Exhibit 99.1

Exhibit 99.1

Barclays Capital 2009 CEO Energy/Power Conference

September 9 - 10

Copyright © 2009 Portland General Electric. All Rights Reserved.

Cautionary Statement

Information Current as of August 3, 2009

Except as expressly noted, the information in this presentation is current as of August 3, 2009 — the date on which PGE filed its Quarterly Report on Form 10-Q for the second quarter ended June 30, 2009 — and should not be relied upon as being current as of any subsequent date. PGE undertakes no duty to update the presentation, except as may be required by law.

Forward-Looking Statements

This presentation contains statements that are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements include statements regarding earnings guidance, statements regarding growth prospects, statements regarding future financing activities and capital expenditures, statements regarding the cost and completion of capital projects, such as the smart meter project and the Biglow Canyon Wind Farm, as well as other statements containing words such as “will,” “anticipates,” “believes,” “intends,” “estimates,” “promises,” “expects,” “should,” “conditioned upon” and similar expressions. Investors are cautioned that any such forward-looking statements are subject to risks and uncertainties, including the effects of the economic downturn in the state of Oregon, including reductions in demand for electricity and the sale of excess energy into a declining wholesale market; final regulatory review and approval of the deferral of excess power costs related to Boardman’s outage; regulatory approval and rate treatment of the smart meter and Biglow Canyon Wind Farm projects; operational risks relating to the Company’s generation facilities, including unscheduled plant outages, which may result in unanticipated operating, maintenance and repair costs, as well as replacement power costs; the costs of compliance with environmental laws and regulations, including those that govern emissions from thermal power plants; changes in weather, hydroelectric, and energy market conditions, which could affect the availability and cost of purchased power and fuel; and the outcome of various legal and regulatory proceedings; and general economic and financial market conditions. As a result, actual results may differ materially from those projected in the forward-looking statements. All forward-looking statements included in this news release are based on information available to the Company on the date hereof and such statements speak only as of the date hereof. The Company assumes no obligation to update any such forward-looking statement. Prospective investors should also review the risks and uncertainties listed in the Company’s most recent Annual Report on Form 10-K and the Company’s reports on Forms 8-K and 10-Q filed with the United States Securities and Exchange Commission, including Management’s Discussion and Analysis of Financial Condition and Results of Operation and the risks described therein from time to time.

Any forward-looking statement speaks only as of the date on which such statement is made, and, except as required by law, PGE undertakes no obligation to update any forward-looking statement.

2

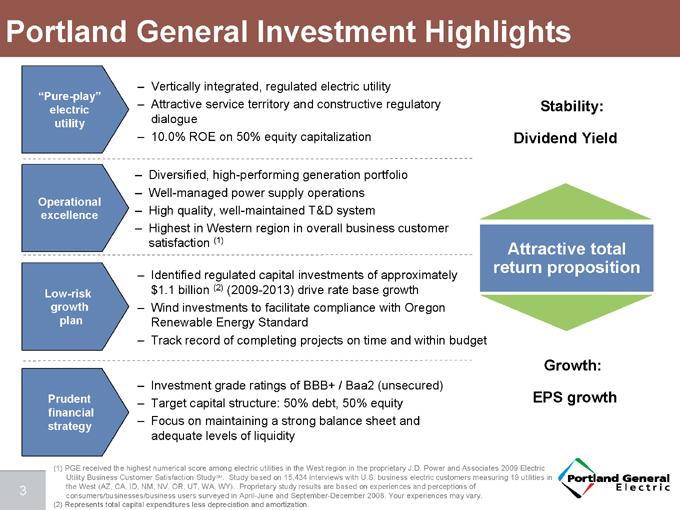

Portland General Investment Highlights

“Pure-play” electric utility

– Vertically integrated, regulated electric utility

– Attractive service territory and constructive regulatory dialogue

– 10.0% ROE on 50% equity capitalization

Operational excellence

– Diversified, high-performing generation portfolio

– Well-managed power supply operations

– High quality, well-maintained T&D system

– Highest in Western region in overall business customer satisfaction (1)

Low-risk growth plan

– Identified regulated capital investments of approximately $1.1 billion (2) (2009-2013) drive rate base growth

– Wind investments to facilitate compliance with Oregon Renewable Energy Standard

– Track record of completing projects on time and within budget

Prudent financial strategy

– Investment grade ratings of BBB+ / Baa2 (unsecured)

– Target capital structure: 50% debt, 50% equity

– Focus on maintaining a strong balance sheet and adequate levels of liquidity

Stability:

Dividend Yield

Attractive total return proposition

Growth:

EPS growth

(1) PGE received the highest numerical score among electric utilities in the West region in the proprietary J.D. Power and Associates 2009 Electric Utility Business Customer Satisfaction StudySM. Study based on 15,434 interviews with U.S. business electric customers measuring 19 utilities in the West (AZ, CA, ID, NM, NV, OR, UT, WA, WY). Proprietary study results are based on experiences and perceptions of consumers/businesses/business users surveyed in April-June and September-December 2008. Your experiences may vary.

(2) Represents total capital expenditures less depreciation and amortization.

3

Portland General Strategic Direction

Mission: To be a company our customers and communities can depend upon to provide electric service in a safe, responsible and reliable manner, with excellent customer service, at a reasonable price.

Operational Excellence

Customer satisfaction Operational efficiency Power supply, system reliability and service quality Engage and develop our people

Business Growth

Strategic system investments Encourage economic vitality Capitalize on emerging technologies

Corporate Responsibility

Listen and lead in public policy Trusted convener for customers and stakeholders Continued commitment to the Oregon community

