SECOND QUARTER 2014 ASSOCIATED BANC-CORP INVESTOR PRESENTATION Exhibit 99.1 |

FORWARD-LOOKING STATEMENTS 1 Important note regarding forward-looking statements: Statements made in this presentation which are not purely historical are forward-looking statements, as defined in the Private Securities Litigation Reform Act of 1995. This includes any statements regarding management’s plans, objectives, or goals for future operations, products or services, and forecasts of its revenues, earnings, or other measures of performance. Such forward-looking statements may be identified by the use of words such as “believe”, “expect”, “anticipate”, “plan”, “estimate”, “should”, “will”, “intend”, “outlook”, or similar expressions. Forward-looking statements are based on current management expectations and, by their nature, are subject to risks and uncertainties. Actual results may differ materially from those contained in the forward-looking statements. Factors which may cause actual results to differ materially from those contained in such forward-looking statements include those identified in the company’s most recent Form 10-K and subsequent SEC filings. Such factors are incorporated herein by reference. |

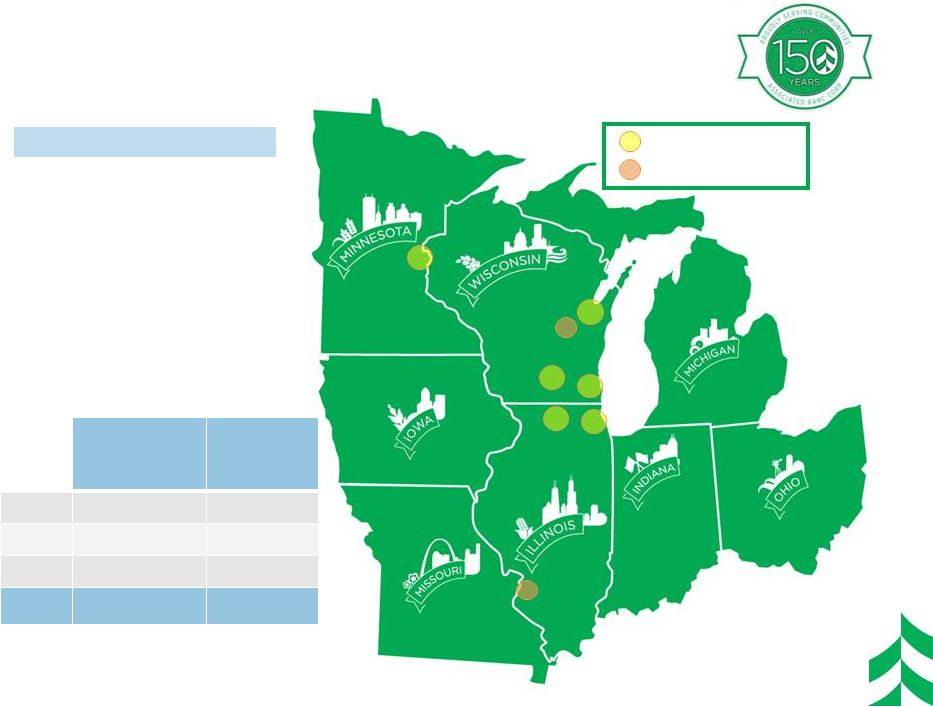

OUR FOOTPRINT AND FRANCHISE • Top 50, publicly traded, U.S. bank holding company • $25 billion in assets; largest bank headquartered in Wisconsin • 227 branches serving approximately one million customers ASBC Deposits² ($ in billions) ASBC Branches² WI $12.2 161 IL $3.8 43 MN $1.5 23 Total $17.5 227 1 FDIC market share data 6/30/13 2 As of 3/31/14 (Period End) 2 >$1bn deposits¹ >$500mm deposits¹ About Associated 1861 1999 1987 2011 2011 2006 2012 |

