Exhibit 99.1

Greater Bay Bancorp slide presentation

as of March 31, 2003

Greater Bay Bancorp

The Capital Group

June 11, 2003

Greater Bay Bancorp

Certain matters discussed in this presentation constitute forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward looking statements relate to the Company’s current expectations regarding future operating results, net interest margin, net loan charge-offs, growth in loans and deposits, compliance with the cure agreement, and the strength of the local economy. These forward looking statements are subject to certain risks and uncertainties that could cause the actual results, performance or achievements to differ materially from those expressed, suggested or implied by the forward looking statements. These risks and uncertainties include, but are not limited to: (1) the impact of changes in interest rates, a decline in economic conditions at the international, national and local levels and increased competition among financial service providers on the Company's results of operations, the Company’s ability to continue its net interest spread, and the quality of the Company’s earning assets; (2) any difficulties that may be encountered in integrating newly acquired businesses and in realizing operating efficiencies; (3) government regulation; and (4) the other risks set forth in the Company’s reports filed with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended December 31, 2002.

Company Snapshot

| Company Name | Greater Bay Bancorp |

| Nasdaq NM | GBBK |

| Shares Outstanding | 52 million |

| Market Value* | $1.2 billion |

| Assets | $8 billion |

| LTM Net Income | $124 million |

| Common Equity | $600 million |

| Preferred Equity: | |

| Convertible Preferred $81 million | |

| Perpetual Preferred $15 million | |

* Calculated using closing price of GBBK stock on 6/5/03

Company Vision

- Create superior, long-term economic returns for our shareholders.

- Provide exceptional, relationship based value to our clients.

- Attract and retain outstanding employees.

Franchise Overview

- Formed late 1996 with merger of Cupertino National Bancorp and Mid-Peninsula Bancorp.

- Currently largest independent community bank holding company headquartered in Northern California.

- Diversified financial services provider.

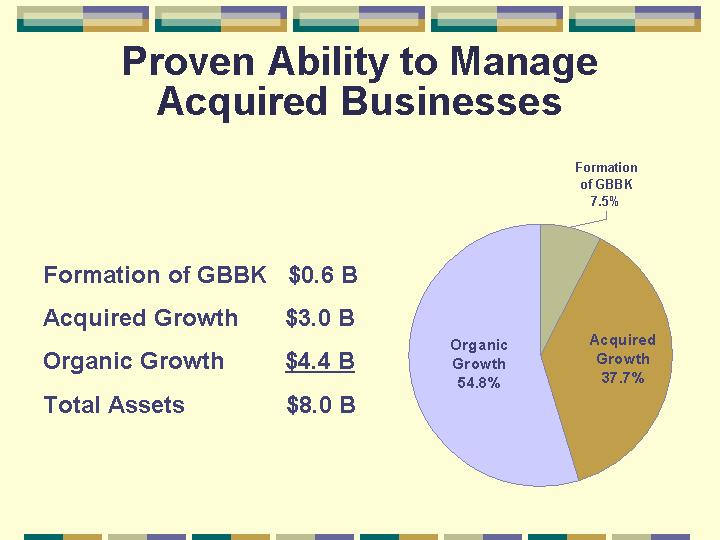

Proven Ability to Manage

Acquired Businesses

| Formation of GBBK | $0.6 B |

| Acquired Growth | $3.0 B |

| Organic Growth | $4.4 B |

| Total Assets | $8.0 B |

[CHART]

| Organic Growth | 54.8% |

| Acquired Growth | 37.7% |

| Formation of GBBK | 7.5% |

Acquisition Strategy

“Ring the Bay”

Greater Bay now has a presence in all of the key

sub-markets of the San Francisco Bay Area

Successful Acquisition Strategy

13 acquisitions completed since formation, adding $3.0 billion

in assets and extending market reach throughout the San Francisco Bay Area

| Assets ($ in millions) | ||

| 12/97 | Peninsula Bank of Commerce | $200 |

| 05/98 | Golden Gate Bank | $150 |

| 08/98 | Pacific Business Funding | $ 15 |

| 05/99 | Bay Area Bank | $200 |

| 10/99 | Bay Bank of Commerce | $200 |

| 01/00 | Mt. Diablo National Bank | $250 |

| 05/00 | Coast Commercial Bank | $400 |

| 07/00 | Bank of Santa Clara | $400 |

| 11/00 | The Matsco Companies | $285 |

| 03/01 | CAPCO Financial Company, Inc. | $ 15 |

| 12/01 | San Jose National Bank | $680 |

| 03/02 | ABD Insurance | N/A * |

* Gross annual premiums of $1 billion

Diversified Financial Services Provider

| Greater Bay Bancorp | |||

| Regional Banking | ABD Insurance | Specialty Finance | Trust |

* No underwriting risk.

