Exhibit 99.1

2011 Investor and Analyst Conference

November 14, 2011

RELIABLE. ANSWERS.

DukeREALTY

RELIABLE. ANSWERS

Denny Oklak

Chairman & CEO

Christie Kelly

Executive VP & CFO

Jim Bremner

President, Healthcare

Jim Connor

Senior Regional EVP

Sam O’Briant

Regional EVP

Jeff Turner

Regional EVP

© 2011 Duke Realty Corporation | 2

RELIABLE. ANSWERS

Ron Hubbard

VP, Investor Relations

Deeni Taylor

EVP, Healthcare

Jeff Thornton

SVP, South Region

Randy Wood

VP, South Region

© 2011 Duke Realty Corporation | 3

Opening

Market outlook

Strategic performance

Capital Strategy and 2011 guidance

Blackstone transaction overview

Medical office and Baylor overview

Dallas market overview

Closing comments

AGENDA

© 2011 Duke Realty Corporation | 4

RELIABLE. ANSWERS

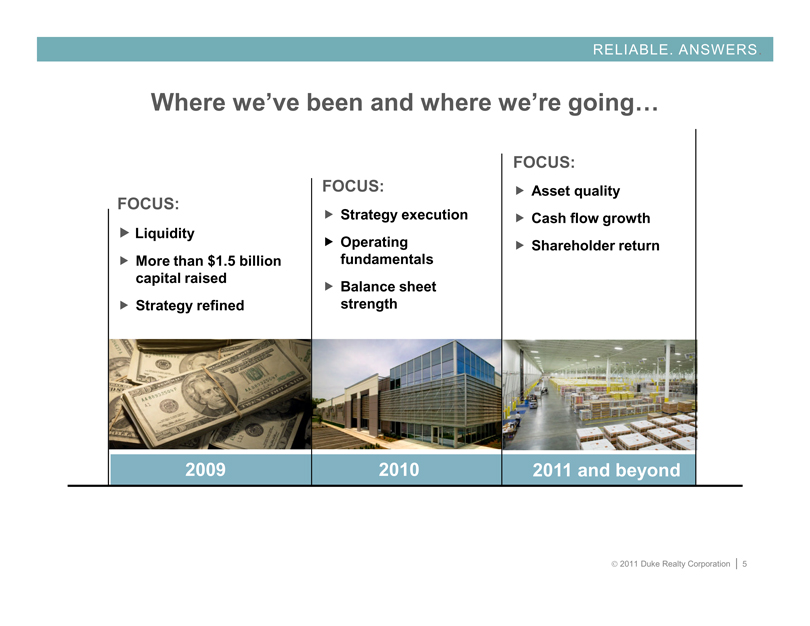

Where we’ve been and where we’re going…

FOCUS:

Liquidity

More than $1.5 billion capital raised

Strategy refined

FOCUS:

Strategy execution

Operating fundamentals

Balance sheet strength

FOCUS: Asset quality

Cash flow growth

Shareholder return

2009

2010

2011 and beyond

© 2011 Duke Realty Corporation | 5

RELIABLE. ANSWERS

Market Outlook

Industrial Market Continues Slow Recovery

Net absorption in U.S. for Q3 2011 was positive for the 6th consecutive quarter

Strong demand for high quality available space remains

Manufacturing sector showing signs of rebounding; industrial capacity utilization up

ISM index has been steady with a slight uptick in September

Manufacturing sector, wholesale trade and transportation realizing a majority of recent job growth

Suburban Office Market Still Challenging

Economic and federal budget uncertainty limiting business investment and expansion decisions

Office sector recovery continuing, but slowly …

Recovery is still chugging along though, with Q3 vacancy declining to 13%, down 20 bps from

previous quarter

Absorption was strongest since 2007 and supply additions were a record low

Medical Office Traction Remains

Operators now making expansion decisions after two year pause

Relationships are a key driver of on campus MOB business

Demographics and economics positive growth drivers

Medical office development and acquisition activity continues

Still challenging, but trends improving in all product types

© 2011 Duke Realty Corporation | 6

Source: PPR

RELIABLE. ANSWERS

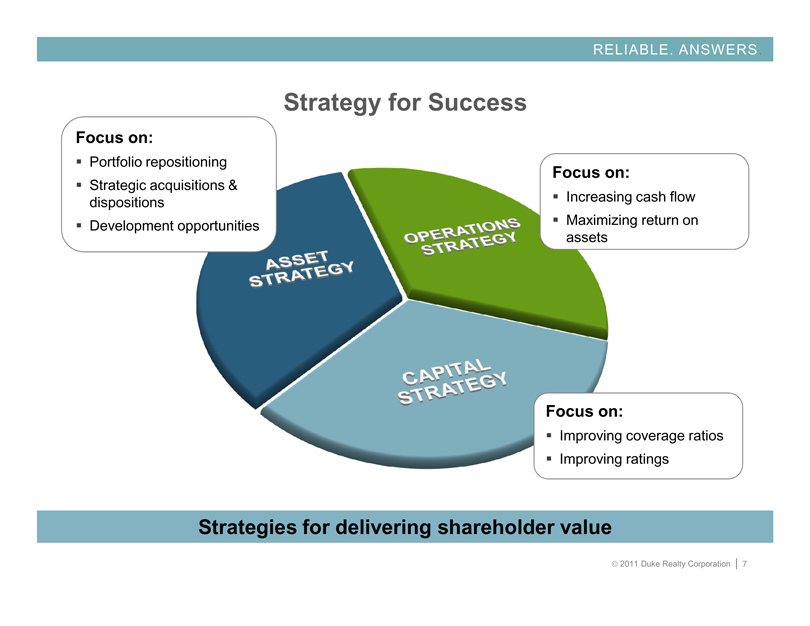

Strategy for Success

Focus on:

Portfolio repositioning

Strategic acquisitions & dispositions

Development opportunities

Focus on:

Increasing cash flow

Maximizing return on assets

Focus on:

Improving coverage ratios

Improving ratings

ASSET STRATEGY

OPERATIONS STRATEGY

CAPITAL STRATEGY

Strategies for delivering shareholder value

© 2011 Duke Realty Corporation | 7

RELIABLE. ANSWERS

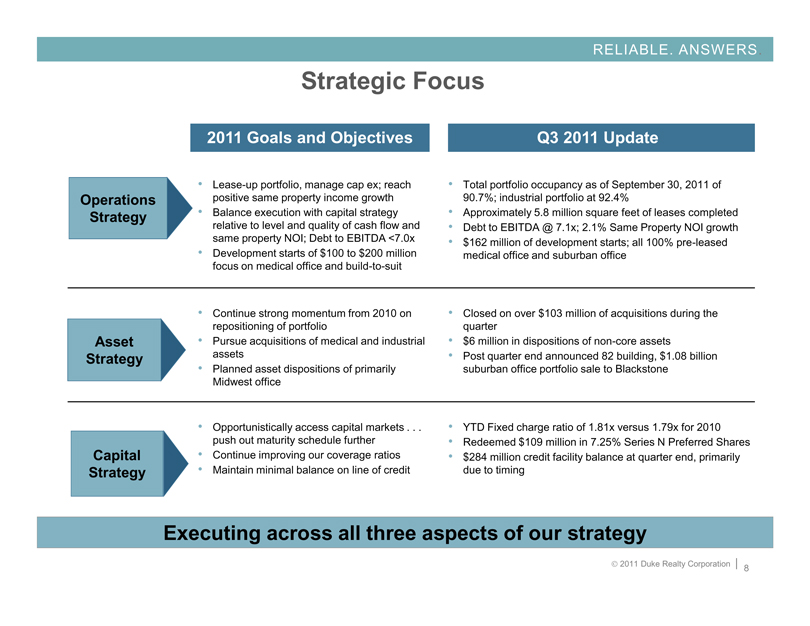

Strategic Focus

2011 Goals and Objectives

Operations Strategy

• Lease-up portfolio, manage cap ex; reach positive same property income growth

• Balance execution with capital strategy relative to level and quality of cash flow and same property NOI; Debt to EBITDA <7.0x

• Development starts of $100 to $200 million focus on medical office and build-to-suit

Q3 2011 Update

Total portfolio occupancy as of September 30, 2011 of 90.7%; industrial portfolio at 92.4%

Approximately 5.8 million square feet of leases completed

Debt to EBITDA @ 7.1x; 2.1% Same Property NOI growth

$162 million of development starts; all 100% pre-leased medical office and suburban office

Asset Strategy

Continue strong momentum from 2010 on repositioning of portfolio

Pursue acquisitions of medical and industrial assets

Planned asset dispositions of primarily Midwest office

Closed on over $103 million of acquisitions during the quarter

$6 million in dispositions of non-core assets

Post quarter end announced 82 building, $1.08 billion suburban office portfolio sale to Blackstone

Capital Strategy

Opportunistically access capital markets . . . push out maturity schedule further

Continue improving our coverage ratios

Maintain minimal balance on line of credit

YTD Fixed charge ratio of 1.81x versus 1.79x for 2010

Redeemed $109 million in 7.25% Series N Preferred Shares

$284 million credit facility balance at quarter end, primarily due to timing

Executing across all three aspects of our strategy

© 2011 Duke Realty Corporation | 8

OPERATIONS STRATEGY

© 2011 Duke Realty Corporation | 9

OPERATIONS STRATEGY

Focus on Fundamentals

LEASING OF PORTFOLIO

STRATEGIC NEW DEVELOPMENT

AND LAND DISPOSITION

AFFO PAYOUT

Maximize return on assets

© 2011 Duke Realty Corporation | 10

OPERATIONS STRATEGY

New, High Quality Portfolio with Long-term Leases

Portfolio average

Bulk Industrial

Suburban Office

Medical Office

Property age 10.4 years 13.0 years 2.5 years

Property size 215,000 SF 115,000 SF 106,000 SF

Lease term 7.0 years 7.2 years 11.7 years

Tenant size 70,000 SF 12,000 SF 10,000 SF

Premier portfolio of assets

Note: All information as of September 30, 2011 with proposed Blackstone sale assets removed

© 2011 Duke Realty Corporation | 11

OPERATIONS STRATEGY

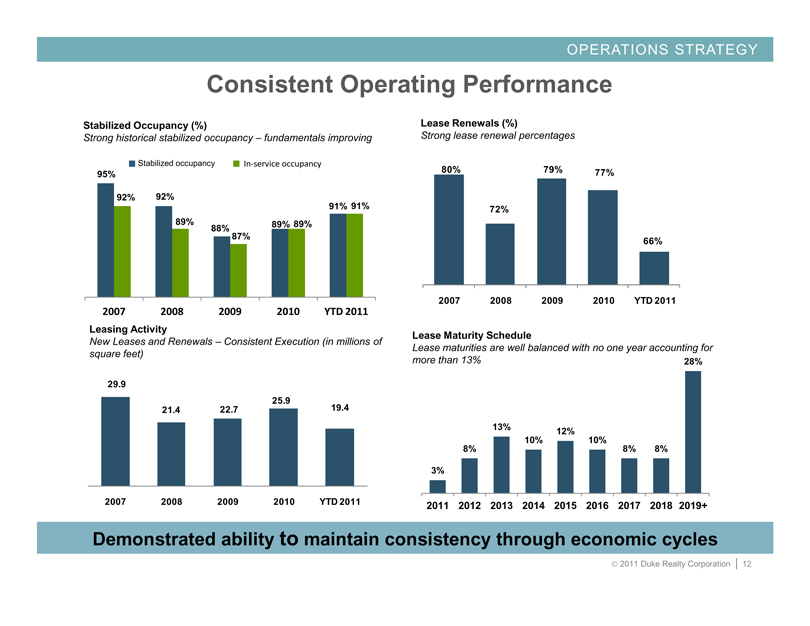

Consistent Operating Performance

Stabilized Occupancy (%)

Strong historical stabilized occupancy – fundamentals improving

Stabilized occupancy

In-service occupancy

95%

92%

92%

89%

88%

87%

89%

89%

91%

91%

2007 2008 2009 2010 YTD 2011

Lease Renewals (%)

Strong lease renewal percentages

80%

72%

79%

77%

66%

2007 2008 2009 2010 YTD 2011

Leasing Activity

New Leases and Renewals – Consistent Execution (in millions of square feet)

29.9

21.4

22.7

25.9

19.4

2007 2008 2009 2010 YTD 2011

Lease Maturity Schedule

Lease maturities are well balanced with no one year accounting for

more than 13%

3%

8%

13%

10%

12%

10%

8%

8%

28%

2011 2012 2013 2014 2015 2016 2017 2018 2019+

Demonstrated ability to maintain consistency through economic cycles

© 2011 Duke Realty Corporation | 12

RELIABLE. ANSWERS

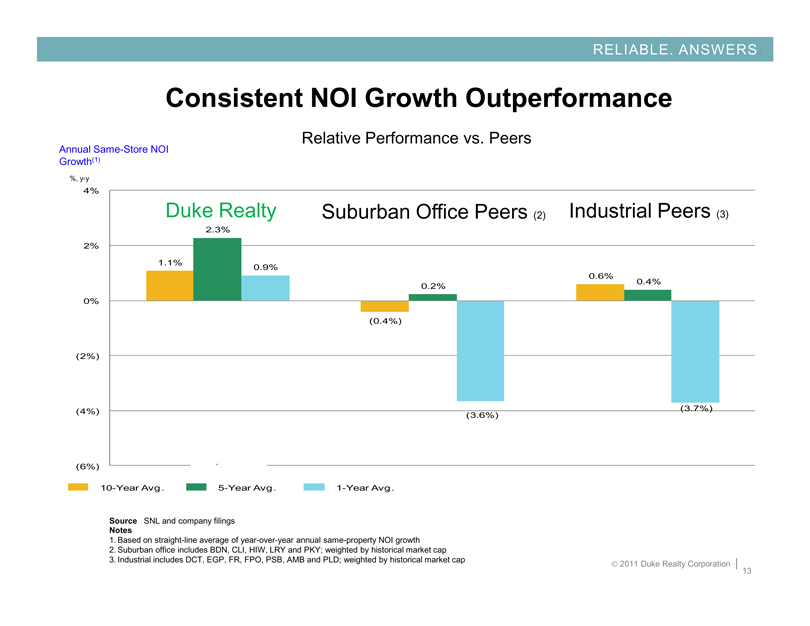

Consistent NOI Growth Outperformance

Relative Performance vs. Peers

Annual Same-Store NOI Growth(1)

%, y-y

4%

2%

0%

(2%)

(4%)

(6%)

Duke Realty

Suburban Office Peers (2)

Industrial Peers (3)

1.1%

2.3%

0.9%

(0.4%)

0.2%

(3.6%)

0.6%

0.4%

(3.7%)

10-Year Avg.

5-Year Avg.

1-Year Avg.

