UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number: | | 811-04438 |

| | | |

| Exact name of registrant as specified in charter: | | Aberdeen Australia Equity Fund, Inc. |

| | | |

| Address of principal executive offices: | | 1900 Market Street, Suite 200 |

| | | Philadelphia, PA 19103 |

| | | |

| Name and address of agent for service: | | Andrea Melia |

| | | abrdn Inc. |

| | | 1900 Market Street Suite 200 |

| | | Philadelphia, PA 19103 |

| | | |

| Registrant’s telephone number, including area code: | | 1-800-522-5465 |

| | | |

| Date of fiscal year end: | | October 31 |

| | | |

| Date of reporting period: | | October 31, 2021 |

Item 1. Reports to Stockholders.

Aberdeen Australia Equity Fund, Inc. (IAF)

Annual Report

October 31, 2021

abrdn.com

Managed Distribution Policy (unaudited)

The Board of Directors of the Aberdeen Australia Equity Fund, Inc. (the "Fund") has authorized a managed distribution policy ("MDP") of paying quarterly distributions at an annual rate, set once a year, that is a percentage of the rolling average of the Fund's net asset values over the preceding three month period ending on the last day of the month immediately preceding the distribution's declaration date. With each distribution, the Fund will issue a notice to shareholders and an accompanying press release which will provide detailed information

regarding the estimated amount and composition of the distribution and other information required by the Fund's MDP exemptive order. The Fund's Board of Directors may amend or terminate the MDP at any time without prior notice to shareholders; however, at this time, there are no reasonably foreseeable circumstances that might cause the termination of the MDP. You should not draw any conclusions about the Fund's investment performance from the amount of distributions or from the terms of the Fund's MDP.

Distribution Disclosure Classification (unaudited)

The Fund's policy is to provide investors with a stable distribution rate. Each quarterly distribution will be paid out of current income, supplemented by realized capital gains and, to the extent necessary, paid-in capital.

The Fund is subject to U.S. corporate, tax and securities laws. Under U.S. tax rules, the amount applicable to the Fund and character of distributable income for each fiscal period depends on the actual exchange rates during the entire year between the U.S. Dollar and the currencies in which Fund assets are denominated and on the aggregate gains and losses realized by the Fund during the entire year.

Therefore, the exact amount of distributable income for each fiscal year can only be determined as of the end of the Fund's fiscal year, October 31. Under Section 19 of the Investment Company Act of 1940,

as amended (the "1940 Act"), the Fund is required to indicate the sources of certain distributions to shareholders. The estimated distribution composition may vary from quarter to quarter because it may be materially impacted by future income, expenses and realized gains and losses on securities and fluctuations in the value of the currencies in which Fund assets are denominated.

The distributions for the fiscal year ended October 31, 2021 consisted of 29% net investment income and 71% net realized gains.

In January 2022, a Form 1099-DIV will be sent to shareholders, which will state the final amount and composition of distributions and provide information with respect to their appropriate tax treatment for the 2021 calendar year.

| Aberdeen Australia Equity Fund, Inc. |

Letter to Shareholders (unaudited)

Dear Shareholder,

We present this Annual Report, which covers the activities of Aberdeen Australia Equity Fund, Inc. (the "Fund"), for the fiscal year ended October 31, 2021. The Fund's principal investment objective is long-term capital appreciation through investment primarily in equity securities of Australian companies listed on the Australian Stock Exchange Limited. Its secondary objective is current income, which is expected to be derived primarily from dividends and interest on Australian corporate and governmental securities.

Total Investment Return1

For the fiscal year ended October 31, 2021, the total return to shareholders of the Fund based on the net asset value ("NAV") and market price of the Fund, respectively, compared to the Fund's benchmark are as follows:

| NAV2,3 | | 38.1% | |

| Market Price2 | | 50.5% | |

| S&P/ASX 200 Accumulation Index ("ASX 200") (Net)4 | | 36.6% | |

For more information about Fund performance, please see the Report of the Investment Manager (page 4) and Total Investment Returns (page 7).

NAV, Market Price and Premium/Discount

The below table represents comparison from current fiscal year end to prior fiscal year end of market price to NAV and associated Premium(+) and Discount(-).

| | |

NAV | | | Closing

Market

Price | | | Premium(+)/

Discount(-) | |

| 10/31/2021 | | $6.44 | | | $6.08 | | | -5.6% | |

| 10/31/2020 | | $5.16 | | | $4.47 | | | -13.4% | |

During the fiscal year ended October 31, 2021, the Fund's NAV was within a range of $5.22 to $6.55 and the Fund's market price traded within a range of $4.51 to $6.62. During the fiscal year ended October 31, 2021, the Fund's shares traded within a range of a premium(+)/discount(-) of -15.6% to +7.5%.

Managed Distribution Policy

The Fund has a managed distribution policy of paying quarterly distributions at an annual rate, set once a year, as a percentage of the rolling average of the Fund's net asset values over the preceding three month period ending on the last day of the month immediately preceding the distribution's declaration date. In March 2021, the Board of Directors of the Fund (the "Board") determined the rolling distribution rate to be 10% for the 12-month period commencing with the distribution payable in June 2021. This policy will be subject to regular review by the Board. The distributions will be made from current income, supplemented by realized capital gains and, to the extent necessary, paid-in capital, which is a nontaxable return of capital.

On November 9, 2021, the Fund announced that it will pay on January 11, 2022, a stock distribution of US $0.16 per share to all shareholders of record as of November 19, 2021. This stock distribution will automatically be paid in newly issued shares of the Fund unless otherwise instructed by the shareholder. Shares of common stock will be issued at the lower of the NAV per share or the market price per share with a floor for the NAV of not less than 95% of the market price. Fractional shares will generally be settled in cash, except for registered shareholders with book entry accounts at Computershare Investor Services who will have whole and fractional shares added to their account.

Shareholders may request to be paid their quarterly distributions in cash instead of shares of common stock by providing advance notice to the bank, brokerage or nominee who holds their shares if the shares are in "street name" or by filling out in advance an election card received from Computershare Investor Services if the shares are in registered form.

The Fund is covered under exemptive relief received by the Fund's investment manager from the U.S. Securities and Exchange Commission ("SEC") that allows the Fund to distribute long-term capital gains as frequently as monthly in any one taxable year.

Loan Facility and Use of Leverage

The Fund is permitted to borrow for investment purposes as may be permitted by the 1940 Act or any rule, order or interpretation thereunder. This allows the Fund to borrow for investment purposes in the amount up to 33 1/3% of the Fund's total assets.

On October 13, 2020, the Fund entered into a 3-year term revolving credit facility with a committed facility of AUD$20million with State

| 1 | Past performance is no guarantee of future results. Investment returns and principal value will fluctuate and shares, when sold, may be worth more or less than original cost. Current performance may be lower or higher than the performance quoted. Net asset value return data include investment management fees, custodial charges and administrative fees (such as Director and legal fees) and assumes the reinvestment of all distributions. |

| 2 | Assuming the reinvestment of dividends and distributions. |

| 3 | The Fund's total return is based on the reported NAV for each financial reporting period end and may differ from what is reported on the Financial Highlights due to financial statement rounding or adjustments. |

| 4 | The ASX 200 is a market-capitalization weighted and float-adjusted stock market index of Australian stocks listed on the Australian Securities Exchange from S&P Global Ratings. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index. |

| Aberdeen Australia Equity Fund, Inc. | 1 |

Letter to Shareholders (unaudited) (continued)

Street Global Advisors. The Fund's outstanding balance as of October 31, 2021 was AUD$10 million on the revolving credit facility. Under the terms of the loan facility and applicable regulations, the Fund is required to maintain certain asset coverage ratios for the amount of its outstanding borrowings.

Open Market Repurchase Program

The Fund's policy is generally to buy back Fund shares on the open market when the Fund trades at certain discounts to NAV and management believes such repurchases may enhance shareholder value. During the fiscal year ended October 31, 2021, the Fund did not repurchase any shares.

Portfolio Holdings Disclosure

The Fund's complete schedule of portfolio holdings for the second and fourth quarters of each fiscal year are included in the Fund's semiannual and annual reports to shareholders. The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. These reports are available on the SEC's website at sec.gov. The Fund makes the information available to shareholders upon request and without charge by calling Investor Relations toll-free at 1-800-522-5465.

