UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file Number: 811-04337 |

HERITAGE CASH TRUST

|

| (Exact name of Registrant as Specified in Charter) |

|

880 Carillon Parkway St. Petersburg, FL 33716 (Address of Principal Executive Office) (Zip Code) |

Registrant’s Telephone Number, including Area Code: (727) 573-3800

RICHARD K. RIESS, PRESIDENT

880 Carillon Parkway

St. Petersburg, FL 33716

|

| (Name and Address of Agent for Service) |

Copy to:

CLIFFORD J. ALEXANDER, ESQ.

Kirkpatrick & Lockhart Nicholson Graham LLP

1601 K Street, NW

Washington, D.C. 20006-1600

Date of fiscal year end: August 31

Date of reporting period: February 28, 2006

| Item 1. | Reports to Shareholders |

Heritage

Cash

Trust

Money Market Fund

Semiannual Report

(Unaudited) and Investment Performance Review for the Six-Month Period Ended February 28, 2006

March 15, 2006

Dear Fellow Shareholders:

I am pleased to provide you with the semiannual report for the Heritage Cash Trust–Money Market Fund (the “Fund”) for the six-month period ended February 28, 2006. The Fund’s seven-day current yield(a) increased from 2.83% on August 31, 2005 to 3.78% on February 28, 2006. The increase in the yield can be attributed primarily to decisions by the Federal Reserve’s Federal Open Market Committee to raise the federal funds rate from 3.50% at the beginning of the period to 4.50%. The Committee increased the federal funds rate by 0.25% at each of the Federal Open Market Meetings that were held during the period. This performance data represents past performance and past performance does not guarantee future results. Current performance may be higher or lower than the performance data quoted. To obtain more current performance, please visit the Fund’s website at www.HeritageFunds.com.

As of February 28, 2006, approximately 56% of the Fund’s net assets were invested in commercial paper or certificates of deposit rated A-1+, the highest short-term rating classification by Standard & Poor’s Rating Group (“S&P”) while 6% of net assets were invested in short-term obligations rated A-1, the next highest rating category. Approximately 38% of the Fund’s net assets were invested in short-term obligations issued by U.S. Government Sponsored Enterprises, including Fannie Mae, Freddie Mac and Federal Home Loan Bank(b). This, along with other factors, satisfies the standards necessary to retain the Fund’s AAAm rating from S&P(c). Ratings are subject to change and do not remove market risk from your investment.

On behalf of Heritage, I thank you for your continuing investment in the Heritage Cash Trust–Money Market Fund. As always, should you have any questions, please contact your financial advisor or Heritage at (800) 421-4184.

Sincerely,

Stephen G. Hill

President

(a) An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund. Please consider the investment objectives, risks, charges, and expenses of any fund carefully before investing. Contact Heritage at (800) 421-4184 or your financial advisor for a prospectus, which contains this and other important information about the Fund. Read the prospectus carefully before you invest.

(b) U.S. Government-Sponsored Enterprises are generally private entities sponsored by Acts of Congress but they are not guaranteed by the full faith and credit of the U.S. Government.

(c) Standard & Poor’s, a widely recognized independent authority on credit quality, rates certain money market funds based on weekly analysis. When rating a money market fund, Standard & Poor’s assesses the safety of principal. According to Standard & Poor’s, a fund rated AAAm (‘‘m’’ denotes money market fund) offers excellent safety features and has superior capacity to maintain principal value and limit exposure to loss. In evaluating safety, Standard & Poor’s focuses on credit quality, liquidity, and management of the Fund.

1

Heritage Cash Trust—Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

| | | | | |

Principal

Amount

| | | | Value

|

Commercial Paper—59.7%(a)

| | | |

Domestic—29.7%

| | | |

Banks—6.3%

| | | |

| $ 50,000,000 | | Bank of America Corporation,

4.54%, 04/07/06 | | $ | 49,766,694 |

| 50,000,000 | | Bank of America Corporation,

4.57%, 04/17/06 | | | 49,701,681 |

| 50,000,000 | | Bank of America Corporation,

4.61%, 04/25/06 | | | 49,647,847 |

| 50,000,000 | | J.P. Morgan Chase & Company, Inc., 4.47%, 03/16/06 | | | 49,906,875 |

| 50,000,000 | | J.P. Morgan Chase & Company, Inc., 4.55%, 04/17/06 | | | 49,702,986 |

| 50,000,000 | | State Street Corporation,

4.36%, 03/06/06 | | | 49,969,722 |

| 50,000,000 | | State Street Corporation,

4.39%, 03/14/06 | | | 49,920,736 |

| | | | |

|

|

| | | | | | 348,616,541 |

| | | | |

|

|

Beverages—0.7%

| | | |

| 10,550,000 | | The Coca-Cola Company,

4.48%, 04/03/06 | | | 10,506,675 |

| 30,000,000 | | The Coca-Cola Company,

4.51%, 04/13/06 | | | 29,838,392 |

| | | | |

|

|

| | | | | | 40,345,067 |

| | | | |

|

|

Chemicals—0.3%

| | | |

| 13,585,000 | | E.I. du Pont de Nemours and Company, 4.45%, 03/20/06 | | | 13,553,094 |

| | | | |

|

|

Cosmetics/Personal Care—6.1%

| | | |

| 50,000,000 | | Colgate-Palmolive Company,

4.47%, 03/09/06 | | | 49,950,333 |

| 37,100,000 | | Colgate-Palmolive Company,

4.46%, 03/13/06 | | | 37,044,845 |

| 50,000,000 | | Kimberly-Clark Worldwide,

4.36%, 03/01/06 | | | 50,000,000 |

| 50,000,000 | | Kimberly-Clark Worldwide,

4.49%, 04/06/06 | | | 49,775,500 |

| 50,000,000 | | The Procter & Gamble Company, 4.47%, 03/17/06 | | | 49,900,667 |

| | | | |

Principal

Amount

| | | | Value

|

Commercial Paper (continued)

| | |

| 82,420,000 | | The Procter & Gamble Company, 4.47%, 03/22/06 | | 82,205,090 |

| 17,580,000 | | The Procter & Gamble Company, 4.47%, 03/24/06 | | 17,529,794 |

| | | | |

|

| | | | | 336,406,229 |

| | | | |

|

Diversified Manufacturer—2.9%

| | |

| 10,000,000 | | 3M Company, 4.40%, 03/23/06 | | 9,973,111 |

| 40,000,000 | | General Electric Company,

4.48%, 03/06/06 | | 39,975,111 |

| 110,000,000 | | General Electric Company,

4.38%, 03/07/06 | | 109,919,700 |

| | | | |

|

| | | | | 159,867,922 |

| | | | |

|

Financial Services—2.7%

| | |

| 50,000,000 | | Citigroup Funding Inc.,

4.40%, 03/02/06 | | 49,993,889 |

| 50,000,000 | | Citigroup Funding Inc.,

4.45%, 03/02/06 | | 49,993,819 |

| 50,000,000 | | Citigroup Funding Inc.,

4.42%, 03/21/06 | | 49,877,222 |

| | | | |

|

| | | | | 149,864,930 |

| | | | |

|

Office/Business Equipment—1.8%

| | |

| 30,370,000 | | Pitney Bowes, Inc.,

4.45%, 03/06/06 | | 30,351,230 |

| 50,000,000 | | Pitney Bowes, Inc.,

4.46%, 03/20/06 | | 49,882,306 |

| 19,630,000 | | Pitney Bowes, Inc.,

4.47%, 03/27/06 | | 19,566,628 |

| | | | |

|

| | | | | 99,800,164 |

| | | | |

|

Oil & Gas—5.5%

| | |

| 50,000,000 | | ChevronTexaco Funding Corporation, 4.47%, 04/03/06 | | 49,795,125 |

| 50,000,000 | | ChevronTexaco Funding Corporation, 4.49%, 04/11/06 | | 49,744,319 |

| 50,000,000 | | ChevronTexaco Funding Corporation, 4.50%, 04/13/06 | | 49,731,250 |

| 65,000,000 | | Shell International Finance BV,

4.31%, 03/03/06 | | 64,984,436 |

| 37,846,000 | | Shell International Finance BV,

4.52%, 04/05/06 | | 37,679,688 |

The accompanying notes are an integral part of the financial statements.

