Exhibit 99.1

Slide Presentation of Greater Bay Bancorp as of September 30, 2006

1 Greater Bay Bancorp Greater Bay Bancorp Investor Presentation November 2006 |

2 Greater Bay Bancorp Greater Bay Bancorp Certain matters discussed in this presentation constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward looking statements relate to the Company’s current expectations regarding future operating results, net interest margin, net loan charge-offs, asset quality, level of loan loss reserves, growth in loans and deposits, the strength of the local economy and the Company’s intent to adopt SAB 108 as of December 31, 2006. These forward looking statements are subject to certain risks and uncertainties that could cause the actual results, performance or achievements to differ materially from those expressed, suggested or implied by the forward looking statements. These risks and uncertainties include, but are not limited to: (1) the impact of changes in interest rates, a decline in economic conditions at the local, national and international levels and increased competition among financial service providers on the Company’s results of operations and the quality of the Company’s earning assets; (2) government regulation, including ABD’s receipt of requests for information from state insurance commissioners and subpoenas from state attorneys general related to the ongoing insurance industry- wide investigations into contingent commissions and override payments; and (3) the other risks set forth in the Company‘s reports filed with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended December 31, 2005. Greater Bay does not undertake, and specifically disclaims, any obligation to update any forward-looking statements to reflect occurrences or unanticipated events or circumstances after the date of such statements. |

3 Company Profile As of September 30, 2006 Company Profile As of September 30, 2006 $4.6 billion Core Loans (1) 1.00% / 10.2% Q3 ROA / ROCE $1.3 billion Market Capitalization (3) $734 million Common Equity 51.0 million Common Shares Outstanding $0.32 Q3 Diluted EPS $18.5 million Q3 Net Income $4.1 billion Core Deposits (2) $7.3 billion Total Assets (1) Excludes purchased whole loans (2) Excludes brokered and wholesale institutional deposits (3) As of November 6, 2006 |

4 Investment Rationale Investment Rationale Largest independent banking franchise in Northern California operating in lucrative San Francisco Bay Area regional market. – Proven record of organic growth. – Established track record as acquirer of choice. Diversified provider of financial services in three distinct business areas. – Mitigates geographic and sector-specific concentrations. – Balanced spread and fee revenue mix. |

5 Investment Rationale Investment Rationale Strong financial fundamentals and sound credit metrics. Experienced and proven executive management team. Leading to long-term record of superior shareholder return. |

6 An Exceptional Regional Market An Exceptional Regional Market |

7 Greater San Francisco Bay Area Greater San Francisco Bay Area |

8 Greater San Francisco Bay Area Profile Greater San Francisco Bay Area Profile Recognized global leadership in technological innovation, advancement, and growth. – Unmatched concentration of venture capital funding and investment. – Entrepreneurial spirit and results-oriented ethic. Highest levels of worker productivity and per capita income in the nation. Highest level of workforce education in the nation. Exceptionally strong international trade position. |

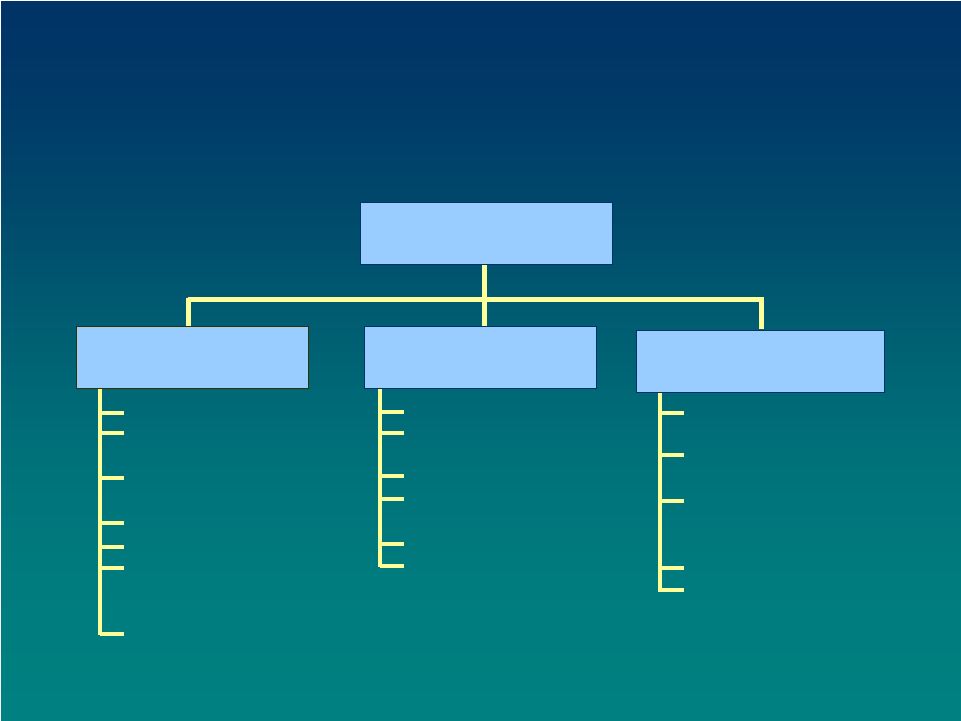

9 Diversified Financial Services Provider Diversified Financial Services Provider Greater Bay Bancorp Community Banking Loans of $3.0 billion Core deposits of $4.1 billion 8 distinct community bank brands 41 offices Relationship based Centralized operations, international and cash management support Bay Area in scope Assets of $1.7 billion Commercial finance to health care businesses Small ticket leasing Factoring and asset based lending SBA lending National in scope Annual premiums of $2.2 billion 2005 revenues of $154 million Offering P&C and D&O, employee benefits, risk management services No underwriting risk Western U.S. in scope Specialty Finance Insurance Brokerage |

