UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file Number: 811-04338

EAGLE CAPITAL APPRECIATION FUND

(Exact name of Registrant as Specified in Charter)

880 Carillon Parkway

St. Petersburg, FL 33716

(Address of Principal Executive Office) (Zip Code)

Registrant’s Telephone Number, including Area Code: (727) 567-8143

RICHARD J. ROSSI, PRESIDENT

880 Carillon Parkway

St. Petersburg, FL 33716

(Name and Address of Agent for Service)

Copy to:

FRANCINE J. ROSENBERGER, ESQ.

K&L Gates, LLP

1601 K Street, NW

Washington, D.C. 20006

Date of fiscal year end: October 31

Date of reporting period: October 31, 2010

Explanatory Note: The Board of Officers were elected November 16, 2010.

| Item 1. | Reports to Shareholders |

EAGLE MUTUAL FUNDS

| | |

| Annual Report | | |

| |

and Investment Performance Review for the fiscal year ended October 31, 2010 | | |

| |

| Eagle Capital Appreciation Fund | | |

| |

| Eagle Growth & Income Fund | | |

| |

| Eagle International Equity Fund | | |

| |

| Eagle Investment Grade Bond Fund | | |

| |

| Eagle Large Cap Core Fund | | |

| |

| Eagle Mid Cap Growth Fund | | |

| |

| Eagle Mid Cap Stock Fund | | |

| |

| Eagle Small Cap Core Value Fund | | |

| |

| Eagle Small Cap Growth Fund | | |

| |

| Privacy Notice | | |

| |

Eagle Family of Funds | | |

| EAGLE | | Family of Funds |

Table of Contents

| | |

|

Visit eagleasset.com/eDelivery to receive shareholder communications including prospectuses and fund reports with a service that helps protect the environment:

Environmentally friendly. Go green with eDelivery by reducing the number of trees used to produce paper.

Efficient. Stop waiting on regular mail. Your documents will be sent via email as soon as they are available.

Easy. Download and save files using your home computer with a few clicks of a mouse.

President’s Letter

Dear Fellow Shareholders:

I am pleased to present the annual report and investment performance review of the Eagle Family of Funds for the fiscal year ended October 31, 2010 (the “reporting period”). In March 2010, Eagle launched the Investment Grade Bond Fund to offer greater diversification to shareholders.

Major U.S. indices posted solid gains during the reporting period, extending the rally that began in March 2009. Cyclical, higher beta companies saw the biggest gains in their share prices, while growth stocks generally outperformed value stocks. The markets have been encouraged by some indications of economic expansion, improving corporate earnings, currently benign inflation and continued low interest rates.

Significant uncertainty exists regarding the strength of the recovery, which appears to be slower than recoveries from previous recessions. High unemployment and problems in the housing market continue. These negative forces have led to mortgage rates remaining very low.

Internationally, concerns surrounding the European sovereign debt crisis and uncertainty around bank stress tests negatively impacted the markets early in the reporting period. The euro suffered as questions were raised regarding whether it could survive as a common currency. As the year progressed, no European country defaulted and positive stress test results were announced, causing a temporary rally in international equities and the euro. As the reporting period ended, concerns surrounding European debt persisted.

In the commentaries that follow, each fund’s portfolio managers discuss the specific performance in their funds. While performance during the reporting period was encouraging and positive signs of economic growth are present, it bears remembering that markets remain volatile. During the reporting period, there were two notable corrections

in the equity markets. Market corrections and movement can create opportunities for long-term, fundamental stock picking over time.

In an effort to save costs and reduce environmental impact, Eagle is able to offer many reports electronically. If you would like to begin receiving this report and other reports from the Eagle Family of Funds electronically, please visit our website, eagleasset.com, and enroll for electronic delivery. Doing so will reduce the amount of paper we consume which saves the Funds (and their shareholders) money and will help the environment. Enrolling in this service will not affect the delivery of your account statements or other confidential communications.

I would like to remind you that investing in any mutual fund carries certain risks. The principal risk factors for each fund are described at the end of this report. Carefully consider the investment objectives, charges and expenses of any fund before you invest. Contact us at 800.421.4184 or eagleasset.com or your financial advisor for a prospectus, which contains this and other important information about the Eagle Family of Funds. Our website also has timely information about the Funds, including performance and portfolio holdings.

We are grateful for your continued support and confidence in the Eagle Family of Funds.

Sincerely,

Richard J. Rossi

President

December 8, 2010

| | |

| Performance Summary and Commentary |

| Eagle Capital Appreciation Fund | | |

Meet the managers | Steven M. Barry and David G. Shell, CFA are Chief Investment Officers and Senior Portfolio Managers at Goldman Sachs Asset Management L.P. and have been responsible for the day-to-day management of the Eagle Capital Appreciation Fund (the “Fund”) since 2002. Mr. Shell has been affiliated with the Fund since 1987 and has 23 years of investment experience; Mr. Barry joined the team in 1999 and has 24 years of investment experience.

Investment highlights | The Fund invests primarily in common stocks. The Fund’s portfolio management team believes that wealth is created through the long-term ownership of a growing business. They take a “bottom-up” approach to investing based on in-depth, fundamental research. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. The portfolio managers use an intensive research process and each company is analyzed as if they were going to own and operate that company indefinitely. Key characteristics of the companies in which the Fund currently seeks to invest may include: dominant market share, established brand name, pricing power, recurring revenue stream, free cash flow, high returns on invested capital, predictable growth, sustainable growth, long product life cycle, enduring competitive advantage, favorable demographic trends and excellent management.

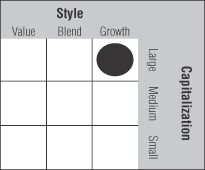

This Morningstar Style Box™ shows the Fund’s investment style and size of companies held in the Fund.

© Copyright 2010 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

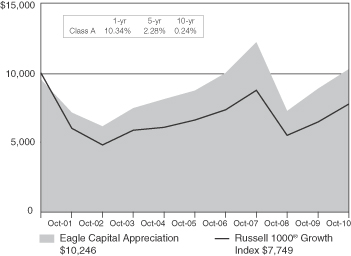

Performance summary | The Fund’s Class A shares returned 15.85% (excluding front-end sales charges) during the fiscal year ended October 31, 2010, underperforming its benchmark index, the Russell 1000® Growth Index, which returned 19.65%. The Russell 1000® Growth Index measures

performance of those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values and is representative of U.S. securities exhibiting growth characteristics. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 11/1/00 to 10/31/10 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The Fund delivered strong absolute performance during the fiscal year ended October 31, 2010. The Fund’s top performing sectors were telecommunication services and information technology. While all market sectors delivered positive returns, the energy and health care sectors lagged.

The Fund trailed its benchmark, the Russell 1000® Growth Index, during the period due to relative underperformance in the consumer discretionary, health care and industrials sectors. In the strong performing consumer discretionary sector, the Fund was hurt by its underweight position and underperformance of its holdings. An overweight position coupled with stock selection in the underperforming health

| | |

| Performance Summary and Commentary |

| Eagle Capital Appreciation Fund (cont’d) |

care sector detracted. The Fund had no holdings in the strong performing industrials sector. On the positive side, the Fund benefited from its overweight allocation to the top performing telecommunication services sector, combined with strong stock selection. Positive stock selection in the information technology sector also contributed to performance.