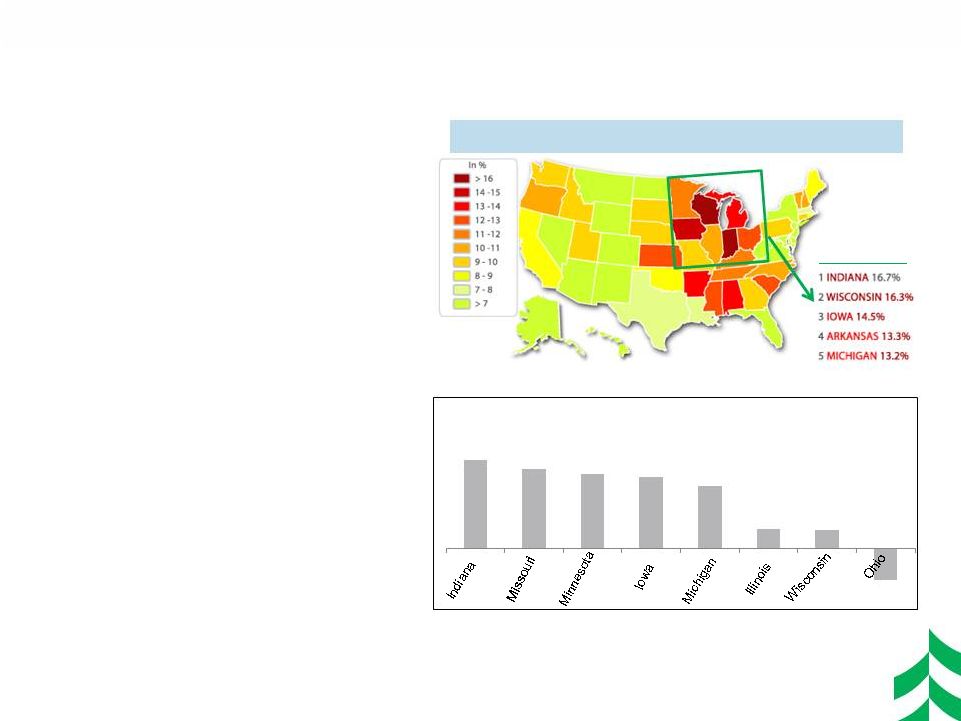

ATTRACTIVE MIDWEST MARKETS 3 • Service a Large Market Place: (Footprint is ~ 20% of USA)¹ • Manufacturing Concentrated: (Indiana, Wisconsin, and Iowa) for concentration of manufacturing jobs and two other states in the top 10 • Favorable Employment Dynamics: Minnesota, and Wisconsin all have unemployment rates that are under 6%³ • Positive Economic Trends: Adding jobs in footprint 1 US Census Bureau 2012 ; 2 Area Development Online – Author: Mark Crawford (Winter 2013); March 2014 US Bureau of Labor Statistics; 4 March 2014 US Bureau of Labor Statistics - Local Area Unemployment Statistics Manufacturing Share of Non-Farm Employment ² 4 of Top 5 29.8 26.8 25.1 23.9 21.0 6.5 6.1 -10.8 March 2013 to March 2014 Net Change in Employment (in ‘000’s) 4 Top 3 states Indiana, Iowa, 3 |

ASSOCIATED AT ITS CORE 4 Community bank values, flexibility, decision- making, attention to relationships and service Big bank products, strength, lending limits, efficiency, innovation, depth of expertise |

1Q 2014 HIGHLIGHTS AND OUTLOOK 5 • Record Commercial Loan Growth of $420 mm – Total average loans of $16.2 bn, up 3% from 4Q13 • Disciplined Expense Management – Noninterest expenses down $12 mm from 4Q13 – FTEs down 7% from 1Q13 • Consistent Capital Deployment – Repurchased $39 mm of common stock 1Q 2014 Highlights: Outlook – Growing the Franchise & Creating Long- Term Shareholder Value • Continued focus on organic growth opportunities • Defending NIM compression in low-rate environment • Strong focus on efficiency & expense management • Disciplined focus on deploying capital to drive long-term shareholder value – Repurchased 1.6 million shares of common stock in April 2014 |

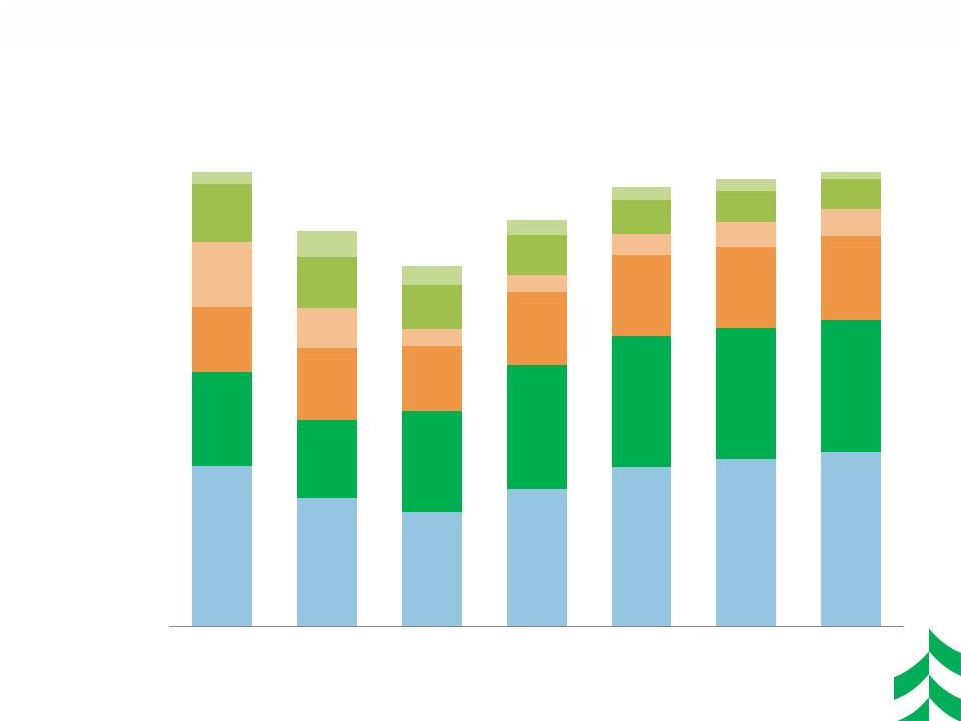

RESHAPING & REBUILDING THE LOAN PORTFOLIO 6 1 Based on Average Annual Balances, $ in Billions Installment HELOCs & 2 Liens Residential Mortgage & HE 1 Liens Construction CRE Investor Commercial & Business Lending $16.4 $13.9 $12.7 $14.3 $15.5 5% 7% 5% 12% 12% 13% 14% 14% 20% 35% 10% 19% 20% 31% 4% 18% 28% 33% $15.7 $16.2 4% 10% 4% 18% 31% 33% 3% 8% 4% 19% 30% 36% 3% 7% 5% 18% 29% 38% 2% 7% 6% 19% 29% 37% Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q4 2013 Q1 2014 nd st ¹ |

