Exhibit 1.2

Management’s Discussion and Analysis

for the Year Ended December 31, 2012

TABLE OF CONTENTS

| Introduction | 3 |

| Core Business and Strategy | 4 |

| Highlights of 2012 | 5 |

| 2013 Operating Outlook | 7 |

| 2013 Project Development Outlook | 12 |

| 2012 Operating Performance | 12 |

| 2012 Project Development Update | 22 |

| Overview of 2012 Financial Results | 24 |

| Investments and Investment Income | 32 |

| General and Administrative Expense | 32 |

| Related Party Transactions | 32 |

| Exploration and Project Development | 33 |

| Liquidity Position | 34 |

| Capital Resources | 34 |

| Financial Instruments | 36 |

| Closure and Decommissioning Cost Provision | 37 |

| Contractual Commitments and Contingencies | 38 |

| Minefinders Transaction | 39 |

| Purchase Allocation | 40 |

| Risks and Uncertainties | 43 |

| Significant Judgements and Key Sources of Estimation Uncertainty in the Application of Accounting Policies | 51 |

| Changes in Accounting Standards | 56 |

| Governance Corporate Social Responsibility and EnvironmentAL Stewardship | 58 |

| Subsequent Events | 60 |

| Disclosure Controls and Procedures | 61 |

| Mineral Reserves and Resources | 63 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

March 22, 2013

INTRODUCTION

Management’s discussion and analysis (“MD&A”) is intended to help the reader understand the significant factors that have affected Pan American Silver Corp.’s and its subsidiaries’ (“Pan American” or the “Company”) performance and such factors that may affect its future performance. The MD&A should be read in conjunction with the Company’s Audited Consolidated Financial Statements for the year ended December 31, 2012 and the related notes contained therein. All amounts in this MD&A and in the consolidated financial statements are expressed in United States dollars (“USD”), unless identified otherwise. The Company reports its financial position, results of operations and cash flows in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). Pan American’s significant accounting policies are set out in Note 2 of the Audited Consolidated Financial Statements. This MD&A refers to various non-Generally Accepted Accounting Principles (“GAAP”) measures, such as “cash and total cost per ounce of silver”, which are used by the Company to manage and evaluate operating performance at each of the Company’s mines and are widely reported in the silver mining industry as benchmarks for performance, but do not have standardized meaning. To facilitate a better understanding of these measures as calculated by the Company, detailed descriptions and reconciliations have been provided where applicable.

Except for historical information contained in this MD&A, the following disclosures are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and forward-looking information within the meaning of applicable Canadian provincial securities laws or are future oriented financial information and as such are based on an assumed set of economic conditions and courses of action. Please refer to the cautionary note regarding the risks associated with forward looking statements at the back of this MD&A and the “Risks Related to Pan American’s Business” contained in the Company’s most recent Form 40-F and Annual Information Form on file with the U.S. Securities and Exchange Commission and the Canadian provincial securities regulatory authorities. Additional information about Pan American and its business activities, including its Annual Information Form, is available on SEDAR at www.sedar.com

The scientific or technical information in this MD&A, which includes mineral reserve and resource estimates for the Huaron, Morococha, Alamo Dorado, La Colorada, Dolores, Manantial Espejo, San Vicente, Pico Machay, and Calcatreu properties were based upon information prepared by or under the supervision of Michael Steinmann, P.Geo., Executive Vice President Geology & Exploration and Martin G. Wafforn, P.Eng., Vice President Technical Services, who are “Qualified Persons” for purposes of National Instrument 43-101. Navidad resource estimates were prepared by Pamela De Mark, P. Geo., Director, Resources who is also a Qualified Person for purposes of National Instrument 43-101. Mineral resource estimates for Hog Heaven and Waterloo are based on historical third party estimates.

This MD&A includes estimates of future silver and other metal sale prices as well as production rates for silver and other metals, future cash and total costs of production at each of the Company’s properties, and capital expenditure forecast at each of the Company’s properties which are all forward-looking estimates. No assurance can be given that the forecasted sale prices of silver and other metals, quantities of silver and other metals will be produced, or that projected cash costs or forecast capital costs will be achieved. Expected future metal prices, production, cash costs and capital costs are inherently uncertain and could materially change over time. The Company’s mineral production, cash costs, and capital expenditures may differ materially from the forecasts in this MD&A. Readers should review those matters discussed herein under the heading “Risks and Uncertainties” and are advised to read the “Cautionary Note Regarding Forward Looking statements” contained herein.

CORE BUSINESS AND STRATEGY

Pan American engages in silver mining and related activities, including exploration, mine development, extraction, processing, refining and reclamation. The Company owns and operates silver mines located in Peru, Mexico, Argentina, and Bolivia. In addition, the Company is exploring for new silver deposits and opportunities throughout North and South America. The Company is listed on the Toronto Stock Exchange (Symbol: PAA) and on the NASDAQ Exchange in New York (Symbol: PAAS).

Pan American’s vision is to be the world’s pre-eminent silver producer, with a reputation for excellence in discovery, engineering, innovation and sustainable development. To achieve this vision, we base our business on the following strategy:

•Generate sustainable profits and superior returns on investments through the safe, efficient and environmentally sound development and operation of silver assets

•Constantly replace and grow our mineable silver reserves and resources through targeted near-mine exploration and global business development

•Foster positive long term relationships with our employees, our shareholders, our communities and our local governments through open and honest communication and ethical and sustainable business practices

•Continually search for opportunities to upgrade and improve the quality of our silver assets both internally and through acquisition

•Encourage our employees to be innovative, responsive and entrepreneurial throughout our entire organization

To execute this strategy, Pan American has assembled a sector leading team of mining professionals with a depth of exploration, construction, operating, and financing knowledge and experience that allows the Company to confidently advance early stage projects through construction and into operation.

Pan American is determined to conduct its business in a responsible and sustainable manner. Caring for the environment in which we operate, contributing to the long-term development of our host communities and ensuring that our employees can work in a safe and secure manner are core values at Pan American. We are committed to

| Pan American Silver Corp. | 4 |

maintaining positive relations with our employees, the local communities and the government agencies, all of whom we view as partners in our enterprise.

Pan American’s priority at every operation is the safety of our employees. We believe that comprehensive and continuous training is fundamental to the safety of our employees. With our safety training and strictly enforced safety procedures, our goal is to continually improve our safety performance and remain industry leaders in the health and safety of our workers.

The Company recognizes that the skills, innovation and dedication of our employees and contractors are important drivers of our success. We also recognize the vital contribution they make to the economic prosperity of the communities in which we operate. As such, we offer leading career development opportunities, competitive remuneration, an engaging working environment and a supportive culture where fairness, respect, safety and diversity are valued and practiced.

The Company is committed to operating our mines and developing new projects in an environmentally responsible manner. We have developed a comprehensive environmental policy, which all operations adhere to and apply to their short and long-term plans. This policy addresses topics that include water use and recycling, waste disposition, the research and use of alternative energies, compliance with required laws, closure requirements and education initiatives. Each operation runs unique environmental programs according to its location, needs, resources and processes. We have a proactive approach to minimizing and mitigating environmental impacts during all phases of the mining cycle from exploration through project development and into full mining operations. This is accomplished by applying prudent design and operating practices, continuous monitoring and by providing training and education for the employees and contractors who work at our facilities.

OPERATIONS & PROJECT DEVELOPMENT

| · | Record Silver and Gold Production |

Silver production was a record 25.1 million ounces in 2012, an increase of 15% over the 21.9 million ounces produced in 2011, while gold production also set a new Company record at 112,300 ounces, 43% higher than 2011 production. While these increases in precious metal production were mainly attributable to additional production from the Dolores mine in Mexico, which was acquired upon the closing of the Minefinders transaction on March 30, 2012, increases in silver production over 2011 were recorded at all of Pan American’s mines, other than Manantial Espejo in Argentina. These increases in silver production more than offset the loss of production resulting from the sale of the Quiruvilca mine in Peru on June 1, 2012.

| · | Minefinders acquisition completed |

On March 30, 2012, the Company completed the previously announced plan of arrangement under the Business Corporations Act (Ontario) whereby Pan American acquired all of the issued and outstanding common shares of Minefinders.

| Pan American Silver Corp. | 5 |

Pan American’s management believes that the strategic benefits to shareholders resulting from the acquisition include: (i) enhanced portfolio diversification of producing assets into a more stable mining jurisdiction, (ii) additional near-term cash flow, (iii) improved organic growth opportunities, (iv) a meaningful reduction of average silver cash costs across the Company’s production portfolio, (v) addition of significant silver and gold mineral reserves and resources with excellent potential to increase even further through exploration; and (vi) increases in the Company’s exposure to the prices of silver and gold.

