As Filed with the Securities and Exchange Commission on June 3, 2009

Registration Statement No. 333-_______

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

INTEGRATED FREIGHT SYSTEMS, INC.

(Exact name of registrant as specified in its charter)

FLORIDA

(State or other jurisdiction of incorporation or organization)

4213

(Primary Standard Industrial Classification Code Number)

26-2669164

(I.R.S. Employer Identification Number)

6371 Business Boulevard,

Suite 200

Sarasota, Florida 34240

1-888-623-4378

(Address, including zip code, and telephone number, including area code,

of registrant’s principal executive offices)

Paul A. Henley, President

Integrated Freight Systems, Inc.

6371 Business Boulevard

Suite 200

Sarasota, Florida 34240

1-888-623-4378

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copy to:

Jackson L. Morris

3116 W. North A Street

Tampa, Florida 33609-1544

Phone: 813-874-8854

Fax: 800-310-1695

E-mail: jackson.morris@rule144solution.com

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after the effective date of this registration statement.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

Large accelerated filer o Accelerated filer o Non-accelerated filer o Smaller reporting company x

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

o Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer)

o Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer)

CALCULATION OF REGISTRATION FEE

Title of each class of securities to be registered | Amount to be registered (4) | Proposed maximum offering price per unit (5) | Proposed maximum aggregate offering price | Amount of registration fee | |

Common stock, $0.001 par value per share (1) | 404,961 | $ | 0.57 | $ | 0.0014 | $ | 23.00 |

Common stock purchase warrants (2) | 404,961 | $ | 0 | $ | 0.00 | $ | |

Common stock, $0.001 par value per share (3) | 404,961 | $ | 0.50 | $ | 202,481 | $ | 12.00 |

| | | | | TOTAL | $ | 35.00 |

| | | | | | | | |

(1) Shares issuable in automatic replacement of shares of PlanGraphics, Inc. upon consummation of merger of PlanGraphics into the registrant. Includes a sufficient number of a additional shares to round up fractional shares or the next whole share.

(2) Warrants issuable with shares issuable in automatic replacement of shares of PlanGraphics, Inc. upon consummation of merger of PlanGraphics into the registrant.

(3) Shares issuable upon exercise of the warrants.

(4) Subject to increase for rounding up of fractional shares and common stock purchase warrants related thereto.

(5) The proposes maximum offering price per unit has been calculated in accordance with Rule 457(c) using the average of the high and low prices reported in the OTC Bulletin Board on May 28, 2009, or $0.12, multiplied by the reverse split ratio of 244.8598 to arrive at an equivalent post-reverse-split price per share.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

PRELIMINARY INFORMATION STATEMENT/PROSPECTUS SUBJECT TO

COMPLETION - DATED JUNE 3, 2009

Integrated Freight Systems, Inc.

Suite 200

6371 Business Boulevard

Sarasota, Florida 34240

Notice of Action by Written Consent to be taken June ____, 2009

TO: The Stockholders of PlanGraphics, Inc.

We Are Not Asking You For A Proxy.

You Are Requested Not To Send Us A Proxy.

A meeting will not be held. The actions described generally below will be approved by Integrated Freight Systems, Inc., as the majority stockholder of PlanGraphics, Inc.

Integrated Freight Systems, Inc., a Florida corporation, the majority stockholder of PlanGraphics, Inc., plans to approve the following proposals by written consent twenty days following the mailing of this information statement/prospectus to stockholders of PlanGraphics, Inc.

Proposal No. 1. A reverse split of PlanGraphics’ issued and outstanding common stock in a ratio of one to 244.8598, which will result in 404,961 shares issued and outstanding held by persons other Integrated Freight Systems.

Proposal No. 2. The sale of PlanGraphics’ operating subsidiary, PlanGraphics, Inc., a Maryland corporation, to John C. Antenucci, PlanGraphics’ current sole director and chief executive officer. In order to distinguish the two companies with the same name, the parent company is referred to as PlanGraphics and the subsidiary company is referred to as PGI.

Proposal No. 3. PlanGraphics’ merger into Integrated Freight Systems, which will result in the conversion of the 404,961 share of PlanGraphics’ common stock held by persons other than Integrated Freight Systems into 404,961 shares of Integrated Freight Systems common stock accompanied by the issue of 404,961 common stock purchase warrants to the persons holding the 404,961 shares.

This document is both (1) an information statement pursuant to Regulation 14C under the Securities Exchange Act of 1934 containing information about the three proposed actions set forth above which are to be approved by written consent of PlanGraphics’ majority stockholder and (2) a prospectus of Integrated Freight Systems with respect to its 404,961 shares of common stock into which the common stock of PlanGraphics will be automatically converted in the merger of PlanGraphics into Integrated Freight Systems, 404,961 common stock purchase warrants to accompany the converted common stock and the 404,961 shares of common stock issuable upon exercise of the common stock purchase warrants.

PlanGraphics’ common stock is quoted on the OTC Bulletin Board under the symbols PGRA. There is no public market for Integrated Freight Systems common stock. As a result of the planned merger of PlanGraphics into Integrated Freight Systems, in which Integrated Freight Systems will succeed to PlanGraphics’ registration pursuant to Section 12(g) of the Securities Exchange Act of 1934, it is expected that PlanGraphics trading symbol will be change to reflect its change of name to Integrated Freight Systems in the planned merger.

YOU SHOULD CAREFULLY CONSIDER THE RISK FACTORS BEGINNING ON PAGE 16.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR PASSED UPON

THE ADEQUACY OR ACCURACY OF THIS PROSPECTUS. ANY REPRESENTATION

TO THE CONTRARY IS A CRIMINAL OFFENSE.

This information statement/prospectus is dated June __, 2009 and is first being mailed to PlanGraphics’ stockholders on or about that date.

3

HOW TO OBTAIN A COPY OF INFORMATION INCORPORATED FROM OTHER SOURCES

This information statement/prospectus incorporates important business and financial information about PlanGraphics that is not included in or delivered with this information statement/prospectus. This information is available without charge to security holders upon written or oral request. Please contact Frederick G. Beisser, Chief Financial Officer, PlanGraphics, Inc., 112 East Main Street, Frankfort, KY 40601, telephone (502) 223-1501, to receive a copy of this information. Requests for this information will be honored for twenty days after the date of this information statement/prospectus. This information is also available on the Internet at www.plangraphics.com. See also, “Where You Can Find Additional Information About PlanGraphics”.

TABLE OF CONTENTS

| Page |

Parties to the Transactions | 5 |

Roadmap to the Transactions | 5 |

Dissenter’s Rights | 6 |

Persons Who Have an Interest in the Matters to be Acted Upon | 6 |

PlanGraphics’ Voting Securities and Principal Stockholders | 6 |

Integrated Freight Systems’ Recent Purchase of Control of PlanGraphics | 7 |

Events Leading Up to Integrated Freight Systems Purchase of Control of PlanGraphics | 8 |

Explanation of Proposals to be Approved by Integrated Freight Systems | 9 |

No Merger Agreement | 11 |

Accounting and Tax Matters | 11 |

Comparison of Stockholder Rights | 12 |

Documents Incorporated by Reference and Where You can Find Them | 13 |

Information about Integrated Freight Systems | 13 |

Summaries of Referenced Documents | 13 |

Forward–Looking Statements | 14 |

Integrated Freight Systems Discussion and Analysis of Results of Operations and Financial Condition | 14 |

