UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2009

Commission file number: 1-13283

Penn Virginia Corporation

(Exact name of registrant as specified in its charter)

| | |

| Virginia | | 23-1184320 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification Number) |

Three Radnor Corporate Center, Suite 300

100 Matsonford Road

Radnor, Pennsylvania 19087

(Address of principal executive offices)

Registrant’s telephone number, including area code: (610) 687-8900

Securities registered pursuant to Section 12(b) of the Act:None

Securities registered pursuant to Section 12(g) of the Act:

| | |

| Title of each class | | Name of exchange on which registered |

| Common Stock, $0.01 Par Value | | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yesx Noo

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934 (“Exchange Act”). Yeso Nox

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesx Noo

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check One)

| | | | | | |

| Large accelerated filerx | | Accelerated filero | | Non-accelerated filero | | Smaller reporting companyo |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yeso Nox

The aggregate market value of common stock held by non-affiliates of the registrant was $532,899,076 as of June 30, 2009 (the last business day of its most recently completed second fiscal quarter), based on the last sale price of such stock as quoted on the New York Stock Exchange. For purposes of making this calculation only, the registrant has defined affiliates as including all directors and executive officers of the registrant, but excluding any institutional shareholders. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of February 22, 2010, 45,409,837 shares of common stock of the registrant were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement relating to the registrant’s Annual Meeting of Shareholders, to be held on May 5, 2010, is incorporated by reference in Part III of this Form 10-K.

i

TABLE OF CONTENTS

Forward-Looking Statements

Certain statements contained herein that are not descriptions of historical facts are “forward-looking” statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, or Exchange Act. Because such statements include risks, uncertainties and contingencies, actual results may differ materially from those expressed or implied by such forward-looking statements. These risks, uncertainties and contingencies include, but are not limited to, the following:

| • | the volatility of commodity prices for natural gas, NGLs, crude oil and coal; |

| • | our ability to access external sources of capital; |

| • | uncertainties relating to the occurrence and success of capital-raising transactions, including securities offerings and asset sales; |

| • | reductions in the borrowing base under our revolving credit facility, or Revolver; |

| • | our ability to develop and replace oil and gas reserves and the price for which such reserves can be acquired; |

| • | any impairment write-downs of our reserves or assets; |

| • | reductions in our anticipated capital expenditures; |

| • | the relationship between natural gas, NGL, crude oil and coal prices; |

| • | the projected demand for and supply of natural gas, NGLs, crude oil and coal; |

| • | the availability and costs of required drilling rigs, production equipment and materials; |

| • | our ability to obtain adequate pipeline transportation capacity for our oil and gas production; |

| • | competition among producers in the oil and natural gas and coal industries generally and among natural gas midstream companies; |

| • | the extent to which the amount and quality of actual production of our oil and natural gas or Penn Virginia Resource Partners, L.P., or PVR’s, coal differ from estimated proved oil and gas reserves and recoverable coal reserves; |

| • | PVR’s ability to generate sufficient cash from its businesses to maintain and pay the quarterly distribution to its general partner and its unitholders; |

| • | the experience and financial condition of PVR’s coal lessees and natural gas midstream customers, including the lessees’ ability to satisfy their royalty, environmental, reclamation and other obligations to PVR and others; |

| • | operating risks, including unanticipated geological problems, incidental to our business and to PVR’s coal and natural resource management or natural gas midstream business; |

| • | PVR’s ability to acquire new coal reserves or natural gas midstream assets and new sources of natural gas supply and connections to third-party pipelines on satisfactory terms; |

| • | PVR’s ability to retain existing or acquire new natural gas midstream customers and coal lessees; |

| • | the ability of PVR’s lessees to produce sufficient quantities of coal on an economic basis from PVR’s reserves and obtain favorable contracts for such production; |

| • | the occurrence of unusual weather or operating conditions including force majeure events; |

| • | delays in anticipated start-up dates of our oil and natural gas production, of PVR’s lessees’ mining operations and related coal infrastructure projects and new processing plants in PVR’s natural gas midstream business; |

| • | environmental risks affecting the drilling and producing of oil and gas wells, the mining of coal reserves or the production, gathering and processing of natural gas; |

ii

TABLE OF CONTENTS

| • | the timing of receipt of necessary governmental permits by us and by PVR or PVR’s lessees; |

| • | changes in governmental regulation or enforcement practices, especially with respect to environmental, health and safety matters, including with respect to emissions levels applicable to coal-burning power generators; |

| • | uncertainties relating to the outcome of current and future litigation regarding mine permitting; |

| • | risks and uncertainties relating to general domestic and international economic (including inflation, interest rates and financial and credit markets) and political conditions (including the impact of potential terrorist attacks); |

| • | Penn Virginia GP Holdings, L.P.’s ability to generate sufficient cash from its interests in PVR to maintain and pay the quarterly distribution to its unitholders; |

| • | uncertainties relating to our continued ownership of interests in PVG and PVR; and |

| • | other risks set forth in Item 1A of this Annual Report on Form 10-K for the year ended December 31, 2009. |

Additional information concerning these and other factors can be found in our press releases and public periodic filings with the Securities and Exchange Commission. Many of the factors that will determine our future results are beyond the ability of management to control or predict. Readers should not place undue reliance on forward-looking statements, which reflect management’s views only as of the date hereof. We undertake no obligation to revise or update any forward-looking statements, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

iii

TABLE OF CONTENTS

Part I

Item 1 Business

General

Penn Virginia Corporation (NYSE: PVA) is an independent oil and gas company primarily engaged in the development, exploration and production of natural gas and oil in various domestic onshore regions including East Texas, the Mid-Continent, Appalachia and Mississippi. We also indirectly own partner interests in Penn Virginia Resource Partners, L.P. (NYSE: PVR), or PVR, a publicly traded limited partnership formed by us in 2001. Our ownership interests in PVR are held principally through our general partner interest and our 51.4% limited partner interest in Penn Virginia GP Holdings, L.P. (NYSE: PVG), or PVG, a publicly traded limited partnership formed by us in 2006. As of December 31, 2009, PVG owned an approximate 37% limited partner interest in PVR and 100% of the general partner of PVR, which holds a 2% general partner interest in PVR and all of the incentive distribution rights, or IDRs. During 2009, we sold a portion of our limited partner interest in PVG in a public offering, reducing our limited partner interest in PVG from 77% to 51.4%. See “— Corporate Structure.”

PVG consolidates PVR’s results into its financial statements because PVG controls PVR’s general partner. We consolidate PVG’s results into our financial statements because we control PVG’s general partner. PVG and PVR function with capital structures that are independent of each other and us. While we report consolidated financial results of PVR’s coal and natural resource management and natural gas midstream businesses, the only cash we received from those businesses is in the form of cash distributions we received from PVG and PVR in respect of our partner interests in each of them. We received cash distributions of $42.3 million, $44.0 million and $29.8 million in the years ended December 31, 2009, 2008 and 2007 as a result of our partner interests in PVG and PVR.

Unless the context requires otherwise, references to the “Company,” “Penn Virginia,” “we,” “us” or “our” in this Annual Report on Form 10-K refer to Penn Virginia Corporation and its subsidiaries.

Segments

We are engaged in three primary business segments: (i) oil and gas, (ii) coal and natural resource management and (iii) natural gas midstream. We operate our oil and gas segment, and PVR operates the coal and natural resource management and natural gas midstream segments.

