compensation plans and arrangements, the Committee considers whether the deductibility of such compensation will be limited under Section 162(m) of the Code, and, in appropriate cases, will attempt to structure such compensation so that any such limitation will not apply.

COMPENSATION COMMITEE

Geoffrey Nunes, Chair

Thomas M. Ryan

Norman Axelrod

19

Report of the Audit Committee

The Audit Committee is composed of three independent directors (Ms. Puhy, Chair, Mr. Lesser and Mr. Nunes) and operates under a written charter adopted by the Board of Directors in 2000. The Audit Committee reviews the Company's financial reporting process on behalf of the Board of Directors, reviews the financial information issued to shareholders and others, and monitors the systems of internal control and the audit process. Management has primary responsibility for the financial statements and the reporting process.

The Audit Committee has met and held discussions with management and the independent auditors. In our discussions, management has represented to the Audit Committee that the Company's consolidated financial statements were prepared in accordance with generally accepted accounting principles. The Audit Committee has reviewed and discussed the consolidated financial statements with both management and Ernst & Young LLP, our independent auditors. The Audit Committee meets with our independent auditors, with and without management present, to discuss the results of their examinations, the evaluations of the Company's internal controls and the overall quality of the Company's financial reporting. The Audit Committee discussed with the independent auditors matters required to be discussed by Statement on Auditing Standards No. 61 (Communication with Audit Committees).

The Company's independent auditors also provided to the Committee the written disclosures and the letter required by Independence Standards Board Standard No. 1 (Independence Discussions with Audit Committees), and the Audit Committee has considered and discussed with Ernst & Young the firm's independence and the compatibility of the non-audit services provided by the firm with its independence. Based on the Audit Committee's review of the audited financial statements and the various discussions noted above, the Audit Committee recommended that the Board of Directors include the audited consolidated financial statements in the Company's Annual Report on Form 10-K for the year ended December 31, 2001.

AUDIT COMMITEE

Dorothy E. Puhy, Chair

Richard G. Lesser

Geoffrey Nunes

20

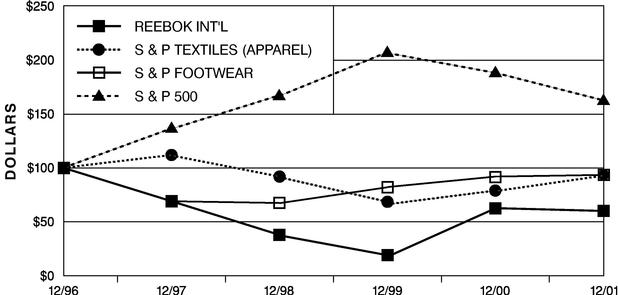

Performance Graph

The following graph shows a five-year comparison of cumulative total returns for the Company's Common Stock, the Standard & Poor's 500 Stock Index, and the Standard & Poor's Shoes and Textile Apparel Manufacturers Indices* from December 31, 1996 to December 31, 2001. The graph assumes an investment of $100 on December 31, 1996 in each of the Company's Common Stock and the stocks comprising the Standard & Poor's 500 Stock Index and the Standard & Poor's Shoes and Textile Apparel Manufacturers Indices. Performance shown for each of the indices assumes that all dividends were reinvested.

TOTAL SHAREHOLDER RETURNS

(Dividends Reinvested)

*The Standard & Poor's Shoes and Textile Apparel Manufacturers Indices were selected in order to compare the Company's performance with companies in each of the two primary lines of business in which the Company is engaged. The indices do not, however, include all of the Company's competitors, nor all product categories and lines of business in which the Company is engaged.

The Stock Performance shown on the Performance Graph above is not necessarily indicative of future performance. The Company will not make nor endorse any predictions as to future stock performance.

