Exhibit 1.2

Management’s Discussion

and Analysis

FOR THE THREE AND SIX MONTHS ENDED JUNE 30, 2017

| TABLE OF CONTENTS | |

| Q2 2017 Highlights | |

| Q2 2017 Operating Performance | |

| Operating Outlook for 2017 | |

| Project Development Update | |

| Overview of Q2 2017 Financial Results | |

Disclosure Controls and Procedures and Technical Information | |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

August 9, 2017

| INTRODUCTION | ||

This Management’s Discussion and Analysis (“MD&A”) is intended to help the reader understand the significant factors that influence the performance of Pan American Silver Corp. and its subsidiaries (collectively “Pan American”, “we”, “us”, “our” or the “Company”) and such factors that may affect its future performance. This MD&A should be read in conjunction with the Company’s audited consolidated financial statements for the year ended December 31, 2016 (the “2016 Financial Statements”) and the related notes contained therein, and the unaudited condensed interim consolidated financial statements for three and six months ended June 30, 2017 and 2016 (the "Q2 2017 Financial Statements"), and the related notes contained therein. All amounts in this MD&A, the 2016 Financial Statements, and the Q2 2017 Financial Statements are expressed in United States dollars (“USD”), unless identified otherwise. The Company reports its financial position, results of operations and cashflows in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board. Pan American’s significant accounting policies are set out in Note 2 of the 2016 Financial Statements.

This MD&A refers to various non-Generally Accepted Accounting Principles (“non-GAAP”) measures, such as “all-in sustaining cost per silver ounce sold", “cash costs per ounce of silver”, "total debt", “working capital’, “general and administrative cost per silver ounce produced”, “adjusted earnings” and “basic adjusted earnings per share”, which are used by the Company to manage and evaluate operating performance at each of the Company’s mines and are widely reported in the mining industry as benchmarks for performance, but do not have standardized meaning under IFRS. To facilitate a better understanding of these non-GAAP measures as calculated by the Company, additional information has been provided in this MD&A. Please refer to the section of this MD&A entitled “Alternative Performance (Non-GAAP) Measures” for a detailed description of “all-in sustaining cost per silver ounce sold”, “cash costs per ounce of silver”, “working capital”, “general and administrative cost per silver ounce produced”, “adjusted earnings“ and “basic adjusted earnings per share”, as well as details of the Company’s by-product credits and a reconciliation of these measures to the Q2 2017 Financial Statements.

Any reference to “cash costs” or “cash costs per ounce of silver” in this MD&A should be understood to mean cash costs per ounce of silver, net of by-product credits. Any reference to “AISCSOS” in this MD&A should be understood to mean all-in sustaining costs per silver ounce sold, net of by-product credits.

Except for historical information contained in this MD&A, the following disclosures are forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and forward-looking information within the meaning of applicable Canadian provincial securities laws or are future oriented financial information and as such are based on an assumed set of economic conditions and courses of action. Please refer to the cautionary note regarding forward-looking statements and information at the back of this MD&A and the “Risks Related to Pan American’s Business” contained in the Company’s most recent Annual Information Form on file with the Canadian provincial securities regulatory authorities and Form 40-F on file with the U.S. Securities and Exchange Commission (the “SEC”). Additional information about Pan American and its business activities, including its Annual Information Form, is available on SEDAR at www.sedar.com

| PAN AMERICAN SILVER CORP. | 2 | |

| CORE BUSINESS AND STRATEGY | ||

Pan American engages in silver mining and related activities, including exploration, mine development, extraction, processing, refining and reclamation. The Company owns and operates silver mines located in Peru, Mexico, Argentina, and Bolivia. In addition, the Company is exploring for new silver deposits and opportunities throughout North and South America. The Company is listed on the Toronto Stock Exchange (Symbol: PAAS) and on the Nasdaq Global Select Market (“NASDAQ”) in New York (Symbol: PAAS).

Pan American’s vision is to be the world’s pre-eminent silver producer, with a reputation for excellence in discovery, engineering, innovation and sustainable development. To achieve this vision, we base our business on the following strategy:

| • | Generate sustainable profits and superior returns on investments through the safe, efficient and environmentally sound development and operation of silver assets |

| • | Constantly replace and grow our mineable silver reserves and resources through targeted near-mine exploration and global business development |

| • | Foster positive long-term relationships with our employees, our shareholders, our communities and our local governments through open and honest communication and ethical and sustainable business practices |

| • | Continually search for opportunities to upgrade and improve the quality of our silver assets both internally and through acquisition |

| • | Encourage our employees to be innovative, responsive and entrepreneurial throughout our entire organization |

To execute this strategy, Pan American has assembled a sector-leading team of mining professionals with a depth of knowledge and experience in all aspects of our business, which enables the Company to confidently advance early stage projects through construction and into operation.

Pan American is determined to conduct its business in a responsible and sustainable manner. Caring for the environment in which we operate, contributing to the long-term development of our host communities and ensuring that our employees can work in a safe and secure manner are core values at Pan American. We are committed to maintaining positive relations with our employees, the local communities and the government agencies, all of whom we view as partners in our enterprise.

| PAN AMERICAN SILVER CORP. | 3 | |

| Q2 2017 HIGHLIGHTS | ||

Operations & Project Development

| • | Silver production of 6.30 million ounces |

Pan American produced 6.30 million ounces in the three months ended June 30, 2017 ("Q2 2017"), comparable to the 6.33 million ounces produced in the second quarter of 2016 ("Q2 2016"). Q2 2017 production brought silver production for the six months ended June 30, 2017 ("H1 2017") to 12.5 million ounces, in line with the production rate required to achieve management’s full year forecast range of 24.5 to 26.0 million ounces.

| • | Cash Costs of $5.71 per ounce and 2017 annual Cash Costs forecast lowered |

Consolidated cash costs for Q2 2017 were $5.71 per ounce, $0.14 per ounce or 3% higher than the Q2 2016 cash costs of $5.57 per ounce. H1 2017 cash costs of $5.94 per ounce were $0.87 per ounce or 13% lower than cash costs for the six months ended June 30, 2016 ("H1 2016"). Given cash costs for H1 2017 were $0.51 per ounce, or 8%, less than the low end of management’s 2017 annual forecast range of $6.45 to $7.45 per ounce, management has revised the 2017 annual forecast range for cash costs to $5.50 to $6.50 per ounce, representing a 14% decrease from the mid-point of the original forecast.

| • | By-Product production in-line with expectations |

Gold production in Q2 2017 was 37.7 thousand ounces, 10.7 thousand ounces less than in Q2 2016, bringing H1 2017 production to 75.4 thousand ounces, 16% lower than in H1 2016. Given the higher anticipated production for the remainder of the year at both Dolores and Manantial Espejo, management reaffirms the 2017 annual gold production forecast of 155.0 to 165.0 thousand ounces.

Q2 2017 zinc, lead, and copper production of 13.7 thousand tonnes, 5.5 thousand tonnes and 3.5 thousand tonnes, respectively, were within management's expectations based on current mine plans and brought H1 2017 zinc, lead, and copper production to 26.5 thousand tonnes, 10.8 thousand tonnes, and 6.7 thousand tonnes, respectively. Management reaffirms the 2017 annual zinc, lead and copper production forecasts of 56.5 to 58.5 thousand tonnes, 19.0 to 20.0 thousand tonnes, and 8.8 to 9.3 thousand tonnes, respectively.

| • | Progress on the Dolores expansion project |

During Q2 2017 the Company invested $13.7 million on the Dolores expansion projects, essentially completing the construction of the new pulp agglomeration plant. Commissioning of the new plant is now underway. Development of the underground mine is also progressing well, and remains on-track for production to begin before the end of 2017.

Financial

| • | Increased revenues, net earnings, and adjusted earnings |

Q2 2017 revenue of $201.3 million was $9.1 million higher than in Q2 2016, mainly as a result of higher metal prices. Realized silver prices per ounce averaged $17.19 for Q2 2017 compared with $16.87 during Q2 2016. Net earnings in Q2 2017 were $36.0 million ($0.23 basic earnings per share) compared with $34.2 million ($0.22 basic earnings per share) in Q2 2016. Q2 2017 adjusted earnings of $22.3 million ($0.15 basic earnings per share) were $4.3 million (or $0.03 basic earnings per share) higher than Q2 2016 adjusted earnings.

| • | Strong liquidity and working capital position |

The Company had cash and short-term investment balances of $198.2 million and working capital of $429.6 million as at June 30, 2017. At the end of Q2 2017, the Company had total debt outstanding of $46.7 million and $263.8 million available under its revolving credit facility.

| PAN AMERICAN SILVER CORP. | 4 | |

| • | All-in Sustaining Costs per Silver Ounce Sold and 2017 AISCSOS forecast lowered |

Q2 2017 consolidated AISCSOS were $10.73, $0.58 lower than in Q2 2016. H1 2017 AISCSOS of $11.66 were closer to the low end of management’s 2017 annual forecast of $11.50 to $12.90. Based on the H1 2017 AISCSOS results, and the expected results for the remainder of 2017, management has lowered the annual 2017 AISCSOS guidance to $10.50 - $11.50, representing a 10% decrease from the mid-point of the original forecast.

| Q2 2017 OPERATING PERFORMANCE | ||

The following table provides silver production and cash costs, net of by-product credits, at each of Pan American’s operations for the respective three and six months ended June 30, 2017 and 2016:

Silver Production (ounces ‘000s) | Cash Costs(1) ($ per ounce) | ||||||||||||||||

| Three months ended June 30, | Six months ended June 30, | Three months ended June 30, | Six months ended June 30, | ||||||||||||||

| 2017 | 2016 | 2017 | 2016 | 2017 | 2016 | 2017 | 2016 | ||||||||||

| La Colorada | 1,731 | 1,373 | 3,361 | 2,745 | 3.38 | 7.66 | 3.20 | 7.00 | |||||||||

| Dolores | 1,037 | 966 | 2,002 | 2,039 | 0.12 | (0.64 | ) | (0.74 | ) | 2.91 | |||||||

| Alamo Dorado | 261 | 533 | 608 | 1,094 | 11.18 | 13.54 | 17.03 | 12.68 | |||||||||

| Huaron | 898 | 953 | 1,794 | 1,906 | 2.24 | 5.70 | 1.51 | 6.83 | |||||||||

Morococha(2) | 634 | 577 | 1,278 | 1,276 | (2.35 | ) | 1.35 | (2.78 | ) | 3.51 | |||||||

San Vicente(3) | 766 | 1,145 | 1,701 | 2,232 | 14.02 | 12.27 | 13.16 | 12.06 | |||||||||

| Manantial Espejo | 975 | 785 | 1,762 | 1,461 | 15.11 | (2.40 | ) | 17.46 | 2.47 | ||||||||

Consolidated Total (4) | 6,303 | 6,332 | 12,507 | 12,753 | 5.71 | 5.57 | 5.94 | 6.81 | |||||||||

| (1) | Cash costs is a non-GAAP measure. Please refer to the section “Alternative Performance (Non-GAAP) Measures” of this MD&A for a detailed description of the cash cost calculation, details of the Company’s by-product credits and a reconciliation of this measure to the Q2 2017 Financial Statements. |

| (2) | Morococha data represents Pan American's 92.3% interest in the mine's production. |

| (3) | San Vicente data represents Pan American's 95.0% interest in the mine's production. |

| (4) | Totals may not add due to rounding. |

| PAN AMERICAN SILVER CORP. | 5 | |

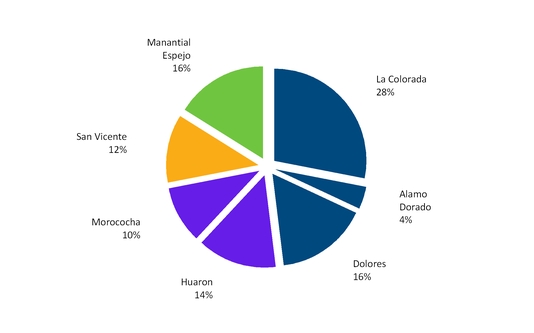

Q2 2017 Silver Production

The chart below presents silver production by mine in Q2 2017:

Consolidated silver production of 6.30 million ounces in Q2 2017 was consistent with the 6.33 million ounces produced in Q2 2016. The comparable quarter-over-quarter production reflects increases at La Colorada and Manantial Espejo, partially offsetting decreases at Alamo Dorado and at San Vicente. Production at the remaining operations was essentially comparable quarter-over-quarter. Each operation’s silver production and quarter-over-quarter variances are further discussed in the “Individual Mine Performance” section of this MD&A.

Q2 2017 Cash Costs

Consolidated cash costs per ounce of silver for Q2 2017 and H1 2017 were $5.71 and $5.94, respectively, representing a 3% increase and 13% reduction from Q2 2016 and H1 2016, respectively. Quarter-over-quarter by-product credits per ounce decreased by $0.34, largely the result of a 22% decrease in gold production driven by declines at Manantial Espejo. The decrease in by-product credits was partially offset by lower consolidated direct operating costs per ounce. The decreased direct operating costs were primarily driven by Alamo Dorado operations winding down and lower costs at Dolores, partially offset by increased costs at Manantial Espejo. The higher cost at Manantial Espejo was due largely to severance costs associated with the termination of open pit mining activities, high inflation and the elimination of certain export incentive credits, which had reduced 2016 direct operating costs. Total severance costs incurred at Manatial Espejo and Alamo Dorado during Q2 2017 totaled $3.2 million and increased consolidated Q2 2017 cash costs by $0.54 per ounce. H1 2017 and H1 2016 cash costs variances were driven by similar factors, with the exception of period-over-period by-product credits, which were higher in 2017 due to higher by-product metal prices and increased zinc and lead production more than offsetting declines in gold and copper production.

Each operation’s cash costs and quarter-over-quarter variances are separately discussed in the “Individual Mine Performance” section of this MD&A.

| PAN AMERICAN SILVER CORP. | 6 | |

Q2 2017 By-Product Production

The following table provides the Company’s by-product production for Q2 2017 and Q2 2016:

| By-Product Production | ||||||||

| Three months ended June 30, | Six months ended June 30, | |||||||

| 2017 | 2016 | 2017 | 2016 | |||||

| Gold – koz | 37.7 | 48.4 | 75.4 | 89.6 | ||||

| Zinc – kt | 13.7 | 12.7 | 26.5 | 25.5 | ||||

| Lead – kt | 5.5 | 5.0 | 10.8 | 9.8 | ||||

| Copper – kt | 3.5 | 4.4 | 6.7 | 8.3 | ||||

Gold production during Q2 2017 was 37.7 thousand ounces, 22% lower than in Q2 2016 due primarily to lower ore grades at Manantial Espejo and Dolores and the windup of Alamo Dorado operations.

Zinc production in Q2 2017 was 8% higher than Q2 2016 driven by higher ore grade and throughput at La Colorada, offset by lower grades at Huaron and Morococha. Quarter-over-quarter lead production increased 10%, driven mainly by higher throughput and grades at La Colorada. Q2 2017 copper production was 20% lower than in Q2 2016, primarily the result of lower copper grades at Morococha. Each operation’s by-product production and quarter-over-quarter variances are separately discussed in the “Individual Mine Performance” section of this MD&A.

2017 Average Market Metal Prices

The following tables set out the average market price for each metal produced for Q2 2017 and Q2 2016:

| Average Market Metal Prices | ||||||||

| Three months ended June 30, | Six months ended June 30, | |||||||

| 2017 | 2016 | 2017 | 2016 | |||||

| Silver $/ounce | 17.21 | 16.78 | 17.32 | 15.82 | ||||

| Gold $/ounce | 1,257 | 1,260 | 1,238 | 1,221 | ||||

| Zinc $/tonne | 2,596 | 1,918 | 2,690 | 1,799 | ||||

| Lead $/tonne | 2,161 | 1,719 | 2,221 | 1,731 | ||||

| Copper $/tonne | 5,662 | 4,729 | 5,749 | 4,701 | ||||

| PAN AMERICAN SILVER CORP. | 7 | |

Q2 2017 AISCSOS

The following table reflects the quantities of payable silver sold and AISCSOS at each of Pan American’s operations for the three months ended June 30, 2017, as compared to the same period in 2016:

Payable Silver Sold (ounces ‘000s) | AISCSOS(1) ($ per ounce) | ||||||||||||||||

| Three months ended June 30, | Six months ended June 30, | Three months ended June 30, | Six months ended June 30, | ||||||||||||||

| 2017 | 2016 | 2017 | 2016 | 2017 | 2016 | 2017 | 2016 | ||||||||||

| La Colorada | 1,678 | 1,479 | 3,363 | 2,629 | 5.86 | 8.84 | 5.80 | 8.98 | |||||||||

| Dolores | 1,039 | 1,058 | 1,931 | 2,008 | 7.28 | 14.30 | 8.66 | 16.69 | |||||||||

| Alamo Dorado | 342 | 585 | 642 | 1,271 | 21.53 | 12.77 | 19.34 | 11.06 | |||||||||

| Huaron | 766 | 818 | 1,550 | 1,653 | 5.01 | 10.05 | 5.55 | 11.01 | |||||||||

| Morococha | 638 | 550 | 1,215 | 1,225 | 3.30 | 6.61 | 3.50 | 6.87 | |||||||||

| San Vicente | 865 | 707 | 1,752 | 1,456 | 13.81 | 16.97 | 14.33 | 15.97 | |||||||||

| Manantial Espejo | 981 | 645 | 1,843 | 1,317 | 18.13 | (3.51 | ) | 22.53 | 3.42 | ||||||||

Consolidated Total (2) | 6,311 | 5,843 | 12,297 | 11,559 | 10.73 | 11.31 | 11.66 | 12.21 | |||||||||

| (1) | AISCSOS is a non-GAAP measure. Please refer to the section “Alternative Performance (Non-GAAP) Measures” of this MD&A for a detailed description of the AISCSOS calculation and a reconciliation of this measure to the Q2 2017 Financial Statements. G&A costs are included in the consolidated AISCSOS, but not allocated in calculating AISCSOS for each operation. |

| (2) | Totals may not add due to rounding. |

Consolidated AISCSOS for Q2 2017 and H1 2017, were $10.73 and $11.66, respectively, representing a 5% reduction from the comparable AISCSOS amounts in Q2 2016 and H1 2016.

The quarter-over-quarter decrease largely reflects: increased by-product credits from higher by-product metal prices; decreased direct selling costs from improved contract terms for concentrate treatment and refining; decreased royalties due to certain royalty payments at the time shipments were exported differing from the quarter the sale of the shipment was recognized; increased volumes of silver sold, mainly from additional production at La Colorada and the timing of sales at Manantial Espejo and San Vicente. These AISCSOS reducing factors were partially offset by increased production costs, primarily from higher operating costs at Manantial Espejo, net realizable value ("NRV") inventory adjustments, and an increase in exploration expenses.

The decline in H1 2017 AISCSOS from H1 2016 was driven by similar factors as to the quarter-over-quarter variance, with more significant AISCSOS reductions resulting from higher by-product credits due to higher metal prices as well as increased lead and silver sales volumes, which were offset by higher NRV inventory adjustments.