Deliver Value to Customers and Shareholders

4

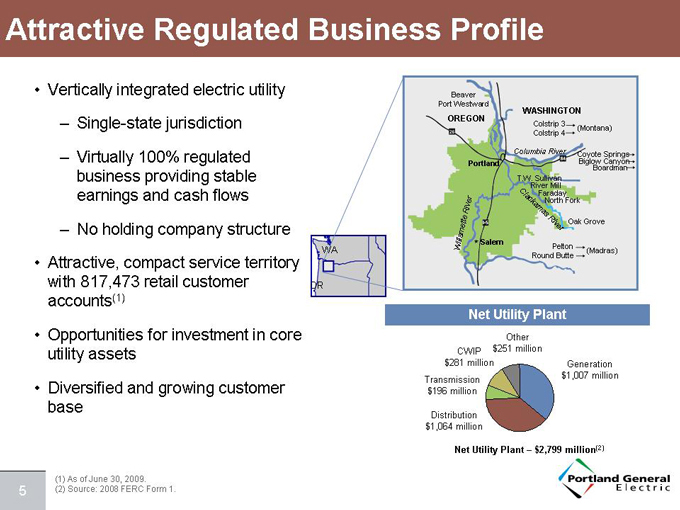

Attractive Regulated Business Profile

• Vertically integrated electric utility

– Single-state jurisdiction

– Virtually 100% regulated business providing stable earnings and cash flows

– No holding company structure

• Attractive, compact service territory with 817,473 retail customer accounts(1)

• Opportunities for investment in core utility assets

• Diversified and growing customer base

Beaver Port Westward

WASHINGTON OREGON

Colstrip 3 (Montana) Colstrip 4

Portland Columbia River Coyote Springs

Biglow Canyon Boardman

T.W. Sullivan River Mill Faraday North Fork

Clackamas River Willamette River

Oak Grove Salem Pelton (Madras) Round Butte

Net Utility Plant

Other $251 million CWIP $281 million Generation $1,007 million Transmission $196 million

Distribution $1,064 million

Net Utility Plant – $2,799 million(2)

(1) As of June 30, 2009. (2) Source: 2008 FERC Form 1.

5

Attractive Service Territory

Weather Adjusted Annual Load (1)

Annual Load

(thousands of MWH)

20,000 19,000 18,000 17,000

2003 2004 2005 2006 2007 2008

1. 4% annual growth

2008 Retail Revenues by Customer Group (2)

Industrial 10%

Commercial 40% Residential 50%

Total = $1.5 Billion

• Compounded annual customer growth of 1.5% and load(1) growth of 1.4% since 2003

• Growth in Oregon’s economy is expected to require further investment by PGE to meet increased energy demand

– Population growth in Oregon has exceeded United States average: 1.2% vs. 1.0% from 2007-2008

– Population growth of counties in PGE’s service area has exceeded rest of state

• Load growth for 2009 is forecasted to decline by approximately 2.5% relative to 2008 on a weather-adjusted basis driven primarily by:

– Reduction in commercial and industrial energy usage

– Residential usage is expected to by slightly below 2008 levels

(1) Adjusted for weather and certain industrial customers.

(2) No single customer accounts for more than 2% of total retail revenues.

6

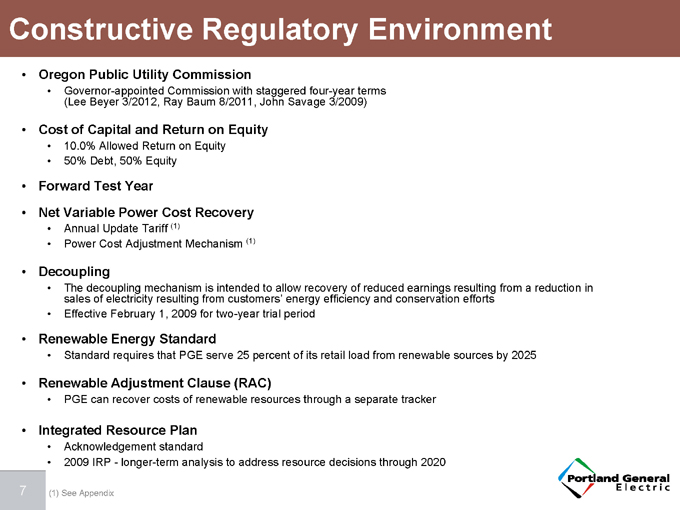

Constructive Regulatory Environment

• Oregon Public Utility Commission

• Governor-appointed Commission with staggered four-year terms (Lee Beyer 3/2012, Ray Baum 8/2011, John Savage 3/2009)

• Cost of Capital and Return on Equity

• 10.0% Allowed Return on Equity

• 50% Debt, 50% Equity

• Forward Test Year

• Net Variable Power Cost Recovery

• Annual Update Tariff (1)

• Power Cost Adjustment Mechanism (1)

• Decoupling

• The decoupling mechanism is intended to allow recovery of reduced earnings resulting from a reduction in sales of electricity resulting from customers’ energy efficiency and conservation efforts

• Effective February 1, 2009 for two-year trial period

• Renewable Energy Standard

• Standard requires that PGE serve 25 percent of its retail load from renewable sources by 2025

• Renewable Adjustment Clause (RAC)

• PGE can recover costs of renewable resources through a separate tracker

• Integrated Resource Plan

• Acknowledgement standard

• 2009 IRP - longer-term analysis to address resource decisions through 2020

(1) See Appendix

7

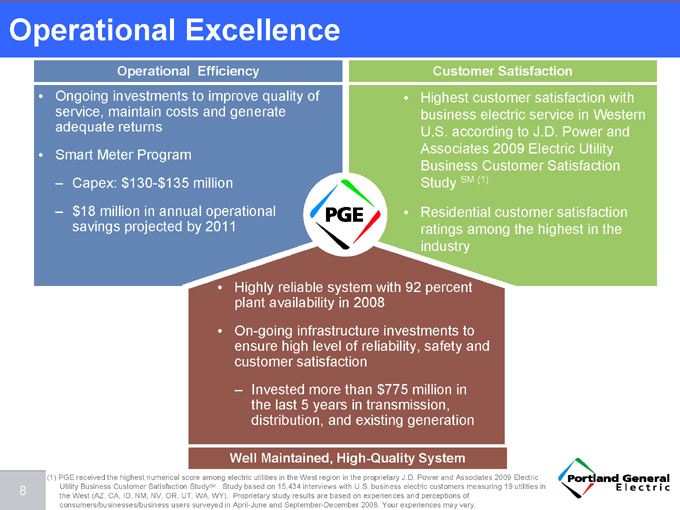

Operational Excellence

Operational Efficiency

Ongoing investments to improve quality of service, maintain costs and generate adequate returns Smart Meter Program

