UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-01835

Pioneer Series Trust XI

(Exact name of registrant as specified in charter)

60 State Street, Boston, MA 02109

(Address of principal executive offices) (ZIP code)

Christopher J. Kelley, Amundi Asset Management, Inc.,

60 State Street, Boston, MA 02109

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 742-7825

Date of fiscal year end: December 31, 2023

Date of reporting period: January 1, 2023 through December 31, 2023

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Pioneer Core Equity Fund

Annual Report | December 31, 2023

| | | | | |

| A: PIOTX | C: PCOTX | K: PCEKX | R: CERPX | Y: PVFYX |

visit us: www.amundi.com/us

Pioneer Core Equity Fund | Annual Report | 12/31/231

Portfolio Management Discussion | 12/31/23

In the following discussion, Craig D. Sterling discusses the market environment and the factors that influenced the performance of Pioneer Core Equity Fund during the 12-month period ended December 31, 2023. Mr. Sterling, Managing Director, Director of Core Equity and Head of Equity Research, US, and a portfolio manager at Amundi Asset Management US, Inc. (Amundi US), is responsible for the day-to-day management of the Fund’s investment portfolio, along with Ashesh “Ace” Savla, Team Leader of US Equity Quantitative Research, a vice president, and a portfolio manager at Amundi US.

| Q | How did the Fund perform during the 12-month period ended December 31, 2023? |

| A | Pioneer Core Equity Fund’s Class A shares returned 18.19% at net asset value (NAV) during the 12-month period ended December 31, 2023, while the Fund’s benchmark, the Standard & Poor’s 500 Index (S&P 500), returned 26.29%. During the same period, the average return of the 1,438 mutual funds in Morningstar’s Large Blend Funds category was 22.14%. |

| Q | Which of your investment decisions had the greatest effects on the Fund’s benchmark-relative performance during the 12-month period ended December 31, 2023? |

| A | For the year ended December 31, 2023, the Fund’s relative underperformance was mainly due to weaker security selection results in the health care sector, mainly within the pharmaceuticals segment, and stock selection results in the information technology and consumer discretionary sectors. The largest individual detractor from benchmark-relative performance was our decision to avoid the Fund owning benchmark constituent NVIDIA (+239%) for valuation reasons. Shares of the graphic processing unit manufacturer soared in 2023 on better-than-expected financial results driven largely by spending, and investor exuberance, around generative artificial intelligence. While we appreciate the significant franchises NVIDIA has in gaming and data center silicon, we chose for the Fund not to hold NVIDIA based on our belief that the valuation was not attractive relative to NVIDIA's growth opportunities and potential future competitive responses and market dynamics. Other noteworthy detractors from the Fund's benchmark-relative performance included a larger-than-benchmark weight in Pfizer (-41%) and |

2Pioneer Core Equity Fund | Annual Report | 12/31/23

| | our decision to avoid owning Apple (+49%) because it did not meet our strict valuation criteria. In contrast, the largest contributors to the Fund's relative performance were positive security selection results in the energy sector and our decision to underweight the utilities sector. Security selection in, and an underweight to, the consumer staples sector also contributed favorably to Fund performance, mainly within the household & personal products segment. The largest individual contributor to the Fund's benchmark-relative performance was an overweight position in Advanced Micro Devices (+127%). The company continued to gain market share from Intel due to innovation and, along with NVIDIA, domination in the graphic processing unit market, which serves the fast-growing autonomous vehicles and data center markets. Also boosting Fund performance was an overweight in Meta Platforms (+194%), the parent company of Facebook, and an overweight in the cloud-based software developer, Salesforce (+98%). |

| Q | Did the Fund have any exposure to derivative securities during the 12-month period ended December 31, 2023? |

| A | No, the Fund had no exposure to derivatives during the period. |

| Q | What’s your investment outlook as the Fund enters a new fiscal year? |

| A | The resilience of the US economy in 2023 was quite remarkable. Rate increases leading up to mid-2023 were about the fastest ever, and inflation, though declining from very high levels, remained considerably above the Federal Reserve's target of 2%. Investors' views of the equity market gradually shifted over the course of the year from generally cautious, or pessimistic (ourselves included) at the start of 2023, to optimistic by year end. The equity market appears to be all in on the possibility of a soft landing. |

| | Returns were primarily driven by the “Magnificent 7” through the mid-October 2023 low, but the market recovery was led by a much broader set of stocks. This later point has aided the bullish camp, and generally speaking, we would agree that it is a positive. |

| | We continue to believe that some economic weakness will begin to appear as the cumulative impact of higher interest rates, depleted excess savings, and a difficult political environment all |

Pioneer Core Equity Fund | Annual Report | 12/31/233

| | converge during the year. Offsetting these headwinds, in part, will likely be the impact of prior fiscal stimulus such as the Inflation Reduction Act. |

| | The Federal Reserve has become less hawkish over the past 6 months, but it remains more hawkish than most market participants. The market is now pricing in about six rate cuts in 2024, which we would view as unlikely unless the economy slows dramatically. Further interest rate increases remain possible, even if unlikely, particularly if growth continues to surprise to the upside. We would likely view rate cuts as a negative catalyst for the stock market, as the Federal Reserve very rarely cuts interest rates for good reasons. |

| | Earnings estimates for 2024 are about 11% above expectations for 2023, which is roughly flat on 2022. The slight recovery in earnings that began in the third quarter of 2023 is expected to continue for the next couple of years. In the near term we expect further margin contraction for the majority of companies, and we believe that earnings estimates for the next several quarters remain overly optimistic. A mild recession, in our view, is more likely than a “soft landing,” though the odds of a soft landing may have risen somewhat over the past several months. In either scenario, earnings estimates will likely decline as companies take a more cautious approach given economic uncertainty. If the stock market adequately discounts a potential recession, we would anticipate becoming more constructive. |

| | In this market environment, we are focused on bottom-up, fundamental stock selection and we are opportunistically taking advantage of market volatility to pursue investments in what we believe are high-quality names whose valuations are meaningfully below where we think they should be, and that could offer a favorable risk/reward trade-off. We continuously re-evaluate our assumptions, forecasts and the overall investment landscape to own, what we believe, are the best long-term ideas in large cap space as the outcome of an investment process centered on an experienced analyst team and a consistent, repeatable analytical framework grounded in economic profit. |

4Pioneer Core Equity Fund | Annual Report | 12/31/23

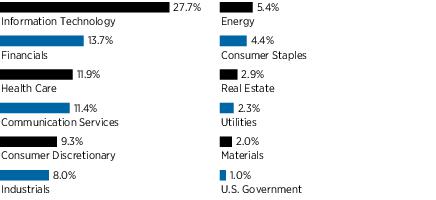

| | From a positioning perspective at year-end, the Fund’s three largest sector overweights included the communication services, energy and financials sectors. Conversely, the Fund’s three largest sector underweights included the consumer staples, consumer discretionary and information technology sectors. |

| | The Fund has a modest underweight to the health care sector where our biggest conviction is in the equipment and services segment, as we believe that hospital surgical procedures should begin to pick up now that Covid is further behind us. We own several companies in the health care sector. |

| | The Fund has reduced its bank exposure to a slight underweight although we maintain selective exposure to large regional banks, or “super-regionals” which have either invested in technology or have advantageous deposit bases and/or revenue opportunities from integration of recent acquisitions and should demonstrate above-industry peer growth and operating leverage from benefits related to mergers and acquisitions. |

| | Lastly, while valuations have increased for the energy sector broadly, we continue to own a mix of attractively valued equipment & services and integrated oil & gas companies. In addition to the current supply/demand headwinds, we believe that the sector is on a longer-term path forward after companies have changed their manager incentive programs to reflect return on invested capital to be better aligned with shareholders and are not spending on growth in oil production after years of overspending on new projects. More recently, we have been overweight the European majors on relative valuation and following the path of the US energy sector in emphasizing shareholder value and more disciplined capital allocation. |

| | Thank you for your continued support and confidence in our stewardship of Pioneer Core Equity Fund, and in Amundi Asset Management US, Inc. (Amundi US). |

Pioneer Core Equity Fund | Annual Report | 12/31/235

Please refer to the Schedule of Investments on pages 16 - 20 for a full listing of Fund securities.