Proxy Voting

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12 month period ended June 30 is available by August 31 of the relevant year: (1) without charge upon request by calling Investor Relations toll-free at 1-800-522-5465; and (2) on the SEC's website at sec.gov.

Unclaimed Share Accounts

Please be advised that abandoned or unclaimed property laws for certain states require financial organizations to transfer (escheat) unclaimed property (including Fund shares) to the state. Each state has its own definition of unclaimed property, and Fund shares could be considered "unclaimed property" due to account inactivity (e.g., no owner-generated activity for a certain period), returned mail (e.g., when mail sent to a shareholder is returned to the Fund's transfer agent as undeliverable), or a combination of both. If your Fund shares are categorized as unclaimed, your financial advisor or the Fund's transfer agent will follow the applicable state's statutory requirements to contact you, but if unsuccessful, laws may require that the shares be escheated to the appropriate state. If this happens, you will have to contact the state to recover your property, which may involve time and expense. For more information on unclaimed property and how

to maintain an active account, please contact your financial adviser or the Fund's transfer agent.

COVID-19

Beginning in the first quarter of 2020, the illness caused by a novel coronavirus, COVID-19, has resulted in a global pandemic and major disruption to economies and markets around the world, including the United States. Financial markets have experienced extreme volatility and severe losses. Some sectors of the economy and individual issuers have experienced particularly large losses. These circumstances may continue for an extended period of time, and as a result may affect adversely the value and liquidity of the Fund's investments. The rapid development and fluidity of this situation precludes any prediction as to the ultimate adverse impact of COVID-19 on economic and market conditions, and, as a result, present uncertainty and risk with respect to the Fund and the performance of its investments and ability to pay distributions. The full extent of the impact and effects of COVID-19 will depend on future developments, including, among other factors, the duration and spread of the outbreak, along with related travel advisories, quarantines and restrictions, the recovery time of the disrupted supply chains and industries, the impact of labor market interruptions, the impact of government interventions, and uncertainty with respect to the duration of the global economic slowdown.

LIBOR

Under the revolving credit facility, the Fund is charged interest on amounts borrowed at a variable rate, which may be based on the London Interbank Offered Rate ("LIBOR") plus a spread. The Fund may invest in certain debt securities, derivatives or other financial instruments that utilize LIBOR as a "benchmark" or "reference rate" for various interest rate calculations. In July 2017, the United Kingdom Financial Conduct Authority ("FCA"), which regulates LIBOR, announced a desire to phase out the use of LIBOR by the end of 2021. However, subsequent announcements by the FCA, the LIBOR administrator and other regulators indicate that it is possible that the most widely used LIBOR rates may continue until mid-2023. It is anticipated that LIBOR ultimately will be discontinued or the regulator will announce that it is no longer sufficiently robust to be representative of its underlying market around that time. Although financial regulators and industry working groups have suggested alternative reference rates, such as European Interbank Offered Rate ("EURIBOR"), Sterling Overnight Interbank Average Rate ("SONIA") and Secured Overnight Financing Rate ("SOFR"), global consensus on alternative rates is lacking and the process for amending existing contracts or instruments to transition away from LIBOR remains unclear. The elimination of LIBOR or changes to other reference rates or any other changes or reforms to the determination or supervision of reference rates could have an adverse impact on the market for, or

| 2 | Aberdeen Australia Equity Fund, Inc. |

Letter to Shareholders (unaudited) (concluded)

value of, any securities or payments linked to those reference rates, which may adversely affect the Fund's performance and/or net asset value. Uncertainty and risk also remain regarding the willingness and ability of issuers and lenders to include revised provisions in new and existing contracts or instruments. Consequently, the transition away from LIBOR to other reference rates may lead to increased volatility and illiquidity in markets that are tied to LIBOR, fluctuations in values of LIBOR-related investments or investments in issuers that utilize LIBOR, increased difficulty in borrowing or refinancing and diminished effectiveness of hedging strategies, adversely affecting the Fund's performance. Furthermore, the risks associated with the expected discontinuation of LIBOR and transition may be exacerbated if the work necessary to effect an orderly transition to an alternative reference rate is not completed in a timely manner. Because the usefulness of LIBOR as a benchmark could deteriorate during the transition period, these effects could occur prior to the end of 2021.

abrdn

abrdn plc, formerly known as Standard Life Aberdeen plc, was renamed on September 27, 2021. In connection with this re-branding, the entities within abrdn plc group, including investment advisory entities, have been or will be renamed in the near future. In addition, the fund names are anticipated to be re-branded over the next year.

Investor Relations Information

As part of abrdn's commitment to shareholders, we invite you to visit the Fund on the web at www.aberdeeniaf.com. Here, you can view monthly fact sheets, quarterly commentary, distribution and performance information, and other Fund literature.

Enroll in abrdn's email services and be among the first to receive the latest closed-end fund news, announcements, videos, and other information. In addition, you can receive electronic versions of important Fund documents, including annual reports, semi-annual reports, prospectuses and proxy statements. Sign up today at https://www.abrdn.com/en-us/cefinvestorcenter/contact-us/preferences

Contact Us:

| • | Visit: https://www.abrdn.com/en-us/cefinvestorcenter |

| • | Email: Investor.Relations@abrdn.com; or |

| • | Call: 1-800-522-5465 (toll free in the U.S.). |

Yours sincerely,

/s/ Christian Pittard

Christian Pittard

President

All amounts are U.S. Dollars unless otherwise stated.

| Aberdeen Australia Equity Fund, Inc. | 3 |

Report of the Investment Manager (unaudited)

Market/economic review

Australian equities advanced in tandem with their peers across the Asia-Pacific region and the wider developed markets over the 12-month reporting period ended October 31, 2021. Investors' optimism that the expanding rollout of COVID-19 vaccines would fuel a faster global recovery bolstered stock prices. Improving economic data in Australia and from key trading partners, as well as the Reserve Bank of Australia's (RBA) loose monetary policy, further buoyed market sentiment. The resource-rich market also gained from a rally in key commodities, including oil and iron ore. All of these factors offset worries about Australia's worsening relations with China and a rise in COVID-19 cases later in the period.

Late in the reporting period, there was optimism across the country as COVID-19-induced lockdowns eased in many regions. New South Wales moved to a two-tier system, giving vaccinated citizens greater freedom. Melbourne was released from lockdown after nearly nine months of restrictions. Vaccination rates have continued to rise, with more than 77% of adults in Australia fully vaccinated as of the end of the reporting period on October 31, 2021.1 On the same day, the Australian government also lifted the travel ban restricting Australian citizens from leaving the country. Furthermore, the government indicated that rules for foreigners could also be relaxed soon thereafter.

Thanks to the greater freedoms, recent Australian Performance of Manufacturing Index (PMI) data showed a notable uptick in business sentiment. Economic reopening increased the services sector figure in October 2021, after three months of contraction.

As expected, the RBA maintained the cash rate at a record low of 0.1% during its meeting in September 2021. The central bank stated that interest rates would remain at this level until inflation is comfortably within its target range of 2-3%. The RBA still plans to trim the purchase of government bonds to AUD$4 billion (US$2.9 billion) per week until at least mid-February 2022.

Fund performance review

Aberdeen Australia Equity Fund, Inc. returned 38.1% on a net asset value basis for the 12-month reporting period ended October 31, 2021, versus the 36.6% return of its benchmark, the S&P ASX 200 Accumulation Index (net dividends). During the period, there was a broad market rotation away from quality growth-oriented companies in favor of those seen as benefiting more from the economic rebound.

At the end of the reporting period, the Fund's largest position was in the financials sector, although it had an underweight allocation relative to the benchmark index. Stock selection within the financials sector hampered the Fund's performance relative to its benchmark index for the reporting period, as banking stocks performed well due to expectations of an economic rebound. The banking sector benefited from structurally lower loan losses, a steepening of the yield curve and forecasts of higher credit growth from the recovery in the housing market. We feel that Australian lenders are well capitalized, with potential for additional capital returns to shareholders. The Fund's relatively small position in Westpac Banking Corp. weighed on the Fund's relative performance, although the holding in Commonwealth Bank of Australia helped to offset those losses.

