UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the Year Ended December 31, 2006

Commission File No. 1-8968

ANADARKO PETROLEUM CORPORATION

1201 Lake Robbins Drive, The Woodlands, Texas 77380-1046

(832) 636-1000

| | |

| Incorporated in the State of Delaware | | Employer Identification No. 76-0146568 |

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, par value $0.10 per share

Preferred Stock Purchase Rights

The above Securities are listed on the New York Stock Exchange.

Securities registered pursuant to Section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yesx No¨.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes¨ Nox.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yesx No¨.

Indicate by check mark if the disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.¨.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. Large accelerated filer x Accelerated filer¨ Non-accelerated filer¨.

Indicate by check mark whether the registrant is a shell company. Yes¨ Nox.

The aggregate market value of the Company’s common stock held by non-affiliates of the registrant on June 30, 2006 was $21.8 billion based on the closing price as reported on the New York Stock Exchange.

The number of shares outstanding of the Company’s common stock as of January 31, 2007 is shown below:

| | |

| Title of Class | | Number of Shares Outstanding |

| Common Stock, par value $0.10 per share | | 463,098,338 |

| | |

Part of Form 10-K | | Documents Incorporated By Reference |

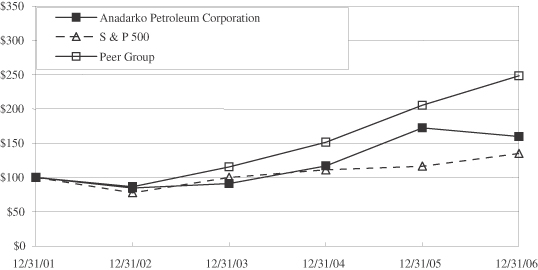

Part II | | Portions of the Anadarko Petroleum Corporation 2006 Annual Report to Stockholders. |

| |

Part III | | Portions of the Proxy Statement for the Annual Meeting of Stockholders of Anadarko Petroleum Corporation to be held May 16, 2007 (to be filed with the Securities and Exchange Commission prior to April 30, 2007). |

TABLE OF CONTENTS

1

PART I

Item 1. Business

General

Anadarko Petroleum Corporation is among the largest independent oil and gas exploration and production companies in the world, with 3.01 billion barrels of oil equivalent (BOE) of proved reserves as of December 31, 2006. The Company’s major areas of operation are located onshore in the United States, the deepwater of the Gulf of Mexico and Algeria. Anadarko also has production in China, Venezuela and Qatar, a development project in Brazil and is executing strategic exploration programs in several other countries. The Company actively markets natural gas, oil and natural gas liquids (NGLs) and owns and operates gas gathering and processing systems. In addition, the Company engages in the hard minerals business through non-operated joint ventures and royalty arrangements in several coal, trona (natural soda ash) and industrial mineral mines located on lands within and adjacent to its Land Grant holdings. The Land Grant is an 8 million acre strip running through portions of Colorado, Wyoming and Utah where the Company owns most of its fee mineral rights. Anadarko is committed to minimizing the environmental impact of exploration and production activities in its worldwide operations through programs such as carbon dioxide (CO2) sequestration and the reduction of surface area used for production facilities.

On August 10, 2006, Anadarko completed the acquisition of Kerr-McGee Corporation (Kerr-McGee) in an all-cash transaction totaling $16.5 billion plus the assumption of approximately $2.6 billion in debt. On August 23, 2006, Anadarko completed the acquisition of Western Gas Resources, Inc. (Western) in an all-cash transaction totaling $4.8 billion plus the assumption of $625 million in debt. Anadarko financed $22.5 billion for the acquisitions under a 364-day committed acquisition facility. As part of an asset realignment associated with the acquisitions, the Company sold its wholly-owned Canadian oil and gas subsidiary, Anadarko Canada Corporation, in November 2006 for approximately $4.3 billion. Net proceeds from this sale were used to reduce debt under the acquisition facility. At December 31, 2006, the Company had $11 billion remaining outstanding under the acquisition facility.

Anadarko has signed several additional separate and unrelated agreements with various companies for the divestiture of certain non-core properties in the Gulf of Mexico and onshore in the United States for a combined total of approximately $6.5 billion before income taxes. Certain of these agreements have closed and the remaining are expected to close in the first half of 2007.

The Company expects total after-tax proceeds from the Canadian sale and the other transactions mentioned above to be about $9 billion. The Company expects to divest certain other assets by the end of 2007, with expected incremental after-tax proceeds totaling between $2 billion and $6 billion. The proceeds from all of these transactions are being used to reduce indebtedness.

In late 2004, Anadarko completed over $3 billion in pretax asset sales of certain non-core properties through a series of unrelated transactions. Combined, the divested properties represented about 20% of 2004 total oil and gas production and about 11% of Anadarko’s total year-end 2003 proved reserves. The Company used proceeds from these asset sales to reduce debt, repurchase Anadarko common stock and otherwise to have funds available for reinvestment in other strategic options.

Unless noted otherwise, the following information relates to Anadarko’s continuing operations and excludes the discontinued Canadian operations. For additional information, seeAcquisitions and Divestitures andOutlook under Item 7 of this Form 10-K.

Unless the context otherwise requires, the terms“Anadarko”or“Company”refer to Anadarko Petroleum Corporation and its subsidiaries. The Company’s corporate headquarters are located at 1201 Lake Robbins Drive, The Woodlands, Texas 77380, where the telephone number is (832) 636-1000.

Available Information The Company files Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, registration statements and other items with the Securities and Exchange Commission (SEC). Anadarko provides access free of charge to all of these SEC filings, as soon as reasonably practicable after filing or furnishing, on its internet site located at www.anadarko.com. The Company will also make available to any stockholder, without charge, copies of its Annual Report on Form 10-K as filed with the

2

SEC. For copies of this, or any other filing, please contact: Anadarko Petroleum Corporation, Investor Relations Department, P.O. Box 1330, Houston, Texas 77251-1330 or call (832) 636-1216.

In addition, the public may read and copy any materials Anadarko files with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Room 1580, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet site (www.sec.gov) that contains reports, proxy and information statements and other information regarding issuers, like Anadarko, that file electronically with the SEC.

Oil and Gas Properties and Activities

Proved Reserves

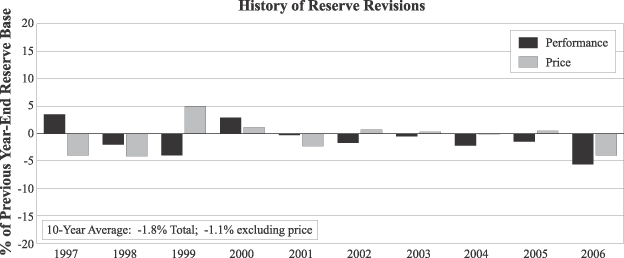

As of December 31, 2006, Anadarko had proved reserves of 10.5 trillion cubic feet (Tcf) of natural gas and 1.3 billion barrels of crude oil, condensate and NGLs. Combined, these proved reserves are equivalent to 3.01 billion barrels of oil or 18.1 Tcf of gas. During 2006, the Company’s reserves increased 23% due to the acquisitions of Kerr-McGee and Western and successful exploration and development drilling onshore in the United States, partially offset by the disposition of Canadian properties, downward revisions primarily related to the K2 complex in the Gulf of Mexico and adjustments in Algeria, and a decrease in natural gas prices. The Company’s reserves have grown 20% over the past three years primarily due to acquisitions and successful exploration and development drilling in the United States, partially offset by the effect of the disposition of the Canadian and other non-core producing properties. As of December 31, 2006, Anadarko had proved developed reserves of 7.6 Tcf of natural gas and 719 million barrels (MMBbls) of crude oil, condensate and NGLs. Proved developed reserves comprise 66% of total proved reserves. In 2006, each of the legacy companies (Anadarko, Kerr-McGee and Western) used a different process to evaluate reserves and to provide for external review and validation. For the Anadarko legacy assets and the Kerr-McGee legacy assets, estimates of proved reserves and associated future net cash flows are made by the Company’s engineers. Netherland, Sewell & Associates, Inc. (NSAI), an independent worldwide petroleum consultant, provided an external review which varied for each legacy company. For the Western legacy assets, the reports of proved reserves estimates were prepared by NSAI. Additional information on procedures performed by NSAI are outlined in their reports which are attached as Exhibit 99 of this Form 10-K.

The Company’s estimates of proved reserves, proved developed reserves and proved undeveloped reserves at December 31, 2006, 2005 and 2004 and changes in proved reserves during the last three years are contained in theSupplemental Information on Oil and Gas Exploration and Production Activities — Unaudited (Supplemental Information)in the Anadarko Petroleum Corporation 2006 Consolidated Financial Statements (Consolidated Financial Statements) under Item 8 of this Form 10-K. Additional information with respect to NSAI’s participation, and the Company’s methods and procedures employed in the reserve estimation process, are also found in theSupplemental Information. The Company files annual estimates of certain proved oil and gas reserves with the U.S. Department of Energy (DOE), which are within 5% of the amounts included in the above estimates.