Client Focus

- Small and mid-sized businesses

- Professional services firms

- Private banking and wealth management

- Custom banking for individuals

- Relationship-driven real estate investors and operators

ABD Insurance and Financial Services

- We completed the acquisition of ABD Insurance and Financial Services (the 16th largest commercial insurance brokerage agency in the country) in March 2002. It has been a very successful partnership and, during the first quarter, ABD provided $36.6 million in fee income.

- No underwriting risk

- Product Focus

- Offering P & C

- Employee benefits

- 401K products

Experienced Senior Management Team

| Position | Name | Years Experience |

| Chief Executive Officer | David L. Kalkbrenner | 35+ |

| Chief Operating Officer | Byron A. Scordelis | 25+ |

| Chief Financial Officer | Steven C. Smith | 25+ |

| Chief Information Officer | Gregg Johnson | 25+ |

| Chief Risk Officer | Kenneth Shannon | 20+ |

| President, Community Banking Group | Susan K. Black | 15+ |

| Chief Lending Officer | David R. Hood | 25+ |

| Community Bank Presidents | 20+ Avg. | |

| GBB Board of Directors 18 diversified and seasoned directors | 25+ Avg. | |

| Community Bank Boards of Directors 90 diversified and seasoned directors | 25+ Avg. |

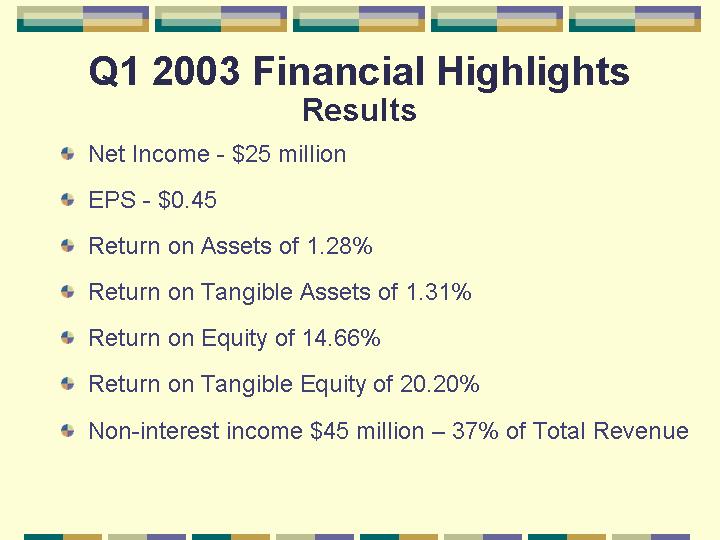

Q1 2003 Financial Highlights

Results

- Net Income - $25 million

- EPS - $0.45

- Return on Assets of 1.28%

- Return on Tangible Assets of 1.31%

- Return on Equity of 14.66%

- Return on Tangible Equity of 20.20%

- Non-interest income $45 million - 37% of Total Revenue

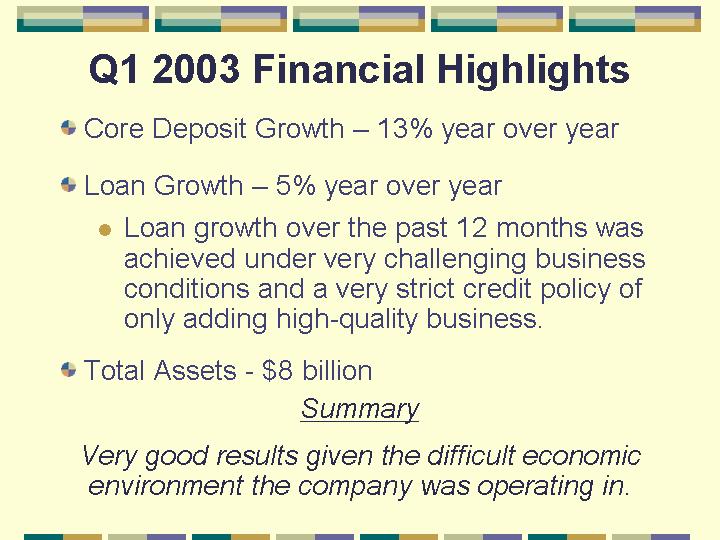

Q1 2003 Financial Highlights

- Core Deposit Growth - 13% year over year

- Loan Growth - 5% year over year

- Loan growth over the past 12 months was achieved under very challenging business conditions and a very strict credit policy of only adding high-quality business.

- Total Assets - $8 billion

Summary