Risk Factors | 16 |

Our Corporate History and Organization | 20 |

Our Business | 20 |

Our Management | 27 |

Biographical Information about Our Directors and Officers | 28 |

Compensation of Our Executive Officers | 30 |

Related Party Transactions | 31 |

Who Owns Our Common Stock | 31 |

Warrants We Have and Will Have Outstanding | 32 |

Lockup – Leak-out Agreements | 32 |

Description of Our Common Stock | 32 |

Legal Matters | 33 |

Experts | 33 |

Where You Can Obtain Additional Information and Exhibits | 33 |

Index to Financial Statements | 34 |

HOW TO OBTAIN MORE COPIES OF THIS INFORMATION STATEMENT/PROXY

Only one copy of this information statement/prospectus is being delivered to two or more stockholders who share the same address, unless we have previously received a request from a stockholder sharing the same address with another stockholder to deliver a copy for each stockholder. If you have not already made this request, we will upon your oral or written request promptly deliver another copy of this information statement/prospectus to you at the shared address, if you so desire. To receive your separate copy of the information statement/prospectus, you may call 941-545-7800 or you may send a request to Integrated Freight Systems, Inc., 200, 6371 Business Boulevard, Sarasota, Florida 34240, attn: Paul A. Henley, President. If you are already receiving multiple copies of PlanGraphics’ annual report, proxy statements and information statements at the shared address and would like to receive only one copy in the future, please either call (502) 223-1501 or you may send a request to PlanGraphics, Inc., 112 East Main Street, Frankfort, KY 40601, attn: Frederick G. Beisser, Chief Financial Officer.

4

PARTIES TO THE TRANSACTIONS

The two parties to the merger transaction described in this information statement/prospectus are:

• Integrated Freight Systems, Inc., a Florida corporation, with its principal executive offices located at Suite 200, 6371 Business Boulevard, Sarasota, Florida 34240. Its telephone number at that address is 941-545-7800. Integrated Freight Systems does not have a web site. Integrated Freight Systems is a holding company engaged in the motor freight industry.

• PlanGraphics, Inc., a Colorado corporation, with its principal executive offices located at 112 East Main Street, Frankfort, KY 40601. Its telephone number at that address is (502) 223-1501. Its web site address is www.plangraphics.com. PlanGraphics is a holding company engaged in full life-cycle systems integration and implementation providing a broad range of services in the design and implementation of information technology related to spatial information management in the public and commercial sectors.

ROADMAP TO THE TRANSACTIONS

The following is an explanation of all the transactions related to and of which the proposals described in this information statement/prospectus are a part:

• Integrated Freight Systems has acquired 401,559,467 shares, or 80.2 percent, of PlanGraphics issued and outstanding common stock.

• Integrated Freight Systems will approve a reverse stock split in a ratio of one share for each 244.8598 shares outstanding, with the result that PlanGraphics stockholders other than Integrated Freight Systems will own 404,961 shares and Integrated Freight Systems will own 1,639,716 shares.

• PlanGraphics will transfer all of its assets to PGI, its wholly owned subsidiary, which will assume essentially all of PlanGraphics liabilities, and Integrated Freight Systems will issue 177,170 shares of its common stock to PGI. Integrated Freight Systems will issue 134,852 shares of its common stock in payment of other liabilities of PlanGraphics that are owed principally to John C. Antenucci and Frederick G. Beisser for accrued compensation. The shares Integrated Freight Systems issues to PGI, Mr. Antenucci and Mr. Beisser will be accompanied by an equal number of common stock purchase warrants exercisable at a price of $0.50 for two years.

• Integrated Freight Systems will approve the sale of PGI to Mr. Antenucci.

• Integrated Freight Systems will approve the plan of merger described below pursuant to which PlanGraphics will be merged into Integrated Freight Systems, and cease to exist as a separate corporation.

• In the merger, the 404,961 issued and outstanding shares of PlanGraphics owned by stockholders other than Integrated Freight Systems will be converted automatically into 404,961 shares of Integrated Freight Systems and the issued and outstanding shares of PlanGraphics owned by Integrated Freight Systems will become treasury shares and be cancelled. In addition, Integrated Freight Systems will issue 404,961 non-transferable common stock purchase warrants to the former stockholders of PlanGraphics, excluding itself. The warrants will exercisable at a price of $0.50 per share for two years.

• Integrated Freight Systems will succeed to PlanGraphics' registration under Section 12(g) of the Securities Exchange Act of 1934.

In furtherance of the transactions outlined above, and to comply with the requirements of the Colorado Business Corporation Act, Integrated Freight Systems, as the majority stockholder of PlanGraphics, plans to approve by written consent the proposals set forth in the Notice to PlanGraphics Stockholder on the cover page. This approval will occur twenty days following the mailing of this information statement/prospectus to PlanGraphics stockholders.

5

Integrated Freight Systems believes that the transactions described above are in the best interest of PlanGraphics stockholders and its own stockholders. Integrated Freight Systems believes these transactions are essential to the achievement of greater market value per share than would be possible if PlanGraphics were to continue in its current business. PlanGraphics has advised that payment of cash for redemption of the preferred stock, as described below, would not have been possible, and the failure to redeem upon request would have caused PlanGraphics to be in default on this senior security and would have forced PlanGraphics to seek reorganization or liquidation in bankruptcy. Revenues from PlanGraphics continuing operations have been insufficient to sustain both the costs of its operations and the costs associated with being a registered and publicly traded company.

DISSENTER'S RIGHTS

PlanGraphics is incorporated in Colorado. PlanGraphics’ stockholders do not have dissenter’s rights arising from PlanGraphics’ planned merger into Integrated Freight Systems, under §7-113-102 of the Colorado Business Corporation Act because PlanGraphics has more than two thousand stockholders of record now and is expected to have at least two thousand stockholders of record on the date the action by written consent is to be taken by Integrated Freight Systems.

PERSONS WHO HAVE AN INTEREST IN THE MATTERS TO BE ACTED UPON

John C. Antenucci is now PlanGraphics’ sole director and its chief executive officer, but as a result of the merger he will hold no positions with the surviving company – Integrated Freight Systems. Mr. Antenucci has an interest in approval of the sale of PGI to him, as a result of which he will be the sole stockholder of PGI. As a result of this sale, PlanGraphics will cease to be in its current business. In satisfaction of deferred compensation due from PlanGraphics, Mr. Antenucci will also receive 59,327 shares of common stock and 59,327 common stock purchase warrants from Integrated Freight Systems in a transaction related to his purchase of PGI. The common stock purchase warrants will be exercisable for a two year period at a price of $0.50 per share. Mr. Antenucci’s vote as a director and as a stockholder is not required for approval of the sale of PGI to him, however, his approval is indicated by his agreement to purchase PGI and to enter into the other transactions described in this information statement/prospectus.

PLANGRAPHICS' VOTING SECURITIES AND PRINCIPAL STOCKHOLDERS

PlanGraphics’ issued and outstanding common stock is the only security it has that is entitled to vote or give consents on the proposals made by Integrated Freight Systems. PlanGraphics has 500,718,173 shares issued and outstanding on the date of this information statement/prospectus. Integrated Freight Systems believes that PlanGraphics does not intend to issue any additional shares prior to the date the action by written consent is to be taken by Integrated Freight Systems.

A vote in favor of or consent to the actions described in this information statement by a majority of the issued and outstanding shares of common stock is required for approval of these actions. Integrated Freight Systems owns 401,599,467 shares, or 80.2 percent, of PlanGraphics issued and outstanding common stock. Integrated Freight Systems is able and intends to approve the actions described in this information statement/prospectus without the vote or consent of any other holder of common stock. Integrated Freight Systems has proposed these actions and will give its consent in approval of them.

6

The following table identifies PlanGraphics’ principal stockholders, who include:

- each of PlanGraphics’ directors and executive officers,

- PlanGraphics’ directors and executive officers as a group, and

- others who own more than five percent of PlanGraphics’ common stock.