Oil and Gas Segment Overview

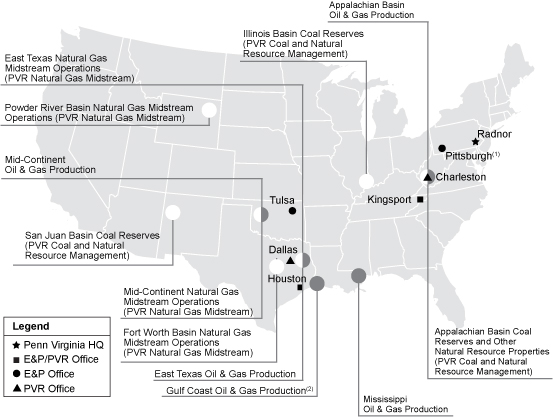

We have a geographically diverse asset base with core areas of operation in the East Texas, Mid-Continent, Appalachian and Mississippi regions of the United States. As of December 31, 2009, we had proved natural gas and oil reserves of approximately 935 Bcfe, of which 83% were natural gas and 47% were proved developed. Our operations include both conventional and unconventional developmental drilling opportunities, as well as some exploratory prospects.

As of December 31, 2009, 97% of our proved reserves were located in primarily longer-lived, lower-risk basins in East Texas, the Mid-Continent, Appalachia and Mississippi, which comprised 43%, 21%, 14% and 19%, respectively, of the proved reserves. We sold our Gulf Coast properties, representing 3% of proved reserves, in a transaction that closed on January 29, 2010. In 2009, we produced 51.0 Bcfe, a 9% increase compared to 46.9 Bcfe in 2008, with East Texas, the Mid-Continent, Appalachia, Mississippi and the Gulf Coast comprising 26%, 25%, 23%, 15% and 11% of total production volumes. In the three years ended December 31, 2009, we drilled 607 gross (413.3 net) wells, of which 93% were successful in producing natural gas in commercial quantities. For a more detailed discussion of our reserves and production, see Item 2, “Properties.”

The primary development play types that our oil and gas operations are focused on include: (i) the horizontal Lower Bossier (Haynesville) Shale and Cotton Valley plays in East Texas, (ii) the horizontal Granite Wash play in the Mid-Continent and (iii) the predominantly horizontal Selma Chalk play in Mississippi. In addition, we intend to focus on drilling exploratory wells in the Marcellus Shale play in Appalachia in order to determine whether our leasehold acreage position there will support a development program.

1

TABLE OF CONTENTS

We have grown our reserves and production primarily through development and exploratory drilling, complemented to a lesser extent by making strategic acquisitions. Despite a challenging year in 2009, we replaced approximately 147% of our 2009 production entirely through the drillbit by adding approximately 75 Bcfe of proved reserves from extensions, discoveries and additions, net of revisions. In 2009, capital expenditures in our oil and gas segment were $171.8 million, of which $140.2 million, or 82%, was related to development drilling and $18.7 million, or 11%, was related to leasehold acquisitions. The remaining $12.9 million, or 7%, was related to exploration drilling, pipelines, gathering and facilities.

As of December 31, 2009, we owned 1.1 million net acres of leasehold interests, approximately 34% of which were undeveloped. Many of our proved undeveloped locations and additional potential drilling locations are direct offsets or extensions from existing production. We believe our existing undeveloped acreage position represents over 10 years of drilling opportunities based on our historical drilling rate.

PVR Coal and Natural Resource Management Segment Overview

The PVR coal and natural resource management segment primarily involves the management and leasing of coal properties and the subsequent collection of royalties. PVR also earns revenues from other land management activities, such as selling standing timber, leasing fee-based coal-related infrastructure facilities to certain lessees and end-user industrial plants, collecting oil and gas royalties and from coal transportation, or wheelage, fees.

As of December 31, 2009, PVR owned or controlled approximately 829 million tons of proven and probable coal reserves in Central and Northern Appalachia, the San Juan Basin and the Illinois Basin. PVR enters into long-term leases with experienced, third-party mine operators, providing them the right to mine PVR’s coal reserves in exchange for royalty payments. PVR actively works with its lessees to develop efficient methods to exploit its reserves and to maximize production from PVR’s properties. PVR does not operate any mines. In 2009, PVR’s lessees produced 34.3 million tons of coal from its properties and paid PVR coal royalties revenues of $120.4 million, for an average royalty per ton of $3.51. Approximately 82% of PVR’s coal royalties revenues in 2009 were derived from coal mined on PVR’s properties under leases containing royalty rates based on the higher of a fixed base price or a percentage of the gross sales price. The balance of PVR’s coal royalties revenues for the respective periods was derived from coal mined on PVR’s properties under leases containing fixed royalty rates that escalate annually. See “— Contracts — PVR Coal and Natural Resource Management Segment” for a description of PVR’s coal leases.

PVR Natural Gas Midstream Segment Overview

PVR’s natural gas midstream segment is engaged in providing natural gas processing, gathering and other related services. As of December 31, 2009, PVR owned and operated natural gas midstream assets located in Oklahoma and Texas, including six natural gas processing facilities having 400 MMcfd of total capacity and approximately 4,118 miles of natural gas gathering pipelines. PVR’s natural gas midstream business earns revenues primarily from gas processing contracts with natural gas producers and from fees charged for gathering natural gas volumes and providing other related services. In addition, PVR owns a 25% member interest in Thunder Creek Gas Services, LLC, or Thunder Creek, a joint venture that gathers and transports CBM in Wyoming’s Powder River Basin. PVR also owns a natural gas marketing business, which aggregates third-party volumes and sells those volumes into intrastate pipeline systems and at market hubs accessed by various interstate pipelines.

In 2009, system throughput volumes at PVR’s gas processing plants and gathering systems, including gathering-only volumes, were 121.3 Bcf, or approximately 332 MMcfd.

Business Strategy

We intend to pursue the following business strategies:

| • | Grow primarily through development drilling. We anticipate spending up to $425 million on oil and gas capital expenditures in 2010. We plan to allocate up to $275 million, or approximately 65%, of this amount to development drilling and related projects in our core areas of East Texas, the Mid-Continent and Mississippi. We are applying horizontal drilling technology in each of the core areas which may result in increased reserve additions, higher production rates and increased rates of return. |

2

TABLE OF CONTENTS

| • | Useexploratory drilling to provide operational balance and future development growth opportunities. We anticipate allocating up to $45 million, or approximately 11%, of our 2010 oil and gas capital expenditures to our exploratory drilling activities, including new prospects in the Granite Wash play in the Mid-Continent and the Marcellus Shale play in Pennsylvania. Both regions have prolific reserve and production growth potential. |

| • | Pursue selective leasehold and producing property acquisition opportunities in existing basins. Historically, the majority of our growth in proved reserves and production has been achieved by drilling wells, or “through the drillbit.” Our experienced team of management and technical professionals looks for opportunities to extend our leasehold acreage holdings, especially in our core areas and in the Marcellus Shale play in Pennsylvania. We anticipate allocating up to $85 million, or approximately 20%, of our 2010 oil and gas capital expenditures to leasehold acquisitions. While we do not presently anticipate producing property acquisitions in our 2010 oil and gas capital expenditures, we may consider making these types of acquisitions in our core and target areas as opportunities arise. |

| • | Manage risk exposure through an active hedging program. We actively manage our exposure to commodity price fluctuations by hedging the commodity price risk for our expected production through the use of derivatives, typically costless collar contracts. The level of our hedging activity and duration of the instruments employed depend upon our cash flow at risk, available hedge prices and our operating strategy. For 2010, we have hedged approximately 55% of our estimated natural gas production, at average floor and ceiling prices of $6.09 and $8.19 per MMBtu, respectively. |

| • | Manage cash liquidity and balance sheet debt levels. In response to difficult conditions in the financial and commodity markets during 2009, we significantly reduced oil and gas capital spending levels from 2008, while taking steps to improve our balance sheet and cash liquidity by raising $65 million of new equity capital and completing a $300 million initial public debt offering. We also improved our cash liquidity position by selling non-core assets during 2009, including the sale of a portion of our holdings in PVG for net proceeds of $118.1 million, excluding transaction costs, as well as certain oil and gas assets. We expect to continue to use debt financing, supplemented with equity issuances and the sale of other non-core assets potentially including all or part of our interests in PVG, to fund our growth profile while maintaining a conservative capital structure. |

Contracts

Oil and Gas Segment

Transportation. We have entered into contracts which provide firm transportation capacity rights for specified volumes per day on a pipeline system for terms ranging from one to 15 years. The contracts require us to pay transportation demand charges regardless of the amount of pipeline capacity we use. We may sell excess capacity to third parties at our discretion.