Heritage Cash Trust—Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | |

Principal

Amount

| | | | Value

|

Commercial Paper (continued)

| | | |

| $ 47,154,000 | | Shell International Finance BV,

4.52%, 04/10/06 | | $ | 46,917,182 |

| | | | |

|

|

| | | | | | 298,852,000 |

| | | | |

|

|

Pharmaceuticals—1.1%

| | | |

| 21,065,000 | | Pfizer Investment Capital Ltd.,

4.47%, 03/24/06 | | | 21,004,842 |

| 41,100,000 | | Pfizer Investment Capital Ltd.,

4.54%, 04/21/06 | | | 40,835,950 |

| | | | |

|

|

| | | | | | 61,840,792 |

| | | | |

|

|

Retail—2.3%

| | | |

| 50,000,000 | | Wal-Mart Stores Inc.,

4.37%, 03/07/06 | | | 49,963,583 |

| 50,000,000 | | Wal-Mart Stores Inc.,

4.32%, 03/14/06 | | | 49,922,000 |

| 25,000,000 | | Wal-Mart Stores Inc.,

4.36%, 03/21/06 | | | 24,939,444 |

| | | | |

|

|

| | | | | | 124,825,027 |

| | | | |

|

|

| Total Domestic (cost $1,633,971,766) | | | 1,633,971,766 |

| | | | |

|

|

Foreign—30.0%(b)

| | | |

Banks—16.3%

| | | |

| 50,000,000 | | ABN AMRO North America Finance Inc., 4.36%, 03/10/06 | | | 49,945,500 |

| 50,000,000 | | ABN AMRO North America Finance Inc., 4.41%, 03/13/06 | | | 49,926,500 |

| 50,000,000 | | Barclays U.S. Funding Corporation, 4.46%, 03/20/06 | | | 49,882,438 |

| 50,000,000 | | Barclays U.S. Funding Corporation, 4.49%, 03/27/06 | | | 49,837,861 |

| 25,000,000 | | Danske Corporation,

4.50%, 03/08/06 | | | 24,978,149 |

| 25,000,000 | | Danske Corporation,

4.50%, 03/13/06 | | | 24,962,542 |

| 50,000,000 | | Danske Corporation,

4.59%, 04/24/06 | | | 49,655,750 |

| 60,000,000 | | Deutsche Bank Financial Inc.,

4.36%, 03/03/06 | | | 59,985,467 |

| 40,000,000 | | Deutsche Bank Financial Inc.,

4.43%, 03/17/06 | | | 39,921,333 |

| | | | |

Principal

Amount

| | | | Value

|

Commercial Paper (continued)

| | |

| 50,000,000 | | HBOS Treasury Services PLC,

4.53%, 04/07/06 | | 49,767,208 |

| 50,000,000 | | HBOS Treasury Services PLC,

4.54%, 04/07/06 | | 49,766,951 |

| 32,900,000 | | KFW International Finance,

4.45%, 03/03/06 | | 32,891,866 |

| 17,100,000 | | KFW International Finance,

4.40%, 03/15/06 | | 17,070,740 |

| 40,000,000 | | KFW International Finance,

4.52%, 04/13/06 | | 39,784,044 |

| 10,000,000 | | KFW International Finance,

4.53%, 04/17/06 | | 9,940,858 |

| 100,000,000 | | Rabobank USA Financial Corporation, 4.55%, 03/01/06 | | 100,000,000 |

| 50,000,000 | | Royal Bank of Scotland,

4.40%, 03/09/06 | | 49,951,167 |

| 50,000,000 | | Royal Bank of Scotland,

4.54%, 04/10/06 | | 49,748,056 |

| 50,000,000 | | UBS Finance Delaware, LLC,

4.50%, 03/23/06 | | 49,862,500 |

| 50,000,000 | | UBS Finance Delaware, LLC,

4.58%, 04/18/06 | | 49,694,667 |

| | | | |

|

| | | | | 897,573,597 |

| | | | |

|

Financial Services—4.5%

| | |

| 50,000,000 | | Siemens Capital Corporation,

4.50%, 03/29/06 | | 49,825,000 |

| 44,950,000 | | Siemens Capital Corporation,

4.50%, 03/31/06 | | 44,781,438 |

| 50,000,000 | | Toyota Motor Credit Corporation,

4.44%, 03/24/06 | | 49,858,167 |

| 40,000,000 | | Toyota Motor Credit Corporation,

4.50%, 03/31/06 | | 39,850,000 |

| 60,000,000 | | Toyota Motor Credit Corporation,

4.51%, 04/05/06 | | 59,736,917 |

| | | | |

|

| | | | | 244,051,522 |

| | | | |

|

Food—4.2%

| | |

| 34,100,000 | | Nestle Capital Corporation,

4.45%, 03/06/06 | | 34,078,924 |

| 50,000,000 | | Nestle Capital Corporation,

4.48%, 04/03/06 | | 49,794,667 |

The accompanying notes are an integral part of the financial statements.

Heritage Cash Trust—Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | |

Principal

Amount

| | | | Value

|

Commercial Paper (continued)

| | | |

| $ 29,700,000 | | Nestle Capital Corporation,

4.53%, 04/17/06 | | $ | 29,524,349 |

| 36,200,000 | | Nestle Capital Corporation,

4.54%, 04/18/06 | | | 35,981,111 |

| 20,000,000 | | Unilever Capital Corporation,

4.47%, 03/21/06 | | | 19,950,333 |

| 12,200,000 | | Unilever Capital Corporation,

4.46%, 03/23/06 | | | 12,166,748 |

| 10,000,000 | | Unilever Capital Corporation,

4.47%, 03/24/06 | | | 9,971,442 |

| 40,000,000 | | Unilever Capital Corporation,

4.47%, 03/27/06 | | | 39,870,867 |

| | | | |

|

|

| | | | | | 231,338,441 |

| | | | |

|

|

Pharmaceuticals—2.7%

| | | |

| 45,000,000 | | GlaxoSmithKline Finance PLC,

4.48%, 03/30/06 | | | 44,837,600 |

| 15,000,000 | | GlaxoSmithKline Finance PLC,

4.49%, 03/30/06 | | | 14,945,746 |

| 90,000,000 | | GlaxoSmithKline Finance PLC,

4.53%, 04/19/06 | | | 89,445,075 |

| | | | |

|

|

| | | | | | 149,228,421 |

| | | | |

|

|

Regional Agencies—2.3%

| | | |

| 10,000,000 | | The Canadian Wheat Board,

4.29%, 03/06/06 | | | 9,994,042 |

| 15,000,000 | | The Canadian Wheat Board,

4.29%, 03/07/06 | | | 14,989,275 |

| 30,000,000 | | The Canadian Wheat Board,

4.45%, 04/05/06 | | | 29,870,208 |

| 35,000,000 | | The Canadian Wheat Board,

4.51%, 04/20/06 | | | 34,781,007 |

| 35,000,000 | | The Canadian Wheat Board,

4.51%, 04/24/06 | | | 34,763,225 |

| | | | |

|

|

| | | | | | 124,397,757 |

| | | | |

|

|

| Total Foreign (cost $1,646,589,738) | | | 1,646,589,738 |

| | | | |

|

|

| Total Commercial Paper (cost $3,280,561,504) | | | 3,280,561,504 |

| | | | |

|

|

| | | | |

Principal

Amount

| | | | Value

|

U.S. Government-Sponsored Enterprises—38.5%(a)

|

| 45,000,000 | | Fannie Mae, 4.26%, 03/01/06 | | 45,000,000 |

| 50,000,000 | | Fannie Mae, 4.33%, 03/09/06 | | 49,951,889 |

| 49,875,000 | | Fannie Mae, 4.26%, 03/22/06 | | 49,751,119 |

| 19,944,000 | | Fannie Mae, 4.28%, 03/22/06 | | 19,894,206 |

| 40,000,000 | | Fannie Mae, 4.42%, 03/29/06 | | 39,862,489 |

| 98,000,000 | | Fannie Mae, 4.33%, 04/05/06 | | 97,587,447 |

| 100,000,000 | | Fannie Mae, 4.34%, 04/05/06 | | 99,578,056 |

| 49,500,000 | | Fannie Mae, 4.35%, 04/05/06 | | 49,290,897 |

| 85,000,000 | | Fannie Mae, 4.48%, 04/12/06 | | 84,555,693 |

| 50,000,000 | | Fannie Mae, 4.49%, 05/03/06 | | 49,607,125 |

| 27,085,000 | | Fannie Mae, 4.50%, 05/03/06 | | 26,871,706 |

| 50,000,000 | | Federal Home Loan Bank,

4.25%, 03/08/06 | | 49,958,681 |

| 35,000,000 | | Federal Home Loan Bank,

4.26%, 03/08/06 | | 34,971,008 |

| 50,000,000 | | Federal Home Loan Bank,

4.28%, 03/10/06 | | 49,946,500 |

| 40,000,000 | | Federal Home Loan Bank,

4.33%, 03/15/06 | | 39,932,644 |

| 20,000,000 | | Federal Home Loan Bank,

4.32%, 03/17/06 | | 19,961,600 |

| 50,000,000 | | Federal Home Loan Bank,

4.35%, 03/24/06 | | 49,861,042 |

| 40,000,000 | | Federal Home Loan Bank,

4.30%, 03/31/06 | | 39,856,667 |

| 36,333,000 | | Federal Home Loan Bank,

4.45%, 04/12/06 | | 36,144,371 |

| 135,000,000 | | Federal Home Loan Bank,

4.49%, 04/19/06 | | 134,174,962 |

| 50,000,000 | | Federal Home Loan Bank,

4.52%, 04/26/06 | | 49,648,444 |

| 20,000,000 | | Federal Home Loan Bank,

4.52%, 04/28/06 | | 19,854,356 |

| 50,000,000 | | Federal Home Loan Bank,

4.49%, 05/03/06 | | 49,607,125 |

| 50,000,000 | | Federal Home Loan Bank,

4.50%, 05/05/06 | | 49,593,750 |

| 100,000,000 | | Federal Home Loan Bank,

4.52%, 05/12/06 | | 99,097,000 |

| 68,000,000 | | Freddie Mac, 4.25%, 03/07/06 | | 67,951,890 |

| 44,000,000 | | Freddie Mac, 4.34%, 03/10/06 | | 43,952,260 |

The accompanying notes are an integral part of the financial statements.