Source SNL and company filings

Notes

1. Based on straight-line average of year-over-year annual same-property NOI growth

2. Suburban office includes BDN, CLI, HIW, LRY and PKY; weighted by historical market cap

3. Industrial includes DCT, EGP, FR, FPO, PSB, AMB and PLD; weighted by historical market cap

© 2011 Duke Realty Corporation | 13

OPERATIONS STRATEGY

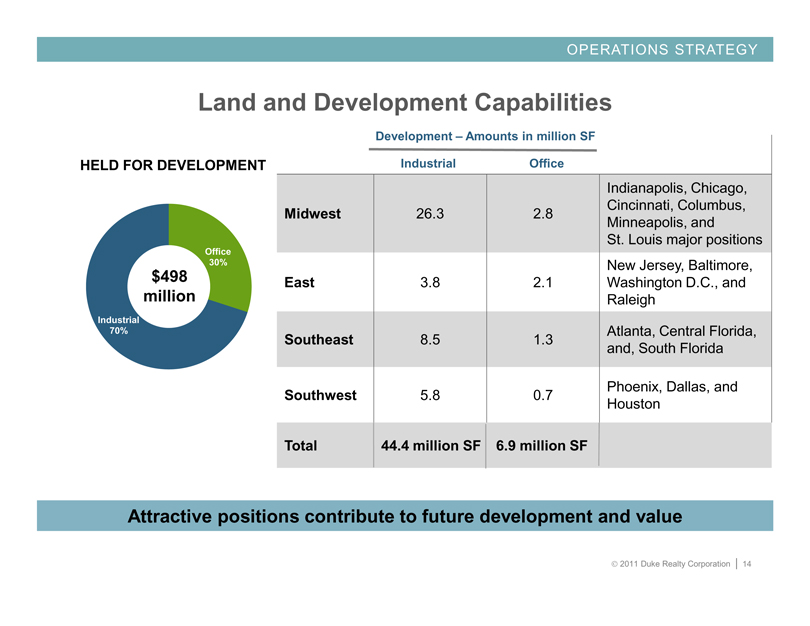

Land and Development Capabilities

HELD FOR DEVELOPMENT

$498 million

Office 30%

Industrial 70%

Development – Amounts in million SF

Industrial

Office

Midwest

26.3

2.8

Indianapolis, Chicago, Cincinnati, Columbus, Minneapolis, and St. Louis major positions

East

3.8

2.1

New Jersey, Baltimore, Washington D.C., and Raleigh

Southeast

8.5

1.3

Atlanta, Central Florida, and, South Florida

Southwest

5.8

0.7

Phoenix, Dallas, and Houston

Total

44.4 million SF

6.9 million SF

Attractive positions contribute to future development and value

© 2011 Duke Realty Corporation | 14

OPERATIONS STRATEGY

Atlanta - Office

• Headquarters Build to Suit for Primerica, A2/AA- rated financial services Company

• 345,000 square feet

• Fifteen year lease term

• Owned land at Legacy Office Park in Gwinnett County, 37 acres

• First development at this park

• $65 million project

Strategic new development on Duke Realty land

© 2011 Duke Realty Corporation | 15

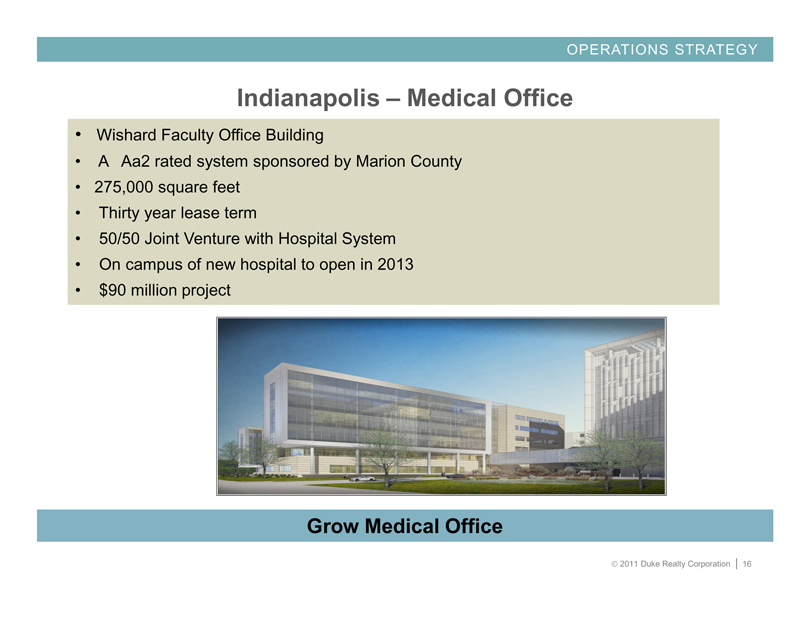

OPERATIONS STRATEGY

Indianapolis – Medical Office

• Wishard Faculty Office Building

• A Aa2 rated system sponsored by Marion County

• 275,000 square feet

• Thirty year lease term

• 50/50 Joint Venture with Hospital System

• On campus of new hospital to open in 2013

• $90 million project

Grow Medical Office

© 2011 Duke Realty Corporation | 16

OPERATIONS STRATEGY

2010 PERFORMANCE

Total portfolio occupancy of 89.1%

Industrial at 90.5% occupancy

Nearly 26 million SF leases – highest volume since 2007

2011 GOALS

Performance YTD:

Total portfolio occupancy of 90.7%

Industrial at 92.4% occupancy

19.4M SF of leases

Strong same property performance

Quality, well-positioned assets to drive performance

© 2011 Duke Realty Corporation | 17

ASSET STRATEGY

© 2011 Duke Realty Corporation | 18

ASSET STRATEGY

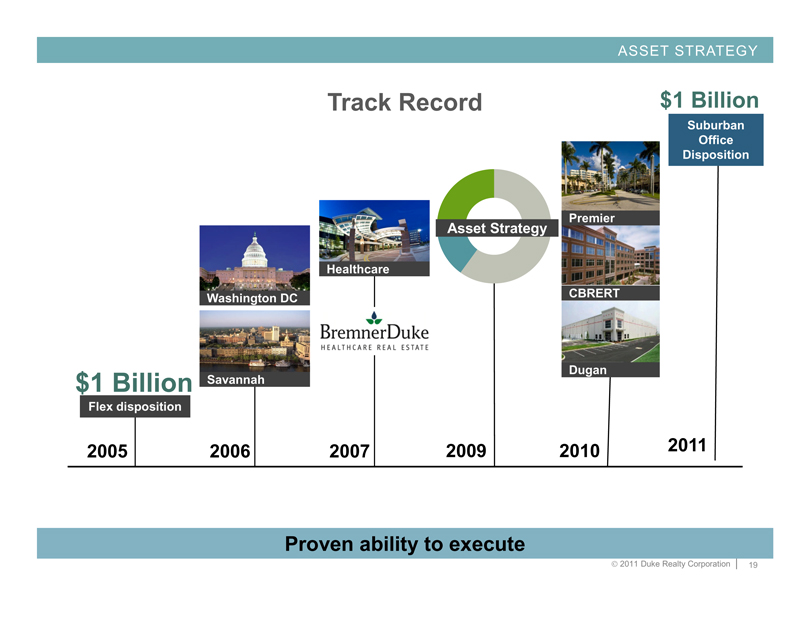

Track Record

$1 Billion

Flex disposition

Washington DC

Savannah

Healthcare

BremnerDuke

HEALTHCARE REAL ESTATE

Asset Strategy

Premier

CBRERT

Dugan

$1 Billion

Suburban Office Disposition

2005

2006

2007

2009

2010

2011

Proven ability to execute

© 2011 Duke Realty Corporation | 19

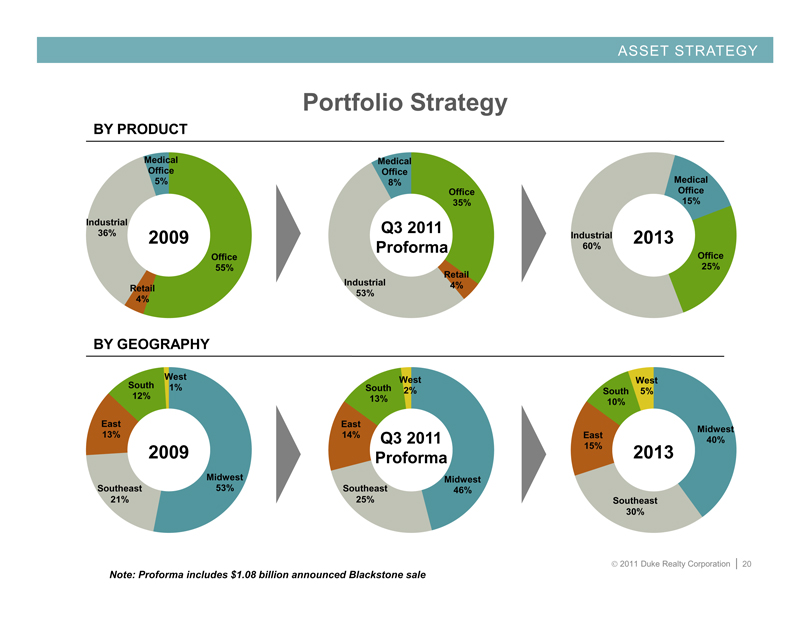

ASSET STRATEGY

Portfolio Strategy

BY PRODUCT

Medical Office 5%

Industrial 36%

Retail 4%

Office 55%

2009

Medical Office 8%

Office 35%

Retail 4%

Industrial 53%

Q3 2011 Proforma

Medical Office 15%

Office 25%

Industrial 60%

2013

BY GEOGRAPHY

West

1%

Midwest 53%

Southeast 21%

East 13%

South 12%

2009

West

2%

Midwest 46%

Southeast 25%

East 14%

South 13%

Q3 2011 Proforma

West

5%

Midwest 40%

Southeast 30%

East 15%

South 10%

2013

Note: Proforma includes $1.08 billion announced Blackstone sale

© 2011 Duke Realty Corporation | 20

ASSET STRATEGY

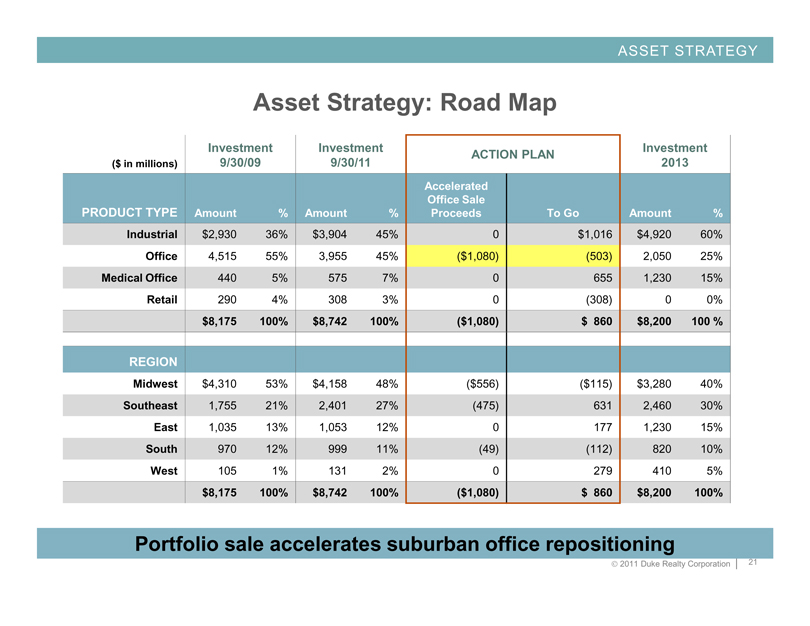

Asset Strategy: Road Map

($ in millions) Investment 9/30/09 Investment 9/30/11 ACTION PLAN Investment 2013

PRODUCT TYPE Amount % Amount % Accelerated Office Sale Proceeds To Go Amount %

Industrial $2,930 36% $3,904 45% 0 $1,016 $4,920 60%

Office 4,515 55% 3,955 45% ($1,080) (503) 2,050 25%

Medical Office 440 5% 575 7% 0 655 1,230 15%

Retail 290 4% 308 3% 0 (308) 0 0%

$8,175 100% $8,742 100% ($1,080) $860 $8,200 100%

REGION

Midwest $4,310 53% $4,158 48% ($556) ($115) $3,280 40%

Southeast 1,755 21% 2,401 27% (475) 631 2,460 30%

East 1,035 13% 1,053 12% 0 177 1,230 15%

South 970 12% 999 11% (49) (112) 820 10%

West 105 1% 131 2% 0 279 410 5%

$8,175 100% $8,742 100% ($1,080) $860 $8,200 100%

Portfolio sale accelerates suburban office repositioning

© 2011 Duke Realty Corporation | 21

ASSET STRATEGY

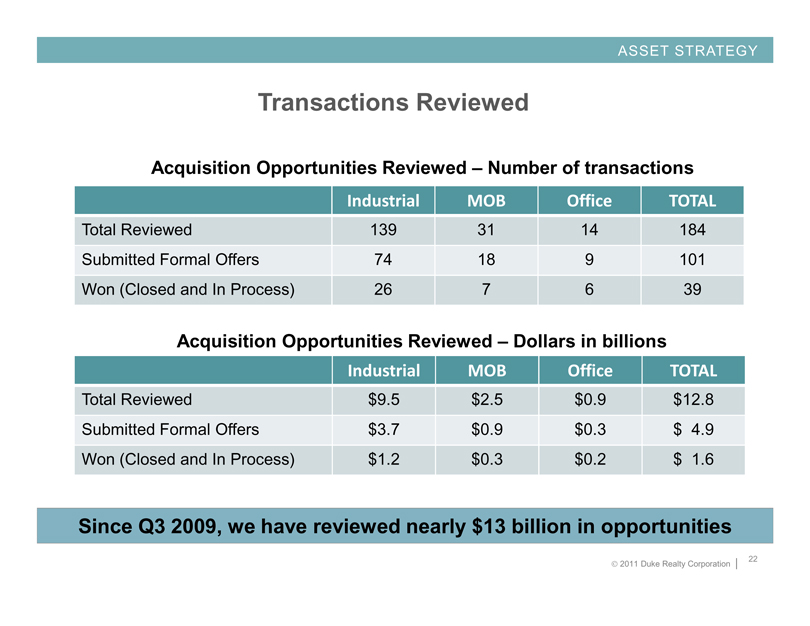

Transactions Reviewed

Acquisition Opportunities Reviewed – Number of transactions

Industrial MOB Office TOTAL

Total Reviewed 139 31 14 184

Submitted Formal Offers 74 18 9 101

Won (Closed and In Process) 26 7 6 39

Acquisition Opportunities Reviewed – Dollars in billions

Industrial MOB Office TOTAL

Total Reviewed $9.5 $2.5 $0.9 $12.8

Submitted Formal Offers $3.7 $0.9 $0.3 $4.9

Won (Closed and In Process) $1.2 $0.3 $0.2 $1.6

Since Q3 2009, we have reviewed nearly $13 billion in opportunities

© 2011 Duke Realty Corporation | 22

ASSET STRATEGY

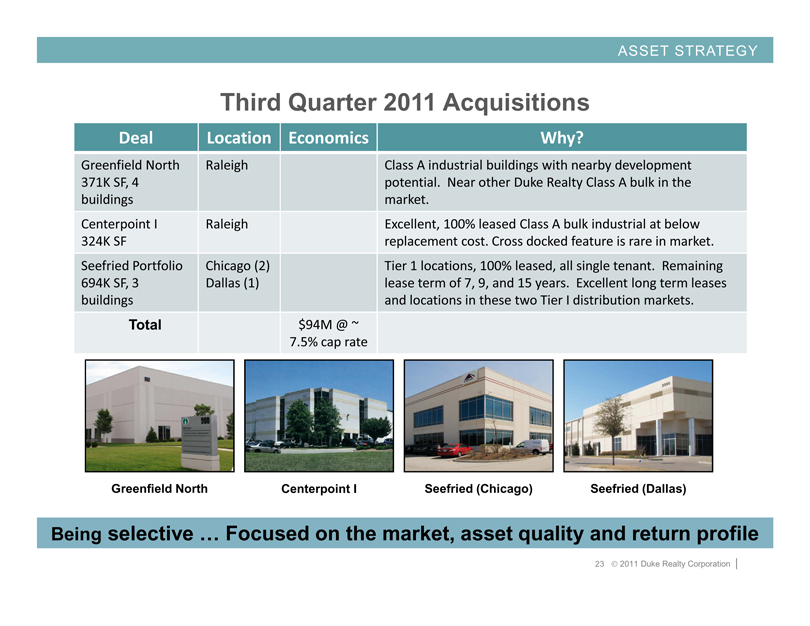

Third Quarter 2011 Acquisitions

Deal

Location

Economics

Why?

Greenfield North 371K SF, 4 buildings

Raleigh

Class A industrial buildings with nearby development potential. Near other Duke Realty Class A bulk in the market.

Centerpoint I 324K SF

Raleigh

Excellent, 100% leased Class A bulk industrial at below replacement cost. Cross docked feature is rare in market.

Seefried Portfolio 694K SF, 3 buildings

Chicago (2) Dallas (1)

Tier 1 locations, 100% leased, all single tenant. Remaining lease term of 7, 9, and 15 years. Excellent long term leases and locations in these two Tier I distribution markets.

