UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-04409

Eaton Vance Municipals Trust

(Exact Name of Registrant as Specified in Charter)

Two International Place, Boston, Massachusetts 02110

(Address of Principal Executive Offices)

Deidre E. Walsh

Two International Place, Boston, Massachusetts 02110

(Name and Address of Agent for Services)

(617) 482-8260

(Registrant’s Telephone Number)

July 31

Date of Fiscal Year End

January 31, 2023

Date of Reporting Period

Item 1. Reports to Stockholders

Eaton Vance

Municipals Trust

Semiannual Report

January 31, 2023

Arizona • Connecticut • Minnesota • New Jersey • Pennsylvania

Commodity Futures Trading Commission Registration. The Commodity Futures Trading Commission (“CFTC”) has adopted regulations that subject registered investment companies and advisers to regulation by the CFTC if a fund invests more than a prescribed level of its assets in certain CFTC-regulated instruments (including futures, certain options and swap agreements) or markets itself as providing investment exposure to such instruments. The investment adviser has claimed an exclusion from the definition of “commodity pool operator” under the Commodity Exchange Act with respect to its management of each Fund. Accordingly, neither the Funds nor the adviser with respect to the operation of the Funds is subject to CFTC regulation. Because of its management of other strategies, the Funds' adviser is registered with the CFTC as a commodity pool operator. The adviser is also registered as a commodity trading advisor.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

This report must be preceded or accompanied by a current summary prospectus or prospectus. Before investing, investors should consider carefully the investment objective, risks, and charges and expenses of a mutual fund. This and other important information is contained in the summary prospectus and prospectus, which can be obtained from a financial intermediary. Prospective investors should read the prospectus carefully before investing. For further information, please call 1-800-262-1122.

Semiannual Report January 31, 2023

Eaton Vance

Municipal Income Funds

Eaton Vance

Arizona Municipal Income Fund

January 31, 2023

Performance

Portfolio Manager(s) Trevor G. Smith

| % Average Annual Total Returns1,2 | Class

Inception Date | Performance

Inception Date | Six Months | One Year | Five Years | Ten Years |

| Class A at NAV | 12/13/1993 | 07/25/1991 | 0.49% | (3.36)% | 1.54% | 1.92% |

| Class A with 3.25% Maximum Sales Charge | — | — | (2.83) | (6.49) | 0.87 | 1.58 |

| Class C at NAV | 12/16/2005 | 07/25/1991 | (0.01) | (4.18) | 0.77 | 1.32 |

| Class C with 1% Maximum Deferred Sales Charge | — | — | (1.00) | (5.12) | 0.77 | 1.32 |

| Class I at NAV | 08/03/2010 | 07/25/1991 | 0.59 | (3.17) | 1.74 | 2.13 |

|

| Bloomberg Municipal Bond Index | — | — | 0.73% | (3.25)% | 2.07% | 2.38% |

| Bloomberg Arizona Municipal Bond Index | — | — | 0.42 | (3.62) | 1.80 | 2.25 |

| % Total Annual Operating Expense Ratios3 | Class A | Class C | Class I |

| | 0.69% | 1.44% | 0.49% |

| % Distribution Rates/Yields4 | Class A | Class C | Class I |

| Distribution Rate | 2.46% | 1.71% | 2.66% |

| Taxable-Equivalent Distribution Rate | 4.37 | 3.04 | 4.72 |

| SEC 30-day Yield | 2.36 | 1.70 | 2.64 |

| Taxable-Equivalent SEC 30-day Yield | 4.20 | 3.03 | 4.69 |

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Furthermore, returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the redemption of Fund shares. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Arizona Municipal Income Fund

January 31, 2023

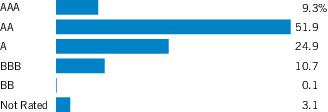

| Credit Quality (% of total investments)1 |

Footnotes:

| 1 | For purposes of the Fund’s rating restrictions, ratings are based on Moody’s Investors Service, Inc. (“Moody’s”), S&P Global Ratings (“S&P”) or Fitch Ratings (“Fitch”), as applicable. If securities are rated differently by the ratings agencies, the highest rating is applied. Ratings, which are subject to change, apply to the creditworthiness of the issuers of the underlying securities and not to the Fund or its shares. Credit ratings measure the quality of a bond based on the issuer’s creditworthiness, with ratings ranging from AAA, being the highest, to D, being the lowest based on S&P’s measures. Ratings of BBB or higher by S&P or Fitch (Baa or higher by Moody’s) are considered to be investment-grade quality. Credit ratings are based largely on the ratings agency’s analysis at the time of rating. The rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition and does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. Holdings designated as “Not Rated” (if any) are not rated by the national ratings agencies stated above. |

Eaton Vance

Connecticut Municipal Income Fund

January 31, 2023

Performance

Portfolio Manager(s) Trevor G. Smith

| % Average Annual Total Returns1,2 | Class

Inception Date | Performance

Inception Date | Six Months | One Year | Five Years | Ten Years |

| Class A at NAV | 04/19/1994 | 05/01/1992 | 0.77% | (2.88)% | 1.54% | 1.86% |

| Class A with 3.25% Maximum Sales Charge | — | — | (2.50) | (6.07) | 0.87 | 1.53 |

| Class C at NAV | 02/09/2006 | 05/01/1992 | 0.28 | (3.63) | 0.78 | 1.25 |

| Class C with 1% Maximum Deferred Sales Charge | — | — | (0.72) | (4.58) | 0.78 | 1.25 |

| Class I at NAV | 03/03/2008 | 05/01/1992 | 0.87 | (2.69) | 1.75 | 2.07 |

|

| Bloomberg Municipal Bond Index | — | — | 0.73% | (3.25)% | 2.07% | 2.38% |

| Bloomberg Connecticut Municipal Bond Index | — | — | 0.90 | (1.74) | 2.47 | 2.23 |

| % Total Annual Operating Expense Ratios3 | Class A | Class C | Class I |

| | 0.69% | 1.44% | 0.49% |

| % Distribution Rates/Yields4 | Class A | Class C | Class I |

| Distribution Rate | 2.38% | 1.63% | 2.58% |

| Taxable-Equivalent Distribution Rate | 4.56 | 3.13 | 4.94 |

| SEC 30-day Yield | 2.29 | 1.63 | 2.57 |

| Taxable-Equivalent SEC 30-day Yield | 4.39 | 3.12 | 4.92 |

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Furthermore, returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the redemption of Fund shares. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Connecticut Municipal Income Fund

January 31, 2023

| Credit Quality (% of total investments)1 |

Footnotes:

| 1 | For purposes of the Fund’s rating restrictions, ratings are based on Moody’s Investors Service, Inc. (“Moody’s”), S&P Global Ratings (“S&P”) or Fitch Ratings (“Fitch”), as applicable. If securities are rated differently by the ratings agencies, the highest rating is applied. Ratings, which are subject to change, apply to the creditworthiness of the issuers of the underlying securities and not to the Fund or its shares. Credit ratings measure the quality of a bond based on the issuer’s creditworthiness, with ratings ranging from AAA, being the highest, to D, being the lowest based on S&P’s measures. Ratings of BBB or higher by S&P or Fitch (Baa or higher by Moody’s) are considered to be investment-grade quality. Credit ratings are based largely on the ratings agency’s analysis at the time of rating. The rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition and does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. Holdings designated as “Not Rated” (if any) are not rated by the national ratings agencies stated above. |

Eaton Vance

Minnesota Municipal Income Fund

January 31, 2023

Performance

Portfolio Manager(s) Christopher J. Eustance, CFA and Julie P. Callahan, CFA

| % Average Annual Total Returns1,2 | Class

Inception Date | Performance

Inception Date | Six Months | One Year | Five Years | Ten Years |

| Class A at NAV | 12/09/1993 | 07/29/1991 | 0.57% | (2.15)% | 1.69% | 1.84% |

| Class A with 3.25% Maximum Sales Charge | — | — | (2.71) | (5.33) | 1.02 | 1.51 |

| Class C at NAV | 12/21/2005 | 07/29/1991 | 0.23 | (2.88) | 0.93 | 1.24 |

| Class C with 1% Maximum Deferred Sales Charge | — | — | (0.77) | (3.84) | 0.93 | 1.24 |

| Class I at NAV | 08/03/2010 | 07/29/1991 | 0.67 | (1.95) | 1.89 | 2.04 |

|

| Bloomberg Municipal Bond Index | — | — | 0.73% | (3.25)% | 2.07% | 2.38% |

| Bloomberg Minnesota Municipal Bond Index | — | — | 0.96 | (2.54) | 1.93 | 2.08 |

| % Total Annual Operating Expense Ratios3 | Class A | Class C | Class I |

| | 0.66% | 1.41% | 0.46% |

| % Distribution Rates/Yields4 | Class A | Class C | Class I |

| Distribution Rate | 2.20% | 1.45% | 2.40% |

| Taxable-Equivalent Distribution Rate | 4.45 | 2.95 | 4.85 |

| SEC 30-day Yield | 2.22 | 1.56 | 2.49 |

| Taxable-Equivalent SEC 30-day Yield | 4.50 | 3.16 | 5.05 |

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Furthermore, returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the redemption of Fund shares. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Minnesota Municipal Income Fund

January 31, 2023

| Credit Quality (% of total investments)1 |

Footnotes:

| 1 | For purposes of the Fund’s rating restrictions, ratings are based on Moody’s Investors Service, Inc. (“Moody’s”), S&P Global Ratings (“S&P”) or Fitch Ratings (“Fitch”), as applicable. If securities are rated differently by the ratings agencies, the highest rating is applied. Ratings, which are subject to change, apply to the creditworthiness of the issuers of the underlying securities and not to the Fund or its shares. Credit ratings measure the quality of a bond based on the issuer’s creditworthiness, with ratings ranging from AAA, being the highest, to D, being the lowest based on S&P’s measures. Ratings of BBB or higher by S&P or Fitch (Baa or higher by Moody’s) are considered to be investment-grade quality. Credit ratings are based largely on the ratings agency’s analysis at the time of rating. The rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition and does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. Holdings designated as “Not Rated” (if any) are not rated by the national ratings agencies stated above. |