We believe each of these persons has sole voting and investment power over the shares they own, except as noted. The address of PlanGraphics’ directors and executive officers is PlanGraphics’ address.

| Number of Shares | |

Name | Before Reverse

Split | After Reverse Split | Percent |

John C. Antenucci, PlanGraphics’ sole director and chief executive officer | 12,655,025 | 51,683 | (1) | 2.53 | % |

Frederick G. Beisser, PlanGraphics’ chief financial officer | 1,479,900 | 6,044 | (2) | * | % |

Directors & executive officers as a group (2 persons) | 14,134,925 | 57,727 | | 2.82 | % |

Integrated Freight Systems, Inc. | 401,599,467 | 1,640,120 | | 80.20 | % |

Suite 200, 6271 Business Boulevard, Sarasota, FL 34240 | | |

(1) The pre and post-split number of shares includes 6,610,790 shares of common stock issuable pursuant to the exercise of options and 205,000 shares of common stock owned by Mr. Antenucci's spouse and minor child, for which he is deemed to be a beneficial owner. This table does not include shares of Integrated Freight Systems to be issued to Mr. Antenucci in transactions described in this information statement/prospectus.

(2) The pre and post-split number of shares includes 1,000,000 shares of common stock issuable pursuant to the exercise of options. This table does not include shares of Integrated Freight Systems to be issued to Mr. Beisser in transactions described in this information statement/prospectus.

PlanGraphics board of directors is not taking a position on any of the transactions that will be approved solely by Integrated Freight Systems acting as PlanGraphics controlling stockholder. Mr. Antenucci, in his capacity of the sole director of PlanGraphics, is not a disinterested party with respect to the sale of PGI to him.

INTEGRATED FREIGHT SYSTEMS' RECENT PURCHASE OF CONTROL OF PLANGRAPHICS

Integrated Freight Systems effectively acquired 401,599,467 shares of PlanGraphics’ common stock which now owns on May 18, 2009 by purchase and redemption of 500 shares of PlanGraphics’ preferred stock. PlanGraphics sold the preferred stock to Nutmeg/Fortuna Fund LLLP as described below. Integrated Freight Systems paid Nutmeg/Fortuna $167,000 in the form of its one-year promissory note and 1,307,822 shares of its common stock. As issued, PlanGraphics’ preferred stock, which was non-voting, was redeemable only for cash and not redeemable for common stock. Nutmeg/Fortuna made a request for redemption of the preferred stock, which PlanGraphics was obligated to honor by payment of cash for the principal amount of $500,000 plus accrued and unpaid dividends of $162,573.12 within sixty days following receipt of the request. Nutmeg/Fortuna Fund offered to accept shares of PlanGraphics common stock in lieu of cash, provided that the redemption could be made only by its transferee, which was to be Integrated Freight Systems. PlanGraphics issued its common stock in redemption of the preferred stock on June 2, 2009, resulting in Integrated Freight Systems acquiring control of PlanGraphics. Integrated Freight Systems has made the proposals described in the Notice to PlanGraphics Stockholders to complete several conditions subsequent to Integrated Freight Systems’ purchase and redemption of PlanGraphics’ preferred stock.

7

EVENTS LEADING TO INTEGRATED FREIGHT SYSTEMS’ PURCHASE OF CONTROL OF PLANGRAPHICS

PlanGraphics, its clients and primary market were detrimentally impacted by the attacks of September 11, 2001. Though work with a major customer continued during the response to the 9/11 attack and the ensuing recovery operations, the customer fell seriously behind in its payments to PlanGraphics, peaking in excess of at $2.5 million; the payments in arrears not being satisfied until December, 2003. The relatively limited working capital remaining after a previous rights offering was insufficient to sustain PlanGraphics while awaiting payment for the overdue amounts. As a consequence PlanGraphics was seriously stressed financially. The stress caused significant delays in meeting payroll and subcontractor payments, caused attrition among the professional and technical staff, required reduction of previous significant levels of sales and marketing activities and generated concerns in the market regarding PlanGraphics ability to service customers. PlanGraphics has not been able to recover from the stress point that caused constrained cash flows, delays in payroll and expense reimbursements.

As disclosed in its SEC filings, PlanGraphics retained the assistance of third party consultants and investment bankers beginning in 2001 and through 2007, seeking ways to create value for its stockholders through strategic initiatives or the sale to or merger of all or part of its organization with a third party. Discussions and negotiation with multiple firms were held during the intervening time period without success. To obtain relief from constrained cash flow exacerbated by increased cost of regulatory compliance, PlanGraphics sold 500 shares of mandatory redeemable preferred stock with a twelve percent cumulative dividend and a warrant exercisable for eighty percent of PlanGraphics’ common shares, among other terms, to the Nutmeg Group and its managed funds of Northbridge, Illinois for $500,000 on August 21, 2006. Nutmeg failed to exercise its control warrant before its expiration.

Even though PlanGraphics was unable to repay the preferred stock by February 17, 2007, Nutmeg did not request redemption as it was permitted to do. With the onset of the economic downturn and its impact on PlanGraphics' primary customer base of state and local governments, it became increasingly difficult to generate sufficient cash flow to meet the costs of PlanGraphics associated with its obligations to file reports with the SEC. In January 2009, PlanGraphics borrowed $30,000 from Nutmeg Group’s associated fund on a convertible debenture note for the purpose of paying its outside auditor for previous work and to initiate the review of its first quarter report on Form 10-Q. The debenture is convertible by the lender into common shares of PlanGraphics. PlanGraphics has been unable to pay the debenture according to its terms. PGI will assume the debenture in the transactions involving Integrated Freight Systems described in this information statement/prospectus.

In February 2009, Nutmeg Group introduced PlanGraphics to Integrated Freight Systems with the objective of creating a transaction that would both benefit Integrated Freight Systems and achieve greater value for the Nutmeg Group’s associated fund’s investment, together with all stockholders, in PlanGraphics. Negotiations among the parties has culminated in agreements for the transactions described in this information statement/prospectus. Nutmeg Group’s associated fund holding the preferred stock submitted a redemption request on May 15, 2009 for the cash redemption of the $500,000 principal of, plus accrued and unpaid dividends on, the preferred stock. The redemption request included an offer for redemption of the preferred stock and accrued and unpaid dividends by the issuance of PlanGraphics’ common stock, the number of shares to be determined by dividing the redemption amount by $0.0016, which represented the per share volume weighted average of the highest and lowest closing prices for the PlanGraphics’ common stock published by OTC Bulletin Board for the period of February 15 to April 15, 2009. This offer was preconditioned on the sale of the preferred stock to Integrated Freight Systems. Being unable to redeem the preferred stock for cash now or in the foreseeable future, if ever, PlanGraphics accepted the offer to redeem the preferred stock through the issuance of 401,599,467 shares of common stock to Integrated Freight Systems, subsequent to the Nutmeg Group’s associated fund’s sale of the preferred stock to Integrated Freight Systems.

8

EXPLANATION OF PROPOSALS TO BE APPROVED BY INTEGRATED FREIGHT SYSTEMS

PROPOSAL NO. 1.

A reverse split of PlanGraphics’ issued and outstanding common stock in a ratio of one to 244.8598.

The resolution to be approved by Integrated Freight Systems will cause a reduction in the 500,781,173 issued and outstanding shares of PlanGraphics to 2,044,918, subject to rounding up of each fractional share held by any stockholder to the next whole share. Holders of PlanGraphics common stock other than Integrated Freight Systems will hold 404,961 shares, subject to rounding up. The par value of the common stock and the total number of authorized shares will not be changed. All holders of common stock will be treated equally, nor will articles of amendment be required.