Under performers | Pharmaceutical manufacturer Baxter International, Inc. detracted from performance. Early in the year, the company trimmed its earnings forecast for 2010 due to a weaker outlook for its bioscience (blood plasma) business. Competition in the blood plasma market has increased, making it more difficult for Baxter International to price its products at a premium. While we expect uncertainty in the plasma business to remain an overhang in the near-term, we continue to believe the company trades at an attractive valuation due to its robust product pipeline and its market leading franchise. The Fund continues to hold the security.

Shares of Staples, Inc., an office supply retailer, traded down during the reporting period. The company remains focused on cost cutting, gaining market share from competitors, and expanding its geographic footprint in less saturated markets. Staples continues to make investments in new business processes that should strengthen its brand and position it for growth over the long-term. We believe Staples should also benefit from pent up demand given the drawdown of inventory by its corporate clients. We continue to hold the stock in the Fund as we expect that normalization in inventory levels should generate demand growth for the company.

CME Group, Inc., the world’s largest futures and options exchange, detracted from performance given lingering concerns over the rulemaking process following financial reform legislation. In addition, the company’s trading volumes, particularly those used to hedge changes in interest rates, remain under pressure due to market expectations that low rates will persist. We continue to believe CME Group will be a long-term beneficiary of the migration from over-the-counter (OTC) derivatives markets to exchanges. Furthermore, we believe the company’s OTC clearing house business is a significant growth opportunity, as it meets its customers’ demands for more transparency and less counterparty risk. The Fund continues to hold the stock.

Data center services company, Equinix, Inc. declined after pre-announcing a third quarter and full year 2010 revenue shortfall that was greater than market expectations. We believe the poor results were primarily driven by pricing concessions the company is making to retain key customers. The price

concessions appear to be the result of increasing competition at the basic service level and pricing pressure from key clients. The company’s key clients are dominant players in the social media, mobile computing, and telecom industries, and have a critical “hub” role in the data center. We trimmed the Fund’s position before the stock hit its lows due to greater uncertainty in how pricing related to these customers will develop in future years. Despite these headwinds, we believe the company should show strong organic revenue growth this year and can sustain it into future years.

Charles Schwab Corp. detracted from performance as persistently low short-term interest rates continue to force the financial services firm to waive fees on its money market funds. With uncertainty in global markets, rates are expected to remain low through 2011, forcing these waivers to continue. Furthermore, Bank of America/Merrill Lynch re-launched a competing online brokerage offering, which weighed on sentiment. The Fund still owns the stock, as we believe the company continues to execute on its business model and remains attractively valued and should benefit once interest rates move higher.

Top performers | CB Richard Ellis, Inc., the world’s leading commercial real estate services firm, contributed to performance over the past twelve months after reporting earnings that exceeded expectations. The results were driven by strong revenues in property sales and leasing, as well as cost reductions during the recent downturn which resulted in significant operating leverage. We continue to have conviction in the company given the strength of its franchise, its service-oriented business model, and its strong management team.

Wireless tower companies American Tower Corp. and Crown Castle International Corp. contributed to performance as both companies reported strong revenue and earnings growth. We believe the tower companies are well-positioned in a growing industry with high barriers to entry. Specifically, as the wireless communication industry continues to evolve from primarily voice to more data usage, the demands on the networks increase. In our view, this will lead to a greater need for more antennae to be placed on the towers, thereby increasing leasing revenues. Furthermore, we believe that the contracts used in the companies’ business models are attractive, as they provide a very predictable stream of revenue and recurring cash flow.

Broadcom Corp., a global leader in semiconductors for wired and wireless communications, contributed to performance during the period. Shares of Broadcom outperformed the market as the company reported first quarter earnings that

| | |

| Performance Summary and Commentary |

| Eagle Capital Appreciation Fund (cont’d) |

beat consensus estimates and provided a better-than-expected second quarter outlook. The results were driven by strength in the company’s mobile/wireless and enterprise networking business segments. In our view, Broadcom has significant growth opportunities in the wireless connectivity markets, as it currently ships to five of the six largest cellular handset manufacturers. Specifically, the company recently signed agreements with Samsung and Nokia, which are providing a tailwind to unit sales growth.

Oracle Corp. contributed to performance after the company reported growth in earnings and revenue. The company’s software license revenues and product support revenues were above expectations as demand improved. In addition, we believe that the acquisition of Sun Microsystems should complement Oracle’s product portfolio and strengthen its long-term industry position.

The Fund continues to hold each of the securities noted above as “top performers.”

| | |

| Performance Summary and Commentary |

| Eagle Growth & Income Fund | | |

Meet the managers | William V. Fries, CFA, Managing Director, and Cliff Remily, CFA, of Thornburg Investment Management, Inc. are Co-Portfolio Managers of the Eagle Growth & Income Fund (the “Fund”). Mr. Fries has more than 39 years of investment experience and has been Co-Portfolio Manager since 2001. Mr. Remily was named Co-Portfolio Manager in January 2009 and has over 10 years of industry experience.

Investment highlights | The Fund invests primarily in domestic equity securities (primarily common stocks) and can invest up to 30% of its net assets in foreign securities including up to 10% of its net assets in emerging markets securities. The Fund can also invest in fixed income securities. The Fund’s portfolio managers look for promising investments that can be purchased at a discount to their estimate of each investment’s intrinsic value. They seek investments that deliver a competitive total return over multiple time horizons. Holdings are classified in three categories: basic value, consistent earners and emerging franchises as a means of structuring diversification. Dividends and dividend growth are a consideration in stock selection and may include stocks outside the traditional dividend paying areas.

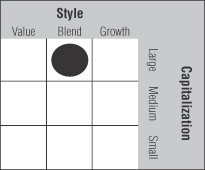

This Morningstar Style Box™ shows the Fund’s investment style and size of companies held in the Fund.

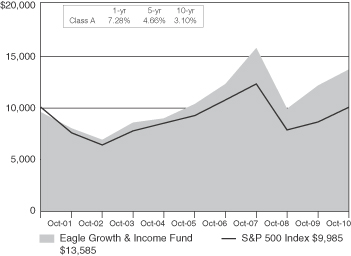

Performance summary | The Fund’s Class A shares returned 12.65% (excluding front-end sales charges) during the fiscal year ended October 31, 2010, underperforming its benchmark index, the Standard & Poor’s 500 Composite Stock Index (“S&P 500 Index”) which returned 16.52%. The S&P 500 Index is an unmanaged index of 500 U.S. stocks and gives a broad look at how stock prices have performed. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 11/1/00 to 10/31/10 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance summary | The Fund participated in the market’s rally over the past year with positive absolute returns in every sector. For the fiscal year ended October 31, 2010, the Fund’s average return from its investments in the consumer discretionary sector was greater than 33%, followed by industrials (up over 26%) and finally consumer staples, information technology, telecommunication services and energy (up over 10% each). The Fund’s international exposure also had a positive impact and contributed approximately 5% to absolute performance.