| · | Exploration Success |

On August 15, 2012, the Company reported excellent drill results from this year's ongoing exploration programs at the La Colorada mine and one of its development projects, the Waterloo silver project in San Bernardino County, California. At La Colorada, the drill program continued to target both oxide and sulphide mineralization with impressive results being returned in both areas of the mine, which have been incorporated into the December 2012 Mineral Reserves and Resources update. At Waterloo, Pan American decided to actively evaluate the potential of the property and started a first phase drilling campaign in 2012. The initial drill program consisted of 11 reverse circulation (“RC”) holes for a total of 974 metres, with all holes returning consistent high grade and wide intersects starting from the surface in most holes. Work to evaluate Waterloo’s development potential is continuing with a second phase of RC and diamond drilling in order to confirm the historic mineral resource, metallurgical testing, geological mapping and topographic surveying.

| · | Navidad Development Pending Provincial Legislation Reform |

In July 2012, Pan American reported that the Governor of the province of Chubut submitted a draft bill to the provincial legislature that would regulate all oil and gas and mining activities in the province. The draft legislation incorporated the long-awaited and expected zoning of the province, which would allow for the development of Navidad as an open pit mine. However, the same draft legislation proposed to introduce a series of new regulations which would significantly increase provincial royalties and impose the province’s direct participation in all mining projects, including Navidad. In view of the uncertainty surrounding the legislation, the Company has been forced to place the Navidad project on care and maintenance in the fourth quarter. As a consequence of these events, as well as rampant inflation in Argentina, Pan American recognized an impairment charge of $100 million against the carrying value of the project in the fourth quarter of 2012.

The Company remains committed to the eventual development of Navidad and to contributing to the positive economic and social development of the province of Chubut should a more favorable legislative framework be adopted.

| · | Robust Proven and Probable Silver Mineral Reserves |

A successful exploration and resource conversion program in 2012 more than replaced mineral reserves that were mined during the year. As at December 31, 2012, Proven and Probable mineral reserves totalled 317 million ounces. For the complete breakdown of mineral reserves and resources by property and category, refer to section “Mineral Reserves and Resources” contained herein.

| Pan American Silver Corp. | 6 |

FINANCIAL

| · | Record Revenue |

Revenue in 2012 was a record $929 million, an increase of 9% over 2011 revenue, driven primarily by increased quantities of silver and gold sold, partially offset by lower realized prices for silver and base metals.

| · | Strong Margins and Adjusted Earnings (1) |

Adjusted earnings in 2012 remained healthy at $178 million or $1.26 per share although representing a decline from 2011 results of $251 million of $2.36 per share primarily due to lower realized prices for all metals sold, other than gold. Pan American was able to achieve a gross margin (mine operating earnings/revenue) of 34% in 2012 despite operating cost pressures and the lower realized metal prices sold, other than gold, as compared to a gross margin of 48% achieved in 2011.

| (1) | Please refer to the section Alternative Performance (Non-GAAP) Measures for a detailed description of Adjusted Earnings. |

| · | Robust Operating Cash Flow and Record Liquidity and Working Capital Position |

Cash flow from operations was $193 million, which was sufficient to fund all of the Company’s capital programs and add to our liquidity. The Company had cash and a short term investment balance of $542 million and a working capital position at a record $779 million at December 31, 2012, an increase of $51 million and $212 million, respectively, from a year ago.

| · | Return of Value to Shareholders |

Strong operating cash flow and net cash acquired from Minefinders facilitated the continued return of value to shareholders in 2012 by way of approximately $25 million in dividend payments and $42 million of common share repurchases under the Company’s normal course issuer bid programs. The Company received approval and commenced a second share repurchase program in 2012 after completing the first program, which started in September, 2011 and finished in July, 2012. The Company also announced in February 2013 an increase to its existing quarterly dividends, bringing the quarterly dividend to an industry leading $0.125 per share or $0.50 on an annual basis.

2013 OPERATING OUTLOOK

These estimates are forward-looking statements and information and; they are subject to the cautionary note regarding the risks associated with forward looking statements and information at the end of this MD&A.

The following tables set out management’s 2013 forecast for each operation’s silver production, cash and total costs per ounce, by-product production, and expected capital investments.

| Pan American Silver Corp. | 7 |

Silver Production, Cash and Total Costs Forecasts

| Silver Production ounces million | Cash Costs per ounce (1) | Total Costs per ounce (1) | |

| La Colorada | 4.60 - 4.70 | $9.00 - $9.75 | $10.33 - $11.08 |

| Alamo Dorado | 4.80 - 5.00 | $8.25 - $8.50 | $11.21 - $11.46 |

| Dolores | 3.25 - 3.45 | $2.25 - $3.50 | $19.02 - $20.27 |

| Huaron | 2.85 - 2.95 | $20.00 - $22.00 | $23.82 - $25.82 |

| Morococha | 2.40 - 2.60 | $20.50 - $22.25 | $26.46 - $28.16 |

| San Vicente | 3.75 - 3.85 | $17.26 - $18.00 | $20.57 - $21.31 |

| Manantial Espejo | 3.35 - 3.45 | $13.00 - $14.25 | $21.06 - $22.31 |

| Consolidated Total | 25.00 - 26.00 | $11.80 - $12.80 | $17.57- $18.57 |

| (1) | Cash costs per ounce and total costs per ounce are non-GAAP measurements. Please refer to section Alternative Performance (Non-GAAP) Measures for a detailed reconciliation of these measures to our cost of sales. The cash cost forecasts assume by-product credit prices of $1,925/tonne ($0.87lb) for zinc, $1,975/tonne ($0.90/lb) for lead, $7,800/tonne ($3.54/lb) for copper, and $1,600/oz for gold. |

By-product Production Forecast

Gold ounces | Zinc tonnes | Lead tonnes | Copper tonnes | |

| La Colorada | 4,300 - 4,500 | 5,000 - 5,800 | 2,800 - 2,900 | - |

| Alamo Dorado | 16,000 -16,500 | - | - | 70 - 80 |

| Dolores | 63,500 - 68,000 | - | - | - |

| Huaron | 500 - 1,000 | 11,000 - 11,700 | 4,200 - 4,500 | 1,750 - 2,100 |

| Morococha | 2,200 - 2,500 | 13,500 - 15,000 | 3,950 - 4,500 | 1,680 - 1,820 |

| San Vicente | - | 6,000 - 6,500 | 550 - 600 | - |

| Manantial Espejo | 53,500 - 57,500 | - | - | - |

| Consolidated Total | 140,000 - 150,000 | 36,000 - 39,000 | 11,500 - 12,500 | 3,500 - 4,000 |

Capital Expenditure Forecasts

| (in millions) | ||

| La Colorada | $ | 15.0 |

| Alamo Dorado | $ | 7.5 |

| Dolores | $ | 37.0 |

| Huaron | $ | 20.0 |

| Morococha | $ | 15.0 |

| San Vicente | $ | 11.5 |

| Manantial Espejo | $ | 20.0 |

| Mine Capital | $ | 126.0 |

| Project Development Capital (Dolores) | $ | 31.0 |

| Total Capital | $ | 157.0 |

| Pan American Silver Corp. | 8 |

2013 Mine Operation Forecasts

| · | La Colorada Mine |

Increased overall throughput rates, combined with stable grades and recovery rates are expected to result in higher silver, gold and base metal production in 2013.

Cash costs per ounce are expected to increase by between 4% and 13% from 2012’s actual costs due to an expected increase to direct operating costs and treatment charges with a higher component of sulfide ore processing leading to an increase in base metal rich flotation concentrate production, partially offset by the benefits of higher silver production and by an increase in by-product credits.

Capital expenditures at La Colorada in 2013 are expected to decline substantially from 2012 levels, down to $15 million. Our capital plans at La Colorada are comprised mostly of expenditures related to mine development and equipment purchases for the Estrella and Candelaria mines, an Estrella mine expansion, a continuation of the near-mine exploration drilling program, and an expansion of the crusher/plant dam.

| · | Alamo Dorado Mine |

The silver grades at Alamo Dorado are expected to decline from the 2012 levels as the reserve depletes, which is expected to result in a modest decline in silver production in 2013 compared with 2012. Similarly, gold grades are also expected to decline, resulting in a decrease in gold production.

Cash costs are expected to increase sharply by 64% to 68% per ounce over 2012 costs, as a result of expected increases in direct operating costs coupled with lower by-product gold production. Cost increases are expected for materials (most notably cyanide and explosives), labour, power, security and community relations.

Capital expenditures are expected to be $7.5 million, predominantly for pre-stripping of the phase II pit expansion, which is expected to cost $5.6 million.

| · | Dolores Mine |

Silver grades at Dolores are expected to remain at 2012 levels in 2013; whereas, the gold grades are expected to increase according to the areas planned to be mined. Based on the expected grades and benefiting from a full year of production, the mine will maintain annual silver production rates steady with 2012 rates, resulting in 23% to 30% increased expected silver production and 46% and 56% increased expected gold production.

