We make things work for you.

Public Service Enterprise Group

Presentation to the Financial Community

New York, New York

March 18, 2009

Forward-Looking Statement

Readers are cautioned that statements contained in this presentation about our and our subsidiaries’ future performance, including future revenues, earnings, strategies, prospects and all other statements that are not purely historical, are forward-looking statements for purposes of the safe harbor provisions under The Private Securities Litigation Reform Act of 1995. Although we believe that our expectations are based on reasonable assumptions, we can give no assurance they will be achieved. The results or events predicted in these statements may differ materially from actual results or events. Factors which could cause results or events to differ from current expectations include, but are not limited to:

Adverse changes in energy industry, policies and regulation, including market structures and rules.

Any inability of our energy transmission and distribution businesses to obtain adequate and timely rate relief and regulatory approvals from federal and state regulators.

Changes in federal and state environmental regulations that could increase our costs or limit operations of our generating units.

Changes in nuclear regulation and/or developments in the nuclear power industry generally, that could limit operations of our nuclear generating units.

Actions or activities at one of our nuclear units that might adversely affect our ability to continue to operate that unit or other units at the same site.

Any inability to balance our energy obligations, available supply and trading risks.

Any deterioration in our credit quality.

Availability of capital and credit at reasonable pricing terms and our ability to meet cash needs.

Any inability to realize anticipated tax benefits or retain tax credits.

Increases in the cost of or interruption in the supply of fuel and other commodities necessary to the operation of our generating units.

Delays or cost escalations in our construction and development activities.

Adverse investment performance of our decommissioning and defined benefit plan trust funds, and changes in discount rates and funding requirements.

Changes in technology and increased customer conservation.

For further information, please refer to our Annual Report on Form 10-K, including Item 1A. Risk Factors, and subsequent reports on Form 10-Q and Form 8-K filed with the Securities and Exchange Commission. These documents address in further detail our business, industry issues and other factors that could cause actual results to differ materially from those indicated in this presentation. In addition, any forward-looking statements included herein represent our estimates only as of today and should not be relied upon as representing our estimates as of any subsequent date. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so, even if our internal estimates change, unless otherwise required by applicable securities laws.

Delivering Value: Today and Tomorrow

2

GAAP Disclaimer

PSEG presents Operating Earnings in addition to its Net Income reported

in accordance with accounting principles generally accepted in the United

States (GAAP). Operating Earnings is a non-GAAP financial measure that

differs from Net Income because it excludes the impact of the sale of

certain non-core domestic and international assets and material

impairments and lease-transaction-related charges. PSEG presents

Operating Earnings because management believes that it is appropriate

for investors to consider results excluding these items in addition to the

results reported in accordance with GAAP. PSEG believes that the non-

GAAP financial measure of Operating Earnings provides a consistent and

comparable measure of performance of its businesses to help

shareholders understand performance trends. This information is

not intended to be viewed as an alternative to GAAP information. The last

slide in this presentation includes a list of items excluded from Net Income

to reconcile to Operating Earnings, with a reference to that slide included

on each of the slides where the non-GAAP information appears.

Delivering Value: Today and Tomorrow

3

Agenda

Stephen Byrd

PSEG Energy Holdings – Review and Outlook

9:00 – 9:30

PSE&G and PSEG Energy Holdings – Q&A

9:30 – 9:45

Presenter

Presentation

Time

Ralph Izzo

Summary and Q&A

Tom O’Flynn

PSEG Financial Review and Outlook

11:45 – 12:15

Dan Cregg

PSEG Power – Financial Outlook

11:15 – 11:45

Joe Hopf

PSEG Power – Market Overview

10:45 – 11:15

Bill Levis

PSEG Power – Review and Outlook

10:00 – 10:45

BREAK

Ralph LaRossa

PSE&G – Review and Outlook

8:30 – 9:00

Ralph Izzo

PSEG Strategic Overview

8:00 – 8:30

Kathleen Lally

Welcome / Introduction

8:00

Delivering Value: Today and Tomorrow

4

We make things work for you.

PSEG - Review and Outlook

Ralph Izzo

Chairman, President and Chief Executive Officer

Public Service Enterprise Group …

… an energy provider

meeting the needs of customers

and shareholders.