Also contained in theSupplemental Informationin the Consolidated Financial Statements are the Company’s estimates of future net cash flows and discounted future net cash flows from proved reserves. SeeOperating ResultsandCritical Accounting Policies and Estimatesunder Item 7 of this Form 10-K for additional information on the Company’s proved reserves.

3

Sales Volumes and Prices

The following table shows the Company’s annual sales volumes from continuing operations. Volumes for natural gas are in billion cubic feet (Bcf) at a pressure base of 14.73 pounds per square inch. For the computation of million barrels of oil equivalent (MMBOE), six thousand cubic feet (Mcf) of gas is the energy equivalent of one barrel of oil, condensate or NGLs.

| | | | | | |

| | | 2006 | | 2005 | | 2004 |

United States | | | | | | |

Natural gas (Bcf) | | 558 | | 414 | | 499 |

Oil and condensate (MMBbls) | | 39 | | 24 | | 32 |

Natural gas liquids (MMBbls) | | 15 | | 13 | | 16 |

Total (MMBOE) | | 147 | | 106 | | 131 |

| | | |

Algeria | | | | | | |

Oil and condensate (MMBbls) | | 23 | | 24 | | 22 |

Total (MMBOE) | | 23 | | 24 | | 22 |

| | | |

Other International | | | | | | |

Oil and condensate (MMBbls) | | 8 | | 8 | | 8 |

Total (MMBOE) | | 8 | | 8 | | 8 |

| | | |

Total | | | | | | |

Natural gas (Bcf) | | 558 | | 414 | | 499 |

Oil and condensate (MMBbls) | | 70 | | 56 | | 62 |

Natural gas liquids (MMBbls) | | 15 | | 13 | | 16 |

Total (MMBOE) | | 178 | | 138 | | 161 |

4

The following table shows the Company’s annual average sales prices and average production costs from continuing operations. The impact on average sales prices from derivative instruments the Company utilizes to manage price risk related to the Company’s sales volumes is shown separately in the table. Natural gas sales, and oil and condensate sales for 2006 include net unrealized gains related to these derivatives of $579 million and $258 million, respectively. Unrealized gains (losses) related to derivatives were not material in 2005 or 2004. Production costs are costs incurred to operate and maintain the Company’s wells and related equipment and include cost of labor, well service and repair, location maintenance, power and fuel, transportation, cost of product, property taxes, production and severance taxes and production related general and administrative costs. Certain amounts for prior years have been reclassified to conform to the current presentation. Additional information on volumes, prices and markets is contained inFinancial ResultsandGathering, Processing and Marketing Strategiesunder Item 7 of this Form 10-K. Additional detail of production costs is contained in theSupplemental Informationunder Item 8 of this Form 10-K. Information on major customers is contained inNote 15of theNotes to Consolidated Financial Statements under Item 8 of this Form 10-K.

| | | | | | | | | | | |

| | | 2006 | | 2005 | | | 2004 | |

United States | | | | | | | | | | | |

Sales price | | | | | | | | | | | |

Natural gas (per Mcf) | | $ | 6.14 | | $ | 7.44 | | | $ | 5.62 | |

Gains (losses) on derivatives | | | 1.36 | | | (0.28 | ) | | | (0.44 | ) |

| | | | | | | | | | | |

Total price per Mcf | | $ | 7.50 | | $ | 7.16 | | | $ | 5.18 | |

| | | |

Oil and condensate (per barrel) | | | 59.41 | | | 51.67 | | | | 38.71 | |

Gains (losses) on derivatives | | | 9.18 | | | (7.32 | ) | | | (7.06 | ) |

| | | | | | | | | | | |

Total price per barrel | | $ | 68.59 | | $ | 44.35 | | | $ | 31.65 | |

| | | |

Natural gas liquids (per barrel) | | | 39.58 | | | 34.56 | | | | 27.84 | |

| | | |

Total (per BOE) | | | 50.77 | | | 42.29 | | | | 30.83 | |

Production cost (per BOE) | | $ | 10.07 | | $ | 8.41 | | | $ | 6.68 | |

| | | |

Algeria | | | | | | | | | | | |

Sales price | | | | | | | | | | | |

Oil and condensate (per barrel) | | $ | 65.59 | | $ | 54.38 | | | $ | 34.78 | |

Production cost (per BOE) | | $ | 7.75 | | $ | 2.88 | | | $ | 2.94 | |

| | | |

Other International | | | | | | | | | | | |

Sales price | | | | | | | | | | | |

Oil and condensate (per barrel) | | $ | 48.58 | | $ | 39.37 | | | $ | 27.91 | |

Production cost (per BOE) | | $ | 9.38 | | $ | 8.40 | | | $ | 7.93 | |

| | | |

Total | | | | | | | | | | | |

Sales price | | | | | | | | | | | |

Natural gas (per Mcf) | | $ | 6.14 | | $ | 7.44 | | | $ | 5.62 | |

Gains (losses) on derivatives | | | 1.36 | | | (0.28 | ) | | | (0.44 | ) |

| | | | | | | | | | | |

Total price per Mcf | | $ | 7.50 | | $ | 7.16 | | | $ | 5.18 | |

| | | |

Oil and condensate (per barrel) | | | 60.29 | | | 51.03 | | | | 37.12 | |

Gains (losses) on derivatives | | | 5.15 | | | (3.19 | ) | | | (4.84 | ) |

| | | | | | | | | | | |

Total price per barrel | | $ | 65.44 | | $ | 47.84 | | | $ | 32.28 | |

| | | |

Natural gas liquids (per barrel) | | | 39.58 | | | 34.56 | | | | 27.84 | |

| | | |

Total (per BOE) | | | 52.61 | | | 44.19 | | | | 31.23 | |

Production cost (per BOE) | | $ | 9.75 | | $ | 7.47 | | | $ | 6.23 | |

5

Properties and Activities — United States

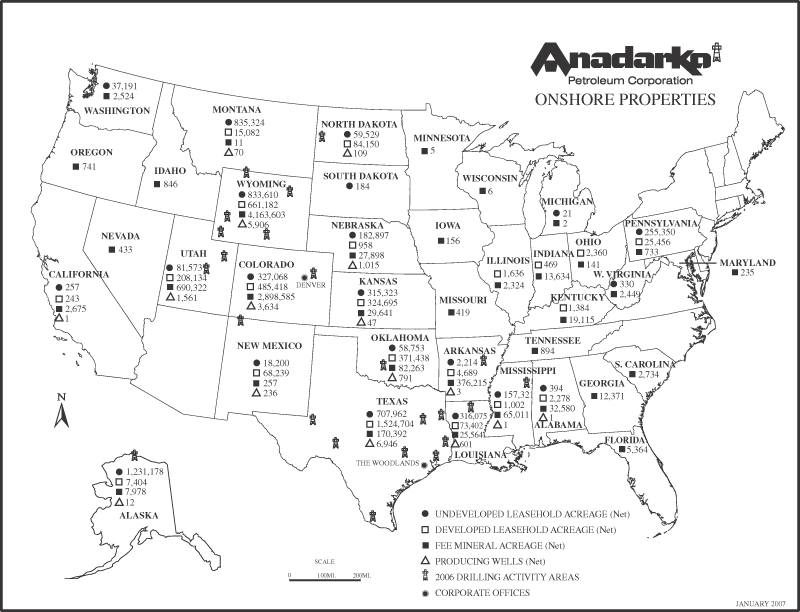

Overview Anadarko’s active areas in the United States include the Lower 48 states, Alaska and the Gulf of Mexico. Reserves in the United States comprised 88% of Anadarko’s total proved reserves at year-end 2006. During 2006, the Company’s drilling efforts in the United States resulted in 1,238 gas wells, 250 oil wells and 12 dry holes. The accompanying maps illustrate Anadarko’s net undeveloped and developed lease and fee mineral acreage, number of net producing wells and other data relevant to its domestic onshore and offshore oil and gas operations.