All investments are subject to risk, including the possible loss of principal. In the past several years, financial markets have experienced increased volatility and heightened uncertainty. The market prices of securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict including Russia's military invasion of Ukraine, sanctions against Russia, other nations or individuals or companies and possible countermeasures, market disruptions caused by tariffs, trade disputes or other government actions, or adverse investor sentiment. These conditions may continue, recur, worsen or spread.

At times, the Fund’s investments may represent industries or industry sectors that are interrelated or have common risks, making the Fund more susceptible to any economic, social, political, or regulatory developments or other risks affecting those industries and sectors.

The market prices of securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues or adverse investor sentiment.

Investing in foreign and/or emerging markets securities involves risks relating to interest rates, currency exchange rates, economic, social and political conditions, which could increase volatility. These risks are magnified in emerging markets.

For more information on this or any Pioneer fund, please visit amundi.com/usinvestors or call 1-800-622-9876. This material must be preceded or accompanied by the Fund's current prospectus or summary prospectus.

Any information in this shareholder report regarding market or economic trends or the factors influencing the Fund’s historical or future performance are statements of opinion as of the date of this report. Past performance is not a guarantee of future results.

6Pioneer Core Equity Fund | Annual Report | 12/31/23

Portfolio Summary | 12/31/23

Sector Distribution

(As a percentage of total investments)*

10 Largest Holdings

| (As a percentage of total investments)* |

| 1. | Alphabet, Inc., Class A | 5.30% |

| 2. | Amazon.com, Inc. | 4.97 |

| 3. | Microsoft Corp. | 4.27 |

| 4. | Bank of New York Mellon Corp. | 3.48 |

| 5. | International Business Machines Corp. | 3.42 |

| 6. | Colgate-Palmolive Co. | 3.25 |

| 7. | Cisco Systems, Inc. | 3.01 |

| 8. | Meta Platforms, Inc., Class A | 2.98 |

| 9. | Advanced Micro Devices, Inc. | 2.91 |

| 10. | Microchip Technology, Inc. | 2.90 |

* Excludes short-term investments and all derivative contracts except for options purchased. The Fund is actively managed, and current holdings may be different. The holdings listed should not be considered recommendations to buy or sell any securities.

Pioneer Core Equity Fund | Annual Report | 12/31/237

Prices and Distributions | 12/31/23

Net Asset Value per Share

| Class | 12/31/23 | 12/31/22 |

| A | $20.76 | $18.08 |

| C | $16.50 | $14.47 |

| K | $20.77 | $18.08 |

| R | $20.50 | $17.87 |

| Y | $21.21 | $18.46 |

| | | |

Distributions per Share: 1/1/23 - 12/31/23

| Class | Net

Investment

Income | Short-Term

Capital Gains | Long-Term

Capital Gains |

| A | $0.2159 | $— | $0.3723 |

| C | $0.0766 | $— | $0.3723 |

| K | $0.2751 | $— | $0.3723 |

| R | $0.1662 | $— | $0.3723 |

| Y | $0.2586 | $— | $0.3723 |

Index Definition

The Standard & Poor’s 500 Index is an unmanaged, commonly used measure of the broad U.S. stock market. Indices are unmanaged and their returns assume reinvestment of dividends and do not reflect any fees or expenses. It is not possible to invest directly in an index.

The index defined here pertains to the “Value of $10,000 Investment” and “Value of $5 Million Investment” charts on pages 9 – 13.

8Pioneer Core Equity Fund | Annual Report | 12/31/23

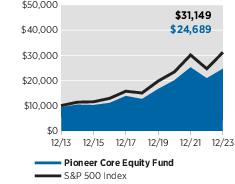

| Performance Update | 12/31/23 | Class A Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $10,000 investment made in Class A shares of Pioneer Core Equity Fund at public offering price during the periods shown, compared to that of the Standard & Poor’s 500 Index.

Average Annual Total Returns

(As of December 31, 2023) |

| Period | Net

Asset

Value

(NAV) | Public

Offering

Price

(POP) | S&P

500

Index |

| 10 Years | 10.11% | 9.46% | 12.03% |

| 5 Years | 14.29 | 12.95 | 15.69 |

| 1 Year | 18.19 | 11.41 | 26.29 |

Expense Ratio

(Per prospectus dated May 1, 2023) |

| Gross |

| 0.87% |

Value of $10,000 Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

NAV results represent the percent change in net asset value per share. NAV returns would have been lower had sales charges been reflected. POP returns reflect deduction of maximum 5.75% sales charge. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for a more current expense ratio.

Pioneer Core Equity Fund | Annual Report | 12/31/239

| Performance Update | 12/31/23 | Class C Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $10,000 investment made in Class C shares of Pioneer Core Equity Fund during the periods shown, compared to that of the Standard & Poor’s 500 Index.

Average Annual Total Returns

(As of December 31, 2023) |

| Period | If

Held | If

Redeemed | S&P

500

Index |

| 10 Years | 9.22% | 9.22% | 12.03% |

| 5 Years | 13.39 | 13.39 | 15.69 |

| 1 Year | 17.27 | 16.27 | 26.29 |

Expense Ratio

(Per prospectus dated May 1, 2023) |

| Gross |

| 1.57% |

Value of $10,000 Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

Class C shares held for less than one year are subject to a 1% contingent deferred sales charge (CDSC). “If Held” results represent the percent change in net asset value per share. “If Redeemed” returns reflect deduction of the CDSC for the one-year period, assuming a complete redemption of shares at the last price calculated on the last business day of the period, and no CDSC for the five- and 10-year periods. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for a more current expense ratio.

10Pioneer Core Equity Fund | Annual Report | 12/31/23

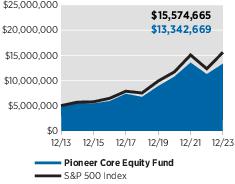

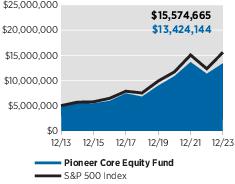

| Performance Update | 12/31/23 | Class K Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $5 million investment made in Class K shares of Pioneer Core Equity Fund during the periods shown, compared to that of the Standard & Poor’s 500 Index.

Average Annual Total Returns

(As of December 31, 2023) |

| Period | Net

Asset

Value

(NAV) | S&P

500

Index |

| 10 Years | 10.31% | 12.03% |

| 5 Years | 14.66 | 15.69 |

| 1 Year | 18.57 | 26.29 |

Expense Ratio

(Per prospectus dated May 1, 2023) |

| Gross |

| 0.57% |

Value of $5 Million Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

The performance shown for Class K shares for the period prior to the commencement of operations of Class K shares on May 4, 2018, is the net asset value performance of the Fund’s Class A shares, which has not been restated to reflect any differences in expenses, including Rule 12b-1 fees applicable to Class A shares. Since fees for Class A shares generally are higher than those of Class K shares, the performance of Class K shares prior to their inception would have been higher than the performance shown. For the period beginning May 4, 2018, the actual performance of Class K shares is reflected. Class K shares are not subject to sales charges and are available for limited groups of eligible investors, including institutional investors. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for a more current expense ratio.

Pioneer Core Equity Fund | Annual Report | 12/31/2311

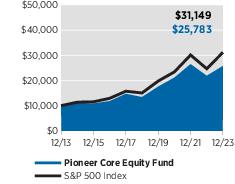

| Performance Update | 12/31/23 | Class R Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $10,000 investment made in Class R shares of Pioneer Core Equity Fund during the periods shown, compared to that of the Standard & Poor’s 500 Index.