Stock selection in the materials sector also contributed positively to the Fund's relative performance for the reporting period. The position in mining company BHP Group Ltd. posted strong results and a higher-than-expected dividend during the reporting period. The company continued to execute well operationally, with record iron ore production alongside lower operating costs, despite the effects of COVID-19, weather disruptions and other inflationary pressures. Miner Oz Minerals' stock price increased over the reporting period due to sustained strength in copper prices. The lack of exposure to iron ore producer Fortescue Metals Group Ltd. also enhanced Fund performance. Conversely, the Fund's holding in gold producer Northern Star Resources Ltd. was a major detractor from performance as its shares tracked a decline in the price of gold.

Stock selection in the healthcare sector weighed on Fund performance over the reporting period. Medical device manufacturer Fisher & Paykel Healthcare Corp. Ltd. recorded generally positive results over the period, as its humidification and nasal high-flow products were used worldwide to treat COVID-19 patients. However, investors appeared to be disappointed about uncertainty in the coming year. Management cited hospital stocking and destocking, along with unpredictable COVID-19 surges, as reasons why the company is unable to provide clear near-term earnings guidance. While hearing device implant maker Cochlear Ltd.'s results for its 2021 fiscal year were largely in line with investors' expectations, its shares underperformed as management's earnings guidance for the company's 2022 fiscal year did not meet the market's expectations. Cochlear's business also was hampered by ongoing COVID-19 restrictions in several regions. The Fund's holding in biotechnology firm CSL Ltd. also detracted from performance for the reporting period.

| 1 | Source: Australian Government Department of Health, November 2021 |

| 4 | Aberdeen Australia Equity Fund, Inc. |

Report of the Investment Manager (unaudited) (continued)

The stock price of the Fund's holding in gaming company Aristocrat Leisure Ltd. increased over the reporting period as its core U.S. market reopened and its digital gaming business performed well. Cloud-based accounting software provider Xero Ltd. contributed positively to Fund performance despite bouts of investors' profit-taking amid the market's rotation into lower-valuation cyclical stocks. The company continued to see notable subscriber growth in a challenging environment while effectively managing expenses. We maintain a positive view of Xero's market-leading product, track record of execution, and the growth potential of its platform.

Regarding key portfolio activity, early in the reporting period, we established a new position in retail conglomerate Wesfarmers Ltd. as we believe that the Australian housing market recovery will drive robust earnings at its market-leading household hardware chain, Bunnings. We purchased shares of power-generation company Mercury NZ Ltd. given our positive view of the company's exposure to 100% renewable-electricity generation, and we felt that a share-price pullback offered an attractive entry point. We also initiated a holding in Pro Medicus Ltd., which supplies imaging software to hospitals globally. We believe that the company has a high-quality, high-margin business with long-term recurring revenue streams and a track record of delivering robust organic growth. Additionally, we established a new position in James Hardie Industries plc, a leading fiber cement manufacturer leveraged to the U.S. housing market. We believe that a backdrop of low interest rates, government stimulus and a firmer recovery in employment prospects will be conducive to higher levels of housing activity. The company is also executing on growth initiatives that are expected to enhance its business in the medium term. Toward the end of the reporting period, we established new positions in IDP Education Ltd. and Megaport Ltd. In our view, global student placement services provider IDP Education should benefit from the reopening of international borders, with the company also investing heavily into its digital offering. We think that universities will continue to value IDP's services after COVID-19 restrictions end. We believe that IT services provider Megaport is positioned well to benefit from the global structural shift into cloud computing.

Furthermore, we initiated a holding in gold mining company Evolution Mining Ltd. We have been monitoring the company for some time as its management has a strong track record of extracting value from

underperforming assets sold off by its larger peers. In our opinion, this is illustrated by the announcement of additional asset purchases from its peer, Northern Star Resources. We believe that the company's anticipated synergistic2 benefits should be achievable.

We funded the new holding in Evolution Mining by selling the Fund's shares in Newcrest Mining Ltd. We also exited the Fund's position in energy infrastructure company APA Group, as we lacked conviction in the company's revised growth strategy. We think that the energy transition that we are currently witnessing potentially could put the company's existing asset and earnings streams at risk, which is a key issue that we feel remains unaddressed and could exert growing pressure on its business over time.

We sold the Fund's shares in Westpac Banking Corp., due to the company's poor management execution, ongoing impairments,3 and remediation of various business lines. We sold the position prior to Westpac's most recent earnings announcement, as we anticipated the disappointing results. Earlier in the reporting period, we reduced and subsequently exited the Fund's position in a2 Milk Co. Ltd., a producer of protein-free milk, given our concerns over the daigou sales channel4 and excess inventory in its supply chain.

This Fund pays a quarterly distribution to shareholders. Funding from the distribution is a combination of capital gains from trading, income received in the form or dividends from underlying securities and retained earnings (capital). While the Fund's primary objective is capital returns for shareholders, we also manage Fund cash flows in an effort to meet the Fund's quarterly distribution target. This policy did not have a material effect on the Fund's investment strategy over the reporting period. During the 12-month period ended October 31, 2021, the distributions comprised dividend income and capital gains. Over the 12-month period ended October 31, 2021, the Fund issued total distributions of $0.59 per share.

We have the Fund Board's approval and a credit facility5 for AUD$20 million of leverage in the Fund. We invested AUD$10 million of this total across the Fund's portfolio in October 2020, and we have held this position since that time. The loan is rolled over on a monthly basis and, if there were a meaningful pullback in the Australian equity market, we would look to invest further.

| 2 | Synergy refers to the concept that the combined value and performance of two companies will be greater than the sum of the separate individual parts. |

| 3 | An impairment is a permanent reduction in the value of a company's asset. |

| 4 | The daigou sales channel refers to cross-border exporting in which an individual or a syndicated group of exporters outside of China purchases commodities (mainly luxury goods, but also groceries occasionally) for customers in China. |

| 5 | A credit facility is a type of loan that allows the borrowing business to take out money over an extended period of time rather than reapplying for a loan each time it needs money. |

| | Aberdeen Australia Equity Fund, Inc. | 5 |

Report of the Investment Manager (unaudited) (concluded)

Outlook

As we see the Australian economy begin to reopen, we anticipate that there will be a strong rebound in the fundamental drivers of business confidence, consumer sentiment and unemployment. While we believe that the momentum in corporate earnings growth has peaked, we still think that there will be a positive growth trend over the coming months and the upturn in corporate earnings should continue.

In addition, the RBA's pledge to keep interest rates lower for longer should support asset prices. In our view, a strengthening property market also should boost consumer spending, construction and employment. At the corporate level, as the economic recovery continues, companies are likely to move from capital preservation to capital allocation, with a notable pick-up in M&A activity and capital management.

We remain committed to our bottom-up investment style with a focus on what we believe are high-quality companies. We favor businesses that, in our view, have clear growth prospects that are leveraged to long-term structural shifts. The relative defensiveness of the Fund's holdings, in terms of their robust balance sheets and prospects for through-cycle earnings and dividend growth, is an added advantage. Many of the Fund's company holdings are also leaders on governance

and sustainability, which we believe positions them well to adapt to future challenges and opportunities. In our view, this should enable the Fund to perform well amid the current market uncertainties and over the long term.

Risk Considerations

Past performance is not an indication of future results.

Foreign securities in which the Fund may invest may be more volatile, harder to price and less liquid than U.S. securities. They are subject to risks associated with less stringent accounting and regulatory standards, the impact of currency exchange rate fluctuation political and economic instability, reduced information about issuers, higher transaction costs and delayed settlement. There are also risks associated with investing in Australia, including the risk of investing in a single-country Fund. The Fund focuses its investments in the Australia region, which subjects the Fund to more volatility and greater risk of loss than geographically diverse funds. Equity stocks of small and mid-cap companies carry greater risk, and more volatility than equity stocks of larger, more established companies.

abrdn Asia Limited (formerly known as Aberdeen Standard Investments (Asia) Limited)

| 6 | Aberdeen Australia Equity Fund, Inc. | |

Total Investment Return (unaudited)

The following table summarizes the average annual Fund performance compared to the S&P ASX 200 Index, the Fund's benchmark, for the 1-year, 3-year, 5-year and 10-year periods ended as of October 31, 2021.

| | | 1 Year | | | 3 Years | | | 5 Years | | | 10 Years | |

| Net Asset Value (NAV) | | 38.1% | | | 17.3% | | | 12.4% | | | 6.5% | |

| Market Price | | 50.5% | | | 17.5% | | | 13.2% | | | 5.7% | |

| S&P/ASX 200 (Net) | | 36.6% | | | 13.8% | | | 10.3% | | | 6.0% | |

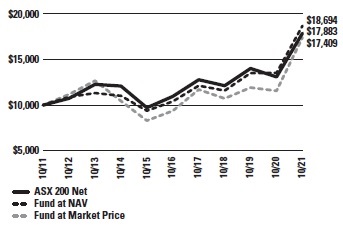

Performance of a $10,000 Investment (as of October 31, 2021)

This graph shows the change in value of a hypothetical investment of $10,000 in the Fund for the period indicated. For comparison, the same investment is shown in the indicated index.