10 Community Banking Community Banking |

11 Community Banking Business Community Banking Business Operating 8 separate banking identities under single consolidated charter – 41 office locations throughout the Greater Bay Area. Common data processing platform, credit policies and operating procedures – served and supported by single administrative staff. Relationship focused: – Loans: Commercial ($500M-5MM), CRE ($1-10MM), and construction ($1-10MM). – Deposits: Full suite of business and personal products. – Local people in local markets making local decisions based upon local knowledge. |

12 Community Banking Footprint Community Banking Footprint |

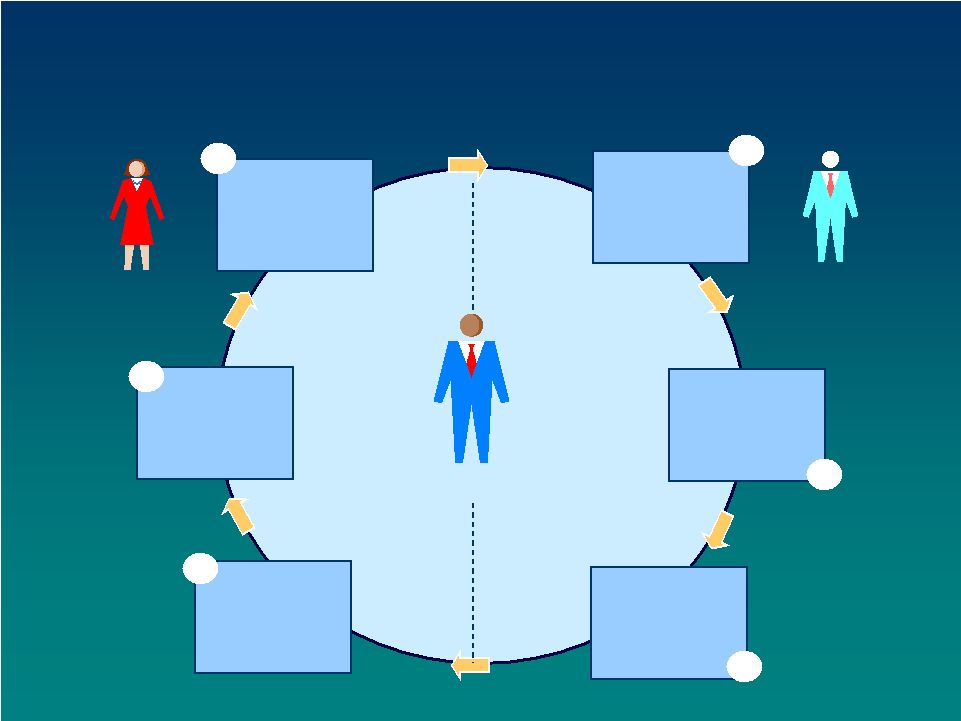

13 Client-Centric Banking Model Client-Centric Banking Model Install Sell Service Craft Locate and Diagnose 1 5 4 2 3 Client Link and Build 6 Relationship Management Business Development |

14 Business Development Group Initiatives Business Development Group Initiatives Proven executive hired in Q4 2005 to build & manage team. 16 proven BDOs recruited to date. – Top performers from two major local competitors. – Virtually all BDOs from large banks. – Targeted to grow to 17 by year-end. Each BDO expected to generate $20MM in annual loan/line commitments and related deposit business. – Commercial and owner-occupied CRE in nature. – Target size of $1-6 MM per commitment. |

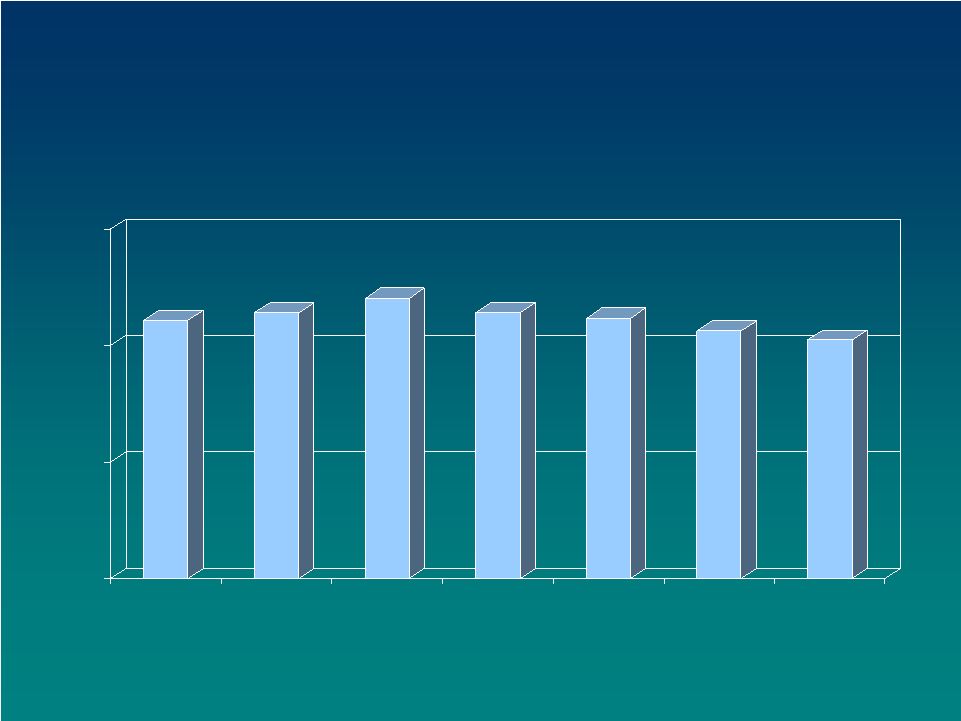

15 Core Deposit Balances (1) $4.43 $4.56 $4.81 $4.56 $4.47 $4.25 $4.10 $0 $2 $4 $6 2002 2003 2004 2005 Q1 '06 Q2 '06 Q3 '06 ($ in Billions) (1) Core deposits exclude brokered and wholesale institutional deposits. |