Cash costs per ounce are expected to decrease in the range of 14% to 44%, primarily due to the significantly higher gold by-product gold production credits on a per ounce basis. Unit operating costs are expected to remain similar to 2012’s actual costs, with increases expected in materials and labour costs largely being offset by reductions in mine site general and administrative costs.

| Pan American Silver Corp. | 9 |

Capital expenditures, excluding the leach pad expansions projects and mine optimization projects, are expected to be $37 million, predominantly related to mine operations, comprised of pre-stripping of approximately $18 million, truck rehabilitation and other mobile equipment purchases of approximately $8 million, near-mine exploration of approximately $4 million and other sustaining infrastructure of approximately $7 million. In addition to the Dolores “mine capital” budget, capital expenditures relating to the construction and expansion of the mine’s leach pads and mine optimization projects are presented and discussed separately under the next section, 2013 Project Development Outlook.

| · | Huaron Mine |

In 2013, we plan to modestly increase mining and milling rates at Huaron by approximately 6% from the 2012 rates by increasing the amount of efficient long-hole stoping mining methods in well-defined areas of the mine. The increased throughput is expected to be offset by modestly lower silver grades and recoveries, resulting in similar silver production to 2012. Base metal production is also expected to remain similar to 2012 levels.

Cash costs per ounce are expected to increase by 14% to 26% over the 2012 cash costs due to higher expected operating costs combined with a reduction in by-product credits resulting from the assumption of lower by-product metal prices. Operating costs are expected to rise primarily as a result of higher materials costs, wage increases, increased mine development advances and a stronger local currency.

Capital spending plans at Huaron in 2013 are expected to reach $20 million, allowing for the continuation of long term mine developments advances. A large portion of the budget is also allocated to complete the significant tailings dam expansion project initiated in 2012, the purchase and overhaul of mobile mine equipment, as well as near-mine exploration.

| · | Morococha Mine |

Tonnes milled, silver and zinc grades and recoveries at Morococha in 2013 are all expected to improve slightly compared to 2012 actuals, resulting in an expected 15% to 25% increase in produced silver and similar increases in by-product base metal production.

We anticipate that the improved production rates at Morococha will result in cash costs per ounce being 5% to 13% lower than 2012 cash costs. Base metal by-product credits are expected to remain steady as higher levels of base metal production is expected to be offset by lower metal prices, relative to 2012. Operating costs per tonne milled are expected to decline over 2012 actual costs primarily as a result of the benefit of an improvement in throughput rates and implementation of more mechanized mining methods in certain areas, despite increased materials costs and a stronger local currency.

Morococha’s capital budget totals $15 million, and represents a substantial reduction from capital expenditure levels in 2012. The majority of the capital expenditures in 2013 are planned for the mine and include ramp development advances and ventilation

| Pan American Silver Corp. | 10 |

system expansions, overhaul and replacements of certain aged mobile mine equipment and near-mine exploration activities.

| · | San Vicente Mine |

Our plans for San Vicente in 2013 contemplate a rise in throughput rates while being able to hold silver grades and recoveries close to 2012 levels. Based on those operating parameters, San Vicente is expected to contribute around 3.8 million ounces of silver to Pan American in 2013 for our 95% interest. Continued development of the high-grade Litoral vein is expected to deliver ore with higher zinc and lead grades than in 2012, and should result in significant increases in zinc and lead production.

Cash costs per ounce are expected to decline by at least 5% over the 2012 actual cash costs due primarily to an increase in by-product credits from higher zinc and lead production in 2013 partially offset with lower base metal price projections. Royalties payable to Comibol, which are calculated on operating cash flow, are expected to constitute as much as 40% of our cash costs in 2013. Costs per tonne milled are budgeted to increase by 7% as compared to 2012 as a result of a 10% increase in operating costs driven predominantly by an 11% increase in materials and a 6% increase in labour costs, partially offset by the cost benefit of processing higher tonnage.

The capital budget for 2013 at San Vicente totals $11.5 million and includes $5.0 million for mine development and underground mobile equipment maintenance, and $3.6 million for a raise of the tailings dam.

| · | Manantial Espejo Mine |

Our key objectives for 2013 at Manantial Espejo are to increase plant throughput by 7% to 2,150 tonnes per day at a slightly lower silver grade, but a substantially higher gold grade according to the areas of mining scheduled. Achieving the increased throughput rates is dependent on improving mobile equipment and plant availabilities and utilizations from 2012 levels. With steady recovery rates, we expect silver production to decline to around 3.4 million ounces and an increase to gold production to between 53,500 and 57,500 ounces, an increase of at least 23% over 2012 gold production

Cash costs per ounce at Manantial Espejo in 2013 are expected to decline by between 3% and 11%, thanks in large part to higher gold by-product credits and the continued devaluation of the Argentine peso. Operating costs are expected to increase by approximately 9% due to the expectation of continued cost inflation in Argentina, which especially affects costs of labor and consumables, largely offset by the weaker local currency.

Capital investments in 2013 total $20 million and include the open pit pre-strip development and equipment acquisitions, which are expected to require $13.5 million, while another $2.5 million will be incurred in underground mine development. Expanding and improving the camp infrastructure and mill upgrades are both expected to require approximately $1.1 million each.

| Pan American Silver Corp. | 11 |

2013 PROJECT DEVELOPMENT OUTLOOK

The Company’s 2013 Project Development efforts will be primarily dedicated to the Dolores leach pad expansions. We anticipate project capital spending of $31 million at Dolores, $26 million of which is related to expanding the leach pads (pad #2 expansion and pad #3 construction) and $5 million for initiation of an interconnecting grid power line project as well as advancing a study to increase metal recoveries with a grinding circuit.

2012 OPERATING PERFORMANCE

The following table reflects silver production and cash costs at each of Pan American’s operations for 2012, as compared to 2011 and 2010.

Silver Production (ounces ‘000s) | Cash Costs(1) ($ per ounce) | ||||||||||

| 2012 | 2011 | 2010 | 2012 | 2011 | 2010 | ||||||

| La Colorada | 4,431 | 4,296 | 3,702 | $8.64 | $7.74 | $8.59 | |||||

| Alamo Dorado | 5,364 | 5,300 | 6,721 | $5.05 | $4.80 | $3.16 | |||||

| Dolores | 2,652 | - | - | $4.05 | - | - | |||||

| Huaron | 2,909 | 2,769 | 2,987 | $17.51 | $14.03 | $12.35 | |||||

| Quiruvilca | 275 | 881 | 1,245 | $36.33 | $17.47 | $5.87 | |||||

Morococha(2) | 2,083 | 1,712 | 2,633 | $23.48 | $16.11 | $4.43 | |||||

San Vicente(3) | 3,726 | 3,130 | 3,033 | $18.92 | $13.48 | $8.21 | |||||

| Manantial Espejo | 3,632 | 3,767 | 3,965 | $14.65 | $7.36 | $1.61 | |||||

Consolidated Total(4) | 25,075 | 21,855 | 24,286 | $12.03 | $9.44 | $5.69 | |||||

| (1) | Cash costs per ounce is a non-GAAP measurement. Please refer to section Alternative Performance (Non-GAAP) Measures for a detailed reconciliation of this measure to our cost of sales. |

| (2) | Morococha data represents Pan American's 92.2% interest in the mine's production. |

| (3) | San Vicente data represents Pan American's 95.0% interest in the mine's production. |

| (4) | Totals may not foot due to rounding. |

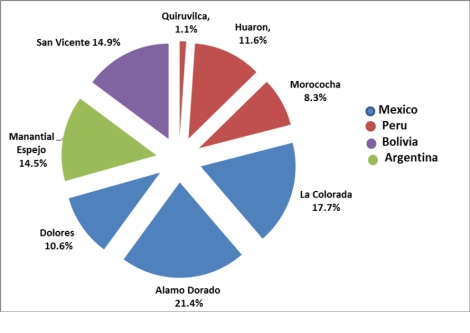

The graph below presents silver production by mine in 2012 and highlights the diverse nature of Pan American’s silver production.

| Pan American Silver Corp. | 12 |

In 2012, Pan American’s silver production increased by 15% from production levels in 2011 of 21.9 million ounces. While this increase was mainly attributable to additional production from the Dolores mine, which was acquired upon the closing of the Minefinders acquisition transaction on March 30, 2012, increases in silver production were recorded at all of Pan American’s mines, other than Manantial Espejo. These increases in silver production more than offset the loss of production resulting from the sale of the Quiruvilca mine on June 1, 2012.

Silver production in 2012 was at the higher end of management’s forecast range of between 24.25 million and 25.5 million ounces as described in the Q1 2012 MD&A, which incorporated production from Dolores into our forecast. Alamo Dorado, La Colorada, Huaron, Morococha, and San Vicente were at or exceeded the high end of our guidance, while only Manantial Espejo and Dolores were below guidance.