Aberdeen Standard Investments Inc. has entered into an agreement with the Fund to limit investor relations services fees, without which performance would be lower. This agreement aligns with the term of the advisory agreement and may not be terminated prior to the end of the current term of the advisory agreement. See Note 3 in the Notes to Financial Statements.

Returns represent past performance. Total investment return at NAV is based on changes in the NAV of Fund shares and assumes reinvestment of dividends and distributions, if any, at market prices pursuant to the dividend reinvestment program. All return data at NAV includes fees charged to the Fund, which are listed in the Fund's Statement of Operations under "Expenses". The Fund's total investment return is based on the reported NAV on each financial reporting period end. Total investment return at market value is based on changes in the market price at which the Fund's shares traded on the NYSE American during the period and assumes reinvestment of dividends and distributions, if any, at market prices pursuant to the dividend reinvestment program sponsored by the Fund's transfer agent. Because the Fund's shares trade in the stock market based on investor demand, the Fund may trade at a price higher or lower than its NAV. Therefore, returns are calculated based on both market price and NAV. Past performance is no guarantee of future results. The performance information provided does not reflect the deduction of taxes that a shareholder would pay on distributions received from the Fund. The current performance of the Fund may be lower or higher than the figures shown. The Fund's yield, return, market price and NAV will fluctuate. Performance information current to the most recent month-end is available at www.aberdeeniaf.com or by calling 800-522-5465.

The net operating expense ratio both excluding and net of fee waivers based on the fiscal year ended October 31, 2021 was 1.55%. The net operating expense ratio, net of fee waivers and excluding interest expense, based on the fiscal year ended October 31, 2021 was 1.49%.

| Aberdeen Australia Equity Fund, Inc. | 7 |

Portfolio Summary (unaudited)

The following table summarizes the sector composition of the Fund's portfolio, in S&P Global Inc.'s Global Industry Classification Standard ("GICS") Sectors, expressed as a percentage of net assets as of October 31, 2021.

| Top Sectors | | As a Percentage of Net Assets | |

| Financials | | 30.1% | * |

| Materials | | 17.2% | |

| Health Care | | 15.7% | |

| Consumer Discretionary | | 8.4% | |

| Information Technology | | 8.3% | |

| Real Estate | | 7.5% | |

| Communication Services | | 4.4% | |

| Industrials | | 3.7% | |

| Consumer Staples | | 3.4% | |

| Energy | | 3.1% | |

| Utilities | | 1.5% | |

| Short-Term Investment | | 0.2% | |

| Liabilities in Excess of Other Assets | | (3.5)% | |

| | | 100.0% | |

| * | The sectors, as classified by GICS, are comprised of several industries. As of October 31, 2021 the Fund's holdings in the Financials sector were allocated to three industries: Banks (19.9%), Capital Markets (7.6%) and Insurance (2.6%). |

Top Ten Equity Holdings (unaudited)

The following were the Fund's top ten equity holdings as of October 31, 2021:

| Name of Security | | As a Percentage of Net Assets | |

| Commonwealth Bank of Australia | | 9.6% | |

| CSL Ltd. | | 7.3% | |

| BHP Group PLC | | 7.1% | |

| National Australia Bank Ltd. | | 6.6% | |

| Xero Ltd. | | 4.7% | |

| Macquarie Group Ltd. | | 4.6% | |

| Aristocrat Leisure Ltd. | | 4.1% | |

| Goodman Group, REIT | | 4.0% | |

| Australia & New Zealand Banking Group Ltd. | | 3.8% | |

| Telstra Corp. Ltd. | | 3.5% | |

| 8 | Aberdeen Australia Equity Fund, Inc. | |

Portfolio of Investments

As of October 31, 2021

| Shares | | Description | Industry and Percentage

of Net Assets | | Value

(US$) | |

| LONG-TERM INVESTMENTS—103.3% | | | | |

| COMMON STOCKS—103.3% | | | | |

| AUSTRALIA—90.7% | | | | |

| 23,850 | | Afterpay Ltd.(a) | Information Technology Services—1.4% | | $ 2,209,449 | |

| 72,600 | | Altium Ltd. | Software—1.3% | | 2,022,392 | |

| 179,842 | | Aristocrat Leisure Ltd. | Hotels, Restaurants & Leisure—4.1% | | 6,378,405 | |

| 74,100 | | ASX Ltd. | Capital Markets—3.0% | | 4,659,985 | |

| 447,300 | | AusNet Services | Electric Utilities—0.5% | | 831,821 | |

| 276,500 | | Australia & New Zealand Banking Group Ltd. | Banks—3.8% | | 5,884,050 | |

| 1,530,200 | | Beach Energy Ltd. | Oil, Gas & Consumable Fuels—1.1% | | 1,607,484 | |

| 412,900 | | BHP Group PLC | Metals & Mining—7.1% | | 10,905,338 | |

| 179,600 | | Charter Hall Group | Equity Real Estate Investment Trusts (REIT)—1.5% | | 2,356,337 | |

| 31,600 | | Cochlear Ltd. | Health Care—3.4% | | 5,285,482 | |

| 185,500 | | Commonwealth Bank of Australia | Banks—9.6% | | 14,703,137 | |

| 49,700 | | CSL Ltd. | Biotechnology—7.3% | | 11,308,752 | |

| 309,800 | | Endeavour Group Ltd. | Food & Staples Retailing—1.0% | | 1,591,897 | |

| 1,031,400 | | Evolution Mining Ltd.(a) | Metals & Mining—1.8% | | 2,800,188 | |

| 375,300 | | Goodman Group, REIT | Equity Real Estate Investment Trusts (REIT)—4.0% | | 6,213,797 | |

| 75,000 | | IDP Education Ltd.(a) | Diversified Consumer Services—1.4% | | 2,121,979 | |

| 544,500 | | Insurance Australia Group Ltd. | Insurance—1.3% | | 1,972,982 | |

| 63,700 | | James Hardie Industries PLC | Construction Materials—1.6% | | 2,502,531 | |

| 47,800 | | Macquarie Group Ltd. | Capital Markets—4.6% | | 7,056,668 | |

| 745,200 | | Medibank Pvt Ltd. | Insurance—1.2% | | 1,872,784 | |

| 96,100 | | Megaport Ltd.(a) | Information Technology Services—0.9% | | 1,300,551 | |

| 1,414,000 | | Mirvac Group, REIT | Equity Real Estate Investment Trusts (REIT)—2.0% | | 3,017,709 | |

| 463,600 | | National Australia Bank Ltd. | Banks—6.6% | | 10,079,580 | |

| 382,800 | | Northern Star Resources Ltd. | Metals & Mining—1.7% | | 2,650,061 | |

| 250,500 | | OZ Minerals Ltd. | Metals & Mining—3.1% | | 4,764,975 | |

| 40,100 | | Pro Medicus Ltd. | Health Care Technology—1.1% | | 1,619,376 | |

| 45,700 | | Rio Tinto PLC—London Listing | Metals & Mining—1.9% | | 2,849,462 | |

| 395,800 | | Sydney Airport(a) | Transportation Infrastructure—1.6% | | 2,454,529 | |

| 1,848,000 | | Telstra Corp. Ltd. | Diversified Telecommunication Services—3.5% | | 5,341,603 | |

| 102,800 | | Wesfarmers Ltd. | Multiline Retail—2.9% | | 4,447,716 | |

| 176,400 | | Woodside Petroleum Ltd. | Oil, Gas & Consumable Fuels—2.0% | | 3,083,750 | |

| 130,000 | | Woolworths Group Ltd. | Food & Staples Retailing—2.4% | | 3,744,626 | |

| | | 139,639,396 | |

| NEW ZEALAND—10.4% | |

| 564,600 | | Auckland International Airport Ltd.(a) | Transportation Infrastructure—2.1% | | 3,201,649 | |

| 120,100 | | Fisher & Paykel Healthcare Corp. Ltd. | Health Care—1.7% | | 2,679,572 | |

| 333,900 | | Mercury NZ Ltd.(a) | Electric Utilities—1.0% | | 1,499,523 | |

| 442,200 | | Spark New Zealand Ltd.(a) | Diversified Telecommunication Services—0.9% | | 1,441,155 | |

| 63,800 | | Xero Ltd.(a) | Software—4.7% | | 7,274,654 | |

| | | 16,096,553 | |

| UNITED STATES—2.2% | |

| 117,300 | | ResMed, Inc., GDR | Health Care—2.2% | | 3,332,017 | |

| | | Total Long-Term Investments—103.3% (cost $115,758,086) | | 159,067,966 | |

| | Aberdeen Australia Equity Fund, Inc. | 9 |

Portfolio of Investments (concluded)