Eaton Vance

New Jersey Municipal Income Fund

January 31, 2023

Performance

Portfolio Manager(s) Cynthia J. Clemson, Christopher J. Eustance, CFA and Julie P. Callahan, CFA

| % Average Annual Total Returns1,2 | Class

Inception Date | Performance

Inception Date | Six Months | One Year | Five Years | Ten Years |

| Class A at NAV | 04/13/1994 | 01/08/1991 | 0.02% | (4.97)% | 1.91% | 2.10% |

| Class A with 3.25% Maximum Sales Charge | — | — | (3.27) | (8.10) | 1.23 | 1.76 |

| Class C at NAV | 12/14/2005 | 01/08/1991 | (0.41) | (5.79) | 1.13 | 1.48 |

| Class C with 1% Maximum Deferred Sales Charge | — | — | (1.40) | (6.71) | 1.13 | 1.48 |

| Class I at NAV | 03/03/2008 | 01/08/1991 | 0.12 | (4.87) | 2.09 | 2.29 |

|

| Bloomberg Municipal Bond Index | — | — | 0.73% | (3.25)% | 2.07% | 2.38% |

| Bloomberg New Jersey Municipal Bond Index | — | — | 1.08 | (3.00) | 2.94 | 2.98 |

| % Total Annual Operating Expense Ratios3 | Class A | Class C | Class I |

| | 0.69% | 1.44% | 0.49% |

| % Distribution Rates/Yields4 | Class A | Class C | Class I |

| Distribution Rate | 2.72% | 1.98% | 2.92% |

| Taxable-Equivalent Distribution Rate | 5.62 | 4.08 | 6.03 |

| SEC 30-day Yield | 2.56 | 1.90 | 2.84 |

| Taxable-Equivalent SEC 30-day Yield | 5.28 | 3.93 | 5.86 |

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Furthermore, returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the redemption of Fund shares. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

New Jersey Municipal Income Fund

January 31, 2023

| Credit Quality (% of total investments)1 |

Footnotes:

| 1 | For purposes of the Fund’s rating restrictions, ratings are based on Moody’s Investors Service, Inc. (“Moody’s”), S&P Global Ratings (“S&P”) or Fitch Ratings (“Fitch”), as applicable. If securities are rated differently by the ratings agencies, the highest rating is applied. Ratings, which are subject to change, apply to the creditworthiness of the issuers of the underlying securities and not to the Fund or its shares. Credit ratings measure the quality of a bond based on the issuer’s creditworthiness, with ratings ranging from AAA, being the highest, to D, being the lowest based on S&P’s measures. Ratings of BBB or higher by S&P or Fitch (Baa or higher by Moody’s) are considered to be investment-grade quality. Credit ratings are based largely on the ratings agency’s analysis at the time of rating. The rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition and does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. Holdings designated as “Not Rated” (if any) are not rated by the national ratings agencies stated above. |

Eaton Vance

Pennsylvania Municipal Income Fund

January 31, 2023

Performance

Portfolio Manager(s) Christopher J. Eustance, CFA

| % Average Annual Total Returns1,2 | Class

Inception Date | Performance

Inception Date | Six Months | One Year | Five Years | Ten Years |

| Class A at NAV | 06/01/1994 | 01/08/1991 | 0.60% | (4.32)% | 1.43% | 1.79% |

| Class A with 3.25% Maximum Sales Charge | — | — | (2.71) | (7.38) | 0.76 | 1.46 |

| Class C at NAV | 01/13/2006 | 01/08/1991 | 0.13 | (5.02) | 0.66 | 1.18 |

| Class C with 1% Maximum Deferred Sales Charge | — | — | (0.86) | (5.95) | 0.66 | 1.18 |

| Class I at NAV | 03/03/2008 | 01/08/1991 | 0.70 | (4.10) | 1.62 | 1.99 |

|

| Bloomberg Municipal Bond Index | — | — | 0.73% | (3.25)% | 2.07% | 2.38% |

| Bloomberg Pennsylvania Municipal Bond Index | — | — | 0.63 | (3.74) | 2.28 | 2.64 |

| % Total Annual Operating Expense Ratios3 | Class A | Class C | Class I |

| | 0.74% | 1.49% | 0.54% |

| % Distribution Rates/Yields4 | Class A | Class C | Class I |

| Distribution Rate | 2.87% | 2.13% | 3.07% |

| Taxable-Equivalent Distribution Rate | 5.12 | 3.79 | 5.47 |

| SEC 30-day Yield | 2.52 | 1.86 | 2.80 |

| Taxable-Equivalent SEC 30-day Yield | 4.48 | 3.31 | 4.98 |

| % Total Leverage5 | |

| Residual Interest Bond (RIB) Financing | 3.07% |

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Furthermore, returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the redemption of Fund shares. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Pennsylvania Municipal Income Fund

January 31, 2023

| Credit Quality (% of total investments)1,2 |

Footnotes:

| 1 | For purposes of the Fund’s rating restrictions, ratings are based on Moody’s Investors Service, Inc. (“Moody’s”), S&P Global Ratings (“S&P”) or Fitch Ratings (“Fitch”), as applicable. If securities are rated differently by the ratings agencies, the highest rating is applied. Ratings, which are subject to change, apply to the creditworthiness of the issuers of the underlying securities and not to the Fund or its shares. Credit ratings measure the quality of a bond based on the issuer’s creditworthiness, with ratings ranging from AAA, being the highest, to D, being the lowest based on S&P’s measures. Ratings of BBB or higher by S&P or Fitch (Baa or higher by Moody’s) are considered to be investment-grade quality. Credit ratings are based largely on the ratings agency’s analysis at the time of rating. The rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition and does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. Holdings designated as “Not Rated” (if any) are not rated by the national ratings agencies stated above. |

| 2 | The chart includes the municipal bonds held by a trust that issues residual interest bonds, consistent with the Portfolio of Investments. |

Eaton Vance

Municipal Income Funds

January 31, 2023

Endnotes and Additional Disclosures

| 1 | Bloomberg Municipal Bond Index is an unmanaged index of municipal bonds traded in the U.S. Bloomberg Arizona Municipal Bond Index is an unmanaged index of Arizona municipal bonds. Bloomberg Connecticut Municipal Bond Index is an unmanaged index of Connecticut municipal bonds. Bloomberg Minnesota Municipal Bond Index is an unmanaged index of Minnesota municipal bonds. Bloomberg New Jersey Municipal Bond Index is an unmanaged index of New Jersey municipal bonds. Bloomberg Pennsylvania Municipal Bond Index is an unmanaged index of Pennsylvania municipal bonds. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. |

| 2 | Total Returns at NAV do not include applicable sales charges. If sales charges were deducted, the returns would be lower. Total Returns shown with maximum sales charge reflect the stated maximum sales charge. Unless otherwise stated, performance does not reflect the deduction of taxes on Fund distributions or redemptions of Fund shares.Effective November 5, 2020, Class C shares automatically convert to Class A shares eight years after purchase. The average annual total returns listed for Class C reflect conversion to Class A shares after eight years. Prior to November 5, 2020, Class C shares automatically converted to Class A shares ten years after purchase. |

| 3 | Source: Fund prospectus. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report. |

| 4 | The Distribution Rate is based on the Fund’s last regular distribution per share in the period (annualized) divided by the Fund’s NAV at the end of the period. The Fund’s distributions may be comprised of amounts characterized for federal income tax purposes as tax-exempt income, qualified and non-qualified ordinary dividends, capital gains and nondividend distributions, also known as return of capital. The Fund will determine the federal income tax character of distributions paid to a shareholder after the end of the calendar year. This is reported on the IRS form 1099-DIV and provided to the shareholder shortly after each year-end.The Fund’s distributions are determined by the investment adviser based on its current assessment of the Fund’s long-term return potential. As portfolio and market conditions change, the rate of distributions paid by the Fund could change. Taxable-equivalent performance is based on the highest combined federal and state income tax rates, where applicable. Lower tax rates would result in lower tax-equivalent performance. Actual tax rates will vary depending on your income, exemptions and deductions. Rates do not include local taxes. The SEC Yield is a standardized measure based on the estimated yield to maturity of a fund’s investments over a 30-day period and is based on the maximum offer price at the date specified. The SEC Yield is not based on the distributions made by the Fund, which may differ. |

| 5 | Fund employs RIB financing. The leverage created by RIB investments provides an opportunity for increased income but, at the same time, creates special risks (including the likelihood of greater volatility of NAV). The cost of leverage rises and falls with changes in short-term interest rates. See “Floating Rate Notes Issued in Conjunction with Securities Held” in the notes to the financial statements for more information about RIB financing. RIB leverage represents the amount of Floating Rate Notes outstanding at period end as a percentage of |

| | Fund net assets plus Floating Rate Notes. |

| | Fund profiles subject to change due to active management. |

Eaton Vance

Municipal Income Funds

January 31, 2023

Example

As a Fund shareholder, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchases; and (2) ongoing costs, including management fees; distribution and/or service fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of Fund investing and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (August 1, 2022 to January 31, 2023).

Actual Expenses

The first section of each table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second section of each table below provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual Fund return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in each table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second section of each table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would be higher.

