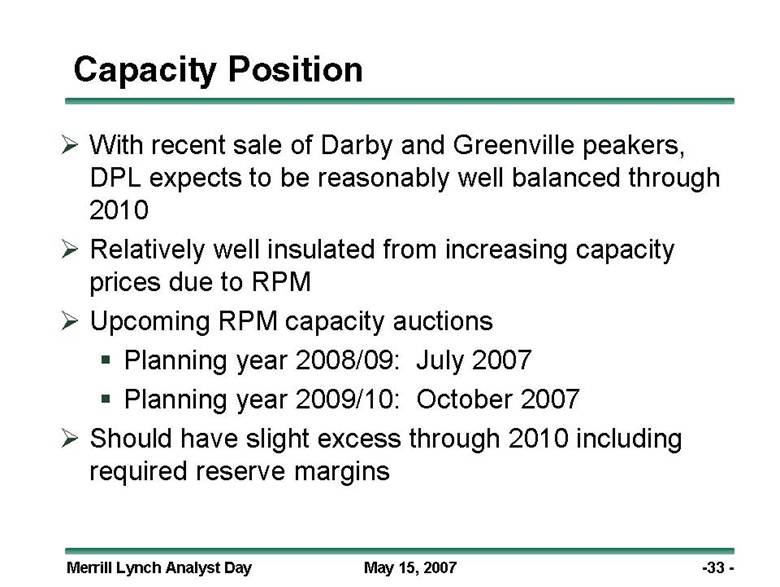

| Notice Regarding Forward-Looking Statements Certain statements contained in this presentation are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Matters discussed in press release that relate to events or developments that are expected to occur in the future, including management’s expectations, strategic objectives, business prospects, anticipated economic performance and financial condition and other similar matters constitute forward-looking statements. Forward-looking statements are based on management’s beliefs, assumptions and expectations of future economic performance, taking into account the information currently available to management. These statements are not statements of historical fact and are typically identified by terms and phrases such as “anticipate,” “believe,” “intend,” “estimate,” “expect,” “continue,” “should,” “could,” “may,” “plan,” “project,” “predict,” “will” and similar expressions. Such forward-looking statements are subject to risks and uncertainties, and investors are cautioned that outcomes and results may vary materially from those projected due to various factors beyond DPL’s control, including but not limited to: abnormal or severe weather and catastrophic weather-related damage; unusual maintenance or repair requirements; changes in fuel costs and purchased power, coal, environmental emissions, gas and other commodity prices; volatility and changes in markets for electricity and other energy-related commodities; increased competition and deregulation in the electric utility industry; increased competition in the retail generation market; changes in interest rates; state, federal and foreign legislative and regulatory initiatives that affect cost and investment recovery, emission levels, rate structures or tax laws; changes in federal and/or state environmental laws and regulations to which DPL and its subsidiaries are subject; the development of Regional Transmission Organizations, including the PJM to which DPL’s operating subsidiary has given control of its transmission functions; changes in DPL’s purchasing processes, delays and supplier availability; significant delays associated with large construction projects; growth in DPL’s service territory and changes in demand and demographic patterns; changes in accounting rules and the effect of accounting pronouncements issued periodically by accounting standard-setting bodies; financial market conditions; the outcomes of litigation and regulatory investigations, proceedings or inquiries; general economic conditions; and the risks and other factors discussed in DPL’s filings with the Securities and Exchange Commission. Forward-looking statements speak only as of the date of the document in which they are made. We disclaim any obligation or undertaking to provide any updates or revisions to any forward-looking statement to reflect any change in our expectations or any change in events, conditions or circumstances on which the forward-looking statement is based. |