As of October 31, 2021

| Shares | Description | Value

(US$) | |

| SHORT-TERM INVESTMENT—0.2% | |

| UNITED STATES—0.2% | |

| 312,405 | State Street Institutional U.S. Government Money Market Fund, Premier Class, 0.03%(b) | $ | 312,405 | | |

| | Total Short-Term Investment—0.2% (cost $312,405) | | 312,405 | | |

| | Total Investments—103.5% (cost $116,070,491)(c) | | 159,380,371 | | |

| | Liabilities in Excess of Other Assets—(3.5)% | | (5,380,425 | ) | |

| | Net Assets—100.0% | $ | 153,999,946 | | |

| (a) | Non-income producing security. |

| (b) | Registered investment company advised by State Street Global Advisors. The rate shown is the 7 day yield as of October 31, 2021. |

| (c) | See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities. |

GDR Global Depository Receipt

PLC Public Limited Company

REIT Real Estate Investment Trust

See Notes to Financial Statements.

| 10 | Aberdeen Australia Equity Fund, Inc. | |

|

Statement of Assets and Liabilities

| Assets |

| | | | | |

| Investments, at value (cost $115,758,086) | | $ | 159,067,966 | |

| Short-term investments, at value (cost $312,405) | | | 312,405 | |

| Foreign currency, at value (cost $1,032,207) | | | 1,038,181 | |

| Receivable for investments sold | | | 3,692,704 | |

| Interest and dividends receivable | | | 7 | |

| Prepaid expenses and other assets | | | 154,482 | |

| Total assets | | | 164,265,745 | |

| | | | | |

| Liabilities | | | | |

| Revolving credit facility payable (Note 7) | | | 7,510,998 | |

| Payable for investments purchased | | | 2,480,902 | |

| Investment management fees payable (Note 3) | | | 141,363 | |

| Investor relations fees payable (Note 3) | | | 18,246 | |

| Administration fees payable (Note 3) | | | 12,680 | |

| Interest payable on bank loan | | | 1,529 | |

| Other accrued expenses | | | 100,081 | |

| Total liabilities | | | 10,265,799 | |

| | | | | |

| Net Assets | | $ | 153,999,946 | |

| | | | | |

| Composition of Net Assets | | | | |

| Common stock (par value $0.01 per share) (Note 5) | | $ | 239,166 | |

| Paid-in capital in excess of par | | | 111,167,263 | |

| Distributable earnings | | | 42,593,517 | |

| Net Assets | | $ | 153,999,946 | |

| Net asset value per share based on 23,916,588 shares issued and outstanding | | $ | 6.44 | |

See Notes to Financial Statements.

| Aberdeen Australia Equity Fund, Inc. | 11 |

Statement of Operations

For the Year Ended October 31, 2021

| Net Investment Income: |

| | |

| Income | |

| Dividends (net of foreign withholding taxes of $61,828) | | $ | 4,761,560 | |

| Interest and other income | | | 57 | |

| Total Investment Income | | | 4,761,617 | |

| | | | | |

| Expenses: | | | | |

| Investment management fee (Note 3) | | | 1,359,117 | |

| Directors' fees and expenses | | | 242,348 | |

| Administration fee (Note 3) | | | 121,042 | |

| Revolving credit facility fees and expenses (Note 7) | | | 86,895 | |

| Investor relations fees and expenses (Note 3) | | | 68,150 | |

| Independent auditors' fees and expenses | | | 65,613 | |

| Transfer agent's fees and expenses | | | 54,580 | |

| Reports to shareholders and proxy solicitation | | | 48,169 | |

| Custodian's fees and expenses | | | 35,675 | |

| Insurance expense | | | 23,436 | |

| Legal fees and expenses | | | 12,968 | |

| Miscellaneous | | | 30,185 | |

| Total operating expenses, excluding interest expense | | | 2,148,178 | |

| Interest expense (Note 7) | | | 77,309 | |

| Net operating expenses | | | 2,225,487 | |

| | | | | |

| Net Investment Income | | | 2,536,130 | |

| | | | | |

| Net Realized/Unrealized Gain/(Loss) from Investments and Foreign Currency Related Transactions: | | | | |

| Net realized gain/(loss) from: | | | | |

| Investment transactions | | | 10,612,788 | |

| Foreign currency transactions | | | 124,631 | |

| | | | 10,737,419 | |

| Net change in unrealized appreciation/(depreciation) on: | | | | |

| Investment transactions | | | 23,902,405 | |

| Foreign currency translation | | | 6,788,206 | |

| | | | 30,690,611 | |

| Net realized and unrealized gain from investments and foreign currency related transactions | | | 41,428,030 | |

| Net Increase in Net Assets Resulting from Operations | | $ | 43,964,160 | |

See Notes to Financial Statements.

| 12 | Aberdeen Australia Equity Fund, Inc. |

Statements of Changes in Net Assets

| | | For the

Year Ended

October 31, 2021 | | | For the

Year Ended

October 31, 2020 | |

| Increase/(Decrease) in Net Assets: | | | | | | | | |

| | | | | | | | | |

| Operations: | | | | | | | | |

| Net investment income | | | $ 2,536,130 | | | | $ 1,726,003 | |

| Net realized gain/(loss) from investment transactions | | | 10,612,788 | | | | (2,240,810 | ) |

| Net realized gain/(loss) from foreign currency transactions | | | 124,631 | | | | (167,381 | ) |

| Net change in unrealized appreciation/(depreciation) on investments | | | 23,902,405 | | | | (8,064,913 | ) |

| Net change in unrealized appreciation on foreign currency translation | | | 6,788,206 | | | | 7,011,672 | |

| Net increase/(decrease) in net assets resulting from operations | | | 43,964,160 | | | | (1,735,429 | ) |

| | | | | | | | | |

| Distributions to Shareholders From: | | | | | | | | |

| Distributable earnings | | | (13,816,862 | ) | | | (4,186,262 | ) |

| Tax return of capital | | | – | | | | (7,662,382 | ) |

| Net decrease in net assets from distributions | | | (13,816,862 | ) | | | (11,848,644 | ) |

| Issuance of 790,087 and 384,175 shares of common stock, respectively due to stock distribution | | | 4,562,491 | | | | 1,717,261 | |

| Change in net assets from common stock transactions | | | 4,562,491 | | | | 1,717,261 | |

| Change in net assets | | | 34,709,789 | | | | (11,866,812 | ) |

| | | | | | | | | |

| Net Assets: | | | | | | | | |

| Beginning of year | | | 119,290,157 | | | | 131,156,969 | |

| End of year | | | $ 153,999,946 | | | | $ 119,290,157 | |

Amounts listed as "–" are $0 or round to $0.