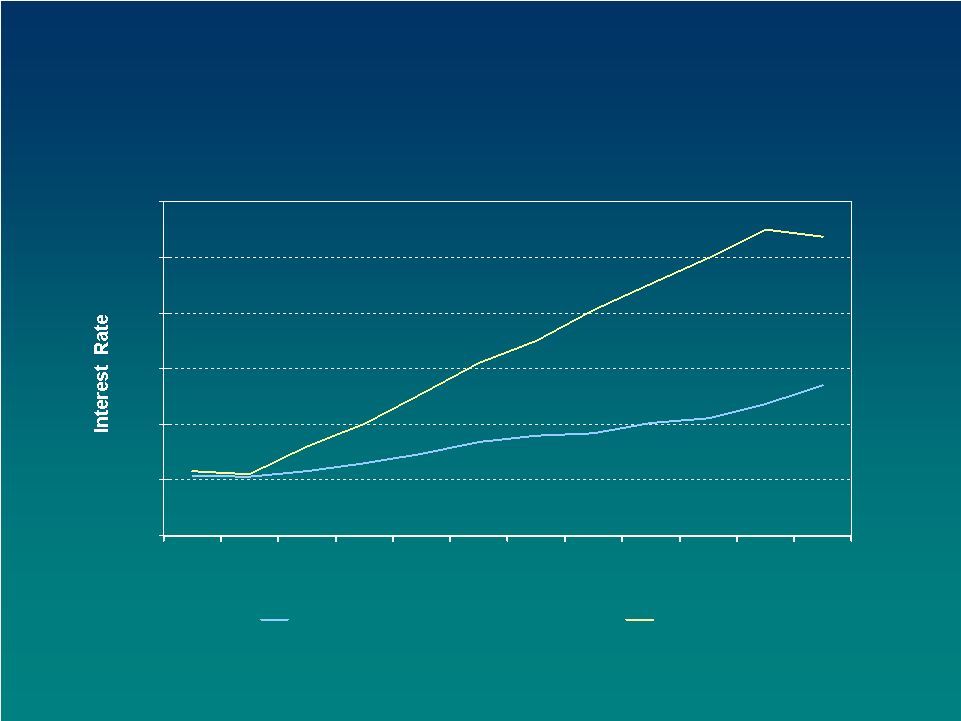

16 Core Deposit Pricing Core Deposit Pricing 0% 1% 2% 3% 4% 5% 6% Dec '03 Dec '04 Dec '05 Sept '06 Interest Bearing Core Deposit Cost LIBOR Core deposits exclude brokered and wholesale institutional deposits. |