Very good results given the difficult economic environment the company was operating in.

Key Factors Impacting Operating Results

- Credit Quality

- Net Interest Margin

- Strong Capital Position

Credit Quality

- Despite the challenging economic environment, our relationship banking philosophy and effective credit management efforts have resulted in relatively low levels of net charge-offs and non-performing assets compared to our peer group.

Credit Quality

Q1 2003

Reserves/ Average Loans

| GBBK | 2.73% |

| Peer* | 1.58% |

Net Charge Offs/ Average Loans

| GBBK | 0.53% |

| Peer* | 0.38% |

NPAs/ Total Assets

| GBBK | 0.51% |

| Peer* | 0.50% |

Reserves/ NPAs

| GBBK | 322% |

| Peer* | 249% |

* Custom peer group defined by GBBK — see schedule A

Net Interest Margin

Management in a Volatile Environment

| 1998 | 1999 | 2000 | 2001 | 2002 | Q1 ’03 | |

| GBBK’s Margin down 123 bps | 5.50% | 5.29% | 5.56% | 4.86% | 4.54% | 4.33% |

| Prime Rate down 525 BPS | 7.80% | 8.50% | 9.50% | 5.00% | 4.25% | 4.25% |

Net Interest Margin

Impact of Further Market Interest Rate Reduction

- GBBK is asset sensitive.

- Over the last year, MBS portfolio has declined approximately $650 million as planned.

- Investment strategy continues to be to invest in short duration securities.

- Give up current yield for stable value

- Position Company to take advantage of rising rates in 2004 and beyond.

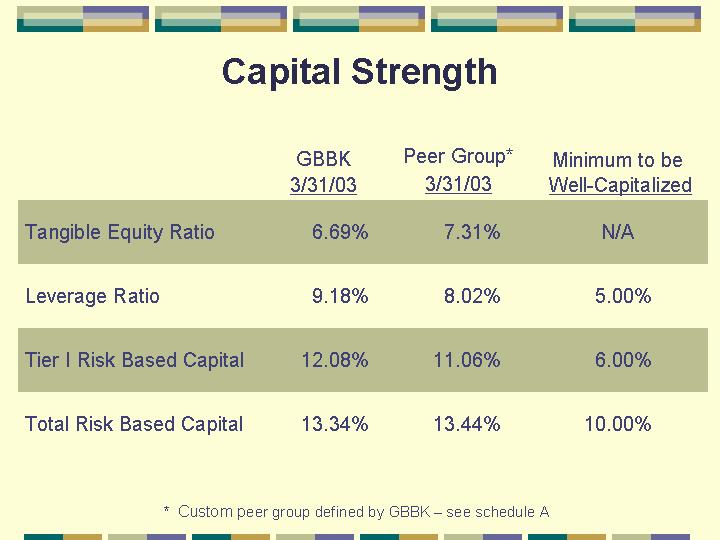

Capital Strength

| GBBK 3/31/03 | Peer Group* 3/31/03 | Minimum to be Well-Capitalized | |

| Tangible Equity Ratio | 6.69% | 7.31% | N/A |

| Leverage Ratio | 9.18% | 8.02% | 5.00% |

| Tier I Risk Based Capital | 12.08% | 11.06% | 6.00% |

| Total Risk Based Capital | 13.34% | 13.44% | 10.00% |

* Custom peer group defined by GBBK - see schedule A

Capital Strength

- Our emphasis on increasing capital ratios during the past year has resulted in a tangible equity to asset ratio of 6.69%, up from 4.99% at March 31, 2002.