Average Annual Total Returns

(As of December 31, 2023) |

| Period | Net

Asset

Value

(NAV) | S&P

500

Index |

| 10 Years | 9.93% | 12.03% |

| 5 Years | 13.94 | 15.69 |

| 1 Year | 17.84 | 26.29 |

Expense Ratio

(Per prospectus dated May 1, 2023) |

| Gross |

| 1.11% |

Value of $10,000 Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

The performance shown for Class R shares for the period prior to the commencement of operations of Class R shares on June 29, 2018, is the net asset value performance of the Fund’s Class A shares, reduced to reflect the higher distribution and service fees of Class R shares. For the period beginning June 29, 2018, the actual performance of Class R shares is reflected. Class R shares are not subject to sales charges and are available for limited groups of eligible investors, including institutional investors. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for a more current expense ratio.

12Pioneer Core Equity Fund | Annual Report | 12/31/23

| Performance Update | 12/31/23 | Class Y Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $5 million investment made in Class Y shares of Pioneer Core Equity Fund during the periods shown, compared to that of the Standard & Poor’s 500 Index.

Average Annual Total Returns

(As of December 31, 2023) |

| Period | Net

Asset

Value

(NAV) | S&P

500

Index |

| 10 Years | 10.38% | 12.03% |

| 5 Years | 14.55 | 15.69 |

| 1 Year | 18.42 | 26.29 |

Expense Ratio

(Per prospectus dated May 1, 2023) |

| Gross |

| 0.66% |

Value of $5 Million Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

Class Y shares are not subject to sales charges and are available for limited groups of eligible investors, including institutional investors. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for a more current expense ratio.

Pioneer Core Equity Fund | Annual Report | 12/31/2313

Comparing Ongoing Fund Expenses

As a shareholder in the Fund, you incur two types of costs:

| (1) | ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses; and |

| (2) | transaction costs, including sales charges (loads) on purchase payments. |

This example is intended to help you understand your ongoing expenses (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 at the beginning of the Fund’s latest six-month period and held throughout the six months.

Using the Tables

Actual Expenses

The first table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period as follows:

| (1) | Divide your account value by $1,000

Example: an $8,600 account value ÷ $1,000 = 8.6 |

| (2) | Multiply the result in (1) above by the corresponding share class’s number in the third row under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. |

Expenses Paid on a $1,000 Investment in Pioneer Core Equity Fund

Based on actual returns from July 1, 2023 through December 31, 2023.

| Share Class | A | C | K | R | Y |

Beginning Account

Value on 7/1/23 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 |

Ending Account Value

(after expenses) on 12/31/23 | $1,056.30 | $1,052.60 | $1,058.10 | $1,055.00 | $1,058.10 |

Expenses Paid

During Period* | $4.56 | $8.64 | $3.01 | $6.11 | $3.42 |

| | |

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.88%, 1.67%, 0.58%, 1.18%, and 0.66% for Class A, Class C, Class K, Class R, and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

14Pioneer Core Equity Fund | Annual Report | 12/31/23

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) that are charged at the time of the transaction. Therefore, the table below is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Expenses Paid on a $1,000 Investment in Pioneer Core Equity Fund

Based on a hypothetical 5% return per year before expenses, reflecting the period from July 1, 2023 through December 31, 2023.

| Share Class | A | C | K | R | Y |

Beginning Account

Value on 7/1/23 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 |

Ending Account Value

(after expenses) on 12/31/23 | $1,020.77 | $1,016.79 | $1,022.28 | $1,019.26 | $1,021.88 |

Expenses Paid

During Period* | $4.48 | $8.49 | $2.96 | $6.01 | $3.36 |

| | |

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.88%, 1.67%, 0.58%, 1.18%, and 0.66% for Class A, Class C, Class K, Class R, and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

Pioneer Core Equity Fund | Annual Report | 12/31/2315

Schedule of Investments | 12/31/23

| Shares | | | | | | Value |

| | UNAFFILIATED ISSUERS — 100.0% | |

| | Common Stocks — 98.8% of Net Assets | |

| | Aerospace & Defense — 1.7% | |

| 371,352 | RTX Corp. | $ 31,245,557 |

| | Total Aerospace & Defense | $31,245,557 |

|

|

| | Air Freight & Logistics — 1.4% | |

| 102,325 | FedEx Corp. | $ 25,885,155 |

| | Total Air Freight & Logistics | $25,885,155 |

|

|

| | Banks — 2.7% | |

| 1,356,797 | Truist Financial Corp. | $ 50,092,945 |

| | Total Banks | $50,092,945 |

|

|

| | Biotechnology — 0.8% | |

| 73,034(a) | Alnylam Pharmaceuticals, Inc. | $ 13,979,438 |

| | Total Biotechnology | $13,979,438 |

|

|

| | Broadline Retail — 5.0% | |

| 593,570(a) | Amazon.com, Inc. | $ 90,187,026 |

| | Total Broadline Retail | $90,187,026 |

|

|

| | Capital Markets — 6.9% | |

| 1,213,520 | Bank of New York Mellon Corp. | $ 63,163,716 |

| 555,697 | Charles Schwab Corp. | 38,231,954 |

| 185,136 | Intercontinental Exchange, Inc. | 23,777,016 |

| | Total Capital Markets | $125,172,686 |

|

|

| | Chemicals — 1.9% | |

| 129,749 | Air Products and Chemicals, Inc. | $ 35,525,276 |

| | Total Chemicals | $35,525,276 |

|

|

| | Communications Equipment — 3.0% | |

| 1,080,593 | Cisco Systems, Inc. | $ 54,591,558 |

| | Total Communications Equipment | $54,591,558 |

|

|

| | Electronic Equipment, Instruments & Components

— 2.8% | |

| 111,432 | CDW Corp. | $ 25,330,722 |

| 161,130(a) | Keysight Technologies, Inc. | 25,634,172 |

| | Total Electronic Equipment, Instruments & Components | $50,964,894 |

|

|

| | Energy Equipment & Services — 1.8% | |

| 978,238 | Baker Hughes Co. | $ 33,436,175 |

| | Total Energy Equipment & Services | $33,436,175 |

|

|

The accompanying notes are an integral part of these financial statements.

16Pioneer Core Equity Fund | Annual Report | 12/31/23

| Shares | | | | | | Value |

| | Entertainment — 2.3% | |

| 460,979 | Walt Disney Co. | $ 41,621,794 |

| | Total Entertainment | $41,621,794 |

|

|

| | Financial Services — 4.0% | |

| 181,132(a) | Fiserv, Inc. | $ 24,061,575 |

| 303,655(a) | PayPal Holdings, Inc. | 18,647,454 |

| 116,233 | Visa, Inc., Class A | 30,261,261 |

| | Total Financial Services | $72,970,290 |

|

|

| | Ground Transportation — 2.3% | |

| 170,590 | Union Pacific Corp. | $ 41,900,316 |

| | Total Ground Transportation | $41,900,316 |

|

|

| | Health Care Equipment & Supplies — 5.1% | |

| 386,337 | Abbott Laboratories | $ 42,524,114 |

| 87,368 | Becton Dickinson & Co. | 21,302,939 |

| 94,882 | Stryker Corp. | 28,413,364 |

| | Total Health Care Equipment & Supplies | $92,240,417 |

|

|

| | Health Care Providers & Services — 2.5% | |

| 98,337 | Humana, Inc. | $ 45,019,662 |

| | Total Health Care Providers & Services | $45,019,662 |

|

|

| | Household Products — 4.4% | |

| 216,988 | Church & Dwight Co., Inc. | $ 20,518,385 |

| 739,656 | Colgate-Palmolive Co. | 58,957,980 |

| | Total Household Products | $79,476,365 |

|

|

| | Interactive Media & Services — 9.1% | |

| 688,566(a) | Alphabet, Inc., Class A | $ 96,185,784 |

| 1,000,000(a) | Bumble, Inc., Class A | 14,740,000 |

| 152,704(a) | Meta Platforms, Inc., Class A | 54,051,108 |

| | Total Interactive Media & Services | $164,976,892 |

|

|

| | IT Services — 5.1% | |

| 398,842 | Cognizant Technology Solutions Corp., Class A | $ 30,124,536 |

| 379,269 | International Business Machines Corp. | 62,029,445 |

| | Total IT Services | $92,153,981 |

|

|

| | Life Sciences Tools & Services — 1.4% | |

| 109,209 | Danaher Corp. | $ 25,264,410 |

| | Total Life Sciences Tools & Services | $25,264,410 |

|

|

| | Machinery — 1.2% | |

| 56,424 | Deere & Co. | $ 22,562,265 |

| | Total Machinery | $22,562,265 |

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Core Equity Fund | Annual Report | 12/31/2317

