Investor

Presentation

May 2008

1

The information contained in this presentation includes certain estimates, projections and

other forward-looking information that reflect our current views with respect to future events

and financial performance. These estimates, projections and other forward-looking

information are based on assumptions that HealthSouth believes, as of the date hereof, are

reasonable. Inevitably, there will be differences between such estimates and actual results,

and those differences may be material.

There can be no assurance that any estimates, projections or forward-looking

information will be realized.

All such estimates, projections and forward-looking information speak only as of the date

hereof. HealthSouth undertakes no duty to publicly update or revise the information

contained herein.

You are cautioned not to place undue reliance on the estimates, projections and other

forward-looking information in this presentation as they are based on current expectations

and general assumptions and are subject to various risks, uncertainties and other factors,

including those set forth in our Form 10-Q for the quarter ended March 31, 2008, Form 10-K

for the fiscal year ended December 31, 2007 and in other documents that we previously filed

with the SEC, many of which are beyond our control, that may cause actual results to differ

materially from the views, beliefs and estimates expressed herein.

Forward-Looking Statements

2

Investment Considerations

Turnaround Complete: 2008 represents the first year current management can

focus 100% on operations

Volume Growth: #1 priority going forward; TeamWorks initiative will help us meet

or exceed our targets

Expense Control: focused on managing expenses in a disciplined manner, while

realizing that our most important "assets" are our dedicated employees

Continued Deleveraging: goal is to reduce leverage to ~4.5X by the end of 2010

Strong Cash Flows: shareholder value enhanced through strategic use of excess

cash flow

Experienced Management Team: proven track record of success

Focus: Debt Reduction & Growing EPS

3

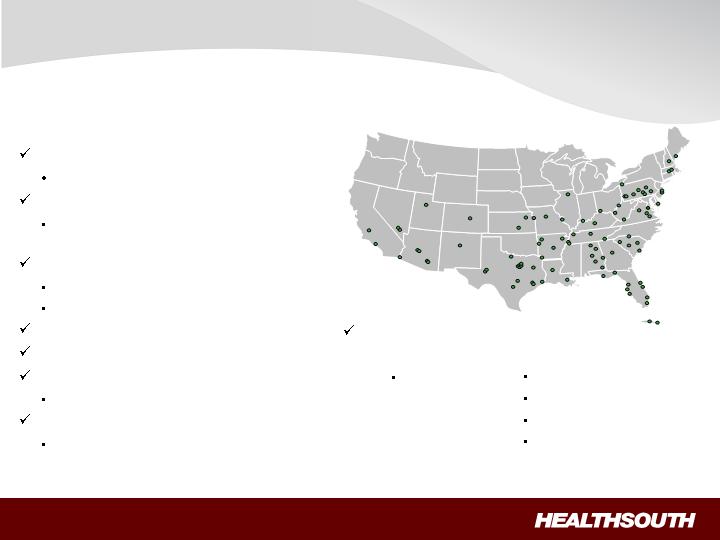

HealthSouth

$1.8 billion

net operating revenues

100 hospitals

26 states

+

60 outpatient satellites & 25 hospital-

based home health agencies

~22,000 employees

Largest Provider of Inpatient Rehabilitative Healthcare Services in the U.S. (1)

(1) Source: Report to Congress: Medicare Payment Policy: March 2008, MedPAC analysis of Providers of service files from CMS

~8% of IRHs

~17% of inpatient beds

4

HealthSouth's Value Proposition

Attractive industry

Aging demographics

Industry leader

Demonstrated ability to grow market

share

Strong operating platform

Industry-leading margins

Commitment to quality

Negligible bad debts

Modest CAPEX requirements

Strong operating cash flows

Deleveraging a priority

~ $2.5 billion NOL's

No federal income taxes for foreseeable

future

Excellent growth opportunities:

2. Development

De-novo

Acquisitions

Consolidations

Joint Ventures

1. Organic

TeamWorks

5

New, independent board

New management

Resolved bond holder

dispute

Settled with DOJ/CMS and

SEC

Reconstructed financial

statements

Sold non-core assets;

reduced debt

“Old” HealthSouth

“New” HealthSouth

Complex company with four

operating divisions and no

synergies -- some actual dis-

synergies

Heavily levered with $3.5 billion of

debt

Over $1 billion total cash outflows

related to government settlements

and professional fees (accounting,

tax and legal)

Non-existent internal controls;

significant material weaknesses at

YE 2004

Corporate governance issues

Post-acute provider with emphasis

on inpatient rehabilitation

Debt reduced to $2.0 billion as of

Q407

Paid last DOJ/CMS & SEC

settlement payments in Q407;

Company can now use excess

cash flow to invest in business

Created comprehensive internal

controls from ground up; 0 material

weaknesses at YE 2007

Leading corporate governance

standards in place

- Outperformed 98.5% of

Russell 3000 (1)

A New Company...