See Notes to Financial Statements.

| Aberdeen Australia Equity Fund, Inc. | 13 |

Financial Highlights

| | | For the Fiscal Years Ended October 31, | |

| | | 2021 | | 2020 | | 2019 | | 2018 | | 2017 | |

| PER SHARE OPERATING PERFORMANCE(a): |

| Net asset value, beginning of year | | $5.16 | | $5.77 | | $5.51 | | $6.39 | | $6.09 | |

| Net investment income | | 0.11 | | 0.08 | | 0.17 | | 0.16 | | 0.17 | |

Net realized and unrealized gains/(losses) on investments and

foreign currencies | | 1.77 | | (0.16 | ) | 0.67 | | (0.40 | ) | 0.77 | |

| Total from investment operations | | 1.88 | | (0.08 | ) | 0.84 | | (0.24 | ) | 0.94 | |

| Distributions from: | | | | | | | | | | | |

| Net investment income | | (0.17 | ) | (0.04 | ) | (0.15 | ) | (0.14 | ) | (0.13 | ) |

| Net realized gains | | (0.42 | ) | (0.14 | ) | (0.13 | ) | (0.43 | ) | (0.16 | ) |

| Tax return of capital | | – | | (0.34 | ) | (0.30 | ) | (0.07 | ) | (0.35 | ) |

| Total distributions | | (0.59 | ) | (0.52 | ) | (0.58 | ) | (0.64 | ) | (0.64 | ) |

| Capital Share Transactions: | | | | | | | | | | | |

| Impact of Stock Distribution | | (0.01 | ) | (0.01 | ) | – | | – | | – | |

| Net asset value, end of year | | $6.44 | | $5.16 | | $5.77 | | $5.51 | | $6.39 | |

| Market value, end of year | | $6.08 | | $4.47 | | $5.16 | | $5.17 | | $6.25 | |

| | | | | | | | | | | | |

| Total Investment Return Based on(b): | | | | | | | | | | | |

| Market value | | 50.49% | | (2.98% | ) | 11.15% | | (8.37% | ) | 24.92% | |

| Net asset value | | 38.09% | | 0.16% | | 16.62% | | (4.48% | ) | 16.61% | |

| | | | | | | | | | | | |

| Ratio to Average Net Assets/Supplementary Data: | | | | | | | | | | | |

| Net assets, end of year (000 omitted) | | $154,000 | | $119,290 | | $131,157 | | $125,219 | | $145,264 | |

| Average net assets (000 omitted) | | $143,765 | | $120,590 | | $129,377 | | $143,263 | | $144,958 | |

| Net operating expenses, net of fee waivers | | 1.55% | | 1.53% | | 1.48% | | 1.46% | | 1.48% | |

| Net operating expenses, excluding fee waivers | | 1.55% | | 1.53% | | 1.48% | | 1.46% | | 1.48% | |

| Net operating expenses, excluding interest expense | | 1.49% | | – | | – | | – | | – | |

| Net investment income | | 1.76% | | 1.43% | | 3.03% | | 2.47% | | 2.68% | |

| Portfolio turnover | | 23% | | 32% | | 20% | | 36% | | 12% | |

| Senior securities (loan facility) outstanding (000 omitted) | | $7,511 | | $7,023 | | $– | | $– | | $– | |

| Asset coverage ratio on revolving credit facility at year end(c) | | 2,150% | | 1,799% | | – | | – | | – | |

| Asset coverage per $1,000 on revolving credit facility at year end | | $21,503 | | $17,987 | | $– | | $– | | $– | |

| (a) | Based on average shares outstanding. |

| (b) | Total investment return based on market value is calculated assuming that shares of the Fund's common stock were purchased at the closing market price as of the beginning of the period, dividends, capital gains and other distributions were reinvested as provided for in the Fund's dividend reinvestment plan and then sold at the closing market price per share on the last day of the period. The computation does not reflect any sales commission investors may incur in purchasing or selling shares of the Fund. The total investment return based on the net asset value is similarly computed except that the Fund's net asset value is substituted for the closing market value. |

| (c) | Asset coverage ratio is calculated by dividing net assets plus the amount of any borrowings, for investment purposes by the amount of the Revolving Credit Facility. |

Amounts listed as "–" are $0 or round to $0.

See Notes to Financial Statements.

| 14 | Aberdeen Australia Equity Fund, Inc. |

Notes to Financial Statements

October 31, 2021

1. Organization

Aberdeen Australia Equity Fund, Inc. (the "Fund") is a non-diversified closed-end management investment company incorporated in Maryland on September 30, 1985. The Fund's principal investment objective is long-term capital appreciation through investment primarily in equity securities of Australian companies listed on the Australian Stock Exchange Limited ("ASX"). Its secondary objective is current income, which is expected to be derived primarily from dividends and interest on Australian corporate and governmental securities. The Fund normally invests at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in equity securities, consisting of common stock, preferred stock and convertible stock, of companies tied economically to Australia (each an "Australian Company"). This 80% investment policy is a non-fundamental policy of the Fund and may be changed by the Board of Directors of the Fund ("the Board") upon 60 days' prior written notice to shareholders. As a fundamental policy, at least 65% of the Fund's total assets must be invested in companies listed on the ASX. abrdn Asia Limited (formerly known as "Aberdeen Standard Investments (Asia) Limited") ("abrdn Asia"), the Fund's investment manager (the "Investment Manager"), uses the following criteria in determining if a company is "tied economically" to Australia: whether the company (i) is a constituent of the ASX; (ii) has its headquarters located in Australia, (iii) pays dividends on its stock in Australian Dollars; (iv) has its accounts audited by Australian auditors; (v) is subject to Australian taxes levied by the Australian Taxation Office; (vi) holds its annual general meeting in Australia; (vii) has common stock/ordinary shares and/or other principal class of securities registered with Australian regulatory authorities for sale in Australia; (viii) is incorporated in Australia; or (ix) has a majority of its assets located in Australia or a majority of its revenues are derived from Australian sources. There can be no assurance that the Fund will achieve its investment objective.

2. Summary of Significant Accounting Policies

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board ("FASB") Accounting Standard Codification Topic 946 Financial Services-Investment Companies.

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. The policies conform to generally accepted accounting principles ("GAAP") in the United States of America. The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of income and expenses for the period. Actual results

could differ from those estimates. The accounting records of the Fund are maintained in U.S. Dollars and the U.S. Dollar is used as both the functional and reporting currency. However, the Australian Dollar is the functional currency for U.S. federal tax purposes.

a. Security Valuation:

The Fund values its securities at current market value or fair value, consistent with regulatory requirements. "Fair value" is defined in the Fund's Valuation and Liquidity Procedures as the price that could be received to sell an asset or paid to transfer a liability in an orderly transaction between willing market participants without a compulsion to transact at the measurement date.

Equity securities that are traded on an exchange are valued at the last quoted sale price on the principal exchange on which the security is traded at the "Valuation Time" subject to application, when appropriate, of the valuation factors described in the paragraph below. Under normal circumstances, the Valuation Time is as of the close of regular trading on the New York Stock Exchange ("NYSE") (usually 4:00 p.m. Eastern Time). In the absence of a sale price, the security is valued at the mean of the bid/ask price quoted at the close on the principal exchange on which the security is traded. Securities traded on NASDAQ are valued at the NASDAQ official closing price. Closed-end funds and exchange-traded funds ("ETFs") are valued at the market price of the security at the Valuation Time. A security using any of these pricing methodologies is determined to be a Level 1 investment.

Foreign equity securities that are traded on foreign exchanges that close prior to Valuation Time are valued by applying valuation factors to the last sale price or the mean price as noted above. Valuation factors are provided by an independent pricing service provider approved by the Board. These valuation factors are used when pricing the Fund's portfolio holdings to estimate market movements between the time foreign markets close and the time the Fund values such foreign securities. These valuation factors are based on inputs such as depositary receipts, indices, futures, sector indices/ETFs, exchange rates, and local exchange opening and closing prices of each security. When prices with the application of valuation factors are utilized, the value assigned to the foreign securities may not be the same as quoted or published prices of the securities on their primary markets. A security that applies a valuation factor is determined to be a Level 2 investment because the exchange-traded price has been adjusted. Valuation factors are not utilized if the independent pricing service provider is unable to provide a valuation factor or if the valuation factor falls below a predetermined threshold; in such case, the security is determined to be a Level 1 investment.

Short-term investments are comprised of cash and cash equivalents invested in short-term investment funds which are redeemable daily.

| Aberdeen Australia Equity Fund, Inc. | 15 |

Notes to Financial Statements (continued)

October 31, 2021

The Fund sweeps available cash into the State Street Institutional U.S. Government Money Market Fund, which has elected to qualify as a "government money market fund" pursuant to Rule 2a-7 under the 1940 Act, and has an objective, which is not guaranteed, to maintain a $1.00 per share NAV. Generally, these investment types are categorized as Level 1 investments.

