Unlocking Value

Merrill Lynch Health Services Conference

November 28, 2006

New York, NY

Forward-Looking Statements

The information contained in this presentation includes certain estimates, projections

and other forward-looking information that reflect our current views with respect to

future events and financial performance. These estimates, projections and other

forward-looking information are based on assumptions that HealthSouth believes, as

of the date hereof, are reasonable. Inevitably, there will be differences between such

estimates and actual results, and those differences may be material.

There can be no assurance that any estimates, projections or forward-looking

information will be realized.

All such estimates, projections and forward-looking information speak only as of the

date hereof. HealthSouth undertakes no duty to publicly update or revise the

information contained herein.

You are cautioned not to place undue reliance on the estimates, projections and other

forward-looking information in this presentation as they are based on current

expectations and general assumptions and are subject to various risks, uncertainties

and other factors, including those set forth in our Form 10-Q for the periods ended

March 30, 2006, June 30, 2006 & Sept. 30, 2006, the Form 10-K for the fiscal year

ended December 31, 2005 and current report on Form 8-K dated May 26, 2006 and in

other documents that we previously filed with the SEC, many of which are beyond our

control, that may cause actual results to differ materially from the views, beliefs and

estimates expressed herein.

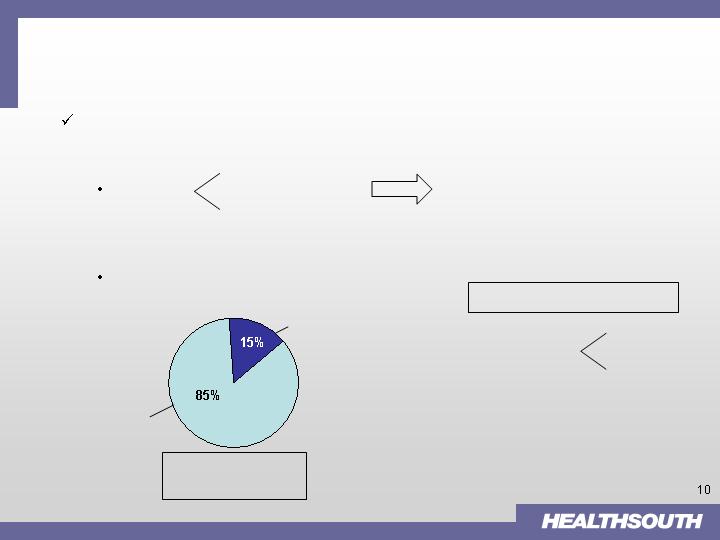

Diversified Healthcare Services Provider

The Company is a leader in each of its four major

operating divisions

Approximately 1,003 facilities in 45 states

YTD Performance (09/30/06)

Net Operating Revenues: $2.3 billion

Operating Earnings of $119.7 million

Adjusted Consolidated EBITDA: $411.8 million

Adjusted Consolidated EBITDA margin: 18.0%

Diagnostic

(6.9%)

Outpatient

6.3%

Surgery

19.7%

Inpatient

81.0%

% of Operating Earnings (b) (c)

(a) Based on facility counts as of Sept. 30, 2006.

(b) Percentages do not include Intersegment Revenues; operating earnings include

operating divisions only

(c) Nine months ended Sept. 30, 2006.

Diagnostic

6.7%

Outpatient

11.0%

Surgery

24.3%

Inpatient

57.1%

Other

0.8%

Diversified Business Portfolio (b) (c) : % of Net Operating Revenues

National Provider of Healthcare Services

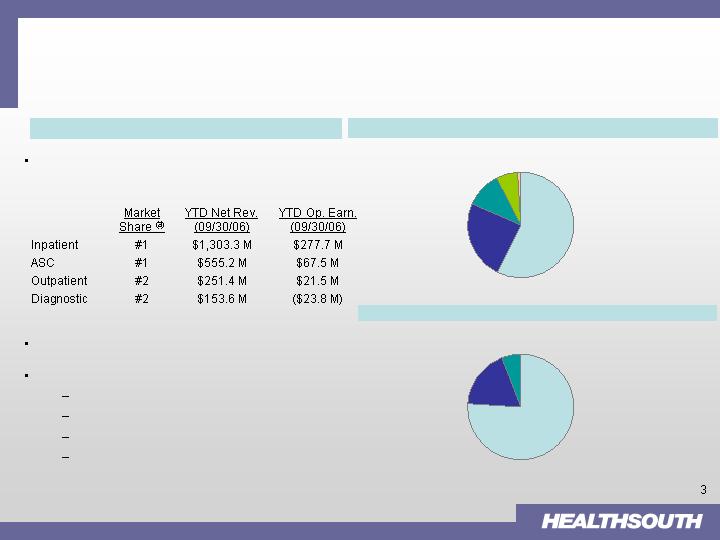

Inpatient Division

Overview

102 Hospital Locations

75% Rule

Nation's largest provider of inpatient rehabilitation

services

193 locations (92 IRFs, 91 outpatient satellites)