Eaton Vance Arizona Municipal Income Fund

| | Beginning

Account Value

(8/1/22) | Ending

Account Value

(1/31/23) | Expenses Paid

During Period*

(8/1/22 – 1/31/23) | Annualized

Expense

Ratio |

| Actual | | | | |

| Class A | $1,000.00 | $1,004.90 | $3.69 | 0.73% |

| Class C | $1,000.00 | $ 999.90 | $7.46 | 1.48% |

| Class I | $1,000.00 | $1,005.90 | $2.68 | 0.53% |

| |

| Hypothetical | | | | |

| (5% return per year before expenses) | | | | |

| Class A | $1,000.00 | $1,021.53 | $3.72 | 0.73% |

| Class C | $1,000.00 | $1,017.75 | $7.53 | 1.48% |

| Class I | $1,000.00 | $1,022.53 | $2.70 | 0.53% |

| * | Expenses are equal to the Fund's annualized expense ratio for the indicated Class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on July 31, 2022. |

Eaton Vance

Municipal Income Funds

January 31, 2023

Fund Expenses — continued

Eaton Vance Connecticut Municipal Income Fund

| | Beginning

Account Value

(8/1/22) | Ending

Account Value

(1/31/23) | Expenses Paid

During Period*

(8/1/22 – 1/31/23) | Annualized

Expense

Ratio |

| Actual | | | | |

| Class A | $1,000.00 | $1,007.70 | $3.64 | 0.72% |

| Class C | $1,000.00 | $1,002.80 | $7.42 | 1.47% |

| Class I | $1,000.00 | $1,008.70 | $2.63 | 0.52% |

| |

| Hypothetical | | | | |

| (5% return per year before expenses) | | | | |

| Class A | $1,000.00 | $1,021.58 | $3.67 | 0.72% |

| Class C | $1,000.00 | $1,017.80 | $7.48 | 1.47% |

| Class I | $1,000.00 | $1,022.58 | $2.65 | 0.52% |

| * | Expenses are equal to the Fund's annualized expense ratio for the indicated Class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on July 31, 2022. |

Eaton Vance Minnesota Municipal Income Fund

| | Beginning

Account Value

(8/1/22) | Ending

Account Value

(1/31/23) | Expenses Paid

During Period*

(8/1/22 – 1/31/23) | Annualized

Expense

Ratio |

| Actual | | | | |

| Class A | $1,000.00 | $1,005.70 | $3.49 | 0.69% |

| Class C | $1,000.00 | $1,002.30 | $7.27 | 1.44% |

| Class I | $1,000.00 | $1,006.70 | $2.48 | 0.49% |

| |

| Hypothetical | | | | |

| (5% return per year before expenses) | | | | |

| Class A | $1,000.00 | $1,021.73 | $3.52 | 0.69% |

| Class C | $1,000.00 | $1,017.95 | $7.32 | 1.44% |

| Class I | $1,000.00 | $1,022.74 | $2.50 | 0.49% |

| * | Expenses are equal to the Fund's annualized expense ratio for the indicated Class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on July 31, 2022. |

Eaton Vance

Municipal Income Funds

January 31, 2023

Fund Expenses — continued

Eaton Vance New Jersey Municipal Income Fund

| | Beginning

Account Value

(8/1/22) | Ending

Account Value

(1/31/23) | Expenses Paid

During Period*

(8/1/22 – 1/31/23) | Annualized

Expense

Ratio |

| Actual | | | | |

| Class A | $1,000.00 | $1,000.20 | $3.73 | 0.74% |

| Class C | $1,000.00 | $ 995.90 | $7.50 | 1.49% |

| Class I | $1,000.00 | $1,001.20 | $2.72 | 0.54% |

| |

| Hypothetical | | | | |

| (5% return per year before expenses) | | | | |

| Class A | $1,000.00 | $1,021.48 | $3.77 | 0.74% |

| Class C | $1,000.00 | $1,017.69 | $7.58 | 1.49% |

| Class I | $1,000.00 | $1,022.48 | $2.75 | 0.54% |

| * | Expenses are equal to the Fund's annualized expense ratio for the indicated Class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on July 31, 2022. |

Eaton Vance Pennsylvania Municipal Income Fund

| | Beginning

Account Value

(8/1/22) | Ending

Account Value

(1/31/23) | Expenses Paid

During Period*

(8/1/22 – 1/31/23) | Annualized

Expense

Ratio |

| Actual | | | | |

| Class A | $1,000.00 | $1,006.00 | $4.30 | 0.85% |

| Class C | $1,000.00 | $1,001.30 | $8.07 | 1.60% |

| Class I | $1,000.00 | $1,007.00 | $3.29 | 0.65% |

| |

| Hypothetical | | | | |

| (5% return per year before expenses) | | | | |

| Class A | $1,000.00 | $1,020.92 | $4.33 | 0.85% |

| Class C | $1,000.00 | $1,017.14 | $8.13 | 1.60% |

| Class I | $1,000.00 | $1,021.93 | $3.31 | 0.65% |

| * | Expenses are equal to the Fund's annualized expense ratio for the indicated Class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on July 31, 2022. |

Eaton Vance

Arizona Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited)

| Tax-Exempt Municipal Obligations — 93.9% |

| Security | Principal

Amount

(000's omitted) | Value |

| Education — 12.6% |

| Arizona Industrial Development Authority, (Academies of Math & Science), 5.00%, 7/1/39(1) | $ | 250 | $ 250,667 |

| Arizona Industrial Development Authority, (Doral Academy of Nevada): | | | |

| 5.00%, 7/15/39(1) | | 55 | 53,891 |

| 5.00%, 7/15/40(1) | | 350 | 340,847 |

| Arizona Industrial Development Authority, (Pinecrest Academy of Nevada), 4.00%, 7/15/50(1) | | 60 | 47,683 |

| Arizona Industrial Development Authority, (Somerset Academy of Las Vegas), 3.00%, 12/15/31(1) | | 525 | 471,487 |

| Arizona State University, 5.00%, 7/1/36 | | 1,150 | 1,203,015 |

| Glendale Industrial Development Authority, AZ, (Midwestern University Foundation), (AMT), 2.125%, 7/1/33 | | 250 | 219,415 |

| La Paz County Industrial Development Authority, AZ, (Harmony Public Schools), 4.00%, 2/15/41 | | 430 | 384,115 |

| Maricopa County Industrial Development Authority, AZ, (Legacy Traditional Schools), 4.00%, 7/1/41(1) | | 500 | 428,895 |

| Northern Arizona University, 5.00%, 6/1/38 | | 1,000 | 1,064,330 |

| Pima County Community College District, AZ: | | | |

| 5.00%, 7/1/33 | | 300 | 337,419 |

| 5.00%, 7/1/35 | | 720 | 799,711 |

| University of Arizona: | | | |

| 5.00%, 6/1/38 | | 1,500 | 1,598,445 |

| 5.00%, 8/1/38 | | 600 | 675,894 |

| 5.00%, 6/1/42 | | 1,500 | 1,647,765 |

| | | | $ 9,523,579 |

| Electric Utilities — 7.6% |

| Mesa, AZ, Utility Systems Revenue: | | | |

| 4.00%, 7/1/31 | $ | 1,160 | $ 1,218,638 |

| 5.00%, 7/1/36 | | 1,000 | 1,210,760 |

| Pinal County Electrical District No. 3, AZ, 5.00%, 7/1/33 | | 1,000 | 1,072,990 |

| Salt River Project Agricultural Improvement and Power District, AZ: | | | |

| 5.00%, 1/1/35 | | 1,000 | 1,114,970 |

| 5.00%, 1/1/45 | | 1,000 | 1,118,350 |

| | | | $ 5,735,708 |

| Escrowed/Prerefunded — 0.3% |

| Kyrene Elementary School District No. 28, AZ, Prerefunded to 7/1/23, 5.50%, 7/1/30 | $ | 200 | $ 202,566 |

| | | | $ 202,566 |

| Security | Principal

Amount

(000's omitted) | Value |

| General Obligations — 10.6% |

| Chandler Unified School District No. 80, AZ, 4.00%, 7/1/33 | $ | 225 | $ 236,048 |

| Paradise Valley Unified School District No. 69, AZ, 4.00%, 7/1/42 | | 1,550 | 1,586,115 |

| Phoenix Union High School District No. 210, AZ, 4.00%, 7/1/39 | | 300 | 308,226 |

| Phoenix, AZ, 5.00%, 7/1/25 | | 1,320 | 1,404,968 |

| Puerto Rico, 5.625%, 7/1/29 | | 500 | 532,445 |

| Scottsdale Unified School District No. 48, AZ, 5.00%, 7/1/31 | | 750 | 835,867 |

| Scottsdale, AZ, 4.00%, 7/1/39(2) | | 1,500 | 1,578,345 |

| Tempe, AZ, 5.00%, 7/1/30 | | 1,000 | 1,143,180 |

| Western Maricopa Education Center District No. 402, AZ, 4.50%, 7/1/34 | | 350 | 355,905 |

| | | | $ 7,981,099 |

| Hospital — 10.1% |

| Arizona Health Facilities Authority, (Scottsdale Lincoln Hospitals), 5.00%, 12/1/39 | $ | 1,665 | $ 1,699,965 |

| Arizona Industrial Development Authority, (Phoenix Children's Hospitals), (LOC: JPMorgan Chase Bank, N.A.), 1.20%, 2/1/48(3) | | 2,000 | 2,000,000 |

| Maricopa County Industrial Development Authority, AZ, (Banner Health): | | | |

| 4.00%, 1/1/44 | | 1,000 | 979,100 |

| 4.00%, 1/1/45 | | 1,000 | 975,870 |

| Maricopa County Industrial Development Authority, AZ, (HonorHealth), 5.00%, 9/1/32 | | 400 | 447,592 |

| Yavapai County Industrial Development Authority, AZ, (Yavapai Regional Medical Center), 5.25%, 8/1/33 | | 500 | 504,735 |

| Yuma Industrial Development Authority, AZ, (Yuma Regional Medical Center), 5.00%, 8/1/32 | | 1,005 | 1,027,301 |

| | | | $ 7,634,563 |

| Housing — 2.3% |

| Phoenix Industrial Development Authority, AZ, (Downtown Phoenix Student Housing II, LLC - Arizona State University): | | | |

| 5.00%, 7/1/39 | $ | 500 | $ 512,375 |

| 5.00%, 7/1/44 | | 250 | 253,132 |

| Phoenix Industrial Development Authority, AZ, (Downtown Phoenix Student Housing, LLC - Arizona State University): | | | |

| 5.00%, 7/1/27 | | 415 | 433,331 |

| 5.00%, 7/1/37 | | 500 | 510,425 |

| | | | $ 1,709,263 |

16

See Notes to Financial Statements.