– Capex: $130-$135 million

– $18 million in annual operational savings projected by 2011

Customer Satisfaction

• Highest customer satisfaction with business electric service in Western U.S. according to J.D. Power and Associates 2009 Electric Utility Business Customer Satisfaction Study SM (1)

• Residential customer satisfaction ratings among the highest in the industry

• Highly reliable system with 92 percent plant availability in 2008

• On-going infrastructure investments to ensure high level of reliability, safety and customer satisfaction

– Invested more than $775 million in the last 5 years in transmission, distribution, and existing generation

Well Maintained, High-Quality System

(1) PGE received the highest numerical score among electric utilities in the West region in the proprietary J.D. Power and Associates 2009 Electric Utility Business Customer Satisfaction StudySM. Study based on 15,434 interviews with U.S. business electric customers measuring 19 utilities in the West (AZ, CA, ID, NM, NV, OR, UT, WA, WY). Proprietary study results are based on experiences and perceptions of consumers/businesses/business users surveyed in April-June and September-December 2008. Your experiences may vary.

8

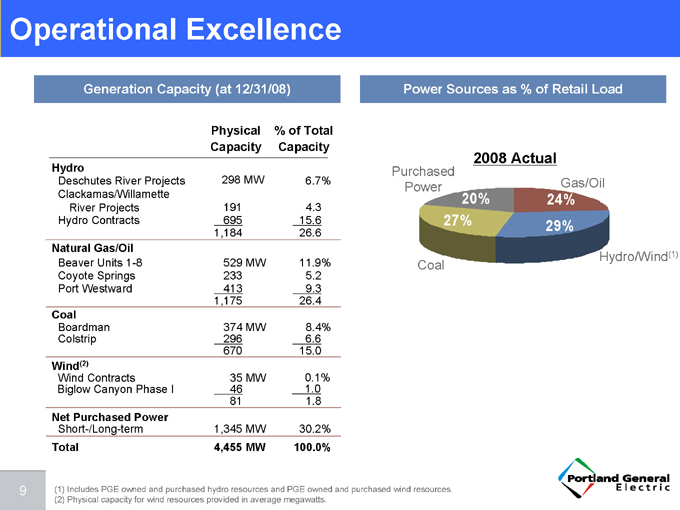

Operational Excellence

Generation Capacity (at 12/31/08)

Physical Capacity % of Total Capacity

Hydro

Deschutes River Projects 298 MW 6.7%

Clackamas/Willamette

River Projects 191 4.3

Hydro Contracts 695 15.6 1,184 26.6

Natural Gas/Oil

Beaver Units 1-8 529 MW 11.9%

Coyote Springs 233 5.2

Port Westward 413 9.3 1,175 26.4

Coal

Boardman 374 MW 8.4%

Colstrip 296 6.6 670 15.0

Wind(2)

Wind Contracts 35 MW 0.1%

Biglow Canyon Phase I 46 1.0 81 1.8

Net Purchased Power

Short-/Long-term 1,345 MW 30.2%

Total 4,455 MW 100.0%

Power Sources as % of Retail Load

2008 Actual

Purchased Power Gas/Oil

20% 24% 27% 29%

Coal Hydro/Wind(1)

(1) Includes PGE owned and purchased hydro resources and PGE owned and purchased wind resources. (2) Physical capacity for wind resources provided in average megawatts.

9

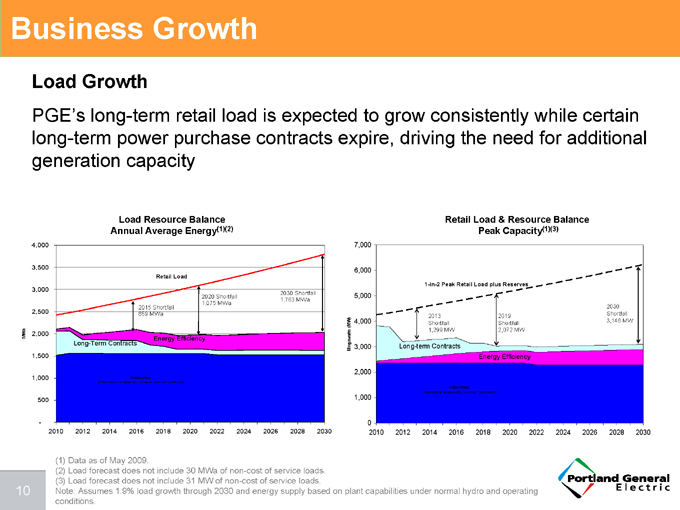

Business Growth

Load Growth

PGE’s long-term retail load is expected to grow consistently while certain long-term power purchase contracts expire, driving the need for additional generation capacity

Load Resource Balance Annual Average Energy(1)(2)

4,000 3,500 3,000 2,500 2,000 1,500 1,000 500 - MWa

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Retail Load

2015 Shortfall 659 MWa 2020 Shortfall 1,075 MWa 2030 Shortfall 1,763 MWa

Energy Efficiency Long-Term Contracts

Generation

(Theoretical availability - Beaver used for peaking)

Retail Load & Resource Balance Peak Capacity(1)(3)

7,000 6,000 5,000 4,000 3,000 2,000 1,000 0 Megawatts (MW)

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

1-in-2 Peak Retail Load plus Reserves

2013 Shortfall 1,299 MW 2019 Shortfall 2,072 MW 2030 Shortfall 3,146 MW

Long-term Contracts

Energy Efficiency

Generation

(Theoretical Availability, Normal Conditions)

(1) Data as of May 2009.

(2) Load forecast does not include 30 MWa of non-cost of service loads. (3) Load forecast does not include 31 MW of non-cost of service loads.

Note: Assumes 1.9% load growth through 2030 and energy supply based on plant capabilities under normal hydro and operating conditions.