Schedule of Investments | 12/31/23 (continued)

| Shares | | | | | | Value |

| | Multi-Utilities — 2.3% | |

| 733,361 | CMS Energy Corp. | $ 42,586,273 |

| | Total Multi-Utilities | $42,586,273 |

|

|

| | Oil, Gas & Consumable Fuels — 3.5% | |

| 657,970 | EQT Corp. | $ 25,437,120 |

| 593,544 | Shell Plc (A.D.R.) | 39,055,195 |

| | Total Oil, Gas & Consumable Fuels | $64,492,315 |

|

|

| | Pharmaceuticals — 2.2% | |

| 1,388,067 | Pfizer, Inc. | $ 39,962,449 |

| | Total Pharmaceuticals | $39,962,449 |

|

|

| | Semiconductors & Semiconductor Equipment —

7.4% | |

| 358,593(a) | Advanced Micro Devices, Inc. | $ 52,860,194 |

| 583,519 | Microchip Technology, Inc. | 52,621,743 |

| 343,969 | Micron Technology, Inc. | 29,354,315 |

| | Total Semiconductors & Semiconductor Equipment | $134,836,252 |

|

|

| | Software — 7.7% | |

| 28,808 | Intuit, Inc. | $ 18,005,864 |

| 206,202 | Microsoft Corp. | 77,540,200 |

| 168,419(a) | Salesforce, Inc. | 44,317,776 |

| | Total Software | $139,863,840 |

|

|

| | Specialized REITs — 2.9% | |

| 146,273 | American Tower Corp. | $ 31,577,415 |

| 162,306 | Digital Realty Trust, Inc. | 21,843,142 |

| | Total Specialized REITs | $53,420,557 |

|

|

| | Specialty Retail — 4.3% | |

| 237,104 | Best Buy Co., Inc. | $ 18,560,501 |

| 93,664 | Home Depot, Inc. | 32,459,259 |

| 56,470(a) | Ulta Beauty, Inc. | 27,669,736 |

| | Total Specialty Retail | $78,689,496 |

|

|

| | Technology Hardware, Storage & Peripherals —

1.7% | |

| 850,325(a) | Pure Storage, Inc., Class A | $ 30,322,590 |

| | Total Technology Hardware, Storage & Peripherals | $30,322,590 |

|

|

| | Trading Companies & Distributors — 1.4% | |

| 331,344(a) | AerCap Holdings NV | $ 24,625,486 |

| | Total Trading Companies & Distributors | $24,625,486 |

|

|

| | Total Common Stocks

(Cost $1,421,426,915) | $1,798,066,360 |

|

|

The accompanying notes are an integral part of these financial statements.

18Pioneer Core Equity Fund | Annual Report | 12/31/23

Principal

Amount

USD ($) | | | | | | Value |

| | U.S. Government and Agency

Obligations — 1.0% of Net Assets | |

| 18,000,000(b) | U.S. Treasury Bills, 1/16/24 | $ 17,963,198 |

| | Total U.S. Government and Agency Obligations

(Cost $17,960,618) | $17,963,198 |

|

|

| Shares | | | | | | |

| | SHORT TERM INVESTMENTS — 0.2% of Net

Assets | |

| | Open-End Fund — 0.2% | |

| 4,001,158(c) | Dreyfus Government Cash Management,

Institutional Shares, 5.25% | $ 4,001,158 |

| | | | | | | $ 4,001,158 |

|

|

| | TOTAL SHORT TERM INVESTMENTS

(Cost $4,001,158) | $4,001,158 |

|

|

| | TOTAL INVESTMENTS IN UNAFFILIATED ISSUERS — 100.0%

(Cost $1,443,388,691) | $ 1,820,030,716 |

| | OTHER ASSETS AND LIABILITIES — (0.0)%† | $ (552,934) |

| | net assets — 100.0% | $1,819,477,782 |

| | | | | | | |

| (A.D.R.) | American Depositary Receipts. |

| REIT | Real Estate Investment Trust. |

| (a) | Non-income producing security. |

| (b) | Security issued with a zero coupon. Income is recognized through accretion of discount. |

| (c) | Rate periodically changes. Rate disclosed is the 7-day yield at December 31, 2023. |

| † | Amount rounds to less than 0.1%. |

Purchases and sales of securities (excluding short-term investments) for the year ended December 31, 2023, aggregated $1,815,117,588 and $1,910,989,345, respectively.

The accompanying notes are an integral part of these financial statements.

Pioneer Core Equity Fund | Annual Report | 12/31/2319

Schedule of Investments | 12/31/23 (continued)

At December 31, 2023, the net unrealized appreciation on investments based on cost for federal tax purposes of $1,445,296,965 was as follows:

| Aggregate gross unrealized appreciation for all investments in which there is an excess of value over tax cost | $395,701,532 |

| Aggregate gross unrealized depreciation for all investments in which there is an excess of tax cost over value | (20,967,781) |

| Net unrealized appreciation | $374,733,751 |

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in the three broad levels below.

| Level 1 | – | unadjusted quoted prices in active markets for identical securities. |

| Level 2 | – | other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risks, etc.). See Notes to Financial Statements — Note 1A. |

| Level 3 | – | significant unobservable inputs (including the Adviser's own assumptions in determining fair value of investments). See Notes to Financial Statements — Note 1A. |

The following is a summary of the inputs used as of December 31, 2023 in valuing the Fund's investments:

| | Level 1 | Level 2 | Level 3 | Total |

| Common Stocks | $1,798,066,360 | $ — | $— | $1,798,066,360 |

| U.S. Government and Agency Obligations | — | 17,963,198 | — | 17,963,198 |

| Open-End Fund | 4,001,158 | — | — | 4,001,158 |

| Total Investments in Securities | $ 1,802,067,518 | $ 17,963,198 | $ — | $ 1,820,030,716 |

During the year ended December 31, 2023, there were no transfers in or out of Level 3.

The accompanying notes are an integral part of these financial statements.

20Pioneer Core Equity Fund | Annual Report | 12/31/23

Statement of Assets and Liabilities | 12/31/23

| ASSETS: | |

| Investments in unaffiliated issuers, at value (cost $1,443,388,691) | $1,820,030,716 |

| Receivables — | |

| Fund shares sold | 58,053 |

| Dividends | 1,539,107 |

| Interest | 68,839 |

| Other assets | 16,249 |

| Total assets | $1,821,712,964 |

| LIABILITIES: | |

| Payables — | |

| Fund shares repurchased | $ 1,447,736 |

| Trustees' fees | 46,669 |

| Professional fees | 113,126 |

| Transfer agent fees | 110,070 |

| Registration fees | 120,008 |

| Printing fees | 22,477 |

| Custodian fees | 8,687 |

| Management fees | 124,832 |

| Administrative expenses | 70,658 |

| Distribution fees | 61,036 |

| Accrued expenses | 109,883 |

| Total liabilities | $ 2,235,182 |

| NET ASSETS: | |

| Paid-in capital | $1,446,082,766 |

| Distributable earnings | 373,395,016 |

| Net assets | $1,819,477,782 |

| NET ASSET VALUE PER SHARE: | |

| No par value (unlimited number of shares authorized) | |

| Class A (based on $1,754,598,154/84,504,675 shares) | $ 20.76 |

| Class C (based on $5,645,129/342,182 shares) | $ 16.50 |

| Class K (based on $26,802,944/1,290,348 shares) | $ 20.77 |

| Class R (based on $1,146,270/55,909 shares) | $ 20.50 |

| Class Y (based on $31,285,285/1,475,026 shares) | $ 21.21 |

| MAXIMUM OFFERING PRICE PER SHARE: | |

| Class A (based on $20.76 net asset value per share/100%-5.75% maximum sales charge) | $ 22.03 |

The accompanying notes are an integral part of these financial statements.