Meeting

Commitments

Delivering

Value Today

Positioned for

the Future

Delivering Value: Today and Tomorrow

6

PSEG: Establishing a foundation…

Meeting Commitments

Achieved earnings targets

Operational excellence drove results

Sharpened business focus; international assets sold

Balance sheet strengthened; credit outlook improved

Attractive dividend growth rate

… and building a record that sets us apart.

Delivering Value: Today and Tomorrow

7

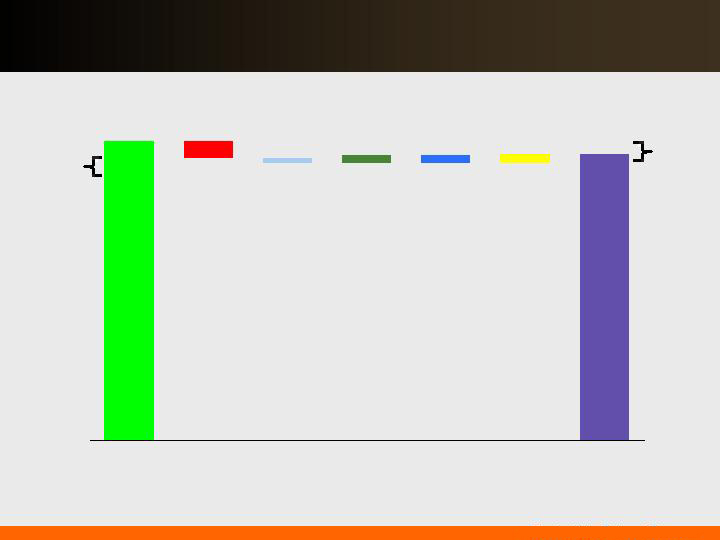

2006 Operating

Earnings*

2007 Operating

Earnings*

2008 Operating

Earnings*

$2.72

$1.72

$2.92

$1.72

$1.87

$2.57

$2.72

$2.80

$3.05

We have achieved the targets we set for earnings...

… despite the turmoil of recent years.

Guidance

Range

Guidance

Range

Guidance

Range

*See page 139 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings

Initial

Guidance

$2.30

$2.50

**

**2008 Operating results include ($0.11) impact from NDT and MTM

Delivering Value: Today and Tomorrow

8

PSEG Power’s focus on operational excellence…

… resulted in a record year of power generation.

30,000

40,000

50,000

60,000

50

75

100

0

25

50

Total Generation (GWh)

Nuclear Capacity

Factor (%)

Combined Cycle

Capacity Factor (%)

2007

2008

2007

2008

2007

2008

Delivering Value: Today and Tomorrow

9

PSE&G’s focus on operational excellence…

0.5

1.0

2005

2006

2007

2008

50

60

70

80

2005

2006

2007

2008

90%

95%

100%

2005

2006

2007

2008

0%

50%

100%

2005

2006

2007

2008

SAIFI

CAIDI

Gas Leak Response Rate

General Inquiry Service Level

Top Quartile Benchmark

PSE&G Performance

… continued a tradition of industry-leading reliability.

Delivering Value: Today and Tomorrow

10

A focus on value …

… producing a strong financial base.

Sale of international

assets yielded

$ 1.5B over 2007-

2008.

Debt reduced $1.8B*.

Stable credit

outlook achieved.

Improved credit

metrics.

* $1.8B reduction at Enterprise and PSEG Energy Holdings over 2007-2008.

Delivering Value: Today and Tomorrow

11

Making decisions and achieving results…

… to strengthen operational and financial position.

Delivering Value Today

2009 earnings guidance represents continued

growth

Operational excellence improving results

Core business investments providing attractive

returns

Dividend increased – 6th consecutive year; 102nd

year of paying an annual dividend

Strong financial position – credit metrics, liquidity

Delivering Value: Today and Tomorrow

12

Strong operations and risk controls…

… position us to meet challenges of today’s market.

Asset optimization yielding

results

Forecasting record power generation

for 2009

Power’s BET (Back-end Technology)

construction on time, on budget

7th successful BGS auction insulates

Power from market volatility

On track to achieve

earnings growth in 2009.

