| | |

| UNITED STATES

SECURITIES AND EXCHANGE COMMISSION |

| | |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | |

| Investment Company Act file number: | (811-04345) |

| | |

| Exact name of registrant as specified in charter: | Putnam Tax Free Income Trust |

| | |

| Address of principal executive offices: | 100 Federal Street, Boston, Massachusetts 02110 |

| | |

| Name and address of agent for service: | Stephen Tate, Vice President

100 Federal Street

Boston, Massachusetts 02110 |

| | |

| Copy to: | Bryan Chegwidden, Esq.

Ropes & Gray LLP

1211 Avenue of the Americas

New York, New York 10036 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: | July 31, 2023 |

| | |

| Date of reporting period: | August 1, 2022 – January 31, 2023 |

| | |

|

Item 1. Report to Stockholders: | |

| | |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |

Putnam

Strategic Intermediate

Municipal Fund

Semiannual report

1 | 31 | 23

Message from the Trustees

March 10, 2023

Dear Fellow Shareholder:

Stock and bond markets rose in early 2023 as inflation continued to ease and the U.S. Federal Reserve moderated its interest-rate increases. Investors showed optimism that the Fed might slow the economy and reduce inflation without causing a recession. Still, caution may be warranted. While the Fed has reduced the size of its interest-rate increases, it also signaled that more rate hikes are likely if concerns persist about a resurgence in inflation.

Putnam’s investment teams believe a recession is possible this year or next. However, they also are finding what they believe to be attractive investment opportunities in a range of asset classes, including stocks and taxable and tax-exempt bonds. As active researchers, our teams analyze interest-rate and credit risks as they seek out investments for your fund. They also consider how stocks and bonds are likely to perform in uncertain economic conditions.

Thank you for investing with Putnam.

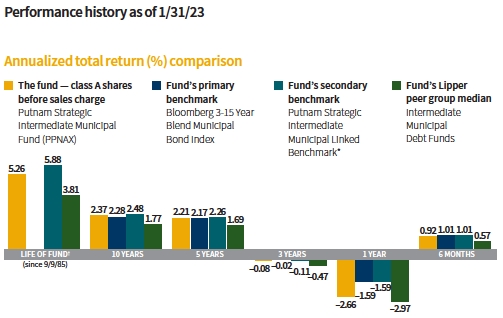

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 2.25%; had they, returns would have been lower. Performance for class A shares before their inception (9/20/93) is derived from the historical performance of class B shares. See page 3 and pages 9–12 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

Before August 28, 2020, the fund was managed with a materially different investment strategy and may have achieved materially different performance results under its current investment strategy from that shown for periods before this date.

Returns for periods of less than one year are not annualized.

All Bloomberg indices are provided by Bloomberg Index Services Limited.

Lipper peer group median is provided by Lipper, a Refinitiv company.

* The Putnam Strategic Intermediate Municipal Linked Benchmark represents the performance of the Bloomberg Municipal Bond Index through August 27, 2020, and the performance of the Bloomberg 3-15 Year Blend Municipal Bond Index thereafter.

† The fund’s primary benchmark, the Bloomberg 3-15 Year Blend Municipal Bond Index, was introduced on 1/31/90, which post-dates the inception of the fund.

|

| 2 Strategic Intermediate Municipal Fund |

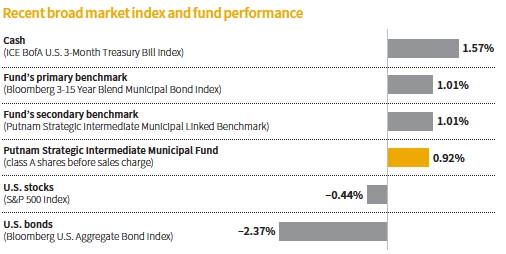

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 1/31/23. See page 2 and pages 9–12 for additional fund performance information. Index descriptions can be found on pages 15–16.

All Bloomberg indices are provided by Bloomberg Index Services Limited.

|

| Strategic Intermediate Municipal Fund 3 |

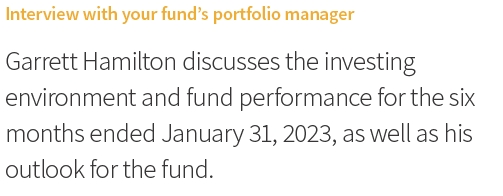

Garrett, how was the market environment for intermediate-term municipal bonds during the six-month period ended January 31, 2023?

After a challenging first few months, intermediate-term municipal bonds regained their footing. November 2022 was especially strong for the asset class, despite the Federal Reserve’s announcement of its fourth consecutive 0.75% interest-rate increase on November 3. Investors were heartened to see that the Consumer Price Index [CPI], a widely used measure of inflation, came in better than expected at 7.7% for October 2022. Investors interpreted this as evidence that the Fed was making progress in subduing stubbornly high prices. As the month ended, the Fed hinted it might temper the degree of interest-rate hikes as early as December 2022.

The CPI for November also showed progress, with year-over-year inflation falling to 7.1%. It was the smallest 12-month increase since December 2021. In our view, this gave the Fed room to raise its benchmark interest rate by only half a percentage point on December 15, 2022. However, Fed policymakers also signaled the fight against inflation was not over. Fed Chair Jerome Powell stated that “it will take

|

| 4 Strategic Intermediate Municipal Fund |

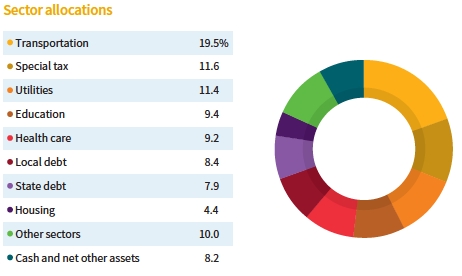

Allocations are shown as a percentage of the fund’s net assets as of 1/31/23. Cash and net other assets, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Summary information may differ from the information in the portfolio schedule notes included in the financial statements due to the inclusion of derivative securities, any interest accruals, the timing of matured security transactions, the use of different classifications of securities for presentation purposes, and rounding. Holdings and allocations may vary over time.

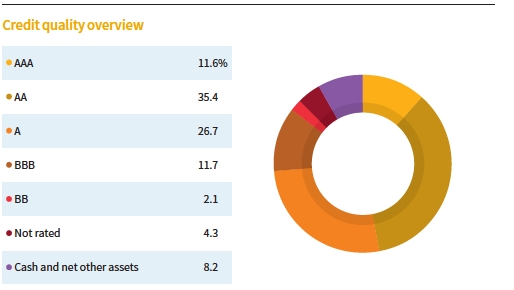

Credit qualities are shown as a percentage of the fund’s net assets as of 1/31/23. A bond rated BBB or higher (SP-3 or higher, for short-term debt) is considered investment grade. This chart reflects the highest security rating provided by one or more of Standard & Poor’s, Moody’s, and Fitch. Ratings may vary over time.

Cash and net other assets, if any, represent the market value weights of cash, derivatives, and short-term securities in the portfolio. The fund itself has not been rated by an independent rating agency.

|

| Strategic Intermediate Municipal Fund 5 |

substantially more evidence to give confidence that inflation is on a sustained downward path.” Minutes from the central bank’s policy meeting in December revealed that Fed officials agreed it would be appropriate to slow the pace of its aggressive rate hikes to minimize the risks to economic growth. At period-end, the Fed raised its benchmark rate by 0.25%, elevating its benchmark interest rate to a target range of 4.50%–4.75%.

Market technicals improved during the period as well. Demand rebounded amid the improvement in market sentiment. At the same time, new issue supply was well below average due to the sharp rise in interest rates. This imbalance aided returns. With these positive developments, November 2022’s return of 3.76% represented the strongest monthly return for the Bloomberg 3-15 Year Blend Municipal Bond Index [the fund’s primary benchmark] since 1990.

For the six months ended January 31, 2023, the fund’s primary benchmark returned 1.01%. Intermediate-term municipal bonds outperformed longer-term and shorter-term cohorts. From a credit perspective, investment-grade municipal bonds performed better than higher-yielding, lower-rated bonds, which aided our positioning.

What is your current assessment of the health of the municipal bond market?

Municipal credit fundamentals continue to be stable, in our view. Higher employment and increasing wages have bolstered tax receipts. Home values, a factor in property tax revenues, have been facing headwinds in the form of rising mortgage rates. We believe assessed values, another factor in taxes, should continue to reflect growth given the roughly two-year lag between tax assessments and actual property values.

State and local tax collections were up 16% year over year through the third quarter of 2022 compared with the same period in 2021 [most recent data available]. Unprecedented fiscal support during the Covid-19 pandemic, as well as strong economic growth during the second half of 2020 and 2021, put most state and local governments in their best fiscal shape in more than a decade, in our view. Municipal defaults are running near long-term averages as of January 31, 2023, and they remain a very small percentage of the market. As such, we believe the credit outlook remains favorable, though we continue to actively monitor the market. We expect economic conditions to slow during 2023, which could impact municipal bond credit quality, in our view.

How did the fund perform during the period?

For the six months ended January 31, 2023, the fund’s class A shares underperformed the primary and secondary benchmarks but outperformed the median return of its Lipper peer group, Intermediate Municipal Debt Funds.

What strategies or holdings influenced the fund’s performance during the reporting period?

During the early months of the reporting period, the Fed’s hawkish monetary policy and investors’ risk-averse sentiment contributed to a sharp sell-off. This propelled bond yields higher and bond prices, which move in the opposite direction of yields, lower. Credit spreads widened, presenting attractively priced investment opportunities, in our view. We moved the portfolio to a long duration position versus its Lipper peers by adding bonds with maturities in the 7- to 15-year range. Our additions were generally focused on higher-rated investment-grade bonds.

The fund held an overweight exposure to lower-investment-grade bonds and those rated A relative to the benchmark. We remain

|

| 6 Strategic Intermediate Municipal Fund |

cautious on lower-rated municipal bonds in general, given our view that the Fed’s aggressive tightening cycle could result in slower U.S. economic growth in 2023. However, we have found value in some of the upper tiers of the high-yield market. While credit spreads widened over the period, they were not excessively wide versus previous recessionary periods, in our view. The fund was invested in a wide range of sectors, including public power, airport, and local general obligation bonds.

The fund remained underweight in its exposure to Puerto Rico municipal debt relative to its Lipper peer group. However, we note that the U.S. territory has experienced recent improvement in credit fundamentals since coming out of bankruptcy in March 2022. We continue to closely monitor Puerto Rico’s credit fundamentals and remain vigilant for investment opportunities.