The following table presents selected 2006 United States operating data by area.

| | | | | | | | | | | | |

| | | Sales Volumes | | Producing

Wells(1) | | | | |

| | | Natural Gas

(MMcf/d) | | Oil and NGLs

(MBbls/d) | | Total

(MBOE/d) | | | Drilling Statistics |

| | | | | | | Wells

Drilled(2) | | Success

Rate |

Rockies: | | | | | | | | | | | | |

Tight Gas | | | | | | | | | | | | |

- Greater Natural Buttes | | 80 | | 1 | | 14 | | 1,732 | | 123 | | 100.0% |

- Wattenberg | | 81 | | 7 | | 20 | | 3,930 | | 63 | | 100.0% |

- Wamsutter | | 96 | | 9 | | 25 | | 1,231 | | 155 | | 99.4% |

- Pinedale and Jonah | | 34 | | — | | 6 | | 449 | | 71 | | 100.0% |

Coalbed Methane | | 123 | | — | | 21 | | 7,174 | | 541 | | 100.0% |

Enhanced Oil Recovery | | 25 | | 16 | | 20 | | 1,571 | | 180 | | 100.0% |

Other | | 85 | | 3 | | 17 | | 2,953 | | 13 | | 92.3% |

| | | | | | | | | | | | |

| | 524 | | 36 | | 123 | | 19,040 | | 1,146 | | 99.8% |

Southern Region: | | | | | | | | | | | | |

Vernon | | 188 | | — | | 31 | | 357 | | 67 | | 98.5% |

Bossier | | 183 | | — | | 31 | | 1,063 | | 38 | | 100.0% |

Carthage | | 87 | | 4 | | 19 | | 1,328 | | 40 | | 100.0% |

Haley | | 113 | | — | | 19 | | 3 | | 25 | | 96.0% |

Ozona | | 50 | | 1 | | 9 | | 44 | | 55 | | 100.0% |

Austin Chalk | | 89 | | 21 | | 36 | | 2,126 | | 41 | | 100.0% |

South Texas/Other | | 177 | | 26 | | 55 | | 9,073 | | 62 | | 95.2% |

| | | | | | | | | | | | |

| | 887 | | 52 | | 200 | | 13,994 | | 328 | | 98.5% |

| | | | | | | | | | | | |

Total Onshore - Lower 48 States | | 1,411 | | 88 | | 323 | | 33,034 | | 1,474 | | 99.5% |

| | | | | | |

Alaska | | — | | 22 | | 22 | | 55 | | 10 | | 90.0% |

Gulf of Mexico | | | | | | | | | | | | |

Marco Polo/K2 | | 14 | | 18 | | 20 | | 10 | | 4 | | 100.0% |

Nansen | | 23 | | 3 | | 7 | | 15 | | — | | |

Boomvang | | 4 | | 2 | | 3 | | 10 | | — | | |

Gunnison | | 17 | | 3 | | 6 | | 13 | | — | | |

Red Hawk | | 23 | | — | | 4 | | 2 | | — | | |

Constitution/Ticonderoga | | 16 | | 8 | | 10 | | 6 | | 1 | | 100.0% |

Other | | 21 | | 6 | | 9 | | 124 | | 11 | | 63.6% |

| | | | | | | | | | | | |

| | 118 | | 40 | | 59 | | 180 | | 16 | | 75.0% |

| | | | | | | | | | | | |

Total United States | | 1,529 | | 150 | | 404 | | 33,269 | | 1,500 | | 99.2% |

| | | | | | | | | | | | |

(1) | Gross number of wells in which Anadarko has an interest. |

(2) | Includes 1,433 gross development wells with a 99.6% success rate and 67 gross exploration wells with a 91% success rate. |

6

| | | | | | | | | | | | |

| | | Undeveloped | | | Developed | | | | | | | |

| | Leasehold

|

| | Leasehold

|

| | Fee

Mineral |

| | Producing | |

| | Acreage (Net | ) | | Acreage

|

(Net) | | Acreage

|

(Net) | | Wells (Net | ) |

Onshore: | | | | | | | | | | | | |

United States | | | | | | | | | | | | |

Alabama | | 394 | | | 2,278 | | | 32,580 | | | 1 | |

Alaska* | | 1,231,178 | | | 7,404 | | | 7,978 | | | 12 | |

Arkansas* | | 2,214 | | | 4,689 | | | 376,215 | | | 3 | |

California | | 257 | | | 243 | | | 2,675 | | | 1 | |

Colorado* | | 327,068 | | | 485,418 | | | 2,898,585 | | | 3,634 | |

Florida | | -- | | | -- | | | 5,364 | | | -- | |

Georgia | | -- | | | -- | | | 12,371 | | | -- | |

Idaho | | -- | | | -- | | | 846 | | | -- | |

Illinois | | -- | | | 1,636 | | | 2,324 | | | -- | |

Indiana | | -- | | | 469 | | | 13,634 | | | -- | |

Iowa | | -- | | | -- | | | 156 | | | -- | |

Kansas | | 315,323 | | | 324,695 | | | 29,641 | | | 47 | |

Kentucky | | -- | | | 1,384 | | | 19,115 | | | -- | |

Louisiana* | | 316,075 | | | 73,402 | | | 25,564 | | | 601 | |

Maryland | | -- | | | -- | | | 235 | | | -- | |

Michigan | | 21 | | | -- | | | 2 | | | -- | |

Minnesota | | -- | | | -- | | | 5 | | | -- | |

Mississippi* | | 157,321 | | | 1,002 | | | 65,011 | | | 1 | |

Missouri | | -- | | | -- | | | 419 | | | -- | |

Montana | | 835,324 | | | 15,082 | | | 11 | | | 70 | |

Nebraska | | 182,897 | | | 958 | | | 27,898 | | | 1,015 | |

Nevada | | -- | | | -- | | | 433 | | | -- | |

New Mexico* | | 18,200 | | | 68,239 | | | 257 | | | 236 | |

North Dakota* | | 59,529 | | | 84,150 | | | -- | | | 109 | |

Ohio | | -- | | | 2,360 | | | 141 | | | -- | |

Oklahoma* | | 58,753 | | | 371,438 | | | 82,263 | | | 791 | |

Oregon | | -- | | | -- | | | 741 | | | -- | |

Pennsylvania | | 255,350 | | | 25,456 | | | 733 | | | -- | |

South Carolina | | -- | | | -- | | | 2,734 | | | -- | |

South Dakota | | 184 | | | -- | | | -- | | | -- | |

Tennessee | | -- | | | -- | | | 894 | | | -- | |

Texas* | | 707,962 | | | 1,524,704 | | | 170,392 | | | 6,946 | |

Utah* | | 81,573 | | | 208,134 | | | 690,322 | | | 1,561 | |

Washington | | 37,191 | | | -- | | | 2,524 | | | -- | |

West Virginia | | 330 | | | -- | | | 2,449 | | | -- | |

Wisconsin | | -- | | | -- | | | 6 | | | -- | |

Wyoming* | | 833,610 | | | 661,182 | | | 4,163,603 | | | 5,906 | |

| | | | | | | | | | | | |

Corporate Offices: | | | | | | | | | | | | |

United States | | | | | | | | | | | | |

The Woodlands, Texas | | | | | | | | | | | | |

Denver, Colorado | | | | | | | | | | | | |

* 2006 Drilling Activity Areas | |

7

In late 2006, as part of the asset realignment associated with the 2006 acquisitions, Anadarko signed several separate and unrelated agreements for the sale of properties and announced intentions to divest certain other non-core assets. In November 2006, Anadarko reached an agreement to sell its interests in the Knotty Head and Big Foot oil discoveries, as well as the Big Foot North prospect in the Gulf of Mexico for $901 million. In December 2006, the Company reached an agreement to sell its Vernon and Ansley fields, located in Jackson Parish, Louisiana, for $1.6 billion. In January 2007, Anadarko signed two separate and unrelated agreements to sell its interests in the Williston basin, Elk basin and Gooseberry area of the Northern Rockies for a total of $810 million, as well as an agreement to divest control of Anadarko’s interests in 28 Permian basin oil fields in West Texas for $1 billion. Certain of these transactions have closed and the remaining transactions are expected to close in the first half of 2007.

In February 2007, Anadarko signed an agreement to sell its interests in certain natural gas properties in Oklahoma and Texas for $860 million. This agreement is expected to close during the second quarter of 2007. During February, Anadarko also closed on the sale of its Genghis Khan discovery in the deepwater Gulf of Mexico for $1.33 billion. Anadarko will use the net proceeds from all of these sales to further reduce debt under the acquisition facility.

Onshore — Lower 48 States At the end of 2006, about 72% of the Company’s proved reserves were located onshore in the Lower 48 states with 38% in the Rockies. The Company’s 2007 capital budget for this area is about $2.0 billion with over 46% of the capital allocated to the Rockies in unconventional tight gas plays and coalbed methane (CBM) development.

Rocky Mountains During 2006, Anadarko significantly increased its tight gas and CBM holdings in the Rocky Mountains area through the acquisitions of Kerr-McGee and Western. The acquisitions included tight gas plays in the Greater Natural Buttes, Wattenberg and the Pinedale Anticline and Jonah fields. The majority of the Company’s legacy activity in the Rocky Mountains area is associated with developing tight gas in the Wamsutter area, conventional reservoirs, CBM and enhanced oil recovery (EOR) projects.

The 2006 drilling program in the Greater Natural Buttes area in Uintah County, Utah was primarily focused on exploitation of the Wasatch and Mesa Verde formations. The Company operates approximately 1,180 wells in the Greater Natural Buttes field area and has an interest in over 550 non-operated wells.

The Wattenberg gas field is located in the DJ basin in northeast Colorado. The Company’s primary exploitation focus in this area includes activities such as deepenings, fracture stimulations, re-completions and infill drilling. The infill drilling program was accelerated in 2006 following the approval of down-spacing which created a significant increase in drill sites.

During 2006, Anadarko was active in the Wamsutter and Moxa Arch fields, both located on the Land Grant. The Land Grant provides the Company with the added benefit of royalty revenues upon the success of outside operators as they drill on Anadarko’s net revenue fee acreage. The Land Grant also provides the Company with a large captured area on which to explore. In 2007, Anadarko intends to participate in over 200 wells in this area.