10

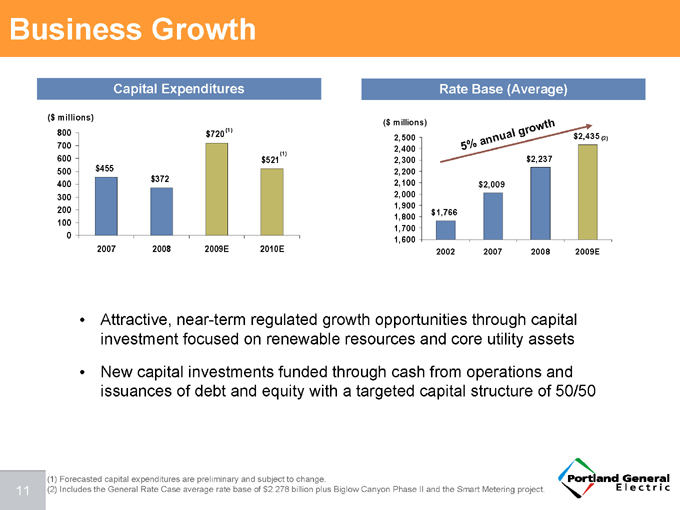

Business Growth

Capital Expenditures

($ millions)

800 700 600 500 400 300 200 100 0

2007 2008 2009E 2010E

$455 $372 $720(1) $521(1)

Rate Base (Average)

($ millions)

2,500 2,400 2,300 2,200 2,100 2,000 1,900 1,800 1,700 1,600

2002 2007 2008 2009E

5% annual growth

$1,766 $2,009 $2,237 $2,435 (2)

Attractive, near-term regulated growth opportunities through capital investment focused on renewable resources and core utility assets

New capital investments funded through cash from operations and issuances of debt and equity with a targeted capital structure of 50/50

(1) Forecasted capital expenditures are preliminary and subject to change.

(2) Includes the General Rate Case average rate base of $2.278 billion plus Biglow Canyon Phase II and the Smart Metering project.

11

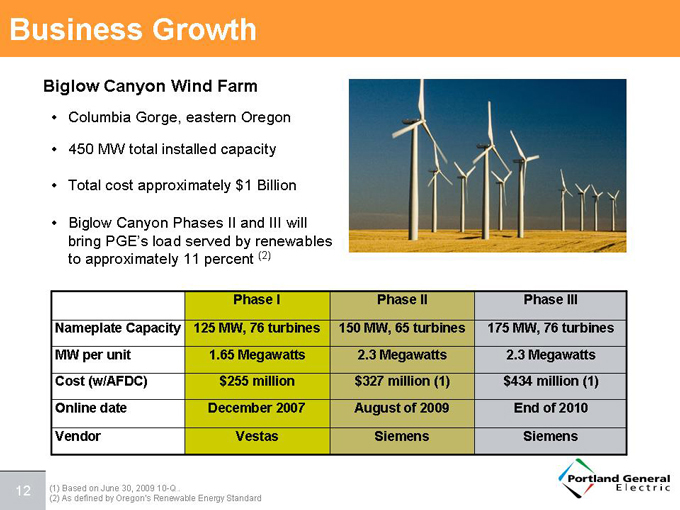

Business Growth

Biglow Canyon Wind Farm

• Columbia Gorge, eastern Oregon

• 450 MW total installed capacity

• Total cost approximately $1 Billion

• Biglow Canyon Phases II and III will bring PGE’s load served by renewables to approximately 11 percent (2)

Nameplate Capacity MW per unit Cost (w/AFDC) Online date Vendor

Phase I 125 MW, 76 turbines 1.65 Megawatts $255 million December 2007 Vestas

Phase II 150 MW, 65 turbines 2.3 Megawatts $327 million (1) August of 2009 Siemens

Phase III 175 MW, 76 turbines 2.3 Megawatts $434 million (1) End of 2010 Siemens

(1) Based on June 30, 2009 10-Q .

(2) As defined by Oregon’s Renewable Energy Standard

12

Business Growth

2009 Integrated Resource Plan (IRP)

• Public planning process with OPUC acknowledgement standard

• Addresses resource decisions through 2020

Schedule:

• Early September 2009: Draft plan filed

• November 2009: Final plan filed

• First Quarter 2010: OPUC acknowledge action plan

Expected resource requirements could include purchase power agreements, new facilities to meet base load and capacity needs, the expansion of energy efficiency programs, and additional renewable resources

Potential Capital Projects:

• New energy resources

• 300-500 MW natural gas facility

• New capacity resources

• 100-200 MW natural gas facility

• Emissions controls at Boardman Coal Plant

• Additional renewable resources

13

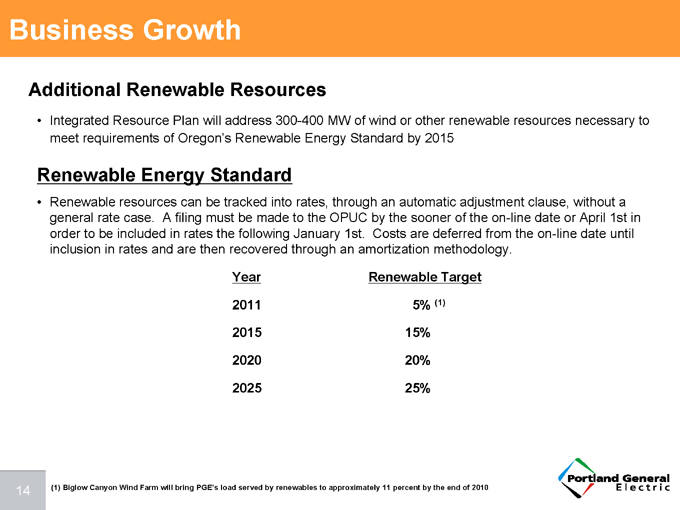

Business Growth

Additional Renewable Resources

• Integrated Resource Plan will address 300-400 MW of wind or other renewable resources necessary to meet requirements of Oregon’s Renewable Energy Standard by 2015

Renewable Energy Standard

• Renewable resources can be tracked into rates, through an automatic adjustment clause, without a general rate case. A filing must be made to the OPUC by the sooner of the on-line date or April 1st in order to be included in rates the following January 1st. Costs are deferred from the on-line date until inclusion in rates and are then recovered through an amortization methodology.