Also have 10 LTCH facilities

YTD Performance (09/30/06)

Net Operating Revenues: $1,303.3 million

Operating Earnings: $277.7 million; Margin: 21.3%

Compliant Case Growth approximately 5.4%

Government regulation limiting types of patients IRFs

can admit (“Compliant Cases”)

13 categories

Phase-in = 50%; 60%; 65%; 75%

Threshold frozen at 60% for an additional year

(07/01/07)

HealthSouth outperforms the market with compliant

case growth

Research underway; Symposium Q1 2007

Rule creating roll-up/consolidation opportunities

Payor Mix(1) for the nine months ended 9/30/2006

State Concentrations

(2)

Cummulative %

(2)

IRF

LTCH

TX

15

1

16%

PA

9

2

26%

FL

9

1

36%

AL

6

42%

TN

6

48%

LA

2

3

53%

AZ

5

58%

SC

5

63%

(1) Net Patient Revenue

(2) Number of IRF's & LTCH's Only

Managed Care

18.7%

Medicare

71.2%

Patients

0.2%

Other 3

rd

Party

5.1%

Medicaid

2.1%

Workers Comp

2.7%

Strategic Repositioning

August 14, 2006: HealthSouth announced it would seek strategic

alternatives for its Surgery and Outpatient business segments

Diagnostic business segment previously designated as “non-

core”

The “new” HealthSouth = Focus on Inpatient Rehabilitation

Facilities (“IRF”)

Future growth opportunities in other post-acute segments

Long-Term Acute Care

Home Health

Hospice

Integrated, post-acute payment system (Medicare)

Repositioning Rationale

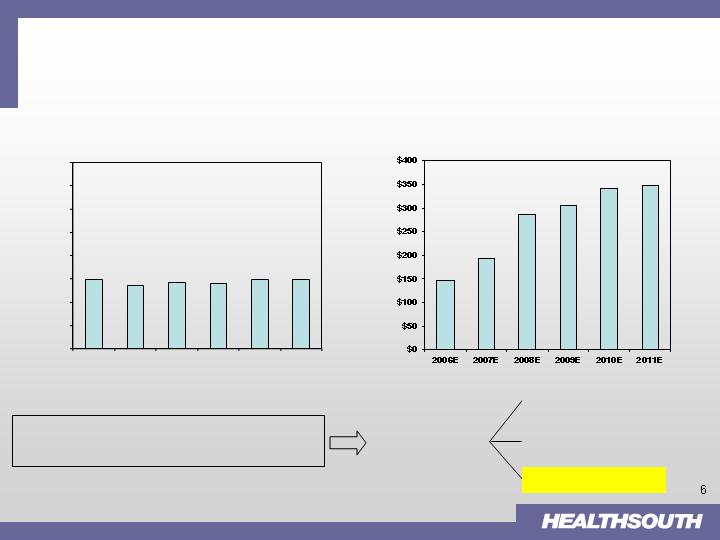

Significant CAPEX Required to Fund Growth

($ in millions)

Incremental Cumulative Growth

CAPEX vs. Base CAPEX ~ $760MM

How to Fund?

Borrow (can’t take on

more debt)

Float Equity (can’t dilute

shareholders)

Divest Segments

“Base Case”

“Growth Case”

$0>

$50

$100

$150

$200

$250

$300

$350

$400

2006E

2007E

2008E

2009E

2010E

2011E

Repositioning Rationale (cont’d)

Orthopedic surgeons used to:

Admit knees/hips to our rehab

hospitals (~20+% of total

discharges)

Referred 50+% of our

outpatient P.T. patients

Referred a disproportionate

amount to our MRIs/ CTs

Did surgeries in our ASCs

Today Orthopedic Surgeons:

Cannot admit most of their

knee/hip patients because of

the 75% Rule

Directly compete with our

Outpatient and Diagnostic

centers by offering these

services in their offices

Remain as partners in ASCs;

the only remaining “synergy”

In some instances, the strategic interests between Inpatient

and Surgery are at cross-purposes with one another

No strategic or financial synergies among divisions

– Historic connection = Orthopedic care

– No longer consistent with current realities

IRF 7% $9 Billion

IRF Segment

Post Acute Market (2004)

Notes:

1. Source: Medicare Provider Analysis and Review File (2004); Claritas

2. Source: Annual Reports; Verispan data; management analysis

3. Typically a 15 – 30 bed wing / unit of an acute-care hospital

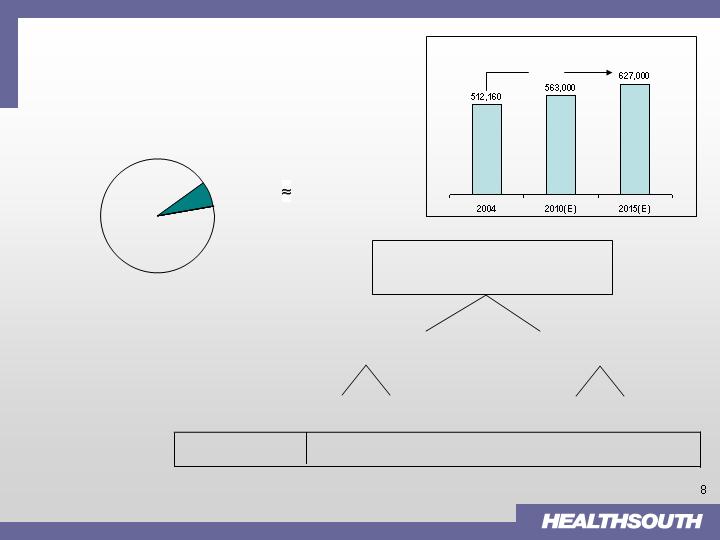

Projected Medicare Compliant Case Growth(1)

+ 22%

=

U.S. IRF Market (

2004

)

(2)

1337 IRFs

Free-standing = 334 (25%)

In-hospital Unit

(3)

= 1003 (75%)

HLS

All Others

For-Profit

Hospitals

Not-for-Profit

Hospitals

Number of IRFs

92

242

266

737

(1) Current overhead calculation of 4.25% of net operating revenue may not be comparable to stand alone entity

(2) 2005 numbers adjusted for discontinued ops facilities in 2006

Inpatient Division

($ in millions)

Inpatient Division – Strong Cash Flow

Characteristics

YTD 09/30/06

2005

(2)

YTD 09/30/06

Annualized

Net Operating Revenues

$1,776.3

$1,303.3

$1,737.7

Operating Earnings

388.3

277.7

370.3

Corporate OH (as a % of revenue)

(1)

(75.5)

(55.4)

(73.9)

Depreciation

65.4

47.5

63.3

Available Cash Before CAPEX & Debt Service

$378.2

$269.8

$359.7

CAPEX (maintenance only)

(38.8)

(30.0)

(40.0)

Cash Available for Growth CAPEX

$339.4

$239.8

$319.7

and Debt Service

Growth Opportunities

Post divestiture, HealthSouth’s growth will occur through organic and

development initiatives

Organic*

2-3% Pricing

1-2% SS Volume

Development:

Current pipeline

~ 40+ projects

*After full implementation of 75% Rule

IRF

LTCH

IRF

1.

Consolidation

(Existing markets)

2.

Acquisition (New markets)

3.

De-novo (Existing or New markets)

LTCH (to supplement IRF presence)

J.V.

Acquire

Mid-to high-single digit

EBITDA growth

Development Strategies

Growth Potential – Illustrative Examples

Incremental EBITDA with No Investment

Capacity Rationalization

“Win - Win” Situation for Both Parties

Higher Margin from Platform Efficiency

Ramp-up Period though Strong IRR

(1) % includes estimated corporate overhead of 4.25%

(2) Assumes HLS owns 80% of JV

($ in thousands)

Consolidation - Joint Venture

DeNovo - Proforma (40 Bed)

Revenue

EBITDA

%

(1)

Revenue

EBITDA

%

(1)

Stand Alone

$10,000

$2,000

16%

Year 1

$8,500

$1,275

11%

Joint Venture

(2)

$14,000

$3,200

19%

Year 2

$10,500

$2,500

20%

- Minority Interest

($640)

Run Rate

$11,500

$2,900

21%

After Consolidation

$14,000

$2,560

14%

Incremental

EBITDA

$560

Investment

$14,000

Investment

$0

5-year Annualized ROI

~ 18%

2006 Development Achievements

Growth is occurring ahead of plan:

Opened new 40-bed IRF in Petersburg, VA

Created joint venture/market consolidation in Tucson, AZ

Merged competitor’s 20-bed IRF with existing HLS 80-bed

IRF

Broke ground on new 40-bed IRF in Fredericksburg, VA

Approved new 50-bed IRF in Phoenix, AZ

Announced acquisition/market consolidation in Wichita Falls, TX

Acquired competitor’s 48-bed IRF; will consolidate patients

to HLS 63-bed IRF

Future Growth Opportunities: Other Post-Acute Sectors

The Post-Acute Market is Sizeable and Remains Highly Fragmented

No Post Acute Care

67%

Post-Acute Usage After Hospital Discharge

Post-Acute Market (2004)

2004 Market Size: $126 B

Source: 2005 CMS, MedPAC and Wall Street research

Post Acute Care

33%

IRF 7%

Skilled Nursing

38%

Home Health

37%

IPF6%

Outpatient 5%

Hospice 4%

Post-Acute Growth Opportunities

Segment

Projected Growth

Inpatient Rehab Facilities (IRFs)

4-6%

Home Health

5-9%

Hospice

12-15%

Long Term Acute Care (LTCH)

10-15%

Skilled Nursing

4-6%

Top 3-5 players in each sector hold the

following market share:

<25% in IRFs

<10% in Home Health

<20% in Hospice

<20% in Skilled Nursing

~50% in LTCH

Summary

HealthSouth: a new Board, a new management team, a new balance

sheet and a new direction.