(1) Source: ISS Governance Services: US Proxy Advisory Services report on HealthSouth Corporation dated April 23, 2008

6

... With a Focused Strategy

With our turnaround complete our focus is now on executing

our strategic plan and growing EPS

Our Goal: To be the preeminent specialty provider of inpatient

rehabilitative care in the U.S. through:

clinical, service and operational excellence;

growing market share in existing markets;

building new hospitals in new markets; and

acquiring, or joint-venturing with, competitors

Longer term, we will evaluate expanding into other,

complementary post-acute services on an opportunistic basis

7

Projected percentage of US population

65 years or older through 2050 (1)

(1) Source: US Census Bureau, 2004

(2) Source: Medicare Provider Analysis and Review File (2004); Claritas

Projected Medicare Compliant Case Growth (2)

+ 22%

Attractive Industry

Aging Demographics = Increased Demand

Demand for post-acute services will increase

as the U.S. population ages

“Compliant Cases” are expected to grow

~2% per year for the foreseeable future, creating

an attractive market.

8

(1) Source: Report to Congress: Medicare Payment Policy; March 2008, MedPAC analysis of Providers of service files from CMS

(2) Typically a 15-30 bed unit/department of an acute care hospital

Inpatient rehabilitation is HLS’ core business -vs- one of many,

secondary services provided by acute-care hospitals

HLS not challenged by Bad Debt or CAPEX issues facing

acute-care hospitals

HLS can attract patients from multiple referral sources

Consolidation opportunities will be pursued

Attractive Industry

Fragmented Provider Base = Opportunities

1

2

Total Number of IRFs

1,224

Free-Standing Hospitals

217 (18%)

In-Hospital Units

1,007 (82%)

For-Profit

179

NFP & Gov’t

828

All Others

123

HLS

94

(1)

(2)

9

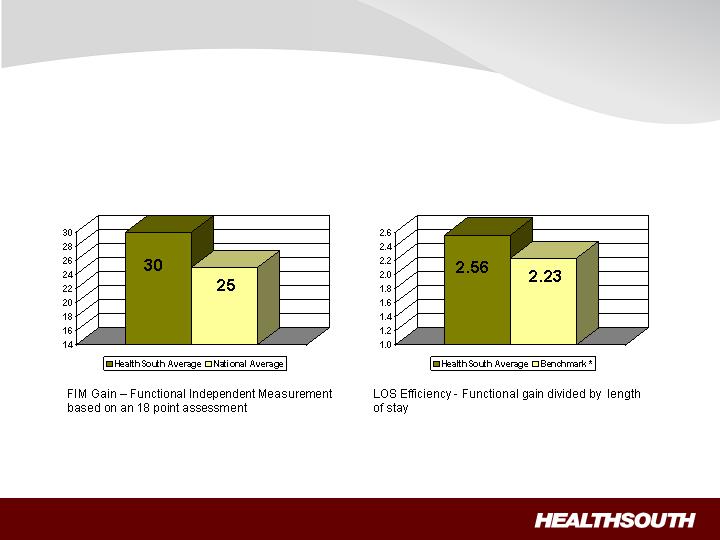

FIM Gains

LOS Efficiency

Source: UDSmr Database –On Demand

Reports - YTD 2007

*Benchmark = Risk Adjusted Expectancy

Leadership Franchise

Value Proposition = Quality of Care

10

IRHs provide a Higher Level of Service…

Leadership Franchise

Differentiation = Better Outcomes at Comparable Costs

8 consecutive hours per day (min.)

24 hours per day

RN oversight and availability

None

Rehabilitation specialty expertise

Nursing training, expertise

2.5 – 4.0

5.0 to 7.5

Nursing hours per patient per day

Not required

Required

MD or DO designated as

Rehabilitation Director

Not required

Required; 3 hour (min.) therapy per day

Multi-disciplinary team approach;

coordinated Program of Care

Once every 30 days (min.)