What do you see on the horizon that could influence your management of the fund?

While it appears to us that inflation has peaked in this cycle, we believe U.S. economic data remains relatively strong. Especially noteworthy is the low U.S. unemployment rate and strong consumer spending. We presume this will keep the Fed on track to continue ratcheting up interest rates to slow economic growth and the jobs market. That said, we think the bulk of the tightening is behind us and Fed monetary policy is set to enter the fine-tuning stage of the cycle. Market expectations are for the Fed to complete its tightening cycle by the summer of 2023.

Seasonal factors are typically weaker in late winter and early spring but turn more favorable in late spring and summer months. Against this backdrop, we believe valuations offer investors attractive tax-free income, as well as the potential for price appreciation once the Fed concludes its monetary tightening cycle.

Thank you, Garrett, for your time and insights today.

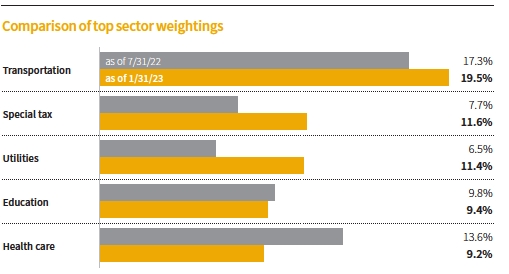

This chart shows how the fund’s top weightings have changed over the past six months. Allocations are shown as a percentage of the fund’s net assets. Current period summary information may differ from the information in the portfolio schedule notes included in the financial statements due to the inclusion of derivative securities, any interest accruals, the timing of matured security transactions, the use of different classifications of securities for presentation purposes, and rounding. Holdings and allocations may vary over time.

|

| Strategic Intermediate Municipal Fund 7 |

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice. Please note that the holdings discussed in this report may not have been held by the fund for the entire period.

Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk. Statements in the Q&A concerning the fund’s performance or portfolio composition relative to those of the fund’s Lipper peer group may reference information produced by Lipper Inc. or through a third party.

|

| 8 Strategic Intermediate Municipal Fund |

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended January 31, 2023, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance information as of the most recent calendar quarter-end and expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Before August 28, 2020, the fund was managed with a materially different investment strategy and may have achieved materially different performance results under its current investment strategy from that shown for periods before this date. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class R6 and Y shares are not available to all investors. See the Terms and definitions section in this report for definitions of the share classes offered by your fund.

Annualized fund performance Total return for periods ended 1/31/23

| | | | | | |

| | Life of fund | 10 years | 5 years | 3 years | 1 year | 6 months |

| Class A (9/20/93) | | | | | | |

| Before sales charge | 5.26% | 2.37% | 2.21% | –0.08% | –2.66% | 0.92% |

| After sales charge | 5.19 | 2.14 | 1.75 | –0.84 | –4.85 | –1.35 |

| Class B (9/9/85) | | | | | | |

| Before CDSC | 5.26 | 1.86 | 1.60 | –0.70 | –3.17 | 0.62 |

| After CDSC | 5.26 | 1.86 | 1.25 | –1.62 | –7.95 | –4.36 |

| Class C (7/26/99) | | | | | | |

| Before CDSC | 5.23 | 1.74 | 1.43 | –0.85 | –3.39 | 0.47 |

| After CDSC | 5.23 | 1.74 | 1.43 | –0.85 | –4.34 | –0.52 |

| Class R6 (5/22/18) | | | | | | |

| Net asset value | 5.17 | 2.62 | 2.47 | 0.18 | –2.35 | 1.08 |

| Class Y (1/2/08) | | | | | | |

| Net asset value | 5.17 | 2.61 | 2.45 | 0.14 | –2.44 | 0.98 |

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A shares reflect the deduction of the maximum 2.25% sales charge levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class R6 and Y shares have no initial sales charge or CDSC. Performance for class A, C, and Y shares before their inception is derived from the historical performance of class B shares, adjusted for the applicable sales charge (or CDSC) and, for class C shares, the higher operating expenses for such shares. Performance for class R6 shares prior to their inception is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R6 shares; had it, returns would have been higher.

Returns for periods of less than one year are not annualized.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B and C share performance reflects conversion to class A shares after eight years.

|

| Strategic Intermediate Municipal Fund 9 |

Comparative annualized index returns For periods ended 1/31/23

| | | | | | |

| | Life of fund | 10 years | 5 years | 3 years | 1 year | 6 months |

| Bloomberg 3-15 Year Blend | | | | | | |

| Municipal Bond Index* | — | 2.28% | 2.17% | –0.02% | –1.59% | 1.01% |

| Putnam Strategic | | | | | | |

| Intermediate Municipal | | | | | | |

| Linked Benchmark† | 5.88% | 2.48 | 2.26 | –0.11 | –1.59 | 1.01 |

| Lipper Intermediate | | | | | | |

| Municipal Debt Funds | | | | | | |

| category median‡ | 3.81 | 1.77 | 1.69 | –0.47 | –2.97 | 0.57 |

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

Returns for periods of less than one year are not annualized.

All Bloomberg indices are provided by Bloomberg Index Services Limited.

Lipper peer group median is provided by Lipper, a Refinitiv company.

* The fund’s primary benchmark, the Bloomberg 3-15 Year Blend Municipal Bond Index, was introduced on 1/31/90, which post-dates the inception of the fund.

† The Putnam Strategic Intermediate Municipal Linked Benchmark represents the performance of the Bloomberg Municipal Bond Index through August 27, 2020, and the performance of the Bloomberg 3-15 Year Blend Municipal Bond Index thereafter.

‡ Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 1/31/23, there were 223, 215, 193, 166, 125, and 26 funds, respectively, in this Lipper category.

|

| 10 Strategic Intermediate Municipal Fund |

Fund price and distribution information For the six-month period ended 1/31/23

| | | | | | |

| Distributions | Class A | Class B | Class C | Class R6 | Class Y |

| Number | 6 | 6 | 6 | 6 | 6 |

| Income1 | $0.162597 | $0.122989 | $0.112979 | $0.184113 | $0.181074 |

| Capital gains2 | — | — | — | — | — |

| Total | $0.162597 | $0.122989 | $0.112979 | $0.184113 | $0.181074 |

| | Before | After | Net | Net | Net | Net |

| | sales | sales | asset | asset | asset | asset |

| Share value | charge | charge | value | value | value | value |

| 7/31/22 | $14.00 | $14.32 | $14.01 | $14.04 | $14.00 | $14.01 |

| 1/31/23 | 13.96 | 14.28 | 13.97 | 13.99 | 13.96 | 13.96 |

| | Before | After | Net | Net | Net | Net |

| Current rate | sales | sales | asset | asset | asset | asset |

| (end of period) | charge | charge | value | value | value | value |

| Current dividend rate3 | 2.34% | 2.29% | 1.75% | 1.60% | 2.61% | 2.59% |

| Taxable equivalent4 | 3.95 | 3.87 | 2.96 | 2.70 | 4.41 | 4.38 |

| Current 30-day | | | | | | |

| SEC yield (with | | | | | | |

| expense limitation)5 | N/A | 2.45 | 1.91 | 1.76 | 2.77 | 2.75 |

| Taxable equivalent4 | N/A | 4.14 | 3.23 | 2.97 | 4.68 | 4.65 |

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (2.25% for class A shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

1 For some investors, investment income may be subject to the federal alternative minimum tax.

2 Capital gains, if any, are taxable for federal and, in most cases, state purposes.

3 Most recent distribution, including any return of capital and excluding capital gains, annualized and divided by share price before or after sales charge at period-end.

4 Assumes maximum 40.80% federal tax rate for 2022. Results for investors subject to lower tax rates would not be as advantageous.

5 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

|

| Strategic Intermediate Municipal Fund 11 |

Annualized fund performance as of most recent calendar quarter

Total return for periods ended 12/31/22

| | | | | | |

| | Life of fund | 10 years | 5 years | 3 years | 1 year | 6 months |

| Class A (9/20/93) | | | | | | |

| Before sales charge | 5.20% | 2.15% | 1.46% | –0.36% | –7.21% | 0.53% |

| After sales charge | 5.13 | 1.92 | 1.00 | –1.11 | –9.29 | –1.73 |

| Class B (9/9/85) | | | | | | |

| Before CDSC | 5.20 | 1.65 | 0.84 | –0.95 | –7.75 | 0.20 |

| After CDSC | 5.20 | 1.65 | 0.50 | –1.87 | –12.30 | –4.76 |

| Class C (7/26/99) | | | | | | |

| Before CDSC | 5.16 | 1.53 | 0.70 | –1.08 | –7.88 | 0.13 |

| After CDSC | 5.16 | 1.53 | 0.70 | –1.08 | –8.80 | –0.87 |

| Class R6 (5/22/18) | | | | | | |

| Net asset value | 5.11 | 2.40 | 1.72 | –0.08 | –6.90 | 0.67 |

| Class Y (1/2/08) | | | | | | |

| Net asset value | 5.11 | 2.40 | 1.71 | –0.10 | –6.92 | 0.61 |

See the discussion following the fund performance table on page 8 for information about the calculation of fund performance.

Returns for periods of less than one year are not annualized.

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

| | | | | |

| | Class A | Class B | Class C | Class R6 | Class Y |

| Total annual operating expenses for the fiscal | | | | | |

| year ended 7/31/22* | 0.84% | 1.44% | 1.59% | 0.58% | 0.59% |

| Annualized expense ratio for the six-month | | | | | |

| period ended 1/31/23† | 0.84% | 1.44% | 1.59% | 0.57% | 0.59% |

Fiscal year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report.

Expenses are shown as a percentage of average net assets.

* Restated to reflect current fees.

† Expense ratios for each class are for the fund’s most recent fiscal half year. As a result of this, ratios may differ from expense ratios based on one-year data in the financial highlights.

|

| 12 Strategic Intermediate Municipal Fund |

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in each class of the fund from 8/1/22 to 1/31/23. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | |

| | Class A | Class B | Class C | Class R6 | Class Y |

| Expenses paid per $1,000*† | $4.25 | $7.28 | $8.03 | $2.89 | $2.99 |

| Ending value (after expenses) | $1,009.20 | $1,006.20 | $1,004.70 | $1,010.80 | $1,009.80 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 1/31/23. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period (184); and then dividing that result by the number of days in the year (365).