Pioneer Core Equity Fund | Annual Report | 12/31/2321

Statement of Operations FOR THE YEAR ENDED 12/31/23

| INVESTMENT INCOME: | | |

| Dividends from unaffiliated issuers | $33,697,722 | |

| Interest from unaffiliated issuers | 388,725 | |

| Total Investment Income | | $ 34,086,447 |

| EXPENSES: | | |

| Management fees | $ 8,730,457 | |

| Administrative expenses | 609,454 | |

| Transfer agent fees | | |

| Class A | 631,881 | |

| Class C | 4,232 | |

| Class K | 37 | |

| Class R | 649 | |

| Class Y | 23,230 | |

| Distribution fees | | |

| Class A | 4,207,925 | |

| Class C | 61,997 | |

| Class R | 5,173 | |

| Shareholder communications expense | 150,715 | |

| Custodian fees | 16,025 | |

| Registration fees | 100,865 | |

| Professional fees | 131,338 | |

| Printing expense | 51,808 | |

| Officers' and Trustees' fees | 106,395 | |

| Miscellaneous | 363,758 | |

| Total expenses | | $ 15,195,939 |

| Net investment income | | $ 18,890,508 |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | | |

| Net realized gain (loss) on: | | |

| Investments in unaffiliated issuers | | $ (4,056,522) |

| Change in net unrealized appreciation (depreciation) on: | | |

| Investments in unaffiliated issuers | | $277,172,149 |

| Net realized and unrealized gain (loss) on investments | | $273,115,627 |

| Net increase in net assets resulting from operations | | $ 292,006,135 |

The accompanying notes are an integral part of these financial statements.

22Pioneer Core Equity Fund | Annual Report | 12/31/23

Statements of Changes in Net Assets

| | Year

Ended

12/31/23 | Year

Ended

12/31/22 |

| FROM OPERATIONS: | | |

| Net investment income (loss) | $ 18,890,508 | $ 15,076,382 |

| Net realized gain (loss) on investments | (4,056,522) | 95,909,587 |

| Change in net unrealized appreciation (depreciation) on investments | 277,172,149 | (484,172,864) |

| Net increase (decrease) in net assets resulting from operations | $ 292,006,135 | $ (373,186,895) |

| DISTRIBUTIONS TO SHAREHOLDERS: | | |

| Class A ($0.59 and $1.28 per share, respectively) | $ (48,991,950) | $ (109,531,375) |

| Class C ($0.45 and $1.17 per share, respectively) | (150,224) | (465,999) |

| Class K ($0.65 and $1.34 per share, respectively) | (809,645) | (2,003,770) |

| Class R ($0.54 and $1.22 per share, respectively) | (29,531) | (59,948) |

| Class Y ($0.63 and $1.33 per share, respectively) | (933,249) | (1,875,435) |

| Total distributions to shareholders | $ (50,914,599) | $ (113,936,527) |

| FROM FUND SHARE TRANSACTIONS: | | |

| Net proceeds from sales of shares | $ 20,534,905 | $ 48,544,168 |

| Reinvestment of distributions | 48,351,215 | 108,491,794 |

| Cost of shares repurchased | (166,692,795) | (194,250,490) |

| Net decrease in net assets resulting from Fund share transactions | $ (97,806,675) | $ (37,214,528) |

| Net increase (decrease) in net assets | $ 143,284,861 | $ (524,337,950) |

| NET ASSETS: | | |

| Beginning of year | $1,676,192,921 | $2,200,530,871 |

| End of year | $1,819,477,782 | $1,676,192,921 |

The accompanying notes are an integral part of these financial statements.

Pioneer Core Equity Fund | Annual Report | 12/31/2323

Statements of Changes in Net Assets (continued)

| | Year

Ended

12/31/23

Shares | Year

Ended

12/31/23

Amount | Year

Ended

12/31/22

Shares | Year

Ended

12/31/22

Amount |

| Class A | | | | |

| Shares sold | 513,525 | $ 10,032,690 | 826,168 | $ 16,983,266 |

| Reinvestment of distributions | 2,330,047 | 47,145,975 | 5,769,096 | 105,679,764 |

| Less shares repurchased | (7,644,447) | (149,631,232) | (8,013,522) | (161,578,206) |

| Net decrease | (4,800,875) | $ (92,452,567) | (1,418,258) | $ (38,915,176) |

| Class C | | | | |

| Shares sold | 30,953 | $ 477,585 | 89,883 | $ 1,399,378 |

| Reinvestment of distributions | 9,449 | 150,079 | 31,825 | 465,600 |

| Less shares repurchased | (144,678) | (2,297,424) | (177,023) | (2,842,843) |

| Net decrease | (104,276) | $ (1,669,760) | (55,315) | $ (977,865) |

| Class K | | | | |

| Shares sold | 141,726 | $ 2,825,381 | 686,516 | $ 14,068,644 |

| Reinvestment of distributions | 7,266 | 147,704 | 29,865 | 548,294 |

| Less shares repurchased | (338,389) | (6,580,262) | (645,560) | (12,968,045) |

Net increase

(decrease) | (189,397) | $ (3,607,177) | 70,821 | $ 1,648,893 |

| Class R | | | | |

| Shares sold | 12,651 | $ 238,569 | 6,871 | $ 139,135 |

| Reinvestment of distributions | 1,483 | 29,531 | 3,316 | 59,948 |

| Less shares repurchased | (8,384) | (164,281) | (22,867) | (443,294) |

Net increase

(decrease) | 5,750 | $ 103,819 | (12,680) | $ (244,211) |

| Class Y | | | | |

| Shares sold | 351,246 | $ 6,960,680 | 715,848 | $ 15,953,745 |

| Reinvestment of distributions | 42,363 | 877,926 | 92,916 | 1,738,188 |

| Less shares repurchased | (399,776) | (8,019,596) | (790,286) | (16,418,102) |

Net increase

(decrease) | (6,167) | $ (180,990) | 18,478 | $ 1,273,831 |

The accompanying notes are an integral part of these financial statements.

24Pioneer Core Equity Fund | Annual Report | 12/31/23

| | Year

Ended

12/31/23 | Year

Ended

12/31/22 | Year

Ended

12/31/21 | Year

Ended

12/31/20 | Year

Ended

12/31/19 |

| Class A | | | | | |

| Net asset value, beginning of period | $ 18.08 | $ 23.39 | $ 22.55 | $ 20.30 | $ 15.93 |

| Increase (decrease) from investment operations: | | | | | |

| Net investment income (loss) (a) | $ 0.21 | $ 0.16 | $ 0.13 | $ 0.16 | $ 0.15 |

| Net realized and unrealized gain (loss) on investments | 3.06 | (4.19) | 5.48 | 4.02 | 4.84 |

| Net increase (decrease) from investment operations | $ 3.27 | $ (4.03) | $ 5.61 | $ 4.18 | $ 4.99 |

| Distributions to shareholders: | | | | | |

| Net investment income | $ (0.22) | $ (0.16) | $ (0.12) | $ (0.15) | $ (0.15) |

| Net realized gain | (0.37) | (1.12) | (4.65) | (1.78) | (0.47) |

| Total distributions | $ (0.59) | $ (1.28) | $ (4.77) | $ (1.93) | $ (0.62) |

| Net increase (decrease) in net asset value | $ 2.68 | $ (5.31) | $ 0.84 | $ 2.25 | $ 4.37 |

| Net asset value, end of period | $ 20.76 | $ 18.08 | $ 23.39 | $ 22.55 | $ 20.30 |

| Total return (b) | 18.19% | (17.24)%(c) | 25.57% | 20.83% | 31.41% |

| Ratio of net expenses to average net assets | 0.88% | 0.87% | 0.88% | 0.90% | 0.90% |

| Ratio of net investment income (loss) to average net assets | 1.08% | 0.81% | 0.54% | 0.78% | 0.80% |

| Portfolio turnover rate | 106% | 75% | 64% | 76% | 93% |

| Net assets, end of period (in thousands) | $1,754,598 | $1,614,739 | $2,121,706 | $1,829,528 | $1,647,120 |

| (a) | The per-share data presented above is based on the average shares outstanding for the period presented. |

| (b) | Assumes initial investment at net asset value at the beginning of each period, reinvestment of all distributions, the complete redemption of the investment at net asset value at the end of each period and no sales charges. Total return would be reduced if sales charges were taken into account. |

| (c) | The class action lawsuit did not have an impact on the total return. |

The accompanying notes are an integral part of these financial statements.