The Fund’s underperformance relative to the benchmark, the S&P 500 Index, was due to both allocation factors and stock selection. For example, the Fund held an overweight position in the telecommunication services sector, which helped relative performance but did not offset the negative stock selection in the sector. The Fund was also underweight in the consumer discretionary sector, which was the top performing sector in the benchmark, and overweight in financials, which was the poorest performing sector.

| | |

| Performance Summary and Commentary |

| Eagle Growth & Income Fund (cont’d) |

Stocks in the consumer staples sector were the highlight over the past year, contributing the most on both an absolute and relative basis; however, this was counteracted by an underweight in the strong performing industrials sector. Although the Fund’s limited fixed income holdings were a positive contributor on an absolute basis, the exposure to fixed income hurt performance on a relative basis.

Under performers | Bank of America Corporation has been under pressure over concerns regarding the uncertainty of whether the bank would be required to put defaulted mortgages back on their balance sheet and potential legal liability associated with originating mortgage backed collateralized debt obligations without fully disclosing quality issues to buyers. In addition, fee revenue has declined given new U.S. banking regulations. The Fund’s long-term investment thesis for this holding is still intact and the Fund continues to hold the position.

Insurer AXA SA underperformed over concerns regarding the company’s ability to grow their variable annuity life business given the financial hardship the greater European Union faced over the past year. Due to these facts the Fund sold its position in the company.

Oil exploration company Diamond Offshore Drilling, Inc. reduced its dividend in the first quarter of calendar year 2010 due to a weakened backlog and expectations for rising costs related to maintaining its older fleet of offshore drilling rigs. On that news, the stock was sold from the Fund and the proceeds were invested in a competitor.

JPMorgan Chase & Co. provided flat overall returns despite building a stronger competitive position within its business segments. Further, the company has continued to increase its capital well above required minimums. This should enhance its ability to make strategic acquisitions, increase its dividend, or buyback shares. Despite the company’s strong fundamentals the overall uncertainty regarding banks and potential regulations has weighed heavily on the stock performance. The Fund still holds the stock.

Pharmaceutical manufacturer Teva Pharmaceutical Industries Ltd., along with most health care companies, underperformed the market as investors grew weary of the likelihood of the U.S. health care overhaul and outsized government deficits. Teva was also exposed to Israel’s re-classification into the developed markets index. The Fund continues to hold the stock.

Top performers | Baidu Inc., the leading internet search provider in China, gained market share rapidly and today remains the leading search provider in China. In addition, the company benefited from an announcement that Google was exiting the Chinese market in 2010. The Fund sold its position in the company at a price target.

Cable services provider Comcast Corporation benefited from new subscriber additions and improved margins as average revenue per subscriber increased (current customers adding additional services). The company also has a strong share buyback program while maintaining an attractive dividend yield. The Fund continues to hold the stock.

McDonald’s Corp. continued to benefit from the recessionary conditions as customers looked for value meals. Investors also became more interested in McDonald’s consistent earner characteristics and the company’s near 3% yield. The Fund still owns the stock.

Tobacco producer Philip Morris International, Inc. benefited from continued growth in volumes as well as a weak U.S. dollar. The company continues to utilize its strong cash generation to pay dividends and repurchase stocks. The dividend yield, which exceeded 4%, attracted investors, especially when compared to the low interest rates on fixed income instruments. The position is still held in the Fund.

Oil exploration company Seadrill Ltd. has a high quality offshore oil drilling fleet (average age of equipment is approximately four years), a progressive dividend policy, and significant cash on the balance sheet which we believe all bode well for the company. They also have very limited exposure to the impact of the Gulf of Mexico oil spill which helped support their performance. The Fund continues to own the stock.

| | |

| Performance Summary and Commentary |

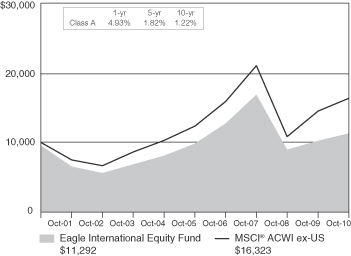

| Eagle International Equity Fund |

Meet the managers | Richard C. Pell is Chief Executive Officer at Artio Global Investors Inc. and Chief Investment Officer at its affiliate, Artio Global Management LLC (“Artio Global”). Rudolph-Riad Younes, CFA, is Head of International Equities at Artio Global. Messrs. Pell and Younes have managed the Eagle International Equity Fund (the “Fund”) since 2002.

Investment highlights | The Fund invests primarily in foreign equity securities. The Fund’s portfolio managers seek investment opportunities within the developed and emerging markets. In the developed markets, a “bottom-up” approach is adopted. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. In the emerging markets, a “top-down” assessment consisting of currency/ interest rate risks, political environments/leadership assessment, growth rates, structural reforms and risk (liquidity) is applied. A top-down method of analysis emphasizes the significance of economy and market cycles. In Japan, given the highly segmented nature of this market comprised of both strong global competitors and protected domestic industries, a hybrid approach encompassing both bottom-up and top-down analyses is conducted.

This Morningstar Style Box™ shows the Fund’s investment style and size of companies held in the Fund.

Performance summary | The Fund’s Class A shares returned 10.14% (excluding front-end sales charges) during the fiscal year ended October 31, 2010, underperforming its benchmark index, which returned 12.62%. The Fund’s benchmark index, the Morgan Stanley Capital International® All Country World Index ex-US (“MSCI® ACWI ex-US”), is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 11/1/00 to 10/31/10 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | Concerns surrounding the European sovereign debt crisis and pending eurozone bank stress tests impacted international markets during most of the first half of the reporting period. Declines in European bourses were further exacerbated by a decline in the euro over this same period as investors began to question the long term viability of the common currency. However, after positive bank stress tests results were announced in July, international equities began to rebound as did the euro, and rallies within equities generally were further supported amid prospects for the U.S. Federal Reserve’s second round of quantitative easing.

For the fiscal year ended October 31, 2010, the Fund realized its largest absolute returns in the consumer staples, materials, industrials, information technology and consumer discretionary sectors, whereas the financials, energy and utilities sectors underperformed. From an absolute performance perspective, emerging markets outperformed their developed market counterparts.

| | |

| Performance Summary and Commentary |

| Eagle International Equity Fund (cont’d) |

For the review period, the Fund underperformed its benchmark index, the MSCI ACWI (ex-US). Stock selection within developed markets detracted as did country and stock selection within emerging markets; however the Fund’s underweight to Japan contributed to relative results, as did the allocation decision between emerging and developed markets.

Within developed markets, the Fund’s positioning in the financials, consumer staples and telecommunications sectors detracted from the Fund’s investment performance. Within emerging markets, stock selection in China detracted from relative performance whereas stock selection in Russia, Taiwan and India had a positive impact.

The Fund participated in the IPO of Pandora (Denmark), a manufacturer and designer of jewelry as well as in Amadeus IT (Spain), involved in software for the global travel and tourism industry, both of which outperformed. The Fund continues to hold both companies. The Fund also benefitted from currency hedging out of the euro into the U.S. dollar amid weakness for the euro. As of the end of the period, the Fund no longer held these hedge positions.

