EXHIBIT 99.1

PART I

Item 1. Business.

PepsiCo, Inc. was incorporated in Delaware in 1919 and was reincorporated in North Carolina in 1986. When used in this report, the terms “we,” “us,” “our,” “PepsiCo” and the “Company” mean PepsiCo, Inc. and its divisions and subsidiaries.

We are a leading global food, snack and beverage company. Our brands – which include Quaker Oats, Tropicana, Gatorade, Lay’s and Pepsi – are household names that stand for quality throughout the world. As a global company, we also have strong regional brands such as Walkers, Gamesa and Sabritas. Either independently or through contract manufacturers, we make, market and sell a variety of convenient, enjoyable and wholesome foods and beverages in over 200 countries. Our portfolio includes oat, rice and grain-based foods, as well as carbonated and non-carbonated beverages. Our largest operations are in North America (United States and Canada), Mexico, Russia and the United Kingdom.

We are united by our unique commitment to Performance with Purpose, which means delivering sustainable growth by investing in a healthier future for people and our planet. Our goal is to continue to build a balanced portfolio of enjoyable and wholesome foods and beverages, find innovative ways to reduce the use of energy, water and packaging and provide a great workplace for our associates. Additionally, we are committed to respecting, supporting and investing in the local communities where we operate by hiring local people, creating products designed for local tastes and partnering with local farmers, governments and community groups. We make this commitment because we are a responsible company, and a healthier future for all people and our planet means a more successful future for PepsiCo.

In recognition of our continuing sustainability efforts, we were again included on the Dow Jones Sustainability North America Index and the Dow Jones Sustainability World Index in September 2010. These indices are compiled annually.

Our Divisions

We are organized into four business units, as follows:

| | 1. | PepsiCo Americas Foods (PAF), which includes Frito-Lay North America (FLNA), Quaker Foods North America (QFNA) and all of our Latin American food and snack businesses (LAF), including our Sabritas and Gamesa businesses in Mexico; |

| | 2. | PepsiCo Americas Beverages (PAB), which includes PepsiCo Beverages Americas and Pepsi Beverages Company; |

1

| | 3. | PepsiCo Europe, which includes all beverage, food and snack businesses in Europe; and |

| | 4. | PepsiCo Asia, Middle East and Africa (AMEA), which includes all beverage, food and snack businesses in AMEA. |

Our four business units are comprised of six reportable segments (referred to as divisions), as follows:

See Note 1 to our consolidated financial statements for financial information about our divisions and geographic areas.

Frito-Lay North America

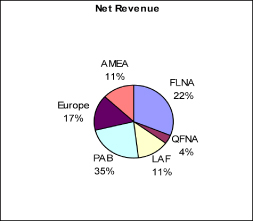

Either independently or through contract manufacturers, FLNA makes, markets, sells and distributes branded snack foods. These foods include Lay’s potato chips, Doritos tortilla chips, Cheetos cheese flavored snacks, Tostitos tortilla chips, branded dips, Ruffles potato chips, Fritos corn chips and SunChips multigrain snacks. FLNA branded products are sold to independent distributors and retailers. In addition, FLNA’s joint venture with Strauss Group makes, markets, sells and distributes Sabra refrigerated dips and spreads. FLNA’s net revenue was $12.6 billion, $12.4 billion and $11.7 billion in 2010, 2009 and 2008, respectively, and approximated 22%, 29% and 27% of our total net revenue in 2010, 2009 and 2008, respectively.

Quaker Foods North America

Either independently or through contract manufacturers, QFNA makes, markets and sells cereals, rice, pasta and other branded products. QFNA’s products include Quaker oatmeal, Aunt Jemima mixes and syrups, Quaker Chewy granola bars, Cap’n Crunch cereal, Quaker grits, Life cereal, Rice-A-Roni, Quaker rice cakes, Pasta Roni and Near East side dishes. These branded products are sold to independent distributors and retailers. QFNA’s net revenue was $2.7 billion in 2010, 2009 and 2008 and approximated 4% of our total net revenue in 2010 and 6% of our total net revenue in both 2009 and 2008.

2

Latin America Foods

Either independently or through contract manufacturers, LAF makes, markets and sells a number of snack food brands including Doritos, Marias Gamesa, Cheetos, Ruffles, Emperador, Saladitas, Sabritas and Lay’s, as well as many Quaker-brand cereals and snacks. These branded products are sold to independent distributors and retailers. LAF’s net revenue was $6.3 billion, $5.7 billion and $5.9 billion in 2010, 2009 and 2008, respectively, and approximated 11%, 13% and 14% of our total net revenue in 2010, 2009 and 2008, respectively.

PepsiCo Americas Beverages

Either independently or through contract manufacturers, PAB makes, markets, sells and distributes beverage concentrates, fountain syrups and finished goods, under various beverage brands including Pepsi, Mountain Dew, Gatorade, 7UP (outside the U.S.), Tropicana Pure Premium, Electropura, Sierra Mist, Epura and Mirinda. PAB also, either independently or through contract manufacturers, makes, markets and sells ready-to-drink tea, coffee and water products through joint ventures with Unilever (under the Lipton brand name) and Starbucks. In addition, PAB licenses the Aquafina water brand to its independent bottlers and markets this brand. Furthermore, PAB manufactures and distributes certain brands licensed from Dr Pepper Snapple Group, Inc. (DPSG), including Dr Pepper and Crush. PAB sells concentrate and finished goods for some of these brands to authorized bottlers, and some of these branded finished goods are sold directly by us to independent distributors and retailers. The bottlers sell our brands as finished goods to independent distributors and retailers. PAB’s net revenue was $20.4 billion, $10.1 billion and $10.9 billion in 2010, 2009 and 2008, respectively, and approximated 35%, 23% and 25% of our total net revenue in 2010, 2009 and 2008, respectively.

See Note 15 for additional information about our acquisitions of The Pepsi Bottling Group, Inc. (PBG) and PepsiAmericas, Inc. (PAS) in 2010.

Europe

Either independently or through contract manufacturers, Europe makes, markets and sells a number of leading snack foods including Lay’s, Walkers, Doritos, Cheetos and Ruffles, as well as many Quaker-brand cereals and snacks, through consolidated businesses as well as through noncontrolled affiliates. Europe also, either independently or through contract manufacturers, makes, markets and sells beverage concentrates, fountain syrups and finished goods under various beverage brands including Pepsi, 7UP and Tropicana. These branded products are sold to authorized bottlers, independent distributors and retailers. In certain markets, however, Europe operates its own bottling plants and distribution facilities. In addition, Europe licenses the Aquafina water brand to certain of its authorized bottlers. Europe also, either independently or through contract manufacturers, makes, markets and sells ready-to-drink tea products through an international joint venture with Unilever (under the Lipton brand name). Europe’s net revenue was $9.6 billion, $7.0 billion and $7.2 billion in 2010, 2009 and 2008,

3

respectively, and approximated 17% our total net revenue in 2010, 2009 and 2008. See Note 15 for additional information about our acquisitions of PBG and PAS in 2010.

Also see “Acquisition of Wimm-Bill-Dann Foods OJSC” below and Note 15 for additional information about our acquisition of Wimm-Bill-Dann Foods OJSC.

Asia, Middle East & Africa

AMEA makes, markets and sells a number of leading snack food brands including Lay’s, Chipsy, Kurkure, Doritos, Cheetos and Smith’s, through consolidated businesses as well as through noncontrolled affiliates. Further, either independently or through contract manufacturers, AMEA makes, markets and sells many Quaker-brand cereals and snacks. AMEA also makes, markets and sells beverage concentrates, fountain syrups and finished goods, under various beverage brands including Pepsi, Mirinda, 7UP and Mountain Dew. These branded products are sold to authorized bottlers, independent distributors and retailers. However, in certain markets, AMEA operates its own bottling plants and distribution facilities. In addition, AMEA licenses the Aquafina water brand to certain of its authorized bottlers. AMEA also, either independently or through contract manufacturers, makes, markets and sells ready-to-drink tea products through an international joint venture with Unilever (under the Lipton brand name). AMEA’s net revenue was $6.3 billion, $5.3 billion and $4.8 billion in 2010, 2009 and 2008, respectively, and approximated 11%, 12% and 11% of our total net revenue in 2010, 2009 and 2008, respectively.

