Filed by Old National Bancorp

Pursuant to Rule 425 under the Securities Act of 1933

Subject Company: United Bancorp, Inc.

Commission File No.: 000-16640

The following excerpts relating to Old National Bancorp’s pending acquisition of United Bancorp, Inc. are from the slide presentation and transcript of a conference call held by executive officers of Old National on February 3, 2014 in connection with Old National’s announcement of its financial results for the quarter and year ended December 31, 2013.

* * *

Additional Information for Shareholders of United Bancorp, Inc.

Communications in this presentation do not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. In connection with the proposed merger, Old National Bancorp (“Old National”) will file with the Securities and Exchange Commission (“SEC”) a Registration Statement on Form S-4 that will include a Proxy Statement of United Bancorp,

Inc. (“United”) and a Prospectus of Old National, as well as other relevant documents concerning the proposed transaction. Shareholders are urged to read the Registration Statement and the Proxy Statement/Prospectus regarding the merger when it becomes available and any other relevant documents filed with the SEC, as well as any amendments or supplements to those documents, because they will contain important information. A free copy of the Proxy Statement/Prospectus, as well as other filings containing information about Old National and United, may be obtained at the

SEC’s Internet site (http://www.sec.gov). You will also be able to obtain these documents, free of charge, from Old National at www.oldnational.com under the tab “Investor Relations” and then under the heading “Financial Information” or from United by accessing United’s website at www.ubat.com under the heading “About Us” and then under the tab “Investor Relations” and then under the tab “SEC Filings.”

Old National and United and certain of their directors and executive officers may be deemed to be participants in the solicitation of proxies from the shareholders of United in connection with the proposed merger. Information about the directors and executive officers of Old National is set forth in the proxy statement for Old National’s 2013 annual meeting of shareholders, as filed with the SEC on a Schedule 14A on March 15, 2013. Information about the directors and executive officers of

United is set forth in the proxy statement for United’s 2013 annual meeting of shareholders, as filed with the SEC on a Schedule 14A on March 25, 2013. Additional information regarding the interests of those participants and other persons who may be deemed participants in the transaction may be obtained by reading the Proxy Statement/Prospectus regarding the proposed merger when it becomes available. Free copies of this document may be obtained as described in the preceding paragraph.

|

5 6

Forward-Looking Statement

This presentation contains certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements include, but are not limited to, descriptions of Old National’s financial condition, results of operations, asset and credit quality trends and profitability and statements about the expected timing, completion, financial benefit and other effects of the proposed mergers with Tower and United. Forward-looking statements can be identified by the use of the words “anticipate,” “believe,” “expect,” “intend,” “could” and “should,” and other words of similar meaning. These forward-looking statements express management’s current expectations or forecasts of future events and, by their nature, are subject to risks and uncertainties and there are a number of factors that could cause actual results to differ materially from those in such statements. Factors that might cause such a difference include, but are not limited to: market, economic, operational, liquidity, credit and interest rate risks associated with Old National’s business; competition; government legislation and policies (including the impact of the Dodd-Frank Wall Street Reform and Consumer Protection Act and its related regulations); ability of Old National to execute its business plan (including the proposed acquisitions of Tower and United); changes in the economy which could materially impact credit quality trends and the ability to generate loans and gather deposits; failure or circumvention of

Old National’s internal controls, failure or disruption of our information systems; failure to adhere to or significant changes in accounting, tax or regulatory practices or requirements; new legal obligations or liabilities or unfavorable resolutions of litigations; other matters discussed in this presentation and other factors identified in the Company’s Annual Report on Form 10-K and other periodic filings with the Securities and Exchange Commission. These forward-looking statements are made only as of the date of this presentation, and Old National undertakes no obligation to release revisions to these forward-looking statements to reflect events or conditions after the date of this presentation.