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended 1/31/23, use the following calculation method. To find the value of your investment on 8/1/22, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | |

| | Class A | Class B | Class C | Class R6 | Class Y |

| Expenses paid per $1,000*† | $4.28 | $7.32 | $8.08 | $2.91 | $3.01 |

| Ending value (after expenses) | $1,020.97 | $1,017.95 | $1,017.19 | $1,022.33 | $1,022.23 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 1/31/23. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the six-month period; then multiplying the result by the number of days in the six-month period (184); and then dividing that result by the number of days in the year (365).

|

| Strategic Intermediate Municipal Fund 13 |

Consider these risks before investing

Capital gains, if any, are taxable for federal and, in most cases, state purposes. Income from federally tax-exempt funds may be subject to state and local taxes. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Bond investments may be more susceptible to downgrades or defaults during economic downturns or other periods of economic stress. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds. Unlike bonds, funds that invest in bonds have fees and expenses. The fund may invest significantly in particular segments of the tax-exempt debt market, making it more vulnerable to fluctuations in the values of the securities it holds than a fund that invests more broadly. Interest the fund receives might be taxable.

The value of investments in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including general economic, political, or financial market conditions; investor sentiment and market perceptions; government actions; geopolitical events or changes; and factors related to a specific issuer, geography, industry, or sector. These and other factors may lead to increased volatility and reduced liquidity in the fund’s portfolio holdings.

Our investment techniques, analyses, and judgments may not produce the outcome we intend. The investments we select for the fund may not perform as well as other securities that we do not select for the fund. We, or the fund’s other service providers, may experience disruptions or operating errors that could negatively impact the fund. You can lose money by investing in the fund.

|

| 14 Strategic Intermediate Municipal Fund |

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions. They are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 2.25% maximum sales charge for class A shares.

Net asset value (NAV) is the price, or value, of one share of a mutual fund, without a sales charge. Net asset values fluctuate with market conditions. They are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are closed to new investments and are only available by exchange from class B shares of another Putnam fund or through dividend and/or capital gains reinvestment. They are not subject to an initial sales charge and may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class R6 shares are not subject to an initial sales charge or CDSC and carry no 12b-1 fee. They are generally only available to employer-sponsored retirement plans, corporate and institutional clients, and clients in other approved programs.

Class Y shares are not subject to an initial sales charge or CDSC and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Fixed income terms

Current rate is the annual rate of return earned from dividends or interest of an investment. Current rate is expressed as a percentage of the price of a security, fund share, or principal investment.

Yield curve is a graph that plots the yields of bonds with equal credit quality against their differing maturity dates, ranging from shortest to longest. It is used as a benchmark for other debt, such as mortgage or bank lending rates.

Comparative indexes

Bloomberg 3-15 Year Blend Municipal Bond Index is an unmanaged index composed of investment-grade municipal securities ranging from 2 and 17 years in maturity.

Bloomberg Municipal Bond Index is an unmanaged index of long-term, fixed-rate, investment-grade tax-exempt bonds.

Bloomberg U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed income securities.

|

| Strategic Intermediate Municipal Fund 15 |

ICE BofA (Intercontinental Exchange Bank of America) U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

Putnam Strategic Intermediate Municipal Linked Benchmark represents the performance of the Bloomberg Municipal Bond Index through August 27, 2020, and the performance of the Bloomberg 3-15 Year Blend Municipal Bond Index thereafter.

S&P 500® Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approve or endorse this material, or guarantee the accuracy or completeness of any information herein, or make any warranty, express or implied, as to the results to be obtained therefrom, and to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith. You cannot invest directly in an index.

ICE Data Indices, LLC (“ICE BofA”), used with permission. ICE BofA permits use of the ICE BofA indices and related data on an “as is” basis; makes no warranties regarding same; does not guarantee the suitability, quality, accuracy, timeliness, and/or completeness of the ICE BofA indices or any data included in, related to, or derived therefrom; assumes no liability in connection with the use of the foregoing; and does not sponsor, endorse, or recommend Putnam Investments, or any of its products or services.

Lipper, a Refinitiv company, is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category medians reflect performance trends for funds within a category.

|

| 16 Strategic Intermediate Municipal Fund |

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single notice of internet availability, or a single printed copy, of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2022, are available in the Individual Investors section of putnam.com and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT within 60 days of the end of such fiscal quarter. Shareholders may obtain the fund’s Form N-PORT on the SEC’s website at www.sec.gov.

Prior to its use of Form N-PORT, the fund filed its complete schedule of its portfolio holdings with the SEC on Form N-Q, which is available online at www.sec.gov.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of January 31, 2023, Putnam employees had approximately $478,000,000 and the Trustees had approximately $64,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

|

| Strategic Intermediate Municipal Fund 17 |

Financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal period.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

|

| 18 Strategic Intermediate Municipal Fund |

| | |

| The fund’s portfolio 1/31/23 (Unaudited) | | |

|

Key to holding’s abbreviations

|

| AGM Assured Guaranty Municipal Corporation |

| BAM Build America Mutual |

| COP Certificates of Participation |

| FHA Insd. Federal Housing Administration Insured |

| FHLMC Coll. Federal Home Loan Mortgage Corporation Collateralized |

| FNMA Coll. Federal National Mortgage Association Collateralized |

| G.O. Bonds General Obligation Bonds |

| GNMA Coll. Government National Mortgage Association Collateralized |

| PSFG Permanent School Fund Guaranteed |

| VRDN Variable Rate Demand Notes, which are floating-rate securities with long-term maturities that carry coupons that reset and are payable upon demand either daily, weekly or monthly. The rate shown is the current interest rate at the close of the reporting period. Rates are set by remarketing agents and may take into consideration market supply and demand, credit quality and the current SIFMA Municipal Swap Index rate, which was 1.66% as of the close of the reporting period. |

|

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* | Rating** | | Principal amount | Value |

| Alabama (0.9%) |

| Black Belt Energy Gas Dist., Gas Supply Mandatory Put Bonds (3/1/27), Ser. D-1, 4.00%, 7/1/52 Mandatory Put Bonds (6/1/27), 6/1/27 | Aa1 | | $1,000,000 | $1,018,635 |

| Jefferson, Cnty. Rev. Bonds, (Refunding warrants) | | | | |

| 5.00%, 9/15/34 | AA | | 1,075,000 | 1,163,805 |

| 5.00%, 9/15/33 | AA | | 125,000 | 136,121 |

| Southeast Energy Auth. Commodity Supply | | | | |

| Mandatory Put Bonds (12/1/29), Ser. A-1, 5.50%, 1/1/53 | A1 | | 1,350,000 | 1,470,465 |

| Mandatory Put Bonds (8/1/28), Ser. B-1, 5.00%, 5/1/53 | A2 | | 3,000,000 | 3,145,326 |

| | | | 6,934,352 |

| Alaska (0.4%) |

| AK State Indl. Dev. & Export Auth. Rev. Bonds, (Tanana Chiefs Conference), Ser. A | | | | |

| 4.00%, 10/1/39 | A+/F | | 2,445,000 | 2,447,994 |

| 4.00%, 10/1/38 | A+/F | | 555,000 | 558,648 |

| | | | 3,006,642 |

| Arizona (1.3%) |

| AZ State Indl. Dev. Auth. Rev. Bonds | | | | |

| (Equitable School Revolving Fund), Ser. A, 5.00%, 11/1/38 | A | | 2,740,000 | 2,889,866 |

| (Equitable School Revolving Fund, LLC), 5.00%, 11/1/33 | A | | 1,000,000 | 1,081,766 |

| Glendale, Indl. Dev. Auth. Sr. Living Fac. Rev. Bonds, (Royal Oaks Life Care Cmnty.) | | | | |

| 4.00%, 5/15/31 | BBB−/F | | 1,000,000 | 925,713 |

| 4.00%, 5/15/29 | BBB−/F | | 1,000,000 | 946,047 |

| Pima Cnty., Indl. Dev. Auth. Sr. Living 144A Rev. Bonds, (La Posada at Park Centre, Inc.), 6.25%, 11/15/35 | BBB+/P | | 2,750,000 | 2,864,056 |

| Salt Verde, Fin. Corp. Gas Rev. Bonds, 5.50%, 12/1/29 | A3 | | 1,000,000 | 1,102,881 |

| | | | 9,810,329 |

| |

Strategic Intermediate Municipal Fund 19 |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| California (15.6%) |

| Anaheim, Union High School Dist. G.O. Bonds, 3.00%, 8/1/38 | Aa2 | | $3,000,000 | $2,714,738 |

| Antioch, Unified School Dist. G.O. Bonds, BAM, 3.00%, 8/1/34 | AA | | 1,185,000 | 1,175,507 |

| CA Cmnty. Choice Fin. Auth. Mandatory Put Bonds (8/1/28), (Green Bonds), Ser. A-1, 4.00%, 5/1/53 | A1 | | 9,675,000 | 9,828,565 |

| CA Cmnty. Hsg. Agcy. Essential Hsg. 144A Rev. Bonds, (Aster Apt.), Ser. A-1, 4.00%, 2/1/56 | BB+/P | | 250,000 | 220,805 |

| CA Hsg. Fin. Agcy. Muni. Certif. Rev. Bonds, Ser. 21-1, Class A, 3.50%, 11/20/35 | BBB+ | | 900,149 | 872,821 |

| CA Muni. Fin. Auth. VRDN (Chevron USA, Inc.), 0.65%, 11/1/35 | VMIG 1 | | 1,400,000 | 1,400,000 |

| CA Pub. Fin. Auth. VRDN, (Sharp Hlth. Care Oblig. Group), Ser. C, 0.45%, 8/1/52 | VMIG 1 | | 1,000,000 | 1,000,000 |

| CA State G.O. Bonds | | | | |

| 5.00%, 2/1/32 (Prerefunded 2/1/23) | Aa2 | | 10,000,000 | 10,000,000 |

| 3.00%, 10/1/36 | Aa2 | | 2,000,000 | 1,938,680 |

| CA State Charter School Fin. Auth. 144A Rev. Bonds, (Aspire Pub. Schools), 5.00%, 8/1/36 | BBB | | 3,225,000 | 3,294,893 |

| CA State Enterprise Dev. Auth. Student Hsg. Rev. Bonds, (Provident Group-SDSU Properties, LLC), Ser. A, 5.00%, 8/1/28 | Baa3 | | 150,000 | 161,552 |