Year Renewable Target

2011 5% (1)

2015 15%

2020 20%

2025 25%

(1) Biglow Canyon Wind Farm will bring PGE’s load served by renewables to approximately 11 percent by the end of 2010

14

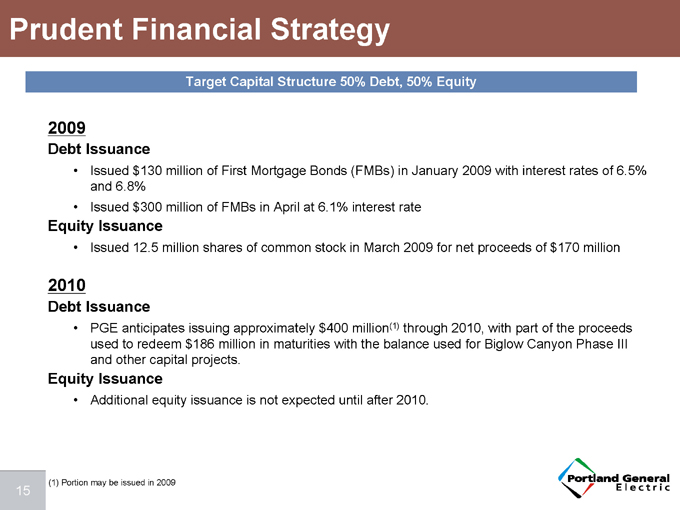

Prudent Financial Strategy

Target Capital Structure 50% Debt, 50% Equity

2009

Debt Issuance

• Issued $130 million of First Mortgage Bonds (FMBs) in January 2009 with interest rates of 6.5% and 6.8%

• Issued $300 million of FMBs in April at 6.1% interest rate

Equity Issuance

• Issued 12.5 million shares of common stock in March 2009 for net proceeds of $170 million

2010

Debt Issuance

• PGE anticipates issuing approximately $400 million(1) through 2010, with part of the proceeds used to redeem $186 million in maturities with the balance used for Biglow Canyon Phase III and other capital projects.

Equity Issuance

• Additional equity issuance is not expected until after 2010.

(1) Portion may be issued in 2009

15

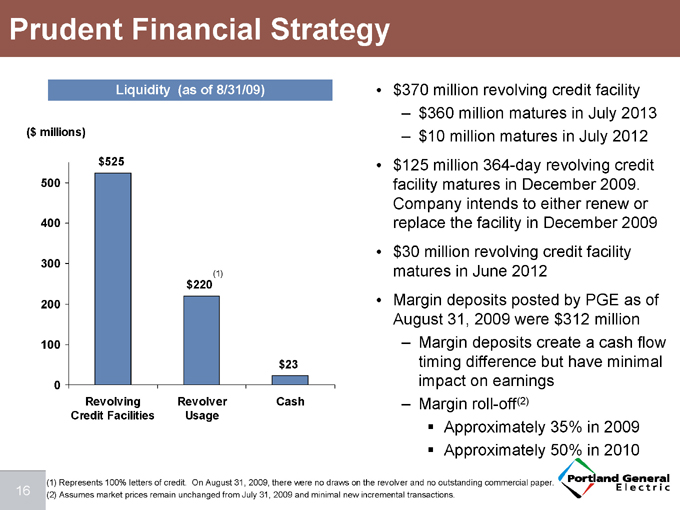

Prudent Financial Strategy

Liquidity (as of 8/31/09)

($ millions)

500 400 300 200 100 0

Revolving Credit Facilities

Revolver Usage

Cash

$525

$220 (1)

$23

$370 million revolving credit facility

$360 million matures in July 2013

$10 million matures in July 2012

$125 million 364-day revolving credit facility matures in December 2009. Company intends to either renew or replace the facility in December 2009

$30 million revolving credit facility matures in June 2012

Margin deposits posted by PGE as of August 31, 2009 were $312 million

Margin deposits create a cash flow timing difference but have minimal impact on earnings

Margin roll-off(2)

Approximately 35% in 2009

Approximately 50% in 2010

(1) Represents 100% letters of credit. On August 31, 2009, there were no draws on the revolver and no outstanding commercial paper. (2) Assumes market prices remain unchanged from July 31, 2009 and minimal new incremental transactions.

16

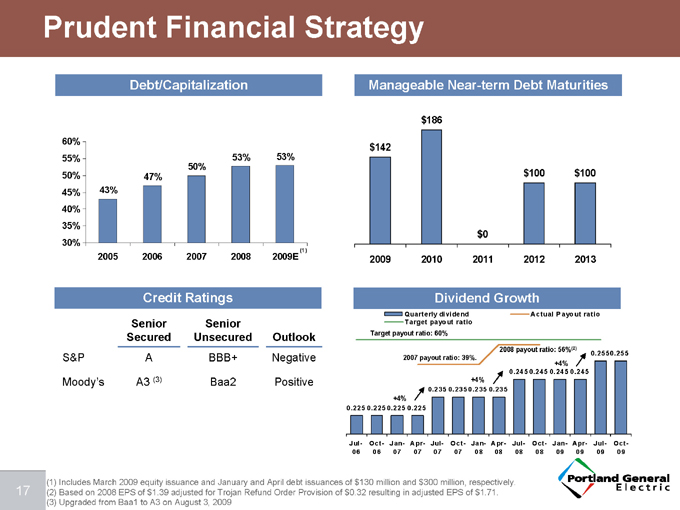

Prudent Financial Strategy

Debt/Capitalization

60% 55% 50% 45% 40% 35% 30%

53% 53% 50% 47% 43%

2005 2006 2007 2008 2009E (1)

Credit Ratings

Senior Secured

Senior Unsecured Outlook

S&P A BBB+ Negative

Moody’s A3 (3) Baa2 Positive

Manageable Near-term Debt Maturities

$186

$142

$100 $100

$0

2009 2010 2011 2012 2013

Dividend Growth

Quarterly dividend Actual Payout ratio Target payout ratio Target payout ratio: 60%

2007 payout ratio: 39%.

