Unlocking Value

Citigroup

Global Health Care Conference

May 23, 2007

Forward-Looking Statements

The information contained in this presentation includes certain estimates, projections

and other forward-looking information that reflect our current views with respect to future

events and financial performance. These estimates, projections and other forward-

looking information are based on assumptions that HealthSouth believes, as of the date

hereof, are reasonable. Inevitably, there will be differences between such estimates and

actual results, and those differences may be material.

There can be no assurance that any estimates, projections or forward-looking

information will be realized.

All such estimates, projections and forward-looking information speak only as of the

date hereof. HealthSouth undertakes no duty to publicly update or revise the

information contained herein.

You are cautioned not to place undue reliance on the estimates, projections and other

forward-looking information in this presentation as they are based on current

expectations and general assumptions and are subject to various risks, uncertainties

and other factors, including those set forth in our Form 10-Q for the periods ended

March 30, 2006, June 30, 2006 & Sept. 30, 2006, the Form 10-K for the fiscal year

ended December 31, 2006 and current report on Form 8-K dated May 26, 2006 and in

other documents that we previously filed with the SEC, many of which are beyond our

control, that may cause actual results to differ materially from the views, beliefs and

estimates expressed herein.

Strategic Repositioning

August 14, 2006: In an effort to deleverage its Balance Sheet

and reposition the Company as a “pure-play” post-acute

provider, HealthSouth announced it would seek strategic

alternatives for its Surgery and Outpatient business segments

Diagnostic business segment previously designated as “non-core”

Sale of Outpatient segment announced January 29, 2007

Purchaser: Select Medical

Sales Price: Approximately $245M (debt-free)

Closed: May 1, 2007

Strategic Repositioning (cont’d)

Sale of Surgery segment announced March 26, 2007:

Purchaser: TPG

Sales Price: Approximately $920 million (debt-free) plus $25

million in options

Closing: Early third quarter 2007

Sale of Diagnostic segment announced April 14, 2007:

Purchaser: The Gores Group

Sales Price: Approximately $47.5 million (debt-free)

Closing: Early third quarter 2007

The “New” HealthSouth: Post-Acute Provider with

Near-Term Focus on Inpatient Rehabilitation

Overview

101 Hospital Locations

Nation's largest provider of inpatient

rehabilitation facilities (IRFs)

174 locations (93 IRFs, 81 outpatient satellites)

Typical IRF: 40 bed 60 bed

Size (sq. ft.): 42,000 62,000

CAPEX: $15-17mm $20-24mm

Major services offered:

Nursing Care (24/7)

Inpatient/Outpatient Physical Therapy

Occupational Therapy

Speech Therapy

Operate 8 long-term acute care hospitals

(“LTCH”)

Other post-acute platforms within

HealthSouth:

Home Health

Skilled Nursing

Payor Mix(1) for the year ended 12/31/2006

State Concentrations

(2)

Cummulative %

(2)

IRF

LTCH

TX

15

1

16%

PA

9

2

26%

FL

9

1

36%

AL

6

42%

TN

6

48%

LA

2

2

52%

AZ

5

57%

SC

5

62%

(1)

Net Patient Revenue

(2)

Number of IRF's & LTCH's Only

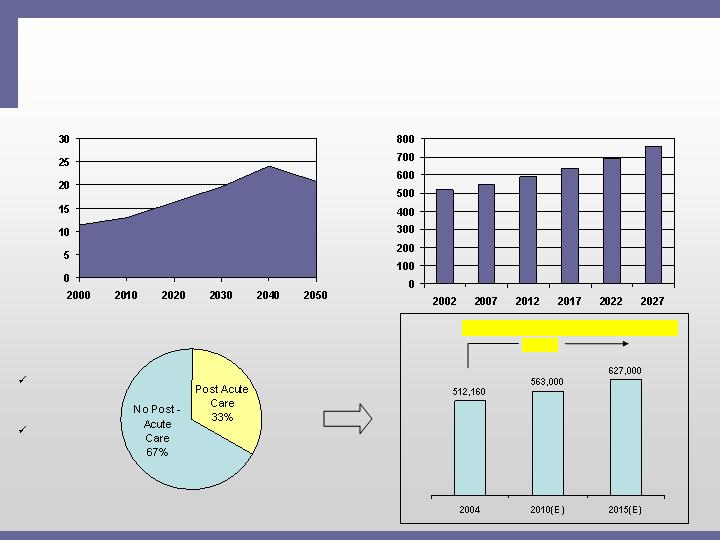

Aging “Baby Boomers” will Continue to Fuel

Demand for IRF Services

National Annual Acute Care Bed Demand in US

2002-2027 Projections (2)

Projected percentage of US population

65 years or older through 2050 (1)

