Exhibit 99.2

Management’s Discussion

and Analysis

FOR THE THREE AND NINE MONTHS ENDED SEPTEMBER 30, 2018

|

| | |

| | PAN AMERICAN SILVER CORP. | 9 |

|

| |

| TABLE OF CONTENTS | |

| | |

| |

| |

| Highlights | |

| Operating Performance | |

| 2018 Annual Operating Outlook | |

| Project Development Update | |

| Overview of Financial Results | |

| |

| |

| |

| |

| |

| |

| |

| |

| Cautionary Note | |

|

| | |

| | PAN AMERICAN SILVER CORP. | 10 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

November 6, 2018

This Management’s Discussion and Analysis (“MD&A”) is intended to help the reader understand the significant factors that influence the performance of Pan American Silver Corp. and its subsidiaries (collectively “Pan American”, “we”, “us”, “our” or the “Company”) and such factors that may affect its future performance. This MD&A should be read in conjunction with the Company’s audited consolidated financial statements for the year ended December 31, 2017 (the "2017 Financial Statements"), and the related notes contained therein, and the unaudited condensed interim consolidated financial statements for the three and nine months ended September 30, 2018 (the “Q3 2018 Financial Statements”), and the related notes contained therein. All amounts in this MD&A, the 2017 Financial Statements, and the Q3 2018 Financial Statements are expressed in United States dollars (“USD”), unless identified otherwise. The Company reports its financial position, results of operations and cash flows in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board. Pan American’s significant accounting policies are set out in Note 2 of the 2017 Financial Statements.

This MD&A refers to various non-Generally Accepted Accounting Principles (“non-GAAP”) measures, such as “all-in sustaining cost per silver ounce sold", “cash costs per ounce of silver”, "total debt", “working capital", “general and administrative cost per silver ounce produced”, “adjusted earnings” and “basic adjusted earnings per share”, which are used by the Company to manage and evaluate operating performance at each of the Company’s mines and are widely reported in the mining industry as benchmarks for performance, but do not have standardized meaning under IFRS. To facilitate a better understanding of these non-GAAP measures as calculated by the Company, additional information has been provided in this MD&A. Please refer to the section of this MD&A entitled “Alternative Performance (Non-GAAP) Measures” for a detailed description of “all-in sustaining cost per silver ounce sold”, “cash costs per ounce of silver”, “working capital”, “general and administrative cost per silver ounce produced”, “adjusted earnings“ and “basic adjusted earnings per share”, as well as details of the Company’s by-product credits and a reconciliation of these measures to the Q3 2018 Financial Statements.

Any reference to “cash costs” or “cash costs per ounce of silver” in this MD&A should be understood to mean cash costs per ounce of silver, net of by-product credits. Any reference to “AISCSOS” in this MD&A should be understood to mean all-in sustaining costs per silver ounce sold, net of by-product credits.

Except for historical information contained in this MD&A, the following disclosures are forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and forward-looking information within the meaning of applicable Canadian provincial securities laws or are future oriented financial information and as such are based on an assumed set of economic conditions and courses of action. Please refer to the cautionary note regarding forward-looking statements and information at the back of this MD&A and the “Risks Related to Pan American’s Business” contained in the Company’s most recent Annual Information Form on file with the Canadian provincial securities regulatory authorities and Form 40-F on file with the U.S. Securities and Exchange Commission (the “SEC”). Additional information about Pan American and its business activities, including its Annual Information Form, is available on SEDAR at www.sedar.com

|

| | |

| | PAN AMERICAN SILVER CORP. | 11 |

|

| | |

| CORE BUSINESS AND STRATEGY | | |

Pan American engages in silver mining and related activities, including exploration, mine development, extraction, processing, refining and reclamation. The Company owns and operates silver mines located in Peru, Mexico, Argentina, and Bolivia. In addition, the Company is exploring for new silver deposits and opportunities throughout North and South America. The Company is listed on the Toronto Stock Exchange (Symbol: PAAS) and on the Nasdaq Global Select Market (“NASDAQ”) in New York (Symbol: PAAS).

Pan American’s vision is to be the world’s pre-eminent silver producer, with a reputation for excellence in discovery, engineering, innovation and sustainable development. To achieve this vision, we base our business on the following strategy:

| |

| • | Generate sustainable profits and superior returns on investments through the safe, efficient and environmentally sound development and operation of silver assets. |

| |

| • | Constantly replace and grow our mineable silver reserves and resources through targeted near-mine exploration and global business development. |

| |

| • | Foster positive long-term relationships with our employees, our shareholders, our communities and our local governments through open and honest communication and ethical and sustainable business practices. |

| |

| • | Continually search for opportunities to upgrade and improve the quality of our silver assets both internally and through acquisition. |

| |

| • | Encourage our employees to be innovative, responsive and entrepreneurial throughout our entire organization. |

To execute this strategy, Pan American has assembled a sector-leading team of mining professionals with a depth of knowledge and experience in all aspects of our business, which enables the Company to confidently advance early stage projects through construction and into operation.

Pan American is determined to conduct its business in a responsible and sustainable manner. Caring for the environment in which we operate, contributing to the long-term development of our host communities and ensuring that our employees can work in a safe and secure manner are core values at Pan American. We are committed to maintaining positive relations with our employees, the local communities and the government agencies, all of whom we view as partners in our enterprise.

|

| | |

| | PAN AMERICAN SILVER CORP. | 12 |

Operations

| |

| • | Silver production of 6.25 million ounces, on track to achieve annual guidance |

Consolidated silver production for the three months ended September 30, 2018 ("Q3 2018") of 6.25 million ounces was 6% more than the 5.89 million produced in the three months ended September 30, 2017 ("Q3 2017"). Silver production for the nine months ended September 30, 2018 ("YTD 2018") totaled 18.6 million ounces, which is in-line with expectations and on-track to achieve management's annual guidance for 2018 of 25.0 million to 26.5 million ounces.

| |

| • | By-product production on track to achieve annual guidance |

Consolidated gold production in Q3 2018 was 42.1 thousand ounces, 1.2 thousand ounces higher than the 40.8 thousand ounces produced in Q3 2017. YTD 2018 gold production of 141.7 thousand ounces is in-line with expected production required to achieve guidance for 2018 of 175.0 thousand to 185.0 thousand ounces.

Zinc production in Q3 2018 was 16.7 thousand tonnes, 19% higher than in the comparable quarter of 2017. Lead production was 5.7 thousand tonnes, 8% more than Q3 2017 production. Copper production of 2.6 thousand tonnes was 30% lower than in Q3 2017. YTD 2018 base metal production was 46.3 thousand tonnes of zinc, 16.1 thousand tonnes of lead, and 7.6 thousand tonnes of copper, all in-line with expectations and on-track to achieve management's guidance for 2018 of 60.0 thousand to 62.0 thousand tonnes of zinc, 21.0 thousand to 22.0 thousand tonnes of lead, and most recent guidance of 9.0 thousand to 10.4 thousand tonnes of copper. Guidance for copper was revised in the second quarter MD&A dated August 8, 2018 (the "Q2 2018 MD&A").

| |

| • | Cash Costs of $5.24 per ounce |

Consolidated cash costs for Q3 2018 were $5.24 per ounce, $2.12 per ounce or 68% higher than in Q3 2017. YTD 2018 cash costs of $2.45 per ounce were $2.59 per ounce or 51% lower than those for the nine months ended September 30, 2017 ("YTD 2017"), and are less than the low end of management’s reduced guidance range of $2.80 to $3.80 per ounce stated in the Q2 2018 MD&A. Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales.

Financial

Revenue in Q3 2018 of $187.7 million was down 2% from Q3 2017, mainly due to lower metal prices being largely offset by increased quantities of metal sold for all products except copper.

Net loss for Q3 2018 was $9.2 million ($0.06 basic loss per share) compared with earnings of $17.8 million ($0.11 basic earnings per share) in Q3 2017. The Q3 2018 loss reflects: decreased mine operating earnings as a result of higher production costs, driven by increased sales volumes and the inclusion of $23.4 million of negative net realizable value ("NRV") inventory adjustments; and increased depreciation and amortization. These factors were partially offset by lower income tax expense.

Adjusted loss in Q3 2018 was $4.7 million ($0.03 basic adjusted loss per share) compared with $23.3 million ($0.15 basic adjusted earnings per share) in Q3 2017. Lower revenue from decreased metal prices, and increased production costs, driven by NRV adjustments, partially offset by lower income tax expense, were the major drivers in the quarter-over-quarter adjusted earnings decrease.

| |

| • | Liquidity and working capital position |

As at September 30, 2018, the Company had cash and short-term investment balances of $252.7 million, working capital of $443.6 million, and $300.0 million available under its undrawn revolving credit facility. Total debt of $8.4 million was related entirely to finance lease liabilities.

| |

| • | All-In Sustaining Costs per Silver Ounce Sold (“AISCSOS”) |

Q3 2018 AISCSOS of $13.73, inclusive of $3.68 per ounce in NRV inventory adjustments, was $5.04, or 58%, higher than in Q3 2017. YTD 2018 AISCSOS of $9.21 was in line with management's reduced guidance for 2018 AISCSOS of

|

| | |

| | PAN AMERICAN SILVER CORP. | 13 |

$8.50 to $10.00, as provided in the Q2 2018 MD&A. AISCSOS is a non-GAAP measure; please refer to the section “Alternative Performance (Non-GAAP) Measures” of this MD&A for a detailed description of the calculation and a reconciliation of this measure to the Q3 2018 Financial Statements.