Heritage Cash Trust—Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | | |

Principal

Amount

| | | | Value

| |

U.S. Government-Sponsored Enterprises (continued)

|

|

| $ 38,733,000 | | Freddie Mac, 4.26%, 03/13/06 | | $ | 38,677,960 | |

| 37,982,000 | | Freddie Mac, 4.27%, 03/14/06 | | | 37,923,434 | |

| 50,000,000 | | Freddie Mac, 4.42%, 03/27/06 | | | 49,840,389 | |

| 84,000,000 | | Freddie Mac, 4.31%, 03/28/06 | | | 83,728,470 | |

| 100,000,000 | | Freddie Mac, 4.33%, 04/04/06 | | | 99,591,056 | |

| 28,900,000 | | Freddie Mac, 4.45%, 04/18/06 | | | 28,728,527 | |

| 110,000,000 | | Freddie Mac, 4.49%, 05/02/06 | | | 109,149,394 | |

| 50,000,000 | | Freddie Mac, 4.51%, 05/08/06 | | | 49,574,055 | |

| 120,000,000 | | Freddie Mac, 4.52%, 05/09/06 | | | 118,961,070 | |

| 25,000,000 | | Freddie Mac Note, 4.76%, 02/09/07 (callable quarterly) | | | 25,000,000 | |

| 25,000,000 | | Freddie Mac Note, 4.92%, 02/28/07 (callable 8/1/06) | | | 25,000,000 | |

| | | | |

|

|

|

Total U.S. Government-Sponsored Enterprises

(cost $2,112,637,282) | | | 2,112,637,282 | |

| | | | |

|

|

|

Certificates of Deposit—1.8%(a)

| | | | |

| 50,000,000 | | Wells Fargo & Company,

4.50%, 03/23/06 | | | 50,000,000 | |

| 50,000,000 | | Wells Fargo & Company,

4.52%, 03/30/06 | | | 50,000,000 | |

| | | | |

|

|

|

Total Certificates of Deposit

(cost $100,000,000) | | | 100,000,000 | |

| | | | |

|

|

|

Total Investment Portfolio excluding repurchase

agreement (cost $5,493,198,786) | | | 5,493,198,786 | |

| | | | |

|

|

|

Repurchase Agreement—0.2%(a)

| | | | |

Repurchase Agreement with State Street Bank and

Trust Company, dated February 28, 2006 @ 4.40%

to be repurchased at $10,881,330 on March 1,

2006, collateralized by $10,935,000 United States

Treasury Notes, 4.750% due November 15, 2008,

(market value $11,106,161 including interest)

(cost $10,880,000) | | | 10,880,000 | |

| | |

|

|

|

Total Investment Portfolio

(cost $5,504,078,786)(c), 100.2%(a) | | | 5,504,078,786 | |

| Other Assets and Liabilities, net, (0.2%)(a) | | | (9,646,528 | ) |

| | |

|

|

|

Net Assets, (consisting of paid-in-capital net of

accumulated net realized loss of $3,174),

100.0% | | | $5,494,432,258 | |

| | |

|

|

|

| | | | |

Class A Shares

| | |

Net asset value, offering and redemption price per share,

($5,490,103,677 divided by 5,490,107,086 shares

outstanding) | | $1.00 |

| | |

|

Class B Shares

| | |

Net asset value, offering and redemption price per share,

($2,068,119 divided by 2,067,946 shares outstanding) | | $1.00 |

| | |

|

Class C Shares

| | |

Net asset value, offering and redemption price per share,

($2,260,462 divided by 2,260,400 shares outstanding) . | | $1.00 |

| | |

|

| (a) | Percentages indicated are based on net assets. |

| (b) | U.S. dollar denominated. |

| (c) | The aggregate identified cost for federal income tax purposes is the same. |

Maturity Schedule(*)

February 28, 2006 (% of total investments)

| | | |

1-7 Days | | 15.8 | % |

8-14 Days | | 12.5 | % |

15-30 Days | | 23.4 | % |

31-60 Days | | 37.3 | % |

61-90 Days | | 10.1 | % |

91-397 Days | | 0.9 | % |

| | |

|

|

Total | | 100.0 | % |

| | |

|

|

| | (*) | The number of days to maturity of each holding is determined in accordance with the provisions of Rule 2a-7 under the Investment Company Act of 1940. |

The accompanying notes are an integral part of the financial statements.

Heritage Cash Trust—Money Market Fund

Understanding Your Fund’s Expenses

(unaudited)

Understanding Your Fund’s Expenses

As a mutual fund investor, you pay two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; and exchange fees; and (2) ongoing costs, such as management fees; distribution (12b-1) fees; and other expenses. Using the tables below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect one-time transaction expenses, such as sales charges (loads) and redemption fees. Therefore, if these transactional costs were included, your costs would have been higher. For more information, see your Fund’s prospectus or contact your financial advisor.

Review Your Fund’s Actual Expenses

The table below shows the actual expenses you would have paid on a $1,000 investment in Heritage Cash Trust—Money Market Fund on September 1, 2005 and held through February 28, 2006. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns after ongoing expenses. This table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

| | | | | | | | | |

Actual

| | Beginning

Account Value September 1, 2005

| | Ending

Account Value February 28, 2006

| | Expenses Paid

During Period*

|

Class A | | $ | 1,000.00 | | $ | 1,016.73 | | $ | 3.65 |

Class B | | $ | 1,000.00 | | $ | 1,016.73 | | $ | 3.65 |

Class C | | $ | 1,000.00 | | $ | 1,016.73 | | $ | 3.65 |

Hypothetical Example for Comparison Purposes

All mutual funds now follow guidelines to assist shareholders in comparing expenses between different funds. Per these guidelines, the table below shows your Fund’s expenses based on a $1,000 investment and assuming for the period a hypothetical 5% rate of return before ongoing expenses, which is not the Fund’s actual return. Please note that you should not use this information to estimate your actual ending account balance and expenses paid during the period. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the Fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison.

| | | | | | | | | |

Hypothetical (5% return before expenses)

| | Beginning

Account Value September 1, 2005

| | Ending

Account Value February 28, 2006

| | Expenses Paid

During Period*

|

Class A | | $ | 1,000.00 | | $ | 1,021.17 | | $ | 3.66 |

Class B | | $ | 1,000.00 | | $ | 1,021.17 | | $ | 3.66 |

Class C | | $ | 1,000.00 | | $ | 1,021.17 | | $ | 3.66 |

| | * | Expenses are calculated using the Fund’s annualized expense ratio of 0.73% for Class A, Class B and Class C shares, multiplied by the average account value for the period, then multiplying the result by the actual number of days in the period (181); and then dividing that result by the actual number of days in the fiscal year (365). |

The accompanying notes are an integral part of the financial statements.

6

Heritage Cash Trust—Money Market Fund

Statement of Operations

For the Six-Month Period Ended February 28, 2006

(unaudited)

| | | | | | |

Investment Income: | | | | | | |

Income: | | | | | | |

Interest | | | | | $ | 105,338,777 |

Expenses: | | | | | | |

Management fee | | $ | 10,574,843 | | | |

Distribution fee (Class A) | | | 3,859,996 | | | |

Distribution fee (Class B) | | | 1,929 | | | |

Distribution fee (Class C) | | | 1,880 | | | |

Shareholder servicing fees | | | 3,778,593 | | | |

Registration fees and expenses | | | 140,053 | | | |

Custodian fee | | | 133,380 | | | |

Reports to shareholders | | | 130,345 | | | |

Federal registration expense | | | 56,663 | | | |

Professional fees | | | 46,377 | | | |

Fund accounting fee | | | 42,414 | | | |

Insurance | | | 37,051 | | | |

Trustees’ fees and expenses | | | 11,701 | | | |

Other | | | 5,920 | | | |

| | |

|

| | | |

Total expenses | | | | | | 18,821,145 |

| | | | | |

|

|

Net investment income from operations | | | | | $ | 86,517,632 |

| | | | | |

|

|

Statements of Changes in Net Assets

| | | | | | | | |

| | | For the Six-Month

Period Ended

February 28, 2006

(unaudited)

| | | For the Fiscal

Year Ended

August 31, 2005

| |

Increase (decrease) in net assets: | | | | | | | | |

Operations: | | | | | | | | |

Net investment income from operations | | $ | 86,517,632 | | | $ | 92,701,142 | |

Distributions to shareholders from: | | | | | | | | |

Net investment income Class A shares, ($0.017 and $0.018 per share, respectively) | | | (86,432,882 | ) | | | (92,594,036 | ) |

Net investment income Class B shares, ($0.017 and $0.018 per share, respectively) | | | (42,861 | ) | | | (55,852 | ) |

Net investment income Class C shares, ($0.017 and $0.018 per share, respectively) | | | (41,889 | ) | | | (51,254 | ) |

| | |

|

|

| |

|

|

|

Net distributions to shareholders | | | (86,517,632 | ) | | | (92,701,142 | ) |

Increase (decrease) in net assets from Fund share transactions | | | 529,561,808 | | | | (145,906,301 | ) |

| | |

|

|

| |

|

|

|

Increase (decrease) in net assets | | | 529,561,808 | | | | (145,906,301 | ) |

Net assets, beginning of period | | | 4,964,870,450 | | | | 5,110,776,751 | |

| | |

|

|

| |

|

|

|

Net assets, end of period | | $ | 5,494,432,258 | | | $ | 4,964,870,450 | |

| | |

|

|

| |

|

|

|

The accompanying notes are an integral part of the financial statements.