2008 payout ratio: 56%(2)

+4% 0.225 0.225 0.225 0.225

+4% 0.235 0.235 0.235 0.235

+4% 0.245 0.245 0.245 0.245

0.2550.255

Jul- Oct- Jan- Apr- Jul- Oct- Jan- Apr- Jul- Oct- Jan- Apr- Jul- Oct-

06 06 07 07 07 07 08 08 08 08 09 09 09 09

(1) Includes March 2009 equity issuance and January and April debt issuances of $130 million and $300 million, respectively. (2) Based on 2008 EPS of $1.39 adjusted for Trojan Refund Order Provision of $0.32 resulting in adjusted EPS of $1.71. (3) Upgraded from Baa1 to A3 on August 3, 2009

17

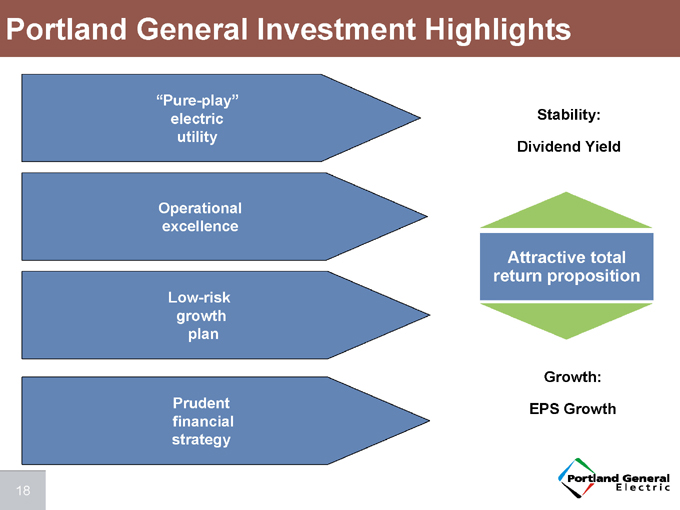

Portland General Investment Highlights

“Pure-play” electric utility

Operational excellence

Low-risk growth plan

Prudent financial strategy

Stability:

Dividend Yield

Attractive total return proposition

Growth:

EPS Growth

18

Investor Relations Contact Information

William J. Valach

Director, Investor Relations 503-464-7395 William.Valach@pgn.com

Portland General Electric Company 121 S.W. Salmon Street Suite 1WTC0403 Portland, OR 97204

www.PortlandGeneral.com

Shane Johnston

Analyst, Investor Relations 503-464-8586 Shane.Johnston@pgn.com

19

Appendix

Table of Contents

Recent Financial Results p.21

General Rate Case p.22

Power Cost Adjustment Mechanism (PCAM) p.23

Decoupling Mechanism p.24-25

Senate Bill 408 p.26

Regulatory, Legal and Other Considerations p.27

Smart Grid p.28

Boardman BART p.29

American Recovery & Reinvestment Act of 2009 p.30

20

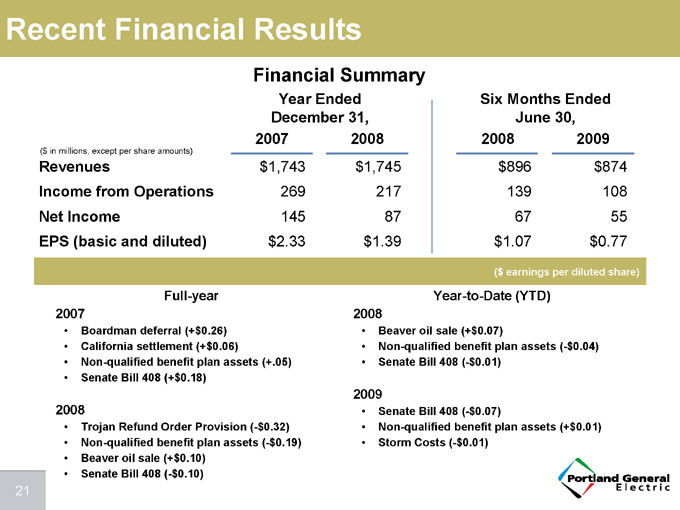

Recent Financial Results

Financial Summary

Year Ended Six Months Ended

December 31, June 30,

2007 2008 2008 2009

($ in millions, except per share amounts)

Revenues $1,743 $1,745 $896 $874

Income from Operations 269 217 139 108

Net Income 145 87 67 55

EPS (basic and diluted) $2.33 $1.39 $1.07 $0.77

($ earnings per diluted share)

Full-year 2007

Boardman deferral (+$0.26)

California settlement (+$0.06)

Non-qualified benefit plan assets (+.05)

Senate Bill 408 (+$0.18)

2008

Trojan Refund Order Provision (-$0.32)

Non-qualified benefit plan assets (-$0.19)

Beaver oil sale (+$0.10)

Senate Bill 408 (-$0.10)

Year-to-Date (YTD) 2008

Beaver oil sale (+$0.07)

Non-qualified benefit plan assets (-$0.04)

Senate Bill 408 (-$0.01)

2009

Senate Bill 408 (-$0.07)

Non-qualified benefit plan assets (+$0.01)

Storm Costs (-$0.01)

21

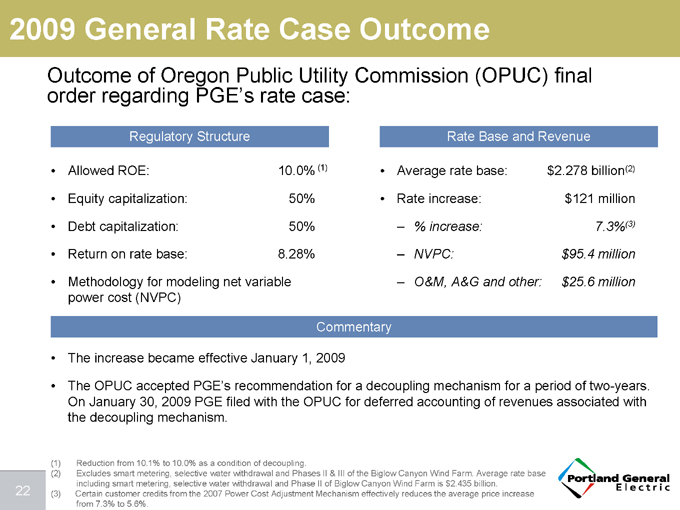

2009 General Rate Case Outcome

Outcome of Oregon Public Utility Commission (OPUC) final order regarding PGE’s rate case:

Regulatory Structure

Allowed ROE: 10.0% (1)

Equity capitalization: 50%

Debt capitalization: 50%

Return on rate base: 8.28%

Methodology for modeling net variable

power cost (NVPC)

Rate Base and Revenue

Average rate base: $2.278 billion(2)

Rate increase: $121 million

% increase: 7.3%(3)

NVPC: $95.4 million

O&M, A&G and other: $25.6 million

Commentary

The increase became effective January 1, 2009

The OPUC accepted PGE’s recommendation for a decoupling mechanism for a period of two-years. On January 30, 2009 PGE filed with the OPUC for deferred accounting of revenues associated with the decoupling mechanism.