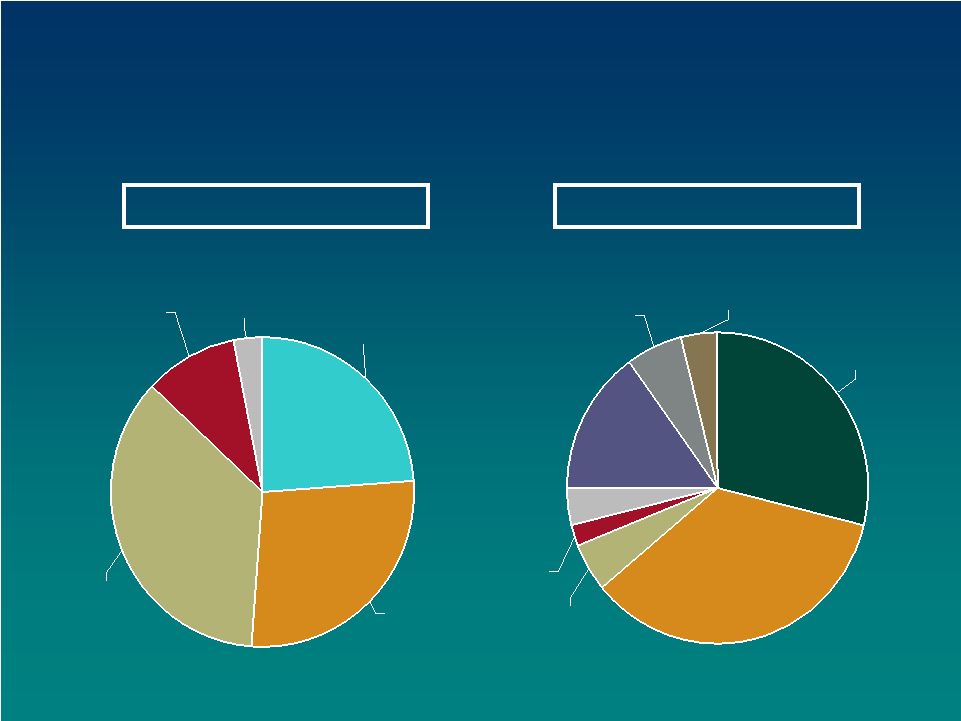

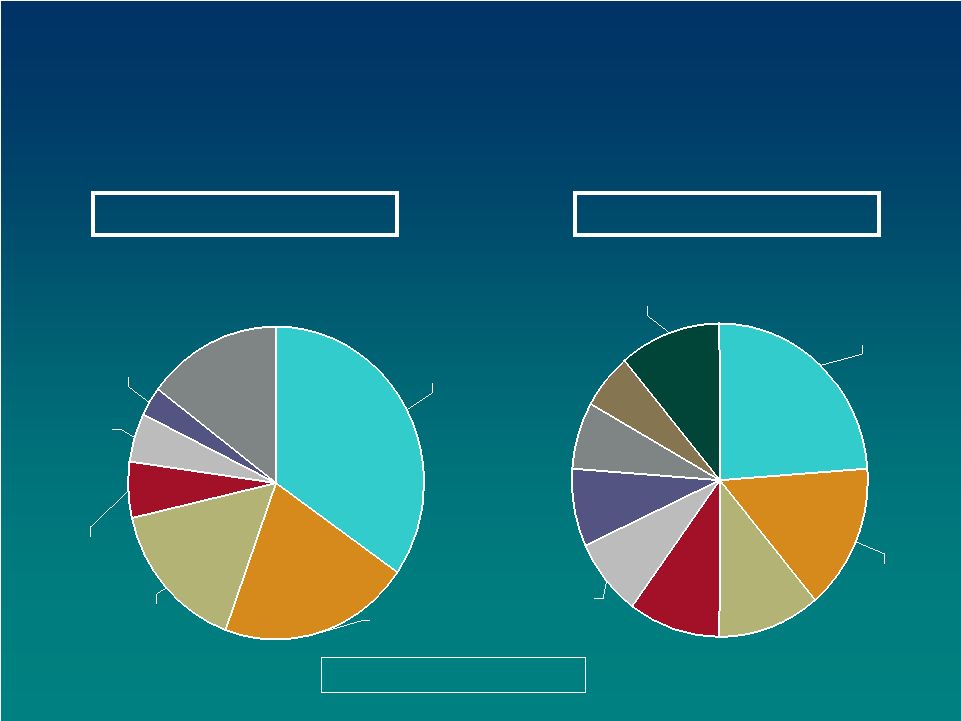

17 (1) Core deposits exclude brokered and wholesale institutional deposits. By Region By Type Demand 24% MMDAs 36% Time Deposits >$100 10% Other Time Deposits 3% Savings & NOW 27% San Mateo 29% Contra Costa 15% Sonoma 4% Santa Clara 35% Santa Cruz & Monterey 6% Alameda 4% Marin 2% San Francisco 5% Community Banking Core Deposits (1) September 30, 2006 |

18 Specialty Finance Specialty Finance |

19 Specialty Finance Business Specialty Finance Business Collection of discrete businesses focused on acquisition and servicing/sale of value-based assets where execution, efficiency, standardization, and productivity are essential to optimizing profitability. Transaction rather than relationship-based. – Relationships essentially limited to intermediaries who source the business (dealers, distributors, etc.). Mandate to compete at high end of credit quality spectrum. – No deviation from target borrower – very disciplined. Intense focus on perpetual growth of credit risk knowledge and on automation-based underwriting as core strategic elements. |

20 Professional dental and veterinary term commercial financing National in scope Matsco Total Loans $947 million (1) Small-ticket leasing National in scope Greater Bay Capital Operating Leases $52 million Finance Leases $231 million Factoring and asset- based lending National in scope Greater Bay Business Funding Total Loans $90 million (1) 504 and 7(A) business sourced direct and via community banks Regional in scope SBA Lending Total Loans $273 million (1) Specialty Finance Group (1) Total loans, gross of deferred costs and fees. |

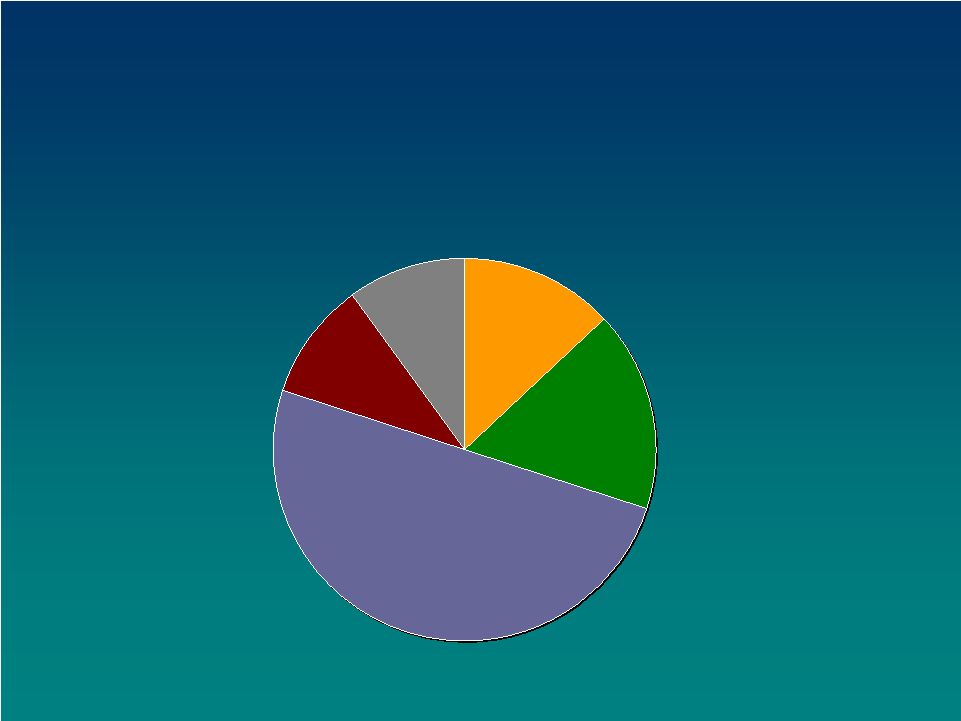

21 Specialty Finance Group Loan Portfolio Composition September 30, 2006 Specialty Finance Group Loan Portfolio Composition September 30, 2006 Matsco (1) 59% Greater Bay Capital (2) 14% SBA Lending (1) 17% Other (1) 4% Greater Bay Business Funding (1) 6% Total Assets: $1.7 billion (1) Total loans, gross of deferred costs and fees. (2) Excludes operating lease totals of $52 million at 09/30/06. |