Heritage Cash Trust—Money Market Fund

Financial Highlights

The following table includes selected data for a share outstanding throughout each period and other performance information derived from the financial statements.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class A Shares

| |

| | | For the Six-

Month Period

Ended February 28,

2006 (unaudited)

| | | For the Fiscal Years Ended August 31

| |

| | | | 2005

| | | 2004

| | | 2003

| | | 2002

| | | 2001

| |

Net asset value, beginning of period | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (a) | | | 0.017 | | | | 0.018 | | | | 0.004 | | | | 0.007 | | | | 0.015 | | | | 0.048 | |

Less Distributions: | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income and net realized gains (a) | | | (0.017 | ) | | | (0.018 | ) | | | (0.004 | ) | | | (0.007 | ) | | | (0.015 | ) | | | (0.048 | ) |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Net asset value, end of period | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total Return (%) | | | 1.67 | (b) | | | 1.84 | | | | 0.42 | | | | 0.66 | | | | 1.53 | | | | 4.87 | |

Ratios (%)/ Supplemental Data: | | | | | | | | | | | | | | | | | | | | | | | | |

Operating expenses, net, to average daily net assets | | | 0.73 | (c) | | | 0.71 | | | | 0.70 | | | | 0.70 | | | | 0.70 | | | | 0.72 | |

Net investment income to average daily net assets | | | 3.36 | (c) | | | 1.82 | | | | 0.42 | | | | 0.65 | | | | 1.51 | | | | 4.69 | |

Net assets, end of period ($ millions) | | | 5,490 | | | | 4,960 | | | | 5,103 | | | | 5,479 | | | | 5,106 | | | | 4,757 | |

| (a) | Includes net realized gains and losses which were less than $.001 per share for each of the periods. |

The accompanying notes are an integral part of the financial statements.

Heritage Cash Trust—Money Market Fund

Financial Highlights

(continued)

The following table includes selected data for a share outstanding throughout each period and other performance information derived from the financial statements.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class B Shares

| | | Class C Shares

| |

| | | For the Six-

Month Period

Ended February 28,

2006 (unaudited)

| | | For the Fiscal Years Ended August 31

| | | For the Six-

Month Period

Ended February 28,

2006 (unaudited)

| | | For the Fiscal Years Ended August 31

| |

| | | | 2005

| | | 2004

| | | 2003

| | | 2002

| | | 2001

| | | | 2005

| | | 2004

| | | 2003

| | | 2002

| | | 2001

| |

Net asset value, beginning of period | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (a) | | | 0.017 | | | | 0.018 | | | | 0.004 | | | | 0.007 | | | | 0.015 | | | | 0.048 | | | | 0.017 | | | | 0.018 | | | | 0.004 | | | | 0.007 | | | | 0.015 | | | | 0.048 | |

Less Distributions: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income and net realized gains (a) | | | (0.017 | ) | | | (0.018 | ) | | | (0.004 | ) | | | (0.007 | ) | | | (0.015 | ) | | | (0.048 | ) | | | (0.017 | ) | | | (0.018 | ) | | | (0.004 | ) | | | (0.007 | ) | | | (0.015 | ) | | | (0.048 | ) |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Net asset value, end of period | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | | | $ | 1.00 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total Return (%) | | | 1.67 | (b) | | | 1.84 | | | | 0.42 | | | | 0.66 | | | | 1.53 | | | | 4.87 | | | | 1.67 | (b) | | | 1.84 | | | | 0.42 | | | | 0.66 | | | | 1.53 | | | | 4.87 | |

Ratios (%)/ Supplemental Data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating expenses, net, to average daily net assets | | | 0.73 | (c) | | | 0.71 | | | | 0.70 | | | | 0.70 | | | | 0.70 | | | | 0.72 | | | | 0.73 | (c) | | | 0.71 | | | | 0.70 | | | | 0.70 | | | | 0.70 | | | | 0.72 | |

Net investment income to average daily net assets | | | 3.33 | (c) | | | 1.77 | | | | 0.42 | | | | 0.67 | | | | 1.52 | | | | 4.40 | | | | 3.34 | (c) | | | 1.76 | | | | 0.42 | | | | 0.67 | | | | 1.47 | | | | 4.63 | |

Net assets, end of period ($ millions) | | | 2 | | | | 3 | | | | 4 | | | | 5 | | | | 6 | | | | 4 | | | | 2 | | | | 2 | | | | 4 | | | | 6 | | | | 6 | | | | 2 | |

| (a) | Includes net realized gains and losses which were less than $.001 per share for each of the periods. |

The accompanying notes are an integral part of the financial statements.

Heritage Cash Trust—Money Market Fund

Notes to Financial Statements

(unaudited)

| Note 1: | Significant Accounting Policies. Heritage Cash Trust (the “Trust”) is organized as a Massachusetts business trust and is registered under the Investment Company Act of 1940, as amended, as a diversified, open-end management investment company consisting of two separate investment portfolios, the Money Market Fund (the “Fund”) and the Municipal Money Market Fund. The Fund seeks to achieve maximum current income consistent with stability of principal. The Fund currently offers Class A and Class C shares. Effective February 1, 2004, Class B shares were not available for direct purchase. Class B shares will continue to be available through exchanges and dividend reinvestments as described in the Fund’s prospectus. Class A, B and C shares have no front end sales charges, but when redeemed, may be subject to a contingent deferred sales charge (CDSC) if they were acquired through an exchange from another Heritage mutual fund. The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts and disclosures. Actual results could differ from those estimates. The following is a summary of significant accounting policies: |

Security Valuation: The Fund uses the amortized cost method of security valuation (as set forth in Rule 2a-7 under the Investment Company Act of 1940, as amended). The amortized cost of an instrument is determined by valuing it at cost at the time of purchase and thereafter accreting/amortizing any purchase discount/premium at a constant rate until maturity.

Repurchase Agreements: The Fund enters into repurchase agreements whereby the Fund, through its custodian, receives delivery of the underlying securities, the market value of which at the time of purchase is required to be in an amount of at least 100% of the resale price. Repurchase agreements involve the risk that the seller will fail to repurchase the security, as agreed. In that case, the Fund will bear the risk of market value fluctuations until the security can be sold and may encounter delays and incur costs in liquidating the security. In the event of bankruptcy or insolvency of the seller, delays and costs may be incurred.

Federal Income Taxes: The Fund is treated as a single corporate taxpayer as provided for in the Tax Reform Act of 1986, as amended. The Fund’s policy is to comply with the requirements of the Internal Revenue Code of 1986, as amended, which are applicable to regulated investment companies and to distribute substantially all of its taxable income to its shareholders. Accordingly, no provision has been made for federal income and excise taxes.

Distribution of Income and Gains: Distributions of net investment income and net realized gains available for distribution are declared daily and paid monthly. The Fund uses the identified cost method for determining realized gain or loss on investments for both financial and federal income tax reporting purposes.

Expenses: The Fund is charged for those expenses that are directly attributable to it, while other expenses are allocated proportionately among the Heritage mutual funds based upon methods approved by the Board of Trustees. Expenses that are directly attributable to a specific class of shares, such as distribution fees, are charged directly to that class. Other expenses of the Fund are allocated to each class of shares based upon their relative percentage of net assets.

Heritage Cash Trust—Money Market Fund

Notes to Financial Statements

(unaudited)

(continued)

Other: Investment security transactions are accounted for on a trade date basis. Interest income is recorded on the accrual basis.