As noted above, Integrated Freight Systems believes the transactions described in this information statement/prospectus will increase stockholder value. Prior to the acquisition of PlanGraphics common stock by Integrated Freight Systems, all of PlanGraphics’ 99,158,706 shares of common stock had the following aggregate public market value:

$0.0024 | High price within the sixty day period prior to redemption | $237,981 |

$0.0017 | Weighted average price within the sixty day period prior to redemption | $168,570 |

$0.0012 | Price at May 29, 2009 | $118,990 |

| | | |

The post split value of the 404,961 shares held by PlanGraphics stockholders other than Integrated Freight Systems will have a post split equivalent market price of $0.57 per share. Following the merger described below, these stockholders will own two percent of Integrated Freight Systems and hold warrants entitling them to purchase 404,961 shares of Integrated Freight Systems’ common stock at a price of $0.50 per share for two years. Integrated Freight Systems believes that its operating performance will be better than PlanGraphics has achieved and could be expected to achieve in the foreseeable future. The reverse split is essential to completion of Integrated Freight Systems’ plan to become a registered, publicly traded company and provide greater value to all of its stockholders. There is, however, no assurance that the public market price for Integrated Freight Systems’ common stock will equal or exceed $0.57 per share.

Integrated Freight Systems has considered certain negative factors often associated with a reverse stock split. These factors included the negative perception of reverse stock splits held by some investors, analysts and other stock market participants; the fact that the stock price of some companies that have effected reverse stock splits has subsequently declined back to pre-reverse stock split levels; the adverse effect on liquidity that might be caused by a reduced number of shares outstanding and in the public float; and costs that may be associated with implementing a reverse stock split. Integrated Freight Systems believes that replacement of PlanGraphics’ business with the entirely new business of Integrated Freights Systems will partially or fully overcome these negative perceptions.

The effective date of the reverse split will be the date of approval by Integrated Freight Systems. At the effective date of the reverse split, the holders of record of PlanGraphics’ common stock would normally be able to exchange their old share certificates for share certificates representing the new number of shares resulting from the reverse split. New stock certificates for PlanGraphics will not be printed, however, and the exchange will be deferred until after the merger of PlanGraphics into Integrated Freight Systems, described in Proposal No. 3, below.

9

PROPOSAL NO. 2.

The sale of PlanGraphics’ operating subsidiary, PlanGraphics, Inc., a Maryland corporation, (PGI) to John C. Antenucci, PlanGraphics’ director and chief executive officer.

The resolution to be approved by Integrated Freight Systems will authorize the sale of PGI to Mr. Antenucci. PlanGraphics conducts all of its operations in PGI, which is also named PlanGraphics, Inc. The following are elements of the transfer of assets and sale of PGI to Mr. Antenucci.

| • | PlanGraphics will transfer all of its assets to PGI, excluding the stock PlanGraphics owns in PGI. |

| • | PGI will assume all of PlanGraphics’ debts and obligations, excluding $28,000 in auditing fees. |

| • | PlanGraphics will sell the stock of PGI to Mr. Antenucci. |

| • | Mr. Antenucci will pay for the stock of PGI by (1) relieving PlanGraphics from its obligation to make severance payments and forego any claim associated with the obligation pursuant to Mr. Antenucci’s Executive Employment Agreement, and (2) voluntarily terminating his Executive Employment Agreement. |

Transactions related to the sale of PGI to Mr. Antenucci are as follows:

| • | PGI will release PlanGraphics from all inter company loans and obligations in exchange for 177,170 shares of Integrated Freight Systems common stock and an equal number of common stock purchase warrants, exercisable for two years at a price of $0.50 per share. |

| • | Mr. Antenucci will release PlanGraphics from its obligation to pay deferred amounts and reimbursements and forego any claims associated therewith in exchange for 59,327 shares of Integrated Freight Systems common stock, an equal number of common stock purchase warrants, exercisable for two years at a price of $0.50 per share, and PGI maintaining tail coverage for three years under its directors and officers liability insurance. |

| • | Mr. Beisser will release PlanGraphics from all severance payments pursuant to his Executive Employment Agreement in exchange for 75,525 shares of Integrated Freight Systems common stock, an equal number of common stock purchase warrants, exercisable for two years at a price of $0.50 per share, and PGI maintaining tail coverage for three years under its directors and officers liability insurance. |

| • | PGI, Mr. Antenucci and Mr. Beisser will each enter into lockup and leak-out agreement with Integrated Freight Systems limiting the resale of its common stock into the public securities market. See “Description of Our Common Stock – Lockup – Leak-out Agreements”. |

The sale of PGI is an integral part of Integrated Freight Systems' plan to utilize PlanGraphics’ registration under Section 12(g) the Securities Exchange Act of 1934 as its vehicle to achieve its own registration under that act by succession to PlanGraphics’ registration and to obtain a public stockholder base with an existing public market. Integrated Freight Systems is engaged in the acquisition and operation of motor freight companies. Integrated Freight Systems does not want to be engaged in the business currently conducted by PlanGraphics. That current business has demonstrated, in the view of Integrated Freight Systems and PlanGraphics’ management, that it is not a suitable business, as it has been and will be conducted, for a registered, publicly traded company. Integrated Freight Systems believes the sale of PGI is in the best interest of PlanGraphics’ existing stockholders and its own stockholders because the sale, among other things described in this information statement/prospectus, eliminates PlanGraphics liabilities and obligations under executive employment agreements and essentially all other liabilities.

10

PROPOSAL NO. 3.

PlanGraphics’ merger into Integrated Freight Systems.

The resolution to be approved by Integrated Freight Systems will authorize the merger of PlanGraphics into Integrated Freight Systems, with the following outcome:

| • | The 404,961 shares of PlanGraphics common stock held by stockholders other than Integrated Freight Systems will be automatically converted into 404,961 shares, or two percent, of Integrated Freight Systems common stock subject to round up of fractional shares. |

| • | Integrated Freight Systems will simultaneous issue 404,961 non transferable common stock purchase warrants, one warrant for each share, to the former stockholders of PlanGraphics other than Integrated Freight Systems, each warrant exercisable for the purchase of one share of Integrated Freight Systems’ common stock at a price of $0.50 within two years. |

| • | The 401,559,467 shares of PlanGraphics owned by Integrated Freight Systems will become treasury stock and be cancelled. |

| • | Integrated Freight Systems will be the surviving corporation in the merger. |

| • | PlanGraphics will be the disappearing corporation in the merger. |

| • | The rights of PlanGraphics stockholders and the obligations and duties to them of the corporation in which they own stock following the merger will be governed by the Florida Business Corporations Act and not the Colorado Business Corporations Act. |

| • | Value of the shares the PlanGraphics stockholders continue to hold as converted into Integrated Freight Systems will depend on the operating performance of and other factors related to its business in motor freight transportation and not PlanGraphics’ current business. |

| • | Integrated Freight Systems will apply to FINRA for a new trading symbol, which will be publicly announced immediately following issuance. |

| • | Integrated Freight Systems will commence filing reports pursuant to §13 of the Securities Exchange Act of 1934, as the successor to PlanGraphics’ registration. |

The effective date of the merger will be the date on which articles of merger are filed in Colorado by PlanGraphics and in Florida by Integrated Freight Systems which is expected to occur simultaneously following the approval of the merger by written consent of Integrated Freight Systems. Immediately following the effective date of the merger, at a date to be announced, the holders of record of PlanGraphics’ common stock will be able to exchange their old PlanGraphics share certificates for Integrated Freight Systems share certificates representing the new number of shares ensuing from the reverse split and the merger.