| CA State Infrastructure & Econ. Dev. Bank | | | | |

| Mandatory Put Bonds (6/1/26), (Museum Associates), 2.36%, 12/1/50 | A3 | | 1,000,000 | 965,609 |

| Mandatory Put Bonds (8/1/24), (CA Academy of Sciences), 2.01%, 8/1/47 | A2 | | 1,500,000 | 1,480,643 |

| CA State Infrastructure & Econ. Dev. Bank Rev. Bonds, (Performing Arts Ctr. of Los Angeles Cnty.), 5.00%, 12/1/29 | A | | 675,000 | 778,221 |

| CA State Muni. Fin. Auth. Rev. Bonds | | | | |

| (CHF-Riverside II, LLC), 5.00%, 5/15/34 | Baa3 | | 915,000 | 968,856 |

| (HumanGood Oblig. Group), Ser. A, 4.00%, 10/1/32 | A−/F | | 1,000,000 | 1,023,503 |

| CA State Poll. Control Fin. Auth. Rev. Bonds, (San Jose Wtr. Co.), 4.75%, 11/1/46 | A | | 1,000,000 | 1,023,613 |

| CA State Pub. Wks. Board Rev. Bonds, Ser. E, 5.00%, 9/1/34 | Aa3 | | 900,000 | 934,482 |

| CA State U. Mandatory Put Bonds (11/1/26), Ser. B-2, 0.55%, 11/1/49 | Aa2 | | 1,000,000 | 893,024 |

| CA Statewide Cmnty. Dev. Auth. 144A Rev. Bonds, (Lancer Edl. Student Hsg.), Ser. A, 3.00%, 6/1/29 | BB/P | | 1,450,000 | 1,332,033 |

| Chula Vista, Muni. Fin. Auth. Special Tax Bonds, 5.50%, 9/1/30 | AA− | | 775,000 | 789,286 |

| Golden State Tobacco Securitization Corp. Rev. Bonds, Ser. B-1, 3.85%, 6/1/50 | BBB− | | 3,000,000 | 2,723,324 |

| Imperial Cnty., Local Trans. Auth. Sales Tax Rev. Bonds, Ser. E, AGM, 5.00%, 6/1/32 | AA | | 8,730,000 | 9,671,940 |

| Indio, Pub. Fin. Auth. Rev. Bonds, Ser. A, BAM | | | | |

| 5.00%, 11/1/33 | AA | | 425,000 | 501,088 |

| 5.00%, 11/1/32 | AA | | 350,000 | 415,738 |

| 5.00%, 11/1/31 | AA | | 375,000 | 441,138 |

| 5.00%, 11/1/30 | AA | | 400,000 | 466,565 |

| |

20 Strategic Intermediate Municipal Fund |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| California cont. |

| Indio, Pub. Fin. Auth. Rev. Bonds, Ser. A, BAM | | | | |

| 5.00%, 11/1/29 | AA | | $310,000 | $356,079 |

| 5.00%, 11/1/28 | AA | | 275,000 | 310,517 |

| Long Beach, Arpt. Syst. Rev. Bonds | | | | |

| Ser. B, AGM, 5.00%, 6/1/38 | AA | | 300,000 | 340,493 |

| Ser. B, AGM, 5.00%, 6/1/36 | AA | | 250,000 | 290,124 |

| Ser. A, AGM, 5.00%, 6/1/35 | AA | | 300,000 | 354,723 |

| Ser. B, AGM, 5.00%, 6/1/35 | AA | | 300,000 | 354,723 |

| Ser. A, AGM, 5.00%, 6/1/34 | AA | | 400,000 | 478,348 |

| Ser. B, AGM, 5.00%, 6/1/34 | AA | | 200,000 | 239,174 |

| Los Angeles Cnty., Dev. Auth. Multi-Fam. Hsg. Mandatory Put Bonds (7/1/26), (VA Building 402), 3.375%, 1/1/46 | Aaa | | 3,250,000 | 3,274,994 |

| Los Angeles, Dept. of Arpt. Rev. Bonds | | | | |

| Ser. H, 5.50%, 5/15/36 | Aa2 | | 3,000,000 | 3,487,361 |

| 5.00%, 5/15/31 | Aa3 | | 1,500,000 | 1,730,459 |

| Ser. A, 5.00%, 5/15/28 | Aa3 | | 1,500,000 | 1,659,133 |

| Ser. C, 5.00%, 5/15/28 | Aa3 | | 2,175,000 | 2,405,743 |

| Ser. A, 4.00%, 5/15/39 | Aa3 | | 1,500,000 | 1,493,145 |

| 4.00%, 5/15/35 | Aa3 | | 600,000 | 615,894 |

| Los Angeles, Dept. of Arpts. Rev. Bonds, Ser. A, 5.00%, 5/15/34 | Aa2 | | 5,700,000 | 5,935,200 |

| Los Angeles, Dept. of Wtr. & Pwr. Rev. Bonds | | | | |

| Ser. A, 5.00%, 7/1/42 | Aa2 | | 7,870,000 | 8,430,692 |

| Ser. B, 5.00%, 7/1/40 | Aa2 | | 2,800,000 | 3,252,054 |

| Port of Oakland Rev. Bonds | | | | |

| 5.00%, 5/1/28 | A2 | | 750,000 | 826,725 |

| 1.081%, 5/1/24 | A1 | | 620,000 | 593,127 |

| San Francisco, City & Cnty. Arpt. Comm. Intl. Arpt. Rev. Bonds, Ser. A | | | | |

| 5.00%, 5/1/35 | A1 | | 1,900,000 | 2,119,345 |

| 5.00%, 5/1/34 | A1 | | 4,585,000 | 5,165,259 |

| 5.00%, 5/1/30 | A1 | | 1,000,000 | 1,125,852 |

| 5.00%, 5/1/29 | A1 | | 2,000,000 | 2,228,097 |

| San Francisco, City & Cnty. Arpt. Comm. Intl. Arpt. VRDN, Ser. B, 1.05%, 5/1/58 | VMIG 1 | | 3,500,000 | 3,500,000 |

| San Francisco, Pub. Fac. Fin. Auth. Rev. Bonds | | | | |

| 5.00%, 6/1/39 | AA+ | | 475,000 | 533,816 |

| 5.00%, 6/1/38 | AA+ | | 400,000 | 450,697 |

| 5.00%, 6/1/37 | AA+ | | 350,000 | 396,131 |

| 5.00%, 6/1/36 | AA+ | | 325,000 | 370,379 |

| 5.00%, 6/1/35 | AA+ | | 280,000 | 322,001 |

| 5.00%, 6/1/34 | AA+ | | 250,000 | 290,170 |

| 5.00%, 6/1/33 | AA+ | | 255,000 | 296,793 |

| Sierra View, Local Hlth. Care Dist. Rev. Bonds | | | | |

| 5.00%, 7/1/30 | A/F | | 620,000 | 696,112 |

| 5.00%, 7/1/27 | A/F | | 625,000 | 678,201 |

| 4.00%, 7/1/26 | A/F | | 300,000 | 310,204 |

| 4.00%, 7/1/25 | A/F | | 290,000 | 296,600 |

| 4.00%, 7/1/24 | A/F | | 235,000 | 238,241 |

| 4.00%, 7/1/23 | A/F | | 260,000 | 261,109 |

| |

Strategic Intermediate Municipal Fund 21 |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| California cont. |

| U. of CA VRDN, Ser. AL-4, 0.40%, 5/15/48 | VMIG 1 | | $1,800,000 | $1,800,000 |

| Yucaipa Special Tax Bonds, (Cmnty. Fac. Dist. No. 98-1 Chapman Heights), 5.375%, 9/1/30 | A | | 375,000 | 376,875 |

| | | | 114,901,214 |

| Colorado (1.6%) |

| CO State Hlth. Fac. Auth. Hosp. Rev. Bonds, (CommonSpirit Hlth.), Ser. A, 5.00%, 11/1/25 | A− | | 350,000 | 369,041 |

| Denver City & Cnty., Arpt. Rev. Bonds | | | | |

| Ser. D, 5.75%, 11/15/36 | Aa3 | | 3,000,000 | 3,791,688 |

| Ser. B, 5.00%, 11/15/42 | Aa3 | | 1,125,000 | 1,268,311 |

| E-470 Pub. Hwy. Auth. Mandatory Put Bonds (9/1/24), Ser. B, 3.231%, 9/1/39 | A2 | | 4,000,000 | 3,983,526 |

| Regl. Trans. Dist. Rev. Bonds, (Denver Transit Partners, LLC), 3.00%, 7/15/37 | Baa1 | | 850,000 | 734,282 |

| Vauxmont, Metro. Dist. G.O. Bonds, AGM | | | | |

| 5.00%, 12/1/34 | AA | | 285,000 | 320,195 |

| 5.00%, 12/1/32 | AA | | 250,000 | 283,817 |

| 5.00%, 12/15/30 | AA | | 125,000 | 134,685 |

| 5.00%, 12/15/29 | AA | | 125,000 | 134,700 |

| 5.00%, 12/15/27 | AA | | 125,000 | 134,756 |

| 5.00%, 12/15/25 | AA | | 125,000 | 133,837 |

| 5.00%, 12/1/25 | AA | | 175,000 | 186,766 |

| | | | 11,475,604 |

| Connecticut (1.2%) |

| CT State Hlth. & Edl. Fac. Auth. Mandatory Put Bonds (7/1/26), (Yale U.), Ser. A-2, 2.00%, 7/1/42 | Aaa | | 1,050,000 | 1,011,035 |

| CT State Hlth. & Edl. Fac. Auth. Rev. Bonds | | | | |

| (Masonicare Issue), Ser. F, 5.00%, 7/1/34 | BBB+/F | | 1,250,000 | 1,251,110 |

| (Masonicare Issue), Ser. F, 5.00%, 7/1/33 | BBB+/F | | 250,000 | 250,844 |

| (Stamford Hosp. Oblig. Group (The)), Ser. M, 5.00%, 7/1/32 | BBB+ | | 1,400,000 | 1,604,328 |

| (U. of New Haven), 5.00%, 7/1/28 | BBB− | | 550,000 | 573,649 |

| (Stamford Hosp. Oblig. Group (The)), Ser. L-1, 4.00%, 7/1/26 | BBB+ | | 700,000 | 714,437 |