Total

$94M @ ~ 7.5% cap rate Greenfield North Centerpoint I Seefried (Chicago) Seefried (Dallas)

Being selective … Focused on the market, asset quality and return profile

23 © 2011 Duke Realty Corporation |

ASSET STRATEGY

2010 PERFORMANCE

$533.2 million of dispositions

$919.1 million of acquisitions

$130 million of development starts

2011 GOALS

Performance YTD:

$525.5 million of dispositions

$358.9 million of acquisitions

$190.3 million of development starts

Continue to make significant progress on strategic plan

Quality portfolio further improving with asset strategy

© 2011 Duke Realty Corporation | 24

CAPITAL STRATEGY AND 2011 GUIDANCE

© 2011 Duke Realty Corporation | 25

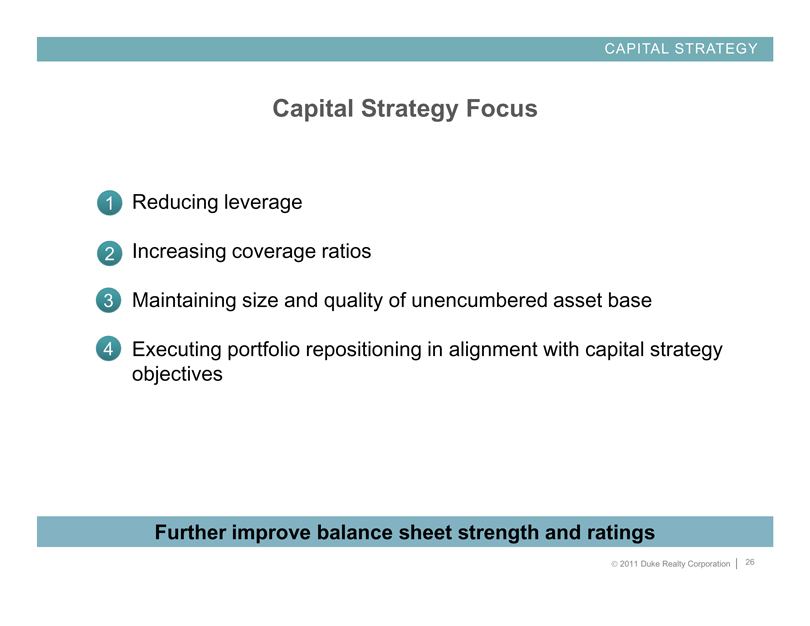

CAPITAL STRATEGY

Capital Strategy Focus

1 Reducing leverage

2 Increasing coverage ratios

3 Maintaining size and quality of unencumbered asset base

4 Executing portfolio repositioning in alignment with capital strategy objectives

Further improve balance sheet strength and ratings

© 2011 Duke Realty Corporation | 26

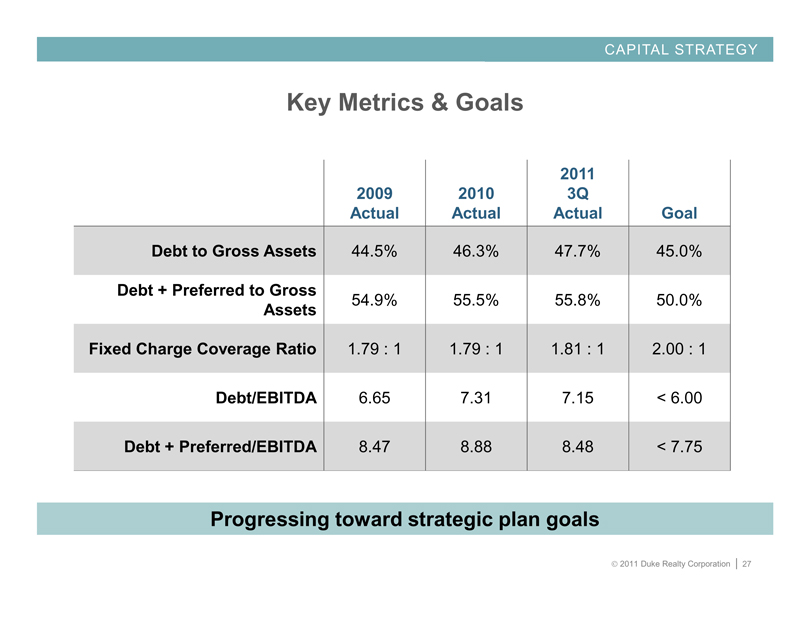

CAPITAL STRATEGY

Key Metrics & Goals

2009 Actual 2010 Actual 2011 3Q Actual Goal

Debt to Gross Assets 44.5% 46.3% 47.7% 45.0%

Debt + Preferred to Gross Assets 54.9% 55.5% 55.8% 50.0%

Fixed Charge Coverage Ratio 1.79 : 1 1.79 : 1 1.81 : 1 2.00 : 1

Debt/EBITDA 6.65 7.31 7.15 < 6.00

Debt + Preferred/EBITDA 8.47 8.88 8.48 < 7.75

Progressing toward strategic plan goals

© 2011 Duke Realty Corporation | 27

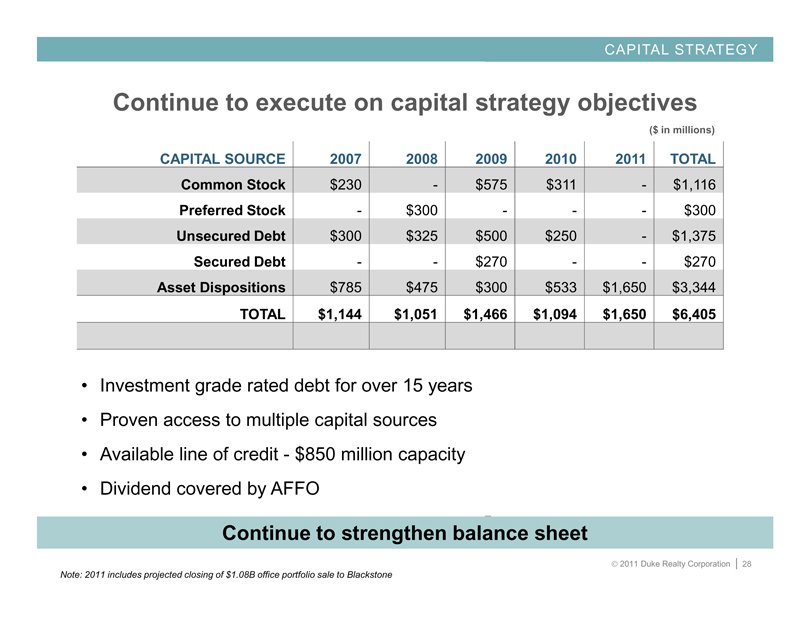

CAPITAL STRATEGY

Continue to execute on capital strategy objectives

($ in millions)

CAPITAL SOURCE 2007 2008 2009 2010 2011 TOTAL

Common Stock $230 - $575 $311 - $1,116

Preferred Stock - $300 - - - $300

Unsecured Debt $300 $325 $500 $250 - $1,375

Secured Debt - - $270 - - $270

Asset Dispositions $785 $475 $300 $533 $1,650 $3,344

TOTAL $1,144 $1,051 $1,466 $1,094 $1,650 $6,405

• Investment grade rated debt for over 15 years

• Proven access to multiple capital sources

• Available line of credit - $850 million capacity

• Dividend covered by AFFO

Continue to strengthen balance sheet

Note: 2011 includes projected closing of $1.08B office portfolio sale to Blackstone

© 2011 Duke Realty Corporation | 28

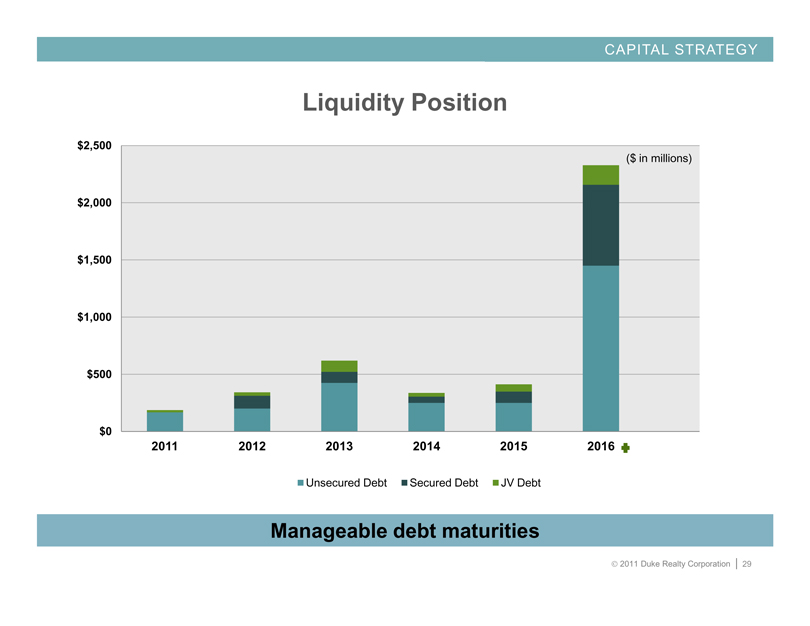

CAPITAL STRATEGY

Liquidity Position

$2,500

$2,000

$1,500

$1,000

$500

$0

($ in millions)

2011 2012 2013 2014 2015 2016

Unsecured Debt

Secured Debt

JV Debt

Manageable debt maturities

© 2011 Duke Realty Corporation | 29

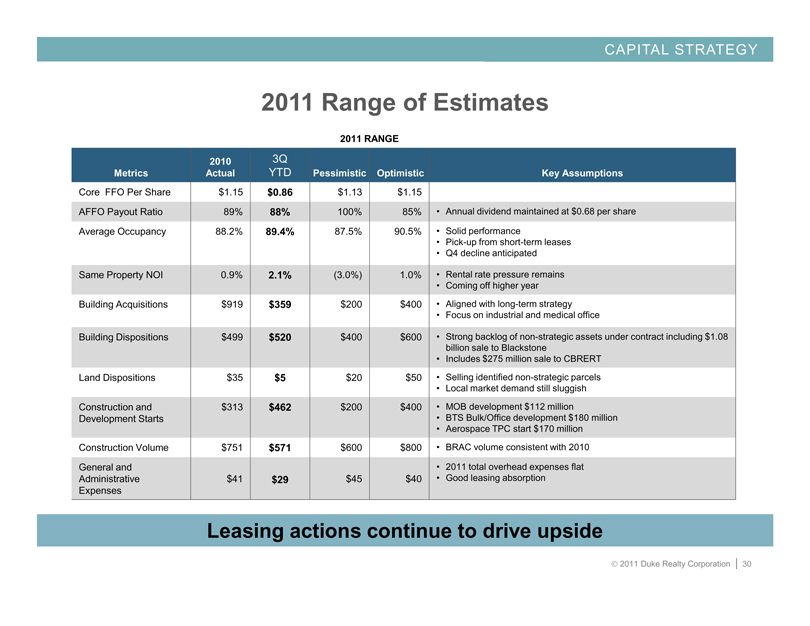

CAPITAL STRATEGY

2011 Range of Estimates

2011 RANGE

Metrics 2010 Actual 3Q YTD Pessimistic Optimistic Key Assumptions

Core FFO Per Share $1.15 $0.86 $1.13 $1.15

AFFO Payout Ratio 89% 88% 100% 85%

• Annual dividend maintained at $0.68 per share

Average Occupancy 88.2% 89.4% 87.5% 90.5% • Solid performance

• Pick-up from short-term leases

• Q4 decline anticipated

Same Property NOI 0.9% 2.1% (3.0%) 1.0%

• Rental rate pressure remains

• Coming off higher year

Building Acquisitions $919 $359 $200 $400

• Aligned with long-term strategy

• Focus on industrial and medical office

Building Dispositions $499 $520 $400 $600

• Strong backlog of non-strategic assets under contract including $1.08

billion sale to Blackstone

• Includes $275 million sale to CBRERT

Land Dispositions $35 $5 $20 $50

• Selling identified non-strategic parcels

• Local market demand still sluggish

Construction and Development Starts $313 $462 $200 $400

• MOB development $112 million

• BTS Bulk/Office development $180 million

• Aerospace TPC start $170 million

Construction Volume $751 $571 $600 $800

• BRAC volume consistent with 2010

General and Administrative Expenses

$41 $29 $45 $40

• 2011 total overhead expenses flat

• Good leasing absorption

Leasing actions continue to drive upside

© 2011 Duke Realty Corporation | 30

CAPITAL STRATEGY

2010 PERFORMANCE

$560 million of capital raised

Retired $100 million of unsecured bonds

Fixed charge ratio of 1.79x and debt to EBITDA of 7.31x

Repurchased ~ $280 million par value of bonds and more than $112 million face amount of Series O preferred stock