NO MERGER AGREEMENT

No parties have entered into an agreement for the merger of PlanGraphics into Integrated Freight Systems. The merger will be a statutory merger under Colorado and Florida corporation law which Integrated Freight Systems will undertake by virtue of its controlling interest in PlanGraphics. A vote of Integrated Freight Systems’ stockholders under the Florida Business Corporation Act is not required because Integrated Freight Systems owns more than eighty percent of the voting securities of PlanGraphics. However, a vote or approval of PlanGraphics’ stockholders is required by the Colorado Business Corporation Act because Integrated Freight owns less than ninety percent of PlanGraphics voting securities.

ACCOUNTING AND TAX MATTERS

The merger of PlanGraphics into Integrated Freight will be treated under generally accepted accounting principles as a purchase of PlanGraphics by Integrated Freight Systems. The existing operations of PlanGraphics will be accounted for as discontinued operations.

11

Reverse Stock Split

The reverse split is intended to qualify as a tax free reorganization under §354 as described in §368(a)(1)(E), a “recapitalization”, of the Internal Revenue Code of 1986. The receipt of the new common stock ensuing from the reverse split, solely in exchange for the old common stock held prior to the reverse split is not expected to result in recognition of gain or loss to the stockholders. The aggregate tax basis of the post-split shares received in the reverse split (including any fraction of a new share deemed to have been received) will be the same as the stockholder’s aggregate tax basis in the pre-split shares. The holding period of the shares of common stock to be received in the reverse split will generally include the holding period of the pre-split shares.

Merger of PlanGraphics into Integrated Freight Systems

The merger is intended to qualify as a tax free reorganization pursuant to §354 as described in §368(a)(1)(A), a “statutory merger”, of the Internal Revenue Code of 1986. Neither Integrated Freight Systems nor PlanGraphics is expected to recognize any gain or loss in connection with the merger. The receipt of the new common stock of Integrated Freight Systems ensuing from the merger by PlanGraphics stockholders, solely in exchange for the old common stock of PlanGraphics held prior to the merger is not expected to result in recognition of gain or loss to the stockholders. The aggregate tax basis of the post-merger shares received in the merger will be the same as the stockholder’s aggregate tax basis in the pre-merger shares. The holding period of the shares of common stock to be received in the merger will generally include the holding period of the pre-merger shares.

The IRS may not agree with this tax treatment

No party has obtained a legal opinion regarding the federal income tax treatment of either the reverse stock split or the merger, nor has a ruling by the Internal Revenue Service been obtained. These views regarding the tax consequences of the reverse split and the merger are not binding upon the Internal Revenue Service or the courts, and there is no assurance that the Internal Revenue Service or the courts would accept the positions expressed above. The state and local tax consequences of the reverse split and the merger may vary significantly as to each stockholder, depending on the state in which such stockholder resides. Each PlanGraphics stockholder is encouraged to seek his or her own tax advice.

COMPARISON OF STOCKHOLDER RIGHTS

The rights of stockholders under the Colorado Business Corporation Act and under the Florida Business Corporation Act are equivalent.

12

DOCUMENTS INCORPORATED BY REFERENCE AND WHERE YOU CAN FIND THEM

PlanGraphics files reports with the U.S. Securities and Exchange Commission pursuant to Section 13 of the Securities Exchange Act of 1934. PlanGraphics’ annual report on Form 10-KSB for the year ended September 30, 2008, quarterly report on Form 10-Q for the six month period ended March 31, 2009, reports on Form 8-K filed on May 18, 2009 and on June 1, 2009 and all reports files subsequently thereto are incorporated herein by reference.

You may read and copy any reports and other materials filed by PlanGraphics with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site at which you may obtain all reports, proxy and information statements, and other information regarding PlanGraphics that it files with the SEC. The address of that web site is http://www.sec.gov. The above information is also available at www.plangaphics.com.

PlanGraphics’ existing operations will be discontinued as a result of the transfer of all of PlanGraphics' assets to PGI and the sale of PGI to Mr. Antenucci as described in “Roadmap to the Transactions” and elsewhere in this information statement/prospectus. Therefore information regarding those operations to be discontinued is deemed to be not material to the operations of Integrated Freight Systems following the merger of PlanGraphics into it and to the investment decision regarding the proposed merger, which Integrated Freight System has made.

INFORMATION ABOUT INTEGRATED FREIGHT SYSTEMS

In the remainder of this information statement/prospectus, “we”, “our” and “us" refer to Integrated Freight Systems and includes our wholly owned subsidiaries, Morris Transportation and Smith Systems Transportation.

SUMMARIES OF REFERENCED DOCUMENTS

This information statement/prospectus contains references to, summaries of and selected information from agreements and other documents. These agreements and documents are filed as exhibits to the registration statement of which this information statement/prospectus is a part. The summaries of and selected information from those agreements and other documents are qualified in their entirely by the full text of the agreements and documents, which you may obtain from the Public Reference Section of or online from the U.S. Securities and Exchange Commission. See “Where You Can Find Additional Information About Us And Exhibits” for instructions as to how to access and obtain this information. Whenever we make reference in this information statement/prospectus to any of our contracts, agreements or other documents, the references are not necessarily complete and you should refer to the exhibits attached to the registration statement of which this information statement/prospectus is a part for copies of the actual contract, agreement or other document.

13

FORWARD-LOOKING STATEMENTS

This information statement/prospectus contains forward-looking statements that involve risks and uncertainties. We may, in some cases, use words such as “project,” “believe,” “anticipate,” “plan,” “expect,” “estimate,” “intend,” “should,” “would,” “could,” “will,” or “may,” or other such words and use verbs in the future tense that convey uncertainty of future events or outcomes to identify these forward-looking statements. There are a number of important factors beyond our control that could cause actual results to differ materially from the results anticipated by these forward-looking statements. These important factors include those that we discuss in this information statement/prospectus under the caption “Risk Factors”, as well as elsewhere in this information statement/prospectus. You should read these factors and the other cautionary statements made in this information statement/prospectus as being applicable to all related forward-looking statements wherever they appear in this information statement/prospectus. If one or more of these factors materialize, or if any underlying assumptions prove incorrect, our actual results, performance or achievements may vary materially from any future results, performance or achievements expressed or implied by these forward-looking statements. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise.

INTEGRATED FREIGHT SYSTEMS DISCUSSION AND ANALYSIS OF RESULTS OF

OPERATIONS AND FINANCIAL CONDITION

Results of Operations and four month period ended December 31, 2008

For the four month period ended December 31, 2008, our pro forma consolidated results of operations reflect the inception period from the date of acquisition of our operating subsidiaries beginning on September 1 through December 31, 2008.

• | Revenues were $6,586,581 |

| |

• | Net loss was $(619,574) |

| |

• | Net loss per diluted share was $(0.05) |

Our industry has been facing significant challenges due to weak demand for transportation and pricing competition.

During this period, price competition has remained intense during the quarter, and we have experienced a high level of bid activity in the quarter. This activity has now tapered off to a more normal pace. While we do not underestimate the pricing challenges ahead of us, we believe our model provides us with the flexibility to respond appropriately in this environment.

Results of Operations for four month period ended December 31, 2008

Revenues | $ 6,586,581 |

Operating Expenses | 6,986,729 |

Income before other operating expenses | (400,148) |

Interest and other (expenses)/income net | (213,830) |

Minority interest in subsidiary | (5,596) |

Net loss to shareholders net of minority interest in subsidiary | (619,574) |

Weighted average shares outstanding | 11,673,176 |

Net loss per fully diluted share | $ (0.05) |

Liquidity and Capital Resources

The growth of our business will continue to require, a significant investment in new revenue equipment. Our primary source of liquidity in the near term will be funds provided by investment and limited internally generated cash flow.

We generated significant cash flow from operations during the first quarter of 2008. Net cash provided by operating activities was $513,845. Depreciation and amortization accounted for $748,794 of non cash expenses. Net cash provided by investment activities was $673,028.