22 Consolidated Loan Portfolio Profile Consolidated Loan Portfolio Profile |

23 Core Loan Portfolio Composition Combined Community Banking and Specialty Finance (1) ($ in Billions) $- $1 $2 $3 $4 $5 2001 2002 2003 2004 2005 Q3 2006 Commercial-Term RE Construction and Land Commercial - Community Banking Commercial-Specialty Finance SNC/Residential/All Other $4.51 $4.81 $4.54 $4.45 $4.49 $4.61 14% 13% 26% 16% 31% 11% 17% 24% 15% 33% 10% 19% 23% 12% 36% 9% 23% 22% 11% 35% 9% 26% 20% 14% 31% 8% 27% 19% 16% 30% (1) Total Loans, gross of deferred costs and fees. |

24 -400 -200 0 200 400 Dec-03 Dec-04 Dec-05 Sep-06 Commercial - Term RE Construction and Land Commercial - Community Banking Commercial - Specialty Finance Total Loans, gross of deferred costs and fees Core Loan Portfolio Evolution (Cumulative Change Since December 2003) ($ in Millions) |

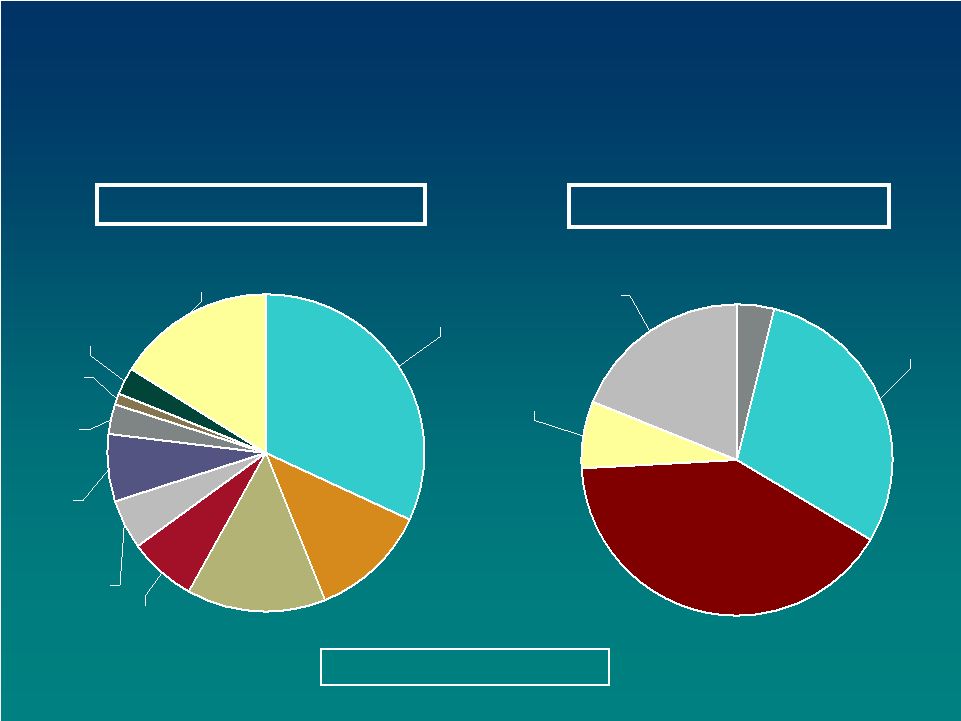

25 Term Commercial Real Estate Loan Composition September 30, 2006 Term Commercial Real Estate Loan Composition September 30, 2006 Retail 21% Industrial 16% Other 15% Office 34% Warehouse 6% R&D 3% Hotel/ Motel 5% San Mateo 11% Contra Costa 8% Marin 7% San Francisco 10% Santa Cruz 6% Sonoma 8% Other 11% Alameda 15% Santa Clara 24% By Type By County Total - $1.4 Billion |

26 Bay Area Office Market and Vacancy Trends Bay Area Office Market and Vacancy Trends $0 $2 $4 $6 1999 2000 2001 2002 2003 2004 2005 0% 5% 10% 15% 20% 25% Avg Rent Vacancy |

27 Construction Loan Portfolio Composition September 30, 2006 Construction Loan Portfolio Composition September 30, 2006 By County Santa Clara 32% San Francisco 12% San Mateo 14% Alameda 7% Santa Cruz 5% Contra Costa 7% Sonoma 3% Marin 1% Other 16% Solano 3% Owner Occupied 4% SFD 30% Condo / Townhome 40% Apartments 7% CRE 19% By Type Total - $586 Million Excludes land loans of $167,110 million. |

28 65-70% 26% < 60% 19% 70-75% 25% 60-65% 25% 75-80% 5% By LTV By Total Commitment Size Total - $762 Million 1-4 Family/Condo Construction Portfolio Commitments September 30, 2006 $20-25MM 14% Over $25MM 22% Under $5MM 30% $15-20MM 4% $10-15MM 14% $5-10MM 16% |

29 Commercial Insurance Brokerage Commercial Insurance Brokerage |

30 Commercial Insurance Services Business Commercial Insurance Services Business Acquired ABD Insurance and Financial Services in March 2002 – a highly-respected provider of commercial insurance brokerage and risk management services. 14 th largest brokerage firm in the nation. Diversified property and casualty (65%) and employee benefit (35%) revenue streams. Key strengths in technology, biotech, wine, construction, and agribusiness industry sectors. |

31 Strategic focus on disciplined expansion (via organic growth and acquisitions) into key western regional markets. – Leverage existing lines of business expertise – and to develop enhanced “provider-of-choice” branding and pricing positions. – Successful expansion into Seattle (2003) and Nevada (2005). – Entered Oregon in 2006. Commercial Insurance Services Business |