| (Yale U.), Ser. A-1, 0.50%, 7/1/42 | Aaa | | 1,450,000 | 1,450,000 |

| CT State Hsg. Fin. Auth. Rev. Bonds, Ser. B-1 | | | | |

| 4.15%, 11/15/44 | Aaa | | 1,355,000 | 1,349,106 |

| 4.10%, 11/15/39 | Aaa | | 565,000 | 565,456 |

| | | | 8,769,965 |

| District of Columbia (1.8%) |

| DC Rev. Bonds | | | | |

| (KIPP DC), Ser. A, 5.00%, 7/1/48 | BBB+ | | 1,250,000 | 1,261,978 |

| (Latin American Montessori Bilingual Pub. Charter School Oblig. Group), 4.00%, 6/1/30 | BB+ | | 1,000,000 | 976,343 |

| Metro. DC Arpt. Auth. Rev. Bonds, Ser. A | | | | |

| 5.00%, 10/1/43 | Aa3 | | 3,650,000 | 3,836,275 |

| 5.00%, 10/1/31 | Aa3 | | 1,000,000 | 1,118,771 |

| 5.00%, 10/1/30 | Aa3 | | 4,410,000 | 5,025,139 |

| |

22 Strategic Intermediate Municipal Fund |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| District of Columbia cont. |

| Metro. Washington DC, Arpt. Auth. Dulles Toll Rd. Rev. Bonds | | | | |

| (Dulles Metrorail & Cap. Impt. Proj.) 4.00%, 10/1/53 T | A− | | $660,000 | $619,004 |

| (Dulles Metrorail & Cap. Impt. Proj.) Ser. B, 4.00%, 10/1/44 T | A− | | 665,000 | 649,853 |

| | | | 13,487,363 |

| Florida (4.8%) |

| Cap. Trust Agcy. 144A Rev. Bonds, (WFCS Holdings II, LLC), Ser. A-1, 3.30%, 1/1/31 | BB/P | | 480,000 | 437,191 |

| Double Branch Cmnty. Dev. Dist. Special Assmt. Bonds, Ser. A-1, 4.25%, 5/1/34 | A | | 360,000 | 360,576 |

| FL State Dept. of Mgt. Svcs. COP, Ser. A, 3.00%, 11/1/35 | Aa1 | | 1,000,000 | 975,040 |

| FL State Dev. Fin. Corp. Ed. Fac. Rev. Bonds, (River City Ed.), 5.00%, 7/1/31 | Baa3 | | 325,000 | 346,000 |

| FL State Dev. Fin. Corp. Ed. Fac. 144A Rev. Bonds, (Drs. Kiran & Pallavi Patel 2017 Foundation for Global Understanding Inc.), 3.00%, 7/1/31 | BB/P | | 200,000 | 183,132 |

| Greater Orlando, Aviation Auth. Arpt. Fac. Rev. Bonds, Ser. A, 5.00%, 10/1/35 | A1 | | 7,500,000 | 7,974,637 |

| Halifax Hosp. Med. Ctr. Rev. Bonds, 5.00%, 6/1/36 | A− | | 1,375,000 | 1,432,063 |

| Orange Cnty., HFA Mandatory Put Bonds (9/1/23), (Dunwoodie Place Preservation, Ltd.), Ser. A, 0.20%, 9/1/24 | AA+ | | 1,920,000 | 1,875,634 |

| Orange Cnty., Hlth. Fac. Auth. Rev. Bonds | | | | |

| (Orlando Hlth.), 5.00%, 10/1/40 | A+ | | 1,000,000 | 1,103,288 |

| (Orlando Hlth.), 5.00%, 10/1/39 | A+ | | 1,500,000 | 1,664,119 |

| (Orlando Hlth.), 5.00%, 10/1/38 | A+ | | 1,000,000 | 1,114,958 |

| (Presbyterian Retirement Cmntys.), 5.00%, 8/1/34 | A−/F | | 1,000,000 | 1,021,515 |

| Orlando Cmnty. Redev. Agcy. Tax Alloc. Bonds, (Republic Drive/Universal), 5.00%, 4/1/23 | A+/F | | 1,630,000 | 1,633,026 |

| Palm Beach Cnty., 144A Rev. Bonds, (Provident Group-LU Properties, LLC), 4.25%, 6/1/31 | BB−/P | | 1,200,000 | 1,143,941 |

| Palm Beach Cnty., Hlth. Fac. Auth. Rev. Bonds, (Acts Retirement-Life Cmnty., Inc.), 5.00%, 11/15/32 | A−/F | | 2,000,000 | 2,055,344 |

| Palm Beach Cnty., School Board COP, Ser. C, 5.00%, 8/1/31 | Aa3 | | 5,400,000 | 5,582,020 |

| Sarasota Cnty., Pub. Hosp. Dist. Rev. Bonds, 5.00%, 7/1/38 | A1 | | 5,000,000 | 5,329,648 |

| Southeast Overtown Park West Cmnty. Redev. Agcy. 144A Tax Alloc. Bonds, Ser. A-1, 5.00%, 3/1/30 | BBB+ | | 240,000 | 244,778 |

| St. John’s Cnty., Indl. Dev. Auth. Rev. Bonds, (Life Care Ponte Vedra Oblig. Group), Ser. A | | | | |

| 4.00%, 12/15/31 | BB+/F | | 200,000 | 185,125 |

| 4.00%, 12/15/30 | BB+/F | | 195,000 | 182,191 |

| 4.00%, 12/15/29 | BB+/F | | 215,000 | 202,499 |

| Village, 144A Special Assmt., (Village Cmnty. Dev. Dist. No. 13), 1.875%, 5/1/25 | BB−/P | | 515,000 | 489,670 |

| | | | 35,536,395 |

| |

Strategic Intermediate Municipal Fund 23 |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| Georgia (2.3%) |

| Burke Cnty., Dev. Auth. Poll. Control | | | | |

| Mandatory Put Bonds (8/19/25), (GA Pwr. Co.), 2.875%, 12/1/49 | Baa1 | | $4,250,000 | $4,179,884 |

| Mandatory Put Bonds (5/25/23), (GA Power Co.), 2.25%, 10/1/32 | Baa1 | | 4,000,000 | 3,983,318 |

| Mandatory Put Bonds (2/3/25), (Oglethorpe Pwr. Corp.), 1.50%, 1/1/40 | Baa1 | | 1,600,000 | 1,527,142 |

| Main Street Natural Gas, Inc. Gas Supply Mandatory Put Bonds (9/1/23), Ser. B, 3.677%, 4/1/48 | Aa1 | | 2,200,000 | 2,199,885 |

| Muni. Election Auth. of GA Rev. Bonds | | | | |

| (Plant Vogtle Units 3 & 4), AGM, 5.00%, 7/1/39 | AA | | 1,000,000 | 1,111,586 |

| (Plant Vogtle Units 3 & 4), AGM, 5.00%, 7/1/36 | AA | | 1,000,000 | 1,136,299 |

| Ser. A, 5.00%, 1/1/34 | A2 | | 2,295,000 | 2,539,419 |

| (Plant Vogtle Units 3 & 4), 4.00%, 1/1/46 | BBB+ | | 330,000 | 303,747 |

| | | | 16,981,280 |

| Illinois (4.7%) |

| Chicago, G.O. Bonds, Ser. A | | | | |

| 5.00%, 1/1/35 | BBB+ | | 3,000,000 | 3,220,654 |

| 4.00%, 1/1/36 | BBB+ | | 1,000,000 | 972,327 |

| Chicago, Board of Ed. G.O. Bonds, Ser. A, 5.00%, 12/1/39 | BB | | 1,000,000 | 1,024,395 |

| Chicago, O’Hare Intl. Arpt. Rev. Bonds, Ser. B, 5.00%, 1/1/33 | A+ | | 5,465,000 | 5,701,702 |

| Chicago, Waste Wtr. Transmission Rev. Bonds | �� | | | |

| 5.00%, 1/1/44 | A | | 500,000 | 501,926 |

| Ser. C, 5.00%, 1/1/39 | A | | 750,000 | 758,308 |

| (2nd Lien), 5.00%, 1/1/39 | A | | 565,000 | 568,042 |

| Ser. C, 5.00%, 1/1/34 | A | | 400,000 | 409,439 |

| Ser. C, 5.00%, 1/1/33 | A | | 405,000 | 414,987 |

| Chicago, Wtr. Wks Rev. Bonds, 5.00%, 11/1/39 | A | | 675,000 | 684,438 |

| IL State G.O. Bonds | | | | |

| 5.00%, 11/1/41 | Baa1 | | 600,000 | 612,492 |

| 5.00%, 1/1/41 | Baa1 | | 340,000 | 346,073 |

| 5.00%, 11/1/34 | Baa1 | | 1,650,000 | 1,717,900 |

| Ser. C, 5.00%, 11/1/29 | Baa1 | | 1,225,000 | 1,308,848 |

| Ser. D, 5.00%, 11/1/28 | Baa1 | | 2,080,000 | 2,231,917 |

| Ser. D, 5.00%, 11/1/27 | Baa1 | | 920,000 | 991,871 |

| 4.125%, 11/1/31 | Baa1 | | 830,000 | 845,752 |

| 4.00%, 1/1/31 | Baa1 | | 695,000 | 704,109 |

| IL State Fin. Auth. | | | | |

| Mandatory Put Bonds (8/15/25), (U. of Chicago Med. Ctr.), Ser. B-1, 5.00%, 8/15/52 | AA+ | | 2,350,000 | 2,471,081 |

| Mandatory Put Bonds (11/15/26), (OSF Hlth. Care Syst. Oblig. Group), Ser. B-2, 5.00%, 5/15/50 | A | | 1,000,000 | 1,067,690 |

| IL State Fin. Auth. Rev. Bonds | | | | |

| (Ascension Hlth. Credit Group), Ser. C, 5.00%, 2/15/34 | AA+ | | 1,100,000 | 1,183,436 |

| (Rosalind Franklin U. of Medicine and Science), Ser. A, 5.00%, 8/1/31 | BBB+ | | 400,000 | 421,112 |

| (Art Institute of Chicago (The)), 5.00%, 3/1/30 | AA | | 1,500,000 | 1,608,151 |

| |

24 Strategic Intermediate Municipal Fund |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| Illinois cont. |

| IL State Fin. Auth. Student Hsg. & Academic Fac. Rev. Bonds | | | | |

| (U. of IL Chicago), 5.00%, 2/15/50 | Baa3 | | $460,000 | $457,311 |

| (CHF-Chicago, LLC), 5.00%, 2/15/47 | Baa3 | | 500,000 | 500,994 |

| Metro. Pier & Exposition Auth. Rev. Bonds, (McCormick Place Expansion), Ser. B, 5.00%, 12/15/33 | A− | | 300,000 | 313,693 |