In the normal course of business the Fund enters into contracts that contain a variety of representations and warranties, which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund and/or its affiliates that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

| Note 2: | Fund Shares. At February 28, 2006, there was an unlimited number of shares of beneficial interest of no par value authorized. |

Transactions in Class A, B and C shares and dollars of the Fund during the six-month period ended February 28, 2006 at a net asset value of $1.00 per share, were as follows:

| | | | | | | | | |

| | | Class A

| | | Class B

| | | Class C

| |

Shares sold/exchanged | | 11,055,377,422 | | | 412,309 | | | 1,406,195 | |

Shares issued on reinvestment of distributions | | 85,827,614 | | | 32,571 | | | 40,418 | |

Shares redeemed | | (10,611,002,474 | ) | | (1,009,574 | ) | | (1,522,673 | ) |

| | |

|

| |

|

| |

|

|

Net increase (decrease) | | 530,202,562 | | | (564,694 | ) | | (76,060 | ) |

Shares outstanding: | | | | | | | | | |

Beginning of period | | 4,959,904,524 | | | 2,632,640 | | | 2,336,460 | |

| | |

|

| |

|

| |

|

|

End of period | | 5,490,107,086 | | | 2,067,946 | | | 2,260,400 | |

| | |

|

| |

|

| |

|

|

Transactions in Class A, B and C shares and dollars of the Fund during the fiscal year ended August 31, 2005 at a net asset value of $1.00 per share, were as follows:

| | | | | | | | | |

| | | Class A

| | | Class B

| | | Class C

| |

Shares sold/exchanged | | 20,203,620,611 | | | 666,616 | | | 3,000,006 | |

Shares issued on reinvestment of distributions | | 90,789,522 | | | 40,688 | | | 45,966 | |

Shares redeemed | | (20,437,276,545 | ) | | (1,932,484 | ) | | (4,860,681 | ) |

| | |

|

| |

|

| |

|

|

Net decrease | | (142,866,412 | ) | | (1,225,180 | ) | | (1,814,709 | ) |

Shares outstanding: | | | | | | | | | |

Beginning of fiscal year | | 5,102,770,936 | | | 3,857,820 | | | 4,151,169 | |

| | |

|

| |

|

| |

|

|

End of fiscal year | | 4,959,904,524 | | | 2,632,640 | | | 2,336,460 | |

| | |

|

| |

|

| |

|

|

Heritage Cash Trust—Money Market Fund

Notes to Financial Statements

(unaudited)

(continued)

| Note 3: | Management, Distribution, Shareholder Servicing Agent, Fund Accounting and Trustees’ Fees. Under the Trust’s Investment Advisory and Administration Agreement with Heritage Asset Management, Inc. (the “Manager” or “Heritage”), Heritage manages, supervises and conducts the business and administrative affairs of the Fund. For these services, the Fund agreed to pay to the Manager an annual fee as a percentage of the Fund’s average daily net assets, computed daily based on the schedule below and payable monthly. The amount payable to the Manager as of February 28, 2006, was $1,736,842. |

| | | |

Fund’s Average

Daily Net Assets

| | Management

Fee Rate

| |

First $500 million | | 0.500 | % |

Next $500 million | | 0.475 | % |

Next $500 million | | 0.450 | % |

Next $500 million | | 0.425 | % |

Next $500 million | | 0.400 | % |

Next $2.5 billion | | 0.375 | % |

Next $2.5 billion | | 0.360 | % |

Next $2.5 billion | | 0.350 | % |

Greater than $10 billion | | 0.340 | % |

Pursuant to a plan adopted in accordance with Rule 12b-1 under the Investment Company Act of 1940, as amended, the Fund is authorized to pay Raymond James & Associates, Inc. (the “Distributor” or “RJA”) a fee of 0.15% of the average daily net assets. Such fee is accrued daily and payable monthly. The amount payable to the Distributor as of February 28, 2006 was $629,837. The Manager, Distributor, Fund Accountant and Shareholder Servicing Agent are all wholly-owned subsidiaries of Raymond James Financial, Inc. (“RJF”).

The Distributor has advised the Fund that it generated $30,283 and $1,246 in contingent deferred sales charges for Class B and Class C shares, respectively during the six-month period ended February 28, 2006. From these fees, the Distributor paid sales commissions to sales persons and incurred other distribution costs.

The Manager is also the Shareholder Servicing Agent and Fund Accountant for the Fund. The Manager charged $3,778,593 for Shareholder Servicing fees and $42,414 for Fund Accounting services, of which $1,205,770 and $8,200 were payable as of February 28, 2006, respectively. For providing Shareholder Servicing, the Manager receives payment from the Fund at a fixed fee per account plus any out-of-pocket expenses. For providing Fund Accounting Services, the Manager receives payment from the Fund at a fixed fee per fund, a fixed fee per class and any out-of-pocket expenses.

Heritage Cash Trust—Money Market Fund

Notes to Financial Statements

(unaudited)

(continued)

Trustees of the Trust also serve as Trustees for Heritage Capital Appreciation Trust, Heritage Growth and Income Trust, Heritage Income Trust and Heritage Series Trust, all of which are investment companies that are also advised by the Manager of the Trust (collectively referred to as the “Heritage Mutual Funds”). Each Trustee of the Heritage Mutual Funds who is not an employee of the Manager or employee of an affiliate of the Manager receives an annual fee of $23,000 and an additional fee of $3,000 for each combined quarterly meeting of the Heritage Mutual Funds attended. In addition, each independent Trustee that serves on the Audit Committee or Compliance Committee will receive $1,000 for attendance at their respective meeting (in person or telephonic). In addition to meeting fees, the Lead Independent Trustee will receive an annual retainer of $2,500, the Compliance Committee Chair will receive an annual retainer of $3,000, and the Audit Committee Chair will receive an annual retainer of $3,500. Trustees’ fees and expenses are paid equally by each portfolio in the Heritage Mutual Funds.

| Note 4: | Federal Income Taxes. The timing and character of certain income and capital gain distributions are determined in accordance with income tax regulations, which may differ from accounting principles generally accepted in the United States of America. As a result, net investment income (loss) and net realized gain (loss) from investment transactions for a reporting period may differ from distributions during such period. These book/tax differences may be temporary or permanent in nature. To the extent these differences are permanent, they are charged or credited to paid in capital or accumulated net realized gain (loss), as appropriate, in the period that the differences arise. Results of operations and net assets are not affected by these reclassifications. For the fiscal year ended August 31, 2005, there were no reclassifications arising from permanent tax differences. As of August 31, 2005, the Fund had net tax basis capital loss carryforwards in the aggregate of $3,174. This capital loss carryforward may be applied to any net taxable capital gain until the expiration date of 2012. All dividends paid by the Fund from net investment income are deemed to be ordinary income for Federal income tax purposes. |

Heritage Cash Trust—Money Market Fund

Additional Information

(unaudited)

Beginning with the Fund’s fiscal quarter ended November 30, 2004, the Fund began filing its complete schedule of portfolio holdings with the Securities Exchange Commission (“SEC”) for the first and third quarters of each fiscal year on Form N-Q; the Fund’s Form N-Q filings are available on the SEC’s website at www.sec.gov; and the Fund’s Form N-Q filings may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

Heritage

Cash

Trust

Municipal Money Market Fund

Semiannual Report

(Unaudited) and Investment Performance Review for the Six-Month Period Ended February 28, 2006

March 15, 2006

Dear Fellow Shareholders:

I am pleased to provide you with the semiannual report for the Heritage Cash Trust–Municipal Money Market Fund (the “Fund”) for the six-month period ended February 28, 2006. Since the prior reporting period, the economy has continued to grow at a healthy pace. In order to prevent the economy from overheating and developing inflationary pressures, the Federal Reserve Bank has continued to increase the target federal funds rate at a measured pace of 0.25% at each of their Federal Open Market Committee meetings held during the period resulting in a rate increase during the reporting period from 3.50% to 4.50%. The Federal Reserve Bank continued to reiterate their balanced view on growth and inflation. Short-term tax-exempt interest rates increased along with federal funds rate. As a result, the Fund’s seven-day current yield(a) increased from 1.85% on August 31, 2005 to 2.54% on February 28, 2006. This performance data represents past performance and past performance does not guarantee future results. Current performance may be higher or lower than the performance data quoted. To obtain more current performance, please visit the Fund’s website at www.HeritageFunds.com.

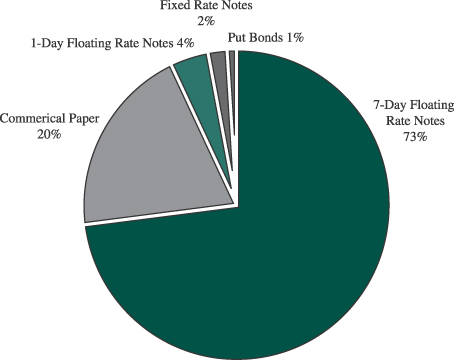

As of February 28, 2006, the Fund’s investment portfolio was comprised of approximately 77% tax-exempt floating rate notes, 2% fixed rate notes, 1% short-term puts, and 20% commercial paper. The large composition of floating rate notes provide the Fund with ample liquidity. The investments in commercial paper provide more relative value than fixed rate notes and bonds. The entire portfolio is invested in highly rated tier-one securities. These high quality investments satisfied the requirements set forth by Standard and Poor’s Rating Group to maintain the Fund’s AAAm rating(b). Ratings are subject to change and do not remove market risk from your investment.

On behalf of Heritage, I thank you for your continued investment in the Heritage Cash Trust–Municipal Money Market Fund. If you have any questions or comments, please contact your financial advisor or Heritage at (800) 421-4184.

Sincerely,

Stephen G. Hill

President

(a) An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund. Please consider the investment objectives, risks, charges, and expenses of any fund carefully before investing. Contact Heritage at (800) 421-4184 or your financial advisor for a prospectus, which contains this and other important information about the Fund. Read the prospectus carefully before you invest.