Under performers | The Fund’s position held in iShares Euro Stoxx 50 Index Fund underperformed, notably during the sovereign debt crisis, the effect of which was magnified due to a declining euro relative to the U.S. dollar. The Fund occasionally invests in this index fund as a way to quickly adjust its overall exposure to a region or specific market. As of the end of the period, the position was no longer held.

Shares held in UniCredit S.p.A. (Italy), OTP Bank Nyrt. (Hungary) and BNP Paribas (France) underperformed. The sovereign debt crisis, centered on Portugal, Ireland, Italy, Greece and Spain, led many banks within the eurozone as well as in Central and Eastern Europe to underperform during the period. As investors tried to assess the level of sovereign debt held by European banks, several credit rating agency downgrades added to these concerns and placed added pressure on the value of the euro versus the U.S. dollar during the first seven months of the reporting period. We remain cautious on the outlook for eurozone banks and remain underweight. We expect these banks to raise new capital, which will likely be dilutive to existing investors but should result in more sound systemic fundamentals. The Fund sold its positions in UniCredit and OTP Bank but maintained its investment in BNP Paribas as we believe they have more limited exposure to sovereign debt and find their business mix to be attractive. Specifically, we are seeing some loan growth

in their home market, a solid investment banking business, adequate capital levels and an attractive valuation.

Shares of drug maker Roche Holding AG (Switzerland), which the Fund no longer holds, underperformed during the period due to two major events. A Phase III trial for a new diabetes drug was halted amid the observation of negative side effects. The company had expectations this drug would become the next blockbuster in their arsenal. Additionally, approval for a breast cancer drug is now in question over concerns regarding its risks and benefits.

Top performers | Cellular phone manufacturer HTC Corp (Taiwan) was the first vendor to deliver a handset running the Android operating system, and has delivered a wide array of handsets to operators all over the world. They currently command a large share of the Android smartphone global market, leading to earnings visibility and strength in their share price. The Fund continues to own the security.

Amid strength in the metals and mining sector, shares of Rio Tinto PLC (UK) outperformed as did the Market Vectors ETF Gold Miners (U.S.). The sector has been well supported as demand for commodities such as copper and silver (used in the manufacture of items such as cable, wire and electrical products) remains strong. The price of gold has also enjoyed price gains in part due to economic uncertainty and burgeoning budget deficits within the developed world. The Fund still owns both of these securities.

Shares of Fraport AG NPV (Germany), the operator of the Frankfurt Airport, outperformed. The company views itself not only as a central traffic junction for aircraft, cars and trains, but also an “Airport City”—a first class address for mobility, shopping, events and real estate. Improving passenger traffic has contributed to outperformance. We view Fraport as a quasi-monopoly and it has been a long-term holding of the Fund’s and remains in the Fund.

iShares MSCI India Index Fund (India) outperformed given continued positive growth prospects for the country going forward. India forms an important component of our emerging market exposure within the Fund. The use of the Index fund has provided us with an expeditious way of adjusting the Fund’s exposure to India. The Fund continues to hold this position.

| | |

| Performance Summary and Commentary |

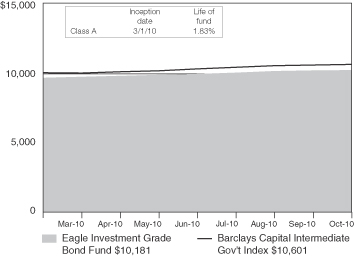

| Eagle Investment Grade Bond Fund |

Meet the managers | James C. Camp, CFA, a Managing Director at Eagle Asset Management (“Eagle”), and Joseph Jackson, CFA, have managed the Eagle Investment Grade Bond Fund (the “Fund”) since inception in March 2010 and are jointly responsible for the day-to-day management of the Fund’s investment portfolio. Mr. Camp and Mr. Jackson have 21 and 11 years of investment experience respectively.

Investment highlights | The Fund invests primarily in investment grade fixed income securities. Investment grade is defined as securities rated [BBB-] or better by Standard & Poor’s Rating Services or an equivalent rating by at least one other nationally recognized statistical rating organization or, for unrated securities, those that are determined to be of equivalent quality by the Fund’s Portfolio Managers. The average portfolio duration of the Fund is expected to vary and may generally range from two to seven years based upon economic and market conditions. The Fund expects to invest in a variety of fixed income securities including, but not limited to, corporate debt securities of U.S. and non-U.S. issuers, including corporate commercial paper; bank certificates of deposit; debt securities issued by states or local governments and their agencies; obligations of non-U.S. Governments and their subdivisions, agencies and government sponsored enterprises; obligations of international agencies or supranational entities (such as the European Union); obligations issued or guaranteed by the U.S. Government and its agencies; mortgage-backed securities and asset-backed securities; commercial real estate securities; and floating rate instruments.

This Morningstar Style Box TM shows the Fund’s investment style and size of companies held in the Fund.

Performance summary | The Fund’s Class A shares returned 5.78% (excluding front-end sales charges) from its inception on March 1, 2010 through October 31, 2010, underperforming its benchmark index, which returned 6.01%. The Fund’s benchmark index, the Barclays Intermediate Government/Credit Bond Index, includes U.S. government and investment grade

credit securities that have a greater than or equal to one year and less than ten years remaining to maturity and have $250 million or more of outstanding face value. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 3/1/10 to 10/31/10 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 3.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The Fund commenced operations on March 1, 2010. During the reporting period ended October 31, 2010, there were three key trends in the bond market as a whole. First, the long end of the yield curve performed extremely well after being one of the worst investments of 2009. This yield curve flattening trend affected all sectors of the market. Next, bonds issued by companies in the financials sector generated excess returns despite the ongoing stress in the U.S. mortgage market, European debt crisis and SEC investigations. Finally, high risk bonds outperformed those of high quality. BBB-rated bonds outperformed bonds of higher quality ratings by more than 1.30% during the period.

| | |

| Performance Summary and Commentary |

| Eagle Investment Grade Bond Fund (cont’d) |

During the reporting period from inception through October 31, 2010, the Fund’s absolute performance was led by an extended rally in U.S. Treasuries. The Fund underperformed its benchmark index. In credit, the Fund’s overweight position in high quality industrial corporate bonds proved to be the largest contributor to the Fund’s relative performance. Conversely, an underweight to the financials sector was the largest detractor. U.S. Treasuries rallied and our underweight position hurt relative returns. This was offset by the Fund holding securities with an average duration in the sector that was significantly longer than the benchmark in a year where the long end of the yield curve outperformed the short end. In the Government-related space, the Fund’s overweight position in FDIC insured bonds hurt the Fund’s investment performance. Fortunately, the Fund’s overweight allocations to Canadian Local Authorities and Supranational Banks earned positive excess returns.

Under performers | Two FDIC insured issues, GE Capital Corp (FDIC-insured) 3% 12/2011 and JPM (FDIC-insured) 3.125% 12/2011, offered little incremental yields over U.S. Treasuries during the low-rate environment of the reporting period. We still hold these bonds in the Fund.