- All other capital ratio are substantially in excess of regulatory well capitalized guidelines and peers.

Economic Capital as a Foundation for

Enterprise-wide Risk Management

- We have developed a return on economic capital model, utilizing the expertise of ERISK that looks at business returns from a risk and concentration perspective.

- The model incorporates GBBK’s risk profile for credit risk, operating risk, interest rate risk and market risk.

- Results show returns on risk adjusted capital by business line.

- Results provide framework, based on risk appetite correlated to ratings targets, to determine capital GBBK can utilize to enhance shareholders’ returns

Required Economic Capital Formulated

to GBBK Risk Appetite

- This chart provides an initial look at GBBK’s economic capital position versus our risk appetite

- GBBK’s Tangible Equity does not include the value of ABD which currently is locked up in goodwill, but is worth more today than when we acquired ABD GBBK in early 2002

- GBBK’s Tangible Equity does not include an allocation of loan loss reserve in excess of expected losses - a very conservative assessment.

| BB | BBB | A | GBBK Tangible Actual |

| ($ in millions) | |||

| $278 | $379 | $435 | $489 |

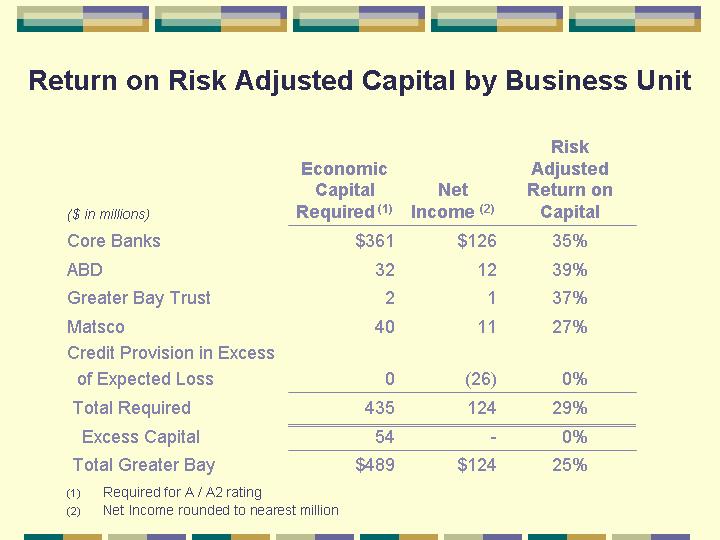

Return on Risk Adjusted Capital by Business Unit

| ($ in millions) | Economic | Income (2) | Adjusted Return on Capital |

| Core Banks | $361 | $126 | 35% |

| ABD | 32 | 12 | 39% |

| Greater Bay Trust | 2 | 1 | 37% |

| Matsco | 40 | 11 | 27% |

| Credit Provision in Excess of Expected Loss | 0 | (26) | 0% |

| Total Required | 435 | 124 | 29% |

| Excess Capital | 54 | - | 0% |

| Total Greater Bay | $489 | $124 | 25% |

(1) Required for A / A2 rating

(2) Net Income rounded to nearest million

Regulatory Update

January 15, 2003

- GBBK announced that it received a notice from the Board of Governors of the Federal Reserve System requiring the Company to enhance management oversight of its Enterprise Wide Risk Management program. The Company prepared a corrective action plan, which was incorporated into a cure agreement with the Federal Reserve Board.

- The action plan included enhancements to policies, procedures, and management strength relating to liquidity, interest rate risk sensitivity, credit risk management and compliance. We have dedicated significant time and resources to addressing these items and expect to complete the corrective action plan in a timely manner.

June 2003

- The Company continues to make progress in complying with all aspects of the cure agreement with the Federal Reserve Board.

- The Company submitted to the Federal Reserve Board all of the required action items to satisfy the cure agreement and believes it is on target to satisfy the terms of the agreement by the required date of July 7, 2003

Looking Forward:

Our Strategy for 2003 and Beyond

Our Future is a Reaffirmation

of Our Past

- The Bay Area economy is mired in an economic slump which has affected our state and our nation, but

- We believe that this remains one of the greatest economic regions in the world.

- And the Bay Area will remain the focal point of our strategic future.

"We are heartened that expectations for the next six months have improved and are keeping our fingers crossed that this growing confidence can produce capital spending to grease the gears of the economy and jumpstart positive growth."