LOAN PORTFOLIO GROWTH AVERAGE LOAN GROWTH OF $416 MILLION OR 3% FROM FOURTH QUARTER 2013 7 1Q 2014 From Prior Quarter Average Net Loan Change ($ in millions) Home Equity & Installment Commercial Real Estate Residential Mortgage Power & Utilities Oil & Gas Mortgage Warehouse General Commercial Loans Total Commercial & Business Lending = +4% (+$249) +5% % Change +7% (3%) (21%) +3% +21% +2% ($73) ($40) $38 $70 $94 $157 $171 |

COMMERCIAL LINE UTILIZATION TRENDS 8 Line utilization increased in all Commercial lines of business Increase from 4Q 13 CRE + 110 bps Specialized + 170 bps Commercial + 200 bps 46.7% 48.5% 48.3% 46.6% 44.8% 46.8% 51.3% 56.5% 60.4% 61.1% 63.1% 64.2% 55.0% 52.9% 56.2% 52.1% 50.4% 52.1% 40.0% 50.0% 60.0% 70.0% 4Q 2012 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 Commercial Banking Commercial Real Estate Specialized Industries |

GROWING NET INTEREST INCOME WHILE MARGIN COMPRESSES 9 Yield on Interest-earning Assets Cost of Interest-bearing Liabilities Net Interest Income & Net Interest Margin ($ in millions) $158 $160 $161 $167 Net Interest Margin $165 <$1 <$1 0.45% 0.41% 0.38% 0.35% 0.31% 0.18% 0.17% 0.15% 0.13% 0.12% 0.27% 0.24% 0.23% 0.22% 0.19% 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 Interest Bearing Other Costs Interest Bearning Deposit Costs 3.52% 3.47% 3.42% 3.50% 3.36% 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 $157 $159 $159 $163 $164 $1 $1 $4 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 Net Interest Income Net of Interest Recoveries Interest Recoveries 3.17% 3.16% 3.13% 3.23% 3.12% |

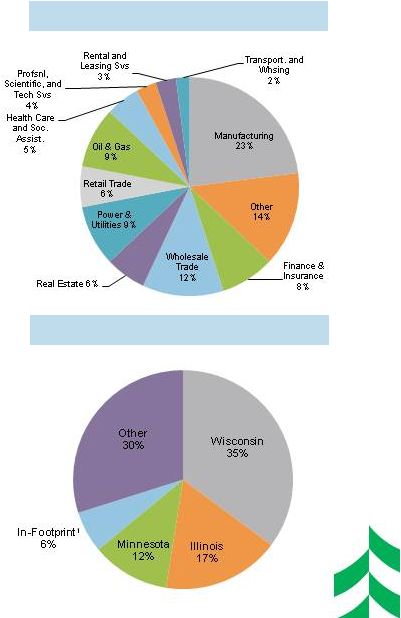

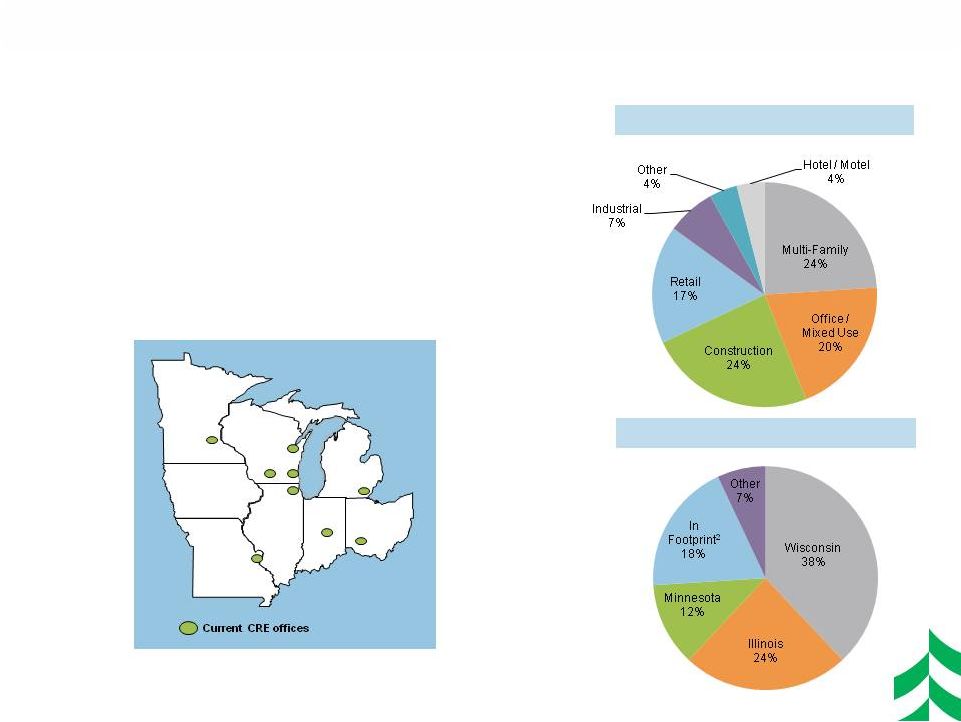

COMMERCIAL & BUSINESS LENDING 10 ($6.4 billion – Mar 2014 – Period End) • More than 280 colleagues serving businesses, municipal governments, and entrepreneurs: – Includes General Commercial and Specialized Lending efforts – Offers unsecured and customized commercial finance lending solutions secured by accounts receivable, inventory, machinery, and equipment – Capital Markets revenue of $13 million in 2013 • Approximately 50 Commercial Deposit and Treasury Management colleagues – Streamlined cash management solutions via our Associated Connect platform for businesses, municipalities, and correspondent banks • Associated Financial Group : More than 240 colleagues supporting our insurance brokerage – Leading benefits consultant in our markets – Providing Risk Management, HR, and Benefits solutions for over 40 years – Insurance revenue of $44 million in 2013 1 Includes Missouri, Indiana, Ohio, Michigan, & Iowa ($6.4 billion – Mar 2014 – Period End) C&BL Loans by Industry C&BL Loans by State |