Marketing. We generally sell our natural gas using spot market and short-term fixed price physical contracts. For the year ended December 31, 2009, approximately 13% and 12% of our oil and gas segment revenues and 4% and 3% of our total consolidated revenues resulted from two of our oil and gas customers, Dominion Field Services, Inc. and Chesapeake Operating, Inc.

PVR Coal and Natural Resource Management Segment

PVR earns most of its coal royalties revenues under long-term leases that generally require its lessees to make royalty payments to it based on the higher of a percentage of the gross sales price or a fixed price per ton of coal they sell. The balance of PVR’s coal royalties revenues is earned under long-term leases that require the lessees to make royalty payments to PVR based on fixed royalty rates that escalate annually. A typical lease either expires upon exhaustion of the leased reserves or has a five to ten-year base term, with the lessee having an option to extend the lease for at least five years after the expiration of the base term. Substantially all of PVR’s leases require the lessee to pay minimum rental payments to PVR in monthly or annual installments, even if no mining activities are ongoing. These minimum rentals are recoupable, usually over a period from one to three years from the time of payment, against the production royalties owed to PVR once coal production commences.

3

TABLE OF CONTENTS

Substantially all of PVR’s leases impose obligations on the lessees to diligently mine the leased coal using modern mining techniques, indemnify PVR for any damages it incurs in connection with the lessee’s mining operations, including any damages PVR may incur due to the lessee’s failure to fulfill reclamation or other environmental obligations, conduct mining operations in compliance with all applicable laws, obtain its written consent prior to assigning the lease and maintain commercially reasonable amounts of general liability and other insurance. Substantially all of the leases grant PVR the right to review all lessee mining plans and maps, enter the leased premises to examine mine workings and conduct audits of lessees’ compliance with lease terms. In the event of a default by a lessee, substantially all of the leases give PVR the right to terminate the lease and take possession of the leased premises.

In addition, PVR earns revenues under coal services contracts, timber contracts and oil and gas leases. PVR’s coal services contracts generally provide that the users of PVR’s coal services pay PVR a fixed fee per ton of coal processed at its facilities. All of PVR’s coal services contracts are with lessees of PVR’s coal reserves and these contracts generally have terms that run concurrently with the related coal lease. PVR’s timber contracts generally provide that the timber companies pay PVR a fixed price per thousand board feet of timber harvested from PVR’s property. PVR receives royalties under its oil and gas leases based on a percentage of the revenues the producers receive for the oil and gas they sell.

PVR Natural Gas Midstream Segment

PVR’s natural gas midstream business generates revenues primarily from gas purchase and processing contracts with natural gas producers and from fees charged for gathering natural gas volumes and providing other related services. During the year ended December 31, 2009, PVR’s natural gas midstream business generated a majority of its gross margin from two types of contractual arrangements under which its margin is exposed to increases and decreases in the price of natural gas and NGLs: (i) gas purchase/keep-whole and (ii) percentage-of-proceeds. For the fourth quarter of 2009, approximately 28% of PVR’s system throughput volumes were gathered or processed under gas purchase/keep-whole contracts, 53% were gathered or processed under percentage-of-proceeds contracts and 19% were gathered or processed under fee-based gathering contracts. A majority of the gas purchase/keep-whole and percentage-of-proceeds contracts include fee-based components such as gathering and compression charges.

In 2009, 21% of the PVR natural gas midstream segment’s revenues and 13% of our total consolidated revenues resulted from one of PVR’s natural gas midstream customers, Conoco, Inc.

Gas Purchase/Keep-Whole Arrangements. Under gas purchase/keep-whole arrangements, PVR generally purchases natural gas at the wellhead at either (i) a percentage discount to a specified index price, (ii) a specified index price less a fixed amount or (iii) a combination of (i) and (ii). PVR then gathers the natural gas to one of its plants where it is processed to extract the entrained NGLs, which are then sold to third parties at market prices. PVR resells the remaining natural gas to third parties at an index price which typically corresponds to the specified purchase index. Because the extraction of the NGLs from the natural gas during processing reduces the BTU content of the natural gas, PVR retains a reduced volume of gas to sell after processing. Accordingly, under these arrangements, PVR’s revenues and gross margins increase as the price of NGLs increases relative to the price of natural gas, and its revenues and gross margins decrease as the price of natural gas increases relative to the price of NGLs. PVR has generally been able to mitigate its exposure in the latter case by requiring the payment under many of its gas purchase/keep-whole arrangements of minimum processing charges which ensure that PVR receives a minimum amount of processing revenues. The gross margins that PVR realizes under the arrangements described in clauses (i) and (iii) above also decrease in periods of low natural gas prices because these gross margins are based on a percentage of the index price.

Percentage-of-Proceeds Arrangements. Under percentage-of-proceeds arrangements, PVR generally gathers and processes natural gas on behalf of producers, sells the resulting residue gas and NGL volumes at market prices and remits to producers an agreed-upon percentage of the proceeds of those sales based on either an index price or the price actually received for the gas and NGLs. Under these types of arrangements, PVR’s revenues and gross margins increase as natural gas prices and NGL prices increase, and its revenues and gross margins decrease as natural gas prices and NGL prices decrease.

4

TABLE OF CONTENTS

Fee-Based Arrangements. Under fee-based arrangements, PVR receives fees for gathering, compressing and/or processing natural gas. The revenues PVR earns from these arrangements are directly dependent on the volume of natural gas that flows through its systems and are independent of commodity prices. To the extent a sustained decline in commodity prices results in a decline in volumes, however, PVR’s revenues from these arrangements would be reduced due to the related reduction in drilling and development of new supply.

In many cases, PVR provides services under contracts that contain a combination of more than one of the arrangements described above. The terms of PVR’s contracts vary based on gas quality conditions, the competitive environment at the time the contracts were signed and customer requirements. The contract mix and, accordingly, exposure to natural gas and NGL prices, may change as a result of changes in producer preferences, expansion in regions where some types of contracts are more common and other market factors.

Natural Gas Marketing Contracts. PVR is also engaged in natural gas marketing by aggregating third-party volumes and selling those volumes into interstate and intrastate pipeline systems such as Enogex and Panhandle Eastern Pipeline and at market hubs accessed by various interstate pipelines. Connect Energy Services, LLC, or Connect Energy, PVR’s wholly owned subsidiary, has earned fees from Penn Virginia Oil & Gas, L.P., or PVOG LP, our wholly owned subsidiary, since September 1, 2006, for marketing a portion of PVOG LP’s natural gas production. For the years ended December 31, 2009 and 2008, PVR’s natural gas marketing activities generated $1.8 million and $5.8 million in net revenues. Fees paid to the PVR natural gas midstream segment by our oil and gas segment are eliminated in consolidation.

Commodity Derivative Contracts

Oil and Gas Segment Commodity Derivatives. We utilize three-way collar derivative contracts to hedge against the variability in cash flows associated with anticipated sales of our future oil and gas production. While the use of derivative instruments limits the risk of adverse price movements, such use may also limit future revenues from favorable price movements.

