Free signup for more

- Track your favorite companies

- Receive email alerts for new filings

- Personalized dashboard of news and more

- Access all data and search results

Filing tables

Filing exhibits

DPL similar filings

- 16 Oct 06 DPL Announces Timing of Third Quarter 2006 Earnings Release, Webcast Conference Call

- 25 Sep 06 Entry into a Material Definitive Agreement

- 8 Sep 06 DPL Names Paul M. Barbas As Chief Executive Officer

- 7 Sep 06 Regulation FD Disclosure

- 21 Aug 06 DPL Completes $400 Million Stock Buyback

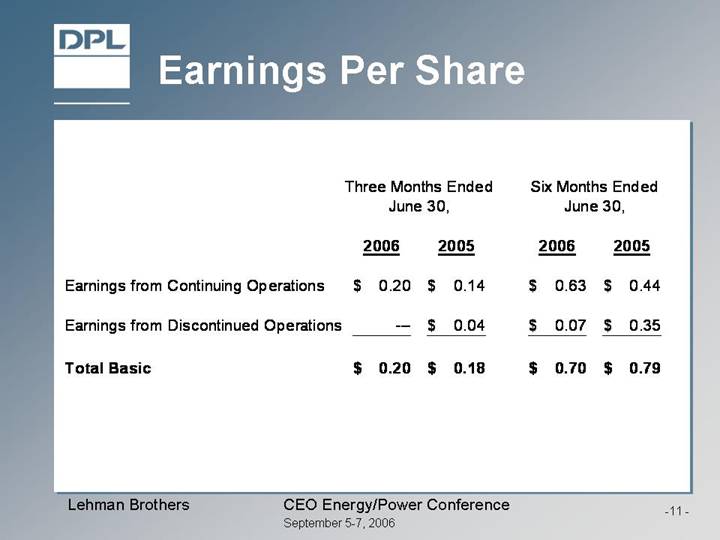

- 4 Aug 06 DPL Reports Second Quarter Earnings

- 28 Jul 06 Regulation FD Disclosure

Filing view

External links