Individual Mine Performance

An analysis of each operation for Q2 2017, compared to Q2 2016 follows. The Project Capital amounts invested in Q2 2017 are further discussed in the "Project Development Update" section of this MD&A.

| PAN AMERICAN SILVER CORP. | 8 | |

La Colorada mine

| Three months ended June 30, | Six months ended June 30, | |||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||

| Tonnes milled - kt | 156.9 | 122.4 | 309.3 | 246.0 | ||||||||

| Average silver grade – grams per tonne | 377 | 387 | 372 | 384 | ||||||||

| Average zinc grade - % | 2.90 | 2.48 | 2.84 | 2.56 | ||||||||

| Average lead grade - % | 1.58 | 1.34 | 1.54 | 1.37 | ||||||||

| Average silver recovery - % | 91.1 | 90.2 | 91.0 | 90.4 | ||||||||

| Average zinc recovery - % | 84.0 | 81.3 | 83.8 | 81.5 | ||||||||

| Average lead recovery - % | 87.7 | 85.9 | 87.4 | 86.8 | ||||||||

| Production: | ||||||||||||

| Silver – koz | 1,731 | 1,373 | 3,361 | 2,745 | ||||||||

| Gold – koz | 0.94 | 0.67 | 1.82 | 1.35 | ||||||||

| Zinc – kt | 3.83 | 2.47 | 7.37 | 5.14 | ||||||||

| Lead – kt | 2.18 | 1.41 | 4.16 | 2.93 | ||||||||

Cash cost per ounce net of by-products(1) | $ | 3.38 | $ | 7.66 | $ | 3.20 | $ | 7.00 | ||||

AISCSOS(2) | $ | 5.86 | $ | 8.84 | $ | 5.80 | $ | 8.98 | ||||

| Payable silver sold - koz | 1,678 | 1,479 | 3,363 | 2,629 | ||||||||

Sustaining capital - (’000s)(3) | $ | 4,680 | $ | 3,471 | $ | 7,715 | $ | 7,126 | ||||

| (1) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| (2) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed description of the AISCSOS calculation and a reconciliation of this measure to the Q2 2017 Financial Statements. |

| (3) | Sustaining capital expenditures excludes $2.8 million and $5.4 million of investing activity cash outflow for Q2 2017 and H1 2017, respectively (Q2 2016 and H1 2016: $15.1 million and $30.8 million, respectively) related to investment capital incurred on the La Colorada expansion project as disclosed in the “Project Development Update” section of this MD&A. |

The La Colorada mine produced 26% more silver in Q2 2017 compared with Q2 2016 due to a 28% increase in throughput rates partially offset by a 3% decline in silver grades. The improved throughput reflects the benefits of the expansion project, which was largely completed in Q4 2016. During Q2 2017, the mine produced 3.8 thousand tonnes of zinc and 2.2 thousand tonnes of lead, 55% and 55% more than in Q2 2016, respectively, due to increased throughput of sulphide ore, as well as improved grades.

Q2 2017 cash costs of $3.38 per ounce of silver were $4.28 lower than the $7.66 per ounce in Q2 2016. The 56% decrease was primarily the result of improved by-product credits due to increased quantities produced and higher prices, as well as increased silver production.

Q2 2017 AISCSOS of $5.86 decreased 34% from $8.84 in Q2 2016. The decrease was the result of improved production rates as the mine ramped up production following the completion of the new shaft and sulphide plant in 2016, as well as the increased base metal prices discussed previously in this section.

Sustaining capital cash outflows totaled $4.7 million in Q2 2017, an increase from $3.5 million in Q2 2016. Sustaining capital in Q2 2017 related primarily to a tailings facility expansion, exploration, underground equipment and a new camp; however, it excludes $2.8 million spent on the La Colorada expansion project during the quarter (Q2 2016 - $15.1 million), which is further described in the Project Development Update section of this MD&A.

| PAN AMERICAN SILVER CORP. | 9 | |

Dolores mine

| Three months ended June 30, | Six months ended June 30, | |||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||

| Tonnes placed - kt | 1,622.8 | 1,534.2 | 3,190.1 | 3,073.5 | ||||||||

| Average silver grade – grams per tonne | 38 | 29 | 40 | 34 | ||||||||

| Average gold grade – grams per tonne | 0.64 | 0.76 | 0.62 | 0.70 | ||||||||

| Average silver produced to placed ratio - % | 51.9 | 66.6 | 48.8 | 61.1 | ||||||||

| Average gold produced to placed ratio - % | 66.8 | 67.3 | 73.3 | 67.6 | ||||||||

| Production: | ||||||||||||

| Silver – koz | 1,037 | 966 | 2,002 | 2,039 | ||||||||

| Gold – koz | 22.4 | 25.4 | 46.8 | 46.8 | ||||||||

Cash cost per ounce net of by-products(1) | 0.12 | (0.64 | ) | (0.74 | ) | 2.91 | ||||||

AISCSOS(2) | 7.28 | 14.30 | 8.66 | 16.69 | ||||||||

| Payable silver sold - koz | 1,039 | 1,058 | 1,931 | 2,008 | ||||||||

Sustaining capital - (’000s)(3) | $ | 13,451 | $ | 15,543 | $ | 18,955 | $ | 29,964 | ||||

| (1) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| (2) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed description of the AISCSOS calculation and a reconciliation of this measure to the Q2 2017 Financial Statements. |

| (3) | Sustaining capital expenditures exclude $13.7 million and $27.8 million of investing activity cash outflow for in Q2 2017 and H1 2017, respectively (Q2 2016 and H1 2016: $13.7 million and $21.5 million, respectively) related to investment capital incurred on Dolores expansion projects, as disclosed in the “Project Development Update” section of this MD&A. |

In Q2 2017, Dolores produced 1.04 million ounces of silver, which is 7% higher than the 0.97 million ounces produced in Q2 2016. The increase was the result of a 31% increase in silver grades stacked due to expected mine sequencing, which was partially offset by the timing of leach pad kinetics resulting in a lower silver produced to silver recovered ratio. Gold production of 22.4 thousand ounces in Q2 2017 was 12% lower than the 25.4 thousand ounces produced in Q2 2016 due to lower gold grades from mine sequencing.

Q2 2017 cash costs were $0.12 per ounce of silver, a $0.76 per ounce increase relative to Q2 2016. The higher cash costs were primarily the result of decreased gold by-product credits partially offset by lower production costs primarily due to a build-up of inventories.

Q2 2017 AISCSOS of $7.28 decreased $7.02 from $14.30 in Q2 2016. The decrease was primarily the result of: a $6.6 million decrease in production costs due to $1.6 million increase in positive NRV adjustments and $5.0 million lower direct operating costs due to increased ore stockpile and heap inventories and lower costs for consumables. In addition, there was a $2.1 million decrease in sustaining capital due to lower leach pad related investments.

Sustaining capital expenditures of $13.5 million in Q2 2017 were lower than the $15.5 million in Q2 2016, primarily due to lower investments in leach pad expansions. Q2 2017 capital expenditures primarily consisted of open pit pre-stripping, leach pad expansion, and new mobile mining equipment. Q2 2017 sustaining capital excludes $13.7 million of cash outflows relating to Dolores expansion projects (Q2 2016 - $13.7 million), which is further discussed in the "Project Development Update" section of this MD&A.

| PAN AMERICAN SILVER CORP. | 10 | |

Alamo Dorado mine

| Three months ended June 30, | Six months ended June 30, | |||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||

| Tonnes milled - kt | 19.0 | 494.8 | 451.8 | 959.4 | ||||||||

| Average silver grade – grams per tonne | 52 | 46 | 43 | 49 | ||||||||

| Average gold grade – grams per tonne | 0.17 | 0.18 | 0.17 | 0.21 | ||||||||

| Average silver recovery - % | 77.2 | 71.2 | 67.6 | 72.7 | ||||||||

| Production: | ||||||||||||

| Silver – koz | 261.4 | 533.4 | 608.0 | 1,093.9 | ||||||||

| Gold – koz | 0.7 | 2.3 | 2.0 | 5.6 | ||||||||

| Copper – tonnes | 8 | 9 | 13 | 27 | ||||||||

Cash cost per ounce net of by-products(1) | 11.18 | 13.54 | 17.03 | 12.68 | ||||||||

AISCSOS(2) | 21.53 | 12.77 | 19.34 | 11.06 | ||||||||

| Payable silver sold - koz | 342 | 585 | 642 | 1,271 | ||||||||

| Sustaining capital - (’000s) | $ | — | $ | — | $ | — | $ | — | ||||

| (1) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| (2) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed description of the AISCSOS calculation and a reconciliation of this measure to the Q2 2017 Financial Statements. |

Q2 2017 silver and gold production was 0.26 million ounces and 0.7 thousand ounces, respectively, and resulted from metal recovered during the clean out of the process facility.

Q2 2017 cash costs were $11.18 per ounce of silver, down $2.36 per ounce from Q2 2016, reflecting the relatively lower cost of clean-up activities compared to the production activities in Q2 2016.

Q2 2017 AISCSOS of $21.53 were $8.76 higher than Q2 2016 AISCSOS of $12.77. The increase was largely attributable to processing lower grade stockpiled material, which resulted in a 42% decrease in the volume of silver ounces sold, and lower by-product credits driven by a 62% decrease in the quantity of gold sold.