Treasury issues of shorter duration, including the Fund’s holding in U.S. Treasury 1.375% 2/2013, lagged those with longer durations for a majority of the year. The Fund has since sold the bond.

The short duration of the Verizon Communication 7.375% 9/2012 bond issued by the telecommunications firm

underperformed along with other shorter term bonds. We sold this bond, maturing in 2012, from the Fund and purchased a longer duration Verizon issue maturing in 2019.

The combination of delinquent mortgage buybacks and the very short average life of the Fannie Mae REMIC Trust 2007-B2AB 5.5% 12/2020 agency mortgage-backed security issue was a hindrance to the Fund’s investment performance. This bond was sold from the Fund.

Top performers | The U.S. Treasury 4.75% 8/2017 bond was the Fund’s largest-weight holding and significantly outperformed the average treasury bond in the benchmark due to its long duration. The Fund continues to own this bond.

Supranational banks and Canadian provincial bonds, Inter-American Development Bank (supranational) 2.5% and 7/2015 and Province of Ontario 2.7% 6/2015, provided strong returns in 2010 as investors diversified away from traditional Agency-sector giants Fannie Mae and Freddie Mac. The Fund still owns these bonds.

The Union Pacific 5.7% 8/2018 railroad bond performed well as businesses focused on economical means of freight transportation. This bond is still held in the Fund.

The Newmont Mining Corp 5.125% 10/2019 gold mining company bond benefited from the significant appreciation in the price of gold over the reporting period. The Fund still owns this bond.

| | |

| Performance Summary and Commentary |

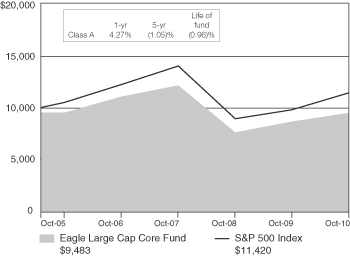

| Eagle Large Cap Core Fund | | |

Meet the managers | Richard Skeppstrom, John “Jay” Jordan, CFA, Craig Dauer, CFA, and Robert Marshall at Eagle Asset Management, Inc. (“Eagle”) have been Co-Portfolio Managers of the Eagle Large Cap Core Fund (the “Fund”) since inception. Mr. Skeppstrom is a Managing Director at Eagle and has 19 years of investment experience. Mr. Jordan, Mr. Dauer and Mr. Marshall have 19, 16 and 23 years of investment experience, respectively.

Investment highlights | The Fund invests primarily in common stocks. When identifying investments for the Fund, the portfolio managers use a “bottom-up” research process that is combined with a proprietary relative-valuation discipline. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. In general, the portfolio managers seek to select securities that, at the time of purchase, have above-average expected returns and at least one of the following characteristics: projected earnings growth rate at or above the benchmark index, above-average earnings quality and stability, or a price-to-earnings ratio comparable to the benchmark index.

This Morningstar Style Box™ shows the Fund’s investment style and size of companies held in the Fund.

Performance summary | The Fund’s Class A shares returned 9.48% (excluding front-end sales charges) during the fiscal year ended October 31, 2010, underperforming its benchmark index, the Standard & Poor’s 500 Composite Stock Index (“S&P 500 Index”) which returned 16.52%. The S&P 500 Index is an unmanaged index of 500 U.S. stocks and gives a broad look at how stock prices have performed. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 5/2/05 to 10/31/10 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The Fund’s gains were led by strong contributions from the information technology, consumer discretionary and industrials sectors. In information technology, the largest contributions were from the Fund’s holdings in the computers & peripherals and software industries. In consumer discretionary, the media and multiline retail industries performed best. In industrials, the Fund benefited from its aerospace & defense holdings. Negative return contributions occurred in the consumer staples and financial sectors, with the greatest underperformance coming from holdings in the food & staples retailing and diversified financial services industries, respectively.

The Fund underperformed its benchmark during the period primarily due to underperformance relative to the benchmark in the information technology, consumer staples and financials sectors. In information technology, the Fund’s holdings in the software and semiconductors industries underperformed. Holdings in the food & staples retailing industry led to relative underperformance in the consumer staples sector. Finally, in

| | |

| Performance Summary and Commentary |

| Eagle Large Cap Core Fund (cont’d) |

financials, the diversified financial services, commercial bank and real estate investment trust industries detracted from performance. On the other hand, the Fund benefited from stock selection in market-weighted energy and stock selection in underweighted telecommunication services.

Under performers | CVS Caremark Corporation was sold in November 2009 following its third quarter earnings announcement when management revealed additional large contract losses in the PBM (pharmacy benefit management—the acquired Caremark business) segment, and meaningfully reduced 2010 guidance for PBM operating earnings.

Bank of America Corporation sold off on cautious guidance following its second quarter earnings release along with concerns about the New York Fed and the Federal Housing Finance Administration’s plans to possibly get more aggressive on putting back bad loans in securitizations to originating banks. The Fund no longer holds this stock.

BP PLC was sold in May 2010. Liability concerns associated with the Deepwater Horizon oil spill in the Gulf of Mexico negatively impacted stock performance during the reporting period, offsetting improving fundamentals within the exploration & production (“E&P”) business. Our ability to develop any conviction around potential future liabilities was severely handicapped.

Video game manufacturer Electronic Arts, Inc. was sold in June 2010. While management made significant progress in improving game quality and production efficiency, the company’s recent video game releases have been viewed by the market as “average”. Given today’s lackluster consumer spending environment, we believed the Fund’s capital would be better off deployed elsewhere.

Wells Fargo & Company fell along with other major banks on concerns that banking regulatory overhaul legislation could result in lower debt ratings for major banks (due to a lack of

assumed government support), along with more recent concerns about the New York Fed and the Federal Housing Finance Administration’s plans to possibly get more aggressive on putting back bad loans in securitizations to originating banks. The stock is held for its strong competitive position and valuation attractiveness.

Top performers | UnitedHealth Group, Inc., along with other managed health care stocks, reacted well to the health care bill that ultimately passed Congress. We believe this legislation will be negative for insurers once fully implemented, but could have been much worse. With the final signing of the bill, the health care debate—and its attendant vilification of health insurers—should be moved to the back burner for a while. The Fund still holds the stock as we view it as an attractive holding.

After selling Apple, Inc. in mid-March at a significant gain, the company reported second quarter results that significantly exceeded our expectation for iPhone units, Mac units, iPod units and gross margin. The sharp market selloff on May 6th, 2010 gave us a chance to repurchase the stock at an attractive price and it remains in the Fund.

Macy’s, Inc. strong performance reflected better-than-expected same store sales, upbeat management guidance, and rising consensus estimates. We believed per store sales productivity was improving, driven by the company’s merchandise localization efforts (customizing product offerings by store), along with improving consumer spending trends. We sold the security from the Fund as it reached its target price.

ConocoPhillips benefited from improved price realizations in the E&P business, strong margins in the domestic refining business, and continued execution of asset sales/deleveraging program. The stock remains a holding in the Fund.