COMMERCIAL REAL ESTATE LENDING 11 CRE Loans by Industry ($4.0 billion – Mar 2014 – Period End) • More than 90 CRE colleagues: – Offices in Chicago, Cincinnati, Detroit, Green Bay, Indianapolis, Madison, Milwaukee, Minneapolis, and St. Louis • Recognized as: – #1 in US Syndicated CRE facilities under $50MM transaction size – #13 in US Syndicated CRE facilities Overall 1 Thomson Reuters LPC-January, 2014 2 Includes Missouri, Indiana, Ohio, Michigan, & Iowa CRE Loans by State ($4.0 billion – Mar 2014 – Period End) 1 1 |

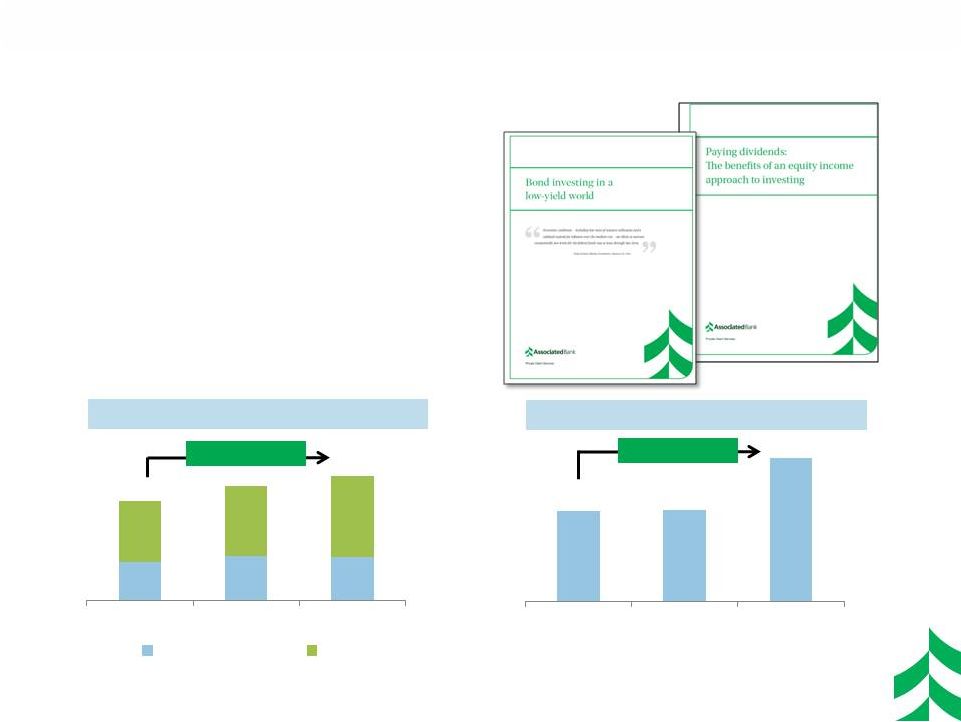

PRIVATE CLIENT & INSTITUTIONAL SERVICES 12 • More than 170 colleagues: – Private banking, personal trust, and portfolio management services for individuals ($500k to $10 million in investible assets) – Corporate trust, asset management and retirement plan services – $20.0 billion of AUM and AUA at March 31, 2014 Assets Under Management ($ in billions) Assets Under Administration ($ in billions) $6.0 $6.9 $7.5 (Thought Papers) $7.9 $8.0 $12.5 Mar 2012 Mar 2013 Mar 2014 $2.3 $2.7 $2.6 $3.7 $4.2 $4.9 Mar 2012 Mar 2013 Mar 2014 Fixed and Cash Equity CAGR = 11% CAGR = 23% |

RETAIL BANKING 13 • Over 2,000 colleagues servicing individuals and small business owners through five business units: – Consumer Banking, Business Banking, Residential Lending, Retail Payments, and Retail Brokerage • #1 mortgage originator in Wisconsin • A leading SBA lender in our markets • Official bank of the Green Bay Packers Beloit, Wisconsin (2013) Residential Mortgage Loans by State ($3.9 billion – Mar 2014 – Period End) 1 Includes Missouri, Indiana, Ohio, Michigan, & Iowa 2 Approximately 40% is in first-lien position Home Equity Loans by State ($1.8 billion – Mar 2014 – Period End) 2 Wisconsin 50% Illinois 32% Minnesota 12% In- Footprint 1 3% Other 3% Wisconsin 62% Illinois 17% Minnesota 12% Other 9% |