| Metro. Wtr. Reclamation Dist. of Greater Chicago G.O. Bonds, Ser. A, 5.00%, 12/1/31 | AA+ | | 1,000,000 | 1,088,935 |

| Romeoville, Rev. Bonds, (Lewis U.) | | | | |

| 5.00%, 10/1/29 | BBB | | 975,000 | 991,669 |

| 5.00%, 10/1/27 | BBB | | 860,000 | 875,530 |

| 5.00%, 10/1/26 | BBB | | 500,000 | 509,092 |

| | | | 34,503,874 |

| Indiana (1.3%) |

| IN State. Fin. Auth. Rev. Bonds, (Rose-Hulman Inst. of Tech., Inc.) | | | | |

| 5.00%, 6/1/32 | A2 | | 200,000 | 227,279 |

| 5.00%, 6/1/31 | A2 | | 200,000 | 227,675 |

| 5.00%, 6/1/30 | A2 | | 200,000 | 228,530 |

| 5.00%, 6/1/29 | A2 | | 175,000 | 197,119 |

| 5.00%, 6/1/28 | A2 | | 100,000 | 110,847 |

| 5.00%, 6/1/27 | A2 | | 180,000 | 196,188 |

| 4.00%, 6/1/34 | A2 | | 235,000 | 245,474 |

| 4.00%, 6/1/33 | A2 | | 210,000 | 220,957 |

| Indianapolis, Local Pub. Impt. Bond Bk. Rev. Bonds, Ser. A | | | | |

| 5.25%, 2/1/54 | Aa1 | | 1,500,000 | 1,617,391 |

| 5.00%, 2/1/44 | Aa1 | | 1,175,000 | 1,268,926 |

| Rockport, Poll. Control Rev. Bonds, (AEP Generating Co.), 3.125%, 7/1/25 | A− | | 4,150,000 | 4,120,411 |

| Silver Creek, School Bldg. Corp. Rev. Bonds | | | | |

| 3.00%, 1/15/36 | AA+ | | 500,000 | 488,100 |

| 3.00%, 1/15/34 | AA+ | | 375,000 | 378,576 |

| | | | 9,527,473 |

| Iowa (0.3%) |

| IA State Fin. Auth. Rev. Bonds, (Lifespace Cmnty., Inc. Oblig. Group), Ser. A, 4.00%, 5/15/46 | BBB/F | | 1,150,000 | 843,707 |

| IA State Fin. Auth. Solid Waste Fac. Mandatory Put Bonds (4/1/24), (Gevo NW Iowa RNG, LLC), 1.50%, 1/1/42 | Aa3 | | 1,700,000 | 1,672,064 |

| | | | 2,515,771 |

| Kentucky (2.9%) |

| KY Pub. Trans. Infrastructure Auth. Rev. Bonds, (1st Tier Downtown Crossing), Ser. A, 6.00%, 7/1/53 (Prerefunded 7/1/23) | Baa2 | | 500,000 | 506,045 |

| KY State Hsg. Corp. Mandatory Put Bonds (10/1/23), (Winterwood II Rural Hsg.), 0.37%, 10/1/24 | Aaa | | 1,295,000 | 1,263,169 |

| KY State Property & Bldg. Comm. Rev. Bonds, (No. 127), Ser. A, 5.00%, 6/1/36 | A1 | | 5,500,000 | 6,305,617 |

| |

Strategic Intermediate Municipal Fund 25 |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| Kentucky cont. |

| KY State Pub. Energy Auth. Gas Supply | | | | |

| Mandatory Put Bonds (6/1/25), Ser. C-1, 4.00%, 12/1/49 | A1 | | $3,150,000 | $3,159,380 |

| Mandatory Put Bonds (1/1/25), Ser. B, 4.00%, 1/1/49 | A1 | | 2,800,000 | 2,800,267 |

| Louisville & Jefferson Cnty., Metro. Govt. Hlth. Syst. Rev. Bonds, (Norton Healthcare, Inc.), Ser. A, 5.00%, 10/1/30 | A | | 2,750,000 | 2,937,178 |

| Louisville and Jefferson Cnty., Metro. Govt. Poll. Control Mandatory Put Bonds (7/1/26), (Louisville Gas and Elec. Co.), 1.75%, 2/1/35 | A1 | | 5,000,000 | 4,739,257 |

| | | | 21,710,913 |

| Louisiana (0.3%) |

| LA Stadium & Exposition Dist. Rev. Bonds, 4.00%, 7/3/23 | BBB+/F | | 500,000 | 500,554 |

| St. John The Baptist Parish Mandatory Put Bonds (7/1/26), (Marathon Oil Corp.), Ser. A-3, 2.20%, 6/1/37 | Baa3 | | 2,000,000 | 1,886,150 |

| | | | 2,386,704 |

| Maryland (0.2%) |

| Frederick Cnty., Edl. Fac. 144A Rev. Bonds, (Mount. St. Mary’s U., Inc.), Ser. A, 5.00%, 9/1/27 | BB+ | | 1,000,000 | 1,017,231 |

| Gaithersburg, Econ. Dev. Rev. Bonds, (Asbury, Oblig. Group), Ser. A, 5.00%, 1/1/36 | BBB/F | | 300,000 | 302,978 |

| MD State Hlth. & Higher Ed. Fac. Auth. Rev. Bonds, (Stevenson U.), 4.00%, 6/1/34 | BBB− | | 250,000 | 256,413 |

| | | | 1,576,622 |

| Massachusetts (3.2%) |

| Lawrence, G.O. Bonds, 4.00%, 6/1/35 | AA | | 1,165,000 | 1,248,687 |

| MA State G.O. Bonds, Ser. A, 5.25%, 4/1/47 | Aa1 | | 1,500,000 | 1,607,672 |

| MA State Dev. Fin. Agcy. 144A Rev. Bonds, (Loomis Oblig. Group), 4.00%, 1/1/26 | BBB | | 470,000 | 467,306 |

| MA State Dev. Fin. Agcy. VRDN (Boston U.), Ser. U-6C, 1.15%, 10/1/42 | VMIG 1 | | 950,000 | 950,000 |

| MA State Hlth. & Edl. Fac. Auth. VRDN (Baystate Total Home Care, Inc.), 1.15%, 7/1/39 | A-1+ | | 1,500,000 | 1,500,000 |

| MA State Hsg. Fin. Agcy. Mandatory Put Bonds (6/1/25), Ser. 216, FHLMC Coll., FNMA Coll., GNMA Coll., 1.85%, 12/1/50 | Aa1 | | 1,000,000 | 964,776 |

| MA State Hsg. Fin. Agcy. Rev. Bonds, Ser. D, 3.10%, 6/1/30 | AA+ | | 720,000 | 719,939 |

| MA State Port Auth. Rev. Bonds, Ser. B, 5.00%, 7/1/39 | Aa2 | | 4,935,000 | 5,015,737 |

| MA State Wtr. Resource Auth. VRDN, Ser. A-3, 1.88%, 8/1/37 | VMIG 1 | | 1,500,000 | 1,500,000 |

| Merrimack Valley Regl. Transit Auth. Rev. Bonds, 3.25%, 6/23/23 | Aa1 | | 9,320,000 | 9,327,426 |

| | | | 23,301,543 |

| Michigan (2.3%) |

| Detroit, G.O. Bonds, 5.50%, 4/1/34 | Ba2 | | 660,000 | 719,077 |

| Kentwood, Economic Dev. Corp. Rev. Bonds, (Holland Home Oblig. Group), 5.00%, 11/15/37 | BBB−/F | | 1,000,000 | 1,006,777 |

| |

26 Strategic Intermediate Municipal Fund |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| Michigan cont. |

| MI State Fin. Auth. Rev. Bonds | | | | |

| Ser. H-1, 5.00%, 10/1/39 (Prerefunded 10/1/24) | AA− | | $525,000 | $538,332 |

| (Local Govt. Loan Program — Detroit Wtr. & Swr. Dept. (DWSD)), Ser. C, 5.00%, 7/1/35 | A+ | | 1,000,000 | 1,041,835 |

| (Detroit Wtr. & Swr.), Ser. C-6, 5.00%, 7/1/33 | AA− | | 140,000 | 143,933 |

| (Great Lakes Wtr. Auth. Wtr. Supply Syst.), 5.00%, 7/1/31 | AA− | | 6,500,000 | 6,690,806 |

| (Detroit), Ser. C-3, 5.00%, 4/1/28 | Aa2 | | 700,000 | 758,062 |

| (Tobacco Settlement), Ser. A-1, 2.326%, 6/1/30 | A | | 497,786 | 476,815 |

| MI State Fin. Auth. Ltd. Oblig. Rev. Bonds | | | | |

| (Lawrence Technological U.), 5.25%, 2/1/32 | BBB− | | 1,145,000 | 1,183,467 |

| (Lawrence Technological U.), 5.00%, 2/1/47 | BBB− | | 2,000,000 | 1,914,881 |

| (Lawrence Tech. U.), 4.00%, 2/1/32 | BBB− | | 285,000 | 275,664 |

| (Lawrence Tech. U.), 4.00%, 2/1/27 | BBB− | | 185,000 | 182,751 |

| Wayne Cnty., Arpt. Auth. Rev. Bonds, Ser. F, 5.00%, 12/1/30 | A1 | | 1,840,000 | 1,938,920 |

| | | | 16,871,320 |

| Minnesota (2.4%) |

| Duluth, COP, (Indpt. School Dist. No. 709), Ser. A, 4.20%, 3/1/34 | Baa3 | | 750,000 | 719,752 |

| Duluth, Econ. Dev. Auth. Rev. Bonds, (Benedictine Hlth. Syst. Oblig. Group), Ser. A, 4.00%, 7/1/31 | BB/P | | 625,000 | 587,395 |

| Duluth, Econ. Dev. Auth. Hlth. Care Fac. Rev. Bonds, (St. Luke’s Hosp. of Duluth Oblig. Group) | | | | |