Autodesk, Inc. was a strong performer for the Fund that was sold to take profits late in the reporting period due to a lack of visibility on the company’s geographically diverse end markets.

| | |

| Performance Summary and Commentary |

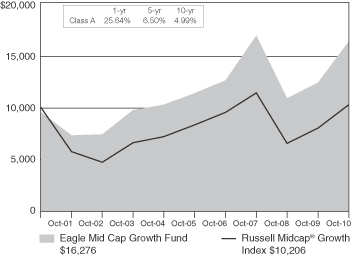

| Eagle Mid Cap Growth Fund |

Meet the managers | Bert L. Boksen, CFA, a Managing Director and Senior Vice President at Eagle Asset Management, Inc. (“Eagle”), is the Portfolio Manager of the Eagle Mid Cap Growth Fund (the “Fund”). Mr. Boksen has 33 years of investment experience. Eric Mintz, CFA, with 15 years of investment experience and Christopher Sassouni, DMD, with 21 years of investment experience and, have been Assistant Portfolio Managers since 2008 and 2006, respectively.

Investment highlights | The Fund invests primarily in stocks of mid-capitalization companies. The Fund’s portfolio managers seek to capture the significant long-term capital appreciation potential of mid-cap, rapidly growing companies. The portfolio managers use a “bottom-up” investment approach through a proprietary research strategy that emphasizes the selection of mid-cap growth stocks that are reasonably priced. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. The Fund’s portfolio managers believe that conducting extensive research on mid-cap companies may enable the Fund to capitalize on market inefficiencies and thus outperform the market.

This Morningstar Style Box™ shows the Fund’s investment style and size of companies held in the Fund.

Performance summary | The Fund’s Class A shares returned 31.91% (excluding front-end sales charges) during the fiscal year ended October 31, 2010, outperforming its benchmark index, which returned 28.03%. The Fund’s benchmark index, the Russell Midcap® Growth Index, measures the performance of those Russell Midcap® companies with higher price-to-book ratios and higher forecasted growth values. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 Investment from 11/1/00 to 10/31/10 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The Fund had strong absolute performance during the one-year reporting period ended October 31, 2010. On an absolute basis, the materials, information technology, consumer staples, and telecommunication services sectors led the Fund’s strong returns. In materials, the chemicals and metals & mining industries posted strong gains. The communications equipment industry posted the highest gains in the information technology sector. The personal products industry rallied most strongly in the consumer staples sector. In telecommunication services, wireless telecommunication services had a strong gain. On an absolute basis, healthcare and financials were the lagging sectors. In healthcare, the healthcare equipment & supplies industry posted a negative return for the year. In financials, the commercial banks and capital markets industries posted modest gains.

| | |

| Performance Summary and Commentary |

| Eagle Mid Cap Growth Fund (cont’d) |

The Fund outperformed its benchmark index during the reporting period. The materials, information technology, consumer staples and energy sectors each contributed to the strong relative returns. The Fund’s overweight position in materials amplified strong stock selection in this sector. The Fund outperformed in information technology due to strong stock selection in the semiconductors & semiconductor equipment, and communications equipment industries. The Fund benefited from an underweight position to consumer staples and very strong absolute performance. An overweight position and strong stock selection in the oil gas & consumable fuels industry led to outperformance in energy. The Fund underperformed relative to the benchmark in the health care sector during the reporting period as holdings in the healthcare equipment & supplies and healthcare providers & services industries underperformed.

Top performers | Chemical producer Huntsman Corporation, is a highly cyclical company that has appreciated as the economic outlook has improved. Further, the company has successfully implemented a cost reduction program. The Fund continues to hold the stock.

Rovi Corp, a provider of television guides for set-top boxes, has recently appreciated due to a new patent license agreement with Apple, in which Rovi will receive license fees for Apple’s use of Rovi’s patents in its AppleTV platform. We believe this bodes well for Rovi’s ability to receive license fees in the future from other companies with streaming on-line video technologies. The Fund continues to hold the stock.

Las Vegas Sands Corp., which owns and operates casino hotels, recently opened a resort in Singapore that has had significantly better than expected results. We continue to hold the stock in the Fund.

Kansas City Southern is a railroad that operates in the U.S., Mexico and adjacent to the Panama Canal. The stock appreciated on strong pricing and volume trends and the Fund continues to hold it.

Nutritional supplement provider NBTY was acquired during the reporting period by Carlyle Group for a 47 percent premium.

Under performers | Apollo Group Inc. is a post-secondary education provider. We sold the stock out of the Fund in the second quarter after the company announced a negative court ruling that is a likely overhang on the stock.

Business advisory services company FTI Consulting, Inc. pre-announced weaker than expected results and specifically cited weakness in bankruptcy, restructuring and M&A consulting activity levels. The Fund sold the stock.

Bally Technologies Inc. produces slot machines and casino operating systems. Sentiment has turned negative for the industry as investors question the thesis that a replacement cycle of machines will occur. We continue to hold the stock in the Fund as we believe the company’s financial health is improving, it is increasing market share and expanding internationally.

Health Management Associates, Inc. operates acute care hospitals in the United States. The stock declined on concerns about decreased utilization. The Fund sold the stock.

Lincare Holdings Inc. is the leading provider of home oxygen equipment and services. Competitive bidding for oxygen-related services came in lower than expected, resulting in cuts to Medicare reimbursement of 32 percent in some areas. We believe Lincare will be able to continue to increase its market share but we sold the stock from the Fund due to uncertainty about future earnings growth given this ongoing reimbursement cutting environment.

| | |

| Performance Summary and Commentary |

| Eagle Mid Cap Stock Fund |

Meet the managers | Todd L. McCallister, Ph.D., CFA, is a Managing Director and Senior Vice President at Eagle Asset Management, Inc. (“Eagle”) and Co-Portfolio Manager of the Eagle Mid Cap Stock Fund (the “Fund”). Mr. McCallister has 23 years of investment experience and has managed the Fund since its inception. Stacey Serafini Thomas, CFA, is a Vice President at Eagle and served as Assistant Portfolio Manager to the Fund from 2000 to 2005, before being named Co-Portfolio Manager. Ms. Thomas has more than 13 years of investment experience.

Investment highlights | The Fund invests primarily in stocks of mid-capitalization companies. The portfolio managers of the Fund employ a “bottom-up” stock-selection process to identify growing, mid-cap companies that are reasonably priced. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. The portfolio managers seek to gain a comprehensive understanding of a company’s management, business plan, financials, real rate of growth and competitive threats and advantages.

This Morningstar Style Box™shows the Fund’s investment style and size of companies held in the Fund.