Acquisition of Wimm-Bill-Dann Foods OJSC

On February 3, 2011, we announced that we had completed the previously announced acquisition of ordinary shares, American Depositary Shares, and Global Depositary Shares of Wimm-Bill-Dann Foods OJSC, a company incorporated in the Russian Federation (WBD), which represent in the aggregate approximately 66% of WBD’s outstanding ordinary shares, pursuant to the purchase agreement dated December 1, 2010 between PepsiCo and certain selling shareholders of WBD for approximately $3.8 billion. The acquisition increased PepsiCo’s total ownership of WBD to approximately 77%. See Note 15 for additional information about our acquisition of WBD.

Our Distribution Network

Our products are brought to market through direct-store-delivery (DSD), customer warehouse and foodservice and vending distribution networks. The distribution system used depends on customer needs, product characteristics and local trade practices. These distribution systems are described under the heading “Our Distribution Network” contained in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

4

Ingredients and Other Supplies

The principal ingredients we use in our food and beverage businesses are apple and pineapple juice and other juice concentrates, aspartame, corn, corn sweeteners, flavorings, flour, grapefruits and other fruits, oats, oranges, potatoes, rice, seasonings, sucralose, sugar, vegetable and essential oils and wheat. Our key packaging materials include plastic resins, including polyethylene terephthalate (PET) and polypropylene resins used for plastic beverage bottles and film packaging used for snack foods, aluminum used for cans, glass bottles, closures, cardboard and paperboard cartons. Fuel and natural gas are also important commodities due to their use in our plants and in the trucks delivering our products. These ingredients, raw materials and commodities are purchased mainly in the open market. We employ specialists to secure adequate supplies of many of these items and have not experienced any significant continuous shortages. The prices we pay for such items are subject to fluctuation. When prices increase, we may or may not pass on such increases to our customers. See Note 10 to our consolidated financial statements for additional information on how we manage our exposure to commodity costs.

Our Brands

We own numerous valuable trademarks which are essential to our worldwide businesses, including Alegro, Amp Energy, Aquafina, Aunt Jemima, Cap’n Crunch, Cheetos, Chester’s, Chipsy, Cracker Jack, Diet Pepsi, Doritos, Duyvis, Emperador, Frito-Lay, Fritos, Fruktovy Sad, Frustyle, Gamesa, Gatorade, G2, G Series, Grandma’s, Izze, Kurkure, Lay’s, Life, Manzanita Sol, Marias Gamesa, Matutano, Mirinda, Miss Vickie’s, Mother’s, Mountain Dew, Mug, Munchies, Naked, Near East, Paso de los Toros, Pasta Roni, Pepsi, Pepsi Max, Pepsi One, Propel, Quaker, Quaker Chewy, Quakes, Red Rock Deli, Rice-A-Roni, Rold Gold, Ruffles, Sabritas, Saladitas, Sakata, Sandora, 7UP and Diet 7UP (outside the United States), Santitas, Sierra Mist, Simba, Smartfood, Smith’s, Snack a Jacks, SoBe, SoBe Lifewater, Sonric’s, Stacy’s, SunChips, Tonus, Tostitos, Trop 50, Tropicana, Tropicana Pure Premium, Tropicana Twister, V Water, Walkers and Ya. We also hold long-term licenses to use valuable trademarks in connection with our products, including Dole and Ocean Spray. Joint ventures in which we participate either own or have the right to use certain trademarks, such as Lipton, Starbucks and Sabra. Trademarks remain valid so long as they are used properly for identification purposes, and we emphasize correct use of our trademarks. We have authorized, through licensing arrangements, the use of many of our trademarks in such contexts as snack food joint ventures and beverage bottling appointments. In addition, we license the use of our trademarks on promotional items for the primary purpose of enhancing brand awareness.

We either own or have licenses to use a number of patents which relate to some of our products, their packaging, the processes for their production and the design and operation of various equipment used in our businesses. Some of these patents are licensed to others.

5

Seasonality

Our beverage and food divisions are subject to seasonal variations. Our beverage sales are higher during the warmer months and certain food sales are higher in the cooler months. Weekly beverage and snack sales are generally highest in the third quarter due to seasonal and holiday-related patterns, and generally lowest in the first quarter. However, taken as a whole, seasonality does not have a material impact on our business.

Our Customers

Our primary customers include wholesale distributors, grocery stores, convenience stores, mass merchandisers, membership stores, authorized independent bottlers and foodservice distributors, including hotels and restaurants. We normally grant our independent bottlers exclusive contracts to sell and manufacture certain beverage products bearing our trademarks within a specific geographic area. These arrangements provide us with the right to charge our independent bottlers for concentrate, finished goods and Aquafina royalties and specify the manufacturing process required for product quality.

Retail consolidation and the current economic environment continue to increase the importance of major customers. In 2010, sales to Wal-Mart Stores, Inc. (Wal-Mart), including Sam’s Club (Sam’s), represented approximately 12% of our total net revenue. Our top five retail customers represented approximately 31% of our 2010 North American net revenue, with Wal-Mart (including Sam’s) representing approximately 18%. These percentages include concentrate sales to our independent bottlers (including concentrate sales to PBG and PAS prior to the February 26, 2010 acquisition date) which were used in finished goods sold by them to these retailers. See “Our Customers” and “Our Related Party Bottlers” contained in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 8 to our consolidated financial statements for more information on our customers, including our independent bottlers and Note 15 to our consolidated financial statements for additional information about acquisitions of PBG and PAS in 2010.

Our Competition

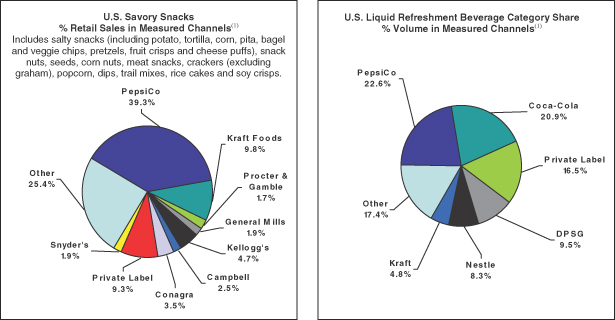

Our businesses operate in highly competitive markets. We compete against global, regional, local and private label manufacturers on the basis of price, quality, product variety and distribution. In U.S. measured channels, our chief beverage competitor, The Coca-Cola Company, has a larger share of CSD (carbonated soft drinks) consumption, while we have a larger share of liquid refreshment beverages consumption. In addition, The Coca-Cola Company has a significant CSD share advantage in many markets outside the United States. Further, our snack brands hold significant leadership positions in the snack industry worldwide. Our snack brands face local, regional and private label competitors, as well as national and global snack competitors, and compete on the basis of price, quality, product variety and distribution. Success in this competitive environment is dependent on effective promotion of existing products, the introduction of new products and the effectiveness of our advertising campaigns, marketing programs and product packaging. We believe that the strength of our brands, innovation and

6

marketing, coupled with the quality of our products and flexibility of our distribution network, allow us to compete effectively.

| (1) | The categories and category share information in the charts above are as of December 2010 and are defined by the following source of the information: Information Resources, Inc. The above charts exclude data from certain customers such as Wal-Mart that do not report data to this service. |

Research and Development

We engage in a variety of research and development activities and continue to invest to accelerate growth in these activities. These activities principally involve the development of new products and improvement in the quality of existing products. In 2010, we created our Global Nutrition Group, led by our Chief Scientific Officer, charged with collaborating with each of our divisions to grow our nutrition portfolio by focusing on four target platforms: fruits and vegetables, grains, dairy and functional nutrition. We also expanded our portfolio of products made with all-natural ingredients, increased the amount of whole grains, fruits, vegetables, nuts, seeds and low-fat dairy in certain of our products and took steps to reduce the average amount of sodium, saturated fat and added sugar per serving in certain of our products. We entered into a long-term collaboration agreement with Senomyx, Inc., a leading company focused on proprietary technologies, to discover and develop sweet enhancers and natural high-potency sweeteners with the intent to bring to the marketplace lower-calorie, great tasting PepsiCo beverages. We invested in agricultural development and the development and implementation of new technologies to both enhance the quality and value of current and proposed product lines and to minimize our impact on the environment, including by building facilities that conserve energy and raw materials and reduce waste and by reviewing our packaging process to continue to reduce total packaging volume, recycle containers, use renewable resources and remove environmentally sensitive materials. Consumer research is

7

excluded from research and development costs and included in other marketing costs. Research and development costs were $488 million in 2010, $414 million in 2009 and $388 million in 2008 and are reported within selling, general and administrative expenses.