The following table provides silver production and cash costs at each of Pan American’s operations for the respective three and nine-month periods ended September 30, 2018 and 2017:

|

| | | | | | | | | | | | | | | | | |

| | | Silver Production (ounces ‘000s) | Cash Costs(1) ($ per ounce) |

| | | Three months ended

September 30, | Nine months ended

September 30, | Three months ended

September 30, | Nine months ended

September 30, |

| | | 2018 | 2017 | 2018 | 2017 | 2018 | 2017 | 2018 | 2017 |

| La Colorada | | 2,020 |

| 1,825 |

| 5,543 |

| 5,186 |

| 3.50 |

| 1.71 |

| 2.13 |

| 2.68 |

|

| Dolores | | 967 |

| 974 |

| 3,257 |

| 2,976 |

| 1.00 |

| (0.57 | ) | (4.12 | ) | (0.69 | ) |

| Alamo Dorado | | — |

| — |

| — |

| 608 |

| NA |

| NA |

| NA |

| 17.03 |

|

| Huaron | | 922 |

| 939 |

| 2,595 |

| 2,733 |

| 3.25 |

| 0.31 |

| 1.19 |

| 1.09 |

|

Morococha(2) | | 758 |

| 634 |

| 2,141 |

| 1,912 |

| (0.65 | ) | (8.16 | ) | (6.06 | ) | (4.56 | ) |

San Vicente(3) | | 867 |

| 806 |

| 2,607 |

| 2,507 |

| 11.14 |

| 12.99 |

| 10.44 |

| 13.11 |

|

| Manantial Espejo | | 718 |

| 715 |

| 2,505 |

| 2,477 |

| 16.50 |

| 12.73 |

| 11.19 |

| 16.10 |

|

Total (4) | | 6,253 |

| 5,893 |

| 18,649 |

| 18,400 |

| 5.24 |

| 3.12 |

| 2.45 |

| 5.04 |

|

| |

| (1) | Cash costs is a non-GAAP measure. Please refer to the section “Alternative Performance (Non-GAAP) Measures” of this MD&A for a detailed description of the cash cost calculation, details of the Company’s by-product credits and a reconciliation of this measure to the Q3 2018 Financial Statements. |

| |

| (2) | Morococha data represents Pan American's 92.3% interest in the mine's production. |

| |

| (3) | San Vicente data represents Pan American's 95.0% interest in the mine's production. |

| |

| (4) | Totals may not add due to rounding. |

Silver Production

Consolidated silver production in Q3 2018 was 0.36 million ounces more than in Q3 2017 as a result of higher production at La Colorada, Morococha, and San Vicente. La Colorada production benefited from the mine expansion completed in 2017, while San Vicente benefited from mechanization programs and improvements to ore control. The increase in production at Morococha was due to mine sequencing. Each operation’s silver production variances are further discussed in the “Individual Mine Performance” section of this MD&A.

Cash Costs

Consolidated cash costs for Q3 2018 were $5.24, up 68% from Q3 2017, as a result of lower by-product credits, primarily from decreased base metal prices, and higher operating costs, primarily due to the expanded operations at our Mexican mines. These factors that increased cash costs were partially offset by decreased direct selling costs from improved contract terms for concentrate treatment and refining.

By-Product Production

The following table provides the Company’s by-product production for the three and nine-month periods ended September 30, 2018 and 2017:

|

| | | | | | | | |

| | By-Product Production |

Three months ended

September 30, | Nine months ended

September 30, |

| 2018 |

| 2017 |

| 2018 |

| 2017 |

|

| Gold – koz | 42.1 |

| 40.8 |

| 141.7 |

| 116.3 |

|

| Zinc – kt | 16.7 |

| 14.1 |

| 46.3 |

| 40.6 |

|

| Lead – kt | 5.7 |

| 5.3 |

| 16.1 |

| 16.1 |

|

| Copper – kt | 2.6 |

| 3.7 |

| 7.6 |

| 10.4 |

|

|

| | |

| | PAN AMERICAN SILVER CORP. | 14 |

The 3% increase in quarterly gold production is mostly due to better grades from mine sequencing and faster recoveries from the pulp agglomeration plant at Dolores.

Zinc production in Q3 2018 was 19% higher than Q3 2017, driven by higher grades at Morococha and San Vicente from mine sequencing, and higher throughput at the expanded La Colorada mine. Lead production in Q3 2018 was 8% higher than Q3 2017, resulting from increased grades due to mine sequencing at both Peruvian operations. Copper production in Q3 2018 was 30% lower than Q3 2017, primarily because of anticipated lower copper grades at both Peruvian mines. Each operation’s by-product production variances are further discussed in the “Individual Mine Performance” section of this MD&A.

Average Market Metal Prices

The following tables set out the average market price for each metal produced for the three and nine-month periods ended September 30, 2018 and 2017:

|

| | | | | | | | |

| Average Market Metal Prices(1) |

Three months ended

September 30, | Nine months ended

September 30, |

| 2018 |

| 2017 |

| 2018 |

| 2017 |

|

| Silver $/ounce | 15.02 |

| 16.84 |

| 16.10 |

| 17.16 |

|

| Gold $/ounce | 1,213 |

| 1,278 |

| 1,282 |

| 1,251 |

|

| Zinc $/tonne | 2,537 |

| 2,963 |

| 3,020 |

| 2,783 |

|

| Lead $/tonne | 2,104 |

| 2,334 |

| 2,337 |

| 2,259 |

|

| Copper $/tonne | 6,105 |

| 6,349 |

| 6,642 |

| 5,952 |

|

| |

| (1) | Average market prices for zinc, lead and copper are the London Metal Exchange cash prices for the three and nine-month periods ended September 30, 2018 and 2017. Silver and gold prices are the London Bullion Metal Association prices for the same periods. |

AISCSOS

The following table reflects the quantities of payable silver sold and AISCSOS at each of Pan American’s operations for the three and nine months ended September 30, 2018, as compared to the same periods in 2017:

|

| | | | | | | | | | | | | | | | |

| Payable Silver Sold (ounces ‘000s) | AISCSOS(1) ($ per ounce) |

Three months ended

September 30, | Nine months ended

September 30, | Three months ended

September 30, | Nine months ended

September 30, |

| 2018 |

| 2017 |

| 2018 |

| 2017 |

| 2018 |

| 2017 |

| 2018 |

| 2017 |

|

| La Colorada | 2,258 |

| 1,642 |

| 5,289 |

| 5,006 |

| 6.27 |

| 3.48 |

| 4.20 |

| 5.04 |

|

| Dolores | 950 |

| 933 |

| 3,335 |

| 2,864 |

| 25.52 |

| 8.03 |

| 11.40 |

| 8.45 |

|

| Alamo Dorado | — |

| 91 |

| — |

| 734 |

| — |

| 6.38 |

| — |

| 17.73 |

|

| Huaron | 785 |

| 818 |

| 2,236 |

| 2,368 |

| 11.07 |

| 2.94 |

| 7.18 |

| 4.65 |

|

| Morococha | 688 |

| 576 |

| 1,978 |

| 1,791 |

| 4.52 |

| (0.46 | ) | 0.59 |

| 2.23 |

|

| San Vicente | 876 |

| 632 |

| 2,551 |

| 2,384 |

| 11.11 |

| 18.62 |

| 11.92 |

| 15.47 |

|

| Manantial Espejo | 810 |

| 562 |

| 2,471 |

| 2,405 |

| 24.78 |

| 19.25 |

| 14.07 |

| 21.76 |

|

Total (2) | 6,366 |

| 5,255 |

| 17,860 |

| 17,552 |

| 13.73 |

| 8.69 |

| 9.21 |

| 10.77 |

|

| |

| (1) | AISCSOS is a non-GAAP measure. Please refer to the section “Alternative Performance (Non-GAAP) Measures” of this MD&A for a detailed description of the AISCSOS calculation and a reconciliation of this measure to the Q3 2018 Financial Statements. G&A costs are included in the consolidated AISCSOS, but not allocated in calculating AISCSOS for each operation. |

| |

| (2) | Totals may not add due to rounding. |

Consolidated AISCSOS for Q3 2018 were $13.73, representing a 58% increase from the comparable period in 2017. The quarter-over-quarter increase was due to the following factors: (i) an increase in negative NRV adjustments of $22.1 million, (ii) increased operating costs due to additional activity at both the expanded operations in Mexico, and (iii) increased cash sustaining capital, primarily due to the timing of cash outflows at Dolores and a tailings storage facility raise and a mine deepening project at Huaron. These increases in AISCSOS were partially offset by higher volumes of silver ounces sold and better concentrate treatment terms.

|

| | |

| | PAN AMERICAN SILVER CORP. | 15 |

Individual Mine Performance

An analysis of performance at each operation in Q3 2018 compared with Q3 2017 follows. The project capital amounts invested in Q3 2018 are further discussed in the Project Development Update section of this MD&A.