Eaton Vance

Arizona Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited) — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Industrial Development Revenue — 4.2% |

| Chandler Industrial Development Authority, AZ, (Intel Corp.), (AMT), 5.00% to 9/1/27 (Put Date), 9/1/52 | $ | 2,000 | $ 2,119,380 |

| Maricopa County Pollution Control Corp., AZ, (El Paso Electric Co.): | | | |

| 3.60%, 2/1/40 | | 250 | 229,138 |

| 4.50%, 8/1/42 | | 850 | 850,221 |

| | | | $ 3,198,739 |

| Insured - Electric Utilities — 2.3% |

| Mesa, AZ, Utility Systems Revenue: | | | |

| (NPFG), 5.00%, 7/1/23 | $ | 430 | $ 434,515 |

| (NPFG), Escrowed to Maturity, 5.00%, 7/1/23 | | 450 | 454,666 |

| (NPFG), Escrowed to Maturity, 5.00%, 7/1/23 | | 120 | 121,295 |

| Puerto Rico Electric Power Authority: | | | |

| (NPFG), 5.25%, 7/1/29 | | 485 | 491,557 |

| Series SS, (NPFG), 5.00%, 7/1/25 | | 245 | 245,299 |

| | | | $ 1,747,332 |

| Insured - General Obligations — 11.8% |

| Apache Junction Unified School District No. 43, AZ, (AGM), 5.00%, 7/1/24 | $ | 1,200 | $ 1,240,968 |

| Marana Unified School District No. 6, AZ, (AGM), 4.00%, 7/1/37 | | 500 | 522,025 |

| Maricopa County Elementary School District No. 2, AZ, (AGM), 5.00%, 7/1/34 | | 1,000 | 1,187,210 |

| Maricopa County Elementary School District No. 3, AZ, (AGM), 5.00%, 7/1/25 | | 2,670 | 2,839,919 |

| Maricopa County Elementary School District No. 25, AZ, (AGM), 4.375%, 7/1/42 | | 2,120 | 2,302,320 |

| Maricopa County Elementary School District No. 66, AZ: | | | |

| (BAM), 4.00%, 7/1/37 | | 375 | 393,236 |

| (BAM), 4.00%, 7/1/39 | | 400 | 414,212 |

| | | | $ 8,899,890 |

| Insured - Lease Revenue/Certificates of Participation — 2.0% |

| Higley Unified School District No. 60, AZ, Certificates of Participation: | | | |

| (AGM), 4.125%, 6/1/42(2) | $ | 500 | $ 506,585 |

| (AGM), 4.25%, 6/1/47(2) | | 1,000 | 1,010,250 |

| | | | $ 1,516,835 |

| Insured - Special Tax Revenue — 4.5% |

| Glendale, AZ, Transportation Excise Tax Revenue, (AGM), 5.00%, 7/1/30 | $ | 1,250 | $ 1,323,500 |

| Security | Principal

Amount

(000's omitted) | Value |

| Insured - Special Tax Revenue (continued) |

| Phoenix Civic Improvement Corp., AZ, (Civic Plaza), (NPFG), 5.50%, 7/1/41 | $ | 1,635 | $ 2,061,310 |

| | | | $ 3,384,810 |

| Other Revenue — 1.9% |

| Salt Verde Financial Corp., AZ, Senior Gas Revenue, 5.00%, 12/1/37 | $ | 1,355 | $ 1,437,316 |

| | | | $ 1,437,316 |

| Senior Living/Life Care — 2.0% |

| Glendale Industrial Development Authority, AZ, (Royal Oaks - Inspirata Pointe), 5.00%, 5/15/41 | $ | 500 | $ 475,225 |

| Glendale Industrial Development Authority, AZ, (Terraces of Phoenix), 4.00%, 7/1/28 | | 225 | 209,273 |

| Tempe Industrial Development Authority, AZ, (Friendship Village of Tempe): | | | |

| 4.00%, 12/1/29 | | 380 | 359,480 |

| 4.00%, 12/1/30 | | 500 | 468,205 |

| | | | $ 1,512,183 |

| Special Tax Revenue — 7.9% |

| American Samoa Economic Development Authority, 5.00%, 9/1/38(1) | $ | 200 | $ 201,568 |

| Bullhead City, AZ, Excise Taxes Revenue: | | | |

| 0.75%, 7/1/25 | | 40 | 37,738 |

| 1.30%, 7/1/28 | | 500 | 459,050 |

| 2.10%, 7/1/36 | | 580 | 474,765 |

| 2.55%, 7/1/46 | | 125 | 92,019 |

| 4.00%, 7/1/32 | | 275 | 293,711 |

| Phoenix Civic Improvement Corp., AZ, Excise Tax Revenue, 4.00%, 7/1/45 | | 1,000 | 1,005,790 |

| Pinal County, AZ, Pledged Revenue: | | | |

| 4.00%, 8/1/33 | | 600 | 640,872 |

| 4.00%, 8/1/36 | | 500 | 520,440 |

| Puerto Rico Sales Tax Financing Corp., 5.00%, 7/1/58 | | 1,000 | 987,740 |

| Queen Creek, AZ, Excise Tax and State Shared Revenue, 5.00%, 8/1/30 | | 1,165 | 1,269,978 |

| | | | $ 5,983,671 |

| Transportation — 6.6% |

| Arizona Transportation Board, Highway Revenue, 5.00%, 7/1/33 | $ | 1,000 | $ 1,032,450 |

| Phoenix Civic Improvement Corp., AZ, Airport Revenue: | | | |

| (AMT), 4.00%, 7/1/37 | | 1,500 | 1,491,900 |

| (AMT), 4.00%, 7/1/38 | | 1,000 | 993,550 |

17

See Notes to Financial Statements.

Eaton Vance

Arizona Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited) — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Transportation (continued) |

Phoenix Civic Improvement Corp., AZ, Airport Revenue:

(continued) | | | |

| (AMT), 5.00%, 7/1/49 | $ | 1,455 | $ 1,513,724 |

| | | | $ 5,031,624 |

| Water and Sewer — 7.2% |

| Central Arizona Water Conservation District, 5.00%, 1/1/35 | $ | 1,500 | $ 1,594,605 |

| Gilbert Water Resources Municipal Property Corp., AZ: | | | |

| 4.00%, 7/1/36 | | 750 | 772,402 |

| Green Bonds, 4.00%, 7/15/47 | | 1,000 | 1,002,640 |

| Phoenix Civic Improvement Corp., AZ, Wastewater System Revenue, 5.00%, 7/1/28 | | 860 | 893,385 |

| Tucson, AZ, Water System Revenue: | | | |

| 5.00%, 7/1/32 | | 545 | 601,844 |

| 5.00%, 7/1/35 | | 530 | 581,092 |

| | | | $ 5,445,968 |

Total Tax-Exempt Municipal Obligations

(identified cost $70,175,010) | | | $ 70,945,146 |

| Taxable Municipal Obligations — 4.8% |

| Security | Principal

Amount

(000's omitted) | Value |

| Education — 0.3% |

| Arizona Industrial Development Authority, (Doral Academy of Northern Nevada), 3.375%, 7/15/25(1) | $ | 175 | $ 167,379 |

| La Paz County Industrial Development Authority, AZ, (Harmony Public Schools), 3.00%, 2/15/24 | | 45 | 44,005 |

| | | | $ 211,384 |

| General Obligations — 0.8% |

| Maricopa County Elementary School District No. 2, AZ, 4.50%, 7/1/24 | $ | 655 | $ 650,952 |

| | | | $ 650,952 |

| Special Tax Revenue — 3.7% |

| Coconino County, AZ, Pledged Revenue, 4.073%, 7/1/23 | $ | 500 | $ 498,680 |

| Cottonwood, AZ, Pledged Revenue, 2.625%, 7/1/35 | | 850 | 692,206 |

| Tempe, AZ, Transit Excise Tax Revenue: | | | |

| 1.145%, 7/1/27 | | 540 | 473,115 |

| Security | Principal

Amount

(000's omitted) | Value |

| Special Tax Revenue (continued) |

| Tempe, AZ, Transit Excise Tax Revenue: (continued) | | | |

| 1.345%, 7/1/28 | $ | 1,330 | $ 1,145,476 |

| | | | $ 2,809,477 |

Total Taxable Municipal Obligations

(identified cost $4,141,962) | | | $ 3,671,813 |

| Security | Notional

Amount

(000's omitted) | Value |

| Transportation — 0.7% |

| HTA TRRB 2005L-745190UR7 Assured Custodial Trust, 5.25%, 7/1/41 | $ | 500 | $ 504,925 |

Total Trust Units

(identified cost $497,285) | | | $ 504,925 |

Total Investments — 99.4%

(identified cost $74,814,257) | | | $ 75,121,884 |

| Other Assets, Less Liabilities — 0.6% | | | $ 430,783 |

| Net Assets — 100.0% | | | $ 75,552,667 |

| The percentage shown for each investment category in the Portfolio of Investments is based on net assets. |

| (1) | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities may be sold in certain transactions in reliance on an exemption from registration (normally to qualified institutional buyers). At January 31, 2023, the aggregate value of these securities is $1,962,418 or 2.6% of the Fund's net assets. |

| (2) | When-issued security. |

| (3) | Variable rate demand obligation that may be tendered at par on any day for payment the same or next business day. The stated interest rate, which generally resets daily, is determined by the remarketing agent and represents the rate in effect at January 31, 2023. |

| The Fund invests primarily in debt securities issued by Arizona municipalities. The ability of the issuers of the debt securities to meet their obligations may be affected by economic developments in a specific industry or municipality. At January 31, 2023, 20.7% of total investments are backed by bond insurance of various financial institutions and financial guaranty assurance agencies. The aggregate percentage insured by an individual financial institution or financial guaranty assurance agency ranged from 1.1% to 14.6% of total investments. |

18

See Notes to Financial Statements.

Eaton Vance

Arizona Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited) — continued

| Abbreviations: |

| AGM | – Assured Guaranty Municipal Corp. |

| AMT | – Interest earned from these securities may be considered a tax preference item for purposes of the Federal Alternative Minimum Tax. |

| BAM | – Build America Mutual Assurance Co. |

| LOC | – Letter of Credit |

| NPFG | – National Public Finance Guarantee Corp. |

19

See Notes to Financial Statements.