A three-way collar contract consists of a collar contract plus a put option contract sold by us with a price below the floor price of the collar. The counterparty to a collar contract is required to make a payment to us if the settlement price for any settlement period is below the floor price for such contract. We are required to make a payment to the counterparty if the settlement price for any settlement period is above the ceiling price for such contract. Neither party is required to make a payment to the other party if the settlement price for any settlement period is equal to or greater than the floor price and equal to or less than the ceiling price for such contract.

The additional put option sold by us requires us to make a payment to the counterparty if the settlement price for any settlement period is below the put option price. By combining the collar contract with the additional put option, we are entitled to a net payment equal to the difference between the floor price of the collar contract and the additional put option price if the settlement price is equal to or less than the additional put option price. If the settlement price is greater than the additional put option price, the result is the same as it would have been with a collar contract only. If market prices are below the additional put option, we would be entitled to receive the market price plus the difference between the additional put option and the floor. See the oil and gas segment commodity derivative table in Item 7A, “Quantitative and Qualitative Disclosures About Market Risk — Price Risk.” This strategy enables us to increase the floor and the ceiling prices of the collar beyond the range of a traditional collar contract while defraying the associated cost with the sale of the additional put option.

We determine the fair values of our oil and gas derivative agreements based on discounted cash flows derived from third-party quoted forward prices for NYMEX Henry Hub gas and West Texas Intermediate crude oil closing prices as of December 31, 2009. The discounted cash flows utilize discount rates adjusted for the credit risk of our counterparties if the derivative is in an asset position and our own credit risk if the derivative is in a liability position.

PVR Natural Gas Midstream Segment Commodity Derivatives. PVR utilizes collar derivative contracts to hedge against the variability in its frac spread. PVR’s frac spread is the spread between the purchase price for the natural gas PVR purchases from producers and the sale price for NGLs that PVR sells after processing. PVR hedges against the variability in its frac spread by entering into costless collar and swap

5

TABLE OF CONTENTS

derivative contracts to sell NGLs forward at a predetermined commodity price and to purchase an equivalent volume of natural gas forward on an MMBtu basis. While the use of derivative instruments limits the risk of adverse price movements, such use may also limit future revenues or cost savings from favorable price movements.

See Note 8 to the Consolidated Financial Statements for a further description of our and PVR’s derivatives programs.

Corporate Structure

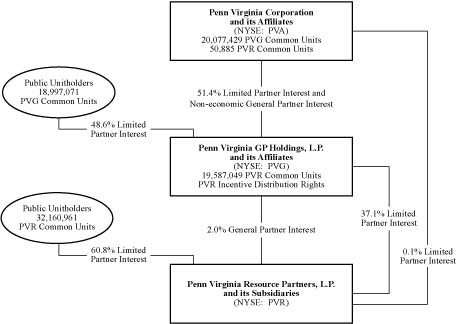

We are a Virginia corporation formed in 1882. As of December 31, 2009, we owned the general partner of PVG and an approximately 51.4% limited partner interest in PVG. PVG owns an approximately 37% limited partner interest in PVR and the general partner of PVR, which holds a 2% general partner interest in PVR and all of the IDRs. We directly owned an additional 0.1% limited partner interest in PVR as of December 31, 2009. The following diagram depicts our ownership of PVG and PVR as of December 31, 2009:

Because PVG controls the general partner of PVR, the financial results of PVR are included in PVG’s consolidated financial statements. Because we control the general partner of PVG, the financial results of PVG are included in our consolidated financial statements. However, PVG and PVR function with capital structures that are independent of each other and us, with each having publicly traded common units and PVR having its own debt instruments. PVG does not currently have any debt instruments. While we report consolidated financial results of PVR’s coal and natural resource management and natural gas midstream businesses, the only cash we receive from those businesses is in the form of cash distributions we receive from PVG and PVR in respect of our partner interests in each of them.

PVG and PVR Distributions

PVG Cash Distributions

PVG paid cash distributions of $1.52 per common unit during the year ended December 31, 2009. In the first quarter of 2010, PVG paid a cash distribution of $0.38 ($1.52 on an annualized basis) per common unit with respect to the fourth quarter of 2009. This distribution was unchanged from the previous distribution paid on November 18, 2009. For the remainder of 2010, PVG expects to pay quarterly cash distributions of at least $0.38 ($1.52 on an annualized basis) per common unit.

6

TABLE OF CONTENTS

PVR Cash Distributions

PVR paid cash distributions of $1.88 per common unit during the year ended December 31, 2009. In the first quarter of 2010, PVR paid a cash distribution of $0.47 ($1.88 on an annualized basis) per common unit with respect to the fourth quarter of 2009. This distribution was unchanged from the previous distribution paid on November 13, 2009. For the remainder of 2010, PVR expects to pay quarterly cash distributions of at least $0.47 ($1.88 on an annualized basis) per common unit.

PVR IDRs

In accordance with PVR’s partnership agreement, IDRs represent the right to receive an increasing percentage of quarterly distributions of PVR’s available cash from operating surplus after the minimum quarterly distribution and the target distribution levels have been achieved. The minimum quarterly distribution is $0.25 ($1.00 on an annualized basis) per unit. PVR’s general partner currently holds 100% of the IDRs, but may transfer these rights separately from its general partner interest to an affiliate (other than an individual) or to another entity as part of the merger or consolidation of PVR’s general partner with or into such entity or the transfer of all or substantially all of PVR’s general partner’s assets to another entity without the prior approval of PVR’s unitholders if the transferee agrees to be bound by the provisions of PVR’s partnership agreement. Prior to September 30, 2011, other transfers of the IDRs will require the affirmative vote of holders of a majority of the outstanding PVR common units. On or after September 30, 2011, the IDRs will be freely transferable. The IDRs are payable as follows:

If for any quarter:

| • | PVR has distributed available cash from operating surplus to its common unitholders in an amount equal to the minimum quarterly distribution; and |

| • | PVR has distributed available cash from operating surplus on outstanding common units in an amount necessary to eliminate any cumulative arrearages in payment of the minimum quarterly distribution; |

then, PVR will distribute any additional available cash from operating surplus for that quarter among the unitholders and its general partner in the following manner:

| • | First, 98% to all unitholders, and 2% to PVR’s general partner, until each unitholder has received a total of $0.275 per unit for that quarter; |

| • | Second, 85% to all unitholders, and 15% to PVR’s general partner, until each unitholder has received a total of $0.325 per unit for that quarter; |

| • | Third, 75% to all unitholders, and 25% to PVR’s general partner, until each unitholder has received a total of $0.375 per unit for that quarter; and |

| • | Thereafter, 50% to all unitholders and 50% to PVR’s general partner. |

Since 2001, PVR has increased its quarterly cash distribution from $0.25 ($1.00 on an annualized basis) per unit to $0.47 ($1.88 on an annualized basis) per unit, which is its most recently declared distribution. These increased cash distributions by PVR have placed PVG, as the owner of PVR’s general partner, at the maximum target cash distribution level as described above and, as a consequence, since reaching such level, PVG, as the owner of PVR’s general partner, has received 50% of available cash in excess of $0.375 per unit.