In the event that a security's market quotations are not readily available or are deemed unreliable (for reasons other than because the foreign exchange on which it trades closes before the Valuation Time), the security is valued at fair value as determined by the Fund's Pricing Committee, taking into account the relevant factors and surrounding circumstances using valuation policies and procedures approved by the Board. A security that has been fair valued by the Fund's Pricing Committee may be classified as Level 2 or Level 3 depending on the nature of the inputs.

In accordance with the authoritative guidance on fair value measurements and disclosures under GAAP, the Fund discloses the fair value of its investments using a three-level hierarchy that classifies the inputs to valuation techniques used to measure the fair value. The hierarchy assigns Level 1, the highest level, measurements to valuations based upon unadjusted quoted prices in active markets for identical assets, Level 2 measurements to valuations based upon other significant observable inputs, including adjusted quoted prices in active markets for similar assets, and Level 3, the lowest level, measurements

to valuations based upon unobservable inputs that are significant to the valuation. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique used to measure fair value including a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability, which are based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity's own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. A financial instrument's level within the fair value hierarchy is based upon the lowest level of any input that is significant to the fair value measurement.

The three-level hierarchy of inputs is summarized below:

Level 1 – quoted prices in active markets for identical investments;

Level 2 – other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, and credit risk); or

Level 3 – significant unobservable inputs (including the Fund's own assumptions in determining the fair value of investments).

A summary of standard inputs is listed below:

| Security Type | | Standard Inputs |

Foreign equities utilizing

a fair value factor | | Depositary receipts, indices, futures, sector indices/ETFs, exchange rates, and local exchange opening and closing prices of each security. |

The following is a summary of the inputs used as of October 31, 2021 in valuing the Fund's investments at fair value. The inputs or methodologies used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. Please refer to the Portfolio of Investments for a detailed breakout of the security types:

| Investments, at Value | | Level 1 – Quoted

Prices ($) | | Level 2 – Other Significant

Observable Inputs ($) | | Level 3 – Significant

Unobservable Inputs ($) | | Total ($) | |

| Investments in Securities | |

| Common Stocks | | $1,499,523 | | $157,568,443 | | $– | | $159,067,966 | |

| Short-Term Investment | | 312,405 | | – | | – | | 312,405 | |

| Total | | $1,811,928 | | $157,568,443 | | $– | | $159,380,371 | |

Amounts listed as "–" are $0 or round to $0.

For the fiscal year ended October 31, 2021, there were no significant changes to the fair valuation methodologies for the type of holdings in the Fund's portfolio.

| 16 | Aberdeen Australia Equity Fund, Inc. |

Notes to Financial Statements (continued)

October 31, 2021

b. Foreign Currency Translation:

Foreign securities, currencies, and other assets and liabilities denominated in foreign currencies are translated into U.S. Dollars at the exchange rate of said currencies against the U.S. Dollar, as of the Valuation Time, as provided by an independent pricing service approved by the Board.

The Valuation Time is as of the close of regular trading on the New York Stock Exchange (usually 4:00 p.m. Eastern Time).

Foreign currency amounts are translated into U.S. Dollars on the following basis:

| (i) | market value of investment securities, other assets and liabilities – at the current daily rates of exchange at the Valuation Time; and |

| (ii) | purchases and sales of investment securities, income and expenses – at the relevant rate of exchange prevailing on the respective dates of such transactions. |

The Fund isolates that portion of the results of operations arising from changes in the foreign exchange rates due to the fluctuations in the market prices of the securities held at the end of the reporting period. Similarly, the Fund isolates the effect of changes in foreign exchange rates from the fluctuations arising from changes in the market prices of portfolio securities sold during the reporting period.

Net exchange gain/(loss) is realized from sales and maturities of portfolio securities, sales of foreign currencies, settlement of securities transactions, dividends, interest and foreign withholding taxes recorded on the Fund's books. Net unrealized foreign exchange appreciation/(depreciation) includes changes in the value of portfolio securities and other assets and liabilities arising as a result of changes in the exchange rate.

Foreign security and currency transactions may involve certain considerations and risks not typically associated with those of domestic origin, including unanticipated movements in the value of the foreign currency relative to the U.S. Dollar. Generally, when the U.S. Dollar rises in value against foreign currency, the Fund's investments denominated in that foreign currency will lose value because the foreign currency is worth fewer U.S. Dollars; the opposite effect occurs if the U.S. Dollar falls in relative value.

c. Security Transactions, Investment Income and Expenses:

Security transactions are recorded on the trade date. Realized and unrealized gains/(losses) from security and currency transactions are calculated on the identified cost basis. Dividend income and corporate actions are recorded generally on the ex-date, except for certain dividends and corporate actions which may be recorded after the ex-date, as soon as the Fund acquires information regarding such dividends

or corporate actions. Interest income and expenses are recorded on an accrual basis.

d. Distributions:

The Fund has a managed distribution policy to pay distributions from net investment income supplemented by net realized foreign exchange gains, net realized capital gains and return of capital distributions, if necessary, on a quarterly basis. The managed distribution policy is subject to regular review by the Board. The Fund will also declare and pay distributions at least annually from net realized gains on investment transactions and net realized foreign exchange gains, if any. Dividends and distributions to shareholders are recorded on the ex-dividend date.

Dividends and distributions to shareholders are determined in accordance with federal income tax regulations, which may differ from GAAP. These differences are primarily due to differing treatments for foreign currencies, loss deferrals and recognition of market discount and premium.

e. Federal Income Taxes:

The Fund, for U.S. federal income purposes is comprised of a separately identifiable unit called a Qualified Business Unit ("QBUs") (see section 987 of the Internal Revenue Code of 1986, as amended (the "IRC")). The Fund has operated with a QBU for U.S. federal income purposes since 1989. The home office is designated as the United States and the QBU is Australia with a functional currency of the Australian dollar. The securities held within the Fund reside within either the home office of the QBU or the home office depending on certain factors including geographic region of the security. As an example, the majority of the Fund's Australian securities reside within the Australian QBU. When sold, the Australian dollar denominated securities within the Australian QBU generate capital gain/loss but not currency gain/loss, because the QBU's functional currency is Australian dollar.

IRC section 987 states that currency gain/loss is generated when money is repatriated from a QBU to the home office. The currency gain/loss would result from the difference between the current exchange rate and the average exchange rate for the year during which money was originally contributed to the QBU from the home office. Based on the QBU structure, there may be sizable differences in the currency gain/loss recognized for U.S. federal income tax purposes and what is reported within the financial statements under GAAP. Additionally, the Fund's composition of the distributions to shareholders is calculated based on U.S. federal income tax requirements whereby currency gain/loss is characterized as income and distributed as such. As of the Fund's fiscal year-end, the calculation of the composition of distributions to shareholders is finalized and reported in the Fund's annual report to shareholders.

| | Aberdeen Australia Equity Fund, Inc. | 17 |

Notes to Financial Statements (continued)

October 31, 2021

The Fund intends to continue to qualify as a "regulated investment company" ("RIC") by complying with the provisions available to certain investment companies, as defined in Subchapter M of the Internal Revenue Code of 1986, as amended, and to make distributions of net investment income and net realized capital gains sufficient to relieve the Fund from all federal income taxes. Therefore, no federal income tax provision is required.

The Fund recognizes the tax benefits of uncertain tax positions only where the position is "more likely than not" to be sustained assuming examination by tax authorities. Management of the Fund has concluded that there are no significant uncertain tax positions that would require recognition in the financial statements. Since tax authorities can examine previously filed tax returns, the Fund's U.S. federal and state tax returns for each of the most recent four fiscal years up to the most recent fiscal year ended October 31, 2020 are subject to such review.

f. Foreign Withholding Tax:

Dividend and interest income from non-U.S. sources received by the Fund are generally subject to non-U.S. withholding taxes. In addition, the Fund may be subject to capital gains tax in certain countries in which it invests. The above taxes may be reduced or eliminated under the terms of applicable U.S. income tax treaties with some of these countries. The Fund accrues such taxes when the related income is earned.

In addition, when the Fund sells securities within certain countries in which it invests, the capital gains realized may be subject to tax. Based on these market requirements and as required under GAAP, the Fund accrues deferred capital gains tax on securities currently held that have unrealized appreciation within these countries. The amount of deferred capital gains tax accrued, if any, is reported on the Statement of Assets and Liabilities.