21

Transactions with Management and Affiliates

In April 1996, the Company entered into a three-year agreement with the Harlem Globetrotters International, Inc. (the "Globetrotters"). In April 1999, the Company and the Globetrotters amended and restated that agreement (the "1999 Agreement"), which extended the arrangement through March 31, 2002. Under the 1999 Agreement, Reebok is the exclusive athletic footwear and apparel sponsor of the Globetrotters and has been granted a license to produce and sell Reebok products bearing the Globetrotters' team trademark for a royalty payment of 5% of Reebok's production cost, with specified guaranteed royalty payments. The 1999 Agreement provides that Reebok will pay the Globetrotters $200,000 per year and supply to the Globetrotters Reebok products having an aggregate wholesale value not to exceed $50,000 per year. During 2001, Reebok paid to the Globetrotters $200,000 in payments due in accordance with the agreement and approximately $175,000 for special promotional appearances and sponsorships. Reebok also supplied products to the Globetrotters with an approximate wholesale value of $50,000. Mannie L. Jackson, a current director of the Company, is the Chairman, Chief Executive Officer and majority owner of the Globetrotters.

Indebtedness of Management

See the section entitled "Employee Agreements" for a description of such arrangements.

PROPOSAL 2: SHAREHOLDER PROPOSAL

THAT ALL MEMBERS OF THE BOARD OF DIRECTORS BE ELECTED ANNUALLY

The following proposal was submitted on behalf of the Connecticut Retirement Plans & Trust Fund ("CRPTF"), a shareholder of the company, by Denise L. Nappier, Treasurer of the State of Connecticut. CRPTF has informed the Company that its address is Office of the Treasurer, 55 Elm Street, Hartford, CT 06106-1773, and that it is the owner of approximately 76,700 shares of the Company's Common stock.

"BE IT RESOLVED, that the shareholders of Reebok International Ltd. urge the board of directors to take the necessary steps to eliminate the classification of the Board of Directors of the Company and to require that all directors stand for election annually. The board declassification shall be completed in a manner that does not affect the unexpired terms of directors previously elected."

"We believe the election of directors is the most powerful way Reebok shareholders influence the strategic direction of our Company. Currently the board is divided into three classes of three members each. Each class serves staggered three-year terms. Because of this structure, shareholders may only vote on roughly one-third of the directors each year.

The staggered term structure of Reebok's board is not in the best interests of shareholders because it reduces accountability and is an unnecessary anti-takeover device. Shareholders should have the opportunity to vote on the performance of the entire board of directors each year. We feel that such annual accountability serves to keep directors closely focused on the performance of top executives and on increasing shareholder value. Annual election of all directors gives shareholders the power to either completely replace their board, or replace a majority of directors, if a situation arises which warrants such drastic action.

We do not believe destaggering the Board of Reebok will be destabilizing to our Company or impact the continuity of director service. Our directors, like the directors of the overwhelming majority of other public companies, are routinely elected with over 95% shareholder approval.

There are indications from studies that classified boards and other anti-takeover devices have an adverse impact on shareholder value. A 1991 study by Lilli Gordon of the Gordon Group and John

22

Pound of Harvard University found that companies with restrictive corporate governance structures, including those with classified boards, are "significantly less likely to exhibit outstanding long-term performance relative to their industry peers."

A growing number of shareholders appear to agree with our concerns. Last year, a majority of shareholders supported proposals asking their boards to repeal classified board structures at 29 companies, including Bristol-Meyers Squibb, May Department Stores, and Southwest Airlines.

We believe that adoption of this proposal will be beneficial to the company and its shareholders."

Statement of Board of Directors Recommending

A Vote Against This Shareholder Proposal

The Board of Directors believes that the present system of electing directors of the Company in three classes is in the best interests of the Company and its stockholders and should not be changed.

A classified board offers important advantages to stockholders and is the preferred method of governance for the majority of Fortune 500 companies. Moreover, a classified board protects shareholders against potentially coercive takeover tactics, whereby a party attempts to acquire control on terms that do not offer the greatest value to all stockholders. Because a classified board prevents the immediate removal of directors, any person seeking to acquire control of the company is encouraged to negotiate with the Board. This ensures the Board sufficient time to develop and consider appropriate strategy and enhances its ability to negotiate the best result for all stockholders.

In addition, Massachusetts law requires all publicly held corporations to have a classified board, unless the company affirmatively exempts itself from such requirement. The legislative history surrounding enacting of this law shows a decided preference for classified boards in the interest of public policy.

The Board believes that a classified board enhances continuity and stability in the Company's management and policies since a majority of the directors at any given time will have had a prior experience and familiarity with the business of the Company. This continuity and stability facilitates more effective long-term planning and is integral to increasing the Company's value to stockholders. Moreover, such continuity helps the Company attract and retain qualified individuals willing to commit the time and dedication necessary to understand the Company, its operations and competitive environment.