(b) Standard & Poor’s, a widely recognized independent authority on credit quality, rates certain money market funds based on weekly analysis. When rating a money market fund, Standard & Poor’s assesses the safety of principal. According to Standard & Poor’s, a fund rated AAAm (‘‘m’’ denotes money market fund) offers excellent safety features and has superior capacity to maintain principal value and limit exposure to loss. In evaluating safety, Standard & Poor’s focuses on credit quality, liquidity, and management of the Fund.

Heritage Cash Trust—Municipal Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

| | | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes—79.6%(a)(b)

|

Alabama—1.5%

| | | |

| $10,550,000 | | Alabama Housing Finance Authority, 3.25%(c)

Multi Family Housing Revenue Bond

Hunter Ridge Apartments Project,

Series 05F, AMT, 03/07/06

LOC: Federal Home Loan Mortgage Corporation | | $ | 10,550,000 |

| 6,400,000 | | Stevenson Industrial Development

Board, 3.25%(c)

Industrial Development Revenue Bond

Mead Corporation Project,

Series 97, AMT, 03/07/06

LOC: JP Morgan Chase Bank | | | 6,400,000 |

| | | | |

|

|

| | | | | | 16,950,000 |

| | | | |

|

|

Arizona—0.9%

| | | |

| 3,400,000 | | Maricopa County Industrial Development Authority, 3.22%(c)

Multi Family Housing Revenue Bond

San Remo Apartments Project,

Series 00A, AMT, 03/07/06

LOC: Federal National Mortgage Association | | | 3,400,000 |

| 6,750,000 | | Maricopa County Industrial Development

Authority, 3.28%(c)

Multi Family Housing Revenue Bond

San Fernando Apartments Project,

Series 04, AMT, 03/07/06

LOC: Federal National Mortgage Association | | | 6,750,000 |

| | | | |

|

|

| | | | | | 10,150,000 |

| | | | |

|

|

Arkansas—1.1%

| | | |

| 6,000,000 | | Arkansas Development Finance

Authority, 3.25%(c)

Industrial Development Revenue Bond

Teris LLC Project,

Series 02, AMT, 03/07/06

LOC: Wachovia Bank, N.A. | | | 6,000,000 |

| | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Arkansas (continued)

| | |

| 6,400,000 | | Pulaski County, 3.26%(c)

Multi Family Housing Revenue Bond Markham Oaks & Indian Hills Apartments Project,

Series 05, AMT, 03/07/06

LOC: Regions Bank | | 6,400,000 |

| | | | |

|

| | | | | 12,400,000 |

| | | | |

|

Colorado—2.2%

| | |

| 14,160,000 | | Colorado Housing & Finance Authority, 3.24%(c)

Pollution Control Revenue Bond

Waste Management Inc. Project,

Series 02, AMT, 03/07/06

LOC: J.P. Morgan Chase Bank | | 14,160,000 |

| 8,300,000 | | Colorado Housing & Finance

Authority, 3.24%(c)

Pollution Control Revenue Bond

Waste Management Inc. Project,

Series 03, AMT, 03/07/06

LOC: Wachovia Bank, N.A. | | 8,300,000 |

| 2,300,000 | | Traer Creek Metropolitan

District, 3.22%(c)

Eagle County Project,

Series 02, 03/07/06

LOC: BNP Paribas | | 2,300,000 |

| | | | |

|

| | | | | 24,760,000 |

| | | | |

|

Connecticut—0.6%

| | |

| 5,300,000 | | Connecticut Housing Finance

Authority, 3.20%(c)

Multi Family Housing Revenue Bond

Mortgage Finance Project, AMBAC,

Series 02B, AMT, 03/07/06

BPA: Federal Home Loan Bank | | 5,300,000 |

The accompanying notes are an integral part of the financial statements.

Heritage Cash Trust—Municipal Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Connecticut (continued)

| | | |

| $ 1,500,000 | | Connecticut State Health & Education Facility Authority, 3.16%(c)

Higher Education Bond

Yale University Project,

Series 03X-2, 03/07/06 | | $ | 1,500,000 |

| | | | |

|

|

| | | | | | 6,800,000 |

| | | | |

|

|

District Of Columbia—0.7%

| | | |

| 8,130,000 | | Metropolitan Washington Airport

Authority, 3.25%(c)

Airport Facilities Revenue Bond

FSA, Series 02C, AMT, 03/07/06

BPA: Dexia | | | 8,130,000 |

| | | | |

|

|

Florida—2.1%

| | | |

| 5,905,000 | | Hillsborough County Housing Finance

Authority, 3.22%(c)

Multi Family Housing Revenue Bond

Brandon Crossing Apartments Project,

Series 98A, AMT, 03/07/06

LOC: Federal National Mortgage Association | | | 5,905,000 |

| 13,000,000 | | Orlando & Orange County Expressway

Authority, 3.15%(c)

Transportation Revenue Bond

AMBAC, Series 05, 03/07/06

BPA: Wachovia Bank, N.A. | | | 13,000,000 |

| 4,400,000 | | Palm Beach County School

Board, 3.18%(c)

Certificates of Participation Project,

FSA, Series 02B, 03/07/06

BPA: Dexia | | | 4,400,000 |

| | | | |

|

|

| | | | | | 23,305,000 |

| | | | |

|

|

| | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Georgia—4.4%

| | |

| 3,200,000 | | Bibb County Development

Authority, 3.19%(c)

Industrial Development Revenue Bond

Mount de Sales Academy Project,

Series 00, 03/07/06

LOC: SunTrust Bank | | 3,200,000 |

| 1,400,000 | | Clayton County Development

Authority, 3.24%(c)

Industrial Development Revenue Bond

C. W. Matthews Contracting Project,

Series 00, AMT, 03/07/06

LOC: Bank of America | | 1,400,000 |

| 3,900,000 | | DeKalb County Housing

Authority, 3.24%(c)

Multi Family Housing Revenue Bond

Mountain Crest Apartments Project,

Series 02A-1, AMT, 03/07/06

LOC: SunTrust Bank | | 3,900,000 |

| 12,525,000 | | East Point Housing Authority, 3.29%(c)

Multi Family Housing Revenue Bond

Eagles Creste Apartments Project,

Series 03, AMT, 03/07/06

LOC: Federal Home Loan Mortgage Corporation | | 12,525,000 |

| 16,000,000 | | Fulton County Development

Authority, 3.29%(c)

Multi Family Housing Revenue Bond

Hidden Creste Apartments Project,

Series 04, AMT, 03/07/06

LOC: J.P. Morgan Chase Bank | | 16,000,000 |

| 2,500,000 | | Gainesville & Hall County Development Authority, 3.30%(c)

Industrial Development Revenue Bond

IMS Gear Project,

Series 00, AMT, 03/07/06

LOC: Wachovia Bank, N.A. | | 2,500,000 |

The accompanying notes are an integral part of the financial statements.

3

Heritage Cash Trust—Municipal Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Georgia (continued)

| | | |

| $ 1,700,000 | | Rockmart Development

Authority, 3.30%(c)

Industrial Development Revenue Bond

C. W. Matthews Contracting Project,

Series 00, AMT, 03/07/06

LOC: Wachovia Bank, N.A. | | $ | 1,700,000 |

| 8,100,000 | | Roswell Housing Authority, 3.25%(c)

Multi Family Housing Revenue Bond

Park Ridge Apartments Project,

Series 03, AMT, 03/07/06

LOC: Federal National Mortgage Association | | | 8,100,000 |

| | | | |

|

|

| | | | | | 49,325,000 |

| | | | |

|

|

Illinois—6.1%

| | | |

| 4,405,000 | | Chicago Industrial Development

Authority, 3.28%(c)

Industrial Development Revenue Bond

Evans Food Products Company Project,

Series 98, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | | 4,405,000 |

| 2,895,000 | | Chicago, 3.28%(c)

Industrial Development Revenue Bond

Andres Imaging & Graphics Project,

Series 00, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | | 2,895,000 |

| 2,935,000 | | Chicago, 3.33%(c)

Multi Family Housing Revenue Bond

North Larrabee Project,

Series 01A, AMT, 03/07/06

LOC: Harris Trust and Savings Bank | | | 2,935,000 |

| 2,900,000 | | Hennepin, 3.28%(c)

Pollution Control Revenue Bond

Hennepin-Hopper Lakes Project,

Series 01, 03/07/06

LOC: Harris Trust and Savings Bank | | | 2,900,000 |

| | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Illinois (continued)

| | |

| 2,000,000 | | Illinois Development Finance

Authority, 3.24%(c)

Industrial Development Revenue Bond

MPP Zinc Plating Plant Project,

AMT, 03/07/06

LOC: Bank of America | | 2,000,000 |

| 2,200,000 | | Illinois Development Finance

Authority, 3.28%(c)

Industrial Development Revenue Bond

Porter Athletic Equipment Project,

AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | 2,200,000 |

| 2,690,000 | | Illinois Development Finance

Authority, 3.28%(c)

Industrial Development

Revenue Bond

Olive Can Company Project,

Series 94, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | 2,690,000 |

| 860,000 | | Illinois Development Finance

Authority, 3.28%(c)

Industrial Development

Revenue Bond

F. C. Limited Partnership Project,

AMT, 03/01/06

LOC: LaSalle National Trust, N.A. | | 860,000 |

| 3,025,000 | | Illinois Development Finance

Authority, 3.28%(c)

Industrial Development Revenue Bond

Touhy Limited Partnership Project,

Series 96, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | 3,025,000 |

The accompanying notes are an integral part of the financial statements.