No sustaining capital expenditures were incurred at Alamo Dorado during Q2 2017 or Q2 2016, as mining activities were completed and the reclamation phase of the mine has commenced.

| PAN AMERICAN SILVER CORP. | 11 | |

Huaron mine

| Three months ended June 30, | Six months ended June 30, | |||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||

| Tonnes milled - kt | 227.6 | 224.7 | 455.1 | 451.0 | ||||||||

| Average silver grade – grams per tonne | 146 | 158 | 146 | 159 | ||||||||

| Average zinc grade - % | 2.75 | 3.12 | 2.79 | 2.97 | ||||||||

| Average lead grade - % | 1.31 | 1.50 | 1.33 | 1.45 | ||||||||

| Average copper grade - % | 0.90 | 0.97 | 0.89 | 0.98 | ||||||||

| Average silver recovery - % | 86.1 | 83.3 | 85.6 | 83.3 | ||||||||

| Average zinc recovery - % | 78.5 | 75.0 | 77.4 | 73.7 | ||||||||

| Average lead recovery - % | 78.6 | 79.5 | 78.7 | 77.8 | ||||||||

| Average copper recovery - % | 79.5 | 76.6 | 78.8 | 76.9 | ||||||||

| Production: | ||||||||||||

| Silver – koz | 898 | 953 | 1,794 | 1,906 | ||||||||

| Gold – koz | 0.44 | 0.23 | 0.69 | 0.41 | ||||||||

| Zinc – kt | 4.91 | 5.19 | 9.76 | 9.76 | ||||||||

| Lead – kt | 2.32 | 2.67 | 4.72 | 5.07 | ||||||||

| Copper – kt | 1.60 | 1.66 | 3.14 | 3.34 | ||||||||

Cash cost per ounce net of by-products(1) | $ | 2.24 | $ | 5.70 | $ | 1.51 | $ | 6.83 | ||||

AISCSOS(2) | $ | 5.01 | $ | 10.05 | $ | 5.55 | $ | 11.01 | ||||

| Payable silver sold – koz | 766 | 818 | 1,550 | 1,653 | ||||||||

| Sustaining capital - (’000s) | $ | 2,102 | $ | 2,250 | $ | 5,207 | $ | 4,387 | ||||

| (1) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| (2) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed description of the AISCSOS calculation and a reconciliation of this measure to the Q2 2017 Financial Statements. |

In Q2 2017, Huaron silver production was 6% lower than Q2 2016, reflecting 8% lower grades, partially offset by higher mill recoveries. As a result of mine sequencing, Q2 2017 zinc, lead and copper production decreased 5%, 13%, and 4% relative to Q2 2016, respectively. Mill recoveries have improved for all metals, except for lead, due to flotation circuit upgrades completed in the past year.

Q2 2017 cash costs of $2.24 per ounce declined 61% relative to Q2 2016. The decrease resulted from higher by-product credits due to higher prices for all three base metals, which more than offset the slightly lower base metal and silver production.

Q2 2017 AISCSOS of $5.01 were 50% lower than the $10.05 for Q2 2016. The decrease was primarily attributable to significantly higher by-product credits due to improved base metal prices, and improved concentrate refining terms.

Sustaining capital expenditures during Q2 2017 totaled $2.1 million, a decrease from the $2.3 million spent in Q2 2016. Sustaining capital investments in each quarter related primarily to equipment replacements and refurbishments, plant and infrastructure upgrades and exploration drilling.

| PAN AMERICAN SILVER CORP. | 12 | |

Morococha mine(1)

| Three months ended June 30, | Six months ended June 30, | |||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||

| Tonnes milled – kt | 170.8 | 168.3 | 334.6 | 336.3 | ||||||||

| Average silver grade – grams per tonne | 133 | 122 | 136 | 136 | ||||||||

| Average zinc grade - % | 2.86 | 3.29 | 2.85 | 3.30 | ||||||||

| Average lead grade - % | 0.79 | 0.79 | 0.79 | 0.76 | ||||||||

| Average copper grade - % | 1.27 | 1.80 | 1.23 | 1.68 | ||||||||

| Average silver recovery - % | 88.5 | 88.2 | 88.4 | 87.6 | ||||||||

| Average zinc recovery - % | 77.3 | 71.4 | 78.7 | 70.8 | ||||||||

| Average lead recovery - % | 64.3 | 56.1 | 65.5 | 57.1 | ||||||||

| Average copper recovery - % | 84.4 | 84.2 | 83.6 | 84.1 | ||||||||

| Production: | ||||||||||||

| Silver – koz | 634 | 577 | 1,278 | 1,276 | ||||||||

| Gold – koz | 1.03 | 0.59 | 1.63 | 1.30 | ||||||||

| Zinc – kt | 3.77 | 3.94 | 7.46 | 7.83 | ||||||||

| Lead – kt | 0.86 | 0.73 | 1.71 | 1.42 | ||||||||

| Copper – kt | 1.76 | 2.51 | 3.35 | 4.66 | ||||||||

Cash cost per ounce net of by-products (2) | $ | (2.35 | ) | $ | 1.35 | $ | (2.78 | ) | $ | 3.51 | ||

AISCSOS(3) | $ | 3.30 | $ | 6.61 | $ | 3.50 | $ | 6.87 | ||||

| Payable silver sold (100%) - koz | 638 | 550 | 1,215 | 1,225 | ||||||||

| Sustaining capital (100%) - (’000s) | $ | 3,999 | $ | 2,368 | $ | 6,270 | $ | 3,689 | ||||

| (1) | Production figures are for Pan American’s 92.3% share only, unless otherwise noted. |

| (2) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to our cost of sales. |

| (3) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed description of the AISCSOS calculation and a reconciliation of this measure to the Q2 2017 Financial Statements. |

Q2 2017, silver production at Morococha was 10% higher than the comparable quarter of 2016 primarily due to a 9% increase in silver head grades. As a result of mine sequencing, Q2 2017 zinc and copper production was down by 4% and 30%, respectively, while lead production increased by 18% relative to Q2 2016.

Cash costs of negative $2.35 per ounce in Q2 2017 were $3.70 per ounce lower than Q2 2016 cash costs of $1.35 per ounce. The reduction was primarily the result of higher by-product prices and higher silver and lead production, which more than offset the lower zinc and copper production.

Q2 2017 AISCSOS of $3.30 were 50% lower than Q2 2016 AISCSOS of $6.61. The decrease was primarily attributable to significantly higher by-product credits due to improved base metal prices, and improved concentrate refining terms. This was partially offset by higher sustaining capital expenditures related to the timing of the purchase of mining equipment.

Sustaining capital expenditures during Q2 2017 totaled $4.0 million, an increase from the $2.4 million in Q2 2016. The increase primarily related to exploration, and the timing of mine equipment purchases and refurbishments.

| PAN AMERICAN SILVER CORP. | 13 | |

San Vicente mine (1)

| Three months ended June 30, | Six months ended June 30, | |||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||

| Tonnes milled – kt | 81.3 | 84.3 | 152.0 | 167.3 | ||||||||

| Average silver grade – grams per tonne | 316 | 453 | 380 | 451 | ||||||||

| Average zinc grade - % | 2.11 | 1.94 | 1.98 | 2.28 | ||||||||

| Average lead grade - % | 0.30 | 0.33 | 0.31 | 0.34 | ||||||||

| Average silver recovery - % | 93.3 | 94.2 | 92.8 | 93.2 | ||||||||

| Average zinc recovery - % | 71.3 | 69.7 | 64.8 | 73.5 | ||||||||

| Average lead recovery - % | 81.3 | 82.0 | 83.0 | 81.5 | ||||||||

| Production: | ||||||||||||

| Silver – koz | 766 | 1,145 | 1,701 | 2,232 | ||||||||

| Gold – koz | 0.12 | — | 0.24 | — | ||||||||

| Zinc – kt | 1.22 | 1.14 | 1.94 | 2.81 | ||||||||

| Lead – kt | 0.10 | 0.20 | 0.21 | 0.42 | ||||||||

| Copper – kt | 0.12 | 0.24 | 0.20 | 0.24 | ||||||||

Cash cost per ounce net of by-products (2) | $ | 14.02 | $ | 12.27 | $ | 13.16 | $ | 12.06 | ||||

AISCSOS(3) | $ | 13.81 | $ | 16.97 | $ | 14.33 | $ | 15.97 | ||||

| Payable silver sold (100%) - koz | 865 | 707 | 1,752 | 1,456 | ||||||||

| Sustaining capital (100%) - (’000s) | $ | 2,241 | $ | 1,295 | $ | 3,807 | $ | 1,756 | ||||

| (1) | Production figures are for Pan American’s 95.0% share only, unless otherwise noted. |

| (2) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| (3) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed description of the AISCSOS calculation and a reconciliation of this measure to the Q2 2017 Financial Statements. |

Q2 2017 silver production decreased 33% relative to Q2 2016, primarily due to a 30% reduction in head grades and 8-days of unscheduled downtime. The downtime was required to address a combination of plant maintenance, employee work stoppages, and safety matters. The decline in ore grades was attributable to development and mining preparation delays of higher-grade stopes, as well as additional mining dilution experienced with the transitioning of certain conventional mine areas into more mechanized mining methods. Quarter-over-quarter lead and copper production both decreased by 50%, which was largely offset by a 7% increase in zinc production. The variations in base metal production was also due to the mine sequencing and mine development shortfalls.

The Q2 2017 cash costs of $14.02 per ounce were 14% higher than the Q2 2016 cash costs of $12.27 per ounce. The increase in cash costs was primarily the result of the lower silver grades realized during the quarter.

Q2 2017 AISCSOS of $13.81 were $3.16 lower that Q2 2016 AISCSOS of $16.97, primarily the result of decreased royalties due to royalty payments, offset by $0.9 million higher in capital expenditures and a reduction in by-product credits due to the timing of zinc concentrate sales.