Eaton Vance

Connecticut Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited)

| Security | Principal

Amount

(000's omitted) | Value |

| Education — 0.9% |

| Yale University, 0.873%, 4/15/25 | $ | 1,000 | $ 927,244 |

Total Corporate Bonds

(identified cost $928,000) | | | $ 927,244 |

| Tax-Exempt Municipal Obligations — 95.6% |

| Security | Principal

Amount

(000's omitted) | Value |

| Bond Bank — 1.1% |

| Connecticut, (Revolving Fund), Green Bonds, 5.00%, 5/1/34 | $ | 1,000 | $ 1,107,830 |

| | | | $ 1,107,830 |

| Education — 23.3% |

| Connecticut Health and Educational Facilities Authority, (Avon Old Farms School): | | | |

| 4.00%, 7/1/41 | $ | 600 | $ 606,360 |

| 5.00%, 7/1/30 | | 175 | 203,007 |

| Connecticut Health and Educational Facilities Authority, (Choate Rosemary Hall): | | | |

| 4.00%, 7/1/33 | | 340 | 371,205 |

| 4.00%, 7/1/34 | | 375 | 405,127 |

| 4.00%, 7/1/35 | | 310 | 331,502 |

| Connecticut Health and Educational Facilities Authority, (Connecticut College): | | | |

| 4.00%, 7/1/36 | | 255 | 261,622 |

| 4.00%, 7/1/37 | | 270 | 274,671 |

| 5.00%, 7/1/26 | | 270 | 289,524 |

| Connecticut Health and Educational Facilities Authority, (Fairfield University), 4.00%, 7/1/42 | | 2,500 | 2,471,900 |

| Connecticut Health and Educational Facilities Authority, (Hopkins School), 5.25%, 7/1/47 | | 1,725 | 1,927,722 |

| Connecticut Health and Educational Facilities Authority, (Quinnipiac University): | | | |

| 4.125%, 7/1/41 | | 500 | 499,185 |

| 5.00%, 7/1/34 | | 1,475 | 1,567,984 |

| Connecticut Health and Educational Facilities Authority, (Sacred Heart University), 5.00%, 7/1/37 | | 450 | 476,811 |

| Connecticut Health and Educational Facilities Authority, (The Taft School): | | | |

| 4.00%, 7/1/28 | | 135 | 146,355 |

| 4.00%, 7/1/29 | | 100 | 108,572 |

| 4.00%, 7/1/30 | | 125 | 135,533 |

| Security | Principal

Amount

(000's omitted) | Value |

| Education (continued) |

| Connecticut Health and Educational Facilities Authority, (The Taft School): (continued) | | | |

| 4.00%, 7/1/33 | $ | 430 | $ 458,922 |

| 4.00%, 7/1/34 | | 1,095 | 1,157,360 |

| 4.00%, 7/1/36 | | 560 | 580,070 |

| Connecticut Health and Educational Facilities Authority, (University of New Haven): | | | |

| 5.00%, 7/1/34 | | 810 | 834,689 |

| 5.00%, 7/1/35 | | 850 | 869,677 |

| Connecticut Health and Educational Facilities Authority, (Yale University): | | | |

| 0.375% to 7/12/24 (Put Date), 7/1/35 | | 1,000 | 957,810 |

| 0.40%, 7/1/36(1) | | 1,000 | 1,000,000 |

| 0.50%, 7/1/36(1) | | 1,700 | 1,700,000 |

| 2.00% to 7/1/26 (Put Date), 7/1/42 | | 1,785 | 1,718,759 |

| 2.80% to 2/10/26 (Put Date), 7/1/48 | | 2,000 | 1,997,820 |

| University of Connecticut, 5.00%, 5/1/25 | | 1,000 | 1,058,650 |

| | | | $ 22,410,837 |

| Escrowed/Prerefunded — 1.7% |

| Connecticut Higher Education Supplemental Loan Authority: | | | |

| (AMT), Prerefunded to 5/15/24, 4.00%, 11/15/30 | $ | 415 | $ 422,665 |

| (AMT), Prerefunded to 11/15/25, 4.125%, 11/15/33 | | 150 | 155,805 |

| Greater New Haven Water Pollution Control Authority, CT, Prerefunded to 8/15/24, 5.00%, 8/15/32 | | 1,000 | 1,040,390 |

| | | | $ 1,618,860 |

| General Obligations — 29.0% |

| Bridgeport, CT, 5.00%, 8/1/32 | $ | 175 | $ 205,730 |

| Colchester, CT, 4.00%, 10/15/28 | | 440 | 452,945 |

| Connecticut: | | | |

| 4.00%, 1/15/38 | | 1,000 | 1,029,570 |

| 4.00%, 6/15/39 | | 300 | 307,647 |

| 4.00%, 6/15/41 | | 300 | 303,849 |

| 5.00%, 4/15/30 | | 1,150 | 1,323,443 |

| Social Bonds, 5.00%, 11/15/42 | | 1,500 | 1,685,775 |

| Darien, CT, 4.00%, 8/1/37 | | 1,310 | 1,360,776 |

| East Haddam, CT: | | | |

| 3.00%, 12/1/35 | | 400 | 395,908 |

| 3.00%, 12/1/37 | | 335 | 318,826 |

| Ellington, CT: | | | |

| 3.00%, 9/15/33 | | 280 | 282,083 |

| 3.00%, 9/15/35 | | 210 | 204,945 |

| Enfield, CT, 4.00%, 8/1/29 | | 500 | 538,375 |

20

See Notes to Financial Statements.

Eaton Vance

Connecticut Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited) — continued

| Security | Principal

Amount

(000's omitted) | Value |

| General Obligations (continued) |

| Greenwich, CT: | | | |

| 4.00%, 7/15/29 | $ | 450 | $ 461,588 |

| 4.00%, 7/15/30 | | 250 | 256,030 |

| 4.00%, 7/15/32 | | 400 | 408,536 |

| Groton, CT: | | | |

| Green Bonds, 4.00%, 4/1/40 | | 1,410 | 1,428,894 |

| Green Bonds, 4.125%, 4/1/41 | | 1,410 | 1,440,738 |

| Guilford, CT, 3.00%, 8/1/34 | | 500 | 501,930 |

| North Haven, CT: | | | |

| 5.00%, 7/15/23 | | 1,475 | 1,492,641 |

| 5.00%, 7/15/25 | | 1,490 | 1,590,188 |

| Norwalk, CT, 4.00%, 8/15/47 | | 1,425 | 1,457,020 |

| Puerto Rico: | | | |

| 5.625%, 7/1/27 | | 328 | 343,944 |

| 5.625%, 7/1/29 | | 750 | 798,667 |

| Rocky Hill, CT, 4.00%, 1/15/33 | | 1,000 | 1,063,970 |

| South Windsor, CT, 4.00%, 2/1/43(2) | | 1,425 | 1,470,217 |

| Thomaston, CT, 3.00%, 8/8/23 | | 2,000 | 2,000,040 |

| Waterbury, CT, 5.00%, 8/1/37 | | 1,150 | 1,315,853 |

| West Haven, CT, 4.00%, 9/15/36 | | 1,500 | 1,514,100 |

| Windsor Locks, CT: | | | |

| 4.125%, 7/15/41 | | 640 | 660,096 |

| 4.25%, 7/15/48 | | 1,280 | 1,329,690 |

| | | | $ 27,944,014 |

| Hospital — 8.5% |

| Connecticut Health and Educational Facilities Authority, (Nuvance Health), 4.00%, 7/1/41 | $ | 1,500 | $ 1,375,785 |

| Connecticut Health and Educational Facilities Authority, (Stamford Hospital): | | | |

| 4.00%, 7/1/46 | | 1,620 | 1,484,033 |

| 5.00%, 7/1/31 | | 1,000 | 1,134,750 |

| Connecticut Health and Educational Facilities Authority, (Trinity Health Corp.), 5.00%, 12/1/33 | | 2,000 | 2,157,780 |

| Connecticut Health and Educational Facilities Authority, (Yale-New Haven Health): | | | |

| 5.00%, 7/1/31 | | 500 | 516,095 |

| 5.00%, 7/1/34 | | 1,520 | 1,564,263 |

| | | | $ 8,232,706 |

| Housing — 6.8% |

| Connecticut Housing Finance Authority: | | | |

| 4.00%, 11/15/38 | $ | 750 | $ 758,228 |

| (FHLMC), (FNMA), (GNMA), 3.20%, 11/15/33 | | 745 | 740,783 |

| (SPA: TD Bank, N.A.), 1.60%, 11/15/50(3) | | 3,000 | 3,000,000 |

| Security | Principal

Amount

(000's omitted) | Value |

| Housing (continued) |

| Connecticut Housing Finance Authority: (continued) | | | |

| Social Bonds, (FHLMC), (FNMA), (GNMA), 4.55%, 11/15/37 | $ | 1,000 | $ 1,060,640 |

| Sustainability Bonds, 4.05%, 11/15/42 | | 1,000 | 1,005,010 |

| | | | $ 6,564,661 |

| Insured - Education — 4.9% |

| Connecticut Health and Educational Facilities Authority, (Loomis Chaffee School): | | | |

| (AMBAC), 5.25%, 7/1/30 | $ | 1,950 | $ 2,288,988 |

| (AMBAC), 5.25%, 7/1/31 | | 2,050 | 2,447,351 |

| | | | $ 4,736,339 |

| Insured - General Obligations — 7.9% |

| Bridgeport, CT, (AGM), 5.00%, 8/15/32 | $ | 1,120 | $ 1,218,246 |

| Hamden, CT, (BAM), 5.00%, 8/15/32 | | 1,375 | 1,594,477 |

| Hartford, CT: | | | |

| (AGC), 5.00%, 8/15/28 | | 500 | 501,135 |

| (AGM), 5.00%, 4/1/31 | | 240 | 240,538 |

| New Britain, CT: | | | |

| (BAM), 4.00%, 3/1/47 | | 2,000 | 1,980,240 |

| (BAM), 5.00%, 3/1/47 | | 1,000 | 1,082,930 |

| New Haven, CT, (AGM), 5.00%, 8/1/25 | | 1,000 | 1,036,600 |

| | | | $ 7,654,166 |

| Insured - Hospital — 1.1% |

| Connecticut Health and Educational Facilities Authority, (Hartford HealthCare Obligated Group), (AGM), 4.00%, 7/1/37 | $ | 1,000 | $ 1,020,600 |

| | | | $ 1,020,600 |

| Insured - Water and Sewer — 3.7% |

| South Central Connecticut Regional Water Authority, (NPFG), 5.25%, 8/1/24 | $ | 3,420 | $ 3,566,205 |

| | | | $ 3,566,205 |

| Senior Living/Life Care — 2.0% |

| Connecticut Health and Educational Facilities Authority, (Covenant Home, Inc.), 5.00%, 12/1/34 | $ | 1,000 | $ 1,043,700 |

| Connecticut Health and Educational Facilities Authority, (Jerome Home): | | | |

| 4.00%, 7/1/23 | | 130 | 130,120 |

| 4.00%, 7/1/31 | | 235 | 224,427 |

| Connecticut Health and Educational Facilities Authority, (McLean Affiliates, Inc.), 5.00%, 1/1/45(4) | | 500 | 483,180 |

| | | | $ 1,881,427 |

21

See Notes to Financial Statements.

