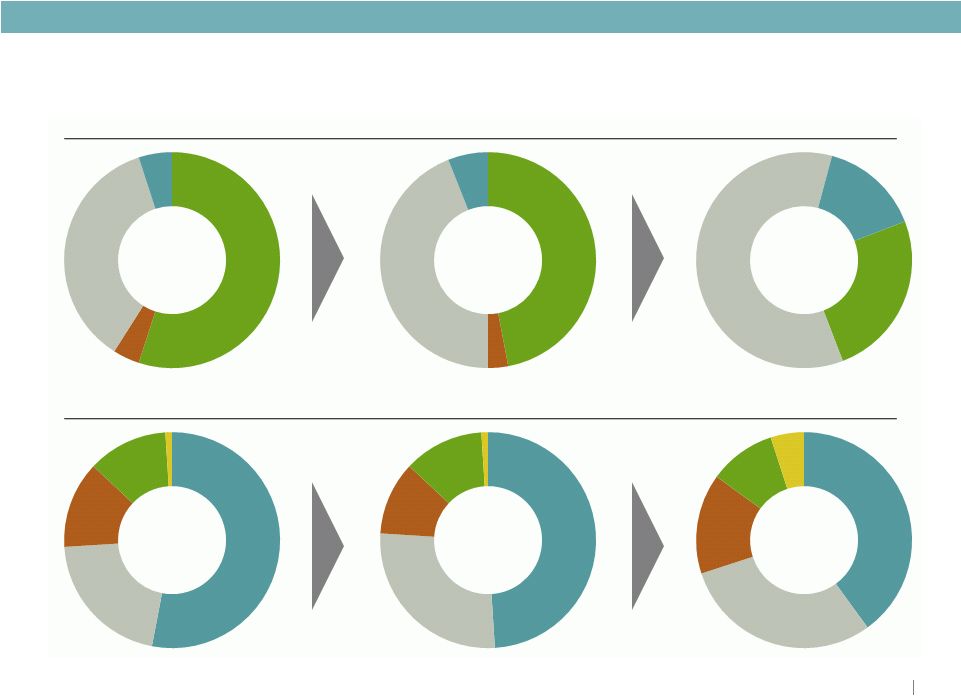

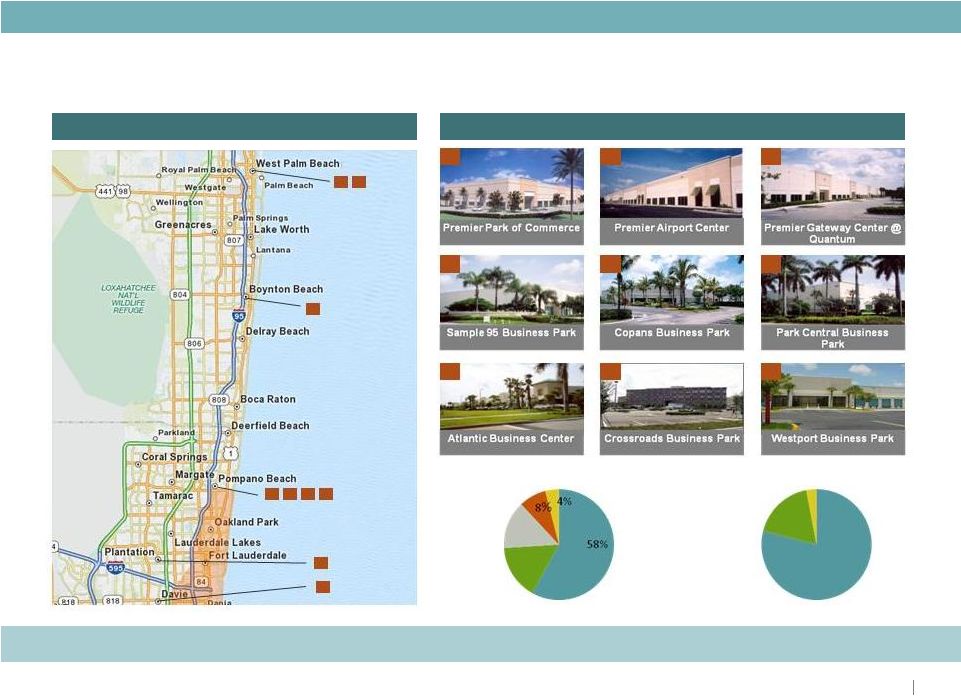

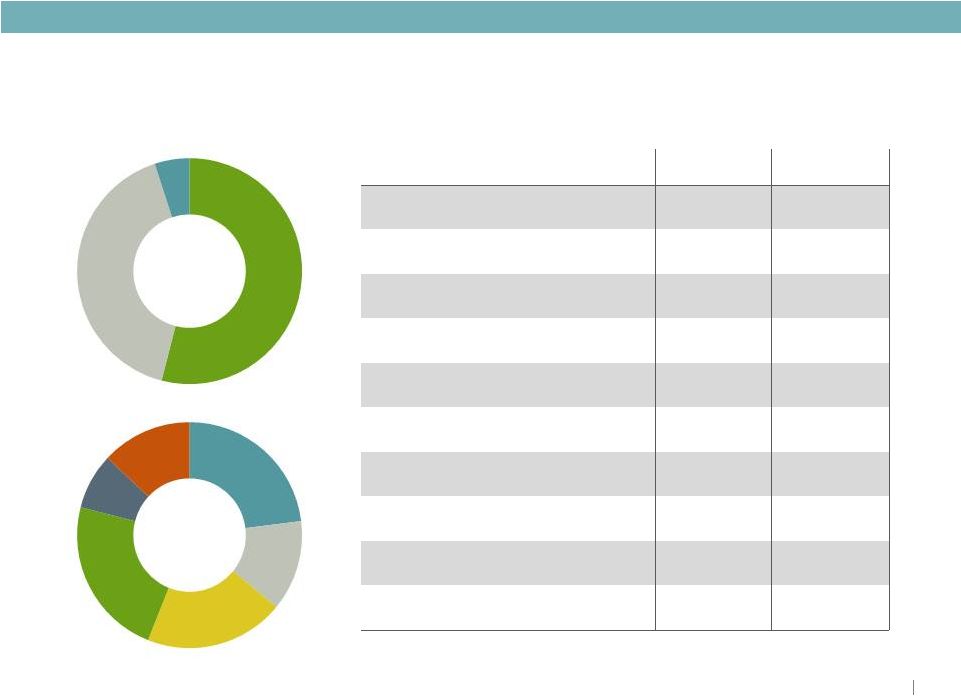

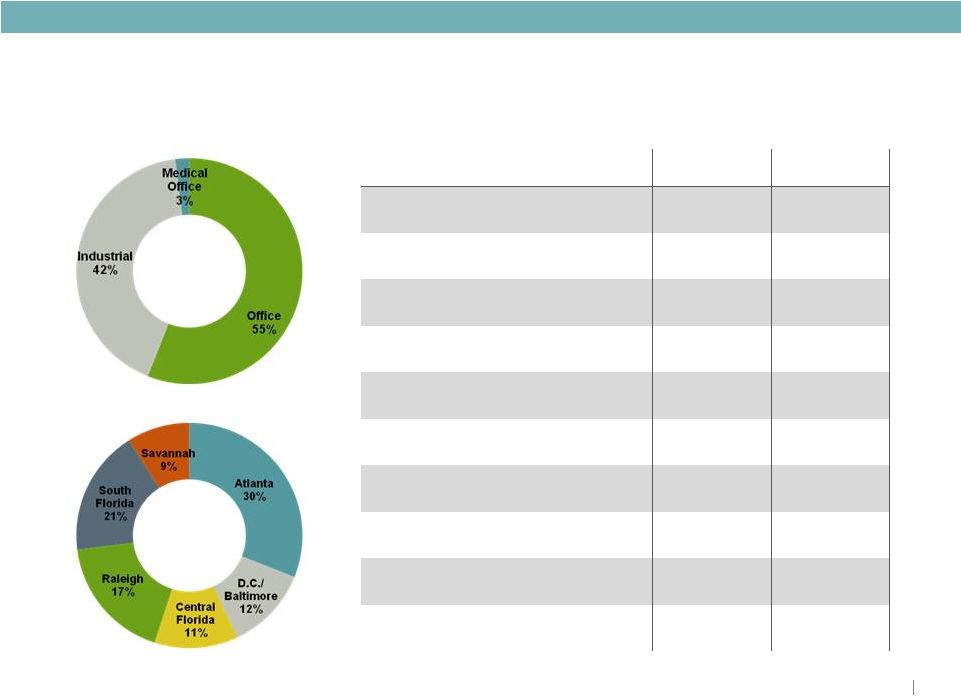

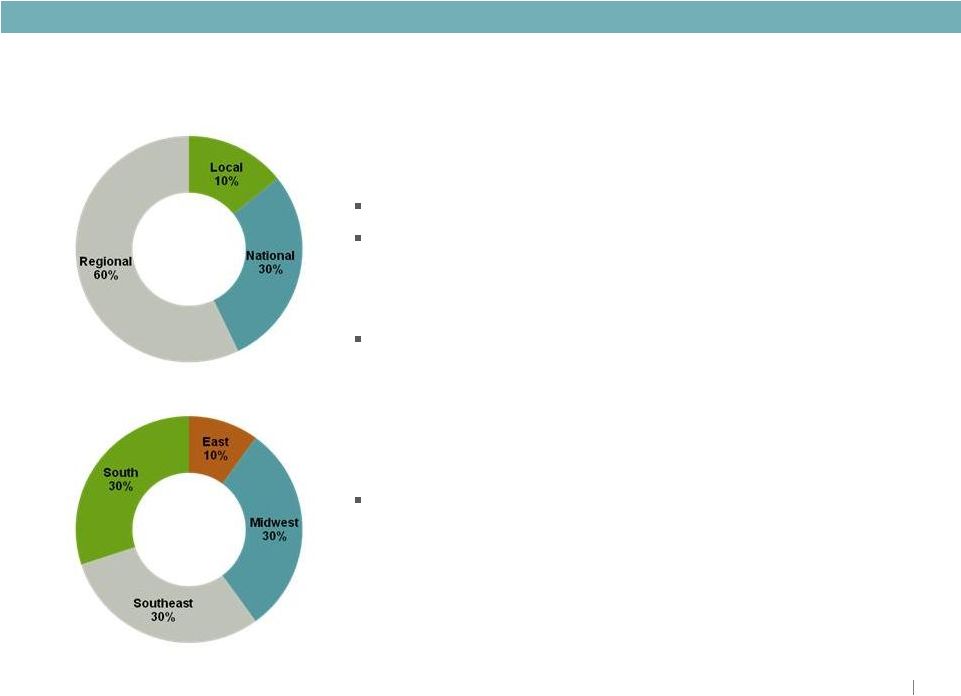

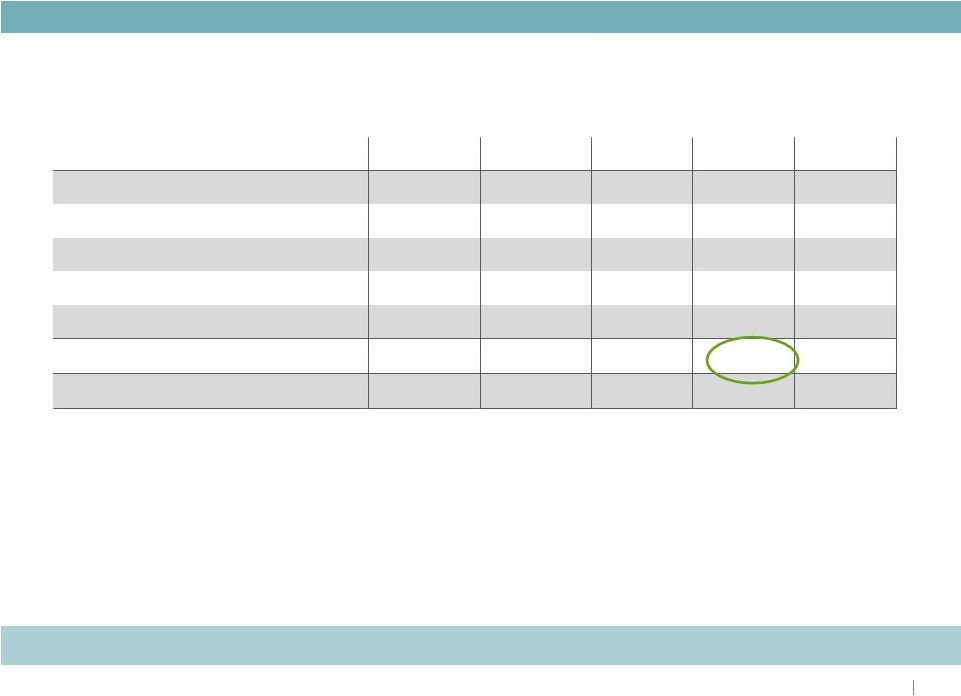

RELIABLE. ANSWERS. © 2011 Duke Realty Corporation Strategic Focus 2011 Goals and Objectives Q1 2011 Update • Lease-up portfolio, manage cap ex; reach positive same property income growth • Balance execution with capital strategy relative to level and quality of cash flow and same property NOI; Debt to EBITDA <7.0x • Development starts of $100 to $200 million focus on medical office and Build-to-Suit • Total portfolio occupancy as of March 31, 2011 of 88.9%; industrial portfolio at 90.2% • More than 5.3 million square feet of leases completed; in-line with Q1 2010 volume of 5.5 million square feet • Debt to EBITDA @ 6.7x;<6.0x by 2013; 0.9% Same Property • One medical office development project started during quarter • Continue strong momentum from 2010 on repositioning of portfolio • Pursue acquisitions of medical and industrial assets • Planned asset dispositions of primarily Midwest office • Closed on remaining $173 million of Premier assets (final closing in April) • Asset dispositions totaled $456 million, including completion of $274 million CBRERT transaction • Opportunistically access capital markets . . . push out maturity schedule further • Continue improving our coverage ratios • Maintain minimal balance on line of credit • Retired $42.5 million of unsecured bonds • Fixed charge ratio of 1.81x • Zero balance outstanding on line of credit, $167 million cash Asset Strategy Operations Strategy Capital Strategy Executing across all three aspects of our strategy 7 |