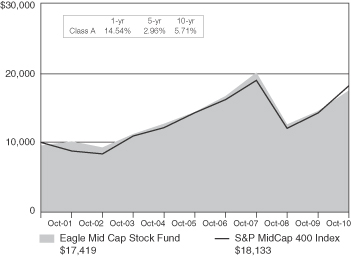

Performance summary | The Fund’s Class A shares returned 20.24% (excluding front-end sales charges) during the fiscal year ended October 31, 2010, underperforming its benchmark index, the Standard & Poor’s MidCap 400 Index (“S&P MidCap 400”) which returned 27.64%. The S&P MidCap 400, is an unmanaged index that measures the performance of the mid-sized company segment of the U.S. market. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 Investment from 11/1/00 to 10/31/10 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The information technology and materials sectors were the Fund’s largest contributors to performance during the fiscal year ended October 31, 2010. In information technology, the Fund’s holdings in information technology services, semiconductors and electronic equipment instrument industries performed well. In materials, current concerns around the health of the U.S. dollar led investors to commodities related holdings. The Fund’s chemicals, packaging, and metals stocks benefited from this. Telecommunication services and financials were the largest underperforming sectors during the reporting period. The telecommunication services sector as a whole has been hit as providers have lowered fees across the board and the competitive environment has heated up. In financials, the Fund’s commercial bank investments underperformed.

Stocks that offer what we view as safety and stability have remained out of favor in the recent markets. We find this to be anomalous, especially given the current economic weakness

| | |

| Performance Summary and Commentary |

| Eagle Mid Cap Stock Fund (cont’d) |

(as reflected by 2.5 percent 10-year Treasury rates) and the strong run that more volatile stocks experienced last year.

The Fund underperformed its benchmark index, the S&P Mid Cap 400, during the reporting period. Relative underperformance was concentrated in the financials and health care sectors. The Fund held an overweight position in the underperforming financial exchanges industry and an underweight position, coupled with underperformance, in real estate investment trusts, which worked to our disadvantage this year. Fundamentally, we still believe in the exchanges. Real estate investment trusts have continued to be overpriced in our opinion, leading to very few opportunities for us. Health care was weighed down by equipment companies underperforming and by not owning the generic pharmaceutical stocks that contributed to the benchmark. On a relative basis, the materials sector performed best. We maintained an overweight position, especially in the packaging and chemicals industries. The Fund’s holdings in materials offer large free cash flow yields, profitability and exposure to emerging markets.

Under performers | Specialty vehicle manufacturer Oshkosh Corporation has traded lower as investors have discounted post-Iraq U.S. military spending. We continue to believe investors are underestimating the sustainable level revenues from the Department of Defense. At current valuations and cash flows, we believe the market is assigning little, if any, value to its access equipment or fire and emergency-vehicle businesses. The Fund still owns the stock.

Beckman Coulter, Inc., a medical equipment manufacturer, preannounced that it would not meet its second-quarter earnings estimates and lowered its guidance. The company was hurt due to continued weakness from the recall of a diagnostic test kit and the management team has struggled with preventing that issue from hurting the overall business. As a result, the Fund sold the stock.

DISH Network Corp had problems this year as the company began to miss estimates on weak subscriber results. We sold the Fund’s position in the subscription television service provider as the quality of the subscribers became a question in the increasingly competitive market.

State Street Corporation missed earnings while the Fund held its shares. The company provides banking and financial processing services to institutions and has recognized lower

net interest revenue in this low interest rate environment. The Fund sold the shares as we expect short-term interest rates to remain low for the foreseeable future, creating a continued drag on earnings growth for the company.

Owning oil and gas exploration firm Petrohawk Energy Corporation hurt the Fund’s investment returns as the price of gas decreased during the Fund’s holding period. We sold the holding from the Fund as natural gas prices did not significantly recover.

Top Performers | Whiting Petroleum Corporation is an energy company that gives us exposure to Bakken Shale, the most potent domestic crude oil region. Its shares were up throughout the reporting period as the company continued to release good results regarding its wells and its price appreciated such that it no longer trades at a discount to its competitors. We continue to hold this company in the Fund.

Technology equipment manufacturer Marvell Technology Group, Ltd. has seen large growth in its wireless networking business. We continue to hold the stock in the Fund as we believe there is growth potential within some of the products that include new tablet computers.

IHS, Inc., a business software and service company, has been up this year after beating earnings and revenue estimates through a mixture of acquisitions and sales growth. The company also tightened its adjusted earnings forecast. The Fund continues to own the company’s shares due to its subscription based revenue and steady cash flow.

Dr. Pepper Snapple Group, Inc. was up after the beverages company reported it will enjoy a favorable renegotiation of its distribution agreements with Coca-Cola, Inc. following that company’s takeover of Coca-Cola Enterprises. This is on the heels of receiving $900 million from Pepsi for similar negotiations, of which more than $400 million was used to pay down debt. We sold the holding from the Fund after we felt that it was fully valued.

Industrial goods manufacturer Ametek Inc. had a strong year as it has seen organic growth, backlog growth, and a continuation in its free cash flow generation. Furthermore, the company has been steadily acquiring smaller companies while still keeping its balance sheet solid. We continue to hold this position in the Fund.

| | |

| Performance Summary and Commentary |

| Eagle Small Cap Core Value Fund |

Meet the managers | David M. Adams, CFA, Lead Portfolio Manager, and John “Jack” McPherson, CFA, Co-Portfolio Manager, are Managing Directors at Eagle Boston Investment Management, Inc. (“EBIM”) and have been responsible for the day-to-day management of the Eagle Small Cap Core Value Fund (the “Fund”) since its inception. Both Mr. Adams and Mr. McPherson have 20 years of investment experience.

Investment highlights | The Fund invests primarily in equity securities of small-capitalization companies. Using a value approach to investing, the Fund’s portfolio managers seek to capture capital growth by selecting securities that the portfolio managers believe are selling at a discount relative to their underlying value and then hold them until their market value reflects their intrinsic value. To assess value, a “bottom-up” method of analysis is utilized. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. Other factors that the portfolio managers may look for when selecting investments include: management with demonstrated ability and commitment to the company, above-average potential for earnings and revenue growth, low debt levels relative to total capitalization and strong industry fundamentals.

This Morningstar Style Box TM shows the Fund’s investment style and size of companies held in the Fund.

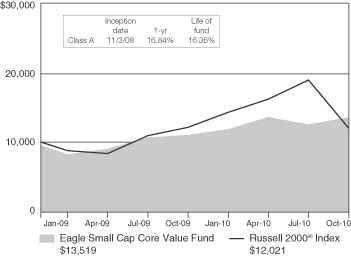

Performance summary | The Fund’s Class A shares returned 22.63% (excluding front-end sales charges) during the fiscal year ended October 31, 2010, underperforming its benchmark index, which returned 26.58%. The Fund’s benchmark index, the Russell 2000 ® Index, is an unmanaged index comprised of the 2,000 smallest companies in the Russell 3000 ® Index. The Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 Investment from 11/1/00 to 10/31/10 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | For the fiscal year ended October 31, 2010, the Fund benefited from strong absolute performance in the consumer staples, materials, telecommunication services, and information technology and consumer discretionary sectors. While the industrial, utility and financial sectors all generated positive returns for the period, they lagged the overall return for the Fund.