Regulatory Environment and Environmental Compliance

The conduct of our businesses, and the production, distribution, sale, advertising, labeling, safety, transportation and use of many of our products, are subject to various laws and regulations administered by federal, state and local governmental agencies in the United States, as well as to foreign laws and regulations administered by government entities and agencies in markets where we operate. It is our policy to abide by the laws and regulations around the world that apply to our businesses.

In the United States, we are required to comply with federal laws, such as the Food, Drug and Cosmetic Act, the Occupational Safety and Health Act, the Clean Air Act, the Clean Water Act, the Resource Conservation and Recovery Act, the Federal Motor Carrier Safety Act, The Foreign Corrupt Practices Act, laws governing equal employment opportunity, customs and foreign trade laws and regulations, laws regulating the sales of products in schools, and various other federal statutes and regulations. We are also subject to various state and local statutes and regulations, including California Proposition 65 which requires that a specific warning appear on any product that contains a component listed by the State of California as having been found to cause cancer or birth defects. Many food and beverage producers who sell products in California, including PepsiCo, may be required to provide warning labels on their products. See also “Changes in the legal and regulatory environment could limit our business activities, increase our operating costs, reduce demand for our products or result in litigation” in “Risk Factors” in Item 1A. of our Annual Report on Form 10-K for the fiscal year ended December 25, 2010 (2010 Form 10-K). Outside the United States, we are subject to numerous similar and other laws and regulations, including anti-corruption laws and regulations. In addition, in many jurisdictions, compliance with competition laws is of special importance to us due to our competitive position in those jurisdictions. We rely on legal and operational compliance programs, as well as local in-house and outside counsel, to guide our businesses in complying with applicable laws and regulations of the countries in which we do business.

Legislation has been enacted in certain U.S. states and in certain of the countries in which our products are sold that requires collection and recycling of containers or that prohibits the sale of our beverages in certain non-refillable containers unless a deposit or other fee is charged. It is possible that similar or more restrictive legal requirements may be proposed or enacted in the future. In addition, proposals have been introduced in certain jurisdictions in which we operate which would impose special taxes on products we sell. For example, various federal, state and local government officials have raised the possibility of taxing the sale of certain “sugared” beverages, including non-diet soft drinks, fruit drinks, teas and flavored waters, to help pay for the cost of certain government programs.

8

The cost of compliance with U.S. and foreign laws does not have a material financial impact on our operations.

We are also subject to national and local environmental laws in the United States and in foreign countries in which we do business, including laws related to water consumption and treatment, wastewater and air emissions, handling and disposal of waters, and, in the United States, the Comprehensive Environmental Response, Compensation and Liability Act, the Resource Conservation and Recovery Act and other federal and state laws regarding handling, release and disposal of wastes at on-site and off-site locations. We are committed to meeting all applicable environmental compliance requirements. We and our subsidiaries are subject to environmental remediation obligations in the normal course of business, as well as remediation and related indemnification obligations in connection with certain historical activities and contractual obligations of businesses acquired by our subsidiaries. While neither the results of these proceedings nor any indemnification obligations or other liabilities of our subsidiaries in connection therewith can be predicted with certainty, environmental compliance costs have not had, and are not expected to have, a material impact on our capital expenditures, earnings or competitive position. See also “Changes in the legal and regulatory environment could limit our business activities, increase our operating costs, reduce demand for our products or result in litigation” in “Risk Factors” in Item 1A. of our 2010 Form 10-K.

Employees

As of December 25, 2010, we employed approximately 294,000 people worldwide, including approximately 108,000 people within the United States. Our employment levels are subject to seasonal variations. We or our subsidiaries are a party to numerous collective bargaining agreements. We expect that we will be able to renegotiate these collective bargaining agreements on satisfactory terms when they expire. We believe that relations with our employees are generally good.

Available Information

We are required to file annual, quarterly and current reports, proxy statements and other information with the U.S. Securities and Exchange Commission (SEC). The public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC athttp://www.sec.gov.

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, are also available free of charge on our Internet site athttp://www.pepsico.com as soon as reasonably practicable after such reports are electronically filed with or furnished to the SEC. The information on our

9

website is not, and shall not be deemed to be, a part hereof or incorporated into this or any of our other filings with the SEC.

10

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

| | | | |

OUR BUSINESS | | | | |

Executive Overview | | | 13 | |

Our Operations | | | 16 | |

Our Customers | | | 18 | |

Our Distribution Network | | | 19 | |

Our Competition | | | 20 | |

Other Relationships | | | 20 | |

Our Business Risks | | | 21 | |

OUR CRITICAL ACCOUNTING POLICIES | | | | |

Revenue Recognition | | | 24 | |

Goodwill and Other Intangible Assets | | | 25 | |

Income Tax Expense and Accruals | | | 27 | |

Pension and Retiree Medical Plans | | | 28 | |

OUR FINANCIAL RESULTS | | | | |

Items Affecting Comparability | | | 32 | |

Results of Operations – Consolidated Review | | | 35 | |

Results of Operations – Division Review | | | 40 | |

Frito-Lay North America | | | 42 | |

Quaker Foods North America | | | 43 | |

Latin America Foods | | | 44 | |

PepsiCo Americas Beverages | | | 45 | |

Europe | | | 46 | |

Asia, Middle East & Africa | | | 48 | |

Our Liquidity and Capital Resources | | | 49 | |

11

| | | | |

Consolidated Statement of Income | | | 53 | |

Consolidated Statement of Cash Flows | | | 54 | |

Consolidated Balance Sheet | | | 56 | |

Consolidated Statement of Equity | | | 57 | |

Notes to Consolidated Financial Statements | | | | |

Note 1 – Basis of Presentation and Our Divisions | | | 59 | |

Note 2 – Our Significant Accounting Policies | | | 65 | |

Note 3 – Restructuring, Impairment and Integration Charges | | | 68 | |

Note 4 – Property, Plant and Equipment and Intangible Assets | | | 71 | |

Note 5 – Income Taxes | | | 73 | |

Note 6 – Stock-Based Compensation | | | 76 | |

Note 7 – Pension, Retiree Medical and Savings Plans | | | 78 | |

Note 8 – Noncontrolled Bottling Affiliates | | | 86 | |

Note 9 – Debt Obligations and Commitments | | | 89 | |

Note 10 – Financial Instruments | | | 91 | |

Note 11 – Net Income Attributable to PepsiCo per Common Share | | | 95 | |

Note 12 – Preferred Stock | | | 96 | |

Note 13 – Accumulated Other Comprehensive Loss Attributable to PepsiCo | | | 97 | |

Note 14 – Supplemental Financial Information | | | 98 | |

Note 15 – Acquisitions | | | 99 | |

MANAGEMENT’S RESPONSIBILITY FOR FINANCIAL REPORTING | | | 105 | |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | | 107 | |

SELECTED FINANCIAL DATA | | | 108 | |

FIVE-YEAR SUMMARY | | | 110 | |

GLOSSARY | | | 112 | |

12

Our discussion and analysis is an integral part of our consolidated financial statements and is provided as an addition to, and should be read in connection with, our consolidated financial statements and the accompanying notes. Definitions of key terms can be found in the glossary beginning on page 112. Tabular dollars are presented in millions, except per share amounts. All per share amounts reflect common per share amounts, assume dilution unless noted, and are based on unrounded amounts. Percentage changes are based on unrounded amounts.