The Company’s Pinedale and Jonah fields are located in the Green River basin of southwest Wyoming. These tight gas assets were obtained as part of the Western acquisition. The gas produced at Pinedale and Jonah is transported through Company owned gathering systems that deliver gas to an Anadarko processing facility, located on the Land Grant. Anadarko plans to continue an active drilling program in the area in 2007.

The Company’s CBM operation is located in Wyoming’s Powder River basin. During 2006, the Company increased its acreage position in the Powder River basin with the acquisition of Western. The challenge in developing Wyoming’s CBM is the handling of the large amounts of water associated with de-watering coal. Anadarko’s solution resulted in the construction of a pipeline to transport produced water from the CBM fields to Anadarko’s operated Salt Creek field for underground injection. Other CBM focus areas for the Company include Anadarko’s legacy Helper and Clawson fields in Utah and the Atlantic Rim field in Wyoming.

The Company’s EOR operations at Salt Creek, Monell and Sussex, located in Wyoming, continue to demonstrate year-over-year increases in oil response due to CO2 injection.

8

Southern Region Anadarko’s properties in the southern region are located primarily in Texas, Louisiana and Oklahoma with focus on tight gas, fractured reservoirs and EOR.

Activities at the Company’s properties in east Texas are concentrated in the Bossier play with production and development activities in the Dowdy Ranch, Dew/Mimms Creek, Bald Prairie, Beargrass, Holly Branch and Marquez fields. Anadarko is encouraged with the results of its Cotton Valley infill drilling program in the Carthage area, with plans to increase activity in this play.

Anadarko’s central Texas activity continues to focus on horizontal drilling in the Austin Chalk formation of the Giddings and Brookeland fields. Much of the current activity involves extending the field boundaries and executing a low cost re-entry drilling program.

Operations in west Texas are concentrated on increasing production and reserves in the tight gas play of the Haley field. During 2006, the Company attained record production rates in the Haley field. Other areas of focus for the Company in west Texas include continued development of the Ozona field and waterflood projects in the Permian basin.

In south Texas, the Company had an active drilling program in Starr and Hidalgo counties during 2006. Drilling and completion activities focused primarily on tight gas plays in the Frost and Braulia East fields. The drilling program is expected to continue into 2007.

Alaska Anadarko’s activity in Alaska is concentrated primarily on the North Slope. About 2% of the Company’s proved reserves at year-end 2006 were in Alaska. The Company’s capital budget is about $90 million for Alaska in 2007.

During 2006, activity at the Colville River Unit (Alpine, Fiord and Nanuq fields — 22% WI) on Alaska’s North Slope focused on development and achieving first production from the Nanuq and Fiord satellite fields. Anadarko and the operator are continuing to pursue the state, local and federal permits for three additional Alpine satellites. During 2006, Anadarko participated in a successful exploration well at Qannik (22% WI) within the Colville River area. The Qannik reservoir is also expected to become an Alpine satellite development. Project sanction is expected in early 2007 with first production by early 2009.

Anadarko also obtained, through the acquisition of Kerr-McGee, 20 leases covering approximately 41,000 acres off the coast of Alaska, northwest of Prudhoe Bay, and two leases onshore west of Kuparuk, covering approximately 5,000 acres.

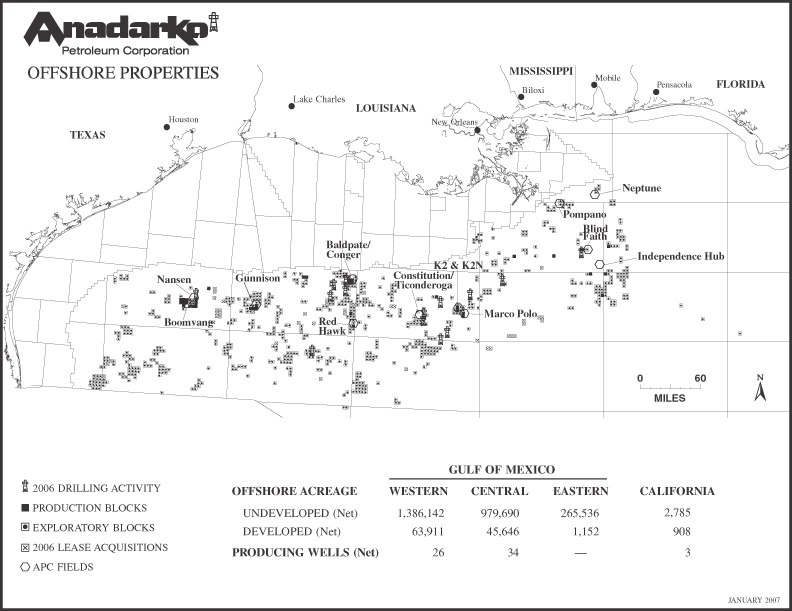

Gulf of Mexico At year-end 2006, about 13% of the Company’s proved reserves were located offshore in the deepwater of the Gulf of Mexico where Anadarko owns an average 63% working interest in 777 blocks and has access to an additional 27 blocks through participation agreements. Anadarko has budgeted about $1 billion for capital spending in the deepwater Gulf of Mexico for 2007, 30% of which relates to exploration.

During 2006, Anadarko significantly increased its holdings in the deepwater Gulf of Mexico through the acquisition of Kerr-McGee. Notable properties acquired in this area include interests in the Nansen, Boomvang, Gunnison, Red Hawk and Constitution/Ticonderoga fields as well as several additional discoveries in the eastern Gulf of Mexico. Including operations acquired with Kerr-McGee, the Company had nine exploration discovery wells in 2006 in the deepwater Gulf of Mexico where efforts focused on the lower Tertiary and the lower/middle Miocene formations. Combined, Anadarko holds interests in nine producing fields and is in the process of developing six additional fields.

Marco Polo/K2 complex Anadarko operates, and a third party owns, the platform and production facilities for the Marco Polo deepwater development project. During 2006, an agreement was reached with partners to unitize the K2 and K2 North fields (65% WI) with Anadarko as operator. These fields are tied back subsea to the Marco Polo platform where four wells were completed during 2006. During 2007, the Company plans to drill additional wells in the area.

Nansen field (50% WI) The Nansen field began production in 2002. The Nansen field was developed with a truss spar in 3,700 feet of water. During 2006, the Company completed a multi-well satellite drilling program in the Northwest Nansen field area with four discoveries and development of a tie-back to the Nansen spar commenced. The Company expects to begin production from this area by late 2007.

9

Boomvang field, East Breaks Blocks 641, 642, 643, 686 and 688 (30% WI), Block 598 (100% WI), and Block 599 (33% WI) The Boomvang field also began production in 2002. The Boomvang field was developed with a truss spar in 3,450 feet of water. During 2006, the Company installed a subsea tie-back of a 2005 discovery with first production expected in the first quarter of 2007. During 2007, the Company plans to drill two additional satellite prospects.

Gunnison field (50% WI) The Gunnison field has been producing since December 2003 and incorporates a truss spar in 3,100 feet of water. During 2006, the Dawson Deep discovery began production as a subsea tie-back to the Gunnison spar.

Red Hawk field (50% WI) The Red Hawk field, located in approximately 5,300 feet of water, began production in 2004 utilizing the world’s first cell spar designed for developing smaller reservoirs in deepwater basins. During 2006, the Company began a compression project which is expected to extend the life of the field.

Constitution/Ticonderoga fields The Constitution field (100% WI) began production in 2006 utilizing a truss spar located in approximately 5,000 feet of water. The Ticonderoga field (50% WI) also began production in 2006 as a subsea tie-back to the Constitution spar. During 2007, the Company plans to bring two wells on production and an additional well is expected to be drilled.

Independence Hub Development plans for a gas processing hub, Independence Hub, and gas export pipeline in the eastern Gulf of Mexico were approved in late 2004. The Company, along with a group of other producers, contracted with a third party to design, construct and own the facility. Anadarko will operate Independence Hub. The facility, capable of processing 1 Bcf of gas per day, will serve several ultra-deepwater natural gas fields, including eight field discoveries operated by Anadarko. These discoveries include interests in the Merganser, Vortex and San Jacinto fields which were acquired with Kerr-McGee during 2006. The initial production will be from fifteen wells, fourteen of which Anadarko has an interest. Nine wells were completed during 2006 and the remaining five wells will be completed during 2007. The Company anticipates first production from the Independence Hub in the second half of 2007.

Other The acquisition of Kerr-McGee also included interests in the Neptune field (50% WI), Conger field (25% WI), Baldpate field (50% WI), Blind Faith field (37.5% WI) and Pompano field (25% WI). Anadarko also has participation agreements to explore deepwater blocks in the central and western Gulf of Mexico. Anadarko’s exploration program in this area is currently focused on the extensive middle-to-lower Miocene play within the foldbelt area and the developing lower tertiary play near the 2006 Kaskida discovery. During 2006, the Company delineated three discoveries: Tonga, Big Foot and Knotty Head, as well as had five additional discoveries; Kaskida, Power Play, Claymore, Caesar and Mission Deep. Anadarko also participated in five unsuccessful wells. The Company expects to participate in approximately four exploration wells and five delineation wells in the region in 2007.