La Colorada mine

|

| | | | | | | | | | | | |

| | Three months ended

September 30, | Nine months ended

September 30, |

| | 2018 |

| 2017 |

| 2018 |

| 2017 |

|

| Tonnes milled - kt | 191.2 |

| 175.3 |

| 538.5 |

| 484.6 |

|

| Average silver grade – grams per tonne | 360 |

| 355 |

| 352 |

| 366 |

|

| Average zinc grade - % | 2.62 |

| 2.70 |

| 2.74 |

| 2.79 |

|

| Average lead grade - % | 1.30 |

| 1.56 |

| 1.36 |

| 1.55 |

|

| Average silver recovery - % | 91.2 |

| 91.2 |

| 91.0 |

| 91.1 |

|

| Average zinc recovery - % | 86.4 |

| 83.1 |

| 86.1 |

| 83.6 |

|

| Average lead recovery - % | 87.3 |

| 86.7 |

| 87.4 |

| 87.1 |

|

| Production: | |

| |

| | |

| Silver – koz | 2,020 |

| 1,825 |

| 5,543 |

| 5,186 |

|

| Gold – koz | 1.14 |

| 1.21 |

| 3.24 |

| 3.03 |

|

| Zinc – kt | 4.33 |

| 3.93 |

| 12.70 |

| 11.30 |

|

| Lead – kt | 2.17 |

| 2.37 |

| 6.40 |

| 6.53 |

|

| | | | | |

Cash cost per ounce net of by-products(1) | $ | 3.50 |

| $ | 1.71 |

| $ | 2.13 |

| $ | 2.68 |

|

| | | | | |

AISCSOS(2) | $ | 6.27 |

| $ | 3.48 |

| $ | 4.20 |

| $ | 5.04 |

|

| | | | | |

| Payable silver sold - koz | 2,258 |

| 1,642 |

| 5,289 |

| 5,006 |

|

| | | | | |

Sustaining capital - (’000s)(3) | $ | 3,902 |

| $ | 3,680 |

| $ | 10,097 |

| $ | 11,394 |

|

| |

| (1) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| |

| (2) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed description of the calculation and a reconciliation of this measure to the Q3 2018 Financial Statements. |

| |

| (3) | Sustaining capital expenditures exclude $1.1 million and $4.2 million of investing activity cash outflow for Q3 2018 and YTD 2018, respectively (Q3 2017 and YTD 2017: $2.0 million and $7.4 million, respectively) related to investment capital incurred on the La Colorada expansion project as disclosed in the “Project Development Update” section of this MD&A. |

Q3 2018 vs. Q3 2017

Production:

| |

| • | Silver: 11% increase, driven primarily from improved throughput attributable to the mine expansion completed in 2017. |

| |

| • | By-products: 10% increase in zinc from improved throughput, partially offset by lower grades from mine sequencing; and an 8% decrease in lead production due to lower grades from mine sequencing, partially offset by the increase in throughput. |

Cash costs: the 105% increase was primarily the result of increased operating costs due to higher direct unit operating costs, particularly power costs, as well as reduced by-product credits from lower base metal prices and lower lead and gold production. These factors were partially offset by the increase in zinc and silver production.

AISCSOS: the 80% increase was driven by the same factors as the increase in cash costs.

Sustaining Capital: primarily related to investments in equipment replacements and rehabilitations, the hydraulic backfill system, plant infrastructure, and increased near-mine exploration activities.

|

| | |

| | PAN AMERICAN SILVER CORP. | 16 |

Dolores mine

|

| | | | | | | | | | | | |

| | Three months ended

September 30, | Nine months ended

September 30, |

| | 2018 |

| 2017 |

| 2018 |

| 2017 |

|

| Tonnes placed - kt | 1,522.9 |

| 1,629.7 |

| 5,084.8 |

| 4,820.5 |

|

| Average silver grade – grams per tonne | 33 |

| 35 |

| 33 |

| 38 |

|

| Average gold grade – grams per tonne | 0.84 |

| 0.67 |

| 0.91 |

| 0.64 |

|

| Average silver produced to placed ratio - % | 59.8 |

| 53.5 |

| 60.2 |

| 50.3 |

|

| Average gold produced to placed ratio - % | 80.5 |

| 70.8 |

| 71.8 |

| 72.4 |

|

| Production: | |

| |

| | |

| Silver – koz | 967 |

| 974 |

| 3,257 |

| 2,976 |

|

| Gold – koz | 33.1 |

| 25.0 |

| 107.2 |

| 71.8 |

|

| | | | | |

Cash cost per ounce net of by-products(1) | $ | 1.00 |

| $ | (0.57 | ) | $ | (4.12 | ) | $ | (0.69 | ) |

| | | | | |

AISCSOS(2) | $ | 25.52 |

| $ | 8.03 |

| $ | 11.40 |

| $ | 8.45 |

|

| | | | | |

| Payable silver sold - koz | 950 |

| 933 |

| 3,335 |

| 2,864 |

|

| | | | | |

Sustaining capital - (’000s)(3) | $ | 9,971 |

| $ | 3,812 |

| $ | 35,587 |

| $ | 22,768 |

|

| |

| (1) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| |

| (2) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed description of the calculation and a reconciliation of this measure to the Q3 2018 Financial Statements. |

| |

| (3) | Sustaining capital expenditures exclude $1.8 million and $10.3 million of investing activity cash outflow for Q3 2018 and YTD 2018, respectively (Q3 2017 and YTD 2017: $12.5 million and $40.3 million, respectively) related to investment capital incurred on Dolores expansion projects, as disclosed in the “Project Development Update” section of this MD&A. |

Q3 2018 vs. Q3 2017

Production:

| |

| • | Silver: 1% lower due to a reduction in stacking rates and silver grades resulting from the re-sequencing of the mine plan because of the 15-day suspension of mining activities in June and seasonal heavy rains affecting access to certain ore zones, partially offset by enhanced recoveries attributable to the pulp agglomeration plant completed in 2017. Delivery of additional plate and frame expansion kits, to maximize the capacity of the existing filter units in the pulp agglomeration plant, occurred in Q3 2018 and installation is planned for the fourth quarter of 2018. |

| |

| • | By-products: 33% increase in gold due to better grades from mine sequencing, and higher recoveries due to the addition of the pulp agglomeration plant and the timing of leach pad kinetics, partially offset by a reduction in stacking rates during the quarter. |

Cash costs: increased $1.57 per ounce due to higher operating costs associated with the pulp agglomeration plant, higher direct unit operating costs, particularly power costs, delays in the ramp up of stope mining in the underground mine, and greater waste mining due to the re-sequencing of the mine plan. These factors were partially offset by greater by-product credits from higher gold production.

AISCSOS: increased $17.49 per ounce, due to the following factors: (i) negative NRV adjustments that resulted in a quarter over quarter increase of $14.20 per ounce, (ii) a $6.2 million increase in cash sustaining capital expenditures due mostly to the timing of payables and higher pre-stripping rates to offset the mine suspension in Q2 2018, and (iii) higher direct operating costs as described above. These factors were partially offset by higher by-product credits from higher gold sales during the quarter.

Sustaining Capital: comprised mainly of pre-stripping and the restart of the leach pad expansions, both of which were at higher levels of activity compared to Q3 2017.

|

| | |

| | PAN AMERICAN SILVER CORP. | 17 |

Huaron mine

|

| | | | | | | | | | | | |

| | Three months ended

September 30, | Nine months ended

September 30, |

| | 2018 |

| 2017 |

| 2018 |

| 2017 |

|

| Tonnes milled - kt | 244.8 |

| 241.5 |

| 683.0 |

| 696.6 |

|

| Average silver grade – grams per tonne | 141 |

| 142 |

| 142 |

| 145 |

|

| Average zinc grade - % | 2.39 |

| 2.65 |

| 2.42 |

| 2.74 |

|

| Average lead grade - % | 1.29 |

| 1.11 |

| 1.17 |

| 1.26 |

|

| Average copper grade - % | 0.81 |

| 0.90 |

| 0.76 |

| 0.89 |

|

| Average silver recovery - % | 82.3 |

| 85.6 |

| 82.5 |

| 85.6 |

|

| Average zinc recovery - % | 75.8 |

| 77.7 |

| 75.9 |

| 77.5 |

|

| Average lead recovery - % | 73.8 |

| 76.8 |

| 74.3 |

| 78.1 |

|

| Average copper recovery - % | 79.1 |

| 80.9 |

| 76.6 |

| 79.5 |

|

| Production: | |

| |

| | |

| Silver – koz | 922 |

| 939 |

| 2,595 |

| 2,733 |

|

| Gold – koz | 0.21 |

| 0.27 |

| 0.57 |

| 0.96 |

|

| Zinc – kt | 4.45 |

| 4.97 |

| 12.56 |

| 14.73 |

|

| Lead – kt | 2.33 |

| 2.03 |

| 5.88 |

| 6.74 |

|

| Copper – kt | 1.57 |

| 1.74 |

| 3.92 |

| 4.89 |

|

| | | | | |

Cash cost per ounce net of by-products(1) | $ | 3.25 |

| $ | 0.31 |

| $ | 1.19 |

| $ | 1.09 |

|

| | | | | |

AISCSOS(2) | $ | 11.07 |

| $ | 2.94 |

| $ | 7.18 |

| $ | 4.65 |

|

| | | | | |

| Payable silver sold – koz | 785 |

| 818 |

| 2,236 |

| 2,368 |

|

| | | | | |

| Sustaining capital - (’000s) | $ | 5,733 |

| $ | 1,512 |

| $ | 11,456 |

| $ | 6,719 |

|

| |

| (1) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| |

| (2) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed description of the calculation and a reconciliation of this measure to the Q3 2018 Financial Statements. |

Q3 2018 vs. Q3 2017

Production:

| |

| • | Silver: 2% lower, primarily due to lower recoveries from mine sequencing into different ore types. |

| |

| • | By-products: 10% decrease in both zinc and copper production, and a 14% increase in lead production as a result of mine sequencing. |

Cash costs: $2.94 per ounce higher due primarily to higher direct unit operating costs and reduced by-product credits from lower base metal prices and lower zinc and copper production, partially offset by improved concentrate treatment terms.