Q2 2017 sustaining capital expenditures totaled $2.2 million, an increase from $1.3 million in Q2 2016. The quarter-over-quarter increase is primarily related to exploration and the timing of mine equipment purchases and refurbishments.

| PAN AMERICAN SILVER CORP. | 14 | |

Manantial Espejo mine

| Three months ended June 30, | Six months ended June 30, | |||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||

| Tonnes milled - kt | 193.8 | 166.5 | 382.2 | 347.5 | ||||||||

| Average silver grade – grams per tonne | 170 | 168 | 156 | 145 | ||||||||

| Average gold grade – grams per tonne | 2.11 | 3.78 | 1.94 | 3.21 | ||||||||

| Average silver recovery - % | 90.9 | 89.8 | 91.4 | 90.9 | ||||||||

| Average gold recovery - % | 94.3 | 94.4 | 93.9 | 94.4 | ||||||||

| Production: | ||||||||||||

| Silver – koz | 975 | 785 | 1,762 | 1,461 | ||||||||

| Gold – koz | 12.05 | 19.20 | 22.18 | 34.09 | ||||||||

Cash cost per ounce net of by-products (1) | $ | 15.11 | $ | (2.40 | ) | $ | 17.46 | $ | 2.47 | |||

AISCSOS(2) | $ | 18.13 | $ | (3.51 | ) | $ | 22.53 | $ | 3.42 | |||

| Payable silver sold - koz | 981 | 645 | 1,843 | 1,317 | ||||||||

| Sustaining capital - (’000s) | $ | 166 | $ | 495 | $ | 1,264 | $ | 1,441 | ||||

| (1) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| (2) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed description of the AISCSOS calculation and a reconciliation of this measure to the Q2 2017 Financial Statements. |

Q2 2017 silver production increased 24% from Q2 2016, mainly as a result of higher throughput due to a full quarter of production in Q2 2017 compared to Q2 2016 when there was a two week labor related work stoppage. Gold production decreased by 37% due to an expected 44% decrease in head grades related to mine sequencing.

Q2 2017 cash costs of $15.11 per ounce was a $17.51 increase from the negative $2.40 per ounce in Q2 2016. The main factors driving the increase were a 38% decrease in by-product credits, due to lower gold grades, and a 34% increase in direct unit operating costs. The increase in direct unit operating costs reflects severance payments associated with the culmination of the majority of open pit mining activities in Q2 2017, higher inflation and the elimination of the Patagonian Port export credit in Q4 2016.

Q2 2017 AISCSOS of $18.13 were $21.64 higher than Q2 2016 AISCSOS of negative $3.51. The increase was driven by: higher direct unit operating costs; decreased positive NRV inventory adjustments; a decline in gold quantities produced and sold due primarily to lower gold grades; and an increase in direct selling costs due to the elimination of the Patagonian Port export credit in Q4 2016. These factors were partially offset by a 52% increase in silver ounces sold.

In Q2 2017, sustaining capital expenditures totaled $0.2 million, comparable with the $0.5 million in Q2 2016. The quarter-over-quarter decrease was primarily the result of lower exploration drilling in the current quarter.

| PAN AMERICAN SILVER CORP. | 15 | |

| OPERATING OUTLOOK FOR 2017 | ||

Production

Q2 2017 consolidated silver production of 6.30 million ounces brought H1 2017 production to 12.5 million ounces, in line with the rate required to achieve management’s full year forecast range of 24.5 to 26.0 million silver ounces. With the expected silver production for the remainder of the year, management reaffirms the 2017 annual silver production forecast, as indicated in the 2016 annual MD&A dated March 22, 2017.

Gold production in Q2 2017 was 37.7 thousand ounces bringing H1 2017 production to 75.4 thousand ounces. Given the anticipated increased production for the remainder of 2017 at both Dolores and Manantial Espejo, management reaffirms the 2017 annual gold production forecast of 155.0 to 165.0 thousand ounces.

Q2 2017 zinc, lead, and copper production of 13.7 thousand tonnes, 5.5 thousand tonnes and 3.5 thousand tonnes, respectively, were within management's expectations based on current mine plans. With H1 2017 zinc, lead, and copper production of 26.5 thousand tonnes, 10.8 thousand tonnes, and 6.7 thousand tonnes, respectively, management reaffirms the 2017 annual zinc, lead and copper production forecasts of 56.5 to 58.5 thousand tonnes, 19.0 to 20.0 thousand tonnes, and 8.8 to 9.3 thousand tonnes, respectively.

Cash Costs and AISCSOS

The following tables summarize the first half of 2017 cash costs and AISCSOS achieved for each operation compared to the 2017 annual amounts forecast in the 2016 MD&A. For the purposes of these comparisons, the check marks have the following meanings:

| üü | Actual results were better than 2017 annual guidance range |

| ü | Actual results met 2017 annual guidance range |

| û | Actual results fell short of 2017 annual guidance range |

2017 Cash Costs(1) ($ per ounce) | 2017 AISCSOS(2) ($ per ounce) | |||||||

Forecast (3) | H1 2017 | Forecast (3) | H1 2017 | |||||

| La Colorada | 3.35 – 3.95 | 3.20 | üü | 5.00 – 5.90 | 5.80 | ü | ||

| Dolores | 1.25 – 2.25 | (0.74 | ) | üü | 11.00 – 12.50 | 8.66 | üü | |

| Alamo Dorado | 18.00 – 20.00 | 17.03 | üü | 18.40 – 19.40 | 19.34 | ü | ||

| Huaron | 5.95 – 6.95 | 1.51 | üü | 9.25 – 10.50 | 5.55 | üü | ||

| Morococha | 3.15 – 4.15 | (2.78 | ) | üü | 8.25 – 9.75 | 3.50 | üü | |

| San Vicente | 10.90 – 11.90 | 13.16 | û | 13.80 – 14.80 | 14.33 | ü | ||

| Manantial Espejo | 15.35 – 16.25 | 17.46 | û | 16.90 – 18.10 | 22.53 | û | ||

| Consolidated Total | 6.45 – 7.45 | 5.94 | üü | 11.50 – 12.90 | 11.66 | ü | ||

| (1) | Cash costs per ounce is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed description of the cash cost calculation, details of the Company’s by-product credits and a reconciliation of this measure to the Q2 2017 Financial Statements. |

| (2) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (non-GAAP) Measures” section of this MD&A for a detailed description of the AISCSOS calculation and a reconciliation of this measure to the Q2 2017 Financial Statements. |

| (3) | Forecast amount per 2016 annual MD&A dated March 22, 2017. |

H1 2017 consolidated cash costs of $5.94 were $0.51 per ounce, or 8%, less than the low end of management’s 2017 annual forecast range of $6.45 to $7.45. Based on this performance, and the expected results for the remainder of 2017, which are largely influenced by commodity prices and currency exchange rate assumptions, management is revising its full-year 2017 cash cost guidance to between $5.50 and $6.50 per ounce.

| PAN AMERICAN SILVER CORP. | 16 | |

The revised 2017 annual cash costs per mine are as follows:

Revised 2017 Annual Cash Costs Forecast (1) ($ per ounce) | |

| La Colorada | 3.00 – 3.50 |

| Dolores | (1.60) – 0.00 |

| Alamo Dorado | 17.03 |

| Huaron | 3.35 – 4.50 |

| Morococha | 1.00– 2.00 |

| San Vicente | 11.50 – 13.00 |

| Manantial Espejo | 16.90 – 17.50 |

| Consolidated Total | 5.50 – 6.50 |

| (1) | Cash costs per ounce is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed description of the cash cost calculation. |

H1 2017 consolidated AISCSOS of $11.66 were closer to the low end of management’s 2017 annual forecast of $11.50 to $12.90. Based on the H1 2017 AISCSOS results, and the expected results for the remainder of 2017, management has lowered the annual 2017 AISCSOS guidance to $10.50 - $11.50.

The revised 2017 AISCSOS per mine are as follows:

Revised 2017 Annual AISCSOS Forecast (1) ($ per ounce) | |

| La Colorada | 4.75 – 5.50 |

| Dolores | 7.25 – 8.50 |

| Alamo Dorado | 17.25 |

| Huaron | 6.75 – 7.75 |

| Morococha | 6.50 – 7.50 |

| San Vicente | 13.50 – 14.75 |

| Manantial Espejo | 19.00 – 19.75 |

| Consolidated Total | 10.50 – 11.50 |

| (1) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed description of the AISCSOS calculation. |

| PAN AMERICAN SILVER CORP. | 17 | |

Capital Expenditures

Total sustaining and project capital investment during H1 2017 were as follows:

| 2017 Capital Investment | Original Annual Forecast(1) | Actual (2) | ||||

| (in millions of USD) | Six months ended June 30, 2017 | |||||

| La Colorada | 10.5 – 11.5 | 6.5 | ||||

| Dolores | 39.0 – 40.0 | 14.8 | ||||

| Alamo Dorado | — | — | ||||

| Huaron | 8.0 – 9.0 | 4.4 | ||||

| Morococha | 9.0 – 10.0 | 6.3 | ||||

| San Vicente | 12.0 – 13.0 | 3.8 | ||||

| Manantial Espejo | 3.5 – 4.5 | 1.3 | ||||

Sustaining Capital total(2) | 82.0 - 88.0 | 37.0 | ||||

| La Colorada project capital | 6.5 – 7.5 | 3.0 | ||||

| Dolores project capital | 51.5 – 54.5 | 26.9 | ||||

| Project Capital Total | 58.0 - 62.0 | 29.9 | ||||

| Consolidated Total | 140.0 – 150.0 | 66.9 | ||||

| (1) | Annual guidance as provided in 2016 annual MD&A dated March 22, 2017. |

| (2) | The sustaining capital amounts capitalized in H1 2017 were $6.2 million less than the $43.2 million of H1 2017 sustaining capital cash outflows, which are included in the H1 2017 AISCSOS calculation, shown in the “Alternative Performance (non-GAAP) Measures” section of this MD&A, and are different from the sustaining capital amounts in the tables included in the "Individual Mine Performance" section of this MD&A. These differences are due to the timing difference between the cash payment of capital investments compared to the period in which investments are capitalized. |

Total sustaining capital investment for H1 2017 was $37.0 million, while project capital investment totaled $29.9 million. Management continues to expect sustaining capital in 2017 to be between $82.0 and $88.0 million, however, now expects project capital to increase to be between $73.5 and $78.5 million due to an approximately $5.0 million increase in Dolores expansion and approximately $11.0 million to $12.5 million to advance the Joaquin and COSE project developments in Argentina, partially offset by slightly lower project capital at La Colorada.