Bay Area Council

Business Confidence Survey

May 2003

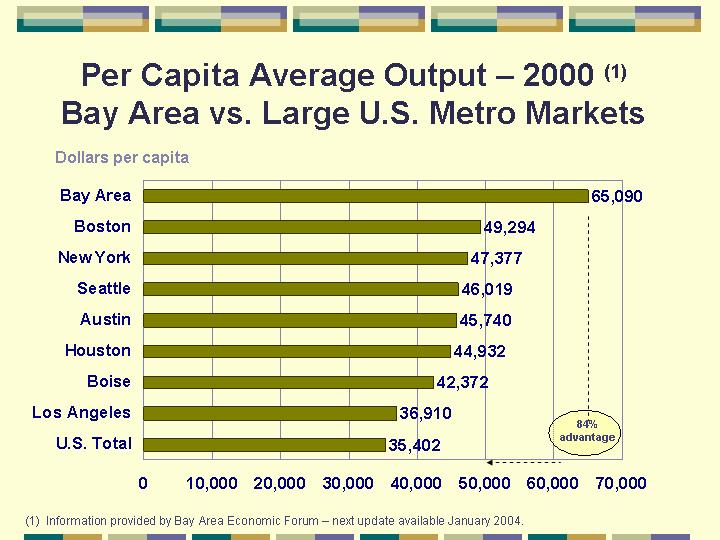

Per Capita Average Output -2000 (1)

Bay Area vs. Large U.S. Metro Markets

| Dollars per capita | ||||||||

| Bay Area | Boston | New York | Seattle | Austin | Houston | Boise | Los Angeles | U.S. Total |

| 65,090 | 49,294 | 47,377 | 46,019 | 45,740 | 44,932 | 42,372 | 36,910 | 35,402 |

(1) Information provided by Bay Area Economic Forum -next update available January 2004.

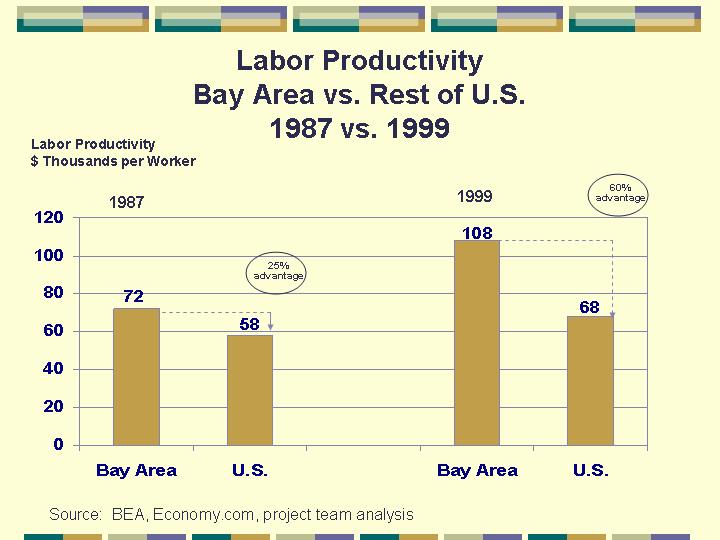

Labor Productivity

Bay Area vs. Rest of U.S.