Lynell Walton, Director of Investor Relations

… And just a few weeks ago we announced our intent to partner with United Bancorp and enter the vibrant market of Ann Arbor, Michigan…

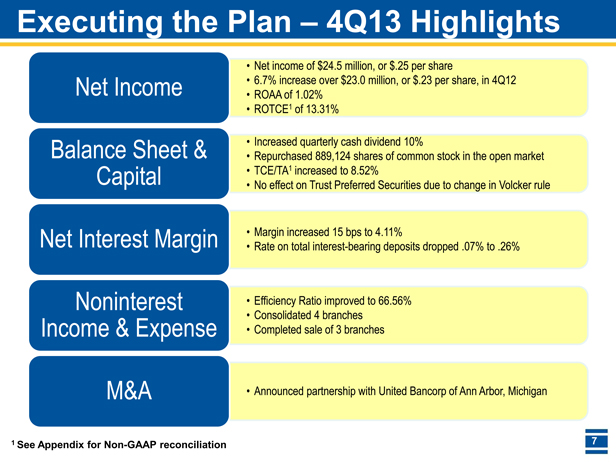

Executing the Plan – 4Q13 Highlights

Net income of $24.5 million, or $.25 per share

Net Income 6.7% increase over $23.0 million, or $.23 per share, in 4Q12

ROAA of 1.02%

ROTCE1 of 13.31%

Balance Sheet & Increased quarterly cash dividend 10%

Repurchased 889,124 shares of common stock in the open market

Capital TCE/TA1 increased to 8.52%

No effect on Trust Preferred Securities due to change in Volcker rule

Net Interest Margin Margin increased 15 bps to 4.11%

Rate on total interest-bearing deposits dropped .07% to .26%

Noninterest Efficiency Ratio improved to 66.56%

Consolidated 4 branches

Income & Expense Completed sale of 3 branches

M&A Announced partnership with United Bancorp of Ann Arbor, Michigan

1 See Appendix for Non-GAAP reconciliation

7

…2013 also saw Old National’s entry into southern Michigan with a branch purchase and of course we have 2 pending partnerships – Tower Financial in Fort Wayne, Indiana and United Bancorp in Ann Arbor, Michigan…

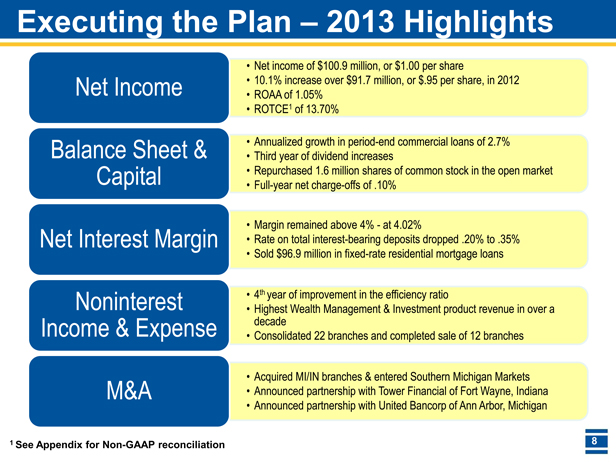

Executing the Plan – 2013 Highlights

Net income of $100.9 million, or $1.00 per share

Net Income 10.1% increase over $91.7 million, or $.95 per share, in 2012

ROAA of 1.05%

ROTCE1 of 13.70%

Balance Sheet & Annualized growth in period-end commercial loans of 2.7%

Third year of dividend increases

Capital Repurchased 1.6 million shares of common stock in the open market

Full-year net charge-offs of .10%

Margin remained above 4% - at 4.02%

Net Interest Margin Rate on total interest-bearing deposits dropped .20% to .35%

Sold $96.9 million in fixed-rate residential mortgage loans

Noninterest 4th year of improvement in the efficiency ratio

Highest Wealth Management & Investment product revenue in over a

Income & Expense decade

Consolidated 22 branches and completed sale of 12 branches

Acquired MI/IN branches & entered Southern Michigan Markets

M&A Announced partnership with Tower Financial of Fort Wayne, Indiana

Announced partnership with United Bancorp of Ann Arbor, Michigan

1 See Appendix for Non-GAAP reconciliation

Christopher A. Wolking, Senior EVP and Chief Financial Officer

…In the fourth quarter, accretion from acquired assets and liabilities accounted for 81 basis points of our net interest margin or $16.8 million. Accretion income should decline as acquired loans mature or are otherwise paid out. We expect somewhat lower accretion income from acquired loans in 2014 with a larger decline in 2015. Since we have not yet closed on either Tower or UBMI, of course, we have not marked these assets to fair value. But, out initial reviews of these portfolios indicate the percentage discount to adjust to fair value will be lower for these portfolios compared to previous acquisitions…