14

Net cash used in financing activities was approximately $1.14 million for the four months ended December 31, 2008. The decrease in cash used in financing activities is primarily due to repayment of long term debt.

Shareholder equity for the consolidated companies was $683,417.

We will continue to have significant capital requirements over the long-term, which may require us to incur debt or seek additional equity capital. The availability of additional capital will depend upon prevailing market conditions, the market price of our common stock, and several other factors over which we have limited control, as well as our financial condition and results of operations. Nevertheless, based on our recent operating results, current cash position, anticipated future cash flows, and sources of financing that we expect will be available to us, we do not expect that we will experience any significant liquidity constraints in the foreseeable future.

Critical Accounting Policies and Estimates

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires that management make a number of assumptions and estimates that affect the reported amounts of assets, liabilities, revenue, and expenses in our consolidated financial statements and accompanying notes. Management bases its estimates on historical experience and various other assumptions believed to be reasonable. Although these estimates are based on management's best knowledge of current events and actions that may impact us in the future, actual results may differ from these estimates and assumptions. Our critical accounting policies are those that affect, or could affect our financial statements materially and involve a significant level of judgment by management. The accounting policies we deem most critical to us include, revenue recognition, depreciation, claims accrual, accounting for income taxes and share based payments. There have been no significant changes to our critical accounting policies and estimates during the four months ended December 31, 2008.

15

Controls and Procedures

Regulation S-K - Item 4T CONTROLS AND PROCEDURES

307 – Disclosure controls and procedures: As of the quarter ended December 31, 2008, we did not carry out an evaluation of the effectiveness of our disclosure controls and procedures, with the participation of our principal executive and principal financial officers, because we were not a registered company at that time. Disclosure controls and procedures are defined in Exchange Act Rule 15d–15(e) as “controls and other procedures of an issuer that are designed to ensure that information required to be disclosed by the issuer in the reports that it files or submits under the Act (15 U.S.C. 78a et seq.) is recorded, processed, summarized and reported, within the time periods specified in the Commission's rules and forms and include, without limitation, controls and procedures designed to ensure that information required to be disclosed by an issuer in the reports that it files or submits under the Act is accumulated and communicated to the issuer's management, including its principal executive and principal financial officers, or persons performing similar functions, as appropriate to allow timely decisions regarding required disclosure.” If we had undertaken such evaluation, our president/chief executive officer would have concluded that, as of December 31, 2009, such disclosure controls and procedures were not effective. We did not have a chief financial officer at that date.

308T(b) – Changes in internal control over financial reporting: We did not have any nor did we adopt or make any changes to internal control over financial reporting during the quarter ended December 31, 2009.

Limitations on the Effectiveness of Internal Control: Our management does not expect that our disclosure controls and procedures or our internal control over financial reporting, when adopted, will necessarily prevent all fraud and material errors. An internal control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of the inherent limitations on all internal control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty, and that breakdowns can occur because of simple error or mistake. Additionally, controls can be circumvented by the individual acts of some persons, by collusion of two or more people, and/or by management override of the control. The design of any system of internal control is also based in part upon certain assumptions about risks and the likelihood of future events, and there is no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Over time, controls may become inadequate because of changes in circumstances and the degree of compliance with the policies and procedures may deteriorate. Because of the inherent limitations in a cost-effective internal control system, financial reporting misstatements due to error or fraud may occur and not be detected on a timely basis.

RISK FACTORS

In addition to the forward-looking statements outlined previously in this information statement/prospectus and other comments regarding risks and uncertainties included in the description of our business, the following risk factors should be carefully considered when evaluating our business. Our business, financial condition or financial results could be materially and adversely affected by any of these risks. The following risk factors do not include factors or risks which apply to or may be experienced by motor freight companies in general or which arise or result from general economic conditions.

16

The terms of our amended secured acquisition notes enable the stockholders of the acquired companies to recover their companies if we default on our obligations.

The amended promissory notes we have given to the purchase both of our subsidiary companies we have acquired are secured by a pledge of the stock in the acquired companies. In the event of our breach of the promissory notes, the persons from whom we acquired the companies may realize on the collateral and recover their ownership of our subsidiary companies. Our breach of the promissory notes and the resulting loss of our operating subsidiaries would have a material adverse effect on our business. If this were to occur, we would have either a material reduction in our business or we would not have any business. Events of default include:

| • | Failure to make timely payments on the amended notes and other amounts; |

| • | Failure to refinance certain equipment loans such that personal guaranties are eliminated; and |

| • | Failure to achieve a public market for our common stock; and |

| • | Performance of other obligations. |

The time period after which each of the foregoing events of default become defaults are subject to extension by mutual agreement between the persons from whom we have acquired the companies and us. There is no assurance we will be able to prevent one or more of these events of default from occurring. See “Our Business – Terms of Our Acquisitions”.

We may experience difficulty in combining and consolidating the management and operations of our acquired companies which could have a material adverse impact on our operations and financial performance.

We have purchased our operating subsidiaries and expect any additional subsidiaries we purchase to be made from the founders and management of the acquired companies, all of whom have been responsible for their own businesses and methods of operations as independent business owners. While these individuals will continue to be responsible to a degree for the continuing operations of our operating subsidiaries, we intend to centralize and standardize many areas of operations. Notwithstanding that many of these individuals from whom we have and plan to acquire our operating subsidiaries will serve on our board of directors, we may be unable to develop a cohesive corporate culture in which these individuals will be willing to forego their former independence. Our inability to successfully combine and consolidate the policies, procedures and operations of our subsidiaries can be expected to have a material adverse effect on our business and prospects, financial and otherwise.

If we are unable to successfully execute our growth strategy, our business and future results of operations may suffer.

Our growth strategy includes the acquisition of additional motor freight companies to increase revenues, to selectively expand our geographic footprint and to broaden the scope of our service offerings. If we are unable to acquire additional motor freight companies at prices that meet our financial model, our growth will be limited to expanding sales and reducing expenses in our existing subsidiaries.

We are significantly dependent on the continued services of Paul A. Henley to realize our growth strategy.

We are dependent upon the vision and efforts of Mr. Henley, our founder and principal stockholder, for the realization of our growth strategy. In the event Mr. Henley’s services were to be unavailable to us, our continued activity to expand our business operations through acquisition could be substantially impaired or be abandoned.

17

Our management owns more than a majority of our outstanding common stock and outside stockholders will be unable to influence management decisions or elect their nominees to our board of directors, if they should so desire.

Our management will control 62.05 percent and 58.19 percent, respectively before and after the merger and including the issue of 600,000 shares to one of our directors and officers in the event of conversion of a secured promissory note, of our issued and outstanding common stock following the completion of the merger with PlanGraphics described in this information statement/prospectus. All corporate actions involving amendment of our articles of incorporation (such as name change and increase in authorized shares), election of directors and other extraordinary actions and transactions such as certain mergers, consolidations and recapitalizations and sales of all or substantially all of our assets, require the approval of only a majority of the issued and outstanding shares of our common stock. Accordingly, our management will be able to approve any such actions and transactions and elect all directors even if all of the outside stockholders oppose such transactions, or in the case of directors, nominate other persons for election. Outside, minority stockholders will be unable to effect changes in our management or in our business.

We have significant ongoing cash requirements and expect to incur additional cash requirements that could limit our growth and adversely affect our profitability if we are unable to obtain sufficient financing.