10

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | Producing | |

| | | | | | | Undeveloped | | | Developed | | | Wells | |

| | | | | | | (Net | ) | | (Net | ) | | (Net | ) |

Offshore Acreage: | | | | | | | | | | | | | | |

| | Gulf of

Mexico | | | | | | | | | | | | |

| | | | Western | * | | 1,386,142 | | | 63,911 | | | 26 | |

| | | | Central | * | | 979,690 | | | 45,646 | | | 34 | |

| | | | Eastern | * | | 265,536 | | | 1,152 | | | -- | |

| | | | | | | | | | | | | | |

| | California | | | | | 2,785 | | | 908 | | | 3 | |

| | | | | | | | | | | | | | |

| | APC

fields: | | | | | | | | | | | | |

| | | | Nansen | | | | | | | | | | |

| | | | Boomvang | | | | | | | | | | |

| | | | Gunnison | | | | | | | | | | |

| | | | Baldpate/

Conger |

| | | | | | | | | |

| | | | Red Hawk | | | | | | | | | | |

| | | | Constitution/

Ticonderoga |

| | | | | | | | | |

| | | | K2 & K2N | | | | | | | | | | |

| | | | Marco Polo | | | | | | | | | | |

| | | | Independence

Hub |

| | | | | | | | | |

| | | | Blind Faith | | | | | | | | | | |

| | | | Pompano | | | | | | | | | | |

| | | | Neptune | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

* 2006 Drilling Activity | | | | | | | | | | | | | | |

Production Blocks Exploratory Blocks 2006 Lease Acquisitions APC Fields | | | | | | | | | | | | | | |

11

Properties and Activities — Algeria

Overview Anadarko is engaged in exploration, development and production activities in Algeria’s Sahara Desert. At the end of 2006, about 10% of the Company’s proved reserves were located in Algeria where a total of eight fields discovered by the Company were on production. In 2006, net sales volumes from the Company’s properties in Algeria represented 13% of the Company’s total sales volumes. In 2006, Anadarko participated in 14 wells with a success rate of 86%. In addition, the Company participated in nine injection or service wells during the year. The Company’s 2007 capital budget for Algeria is expected to be about $190 million and the budget provides for drilling about 25 development and service wells and four exploration wells.

Contracts and Partners Anadarko’s interest in the Production Sharing Agreement (PSA) for Blocks 404, 208 and 211 is 50% before participation at the exploitation stage by Sonatrach, the national oil and gas enterprise of Algeria. The Company has two partners, each with a 25% interest, also prior to participation by Sonatrach. Under the terms of the PSA, oil reserves that are discovered, developed and produced are shared by Sonatrach, Anadarko and its two partners. Sonatrach is responsible for 51% of the development and production costs. Anadarko and its partners also have an exploration program underway on Blocks 404, 208 and 211 and has an exploration license, under separate PSA, for Block 403c/e (33% interest). Anadarko and its joint venture partners fund Sonatrach’s share of exploration costs and are entitled to recover these exploration costs out of production in the exploitation phase.

As of August 2006, Anadarko became subject to a new Algerian exceptional profits tax. For additional information seeRisk Factors under Item 1a andOther Developments under Item 7 of this Form 10-K.

Production and Development On Block 404, production from the HBNS field averaged 119 MBbls/d of oil (gross) and production from five of the satellite fields averaged 42 MBbls/d of oil (gross) in 2006. Production from the HBN field, which extends from Block 404 into Block 403 and is unitized with other companies, averaged 73 MBbls/d of oil (gross) in 2006. Anadarko is also actively involved in the unitized Ourhoud field which is located in the southern portion of Block 404 and extends into Block 406a and Block 405. Production from the Ourhoud field averaged 235 MBbls/d of oil (gross) in 2006. Anadarko has several fields farther south on Block 208. Development of the Block 208 fields, including the design of a new production facility, is progressing. Initial production from Block 208 is targeted for late 2010.

Exploration During 2006, Anadarko had a satellite discovery at the BBKS-1 and one unsuccessful exploration well. Two wells were drilled to appraise the BBKS discovery with one encountering hydrocarbon bearing sands and the other being plugged and abandoned. During 2007, the Company expects to further test and delineate the BBKS discovery as well as participate in two exploration wells.

12

Properties and Activities — Other International

Overview The Company’s other international oil and gas production and or development operations are located primarily in China, Venezuela, Qatar and Brazil. The Company has exploration acreage in Brazil, China, Indonesia, Trinidad, Qatar and other selected areas. About 2% of the Company’s total proved reserves were located in these other international locations at year-end 2006. During 2006, net sales volumes from the Company’s other international properties accounted for 4% of the Company’s total volumes. In 2007, the Company’s capital budget is expected to be about $390 million for these other international projects and provides for drilling about 17 development and 17 exploration wells.

China The Company’s interests in China were acquired with the Kerr-McGee acquisition in 2006. Anadarko’s development and production project in China straddles Block 04/36 and 05/36 in Bohai Bay in approximately 75 feet of water. The project consists of a gathering platform and two smaller unmanned satellite platforms, which are tied back to a floating production, storage and offloading vessel. During 2007, the Company plans to continue development drilling in the area. At the end of 2006, net production from China was approximately 17 MBbls/d of oil.

The Company also has exploration projects (100% WI in exploration phase) underway at Bohai Bay Blocks 09/18 and 09/06 and South China Sea Block 43/11. During 2006, Anadarko participated in three exploration wells with one discovery. During 2007, the Company plans to drill two exploration wells in Bohai Bay.

Venezuela The Company’s operations in Venezuela are located in the Oritupano-Leona contract area. As a result of contract and structural changes imposed by the government of Venezuela, Anadarko’s interest in its Venezuela oil and gas properties was converted from the operating service agreement, under which Anadarko’s interest was previously consolidated in results of operations, to an 18% equity interest in a new operating company, Empresa Mixta Petroritupano. The conversion was completed in the fourth quarter of 2006. With respect to this investment, Anadarko is currently analyzing its options, including a possible sale. For additional information seeOther Developments under Item 7 of this Form 10-K.

Qatar The Company had interests in 1,549,000 undeveloped lease acres and 19,000 developed acres in Qatar at year-end 2006. Anadarko is the operator and has a 92.5% interest in the Al Rayyan field, which is part of an Exploration and Production Sharing Agreement (EPSA) covering Blocks 12 and 13. Production from the Al Rayyan field, located on Block 12, totaled 2.2 MMBbls of oil (net) in 2006. The Company also has an exploration program under EPSAs covering Block 4 (60% interest) and Block 11 (49% interest). With respect to the producing assets, Anadarko is currently analyzing its options, including a possible sale.

Brazil The majority of Anadarko’s interests in Brazil were acquired with the Kerr-McGee acquisition in 2006. Anadarko now holds interests in more than one million gross undeveloped acres in Brazil. The Company holds a 50% interest in the Peregrino field located in the Campos basin. Anadarko expects development of the field to be sanctioned in 2007 with first production in 2010. In 2007, the Company plans to drill an appraisal well and acquire 3-D seismic.

Anadarko also holds exploration interests in several blocks located offshore in the Campos and Espírito Santo basins. Work obligations for the contract areas include the acquisition of 3-D seismic and a drilling commitment, with six wells still remaining. In 2007, Anadarko expects to acquire seismic and participate in one exploration well.

Trinidad The Company has a program underway offshore Trinidad on Blocks 3a (25% interest) and 3b (34.5% interest). In 2006, the Company had a discovery on Block 3a that tested 5 MBbls/d in 180 feet of water. Appraisal drilling is underway to help determine commerciality of the discovery. During 2007, the Company expects to drill about three exploration wells on its Trinidad blocks.

13

Indonesia Anadarko has a participating interest in approximately 5.1 million exploration acres in Indonesia through a combination of several operated and non-operated Production Sharing Contracts (PSC). Anadarko also has entered into an outside-operated agreement, under which the Company has access to an additional 7.4 million acres with an $80 million exploration commitment. In addition, the Company is operator of a PSC for the North East Madura III Block offshore Indonesia. During 2006, Anadarko exchanged an interest in this block (retaining a 60% interest) for varying interests in five blocks located in the Tarakan basin and Makassar Straits of Indonesia. Anadarko also acquired and operates a PSC located in south Sumatra. Anadarko participated in five unsuccessful exploration wells in Indonesia in 2006. During 2007, Anadarko plans to participate in up to nine exploration wells.

Mozambique In 2006, Anadarko signed an Exploration and Production Concession for the 2.64 million acre Offshore Area 1, located in northeast Mozambique in the Rovuma basin. The agreement has a five-year initial exploration term with a commitment to acquire new seismic and drill seven wells. Anadarko will operate the block, initially with a 100% interest.

Other Anadarko also has active exploration projects in Tunisia and several countries in West Africa, as well as activities in other potential new venture areas overseas.