| 5.00%, 6/15/32 | BBB− | | 975,000 | 1,070,436 |

| 5.00%, 6/15/30 | BBB− | | 830,000 | 898,391 |

| Hennepin Cnty., VRDN, Ser. B, 1.65%, 12/1/38 | A-1+ | | 410,000 | 410,000 |

| JPM-Putters-XM0872, VRDN, 1.81%, 11/15/26 | A-1 | | 4,925,000 | 4,925,000 |

| Minneapolis & St. Paul, Hsg. & Redev. Auth. Hlth. Care VRDN, (Allina Hlth. Syst.), Ser. B-1, 1.20%, 11/15/35 | VMIG 1 | | 500,000 | 500,000 |

| Minneapolis & St. Paul, Metro. Arpt. Comm. Rev. Bonds, Ser. A, 5.00%, 1/1/31 | AA− | | 1,580,000 | 1,732,965 |

| Minneapolis, Hlth. Care Syst. VRDN (Fairview Hlth. Svcs. Oblig. Group), Ser. B, 2.10%, 11/15/48 | VMIG 1 | | 1,500,000 | 1,500,000 |

| MN State Higher Ed. Fac. Auth. Rev. Bonds, (Augsburg U.), Ser. A, 5.00%, 5/1/46 | Ba1 | | 750,000 | 708,584 |

| Ramsey, Charter School Rev. Bonds, (PACT Charter School), Ser. A, 5.00%, 6/1/32 | BB+ | | 1,400,000 | 1,403,669 |

| Rochester, Hlth. Care Fac. VRDN, (Mayo Clinic), Ser. B, 1.90%, 11/15/38 | VMIG 1 | | 250,000 | 250,000 |

| St. Paul, Hsg. & Redev. Auth. Charter School Lease Rev. Bonds, (Hmong College Prep Academy), 5.50%, 9/1/36 | BB+ | | 3,000,000 | 3,039,767 |

| | | | 17,745,959 |

| Mississippi (0.8%) |

| MS Bus. Fin. Comm. VRDN (Chevron USA, Inc.) | | | | |

| Ser. C, 1.20%, 12/1/30 | VMIG 1 | | 1,000,000 | 1,000,000 |

| Ser. F, 1.20%, 12/1/30 | VMIG 1 | | 4,565,000 | 4,565,000 |

| MS State Bus. Fin. Corp. Rev. Bonds, (System Energy Resources, Inc.), 2.375%, 6/1/44 | A | | 770,000 | 541,186 |

| | | | 6,106,186 |

| |

Strategic Intermediate Municipal Fund 27 |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| Missouri (0.7%) |

| Kansas City, Indl. Dev. Auth. Arpt. Special Oblig. Rev. Bonds | | | | |

| (Kansas City, Intl. Arpt.), 5.00%, 3/1/32 | A2 | | $1,000,000 | $1,098,195 |

| (Kansas City Intl. Arpt.), 5.00%, 3/1/30 | A2 | | 1,540,000 | 1,719,533 |

| Plaza at Noah’s Ark Cmnty. Impt. Dist. Rev. Bonds | | | | |

| 3.00%, 5/1/26 | B+/P | | 275,000 | 263,457 |

| 3.00%, 5/1/25 | B+/P | | 225,000 | 218,367 |

| 3.00%, 5/1/24 | B+/P | | 200,000 | 196,725 |

| St. Louis, Arpt. Rev. Bonds, 5.00%, 7/1/30 | A2 | | 1,430,000 | 1,609,577 |

| | | | 5,105,854 |

| Montana (0.4%) |

| MT State Board of Regents Higher Ed. Mandatory Put Bonds (11/15/32), U. of MT, AGM, 5.25%, 11/15/52 T | AA | | 2,475,000 | 2,782,843 |

| | | | 2,782,843 |

| Nebraska (0.6%) |

| Central Plains, Energy Mandatory Put Bonds (1/1/24), (No. 4), 5.00%, 3/1/50 | A2 | | 2,500,000 | 2,527,554 |

| Omaha, Pub. Pwr. Dist. Rev. Bonds, Ser. A | | | | |

| 5.00%, 2/1/39 | Aa2 | | 1,000,000 | 1,155,987 |

| 5.00%, 2/1/38 | Aa2 | | 1,000,000 | 1,161,272 |

| | | | 4,844,813 |

| Nevada (1.5%) |

| Clark Cnty., School Dist. G.O. Bonds | | | | |

| Ser. A, 5.00%, 6/15/37 | A1 | | 5,000,000 | 5,703,061 |

| Ser. C, 5.00%, 6/15/28 | A1 | | 4,000,000 | 4,289,180 |

| Ser. B, BAM, 3.00%, 6/15/36 | AA | | 1,000,000 | 925,271 |

| | | | 10,917,512 |

| New Hampshire (0.4%) |

| National Fin. Auth. Rev. Bonds, (Caritas Acquisitions VII, LLC), Ser. A, 3.75%, 8/15/30 | BBB/P | | 1,050,000 | 987,295 |

| NH State Hlth. & Ed. Fac. Auth. Rev. Bonds, (Southern NH Med. Ctr.), 5.00%, 10/1/37 | A− | | 2,000,000 | 2,058,122 |

| | | | 3,045,417 |

| New Jersey (2.4%) |

| NJ State G.O. Bonds, (Covid-19 Emergency Bonds), Ser. A, 3.00%, 6/1/32 | A2 | | 4,000,000 | 4,059,280 |

| NJ State Econ. Dev. Auth. Mandatory Put Bonds (12/3/29), (American Water Co., Inc.), 2.20%, 10/1/39 | A1 | | 3,500,000 | 3,099,955 |

| NJ State Econ. Dev. Auth. Rev. Bonds, Ser. AAA, 5.00%, 6/15/36 | A3 | | 350,000 | 368,350 |

| NJ State Edl. Fac. Auth. Rev. Bonds, (William Paterson U. of NJ (The)), Ser. C, AGM | | | | |

| 5.00%, 7/1/27 | AA | | 100,000 | 109,597 |

| 5.00%, 7/1/26 | AA | | 100,000 | 107,468 |

| 5.00%, 7/1/25 | AA | | 100,000 | 105,327 |

| 5.00%, 7/1/24 | AA | | 100,000 | 103,104 |

| NJ State Hlth. Care Fac. Fin. Auth. VRDN, (AHS Hosp. Corp.), Ser. B, 1.55%, 7/1/36 | VMIG 1 | | 4,000,000 | 4,000,000 |

| |

28 Strategic Intermediate Municipal Fund |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| New Jersey cont. |

| NJ State Trans. Trust Fund Auth. Rev. Bonds | | | | |

| Ser. BB, 5.00%, 6/15/34 | A3 | | $675,000 | $770,093 |

| (Federal Hwy. Reimbursement Notes), 5.00%, 6/15/28 | A+ | | 750,000 | 808,314 |

| South Jersey, Trans. Auth. Syst. Rev. Bonds, Ser. A | | | | |

| 5.00%, 11/1/40 | BBB+ | | 2,500,000 | 2,661,180 |

| 5.00%, 11/1/38 | BBB+ | | 1,140,000 | 1,226,780 |

| BAM, 5.00%, 11/1/37 | AA | | 250,000 | 279,620 |

| | | | 17,699,068 |

| New Mexico (0.3%) |

| Farmington, Poll. Control Rev. Bonds, (Pub. Service Co. of NM), Ser. B, 2.15%, 4/1/33 | Baa2 | | 2,000,000 | 1,680,572 |

| Sante Fe, Retirement Fac. Rev. Bonds, (El Castillo Retirement Res.), 5.00%, 5/15/42 | BB+/F | | 980,000 | 866,763 |

| | | | 2,547,335 |

| New York (15.9%) |

| Albany, Cap. Resource Corp. Rev. Bonds, (Empire Commons Student Hsg., Inc.) | | | | |

| 5.00%, 5/1/26 | A | | 400,000 | 423,414 |

| Ser. A, 5.00%, 5/1/25 | A | | 645,000 | 671,802 |

| 5.00%, 5/1/24 | A | | 575,000 | 588,806 |

| 5.00%, 5/1/23 | A | | 795,000 | 798,887 |

| Build NY City Resource Corp. Rev. Bonds | | | | |

| (Global Cmnty. Charter School), 4.00%, 6/15/32 | BB+ | | 500,000 | 483,638 |

| (Grand Concourse Academy Charter School), 3.40%, 7/1/27 | BBB− | | 300,000 | 300,359 |

| Build NY City Resource Corp. 144A Rev. Bonds, (East Harlem Scholars Academy Charter School), 5.00%, 6/1/32 | BB+ | | 375,000 | 388,708 |

| NY City, G.O. Bonds, Ser. B-1, 5.25%, 10/1/39 | Aa2 | | 2,500,000 | 2,934,794 |

| NY City, VRDN | | | | |

| Ser. I-2, 1.25%, 3/1/40 | VMIG 1 | | 3,600,000 | 3,600,000 |

| Ser. I-4, 1.15%, 4/1/36 | VMIG 1 | | 3,000,000 | 3,000,000 |

| NY City, Hsg. Dev. Corp. Mandatory Put Bonds (12/22/26), (Sustainable Dev.), Ser. F-2-B, FHA Insd., 3.40%, 11/1/62 | AA+ | | 12,750,000 | 12,860,632 |

| NY City, Muni. Wtr. & Swr. Syst. Fin. Auth. Rev. Bonds, Ser. DD, 5.00%, 6/15/40 | Aa1 | | 3,320,000 | 3,587,855 |

| NY City, Muni. Wtr. & Swr. Syst. Fin. Auth. VRDN | | | | |

| 1.15%, 6/15/49 | VMIG 1 | | 1,000,000 | 1,000,000 |

| Ser. DD-1, 1.15%, 6/15/43 | VMIG 1 | | 1,000,000 | 1,000,000 |

| NY City, Transitional Fin. Auth. Rev. Bonds | | | | |

| Ser. F-1, 5.00%, 2/1/51 | AAA | | 2,950,000 | 3,252,302 |

| (Future Tax Secured Revenue), 5.00%, 11/1/40 | AAA | | 4,250,000 | 4,624,600 |

| Ser. C-3, 5.00%, 5/1/40 | AAA | | 8,975,000 | 9,732,600 |

| NY City, Transitional Fin. Auth. Future Tax Secd. Rev. Bonds, Ser. C, 5.00%, 11/1/27 | AAA | | 3,500,000 | 3,702,118 |