The revised 2017 annual sustaining and project capital forecasts are as follows:

| 2017 Capital Investment | Revised Forecast | |||

| (in millions of USD) | ||||

| La Colorada | 11.5 – 12.0 | |||

| Dolores | 38.0 – 39.0 | |||

| Alamo Dorado | — | |||

| Huaron | 8.5 – 9.0 | |||

| Morococha | 11.0 – 11.5 | |||

| San Vicente | 7.5 – 10.5 | |||

| Manantial Espejo | 5.5 – 6.0 | |||

| Sustaining Capital total | 82.0 - 88.0 | |||

| La Colorada project | 6.0 – 6.5 | |||

| Dolores projects | 56.5 – 59.5 | |||

| Joaquin & COSE projects | 11.0 – 12.5 | |||

| Project Capital Total | 73.5 - 78.5 | |||

| Consolidated Total | 155.5 – 166.5 | |||

| PAN AMERICAN SILVER CORP. | 18 | |

| PROJECT DEVELOPMENT UPDATE | ||

The following table reflects the amounts spent at each of Pan American’s major projects in Q2 2017 as compared to Q2 2016.

| Project Development Investment | Three months ended June 30, | Six months ended June 30, | ||||||

| (thousands of USD) | ||||||||

| 2017 | 2016 | 2017 | 2016 | |||||

Dolores Projects (1) | 13,747 | 12,624 | 26,864 | 22,369 | ||||

La Colorada Expansion (2) | 1,229 | 15,395 | 2,991 | 28,142 | ||||

| Total | 14,976 | 28,019 | 29,855 | 50,511 | ||||

| (1) | As a result of periodic changes in accounts payable balances, the amounts capitalized for the projects during the three and six months ended June 30, 2017 were $nil and $0.9 million less than the project cash outflows in those periods, respectively (2016: $1.0 million less and $0.9 million more, respectively) |

| (2) | As a result of periodic changes in accounts payable balances, the amounts capitalized for the project during the three and six months ended June 30, 2017 were $1.5 million more and $2.4 million more than the project cash outflows in those periods, respectively (2016: $0.3 million more and $2.7 million less, respectively) |

Dolores Projects

During Q2 2017, the Company invested $13.7 million on the Dolores expansion projects, with efforts directed at:

| • | completing construction of the new pulp agglomeration plant. Commissioning is underway and the 5,600 tonnes per day ("tpd") crushing and grinding circuits performed well during initial testing. As anticipated, the commissioning team is currently concentrating on bringing the three large plate and frame filter presses on-line; |

| • | continuing development of the Dolores underground mine, including completing a total of 1,235 metres of drift advance and continued diamond drilling of the central and south zones; and |

| • | expansion of the mine ventilation and electrical systems also progressed during Q2 2017. |

The Dolores underground mine project remains on-track for production to begin before the end of 2017. Initial production during the second half of 2017 and early 2018 will focus predominantly on the central zone to allow the completion of definition and mine planning for the south zone. The central zone is expected to commence production in early Q4 2017, and will ramp up to the full designed mining rate through the course of 2018.

The Company expects total project capital to complete both the pulp agglomeration plant and the underground mine to increase by approximately $5.0 million. The Dolores expansion project is expected to increase silver and gold production through a combination of greater throughput and higher recoveries. The Company continues to forecast ramping-up production of the pulp agglomeration plant to the design rate of 5,600 tpd by the end of 2017.

La Colorada Expansion Project

During Q2 2017, the Company invested $1.2 million in the final stages of the La Colorada expansion project, with efforts primarily relating to underground mine development and completing the construction of the new 115kV power line. The underground development advanced ahead of plan and achieved the targeted 1,800 tonnes per day mining and processing rates during the last month of Q2 2017. In addition, the new power line was energized in Q2 2017.

Joaquin and COSE Project Developments

The Company anticipates spending approximately $11.0 million to $12.5 million on advancing the new Joaquin and COSE Projects in Argentina during 2017. At Joaquin, the Company has initiated an approximate 6,200 metre drill program and engineering analysis to determine the quantity of potentially economic material that could be trucked to the Manantial Espejo processing plant for treatment and expects to complete a preliminary economic assessment on the project by year-end 2017. At COSE, the Company is proceeding with a $23.9 million capital investment (excluding the final $7.5 million project acquisition payment due on the earlier of May 31, 2018 or the commencement of commercial production) to construct an underground mine at COSE over the next 18 to 24 months.

| PAN AMERICAN SILVER CORP. | 19 | |

| OVERVIEW OF Q2 2017 FINANCIAL RESULTS | ||

| • | Selected Annual and Quarterly Information |

The following tables set out selected quarterly results for the past six quarters as well as selected annual results for the past two years. The dominant factors affecting results in the quarters and years presented below are volatility of metal prices realized, and the timing of the sales of production, which varies with the timing of shipments. The fourth quarter of 2015 included impairment charges to Morococha, Dolores, and Alamo Dorado, while the third quarter of 2015 included impairment charges to Manantial Espejo.

| 2017 | Quarter Ended | |||||

| (In thousands of USD, other than per share amounts) | March 31 | June 30, | ||||

| Revenue | $ | 198,687 | $ | 201,319 | ||

| Mine operating earnings | $ | 32,875 | $ | 44,782 | ||

| Earnings for the period attributable to equity holders | $ | 19,371 | $ | 35,472 | ||

| Basic earnings per share | $ | 0.13 | $ | 0.23 | ||

| Diluted earnings per share | $ | 0.13 | $ | 0.23 | ||

| Cash flow from operating activities | $ | 38,569 | $ | 42,906 | ||

| Cash dividends paid per share | $ | 0.025 | $ | 0.025 | ||

| Other financial information | ||||||

| Total assets | $ | 1,901,269 | $ | 1,921,813 | ||

Total long-term financial liabilities(1) | $ | 123,918 | $ | 124,019 | ||

| Total attributable shareholders’ equity | $ | 1,422,940 | $ | 1,454,876 | ||

| (1) | Total long-term financial liabilities are comprised of non-current liabilities excluding deferred tax liabilities, deferred revenue, and share purchase warrant liabilities. |

| 2016 | Quarter Ended | Year Ended | |||||||||||||

| (In thousands of USD, other than per share amounts) | March 31 | June 30 | Sept 30 | Dec 31 | Dec 31 | ||||||||||

| Revenue | $ | 158,275 | $ | 192,258 | $ | 233,646 | $ | 190,596 | $ | 774,775 | |||||

| Mine operating earnings | $ | 16,698 | $ | 44,730 | $ | 88,495 | $ | 48,956 | $ | 198,879 | |||||

Earnings for the period attributable to equity holders | $ | 1,738 | $ | 33,804 | $ | 42,766 | $ | 21,777 | $ | 100,085 | |||||

| Basic earnings per share | $ | 0.01 | $ | 0.22 | $ | 0.28 | $ | 0.14 | $ | 0.66 | |||||

| Diluted earnings per share | $ | 0.01 | $ | 0.22 | $ | 0.28 | $ | 0.14 | $ | 0.66 | |||||

| Cash flow from operating activities | $ | 771 | $ | 66,019 | $ | 102,346 | $ | 45,668 | $ | 214,804 | |||||

| Cash dividends paid per share | $ | 0.0125 | $ | 0.0125 | $ | 0.0125 | $ | 0.0125 | $ | 0.0500 | |||||

| Other financial information | |||||||||||||||

| Total assets | $ | 1,898,141 | |||||||||||||

Total long-term financial liabilities(1) | $ | 118,594 | |||||||||||||

| Total attributable shareholders’ equity | $ | 1,396,298 | |||||||||||||

| (1) | Total long-term financial liabilities are comprised of non-current liabilities excluding deferred tax liabilities, deferred revenue, and share purchase warrant liabilities. |

| PAN AMERICAN SILVER CORP. | 20 | |

| 2015 | Quarter Ended | Year Ended | |||||||||||||

| (In thousands of USD, other than per share amounts) | March 31 | June 30 | Sept 30 | Dec 31 | Dec 31 | ||||||||||

| Revenue | $ | 178,125 | $ | 174,189 | $ | 159,414 | $ | 162,960 | $ | 674,688 | |||||

| Mine operating earnings (loss) | $ | 2,630 | $ | (952 | ) | $ | (25,996 | ) | $ | (7,771 | ) | $ | (32,089 | ) | |

Loss for the period attributable to equity holders | $ | (19,371 | ) | $ | (7,322 | ) | $ | (67,048 | ) | $ | (132,909 | ) | $ | (226,650 | ) |

| Basic loss per share | $ | (0.13 | ) | $ | (0.05 | ) | $ | (0.44 | ) | $ | (0.88 | ) | $ | (1.49 | ) |

| Diluted loss per share | $ | (0.13 | ) | $ | (0.05 | ) | $ | (0.44 | ) | $ | (0.88 | ) | $ | (1.49 | ) |

| Cash flow from operating activities | $ | 11,848 | $ | 20,577 | $ | 32,866 | $ | 23,401 | $ | 88,692 | |||||

| Cash dividends paid per share | $ | 0.1250 | $ | 0.0500 | $ | 0.0500 | $ | 0.0500 | $ | 0.2750 | |||||

| Other financial information | |||||||||||||||

| Total assets | $ | 1,715,037 | |||||||||||||

Total long-term financial liabilities(1) | $ | 114,354 | |||||||||||||

| Total attributable shareholders’ equity | $ | 1,297,222 | |||||||||||||

| (1) | Total long-term financial liabilities are comprised of non-current liabilities excluding deferred tax liabilities, deferred revenue, and share purchase warrant liabilities. |

| • | Income Statement: Q2 2017 vs. Q2 2016 |

Net earnings of $36.0 million were recorded in Q2 2017 compared to $34.2 million in Q2 2016, which corresponds to basic earnings per share of $0.23 and $0.22, respectively.