Pioneer Core Equity Fund | Annual Report | 12/31/2325

Financial Highlights (continued)

| | Year

Ended

12/31/23 | Year

Ended

12/31/22 | Year

Ended

12/31/21 | Year

Ended

12/31/20 | Year

Ended

12/31/19 |

| Class C | | | | | |

| Net asset value, beginning of period | $14.47 | $ 19.01 | $19.15 | $17.51 | $ 13.82 |

| Increase (decrease) from investment operations: | | | | | |

| Net investment income (loss) (a) | $ 0.04 | $ 0.01 | $ (0.09)(b) | $ (0.00)† | $ 0.00† |

| Net realized and unrealized gain (loss) on investments | 2.44 | (3.38) | 4.60 | 3.42 | 4.19 |

| Net increase (decrease) from investment operations | $ 2.48 | $ (3.37) | $ 4.51 | $ 3.42 | $ 4.19 |

| Distributions to shareholders: | | | | | |

| Net investment income | $ (0.08) | $ (0.05) | $ — | $ — | $ (0.03) |

| Net realized gain | (0.37) | (1.12) | (4.65) | (1.78) | (0.47) |

| Total distributions | $ (0.45) | $ (1.17) | $ (4.65) | $ (1.78) | $ (0.50) |

| Net increase (decrease) in net asset value | $ 2.03 | $ (4.54) | $ (0.14) | $ 1.64 | $ 3.69 |

| Net asset value, end of period | $16.50 | $ 14.47 | $19.01 | $19.15 | $ 17.51 |

| Total return (c) | 17.27% | (17.76)%(d) | 24.39% | 19.80% | 30.42%(e) |

| Ratio of net expenses to average net assets | 1.67% | 1.57% | 1.81% | 1.70% | 1.69% |

| Ratio of net investment income (loss) to average net assets | 0.28% | 0.09% | (0.41)% | 0.00% † | 0.01% |

| Portfolio turnover rate | 106% | 75% | 64% | 76% | 93% |

| Net assets, end of period (in thousands) | $5,645 | $ 6,460 | $9,539 | $9,484 | $11,208 |

| † | Amount rounds to less than $0.01 or 0.01%. |

| (a) | The per-share data presented above is based on the average shares outstanding for the period presented. |

| (b) | The amount shown for a share outstanding does not correspond with net investment gain (loss) in the Statement of Operations for the period due to timing of the sales and repurchase of shares. |

| (c) | Assumes initial investment at net asset value at the beginning of each period, reinvestment of all distributions, the complete redemption of the investment at net asset value at the end of each period and no sales charges. Total return would be reduced if sales charges were taken into account. |

| (d) | The class action lawsuit did not have an impact on the total return. |

| (e) | If the Fund had not recognized gains in settlement of class action lawsuits during the year ended December 31, 2019, the total return would have been 30.35%. |

The accompanying notes are an integral part of these financial statements.

26Pioneer Core Equity Fund | Annual Report | 12/31/23

| | Year

Ended

12/31/23 | Year

Ended

12/31/22 | Year

Ended

12/31/21 | Year

Ended

12/31/20 | Year

Ended

12/31/19 |

| Class K | | | | | |

| Net asset value, beginning of period | $ 18.08 | $ 23.39 | $ 22.54 | $ 20.28 | $ 15.91 |

| Increase (decrease) from investment operations: | | | | | |

| Net investment income (loss) (a) | $ 0.27 | $ 0.23 | $ 0.21 | $ 0.23 | $ 0.21 |

| Net realized and unrealized gain (loss) on investments | 3.07 | (4.20) | 5.48 | 4.02 | 4.84 |

| Net increase (decrease) from investment operations | $ 3.34 | $ (3.97) | $ 5.69 | $ 4.25 | $ 5.05 |

| Distributions to shareholders: | | | | | |

| Net investment income | $ (0.28) | $ (0.22) | $ (0.19) | $ (0.21) | $ (0.21) |

| Net realized gain | (0.37) | (1.12) | (4.65) | (1.78) | (0.47) |

| Total distributions | $ (0.65) | $ (1.34) | $ (4.84) | $ (1.99) | $ (0.68) |

| Net increase (decrease) in net asset value | $ 2.69 | $ (5.31) | $ 0.85 | $ 2.26 | $ 4.37 |

| Net asset value, end of period | $ 20.77 | $ 18.08 | $ 23.39 | $ 22.54 | $ 20.28 |

| Total return (b) | 18.57% | (16.98)%(c) | 25.93% | 21.23% | 31.85% |

| Ratio of net expenses to average net assets | 0.58% | 0.57% | 0.56% | 0.56% | 0.56% |

| Ratio of net investment income (loss) to average net assets | 1.37% | 1.13% | 0.84% | 1.12% | 1.15% |

| Portfolio turnover rate | 106% | 75% | 64% | 76% | 93% |

| Net assets, end of period (in thousands) | $26,803 | $26,761 | $32,961 | $38,160 | $36,206 |

| (a) | The per-share data presented above is based on the average shares outstanding for the period presented. |

| (b) | Assumes initial investment at net asset value at the beginning of each period, reinvestment of all distributions and the complete redemption of the investment at net asset value at the end of each period. |

| (c) | The class action lawsuit did not have an impact on the total return. |

The accompanying notes are an integral part of these financial statements.

Pioneer Core Equity Fund | Annual Report | 12/31/2327

Financial Highlights (continued)

| | Year

Ended

12/31/23 | Year

Ended

12/31/22 | Year

Ended

12/31/21 | Year

Ended

12/31/20 | Year

Ended

12/31/19 |

| Class R | | | | | |

| Net asset value, beginning of period | $17.87 | $ 23.11 | $22.37 | $20.20 | $15.90 |

| Increase (decrease) from investment operations: | | | | | |

| Net investment income (loss) (a) | $ 0.15 | $ 0.11 | $ 0.06 | $ 0.08 | $ 0.08 |

| Net realized and unrealized gain (loss) on investments | 3.02 | (4.13) | 5.41 | 4.00 | 4.82 |

| Net increase (decrease) from investment operations | $ 3.17 | $ (4.02) | $ 5.47 | $ 4.08 | $ 4.90 |

| Distributions to shareholders: | | | | | |

| Net investment income | $ (0.17) | $ (0.10) | $ (0.08) | $ (0.13) | $ (0.13) |

| Net realized gain | (0.37) | (1.12) | (4.65) | (1.78) | (0.47) |

| Total distributions | $ (0.54) | $ (1.22) | $ (4.73) | $ (1.91) | $ (0.60) |

| Net increase (decrease) in net asset value | $ 2.63 | $ (5.24) | $ 0.74 | $ 2.17 | $ 4.30 |

| Net asset value, end of period | $20.50 | $ 17.87 | $23.11 | $22.37 | $20.20 |

| Total return (b) | 17.84% | (17.43)%(c) | 25.18% | 20.45% | 30.90% |

| Ratio of net expenses to average net assets | 1.18% | 1.11% | 1.16% | 1.24% | 1.25% |

| Ratio of net investment income (loss) to average net assets | 0.77% | 0.55% | 0.23% | 0.40% | 0.43% |

| Portfolio turnover rate | 106% | 75% | 64% | 76% | 93% |

| Net assets, end of period (in thousands) | $1,146 | $ 896 | $1,452 | $ 567 | $ 141 |

| (a) | The per-share data presented above is based on the average shares outstanding for the period presented. |

| (b) | Assumes initial investment at net asset value at the beginning of each period, reinvestment of all distributions and the complete redemption of the investment at net asset value at the end of each period. |

| (c) | The class action lawsuit did not have an impact on the total return. |

The accompanying notes are an integral part of these financial statements.