2011 GOALS

Opportunistically access capital markets

Continue improving coverage ratios

Maintain minimal balance on line of credit

Strong balance sheet … executing according to strategy

© 2011 Duke Realty Corporation | 31

$1.08B PORTFOLIO SALE OVERVIEW

© 2011 Duke Realty Corporation | 32

RELIABLE. ANSWERS

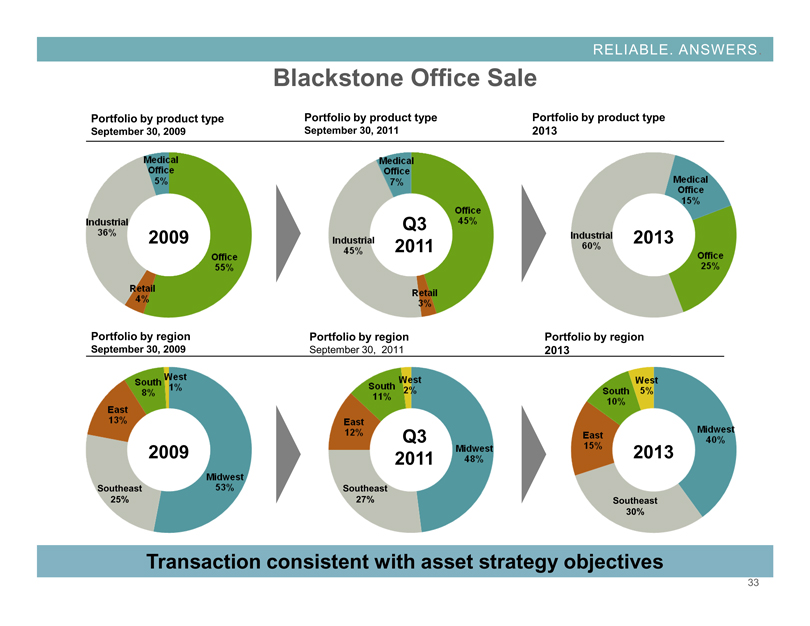

Blackstone Office Sale

Portfolio by product type September 30, 2009

Medical Office 5%

Office 55%

Retail 4%

Industrial 36%

2009

Portfolio by product type September 30, 2011

Medical Office 7%

Office 45%

Retail 3%

Industrial 45%

Q3 2011

Portfolio by product type 2013

Medical Office 15%

Office 25%

Industrial 60%

2013

Portfolio by region September 30, 2009

West 1%

Midwest 53%

Southeast 25%

East 13%

South 8%

2009

Portfolio by region

September 30, 2011

West 2%

Midwest 48%

Southeast 27%

East 12%

South 11%

Q3 2011

Portfolio by region 2013

West 5%

Midwest 40%

Southeast 30%

East 15%

South 10%

2013

Transaction consistent with asset strategy objectives

33

RELIABLE. ANSWERS

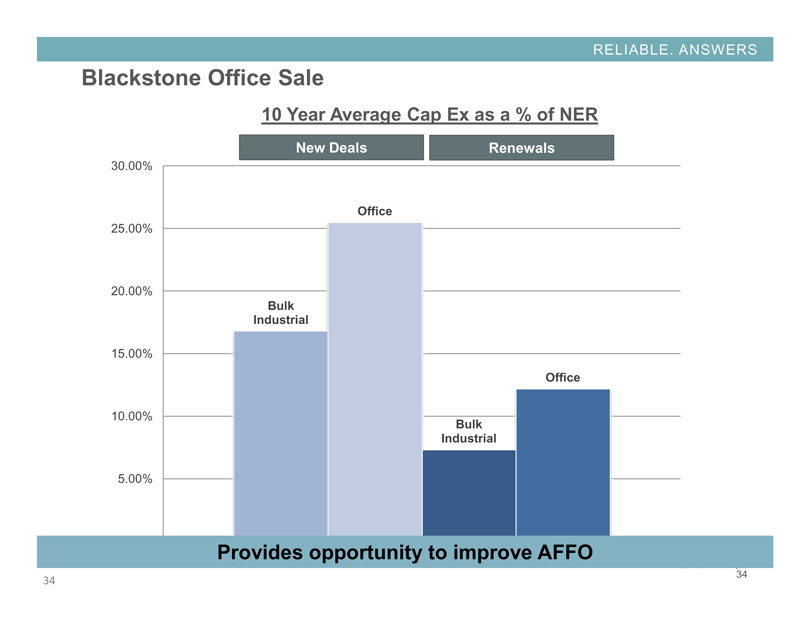

Blackstone Office Sale

10 Year Average Cap Ex as a % of NER

New Deals Renewals

30.00%

25.00%

20.00%

15.00%

10.00%

5.00%

Bulk Industrial

Office

Bulk Industrial

Office

Provides opportunity to improve AFFO

34 34

RELIABLE. ANSWERS

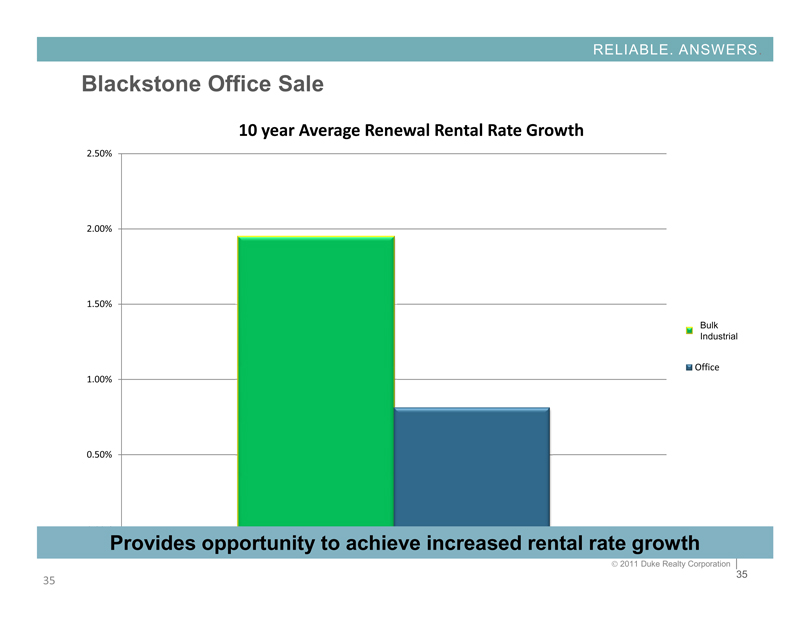

Blackstone Office Sale

10 year Average Renewal Rental Rate Growth

2.50%

2.00%

1.50%

1.00%

0.50%

Bulk

Industrial

Office

Total Bulk

Provides opportunity to achieve increased rental rate growth

© 2011 Duke Realty Corporation |

35 35

RELIABLE. ANSWERS

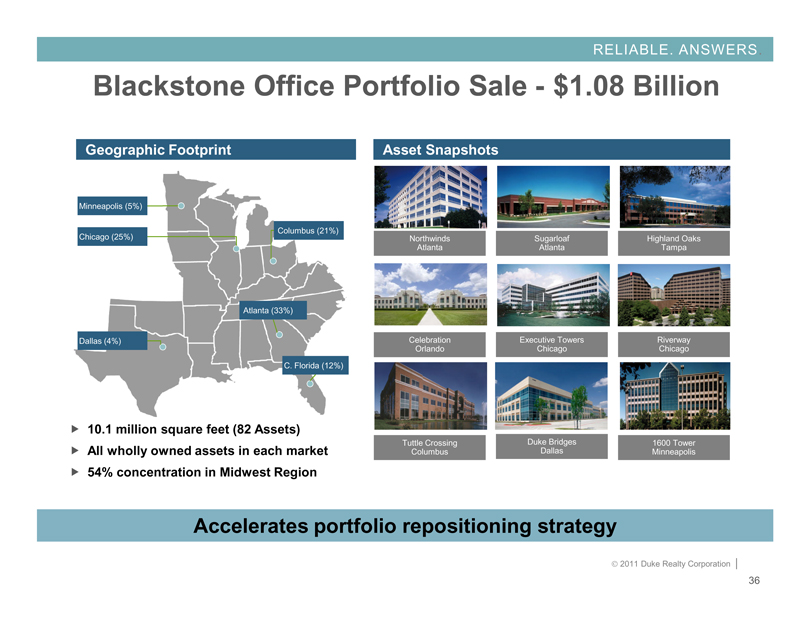

Blackstone Office Portfolio Sale - $1.08 Billion

Geographic Footprint

Minneapolis (5%)

Chicago (25%)

Dallas (4%)

Columbus (21%)

Atlanta (33%)

C. Florida (12%)

Asset Snapshots

Northwinds Atlanta

Sugarloaf Atlanta

Highland Oaks Tampa

Celebration Orlando

Executive Towers Chicago

Riverway Chicago

Tuttle Crossing Columbus

Duke Bridges Dallas

1600 Tower Minneapolis

10.1 million square feet (82 Assets)

All wholly owned assets in each market

54% concentration in Midwest Region

Accelerates portfolio repositioning strategy

© 2011 Duke Realty Corporation |

36

RELIABLE. ANSWERS

Blackstone Sale – Portfolio Analysis

Blackstone Portfolio

Remaining Portfolio

Total Square Feet 10.1 M 23.3 M

# of Properties 82 204

Average Size 126,000 115,000

Average Tenant Size 12,000 12,000

Average Age 15 13

Average Lease Term 6.5 7.2

Lease Expirations (% of total)

2012 13% 9%

2013 19% 12%

2014 11% 8%

© 2011 Duke Realty Corporation | 37

RELIABLE. ANSWERS

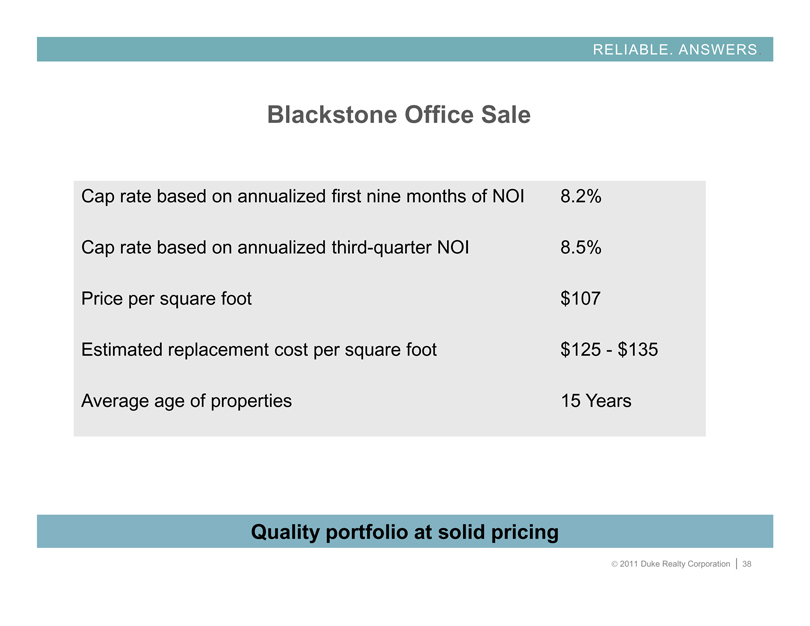

Blackstone Office Sale

Cap rate based on annualized first nine months of NOI 8.2%

Cap rate based on annualized third-quarter NOI 8.5%

Price per square foot $107

Estimated replacement cost per square foot $125 - $135

Average age of properties 15 Years

Quality portfolio at solid pricing

© 2011 Duke Realty Corporation | 38

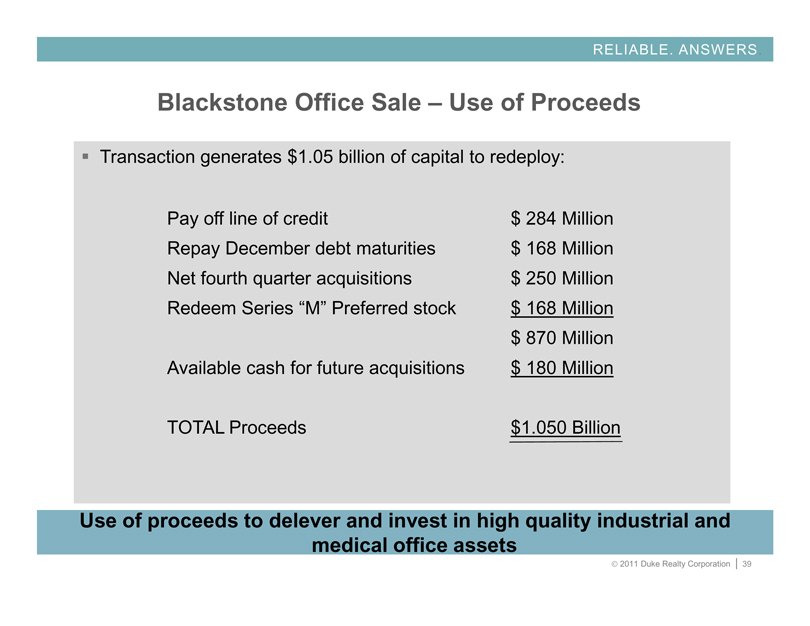

RELIABLE. ANSWERS

Blackstone Office Sale – Use of Proceeds

Transaction generates $1.05 billion of capital to redeploy:

Pay off line of credit $ 284 Million

Repay December debt maturities $ 168 Million

Net fourth quarter acquisitions $ 250 Million

Redeem Series “M” Preferred stock $ 168 Million

$ 870 Million

Available cash for future acquisitions $ 180 Million

TOTAL Proceeds $1.050 Billion

Use of proceeds to delever and invest in high quality industrial and medical office assets

© 2011 Duke Realty Corporation | 39

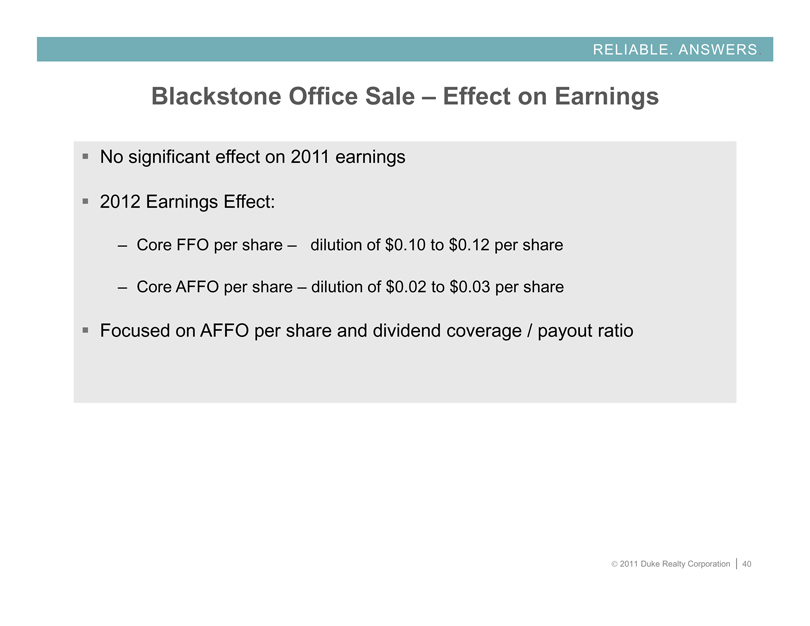

RELIABLE. ANSWERS

Blackstone Office Sale – Effect on Earnings

No significant effect on 2011 earnings

2012 Earnings Effect:

– Core FFO per share – dilution of $0.10 to $0.12 per share

– Core AFFO per share – dilution of $0.02 to $0.03 per share

Focused on AFFO per share and dividend coverage / payout ratio

© 2011 Duke Realty Corporation | 40

RELIABLE. ANSWERS

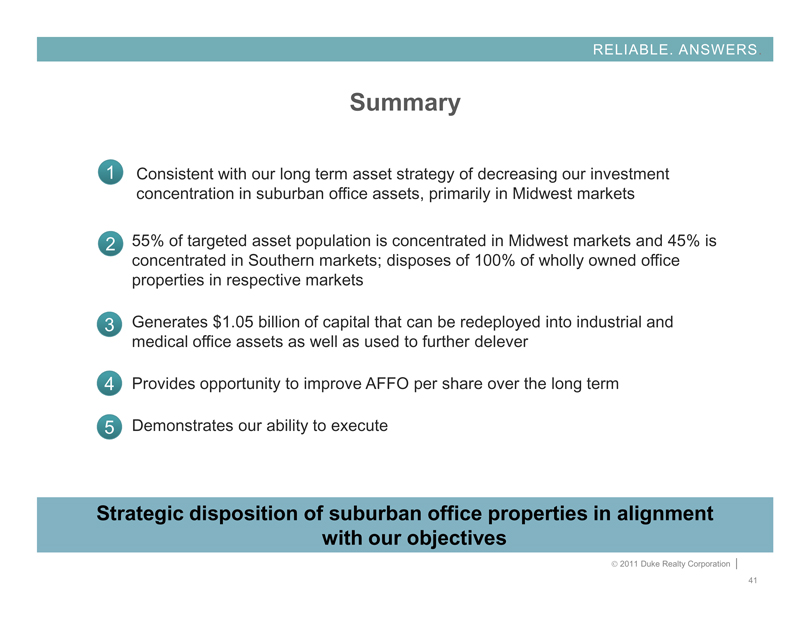

Summary

1 Consistent with our long term asset strategy of decreasing our investment concentration in suburban office assets, primarily in Midwest markets

2 55% of targeted asset population is concentrated in Midwest markets and 45% is concentrated in Southern markets; disposes of 100% of wholly owned office properties in respective markets

3 Generates $1.05 billion of capital that can be redeployed into industrial and medical office assets as well as used to further delever

4 Provides opportunity to improve AFFO per share over the long term

5 Demonstrates our ability to execute

Strategic disposition of suburban office properties in alignment with our objectives

© 2011 Duke Realty Corporation |

41

MEDICAL OFFICE STRATEGY &

Performance Update

© 2011 Duke Realty Corporation | 42

RELIABLE. ANSWERS

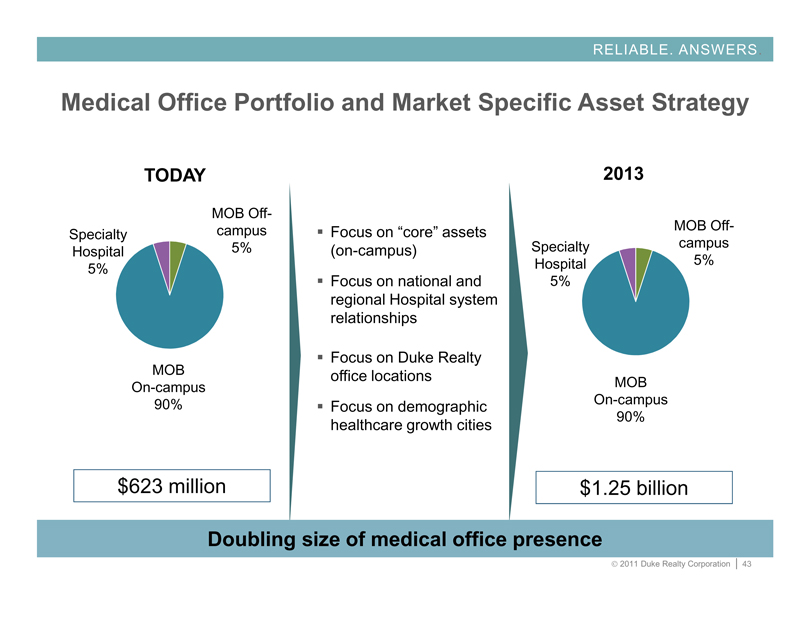

Medical Office Portfolio and Market Specific Asset Strategy

TODAY

Specialty Hospital 5%

MOB Off-campus 5%

MOB On-campus 90%

$623 million

Focus on “core” assets (on-campus)