The following table highlights the key items driving the difference between the net earnings in Q2 2017 as compared to those recorded in Q2 2016:

Net earnings, three months ended June 30, 2016 (in thousands of USD) | $ | 34,226 | ||||||

| Increased revenue: | ||||||||

| Increased realized metal prices | $ | 16,081 | ||||||

| Lower quantities of metal sold | (1,505 | ) | ||||||

| Decreased direct selling costs | 3,892 | |||||||

Increased negative settlement adjustments | (9,407 | ) | ||||||

| Total increase in revenue | $ | 9,061 | ||||||

Increased cost of sales: | ||||||||

| Increased production costs and increased royalty charges | $ | (8,063 | ) | |||||

| Increased depreciation and amortization | (946 | ) | ||||||

| Total increase in cost of sales | $ | (9,009 | ) | |||||

| Decreased income tax expense | 12,033 | |||||||

| Decreased interest and finance expense | 2,609 | |||||||

| Decreased general and administrative expense | 1,825 | |||||||

| Increased foreign exchange gain | 1,676 | |||||||

| Decreased investment income and other expense | 965 | |||||||

| Increased dilution gain, net of share of loss from associate | 649 | |||||||

| Decreased net gain on asset sales, commodity contracts and derivatives | (16,258 | ) | ||||||

| Increased exploration and project development expense | (1,766 | ) | ||||||

| Net earnings, three months ended June 30, 2017 | $ | 36,011 | ||||||

| PAN AMERICAN SILVER CORP. | 21 | |

Revenue for Q2 2017 was $201.3 million, a $9.1 million increase from $192.3 million in Q2 2016. The major factors for the increase were: a $16.1 million price variance from higher realized metal prices; a $3.9 million decrease in direct selling costs, primarily from favorable changes in contract terms relating to concentrate treatment and refining charges; partially offset by a $9.4 million increase to negative settlement adjustments on concentrate shipments and a $1.5 million variance from lower quantities of gold and copper sold.

The following table reflects the metal prices realized by the Company and the quantities of metal sold during each quarter:

| Realized Metal Prices | Quantities of Metal Sold | ||||||||||

| Three months ended June 30, | Three months ended June 30, | ||||||||||

| 2017 | 2016 | 2017 | 2016 | ||||||||

Silver(1) – koz | $ | 17.19 | $ | 16.87 | 6,311 | 5,843 | |||||

Gold(1) – koz | $ | 1,257 | $ | 1,257 | 37.7 | 43.6 | |||||

Zinc(1) – kt | $ | 2,604 | $ | 1,962 | 12.6 | 12.4 | |||||

Lead(1) – kt | $ | 2,203 | $ | 1,731 | 5.2 | 5.0 | |||||

Copper(1) – kt | $ | 5,685 | $ | 4,650 | 3.4 | 4.0 | |||||

| (1) | Metal price stated as dollars per ounce for silver and gold, and dollars per tonne for zinc, lead and copper, inclusive of final settlement adjustments on concentrate sales. |

Increased quarter-over-quarter realized silver and zinc prices of 2% and 33%, respectively, had the most significant impact on revenues. Lead and copper realized prices increased 27%, and 22%, respectively. The quantity of gold sold in Q2 2017 was 14% lower than Q2 2016, largely from lower production at Manantial Espejo and Alamo Dorado. Quarter-over-quarter copper sales volumes were down 15%, driven by copper production declines at Morococha. These sales volume decreases were partially offset by an 8%, 4% and 2% increase in the quantity of silver, lead and zinc sold, respectively.

Mine operating earnings of $44.8 million in Q2 2017 were comparable to the $44.7 million recorded in Q2 2016. The similar quarterly mine operating earnings was the result of the previously discussed $9.1 million increase in revenue being partially offset by a net $9.0 million increase in cost of sales.

Q2 2017 production costs of $121.9 million were $12.9 million higher than in Q2 2016. The quarter-over-quarter variance included a $3.4 million decrease to net cost reducing NRV inventory adjustments, mainly from Manantial Espejo. The remaining increase to production costs included: higher production costs at Manantial Espejo, driven by $3.5 million in open-pit related severance costs, inflation and increased sales volumes; higher costs at San Vicente and La Colorada, primarily from increased sales volumes; partially offset by decreased costs at Dolores from inventory buildups and decreased costs at Alamo Dorado from lower production and sales volumes.

Depreciation and amortization expense ("D&A") of $30.7 million in Q2 2017 was $0.9 million higher than in Q2 2016, largely the result of increased D&A at La Colorada on account of the newly commissioned and depreciable plant and mine shaft, partially offset by decreased D&A at Manantial Espejo due to deferred stripping activities being fully depreciated in 2016. Royalty costs in Q2 2017 were $3.9 million, $4.8 million lower than in Q2 2016, which was largely attributable to the San Vicente royalty payments for shipments in Q1 2017 that were subsequently sold in Q2 2017.

General and Administrative ("G&A") expense was $5.3 million in Q2 2017 compared to $7.1 million in Q2 2016. The $1.8 million decrease was mainly driven by lower accrued bonuses in the current quarter, principally in relation to restricted share unit cash compensation that references the Company’s share price. Share-based compensation was $0.9 million in Q2 2017 compared to $0.9 million in Q2 2016.

Exploration and project development expenses were $4.4 million in Q2 2017 compared to $2.7 million incurred in Q2 2016. The expenses recorded in each quarter primarily related to exploration and project development activities near the Company’s existing mines, at select greenfield projects, and on the holding and maintenance costs associated with the Navidad project, where approximately $0.6 million was spent in Q2 2017 compared to approximately $1.0 million in Q2 2016.

| PAN AMERICAN SILVER CORP. | 22 | |

Foreign exchange (“FX”) gains in Q2 2017 were $0.1 million compared to FX losses of $1.6 million incurred in Q2 2016. Gains in Q2 2017 resulted primarily from the approximate 5% appreciation of the Mexican Peso ("MXN") during the quarter on MXN denominated monetary assets, which were substantially offset by the approximate 8% depreciation of the Argentine peso (“ARS”) on the Company’s ARS denominated monetary assets. The Q2 2016 losses were primarily driven by the devaluation of the MXN and ARS on the Company’s monetary assets denominated in those currencies.

Gain on sale of mineral properties, plant and equipment in Q2 2017 was $0.3 million compared to $17.9 million in Q2 2016. The significant quarter-over-quarter decrease is attributable to no significant asset sales and related gains or losses in Q2 2017 compared to the gain recognized in Q2 2016 on the sale of 75% of the shares in Compania Minera Shalipayco S.A.C. ("Shalipayco") for $15.0 million in cash and a one percent (1%) net smelter returns royalty with a fair value of $3.3 million. Shalipayco is the owner of the Shalipayco zinc development project located in the departments of Pasco and Junín, Peru.

Share of income from associate and dilution gain for Q2 2017 was $0.6 million, compared to $nil in Q2 2016, and related largely to the Company's investment in Maverix Metals Inc. ("Maverix"), accounted for using the equity method whereby the Company records its portion of Maverix's income or loss based on Pan American's fully diluted ownership interest. During Q2 2017, a $0.2 million gain was recognized for the Company's portion of Maverix's estimated income. Further, in Q2 2017 as a result of Maverix issuing common shares to acquire certain royalties assets, Pan American's ownership of Maverix was diluted to approximately 36% (approximately 40% on a fully-diluted basis). The net result of this transaction was the recognition of a $0.5 million dilution gain in Q2 2017, representing the difference between the fair value of Pan American's portion of the assets acquired by Maverix, and the interest in Maverix lost from dilution.

Interest and finance expense for Q2 2017 was $0.1 million recovery compared to a $2.5 million expense in Q2 2016. Q2 2017 included a $2.8 million reversal of a prior year's interest expense accrual. The remaining portion of interest and finance expense consisted of accretion of the Company’s closure liabilities and interest expense associated with the revolving credit facility, short-term loans and leases.

Income tax expense in Q2 2017 was $1.5 million compared to $13.5 million in Q2 2016. The $12.0 million decrease was mainly due to the decrease in earnings before income taxes, changes in current tax expense estimated for prior years, foreign tax rate differences, and the impact of foreign exchange rate fluctuations (mainly the appreciation of the Mexican Peso). These factors resulted in an effective tax rate that varied from the comparable period, as shown in the following table:

| PAN AMERICAN SILVER CORP. | 23 | |

| Three months ended June 30, | ||||||||

| (In thousands of USD, except as noted) | 2017 | 2016 | ||||||

| Earnings before taxes and non-controlling interest | $ | 37,502 | $ | 47,750 | ||||

| Statutory Canadian income tax rate | 26.00 | % | 26.00 | % | ||||

| Income tax expense based on above rates | $ | 9,751 | $ | 12,415 | ||||

| Increase (decrease) due to: | ||||||||

| Non-deductible expenditures | 1,166 | 895 | ||||||

| Foreign tax rate differences | (228 | ) | 1,574 | |||||

| Change in net deferred tax assets not recognized: | ||||||||

| - Argentina exploration expenditures | 521 | 466 | ||||||

| - Other deferred tax assets | (3,179 | ) | (3,145 | ) | ||||

| Non-taxable portion of net earnings of affiliates | (1,264 | ) | (1,229 | ) | ||||

| Effect of other taxes paid (mining and withholding) | 2,448 | 2,037 | ||||||

| Effect of foreign exchange on tax expense | (8,761 | ) | (1,548 | ) | ||||

| Non-taxable impact of foreign exchange | 5,017 | 1,188 | ||||||

| Change in current tax expense estimated for prior years | (4,254 | ) | (424 | ) | ||||

| Other | 274 | 1,295 | ||||||

| Income tax expense | $ | 1,491 | $ | 13,524 | ||||

| Effective income tax rate | 3.98 | % | 28.32 | % | ||||

| • | Statement of Cash Flows: Q2 2017 vs. Q2 2016 |

Cash flow from operations in Q2 2017 totaled $42.9 million, $23.1 million less than the $66.0 million generated in Q2 2016. The decrease was largely the result of: a $20.7 million decrease in operating cash flows from working capital changes and; a $10.2 million increase in taxes paid; partially offset by increased cash mine operating earnings, realized FX gains and other income.