28Pioneer Core Equity Fund | Annual Report | 12/31/23

| | Year

Ended

12/31/23 | Year

Ended

12/31/22 | Year

Ended

12/31/21 | Year

Ended

12/31/20 | Year

Ended

12/31/19 |

| Class Y | | | | | |

| Net asset value, beginning of period | $ 18.46 | $ 23.84 | $ 22.90 | $ 20.59 | $ 16.14 |

| Increase (decrease) from investment operations: | | | | | |

| Net investment income (loss) (a) | $ 0.26 | $ 0.21 | $ 0.19 | $ 0.21 | $ 0.20 |

| Net realized and unrealized gain (loss) on investments | 3.12 | (4.26) | 5.57 | 4.07 | 4.92 |

| Net increase (decrease) from investment operations | $ 3.38 | $ (4.05) | $ 5.76 | $ 4.28 | $ 5.12 |

| Distributions to shareholders: | | | | | |

| Net investment income | $ (0.26) | $ (0.21) | $ (0.17) | $ (0.19) | $ (0.20) |

| Net realized gain | (0.37) | (1.12) | (4.65) | (1.78) | (0.47) |

| Total distributions | $ (0.63) | $ (1.33) | $ (4.82) | $ (1.97) | $ (0.67) |

| Net increase (decrease) in net asset value | $ 2.75 | $ (5.38) | $ 0.94 | $ 2.31 | $ 4.45 |

| Net asset value, end of period | $ 21.21 | $ 18.46 | $ 23.84 | $ 22.90 | $ 20.59 |

| Total return (b) | 18.42% | (17.04)%(c) | 25.84% | 21.04% | 31.80%(d) |

| Ratio of net expenses to average net assets | 0.66% | 0.66% | 0.65% | 0.67% | 0.66% |

| Ratio of net investment income (loss) to average net assets | 1.29% | 0.99% | 0.76% | 1.03% | 1.03% |

| Portfolio turnover rate | 106% | 75% | 64% | 76% | 93% |

| Net assets, end of period (in thousands) | $31,285 | $27,336 | $34,872 | $26,346 | $26,272 |

| (a) | The per-share data presented above is based on the average shares outstanding for the period presented. |

| (b) | Assumes initial investment at net asset value at the beginning of each period, reinvestment of all distributions and the complete redemption of the investment at net asset value at the end of each period. |

| (c) | If the Fund had not recognized gains from class action proceeds during the year ended December 31, 2022, the total return would have been (17.08)%. |

| (d) | If the Fund had not recognized gains in settlement of class action lawsuits during the year ended December 31, 2019, the total return would have been 31.74%. |

The accompanying notes are an integral part of these financial statements.

Pioneer Core Equity Fund | Annual Report | 12/31/2329

Notes to Financial Statements | 12/31/23

1. Organization and Significant Accounting Policies

Pioneer Core Equity Fund (the “Fund”) is a series of Pioneer Series Trust XI (the “Trust”), a Delaware statutory trust. The Fund is registered under the Investment Company Act of 1940, as amended (the "1940 Act") as a diversified, open-end management investment company. The investment objective of the Fund is to seek long-term capital growth.

The Fund offers five classes of shares designated as Class A, Class C, Class K, Class R and Class Y shares. Each class of shares represents an interest in the same portfolio of investments of the Fund and has identical rights (based on relative net asset values) to assets and liquidation proceeds. Share classes can bear different rates of class-specific fees and expenses, such as transfer agent and distribution fees. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different dividends from net investment income earned by each class. The Amended and Restated Declaration of Trust of the Trust gives the Board of Trustees the flexibility to specify either per-share voting or dollar-weighted voting when submitting matters for shareholder approval. Under per-share voting, each share of a class of the Fund is entitled to one vote. Under dollar-weighted voting, a shareholder’s voting power is determined not by the number of shares owned, but by the dollar value of the shares on the record date. Each share class has exclusive voting rights with respect to matters affecting only that class, including with respect to the distribution plan for that class. There is no distribution plan for Class K or Class Y shares.

Amundi Asset Management US, Inc., an indirect, wholly owned subsidiary of Amundi and Amundi’s wholly owned subsidiary, Amundi USA, Inc., serves as the Fund’s investment adviser (the “Adviser”). Amundi Distributor US, Inc., an affiliate of the Adviser, serves as the Fund’s distributor (the “Distributor”).

The Fund is required to comply with Rule 18f-4 under the 1940 Act, which governs the use of derivatives by registered investment companies. Rule 18f-4 permits funds to enter into derivatives transactions (as defined in Rule 18f-4) and certain other transactions notwithstanding the restrictions on the issuance of “senior securities” under Section 18 of the 1940 Act. Rule 18f-4 requires a fund to establish and maintain a comprehensive derivatives risk management program, appoint a derivatives

risk manager and comply with a relative or absolute limit on fund leverage risk calculated based on value-at-risk (“VaR”), unless the fund uses

30Pioneer Core Equity Fund | Annual Report | 12/31/23

derivatives in only a limited manner (a "limited derivatives user"). The Fund is currently a limited derivatives user for purposes of Rule 18f-4.

The Fund is an investment company and follows investment company accounting and reporting guidance under U.S. Generally Accepted Accounting Principles (“U.S. GAAP”). U.S. GAAP requires the management of the Fund to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of income, expenses and gain or loss on investments during the reporting period. Actual results could differ from those estimates.

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements:

| A. | Security Valuation |

| | The net asset value of the Fund is computed once daily, on each day the New York Stock Exchange (“NYSE”) is open, as of the close of regular trading on the NYSE. |

| | Equity securities that have traded on an exchange are valued by using the last sale price on the principal exchange where they are traded. Equity securities that have not traded on the date of valuation, or securities for which sale prices are not available, generally are valued using the mean between the last bid and asked prices or, if both last bid and asked prices are not available, at the last quoted bid price. Last sale and bid and asked prices are provided by independent third party pricing services. In the case of equity securities not traded on an exchange, prices are typically determined by independent third party pricing services using a variety of techniques and methods. |

| | The value of foreign securities is translated into U.S. dollars based on foreign currency exchange rate quotations supplied by a third party pricing source. Trading in non-U.S. equity securities is substantially completed each day at various times prior to the close of the NYSE. The values of such securities used in computing the net asset value of the Fund's shares are determined as of such times. The Adviser may use a fair value model developed by an independent pricing service to value non-U.S. equity securities. |

| | Shares of open-end registered investment companies (including money market mutual funds) are valued at such funds' net asset value. |

| | Securities for which independent pricing services or broker-dealers are unable to supply prices or for which market prices and/or quotations are not readily available or are considered to be unreliable are valued by a |

Pioneer Core Equity Fund | Annual Report | 12/31/2331

| | fair valuation team comprised of certain personnel of the Adviser. The Adviser is designated as the valuation designee for the Fund pursuant to Rule 2a-5 under the 1940 Act. The Adviser’s fair valuation team is responsible for monitoring developments that may impact fair valued securities. |

| | Inputs used when applying fair value methods to value a security may include credit ratings, the financial condition of the company, current market conditions and comparable securities. The Adviser may use fair value methods if it is determined that a significant event has occurred after the close of the exchange or market on which the security trades and prior to the determination of the Fund's net asset value. Examples of a significant event might include political or economic news, corporate restructurings, natural disasters, terrorist activity or trading halts. Thus, the valuation of the Fund's securities may differ significantly from exchange prices, and such differences could be material. |

| B. | Investment Income and Transactions |

| | Dividend income is recorded on the ex-dividend date, except that certain dividends from foreign securities where the ex-dividend date may have passed are recorded as soon as the Fund becomes aware of the ex-dividend data in the exercise of reasonable diligence. |

| | Interest income, including interest on income-bearing cash accounts, is recorded on the accrual basis. Dividend and interest income are reported net of unrecoverable foreign taxes withheld at the applicable country rates and net of income accrued on defaulted securities. |

| | Interest and dividend income payable by delivery of additional shares is reclassified as PIK (payment-in-kind) income upon receipt and is included in interest and dividend income, respectively. |

| | Security transactions are recorded as of trade date. Gains and losses on sales of investments are calculated on the identified cost method for both financial reporting and federal income tax purposes. |

| C. | Foreign Currency Translation |

| | The books and records of the Fund are maintained in U.S. dollars. Amounts denominated in foreign currencies are translated into U.S. dollars using current exchange rates. |

| | Net realized gains and losses on foreign currency transactions, if any, represent, among other things, the net realized gains and losses on foreign currency exchange contracts, disposition of foreign currencies |