7

TABLE OF CONTENTS

Cash Distributions Received

We are currently entitled to receive quarterly cash distributions from PVG and PVR on our limited partner interests in PVG and PVR. As a result of our partner interests in PVG and PVR, we received the following total cash distributions for the periods presented. The reduction in cash distributions we received from 2008 to 2009 was the result of our sale of a portion of our interest in PVG during 2009.

| | | | | | |

| | Year Ended December 31, |

| | | 2009 | | 2008 | | 2007 |

| Penn Virginia GP Holdings, L.P. | | $ | 41,916 | | | $ | 43,435 | | | $ | 29,200 | |

| Penn Virginia Resource Partners, L.P.(1) | | | 363 | | | | 583 | | | | 640 | |

| | | $ | 42,279 | | | $ | 44,018 | | | $ | 29,840 | |

| (1) | Includes PVR distributions for restricted units held by employees and directors. |

Competition

Oil and Gas Segment

The oil and natural gas industry is very competitive, and we compete with a substantial number of other companies that are large, well-established and have greater financial and operational resources than we do, which may adversely affect our ability to compete or grow our business. Many such companies not only engage in the acquisition, exploration, development and production of oil and natural gas reserves, but also carry on refining operations, electricity generation and the marketing of refined products. Competition is particularly intense in the acquisition of prospective oil and natural gas properties and oil and gas reserves. Our competitive position depends on our geological, geophysical and engineering expertise, our financial resources, our ability to develop properties and our ability to select, acquire and develop proved reserves. We compete with other oil and natural gas companies to secure drilling rigs and other equipment necessary for the drilling and completion of wells and recruiting and retaining qualified personnel, including geologists, geo-physicists, engineers and other specialists. Such equipment and labor may be in short supply from time to time. Shortages of equipment, labor or materials may result in increased costs or the inability to obtain such resources as needed. We also compete with substantially larger and independent oil and gas companies in the marketing and sale of oil and natural gas, and the oil and natural gas industry in general competes with other industries supplying energy and fuel to industrial, commercial and individual consumers.

PVR Coal and Natural Resource Management Segment

The coal industry is intensely competitive primarily as a result of the existence of numerous producers. PVR’s lessees compete with both large and small coal producers in various regions of the United States for domestic sales. The industry has undergone significant consolidation which has led to some of the competitors of PVR’s lessees having significantly larger financial and operating resources than most of PVR’s lessees. PVR’s lessees compete on the basis of coal price at the mine, coal quality (including sulfur content), transportation cost from the mine to the customer and the reliability of supply. Continued demand for PVR’s coal and the prices that PVR’s lessees obtain are also affected by demand for electricity, demand for metallurgical coal, access to transportation, environmental and government regulations, technological developments and the availability and price of alternative fuel supplies, including nuclear, natural gas, oil and hydroelectric power. Demand for PVR’s low sulfur coal and the prices PVR’s lessees will be able to obtain for it will also be affected by the price and availability of high sulfur coal, which can be marketed in tandem with emissions allowances which permit the high sulfur coal to meet federal Clean Air Act, or CAA, requirements.

PVR Natural Gas Midstream Segment

PVR experiences competition in all of its natural gas midstream markets. PVR’s competitors include major integrated oil companies, interstate and intrastate pipelines and companies that gather, compress, process, transport and market natural gas. Many of PVR’s competitors have greater financial resources and access to larger natural gas supplies than PVR does.

8

TABLE OF CONTENTS

The ability to offer natural gas producers competitive gathering and processing arrangements and subsequent reliable service is fundamental to obtaining and keeping gas supplies for PVR’s gathering systems. The primary concerns of the producer are:

| • | the pressure maintained on the system at the point of receipt; |

| • | the relative volumes of gas consumed as fuel and lost; |

| • | the gathering/processing fees charged; |

| • | the timeliness of well connects; |

| • | the customer service orientation of the gatherer/processor; and |

| • | the reliability of the field services provided. |

Government Regulation and Environmental Matters

The operations of our oil and gas business and PVR’s coal and natural resource management and natural gas midstream businesses are subject to environmental laws and regulations adopted by various governmental authorities in the jurisdictions in which these operations are conducted.

Oil and Gas Segment

State Regulatory Matters. Various aspects of our oil and natural gas operations are regulated by administrative agencies under statutory provisions of the states where such operations are conducted. All of the jurisdictions in which we own or operate producing crude oil and natural gas properties have statutory provisions regulating the exploration for and production of crude oil and natural gas. These provisions include permitting regulations regarding the drilling of wells, maintaining bonding requirements to drill or operate wells, locating wells, the method of drilling and casing wells, the surface use and restoration of properties upon which wells are drilled and the plugging and abandoning of wells. Our operations are also subject to various conservation laws and regulations. These include the regulation of the size of drilling and spacing units or proration units, the number of wells that may be drilled in an area and the unitization or pooling of crude oil and natural gas properties. In addition, state conservation laws establish maximum rates of production from crude oil and natural gas wells, generally prohibit the venting or flaring of natural gas and impose certain requirements regarding the ratability or fair apportionment of production from fields and individual wells. The effect of these regulations is to limit the amounts of crude oil and natural gas we can produce from our wells and to limit the number of wells or the locations at which we can drill.

Federal Energy Regulatory Commission. The Federal Energy Regulatory Commission, or the FERC, regulates the transportation and sale for resale of natural gas in interstate commerce under the Natural Gas Act of 1938, or the NGA, and the Natural Gas Policy Act of 1978, or the NGPA. In the past, the federal government has regulated the prices at which oil and gas could be sold. The Natural Gas Wellhead Decontrol Act of 1989 removed all NGA and NGPA price and nonprice controls affecting producers’ wellhead sales of natural gas effective January 1, 1993. While sales by producers of their own natural gas production and all sales of crude oil, condensate and NGLs can currently be made at market prices, Congress could reenact price controls in the future.

Commencing in April 1992, the FERC issued Order Nos. 636, 636-A, 636-B and 636-C, or Order No. 636, which require interstate pipelines to provide transportation separate, or “unbundled,” from the pipelines’ sale of gas. Also, Order No. 636 requires pipelines to provide open-access transportation on a basis that is equal for all gas supplies. Although Order No. 636 does not directly regulate gas producers like us, the FERC has stated that it intends for Order No. 636 to foster increased competition within all phases of the natural gas industry. The courts have largely affirmed the significant features of Order No. 636 and numerous related orders pertaining to the individual pipelines, although certain appeals remain pending and the FERC continues to review and modify its open access regulations. In particular, the FERC has issued Order Nos. 637, 637-A and 637-B which, among other things, (i) permit pipelines to charge different maximum cost-based rates for peak and off-peak periods, (ii) encourage auctions for pipeline capacity, (iii) require pipelines to implement imbalance management services and (iv) restrict the ability of pipelines to impose penalties for imbalances, overruns and non-compliance with operational flow orders.

9

TABLE OF CONTENTS

The Energy Policy Act of 2005 amended the NGA and the NGPA and gave the FERC the authority to assess civil penalties of up to $1 million per day per violation for violations of rules, regulations and orders issued under these acts. In addition, the FERC has issued regulations that make it unlawful for any entity in connection with the purchase or sale of natural gas or the purchase or sale of transportation services subject to the jurisdiction of the FERC to use any manipulative or deceptive device or contrivance.

While any additional FERC action on these matters would affect us only indirectly, these changes are intended to further enhance competition in, and prevent manipulation of, natural gas markets. We cannot predict what further action the FERC will take on these matters, nor can we predict whether the FERC’s actions will achieve its stated goal of increasing competition in, and preventing manipulation of, natural gas markets. However, we do not believe that we will be treated materially differently than other natural gas producers with which we compete.

Environmental Matters. Extensive federal, state and local laws govern oil and natural gas operations, regulate the discharge of materials into the environment or otherwise relate to the protection of the environment. Numerous governmental departments issue rules and regulations to implement and enforce such laws that are often difficult and costly to comply with and which carry substantial administrative, civil and even criminal penalties for failure to comply. Some laws, rules and regulations relating to protection of the environment may, in certain circumstances, impose “strict liability” for environmental contamination, rendering a person liable for environmental and natural resource damages and cleanup costs without regard to negligence or fault on the part of such person. Other laws, rules and regulations may restrict the rate of oil and natural gas production below the rate that would otherwise exist or even prohibit exploration or production activities in sensitive areas. In addition, state laws often require some form of remedial action to prevent pollution from former operations, such as closure of inactive pits and plugging of abandoned wells. The regulatory burden on the oil and natural gas industry increases its cost of doing business and consequently affects its profitability. These laws, rules and regulations affect our operations, as well as the oil and gas exploration and production industry in general. We believe that we are in substantial compliance with current applicable environmental laws, rules and regulations and that continued compliance with existing requirements will not have a material adverse impact on us. Nevertheless, changes in existing environmental laws or the adoption of new environmental laws have the potential to adversely affect our operations.