%

Population

Beds per

Thousand

Post-Acute Usage After Discharge

(1) Source: US Census Bureau, 2004

(2) Source: Solucient, LLC: National and Local Impact of Long-Term Demographic Change

on Inpatient Acute Care; Represents demand for additional utilization, not additional beds

(3) Source: Medicare Provider Analysis and Review File (2004); Claritas

Projected Medicare Compliant Case Growth(3)

+ 22%

Post-Acute

Industry

~ $125B

IRF Segment

~ $9B

9

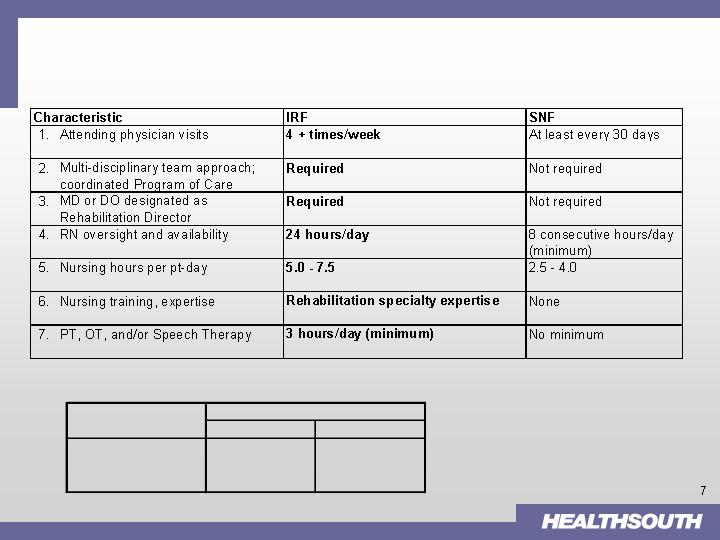

IRFs Provide Greater Nursing and Rehabilitative

Patient Care to Patients…

with significantly shorter length-of-stay (“LOS”)

(1)

NOTE:

(1) Source: Post-Acute care providers: An Overview of Issues. MedPAC analysis of cost reports.

Providers with Consistently

Days

Low Costs

High Costs

SNF average LOS

37.4

30.1

IRF average LOS

10.9

13.3

Growth = Organic and Development

Organic:*

IRF

1.

Consolidation

(existing markets)

2.

De-novo (existing or new markets)

3.

Acquisition (new markets)

LTCH (very limited; to supplement IRF

presence, only)

J.V.

Acquire

2-3% Pricing

1-2% SS Volume

Development: 5-8 new facilities per year

*“Steady-state” basis (post 75% Rule)

Mid- to high-single digit

EBITDA growth

Development Strategies

(1) Source: Report to Congress: Medicare Payment Policy; March 2007

MedPAC analysis of Providers of service files from CMS

(2) Typically a 15-30 bed unit/ department of an acute care hospital

Type of IRF

(1)

2005

HLS = 93

All IRFs

1,231

7.5%

Freestanding

217

42.4%

Hospital-Based

(2)

1,014

Non-Profit

765

For-Profit

305

30.2%

Government

161

Fragmented Sector

Illustrative Development Examples

(in thousands)

(1) Does NOT include estimated corporate overhead of ~4.75% of Net Operating Revenues

(2) Assumes HLS owns ~80% of JV

Higher Margin from Platform

Efficiency

Ramp-up Period though Strong IRR

Incremental EBITDA with No Investment

Capacity Rationalization

“Win - Win” Situation for Both Parties

Consolidation - Joint Venture

DeNovo - Proforma (40 Bed)

Revenue

EBITDA

(1)

%

(1)

Revenue

EBITDA

(1)

%

(1)

Stand Alone

$10,000

$2,000

20%

Year 1

$8,500

$1,275

15%

Joint Venture

(2)

$14,000

$3,200

23%

Year 2

$10,500

$2,500

23%

- Minority Interest

($640)

Run Rate

$11,500

$2,900

25%

After Consolidation

$14,000

$2,560

18%

Incremental

EBITDA

$560

Investment

$15,000-17,000

Investment

$0

5-year Annualized ROI

~ 16-18%

Development Achievements

Opened new 40-bed IRF in Petersburg, VA

Created joint venture/market consolidation in Tucson, AZ

Merged competitor’s 20-bed IRF with existing HLS 80-bed IRF

Approved new 50-bed IRF in Phoenix, AZ

Announced acquisition/market consolidation in Wichita Falls, TX

Acquired competitor’s 48-bed IRF; will consolidate patients to HLS 63-bed IRF

Opened 18 new beds at two facilities

New 40-bed IRF in Puerto Rico (opened: April 17, 2007)