Consolidated cash costs per ounce of silver were $12.03 in 2012, a 27% increase from 2011’s cash costs per ounce of $9.44, but in line with forecast for the year. This increase was moderated by the contribution of low-cost ounces from Dolores, where cash costs averaged $4.05 per ounce for the nine months under Pan American ownership. Excluding the positive influence of Dolores, the increase in cash costs were primarily due to an 11% increase in unit operating costs per tonne, which were driven by increases in mining royalties, an increase in underground mine development rates at Huaron and Morococha, and higher labour and consumable costs. The increase in operating costs was exacerbated by a 10% decrease in by-product credits as a result of lower gold (ex-Dolores) and base metal by-product production in 2012, combined with lower base metal prices.

The following tables set out the Company’s by-product production over the past three years and the metal prices realized for each metal produced:

| Pan American Silver Corp. | 13 |

| By-Product Production | |||||||||

| 2012 | 2011 | 2010 | |||||||

| Gold ounces | 112,283 | 78,426 | 89,555 | ||||||

| Zinc tonnes | 36,848 | 37,234 | 43,103 | ||||||

| Lead tonnes | 12,266 | 12,701 | 13,629 | ||||||

| Copper tonnes | 4,162 | 4,544 | 5,221 | ||||||

| Realized Prices | |||||||||

| 2012 | 2011 | 2010 | |||||||

| Silver/ounce | $ | 31.26 | 35.03 | 19.87 | |||||

| Gold/ounce | $ | 1,672 | 1,567 | 1,216 | |||||

| Zinc/tonne | $ | 1,961 | 2,208 | 2,160 | |||||

| Lead/tonne | $ | 2,052 | 2,402 | 2,147 | |||||

| Copper/tonne | $ | 7,879 | 8,625 | 7,457 | |||||

In 2012, production of gold increased by 43% as a result of additional production from Dolores, which more than offset the decline at Manantial Espejo. Base metal production declined slightly due to the loss of production from the Quiruvilca mine, offset by increased production from continuing operations.

As first discussed in our Q3 2012 MD&A, gold production in 2012 was trending below management’s expectations and we revised our forecast to 114,000 ounces, below our original guidance of 124,000 to 133,000 ounces. The primary reasons for the lower than anticipated gold production were (i) at Manantial Espejo, below planned open-pit mining rates were achieved due to low equipment availability, largely as importation restrictions in Argentina persisted and (ii) at Dolores, more dilution than anticipated was incurred in certain narrow structured gold dominant zones, resulting in lower than expected grades being stacked.

Robust base metal production in 2012 at our Peruvian and Bolivian operations, exceeded the high end of management’s forecasted ranges for zinc (33,000 – 34,000 tonnes), lead (11,000 – 11,500 tonnes) and copper (2,500 – 3,000 tonnes).

An analysis of each operation’s 2012 operating performance follows, as compared to 2011 operating performance, and management’s guidance for 2012, as contained in the 2011 year-end MD&A.

| Pan American Silver Corp. | 14 |

| · | La Colorada Mine |

| Twelve months ended | |||||||

| December 31, | |||||||

| 2012 | 2011 | ||||||

| Tonnes milled | 419,591 | 404,533 | |||||

| Average silver grade – grams per tonne | 374 | 369 | |||||

| Average silver recovery – % | 89.6 | % | 89.5 | % | |||

Silver(1) – ounces | 4,431,111 | 4,295,783 | |||||

| Gold – ounces | 3,578 | 4,104 | |||||

| Zinc – tonnes | 5,599 | 4,466 | |||||

| Lead – tonnes | 2,766 | 2,388 | |||||

Cash costs per ounce (2) | $ | 8.64 | $ | 7.74 | |||

Total costs per ounce (2) | $ | 9.96 | $ | 8.99 | |||

| Payable ounces of silver | 4,215,075 | 4,093,851 | |||||

| Capital Expenditures - thousands | $ | 21,700 | $ | 13,301 | |||

| (1) | Reported metal figures in the tables in this section are volume of metal produced. |

| (2) | Cash costs per ounce and total costs per ounce are non-GAAP measurements. Please refer to section Alternative Performance (Non-GAAP) Measures for a detailed reconciliation of these measures to our cost of sales. |

2012 versus 2011

Silver production at the La Colorada mine in 2012 was 4.4 million ounces, a 3% increase compared to the previous year. This increase was due to higher throughput rates and slightly improved silver grades. Production of lead and zinc benefited from higher throughput, while anticipated lower gold grades led to a modest decrease in gold production.

Cash costs increased by 12% in 2012 compared to 2011 to $8.64 per ounce as a result of higher operating costs while by-product credits remained similar to the prior year as increased base metal production was offset by lower realized prices and gold production.

2012 versus 2012 Guidance

Silver production at La Colorada in 2012 exceeded the top of management’s forecast range of 4.1 million to 4.26 million ounces, as higher than expected throughput rates and grades were achieved. By-product production also benefited from better than expected throughput rates and recoveries, resulting in gold, zinc and lead production which exceeded our guidance.

Actual cash costs of $8.64 were 9% lower than the bottom of management’s forecast range of between $9.50 and $9.90 per ounce. This positive variance at La Colorada was driven by stronger than expected by-product credits, thanks to higher production and prices, while operating costs were largely as expected.

Capital expenditures at La Colorada during 2012 totalled $21.7 million, which exceeded our forecast of $16.1 million. The capital was spent mainly on advancing both oxide and sulfide tailings dam expansions; mine equipment, infrastructure and development; site

| Pan American Silver Corp. | 15 |

infrastructure upgrades and increased exploration drilling particularly given the successes in the Amolillo vein extensions.

| · | Alamo Dorado Mine |

| Twelve months ended | |||||||

| December 31, | |||||||

| 2012 | 2011 | ||||||

| Tonnes milled | 1,697,941 | 1,848,230 | |||||

| Average silver grade – grams per tonne | 116 | 105 | |||||

| Average gold grade – grams per tonne | 0.38 | 0.33 | |||||

| Average silver recovery – % | 85.6 | % | 83.6 | % | |||

| Silver – ounces | 5,364,011 | 5,299,841 | |||||

| Gold – ounces | 17,966 | 16,607 | |||||

| Copper – tonnes | 117 | 66 | |||||

Cash costs per ounce (1) | $ | 5.05 | 4.80 | ||||

Total costs per ounce (1) | $ | 7.95 | 8.29 | ||||

| Payable ounces of silver | 5,345,677 | 5,278,892 | |||||

| Capital Expenditures - thousands | $ | 10,936 | 8,287 | ||||

| (1) | Cash costs per ounce and total costs per ounce are non-GAAP measurements. Please refer to section Alternative Performance (Non-GAAP) Measures for a detailed reconciliation of these measures to our cost of sales. |

2012 versus 2011

Alamo Dorado remained the Company’s largest silver producer in 2012, with silver production of 5.4 million ounces, which was a slight increase from the silver production achieved in 2011. Silver production saw significantly better silver grades and recoveries, partially offset by lower throughput rates, caused by harder ore being processed. Gold production of approximately 18,000 ounces in 2012 represented an 8% increase over production levels in 2011 as better gold grades and recoveries also overcame the effects of lower throughput rates.

Alamo Dorado’s cash costs per ounce were $5.05 in 2012, a 5% increase from the 2011 cash costs of $4.80 due to higher operating costs, partially offset by higher gold by-product credits due to increased production and stronger realized gold prices in 2012.

2012 versus 2012 Guidance

Alamo Dorado’s silver production in 2012 was right at the top of management’s forecast range of 5.07 million to 5.37 million ounces, the result of silver grades that were well above our expectations, however throughput rates lagged. Gold production was 17% above the top of our guidance range of 15,300 ounces as actual gold grades significantly exceeded expectations.

Cash costs were 21% lower than the low end of our forecast range of $6.40 to $6.80 per ounce as a result the strong silver production and higher realized gold by-product credits resulting from stronger than expected gold production and gold metal prices.