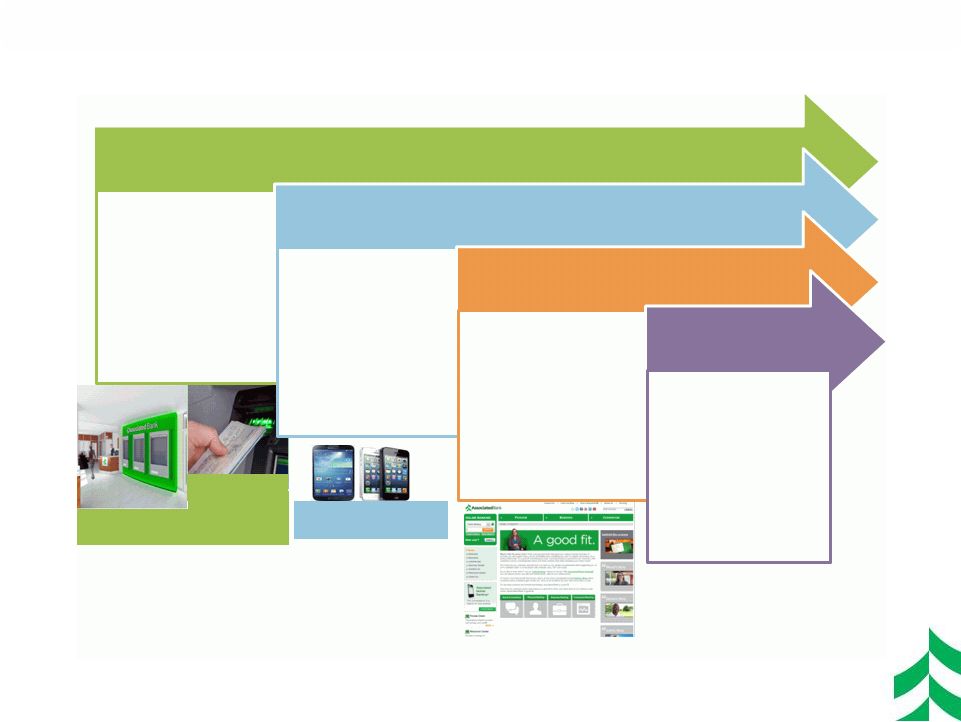

UPDATING OUR MODEL 14 1 Named Top 10 Mobile Banking App in August 2013 (The Financial Brand) Strategic Channel Evolution Deploying Lower Cost Branch Concepts Enhancing Virtual Banking • Deposit Automation ATM • Transaction Express • Financial Outlets • Online & Mobile Banking • Remote Deposit • Person-to- Person Delivering Via Digital Channels Selling Person to Person • Inbound Sales • Outbound Sales • Service to Sales Mobile Banking & Remote Deposit Deposit Automation ATM Financial Outlet • Digital Shopping • Digital Sales • Digital Service 1 |

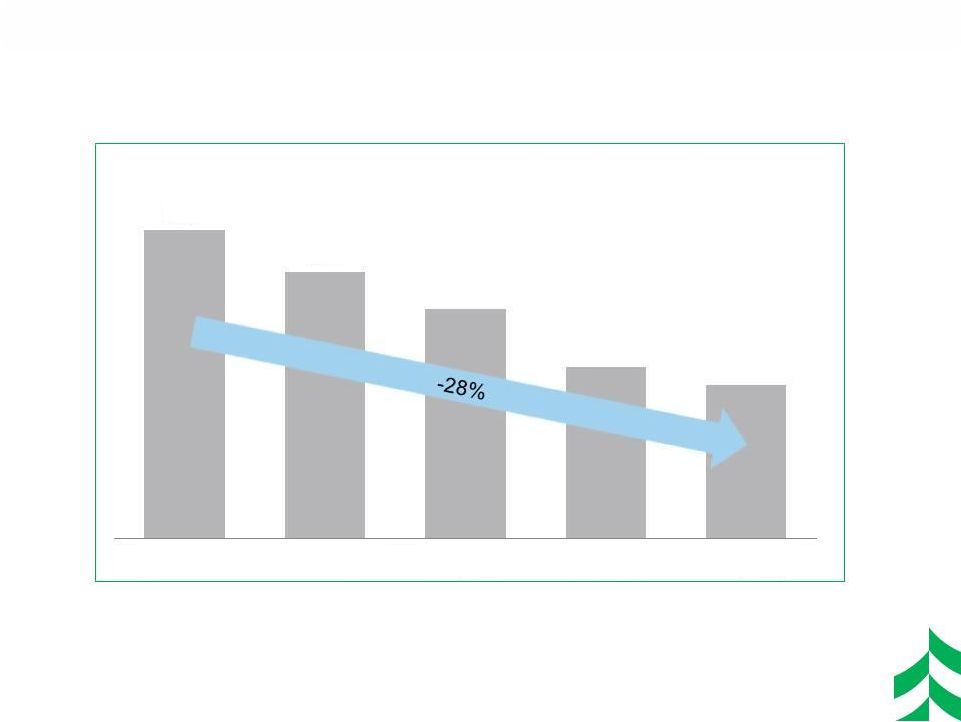

RATIONALIZING THE FOOTPRINT 15 Consolidated or sold 28% of branches since 2007 1 Branch counts are as of period end. 1 315 291 270 237 227 2Q 2007 2Q 2009 2Q 2011 4Q 2013 1Q 2014 |

CHANGING CUSTOMER PREFERENCES (PERCENTAGE OF TOTAL BANK DEPOSIT CUSTOMER BASE) 16 40% 43% 47% 49% 50% 0% 5% 8% 14% 15% 0% 10% 20% 30% 40% 50% 60% 2010 2011 2012 2013 Q1 2014 Active On-line Mobile Banking |