New 40-bed IRF in Fredericksburg, VA (expected to open Q3)

Bed expansion projects approved at five hospitals

Total of 54 beds

Four of these expansions will come on-line in the second half of 2007 with the final

project scheduled to open in 2008

Wellmont Health System Partnership

Joint venture of existing HLS 50-bed IRF in Kingsport, TN

Development of a new 25-bed IRF in Bristol, VA (75% owned by HLS & 25% by

Wellmont); COPN was filed May 1, 2007

2007

2006

2007 Metrics

Consolidated:

Volume growth: 1–2% (full-year)

Net Revenue growth: 2-3%

Operating Earnings

Growth: 3-4%

“As Reported” EBITDA = $275-300 million

Investors should focus on four metrics to evaluate 2007 performance:

1.

Deleveraging the Balance Sheet

2.

Achieving Net Revenue growth of 2-3%

3.

Achieving Operating Earnings growth of 3-4%

4.

Consummating 5-8 development projects by year end

G&A will still have “noise”:

Costs related to all divisions until

closing occurs

General Ledger upgrade investment

Initial development investment

Goal: ~4.75% of Net Revenues

by 2008 year-end

Strong Cash Flow Characteristics

*Total of G&A to all revenues (continuing and discontinuing)

**Targeted rate

***Before tax refund proceeds and proceeds from Corporate complex

(in millions)

at 5.9%*

of Rev.

at 4.75%**

of Rev.

2007 First Quarter EBITDA

68.7

$

68.7

$

Add: Normalization of G&A

18.2

23.5

Sub-total

86.9

$

92.2

$

Less: Capital expenditures

(6.0)

(6.0)

Preferred stock dividend

(6.5)

(6.5)

Cash interest cost***

(56.5)

(56.5)

Excess

17.9

$

23.2

$

Annualized

71.6

$

92.8

$

Normalization of

Gen & Admin Expense

Appendix

Non-GAAP Financial Reconciliations

* After consummation of the divestitures discussed earlier in this Item, and in accordance with our

Credit Agreement (including the March 2007 amendment to the Credit Agreement, as discussed

below), Adjusted Consolidated EBITDA will be calculated on a pro forma basis to give effect to

each divestiture, including pro forma adjustments for the allocation of corporate overhead to each

divested division. No such pro forma adjustments have been made to the above calculation since

no divestitures were consummated as of March 31, 2007.

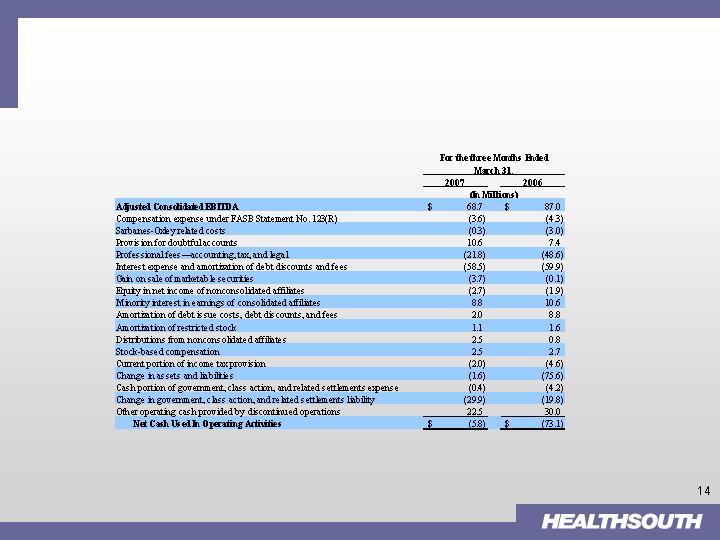

Reconciliation of Net Loss to Adjusted Consolidated EBITDA

2007

2006

Net loss

(56.6)

$

(435.1)

$

Loss from discontinued operations

27.4

2.3

Provision for income tax expense

3.3

13.7

Loss on interest rate swap

4.3

3.8

Interest expense and amortization of debt

discounts and fees

58.5

59.9

Loss on early extinguishment of debt

-

361.1

Professional fees—accounting, tax, and legal

21.8

48.6

Government, class action, and related settlements

(12.2)

4.3

Net noncash loss on disposal of assets

0.1

0.9

Depreciation and amortization

18.2

20.2

Compensation expense under FASB Statement No. 123(R)

3.6

4.3

Sarbanes-Oxley related costs

0.3

3.0

Adjusted Consolidated EBITDA*

68.7

$

87.0

$

For the three months ended

(In Millions)

Appendix (cont’d)

Non-GAAP Financial Reconciliations

Reconciliation of Adjusted Consolidated EBITDA to Net Cash

Used in

Operating Activities