Working capital changes in Q2 2017 resulted in an $8.2 million use of cash comprised mainly of trade and other receivables ("AR") buildups. Comparatively, working capital changes added $12.5 million to Q2 2016 operating cash flows, made largely of accounts payable and accrued liability ("AP") pay downs, and AR collections in the quarter. Quarter-over-quarter increased mine operating earnings excluding non-cash D&A and NRV adjustments were approximately $4.4 million, driven by increased revenues and decreased royalty costs, partially offset by increased production costs (excluding non-cash NRV inventory adjustments).

Investing activities utilized $63.2 million in Q2 2017, inclusive of $15.9 million used on the net purchase of short-term investments. The balance of Q2 2017 investing activities consisted primarily of spending $41.8 million on mineral property, plant and equipment at the Company’s mines and projects, as previously described in the “Operating Performance” section of this MD&A, and $7.5 million towards the acquisition of the COSE project, located in the Santa Cruz province of southern Argentina. In Q2 2016, investing activities utilized $33.4 million inclusive of $4.7 million generated on the net sale of short-term investments, $52.8 million spent on mineral property, plant and equipment additions at the Company’s various operations and projects, and $15.0 million generated on the sale of Shalipayco.

Financing activities in Q2 2017 used $2.5 million compared to $3.8 million in Q2 2016. Cash used in Q2 2017 consisted of $3.8 million paid as dividends to shareholders, $2.5 million obtained from short-term proceeds, $0.4 million in proceeds on share issuances from the exercises of stock options, and $1.0 million of lease repayments. In Q2 2016, $1.9 million of dividends were paid, $1.5 million was used for short-term debt repayment (net of proceeds), $0.8 million of lease payments were made, and $0.6 million in proceeds were generated on share issuances from the exercises of stock options.

| PAN AMERICAN SILVER CORP. | 24 | |

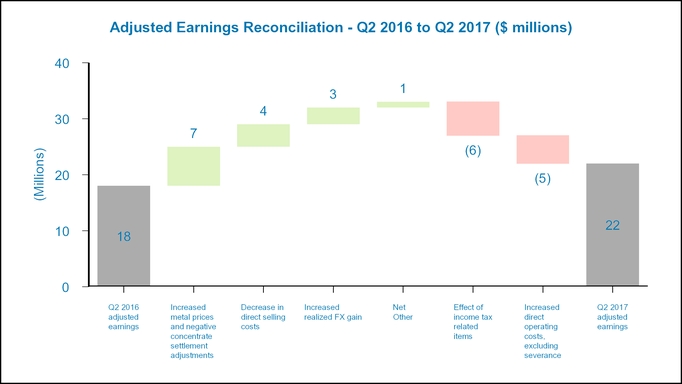

| • | Q2 2017 and Q2 2016 Adjusted Earnings |

Adjusted earnings and basic adjusted earnings per share are non-GAAP measures that the Company considers to better reflect normalized earnings as it eliminates items that in management's judgment are subject to volatility as a result of factors which are unrelated to operations in the period, and/or relate to items that will settle in future periods. Neither adjusted earnings nor basic adjusted earnings per share have any standardized meaning prescribed by GAAP and are therefore unlikely to be comparable to similar measures presented by other companies.

Please refer to the section of this MD&A entitled “Alternative Performance (Non-GAAP) Measures” for a detailed description of “adjusted earnings” and “basic adjusted earnings per share”, and a reconciliation of these second quarter measures to the Q2 2017 Financial Statements.

Adjusted Earnings in Q2 2017 was $22.3 million, representing a basic adjusted earnings per share of $0.15, which was $4.3 million, or $0.03 per share, higher than Q2 2016 adjusted earnings of $18.0 million, and basic adjusted earnings per share of $0.12, respectively.

The following chart illustrates the key factors leading to the change in adjusted earnings from Q2 2016 to Q2 2017:

| PAN AMERICAN SILVER CORP. | 25 | |

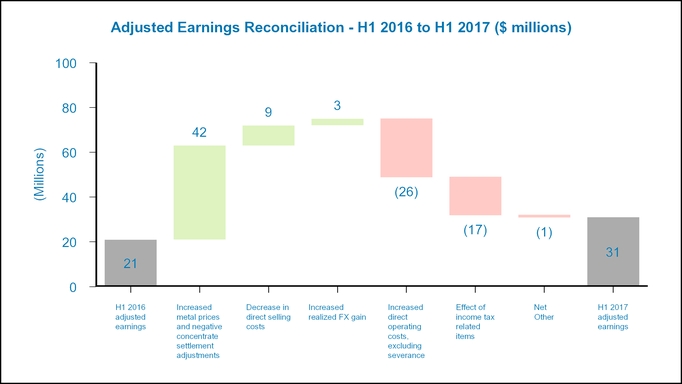

| • | Income Statement: H1 2017 vs. H1 2016 |

Net earnings of $56.0 million were recorded in H1 2017 compared to $36.1 million in H1 2016, which corresponds to basic earnings per share of $0.36 and $0.23, respectively.

The following table highlights the key items driving the difference between the net earnings in H1 2017 and H1 2016:

Net earnings, six months ended June 30, 2016 (in thousands of USD) | $ | 36,101 | ||||||

| Increased revenue: | ||||||||

| Increased realized metal prices | $ | 51,557 | ||||||

| Lower quantities of metal sold | (1,660 | ) | ||||||

| Decreased direct selling costs | 8,747 | |||||||

Increased negative settlement adjustments | (9,171 | ) | ||||||

| Total increase in revenue | $ | 49,473 | ||||||

Increased cost of sales: | ||||||||

| Increased production costs and increased royalty charges | $ | (32,316 | ) | |||||

| Increased depreciation and amortization | (928 | ) | ||||||

| Total increase in cost of sales | $ | (33,244 | ) | |||||

| Decreased income tax expense | 8,292 | |||||||

| Increased foreign exchange gain | 5,957 | |||||||

| Decreased investment income and other expense | 2,621 | |||||||

| Decreased interest and finance expense | 2,017 | |||||||

| Decreased general and administrative expense | 1,800 | |||||||

| Increased dilution gain, net of share of loss from associate | 1,420 | |||||||

| Decreased net gain on asset sales, commodity contracts and derivatives | (14,468 | ) | ||||||

| Increased exploration and project development expense | (4,008 | ) | ||||||

| Net earnings, six months ended June 30, 2017 | $ | 55,961 | ||||||

Revenue for H1 2017 was $400.0 million, a $49.5 million increase from the $350.5 million of revenue recognized in H1 2016. The major factor driving the variance was a $51.6 million price variance from higher realized prices for all metals sold, though mainly from higher realized zinc and silver prices which increased by 48% and 9%, respectively. Other period-over-period variances included: a $1.7 million negative variance from lower quantities of metal sold, driven by a 7% and 23% decline in gold and copper sales volumes, partially offset by a 6% and 18% increase in silver and lead sales volumes, respectively; a $9.2 million negative variance from settlement adjustments on concentrate shipments; and an $8.7 million positive variance from a period-over-period decrease in selling costs, mainly from favorable changes in contract terms relating to concentrate treatment and refining charges.

The following table reflects the metal prices realized by the Company and the quantities of metal sold during each period:

| Realized Metal Prices | Quantities of Metal Sold | ||||||||||

| Six months ended June 30, | Six months ended June 30, | ||||||||||

| 2017 | 2016 | 2017 | 2016 | ||||||||

Silver(1) – koz | $ | 17.31 | 15.88 | 12,297 | 11,559 | ||||||

Gold(1) – koz | $ | 1,238 | 1,219 | 76.7 | 82.9 | ||||||

Zinc(1) – kt | $ | 2,714 | 1,834 | 23.2 | 23.2 | ||||||

Lead(1) – kt | $ | 2,258 | 1,741 | 10.6 | 9.0 | ||||||

Copper(1) – kt | $ | 5,749 | $ | 4,658 | 6.1 | 8.0 | |||||

| (1) | Metal price stated as dollars per ounce for silver and gold, and dollars per tonne for zinc, lead and copper, inclusive of final settlement adjustments on concentrate sales. |

Increased period-over-period realized silver and zinc prices of 9% and 48%, respectively, had the most significant impact on increased revenues. Gold, lead, and copper realized prices increased 2%, 30%, and 23%.

| PAN AMERICAN SILVER CORP. | 26 | |

H1 2017 silver and lead sales volumes were 6% and 18% higher than in H1 2016, respectively. Copper and gold sales volumes decreased by 24% and 7%, respectively, while period over period zinc sales volumes remained consistent.

Mine operating earnings of $77.7 million in H1 2017 were $16.2 million higher than the $61.4 million recorded in H1 2016. The 26% increase was the result of the previously discussed $49.5 million increase in revenue being partially offset by a net $33.2 million increase in cost of sales.

H1 2017 production costs of $251.1 million were $36.3 million higher than those in H1 2016. This production cost variance included a net negative $18.0 million period-over-period change in NRV inventory adjustments (at Manantial Espejo, Dolores and Alamo) which increased H1 2017 costs by $5.5 million and decreased H1 2016 costs by $12.5 million. Similar to the quarter-over-quarter variance, the remaining increase in production costs included: higher production costs at Manantial Espejo, driven by severance costs, inflation and increased sales volumes; higher costs at La Colorada, primarily from increased sales volumes; partially offset by decreased costs at Alamo Dorado from lower production and sales volumes; and decreased costs at Dolores partially from inventory buildups.