As part of the 2008 Consolidated Appropriations Act, the EPA was required to issue a rule requiring mandatory reporting of greenhouse gas emissions above certain thresholds from all sectors of the U.S. economy. The proposed rule included greenhouse gas reporting requirements for oil and natural gas systems (“Subpart W”), including production and distribution facilities, but the EPA received extensive comments to Subpart W relating to the reporting of fugitive and vented emissions from the oil and gas sector. As a result, Subpart W was not included in the final rule. While the EPA may re-issue a proposed rule regarding the reporting of greenhouse gas emissions from oil and natural gas systems, we do not believe that any such future requirement will have a material adverse affect on our business, financial position or results of operations.

OSHA. We are subject to the requirements of the Occupational Safety and Health Act, or OSHA, and comparable state laws that regulate the protection of the health and safety of workers. In addition, the OSHA hazard communication standard requires that information be maintained about hazardous materials used or produced in our operations and that this information be provided to employees, state and local government authorities and citizens.

PVR Coal and Natural Resource Management Segment

General Regulation Applicable to Coal Lessees. PVR’s lessees are obligated to conduct mining operations in compliance with all applicable federal, state and local laws and regulations. These laws and regulations include matters involving the discharge of materials into the environment, employee health and safety, mine permits and other licensing requirements, reclamation and restoration of mining properties after mining is completed, management of materials generated by mining operations, surface subsidence from underground mining, water pollution, legislatively mandated benefits for current and retired coal miners, air quality standards, protection of wetlands, plant and wildlife protection, limitations on land use, storage of petroleum products and substances which are regarded as hazardous under applicable laws and management of

10

TABLE OF CONTENTS

electrical equipment containing polychlorinated biphenyls, or PCBs. These extensive and comprehensive regulatory requirements are closely enforced, PVR’s lessees regularly have on-site inspections and violations during mining operations are not unusual in the industry, notwithstanding compliance efforts by PVR’s lessees. However, none of the violations to date, or the monetary penalties assessed, have been material to us, PVR or, to our knowledge, to PVR’s lessees. Although many new safety requirements have been instituted recently, PVR does not currently expect that future compliance will have a material adverse effect on PVR.

While it is not possible to quantify the costs of compliance by PVR’s lessees with all applicable federal, state and local laws and regulations, those costs have been and are expected to continue to be significant. The lessees post performance bonds pursuant to federal and state mining laws and regulations for the estimated costs of reclamation and mine closing, including the cost of treating mine water discharge when necessary. We do not accrue for such costs because PVR’s lessees are contractually liable for all costs relating to their mining operations, including the costs of reclamation and mine closure. However, PVR does require some smaller lessees to deposit into escrow certain funds for reclamation and mine closure costs or post performance bonds for these costs. Although we believe that the lessees typically accrue adequate amounts for these costs, their future operating results would be adversely affected if they later determined these accruals to be insufficient. Compliance with these laws and regulations has substantially increased the cost of coal mining for all domestic coal producers.

In addition, the utility industry, which is the most significant end-user of coal, is subject to extensive regulation regarding the environmental impact of its power generation activities which could affect demand for coal mined by PVR’s lessees. The possibility exists that new legislation or regulations may be adopted which have a significant impact on the mining operations of PVR’s lessees or their customers’ ability to use coal and may require PVR, its lessees or their customers to change operations significantly or incur substantial costs.

Air Emissions. The CAA and corresponding state and local laws and regulations affect all aspects of PVR’s business, both directly and indirectly. The CAA directly impacts PVR’s lessees’ coal mining and processing operations by imposing permitting requirements and, in some cases, requirements to install certain emissions control equipment, on sources that emit various hazardous and non-hazardous air pollutants. The CAA also indirectly affects coal mining operations by extensively regulating the air emissions of coal-fired electric power generating plants. There have been a series of recent federal rulemakings that are focused on emissions from coal-fired electric generating facilities. Installation of additional emissions control technology and additional measures required under Environmental Protection Agency, or EPA, laws and regulations will make it more costly to build and operate coal-fired power plants and, depending on the requirements of individual state implementation plans, could make coal a less attractive fuel alternative in the planning and building of power plants in the future. Any reduction in coal’s share of power generating capacity could negatively impact PVR’s lessees’ ability to sell coal, which could have a material effect on PVR’s coal royalties revenues.

The EPA’s Acid Rain Program, provided in Title IV of the CAA, regulates emissions of sulfur dioxide from electric generating facilities. Sulfur dioxide is a by-product of coal combustion. Affected facilities purchase or are otherwise allocated sulfur dioxide emissions allowances, which must be surrendered annually in an amount equal to a facility’s sulfur dioxide emissions in that year. Affected facilities may sell or trade excess allowances to other facilities that require additional allowances to offset their sulfur dioxide emissions. In addition to purchasing or trading for additional sulfur dioxide allowances, affected power facilities can satisfy the requirements of the EPA’s Acid Rain Program by switching to lower sulfur fuels, installing pollution control devices such as flue gas desulfurization systems, or “scrubbers,” or by reducing electricity generating levels.

The EPA has promulgated rules, referred to as the “NOx SIP Call,” that require coal-fired power plants and other large stationary sources in 21 eastern states and Washington D.C. to make substantial reductions in nitrogen oxide emissions in an effort to reduce the impacts of ozone transport between states. Additionally, in March 2005, the EPA issued the final Clean Air Interstate Rule, or CAIR, which would have permanently capped nitrogen oxide and sulfur dioxide emissions in 28 eastern states and Washington, D.C. beginning in 2009 and 2010. CAIR required those states to achieve the required emission reductions by requiring power plants to either participate in an EPA-administered “cap-and-trade” program that caps emission in two phases,

11

TABLE OF CONTENTS

or by meeting an individual state emissions budget through measures established by the state. The stringency of the caps under CAIR may have required many coal-fired sources to install additional pollution control equipment, such as wet scrubbers, to comply. This increased sulfur emission removal capability required by CAIR could have resulted in decreased demand for lower sulfur coal, which may have potentially driven down prices for lower sulfur coal. On July 11, 2008, the D.C. Circuit Court of Appeals vacated CAIR in its entirety. The EPA subsequently filed a petition for rehearing or, in the alternative, for a remand of the case without vacatur. On December 23, 2008, the Court issued an opinion to remand without vacating CAIR. Therefore, CAIR will remain in effect while the EPA conducts rulemaking to modify CAIR to comply with the Court’s July 2008 opinion. The Court declined to impose a schedule by which the EPA must complete the rulemaking, but reminded the EPA that the Court does “.not intend to grant an indefinite stay of the effectiveness of this Court’s decision.” The EPA is considering its options on how to proceed.