Eaton Vance

Connecticut Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited) — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Special Tax Revenue — 1.5% |

| American Samoa Economic Development Authority, 5.00%, 9/1/38(4) | $ | 200 | $ 201,568 |

| Puerto Rico Sales Tax Financing Corp., 5.00%, 7/1/58 | | 1,250 | 1,234,675 |

| | | | $ 1,436,243 |

| Student Loan — 0.6% |

| Connecticut Higher Education Supplemental Loan Authority: | | | |

| (AMT), 5.00%, 11/15/28 | $ | 250 | $ 275,275 |

| (AMT), 5.00%, 11/15/29 | | 240 | 266,998 |

| | | | $ 542,273 |

| Transportation — 0.9% |

| Connecticut Airport Authority, (Ground Transportation Center), (AMT), 4.00%, 7/1/49 | $ | 1,000 | $ 864,330 |

| | | | $ 864,330 |

| Water and Sewer — 2.6% |

| South Central Connecticut Regional Water Authority: | | | |

| 4.00%, 8/1/34 | $ | 450 | $ 479,578 |

| 5.00%, 8/1/32 | | 355 | 408,474 |

| Stamford, CT, (Water Pollution Control System): | | | |

| 4.00%, 4/1/44 | | 1,000 | 1,017,450 |

| 5.00%, 9/15/29 | | 200 | 213,864 |

| 5.00%, 9/15/30 | | 125 | 133,500 |

| 5.00%, 4/1/33 | | 100 | 114,961 |

| 5.00%, 4/1/34 | | 100 | 114,829 |

| | | | $ 2,482,656 |

Total Tax-Exempt Municipal Obligations

(identified cost $91,884,810) | | | $ 92,063,147 |

| Taxable Municipal Obligations — 2.9% |

| Security | Principal

Amount

(000's omitted) | Value |

| Education — 0.6% |

| Connecticut Health and Educational Facilities Authority, (Avon Old Farms School): | | | |

| 1.30%, 7/1/23 | $ | 250 | $ 246,205 |

| 1.65%, 7/1/24 | | 300 | 286,851 |

| | | | $ 533,056 |

| Security | Principal

Amount

(000's omitted) | Value |

| General Obligations — 2.3% |

| Connecticut, 3.136%, 4/15/25 | $ | 770 | $ 750,427 |

| Naugatuck, CT: | | | |

| 1.14%, 9/15/26 | | 200 | 177,528 |

| 1.40%, 9/15/27 | | 250 | 217,387 |

| 1.60%, 9/15/28 | | 255 | 217,487 |

| 1.79%, 9/15/29 | | 750 | 629,535 |

| Watertown, CT, 2.25%, 10/15/33 | | 290 | 235,677 |

| | | | $ 2,228,041 |

Total Taxable Municipal Obligations

(identified cost $3,046,646) | | | $ 2,761,097 |

| Security | Notional

Amount

(000's omitted) | Value |

| Transportation — 0.7% |

| HTA TRRB 2005L-745190R75 Assured Custodial Trust, 5.25%, 7/1/41 | $ | 670 | $ 676,599 |

Total Trust Units

(identified cost $675,026) | | | $ 676,599 |

Total Investments — 100.1%

(identified cost $96,534,482) | | | $ 96,428,087 |

| Other Assets, Less Liabilities — (0.1)% | | | $ (128,829) |

| Net Assets — 100.0% | | | $ 96,299,258 |

| The percentage shown for each investment category in the Portfolio of Investments is based on net assets. |

| (1) | Variable rate demand obligation that may be tendered at par on any day for payment the same or next business day. The stated interest rate, which generally resets daily, is determined by the remarketing agent and represents the rate in effect at January 31, 2023. |

| (2) | When-issued security. |

| (3) | Variable rate demand obligation that may be tendered at par on any day for payment the lesser of 5 business days or 7 calendar days. The stated interest rate, which generally resets weekly, is determined by the remarketing agent and represents the rate in effect at January 31, 2023. |

| (4) | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities may be sold in certain transactions in reliance on an exemption from registration (normally to qualified institutional buyers). At January 31, 2023, the aggregate value of these securities is $684,748 or 0.7% of the Fund's net assets. |

22

See Notes to Financial Statements.

Eaton Vance

Connecticut Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited) — continued

| The Fund invests primarily in debt securities issued by Connecticut municipalities. The ability of the issuers of the debt securities to meet their obligations may be affected by economic developments in a specific industry or municipality. At January 31, 2023, 17.6% of total investments are backed by bond insurance of various financial institutions and financial guaranty assurance agencies. The aggregate percentage insured by an individual financial institution or financial guaranty assurance agency ranged from 0.5% to 4.9% of total investments. |

| Abbreviations: |

| AGC | – Assured Guaranty Corp. |

| AGM | – Assured Guaranty Municipal Corp. |

| AMBAC | – AMBAC Financial Group, Inc. |

| AMT | – Interest earned from these securities may be considered a tax preference item for purposes of the Federal Alternative Minimum Tax. |

| BAM | – Build America Mutual Assurance Co. |

| FHLMC | – Federal Home Loan Mortgage Corp. |

| FNMA | – Federal National Mortgage Association |

| GNMA | – Government National Mortgage Association |

| NPFG | – National Public Finance Guarantee Corp. |

| SPA | – Standby Bond Purchase Agreement |

23

See Notes to Financial Statements.

Eaton Vance

Minnesota Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited)

| Tax-Exempt Municipal Obligations — 96.9% |

| Security | Principal

Amount

(000's omitted) | Value |

| Bond Bank — 1.0% |

| Minnesota Public Facilities Authority, (Revolving Fund): | | | |

| 5.00%, 3/1/29 | $ | 1,000 | $ 1,083,840 |

| 5.00%, 3/1/30 | | 1,000 | 1,083,530 |

| | | | $ 2,167,370 |

| Education — 12.5% |

| Minnesota Higher Education Facilities Authority, (Carleton College): | | | |

| 5.00%, 3/1/29 | $ | 2,250 | $ 2,480,535 |

| 5.00%, 3/1/31 | | 1,000 | 1,102,280 |

| 5.00%, 3/1/34 | | 500 | 549,500 |

| Minnesota Higher Education Facilities Authority, (College of Saint Benedict): | | | |

| 4.00%, 3/1/36 | | 400 | 399,140 |

| 5.00%, 3/1/37 | | 1,500 | 1,544,835 |

| 5.00%, 10/1/52 | | 2,000 | 2,125,180 |

| Minnesota Higher Education Facilities Authority, (College of St. Scholastica), 4.00%, 12/1/40 | | 1,850 | 1,693,286 |

| Minnesota Higher Education Facilities Authority, (Gustavus Adolphus College), 5.00%, 10/1/35 | | 565 | 605,776 |

| Minnesota Higher Education Facilities Authority, (Macalester College): | | | |

| 4.00%, 3/1/26 | | 115 | 120,643 |

| 4.00%, 3/1/27 | | 125 | 132,974 |

| 4.00%, 3/1/28 | | 100 | 107,948 |

| 4.00%, 3/1/29 | | 100 | 109,363 |

| 5.00%, 3/1/27 | | 500 | 524,700 |

| 5.00%, 3/1/28 | | 1,010 | 1,059,258 |

| Minnesota Higher Education Facilities Authority, (St. Catherine University), 5.00%, 10/1/32 | | 500 | 545,110 |

| Minnesota Higher Education Facilities Authority, (St. Olaf College): | | | |

| 4.00%, 10/1/35 | | 500 | 510,370 |

| 4.00%, 10/1/46 | | 1,500 | 1,495,350 |

| 5.00%, 12/1/29 | | 1,815 | 1,933,429 |

| Minnesota Higher Education Facilities Authority, (University of St. Thomas): | | | |

| 4.00%, 10/1/32 | | 910 | 961,606 |

| 4.00%, 10/1/36 | | 500 | 509,070 |

| 4.00%, 10/1/37 | | 500 | 506,235 |

| 5.00%, 10/1/30 | | 650 | 714,110 |

| 5.00%, 10/1/34 | | 250 | 279,750 |

| 5.00%, 4/1/35 | | 750 | 796,582 |

| Security | Principal

Amount

(000's omitted) | Value |

| Education (continued) |

| Minnesota State Colleges and Universities, 5.00%, 10/1/26 | $ | 1,535 | $ 1,682,590 |

| St. Paul Housing and Redevelopment Authority, MN, (Hmong College Prep Academy), 5.00%, 9/1/43 | | 1,000 | 960,220 |