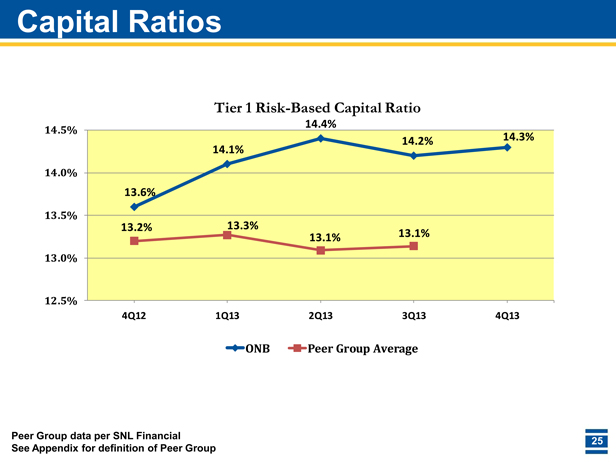

… Our Tier 1 capital ratio continues to track above the average ratio of our peer group – peer banks. Our capital base gives us a latitude to grow organically, acquire additional banks and businesses using cash or continue to return capital to shareholders. We evaluate all of these opportunities constantly and expect to execute capital decisions for the best interest of our shareholders in the long-term. Both, the Tower and UBMI acquisitions, which we expect to close in 2014, include a mix of stock and cash in the purchase consideration...

Net Interest Margin1

4.50% 4.34%

4.04% 4.11%

4.00% 3.97% 3.96%

3.50%

3.00%

2.50%

4Q12 1Q13 2Q13 3Q13 4Q13

IN Community Accretion 0.29% 0.25% 0.29% 0.23% 0.37%

Integra Accretion 0.55% 0.39% 0.32% 0.31% 0.35%

Monroe Accretion 0.10% 0.09% 0.07% 0.09% 0.09%

ONB Core 2 3.40% 3.31% 3.29% 3.33% 3.30%

Earning assets reflect purchased assets, net of discount

1 Fully taxable equivalent basis

2 ONB Core includes contractual interest income of Monroe, Integra and IN Community loans

22

Robert G. Jones, President and Chief Executive Officer

….The target our board has set for managements 2014 incentives is a fourth quarter efficiency ratio of 64.5%. This does represent a slight decline from our fourth quarter incentive efficiency ratio of 63.9%, it is important to note that this does include the negative impact of our Michigan branch purchase, which we estimated approximately $2.3 million for the two quarters we owned them in 2013, nor does that number include the headwinds of the declining accretion income that Chris previously addressed. In addition as part of our normal course of operations, we will be making strategic investments in our technology infrastructure, such as a new teller system and mobile banking, which will ultimately improve our efficiency, but there is an upfront cost. I should note our fourth quarter 2014 target will not include any impact associated with Tower or UBMI…

… Mergers and acquisitions remains a core focus for Old National. With two partnerships currently in the pipeline, we could effectively execute additional partnerships this year, but we will remain diligent in terms of the markets and return to our shareholders…

…United Bank announced their 2013 earnings of $8.8 million, which was slightly better than we had modeled. We held a full three days of introductory meetings after our announcement. On January 29, we kicked off the integration process with our 20 teams. We are very encouraged by both the associate and client reaction to our announcement…