Re-listed on NYSE (symbol: HLS) on October 26, 2006.

By divesting its non-core assets, the Company will be well-positioned to

become a “pure-play” post-acute provider and a consolidator in the

fragmented $126 B post-acute space.

These divestures – along with any proceeds we may receive from tax

refunds and certain derivative litigation – will significantly strengthen the

company’s Balance Sheet through deleveraging.

LTCHs (supplemental to IRFs only)

Near Term

Longer-term

IRFs

Home Health

Hospice

Appendix

Non-GAAP Financial Reconciliations

(In Thousands)

Reconciliation of Net Loss to Adjusted Consolidated EBITDA

2006

2005

2006

2005

Net loss

(76,144)

$

(11,541)

$

(553,718)

$

(332,158)

$

Loss from discontinued operations

3,291

11,735

20,191

30,830

Provision for income tax expense

4,582

10,339

31,457

29,209

Loss on interest rate swap

28,711

-

13,922

-

Loss (gain) on sale of marketable securities

107

-

121

(10)

Interest income

(1,253)

(3,739)

(9,610)

(10,618)

Interest expense and amortization of debt

discounts and fees

82,493

82,904

250,647

253,530

(Gain) loss on early extinguishment of debt

(6)

-

365,636

33

Professional fees—accounting, tax, and legal

23,774

33,072

100,402

113,429

Government, class action, and related

settlements expense

28,420

-

45,733

215,000

Impairment charges

200

1,460

4,022

26,375

Net non-cash loss on disposal of assets

3,448

2,385

8,830

16,672

Depreciation and amortization

38,473

40,249

113,726

128,694

Compensation expense under FASB Statement

No. 123(R)

3,595

-

11,630

-

Sarbanes-Oxley related costs

861

7,738

4,237

22,965

Restructuring activities under FASB Statement

No. 146

1,348

249

4,579

7,456

Adjusted Consolidated EBITDA

141,900

$

174,851

$

411,805

$

501,407

$

Three Months Ended

September 30,

Nine Months Ended

September 30,

Appendix (cont’d)

Non-GAAP Financial Reconciliations

The change in operating cash and assets and liabilities during the nine months ended September 30,

2006 primarily resulted from declining volumes in each of our operating segments, increased receivable

balances (due to current collection trends, the $35.0 million receivable recorded as a recovery from Mr.

Scrushy, and a delay in Medicare payments), and non-cash reductions in various accrued expenses,

including a reduction in estimates associated with legal fees owed to Mr. Scrushy.

Reconciliation of Adjusted Consolidated EBITDA to Net Cash (Used In) Provided By Operating Activities

2006

2005

Adjusted Consolidated EBITDA

411,805

$

501,407

$

Professional fees—accounting, tax, and legal

(100,402)

(113,429)

Sarbanes-Oxley related costs

(4,237)

(22,965)

Interest expense and amortization of debt discounts and fees

(250,647)

(253,530)

Interest income

9,610

10,618

Provision for doubtful accounts

86,364

68,583

Net gain on disposal of assets

(7,977)

(2,656)

Amortization of debt issue costs, debt discounts, and fees

16,312

30,371

Amortization of restricted stock

2,654

1,358

Accretion of debt securities

(53)

(117)

Loss on sale of investments, excluding marketable securities

1,103

3,420

Equity in net income of nonconsolidated affiliates

(16,841)

(21,115)

Distributions from nonconsolidated affiliates

10,455

15,615

Minority interest in earnings of consolidated affiliates

78,367

78,895

Stock-based compensation

8,976

-

Compensation expense under FASB Statement No. 123(R)

(11,630)

-

Current portion of income tax provision

(10,670)

(16,244)

Restructuring charges under FASB Statement No. 146

(4,579)

(7,456)

Recovery of amounts due from Richard M. Scrushy

(35,000)

-

Net cash settlement on interest rate swap

1,448

-

Other operating cash used in discontinued operations

(25,271)

(42,879)

Change in government, class action, and related settlements liability

(87,171)

(133,548)

Change in assets and liabilities, net of acquisitions*

(148,251)

(7,766)

Net Cash (Used In) Provided By Operating Activities*

(75,635)

$

88,562

$

Nine Months Ended

September 30,

(In Thousands)