| University of Minnesota: | | | |

| 5.00%, 4/1/27 | | 500 | 541,920 |

| 5.00%, 8/1/27 | | 625 | 663,781 |

| 5.00%, 4/1/41 | | 2,000 | 2,116,740 |

| | | | $ 26,772,281 |

| Electric Utilities — 6.3% |

| Chaska, MN, Electric System Revenue, 5.00%, 10/1/30 | $ | 550 | $ 586,768 |

| Hutchinson, MN, Public Utility Revenue, 5.00%, 12/1/26 | | 350 | 350,770 |

| Minnesota Municipal Power Agency: | | | |

| 5.00%, 10/1/33 | | 250 | 259,475 |

| 5.00%, 10/1/34 | | 250 | 259,475 |

| 5.00%, 10/1/35 | | 200 | 207,480 |

| Northern Municipal Power Agency, MN: | | | |

| 5.00%, 1/1/30 | | 460 | 499,965 |

| 5.00%, 1/1/31 | | 670 | 718,682 |

| 5.00%, 1/1/41 | | 240 | 251,196 |

| Rochester, MN, Electric Utility Revenue: | | | |

| 5.00%, 12/1/29 | | 700 | 772,212 |

| 5.00%, 12/1/30 | | 700 | 770,049 |

| 5.00%, 12/1/42 | | 820 | 873,767 |

| St. Paul Port Authority, MN, District Energy Revenue: | | | |

| 4.00%, 10/1/42 | | 1,250 | 1,244,325 |

| (AMT), 4.00%, 10/1/40 | | 1,000 | 990,230 |

| Western Minnesota Municipal Power Agency: | | | |

| 5.00%, 1/1/25 | | 750 | 786,338 |

| 5.00%, 1/1/27 | | 750 | 825,480 |

| 5.00%, 1/1/29 | | 1,000 | 1,146,150 |

| 5.00%, 1/1/30 | | 750 | 875,722 |

| 5.00%, 1/1/34 | | 1,000 | 1,070,040 |

| 5.00%, 1/1/36 | | 900 | 957,285 |

| | | | $ 13,445,409 |

| Escrowed/Prerefunded — 0.5% |

| Western Minnesota Municipal Power Agency, Prerefunded to 1/1/24, 5.00%, 1/1/34 | $ | 1,000 | $ 1,023,310 |

| | | | $ 1,023,310 |

| General Obligations — 38.3% |

| Andover, MN, 4.00%, 2/1/30 | $ | 795 | $ 858,473 |

24

See Notes to Financial Statements.

Eaton Vance

Minnesota Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited) — continued

| Security | Principal

Amount

(000's omitted) | Value |

| General Obligations (continued) |

| Anoka-Hennepin Independent School District No. 11, MN: | | | |

| 5.00%, 2/1/27 | $ | 1,000 | $ 1,110,040 |

| 5.00%, 2/1/28 | | 1,040 | 1,154,098 |

| Brooklyn Center Independent School District No. 286, MN, 4.00%, 2/1/40 | | 2,000 | 2,033,600 |

| Brooklyn Center, MN, 4.00%, 2/1/30 | | 1,060 | 1,146,199 |

| Burnsville, MN: | | | |

| 3.00%, 12/20/32 | | 620 | 632,611 |

| 4.00%, 12/20/31 | | 640 | 719,827 |

| Centennial Independent School District No. 12, MN: | | | |

| 0.00%, 2/1/28 | | 1,000 | 858,920 |

| 0.00%, 2/1/35 | | 350 | 223,094 |

| Cloquet Independent School District No. 94, MN, 5.00%, 2/1/30 | | 2,000 | 2,091,380 |

| Coon Rapids, MN, 5.00%, 2/1/33 | | 1,525 | 1,854,339 |

| Dilworth-Glyndon-Felton Independent School District No. 2164, MN, 4.00%, 2/1/27 | | 730 | 770,858 |

| Duluth, MN: | | | |

| 5.00%, 2/1/34 | | 1,000 | 1,064,540 |

| Series 2016A, 5.00%, 2/1/31 | | 1,000 | 1,070,490 |

| Series 2019C, 5.00%, 2/1/31 | | 500 | 573,595 |

| Eden Prairie Independent School District No. 272, MN, 5.00%, 2/1/30 | | 1,000 | 1,128,810 |

| Edina Independent School District No. 273, MN, 5.00%, 2/1/28 | | 1,625 | 1,796,714 |

| Elk River Area Independent School District No. 728, MN, 4.00%, 2/1/32 | | 2,000 | 2,034,200 |

| Hawley Independent School District No. 150, MN, 4.25%, 2/1/46(1) | | 2,250 | 2,291,040 |

| Hennepin County Independent School District No. 281, MN, 5.00%, 2/1/29 | | 1,010 | 1,138,563 |

| Hennepin County Regional Railroad Authority, MN, 5.00%, 12/1/32 | | 675 | 778,302 |

| Hennepin County, MN: | | | |

| 5.00%, 12/1/32 | | 1,000 | 1,224,550 |

| 5.00%, 12/15/33 | | 2,280 | 2,630,048 |

| 5.00%, 12/1/35 | | 2,000 | 2,181,680 |

| 5.00%, 12/1/39 | | 2,000 | 2,344,200 |

| Hopkins Independent School District No. 270, MN, 4.00%, 2/1/25 | | 1,250 | 1,251,825 |

| Mahtomedi Independent School District No. 832, MN, 5.00%, 2/1/31 | | 1,000 | 1,044,690 |

| Maple River Independent School District No. 2135, MN, 4.00%, 2/1/45 | | 1,200 | 1,227,300 |

| Minneapolis Special School District No. 1, MN: | | | |

| 4.00%, 2/1/33 | | 1,500 | 1,602,465 |

| 5.00%, 2/1/32 | | 1,500 | 1,688,970 |

| Security | Principal

Amount

(000's omitted) | Value |

| General Obligations (continued) |

| Minneapolis, MN, 4.00%, 12/1/39 | $ | 2,500 | $ 2,607,975 |

| Minneapolis-St. Paul Metropolitan Council, MN: | | | |

| 4.00%, 3/1/30 | | 1,000 | 1,073,120 |

| 5.00%, 3/1/29 | | 2,000 | 2,331,740 |

| Series 2018C, 5.00%, 3/1/28 | | 2,500 | 2,782,775 |

| Series 2022B, 5.00%, 3/1/28 | | 2,000 | 2,280,860 |

| Minnesota: | | | |

| 5.00%, 8/1/32 | | 2,000 | 2,135,140 |

| 5.00%, 8/1/34 | | 500 | 568,170 |

| 5.00%, 10/1/34 | | 1,000 | 1,115,690 |

| 5.00%, 8/1/38 | | 1,135 | 1,339,232 |

| Pipestone, Rock and Murray Counties Independent School District No. 2689, MN, 5.00%, 2/1/29 | | 1,205 | 1,395,089 |

| Plymouth, MN, 4.00%, 2/1/30 | | 390 | 427,643 |

| Puerto Rico: | | | |

| 5.625%, 7/1/29 | | 1,500 | 1,597,335 |

| 5.75%, 7/1/31 | | 500 | 543,350 |

| Rice County, MN, 4.00%, 2/1/52 | | 3,000 | 3,070,350 |

| Rosemount-Apple Valley-Eagan Independent School District No. 196, MN: | | | |

| 4.00%, 2/1/28 | | 2,000 | 2,105,680 |

| 5.00%, 2/1/27 | | 1,000 | 1,082,830 |

| Russell-Tyler-Ruthton Independent School District No. 2902, MN, 5.00%, 2/1/27 | | 1,400 | 1,547,252 |

| Sartell-St. Stephen Independent School District No. 748, MN: | | | |

| 0.00%, 2/1/32 | | 1,350 | 1,017,657 |

| 0.00%, 2/1/37 | | 1,500 | 871,995 |

| Scott County, MN, 4.00%, 12/1/34 | | 2,000 | 2,146,340 |

| Spring Lake Park Independent School District No. 16, MN, 4.00%, 2/1/29 | | 1,075 | 1,132,846 |

| St. Louis Park Independent School District No. 283, MN, 4.00%, 2/1/31 | | 2,000 | 2,128,020 |

| St. Louis Park, MN, 4.00%, 2/1/28 | | 1,000 | 1,069,210 |

| St. Paul, MN: | | | |

| 5.00%, 12/1/27 | | 750 | 827,077 |

| 5.00%, 5/1/28 | | 1,200 | 1,370,448 |

| Waseca Independent School District No. 829, MN, 4.00%, 2/1/28 | | 1,575 | 1,658,223 |

| Watertown-Mayer Independent School District No. 111, MN, 0.00%, 2/1/36 | | 1,000 | 618,300 |

| Worthington Independent School District No. 518, MN, 4.00%, 2/1/31 | | 730 | 771,741 |

| | | | $ 82,141,509 |

25

See Notes to Financial Statements.

Eaton Vance

Minnesota Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited) — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Hospital — 15.6% |

| Duluth Economic Development Authority, MN, (Essentia Health Obligated Group): | | | |

| 5.00%, 2/15/37 | $ | 1,000 | $ 1,053,300 |

| 5.00%, 2/15/48 | | 3,000 | 3,098,520 |

| Duluth Economic Development Authority, MN, (St. Luke's Hospital of Duluth Obligated Group): | | | |

| 4.00%, 6/15/34 | | 520 | 519,256 |

| 4.00%, 6/15/38 | | 375 | 351,709 |

| 4.00%, 6/15/39 | | 225 | 208,890 |

| 5.25%, 6/15/52 | | 2,000 | 2,068,500 |

| Maple Grove, MN, (Maple Grove Hospital Corp.): | | | |

| 5.00%, 5/1/30 | | 850 | 907,460 |

| 5.00%, 5/1/31 | | 500 | 532,600 |

| 5.00%, 5/1/32 | | 500 | 530,025 |

| Minneapolis and St. Paul Housing and Redevelopment Authority, MN, (Allina Health System): | | | |

| 5.00%, 11/15/28 | | 2,975 | 3,278,182 |

| 5.00%, 11/15/29 | | 915 | 1,006,006 |

| Minneapolis, MN, (Allina Health System), 4.00%, 11/15/39 | | 3,250 | 3,293,582 |

| Minneapolis, MN, (Fairview Health Services), 5.00%, 11/15/28 | | 225 | 237,191 |

| Rochester, MN, (Mayo Clinic): | | | |

| 4.00%, 11/15/48 | | 1,000 | 1,004,310 |

| 5.00%, 11/15/57 | | 750 | 828,143 |

| (SPA: Northern Trust Co.), 1.65%, 11/15/38(2) | | 6,000 | 6,000,000 |

| St. Cloud, MN, (CentraCare Health System), 5.00%, 5/1/46 | | 2,650 | 2,729,102 |