4

Heritage Cash Trust—Municipal Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Illinois (continued)

| | | |

| $ 1,050,000 | | Illinois Development Finance

Authority, 3.28%(c)

Industrial Development Revenue Bond

Emtech Machining & Grinding Project,

Series 96, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | $ | 1,050,000 |

| 3,455,000 | | Illinois Development Finance

Authority, 3.28%(c)

Industrial Development Revenue Bond

Elite Manufacturing Technology

Inc. Project,

Series 99, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | | 3,455,000 |

| 600,000 | | Illinois Development Finance

Authority, 3.30%(c)

Industrial Development Revenue Bond

Azteca Foods Inc. Project,

Series 95, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | | 600,000 |

| 3,380,000 | | Illinois Development Finance

Authority, 3.33%(c)

Industrial Development Revenue Bond

Northwest Pallet Supply Project,

Series 01, AMT, 03/07/06

LOC: Harris Trust and Savings Bank | | | 3,380,000 |

| 10,000,000 | | Illinois Development Finance

Authority, 3.24%(c)

Pollution Control Revenue Bond

Waste Management Inc. Project,

Series 02, AMT, 03/07/06

LOC: J.P. Morgan Chase Bank | | | 10,000,000 |

| 6,715,000 | | Illinois Housing Development

Authority, 3.25%(c)

Multi Family Housing Revenue Bond

Hyde Park Tower Project,

Series 00A, AMT, 03/07/06

LOC: Federal National Mortgage Association | | | 6,715,000 |

| | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Illinois (continued)

| | |

| 3,930,000 | | Illinois Housing Development

Authority, 3.26%(c)

Multi Family Housing Revenue Bond

Sterling Towers Project,

Series 01, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | 3,930,000 |

| 2,400,000 | | Illinois Student Assistance

Commission, 3.26%(c)

Student Loan Revenue Bond

Series 97A, AMT, 03/07/06

LOC: J.P. Morgan Chase Bank | | 2,400,000 |

| 4,310,000 | | Lake County, 3.23%(c)

Multi Family Housing Revenue Bond

Rosewood Apartments Project,

Series 04, AMT, 03/07/06

LOC: Federal Home Loan Mortgage Corporation | | 4,310,000 |

| 4,320,000 | | Lake County, 3.26%(c)

Water & Sewer System Revenue Bond

Countryside Landfill Project,

Series 96B, AMT, 03/07/06

LOC: J.P. Morgan Chase Bank | | 4,320,000 |

| 2,065,000 | | Rock Island County Metropolitan Airport Authority, 3.24%(c)

Airport Facilities Revenue Bond

Quad City International Airport Project, Series 98, AMT, 03/07/06

LOC: U.S. Bank N.A. | | 2,065,000 |

| 1,820,000 | | Wheeling, 3.37%(c)

Industrial Development Revenue Bond

V-S Industries Inc. Project,

Series 00, AMT, 03/07/06

LOC: Harris Trust and Savings Bank | | 1,820,000 |

| 1,100,000 | | Will County, 3.04%(c)

Industrial Development Revenue Bond

BP Amoco Project,

Series 02, AMT, 03/01/06 | | 1,100,000 |

| | | | |

|

| | | | | 69,055,000 |

| | | | |

|

The accompanying notes are an integral part of the financial statements.

5

Heritage Cash Trust—Municipal Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Indiana—1.7%

| | | |

| $ 2,550,000 | | Elkhart County, 3.25%(c)

Multi Family Housing Revenue Bond Johnson Street Apartments Project,

Series 98A, AMT, 03/07/06

LOC: Federal Home Loan Bank | | $ | 2,550,000 |

| 2,500,000 | | Gibson County, 3.25%(c)

Pollution Control Revenue Bond

Toyota Motor Manufacturing Project, Series 97, AMT, 03/07/06 | | | 2,500,000 |

| 3,000,000 | | Gibson County, 3.25%(c)

Pollution Control Revenue Bond

Toyota Motor Manufacturing Project, Series 99A, AMT, 03/07/06 | | | 3,000,000 |

| 1,000,000 | | Gibson County, 3.25%(c)

Pollution Control Revenue Bond

Toyota Motor Manufacturing Project, Series 00A, AMT, 03/07/06 | | | 1,000,000 |

| 4,000,000 | | Gibson County, 3.25%(c)

Pollution Control Revenue Bond

Toyota Motor Manufacturing Project, Series 01, AMT, 03/07/06 | | | 4,000,000 |

| 3,000,000 | | Gibson County, 3.25%(c)

Pollution Control Revenue Bond

Toyota Motor Manufacturing Project, Series 01B, AMT, 03/07/06 | | | 3,000,000 |

| 2,855,000 | | Valparaiso, 3.24%(c)

Industrial Development Revenue Bond Block Heavy & Highway Products Project, Series 99, AMT, 03/07/06

LOC: U.S. Bank N.A. | | | 2,855,000 |

| | | | |

|

|

| | | | | | 18,905,000 |

| | | | |

|

|

Iowa—1.0%

| | | |

| 7,500,000 | | Iowa Higher Education Loan

Authority, 3.19%(c)

Student Loan Revenue Bond

Luther College Project,

Series 02, 03/07/06

LOC: U.S. Bank N.A. | | | 7,500,000 |

| | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Iowa (continued)

| | |

| 3,400,000 | | Orange City, 3.28%(c)

Industrial Development Revenue Bond

Vogel Enterprises LTD Project,

AMT, 03/07/06

LOC: U.S. Bank N.A. | | 3,400,000 |

| | | | |

|

| | | | | 10,900,000 |

| | | | |

|

Kansas—1.3%

| | |

| 6,000,000 | | Dodge City, 3.44%(c)

Industrial Development Revenue Bond

Farmland National Beef Packing

Company Project,

Series 00, AMT, 03/07/06

LOC: Rabobank Nederland | | 6,000,000 |

| 5,850,000 | | Liberal, 3.44%(c)

Industrial Development Revenue Bond

Farmland National Beef Packing

Company Project,

Series 00, AMT, 03/07/06

LOC: Rabobank Nederland | | 5,850,000 |

| 2,700,000 | | Shawnee Industrial Development

Authority, 3.28%(c)

Industrial Development Revenue Bond

Thrall Enterprises Inc. Project,

Series 94, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | 2,700,000 |

| | | | |

|

| | | | | 14,550,000 |

| | | | |

|

Kentucky—1.0%

| | |

| 11,240,000 | | Middletown, 3.22%(c)

Christian Academy of Louisville Project,

Series 04, 03/07/06

LOC: J.P. Morgan Chase Bank | | 11,240,000 |

| | | | |

|

The accompanying notes are an integral part of the financial statements.

6

Heritage Cash Trust—Municipal Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Louisiana—2.3%

| | | |

| $ 3,470,000 | | Caddo-Bossier Parishes Port

Commission, 3.29%(c)

Transportation Revenue Bond

Oakley Louisiana Inc. Project,

Series 98, AMT, 03/07/06

LOC: Regions Bank | | $ | 3,470,000 |

| 1,500,000 | | Calcasieu Parish Industrial Development

Board, 3.30%(c)

Industrial Development Revenue Bond

Hydroserve Westlake LLC Project,

Series 98, AMT, 03/07/06

LOC: J.P. Morgan Chase Bank | | | 1,500,000 |

| 2,320,000 | | DeRidder Industrial Development

Board, 3.29%(c)

Industrial Development Revenue Bond

Pax Inc. Project,

Series 97, AMT, 03/07/06

LOC: J.P. Morgan Chase Bank | | | 2,320,000 |

| 7,655,000 | | St. Charles Parish, 3.04%(c)

Pollution Control Revenue Bond

Shell Oil Company Project,

Series 93, AMT, 03/01/06 | | | 7,655,000 |

| 11,250,000 | | St. Charles Parish, 3.04%(c)

Industrial Development Revenue Bond

Shell Oil Company Project,

Series 92A, AMT, 03/01/06 | | | 11,250,000 |

| | | | |

|

|

| | | | | | 26,195,000 |

| | | | |

|

|

Maine—0.5%

| | | |

| 5,675,000 | | Maine Finance Authority, 3.24%(c) Industrial Development Revenue Bond Jackson Laboratory Project,

Series 02, 03/07/06

LOC: Bank of America | | | 5,675,000 |

| | | | |

|

|

| | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Maryland—0.5%

| | |

| 6,000,000 | | Montgomery County, 3.19%(c)

Industrial Development Revenue Bond Georgetown Preparatory School Project, Series 05, 03/07/06

LOC: Bank of America | | 6,000,000 |

| | | | |

|

Massachusetts—2.8%

| | |

| 15,100,000 | | Massachusetts Bay Transportation

Authority, 3.16%(c)

General Transportation System Bond Series 00, 03/07/06

BPA: Westdeutsche Landesbank | | 15,100,000 |

| 10,400,000 | | Massachusetts Development Finance

Agency, 3.10%(c)

Higher Education Bond

Smith College Project,

Series 01, 03/07/06 | | 10,400,000 |

| 6,260,000 | | Massachusetts Industrial Finance

Agency, 3.24%(c)

Heritage At Hingham Project,

Series 97, AMT, 03/07/06

LOC: Federal National Mortgage Association | | 6,260,000 |

| | | | |

|

| | | | | 31,760,000 |

| | | | |

|

Michigan—0.4%

| | |

| 5,000,000 | | Michigan Municipal Bond Authority, 2.92% Revenue Notes

Series 05B-2, 08/18/06

LOC: J.P. Morgan Chase Bank | | 5,024,426 |

| | | | |

|

Minnesota—2.6%

| | |

| 5,000,000 | | Dakota County Community Development Agency, 3.28%(c)

Multi Family Housing Revenue Bond View Pointe Apartments Project,

Series 04, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | 5,000,000 |

The accompanying notes are an integral part of the financial statements.