Drilling Programs

The Company’s 2006 drilling program, related to continuing operations, focused on known oil and gas areas in the United States (Lower 48, Alaska and Gulf of Mexico) and Algeria. Exploration activity consisted of 76 wells, including 62 wells in the Lower 48, 5 wells offshore in the Gulf of Mexico, 4 wells in Algeria and 5 wells in other international locations. Development activity consisted of 1,461 wells, which included 1,412 wells in the Lower 48, 10 wells in Alaska, 11 wells offshore in the Gulf of Mexico, 10 wells in Algeria and 18 wells in other international locations.

Drilling Statistics

The following table shows the results of the oil and gas wells drilled and tested:

| | | | | | | | | | | | | | |

| | | Net Exploratory | | Net Development | | |

| | | Productive | | Dry Holes | | Total | | Productive | | Dry Holes | | Total | | Total |

2006 | | | | | | | | | | | | | | |

United States | | 37.4 | | 2.3 | | 39.7 | | 831.9 | | 2.2 | | 834.1 | | 873.8 |

Algeria | | 0.8 | | 0.8 | | 1.6 | | 1.8 | | — | | 1.8 | | 3.4 |

Other International | | — | | 2.6 | | 2.6 | | 3.5 | | — | | 3.5 | | 6.1 |

| | | | | | | | | | | | | | |

Total | | 38.2 | | 5.7 | | 43.9 | | 837.2 | | 2.2 | | 839.4 | | 883.3 |

| | | | | | | | | | | | | | |

2005 | | | | | | | | | | | | | | |

United States | | 10.8 | | 3.2 | | 14.0 | | 376.0 | | 1.0 | | 377.0 | | 391.0 |

Algeria | | 0.5 | | 0.3 | | 0.8 | | 2.9 | | 0.2 | | 3.1 | | 3.9 |

Other International | | 0.5 | | — | | 0.5 | | 5.4 | | — | | 5.4 | | 5.9 |

| | | | | | | | | | | | | | |

Total | | 11.8 | | 3.5 | | 15.3 | | 384.3 | | 1.2 | | 385.5 | | 400.8 |

| | | | | | | | | | | | | | |

2004 | | | | | | | | | | | | | | |

United States | | 25.2 | | 9.4 | | 34.6 | | 484.2 | | 4.7 | | 488.9 | | 523.5 |

Algeria | | 1.1 | | 1.5 | | 2.6 | | 2.1 | | — | | 2.1 | | 4.7 |

Other International | | — | | — | | — | | 8.1 | | — | | 8.1 | | 8.1 |

| | | | | | | | | | | | | | |

Total | | 26.3 | | 10.9 | | 37.2 | | 494.4 | | 4.7 | | 499.1 | | 536.3 |

| | | | | | | | | | | | | | |

14

The following table shows the number of wells in the process of drilling or in active completion stages and the number of wells suspended or waiting on completion as of December 31, 2006:

| | | | | | | | |

| | | Wells in the process

of drilling or

in active completion | | Wells suspended or waiting on completion |

| | | Exploration | | Development | | Exploration | | Development |

United States | | | | | | | | |

Gross | | 11 | | 107 | | 30 | | 256 |

Net | | 7.4 | | 52.0 | | 12.3 | | 141.0 |

| | | | |

Algeria | | | | | | | | |

Gross | | — | | 2 | | 2 | | 5 |

Net | | — | | 0.2 | | 0.9 | | 0.3 |

| | | | |

Other International | | | | | | | | |

Gross | | 1 | | 2 | | 1 | | 2 |

Net | | 0.3 | | 0.6 | | 0.3 | | 0.7 |

| | | | |

Total | | | | | | | | |

Gross | | 12 | | 111 | | 33 | | 263 |

Net | | 7.7 | | 52.8 | | 13.5 | | 142.0 |

Productive Wells

As of December 31, 2006, the Company had an ownership interest in productive wells as follows:

| | | | |

| | | Oil Wells* | | Gas Wells* |

United States | | | | |

Gross | | 8,655 | | 24,614 |

Net | | 6,366.6 | | 14,630.0 |

| | |

Algeria | | | | |

Gross | | 161 | | — |

Net | | 32.3 | | — |

| | |

Other International | | | | |

Gross | | 365 | | — |

Net | | 91.8 | | — |

| | |

Total | | | | |

Gross | | 9,181 | | 24,614 |

Net | | 6,490.7 | | 14,630.0 |

__________ * Includes wells containing multiple completions as follows: | | | | |

| | |

Gross | | 1,495 | | 2,604 |

Net | | 1,468.4 | | 2,441.3 |

15

Properties and Leases

The following schedule shows the number of developed lease, undeveloped lease and fee mineral acres in which Anadarko held interests at December 31, 2006:

| | | | | | | | | | | | | | | | |

| | | Developed

Lease | | Undeveloped

Lease | | Fee Minerals | | Total |

| thousands | | Gross | | Net | | Gross | | Net | | Gross | | Net | | Gross | | Net |

United States | | | | | | | | | | | | | | | | |

Onshore — Lower 48 | | 6,039 | | 3,857 | | 6,129 | | 4,190 | | 10,040 | | 8,630 | | 22,208 | | 16,677 |

Offshore | | 284 | | 112 | | 4,162 | | 2,634 | | — | | — | | 4,446 | | 2,746 |

Alaska | | 35 | | 7 | | 3,826 | | 1,249 | | 16 | | 8 | | 3,877 | | 1,264 |

| | | | | | | | | | | | | | | | |

Total | | 6,358 | | 3,976 | | 14,117 | | 8,073 | | 10,056 | | 8,638 | | 30,531 | | 20,687 |

| | | | | | | | | | | | | | | | |

Algeria* | | 225 | | 55 | | 2,640 | | 778 | | — | | — | | 2,865 | | 833 |

Other International | | 81 | | 39 | | 28,861 | | 13,932 | | — | | — | | 28,942 | | 13,971 |

| * | Developed acreage in Algeria relates only to areas with an Exploitation License. A portion of the undeveloped acreage in Algeria will be relinquished in the future consistent with contractual obligations or upon finalization of Exploitation License boundaries. |

Gathering, Processing and Marketing Properties and Activities

Overview Anadarko supports and seeks to enhance the value of its oil and gas operations through its gathering, processing and marketing (GPM) activities. These activities provide for the gathering, processing, transportation and ultimate sale of the Company’s production. In addition, the GPM function provides services for third-party customers.

Gathering and Processing Anadarko invests in gathering and processing facilities (midstream) to complement its oil and gas operations in regions where the Company has significant production. The Company is better able to manage both the value received for, and cost of, gathering, treating and processing natural gas through its ownership and operation of these facilities. In addition, Anadarko’s midstream business provides gathering, treating and processing services for third-party customers, including major and independent producers. Anadarko generates revenues in its gathering and processing activities through various fee structures that include fixed-rate, percent of proceeds, or keep-whole agreements. The Company also processes gas at various third-party plants. During 2007, the Company’s capital budget for midstream operations is expected to be about $500 million.

In 2006, Anadarko significantly increased the size and scope of its midstream business through the acquisitions of Western and Kerr-McGee. With these acquisitions, Anadarko has systems in eight states (Wyoming, Colorado, Utah, New Mexico, Kansas, Oklahoma, Texas and Louisiana) located in major onshore producing basins. The following table provides key statistics for Company-owned gathering and processing facilities.

| | | | | | | | |

| | | Number of

Gathering and

Processing

Facilities | | Miles of

Gathering

Systems | | Total

Horsepower | | 2006

Average

Throughput

(MMcf/d) |

Legacy Anadarko | | 17 | | 3,575 | | 212,294 | | 1,051 |

Acquired with Kerr-McGee | | 2 | | 2,394 | | 124,054 | | 568 |

Acquired with Western | | 16 | | 12,178 | | 661,588 | | 1,480 |

| | | | | | | | |

Total | | 35 | | 18,147 | | 997,936 | | 3,099 |

| | | | | | | | |

16

Marketing The Company’s marketing department actively manages the sales of its natural gas, crude oil and NGLs. In marketing its production, the Company attempts to maximize realized prices while managing credit risk exposure. The Company also purchases natural gas, crude oil and NGLs volumes for resale primarily from partners and producers near Anadarko’s production. These purchases allow the Company to aggregate larger volumes and attract larger, creditworthy customers, which helps enable the Company to maximize prices received for the Company’s production.

The Company sells natural gas under a variety of contracts. The Company has the marketing capability to move large volumes of gas into and out of the daily gas market to take advantage of any price volatility. The Company may also engage in trading activities for the purpose of generating profits from exposure to changes in market prices of natural gas, crude oil, condensate and NGLs. The Company’s marketing strategy includes the use of leased natural gas storage facilities and various derivative instruments. However, the Company does not engage in market-making practices nor does it trade in any non-energy-related commodities. The Company’s marketing function does not participate in any energy marketing-related partnerships.

In 2006, the Company also engaged in sales of greenhouse gas emission reduction credits (ERCs) derived from CO2injection operations in Wyoming. The Company expects additional sales of ERCs in the future.

Minerals Properties and Activities

The Company’s minerals properties contribute to operating income through non-operated joint venture and royalty arrangements in coal, trona and industrial mineral mines across the Company’s extensive fee mineral interest in the Land Grant. The Company reinvests the cash flow from its hard minerals operations primarily into its oil and gas operations.