In March 2005, the EPA finalized the Clean Air Mercury Rule, or CAMR, which was to establish a two-part, nationwide cap on mercury emissions from coal-fired power plants beginning in 2010. It was the subject of extensive controversy and litigation and, in February 2008, the U.S. Circuit Court of Appeals for the District of Columbia vacated CAMR. The EPA appealed the decision to the U.S. Supreme Court in October 2008, but withdrew its petition for certiorari on February 6, 2009. However, a utility group continues to seek certiorari, challenging the court of appeals decision to overturn CAMR. In the meantime, the EPA plans to develop standards consistent with the court of appeal’s ruling, intending to propose air toxics standards for coal- and oil-fired electric generating units by March 10, 2011, and finalize a rule by November 16, 2011. In conjunction with these efforts, on December 24, 2009, the EPA approved an Information Collection Request (ICR) requiring all U.S. power plants with coal-or oil-fired electric generating units to submit emissions information for use in developing air toxics emissions standards. In addition, various states have promulgated or are considering more stringent emission limits on mercury emissions from coal-fired electric generating units.

The EPA has adopted new, more stringent national air quality standards for ozone and fine particulate matter. As a result, some states will be required to amend their existing state implementation plans to attain and maintain compliance with the new air quality standards. In March 2007, the EPA published final rules addressing how states would implement plans to bring regions designated as non-attainment for fine particulate matter into compliance with the new air quality standard. Under the EPA’s final rule, states had until April 2008 to submit their implementation plans to the EPA for approval. Because coal mining operations and coal-fired electric generating facilities emit particulate matter, PVR’s lessees’ mining operations and their customers could be affected when the new standards are implemented by the applicable states.

Likewise, the EPA’s regional haze program to improve visibility in national parks and wilderness areas required affected states to develop implementation plans by December 2007 that, among other things, identify facilities that will have to reduce emissions and comply with stricter emission limitations. This program may restrict construction of new coal-fired power plants where emissions are projected to reduce visibility in protected areas. In addition, this program may require certain existing coal-fired power plants to install emissions control equipment to reduce haze-causing emissions such as sulfur dioxide, nitrogen oxide and particulate matter.

The U.S. Department of Justice, on behalf of the EPA, has filed lawsuits against a number of coal-fired electric generating facilities alleging violations of the new source review provisions of the CAA. The EPA has alleged that certain modifications have been made to these facilities without first obtaining permits required under the new source review program. Several of these lawsuits have settled, but others remain pending. On April 2, 2007, the U.S. Supreme Court ruled in one such case,Environmental Defense v. Duke Energy Corp. The Court held that the EPA is not required to use an “hourly rate test” in determining whether a modification to a coal burning utility requires a permit under the new source review program, thus allowing the EPA to apply a test based on average annual emissions. The use of an annual emissions test could subject more coal-fired utility modification projects to the permitting requirements of the CAA New Source Review Program, such as those that allow plants to run for more hours in a given year. However, Duke is expected to continue to contest remaining issues in the case, and so litigation in this and other pending cases will likely continue. Depending on the ultimate resolution of these cases, demand for PVR’s coal could be affected, which could have an adverse effect on PVR’s coal royalties revenues.

12

TABLE OF CONTENTS

Carbon Dioxide Emissions. The Kyoto Protocol to the United Nations Framework Convention on Climate Change calls for developed nations to reduce their emissions of greenhouse gases to 5% below 1990 levels by 2012. Carbon dioxide, which is a major byproduct of the combustion of coal and other fossil fuels, is subject to the Kyoto Protocol. The Kyoto Protocol went into effect on February 16, 2005 for those nations that ratified the treaty. In 2002, the United States withdrew its support for the Kyoto Protocol, and the United States is not participating in this treaty. Since the Kyoto Protocol became effective, there has been increasing international pressure on the United States to adopt mandatory restrictions on carbon dioxide emissions. In addition, on April 2, 2007 the U.S. Supreme Court held inMassachusetts v. EPA that unless the EPA affirmatively concludes that greenhouse gases are not causing climate change, the EPA must regulate greenhouse gas emissions from new automobiles under the CAA. The Court remanded the matter to the EPA for further consideration. This litigation did not directly concern the EPA’s authority to regulate greenhouse gas emissions from stationary sources, such as coal mining operations or coal-fired power plants. However, the Court’s decision is likely to influence another lawsuit currently pending in the U.S. Court of Appeals for the District of Columbia Circuit, involving a challenge to the EPA’s decision not to regulate carbon dioxide from power plants and other stationary sources under a CAA new source performance standard rule, which specifies emissions limits for new facilities. The court remanded that question to the EPA for further consideration in light of the ruling inMassachusetts v. EPA. On July 11, 2008, the EPA released an advanced notice of proposed rulemaking to regulate greenhouse gases under the CAA in response to the ruling inMassachusetts v. EPA. The notice did not contain a definitive proposal of what a greenhouse gas regulatory program would look like, but it presented the EPA’s analyses and policy alternatives for consideration. The EPA stated that promulgating a program under the CAA would take years to issue. In 2009, EPA took further steps toward greenhouse gas regulation under the CAA, issuing a final rule declaring that six greenhouse gases, including carbon dioxide and methane, “endanger both the public health and the public welfare of current and future generations.” The issuance of this “endangerment finding” allows the EPA to begin regulating greenhouse gas emissions under existing provisions of CAA. In late September and early October of 2009, in anticipation of the issuance of the endangerment finding, the EPA officially proposed two sets of rules regarding possible future regulation of greenhouse gas emissions under the CAA, one that would regulate greenhouse gas emissions from motor vehicles and the other greenhouse gas emissions from large stationary sources such as power plants or industrial facilities. Any decision in this case or any regulatory action by the EPA limiting greenhouse gas emissions from power plants could impact the demand for PVR’s coal, which could have an adverse effect on PVR’s coal royalties revenues.

The permitting of a number of proposed new coal-fired power plants has also recently been contested by environmental organizations for concerns related to greenhouse gas emissions from new plants. For instance, in October 2007, state regulators in Kansas became the first to deny an air emissions construction permit for a new coal-fired power plant based on the plant’s projected emissions of carbon dioxide. State regulatory authorities in Florida and North Carolina have also rejected the construction of new coal-fired power plants based on the uncertainty surrounding the potential costs associated with greenhouse gas emissions from these plants under future laws limiting the emission of carbon dioxide.

In addition, permits for several new coal-fired power plants without limits imposed on their greenhouse gas emissions have been appealed by environmental organizations to the EPA’s Environmental Appeals Board, or EAB, and other judicial forums under the CAA. For example, in June 2008, a Georgia court voided a CAA permit and halted the construction of a coal-fired power plant for failure to address carbon dioxide emissions. Likewise, in November 2008, in another case,In re Deseret Power Electric Cooperative, the EAB remanded the permitting decision back to the Region to reopen the record and reconsider whether carbon dioxide is a pollutant subject to regulation under the CAA with instructions to consider its nationwide implications. In December 2008, the EPA Administrator issued an interpretive rule determining the phrase in the CAA “not subject to regulation” does not include pollutants for which only monitoring and reporting is required. Because carbon dioxide is such a pollutant, this interpretive rule has the effect of precluding any consideration of carbon dioxide emissions in connection with federal permitting under the CAA. Environmental groups filed a Petition for Reconsideration of the interpretive rule. On February 17, 2009, the EPA stated that it would grant the Petition for Reconsideration and allow public comment, but it declined to stay the effectiveness of the interpretive rule at that time.