1987 vs. 1999

Labor Productivity

$ Thousands per Worker

| 1987 | 1999 | |||

| 25% advantage | 60% advantage | |||

| Bay Area | 72 | 108 | ||

| U.S. | 58 | 68 | ||

Source: BEA, Economy.com, project team analysis

Education of Workforce

Bay Area vs. Large U.S. Metro Markets

% of Population with College Degrees

| Bay Area | Austin | Boston | Seattle | New York | Los Angeles | |

| % Over Age 25 with Degree | ||||||

| Bachelor’s Degree | 19.7% | 20.4% | 17.1% | 18.4% | 15.1% | 14.4% |

| Graduate Degree | 11.1% | 10.3% | 10.7% | 8.0% | 10.6% | 7.6% |

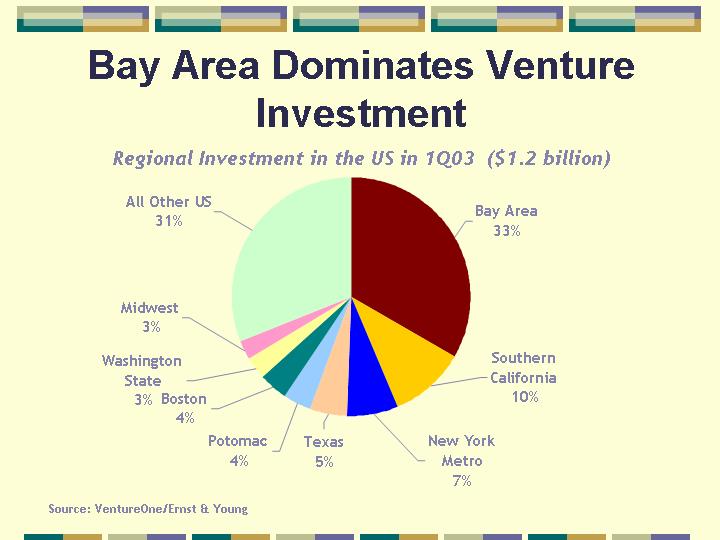

Bay Area Dominates Venture Investment

Regional Investment in the US in 1Q03 ($1.2 billion)

[CHART]

| Bay Area | 33% |

| Southern California | 10% |

| New York Metro | 7% |

| Texas | 5% |

| Potomac | 4% |

| Boston | 4% |

| Washington State | 3% |

| Midwest | 3% |

| All Other US | 31% |

Source: VentureOne/Ernst & Young

Our Future is a Reaffirmation of Our Past

- The Bay Area economy is mired in an economic slump which has affected our state and our nation,but

- We believe that this remains one of the greatest economic regions in the world.

- And the Bay Area will remain the focal point of our strategic future.

- We believe thatrelationship banking rather thantransactional banking must remain at the core of our business model

- And that the local market knowledge of our community bankers provide an advantage that is difficult to match.

- Strength of our credit portfolio affirms this belief - - and defies the skeptics.

Our Future is a Reaffirmation of Our Past

We believe that an uncompromising focus on quality will differentiate us from our peers - - and is the key that will deliver superior long-term value to our shareholders

- Credit quality

- Operating quality

- Attention to detail in serving our clients

- We understand that this is a business and that we work for our shareholders.

- We have no divine right to exist as a business.

- Most efficient competitor sets profit margin for everyone else.

- Our focus must be on factors that deliver quality results.

- Selling money is a commodity business - - providing exceptional service is a value business.

Strategic Goals

- Reaching greater critical mass in the Company's market areas.