32 Bay Area Sacramento Reno Los Angeles/ Southern CA Seattle Additional Major Western Regional Markets ABD Insurance and Financial Services |

33 ABD Geographic Distribution % of 2005 Revenue ABD Geographic Distribution % of 2005 Revenue Nevada Seattle Bay Area Southern CA/ Central Coast Sacramento 10% 10% 13% 17% 50% |

34 ABD 2005 Revenue Distribution By Size of Client Relationship * ($ in 000’s) ABD 2005 Revenue Distribution By Size of Client Relationship * ($ in 000’s) $5-25 16% $25-50 14% Over $750 2% $500-750 4% $250-500 14% $50-100 21% $100-250 29% Property and Casualty * Excludes relationships of less than $5,000 $5-25 15% Over $750 4% $500-750 4% $250-500 12% $100-250 28% $25-50 16% $50-100 21% Employee Benefits |

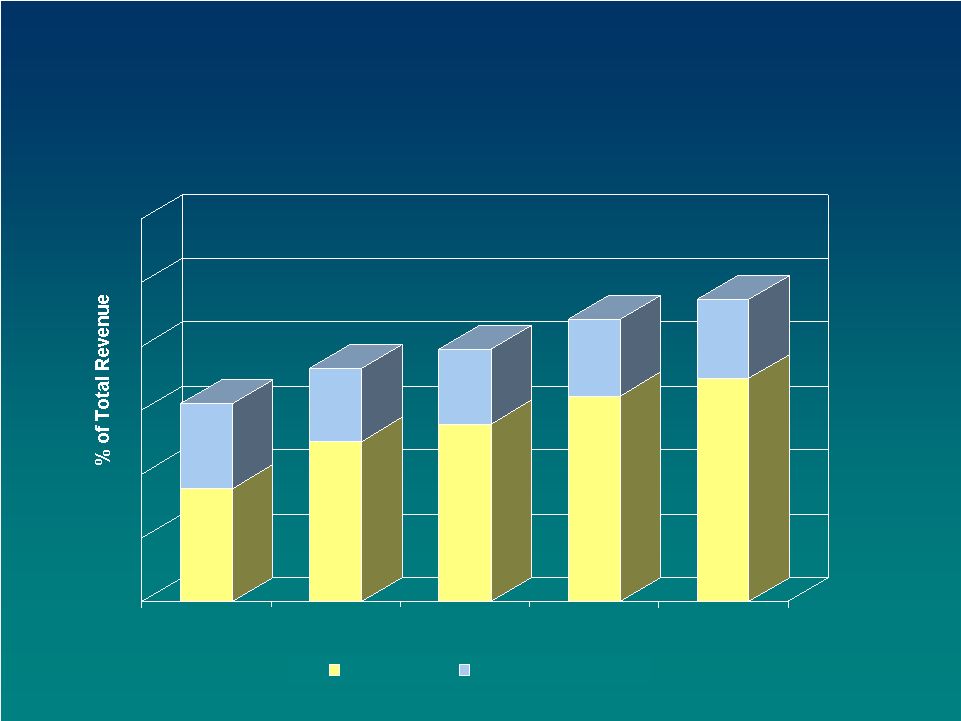

35 Increased Non-Interest Revenue Contribution Increased Non-Interest Revenue Contribution 18% 13% 25% 12% 28% 12% 32% 12% 35% 12% 2002 2003 2004 2005 YTD '06 ABD Other Fee-Based 40% 31% 37% 44% 47% |

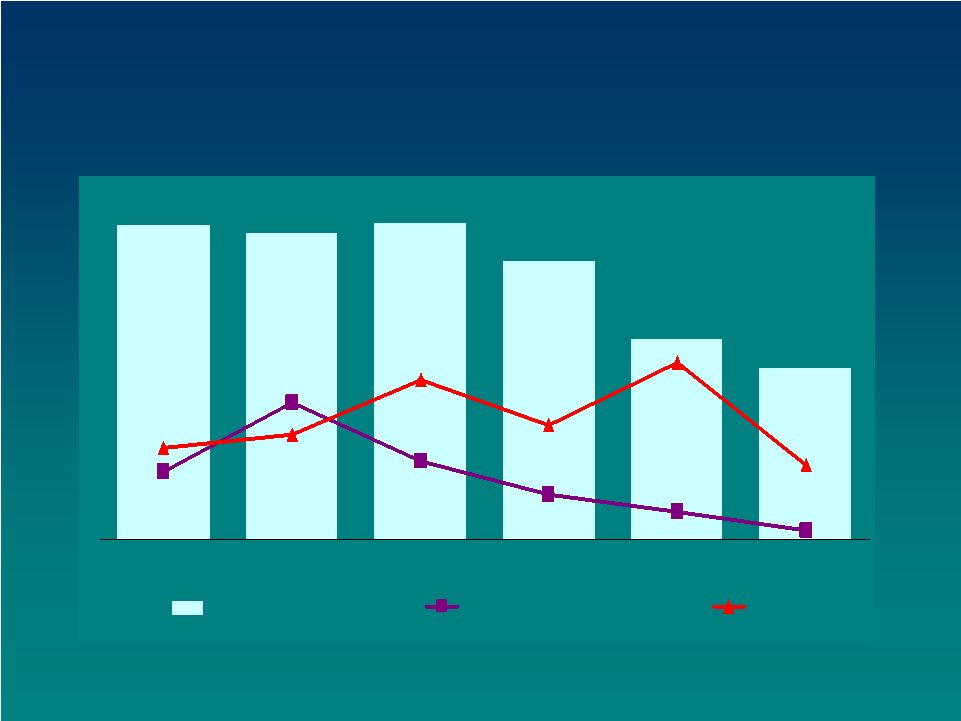

36 Sound Credit Metrics Sound Credit Metrics |

37 Credit Quality Credit Quality 2.63% 2.70% 2.73% 1.73% 2.39% 1.48% 1.18% 0.58% 0.67% 0.08% 0.39% 0.24% 0.79% 0.91% 1.37% 0.99% 1.52% 0.64% Allowance% Net charge-off % NPAs % 2001 2002 2003 2004 200 YTD ‘06 |