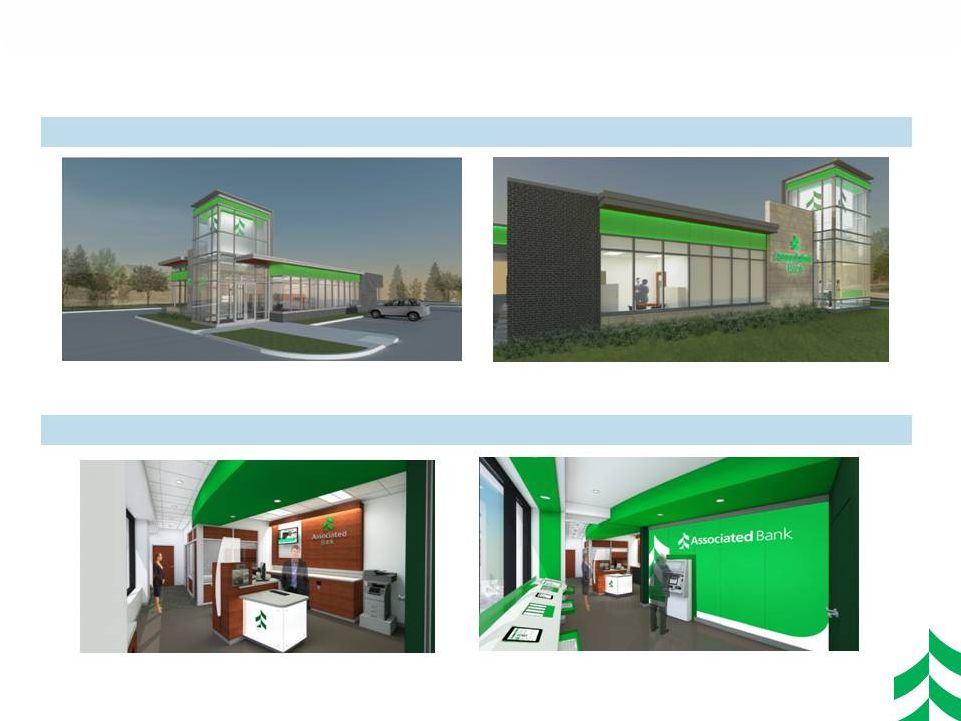

BRANCH EVOLUTION 17 • West Bend, Wisconsin • Green Bay, Wisconsin Branches coming in 2014: Lower construction costs, higher visibility profile • Madison, Wisconsin (UW Campus) Express Branch: Demonstration Kiosk – “Hands On” & Automated Teller Machine |

PURSUING EFFICIENCY GAINS 18 Areas of Focus Back Office Initiatives: • Implementing technology solutions in labor intensive processes Real Estate Initiatives: • Actions to optimize our real estate holdings and capacity Distribution Model Initiatives: • Optimize the ways that we interact with our customers Examples Examples Examples • Consolidation of corporate offices in Green Bay and Chicago • Consolidation of certain operations in Green Bay and Stevens Point • Branch design improvements • Channel development and optimization • New commercial loan system with end to end processing • Outsourcing testing and development • Right-sizing mortgage processing |

NONINTEREST INCOME TRENDS ($ IN MILLIONS) 19 Mortgage Banking Income Core Fee-based ¹ Revenue Other Non-Core² Fee Income Total Noninterest Income 1 – = Trust service fees plus Service charges on deposit accounts plus Card-based and other nondeposit fees plus Insurance commissions plus Brokerage and annuity commissions. This is a non-GAAP measure. Please refer to the April 17,2014 press release tables for a definition of this non-GAAP measure. 2 – = Total Noninterest Income minus Core Fee-based Revenue minus Mortgage Banking Income. This is a non-GAAP financial measure. $18 $19 $4 $8 $6 1Q 20132Q 20133Q 20134Q 20131Q 2014 $55 $55 $58 $57 $57 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 $9 $10 $10 $10 $10 1Q 20132Q 20133Q 20134Q 20131Q 2014 $82 $84 $71 $76 $74 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 Core Fee-based Revenue Other Non-core Fee Income |

NONINTEREST EXPENSE TRENDS ($ IN MILLIONS) 20 Total Noninterest Expense Personnel Spend / FTE ² Trend Efficiency Ratio ¹ 68% 67% 70% 73% 69% Technology Spend ³ Trend Other Non-Personnel Spend 4 Trend 1 – = Noninterest expense, excluding amortization of intangibles, divided by sum of taxable equivalent net interest income plus noninterest income, excluding investment securities gains, net, and asset gains, net. This is a non-GAAP financial measure and the reconciliation to a GAAP measure can be found in the appendix. 2 – FTE = Average Full Time Equivalent Employees 3 – Technology Spend = Data Processing and Equipment expenses 4 – Other Non-Personnel Spend = Total Noninterest Expense less Personnel and Technology spend $168 $169 $165 $179 $168 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 $98 $100 $98 $101 $98 4,841 4,790 4,699 4,584 4,517 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 Personnel Spend FTE $18 $19 $19 $19 $19 $12 $22 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 $52 $50 $49 $58 $51 $20 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 - Efficiency ratio |