AISCSOS: an increase of $8.13 due to the same factors affecting quarter-over-quarter cash costs, as well as higher sustaining capital.

Sustaining Capital: related primarily to equipment replacements and refurbishments, plant and infrastructure upgrades, near-mine exploration, mine deepening and a tailings storage facility raise. The increase from Q3 2017 was related primarily to the tailings storage facility raise and mine deepening projects, both of which began in 2018.

|

| | |

| | PAN AMERICAN SILVER CORP. | 18 |

Morococha mine(1)

|

| | | | | | | | | | | | |

| | Three months ended

September 30, | Nine months ended

September 30, |

| | 2018 |

| 2017 |

| 2018 |

| 2017 |

|

| Tonnes milled – kt | 169.5 |

| 171.7 |

| 509.0 |

| 506.3 |

|

| Average silver grade – grams per tonne | 155 |

| 132 |

| 147 |

| 135 |

|

| Average zinc grade - % | 3.89 |

| 3.09 |

| 3.72 |

| 2.93 |

|

| Average lead grade - % | 0.90 |

| 0.70 |

| 0.87 |

| 0.76 |

|

| Average copper grade - % | 0.67 |

| 1.28 |

| 0.74 |

| 1.25 |

|

| Average silver recovery - % | 91.0 |

| 89.0 |

| 90.3 |

| 88.6 |

|

| Average zinc recovery - % | 87.9 |

| 79.6 |

| 87.0 |

| 79.0 |

|

| Average lead recovery - % | 75.4 |

| 64.0 |

| 75.6 |

| 65.0 |

|

| Average copper recovery - % | 76.7 |

| 84.8 |

| 78.2 |

| 84.0 |

|

| Production: | |

| |

| | |

| Silver – koz | 758 |

| 634 |

| 2,141 |

| 1,912 |

|

| Gold – koz | 0.44 |

| 1.08 |

| 1.90 |

| 2.71 |

|

| Zinc – kt | 5.80 |

| 4.19 |

| 16.40 |

| 11.65 |

|

| Lead – kt | 1.14 |

| 0.75 |

| 3.29 |

| 2.46 |

|

| Copper – kt | 0.85 |

| 1.80 |

| 2.85 |

| 5.15 |

|

| | | | | |

Cash cost per ounce net of by-products (2) | $ | (0.65 | ) | $ | (8.16 | ) | $ | (6.06 | ) | $ | (4.56 | ) |

| | | | | |

AISCSOS(3) | $ | 4.52 |

| $ | (0.46 | ) | $ | 0.59 |

| $ | 2.23 |

|

| | | | | |

| Payable silver sold (100%) - koz | 688 |

| 576 |

| 1,978 |

| 1,791 |

|

| | | | | |

| Sustaining capital (100%) - (’000s) | $ | 3,509 |

| $ | 2,995 |

| $ | 11,801 |

| $ | 9,266 |

|

| |

| (1) | Production figures are for Pan American’s 92.3% share only, unless otherwise noted. |

| |

| (2) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to our cost of sales. |

| |

| (3) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed description of the calculation and a reconciliation of this measure to the Q3 2018 Financial Statements. |

Q3 2018 vs. Q3 2017

Production:

| |

| • | Silver: 20% higher, primarily due to higher grades from mine sequencing. |

| |

| • | By-products: a 52% and 38% increase in lead and zinc production, respectively, and a 53% decrease in copper production, all related to mine sequencing. |

Cash costs: $7.51 per ounce higher, primarily because of lower by-product prices and higher direct unit operating costs, partially offset by higher silver production and better concentrate treatment terms.

AISCSOS: the $4.98 per ounce increase was primarily driven by the same factors affecting quarter-over-quarter cash costs.

Sustaining Capital: primarily related to expanded near-mine exploration, equipment replacements and refurbishments, mine ventilation, and plant and infrastructure upgrades.

|

| | |

| | PAN AMERICAN SILVER CORP. | 19 |

San Vicente mine (1)

|

| | | | | | | | | | | | |

| | Three months ended

September 30, | Nine months ended

September 30, |

| | 2018 |

| 2017 |

| 2018 |

| 2017 |

|

| Tonnes milled – kt | 82.9 |

| 86.6 |

| 244.7 |

| 238.6 |

|

| Average silver grade – grams per tonne | 354 |

| 330 |

| 358 |

| 362 |

|

| Average zinc grade - % | 3.12 |

| 1.79 |

| 2.45 |

| 1.91 |

|

| Average lead grade - % | 0.36 |

| 0.29 |

| 0.34 |

| 0.30 |

|

| Average silver recovery - % | 92.7 |

| 90.8 |

| 93.5 |

| 92.1 |

|

| Average zinc recovery - % | 82.9 |

| 65.8 |

| 77.9 |

| 65.1 |

|

| Average lead recovery - % | 76.1 |

| 75.5 |

| 77.6 |

| 80.4 |

|

| Production: | |

| |

| | |

| Silver – koz | 867 |

| 806 |

| 2,607 |

| 2,507 |

|

| Gold – koz | 0.12 |

| 0.13 |

| 0.39 |

| 0.38 |

|

| Zinc – kt | 2.16 |

| 1.02 |

| 4.65 |

| 2.96 |

|

| Lead – kt | 0.10 |

| 0.15 |

| 0.54 |

| 0.36 |

|

| Copper – kt | 0.21 |

| 0.11 |

| 0.80 |

| 0.31 |

|

| | | | | |

Cash cost per ounce net of by-products (2) | $ | 11.14 |

| $ | 12.99 |

| $ | 10.44 |

| $ | 13.11 |

|

| | | | | |

AISCSOS(3) | $ | 11.11 |

| $ | 18.62 |

| $ | 11.92 |

| $ | 15.47 |

|

| | | | | |

| Payable silver sold (100%) - koz | 876 |

| 632 |

| 2,551 |

| 2,384 |

|

| | | | | |

| Sustaining capital (100%) - (’000s) | $ | 1,731 |

| $ | 2,400 |

| $ | 5,321 |

| $ | 6,207 |

|

| |

| (1) | Production figures are for Pan American’s 95.0% share only, unless otherwise noted. |

| |

| (2) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| |

| (3) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed description of the calculation and a reconciliation of this measure to the Q3 2018 Financial Statements. |

Q3 2018 vs. Q3 2017

Production:

| |

| • | Silver: 8% higher due to a 7% increase in head grades and better recoveries, partially offset by a decrease in throughput while enhancing the mechanization of the mine. The increase in head grades was attributable to efforts to improve mining dilution through better ore control. |

| |

| • | By-products: 112% and 91% increases in zinc and copper, respectively, and a 40% decrease in lead were the result of overall better base metal grades due to mine sequencing and reduced mining dilution. |

Cash costs: 14% lower due to increased base metal quantities, improved concentrate terms, and increased silver production; partially offset by higher direct unit operating costs, largely due to the transition to more mechanized mining methods, and wage increases.

AISCSOS: a 40% reduction due to the same factors affecting quarter-over-quarter cash costs, as well as lower royalty expenses due to the timing of revenue and royalty expense recognition, which had negatively impacted the comparable period.

Sustaining Capital: Q3 2018 expenditures primarily relate to mine equipment replacements and rehabilitations, near-mine exploration, tailings storage facility expansion, and mine site and camp infrastructure.

|

| | |

| | PAN AMERICAN SILVER CORP. | 20 |

Manantial Espejo mine

|

| | | | | | | | | | | | |

| | Three months ended

September 30, | Nine months ended

September 30, |

| | 2018 |

| 2017 |

| 2018 |

| 2017 |

|

| Tonnes milled - kt | 206.1 |

| 206.1 |

| 605.9 |

| 588.3 |

|

| Average silver grade – grams per tonne | 121 |

| 119 |

| 148 |

| 143 |

|

| Average gold grade – grams per tonne | 1.12 |

| 2.05 |

| 1.56 |

| 1.97 |

|

| Average silver recovery - % | 87.5 |

| 89.4 |

| 87.6 |

| 90.8 |

|

| Average gold recovery - % | 94.1 |

| 93.9 |

| 93.5 |

| 93.9 |

|

| Production: | |

| |

| | |

| Silver – koz | 718 |

| 715 |

| 2,505 |

| 2,477 |

|

| Gold – koz | 7.06 |

| 13.18 |

| 28.37 |

| 35.36 |

|

| | | | | |

Cash cost per ounce net of by-products (1) | $ | 16.50 |

| $ | 12.73 |

| $ | 11.19 |

| $ | 16.10 |

|

| | | | | |

AISCSOS(2) | $ | 24.78 |

| $ | 19.25 |

| $ | 14.07 |

| $ | 21.76 |

|

| | | | | |

| Payable silver sold - koz | 810 |

| 562 |

| 2,471 |

| 2,405 |

|

| | | | | |

| Sustaining capital - (’000s) | $ | 763 |

| $ | 1,025 |

| $ | 2,391 |

| $ | 2,288 |

|

| |

| (1) | Cash costs is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed reconciliation of this measure to cost of sales. |

| |

| (2) | AISCSOS is a non-GAAP measure. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed description of the calculation and a reconciliation of this measure to the Q3 2018 Financial Statements. |

Q3 2018 vs. Q3 2017

Production:

| |

| • | Silver: comparable due to slightly better grades, partially offset by lower recoveries. |

| |

| • | By-products: 46% decrease in gold production due to processing of lower grade stockpile ore, as planned. |

Cash costs: a $3.77 per ounce increase as a result of lower by-product credits due to lower gold production and prices, partially offset by lower direct unit operating costs from the devaluation in the Argentine peso and the termination of open pit mining at the end of Q3 2017.