Capital expenditures at Alamo Dorado during 2012 totalled $10.9 million, compared to management’s guidance of $10.3 million primarily for waste pre-stripping, mine equipment, leach tank expansions and site infrastructure upgrades.

| Pan American Silver Corp. | 16 |

| · | Dolores Mine* |

| Nine months ended | |||

| December 31, | |||

| 2012 | |||

| Tonnes milled | 4,346,595 | ||

| Average silver grade – grams per tonne | 42 | ||

| Average gold grade – grams per tonne | 0.40 | ||

| Average silver recovery – % | 45.7 | % | |

| Average gold recovery – % | 78.0 | % | |

| Silver – ounces | 2,652,851 | ||

| Gold – ounces | 43,476 | ||

Cash costs per ounce (1) | $ | 4.05 | |

Total costs per ounce (1) | $ | 16.88 | |

| Payable ounces of silver | 2,646,219 | ||

Capital Expenditures - thousands (2) | $ | 59,038 | |

* | Results for the nine months of 2012 that the Company operated the Dolores mine. |

| (1) | Cash costs per ounce and total costs per ounce are non-GAAP measurements. Please refer to section Alternative Performance (Non-GAAP) Measures for a detailed reconciliation of these measures to our cost of sales. |

| (2) | Sustaining capital expenditures including capital incurred on the leach pad projects as disclosed in the section Project Development Update. |

2012 versus 2012 Guidance

In the first nine months under Pan American stewardship, the Dolores Mine produced 2.7 million ounces of silver and approximately 43,500 ounces of gold. Silver production was 5% below management’s expectations of between 2.8 million and 3 million ounces, a result of mine sequencing and unscheduled crusher repairs that resulted in less ore tonnes stacked than anticipated. Gold production was affected by more dilution than anticipated in some more structurally controlled gold zones being mined during the year, resulting in lower than expected grades being stacked and lagged management’s guidance of between 49,000 and 53,000 ounces in by 11%.

Cash costs for 2012 were $4.05 per ounce of silver, 19% below the $5.00 to $6.00 per ounce forecast provided by management. Operating costs were significantly lower than anticipated, partially offset by lower silver production and lower gold credits than forecasted.

Capital expenditures at Dolores during the last nine months of 2012 totalled $59.0 million, primarily for ongoing leach pad construction, capitalized stripping to develop access to ore that is to be mined in future periods, near-mine exploration drilling, mine equipment refurbishments, and camp expansions. Management continues to focus on stabilizing the heap leach pad operation and advance a thorough analysis of additional optimization opportunities.

| Pan American Silver Corp. | 17 |

| · | Huaron Mine |

| Twelve months ended | |||||||

| December 31, | |||||||

| 2012 | 2011 | ||||||

| Tonnes milled | 683,483 | 614,437 | |||||

| Average silver grade – grams per tonne | 162 | 177 | |||||

| Average zinc grade – % | 2.54 | % | 2.46 | % | |||

| Average silver recovery –% | 81.7 | % | 79.1 | % | |||

| Silver – ounces | 2,909,890 | 2,768,768 | |||||

| Gold – ounces | 655 | 1,339 | |||||

| Zinc – tonnes | 11,824 | 9,555 | |||||

| Lead – tonnes | 4,727 | 4,865 | |||||

| Copper – tonnes | 2,257 | 1,278 | |||||

Cash costs per ounce (1) | $ | 17.51 | $ | 14.03 | |||

Total costs per ounce (1) | $ | 21.02 | $ | 16.89 | |||

| Payable ounces of silver | 2,506,481 | 2,491,190 | |||||

| Capital Expenditures - thousands | $ | 22,936 | $ | 13,021 | |||

| (1) | Cash costs per ounce and total costs per ounce are non-GAAP measurements. Please refer to section Alternative Performance (Non-GAAP) Measures for a detailed reconciliation of these measures to our cost of sales. |

2012 versus 2011

In 2012, mill throughput at Huaron ramped up by 11% relative to 2011 and recoveries improved by 3%, however, these increases were partially offset by an 8% drop in silver grades, resulting in silver production that rose by 5% year-on-year. Zinc and copper production also rose on higher throughput rates and recoveries, by 24% and 77%, respectively. Lead and gold production slipped on account of a drop in grades and recoveries.

Cash costs at Huaron increased by 25% in 2012 to $17.51 per ounce mainly due to a 37% increase in underground mine development advances in actively producing zones, general operating cost escalations and the strengthening local currency. Cash costs benefited from a rise in by-product credits at Huaron as higher production of zinc and copper were only partially offset by lower lead and gold production and by lower base metal prices in 2012.

2012 versus 2012 Guidance

Silver production in 2012 was 3% ahead of management’s forecast of between 2.73 million and 2.82 million ounces. Throughput rates and recoveries positively outperformed management’s expectations, which were the same reasons that all base metal production was above management’s guidance.

The actual cash costs in 2012 were 16% better than the bottom of our forecast range of $20.90 to $22.70 per ounce. This positive performance was attributable to higher by-product credits and better than expected silver production.

Capital expenditures at Huaron during 2012 totalled $22.9 million, compared to our forecast of $19.2 million, primarily for mine development, equipment, a tailings dam expansion, site infrastructure upgrades and exploration.

| Pan American Silver Corp. | 18 |

Morococha Mine*

| Twelve months ended | |||||||

| December 31, | |||||||

| 2012 | 2011 | ||||||

| Tonnes milled | 535,086 | 483,104 | |||||

| Average silver grade – grams per tonne | 143 | 128 | |||||

| Average zinc grade – % | 2.83 | % | 2.74 | % | |||

| Average silver recovery – % | 84.9 | % | 86.1 | % | |||

| Silver – ounces | 2,083,726 | 1,711,668 | |||||

| Gold – ounces | 2,840 | 1,691 | |||||

| Zinc – tonnes | 11,925 | 10,676 | |||||

| Lead – tonnes | 3,601 | 3,050 | |||||

| Copper – tonnes | 1,502 | 1,522 | |||||

Cash costs per ounce (1) | $ | 23.48 | $ | 16.11 | |||

Total costs per ounce (1) | $ | 29.75 | $ | 22.19 | |||

| Payable ounces of silver | 1,776,333 | 1,520,702 | |||||

Capital Expenditures - thousands (2) | $ | 27,194 | $ | 17,289 | |||

| * | Production and cost figures are for Pan American’s 92.2% share only. |

| (1) | Cash costs per ounce and total costs per ounce are non-GAAP measurements. Please refer to section Alternative Performance (Non-GAAP) Measures for a detailed reconciliation of these measures to our cost of sales. |

| (2) | Sustaining capital expenditures including capital incurred at the Morococha project as disclosed in the section Project Development Update. |

2012 versus 2011

Morococha’s 2012 silver production increased by 22% as compared to 2011 mainly due to an 11% increase in throughput rates combined with 12% better silver grades. Zinc, lead and gold production also benefited from higher throughput rates, while lower copper grades and recoveries resulted in similar production of copper to 2011.

Cash costs at Morococha increased by 46% in 2012 to $23.48 per ounce due to the substantially higher operating costs for 2012 compared to 2011. The increase in operating costs was primarily a result of a 17% increase in underground mine development in actively producing zones, general operating cost escalations and the strengthening local currency. By-product credits remained similar to the prior year as higher by-product production was offset by lower realized prices.

2012 versus 2012 Guidance

Silver production performance at Morococha in 2012 was 14% above the top end of management’s guidance range of 1.74 million to 1.82 million ounces. Similarly, actual gold, lead and copper production all exceeded our guidance ranges, while zinc production was within guidance. Mine sequencing as well as better than expected throughput rates and grades were the main reasons for the positive by-product production variances.

| Pan American Silver Corp. | 19 |

The actual cash costs in 2012 were 5% lower than the bottom end of our forecast of $24.60 to $26.50 per ounce due primarily to actual silver production and by-product credits being higher than expected.

Sustaining capital expenditures at Morococha during 2012 totalled $20.8 million, compared to management’s guidance of $19.3 million. The capital spending was primarily on increased long term mine development infrastructure upgrades, exploration drilling, as well as mine and plant equipment replacements. In addition, the Company invested $6.4 million in capital for the Morococha project as described in the “2012 Project Development Update” which follows.

| · | San Vicente Mine* |

| Twelve months ended | |||||||

| December 31, | |||||||

| 2012 | 2012 | ||||||

| Tonnes milled | 306,063 | 282,960 | |||||

| Average silver grade – grams per tonne | 419 | 382 | |||||

| Average zinc grade – % | 2.15 | % | 2.26 | % | |||

| Average silver recovery - % | 90.71 | % | 90.1 | % | |||

| Silver – ounces | 3,726,024 | 3,130,145 | |||||

| Zinc – tonnes | 4,918 | 4,792 | |||||

| Copper – tonnes | - | 649 | |||||

| Lead - tonnes | 432 | - | |||||

Cash costs per ounce (1) | $ | 18.92 | $ | 13.48 | |||

Total costs per ounce (1) | $ | 22.05 | $ | 17.14 | |||

| Payable ounces of silver | 3,390,683 | 2,849,243 | |||||

| Capital Expenditures - thousands | $ | 3,053 | $ | 4,975 | |||

| * | Production and interest figures are for Pan American’s 95.0% share only. |

(1) | Cash costs per ounce and total costs per ounce are non-GAAP measurements. Please refer to section Alternative Performance (Non-GAAP) Measures for a detailed reconciliation of these measures to our cost of sales. |

2012 versus 2011

In 2012, San Vicente’s silver production increased by 19% compared to 2011, mainly due to 10% better grades and 8% higher throughput. Zinc production improved by 3% while a change in the commercial strategy at San Vicente resulted in our silver concentrates being marketed to lead smelters instead of copper smelters, which means that we are now paid for the lead content of the concentrates, but not for the contained copper. As a consequence, for 2012 we report lead production instead of copper production.