(1) Reduction from 10.1% to 10.0% as a condition of decoupling.

(2) Excludes smart metering, selective water withdrawal and Phases II & III of the Biglow Canyon Wind Farm. Average rate base including smart metering, selective water withdrawal and Phase II of Biglow Canyon Wind Farm is $2.435 billion.

(3) Certain customer credits from the 2007 Power Cost Adjustment Mechanism effectively reduces the average price increase from 7.3% to 5.6%.

22

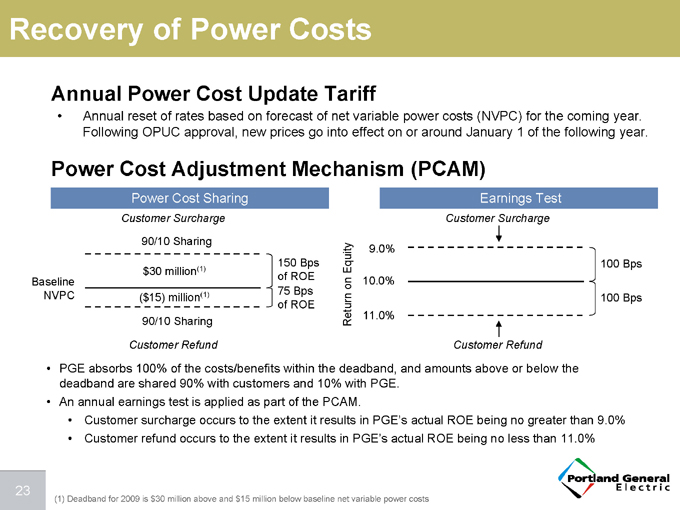

Recovery of Power Costs

Annual Power Cost Update Tariff

Annual reset of rates based on forecast of net variable power costs (NVPC) for the coming year. Following OPUC approval, new prices go into effect on or around January 1 of the following year.

Power Cost Adjustment Mechanism (PCAM)

Power Cost Sharing

Customer Surcharge

90/10 Sharing

150 Bps

$30 million(1) of ROE

Baseline

NVPC ($15) million(1) 75 Bps

of ROE

90/10 Sharing

Customer Refund

Earnings Test

Customer Surcharge

9.0%

Equity 100 Bps

on 10.0%

100 Bps

Return 11.0%

Customer Refund

PGE absorbs 100% of the costs/benefits within the deadband, and amounts above or below the deadband are shared 90% with customers and 10% with PGE.

An annual earnings test is applied as part of the PCAM.

Customer surcharge occurs to the extent it results in PGE’s actual ROE being no greater than 9.0%

Customer refund occurs to the extent it results in PGE’s actual ROE being no less than 11.0%

(1) Deadband for 2009 is $30 million above and $15 million below baseline net variable power costs

23

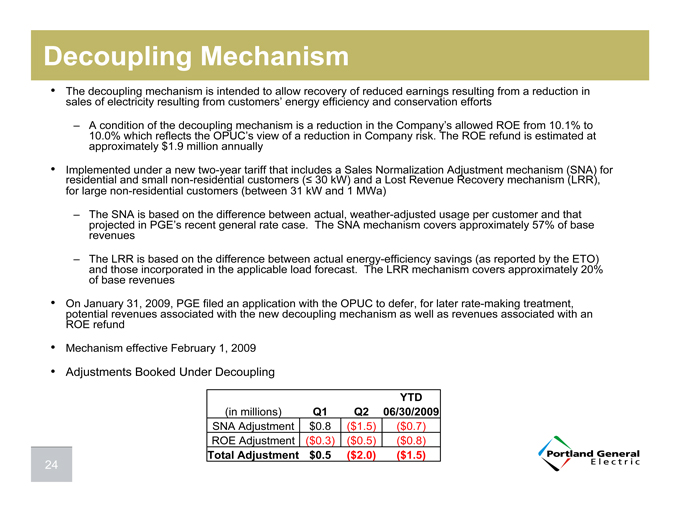

Decoupling Mechanism

The decoupling mechanism is intended to allow recovery of reduced earnings resulting from a reduction in sales of electricity resulting from customers’ energy efficiency and conservation efforts

A condition of the decoupling mechanism is a reduction in the Company’s allowed ROE from 10.1% to 10.0% which reflects the OPUC’s view of a reduction in Company risk. The ROE refund is estimated at approximately $1.9 million annually

Implemented under a new two-year tariff that includes a Sales Normalization Adjustment mechanism (SNA) for residential and small non-residential customers ( 30 kW) and a Lost Revenue Recovery mechanism (LRR), for large non-residential customers (between 31 kW and 1 MWa)

The SNA is based on the difference between actual, weather-adjusted usage per customer and that projected in PGE’s recent general rate case. The SNA mechanism covers approximately 57% of base revenues

The LRR is based on the difference between actual energy-efficiency savings (as reported by the ETO) and those incorporated in the applicable load forecast. The LRR mechanism covers approximately 20% of base revenues

On January 31, 2009, PGE filed an application with the OPUC to defer, for later rate-making treatment, potential revenues associated with the new decoupling mechanism as well as revenues associated with an ROE refund

Mechanism effective February 1, 2009

Adjustments Booked Under Decoupling

YTD

(in millions) Q1 Q2 06/30/2009

SNA Adjustment $0.8 ($1.5) ($0.7)

ROE Adjustment ($0.3) ($0.5) ($0.8)

Total Adjustment $0.5 ($2.0) ($1.5)

24

Decoupling Mechanism

Simplified Decoupling Example Assumptions:

Residential customer Monthly Kwh usage: 1,000 Cost per Kwh: $0.10

Weather adjusted decrease in monthly usage: 10%

PGE cost structure: 50% power costs and 50% all other costs

Analysis:

Base monthly bill: 1,000 x $0.10 = $100 Revised monthly bill due to energy efficiency and/or conservation: 900 x $0.10 = $ 90 Reduction in revenue from customer = $ 10