4+ times per week

Attending physician visits

Nursing Home

Inpatient Rehabilitation Hospital

Service

at Comparable Cost …

~$400

~$900

Average Cost/Day

~$12,000

~30

Nursing Home

~$13,500

~15

Inpatient Rehabilitation Hospital

Average Cost / Admission

Average LOS

11

Financial Overview,

Debt Reduction &

Growth Strategies

12

First Quarter Highlights

Q1 2008 net operating revenues

from inpatient rehabilitation

hospitals increased by 7.7%

compared to Q1 2007

Total discharges increased by

2.7% compared to Q1 2007 and

5.3% sequential improvement

from Q4 2007

Total operating expenses

decreased by 7.1% in Q1 2008

compared to Q1 2007

Adjusted(1) diluted EPS from

continuing operations =

$0.19/share

2008 Q1 Financial Recap

13

(1) Excludes preferred dividends, accelerated depreciation from our corporate campus, professional fees related to derivative litigation and tax recoveries, amounts

classified as government, class action, and related settlements and the loss associated with our interest rate swap

Year-Over-Year

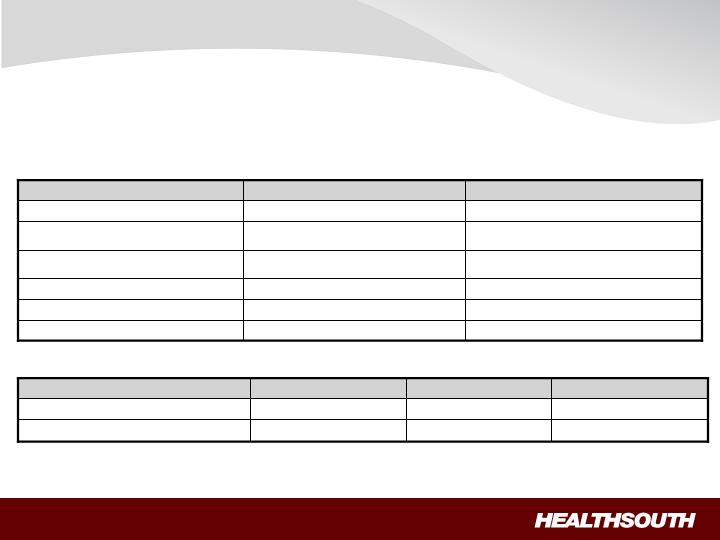

($ In Millions)

Three Months Ended Mar. 31,

2008

2007

Net operating revenues

469.0

$

443.1

$

Adjusted Consolidated EBITDA

89.0

$

68.9

$

Operating Earnings

87.6

$

32.6

$

Discharges

26,517

25,822

Sequential

Three Months Ended

3/31/2008

12/31/2007

Net operating revenues

469.0

$

439.0

$

Adjusted Consolidated EBITDA

89.0

$

87.1

$

Operating Earnings

87.6

$

21.9

$

Discharges

26,517

25,183

14

Strong Cash Flow

All Settlement Payments

completed by 12/31/07

Tax losses available for future

years ~ $2.5 billion

No federal income taxes for

foreseeable future

Excess cash flow will be used for:

Reducing debt

Upgrading existing hospitals

Building new hospitals

Acquiring competitors

Note: Consolidations/JVs typically

do not require any CAPEX

Note: Before Professional Fees (2008 est. $25M) and Preferred Dividends ($26M)

Does not include non-cash amortization and discounts reported on a GAAP basis

Pro-Forma Based on

(In Millions)

Q1 2008

Adjusted Consolidated EBITDA

89.0

$

320.0

$

335.0

$

Less: Est. capital expenditures (maintenance)

(8.7)

(40.0)

(40.0)

Est. cash interest cost and swap payments

(45.8)

(190.0)

(195.0)