The Board is committed to corporate accountability and does not accept the proposition that a classified board insulates directors from responsibility. A classified board permits stockholders to annually change one-third of the directors and thereby substantially change the Board's composition and character. Corporate accountability depends on the selection of responsible and experienced individuals, not on whether they serve terms of one year or three. The Board Affairs Committee reviews the independence of directors and evaluates the contribution of individual directors and the Board's contribution as a whole on an annual basis. This Committee also reviews director nominations, recommends guidelines and criteria for Board membership, and has responsibility for other corporate governance issues.

The Company understands that the Board should be responsive to shareholders and has taken steps to assure corporate accountability through such measures as maintaining a majority of outside directors; and having only independent directors on the Audit Committee, the Compensation Committee and the Board Affairs Committee. In addition, to encourage the alignment of the interests of the members of the Board with those of shareholders, the Board has a policy mandating required levels of stock ownership by its Directors and requiring the deferral of at least 40% of an outside directors' annual retainer into Reebok Common Stock.

23

Finally, shareholders should be aware that adoption of this proposal would not eliminate board classification and institute the annual election of directors, but would constitute merely a recommendation by the stockholders that the Board consider enacting such a change. The affirmative vote of two-thirds of the outstanding shares or a vote of the directors is required to opt out of the Massachusetts law and declassify the Board.

For the reasons outlined above, the Board has concluded that a classified board is in the best interests of the Company and its shareholders, and thus is opposed to the CRPTF's shareholder proposal.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Securities Exchange Act of 1934 requires the Company's executive offers and directors to file initial reports of ownership and reports of changes in ownership with the Securities and Exchange Commission and the New York Stock Exchange. Executive officers and directors are required by SEC regulations to furnish the Company with copies of all Section 16(a) forms they file. To the Company's knowledge, based solely on a review of the copies of such forms furnished to the Company and written representations from the Company's executive officers and directors, all required Section 16(a) filings were timely made during 2001.

Independent Public Accountants

Ernst & Young LLP has been reappointed to audit the consolidated financial statements of the Company for the year ended December 31, 2002, and to report the results of their audit to the Audit Committee of the Board of Directors. A representative of Ernst & Young LLP is expected to be present at the Meeting, will have the opportunity to make a statement if the representative desires to do so, and will be available to respond to appropriate questions from shareholders.

Fees billed to the Company by Ernst & Young LLP during Fiscal Year 2001

Audit Fees:

Audit fees incurred by the Company from Ernst & Young LLP during the Company's 2001 fiscal year for the audit of the Company's annual financial statements and review of those financial statements included in the Company's quarterly reports on Form 10-Q totaled $1,600,000.

Financial Information Systems Design and Implementation Fees:

The Company did not engage Ernst & Young LLP to provide advice to the Company regarding financial information systems design and implementation during the Company's 2001 fiscal year.

All Other Fees:

Fees billed to the Company by Ernst & Young LLP during the Company's 2001 fiscal year for all other non-audit services performed totaled $2,200,000, which includes audit-related services of $700,000 and other non-audit services of $1,500,000. Audit-related services generally include fees for services performed relating to employee benefit plans and statutory audits, accounting consultations and SEC registration statements. The balance of the work included tax compliance and consulting, customs services and expatriate tax services.

24

Advance Notice Procedures

Under the Company's bylaws, nominations for director may be made only (a) by or at the direction of the Board of Directors or an appropriate committee of the Board of Directors or (b) by any stockholder of record who is entitled to vote for the election of directors at the meeting who has delivered written notice to the Clerk of the Company (containing certain information specified in the bylaws) (i) not less than 75 nor more than 120 days prior to the anniversary date of the preceding year's annual meeting or (ii) if the meeting is called for a date which is more than 75 days prior to such anniversary date, not later than the close of business on the 10th day following the day on which notice of such meeting is mailed or publicly disclosed, whichever is earlier. Under recent changes to the federal proxy rules, if a stockholder who wishes to present such a proposal fails to notify the Company by the date required by the Company's bylaws, then the proxies that management solicits for the annual meeting will include discretionary authority to vote on the stockholder's proposal in the event it is properly brought before the meeting, notwithstanding anything to the contrary in the Company's bylaws.