AISCSOS: a 29% increase due to a $7.3 million increase in negative NRV inventory adjustments and lower by-product credits, partially offset by lower operating costs.

Sustaining Capital: primarily related to near-mine exploration.

|

| | |

| | PAN AMERICAN SILVER CORP. | 21 |

|

| | |

| 2018 ANNUAL OPERATING OUTLOOK | | |

All 2018 forecast amounts in this section refer to the management's annual forecasts for 2018, as provided in the Company's 2017 Annual MD&A dated March 22, 2018, and the revised annual forecast for 2018 cash costs, AISCSOS and copper production, as provided in the Q2 2018 MD&A (together, the "2018 Forecast").

Production:

The following table summarizes the YTD 2018 metal production compared to the respective 2018 Forecast amounts:

|

| | | |

| | YTD 2018 Actual | 2018 Forecast | % of 2018 Forecast (1) |

| |

| Silver – Moz | 18.65 | 25.00 - 26.50 | 72% |

| Gold – koz | 141.7 | 175.0 - 185.0 | 79% |

| Zinc – kt | 46.3 | 60.0 - 62.0 | 76% |

| Lead – kt | 16.1 | 21.0 - 22.0 | 75% |

Copper – kt (2) | 7.6 | 9.0 - 10.4 | 78% |

| |

| (1) | Percentage calculated based on mid-point of the related 2018 guidance range. |

| |

| (2) | 2018 Forecast amount per as disclosed in the Q2 2018 MD&A. |

Based on year-to-date production results and the expected production for the remainder of the year, management reaffirms the 2018 Forecast annual consolidated metal production, as shown in the table above.

Cash Costs and AISCSOS:

The following table summarizes YTD 2018 cash costs and AISCSOS for each operation compared to the respective 2018 Forecast amounts.

For the purposes of these comparisons, the symbols have the following meanings:

|

| |

| üü | Actual results were better than 2018 Forecast range |

| ü | Actual results met 2018 Forecast range |

| û | Actual results were short of 2018 Forecast range |

|

| | | | | | |

| | Cash Costs(1) ($ per ounce) | AISCSOS(1) ($ per ounce) |

2018 Forecast(2)

| YTD 2018 Actual | 2018

Forecast(2)

| YTD 2018 Actual |

| La Colorada | 1.90 - 2.50 | $2.13 | ü | 4.80 - 5.70 | $4.20 | üü |

| Dolores | (2.00) - (2.50) | (4.12) | üü | 7.25 - 8.25 | $11.40 | û |

| Huaron | 1.25 - 2.00 | 1.19 | üü | 7.35 - 8.35 | $7.18 | üü |

| Morococha | (4.70) - (3.40) | (6.06) | üü | 3.20 - 5.20 | $0.59 | üü |

| San Vicente | 10.25 - 11.25 | 10.44 | ü | 12.00 - 13.25 | $11.92 | üü |

| Manantial Espejo | 10.75 - 14.50 | 11.19 | ü | 9.00 - 12.75 | $14.07 | û |

| Total | 2.80 - 3.80 | $2.45 | üü | 8.50 - 10.00 | $9.21 | ü |

| |

| (1) | Cash Costs and AISCSOS are non-GAAP measures. Please refer to the “Alternative Performance (Non-GAAP) Measures” section of this MD&A for a detailed description of these calculations and a reconciliation of these measures to the Q3 2018 Financial Statements. |

| |

| (2) | 2018 Forecast amount as disclosed in Q2 2018 MD&A. |

Based on YTD 2018 cash costs and AISCSOS, and the expected results for the remainder of 2018, management is reaffirming the annual 2018 cash costs and AISCSOS forecasts, as provided in the Q2 2018 interim MD&A dated August 8, 2018 and presented in the table above. These estimates are largely influenced by management's assumptions for commodity prices and currency exchange rates.

|

| | |

| | PAN AMERICAN SILVER CORP. | 22 |

Capital Expenditures:

The following table summarizes the YTD 2018 capital expenditures compared to the respective 2018 Forecast amounts:

|

| | | |

| | 2018 Capital Investment ($ millions)

|

| | YTD 2018 Actual(1) | 2018 Forecast | % of Annual Forecast (2) |

| La Colorada | 10.7 | 16.5 – 17.0 | 64% |

| Dolores | 33.5 | 47.5 – 49.0 | 69% |

| Huaron | 10.7 | 17.0 – 17.5 | 62% |

| Morococha | 11.3 | 12.0 – 12.5 | 92% |

| San Vicente | 5.3 | 6.0 – 7.0 | 82% |

| Manantial Espejo | 2.4 | 1.0 – 2.0 | 160% |

| Sustaining Capital Sub-total | 73.9 | 100.0 - 105.0 | 72% |

| Morococha projects | — | 2.0 | —% |

| Mexico projects | 13.1 | 13.0 | 101% |

| Joaquin and COSE projects | 16.4 | 35.0 | 47% |

| Project Capital Sub-total | 29.4 | 50.0 | 59% |

| Total Capital | 103.3 | 150.0 – 155.0 | 68% |

| |

| (1) | Total sustaining capital investments capitalized in YTD 2018 were $2.8 million less than the $76.7 million of sustaining capital cash outflows referenced in the individual mine tables and included in the YTD 2018 AISCSOS calculations, shown in the “Alternative Performance (Non-GAAP) Measures” section of this MD&A. In addition, project capital investments in YTD 2018 were $2.1 million less than the $31.6 million of YTD 2018 project capital cash outflows. These differences are due to the timing between the cash payment of capital investments compared with the period in which the investments are capitalized. |

| |

| (2) | Percentage calculated based on mid-point of the related 2018 guidance range. |

Based on year-to-date capital expenditures and those expected for the remainder of the year, management reaffirms the 2018 Forecast for annual consolidated sustaining capital expenditures; however, management has reduced the 2018 annual consolidated project capital to $40.0 million from $50 million to reflect the timing of expenditures for the Morococha, Joaquin and COSE projects. The revised 2018 capital forecast is as follows:

|

| |

| | 2018 Revised Capital Forecast ($ millions) |

| La Colorada | 17.5 – 18.5 |

| Dolores | 42.0 – 44.0 |

| Huaron | 17.0 – 17.5 |

| Morococha | 14.5 – 15.0 |

| San Vicente | 6.5 – 7.0 |

| Manantial Espejo | 2.5 – 3.0 |

| Sustaining Capital Sub-total | 100.0 - 105.0 |

| Morococha projects | 0 |

| Mexico projects | 15.5 |

| Joaquin and COSE projects | 24.5 |

| Project Capital Sub-total | 40.0 |

| Total Capital | 140.0 – 145.0 |

|

| | |

| | PAN AMERICAN SILVER CORP. | 23 |

|

| | |

| PROJECT DEVELOPMENT UPDATE | | |

The following table reflects the amounts spent at each of Pan American’s major projects in Q3 2018 and YTD 2018 as compared with Q3 2017 and YTD 2017.

|

| | | | | | | | |

| Project Development Investment | Three months ended

September 30, | Nine months ended

September 30, |

| (thousands of USD) |

| | 2018 |

| 2017 |

| 2018 |

| 2017 |

|

Dolores projects (1) | 1,633 |

| 14,040 |

| 8,324 |

| 40,904 |

|

La Colorada projects (2) | 1,460 |

| 3,276 |

| 4,740 |

| 6,267 |

|

Joaquin and COSE projects (3) | 5,253 |

| 607 |

| 16,380 |

| 607 |

|

| Total | 8,346 |

| 17,923 |

| 29,444 |

| 47,778 |

|

| |

| (1) | As a result of periodic changes in accounts payable balances, the amounts capitalized for the projects during Q3 2018 and YTD 2018 were $0.1 million and $2.0 million less than the project cash outflows, respectively (Q3 and YTD 2017: $1.5 million and $0.6 million more, respectively). |

| |

| (2) | As a result of periodic changes in accounts payable balances, the amounts capitalized for the projects during Q3 2018 and YTD 2018 were $0.4 million and $0.5 million more than the project cash outflows, respectively (Q3 and YTD 2017: $1.3 million more and $1.2 million less, respectively). |

| |

| (3) | As a result of periodic changes in accounts payable balances, the amounts capitalized for the projects during Q3 2018 and YTD 2018 were $0.7 million and $0.7 million less than the project cash outflows, respectively (Q3 and YTD 2017: $2.0 million and $2.0 million less, respectively). Amounts in 2017 exclude: 2017 acquisition costs for the Joaquin and COSE assets which had cash components of $15.0 million and $7.5 million respectively; exploration expenditures included in Q3 2017 and YTD 2017 "Exploration and project development expense" of $2.6 million and $3.7 million, respectively; and a $2.0 million prepaid deposit on mining equipment included in "Prepaid expenses and other current assets " as of September 30, 2017. |

During Q3 2018, the Company achieved the following progress on its projects:

Mexico:

The Company invested $1.6 million on completing the Dolores expansion projects, the majority of which was spent on the construction of the underground mine maintenance shop and the acquisition of additional underground mobile equipment units. The underground mine crews were remobilized following the 10-week suspension of underground mining, and the mine is currently being prepared to recommence production and ramp-up in the fourth quarter of 2018.

