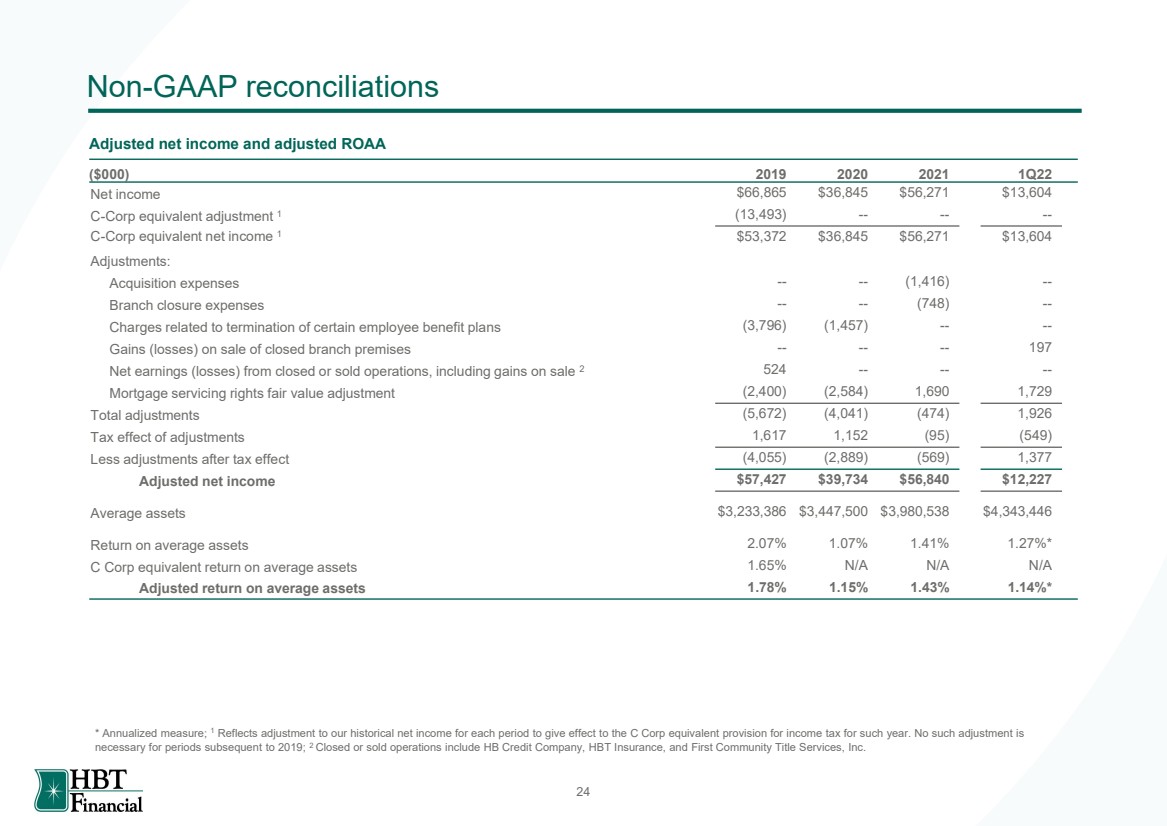

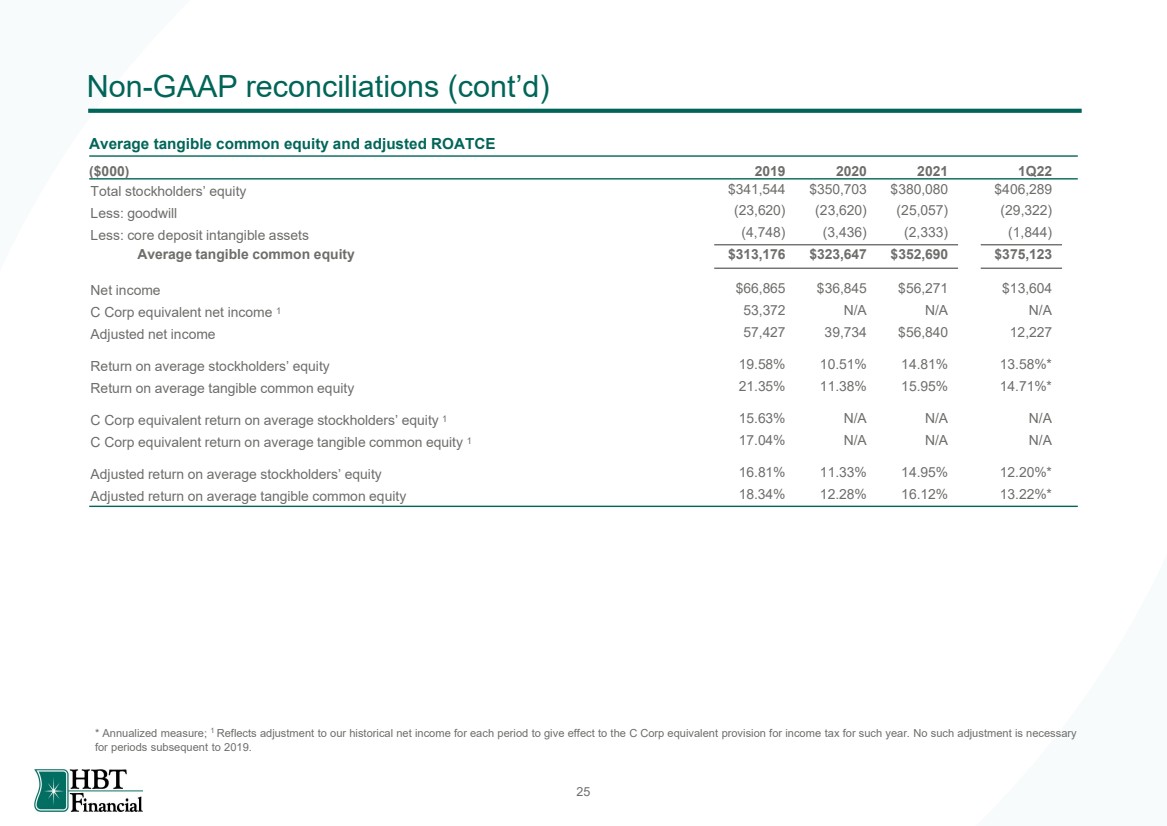

| Forward - Looking Statements Readers should note that in addition to the historical information contained herein, this presentation contains, and future o ral and written statements of the Company and its management may contain, "forward - looking statements" within the meanings of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward - looking statements generally can be identified by the use of forward - lookin g terminology such as "will," "propose," "may," "plan," "seek," "expect," "intend," "estimate," "anticipate," "believe" or "continue," or similar terminology. Any forward - looking statements pr esented herein are made only as of the date of this presentation, and the Company does not undertake any obligation to update or revise any forward - looking statements to reflect changes in assumptions, the occurrence of unanticipated events, or otherwise. Factors that could cause actual results to differ materially from these forward - looking statements include, but are not limited to: ( i ) the strength of the local, state, national and international economies (including effects of inflationary pressures and supply chain constraints); (ii) the economic impact of any future terrorist thr eats and attacks, widespread disease or pandemics (including the COVID - 19 pandemic in the United States), acts of war or other threats thereof, or other adverse external events that could cause econo mic deterioration or instability in credit markets, and the response of the local, state and national governments to any such adverse external events; (iii) changes in accounting policies and practices , a s may be adopted by state and federal regulatory agencies, the FASB or the PCAOB; (iv) changes in state and federal laws, regulations and governmental policies concerning the Company’s general bus iness; (v) changes in interest rates and prepayment rates of the Company’s assets (including the impact of LIBOR phase - out); (vi) increased competition in the financial services sector and the inability to attract new customers; (vii) changes in technology and the ability to develop and