Capital Ratios

Tier 1 Risk-Based Capital Ratio

14 .5% 14.4%

14.2% 14.3%

14.1%

14 .0%

13.6%

13 .5%

13.2% 13.3%

13.1% 13.1%

13 .0%

12 .5%

4Q12 1Q13 2Q13 3Q13 4Q13

ONB Peer Group Average

Peer Group data per SNL Financial See Appendix for definition of Peer Group

25

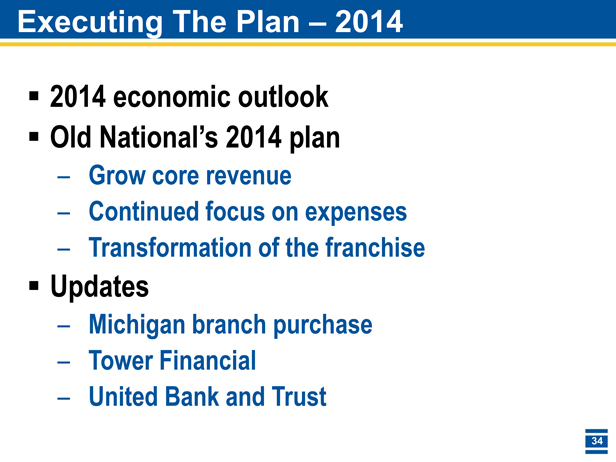

Executing The Plan – 2014

2014 economic outlook

Old National’s 2014 plan

Grow core revenue

Continued focus on expenses Transformation of the franchise

Updates

Michigan branch purchase Tower Financial United Bank and Trust

34

Old National Bancorp

Appendix

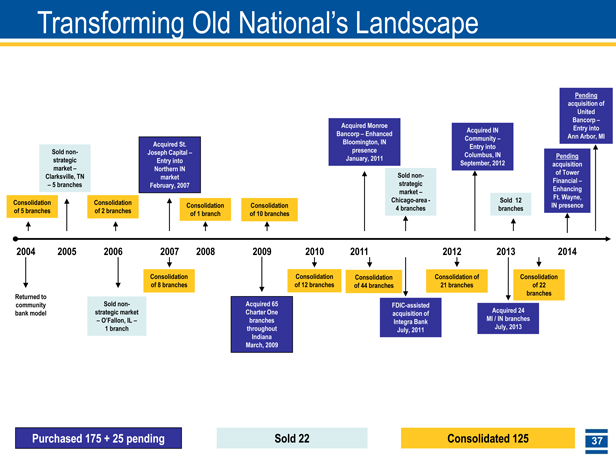

Transforming Old National’s Landscape

Pending

acquisition of

United

Bancorp –

Acquired Monroe Acquired IN Entry into

Bancorp – Enhanced Community – Ann Arbor, MI

Acquired St. Bloomington, IN

Sold non- Joseph Capital – presence Columbus, Entry into IN Pending

strategic Entry into January, 2011 September, 2012 acquisition

market – Northern IN

Clarksville, TN market Sold non- of Tower

– 5 branches February, 2007 strategic Financial –

market – Enhancing

Ft. Wayne,

Consolidation Consolidation Consolidation Consolidation Chicago-area - Sold 12 IN presence

of 5 branches of 2 branches 4 branches branches

of 1 branch of 10 branches

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Consolidation Consolidation Consolidation Consolidation of Consolidation

of 8 branches of 12 branches of 44 branches 21 branches of 22

Returned to branches

community Sold non- Acquired 65 FDIC-assisted

bank model strategic market Charter One acquisition of Acquired 24

– O’Fallon, IL – branches Integra Bank MI / IN branches

1 branch throughout July, 2011 July, 2013

Indiana

March, 2009

Purchased 175 + 25 pending Sold 22 Consolidated 125

37

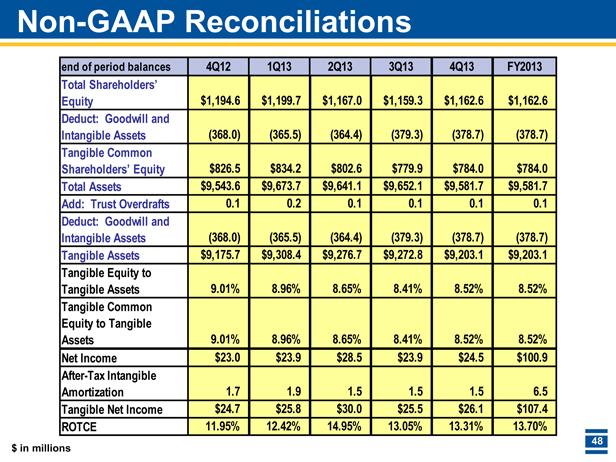

Non-GAAP Reconciliations

end of period balances 4Q12 1Q13 2Q13 3Q13 4Q13 FY2013

Total Shareholders’

Equity $1,194.6 $1,199.7 $1,167.0 $1,159.3 $1,162.6 $1,162.6

Deduct: Goodwill and

Intangible Assets (368.0) (365.5) (364.4) (379.3) (378.7) (378.7)