The Company invested $1.5 million on the La Colorada projects, primarily relating to the construction of a tailings storage facility raise and commissioning of a neutralization plant.

Joaquin and COSE:

The Company invested $3.7 million on the Joaquin project, primarily on the surface facilities and the initial fleet of development mining equipment. Approximately 145 metres of development were completed on the decline access for the underground mine, which was less than plan due to difficult ground being unexpectedly encountered close to surface. Subsequent to Q3 2017, the ramp passed successfully through the difficult ground conditions. The delay in developing the decline access may result in extending completion of the Joaquin project by approximately two months. The Joaquin project remains on budget.

During Q3 2018, the Company invested $1.6 million at COSE, primarily on the decline access to the underground mine. During the quarter, 308 metres of ramp development were completed for a total of 1125 metres to date. Construction commenced on the first underground electrical substation and the fresh air raise bore. The COSE project remains on budget.

|

| | |

| OVERVIEW OF Q3 2018 FINANCIAL RESULTS | | |

Selected Annual and Quarterly Information

The following tables set out selected quarterly results for the past eleven quarters as well as selected annual results for the past two years. The dominant factors affecting results in the quarters and years presented below are volatility of realized metal prices and the timing of sales, which varies with the timing of shipments. The fourth quarter of 2017 included an impairment reversal to Morococha and Calcatreu.

|

| | |

| | PAN AMERICAN SILVER CORP. | 24 |

|

| | | | | | | | | |

| 2018 | Quarter Ended |

| (In thousands of USD, other than per share amounts) | March 31 | June 30 | September 30 |

| Revenue | $ | 206,961 |

| $ | 216,460 |

| $ | 187,717 |

|

| Mine operating earnings (loss) | $ | 55,124 |

| $ | 54,851 |

| $ | (4,412 | ) |

| Earnings (loss) for the period attributable to equity holders | $ | 47,376 |

| $ | 36,187 |

| $ | (9,460 | ) |

| Basic earnings (loss) per share | $ | 0.31 |

| $ | 0.24 |

| $ | (0.06 | ) |

| Diluted earnings (loss) per share | $ | 0.31 |

| $ | 0.24 |

| $ | (0.06 | ) |

| Cash flow from operating activities | $ | 34,400 |

| $ | 66,949 |

| $ | 41,699 |

|

| Cash dividends paid per share | $ | 0.035 |

| $ | 0.035 |

| $ | 0.035 |

|

| Other financial information |

|

| |

|

|

| Total assets |

|

| | $ | 2,004,187 |

|

Total long-term financial liabilities(1) |

|

| | $ | 84,946 |

|

| Total attributable shareholders’ equity |

|

| | $ | 1,576,698 |

|

| |

| (1) | Total long-term financial liabilities are comprised of non-current liabilities excluding deferred tax liabilities, deferred revenue, and share purchase warrant liabilities. |

|

| | | | | | | | | | | | | | | |

| 2017 | Quarter Ended | Year

Ended |

| (In thousands of USD, other than per share amounts) | March 31 | June 30 | Sept 30 | Dec 31 | Dec 31 |

| Revenue | $ | 198,687 |

| $ | 201,319 |

| $ | 190,791 |

| $ | 226,031 |

| $ | 816,828 |

|

| Mine operating earnings | $ | 32,875 |

| $ | 44,782 |

| $ | 47,818 |

| $ | 43,285 |

| $ | 168,760 |

|

| Earnings for the period attributable to equity holders | $ | 19,371 |

| $ | 35,472 |

| $ | 17,256 |

| $ | 48,892 |

| $ | 120,991 |

|

| Basic earnings per share | $ | 0.13 |

| $ | 0.23 |

| $ | 0.11 |

| $ | 0.32 |

| $ | 0.79 |

|

| Diluted earnings per share | $ | 0.13 |

| $ | 0.23 |

| $ | 0.11 |

| $ | 0.32 |

| $ | 0.79 |

|

| Cash flow from operating activities | $ | 38,569 |

| $ | 42,906 |

| $ | 63,793 |

| $ | 79,291 |

| $ | 224,559 |

|

| Cash dividends paid per share | $ | 0.025 |

| $ | 0.025 |

| $ | 0.025 |

| $ | 0.025 |

| $ | 0.100 |

|

| Other financial information | | | | | |

| Total assets | | | | | $ | 1,993,332 |

|

Total long-term financial liabilities(1) | | | | | $ | 90,027 |

|

| Total attributable shareholders’ equity | | | | | $ | 1,516,850 |

|

| |

| (1) | Total long-term financial liabilities are comprised of non-current liabilities excluding deferred tax liabilities, deferred revenue, and share purchase warrant liabilities. |

|

| | | | | | | | | | | | | | | |

| 2016 | Quarter Ended | Year

Ended |

| (In thousands of USD, other than per share amounts) | March 31 | June 30 | Sept 30 | Dec 31 | Dec 31 |

| Revenue | $ | 158,275 |

| $ | 192,258 |

| $ | 233,646 |

| $ | 190,596 |

| $ | 774,775 |

|

| Mine operating earnings | $ | 16,698 |

| $ | 44,730 |

| $ | 88,495 |

| $ | 48,956 |

| $ | 198,879 |

|

| Earnings for the period attributable to equity holders | $ | 1,738 |

| $ | 33,804 |

| $ | 42,766 |

| $ | 21,777 |

| $ | 100,085 |

|

| Basic earnings per share | $ | 0.01 |

| $ | 0.22 |

| $ | 0.28 |

| $ | 0.14 |

| $ | 0.66 |

|

| Diluted earnings per share | $ | 0.01 |

| $ | 0.22 |

| $ | 0.28 |

| $ | 0.14 |

| $ | 0.66 |

|

| Cash flow from operating activities | $ | 771 |

| $ | 66,019 |

| $ | 102,346 |

| $ | 45,668 |

| $ | 214,804 |

|

| Cash dividends paid per share | $ | 0.0125 |

| $ | 0.0125 |

| $ | 0.0125 |

| $ | 0.0125 |

| $ | 0.0500 |

|

| Other financial information | |

| |

| | | |

| Total assets | | | | | $ | 1,898,141 |

|

Total long-term financial liabilities(1) | | | | | $ | 118,594 |

|

| Total attributable shareholders’ equity | | | | | $ | 1,396,298 |

|

| |

| (1) | Total long-term financial liabilities are comprised of non-current liabilities excluding deferred tax liabilities, deferred revenue, and share purchase warrant liabilities. |

|

| | |

| | PAN AMERICAN SILVER CORP. | 25 |

Income Statement: Q3 2018 vs. Q3 2017

A net loss of $9.2 million was recorded in Q3 2018 compared to net earnings of $17.8 million in Q3 2017, which corresponds to a basic loss per share of $0.06 and basic earnings per share of $0.11, respectively.

The following table highlights the key items driving the difference between net loss in Q3 2018 compared with net earnings in Q3 2017:

|

| | | | | | | | | |

Net earnings, three months ended September 30, 2017 (in thousands of USD) | | |

| | $ | 17,826 |

| Note |

| Revenue: | | |

| | |

| |

| Decreased realized metal prices | | $ | (23,836 | ) | | | |

| Higher quantities of metal sold | | 31,241 |

| | | |

| Decreased direct selling costs | | 5,301 |

| | | |

| Increased negative settlement adjustments | | (15,780 | ) | | | |

| Total decrease in revenue | | | | (3,074 | ) | (1) |

| Cost of sales: | | | | | |

| Increased production costs and decreased royalty charges | | $ | (39,870 | ) | | | (2) |

| Increased depreciation and amortization | | (9,286 | ) | | | (3) |

| Total increase in cost of sales | | | | (49,156 | ) | |

| Total decrease in mine operating earnings | | | | (52,230 | ) | |

| Decreased income tax expense | | | | 18,409 |

| (4) |

| Decreased exploration and project development expense | | | | 4,520 |

| (5) |

| Increased investment income and other expense | | | | 2,762 |

| (6) |

| Increased net gain on asset sales, commodity contracts and derivatives | | | | 1,410 |

| (7) |

| Increased foreign exchange loss | | | | (1,288 | ) | (8) |

| Decreased dilution gain, net of share of income from associate | | | | (784 | ) | |

| Decreased interest and finance expense | | | | 203 |

| |

| Increased general and administrative expense | | | | (62 | ) | |

| Net loss, three months ended September 30, 2018 | | |

| | $ | (9,234 | ) | |

| |

| 1. | Revenue for Q3 2018 was $3.1 million lower than in Q3 2017. The major drivers for the decrease were a $23.8 million negative variance from lower metal prices, attributable to decreased precious and base metal prices, and a $15.8 million negative variance from provisional and final settlement adjustments for open concentrate shipments. These decreases were largely offset by increased quantities of metal sold for all metals except copper. The following table reflects the metal prices realized by the Company and the quantities of metal sold during each quarter: |

|

| | | | | | | | | | | |

| | | Realized Metal Prices | Quantities of Metal Sold |

| | | Three months ended

September 30, | Three months ended

September 30, |

| | | 2018 | 2017 | 2018 | 2017 |

Silver(1) | | $ | 14.88 |

| $ | 16.68 |

| 6,366 |

| 5,255 |

|

Gold(1) | | $ | 1,212 |

| $ | 1,277 |

| 44.6 |

| 35.2 |

|

Zinc(1) | | $ | 2,472 |

| $ | 2,974 |

| 13.6 |

| 11.6 |

|

Lead(1) | | $ | 2,072 |

| $ | 2,421 |

| 5.8 |

| 4.9 |

|

Copper(1) | | $ | 6,105 |

| $ | 6,351 |

| 2.5 |

| 3.6 |

|

(1) Metal price stated as dollars per ounce for silver and gold, and dollars per tonne for zinc, lead and copper, inclusive of final settlement adjustments on concentrate sales. Metal quantities stated as koz for silver and gold and kt for zinc, lead and copper.