The Company’s low sulfur coal deposits, located primarily in southern Wyoming, compete with other western coal producers for industrial and utility boiler markets, which burn the coal to produce steam used to generate electricity. The Company’s coal interests use both surface and underground mining methods of extraction. Because of the high extraction and transportation costs, additional development of the Company’s reserves is dependent on increased coal usage in local markets. In addition to fee mineral ownership of and royalty interests in coal reserves, the Company owns a 50% non-operating interest in Black Butte Coal Company. Black Butte Coal Company produces approximately 3 million tons of coal per year.

The world’s largest known deposit of trona, comprising 90% of the world’s trona resources, is located in the Green River basin in southwestern Wyoming. Natural soda ash, which is produced by refining trona ore, is used primarily in the production of glass, in the paper and water treatment industries and in the manufacturing of certain chemicals and detergents. The Company owns interests in lands containing approximately 50% of these reserves and has leased a portion of those lands to companies that mine and refine trona. In addition to fee mineral ownership of and royalty interest in trona reserves, the Company owns a 49% non-operating interest in the OCI Wyoming LP (OCI) soda ash refining facility near Green River, Wyoming. The OCI facility typically produces about 2 million tons of soda ash per year.

During 2004, the Company entered into an agreement whereby it sold a portion of its future royalties associated with existing coal and trona leases to a third party for $158 million, net of transaction costs. The Company conveyed a limited-term nonparticipating royalty interest, which was carved out of its royalty interests, that entitles the third party to receive certain amounts in future coal and trona royalty revenue over an 11-year period. For additional information, seeNote 10 — Sale of Future Hard Minerals Royalty Revenuesof theNotes to Consolidated Financial Statementsunder Item 8 of this Form 10-K.

Segment and Geographic Information

Information on operations by segment and geographic location is contained inNote 16of theNotes to Consolidated Financial Statements under Item 8 of this Form 10-K.

Employees

As of December 31, 2006, the Company had approximately 5,200 employees. Anadarko considers its relations with its employees to be satisfactory. The Company has had no significant work stoppages or strikes associated with its employees.

17

Regulatory Matters and Additional Factors Affecting Business

SeeRisk Factorsunder Item 1a of this Form 10-K.

Title to Properties

As is customary in the oil and gas industry, only a preliminary title review is conducted at the time properties believed to be suitable for drilling operations are acquired by the Company. Prior to the commencement of drilling operations, a thorough title examination of the drill site tract is conducted and curative work is performed with respect to significant defects, if any, before proceeding with operations. Anadarko believes the title to its leasehold properties is good and defensible in accordance with standards generally acceptable in the oil and gas industry subject to such exceptions that, in the opinion of legal counsel for the Company, are not so material as to detract substantially from the use of such properties.

The leasehold properties owned by the Company are subject to royalty, overriding royalty and other outstanding interests customary in the industry. The properties may be subject to burdens such as liens incident to operating agreements and current taxes, development obligations under oil and gas leases and other encumbrances, easements and restrictions. Anadarko does not believe any of these burdens will materially interfere with its use of these properties.

Capital Spending

SeeCapital Resources and Liquidityunder Item 7 of this Form 10-K.

Ratios of Earnings to Fixed Charges and Earnings to Combined Fixed Charges and Preferred Stock Dividends

| | | | | | |

| | | 2006 | | 2005 | | 2004 |

Ratio of earnings to fixed charges | | 6.37 | | 12.99 | | 5.66 |

Ratio of earnings to combined fixed charges and preferred stock dividends | | 6.32 | | 12.63 | | 5.56 |

These ratios were computed by dividing earnings by either fixed charges or combined fixed charges and preferred stock dividends. For this purpose, earnings include income from continuing operations before income taxes and fixed charges and excludes undistributed earnings of equity investees. Fixed charges include interest and amortization of debt expenses and the estimated interest component of rentals. Preferred stock dividends are adjusted to reflect the amount of pretax earnings required for payment.

Item 1a. Risk Factors

Forward Looking Statements The Company has made in this report, and may from time to time otherwise make in other public filings, press releases and discussions with Company management, forward looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 concerning the Company’s operations, economic performance and financial condition. These forward looking statements include information concerning future production and reserves, schedules, plans, timing of development, contributions from oil and gas properties, and those statements preceded by, followed by or that otherwise include the words “believes,” “expects,” “anticipates,” “intends,” “estimates,” “projects,” “target,” “goal,” “plans,” “objective,” “should” or similar expressions or variations on such expressions. For such statements, the Company claims the protection of the safe harbor for forward looking statements contained in the Private Securities Litigation Reform Act of 1995. Although the Company believes that the expectations reflected in such forward looking statements are reasonable, it can give no assurance that such expectations will prove to have been correct. Important factors that could cause actual results to differ materially from the Company’s expectations include, but are not limited to, the Company’s assumptions about energy markets, production levels,

18

reserve levels, operating results, competitive conditions, technology, the availability of capital resources, capital expenditures and other contractual obligations, the supply and demand for oil, natural gas, NGLs and other products or services, the price of oil, natural gas, NGLs and other products or services, the weather, inflation, the availability of goods and services, drilling risks, future processing volumes and pipeline throughput, general economic conditions, either internationally or nationally or in the jurisdictions in which the Company or its subsidiaries are doing business, legislative or regulatory changes, including changes in environmental regulation, environmental risks and liability under federal, state and foreign environmental laws and regulations, potential environmental obligations arising from Kerr-McGee’s former chemical business, the securities or capital markets, the ability to successfully integrate the operations of the Company, Kerr-McGee and Western, our ability to repay the debt issued for the acquisition of Kerr-McGee and Western, the outcome of proceedings related to the Algerian exceptional profits tax, and other factors discussed below and elsewhere in this Form 10-K and in the Company’s public filings, press releases and discussions with Company management. Anadarko undertakes no obligation to publicly update or revise any forward looking statements.

We may not be able to successfully integrate Kerr-McGee’s and Western’s operations with our operations.

Integration of the three previously independent companies is a complex, time consuming and costly process. Failure to timely and successfully integrate these companies may have a material adverse effect on the combined company’s business, financial condition and result of operations. The difficulties of combining the companies present challenges to our management, including:

| | • | | operating a significantly larger combined company; |

| | • | | integrating personnel with diverse backgrounds and organizational cultures; |

| | • | | experiencing operational interruptions or the loss of key employees, customers or suppliers; and |

| | • | | consolidating other corporate and administrative functions. |

The combined company is also exposed to risks that are commonly associated with transactions similar to the mergers, such as unanticipated liabilities and costs, some of which may be material, and diversion of management’s attention. As a result, the anticipated benefits of the mergers may not be fully realized, if at all.

Our debt and other financial commitments may limit our financial and operating flexibility.

We incurred approximately $24.9 billion in debt (including debt assumed) to consummate the Kerr-McGee and Western mergers. Our total debt was about $23.0 billion as of December 31, 2006. We also have various commitments for operating leases, drilling contracts and transportation and purchase obligations for services and products. Our financial commitments could have important consequences to you. For example, it could:

| | • | | increase our vulnerability to general adverse economic and industry conditions; |

| | • | | limit our ability to fund future working capital and capital expenditures, to engage in future acquisitions or development activities, or to otherwise realize the value of our assets and opportunities fully because of the need to dedicate a substantial portion of our cash flow from operations to payments on our debt or to comply with any restrictive terms of our debt; |

| | • | | limit our flexibility in planning for, or reacting to, changes in the industry in which we operate; and |

| | • | | place us at a competitive disadvantage compared to our competitors that have less debt and fewer financial commitments. |

19

A downgrade in our credit rating could negatively impact our cost of capital.

Standard and Poor’s (S&P) and Moody’s Investor Services (Moody’s) rate our debt at “BBB-” with a stable outlook and “Baa3” with a negative outlook, respectively. Although we are not aware of any current plans of S&P or Moody’s to lower their respective ratings on our debt, we cannot be assured that such credit ratings will not be downgraded. Although we do not have any rating downgrade triggers that would accelerate the maturity dates of outstanding debt, a downgrade in our credit ratings could negatively impact our cost of capital or our ability to effectively execute aspects of our strategy.

Failure to close our pending or planned asset divestitures could hinder our ability to reduce our debt.

Total debt at December 31, 2006, includes $11 billion outstanding under our 364-day acquisition facility that is due in August 2007. We intend to repay the majority of the remaining balance with proceeds from announced or targeted divestitures, free cash provided by operations and possible securities issuances. An unexpected delay or inability to complete pending or planned asset divestitures could have a material adverse effect on Anadarko’s ability to reduce its debt, which could negatively impact Anadarko’s stock price, credit rating and financial condition. For more information, seeOutlook under Item 7 of this Form 10-K.

We may incur substantial costs to comply with environmental requirements, including costs arising from Kerr-McGee’s former chemical business.