Focus on national and regional Hospital system relationships

Focus on Duke Realty office locations

Focus on demographic healthcare growth cities

2013

Specialty Hospital 5%

MOB On-campus 90%

MOB Off-campus 5%

$1.25 billion

Doubling size of medical office presence

© 2011 Duke Realty Corporation | 43

MEDICAL OFFICE OVERVIEW

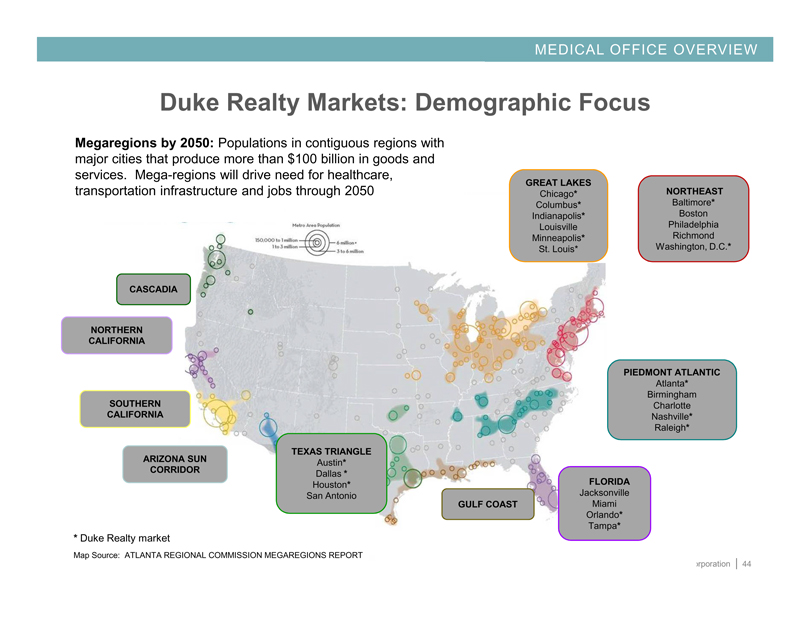

Duke Realty Markets: Demographic Focus

Megaregions by 2050: Populations in contiguous regions with major cities that produce more than $100 billion in goods and services. Mega-regions will drive need for healthcare, transportation infrastructure and jobs through 2050

Metro Area Population

150,000 to 1 million

1 to 3 million

6 million *

3 to 6 million

GREAT LAKES

Chicago* Columbus* Indianapolis* Louisville Minneapolis* St. Louis*

NORTHEAST

Baltimore* Boston Philadelphia Richmond Washington, D.C.*

PIEDMONT ATLANTIC

Atlanta* Birmingham Charlotte Nashville* Raleigh*

FLORIDA

Jacksonville Miami Orlando* Tampa*

GULF COAST

TEXAS TRIANGLE

Austin* Dallas * Houston* San Antonio

ARIZONA SUN CORRIDOR

SOUTHERN CALIFORNIA

NORTHERN CALIFORNIA

CASCADIA

* Duke Realty market

Map Source: ATLANTA REGIONAL COMMISSION MEGAREGIONS REPORT

Corporation | 44

MEDICAL OFFICE OVERVIEW

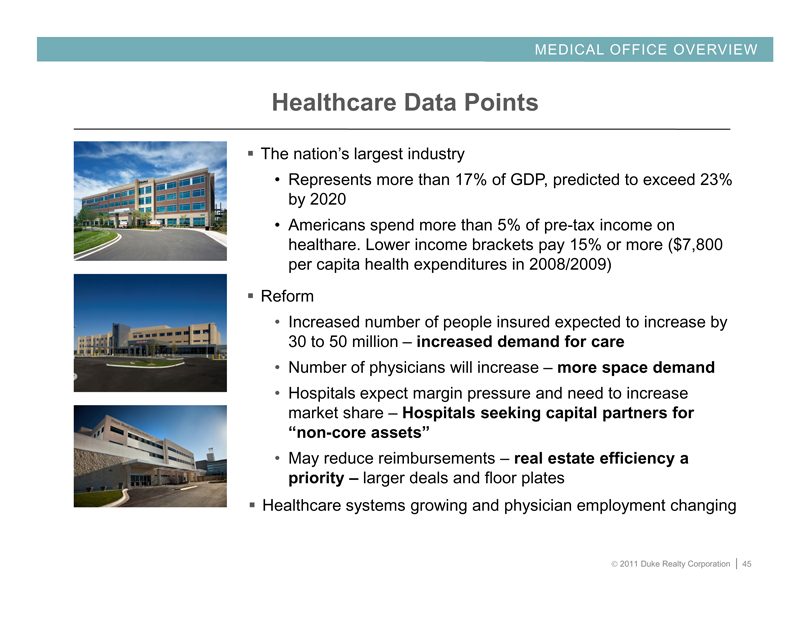

Healthcare Data Points

The nation’s largest industry

• Represents more than 17% of GDP, predicted to exceed 23% by 2020

• Americans spend more than 5% of pre-tax income on healthare. Lower income brackets pay 15% or more ($7,800 per capita health expenditures in 2008/2009)

Reform

• Increased number of people insured expected to increase by 30 to 50 million – increased demand for care

• Number of physicians will increase – more space demand

• Hospitals expect margin pressure and need to increase market share – Hospitals seeking capital partners for “non-core assets”

• May reduce reimbursements – real estate efficiency a priority – larger deals and floor plates

Healthcare systems growing and physician employment changing

© 2011 Duke Realty Corporation | 45

MEDICAL OFFICE OVERVIEW

Demand Driver

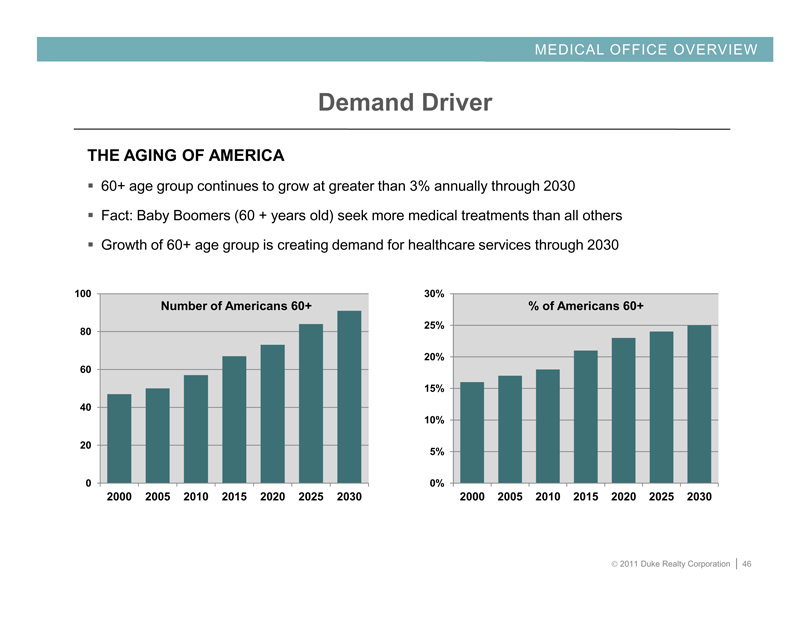

THE AGING OF AMERICA

60+ age group continues to grow at greater than 3% annually through 2030

Fact: Baby Boomers (60 + years old) seek more medical treatments than all others

Growth of 60+ age group is creating demand for healthcare services through 2030

100

80

60

40

20

0

Number of Americans 60+

2000 2005 2010 2015 2020 2025 2030

30%

25%

20%

15%

10%

5%

0%

% of Americans 60+

2000 2005 2010 2015 2020 2025 2030

© 2011 Duke Realty Corporation | 46

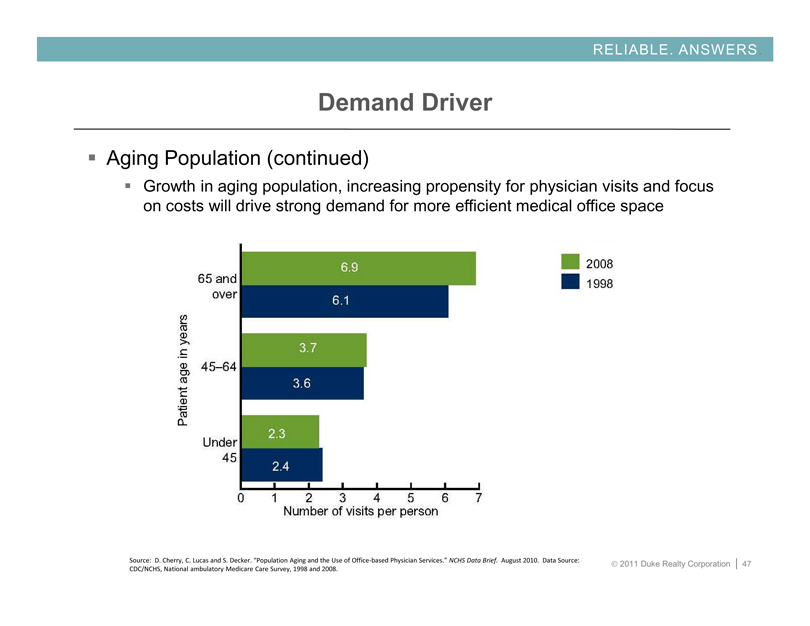

RELIABLE. ANSWERS

Demand Driver

Aging Population (continued)

Growth in aging population, increasing propensity for physician visits and focus on costs will drive strong demand for more efficient medical office space

Patient in years

65 and over

45-64

Under 45

6.9

6.1

3.7

3.6

2.3

2.4

0 1 2 3 4 5 6 7

Number of visits per person

2008

1998

Source: D. Cherry, C. Lucas and S. Decker. “Population Aging and the Use of Office-based Physician Services.” NCHS Data Brief. August 2010. Data Source: CDC/NCHS, National ambulatory Medicare Care Survey, 1998 and 2008.

© 2011 Duke Realty Corporation | 47

MEDICAL OFFICE OVERVIEW

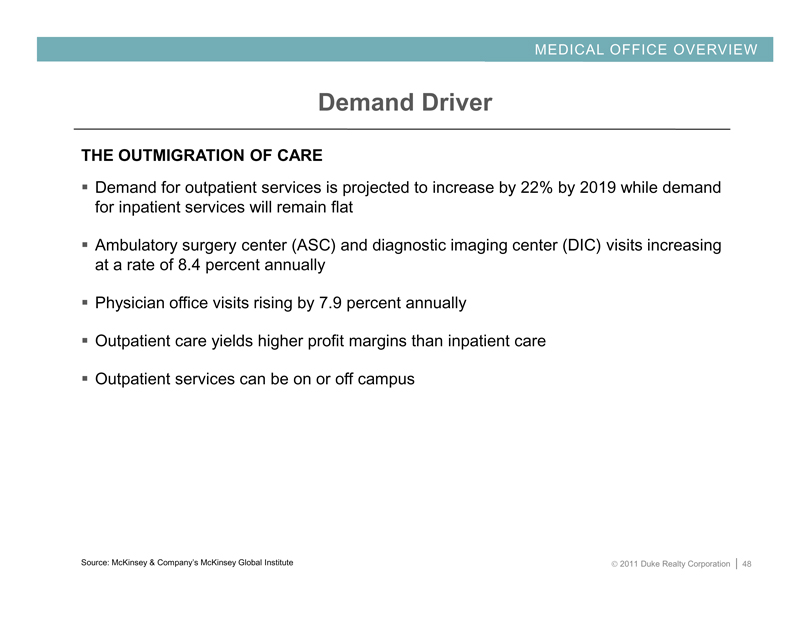

Demand Driver

THE OUTMIGRATION OF CARE

Demand for outpatient services is projected to increase by 22% by 2019 while demand for inpatient services will remain flat

Ambulatory surgery center (ASC) and diagnostic imaging center (DIC) visits increasing at a rate of 8.4 percent annually

Physician office visits rising by 7.9 percent annually

Outpatient care yields higher profit margins than inpatient care

Outpatient services can be on or off campus

Source: McKinsey & Company’s McKinsey Global Institute

© 2011 Duke Realty Corporation | 48

RELIABLE. ANSWERS

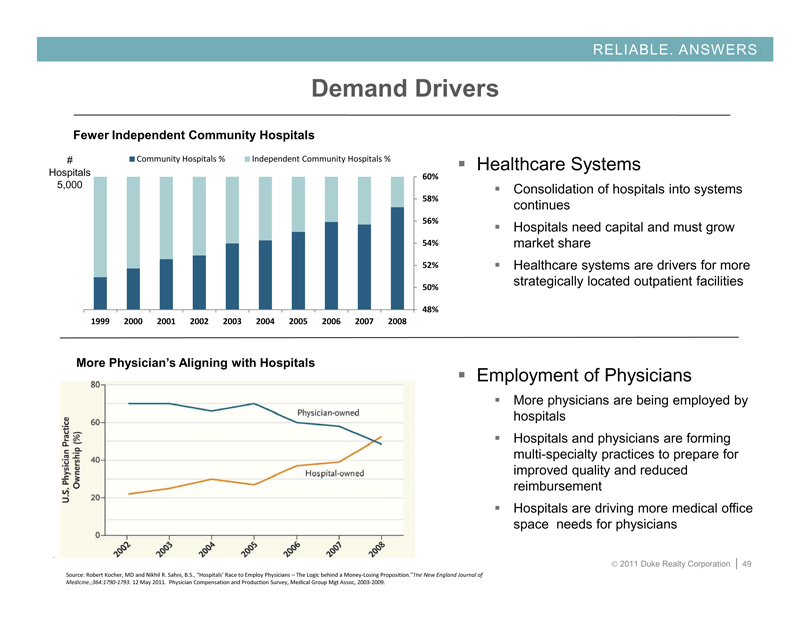

Demand Drivers

Fewer Independent Community Hospitals

# Hospitals 5,000

Community Hospitals %

Independent Community Hospitals %

60%

58%

56%

54%

52%

50%

48%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Healthcare Systems

Consolidation of hospitals into systems continues

Hospitals need capital and must grow market share

Healthcare systems are drivers for more strategically located outpatient facilities

More Physician’s Aligning with Hospitals

U.S. Physician Practice Ownership (%)

80 60 40 20 0

Physician-owned

Hospital-owned

2002 2003 2004 2005 2006 2007 2008

Employment of Physicians

More physicians are being employed by hospitals

Hospitals and physicians are forming multi-specialty practices to prepare for improved quality and reduced reimbursement

Hospitals are driving more medical office space needs for physicians

Source: Robert Kocher, MD and Nikhil R. Sahni, B.S., “Hospitals’ Race to Employ Physicians – The Logic behind a Money-Losing Proposition.”The New England Journal of Medicine.;364:1790-1793. 12 May 2011. Physician Compensation and Production Survey, Medical Group Mgt Assoc, 2003-2009.