CAPITAL MANAGEMENT PRIORITIES 21 Funding Organic Growth Paying a Competitive Dividend Non-organic Growth Opportunities Share Buybacks and Redemptions 2012 2013 • Fund Loan Growth and other Capital Investments • Repurchased $60 mm of Common Stock • Redeemed $205 mm in Trust Preferred • Repurchased $120 mm of Common Stock • Retired $26 mm in Sub-Debt • Increased quarterly dividend in Q4 2012 • Paid $0.23/ common share • Increased quarterly dividend in Q4 2013 • Paid $0.33/ common share • Focused on Cost Take-out Driven Depository M&A • Maintaining Discipline in Pricing of any Transaction 2014 • Repurchased $39 mm of Common Stock in Q1 2014 and $30 mm in Q2 2014 • Retired $155 mm in Senior Notes in Q1 2014 • Declared quarterly common dividend of $0.09/ share in Q1 2014 |

CAPITAL DEPLOYMENT OPPORTUNITIES 22 Basel I ASBC 1Q = 11.2% 1Q 10.5% 8% - 9.5% Basel III ASBC ³ Basel III 2 Systematically Important Financial Institutions 1 Regional and Community Banks = 7% ¹ +1 - 2.5% 2 Organic Asset Growth Non Organic Cash Acquisition Repurchase / Special Dividend Capacity 3 In July 2013, the Federal Reserve and the OCC published final rules (the “Basel III Capital Rules”) establishing a new comprehensive capital framework for U.S. banking organizations. 10.5% is 1Q estimate of Basel III capital ratio. Potential Excess Capital 1.0 – 2.5% Capital Deployment Options ~ ~ |

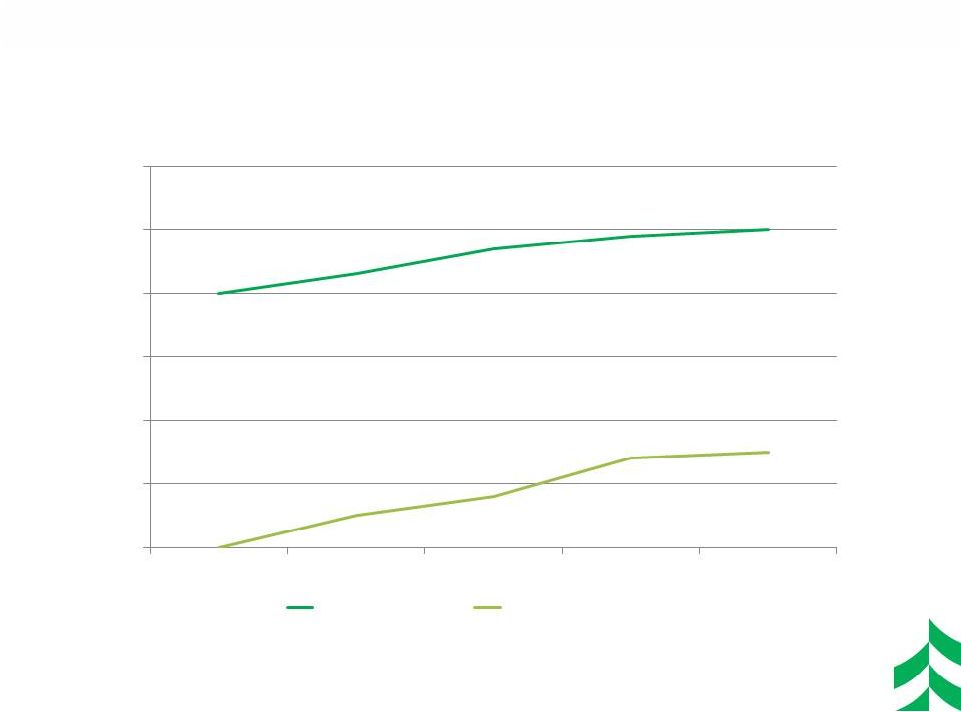

WHY ASSOCIATED 23 • Strong Capital Profile & Opportunities for Capital Deployment • Committed to Efficiency Ratio Improvement • Leading Midwest Bank Operating in Attractive Markets • Core Organic Growth Opportunity • Disciplined Loan and Deposit Pricing • Improving Credit Quality • Improving Earnings Profile Reasons to Invest Net Income Available to Common & ROT1CE ¹ Management Team Focused on Creating Long-Term Shareholder Value Net Income Available to Common ($ in millions) Return on Tier 1 Common Equity 1 – Return on Tier 1 Common Equity (ROT1CE) = Management uses Tier 1 common equity, along with other capital measures, to assess and monitor our capital position. This is a non-GAAP financial measure. Please refer to the appendix for a definition of this and other non-GAAP items. $115 $174 $184 6.7% 9.5% 9.8% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% $0 $30 $60 $90 $120 $150 $180 $210 $240 2011 2012 2013 |

APPENDIX 24 |

IMPROVEMENT IN CREDIT QUALITY INDICATORS ($ IN MILLIONS) 25 $344 $310 $277 $235 $220 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 Potential Problem Loans $225 $217 $208 $185 $178 1.45% 1.38% 1.33% 1.17% 1.08% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% $- $4 $8 $12 $16 $20 $24 $28 $36 $40 $48 $52 $56 $60 $64 $68 $72 $76 $80 $84 $88 $96 $100 $108 $112 $116 $120 $124 $132 $136 $140 $144 $148 $152 $156 $160 $164 $168 $176 $180 $188 $192 $196 $200 $204 $212 $216 $220 $224 $228 $232 $236 $240 $244 $248 $252 $256 $264 $268 $272 $276 $280 $284 $288 $292 $300 $304 $308 $312 $316 $320 $324 $328 $332 $336 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 Nonaccruals Nonaccruals / Loans $14 $14 $5 $5 $5 0.38% 0.35% 0.14% 0.14% 0.14% 0.00% 0.20% 0.40% 0.60% 0.80% 1.00% 1.20% 1.40% $20 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 Net Charge Offs NCOs / Avg Loans 127% 127% 131% 145% 151% 1.84% 1.76% 1.74% 1.69% 1.63% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% 4.50% 0% 80% 160% 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 ALLL/ Nonaccruals ALLL/ Total Loans |