OUR BUSINESS

Executive Overview

We are a leading global food, snack and beverage company. Our brands – which include Quaker Oats, Tropicana, Gatorade, Lay’s and Pepsi – are household names that stand for quality throughout the world. As a global company, we also have strong regional brands such as Walkers, Gamesa and Sabritas. Either independently or through contract manufacturers, we make, market and sell a variety of convenient, enjoyable and wholesome foods and beverages in over 200 countries. Our portfolio includes oat, rice and grain-based foods, as well as carbonated and non-carbonated beverages. Our largest operations are in North America (United States and Canada), Mexico, Russia and the United Kingdom. Additional information concerning our divisions and geographic areas is presented in Note 1.

We are united by our unique commitment to Performance with Purpose, which means delivering sustainable growth by investing in a healthier future for people and our planet. Our goal is to continue to build a balanced portfolio of enjoyable and wholesome foods and beverages, find innovative ways to reduce the use of energy, water and packaging and provide a great workplace for our associates. Additionally, we are committed to respecting, supporting and investing in the local communities where we operate by hiring local people, creating products designed for local tastes and partnering with local farmers, governments and community groups. We make this commitment because we are a responsible company and a healthier future for all people and our planet means a more successful future for PepsiCo.

In recognition of our continuing sustainability efforts, we were again included on the Dow Jones Sustainability North America Index and the Dow Jones Sustainability World Index in September 2010. These indices are compiled annually.

Our management monitors a variety of key indicators to evaluate our business results and financial conditions. These indicators include market share, volume, net revenue, operating profit, management operating cash flow, earnings per share and return on invested capital.

13

Strategies to Drive Our Growth into the Future

We remain focused on growing our business with the objectives of improving our financial results and increasing returns for our shareholders. We continue to focus on delivering strong financial performance in both the near term and the long term, while making global investments in key regions and targeted product categories to drive sustainable growth. We have identified six key challenges and related strategic business imperatives that we believe will enable us to drive growth into the future:

Build and extend our macro snack portfolio

Our first imperative is to build and extend our macro snack portfolio. Building and extending our profitable macro snacks business is important to our future. PepsiCo is the largest player in the macro snack category, and we believe there is still room for growth. Our goal in the macro snacks business is to grow our core salty snack brands that are loved and respected around the world, while expanding into adjacent categories like crackers, bread bites and baked snacks. We will work to continue to grow our portfolio from Fun-for-You to Better-for-You products—while adding many Good-for-You products that are designed to meet growing global demand for wholesome and convenient nutrition. We will also strive to create new flavors in tune with local tastes, which reflect local culture and traditions. We believe that by doing so, we will position ourselves to gain share, while continuing to grow the top- and bottom-line in our macro snack business.

Sustainably and profitably grow our beverage business worldwide

Our second imperative is to sustainably and profitably grow our beverage business worldwide. The U.S. liquid refreshment beverage category and challenging economic conditions facing consumers continue to place pressure on our beverage business worldwide. In the face of this pressure, we continue to take action to ensure sustainable profitable growth in our beverage business worldwide. In 2010, we revitalized both the Gatorade brand and the no-calorie carbonated category by promoting Pepsi Max. Our focus in 2011 will be on taking our North American beverage business and growing it sustainably for the future, while continuing to invest in emerging and developing markets—including the vital China and India markets.

Unleash the power of the Power of One to provide better value for our customers

Our third imperative is to unleash the power of the Power of One to provide better value for customers. We must maintain mutually beneficial relationships with our customers to effectively compete. We are a leader in two extraordinary consumer categories that have special relevance to our customers across the globe. Our snacks and beverages are both high-velocity categories; both generate retail traffic; both are profitable; and both deliver strong cash flow. Studies show that 85 percent of the time, when a person eats a snack, he or she also reaches for a beverage. To realize the value of Power of One in 2010, we successfully completed our bottling acquisitions, which enabled us to better service our customers. We also continued, with a critical mass of SAP implementations, to

14

standardize processes, improve organizational alignment and benchmark performance. In 2011, we are re-focusing our efforts with a systematic approach to unlock the Power of One across the entire value chain. We believe the opportunities in the U.S., in particular, are vast. We will work to make Power of One changes at every level: from the way our products reach our customers; to how our products are displayed; to the channels through which our products are marketed and advertised.

Build and expand our nutrition business

Our fourth imperative is to build and expand our nutrition business and our global nutrition initiatives, to rapidly grow our Good-for-You portfolio of products—both organically and through strategic tuck-in acquisitions. Consumer tastes and preferences are constantly changing and our success depends on our ability to respond to consumer trends, including responding to consumers’ desire for healthier choices. Our basic belief is that companies succeed when society succeeds, and what is good for the world should be good for business. This includes encouraging people to live healthier lives by offering a portfolio of both enjoyable and wholesome foods and beverages. With the acquisition of Wimm-Bill-Dann Foods OJSC (WBD), PepsiCo’s annual revenues from nutritious and functional foods are expected to rise from $10 billion to nearly $13 billion. We also are expanding our portfolio of products made with all-natural ingredients, increasing the amount of whole grains, fruits, vegetables, nuts, seeds and low-fat dairy in certain of our products and taking steps to reduce the average amount of sodium, saturated fat and added sugar per serving in certain of our products.

Cherish our PepsiCo associates

Our fifth imperative is to cherish our PepsiCo associates. Our continued growth requires us to hire, retain and develop our leadership bench. We are fortunate to employ, worldwide, a truly remarkable set of associates. The market becomes more competitive every day and innovation is the key to success. It is people who hold that key and to be a good employer is one of the most important strategic decisions a company has to make.

Achieve excellent performance

Our sixth and final imperative is the sum total of the other five. Our continued success requires that we do everything we can to position ourselves to achieve excellent performance in each of the areas mentioned above. By focusing on the five key challenges and related strategic business imperatives discussed above, we believe we can achieve this goal.

15

Our Operations

We are organized into four business units, as follows:

| | 1) | PepsiCo Americas Foods (PAF), which includes Frito-Lay North America (FLNA), Quaker Foods North America (QFNA) and all of our Latin American food and snack businesses (LAF), including our Sabritas and Gamesa businesses in Mexico; |

| | 2) | PepsiCo Americas Beverages (PAB), which includes PepsiCo Beverages Americas and Pepsi Beverages Company; |

| | 3) | PepsiCo Europe, which includes all beverage, food and snack businesses in Europe; and |

| | 4) | PepsiCo Asia, Middle East and Africa (AMEA), which includes all beverage, food and snack businesses in AMEA. |

Our four business units are comprised of six reportable segments (referred to as divisions), as follows:

Frito-Lay North America

Either independently or through contract manufacturers, FLNA makes, markets, sells and distributes branded snack foods. These foods include Lay’s potato chips, Doritos tortilla chips, Cheetos cheese flavored snacks, Tostitos tortilla chips, branded dips, Ruffles potato chips, Fritos corn chips and SunChips multigrain snacks. FLNA branded products are sold to independent distributors and retailers. In addition, FLNA’s joint venture with Strauss Group makes, markets, sells and distributes Sabra refrigerated dips and spreads.