| |

| 2. | Production costs in Q3 2018 were $40.8 million higher than in Q3 2017. The increase was mainly the result of negative NRV adjustments and higher costs due to the expanded operations at both Mexican mines. The NRV inventory adjustments increased Q3 2018 production costs by $23.4 million compared to a $1.3 million increase in Q3 2017. Royalty expense decreased by $0.9 million over Q3 2017, mainly attributable to the timing of royalty payments at San Vicente. |

|

| | |

| | PAN AMERICAN SILVER CORP. | 26 |

| |

| 3. | Depreciation and amortization ("D&A") expense was $9.3 million higher than in Q3 2017, largely because of increased D&A at Dolores and La Colorada from increased metal production and sales volumes, and a higher capital base attributable to the expansions at both operations. |

| |

| 4. | Income tax recovery of $7.9 million in Q3 2018 was $18.4 million lower than the $10.5 million income tax expense in Q3 2017. The lower taxes were largely attributable to the decrease in net earnings before tax, as well as the appreciation of the MXN during the quarter, which increased the MXN denominated tax assets. |

| |

| 5. | Exploration and project development expenses were $3.0 million in Q3 2018 compared to $7.5 million in Q3 2017. The decrease was primarily related to the capitalization of expenditures for the COSE and Joaquin projects in Q3 2018, which were expensed in the comparable period, and a non-recurring $1.9 million non-cash write-down of certain project development costs, which was recognized in Q3 2017. The remaining expenses recorded in each quarter primarily related to exploration and project development activities near the Company’s existing mines and at select greenfield projects, and the holding and maintenance costs associated with the Navidad project. Approximately $1.0 million was spent on the Navidad project in Q3 2018 compared to approximately $0.5 million in Q3 2017 due to increased permitting and community relations activities. |

| |

| 6. | Other expense for Q3 2018 was $0.3 million compared to $3.3 million in Q3 2017. The expenses recorded in each quarter were primarily related to adjustments in the closure and decommissioning liability for the Alamo Dorado property. |

| |

| 7. | Gain on commodity and foreign currency contracts for Q3 2018 was $1.8 million compared to a $0.3 million loss in Q3 2017. The gain in Q3 2018 reflects the impact of lower base metal prices on commodity contracts. |

| |

| 8. | Foreign exchange (“FX”) losses in Q3 2018 were $3.1 million compared to $1.9 million in Q3 2017. Losses in Q3 2018 resulted primarily from the effect of the approximately 43% depreciation of the Argentine peso ("ARS") on the Company's ARS denominated monetary assets. FX losses in Q3 2017 resulted primarily from the effect of the approximately 4% depreciation of the ARS on ARS denominated monetary assets. |

Statement of Cash Flows: Q3 2018 vs. Q3 2017

Cash flow from operations in Q3 2018 totaled $41.7 million, $22.1 million less than the $63.8 million generated in Q3 2017. The reduction was largely from an approximately $20.8 million decrease in cash flows from lower mine operating earnings and a $7.1 million increase in income tax payments, partially offset by decreased exploration and project development costs.

Working capital changes in Q3 2018 resulted in a $4.2 million source of cash compared with a $6.9 million source of cash in Q3 2017. The Q3 2018 changes were comprised mainly of a reduction in accounts receivables, partially offset by inventory build-ups.

Investing activities utilized $35.3 million in Q3 2018, inclusive of $3.5 million for the net purchase of short-term investments. The balance related primarily to $33.6 million on mineral properties, plant and equipment at the Company’s mines and projects, as previously described in the “Operating Performance” section of this MD&A. Investing cash flows in Q3 2018 included $1.5 million in proceeds from commodity derivative contracts. In Q3 2017, investing activities utilized $44.9 million inclusive of $12.5 million used for the net purchase of short-term investments, with $32.0 million spent on mineral properties, plant and equipment at the Company’s mines and projects.

Financing activities in Q3 2018 used $7.4 million compared to $43.7 million in Q3 2017. Cash used in Q3 2018 mainly consisted of $5.4 million paid as dividends to shareholders and $2.2 million of lease repayments. In Q3 2017, cash used in financing activities consisted primarily of $38.7 million in repayments of short-term debt and $3.8 million in dividends to shareholders.

|

| | |

| | PAN AMERICAN SILVER CORP. | 27 |

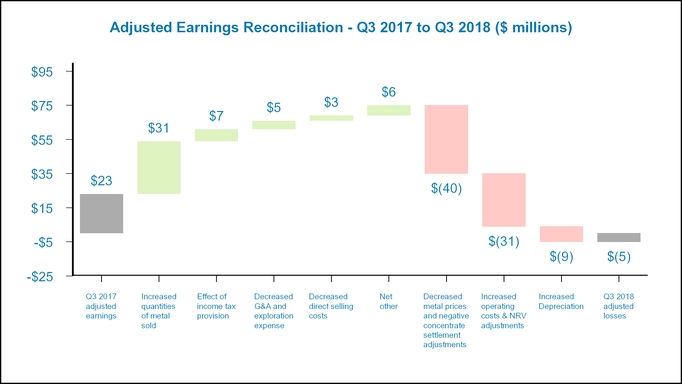

Adjusted Earnings (Loss): Q3 2018 vs Q3 2017

Adjusted earnings (loss) is a non-GAAP measure. Please refer to the section of this MD&A entitled “Alternative Performance (Non-GAAP) Measures” for a detailed description of “adjusted earnings”, and a reconciliation of these measures to the Q3 2018 Financial Statements.

Adjusted Loss in Q3 2018 was $4.7 million, representing basic adjusted loss per share of $0.03, which was $28.0 million, or $0.18 per share, lower than Q3 2017 adjusted earnings of $23.3 million, and basic adjusted earnings per share of $0.15, respectively.

The following chart illustrates the key factors leading to the change in adjusted earnings from Q3 2017 to Q3 2018:

|

| | |

| | PAN AMERICAN SILVER CORP. | 28 |

Income Statement: YTD 2018 vs. YTD 2017

Net earnings of $75.6 million were recorded in YTD 2018 compared to $73.8 million in YTD 2017, which corresponds to basic earnings per share of $0.48 and $0.47, respectively.

The following table highlights the key items driving the difference between net earnings in YTD 2018 compared with YTD 2017:

|

| | | | | | | | | |

Net earnings, nine months ended September 30, 2017 (in thousands of USD) | | |

| | $ | 73,787 |

| Note |

| Revenue: | | |

| | |

| |

| Decreased realized metal prices | | $ | (4,681 | ) | | | |

| Higher quantities of metal sold | | 33,146 |

| | | |

| Decreased direct selling costs | | 11,431 |

| | | |

| Increased negative settlement adjustments | | (19,555 | ) | | | |

| Total increase in revenue | | | | 20,341 |

| (1) |

| Cost of sales: | | | | | |

| Increased production costs and increased royalty charges | | $ | (18,857 | ) | | | (2) |

| Increased depreciation and amortization | | (21,396 | ) | | | (3) |

| Total increase in cost of sales | | | | (40,253 | ) | |

| Total decrease in mine operating earnings | | | | (19,912 | ) | |

| Increased foreign exchange loss | | | | (10,503 | ) | (4) |

| Increased dilution gain, net of share of loss from associate | | | | 12,068 |

| (5) |

| Increased net gain on asset sales, commodity contracts and derivatives | | | | 7,985 |

| (6) |

| Decreased exploration and project development expense | | | | 7,857 |

| (7) |

| Decreased income tax expense | | | | 4,717 |

| (8) |

| Increased investment income and other expense | | | | 1,155 |

| |

| Increased interest and finance expense | | | | (1,002 | ) | |

| Increased general and administrative expense | | | | (534 | ) | |

| Net earnings, nine months ended September 30, 2018 | | |

| | $ | 75,618 |

| |

| |

| 1. | Revenue for YTD 2018 was $20.3 million higher than in YTD 2017. The major factor for the increase was a $33.1 million quantity variance, which was attributable to increased gold, zinc, and silver sales volumes, partially offset by lower copper sales. Decreased direct selling costs of $11.4 million, primarily from favorable changes in contract terms relating to concentrate treatment and refining charges, also contributed to the increase in revenues. Partially offsetting these factors were a $19.6 million increase in negative provisional and final settlement adjustments on concentrate shipments, and a $4.7 million decrease to revenue from lower metal prices. The following table reflects the metal prices realized by the Company and the quantities of metal sold during each period: |

|

| | | | | | | | | | | |

| | | Realized Metal Prices | Quantities of Metal Sold |

| | | Nine months ended

September 30, | Nine months ended

September 30, |

| | | 2018 | 2017 | 2018 | 2017 |

Silver(1) | | $ | 15.98 |

| $ | 17.12 |

| 17,860 |

| 17,552 |

|

Gold(1) | | $ | 1,283 |

| $ | 1,250 |

| 137.3 |

| 111.9 |

|

Zinc(1) | | $ | 2,981 |

| $ | 2,801 |

| 39.1 |

| 34.8 |

|

Lead(1) | | $ | 2,286 |

| $ | 2,309 |

| 15.2 |

| 15.5 |

|

Copper(1) | | $ | 6,641 |

| $ | 5,992 |

| 7.1 |

| 9.7 |

|

(1) Metal price stated as dollars per ounce for silver and gold, and dollars per tonne for zinc, lead and copper, inclusive of final settlement adjustments on concentrate sales. Metal quantities stated as koz for silver and gold and kt for zinc, lead and copper.