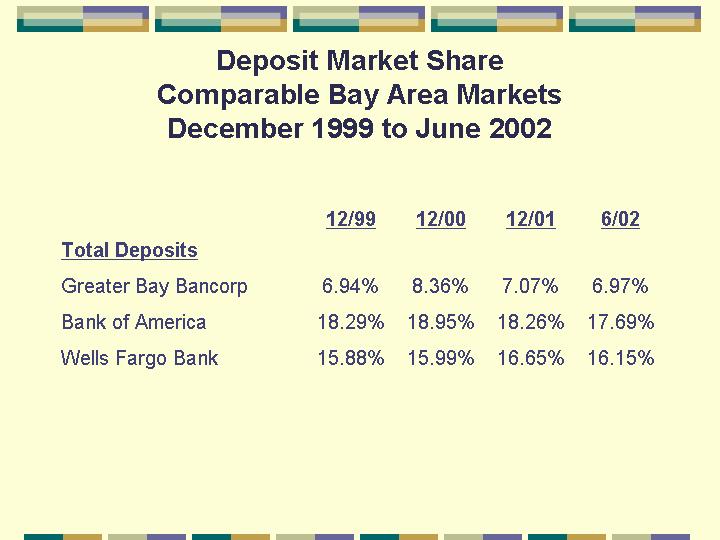

Deposit Market Share

Comparable Bay Area Markets

December 1999 to June 2002

| Total Deposits | ||||

| Greater Bay Bancorp | ||||

| Bank of America | ||||

| Wells Fargo Bank |

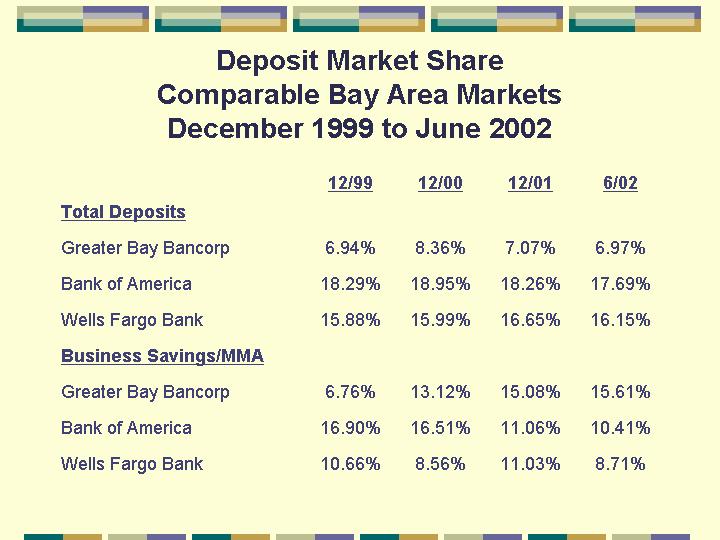

Deposit Market Share

Comparable Bay Area Markets

December 1999 to June 2002

| Total Deposits | ||||

| Greater Bay Bancorp | ||||

| Bank of America | ||||

| Wells Fargo Bank | ||||

| Business Savings/MMA | ||||

| Greater Bay Bancorp | ||||

| Bank of America | ||||

| Wells Fargo Bank |

Strategic Goals

Reaching greater critical mass in the Company’s market areas.

- Generating increased fee income through cross-selling broader services.

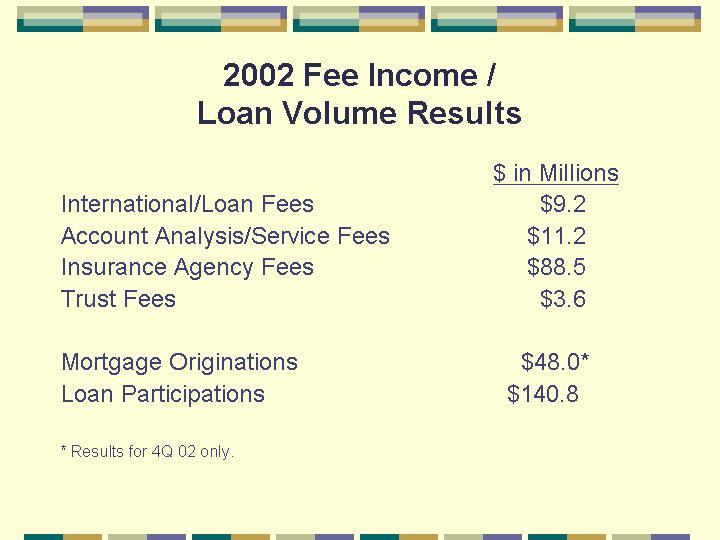

2002 Fee Income /

Loan Volume Results

| $ in Millions | |

| International/Loan Fees | |

| Account Analysis/Service Fees | |

| Insurance Agency Fees | |

| Trust Fees | |

| Mortgage Originations | |

| Loan Participations |

* Results for 4Q 02 only.

Strategic Goals

- Reaching greater critical mass in the Company’s market areas.

- Generating increased fee income through cross-selling broader services.

- Continue to diversify revenue stream.

Non-Interest Income (1)

Revenue | Revenue | Revenue | |||

(1) As a result of the ABD acquisition in March 2002, the Company’s 2002 results included insurance agency commissions and fees totaling $88.5 million. These were no such insurance agency commissions in 2001.

Strategic Goals

- Reaching greater critical mass in the Company’s market areas.

- Generating increased fee income through cross-selling broader services.

- Continue to diversify revenue stream.