| St. Paul Housing and Redevelopment Authority, MN, (Fairview Health Services): | | | |

| 5.00%, 11/15/31 | | 1,000 | 1,081,490 |

| 5.00%, 11/15/34 | | 500 | 535,910 |

| 5.00%, 11/15/47 | | 500 | 516,360 |

| St. Paul Housing and Redevelopment Authority, MN, (HealthPartners Obligated Group): | | | |

| 5.00%, 7/1/29 | | 500 | 523,725 |

| 5.00%, 7/1/30 | | 1,000 | 1,047,370 |

| 5.00%, 7/1/32 | | 1,995 | 2,083,758 |

| | | | $ 33,435,389 |

| Housing — 1.7% |

| Minnesota Housing Finance Agency: | | | |

| 2.15%, 7/1/45 | $ | 900 | $ 650,340 |

| 4.00%, 8/1/39 | | 2,055 | 2,103,395 |

| (FHLMC), (FNMA), (GNMA), 2.40%, 1/1/35 | | 605 | 524,747 |

| (FHLMC), (FNMA), (GNMA), 3.15%, 1/1/37 | | 285 | 281,349 |

| | | | $ 3,559,831 |

| Security | Principal

Amount

(000's omitted) | Value |

| Insured - Electric Utilities — 4.8% |

| Central Minnesota Municipal Power Agency: | | | |

| (AGM), 4.00%, 1/1/42 | $ | 340 | $ 345,328 |

| (AGM), 5.00%, 1/1/30 | | 200 | 231,728 |

| Puerto Rico Electric Power Authority, (NPFG), 5.25%, 7/1/32 | | 1,150 | 1,158,130 |

| Southern Minnesota Municipal Power Agency, (NPFG), 0.00%, 1/1/25 | | 9,000 | 8,520,120 |

| | | | $ 10,255,306 |

| Insured - Hospital — 1.0% |

| Minneapolis, MN, (Fairview Health Services), (AGM), 5.00%, 11/15/44 | $ | 2,000 | $ 2,050,500 |

| | | | $ 2,050,500 |

| Lease Revenue/Certificates of Participation — 3.8% |

| Anoka-Hennepin Independent School District No. 11, MN, 5.00%, 2/1/34 | $ | 1,000 | $ 1,022,280 |

| Minnesota: | | | |

| 5.00%, 3/1/27 | | 3,000 | 3,335,550 |

| 5.00%, 6/1/29 | | 1,335 | 1,344,826 |

| 5.00%, 6/1/38 | | 2,500 | 2,512,925 |

| | | | $ 8,215,581 |

| Other Revenue — 2.8% |

| Center City, MN, (Hazelden Betty Ford Foundation): | | | |

| 4.00%, 11/1/28 | $ | 825 | $ 828,275 |

| 4.00%, 11/1/34 | | 500 | 487,150 |

| 5.00%, 11/1/27 | | 400 | 409,856 |

| 5.00%, 11/1/29 | | 300 | 305,808 |

| Minnesota Municipal Gas Agency: | | | |

| (Liq: Royal Bank of Canada), 3.881%, (67% of SOFR + 1.00%), 12/1/27 (Put Date), 12/1/52(3) | | 2,000 | 1,957,960 |

| (Liq: Royal Bank of Canada), 4.00% to 12/1/27 (Put Date), 12/1/52 | | 2,045 | 2,085,328 |

| | | | $ 6,074,377 |

| Senior Living/Life Care — 2.6% |

| Apple Valley, MN, (PHS Apple Valley Senior Housing, Inc.): | | | |

| 4.50%, 9/1/53 | $ | 940 | $ 858,493 |

| 5.00%, 9/1/43 | | 1,000 | 1,002,350 |

| North Oaks, MN, (Waverly Gardens): | | | |

| 4.00%, 10/1/25 | | 1,600 | 1,605,952 |

| 4.00%, 10/1/26 | | 1,680 | 1,685,611 |

26

See Notes to Financial Statements.

Eaton Vance

Minnesota Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited) — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Senior Living/Life Care (continued) |

| Wayzata, MN, (Folkestone Senior Living Community), 4.00%, 8/1/44 | $ | 435 | $ 364,430 |

| | | | $ 5,516,836 |

| Special Tax Revenue — 2.1% |

| American Samoa Economic Development Authority, 5.00%, 9/1/38(4) | $ | 200 | $ 201,568 |

| Hennepin County, MN, Sales Tax Revenue, 5.00%, 12/15/24 | | 1,325 | 1,386,652 |

| Puerto Rico Sales Tax Financing Corp., 5.00%, 7/1/58 | | 3,000 | 2,963,220 |

| | | | $ 4,551,440 |

| Transportation — 3.9% |

| Minneapolis-St. Paul Metropolitan Airports Commission, MN: | | | |

| 5.00%, 1/1/27 | $ | 1,000 | $ 1,099,850 |

| 5.00%, 1/1/35 | | 1,000 | 1,019,240 |

| 5.00%, 1/1/52 | | 1,500 | 1,623,030 |

| (AMT), 5.00%, 1/1/28 | | 1,250 | 1,359,025 |

| (AMT), 5.00%, 1/1/33 | | 1,200 | 1,327,056 |

| (AMT), 5.25%, 1/1/47 | | 1,750 | 1,896,755 |

| | | | $ 8,324,956 |

Total Tax-Exempt Municipal Obligations

(identified cost $208,456,616) | | | $207,534,095 |

Total Investments — 96.9%

(identified cost $208,456,616) | | | $207,534,095 |

| Other Assets, Less Liabilities — 3.1% | | | $ 6,684,874 |

| Net Assets — 100.0% | | | $214,218,969 |

| The percentage shown for each investment category in the Portfolio of Investments is based on net assets. |

| (1) | When-issued security. |

| (2) | Variable rate demand obligation that may be tendered at par on any day for payment the lesser of 5 business days or 7 calendar days. The stated interest rate, which generally resets weekly, represents the rate in effect at January 31, 2023. |

| (3) | Floating rate security. The stated interest rate represents the rate in effect at January 31, 2023. |

| (4) | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities may be sold in certain transactions in reliance on an exemption from registration (normally to qualified institutional buyers). At January 31, 2023, the aggregate value of these securities is $201,568 or 0.1% of the Fund's net assets. |

| The Fund invests primarily in debt securities issued by Minnesota municipalities. The ability of the issuers of the debt securities to meet their obligations may be affected by economic developments in a specific industry or municipality. At January 31, 2023, 5.9% of total investments are backed by bond insurance of various financial institutions and financial guaranty assurance agencies. The aggregate percentage insured by an individual financial institution or financial guaranty assurance agency ranged from 1.3% to 4.7% of total investments. |

| Abbreviations: |

| AGM | – Assured Guaranty Municipal Corp. |

| AMT | – Interest earned from these securities may be considered a tax preference item for purposes of the Federal Alternative Minimum Tax. |

| FHLMC | – Federal Home Loan Mortgage Corp. |

| FNMA | – Federal National Mortgage Association |

| GNMA | – Government National Mortgage Association |

| NPFG | – National Public Finance Guarantee Corp. |

| SOFR | – Secured Overnight Financing Rate |

27

See Notes to Financial Statements.

Eaton Vance

New Jersey Municipal Income Fund

January 31, 2023

Portfolio of Investments (Unaudited)

| Tax-Exempt Municipal Obligations — 91.5% |

| Security | Principal

Amount

(000's omitted) | Value |

| Bond Bank — 1.2% |

| New Jersey Infrastructure Bank: | | | |

| Green Bonds, 5.00%, 9/1/36 | $ | 1,000 | $ 1,197,120 |

| Green Bonds , 5.00%, 9/1/38 | | 500 | 586,520 |

| | | | $ 1,783,640 |

| Education — 2.8% |

| Essex County Improvement Authority, NJ, (Friends of TEAM Charter Schools, Inc.), 4.00%, 6/15/56 | $ | 1,550 | $ 1,344,811 |

| New Jersey Educational Facilities Authority, (Montclair State University), 5.00%, 7/1/30 | | 1,765 | 1,818,374 |

| New Jersey Educational Facilities Authority, (Princeton University), 5.00%, 7/1/42 | | 1,000 | 1,084,910 |

| | | | $ 4,248,095 |

| Escrowed/Prerefunded — 1.4% |

| Delaware River Port Authority of Pennsylvania and New Jersey, Prerefunded to 1/1/24, 5.00%, 1/1/28 | $ | 2,000 | $ 2,045,700 |

| | | | $ 2,045,700 |

| General Obligations — 17.0% |

| Bergen County Improvement Authority, NJ, (Bergen New Bridge Medical Center), 5.00%, 8/1/42 | $ | 2,575 | $ 2,964,726 |

| Burlington County Bridge Commission, NJ: | | | |

| 5.00%, 8/1/30 | | 500 | 570,680 |

| 5.00%, 8/1/31 | | 410 | 468,339 |

| 5.00%, 8/1/32 | | 250 | 285,283 |

| 5.00%, 10/1/36 | | 1,000 | 1,095,830 |

| Chester Township, NJ: | | | |

| 2.00%, 10/1/29 | | 1,000 | 940,600 |

| 2.00%, 10/1/30 | | 495 | 459,291 |

| East Brunswick Board of Education, NJ, 4.00%, 8/1/34 | | 1,200 | 1,292,964 |

| East Brunswick, NJ, 2.00%, 7/15/30 | | 2,375 | 2,209,890 |

| Essex County, NJ: | | | |

| 2.00%, 9/1/31 | | 995 | 890,853 |

| 2.00%, 9/1/32 | | 2,935 | 2,590,724 |

| 4.00%, 8/15/33 | | 1,170 | 1,302,818 |

| Gloucester County Improvement Authority, NJ, 4.00%, 4/1/35 | | 2,000 | 2,051,420 |

| Jersey City, NJ, 5.00%, 11/1/33 | | 800 | 889,736 |

| Monmouth County Improvement Authority, NJ: | | | |

| 3.00%, 12/1/36 | | 100 | 97,140 |