| |

| 2. | Production and royalty costs in YTD 2018 were $18.5 million and $0.4 million higher, respectively, than in YTD 2017. The higher production costs were mainly the result of: (i) a $14.2 million increase in direct operating costs from higher sales volumes and the addition of the pulp agglomeration plant at Dolores, partially offset |

|

| | |

| | PAN AMERICAN SILVER CORP. | 29 |

by a decrease in production costs from the cessation of Alamo Dorado production, and lower costs at Manantial Espejo driven by the devaluation of the Argentine peso; and (ii) a $4.3 million increase in negative NRV inventory adjustments at Manantial Espejo and Dolores. The NRV inventory adjustments increased production costs in YTD 2018 by $11.1 million compared with a $6.8 million increase in YTD 2017.

| |

| 3. | D&A expense was $21.4 million higher than in YTD 2017, largely the result of increased D&A at Dolores and La Colorada, due to increased metal production and sales volumes, and at Morococha on account of the impairment reversal in the fourth quarter of 2017, which increased the mine's depreciable assets. |

| |

| 4. | FX losses in YTD 2018 were $9.7 million compared to FX gains of $0.8 million in YTD 2017. Losses in YTD 2018 resulted primarily from the effect of the devaluation of the ARS on the Company's ARS denominated monetary assets. The YTD 2017 gains were driven largely by the appreciation of the MXN on the Company's MXN denominated cash and tax receivables. |

| |

| 5. | Share of income from associate and dilution gain for YTD 2018 was $12.1 million higher than in YTD 2017. The increase was driven primarily by a $13.4 million dilution gain recognized in relation to Maverix Metals Inc. issuing common shares to acquire certain royalty assets in Q2 2018. |

| |

| 6. | Gain on sale of mineral properties, plant and equipment was $7.0 million higher in YTD 2018 than in YTD 2017. The YTD 2018 gain was attributable to the Q1 2018 sale of 100% of the Company's shares in Minera Aquiline Argentina SA, which owned the Calcatreu project in Argentina. |

| |

| 7. | Exploration and project development expenses for YTD 2018 were $7.6 million compared to $15.5 million in YTD 2017. The reduction was primarily the result of the following: (i) reduced greenfield exploration in response to decreased metal prices; (ii) expenditures at the COSE and Joaquin projects, which were expensed in the comparable period and are now being capitalized; and (ii) a non-recurring $1.9 million non-cash write-down of certain project development costs, which impacted the prior period. |

| |

| 8. | Income tax expense in YTD 2018 was $4.7 million lower than in YTD 2017. The decrease was largely attributable to deferred tax assets of approximately $11.7 million recorded in Q2 2018 as a result of the restructuring of certain inter-company debts. This decrease was partially offset by fluctuations in the MXN, which appreciated significantly more in the first nine months of 2017 than during the same period in 2018, thus the corresponding future income tax expense resulting from the increased MXN denominated tax asset base in 2018 was significantly less than in 2017. |

Statement of Cash Flows: YTD 2018 vs. YTD 2017

Cash flow from operations in YTD 2018 totaled $143.0 million, $2.2 million less than the $145.3 million generated in YTD 2017. The decrease was mainly due to a $22.4 million increase in income tax payments, largely offset by a $4.1 million increase in cash flows from working capital changes, a $7.9 million reduction in exploration and project development expenditures, and an approximately $5.7 million increase in cash mine operating earnings from higher revenues net of increased operating costs.

Working capital changes in YTD 2018 resulted in a $0.6 million source of cash, comprised mainly of a reduction in accounts receivable balances, largely offset by accounts payable and accrued liability pay-downs, reclamation expenditures at Alamo Dorado, and a build-up in inventories. Comparatively, working capital changes reduced operating cash flows by $3.5 million in YTD 2017, comprised mainly of inventory build-ups and reclamation expenditures being partially offset by a build-up in accounts payable and accrued liabilities.

Investing activities utilized $108.1 million in YTD 2018, inclusive of $15.5 million for the net purchase of short-term investments. The balance related primarily to $102.0 million on mineral properties, plant and equipment additions at the Company’s mines and projects, $7.5 million disbursed for the final payment for the acquisition of the COSE project, partially offset by $15.8 million in proceeds received from asset sales (the majority from the sale of the Company's shares in Minera Aquiline SA, which owned the Calcatreu project). In YTD 2017, investing activities utilized $141.0 million inclusive of $13.6 million for the net purchase of short-term investments, $105.8 million spent on mineral properties, plant and equipment at the Company’s mines and projects, and $20.2 million for the acquisition of the COSE and Joaquin projects.

|

| | |

| | PAN AMERICAN SILVER CORP. | 30 |

Financing activities in YTD 2018 used $24.4 million compared to $49.0 million in YTD 2017. Cash used in YTD 2018 consisted of $15.9 million paid as dividends to shareholders, $5.7 million of lease repayments and $3.0 million used to repay short-term loans, partially offset by $1.1 million generated on the issuance of shares related to the exercise of stock options. In YTD 2017, cash used in financing activities consisted of a $36.2 million repayment of the revolving credit facility, $11.5 million in dividends to shareholders and $3.2 million of lease repayments, partially offset by $2.6 million generated on the issuance of shares related to the exercise of stock options.

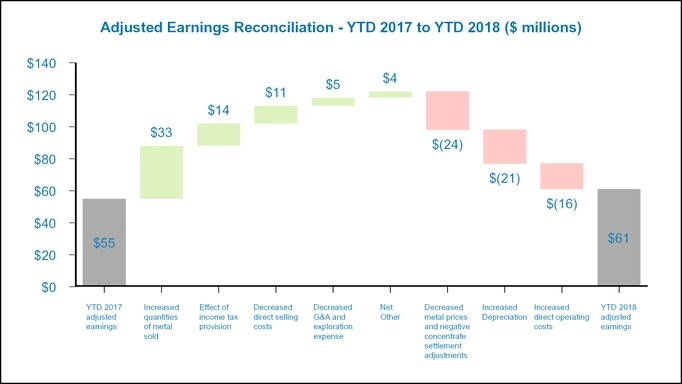

Adjusted Earnings: YTD 2018 vs YTD 2017

Adjusted earnings is a non-GAAP measure. Please refer to the section of this MD&A entitled “Alternative Performance (Non-GAAP) Measures” for a detailed description of “adjusted earnings”, and a reconciliation of these measures to the Q3 2018 Financial Statements.

Adjusted Earnings in YTD 2018 were $61.5 million, representing basic adjusted earnings per share of $0.40, which was $6.8 million, or $0.04 per share, higher than YTD 2017 adjusted earnings of $54.6 million, and basic adjusted earnings per share of $0.36.

The following chart illustrates the key factors leading to the change in adjusted earnings from YTD 2017 to YTD 2018:

|

| | |

| | PAN AMERICAN SILVER CORP. | 31 |

|

| | |

| LIQUIDITY AND CAPITAL POSITION | | |

|

| | | | | | | | | | |

| Liquidity and Capital Measures (in $000s) | September 30, 2018 | June 30, 2018 | Dec 31, 2017 | Q3 2018

Change | YTD 2018 Change |

| Cash and cash equivalents ("Cash") | 186,424 |

| 187,403 |

| 175,953 |

| (979 | ) | 10,471 |

|

| Short-term Investments ("STI") | 66,233 |

| 62,845 |

| 51,590 |

| 3,388 |

| 14,643 |

|

| Cash and STI | 252,657 |

| 250,248 |

| 227,543 |

| 2,409 |

| 25,114 |

|

| Working Capital | 443,586 |

| 463,096 |

| 410,756 |

| (19,510 | ) | 32,830 |

|

| Revolving Credit Facility ("RCF") | 300,000 |

| 300,000 |

| 300,000 |

| — |

| — |

|

| Amount drawn on RCF | — |

| — |

| — |

| — |

| — |

|

Total debt (1) | 8,439 |

| 9,700 |

| 10,559 |

| (1,261 | ) | (2,120 | ) |

| |

| (1) | Total debt is a Non-GAAP measure calculated as the total of amounts drawn on the RCF, finance lease liabilities and loans payable. |

The Company's net liquidity position increased by $2.4 million during Q3 2018. Operating cash flows of $41.7 million, which included $12.9 million in tax payments and a $4.2 million source of cash from working capital changes, more than funded the Company's investing and financing activities in the quarter.