Tangible Common

Shareholders’ Equity $826.5 $834.2 $802.6 $779.9 $784.0 $784.0

Total Assets $9,543.6 $9,673.7 $9,641.1 $9,652.1 $9,581.7 $9,581.7

Add: Trust Overdrafts 0.1 0.2 0.1 0.1 0.1 0.1

Deduct: Goodwill and

Intangible Assets (368.0) (365.5) (364.4) (379.3) (378.7) (378.7)

Tangible Assets $9,175.7 $9,308.4 $9,276.7 $9,272.8 $9,203.1 $9,203.1

Tangible Equity to

Tangible Assets 9.01% 8.96% 8.65% 8.41% 8.52% 8.52%

Tangible Common

Equity to Tangible

Assets 9.01% 8.96% 8.65% 8.41% 8.52% 8.52%

Net Income $23.0 $23.9 $28.5 $23.9 $24.5 $100.9

After-Tax Intangible

Amortization 1.7 1.9 1.5 1.5 1.5 6.5

Tangible Net Income $24.7 $25.8 $30.0 $25.5 $26.1 $107.4

ROTCE 11.95% 12.42% 14.95% 13.05% 13.31% 13.70%

$ in millions

48

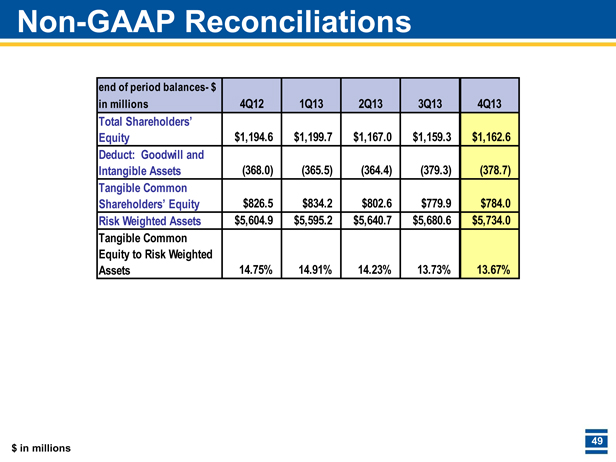

Non-GAAP Reconciliations

end of period balances- $

in millions 4Q12 1Q13 2Q13 3Q13 4Q13

Total Shareholders’

Equity $1,194.6 $1,199.7 $1,167.0 $1,159.3 $1,162.6

Deduct: Goodwill and

Intangible Assets (368.0) (365.5) (364.4) (379.3) (378.7)

Tangible Common

Shareholders’ Equity $826.5 $834.2 $802.6 $779.9 $784.0

Risk Weighted Assets $5,604.9 $5,595.2 $5,640.7 $5,680.6 $5,734.0

Tangible Common

Equity to Risk Weighted

Assets 14.75% 14.91% 14.23% 13.73% 13.67%

$ in millions

49

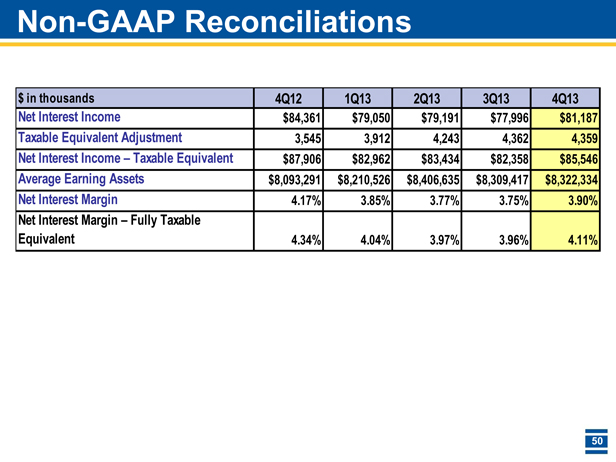

Non-GAAP Reconciliations

$ in thousands 4Q12 1Q13 2Q13 3Q13 4Q13

Net Interest Income $84,361 $79,050 $79,191 $77,996 $81,187

Taxable Equivalent Adjustment 3,545 3,912 4,243 4,362 4,359

Net Interest Income – Taxable Equivalent $87,906 $82,962 $83,434 $82,358 $85,546

Average Earning Assets $8,093,291 $8,210,526 $8,406,635 $8,309,417 $8,322,334

Net Interest Margin 4.17% 3.85% 3.77% 3.75% 3.90%

Net Interest Margin – Fully Taxable

Equivalent 4.34% 4.04% 3.97% 3.96% 4.11%

50

(Q –Emlen Harmon):Got you. I mean, is there anything when you guys think about the – again the Michigan – at the Southwest Michigan and the Northern Indiana branches. I mean, anything within those that would make you think you couldn’t get to the kind of efficiency ratio that the rest of the bank has reached over time?