Quaker Foods North America

Either independently or through contract manufacturers, QFNA makes, markets and sells cereals, rice, pasta and other branded products. QFNA’s products include Quaker oatmeal, Aunt Jemima mixes and syrups, Quaker Chewy granola bars, Cap’n Crunch cereal, Quaker grits, Life cereal, Rice-A-Roni, Quaker rice cakes, Pasta Roni and Near East side dishes. These branded products are sold to independent distributors and retailers.

16

Latin America Foods

Either independently or through contract manufacturers, LAF makes, markets and sells a number of snack food brands including Doritos, Marias Gamesa, Cheetos, Ruffles, Emperador, Saladitas, Sabritas and Lay’s, as well as many Quaker-brand cereals and snacks. These branded products are sold to independent distributors and retailers.

PepsiCo Americas Beverages

Either independently or through contract manufacturers, PAB makes, markets, sells and distributes beverage concentrates, fountain syrups and finished goods, under various beverage brands including Pepsi, Mountain Dew, Gatorade, 7UP (outside the U.S.), Tropicana Pure Premium, Electropura, Sierra Mist, Epura and Mirinda. PAB also, either independently or through contract manufacturers, makes, markets and sells ready-to-drink tea, coffee and water products through joint ventures with Unilever (under the Lipton brand name) and Starbucks. In addition, PAB licenses the Aquafina water brand to its independent bottlers and markets this brand. Furthermore, PAB manufactures and distributes certain brands licensed from Dr Pepper Snapple Group, Inc. (DPSG), including Dr Pepper and Crush. PAB sells concentrate and finished goods for some of these brands to authorized bottlers, and some of these branded finished goods are sold directly by us to independent distributors and retailers. The bottlers sell our brands as finished goods to independent distributors and retailers. PAB’s volume reflects sales to its independent distributors and retailers, as well as the sales of beverages bearing our trademarks that bottlers have reported as sold to independent distributors and retailers. BCS and CSE are not necessarily equal during any given period due to seasonality, timing of product launches, product mix, bottler inventory practices and other factors. However, the difference between BCS and CSE measures has been greatly reduced since our acquisitions of our anchor bottlers, PBG and PAS, on February 26, 2010, as we now consolidate these bottlers and thus eliminate the impact of differences between BCS and CSE for a substantial majority of PAB’s total volume. While our revenues are not entirely based on BCS volume, as there continue to be independent bottlers in the supply chain, we believe that BCS is a valuable measure as it quantifies the sell-through of our products at the consumer level.

See Note 15 for additional information about our acquisitions of PBG and PAS in 2010.

Europe

Either independently or through contract manufacturers, Europe makes, markets and sells a number of leading snack foods including Lay’s, Walkers, Doritos, Cheetos and Ruffles, as well as many Quaker-brand cereals and snacks, through consolidated businesses as well as through noncontrolled affiliates. Europe also, either independently or through contract manufacturers, makes, markets and sells beverage concentrates, fountain syrups and finished goods under various beverage brands including Pepsi, 7UP and Tropicana. These branded products are sold to authorized bottlers, independent distributors and retailers. In certain markets, however, Europe operates its own bottling plants and distribution facilities. In addition, Europe licenses the Aquafina water brand to certain of

17

its authorized bottlers. Europe also, either independently or through contract manufacturers, makes, markets and sells ready-to-drink tea products through an international joint venture with Unilever (under the Lipton brand name).

Europe reports two measures of volume. Snacks volume is reported on a system-wide basis, which includes our own sales and the sales by our noncontrolled affiliates of snacks bearing Company-owned or licensed trademarks. Beverage volume reflects Company-owned or authorized bottler sales of beverages bearing Company-owned or licensed trademarks to independent distributors and retailers (see PepsiCo Americas Beverages above).

See “Acquisition of Wimm-Bill-Dann Foods OJSC” in “Business” in Item 1. and Note 15 for additional information about our acquisitions of PBG and PAS in 2010 and our acquisition of WBD.

Asia, Middle East & Africa

AMEA makes, markets and sells a number of leading snack food brands including Lay’s, Chipsy, Kurkure, Doritos, Cheetos and Smith’s, through consolidated businesses as well as through noncontrolled affiliates. Further, either independently or through contract manufacturers, AMEA makes, markets and sells many Quaker-brand cereals and snacks. AMEA also makes, markets and sells beverage concentrates, fountain syrups and finished goods, under various beverage brands including Pepsi, Mirinda, 7UP and Mountain Dew. These branded products are sold to authorized bottlers, independent distributors and retailers. However, in certain markets, AMEA operates its own bottling plants and distribution facilities. In addition, AMEA licenses the Aquafina water brand to certain of its authorized bottlers. AMEA also, either independently or through contract manufacturers, makes, markets and sells ready-to-drink tea products through an international joint venture with Unilever (under the Lipton brand name). AMEA reports two measures of volume (see Europe above).

Our Customers

Our primary customers include wholesale distributors, grocery stores, convenience stores, mass merchandisers, membership stores, authorized independent bottlers and foodservice distributors, including hotels and restaurants. We normally grant our independent bottlers exclusive contracts to sell and manufacture certain beverage products bearing our trademarks within a specific geographic area. These arrangements provide us with the right to charge our independent bottlers for concentrate, finished goods and Aquafina royalties and specify the manufacturing process required for product quality.

Since we do not sell directly to the consumer, we rely on and provide financial incentives to our customers to assist in the distribution and promotion of our products. For our independent distributors and retailers, these incentives include volume-based rebates, product placement fees, promotions and displays. For our independent bottlers, these incentives are referred to as bottler funding and are negotiated annually with each bottler to support a variety of trade and consumer programs, such as consumer incentives,

18

advertising support, new product support, and vending and cooler equipment placement. Consumer incentives include coupons, pricing discounts and promotions, and other promotional offers. Advertising support is directed at advertising programs and supporting independent bottler media. New product support includes targeted consumer and retailer incentives and direct marketplace support, such as point-of-purchase materials, product placement fees, media and advertising. Vending and cooler equipment placement programs support the acquisition and placement of vending machines and cooler equipment. The nature and type of programs vary annually.

Retail consolidation and the current economic environment continue to increase the importance of major customers. In 2010, sales to Wal-Mart (including Sam’s) represented approximately 12% of our total net revenue. Our top five retail customers represented approximately 31% of our 2010 North American net revenue, with Wal-Mart (including Sam’s) representing approximately 18%. These percentages include concentrate sales to our independent bottlers (including concentrate sales to PBG and PAS prior to the February 26, 2010 acquisition date) which were used in finished goods sold by them to these retailers.

See Note 15 for additional information about our acquisitions of PBG and PAS in 2010.

Our Related Party Bottlers

Prior to our acquisitions of PBG and PAS on February 26, 2010, we had noncontrolling interests in these bottlers. Because our ownership was less than 50%, and since we did not control these bottlers, we did not consolidate their results. Instead, we included our share of their net income based on our percentage of economic ownership in our income statement as bottling equity income. On February 26, 2010, in connection with our acquisitions of PBG and PAS, we began to consolidate the results of these bottlers. Our share of the net income of Pepsi Bottling Ventures LLC (PBV) is reflected in bottling equity income. Our share of income or loss from other noncontrolled affiliates is recorded as a component of selling, general and administrative expenses. See Note 8 for additional information on these related parties and related party commitments and guarantees.

Our Distribution Network

Our products are brought to market through DSD, customer warehouse and foodservice and vending distribution networks. The distribution system used depends on customer needs, product characteristics and local trade practices.

Direct-Store-Delivery

We, our independent bottlers and our distributors operate DSD systems that deliver snacks and beverages directly to retail stores where the products are merchandised by our employees or our bottlers.DSD enables us to merchandise with maximum visibility and appeal. DSD is especially well-suited to products that are restocked often and respond to in-store promotion and merchandising.

19

Customer Warehouse

Some of our products are delivered from our manufacturing plants and warehouses to customer warehouses and retail stores. These less costly systems generally work best for products that are less fragile and perishable, have lower turnover, and are less likely to be impulse purchases.