Our business is capital intensive, involving the frequent purchase of new power units and trailers. In addition, we have issued and expect to continue issuing promissory notes for the cost of acquisitions. Due to the existing uncertainty in the capital and credit markets, capital and loans may not be available on terms acceptable to us. If we are unable in the future to generate sufficient cash flow from operations or borrow the necessary capital to fund our operations and acquisitions, we will be forced to operate our equipment for longer periods of time and to limit our growth, which could have a material adverse effect on our operating results. In addition, our business has significant operating cash requirements. If our cash requirements are high or our cash flow from operations is low during particular periods, we may need to seek additional financing, which may be costly or difficult to obtain. If any of the financial institutions that have extended credit commitments to us are or continue to be adversely affected by current economic conditions and disruption to the capital and credit markets, they may become unable to fund borrowings under their credit commitments or otherwise fulfill their obligations to us, which could have a material and adverse impact on our financial condition and our ability to borrow additional funds, if needed, for working capital, capital expenditures, acquisitions and other corporate purposes.

We derive twenty-five percent of our revenue from four customers, the loss of one or more of which could have a material adverse effect on our business.

For the period ended December 31, 2008, our top four customers, based on revenue, accounted for approximately twenty-five percent of our revenue. A reduction in or termination of our services by one or more of our major customers could have a material adverse effect on our business and operating results. A default in payments of invoices by one or more of these customers could have a material adverse effect on our financial condition. See “Our Business – Our customers and marketing”.

Our operations are subject to various environmental laws and regulations, the violation of which could result in substantial fines or penalties.

We are subject to various federal, state and local environmental laws and regulations dealing with the handling and transportation of hazardous materials ("hazmat") and waste ("hazwaste") (which is a material portion of our existing business). We operate in industrial areas, where truck terminals and other industrial activities are located, and where groundwater or other forms of environmental contamination have occurred. Our operations involve the risks of fuel spillage or seepage, environmental damage and hazardous waste disposal, among others. If a spill or other accident involving fuel, oil or hazardous substances occurs, or if we are found to be in violation of applicable laws or regulations, it could have a material adverse effect on our business and operating results. One of our subsidiaries specializes in transport of hazardous materials and waste. If we should fail to comply with applicable environmental laws and regulations, we could be subject to substantial fines or penalties, to civil and criminal liability and to loss of our licenses to transport the hazardous materials and waste. Under certain environmental laws, we could also be held responsible for any costs relating to contamination at our past facilities and at third-party waste disposal sites. Any of these consequences from violation of such laws and regulations could be expected to have a material adverse effect on our business and prospects, financial and otherwise.

18

The Environmental Protection Agency has issued regulations that require progressive reductions in exhaust emissions from diesel engines through 2010. These regulations are expected to result in higher prices for power units and increased fuel and maintenance costs, and there is no assurance that continued increases in pricing or costs will not have an adverse effect on our business and operations.

Our information management systems are diverse, may prove inadequate and may be difficult to integrate or replace.

We depend upon our information management systems for many aspects of our business. Each company we acquire will have its own information management system with which its employees are acquainted. None of these systems may be adequate to our consolidated operations and may not be compatible with a centralized information management system. We expect to require additional software to initially integrate existing systems or to ultimately replace these diverse systems. Switching to new information management systems is often difficult, resulting in disruption, delays and lost productivity, which could impact our dispatching, collections and other operations. Our business will be materially and adversely affected if our information management systems are disrupted or if we are unable to improve, upgrade, integrate, expand or replace our systems as we continue to execute our growth strategy.

Increases in driver compensation or difficulty in attracting drivers could affect our profitability and ability to grow.

In recent years, the transportation industry has experienced substantial difficulty in attracting and retaining qualified drivers, including independent contract drivers. With increased competition for drivers, we could experience greater difficulty in attracting sufficient numbers of qualified drivers. In addition, due in part to current economic conditions, including the cost of fuel and insurance, the available pool of independent contractor drivers is smaller than it has been historically. Accordingly, we may and periodically do face difficulty in attracting and retaining drivers for all of our current tractors and for those we may add. We may face difficulty in increasing the number of our independent contractor drivers. In addition, our industry suffers from high turnover rates of drivers. Our turnover rate requires us to recruit a substantial number of drivers. Moreover, our turnover rate could increase. If we are unable to continue to attract drivers and contract with independent contractors, we could be required to continue adjusting our driver compensation package beyond the norm or let equipment sit idle. An increase in our expenses or in the number of power units without drivers could materially and adversely affect our growth and profitability. Our operations may be affected in other ways by a shortage of qualified drivers in the future, such as temporary under-utilize our fleet and difficulty in meeting shipper demands. If we encounter difficulty in attracting or retaining qualified drivers, our ability to service our customers and increase our revenue could be adversely affected.

Interest Rate Risk

We are subject to interest rare risk to the extent we borrow against our line of credit or incur debt in the acquisition of revenue equipment or otherwise. We attempt to manage our interest rate risk by managing the amount of debt we carry. We did not have any debt outstanding at March 31, 2009, and therefore had no market risk related to debt.

Commodity Price Risk

We also are subject to commodity price risk with respect to purchases of fuel. The price and availability of diesel fuel can fluctuate due to market factors that are beyond our control. We believe fuel surcharges are effective at mitigating most, but not all, of the risk of high fuel prices because we do not recover the full amount of fuel price increases. As of December 31, 2008, we did not have any derivative financial instruments to reduce our exposure to fuel price fluctuations.

19

"Penny stock” rules may make buying and selling our common stock difficult.

Trading in our securities is expected to be subject, at least initially, to the "penny stock" rules. The SEC has adopted regulations that generally define a penny stock to be any equity security that has a market price of less than $4.00 per share, subject to certain exceptions, none of which apply to our common stock. These rules require that a broker-dealer who recommends our common stock to persons other than its existing customers and accredited investors, must, prior to the sale:

| • | Make a suitability determination prior to selling a penny stock to the purchaser; |

| • | Receive the purchaser's written consent to the transaction; |

| • | Provide certain written disclosures to the purchaser; |

| • | Deliver a disclosure schedule explaining the penny stock market and the risks associated with trading in the penny stock market; |

| • | Disclose commissions payable to both the broker-dealer and the registered representative; and |

| • | Disclose current quotations for the common stock. |

The additional burdens imposed upon broker-dealers by these requirements may discourage broker-dealers from effecting transactions in our common stock, which could severely limit the market price and liquidity of our common stock. These requirements may restrict the ability of broker-dealers to sell our common stock and may affect your ability to resell our common stock.

OUR CORPORATE HISTORY AND ORGANIZATION

We were incorporated in Florida on May 13, 2008 by Paul A. Henley, our founder, a director and our chief executive officer. We intend to change our name to Integrated Freight Corporation before the completion of the merger with PlanGraphics, described above.

Mr. Henley founded us for the purpose of acquiring one or more operating motor freight companies. We acquired our existing business in the fall of 2008 by purchase of two, well established motor freight carriers. The following table presents information about these acquisitions.

Company Name | Year Established | Acquisition Date |

Morris Transportation, Inc. | 1998 | As of September 1, 2008 |

Smith Systems Transportation, Inc. | 1992 | As of September 1, 2008 |

We are operating these subsidiaries as independent companies under the management of their founders and stockholders from whom we purchased them. We expect this management arrangement to continue while we gradually combine and consolidate the elements of their operations that are duplicative.

The address of our executive offices is Suite 200, 6371 Business Boulevard, Sarasota, Florida 34240 and our telephone number at that address is 941-545-7800. We do not have a web site.

OUR BUSINESS

Overview

We are a small motor freight company providing truck load service primarily in two markets in the mid-West United States. We do not specialize in any specific types of freight or commodities. We carry dry freight, refrigerated freight and hazmat and hazwaste (hazardous materials and waste). We provide long-haul, regional and local service to our customers.