© 2011 Duke Realty Corporation | 49

MEDICAL OFFICE OVERVIEW

Development Focus

ACTION PLAN

National brand awareness

Be “Experts”

– Speak at national conferences (ASHE, BOMA)

– Third party references

National system relationships

– Ascension

– Tenet

– HCA

– Adventist

Regional system relationships

– Baylor Health

– Rex Healthcare

– Carolina Healthcare Systems

– Advocate

Local 10%

National 30%

Regional 60%

System Focus

© 2011 Duke Realty Corporation | 50

RELIABLE. ANSWERS

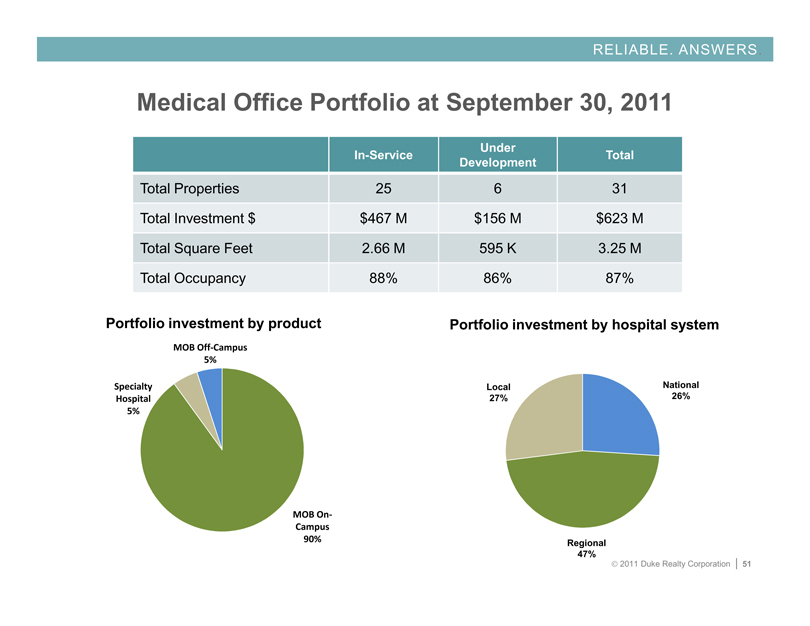

Medical Office Portfolio at September 30, 2011

In-Service Under Development Total

Total Properties 25 6 31

Total Investment $ $467 M $156 M $623 M

Total Square Feet 2.66 M 595 K 3.25 M

Total Occupancy 88% 86% 87%

Portfolio investment by product

MOB Off-Campus 5%

MOB On-Campus 90%

Specialty Hospital 5%

Portfolio investment by hospital system

National 26%

Regional 47%

Local 27%

© 2011 Duke Realty Corporation | 51

RELIABLE. ANSWERS

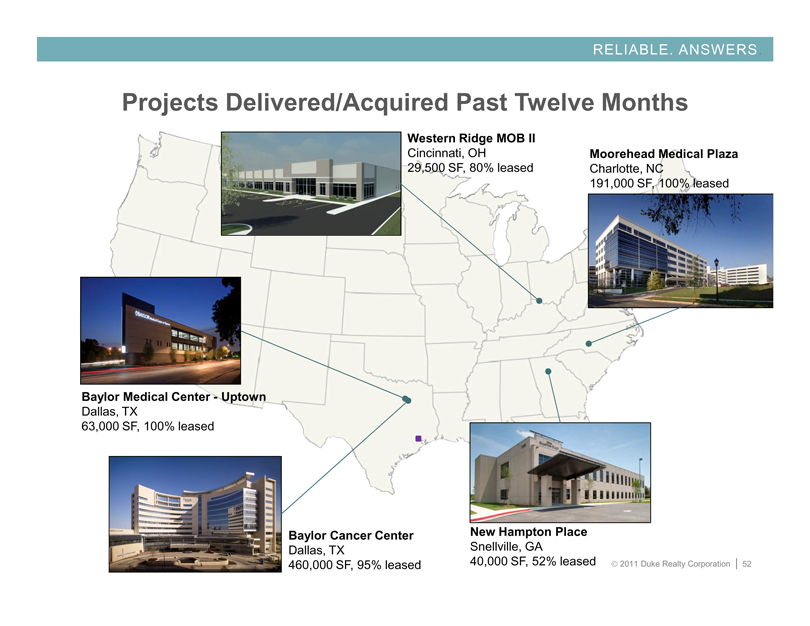

Projects Delivered/Acquired Past Twelve Months

Western Ridge MOB II

Cincinnati, OH

29,500 SF, 80% leased

Moorehead Medical Plaza

Charlotte, NC

191,000 SF, 100% leased

New Hampton Place

Snellville, GA

40,000 SF, 52% leased

Baylor Cancer Center

Dallas, TX

460,000 SF, 95% leased

Baylor Medical Center - Uptown

Dallas, TX

63,000 SF, 100% leased

© 2011 Duke Realty Corporation | 52

RELIABLE. ANSWERS

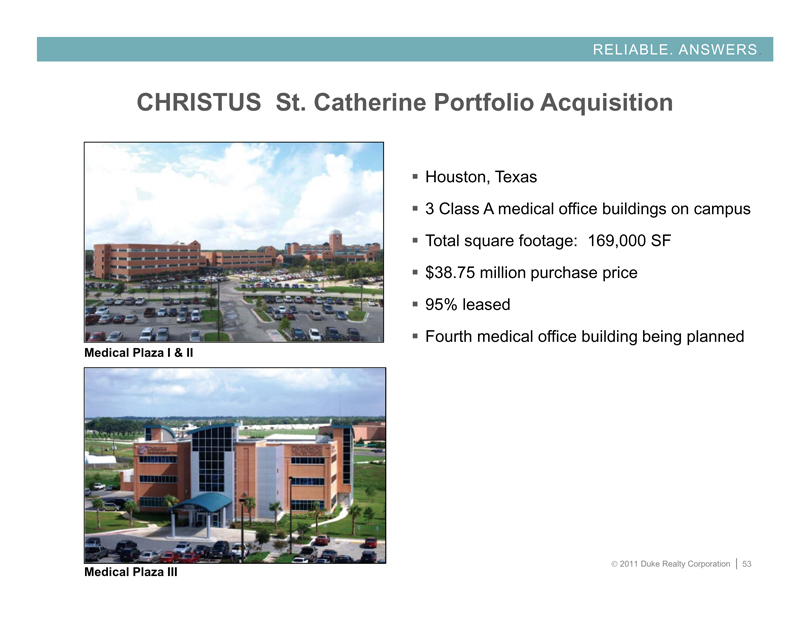

CHRISTUS St. Catherine Portfolio Acquisition

Houston, Texas

3 Class A medical office buildings on campus Total square footage: 169,000 SF

$38.75 million purchase price 95% leased

Fourth medical office building being planned

Medical Plaza I & II

Medical Plaza III

© 2011 Duke Realty Corporation | 53

RELIABLE. ANSWERS

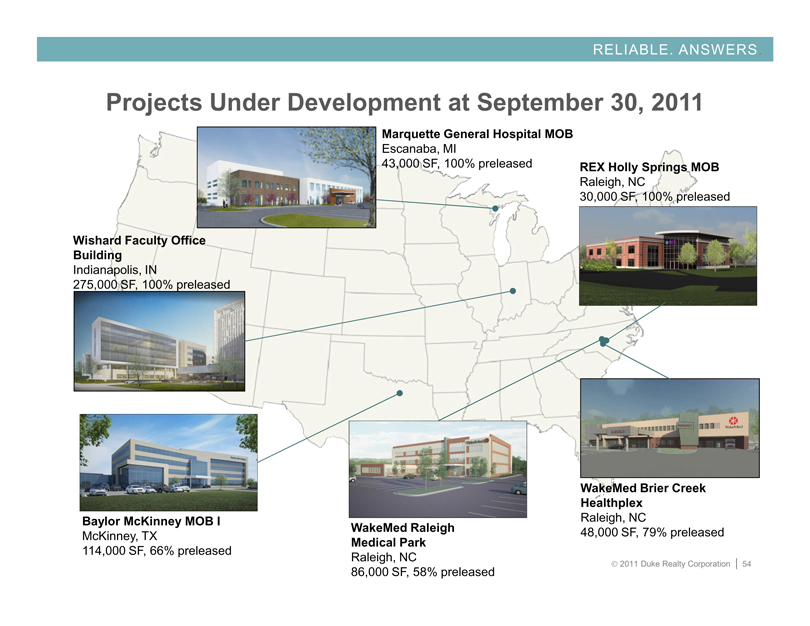

Projects Under Development at September 30, 2011

Marquette General Hospital MOB

Escanaba, MI

43,000 SF, 100% preleased

REX Holly Springs MOB

Raleigh, NC

30,000 SF, 100% preleased

WakeMed Brier Creek Healthplex

Raleigh, NC

48,000 SF, 79% preleased

WakeMed Raleigh Medical Park

Raleigh, NC

86,000 SF, 58% preleased

Baylor McKinney MOB I

McKinney, TX

114,000 SF, 66% preleased

Wishard Faculty Office Building

Indianapolis, IN

275,000 SF, 100% preleased

© 2011 Duke Realty Corporation | 54

RELIABLE. ANSWERS

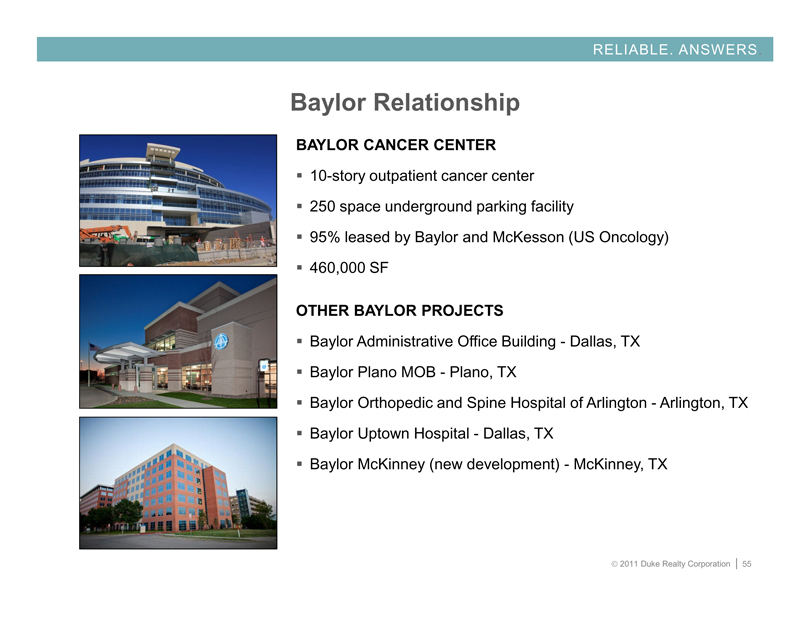

Baylor Relationship

BAYLOR CANCER CENTER

10-story outpatient cancer center

250 space underground parking facility

95% leased by Baylor and McKesson (US Oncology)

460,000 SF

OTHER BAYLOR PROJECTS

Baylor Administrative Office Building - Dallas, TX

Baylor Plano MOB - Plano, TX

Baylor Orthopedic and Spine Hospital of Arlington - Arlington, TX

Baylor Uptown Hospital - Dallas, TX

Baylor McKinney (new development) - McKinney, TX

© 2011 Duke Realty Corporation | 55

RELIABLE. ANSWERS

Goal: Grow Medical Office to $1.25 Billion by 2013

Our Plan

Existing healthcare assets ≈ $775 Million by 1/31/2012

Win developments ≈ $200 Million in 2012 and 2013

Acquire ≈ $200-$250 Million in 2012 and 2013

Our Focus

Growth regions (Southeast, South) Health system relationships On-campus assets

Class A product (50,000 – 400,000 + square feet)

National industry expert

© 2011 Duke Realty Corporation | 56

DALLAS MARKET OVERVIEW

© 2011 Duke Realty Corporation | 57

DALLAS OVERVIEW

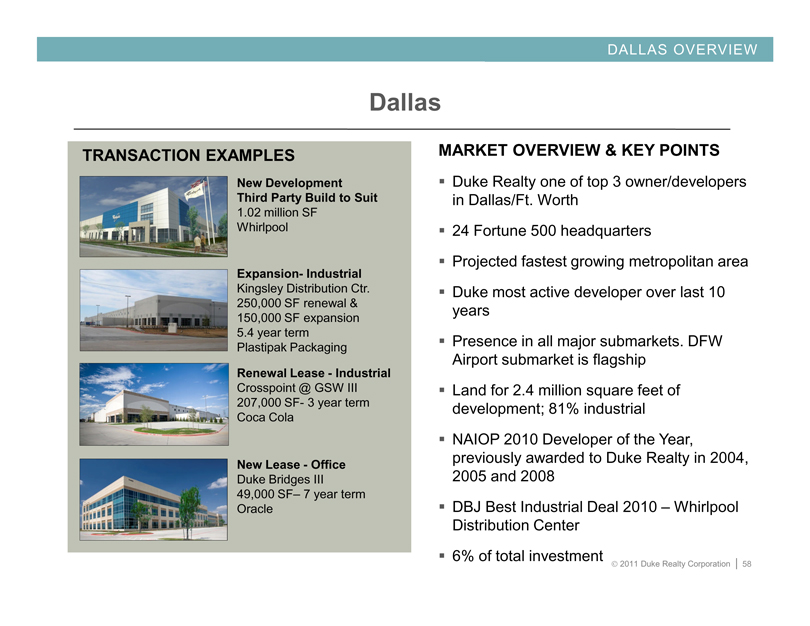

Dallas

TRANSACTION EXAMPLES

New Development Third Party Build to Suit

1.02 million SF

Whirlpool

Expansion- Industrial

Kingsley Distribution Ctr. 250,000 SF renewal & 150,000 SF expansion

5.4 year term Plastipak Packaging

Renewal Lease - Industrial

Crosspoint @ GSW III 207,000 SF- 3 year term Coca Cola

New Lease - Office

Duke Bridges III

49,000 SF– 7 year term Oracle

MARKET OVERVIEW & KEY POINTS

Duke Realty one of top 3 owner/developers in Dallas/Ft. Worth

24 Fortune 500 headquarters

Projected fastest growing metropolitan area

Duke most active developer over last 10 years

Presence in all major submarkets. DFW Airport submarket is flagship

Land for 2.4 million square feet of development; 81% industrial

NAIOP 2010 Developer of the Year, previously awarded to Duke Realty in 2004, 2005 and 2008

DBJ Best Industrial Deal 2010 – Whirlpool Distribution Center

6% of total investment

© 2011 Duke Realty Corporation | 58

DALLAS OVERVIEW

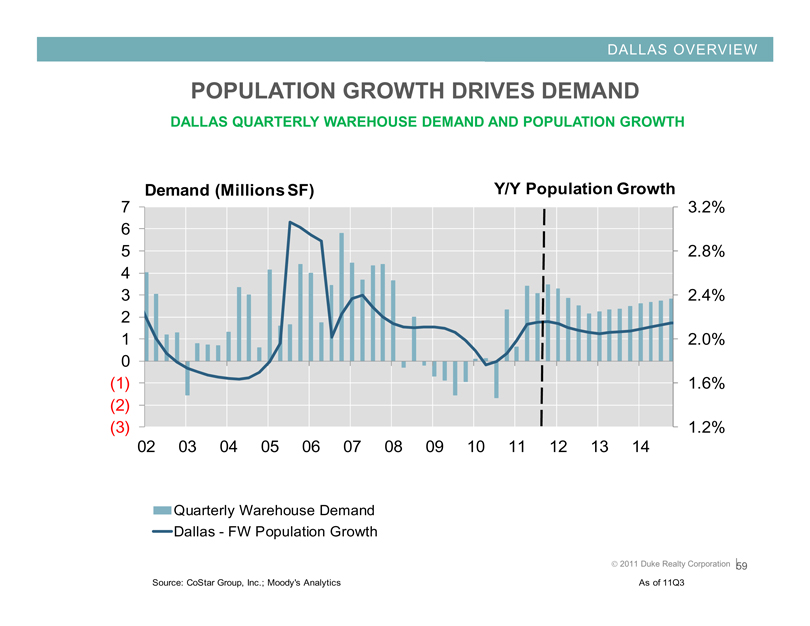

POPULATION GROWTH DRIVES DEMAND

DALLAS QUARTERLY WAREHOUSE DEMAND AND POPULATION GROWTH

Demand (Millions SF)

Y/Y Population Growth

7

6

5

4

3

2

1

0

(1)

(2)

(3)

3.2%

2.8%

2.4%

2.0%

1.6%

1.2%

02 03 04 05 06 07 08 09 10 11 12 13 14

Quarterly Warehouse Demand Dallas - FW Population Growth

Source: CoStar Group, Inc.; Moody’s Analytics

© 2011 Duke Realty Corporation | 59

As of 11Q3

DALLAS OVERVIEW

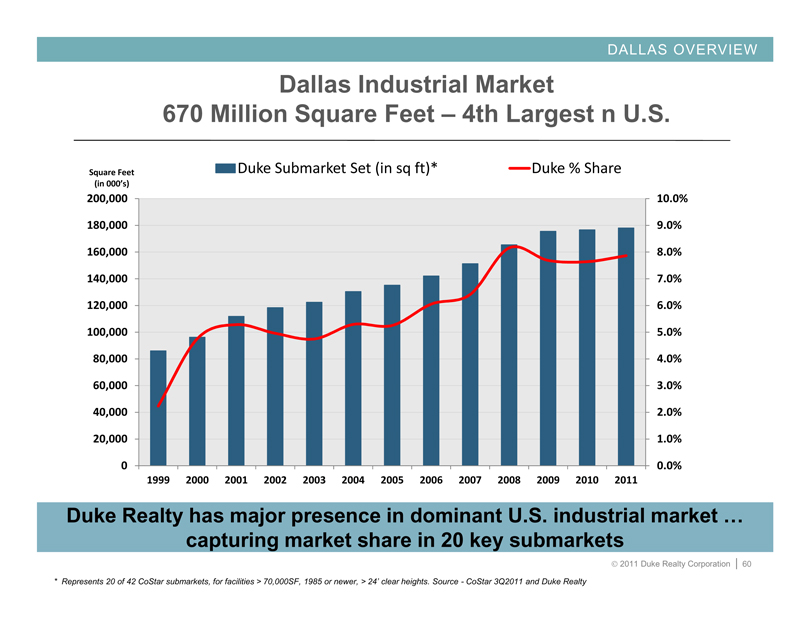

Dallas Industrial Market

670 Million Square Feet – 4th Largest n U.S.

Duke Submarket Set (in sq ft)*

Duke % Share

Square Feet

(in 000’s)