Foodservice and Vending

Our foodservice and vending sales force distributes snacks, foods and beverages to third-party foodservice and vending distributors and operators. Our foodservice and vending sales force also distributes certain beverages through our independent bottlers. This distribution system supplies our products to restaurants, businesses, schools, stadiums and similar locations.

Our Competition

Our businesses operate in highly competitive markets. We compete against global, regional, local and private label manufacturers on the basis of price, quality, product variety and distribution. In U.S. measured channels, our chief beverage competitor, The Coca-Cola Company, has a larger share of CSD consumption, while we have a larger share of liquid refreshment beverages consumption. In addition, The Coca-Cola Company has a significant CSD share advantage in many markets outside the United States. Further, our snack brands hold significant leadership positions in the snack industry worldwide. Our snack brands face local, regional and private label competitors, as well as national and global snack competitors, and compete on the basis of price, quality, product variety and distribution. Success in this competitive environment is dependent on effective promotion of existing products, the introduction of new products and the effectiveness of our advertising campaigns, marketing programs and product packaging. We believe that the strength of our brands, innovation and marketing, coupled with the quality of our products and flexibility of our distribution network, allow us to compete effectively.

Other Relationships

Certain members of our Board of Directors also serve on the boards of certain vendors and customers. Those Board members do not participate in our vendor selection and negotiations nor in our customer negotiations. Our transactions with these vendors and customers are in the normal course of business and are consistent with terms negotiated with other vendors and customers. In addition, certain of our employees serve on the boards of PBV and other affiliated companies and do not receive incremental compensation for their Board services.

20

Our Business Risks

We are subject to risks in the normal course of business. See “Risk Factors” in Item 1A. of our 2010 Form 10-K and “Executive Overview” above and “Market Risks” below for more information about these risks.

Risk Management Framework

The achievement of our strategic and operating objectives will necessarily involve taking risks. Our risk management process is intended to ensure that risks are taken knowingly and purposefully. As such, we leverage an integrated risk management framework to identify, assess, prioritize, manage, monitor and communicate risks across the Company. This framework includes:

| | • | | The PepsiCo Risk Committee (PRC), comprised of a cross-functional, geographically diverse, senior management group which meets regularly to identify, assess, prioritize and address strategic and reputational risks; |

| | • | | Division Risk Committees (DRCs), comprised of cross-functional senior management teams which meet regularly to identify, assess, prioritize and address division-specific operating risks; |

| | • | | PepsiCo’s Risk Management Office, which manages the overall risk management process, provides ongoing guidance, tools and analytical support to the PRC and the DRCs, identifies and assesses potential risks and facilitates ongoing communication between the parties, as well as to PepsiCo’s Audit Committee and Board of Directors; |

| | • | | PepsiCo Corporate Audit, which evaluates the ongoing effectiveness of our key internal controls through periodic audit and review procedures; and |

| | • | | PepsiCo’s Compliance Department, which leads and coordinates our compliance policies and practices. |

Market Risks

We are exposed to market risks arising from adverse changes in:

| | • | | commodity prices, affecting the cost of our raw materials and energy; |

| | • | | foreign exchange rates; and |

In the normal course of business, we manage these risks through a variety of strategies, including productivity initiatives, global purchasing programs and hedging strategies. Ongoing productivity initiatives involve the identification and effective implementation of meaningful cost-saving opportunities or efficiencies. Our global purchasing programs include fixed-price purchase orders and pricing agreements. See Note 9 for further information on our non-cancelable purchasing commitments. Our hedging strategies include the use of derivatives. Certain derivatives are designated as either cash flow or fair value hedges and qualify for hedge accounting treatment, while others do not qualify

21

and are marked to market through earnings. Cash flows from derivatives used to manage commodity, foreign exchange or interest risks are classified as operating activities. We do not use derivative instruments for trading or speculative purposes. We perform assessments of our counterparty credit risk regularly, including a review of credit ratings, credit default swap rates and potential nonperformance of the counterparty. Based on our most recent assessment of our counterparty credit risk, we consider this risk to be low. In addition, we enter into derivative contracts with a variety of financial institutions that we believe are creditworthy in order to reduce our concentration of credit risk and generally settle with these financial institutions on a net basis.

The fair value of our derivatives fluctuates based on market rates and prices. The sensitivity of our derivatives to these market fluctuations is discussed below. See Note 10 for further discussion of these derivatives and our hedging policies. See “Our Critical Accounting Policies” for a discussion of the exposure of our pension plan assets and pension and retiree medical liabilities to risks related to market fluctuations.

Inflationary, deflationary and recessionary conditions impacting these market risks also impact the demand for and pricing of our products. See “Risk Factors” in Item 1A. of our 2010 Form 10-K for further discussion.

Commodity Prices

We expect to be able to reduce the impact of volatility in our raw material and energy costs through our hedging strategies and ongoing sourcing initiatives.

Our open commodity derivative contracts that qualify for hedge accounting had a face value of $590 million as of December 25, 2010 and $151 million as of December 26, 2009. These contracts resulted in net unrealized gains of $46 million as of December 25, 2010 and net unrealized losses of $29 million as of December 26, 2009. At the end of 2010, the potential change in fair value of commodity derivative instruments, assuming a 10% decrease in the underlying commodity price, would have decreased our net unrealized gains in 2010 by $64 million.

Our open commodity derivative contracts that do not qualify for hedge accounting had a face value of $266 million as of December 25, 2010 and $231 million as of December 26, 2009. These contracts resulted in net gains of $26 million in 2010 and net losses of $57 million in 2009. At the end of 2010, the potential change in fair value of commodity derivative instruments, assuming a 10% decrease in the underlying commodity price, would have decreased our net gains in 2010 by $29 million.

Foreign Exchange

Financial statements of foreign subsidiaries are translated into U.S. dollars using period-end exchange rates for assets and liabilities and weighted-average exchange rates for revenues and expenses. Adjustments resulting from translating net assets are reported as a separate component of accumulated other comprehensive loss within shareholders’ equity under the caption currency translation adjustment.

22

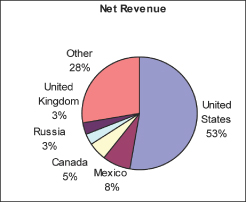

Our operations outside of the U.S. generate over 45% of our net revenue, with Mexico, Canada, Russia and the United Kingdom comprising approximately 20% of our net revenue. As a result, we are exposed to foreign currency risks. During 2010, favorable foreign currency contributed 1 percentage point to net revenue growth, primarily due to appreciation of the Mexican peso, Canadian dollar and Brazilian real, partially offset by depreciation of the Venezuelan bolivar. Currency declines against the U.S. dollar which are not offset could adversely impact our future results.

In addition, we continue to use the official exchange rate to translate the financial statements of our snack and beverage businesses in Venezuela. We use the official rate as we currently intend to remit dividends solely through the government-operated Foreign Exchange Administration Board (CADIVI). As of the beginning of our 2010 fiscal year, the results of our Venezuelan businesses were reported under hyperinflationary accounting. This determination was made based upon Venezuela’s National Consumer Price Index (NCPI) which indicated cumulative inflation in Venezuela in excess of 100% for the three-year period ended November 30, 2009. Consequently, the functional currency of our Venezuelan entities was changed from the bolivar fuerte (bolivar) to the U.S. dollar. Effective January 11, 2010, the Venezuelan government devalued the bolivar by resetting the official exchange rate from 2.15 bolivars per dollar to 4.3 bolivars per dollar; however, certain activities were permitted to access an exchange rate of 2.6 bolivars per dollar. Effective June 2010, the Central Bank of Venezuela began accepting and approving applications, under certain conditions, for non-CADIVI exchange transactions at the weighted-average implicit exchange rate obtained from the Transaction System for Foreign Currency Denominated Securities (SITME). As of December 25, 2010, this rate was 5.3 bolivars per dollar. We continue to use all available options, including CADIVI, SITME and bond auctions, to obtain U.S. dollars to meet our operational needs. In 2010, the majority of our transactions were remeasured at the 4.3 exchange rate, and as a result of the change to hyperinflationary accounting and the devaluation of the bolivar, we recorded a one-time net charge of $120 million in the first quarter of 2010. In 2010, our operations in Venezuela comprised 4% of our cash and cash equivalents balance and generated less than 1% of our net revenue. As of January 1, 2011, the Venezuelan government unified the country’s two official exchange rates (4.3 and 2.6 bolivars per dollar) by eliminating the 2.6 bolivars per dollar rate, which was previously permitted for certain activities. This change did not, nor is expected to, have a material impact on our financial statements.