PGE cost structure of lost revenue: $5 in power costs $5 in all other costs (fixed costs)

Financial impact on PGE:

Power costs: Approximately $0 earnings impact on PGE, assuming power sold on the market at PGE average cost in prices

All other costs: Approximately $0 earnings impact due to $5 booked as a regulatory asset for future recovery from customers (through the decoupling mechanism)

25

Oregon Senate Bill 408

Beginning January 1, 2006, SB 408 requires the OPUC to track estimated income taxes collected by Oregon utilities in rates and compare this amount to adjusted taxes paid to taxing authorities by the utility or corporate consolidated group. The OPUC may establish deferral accounts to capture the difference

SB 408 requires an annual rate adjustment if difference between taxes authorized to be collected by the utility and taxes paid by the utility to taxing authorities exceed $100,000

Report for prior calendar year is filed in October with the refund or collection beginning in June of the following year. For example:

The 2008 report of taxes paid will be filed in October 2009. New tariff goes into effect June 2010, if necessary

Primary issue for PGE is the so called “double whammy” effect, due to the OPUC adopting a fixed reference point for margins and effective tax rates. The double whammy can result in unusual outcomes and increased financial volatility in certain situations. The OPUC stated in the final order that it will be responsive to concerns related to the consequences of the double whammy problem, and may address those concerns in other regulatory proceedings

Historical/expected outcomes:

2006: Customer refund of approximately $37.2 million plus accrued interest

2007: Customer collection of $14.7 million plus accrued interest

2008: Expected customer refund of approximately $10 million plus accrued interest

26

Regulatory, Legal and Other Considerations

Selective Water Withdrawal Project

Pelton/Round Butte project to restore fish passage on the upper Deschutes River

Capital cost (PGE share) approximately $80 million (including AFDC)

On April 14, 2009 PGE filed a motion to suspend procedure schedule due to delay in construction

The project is now expected to be completed in Q1 2010

OPUC docket: UE 204

Colstrip Coal Plant

PGE has a 20% ownership interest in Units 3 and 4 of the Colstrip coal plant

During the 2009 scheduled maintenance outage of Unit 4, two rotors were found to be damaged

Based on input from the Colstrip operator, we expect the outage to last till mid-November 2009

Repair costs are expected to be approximately $2 million (PGE’s Share)

Replacement power costs are estimated to cost PGE approximately $11 million

Boardman Coal Plant

The scheduled 2009 maintenance outage had been extended to mid-August due to generator rotor issues

The Plant went back into service on August 10th

Replacement power costs for PGE were approximately $4 million

Repair costs are not expected to be material

Boardman Coal Plant Deferral

Request with the OPUC to amortize a $26.4 million deferral of replacement power costs, plus accrued interest ($9.2 million as of June 30, 2009) associated with the forced outage of Boardman from November 18, 2005 through February 5, 2006

Request subject to prudency review and regulated earnings test

OPUC docket: UE 196

Trojan Nuclear Plant: Recovery of Return on Investment

OPUC Proceedings – Dockets: DR 10, UE 88, UM 989

Begun refund notification/application process and expect refunding to be complete by end of November.

Class Action Proceedings

27

Smart Grid

Smart Meters

Provides two-way communications with residential and commercial customers

Vendor: Sensus Metering Systems

Technology: FlexNet radio frequency technology

Deployment: 850,000 residential and commercial customer meters

As of August 31, 2009 over 180,000 meters have been installed

Approximately 400,000 meters will be installed by year end 2009 with estimated completion by the end of 2010

Estimated cost: $130 million - $135 million

OPUC approved limited term tariff: June 1, 2008 through December 31, 2010. After 2010 the projects costs, net of savings, would be permanently incorporated into rates in a future rate case

Distribution System

Pursuing direct load control programs

Optimizing distribution system through advanced technology

28

Boardman BART Update

Best Available Retrofit Technology (BART) for compliance with EPA Regional Haze Rule

In June 2009, the Oregon Environmental Quality Commission (OEQC) adopted a rule that would require the installation of emission at Boardman under a phased-in approach:

Phase 1: Installation of low NOx burners, completion by 2011

Phase 2: Installation of semi-dry scrubber and bag house to address mercury and sulfur dioxide removal, completion by 2014

Phase 3: Installation of Selective Catalytic Reduction for additional NOx controls, completion by 2017 Phases 1 and 2 would meet federal BART requirements. Phase 3 would meet the requirements to make reasonable progress towards haze emission reduction goals.

PGE cost estimate for Phases 1, 2 and 3 for the controls required by the OEQC rule: $520 to $560 million (1)

Based upon the expected cost relating to carbon, replacement generation, coal and natural gas, and emission controls required to meet the OEQC’s rule, PGE believes the long term continued operation of Boardman will best meet the economic interests of its customers.

Schedule:

EPA approval 2010

(1) 100% of estimated total costs and excludes AFDC.

29

American Recovery & Reinvestment Act of 2009

PGE is evaluating the impact and certain benefits that may be available under the American Recovery and Reinvestment Act of 2009 (the Act)

The Act provides a number of enhanced tax benefits, many of which are highly favorable to renewable energy projects such as PGE’s Biglow Canyon windfarm:

For windfarms the Production Tax Credit (PTC) was extended from 2009 through 2012

In lieu of the PTC, companies may elect either:

Investment Tax Credit (ITC) – upfront 30% tax credit

Treasury Department Grants (1) – Cash payment in lieu of claiming PTC or ITC

PGE has completed an initial assessment of these alternatives and determined that continuing to claim PTCs for Biglow Canyon Phase II will provide a larger customer benefit.

PGE will continue to review the alternatives of PTC, ITC or Treasury Department Grants for Biglow Canyon Phase III, which is expected to be placed in service in 2010.

The availability of any such grants under the Act and the Company’s final determination of whether to seek such grants or other benefits under the Act are subject to various other factors. Accordingly, there is no assurance that the Company will either seek or receive any grants or other benefits under the Act.

(1) For qualifying renewable energy facilities placed in service in either 2009 or 2010, or for qualifying renewable energy facilities on which construction commenced during 2009 or 2010 and that are placed in service after 2010 but prior to 2013.

30

Portland General Electric

31