Prior to the merger, Kerr-McGee spun off its chemical manufacturing business to a newly created and separate company, Tronox Incorporated (Tronox). Under the terms of a Master Separation Agreement (MSA), Kerr-McGee agreed to reimburse Tronox for certain qualifying environmental remediation costs, subject to certain limitations and conditions and up to a maximum aggregate reimbursement of $100 million. However, Kerr-McGee could be subject to joint and several liability for certain costs of cleaning up hazardous substance contamination attributable to the facilities and operations conveyed to Tronox if Tronox becomes insolvent or otherwise unable to pay for certain remediation costs. As a result of the merger, we will be responsible to provide reimbursements to Tronox pursuant to the MSA, and we may be subject to potential joint and several liability, as the successor to Kerr-McGee, if Tronox is unable to perform certain remediation obligations.

Commodity pricing and demand may limit our productivity and profitability.

Crude oil prices continue to be affected by political developments worldwide, pricing decisions and production quotas of OPEC and volatile trading patterns in the commodity futures markets. In addition, in OPEC countries in which we have production such as Algeria and Qatar, when the world oil market is weak, we may be subject to periods of decreased production due to government-mandated cutbacks. Natural gas prices also continue to be highly volatile. In periods of sharply lower commodity prices, we may curtail production and capital spending projects, as well as delay or defer drilling wells in certain areas because of lower cash flows. Changes in crude oil and natural gas prices can impact our determination of proved reserves and our calculation of the standardized measure of discounted future net cash flows relating to oil and gas reserves. In addition, demand for oil and gas in the United States and worldwide may affect our level of production.

Under the full cost method of accounting, a noncash charge to earnings related to the carrying value of our oil and gas properties on a country-by-country basis may occur.

Whether we will be required to take such a charge depends on the prices for crude oil and natural gas at the end of any quarter, as well as the effect of both capital expenditures and changes in proved reserves during that quarter. See Note 1 — Summary of Significant Accounting Policiesunder Item 8 for additional information on the ceiling test.

Our results of operations could be adversely affected by goodwill impairments.

As a result of mergers and acquisitions, at December 31, 2006 we had approximately $4.3 billion of goodwill on our balance sheet. Goodwill is not amortized, but instead must be tested at least annually for

20

impairment by applying a fair-value-based test. Goodwill is deemed impaired to the extent that its carrying amount exceeds the fair value of the reporting unit. Although our latest tests indicate that no goodwill impairment is currently required, future deterioration in market conditions could lead to goodwill impairments that could have a substantial negative effect on our profitability.

We are subject to complex laws and regulations relating to environmental protection that can adversely affect the cost, manner and feasibility of doing business.

Our operations and properties are subject to numerous federal, state and local laws and regulations relating to environmental protection from the time projects commence until abandonment. These laws and regulations govern, among other things:

| | • | | the amounts and types of substances and materials that may be released into the environment; |

| | • | | the issuance of permits in connection with exploration, drilling and production activities; |

| | • | | the release of emissions into the atmosphere; |

| | • | | the discharge and disposition of generated waste materials; |

| | • | | offshore oil and gas operations; |

| | • | | the reclamation and abandonment of wells and facility sites; and |

| | • | | the remediation of contaminated sites. |

In addition, these laws and regulations may impose substantial liabilities for our failure to comply with them or for any contamination resulting from our operations. For a description of certain environmental proceedings in which we are involved, seeLegal Proceedingsunder Item 3 of this Form 10-K.

We may not be insured against all of the operating risks to which our business is exposed.

Our business is subject to all of the operating risks normally associated with the exploration for and production, gathering, processing and transportation of oil and gas, including blowouts, cratering and fire, any of which could result in damage to, or destruction of, oil and gas wells or formations or production facilities and other property and injury to persons. As protection against financial loss resulting from these operating hazards, we maintain insurance coverage, including certain physical damage, employer’s liability, comprehensive general liability and worker’s compensation insurance. However, we are not fully insured against all risks in all aspects of our business, such as political risk, business interruption risk and risk of major terrorist attacks. The occurrence of a significant event against which we are not fully insured could have a material adverse effect on our financial position.

Material differences between the estimated and actual timing of critical events may affect the completion of and commencement of production from development projects.

We are involved in several large development projects. Key factors that may affect the timing and outcome of such projects include:

| | • | | project approvals by joint venture partners; |

| | • | | timely issuance of permits and licenses by governmental agencies; |

| | • | | manufacturing and delivery schedules of critical equipment; and |

| | • | | commercial arrangements for pipelines and related equipment to transport and market hydrocarbons. |

Delays and differences between estimated and actual timing of critical events may affect the forward looking statements related to large development projects.

21

Our domestic operations are subject to governmental risks that may impact our operations.

Our domestic operations have been, and at times in the future may be, affected by political developments and by federal, state and local laws and regulations such as restrictions on production, changes in taxes, royalties and other amounts payable to governments or governmental agencies, price or gathering rate controls and environmental protection regulations.

We operate in other countries and are subject to political, economic and other uncertainties.

Our operations in areas outside the United States are subject to various risks inherent in foreign operations. These risks may include, among other things:

| | • | | loss of revenue, property and equipment as a result of hazards such as expropriation, war, insurrection and other political risks; |

| | • | | increases in taxes and governmental royalties; |

| | • | | renegotiation of contracts with governmental entities; |

| | • | | changes in laws and policies governing operations of foreign-based companies; and |

| | • | | currency restrictions and exchange rate fluctuations. |

Our international operations may also be adversely affected by laws and policies of the United States affecting foreign trade and taxation.

Realization of any of these factors could materially adversely affect our financial position.

We may be subject to increased tax payment obligations in connection with our operations in Algeria. Such increases could impact results of operations, cash flows and proved reserves.

In July 2006, the Algerian parliament approved legislation establishing an exceptional profits tax on foreign companies’ Algerian oil and gas production. In December 2006, implementing regulations regarding this legislation were issued and Sonatrach notified us as to the applicable regulatory provisions. The regulations provide for an exceptional profits tax imposed on gross production at rates of taxation ranging from 5% to 50% based on average daily production volumes for each calendar month. Uncertainty exists as to whether the exceptional profits tax will apply to the full value of our production or only to the value of our production in excess of $30 per barrel.

In the fourth quarter of 2006, we recorded a $103 million liability for the exceptional profits tax based on the assumption that the tax applies only to production value in excess of $30 per barrel. If the exceptional profits tax is applied to the full value of production, we estimate the 2006 liability for exceptional profits tax would be $190 million.

We currently have 111 million barrels of proved undeveloped reserves in Algeria, the economics of which are sensitive to the exceptional profits tax. We are reviewing whether these reserves remain economic under existing development plans if the exceptional profits tax is applied to the entire production value.

We are not yet in a position to confirm the probable interpretation of the law, but are continuing to monitor further guidance to determine the law’s ultimate application. For additional information seeOther Developments under Item 7 if this Form 10-K.

The oil and gas exploration and production industry is very competitive, and some of our exploration and production competitors have greater financial and other resources than we do.

The oil and gas business is highly competitive in the search for and acquisition of reserves and in the gathering and marketing of oil and gas production. Our competitors include major oil and gas companies,

22

independent oil and gas companies, individual producers, gas marketers and major pipeline companies, as well as participants in other industries supplying energy and fuel to industrial, commercial and individual consumers. Some of our competitors may have greater and more diverse resources upon which to draw than we do. If we are not successful in our competition for oil and gas reserves or in our marketing of production, our financial condition and results of operations may be adversely affected.

Our commodity price risk management and trading activities may prevent us from benefiting fully from price increases and may expose us to other risks.

To the extent that we engage in price risk management activities to endeavor to protect ourselves from commodity price declines, the Company will be prevented from realizing the full benefits of price increases above the levels of the derivative instruments used to manage price risk. In addition, we engage in speculative trading in hydrocarbon commodities, which subjects us to additional risk.

Our drilling activities may not be productive.

Drilling for oil and gas involves numerous risks, including the risk that we will not encounter commercially productive oil or gas reservoirs. The costs of drilling, completing and operating wells are often uncertain, and drilling operations may be curtailed, delayed or canceled as a result of a variety of factors, including:

| | • | | unexpected drilling conditions; |

| | • | | pressure or irregularities in formations; |

| | • | | equipment failures or accidents; |

| | • | | fires, explosions, blow-outs and surface cratering; |

| | • | | marine risks such as capsizing, collisions and hurricanes; |

| | • | | other adverse weather conditions; and |

| | • | | shortages or delays in the delivery of equipment. |

Certain of our future drilling activities may not be successful and, if unsuccessful, this failure could have an adverse effect on our future results of operations and financial condition. While all drilling, whether developmental or exploratory, involves these risks, exploratory drilling involves greater risks of dry holes or failure to find commercial quantities of hydrocarbons. Because of the percentage of our capital budget devoted to higher-risk exploratory projects, it is likely that we will continue to experience significant exploration and dry hole expenses.

We are vulnerable to risks associated with operating in the Gulf of Mexico that could negatively impact our operations and financial results.

Our operations and financial results could be significantly impacted by conditions in the Gulf of Mexico because we explore and produce extensively in that area. As a result of this activity, we are vulnerable to the risks associated with operating in the Gulf of Mexico, including those relating to:

| | • | | adverse weather conditions; |

| | • | | oil field service costs and availability; |