The performance of the Fund trailed its benchmark index during the reporting period. Relative to the benchmark, the Fund outperformed in the consumer staples, health care and materials sectors. In consumer staples, the Fund benefited from strong stock selection. In health care and materials, the Fund was underweight to the index, but strong stock selection led to outperformance. Sectors detracting from relative performance were industrials, information technology and consumer discretionary. In the industrial and consumer discretionary sectors, the Fund was underweight and underperformed. With respect to information technology holdings, an overweight position combined with underperformance from a stock selection led to relative lag to the benchmark.

| | |

| Performance Summary and Commentary |

| Eagle Small Cap Core Value Fund (cont’d) |

A key factor contributing to the Fund’s relative underperformance was the Fund’s below average exposure to higher beta areas of the market versus the Russell 2000® Index. A higher beta stock is one that has a higher degree of volatility, and thus risk, than the average stock in a market. During the reporting period, the highest beta stocks were the strongest performers, reflecting a higher tolerance for risk among investors.

The Fund’s fundamental focus on higher quality companies with below average debt combined with our value oriented investing approach generally results in below average exposure to the riskier market segments. We believe that higher quality stocks tend to outperform higher beta stocks over longer periods of time and we remain committed to focusing on the higher quality segment of the market.

Under performers | LECG Corp., a provider of consulting services to large corporations, fell 75%. While demand for the company’s services remains weak, there has been no new news released that would justify the drop. The drop appears to be a function of the stock’s limited trading liquidity combined with a motivated seller. We remain holders of the stock but continue to evaluate the situation.

1-800-FLOWERS.COM, Inc. is a gift retailer that is experiencing a difficult consumer environment for their various products given the overall state of the U.S. economy, which caused its shares to drop 53%. We believe the long-term potential for the business remains attractive and continue to hold the stock in the Fund.

Oil and gas exploration firm Comstock Resources, Inc. declined 46% as weak natural gas prices offset continued strong developments within their major production areas. The Fund continues to hold the position as we believe the company has attractive drilling sites in some of the more important natural gas producing regions of the country.

Net 1 U.E.P.S. Technologies Inc., a provider of transaction processing services to governmental agencies serving poor and unbanked populations globally, dropped 30% despite issuing a decent earnings report for the period. The market reacted negatively as the company continues to await clarity regarding the contract renewal of their largest client. We view the

uncertainty as being discounted in the share price and therefore continue to hold the position in the Fund.

SWS Group Inc., an investment banking and brokerage firm, fell 39%. Weak trading volumes in their brokerage business, a low interest rate environment and write-offs of their loan portfolio, combined with resignation of the company’s CEO, helped drive down the stock. While disappointed with the CEO’s resignation, we don’t view it as negatively impacting the original investment thesis. We continue to believe the company is positioned to benefit from a rebound in market trading activity and an eventual increase in short-term interest rates. The Fund still owns the stock.

Top performers | Herbalife Ltd., a multi-level marketer of nutritional supplements rose 90% as the company reported strong quarterly earnings growth and reiterated a strong future outlook based largely on the continued success of the rollout of their daily consumption model. We continue to hold the position in the Fund.

AMERIGROUP Corp., a provider of Medicaid managed care services to state government agencies, rose 89%. The strength of the stock appears to be a function of the strong underlying fundamentals of the business, namely increasing Medicaid enrollments nationally. We continue to hold the position in the Fund.

Sonic Solutions, a technology firm saw its shares increase dramatically (146%) during the reporting period as the company announced several new partners for its CinemaNow product, along with their strategic acquisition of DivX, which we believe continues to validate the long-term earnings potential of the company. We continue to hold the position in the Fund.

Sybase Inc., an industry leader in delivering enterprise and mobile software to manage, analyze and mobilize information was acquired by SAP and appreciated 63% during the period. The Fund no longer owns the stock as the merger was completed in July 2010.

FGX International designed and marketed products under brands such as Foster Grant. The company was acquired by a European competitor, Essilor, during the reporting period at a premium, leading to a gain of over 50%. The Fund no longer owns the stock as the merger was completed in March 2010.

| | |

| Performance Summary and Commentary |

| Eagle Small Cap Growth Fund |

Meet the managers | Bert L. Boksen, CFA, a Managing Director and Senior Vice President at Eagle Asset Management, Inc. (“Eagle”), has been responsible for the management of the Eagle Small Cap Growth Fund (the “Fund”) since 1995. Mr. Boksen has 33 years of investment experience. Eric Mintz, CFA, has 15 years of investment experience and has been Assistant Portfolio Manager since 2008.

Investment highlights | The Fund invests primarily in stocks of small-capitalization companies. Using a “bottom-up” approach, the Fund’s portfolio managers seek to capture the significant long-term capital appreciation potential of small, rapidly growing companies. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. The portfolio managers also look for small-cap growth companies that are reasonably priced. Since small-cap companies often have narrower markets than large-cap companies, the portfolio managers believe that conducting extensive proprietary research on small-cap growth companies may enable the Fund to capitalize on market inefficiencies and thus outperform the market.

This Morningstar Style Box™ shows the Fund’s investment style and size of companies held in the Fund.

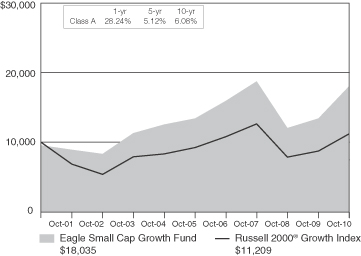

Performance summary | The Fund’s Class A shares returned 34.62% (excluding front-end sales charges) during the fiscal year ended October 31, 2010, outperforming its benchmark index, which returned 28.67%. The Fund’s benchmark index, the Russell 2000® Growth Index, is an unmanaged index comprised of Russell 2000® companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000® Index is an unmanaged index comprised of the 2,000 smallest companies in the Russell 3000® Index. The Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the

expenses associated with the active management of an actual portfolio.

Growth of a $10,000 Investment from 11/1/00 to 10/31/10 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The Fund had strong absolute performance during the one-year reporting period ended October 31, 2010. On an absolute basis, materials, consumer staples and energy led the Fund’s strong returns. In materials, the Fund’s holdings in the chemicals and metals & mining industries posted strong gains. The personal products industry fueled the consumer staples sector. In energy, the Fund’s investments in the energy equipment & services and oil, gas & consumable fuels industries had strong performance.

On an absolute basis, the financials, healthcare and industrials sectors lagged. The Fund’s investments in the financials sector posted a slightly negative return overall with the capital markets, thrifts & mortgage finance, and commercial banks industries each finishing down for the year. The healthcare sector finished positive for the year although investments in the healthcare providers & services and life science tools &

| | |

| Performance Summary and Commentary |

| Eagle Small Cap Growth Fund (cont’d) |

services industries underperformed. The construction & engineering industry posted negative returns in industrials.

The Fund outperformed its benchmark, the Russell 2000 Growth Index, during the one-year period ended October 31, 2010. The materials, energy, information technology, consumer staples and consumer discretionary sectors each contributed to the strong returns. The Fund’s overweight position in materials and energy amplified strong stock selection in those sectors. The Fund outperformed in information technology due to strong stock selection and an overweight position in the software, electronic equipment instruments & components and computers & peripherals industries. Consumer staples contributed to returns despite an underweight position due to very strong absolute performance. Consumer discretionary outperformed due to strong stock selection, particularly within the diversified consumer services industry.