Excess

34.5

$

90.0

$

100.0

$

Excess per fully diluted share

0.37

$

0.98

$

1.09

$

2008 Guidance Range

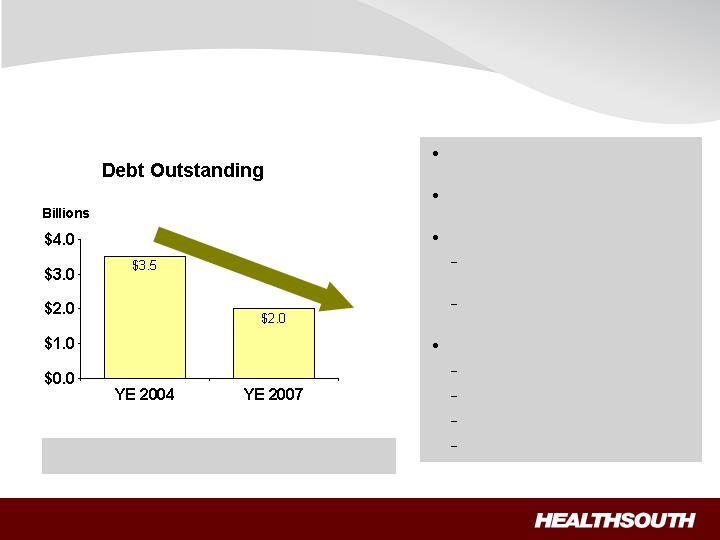

Debt Reduction

Significant debt reduction since

2004

No near-term refinancing

requirements

Priority: reduce high cost debt

Purchased $5M of 10.75%

Senior Notes in Jan/Feb 2008

Will repay $30M of 10.75%

Senior Sub Note in Q4 2008

Future debt reduction from:

Sale of Corporate Campus

Additional income tax recoveries

Excess cash from operations

Derivative proceeds

Goal: 4.5x leverage by YE 2010

15

Growth: Acquisitions and Consolidations

Acquisitions

Opportunistic "tuck-in" IRHs

Active in marketplace as we believe we're the natural consolidator in

IRH space

We will continue to be very disciplined in our approach -- carefully

evaluating these opportunities against our deleveraging priority

Consolidations

Capacity rationalization

Incremental EBITDA with no cash investment

Joint Venture consolidations can be complex

16

Growth: De-novo

17

New and existing markets

Real estate lease option available

at $3 - $5 million cash up-front

cost

Goal: Launch 5 /yr

Pre-construction ~ 6 months

Construction ~ 12 months

Ramp-up to cash positive ~ 6

months

(In Thousands)

(1) Does NOT include estimated corporate overhead of ~4.75% of net operating revenues or rent on a leased facility

(2) Does not assume any income tax implications

De-novo - Pro forma (40 Bed)

Revenue

EBITDA

(1)

%

(1)

Year 1

$8,500

$1,275

15%

Year 2

$10,500

$2,500

24%

Run Rate

$11,500

$2,900

25%

Investment

$15,000-17,000

5-year Annualized ROI

(2)

14% -18%

Investment Considerations

Turnaround Complete: 2008 represents the first year current management can

focus 100% on operations

Volume Growth: #1 priority going forward; TeamWorks initiative will help us meet

or exceed our targets

Expense Control: focused on managing expenses in a disciplined manner, while

realizing that our most important "assets" are our dedicated employees

Continued Deleveraging: goal is to reduce leverage to ~4.5X by the end of 2010

Strong Cash Flows: shareholder value enhanced through strategic use of excess

cash flow

Experienced Management Team: proven track record of success

Focus: Debt Reduction & Growing EPS

18

Appendix

19

2008 Guidance

Note: The above guidance does not incorporate any assumptions related to: (1) mark-to-market adjustments to the liability associated with our securities litigation settlement that

are required until issuance of the common stock and warrants; and (2) any gain or loss associated with our interest rate swap over the remaining term of this agreement.

Inpatient discharges are expected to grow 2% to 4% year over year

Consolidated net operating revenues to be in the range of $1.80 billion to

$1.85 billion

Adjusted consolidated EBITDA is expected to be in the range of $320 million

to $335 million

Diluted loss per share available to common shareholders will be in the range

of ($0.08) to $0.00 per share

Our adjusted diluted earnings per share will be in the range of $0.30 per share to

$0.38 per share

Excludes accelerated depreciation from our corporate campus (~$10M) and professional fees

related to derivative litigation and tax recoveries (~$25M)

20

Review of Key Assumptions to EPS Growth

Key Assumptions:

SS Discharges: 2+%/yr

(2% - 4% guidance for 2008)

Pricing: 2-3%/yr

SW&B: 3-4%/yr

G&A: 4.75% of net op. revenues

Other op. expense: = inflation

Interest expense: $180-190M

(at current debt levels)

Federal income taxes: $0

(for foreseeable future)