| NY State Dorm. Auth. Personal Income Tax Rev. Bonds, Ser. A | | | | |

| 5.00%, 3/15/40 | Aa1 | | 655,000 | 717,863 |

| 5.00%, 3/15/34 | Aa1 | | 5,020,000 | 5,453,191 |

| 3.00%, 3/15/42 | Aa1 | | 7,915,000 | 6,730,950 |

| |

Strategic Intermediate Municipal Fund 29 |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| New York cont. |

| NY State Hsg. Fin. Agcy. VRDN (8 East 102nd St., LLC), Ser. A, 1.87%, 5/1/44 | VMIG 1 | | $3,780,000 | $3,780,000 |

| NY State Mtge. Agcy. Rev. Bonds, Ser. 196, 2.60%, 4/1/25 | Aa1 | | 750,000 | 742,881 |

| NY State Thruway Auth. Rev. Bonds, (Green Bonds-Bidding Group 1), 5.00%, 3/15/55 | AA+ | | 10,000,000 | 10,925,772 |

| NY State Trans. Special Fac. Dev. Corp. Rev. Bonds | | | | |

| (JFK Intl. Arpt. Term. 4, LLC), 5.00%, 12/1/29 | Baa1 | | 500,000 | 547,540 |

| (American Airlines, Inc.), 2.25%, 8/1/26 | B/F | | 205,000 | 193,709 |

| Orange Cnty., Funding Corp. Rev. Bonds, (Mount St. Mary College), 5.00%, 7/1/29 | BBB+/F | | 1,170,000 | 1,228,963 |

| Port Auth. of NY & NJ Rev. Bonds | | | | |

| Ser. 218, 5.00%, 11/1/49 T | AA− | | 1,535,000 | 1,611,627 |

| 5.00%, 1/15/47 | Aa3 | | 3,000,000 | 3,227,431 |

| 5.00%, 1/15/37 | Aa3 | | 1,000,000 | 1,118,063 |

| 5.00%, 1/15/36 | Aa3 | | 1,000,000 | 1,128,165 |

| Ser. 197, 5.00%, 11/15/35 | Aa3 | | 5,000,000 | 5,220,540 |

| Ser. 227, 3.00%, 10/1/27 | Aa3 | | 5,000,000 | 5,025,325 |

| Triborough Bridge & Tunnel Auth. Rev. Bonds, (Metro. Trans. Auth.), Ser. A, 5.00%, 11/15/24 | AA+ | | 15,500,000 | 16,235,015 |

| | | | 116,837,550 |

| North Carolina (0.3%) |

| NC State Med. Care Comm. Hlth. Care Fac. Rev. Bonds, (Lutheran Svcs. for the Aging, Inc. Oblig. Group), Ser. C | | | | |

| 5.00%, 3/1/28 | BB/P | | 365,000 | 366,284 |

| 5.00%, 3/1/27 | BB/P | | 460,000 | 463,863 |

| 5.00%, 3/1/26 | BB/P | | 440,000 | 445,363 |

| 4.00%, 3/1/29 | BB/P | | 755,000 | 715,047 |

| | | | 1,990,557 |

| Ohio (2.4%) |

| Cleveland-Cuyahoga Cnty., Rev. Bonds, (Euclid Ave. Dev., Corp.), 5.00%, 8/1/39 | A3 | | 3,000,000 | 3,054,623 |

| Cuyahoga Cnty., Econ. Dev. Rev. Bonds | | | | |

| 5.00%, 1/1/38 | A | | 1,380,000 | 1,508,207 |

| 5.00%, 1/1/36 | A | | 425,000 | 469,827 |

| Franklin Cnty., Hlth. Care Fac. Rev. Bonds, (Friendship Village of Dublin Oblig. Group), 5.00%, 11/15/34 | BBB+/F | | 700,000 | 708,533 |

| OH State Higher Edl. Fac. Comm. Rev. Bonds | | | | |

| (Kenyon College), 5.00%, 7/1/36 ### | A2 | | 1,250,000 | 1,379,431 |

| (Kenyon College), 5.00%, 7/1/35 ### | A2 | | 1,700,000 | 1,897,231 |

| (Cleveland Inst. of Music (The)), 5.00%, 12/1/32 | BBB− | | 600,000 | 659,134 |

| (John Carroll U.), 5.00%, 10/1/30 | Baa1 | | 455,000 | 502,366 |

| (John Carroll U.), 5.00%, 10/1/29 | Baa1 | | 810,000 | 887,529 |

| (John Carroll U.), 5.00%, 10/1/28 | Baa1 | | 370,000 | 402,093 |

| (John Carroll U.), 5.00%, 10/1/27 | Baa1 | | 350,000 | 376,036 |

| (John Carroll U.), 5.00%, 10/1/26 | Baa1 | | 350,000 | 371,225 |

| (John Carroll U.), 5.00%, 10/1/25 | Baa1 | | 220,000 | 229,892 |

| |

30 Strategic Intermediate Municipal Fund |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| Ohio cont. |

| OH State Hosp. Rev. Bonds, (Premier Hlth. Partners Oblig. Group) | | | | |

| 5.00%, 11/15/27 | Baa1 | | $240,000 | $259,850 |

| 5.00%, 11/15/26 | Baa1 | | 285,000 | 304,315 |

| 5.00%, 11/15/24 | Baa1 | | 135,000 | 139,313 |

| Ohio State Air Qlty. Dev. Auth. Mandatory Put Bonds (6/1/27), (Duke Energy Corp.), Ser. 22B, 4.00%, 9/1/30 | Baa2 | | 3,250,000 | 3,325,094 |

| Port of Greater Cincinnati Dev. Auth. 144A Rev. Bonds, 4.25%, 12/1/50 | BB/P | | 750,000 | 593,817 |

| Scioto Cnty., Hosp. Rev. Bonds, (Southern OH Med. Ctr.), 5.00%, 2/15/33 | A3 | | 500,000 | 517,938 |

| Warren Cnty., Hlth. Care Fac. Rev. Bonds, (Otterbein Homes Oblig. Group), Ser. A, 5.75%, 7/1/33 (Prerefunded 7/1/23) | A | | 500,000 | 506,721 |

| | | | 18,093,175 |

| Oregon (0.5%) |

| Keizer, Special Assmt. Bonds, (Keizer Station), Ser. A, 5.20%, 6/1/31 | Aa3 | | 215,000 | 219,266 |

| Port of Portland, Arpt. Rev. Bonds | | | | |

| Ser. 24B, 5.00%, 7/1/33 | AA− | | 2,000,000 | 2,135,928 |

| Ser. 28, 5.00%, 7/1/28 | AA− | | 1,000,000 | 1,105,790 |

| | | | 3,460,984 |

| Pennsylvania (6.0%) |

| Allegheny Cnty., Arpt. Auth. Rev. Bonds, Ser. A, 4.00%, 1/1/40 | AA | | 1,250,000 | 1,218,900 |

| Chester Cnty., Indl. Dev. Auth. Student Hsg. Rev. Bonds, (West Chester U. Student Hsg., LLC), Ser. A, 5.00%, 8/1/45 | Ba2 | | 750,000 | 731,190 |

| Dallas, Area Muni. Auth. U. Rev. Bonds, (Misericordia U.), 5.00%, 5/1/29 | Baa3 | | 300,000 | 302,342 |

| Geisinger, Auth. Rev. Bonds, (Geisinger Hlth. Syst.), Ser. A-2, 5.00%, 2/15/39 | AA− | | 3,275,000 | 3,433,450 |

| Lackawanna Cnty., Indl. Dev. Auth. Rev. Bonds, (Scranton U.), 4.00%, 11/1/40 | A− | | 500,000 | 484,699 |

| Lancaster, Indl. Dev. Auth. Rev. Bonds, (Landis Homes Oblig. Group), 4.00%, 7/1/46 | BBB−/F | | 675,000 | 547,148 |

| Monroeville, Fin. Auth. Rev. Bonds, (U. of Pittsburgh Med. Ctr.), Ser. B | | | | |

| 5.00%, 2/15/38 | A2 | | 2,200,000 | 2,415,041 |

| 5.00%, 2/15/24 | A2 | | 500,000 | 511,895 |

| PA Rev. Bonds, (City of Philadelphia, Wtr. & Wastewater) | | | | |

| 4.00%, 1/1/32 | Baa2 | | 540,000 | 555,342 |

| 4.00%, 1/1/31 | Baa2 | | 165,000 | 170,040 |

| 4.00%, 1/1/30 | Baa2 | | 115,000 | 118,374 |

| 4.00%, 1/1/29 | Baa2 | | 725,000 | 745,799 |

| PA State Econ. Dev. Fin. Auth. Rev. Bonds, (PennDOT Major Bridges) | | | | |

| 5.25%, 6/30/36 | Baa2 | | 1,650,000 | 1,836,345 |

| 5.25%, 6/30/35 | Baa2 | | 2,030,000 | 2,283,165 |

| |

Strategic Intermediate Municipal Fund 31 |

| | | | |

| MUNICIPAL BONDS AND NOTES (96.8%)* cont. | Rating** | | Principal amount | Value |

| Pennsylvania cont. |

| PA State Tpk. Comm. Rev. Bonds, Ser. B-1, 5.00%, 6/1/42 | A3 | | $675,000 | $706,365 |

| Philadelphia, Arpt. Rev. Bonds, Ser. C, 5.00%, 7/1/24 | A2 | | 4,000,000 | 4,105,645 |

| Philadelphia, Auth. for Indl. Dev. Rev. Bonds, (LaSalle U.), 5.00%, 5/1/25 | BB | | 1,815,000 | 1,820,961 |

| Philadelphia, Auth. for Indl. Dev. City Agreement Rev. Bonds, 5.00%, 12/1/27 | A2 | | 3,000,000 | 3,200,009 |

| Philadelphia, School Dist. G.O. Bonds, Ser. F, 5.00%, 9/1/29 | A1 | | 6,620,000 | 7,140,451 |

| Pittsburgh Wtr. & Swr. Auth. Mandatory Put Bonds (12/1/23), Ser. C, AGM, 2.31%, 9/1/40 | AA | | 1,875,000 | 1,873,669 |

| Scranton, School Dist. G.O. Bonds, Ser. 14-R, 3.821%, 4/1/31 | A1 | | 5,275,000 | 5,273,765 |

| Southeastern PA Trans. Auth. Rev. Bonds, (Asset Impt. Program) | | | | |

| 5.25%, 6/1/40 | Aa3 | | 1,250,000 | 1,459,983 |

| 5.25%, 6/1/39 | Aa3 | | 1,500,000 | 1,762,406 |