Cash costs at San Vicente increased by 40% to $18.92 in 2012 as compared to the previous year. The higher cash costs in 2012 resulted from the combined effect of (i) a 113% increase in royalties as a result of increasing the COMIBOL royalty at San Vicente following the recovery of our investment as defined in the joint venture contract, (ii) a 44% increase in smelting costs, primarily due to the deterioration in terms for high silver grade concentrates, (iii) a 13% increase in operating costs, primarily driven by increases in labour costs, and (iv) lower by-product credits due to lower base metal prices and the switch from a copper payment to a lead payment for our concentrates.

| Pan American Silver Corp. | 20 |

2012 versus 2012 Guidance

Silver production attributable to Pan American in 2012 of 3.7 million ounces was 6% over management’s forecast range of 3.4 million to 3.52 million ounces, as silver grades surprised on the upside. Higher than expected lead grades resulted in an 11% positive variance above management’s guidance range while lower than expected zinc grades and recoveries resulted in zinc production that fell 7% short of guidance.

Actual cash costs of $18.92 were 1% above management’s forecast range due to marginally lower than expected by-product credits on lower than expected zinc production.

Capital expenditures at San Vicente during 2012 totalled $2.9 million, which was below management’s forecast of $5.4 million. Capital spending in 2012 was for mine infrastructure upgrades, additional underground mine equipment and exploration drilling.

| · | Manantial Espejo Mine |

| Twelve months ended | |||||||

| December 31, | |||||||

| 2012 | 2011 | ||||||

| Tonnes milled | 734,335 | 697,205 | |||||

| Average silver grade – grams per tonne | 170 | 185 | |||||

| Average gold grade – grams per tonne | 1.94 | 2.48 | |||||

| Average silver recovery - % | 89.8 | % | 90.2 | % | |||

| Average gold recovery - % | 94.2 | % | 95.1 | % | |||

| Silver – ounces | 3,632,550 | 3,766,504 | |||||

| Gold – ounces | 43,339 | 52,998 | |||||

Cash costs per ounce (1) | $ | 14.65 | $ | 7.36 | |||

Total costs per ounce (1) | $ | 22.73 | $ | 15.89 | |||

| Payable ounces of silver | 3,625,285 | 3,758,971 | |||||

| Capital Expenditures - thousands | $ | 15,858 | $ | 16,916 | |||

| (1) | Cash costs per ounce and total costs per ounce are non-GAAP measurements. Please refer to section Alternative Performance (Non-GAAP) Measures for a detailed reconciliation of these measures to our cost of sales. |

2012 versus 2011

Silver production at the Manantial Espejo mine in 2012 was 3.6 million ounces, a 4% decrease from the production level in 2011. This decrease was a result of an 8% decline in grades combined with a slight dip in recoveries, which outweighed the 5% lift in throughput rates from the previous year. Gold production dropped by 18% in 2012 due similarly to lower gold grades and recoveries according to the mine sequencing, which was expected to be approximately 2.05 grams per tonne. Lower gold grades were also partially offset by higher throughput rates.

In 2012, cash costs at Manantial Espejo increased to $14.65, almost double 2011’s cash costs of $7.36 per ounce. The main drivers of the increase in cash costs were a 13% increase in operating costs together with a 13% decline in by-product gold credits. The higher operating costs were mainly due to an increase in labour costs and the effects from the high sustained inflation rates in Argentina.

| Pan American Silver Corp. | 21 |

2012 versus 2012 Guidance

In 2012, Manantial Espejo’s actual throughput rates and silver grades were below management’s forecast, resulting in 15% lower silver production than our forecast range of 4.25 million to 4.5 million ounces. Throughput rates were significantly challenged by mobile equipment availability issues largely as a consequence of importation restrictions that severely limited the flow of spare parts and materials necessary to sustain operations. Gold production suffered for the same reasons, resulting in a 20% negative variance compared to the lower limit of our range forecast of 54,200 to 58,400 ounces.

The actual cash costs in 2012 of $14.65 per ounce were 41% above the forecast range of $8.60 to $10.40 per ounce. The main drivers for the higher than expected cash costs were lower than expected silver production, compounded by lower by-product gold credits.

Capital expenditures at Manantial Espejo during 2012 totalled $15.2 million, compared to management’s forecast capital expenditures of $17.2 million. The capital expenditures consisted mainly of camp upgrades, mine development including capitalized stripping, mine and plant equipment upgrades, and infrastructure improvements.

2012 PROJECT DEVELOPMENT UPDATE

The following table reflects the amounts spent at each of Pan American’s significant projects in 2012, as compared to 2011 and 2010. Our accounting policies determine what portion of the amounts spent at our projects is capitalized and what portion is expensed during the period.

| Total Project Spending | ||||||

| 2012 | 2011 | 2010 | ||||

| Navidad | $ | 20,044 | $ | 33,200 | $ | 37,177 |

| Dolores leach pads | $ | 21,291 | $ | - | $ | - |

| Morococha Project | $ | 6,389 | $ | 26,218 | $ | 10,259 |

| Calcatreu | $ | 2.407 | $ | 1,656 | $ | 323 |

| Waterloo | $ | 848 | $ | - | $ | - |

| La Preciosa | $ | 989 | $ | 2,400 | $ | 9,989 |

| · | Navidad |

At the Navidad project, the Company spent a total of $20.0 million in 2012, of which $11.3 million was capitalized.

Work during the first half of 2012 focused on the advancement of the project’s Environmental Impact Assessment (“EIA”) and progressing an updated feasibility study. Progress included updated economics based on current capital and operating costs estimates, and the inclusion of additional mineral resources defined by our exploration drilling program. Work on the updated feasibility study and EIA was suspended in July 2012 pending clarity and final definition of the draft mining legislation in the province of Chubut, Argentina where Navidad is located. Pan American has curtailed activities related to project engineering, procurement and development until the new the law is

| Pan American Silver Corp. | 22 |

passed and the final tax and royalties implications can be assessed. Local community support activities in Chubut continued in order to sustain the social acceptance of the project which the Company has worked hard to obtain. The EIA is well advanced, with finalization pending on the passing of a law that permits open pit mining in Chubut. With the project placed on care and maintenance in the fourth quarter, as part of the fourth quarter testing for the recoverability of asset carrying values (impairment testing), the Company recorded a partial write-down against the carrying value of the Navidad project. Please see the Income Statement section of this MD&A for discussion of this non-cash charge.

| · | Dolores |

At the Dolores leach pad projects, the Company spent a total of $21.3 million in the nine months of 2012 that the mine operated under the Company’s stewardship. Management continued to focus on achieving increased reliability of heap leach pad #2 and advancing the construction of pad #3 in order to stabilize the current operation and allow thorough analysis of potential optimization opportunities.

| · | Morococha |

At the Morococha plant relocation project, the Company invested $6.4 million in 2012, largely completing this project. The main focus of the work in 2012 included:

| · | Completed construction of all new surface buildings, which include an administration building, maintenance shop, warehouse, change house, kitchen, 300 person camp, laboratory, and compressor building. Connecting these new facilities to a power supply is scheduled to be completed in early 2013. |

| · | Completed new main water supply lines and new compressed air line for the mine operations. |

| · | Waterloo |

At the Waterloo project, the Company decided to actively evaluate the potential of the property and started a drilling campaign in 2012 concluding the year with approximately 2,700 meters of RC and diamond drilling. Further efforts were focused on metallurgical test work, geological mapping and geophysical surveys, the initial results of which were encouraging of the project’s potential.

| · | La Preciosa |

In early April 2012, the Company provided notice to Orko Silver Corp. (“Orko”) that it had decided not to deliver a feasibility study for the La Preciosa project, as required under the terms of the joint venture agreement between Orko and Pan American. As a result, Pan American relinquished its right to earn a 55% interest in the La Preciosa project. After completing almost three years of exploration, engineering and project development work, the Company came to the conclusion that any continued participation in the La Preciosa project is unlikely to generate a rate of return that meets Pan American's internal economic hurdle rate. Because the Company had no carrying value in this project, there was no loss on relinquishment of the project.

| Pan American Silver Corp. | 23 |

| · | Calcatreu |

At the Calcatreu project, the Company spent $2.4 million in 2012, all of which was expensed. Work during the year included:

| · | Completion of nearly 3,000 meters of diamond drilling, mostly as confirmation holes and the collection of fresh metallurgical samples. Results of testing performed on these samples are still pending and the Company has not yet had an opportunity to confirm and update the resource estimate, which was prepared in April 2008 by Micon for Aquiline Resources Inc., the previous owners of the project. |

OVERVIEW OF 2012 FINANCIAL RESULTS

For the year ended December 31, 2012, the Company’s net income and cash flow from operations decreased from the comparable period in 2011. The results were primarily due to lower realized metal prices, partially offset by higher quantities of all metals sold. A partial write-down of the Navidad project book value was recorded in the fourth quarter of 2012 due to economic conditions having deteriorated in Argentina and the lack of clarity with regards to progress towards a change in the law in Chubut that would allow for the construction of the mine as an open pit operation.