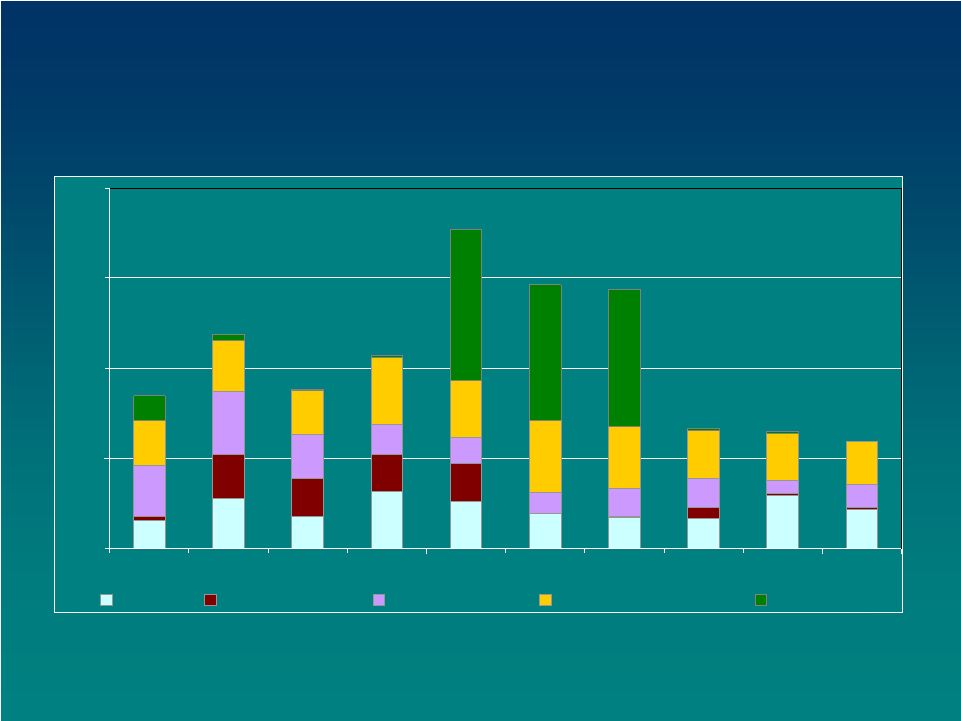

38 Non-Performing Assets by Loan Type Non-Performing Assets by Loan Type $0 $25 $50 $75 $100 6/30/04 9/30/04 12/31/04 3/31/05 6/30/05 9/30/05 12/31/05 3/31/06 6/30/06 9/30/06 CRE Const./Land Commercial Specialty Finance All Other $42 $59 $44 $53 $88* $73* $72* * Includes single borrowing relationship representing $41.6MM at 6/30/05, $36.6MM at 9/30/05 and $36.8MM 12/31/05. $33 $33 $30 |

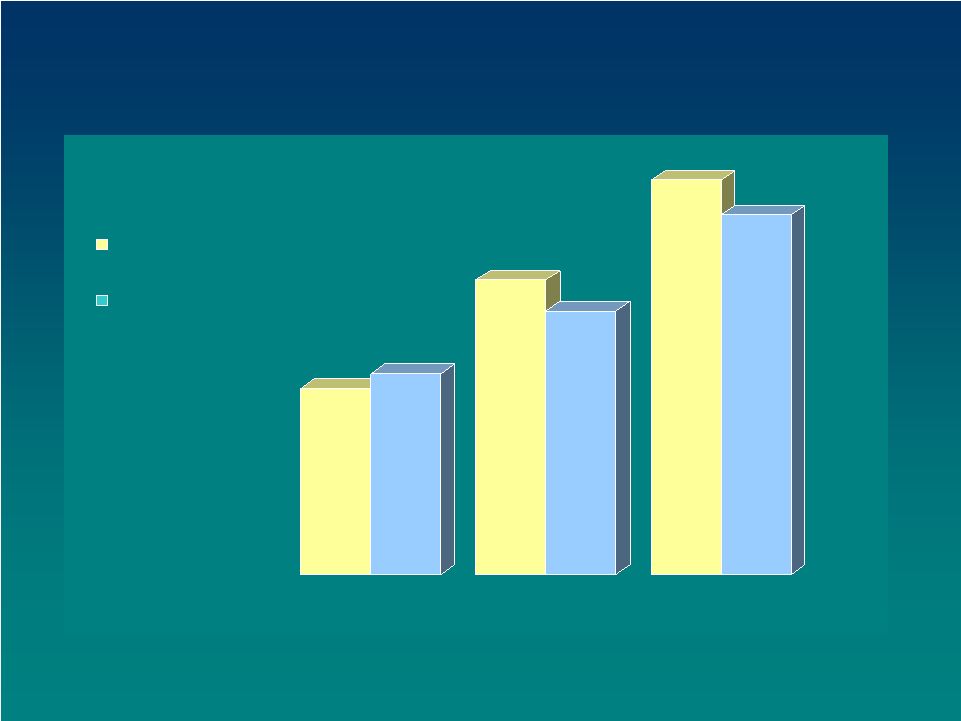

39 Strong Financial Indicators Strong Financial Indicators |

40 Solid Capital Base September 30, 2006 Solid Capital Base September 30, 2006 6.3% 6.8% 10.0% 9.0% 13.4% 12.2% GBBK GBBK Peer Group* Tangible Common % Total Common % Total Risk- Based Ratio * Comparable bank holding companies with assets between $5-$11 billion. |