Fair Value Composition – March 31, 2014 Investment Portfolio – March 31, 2014 Credit Rating ($ in thousands) Fair Value (000’s) % of Total Govt & Agency $4,583,810 83.8% AAA 97,113 1.8% AA 640,647 11.7% A 140,683 2.6% BAA1, BAA2 & BAA3 - 0.0% BA1 & Lower 1,943 0.0% Non-rated 6,857 0.2% TOTAL Market Value $5,471,054 100.0% Type Amortized Cost (000’s) Fair Value (000’s) TEY (%) Duration (Yrs) Govt & Agencies $1,001 $1,002 0.30 0.38 MBS 2,922,287 2,925,249 2.64 3.62 CMOs 848,403 846,690 2.54 3.00 GNMA CMBS 839,488 813,567 2.02 4.76 Municipals 834,192 858,490 5.26 4.81 ABS 21,318 21,282 0.55 0.28 Corporates 4,702 4,721 1.22 1.92 Other 18 53 - - TOTAL HTM & AFS $5,471,409 $5,471,054 2.90 3.85 INVESTMENT SECURITIES PORTFOLIO 26 Portfolio Ratings Composition – March 31, 2014 Type Fair Value (000’s) % of Total 0% RWA $881,534 16.1% 20% RWA 4,562,745 83.4% 50% RWA 21,930 0.4% =>100% RWA 7,149 0.1% Not subject to RW (2,304) -0.0% TOTAL Market Value $5,471,054 100% Risk Weighting Profile – March 31, 2014 MBS Fixed 17% MBS Hybrid 37% CMOs 15% GNMA CMBS 15% Municipals 16% |

SEGMENT PROFITABILITY YTD MARCH 2014 27 * Average Earning Assets ASBC Earning Assets* = $21.9 bn Total Revenue = $238.5 mm Net Income = $45.2 mm ROT1CE: 9.4% Consumer Banking Segment Earning Assets* = $7.2 bn Total Revenue = $115.4 mm Net Income = $7.2 mm ROT1CE: 5.9% Risk Management & Shared Services Segment Earning Assets* = $5.8 bn Total Revenue = $25.3 mm Net Income = $13.7 mm ROT1CE: 8.1% Commercial Banking Segment Earning Assets* = $8.9 bn Total Revenue = $97.8 mm Net Income = $24.4 mm ROT1CE: 12.5% |

NONINTEREST INCOME AND EXPENSE COMPOSITION FIRST QUARTER 2014 28 Noninterest Income by Category Noninterest Expense by Category ($74 million) ($168 million) Mortgage Banking 9% Svc Chg on Deposits 22% Card & Other Non Deposit 17% Trust Service Fees 16% Insurance 17% Capital Market 3% Brokerage & Annuity 5% BOLI 6% Other 5% Personnel 58% All other 16% Occupancy 9% Technology 8% Equipment 4% Legal & Professional 2% FDIC 3% |

RECONCILIATION AND DEFINITIONS OF NON-GAAP ITEMS 29 (1) Efficiency ratio is defined by the Federal Reserve guidance as noninterest expense divided by the sum of net interest income plus noninterest income, excluding investment securities gains / losses, net. Efficiency ratio, fully taxable equivalent, is noninterest expense, excluding other intangible amortization, divided by the sum of taxable equivalent net interest income plus noninterest income, excluding investment securities gains / losses, net and asset gains / losses, net. This efficiency ratio is presented on a taxable equivalent basis, which adjusts net interest income for the tax-favored status of certain loans and investment securities. Management believes this measure to be the preferred industry measurement of net interest income as it enhances the comparability of net interest income arising from taxable and tax-exempt sources and it excludes certain specific revenue items (such as investment securities gains / losses, net and asset gains / losses, net). Definition of Tier 1 Common Equity : Tier 1 Common Equity (T1CE), a non-GAAP financial measure, is used by banking regulators, investors and analysts to assess and compare the quality and composition of our capital with the capital of other financial services companies. Management uses Tier 1 common equity, along with other capital measures, to assess and monitor our capital position. Tier 1 Common Equity is Tier 1 capital excluding qualifying perpetual preferred stock and qualifying trust preferred securities. 1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 Efficiency Ratio Reconciliation: Efficiency ratio (1) 70.03% 69.01% 71.45% 73.70% 70.41% Taxable equivalent adjustment (1.46) (1.38) (1.50) (1.49) (1.35) Asset gains (losses), net 0.24 (0.01) 0.59 0.80 0.22 Other intangible amortization (0.42) (0.41) (0.44) (0.42) (0.42) Efficiency ratio, fully taxable equivalent (1) 68.39% 67.21% 70.10% 72.59% 68.86% |

OUR VISION 30 will be the most admired Midwestern financial services company, distinguished by sound, value-added financial solutions with personal service for our customers, built upon a strong commitment to our colleagues and the communities we serve, resulting in exceptional value for our shareholders. ASSOCIATED |