The following table sets out selected quarterly results for the past twelve quarters, which are stated in thousands of USD, except for the per share amounts. The dominant factor affecting results in the quarters presented below is volatility of metal prices realized, near continuous industry wide cost pressures, and the timing of the sales of production which varies. Results starting with the second quarter of 2012 include those of the Dolores mine acquired with the completion of the Minefinders acquisition on March 30, 2012.

| Quarters Ended | Year Ended | |||||||||||||||||||

| 2012 | March 31 | June 30 | Sept 30 | Dec 31 | Dec 31 | |||||||||||||||

| Revenue | $ | 228,819 | $ | 200,597 | $ | 251,843 | $ | 247,335 | $ | 928,594 | ||||||||||

| Mine operating earnings | $ | 101,896 | $ | 56,296 | $ | 68,160 | $ | 85,011 | $ | 311,363 | ||||||||||

| Attributable earnings (loss) for the period | $ | 49,883 | $ | 43,924 | $ | 22,612 | $ | (29,411 | ) | $ | 87,513 | |||||||||

Adjusted attributable earnings for the period(1) | $ | 69,231 | $ | 15,229 | $ | 37,604 | $ | 55,777 | $ | 177,859 | ||||||||||

| Basic earnings (loss) per share | $ | 0.47 | $ | 0.29 | $ | 0.15 | $ | (0.19 | ) | $ | 0.62 | |||||||||

| Diluted earnings (loss) per share | $ | 0.47 | $ | 0.23 | $ | 0.15 | $ | (0.24 | ) | $ | 0.55 | |||||||||

| Cash flow from (used in) operating activities | $ | 37,395 | $ | (5,200 | ) | $ | 79,507 | $ | 81,603 | $ | 193,305 | |||||||||

| Cash dividends paid per share | $ | 0.0375 | $ | 0.0375 | $ | 0.05 | $ | 0.05 | $ | 0.175 | ||||||||||

| Other financial information | ||||||||||||||||||||

| Total assets | $ | 3,387,979 | ||||||||||||||||||

| Total long term financial liabilities | $ | 143,022 | ||||||||||||||||||

| Total attributable shareholders’ equity | $ | 2,719,401 | ||||||||||||||||||

| Pan American Silver Corp. | 24 |

| Quarters Ended | Year Ended | |||||||||||||||||||

| 2011 | March 31 | June 30 | Sept. 30 | Dec 31 | Dec 31 | |||||||||||||||

| Revenue | $ | 190,481 | $ | 231,866 | $ | 220,567 | $ | 212,361 | $ | 885,275 | ||||||||||

| Mine operating earnings | $ | 96,018 | $ | 118,629 | $ | 106,208 | $ | 88,270 | $ | 409,125 | ||||||||||

| Attributable earnings for the period | $ | 92,161 | $ | 112,623 | $ | 52,354 | $ | 95,356 | $ | 352,494 | ||||||||||

Adjusted attributable earnings for the period(1) | $ | 64,638 | $ | 76,093 | $ | 45,573 | $ | 64,362 | $ | 250,666 | ||||||||||

| Basic earnings per share | $ | 0.86 | $ | 1.04 | $ | 0.49 | $ | 0.89 | $ | 3.31 | ||||||||||

Diluted earnings per share(2) | $ | 0.60 | $ | 1.04 | $ | 0.48 | $ | 0.89 | $ | 3.31 | ||||||||||

| Cash flow from operating activities | $ | 59,465 | $ | 104,127 | $ | 90,896 | $ | 104,967 | $ | 359,455 | ||||||||||

| Cash dividends paid | $ | 0.025 | $ | 0.025 | $ | 0.025 | $ | 0.025 | $ | 0.10 | ||||||||||

| Other financial information | ||||||||||||||||||||

| Total assets | $ | 1,951,796 | ||||||||||||||||||

| Total long term financial liabilities | $ | 118,984 | ||||||||||||||||||

| Total shareholders’ equity | $ | 1,593,839 | ||||||||||||||||||

| Quarters Ended | Year Ended | |||||||||||||||||||

| 2010 | March 31 | June 30 | Sept 30 | Dec 31 | Dec 31 | |||||||||||||||

| Revenue | $ | 135,819 | $ | 150,558 | $ | 164,530 | $ | 195,646 | $ | 646,553 | ||||||||||

| Mine operating earnings | $ | 37,776 | $ | 52,269 | $ | 61,293 | $ | 89,777 | $ | 241,115 | ||||||||||

| Attributable earnings (loss) for the period | $ | 26,276 | $ | (6,262 | ) | $ | 21 | $ | (6,324 | ) | $ | 13,711 | ||||||||

Adjusted attributable earnings for the period(1) | $ | 17,128 | $ | 4,504 | $ | 27,372 | $ | 55,368 | $ | 104,372 | ||||||||||

| Basic earnings (loss) per share | $ | 0.25 | $ | (0.06 | ) | $ | 0.00 | $ | (0.06 | ) | $ | 0.13 | ||||||||

| Diluted earnings (loss) per share | $ | 0.24 | $ | (0.04 | ) | $ | 0.00 | $ | (0.07 | ) | $ | 0.13 | ||||||||

| Cash flow from (used in) operating activities | $ | 48,646 | $ | 45,338 | $ | 65,066 | $ | 83,206 | $ | 242,256 | ||||||||||

| Cash dividends paid | $ | 0.025 | $ | - | $ | 0.025 | $ | 0.025 | $ | 0.075 | ||||||||||

| Other financial information | ||||||||||||||||||||

| Total assets | $ | 1,738,796 | ||||||||||||||||||

| Total long term financial liabilities | $ | 228,054 | ||||||||||||||||||

| Total shareholders’ equity | $ | 1,341,358 | ||||||||||||||||||

| (1) | Adjusted attributable earnings for the period is an alternative performance measure. Please refer to the section, Alternative Performance (Non-GAAP) Measures, of this MD&A for a calculation of adjusted earnings for the period. |

| (2) | The diluted earnings per share for the three months ended March 31, 2011 has been revised to $0.60 per share from the amount previously presented of $0.86 per share, to properly reflect the effect under IFRS of the dilutive share purchase warrants which are classified as a liability. |

The following graph illustrates the key factors leading to the change in adjusted net earnings between 2011 and the year ended December 31, 2012. Analysis of the key factors and the changes is discussed in the section that follows.

| Pan American Silver Corp. | 25 |

The following table reflects the metal prices that the Company realized and the quantities of metal sold during each respective period. As seen below, there was an decline in realized metal prices for silver, zinc, lead and copper, however a sharp jump in the quantities of precious metals sold in 2012 compared to 2011.

| Realized Metal Prices | Quantities of Metal Sold | |||||||||||||||

| Year ended December 31, | Year ended December 31, | |||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| Silver – in ounces | $ | 31.26 | (1) | $ | 35.03 | 23,037,493 | 19,516,483 | |||||||||

| Gold – in ounces | $ | 1,6721 | (1) | $ | 1,568 | 108,075 | 75,904 | |||||||||

| Zinc – in tonnes | $ | 1,961 | (2) | $ | 2,208 | 31,443 | 30,157 | |||||||||

| Lead – in tonnes | $ | 2,052 | (2) | $ | 2,402 | 11,396 | 11,885 | |||||||||

| Copper – in tonnes | $ | 7,879 | (2) | $ | 8,625 | 3,412 | 3,991 | |||||||||

| (1) | Metal price per ounce. |

| (2) | Metal price stated as cash settlement per tonne. |

| · | Income Statement |

Earnings for 2012 were $87.5 million, compared to earnings of $354.1 million in 2011. Basic earnings per share for 2012 were $0.62 compared to $3.31 in 2011. A key reason behind the decrease in earnings was that the Company recorded a non-cash write-down of the carrying value of $100.0 million on the Navidad project as discussed below. Adjusted earnings were $177.9 million for 2012 compared to $251.2 million in 2011 (please refer to the section, “Alternative Performance (Non-GAAP) Measures”, of this MD&A for description of adjusted earnings). Adjusted basic earnings per share for 2012 were $1.26 compared to $2.36 for 2011 which was significantly impacted by the Minefinders transaction for which 49.4 million shares were issued. Adjusted earnings benefited from increases in overall quantities of most metals sold, as reflected in the tables above, but offset by decreases in the realized metal prices received. Higher cost

| Pan American Silver Corp. | 26 |

of sales in 2012, which includes production costs, depreciation and amortization, and royalty expense, reflected an increase in the quantities sold, operating costs escalation discussed in the section “Operating Performance”, as well as higher amortization and depreciation charges resulting from the Dolores acquisition.