200,000

180,000

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

0

10.0%

9.0%

8.0%

7.0%

6.0%

5.0%

4.0%

3.0%

2.0%

1.0%

0.0%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Duke Realty has major presence in dominant U.S. industrial market … capturing market share in 20 key submarkets

* Represents 20 of 42 CoStar submarkets, for facilities > 70,000SF, 1985 or newer, > 24’ clear heights. Source - CoStar 3Q2011 and Duke Realty

© 2011 Duke Realty Corporation | 60

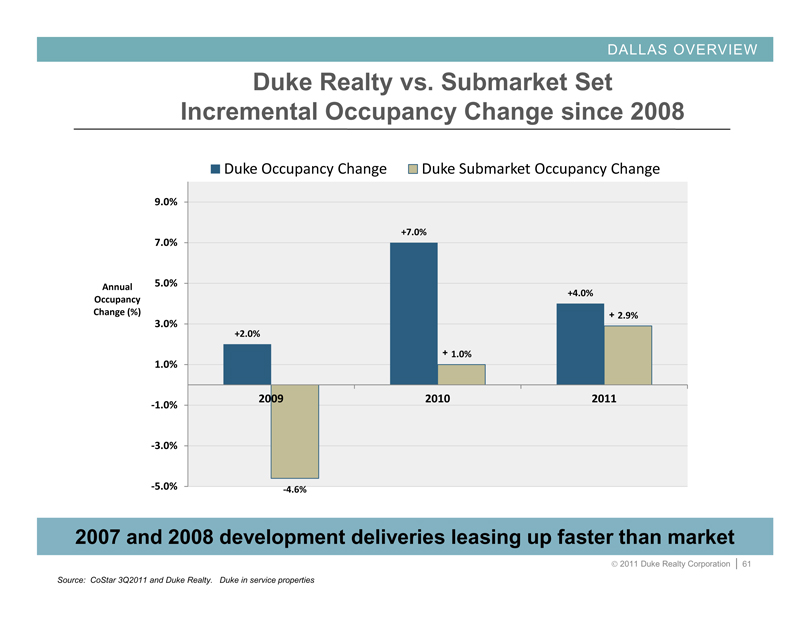

DALLAS OVERVIEW

Duke Realty vs. Submarket Set Incremental Occupancy Change since 2008

Duke Occupancy Change

Duke Submarket Occupancy Change

Annual Occupancy Change (%)

9.0%

7.0%

5.0%

3.0%

1.0%

-1.0%

-3.0%

-5.0%

+2.0%

+7.0%

+ 1.0%

+4.0%

+ 2.9%

2009

2010

2011

-4.6%

2007 and 2008 development deliveries leasing up faster than market

Source: CoStar 3Q2011 and Duke Realty. Duke in service properties

© 2011 Duke Realty Corporation | 61

DALLAS OVERVIEW

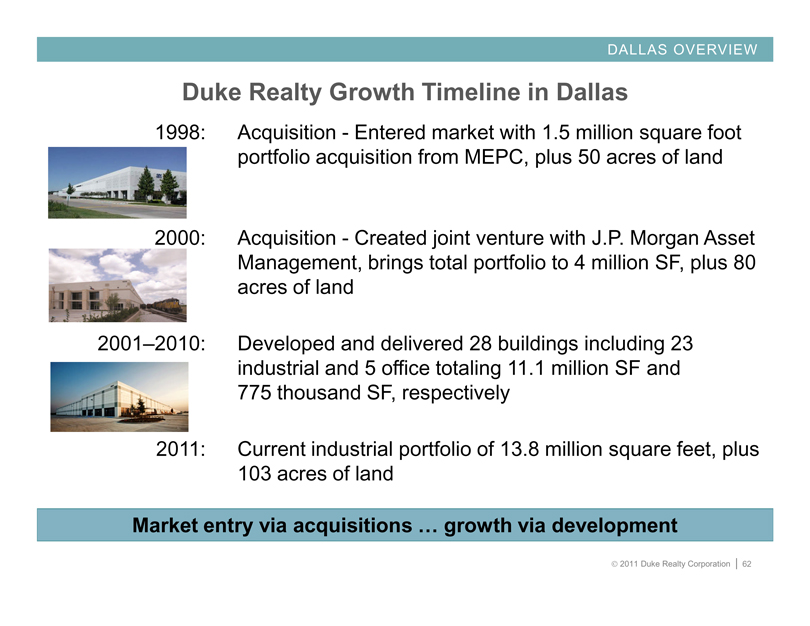

Duke Realty Growth Timeline in Dallas

1998:

Acquisition - Entered market with 1.5 million square foot portfolio acquisition from MEPC, plus 50 acres of land

2000:

Acquisition - Created joint venture with J.P. Morgan Asset Management, brings total portfolio to 4 million SF, plus 80 acres of land

2001–2010:

Developed and delivered 28 buildings including 23 industrial and 5 office totaling 11.1 million SF and 775 thousand SF, respectively

2011:

Current industrial portfolio of 13.8 million square feet, plus 103 acres of land

Market entry via acquisitions … growth via development

© 2011 Duke Realty Corporation | 62

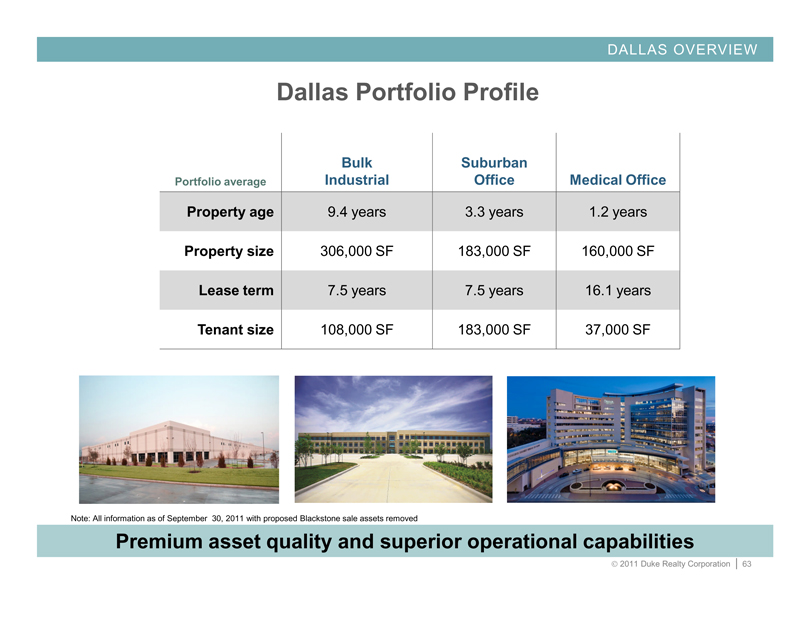

DALLAS OVERVIEW

Dallas Portfolio Profile

Portfolio average Bulk Industrial Suburban Office Medical Office

Property age 9.4 years 3.3 years 1.2 years

Property size 306,000 SF 183,000 SF 160,000 SF

Lease term 7.5 years 7.5 years 16.1 years

Tenant size 108,000 SF 183,000 SF 37,000 SF

Note: All information as of September 30, 2011 with proposed Blackstone sale assets removed

Premium asset quality and superior operational capabilities

© 2011 Duke Realty Corporation | 63

DALLAS OVERVIEW

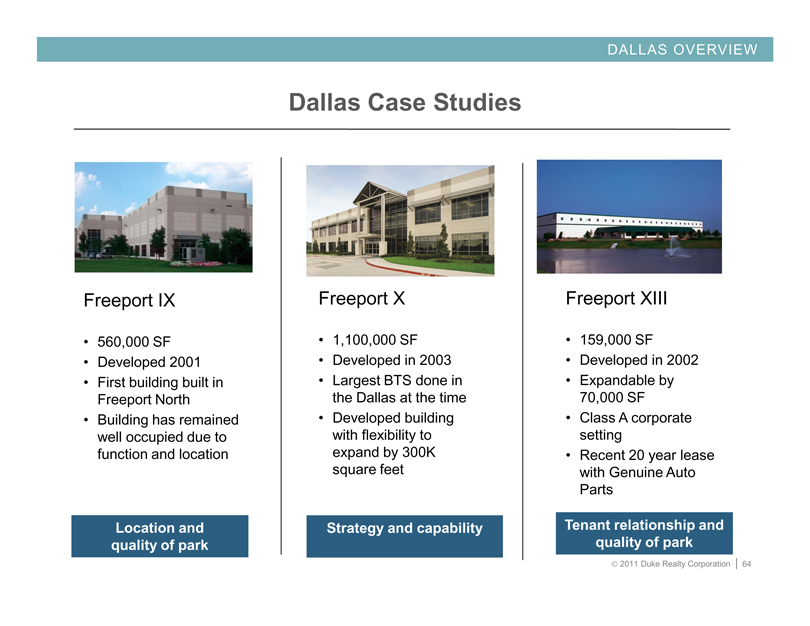

Dallas Case Studies

Freeport IX

• 560,000 SF

• Developed 2001

• First building built in Freeport North

• Building has remained well occupied due to function and location

Location and quality of park

Freeport X

• 1,100,000 SF

• Developed in 2003

• Largest BTS done in the Dallas at the time

• Developed building with flexibility to expand by 300K square feet

Strategy and capability

Freeport XIII

• 159,000 SF

• Developed in 2002

• Expandable by 70,000 SF

• Class A corporate setting

• Recent 20 year lease with Genuine Auto Parts

Tenant relationship and quality of park

© 2011 Duke Realty Corporation | 64

DALLAS OVERVIEW

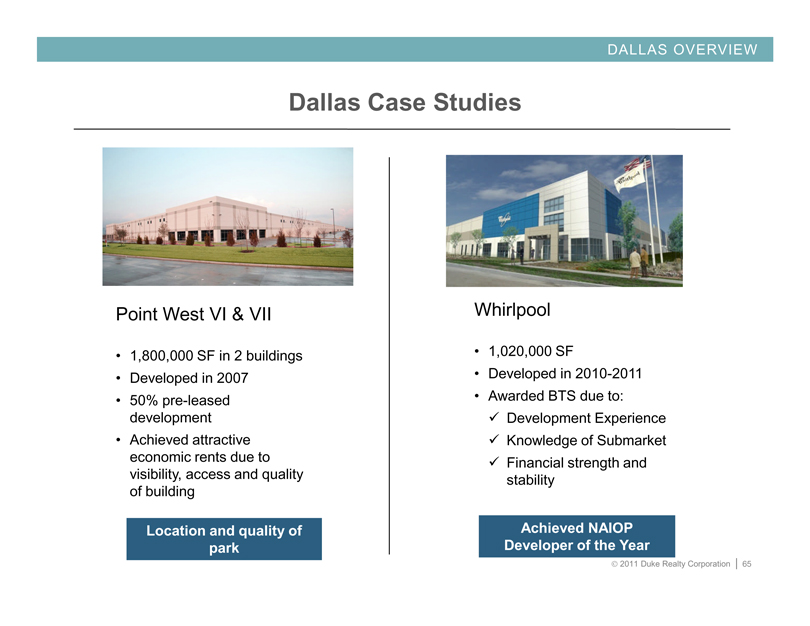

Dallas Case Studies

Point West VI & VII

• 1,800,000 SF in 2 buildings

• Developed in 2007

• 50% pre-leased development

• Achieved attractive economic rents due to visibility, access and quality of building

Location and quality of park

Whirlpool

• 1,020,000 SF

• Developed in 2010-2011

• Awarded BTS due to:ü Development Experienceü Knowledge of Submarketü Financial strength and stability

Achieved NAIOP Developer of the Year

© 2011 Duke Realty Corporation | 65

DALLAS OVERVIEW

Dallas Summary

þ Location: Strongest metro locations among larger owner peers

þ Quality: Newest, state of the art portfolio

þ Operations: Consistent operating performance and highly regarded team

Reputation:

Ability to execute with Duke management caliber and deep/ready access to capital

© 2011 Duke Realty Corporation | 66

CLOSING REMARKS

© 2011 Duke Realty Corporation | 67

OPERATIONS STRATEGY

New, High Quality Portfolio with Long-term Leases

Portfolio average Bulk Industrial Suburban Office Medical Office

Property age 10.4 years 13.0 years 2.5 years

Property size 215,000 SF 115,000 SF 106,000 SF

Lease term 7.0 years 7.2 years 11.7 years

Tenant size 70,000 SF 12,000 SF 10,000 SF

Premier portfolio of assets

Note: All information as of September 30, 2011 with proposed Blackstone sale assets removed

© 2011 Duke Realty Corporation | 68

RELIABLE. ANSWERS

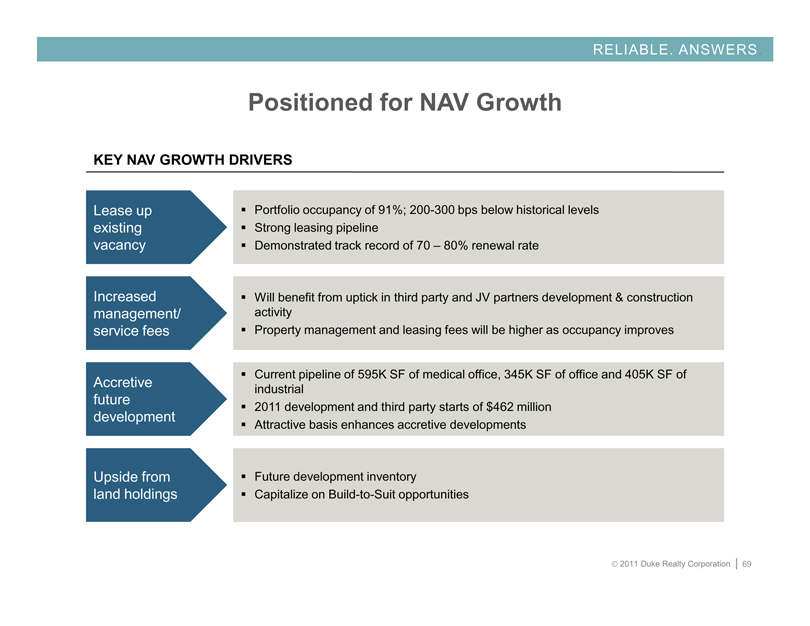

Positioned for NAV Growth

KEY NAV GROWTH DRIVERS

Lease up existing vacancy

Portfolio occupancy of 91%; 200-300 bps below historical levels Strong leasing pipeline Demonstrated track record of 70 – 80% renewal rate

Increased management/ service fees

Will benefit from uptick in third party and JV partners development & construction activity Property management and leasing fees will be higher as occupancy improves

Accretive future development

Current pipeline of 595K SF of medical office, 345K SF of office and 405K SF of industrial 2011 development and third party starts of $462 million Attractive basis enhances accretive developments

Upside from land holdings

Future development inventory

Capitalize on Build-to-Suit opportunities

© 2011 Duke Realty Corporation | 69

RELIABLE. ANSWERS

WHY DUKE REALTY?