32Pioneer Core Equity Fund | Annual Report | 12/31/23

| | and the difference between the amount of income accrued and the U.S. dollars actually received. Further, the effects of changes in foreign currency exchange rates on investments are not segregated on the Statement of Operations from the effects of changes in the market prices of those securities, but are included with the net realized and unrealized gain or loss on investments. |

| D. | Federal Income Taxes |

| | It is the Fund's policy to comply with the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute all of its net taxable income and net realized capital gains, if any, to its shareholders. Therefore, no provision for federal income taxes is required. As of December 31, 2023, the Fund did not accrue any interest or penalties with respect to uncertain tax positions, which, if applicable, would be recorded as an income tax expense on the Statement of Operations. Tax returns filed within the prior three years remain subject to examination by federal and state tax authorities. |

| | The amount and character of income and capital gain distributions to shareholders are determined in accordance with federal income tax rules, which may differ from U.S. GAAP. Distributions in excess of net investment income or net realized gains are temporary over distributions for financial statement purposes resulting from differences in the recognition or classification of income or distributions for financial statement and tax purposes. Capital accounts within the financial statements are adjusted for permanent book/tax differences to reflect tax character, but are not adjusted for temporary differences. |

| | A portion of the dividend income recorded by the Fund is from distributions by publicly traded real estate investment trusts (“REITs”), and such distributions for tax purposes may also consist of capital gains and return of capital. The actual return of capital and capital gains portions of such distributions will be determined by formal notifications from the REITs subsequent to the calendar year-end. Distributions received from the REITs that are determined to be a return of capital are recorded by the Fund as a reduction of the cost basis of the securities held and those determined to be capital gain are reflected as such on the Statement of Operations. |

| | At December 31, 2023, the Fund was permitted to carry forward indefinitely $1,823,589 of short-term losses and $0 of long-term losses. |

Pioneer Core Equity Fund | Annual Report | 12/31/2333

| | The tax character of distributions paid during the years ended December 31, 2023 and December 31, 2022, was as follows: |

| | 2023 | 2022 |

| Distributions paid from: | | |

| Ordinary income | $18,862,994 | $ 19,026,991 |

| Long-term capital gains | 32,051,605 | 94,909,536 |

| Total | $ 50,914,599 | $113,936,527 |

The following shows the components of distributable earnings (losses) on a federal income tax basis at December 31, 2023:

| | 2023 |

| Distributable earnings/(losses): | |

| Undistributed ordinary income | $ 484,854 |

| Capital loss carryforward | (1,823,589) |

| Net unrealized appreciation | 374,733,751 |

| Total | $ 373,395,016 |

The difference between book-basis and tax-basis unrealized appreciation is attributable to the tax deferral of losses on wash sales.

As of the date of this report, a significant portion of the Fund’s net asset value is attributable to net unrealized capital gains on portfolio securities. If the Fund realizes capital gains in excess of realized capital losses in any fiscal year, it makes capital gain distributions to shareholders. You may receive distributions that are attributable to appreciation that was present in the Fund’s portfolio securities at the time you made your investment but had not been realized at that time, or that are attributable to capital gains or other income that, although realized by the Fund, had not yet been distributed at the time you made your investment. Unless you purchase shares through a tax-advantaged account, these distributions will be taxable to you even though they economically represent a return of a portion of your investment. You may want to avoid buying shares when the Fund is about to declare a dividend or capital gain distribution. You should consult your tax adviser before buying shares no matter when you are investing.

| E. | Fund Shares |

| | The Fund records sales and repurchases of its shares as of trade date. The Distributor earned $23,848 in underwriting commissions on the sale of Class A shares during the year ended December 31, 2023. |

34Pioneer Core Equity Fund | Annual Report | 12/31/23

| F. | Class Allocations |

| | Income, common expenses and realized and unrealized gains and losses are calculated at the Fund level and allocated daily to each class of shares based on its respective percentage of adjusted net assets at the beginning of the day. |

| | Distribution fees are calculated based on the average daily net asset value attributable to Class A, Class C and Class R shares of the Fund, respectively (see Note 5). Class K and Class Y shares do not pay distribution fees. All expenses and fees paid to the Fund's transfer agent for its services are allocated among the classes of shares based on the number of accounts in each class and the ratable allocation of related out-of-pocket expenses (see Note 4). |

| | Distributions to shareholders are recorded as of the ex-dividend date. Distributions paid by the Fund with respect to each class of shares are calculated in the same manner and at the same time, except that net investment income dividends to Class A, Class C, Class K, Class R and Class Y shares can reflect different transfer agent and distribution expense rates. |

| G. | Risks |

| | The value of securities held by the Fund may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political or regulatory conditions, recessions, the spread of infectious illness or other public health issues, inflation, changes in interest rates, armed conflict such as between Russia and Ukraine or in the Middle East, sanctions against Russia, other nations or individuals or companies and possible countermeasures, lack of liquidity in the bond markets or adverse investor sentiment. In the past several years, financial markets have experienced increased volatility, depressed valuations, decreased liquidity and heightened uncertainty. These conditions may continue, recur, worsen or spread. Inflation and interest rates have increased and may rise further. These circumstances could adversely affect the value and liquidity of the Fund's investments and negatively impact the Fund's performance. |

| | The long-term impact of the COVID-19 pandemic and its subsequent variants on economies, markets, industries and individual issuers, are not known. Some sectors of the economy and individual issuers have experienced or may experience particularly large losses. Periods of extreme volatility in the financial markets, reduced liquidity of many instruments, increased government debt, inflation, and disruptions to supply chains, consumer demand and employee availability, may |

Pioneer Core Equity Fund | Annual Report | 12/31/2335

| | continue for some time. Following Russia's invasion of Ukraine, Russian securities lost all, or nearly all, their market value. Other securities or markets could be similarly affected by past or future political, geopolitical or other events or conditions. |

| | Governments and central banks, including the U.S. Federal Reserve, have taken extraordinary and unprecedented actions to support local and global economies and the financial markets. These actions have resulted in significant expansion of public debt, including in the U.S. The consequences of high public debt, including its future impact on the economy and securities markets, may not be known for some time. |

| | The U.S. and other countries are periodically involved in disputes over trade and other matters, which may result in tariffs, investment restrictions and adverse impacts on affected companies and securities. For example, the U.S. has imposed tariffs and other trade barriers on Chinese exports, has restricted sales of certain categories of goods to China, and has established barriers to investments in China. Trade disputes may adversely affect the economies of the U.S. and its trading partners, as well as companies directly or indirectly affected and financial markets generally. If the political climate between the U.S. and China does not improve or continues to deteriorate, if China were to attempt unification of Taiwan by force, or if other geopolitical conflicts develop or get worse, economies, markets and individual securities may be severely affected both regionally and globally, and the value of the Fund's assets may go down. |

| | At times, the Fund’s investments may represent industries or industry sectors that are interrelated or have common risks, making the Fund more susceptible to any economic, political, or regulatory developments or other risks affecting those industries and sectors. |

| | Normally, the Fund invests at least 80% of its net assets (plus the amount of borrowings, if any, for investment purposes) in equity securities, primarily of U.S. issuers. |

| | The Fund may invest in REIT securities, the value of which can fall for a variety of reasons, such as declines in rental income, fluctuating interest rates, poor property management, environmental liabilities, uninsured damage, increased competition, or changes in real estate tax laws. |

| | The Fund’s investments in foreign markets and countries with limited developing markets may subject the Fund to a greater degree of risk than investments in a developed market. These risks include disruptive political or economic conditions, military conflicts and sanctions, terrorism, sustained economic downturns, financial instability, less |

36Pioneer Core Equity Fund | Annual Report | 12/31/23