Exchange rate gains or losses related to foreign currency transactions are recognized as transaction gains or losses in our income statement as incurred. We may enter into derivatives, primarily forward contracts with terms of no more than two years, to manage our exposure to foreign currency transaction risk. Our foreign currency derivatives had a total face value of $1.7 billion as of December 25, 2010 and $1.2 billion as of December 26, 2009. The contracts that qualify for hedge accounting resulted in net unrealized losses of $15 million as of December 25, 2010 and $20 million as of December 26, 2009. At the end of 2010, we estimate that an unfavorable 10% change in the exchange rates would have increased our net unrealized losses by $119 million. The contracts that do not qualify for hedge accounting resulted in net losses of $6 million in 2010 and a net

23

gain of $1 million in 2009. All losses and gains were offset by changes in the underlying hedged items, resulting in no net material impact on earnings.

Interest Rates

We centrally manage our debt and investment portfolios considering investment opportunities and risks, tax consequences and overall financing strategies. We use various interest rate derivative instruments including, but not limited to, interest rate swaps, cross-currency interest rate swaps, Treasury locks and swap locks to manage our overall interest expense and foreign exchange risk. These instruments effectively change the interest rate and currency of specific debt issuances. Certain of our fixed rate indebtedness has been swapped to floating rates. The notional amount, interest payment and maturity date of the interest rate and cross-currency swaps match the principal, interest payment and maturity date of the related debt. Our Treasury locks and swap locks are entered into to protect against unfavorable interest rate changes relating to forecasted debt transactions.

Assuming year-end 2010 variable rate debt and investment levels, a 1-percentage-point increase in interest rates would have increased net interest expense by $43 million in 2010.

OUR CRITICAL ACCOUNTING POLICIES

An appreciation of our critical accounting policies is necessary to understand our financial results. These policies may require management to make difficult and subjective judgments regarding uncertainties, and as a result, such estimates may significantly impact our financial results. The precision of these estimates and the likelihood of future changes depend on a number of underlying variables and a range of possible outcomes. Other than our accounting for pension plans, our critical accounting policies do not involve the choice between alternative methods of accounting. We applied our critical accounting policies and estimation methods consistently in all material respects, and for all periods presented, and have discussed these policies with our Audit Committee.

Our critical accounting policies arise in conjunction with the following:

| | • | | goodwill and other intangible assets; |

| | • | | income tax expense and accruals; and |

| | • | | pension and retiree medical plans. |

Revenue Recognition

Our products are sold for cash or on credit terms. Our credit terms, which are established in accordance with local and industry practices, typically require payment within 30 days of delivery in the U.S., and generally within 30 to 90 days internationally, and may allow discounts for early payment. We recognize revenue upon shipment or delivery to our customers based on written sales terms that do not allow for a right of return. However,

24

our policy for DSD and certain chilled products is to remove and replace damaged and out-of-date products from store shelves to ensure that consumers receive the product quality and freshness they expect. Similarly, our policy for certain warehouse-distributed products is to replace damaged and out-of-date products. Based on our experience with this practice, we have reserved for anticipated damaged and out-of-date products.

Our policy is to provide customers with product when needed. In fact, our commitment to freshness and product dating serves to regulate the quantity of product shipped or delivered. In addition, DSD products are placed on the shelf by our employees with customer shelf space and storerooms limiting the quantity of product. For product delivered through our other distribution networks, we monitor customer inventory levels.

As discussed in “Our Customers,” we offer sales incentives and discounts through various programs to customers and consumers. Sales incentives and discounts are accounted for as a reduction of revenue and totaled $29.1 billion in 2010, $12.9 billion in 2009 and $12.5 billion in 2008. Sales incentives include payments to customers for performing merchandising activities on our behalf, such as payments for in-store displays, payments to gain distribution of new products, payments for shelf space and discounts to promote lower retail prices. A number of our sales incentives, such as bottler funding to independent bottlers and customer volume rebates, are based on annual targets, and accruals are established during the year for the expected payout. These accruals are based on contract terms and our historical experience with similar programs and require management judgment with respect to estimating customer participation and performance levels. Differences between estimated expense and actual incentive costs are normally insignificant and are recognized in earnings in the period such differences are determined. The terms of most of our incentive arrangements do not exceed a year, and therefore do not require highly uncertain long-term estimates. For interim reporting, we estimate total annual sales incentives for most of our programs and record a pro rata share in proportion to revenue. Certain arrangements, such as fountain pouring rights, may extend beyond one year. Payments made to obtain these rights are recognized over the shorter of the economic or contractual life, as a reduction of revenue, and the remaining balances of $296 million, as of both December 25, 2010 and December 26, 2009, are included in current assets and other assets on our balance sheet.

We estimate and reserve for our bad debt exposure based on our experience with past due accounts and collectibility, the aging of accounts receivable and our analysis of customer data. Bad debt expense is classified within selling, general and administrative expenses in our income statement.

Goodwill and Other Intangible Assets

We sell products under a number of brand names, many of which were developed by us. The brand development costs are expensed as incurred. We also purchase brands in acquisitions. Upon acquisition, the purchase price is first allocated to identifiable assets and liabilities, including brands, based on estimated fair value, with any remaining purchase price recorded as goodwill. Determining fair value requires significant estimates and assumptions based on an evaluation of a number of factors, such as

25

marketplace participants, product life cycles, market share, consumer awareness, brand history and future expansion expectations, amount and timing of future cash flows and the discount rate applied to the cash flows.

We believe that a brand has an indefinite life if it has a history of strong revenue and cash flow performance, and we have the intent and ability to support the brand with marketplace spending for the foreseeable future. If these perpetual brand criteria are not met, brands are amortized over their expected useful lives, which generally range from five to 40 years. Determining the expected life of a brand requires management judgment and is based on an evaluation of a number of factors, including market share, consumer awareness, brand history and future expansion expectations, as well as the macroeconomic environment of the countries in which the brand is sold.

Perpetual brands and goodwill, including the goodwill that is part of our noncontrolled bottling investment balances, are not amortized. Perpetual brands and goodwill are assessed for impairment at least annually. If the carrying amount of a perpetual brand exceeds its fair value, as determined by its discounted cash flows, an impairment loss is recognized in an amount equal to that excess. Goodwill is evaluated using a two-step impairment test at the reporting unit level. A reporting unit can be a division or business within a division. The first step compares the book value of a reporting unit, including goodwill, with its fair value, as determined by its discounted cash flows. If the book value of a reporting unit exceeds its fair value, we complete the second step to determine the amount of goodwill impairment loss that we should record. In the second step, we determine an implied fair value of the reporting unit’s goodwill by allocating the fair value of the reporting unit to all of the assets and liabilities other than goodwill (including any unrecognized intangible assets). The amount of impairment loss is equal to the excess of the book value of the goodwill over the implied fair value of that goodwill.

Amortizable brands are only evaluated for impairment upon a significant change in the operating or macroeconomic environment. If an evaluation of the undiscounted future cash flows indicates impairment, the asset is written down to its estimated fair value, which is based on its discounted future cash flows.