7

Heritage Cash Trust—Municipal Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Minnesota (continued)

| | | |

| $ 2,655,000 | | Dakota County Community Development Agency, 3.10%(c)

Multi Family Housing Revenue Bond Regatta Commons Project,

Series 03A, AMT, 03/01/06

LOC: LaSalle National Trust, N.A. | | $ | 2,655,000 |

| 3,800,000 | | Plymouth Housing Authority, 3.23%(c) Multi Family Housing Revenue Bond

At the Lake Apartments Project,

Series 04, AMT, 03/07/06

LOC: Federal Home Loan Mortgage Corporation | | | 3,800,000 |

| 6,000,000 | | St. Anthony, 3.28%(c)

Multi Family Housing Revenue Bond

St. Anthony Leased Housing Project, Series 04A, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | | 6,000,000 |

| 5,000,000 | | St. Paul & Ramsey County Housing & Redevelopment Authority, 3.28%(c) Multi Family Housing Revenue Bond

St. Paul Leased Housing Association I Project,

Series 02A, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | | 5,000,000 |

| 3,000,000 | | St. Paul Housing & Redevelopment

Authority, 3.30%(c)

Multi Family Housing Revenue Bond

Bridgecreek Senior Place Project,

Series 04A, AMT, 03/07/06

LOC: LaSalle National Trust, N.A. | | | 3,000,000 |

| 4,000,000 | | St. Paul Port Authority, 3.25%(c)

Transportation Revenue Bond

District Heating Project,

Series 03-2F, AMT, 03/07/06

LOC: Dexia | | | 4,000,000 |

| | | | |

|

|

| | | | | | 29,455,000 |

| | | | |

|

|

| | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

Mississippi—1.1%

| | |

| 3,000,000 | | Mississippi Business Finance

Corporation, 3.29%(c)

Industrial Development Revenue Bond

EPCO Carbon Dioxide Products

Inc. Project,

Series 02, AMT, 03/07/06

LOC: Regions Bank | | 3,000,000 |

| 9,800,000 | | Mississippi Home Corporation, 3.32%(c)

Multi Family Housing Revenue Bond

Summer Park Apartments Project,

Series 99D-1, AMT, 03/07/06

LOC: Wachovia Bank, N.A. | | 9,800,000 |

| | | | |

|

| | | | | 12,800,000 |

| | | | |

|

Nevada—2.0%

| | |

| 5,350,000 | | Clark County, 3.05%(c)

Pollution Control Revenue Bond

Cogeneration Association 2 Project,

AMT, 03/01/06

LOC: ABN-AMRO Bank N.V. | | 5,350,000 |

| 13,500,000 | | Director of the State of Nevada Department

of Business & Industry, 3.25%(c)

Pollution Control Revenue Bond

Barrick Goldstrike Mines Project,

AMT, 03/07/06

LOC: Royal Bank Of Canada | | 13,500,000 |

| 1,790,000 | | Nevada Housing Finance Agency, 3.22%(c)

Multi Family Housing Revenue Bond

Fremont Meadows Apartments Project,

Series 97, AMT, 03/07/06

LOC: Federal Home Loan Bank | | 1,790,000 |

| 2,000,000 | | Nevada Housing Finance Agency, 3.22%(c)

Multi Family Housing Revenue Bond

Horizon Pines Apartments Project,

Series 00A, AMT, 03/07/06

LOC: Federal National Mortgage Association | | 2,000,000 |

| | | | |

|

| | | | | 22,640,000 |

| | | | |

|

The accompanying notes are an integral part of the financial statements.

8

Heritage Cash Trust—Municipal Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

New Hampshire—0.9%

| | | |

| $ 5,300,000 | | New Hampshire Health & Education

Facilities Authority, 3.21%(c)

Higher Education Bond

Brewster Academy Issue Project,

Series 05, 03/07/06

LOC: Allied Irish Banks | | $ | 5,300,000 |

| 5,000,000 | | New Hampshire Health & Education

Facilities Authority, 3.24%(c)

Hospital Revenue Bond

Easter Seals Project,

Series 04H-A, 03/07/06

LOC: Royal Bank of Scotland | | | 5,000,000 |

| | | | |

|

|

| | | | | | 10,300,000 |

| | | | |

|

|

New Jersey—0.6%

| | | |

| 6,200,000 | | New Jersey Economic Development

Authority, 3.23%(c)

Industrial Development Revenue Bond

Port Newark Container

Terminal Project,

Series 03, AMT, 03/07/06

LOC: Citibank | | | 6,200,000 |

| | | | |

|

|

New Mexico—2.1%

| | | |

| 11,600,000 | | New Mexico Hospital Equipment Loan Council, 3.20%(c)

Hospital Revenue Bond

Presbyterian Healthcare

Services Project,

FSA, Series 05A, 03/07/06

BPA: Citibank | | | 11,600,000 |

| 12,600,000 | | New Mexico Hospital Equipment Loan

Council, 3.20%(c)

Hospital Revenue Bond

Presbyterian Healthcare

Services Project,

FSA, Series 05B, 03/07/06

BPA: Citibank | | | 12,600,000 |

| | | | |

|

|

| | | | | | 24,200,000 |

| | | | |

|

|

| | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

New York—11.0%

| | |

| 12,100,000 | | City of New York, 3.20%(c)

Series H-6, 03/07/06

LOC: Bank of America | | 12,100,000 |

| 11,000,000 | | City of New York, GO, 3.16%(c)

Series 04H-5, 03/07/06

LOC: Dexia | | 11,000,000 |

| 18,000,000 | | City of New York, GO, 3.14%(c)

Series 03C-4, 03/07/06

LOC: BNP Paribas | | 18,000,000 |

| 15,000,000 | | New York Housing Finance

Agency, 3.20%(c)

Multi Family Housing Revenue Bond

Saxony Apartments Project,

Series 97A, AMT, 03/07/06

LOC: Federal National Mortgage Association | | 15,000,000 |

| 18,000,000 | | New York Local Government Assistance Corporation, 3.19%(c)

FSA, Series 03-4V, 03/07/06

BPA: Westdeutsche Landesbank | | 18,000,000 |

| 25,200,000 | | New York Local Government Assistance Corporation, 3.12%(c)

Series 94B, 03/07/06

LOC: Westdeutsche Landesbank and Bayerische Landesbank | | 25,200,000 |

| 25,000,000 | | Triborough Bridge & Tunnel

Authority, 3.18%(c)

General Revenue Refunding Bond

Series 05B, 03/07/06

BPA: Landesbank Baden Wurttenburg | | 25,000,000 |

| | | | |

|

| | | | | 124,300,000 |

| | | | |

|

North Carolina—1.1%

| | |

| 12,000,000 | | North Carolina Educational Facilities Finance Agency, 3.17%(c)

Higher Education Bond

Duke University Project,

Series B, 03/07/06 | | 12,000,000 |

| | | | |

|

The accompanying notes are an integral part of the financial statements.

9

Heritage Cash Trust—Municipal Money Market Fund

Statement of Net Assets

February 28, 2006

(unaudited)

(continued)

| | | | | |

Principal

Amount

| | | | Value

|

Notes, Bonds & Variable Rate Demand Notes (continued)

|

North Dakota—1.0%

| | | |

| $11,000,000 | | Richland County, 3.39%(c)

Water & Sewer System Revenue Bond

Minn-Dak Farmers Cooperative Project,

Series 02, AMT, 03/07/06

LOC: Wells Fargo Bank | | $ | 11,000,000 |

| | | | |

|

|

Ohio—5.2%

| | | |

| 8,525,000 | | Akron Bath Copley Joint Township Hospital District, 3.23%(c)

Healthcare Facilities Revenue Bond

Sumner on Ridgewood Project,

Series 02, 03/07/06

LOC: KBC Bank | | | 8,525,000 |

| 10,165,000 | | Butler County Health Facility, 3.06%(c) Hospital Revenue Bond

Lifesphere Project,

Series 02, 03/07/06

LOC: U.S. Bank N.A. | | | 10,165,000 |

| 11,800,000 | | Cleveland Airport System, 3.20%(c)

Airport Facilities Revenue Bond

FSA, Series C, 03/07/06

BPA: Dexia and Westdeutsche Landesbank | | | 11,800,000 |