Revenue for 2012 was $928.6 million, a 9% increase from revenue for 2011 of $855.3 million. This increase was driven by a $187.4 million positive volume variance from higher quantities of most metals sold, partially offset by a $95.8 million price variance from lower metal prices realized, with the exception of realized gold prices, which rose by 7% year over year.

Mine operating earnings were $311.4 million in 2012, a decrease of 24% from the $409.1 million generated in 2011. This decrease resulted from higher cost of sales by $171.1 million outweighing an increase in revenue as noted above. Mine operating earnings are equal to revenue less cost of sales, which is considered to be substantially the same as gross margin. In addition to higher operating costs in the current year, depreciation and amortization increased as a result of newly constructed assets put into use and the amortization of the Dolores mine costs.

A write-down of mineral property of $100.0 million was recorded as a non-cash charge on the Navidad project. The impairment charge was a result of deteriorated economic conditions in Argentina including rampant inflation increasing capital and operating costs, government imposed capital restrictions, and the nationalization of certain petroleum assets in 2012, which resulted in higher discount rates used in the company’s impairment testing for this project. Furthermore, the lack of progress by the province of Chubut with regards to legislation that would allow open pit mining at Navidad and define a tax regime that allows for reasonable sharing of the benefits amongst stakeholders, resulted in the incorporation of delays to the start of construction in the Company’s economic value models for the project. In addition, the valuation models also incorporated uncertainty in the potential tax regime outcomes, which negatively impacted the recoverable value of the project. These factors contributed to the Company’s decision to place the project on care and maintenance in December 2012, and resulted in the write-down occurring as of the year-end. The impairment charge was excluded from adjusted earnings due to its non-recurring nature (please refer to the section, “Alternative Performance (Non-GAAP) Measures”, of this MD&A for a description of adjusted earnings).

The Company was required to record an impairment charge when it determined that the accounting carrying value of approximately $568 million related to the Navidad project was greater than the higher of i) the value estimated to be obtained from development and operation of Navidad or ii) the proceeds realizable from the sale of the project. At December 31, 2012, the Company tested the recoverability of its investment in the Navidad project as required under IFRS based on the factors described above and concluded that the recoverable amount was $468 million. The Company used the most up to date internally developed technical information available, a long term silver price of $25 per ounce along with long term lead prices of $1,850 per tonne, a probability weighted range of possible outcomes related to taxation scenarios, regulatory and economic risks including a range of possible future exchange rates between the USD and the Argentine peso (“ARG”) ranging from 4.5 to 10.5 ARG/USD, and a risk adjusted

| Pan American Silver Corp. | 27 |

project specific discount rate of 12.5%. In addition, value was assigned to un-modeled but in-situ resources representative of potential geologic value that such a deposit holds. It was determined that the estimated realizable value of the Navidad project fell short of its carrying value and thus an impairment loss was warranted at December 31, 2012.

The Company evaluated the sensitivity of the recoverable amount of the project to a range of taxation and regulatory outcomes together with a range of discount rates from 10.5% to 13.5%. These scenarios produced recoverable amounts ranging from $732 million to $353 million. Due to the sensitivity of the recoverable amount to the various factors mentioned as well as yet unforeseen factors, any significant change in the key assumptions and inputs could result in additional impairment charges in future periods.

Income taxes for 2012 were $93.8 million, a $23.3 million decrease from the $117.1 million income tax provision recorded in 2011 and are comprised of current and deferred income taxes as follows:

| 2012 | 2011 | |||

| Current taxes | ||||

| Current tax expense in respect of the current year | $ | 93,857 | $ | 110,620 |

| Adjustments recognized in the current year with respect to prior years | 7,193 | (1,273) | ||

| 101,050 | 109,347 | |||

| Deferred taxes | ||||

| Deferred tax expense recognized in the current year | (2,705) | 4,133 | ||

| Adjustments recognized in the current year with respect to prior years | (4,523) | 3,638 | ||

| (7,228) | 7,771 | |||

| Provision for income taxes | $ | 93,822 | $ | 117,118 |

The decrease in the provision for income taxes was primarily a consequence of decreased taxable earnings generated at our operations as well as the effects of various temporary and permanent differences as shown in the table below, which result in effective tax rates that vary considerably from the comparable period and from the amount that would result from applying the Canadian statutory income tax rates to earnings before income taxes. The main factors which have affected the effective tax rates for the year ended December 31, 2012 and the comparable period of 2011 were the unrealized gains and losses on the Company’s warrants position, foreign income tax rate differentials, additional mining taxes paid and withholding taxes paid on income and payments from subsidiaries to parent companies, exploration expenses on properties for which the deductibility of the expenses is not assured, and foreign exchange gains and losses. In addition, the 2012 effective tax rate was affected by the non-deductible write-down of the Navidad mineral property which was not tax affected. The Company expects that these and other factors will continue to cause volatility in effective tax rates in the future.

| Pan American Silver Corp. | 28 |

| Year ended December 31, | ||||

| 2012 | 2011 | |||

| Income before taxes | $ | 181,335 | $ | 471,264 |

| Statutory tax rate | 25% | 26.5% | ||

| Income tax expense based on above rates | $ | 45,334 | $ | 124,885 |

| Increase (decrease) due to: | ||||

| Non-deductible expenses | 5,196 | 2,028 | ||

| Increase to estimated deductible expenses not recorded in earnings | (3,009) | (12,986) | ||

| Change in net deferred assets not recognized | 5,145 | 286 | ||

| Non-taxable unrealized (gain) on derivatives financial instruments warrants | (6,040) | (26,984) | ||

Foreign tax rate differences (1) | (1,141) | 14,642 | ||

| Effect of other taxes paid (mining and withholding) | 9,418 | 9,914 | ||

| Change in net deferred tax assets not recognized for exploration expenses | 2,111 | 6,207 | ||

| Foreign exchange (gain) loss | (2,716) | 2,277 | ||

| Impairment of Navidad | 35,003 | - | ||

| Other | 4,521 | (3,151) | ||

| $ | 93,822 | $ | 117,118 | |

| Effective tax rate | 51.7% | 24.9% | ||

| (1) | The 2012 statutory income tax rates in the countries that the Company has operations in are as follows: Argentina – 35%, Bolivia – 25%, Mexico –29%, Peru – 30%. |

| · | Statement of Cash Flows |

Cash flow from operations, generated $193.3 million in 2012, a 46% decrease from the $359.5 million generated a year ago. A large part of the decrease in cash flow from operations resulted from the timing of the payment of income taxes as well as the decrease in mine operating earnings, as discussed previously. In 2012, $152.3 million was paid in cash income taxes largely as a result of higher taxable income generated in 2011, whereas cash taxes paid in 2011 was $58.7 million and related to the lower operating earnings of 2010. Changes in non-cash working capital used $22.2 million compared with $39.4 million in 2011. The net non-cash working capital used in 2012 consisted primarily of a $30.8 million increase in inventories which was primarily attributable to the timing of doré and concentrate shipments as well as the buildup of ore on the heap leach pads at Dolores, an increase of $19.1 million in accounts receivable and prepaid expenses, which was partially offset by a $27.7 million increase in current liabilities. In 2011, non-cash working capital was primarily increased by a $28.4 million rise in doré and concentrate inventory, and $8.6 million added in accounts receivable.

Investing activities used $39.3 million in 2012, inclusive of $30.4 million generated from net short-term investment liquidations and $86.5 million net cash acquired with Minefinders. As part of the consideration paid for Minefinders, the Company paid $165.4 million in cash but acquired $251.9 million of cash for a net cash acquisition of $86.5 million. The balance of investing activities consisted primarily of spending $159.9 million on capital including $11.3 million at the Navidad project and $21.3 million related to Dolores leach pads and sustaining investments in property, plant and equipment at Dolores, Manantial Espejo, Morococha, La Colorada, Huaron, Alamo Dorado and San Vicente of $37.7 million, $15.2 million, $20.8 million, $21.7 million, $22.9 million, $10.9

| Pan American Silver Corp. | 29 |

million and $2.9 million, respectively. Finally, $2.0 million of refundable VAT tax was paid in Argentina and Bolivia net of collections in addition to other asset expenditures.

Investing activities used $172.6 million in 2011, inclusive of $51.1 million invested in short- term investments. The balance of investing activities consisted primarily of spending $39.1 million on the Navidad project including certain capital equipment and sustaining investments in property, plant and equipment primarily at Manantial Espejo, Morococha, La Colorada, Huaron, Alamo Dorado and San Vicente of $16.9 million, $17.3 million, $13.3 million, $13.0 million, $8.3 million and $5.0 million, respectively. In addition, $26.2 million was spent on the Morococha relocation project and $3.9 million was paid as refundable VAT tax in Argentina and Bolivia.