maintain secure and reliable electronic systems; (viii) unexpected results of acquisitions, which may inc lude failure to realize the anticipated benefits of acquisitions and the possibility that transaction costs may be greater than anticipated; (ix) the loss of key executives or employees; (x) changes in consumer spending; (xi) unexpected outcomes of existing or new litigation involving the Company; (xii) the economic impact of exceptional weather occurrences such as tornadoes, floods and bli zzards; and (xiii) the ability of the Company to manage the risks associated with the foregoing. Readers should note that the forward - looking statements included in this presentation are not a g uarantee of future events, and that actual events may differ materially from those made in or suggested by the forward - looking statements. Additional information concerning the Company and its busines s, including additional factors that could materially affect the Company’s financial results, is included in the Company’s filings with the Securities and Exchange Commission. Non - GAAP Financial Measures This presentation includes certain non - GAAP financial measures. While HBT Financial, Inc. (“HBT” or the “Company”) believes thes e are useful measures for investors, they are not presented in accordance with GAAP. You should not consider non - GAAP measures in isolation or as a substitute for the most directly comparable or other financial measures calculated in accordance with GAAP. Because not all companies use identical calculations, the presentation herein of non - GAAP financial measures may not be comparab le to other similarly titled measures of other companies. Tax equivalent adjustments assume a federal tax rate of 21% and state tax rate of 9.5% during the three months ended March 31, 20 22, December 31, 2021, September 30, 2021, June 30, 2021, and March 31, 2021, and the years ended December 31, 2021, 2020, 2019 and 2018, and a federal tax rate of 35% and state tax rate of 8.63% for the year ended December 31, 2017. For a reconciliation of the non - GAAP measures we use to the most closely comparable GAAP measures, see the Appendix to this presentati on. 1 |