(A - Chris Wolking): No. Not at all. In fact, I would tell you just the opposite. I would tell you that the economy up there, if you didn’t see there was a great article about Grand Rapids over the weekend in the New York Times, and the economy is strong. We’ve got very, very good people. It’s just to build that loan portfolio up to match those deposits is going to take some time. And obviously, they’re going to benefit from the UBMI acquisition, as we get more name recognition in those markets. But, Emlen, I couldn’t be more happy with the team we’ve got up there and the recent activity in the markets, but to do it in our measured credit manner, it’s going to take us a little bit of time, but it will be profitable for a long time versus just a short time then.

(Q-Christopher McGratty): Okay. Just a quick one on the buyback. You bought more stock in the fourth quarter. Was that a function of just two pending deals? Or how should we think about the – your actual ability to buy stock in 2014?

(A – Chris Wolking): No. In fact, Chris, we had that kind of in place obviously with a $2 million share buyback. We look at that really independently of our acquisition outlook, although it has a bearing, of course. But, when you’re only paying out 40%ish of earnings and organic growth was measured, we just had that opportunity and we felt like it was an important opportunity in materializing. And, as we’ve talked about in other calls, we’ve got cash components too for our pending acquisitions. It’s just a way to get our common equity about where we think it should be. So, nothing special, just kind of part of the overall day-in, day-out discussion about capital utilization.

* * *

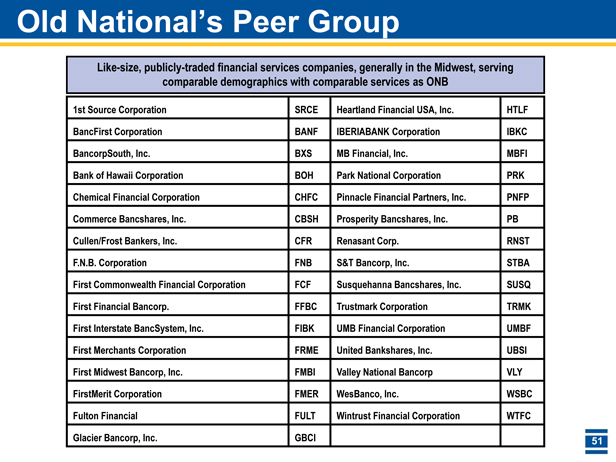

Old National’s Peer Group

Like-size, publicly-traded financial services companies, generally in the Midwest, serving

comparable demographics with comparable services as ONB

1st Source Corporation SRCE Heartland Financial USA, Inc. HTLF

BancFirst Corporation BANF IBERIABANK Corporation IBKC

BancorpSouth, Inc. BXS MB Financial, Inc. MBFI

Bank of Hawaii Corporation BOH Park National Corporation PRK

Chemical Financial Corporation CHFC Pinnacle Financial Partners, Inc. PNFP

Commerce Bancshares, Inc. CBSH Prosperity Bancshares, Inc. PB

Cullen/Frost Bankers, Inc. CFR Renasant Corp. RNST

F.N.B. Corporation FNB S&T Bancorp, Inc. STBA

First Commonwealth Financial Corporation FCF Susquehanna Bancshares, Inc. SUSQ

First Financial Bancorp. FFBC Trustmark Corporation TRMK

First Interstate BancSystem, Inc. FIBK UMB Financial Corporation UMBF

First Merchants Corporation FRME United Bankshares, Inc. UBSI

First Midwest Bancorp, Inc. FMBI Valley National Bancorp VLY

FirstMerit Corporation FMER WesBanco, Inc. WSBC

Fulton Financial FULT Wintrust Financial Corporation WTFC

Glacier Bancorp, Inc. GBCI

51