Alleghany Exhibit 99.1 |

FORWARD-LOOKING STATEMENTS This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are not historical facts but instead represent only Alleghany’s belief regarding future events, many of which, by their nature, are inherently uncertain and outside Alleghany’s control. Except for Alleghany’s ongoing obligation to disclose material information as required by federal securities laws, Alleghany is not under any obligation (and expressly disclaims any obligation) to update or alter any projections, goals, assumptions, or other statements, whether written or oral, that may be made from time to time, whether as a result of new information, future events or otherwise. Factors that could cause Alleghany’s actual results and experience to differ, possibly materially, from those expressed in the forward-looking statements include the factors set forth in Alleghany’s most recent Annual Report on Form 10-K and Quarterly Reports on Form 10-Q filed with the United States Securities and Exchange Commission. Alleghany |

Timeline Otis & Mantis Van Sweringen (1929) Robert Young (1937) Allan Kirby (1958) F.M. Kirby (1967) John J. Burns, Jr. (1992) Weston M. Hicks (2004) Alleghany |

A Rich History Nickel Plate Railroad Chesapeake & Ohio Railroad New York Central MSL Industries Jones Motor World Minerals Investors Diversified Services Chicago Title & Trust Sacramento Savings Bank Underwriters Re Alleghany |

Alleghany 10 Years Ago ($ bn) Capitol Transamerica $ 0.2 15% World Minerals 0.2 15 Other 0.1 6 Operating subsidiaries $ 0.5 36% Parent investments $ 1.0 71% Parent debt, other (0.1) - Parent, net $ 0.9 64% Stockholders’ equity $ 1.4 100% Alleghany |

Alleghany Reinvented: 2002-2012 (2002) (2003) (2006) (2007) (2012) Alleghany |

Alleghany Today ($ bn) TransRe $ 4.3 67% RSUI Group 1.5 23 Other 0.5 9 (Re)insurance $ 6.3 99% Parent investments $ 0.9 14% Parent debt, other (0.8) (13) Parent, net $ 0.1 1% Stockholders’ equity $ 6.4 100% Alleghany |

TransRe • Acquired March 6, 2012 for $3.5 billion in cash and stock • Leading specialty professional reinsurer with 49% of premium outside of US • Produced an underwriting profit in first ten months of Alleghany ownership • Expect combined ratio of ~ 96% absent unusual large catastrophes Alleghany |

RSUI Group • Acquired July 1, 2003 from Royal & Sun Alliance; initial investment $626 million • Cumulative underwriting profits of $1.1 billion under Alleghany ownership • Stockholder’s equity now $1.5 billion at the end of 2012 … after net upstream cash flows of $300 million • Long-term average combined ratio of 81% including Katrina and Sandy Alleghany |

RSUI’s Combined Ratio Alleghany 60% 86% 122% 71% 69% 80% 70% 73% 82% 99% 03 04 05 06 07 08 09 10 11 12 |

RSUI’s Combined Ratio Ex Katrina (2005) and Sandy (2012) Alleghany |

Other Insurance Operations • Capitol Insurance Companies – Small commercial property-casualty and surety • PacificComp – California workers’ compensation • Homesite (33% ownership) – Mono-line homeowners specialty insurer Alleghany |

Alleghany Capital Partners • Bourn & Koch (80%) – machine tools and grinders • Stranded Oil Resources (80%) – oil recovery • ORX Exploration (38%) – high impact oil and gas exploration • Article One Partners (40%) – crowd-sourced patent validation Alleghany |

Opportunities • Better underlying economy = exposure growth • Improving pricing in property lines and select casualty lines • Standard market dislocation = E&S opportunity • Improved competitive position at Capitol and PacificComp • Share repurchases at discount to book value Alleghany |

Challenges • Negative real interest rates hurts economics of the business • Observed increase in frequency of severe weather events • Relentless claims inflation in California workers’ compensation Alleghany |

Alleghany |

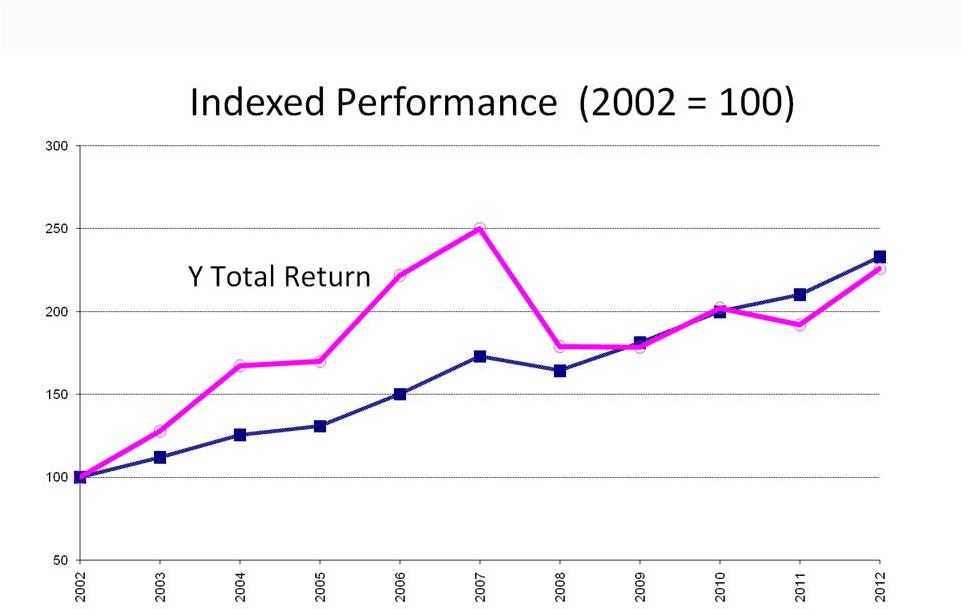

Y Book Value Per Share Alleghany |