Quality portfolio improving with asset strategy

Solid balance sheet improving with capital strategy

Unmatched ability to execute on daily operations

Development capabilities in place with existing land bank

Talent and leadership depth to execute

Delivering on what we say we will do

© 2011 Duke Realty Corporation | 70

APPENDIX

© 2011 Duke Realty Corporation | 71

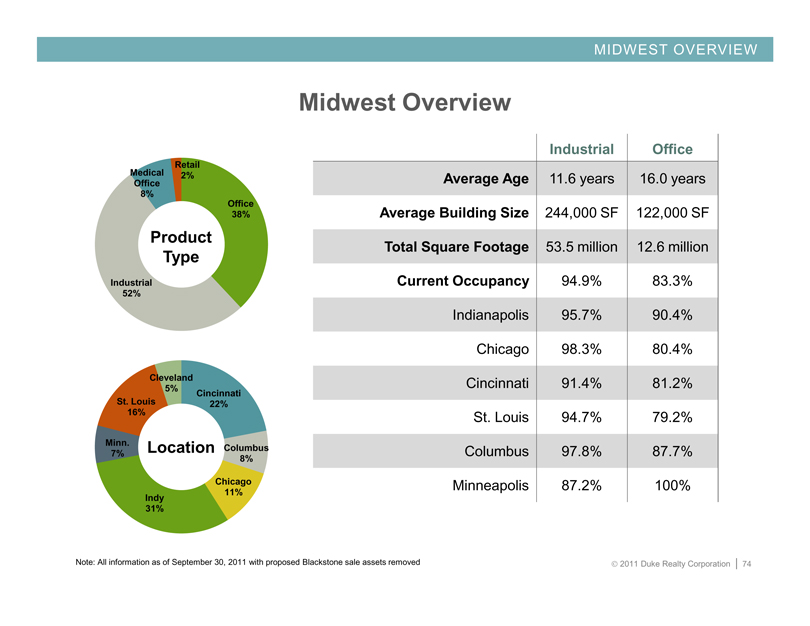

MIDWEST OVERVIEW

Performance Update

© 2011 Duke Realty Corporation | 72

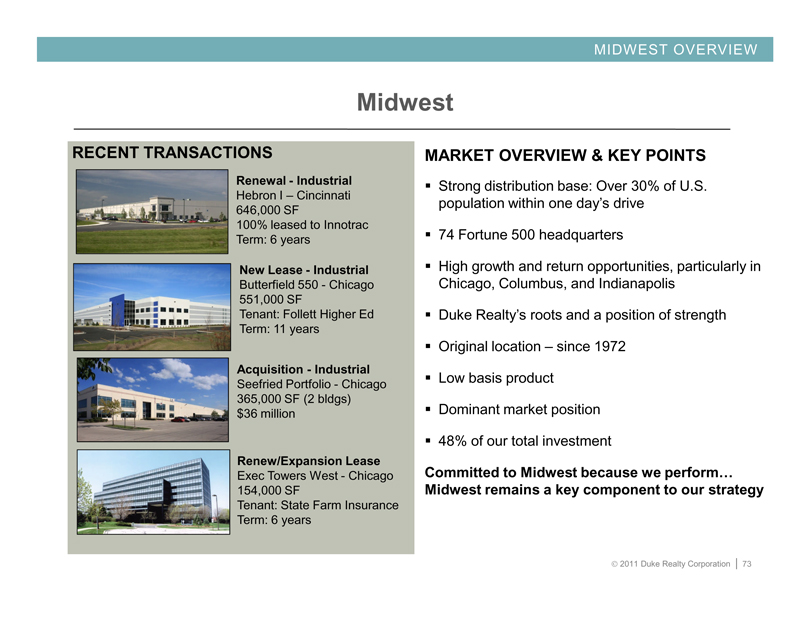

MIDWEST OVERVIEW

Midwest

RECENT TRANSACTIONS

Renewal - Industrial

Hebron I – Cincinnati 646,000 SF

100% leased to Innotrac Term: 6 years

New Lease - Industrial

Butterfield 550 - Chicago 551,000 SF

Tenant: Follett Higher Ed Term: 11 years

Acquisition - Industrial

Seefried Portfolio - Chicago 365,000 SF (2 bldgs) $36 million

Renew/Expansion Lease

Exec Towers West - Chicago 154,000 SF

Tenant: State Farm Insurance Term: 6 years

MARKET OVERVIEW & KEY POINTS

Strong distribution base: Over 30% of U.S. population within one day’s drive

74 Fortune 500 headquarters

High growth and return opportunities, particularly in Chicago, Columbus, and Indianapolis

Duke Realty’s roots and a position of strength Original location – since 1972 Low basis product Dominant market position 48% of our total investment

Committed to Midwest because we perform… Midwest remains a key component to our strategy

© 2011 Duke Realty Corporation | 73

MIDWEST OVERVIEW

Midwest Overview

Industrial Office

Average Age 11.6 years 16.0 years

Average Building Size 244,000 SF 122,000 SF

Total Square Footage 53.5 million 12.6 million

Current Occupancy 94.9% 83.3%

Indianapolis 95.7% 90.4%

Chicago 98.3% 80.4%

Cincinnati 91.4% 81.2%

St. Louis 94.7% 79.2%

Columbus 97.8% 87.7%

Minneapolis 87.2% 100%

Retail 2%

Office 38%

Industrial 52%

Medical Office 8%

Product Type

Cleveland 5%

Cincinnati 22%

Columbus 8%

Chicago 11%

Indy 31%

Minn. 7%

St. Louis 16%

Location

Note: All information as of September 30, 2011 with proposed Blackstone sale assets removed

© 2011 Duke Realty Corporation | 74

MIDWEST OVERVIEW

Midwest Focus

DOMINANT POSITION

BULK INDUSTRIAL

REDUCE OFFICE CONCENTRATION

Enhancing dominant industrial position in Midwest

© 2011 Duke Realty Corporation | 75

EAST & SOUTHEAST OVERVIEW

Performance Update

© 2011 Duke Realty Corporation | 76

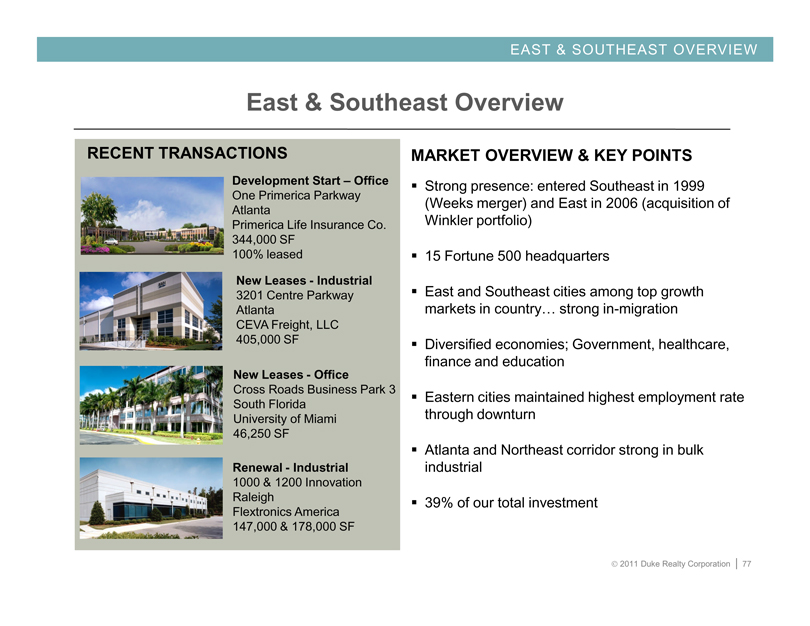

EAST & SOUTHEAST OVERVIEW

East & Southeast Overview

RECENT TRANSACTIONS

Development Start – Office

One Primerica Parkway Atlanta Primerica Life Insurance Co. 344,000 SF

100% leased

New Leases - Industrial

3201 Centre Parkway Atlanta CEVA Freight, LLC 405,000 SF

New Leases - Office

Cross Roads Business Park 3 South Florida University of Miami 46,250 SF

Renewal - Industrial

1000 & 1200 Innovation Raleigh Flextronics America 147,000 & 178,000 SF

MARKET OVERVIEW & KEY POINTS

Strong presence: entered Southeast in 1999 (Weeks merger) and East in 2006 (acquisition of Winkler portfolio)

15 Fortune 500 headquarters

East and Southeast cities among top growth markets in country… strong in-migration

Diversified economies; Government, healthcare, finance and education

Eastern cities maintained highest employment rate through downturn

Atlanta and Northeast corridor strong in bulk industrial

39% of our total investment

© 2011 Duke Realty Corporation | 77

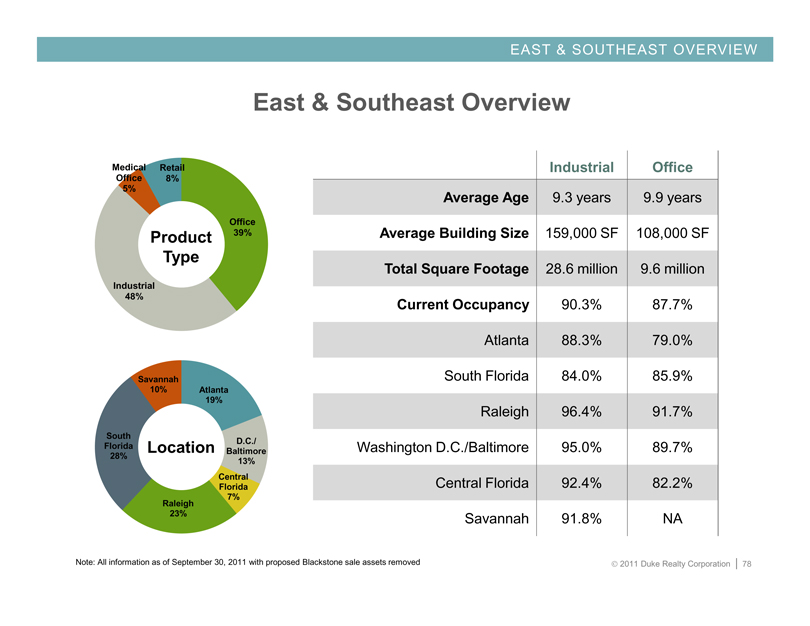

EAST & SOUTHEAST OVERVIEW

East & Southeast Overview

Industrial Office

Average Age 9.3 years 9.9 years

Average Building Size 159,000 SF 108,000 SF

Total Square Footage 28.6 million 9.6 million

Current Occupancy 90.3% 87.7%

Atlanta 88.3% 79.0%

South Florida 84.0% 85.9%

Raleigh 96.4% 91.7%

Washington D.C./Baltimore 95.0% 89.7%

Central Florida 92.4% 82.2%

Savannah 91.8% NA

Retail 8%

Office 39%

Industrial 48%

Medical Office 5%

Product Type

Atlanta 19%

D.C./ Baltimore 13%

Central Florida 7%

Raleigh 23%

South Florida 28%

Savannah 10%

Location

Note: All information as of September 30, 2011 with proposed Blackstone sale assets removed

© 2011 Duke Realty Corporation | 78

EAST & SOUTHEAST OVERVIEW

East & Southeast Focus

BULK INDUSTRIAL/PORTS

LEASE UP AND RENT GROWTH

ACQUISITIONS & DEVELOPMENT

Maximize assets and market position

© 2011 Duke Realty Corporation | 79

SOUTHWEST OVERVIEW

Performance Update

© 2011 Duke Realty Corporation | 80

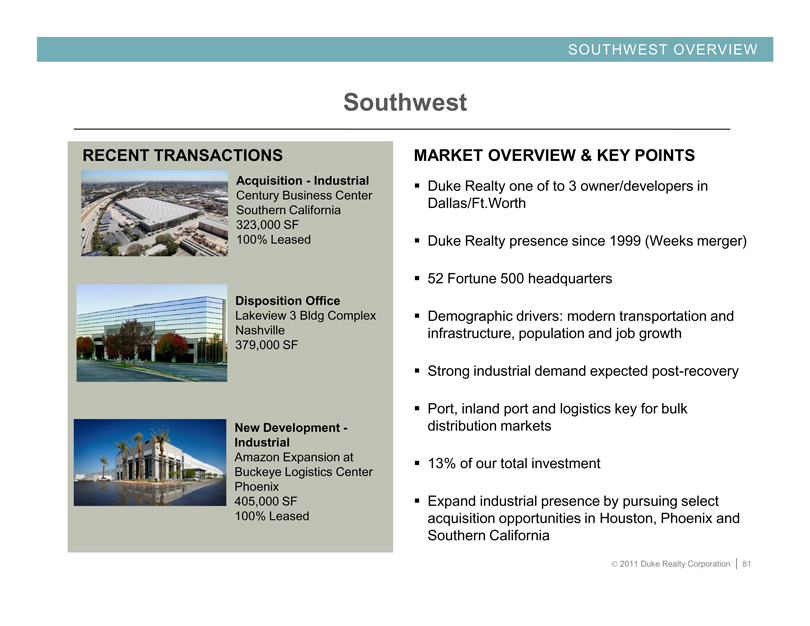

SOUTHWEST OVERVIEW

Southwest

RECENT TRANSACTIONS

Acquisition - Industrial

Century Business Center Southern California 323,000 SF

100% Leased

Disposition Office

Lakeview 3 Bldg Complex Nashville 379,000 SF

New Development - Industrial

Amazon Expansion at Buckeye Logistics Center Phoenix 405,000 SF

100% Leased

MARKET OVERVIEW & KEY POINTS

Duke Realty one of to 3 owner/developers in Dallas/Ft.Worth

Duke Realty presence since 1999 (Weeks merger)

52 Fortune 500 headquarters

Demographic drivers: modern transportation and infrastructure, population and job growth

Strong industrial demand expected post-recovery

Port, inland port and logistics key for bulk distribution markets

13% of our total investment

Expand industrial presence by pursuing select acquisition opportunities in Houston, Phoenix and Southern California

© 2011 Duke Realty Corporation | 81

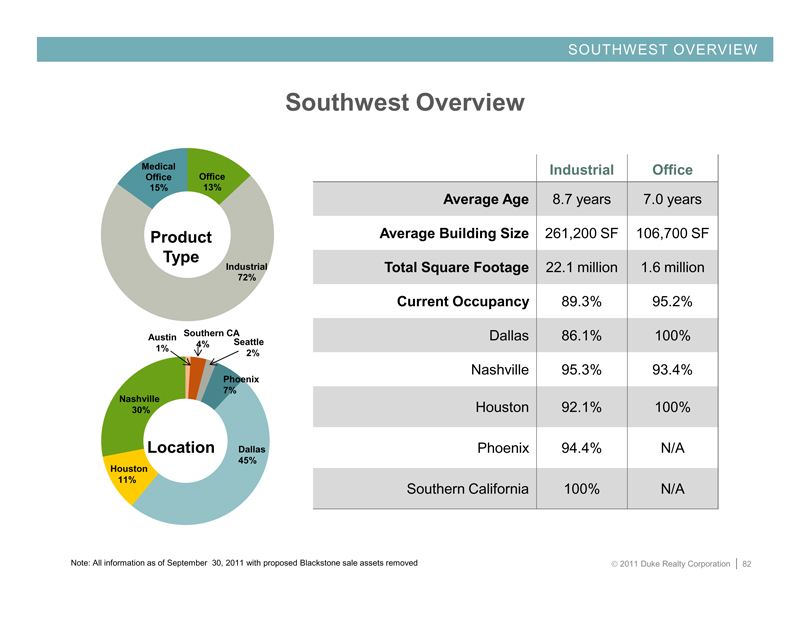

SOUTHWEST OVERVIEW

Southwest Overview

Office 13%

Industrial 72%

Medical Office 15%

Product Type

Southern 4%

CA Seattle 2%

Phoenix 7%

Dallas 45%

Houston 11%

Nashville 30%

Austin 1%

Location

Industrial Office

Average Age 8.7 years 7.0 years

Average Building Size 261,200 SF 106,700 SF

Total Square Footage 22.1 million 1.6 million

Current Occupancy 89.3% 95.2%

Dallas 86.1% 100%

Nashville 95.3% 93.4%

Houston 92.1% 100%

Phoenix 94.4% N/A

Southern California 100% N/A

Note: All information as of September 30, 2011 with proposed Blackstone sale assets removed

© 2011 Duke Realty Corporation | 82

SOUTHWEST OVERVIEW

Southwest Focus

DALLAS LEASE-UP

HOUSTON INDUSTRIAL PORT DALLAS INLAND PORT

SOUTHERN CALIFORNIA EXPANSION

Grow

© 2011 Duke Realty Corporation | 83

RELIABLE. ANSWERS

Forward-Looking Statement

This slide presentation contains statements that constitute “forward-looking statements” within the meaning of the Securities Act of 1933 and the Securities Exchange Act of 1934 as amended by the Private Securities Litigation Reform Act of 1995. These forward-looking statements include, among others, our statements regarding (1) strategic initiatives with respect to our assets, operations and capital and (2) the assumptions underlying our expectations. Prospective investors are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and that actual results may differ materially from those contemplated by such forward-looking statements. A number of important factors could cause actual results to differ materially from those contemplated by forward-looking statements in this slide presentation. Many of these factors are beyond our ability to control or predict. Factors that could cause actual results to differ materially from those contemplated in this slide presentation include the factors set forth in our filings with the Securities and Exchange Commission, including our annual report on Form10-K, quarterly reports on Form 10-Q and current reports on Form 8-K. We believe these forward-looking statements are reasonable, however, undue reliance should not be placed on any forward-looking statements, which are based on current expectations. We do not assume any obligation to update any forward-looking statements as a result of new information or future developments or otherwise.

© 2011 Duke Realty Corporation | 84