Derivative proceeds: TBD

“Restructuring”: ~$25M in ‘08

Comments:

Primary operational focus (TeamWorks)

Beginning in Q409 (P.L. 110-173 “rolls-back”

pricing from Q208 thru Q309)

Higher in 2008 due to investment (“catch-up”) to

make benefits competitive

Target: End-of-Year 2008

Operational focus (TeamWorks)

Cash payments are lower ($170-180M)

(at current debt levels)

NOL’s (~$2.5B)

Will be used to re-pay debt

Fees related to pursuit of derivative proceeds

(a)

(a) Targeted rate of 4.75% (not including FASB Statement No.123(R) costs); (b) Excludes swap payments

(b)

21

Supplemental Non-GAAP Disclosures

Adjusted Consolidated EBITDA

22

2008

2007

Net income (loss)

19.8

$

(56.6)

$

(Income) loss from discontinued operations

(15.9)

27.8

Provision for income tax expense

0.1

3.3

Loss on interest rate swap

36.6

4.3

Interest expense and amortization of debt discounts and fees

47.4

58.5

Loss on early extinguishment of debt

0.3

-

Government, class action, and related settlements

(36.4)

(12.2)

Net noncash loss on disposal of assets

0.1

0.1

Depreciation and amortization

30.1

18.0

Professional fees—accounting, tax, and legal

3.6

21.8

Compensation expense under FASB Statement No. 123(R)

3.3

3.6

Sarbanes-Oxley related costs

-

0.3

Adjusted Consolidated EBITDA

(1)

89.0

$

68.9

$

Three Months Ended March 31,

(In Millions)

(1)

Adjusted Consolidated EBITDA is a non

-

GAAP financial measure. We believe it is useful to investors

as it is used in

our

covenant calculations under our Credit Agreement.

Adjusted Consolidated EBITDA is not a measure of financ

ial performance under accounting principles generally accepted

in the United States

(“GAAP”)

and should not be considered as an alternative to net income (loss) or to cash flows from

operating, investing, and financing activities. Because Adjusted Consolid

ated EBITDA is not a measure determined in

accordance with

GAAP

and is susceptible to varying calculations, Adjusted Consolidated EBITDA, as presented, may not

be comparable to other similarly titled measures presented by other companies.

Our Credit Agreement allows certain items to be added to arrive at Adjusted Consolidated EBITDA that are viewed as not

being ongoing costs once the Company has completed its restructuring.

Supplemental Non-GAAP Disclosures (cont'd)

Adjusted Consolidated EBITDA

23

for future periods.

amount has not been included in the above calculation as it would not be indicative of our Adjusted Consolidated EBITDA

overy. This

EBITDA under our Credit Agreement. This includes interest income associated with our federal income tax rec

addition, we are allowed to add other income, including interest income, to the calculation of Adjusted Consolidated

included in the above table. In

divested as of the beginning of each period presented. Accordingly, these adjustments are not

necessarily indicative of the Adjusted Consolidated EBITDA that would have resulted had the applicable divisions been

these allocation are estimates and are not

for the allocation of corporate overhead to each divested division. However,

our Credit Agreement, Adjusted Consolidated EBITDA is calculated to give effect to each divestiture, including adjustments

atient, and diagnostic divisions, and in accordance with

After consummation of the divestitures of our surgery centers, outp

We define operating earnings as income before (1) loss on early extinguishment of debt

,

(2) interest expense and

amortization of debt discounts and fees

,

(3) other income

,

(4)

loss on interest rate

swap, and (5) income tax expense.

We use operating earnings as an analytical indicator to assess our performance. Our operating earnings for the three

months ended March

31, 200

8

and 200

7

were as follows:

2008

2007

Net operating revenues

469.0

$

443.1

$

Total operating expenses

376.2

404.9

Equity in net income of nonconsolidated affiliates

(2.4)

(2.7)

Minority interests in earnings of consolidated affiliates

7.6

8.3

Operating earnings

87.6

$

32.6

$

Three Months Ended March 31,

(In Millions)

Operating earnings is no

t a defined measure of financial performance under

GAAP

and should not be considered as

an alternative to net

income (

loss

)

. Because operating earnings is not a measure determined in accordance with

GAAP

and is susceptible to varying calculations, operatin

g earnings, as presented, may not be comparable to other

similarly titled measure

s presented by other companies.