13

TABLE OF CONTENTS

A number of states have also either passed legislation or announced initiatives focused on decreasing or stabilizing carbon dioxide emissions associated with the combustion of fossil fuels, and many of these measures have focused on emissions from coal-fired electric generating facilities. For example, ten northeastern and mid-Atlantic states have agreed to implement a regional cap-and-trade program, referred to as the Regional Greenhouse Gas Initiative, or RGGI, to stabilize carbon dioxide emissions from regional power plants beginning in 2009. This initiative aims to reduce emissions of carbon dioxide to levels roughly corresponding to average annual emissions between 2000 and 2004. The members of RGGI agreed to seek to establish in statute and/or regulation a carbon dioxide trading program and have each state’s component of the regional program effective no later than December 31, 2008. Auctions for carbon dioxide allowances under the program began in September 2008. Following the RGGI model, seven Western states and four Canadian provinces have also formed a regional greenhouse gas reduction initiative known as the Western Regional Climate Action Initiative, which calls for an overall reduction of regional greenhouse gas emissions from major industrial and commercial sources, including fossil-fuel fired power plants, in participating states through trading of emissions credits beginning in 2012. Similarly, in 2007, six Midwestern states and one Canadian province signed the Midwestern Greenhouse Gas Reduction Accord to develop and implement steps to reduce greenhouse gas emissions, including developing a market-based, multi-sector cap. Some states have passed laws individually. For example, in 2006, the governor of California signed Assembly Bill 32 into law, requiring the California Air Resources Board to develop regulations and market mechanisms to reduce California’s greenhouse gas emissions by 25% by 2020 with mandatory caps beginning in 2012 for significant sources. In 2007, New Jersey passed a greenhouse gas reduction that would be economy wide, requiring emissions to drop to 1990 levels by 2020 and that emissions be capped at 80% of 2006 levels by 2050.

At the federal level, legislation was introduced in Congress in 2007, 2008 and 2009 to reduce greenhouse gas emissions in the United States. Such or similar federal legislation, which generally seeks to place an economy-wide cap on emissions of greenhouse gases and would require most sources of greenhouse gas emissions to obtain greenhouse gas emission “allowances” corresponding to their annual emissions of greenhouse gases, could be taken up in 2010 or later years. It is possible that future federal and state initiatives to control and put a price on carbon dioxide emissions, or otherwise regulate greenhouse gas emissions, could result in increased costs associated with coal consumption, such as costs to install additional controls to reduce carbon dioxide emissions or costs to purchase emissions reduction credits to comply with future emissions trading programs. Such increased costs for coal consumption could result in some customers switching to alternative sources of fuel, which could negatively impact PVR’s lessees’ coal sales, and thereby have an adverse effect on PVR’s coal royalties revenues.

Surface Mining Control and Reclamation Act of 1977. The Surface Mining Control and Reclamation Act of 1977, or SMCRA, and similar state statutes establish minimum national operational, reclamation and closure standards for all aspects of surface mining, as well as most aspects of deep mining. SMCRA requires that comprehensive environmental protection and reclamation standards be met during the course of and following completion of mining activities. SMCRA also imposes on mine operators the responsibility of restoring the land to its original state and compensating the landowner for types of damages occurring as a result of mining operations, and requires mine operators to post performance bonds to ensure compliance with any reclamation obligations. Moreover, regulatory authorities may attempt to assign the liabilities of PVR’s coal lessees to another entity such as PVR if any of its lessees are not financially capable of fulfilling those obligations on the theory that PVR “owned” or “controlled” the mine operator in such a way for liability to attach. To our knowledge, no such claims have been asserted against PVR to date. In conjunction with mining the property, PVR’s coal lessees are contractually obligated under the terms of their leases to comply with all state and local laws, including SMCRA, with obligations including the reclamation and restoration of the mined areas by grading, shaping and reseeding the soil. Upon completion of the mining, reclamation generally is completed by seeding with grasses or planting trees for use as pasture or timberland, as specified in the approved reclamation plan. Additionally, the Abandoned Mine Lands Program, which is part of SMCRA, imposes a tax on all current mining operations, the proceeds of which are used to restore mines closed before 1977. The maximum tax is 31.5 cents per ton on surface-mined coal and 13.5 cents per ton on underground-mined coal. This tax was set to expire on June 30, 2006, but the program was extended until September 30, 2021.

14

TABLE OF CONTENTS

Federal and state laws require bonds to secure PVR’s lessees’ obligations to reclaim lands used for mining and to satisfy other miscellaneous obligations. These bonds are typically renewable on a yearly basis. It has become increasingly difficult for mining companies to secure new surety bonds without the posting of partial collateral. In addition, surety bond costs have increased while the market terms of surety bonds have generally become less favorable. It is possible that surety bonds issuers may refuse to renew bonds or may demand additional collateral upon those renewals. Any failure to maintain, or inability to acquire, surety bonds that are required by state and federal laws would have a material adverse effect on PVR’s lessees’ ability to produce coal, which could affect PVR’s coal royalties revenues.

Hazardous Materials and Wastes. The Federal Comprehensive Environmental Response, Compensation and Liability Act, or CERCLA, or the Superfund law, and analogous state laws, impose liability, without regard to fault or the legality of the original conduct, on certain classes of persons that are considered to have contributed to the release of a “hazardous substance” into the environment. These persons include the owner or operator of the site where the release occurred and companies that disposed or arranged for the disposal of the hazardous substances found at the site. Persons who are or were responsible for releases of hazardous substances under CERCLA may be subject to joint and several liability for the costs of cleaning up the hazardous substances that have been released into the environment and for damages to natural resources.

Some products used by coal companies in operations generate waste containing hazardous substances. PVR could become liable under federal and state Superfund and waste management statutes if its lessees are unable to pay environmental cleanup costs. CERCLA authorizes the EPA and, in some cases, third parties, to take actions in response to threats to the public health or the environment and to seek recovery from the responsible classes of persons of the costs they incurred in connection with such response. It is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by hazardous substances or other wastes released into the environment. The Resource Conservation and Recovery Act, or RCRA, and corresponding state laws and regulations exclude many mining wastes from the regulatory definition of hazardous wastes. Currently, the management and disposal of coal combustion by-products are also not regulated at the federal level and not uniformly at the state level. If rules are adopted to regulate the management and disposal of these by-products, they could add additional costs to the use of coal as a fuel and may encourage power plant operators to switch to a different fuel.

Clean Water Act. PVR’s coal lessees’ operations are regulated under the Clean Water Act, or the CWA, with respect to discharges of pollutants, including dredged or fill material into waters of the United States. Individual or general permits under Section 404 of the CWA are required to conduct dredge or fill activities in jurisdictional waters of the United States. Surface coal mining operators obtain these permits to authorize such activities as the creation of slurry ponds, stream impoundments and valley fills. Uncertainty over what legally constitutes a navigable water of the United States within the CWA’s regulatory scope may adversely impact the ability of PVR’s coal lessees to secure the necessary permits for their mining activities. Some surface mining activities require a CWA Section 404 “dredge and fill” permit under the CWA for valley fills and the associated sediment control ponds. On June 5, 2007, in response to the U.S. Supreme Court’s divided opinion inRapanos v. United States, the EPA and the U.S. Army Corps of Engineers, or the Corps, issued joint guidance to EPA regions and Corps districts interpreting the geographic extent of regulatory jurisdiction under Section 404 of the CWA. Specifically, the guidance places jurisdictional water bodies into two groups: waters where the agencies will assert regulatory jurisdiction “categorically” and waters where the agencies will assert jurisdiction on a case-by-case basis following a “significant nexus analysis.” It remains to be seen how this guidance will affect the permitting process for obtaining additional permits for valley fills and sediment ponds although it is likely to add uncertainty and delays in the issuance of new permits. Some valley fill surface mining activities have the potential to impact headwater streams that are not relatively permanent, which could therefore trigger a detailed “significant nexus analysis” to determine whether a Section 404 permit would be required. Such analyses could require the extensive collection of additional field data and could lead to delays in the issuance of CWA Section 404 permits for valley fill surface mining operations.

Recent federal district court decisions in West Virginia, and related litigation filed in federal district court in Kentucky, have created additional uncertainty regarding the future ability to obtain certain general permits authorizing the construction of valley fills for the disposal of overburden from mining operations. The Corps is authorized by Section 404 of the CWA to issue “nationwide” permits for specific categories of dredging

15

TABLE OF CONTENTS