In connection with our acquisitions of PBG and PAS, we reacquired certain franchise rights which provided PBG and PAS with the exclusive and perpetual rights to manufacture and/or distribute beverages for sale in specified territories. In determining the useful life of these reacquired franchise rights, we considered many factors including the existing perpetual bottling arrangements, the indefinite period expected for the reacquired rights to contribute to our future cash flows, as well as the lack of any factors that would limit the useful life of the reacquired rights to us, including legal, regulatory, contractual, competitive, economic or other factors. Therefore, certain reacquired franchise rights, as well as perpetual brands and goodwill, will not be amortized, but instead will be tested for impairment at least annually. Certain reacquired and acquired franchise rights are amortizable over the remaining contractual period of the contract in which the right was granted.

26

On December 7, 2009, we reached an agreement with DPSG to manufacture and distribute Dr Pepper and certain other DPSG products in the territories where they were previously sold by PBG and PAS. Under the terms of the agreement, we made an upfront payment of $900 million to DPSG on February 26, 2010. Based upon the terms of the agreement with DPSG, the amount of the upfront payment has been capitalized and will not be amortized, but instead will be tested for impairment at least annually.

Significant management judgment is necessary to evaluate the impact of operating and macroeconomic changes and to estimate future cash flows. Assumptions used in our impairment evaluations, such as forecasted growth rates and our cost of capital, are based on the best available market information and are consistent with our internal forecasts and operating plans. These assumptions could be adversely impacted by certain of the risks discussed in “Risk Factors” in Item 1A. of our 2010 Form 10-K and “Our Business Risks.”

We did not recognize any impairment charges for perpetual brands or goodwill in the years presented. In addition, as of December 25, 2010, we did not have any reporting units that were at risk of failing the first step of the goodwill impairment test. As of December 25, 2010, we had $26.4 billion of perpetual brands and goodwill, of which approximately 65% related to the goodwill and other nonamortizable intangible assets from the acquisitions of PBG and PAS.

Income Tax Expense and Accruals

Our annual tax rate is based on our income, statutory tax rates and tax planning opportunities available to us in the various jurisdictions in which we operate. Significant judgment is required in determining our annual tax rate and in evaluating our tax positions. We establish reserves when, despite our belief that our tax return positions are fully supportable, we believe that certain positions are subject to challenge and that we may not succeed. We adjust these reserves, as well as the related interest, in light of changing facts and circumstances, such as the progress of a tax audit.

An estimated effective tax rate for a year is applied to our quarterly operating results. In the event there is a significant or unusual item recognized in our quarterly operating results, the tax attributable to that item is separately calculated and recorded at the same time as that item. We consider the tax adjustments from the resolution of prior year tax matters to be among such items.

Tax law requires items to be included in our tax returns at different times than the items are reflected in our financial statements. As a result, our annual tax rate reflected in our financial statements is different than that reported in our tax returns (our cash tax rate). Some of these differences are permanent, such as expenses that are not deductible in our tax return, and some differences reverse over time, such as depreciation expense. These temporary differences create deferred tax assets and liabilities. Deferred tax assets generally represent items that can be used as a tax deduction or credit in our tax returns in future years for which we have already recorded the tax benefit in our income statement. We establish valuation allowances for our deferred tax assets if, based on the available evidence, it is more likely than not that some portion or all of the deferred tax assets will

27

not be realized. Deferred tax liabilities generally represent tax expense recognized in our financial statements for which payment has been deferred, or expense for which we have already taken a deduction in our tax return but have not yet recognized as expense in our financial statements.

In 2010, our annual tax rate was 23.0% compared to 26.0% in 2009, as discussed in “Other Consolidated Results.” The tax rate in 2010 decreased 3.0 percentage points primarily reflecting the impact of our acquisitions of PBG and PAS, which includes the reversal of deferred taxes attributable to our previously held equity interests in PBG and PAS, as well as the favorable resolution of certain tax matters in 2010.

Pension and Retiree Medical Plans

Our pension plans cover full-time employees in the U.S. and certain international employees. Benefits are determined based on either years of service or a combination of years of service and earnings. U.S. and Canada retirees are also eligible for medical and life insurance benefits (retiree medical) if they meet age and service requirements. Generally, our share of retiree medical costs is capped at specified dollar amounts which vary based upon years of service, with retirees contributing the remainder of the cost.

See Note 7 for information about certain changes to our U.S. pension and retiree medical plans and changes in connection with our acquisitions of PBG and PAS.

Our Assumptions

The determination of pension and retiree medical plan obligations and related expenses requires the use of assumptions to estimate the amount of benefits that employees earn while working, as well as the present value of those benefits. Annual pension and retiree medical expense amounts are principally based on four components: (1) the value of benefits earned by employees for working during the year (service cost), (2) increase in the liability due to the passage of time (interest cost), and (3) other gains and losses as discussed below, reduced by (4) the expected return on plan assets for our funded plans.

Significant assumptions used to measure our annual pension and retiree medical expense include:

| | • | | the interest rate used to determine the present value of liabilities (discount rate); |

| | • | | certain employee-related factors, such as turnover, retirement age and mortality; |

| | • | | the expected return on assets in our funded plans; |

| | • | | for pension expense, the rate of salary increases for plans where benefits are based on earnings; and |

| | • | | for retiree medical expense, health care cost trend rates. |

Our assumptions reflect our historical experience and management’s best judgment regarding future expectations. Due to the significant management judgment involved, our assumptions could have a material impact on the measurement of our pension and retiree medical benefit expenses and obligations.

28

At each measurement date, the discount rates are based on interest rates for high-quality, long-term corporate debt securities with maturities comparable to those of our liabilities. Our U.S. discount rate is determined using the Mercer Pension Discount Yield Curve (Mercer Yield Curve). The Mercer Yield Curve uses a portfolio of high-quality bonds rated Aa or higher by Moody’s. The Mercer Yield Curve includes bonds that closely match the timing and amount of our expected benefit payments.

The expected return on pension plan assets is based on our pension plan investment strategy, our expectations for long-term rates of return by asset class, taking into account volatilities and correlation among asset classes and our historical experience. We also review current levels of interest rates and inflation to assess the reasonableness of the long-term rates. We evaluate our expected return assumptions annually to ensure that they are reasonable. Our pension plan investment strategy includes the use of actively managed securities and is reviewed annually based upon plan liabilities, an evaluation of market conditions, tolerance for risk and cash requirements for benefit payments. Our investment objective is to ensure that funds are available to meet the plans’ benefit obligations when they become due. Our overall investment strategy is to prudently invest plan assets in a well-diversified portfolio of equity and high-quality debt securities to achieve our long-term return expectations. Our investment policy also permits the use of derivative instruments which are primarily used to reduce risk. Our expected long-term rate of return on U.S. plan assets is 7.8%. Our target investment allocation is 40% for U.S. equity allocations, 20% for international equity allocations and 40% for fixed income allocations. Actual investment allocations may vary from our target investment allocations due to prevailing market conditions. We regularly review our actual investment allocations and periodically rebalance our investments to our target allocations. To calculate the expected return on pension plan assets, we use a market-related valuation method that recognizes investment gains or losses (the difference between the expected and actual return based on the market-related value of assets) for securities included in our equity allocations over a five-year period. This has the effect of reducing year-to-year volatility. For all other asset categories, the actual fair value is used for the market-related value of assets.

The difference between the actual return on plan assets and the expected return on plan assets is added to, or subtracted from, other gains and losses resulting from actual experience differing from our assumptions and from changes in our assumptions determined at each measurement date. If this net accumulated gain or loss exceeds 10% of the greater of the market-related value of plan assets or plan liabilities, a portion of the net gain or loss is included in expense for the following year based upon the average remaining service period of active plan participants, which is approximately 11 years for pension expense and approximately 8 years for retiree medical expense. The cost or benefit of plan changes that increase or decrease benefits for prior employee service (prior service cost/(credit)) is included in earnings on a straight-line basis over the average remaining service period of active plan participants.

The health care trend rate used to determine our retiree medical plan’s liability and expense is reviewed annually. Our review is based on our claim experience, information

29