20

Our Strategy

Truck transportation in general has suffered during the current economic recession. Over 3,000 trucking companies are believed to have ceased operations in 2008. We believe the trucking companies that have survived in the current economic recession, whether presently profitable or marginally unprofitable, represent good future value at the prices for which we believe many of them can be acquired. Many of them will not survive longer without debt and equity funding and cost reductions which they are unlikely to obtain individually. When our economy recovers, we believe that the demand for truck transportation services will return to pre recession levels, with an initially inadequate supply of trucks to meet demand. When the economic recovery occurs, which we cannot predict, we believe we will be well positioned to fill part of the demand for over-the-road freight services.

We intend to continue acquiring well established trucking companies when we can do so at prices which we deem to be advantageous. In the alternative, we may acquire assets. We also plan to expand our service offerings through acquisitions into logistics, brokering, less than a load and expedite/just-in-time services, as opportunities are presented to us.

We believe that we can achieve savings in operating costs by centralizing certain common functions of our subsidiaries, such as fuel and tire purchasing, billing and collections, dispatching, maintenance scheduling and other functions. We believe that with a larger service territory and customer base than any one subsidiary would have working alone, we will be able to achieve greater efficiencies in route and equipment utilization.

Our Markets

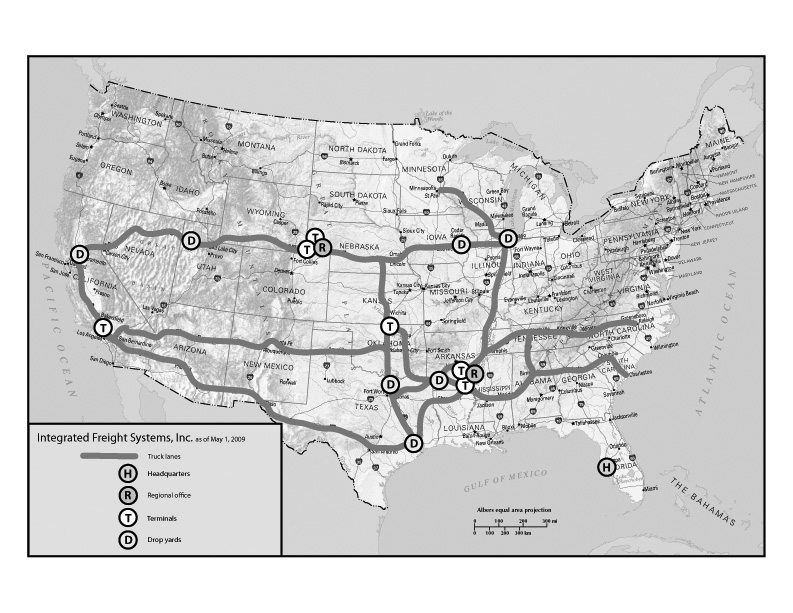

Historically our subsidiary companies have operated in well-established geographic traffic lanes. These lanes are defined by our customers’ distribution patterns. Because there is some overlap within the most heavily traveled lanes, especially between points in the upper Midwest and Texas, management believes that it will continue to realize increased cost and productivity improvements.

The following map displays information about our most traveled lanes.

Our Customers and Marketing

We serve approximately 175 customers on a regular basis. The following table presents information regarding our relationship with our customers. Although we do not have contracts with any of these customers, we have long-standing relationships with most of them.

The following table presents information regarding the percentage-of-revenue concentration of the business with our customers.

Four customers | Up to 25% |

All other customers | 75% or more |

The following table presents information regarding the average length of our trips.

Longest haul (overnight) | 1,950 miles |

Shortest haul | 175 miles |

Average haul | 850 miles |

21

Ninety-eight percent of the freight we haul is dry van freight. The following table presents information regarding the approximate percentage makeup of the freight we haul.

Forest and paper products | 38% |

Hazmat and hazwaste | 39% |

All other freight (freight of all kinds – FAK) | 23% |

Marketing

Mr. Morris, Mr. Smith and one sales person specializing in hazmat and hazwaste constitute our sales and marketing force. We have no formal marketing plan at the present time. We attend relevant trade shows and trade association meetings, and seek to maintain good relations with our existing customers. As we grow our carrier base, of which there is no assurance, we plan to establish a central marketing group that will support the sales and customer service efforts of each subsidiary.

Our People

We believe our employees are our most important asset. The following table presents information about our employees.

Drivers - company | 75 |

Drivers – independent contract* | 48 |

Platform and warehouse | 2 |

Fleet technicians | 6 |

Dispatch | 6 |

Sales | 1 |

Office | 3 |

Administrative and Executive | 5 |

*This is an average number. The number of our contract drivers, who typically own or lease from third parties the tractors they drive, varies depending on our needs. The maximum number of contract drivers we employed during 2008 was a medium of forty-six, with a variance of plus or minus three.

None of our employees are represented by a collective bargaining unit. We consider relations with our employees to be good. We offer basic health insurance coverage to all employees.

Our Drivers

We believe that maintaining a safe and productive professional driver group is essential to providing excellent customer service and achieving profitability. All of our drivers must have three years of verifiable driving experience, a hazmat endorsement (if hauling hazmat), no major violation in the previous thirty-six months and comply with all requirements of employment by federal Department of Transportation and applicable state laws.

As of December 31, 2008, seven of our drivers have driven more than one million miles two of our drivers have driven more than two million miles for us without a preventable accident.

We select drivers, including independent contractors, using our specific guidelines for safety records, driving experience, and personal evaluations. We maintain stringent screening, training, and testing procedures for our drivers to reduce the potential for accidents and the corresponding costs of insurance and claims. We train new drivers in all phases of our policies and operations, as well as in safety techniques and fuel-efficient operation of the equipment. All new drivers also must pass DOT required tests prior to assignment to a vehicle.

22

We primarily pay company-employed drivers a fixed rate per mile. The rate increases based on length of service. Drivers also are eligible for bonuses based upon safe, efficient driving. We pay independent contractors on a fixed rate per mile. Independent contractors pay for their own fuel, insurance, maintenance, and repairs.

Competition in the trucking industry for qualified drivers is normally intense. Our operations have been impacted, and from time-to-time we have experienced under-utilization and increased expense, as a result of a shortage of qualified drivers. We place a high priority on the recruitment and retention of an adequate supply of qualified drivers. Our average annual turn-over rate is less than thirty percent, compared to an industry average of sixty percent.

Our Operations

We currently conduct all of our freight transportation operations, including dispatch and accounting functions, from the headquarters facilities of our operating subsidiaries, using different information management systems and personnel that were employed when acquired our operating subsidiaries. These arrangements produce many overlaps and duplications in facilities, office systems and personnel. We believe that these operating arrangements provide less than optimal results. We intend to centralize many of these functions, as noted above. Centralization is subject to obtaining adequate internal or external financing, of which there is no assurance.

Our Revenue Equipment

The following table presents information regarding our revenue producing equipment.

Power units (tractors) – sleeper | 86 |

Power units (tractors) – day cab | 2 |

Trailers | |

| Flatbed | 6 |

| Dry van | 329 |

| Refrigerated | 30 |

| Other specialized | 9 |

| Tanker | 9 |

The average age of our power units is approximately 3.2 years. All of our power units are GPS equipped. The majority of our power units are Freightliner vehicles. This uniformity allows for reduced inventory of parts required by our maintenance departments. In addition, the training required for our technicians is greater focused on a primary product line. We replace our power units at approximately four years of age. The average age of our trailers is approximately 3.3 years for general freight and twelve years (as needed) for hazmat and hazwaste which may sit idle for extended periods of time. We maintain all of our revenue producing equipment in good order and repair.

We believe we have an optimal tractor to trailer ratio based upon our current and anticipate customer activity.

Diesel Fuel Availability and Cost