41 Interest Rate Risk Profile Interest Rate Risk Profile Neutral risk positioning orientation. – Basically matched across maturity spectrum. – Balanced under 1-year gap, but note that assets reset before liabilities. Investment portfolio continues to be managed for minimal credit and controlled convexity risk. Deposit repricing lag, speed and balance behaviors primary position uncertainty. |

42 Quality Management Quality Management |

43 Experienced and Committed Management Team Experienced and Committed Management Team Franklin Templeton, KeyCorp Allen Gula Chief Information Officer ABD, Minet, COMPRO Dan R. Francis Insurance Brokerage Wells Fargo Colleen M. Anderson Community Banking Stanford University, Bank of America, EurekaBank Peggy Hiraoka Human Resources Wells Fargo, ATT Capital Keith Wilton Specialty Finance Cal Fed, OTS Kenneth Shannon Chief Risk Officer Bank of America James S. Westfall Chief Financial Officer Wells Fargo, Bank of America, EurekaBank Byron A. Scordelis Chief Executive Officer Experience Name Officer |

44 2006 Accomplishments of Note 2006 Accomplishments of Note Continuation of solid and quality growth realized in specialty finance and commercial insurance brokerage businesses. – Integration of insurance acquisition successfully completed. – Sustained brisk expansion of MATSCO and GBC franchises. Repositioning of community bank asset portfolio proceeding in concert with stated objectives. – Balanced migration from CRE to construction. – BDO initiative established and growing. Key risk and control metrics favorably reflect devotion of focus and resources. – Credit quality trends sustainably strengthening. – SOX compliance efforts consistent with control-based ethic. |

45 Recent Developments Community Bank Recent Developments Community Bank Reduced number of bank brands from twelve to eight. – Strategic positioning around “natural” regional community banking economic markets. – Including coalescence of four previously unfocused identities in the Santa Clara Valley around single new regional brand. De novo banking and loan production offices – Santa Rosa – opened August 2006 – Oakland – expected opening November 2006 – Livermore – expected opening April 2007 |

46 Focus on the Future Focus on the Future |

47 Key Objectives Key Objectives Drive top-line revenue growth. – Loan and deposit growth in targeted product types and client profiles. • Emphasis on building C&I, construction, and specialty finance lending. • Focus on deposit franchise growth through expanded banking clientele relationships and service quality differentiation. – Maintain pricing and credit underwriting disciplines – Continued insurance brokerage franchise development. Increase operating cost efficiency – Rationalize responsibilities and structures. – Streamlining administrative processes. |

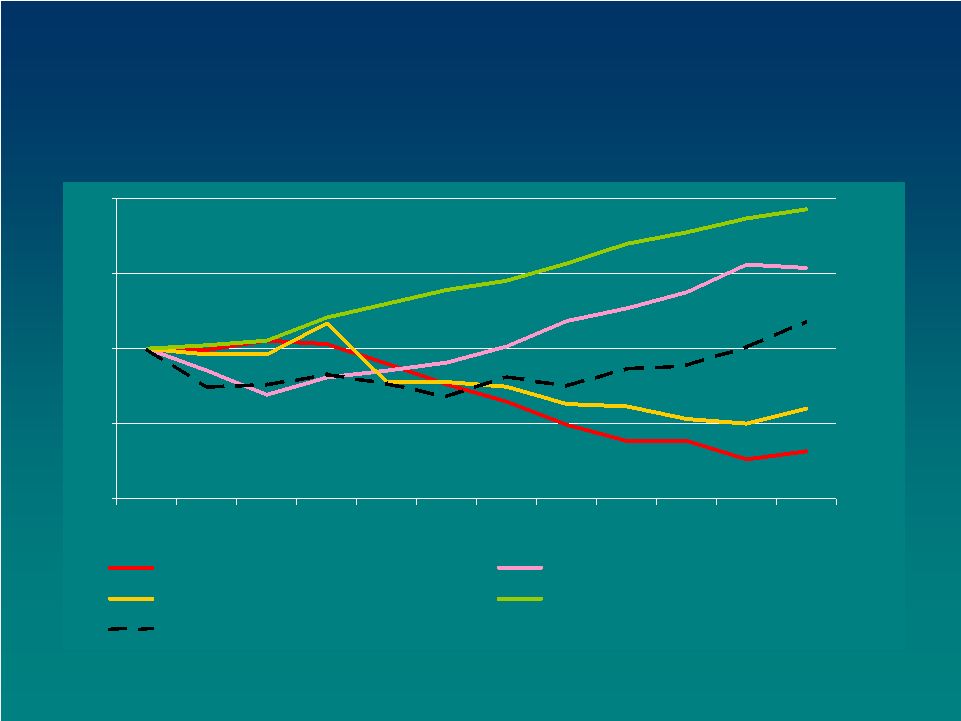

48 Focus on Shareholder Value Focus on Shareholder Value |

49 GBBK Share Price Performance 0% 200% 400% 600% 800% GBBK S&P Bank Index S&P 500 Nasdaq Bank Index |

50 Appendix – Custom Peer Group Appendix – Custom Peer Group Provident Bankshares Corp. Republic Bancorp Inc. Santander Bancorp Sterling Financial Corp. Susquehanna Bancshares, Inc. SVB Financial Group Texas Regional Bancshares, Inc. Trustmark Corp. UCBH Holdings, Inc. UMB Financial Corp. Westamerica Bancorporation Whitney Holding Corp. AMCORE Financial, Inc. Bank of Hawaii Corp. Cathay General Bancorp Central Pacific Financial Corp. Chittenden Corporation Citizens Banking Corp. CVB Financial Corp. First Commonwealth Financial Corp. First Midwest Bancorp, Inc. First Republic Bank FirstMerit Corp. Old National Bancorp Pacific Capital Bancorp |