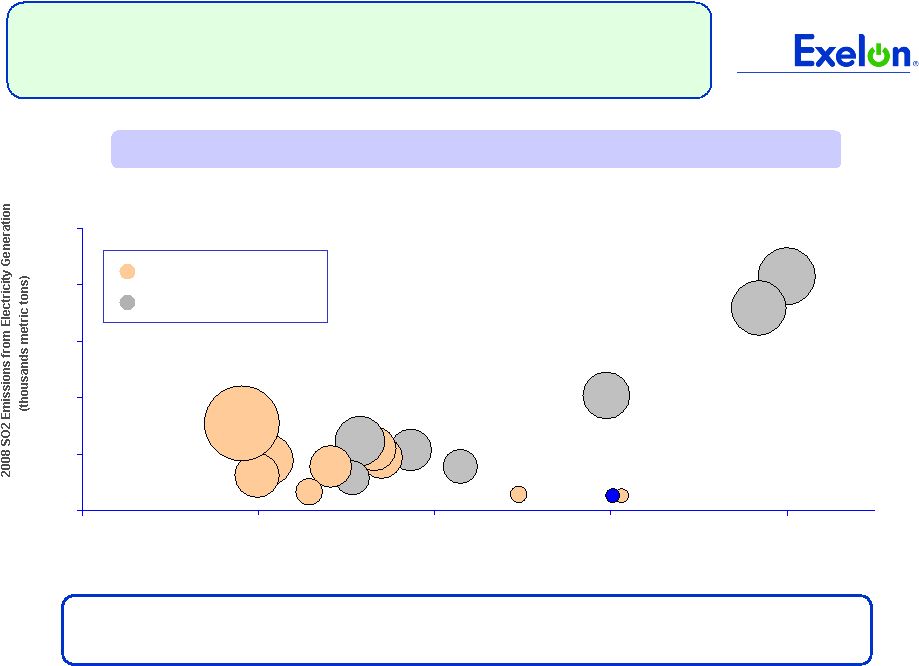

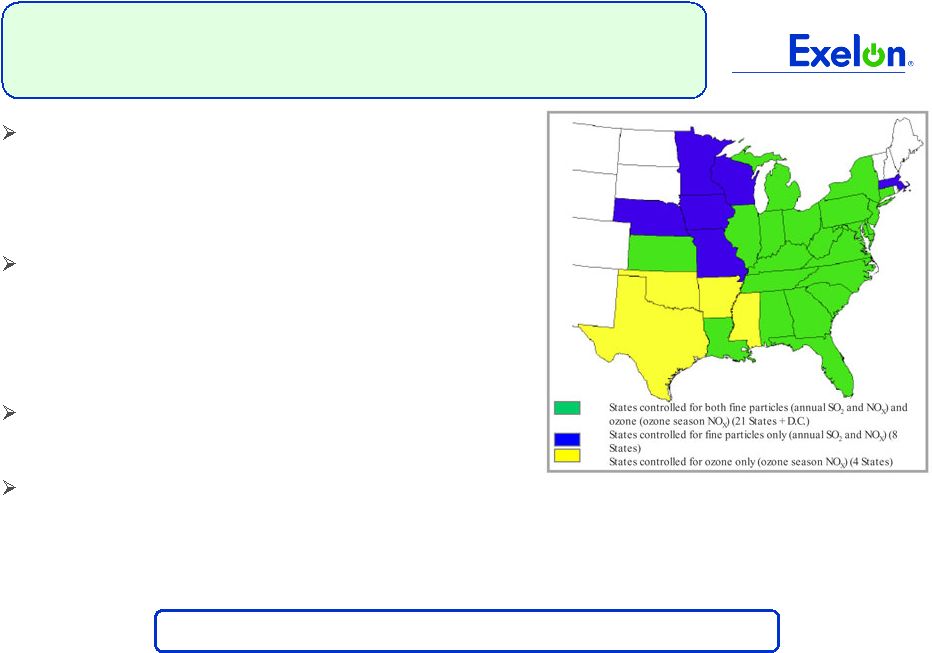

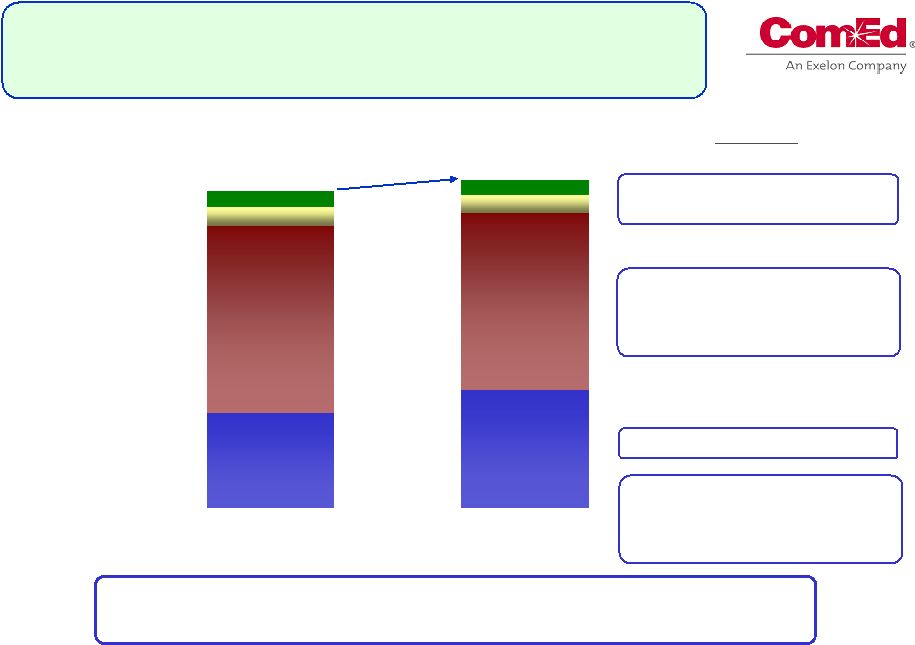

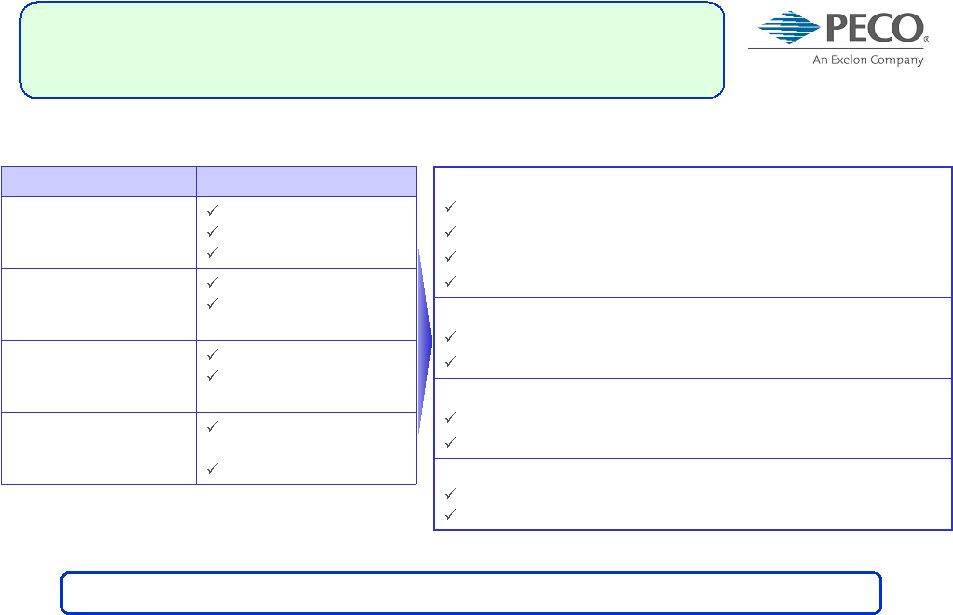

33 Why EPA Regulations Will Not Be Delayed Opposition will have a voice, but the framework and timetable have been set Each NERC region has excess capacity, totaling over 100 GW nationwide Between 2001-2003, industry built over 160 GW of new generation – four times what is projected will retire over next 5 years EPA's modeling indicates that only 14 GW of additional capacity would need to be retrofitted with flue gas desulfurization (FGD) for Phase 2 of the Transport rule (2014) Industry has already demonstrated ability to schedule and sequence outages to comply Well over half of existing units have already installed pollution controls EPA estimates in 2014 that the proposed Transport Rule will have annual net benefits (in 2006$) of $120-290 billion using a 3% discount rate Up to 1 year extension by EPA only if necessary for installation of controls President has only used exemption two times in history (only for national security interests) Supporting Facts Electric system reliability will not be compromised if the industry and its regulators manage the transition Retirements will cause reliability issues on the grid Recent industry trends suggest that it is reasonable to install this quantity of scrubbers according to the proposed timeframe. Timeline is too tight for compliance Proven technologies are commercially available and have already been installed demonstrating that the costs can be managed Total savings to consumer, including healthcare impacts Costs are prohibitive for industry and consumer Federal court would have to determine that the rules are inconsistent with applicable law, which is unlikely to occur because the amended rules are aligned with the court’s expectations Courts will suspend the rules or the President will intervene Reality Opposing Argument |