3. Agreements and Transactions with Affiliates

a. Investment Manager and Investment Adviser:

abrdn Asia serves as investment manager to the Fund and abrdn Australia Limited (formerly known as "Aberdeen Standard Investments Australia Limited") serves as investment adviser to the Fund, pursuant to a management agreement and an advisory agreement, respectively. The Investment Manager and the Investment Adviser are indirect wholly-owned subsidiaries of abrdn plc (formerly known as "Standard Life Aberdeen plc") (collectively the "Advisers").

The Investment Manager makes investment decisions on behalf of the Fund on the basis of recommendations and information furnished to it by the Investment Adviser, including the selection of, and responsibility

for the placement of orders with, brokers and dealers to execute portfolio transactions on behalf of the Fund.

In rendering management services, the Investment Manager may use the resources of advisory subsidiaries of abrdn plc. These affiliates have entered into a memorandum of understanding/ personnel sharing procedures pursuant to which investment professionals from each affiliate, including the Investment Adviser, may render portfolio management and research services to U.S. clients of the Standard Life Aberdeen plc affiliates, including the Fund, as associated persons of the Investment Manager. No remuneration is paid by the Fund with regards to the memorandum of understanding/personnel sharing procedures.

Pursuant to the management agreement, the Fund pays the Investment Manager a fee, payable monthly by the Fund, at the following annual rates: 1.10% of the Fund's average weekly Managed Assets up to $50 million, 0.90% of the Fund's average weekly Managed Assets between $50 million and $100 million and 0.70% of the Fund's average weekly Managed Assets in excess of $100 million. Managed Assets is defined in the management agreement as net assets plus the amount of any borrowings for investment purposes. The Investment Adviser is paid by the Investment Manager, and not the Fund, for its services.

For the fiscal year ended October 31, 2021, abrdn Asia earned $1,359,117 from the Fund for investment management fees.

b. Fund Administration:

Aberdeen Standard Investments, Inc. ("ASII") (to be known as abrdn Inc. effective January 1, 2022), an affiliate of the Advisers, is the Fund's Administrator, pursuant to an agreement under which ASII receives a fee, payable monthly by the Fund, at an annual fee rate of 0.08% of the Fund's average weekly Managed Assets up to $500 million, 0.07% of the Fund's average weekly Managed Assets between $500 million and $1.5 billion, and 0.06% of the Fund's average weekly Managed Assets in excess of $1.5 billion. For the fiscal year ended October 31, 2021, ASII earned $121,042 from the Fund for administration services.

c. Investor Relations:

Under the terms of the Investor Relations Services Agreement, ASII provides and pays third parties to provide investor relations services to the Fund and certain other funds advised by abrdn Asia or its affiliates as part of an Investor Relations Program. Under the Investor Relations Services Agreement, the Fund owes a portion of the fees related to the Investor Relations Program (the "Fund's Portion"). However, investor relations services fees are limited by ASII so that the Fund will only pay up to an annual rate of 0.05% of the Fund's average weekly net assets. Any difference between the capped rate of 0.05%

| 18 | Aberdeen Australia Equity Fund, Inc. | |

Notes to Financial Statements (continued)

October 31, 2021

of the Fund's average weekly net assets and the Fund's Portion is paid for by ASII.

Pursuant to the terms of the Investor Relations Services Agreement, ASII (or third parties engaged by ASII), among other things, provides objective and timely information to shareholders based on publicly-available information; provides information efficiently through the use of technology while offering shareholders immediate access to knowledgeable investor relations representatives; develops and maintains effective communications with investment professionals from a wide variety of firms; creates and maintains investor relations communication materials such as fund manager interviews, films and webcasts, publishes white papers, magazine articles and other relevant materials discussing the Fund's investment results, portfolio positioning and outlook; develops and maintains effective communications with large institutional shareholders; responds to specific shareholder questions; and reports activities and results to the Board and management detailing insight into general shareholder sentiment.

During the fiscal year ended October 31, 2021, the Fund incurred investor relations fees of approximately $68,150. For the fiscal year ended October 31, 2021, ASII did not waive any investor relations fees because the Fund's fees did not reach the capped amount.

4. Investment Transactions

Purchases and sales of investment securities (excluding short-term securities) for the fiscal year ended October 31, 2021, were $34,100,459 and $40,069,213, respectively.

5. Capital

The authorized capital of the Fund is 30 million shares of $0.01 par value per share of common stock. As of October 31, 2021, there were 23,916,588 shares of common stock issued and outstanding.

The following table shows the shares issued by the Fund as a part of a quarterly distribution to shareholders during the fiscal year ended October 31, 2021.

| | Date | | Shares Issued | |

| | December 31, 2020 | | | 177,590 | |

| | March 31, 2021 | | | 191,040 | |

| | June 30, 2021 | | | 195,701 | |

| | September 30, 2021 | | | 225,756 | |

6. Open Market Repurchase Program

On March 1, 2001, the Board approved a stock repurchase program. The Board amended the program on December 12, 2007. The stock repurchase program allows the Fund to repurchase up to 10% of its outstanding common stock in the open market during any 12-month period. The Fund reports repurchase activity on the Fund's website on

a monthly basis. For the fiscal year ended October 31, 2021, the Fund did not repurchase any shares through this program.

7. Revolving Credit Facility

The Fund may use leverage to the maximum extent permitted by the 1940 Act, which permits leverage to exceed 33 1/3% of the Fund's total assets (including the amount obtained through leverage) in certain market conditions.

On October 13, 2020, the Fund entered into a 3-year term revolving credit facility with a committed facility of AUD$20million with State Street Global Advisors. For the fiscal year ended October 31, 2021, the balance of the loan outstanding was AUD$10million and the average interest rate on the loan facility was 1.02% The average balance for the fiscal year was AUD$10million. The interest expense is accrued on a daily basis and is payable to State Street Global Advisors on a monthly basis. Interest expense related to the line of credit for the fiscal year ended October 31, 2021, was $77,309.

The amounts borrowed from the loan facility may be invested to return higher rates than the rates in the Fund's portfolio. However, the cost of leverage could exceed the income earned by the Fund on the proceeds of such leverage. To the extent that the Fund is unable to invest the proceeds from the use of leverage in assets which pay interest at a rate which exceeds the rate paid on the leverage, the yield on the Fund's common stock will decrease. In addition, in the event of a general market decline in the value of assets in which the Fund invests, the effect of that decline will be magnified in the Fund because of the additional assets purchased with the proceeds of the leverage. Non-recurring expenses in connection with the implementation of the loan facility will reduce the Fund's performance.

The Fund's leveraged capital structure creates special risks not associated with unleveraged funds having similar investment objectives and policies. The funds borrowed pursuant to the loan facility may constitute a substantial lien and burden by reason of their prior claim against the income of the Fund and against the net assets of the Fund in liquidation. The Fund is not permitted to declare dividends or other distributions in the event of default under the loan facility. In the event of a default under the loan facility, the lenders have the right to cause a liquidation of the collateral (i.e., sell portfolio securities and other assets of the Fund) and, if any such default is not cured, the lenders may be able to control the liquidation as well. A liquidation of the Fund's collateral assets in an event of default, or a voluntary paydown of the loan facility in order to avoid an event of default, would typically involve administrative expenses and sometimes penalties. Additionally, such liquidations often involve selling off of portions of the Fund's assets at inopportune times which can result in losses when markets are unfavorable. The loan facility has a term of three years and is not a perpetual form of leverage; there can be no assurance that the loan

| | Aberdeen Australia Equity Fund, Inc. | 19 |

Notes to Financial Statements (continued)

October 31, 2021

facility will be available for renewal on acceptable terms, if at all. Bank loan fees and expenses included in the Statement of Operations include fees for the loan facility as well as commitment fees for any portion of the loan facility not drawn upon at any time during the period. During the fiscal year ended October 31, 2021, the Fund incurred fees of approximately USD$86,895.

The credit agreement governing the loan facility includes usual and customary covenants for this type of transaction. These covenants impose on the Fund asset coverage requirements, Fund composition requirements and limits on certain investments, such as illiquid investments, which are more stringent than those imposed on the Fund by the 1940 Act. The covenants or guidelines could impede the Investment Manager or Investment Adviser from fully managing the Fund's portfolio in accordance with the Fund's investment objective and policies. The covenants also include a requirement that the Fund maintain net assets of no less than $50,000,000. Furthermore, non-compliance with such covenants or the occurrence of other events could lead to the cancellation of the loan facility.