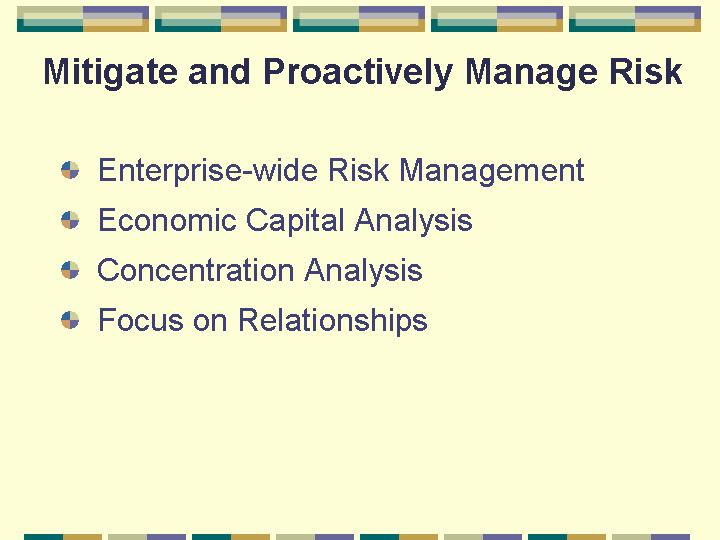

- Continue to mitigate and proactively manage risk.

Mitigate and Proactively Manage Risk

- Enterprise-wide Risk Management

- Economic Capital Analysis

- Concentration Analysis

- Focus on Relationships

Strategic Goals

- Reaching greater critical mass in the Company's market areas.

- Generating increased fee income through cross-selling broader services.

- Continue to diversify revenue stream.

- Continue to mitigate and proactively manage risk.

- Opportunistic market expansion.

Closing Remarks

Stock Price Performance *

- Recently trading at about 10 times last twelve month’s earnings.

- California community banks trading about 18 times.

- Reasons for stock price decline during the past year include market concerns about:

- The Northern California economy, the state deficit, the dot com fall-out and the technology industry in Silicon Valley.

- Real estate valuations, lease rates and vacancy factors in the San Francisco Bay Area.

- Impact of Fed rate decreases on net interest margin.

- Market perception of GBBK's credit quality and overall risk profile.

* As of June 5, 2003

Our Response

- Our responsibility is to deliver results, we cannot control how the market interprets the impact of external issues on our Company.

- We continue to focus on high-quality earnings, while maintaining strong credit quality.

- Our ultimate goal remains long-term shareholder value.

Guidance

- Average loan growth - focus on quality and anticipate exceeding peer banks in market

- Average deposit growth - committed to expanding deposit base and selectively adding new clients that fit

- Net interest margin - continued pressure due to economic conditions and competitive environment

- Credit quality - net charge offs will be in the 60-70 bps range for 2003

Investment Rationale

- Franchise with record of quality growth and consistent profitability.

- Well positioned for economic upturn.

- Strong balance sheet.

- Diversified product capability.

- Internal capital can support strategic growth.

- Community banking credit culture.

- Experienced management team.

- Compelling return opportunity.

Greater Bay Bancorp

The Capital Group

June 11, 2003

Schedule A - Custom Peer Group

| Allfirst Financial, Inc. | Fulton Financial Corporation |

| Associated Banc-Corp | Greater Bay Bancorp |

| BancorpSouth, Inc. | Hibernia Corporation |

| Bank of Hawaii Corporation | Hudson United Bancorp |

| BOK Financial Corporation | International Bancshares Corporation |

| Bremer Financial Corporation | Mercantile Bankshares Corporation |

| Central Bancompany | Old National Bancorp |

| Citizens Banking Corporation | Provident Financial Group, Inc. |

| City National Corporation | RBC Centura Banks, Inc. |

| Colonial BancGroup, Inc. | Riggs National Corporation |

| Commerce Bancorp, Inc. | Sky Financial Group Inc. |

| Commerce Bancshares, Inc. | South Financial Group, Inc. (The) |

| Community First Bankers, Inc. | Southwest Bancorporation of Texas, Inc. |

| Cullen/Frost Bankers, Inc. | Susquehanna Bancshares, Inc. |

| F.N.B. Corporation | Synovus Financial Corp. |

| FBOP Corporation | TCF Financial Corporation |

| First Banks, Inc. | Trustmark Corporation |

| First Citizens BancShares, Inc. | UMB Financial Corporation |

| First Midwest Bancorp, Inc. | United Bankshares, Inc. |

| First National of Nebraska, Incorporated | Valley National Bancorp |

| First Virginia Banks, Inc. | Whitney Holding Corporation |

| Firstbank Holding Company of Colorado | Wilmington Trust Corporation |

| FirstMerit Corporation |