Guidance maintained at

$3.00 - $3.25.

Investment focus on projects

with attractive risk-adjusted

returns

iPower installation on track

Infrastructure

Energy Efficiency

Solar

Delivering Value: Today and Tomorrow

13

… continues 102-year history of paying common dividends.

70%

44%

Payout

Ratio

41% - 44%

43%

66%

63%

$1.10

$1.12

$1.33

$1.17

$1.29

$1.14

2004

2005

2006

2007

2008

2009E

*Indicated annual dividend rate

*

Dividends per Share

Sixth consecutive annual increase in common dividend …

Delivering Value: Today and Tomorrow

14

Operational excellence, financial strength and disciplined investment …

Positioned for the Future

… support shareholder value.

Balanced business mix

BGS: A demonstrated mechanism for meeting

customer supply at market prices for multi-year period

Federal and State policies provide opportunities for

growth – Leadership position in energy policy

T&D investments providing growth with minimal rate

impact

Strong financial position and cash flow provide

flexibility in volatile markets – No need to issue equity

Delivering Value: Today and Tomorrow

15

Energy Policy has moved to the forefront of the national agenda.

PSEG is well-situated to respond.

“No single issue is as fundamental to our future

as energy.”

- President Obama, January 26, 2009

“By embracing new approaches to energy, we are providing the

pathway to both economic prosperity and environmental

protection.”

- Governor Jon Corzine, October 22, 2008

Delivering Value: Today and Tomorrow

16

Anticipate Congressional action in energy legislation…

Energy legislation emphasis

Renewable Portfolio Standard

Transmission expansion

Smart grid investments

Carbon legislation drivers for action

EPA – States – International negotiations

Congress looking for simplicity

Obama Administration’s 10-year budget proposal

includes $645 billion from emission allowances, or $12 –

$15/ton in 2012 and increasing to $15 - $20/ton in 2020

… which could be combined with federal carbon legislation.

Delivering Value: Today and Tomorrow

17

PSEG establishing a policy leadership position …

Power LLC

Energy Holdings

Electric and Gas

Delivery

Leveraged Leases and

Renewable Investments

Regional

Wholesale Energy

… in promoting a sustainable energy future.

PSE&G positioned to

meet NJ’s energy policy

and economic growth

objectives with $1.7

billion investment

program.

PSEG Power’s low-cost

baseload nuclear fleet

well-positioned in

carbon constrained

environment.

PSEG Energy Holdings

positioned to pursue

attractive renewable

generation opportunities.

Compressed Air Energy

Storage (CAES)

Solar

Offshore wind

Delivering Value: Today and Tomorrow

18

PSEG leadership recognized

Named one of the Most

Admired Companies,

2007 & 2008

Dow Jones

Sustainability Indexes

One of 125 companies

named to DJSI North

America and one of only

10 U.S. electric

companies included

ALL BUSINESS

ALL NEW JERSEY

Corporation of the year 2007

One of the 400 best

big companies, 2008

PSE&G named America’s Most

Reliable Utility

Mid-Atlantic Region

winner for the 7th straight year

PSEG Chairman

Ralph Izzo named

CEO of the year

Carbon Disclosure

Leadership Index 2008

2008 Balanced Scorecard

Achievement Award

Solar electric power association

Delivering Value: Today and Tomorrow

19

PSEG – Delivering Value: Today and Tomorrow

Delivering

Value Today

Positioned for

the Future

Achieved earnings targets

Operational excellence

drove results

Sharpened business focus;

international assets sold

Balance sheet

strengthened; credit

outlook improved

Attractive dividend growth

rate

2009 earnings guidance

represents continued

growth

Operational excellence

improving results

Core business

investments providing

attractive returns

Dividend increased – 6th

consecutive year; 102nd

year of paying an annual

dividend

Strong financial position

– credit metrics, liquidity

Balanced business mix

BGS: A demonstrated

mechanism for meeting

customer supply at market

prices for multi-year period

Federal and State policies

provide opportunities for

growth – Leadership position

in energy policy

T&D investments providing

growth with minimal rate

impact

Strong financial position and

cash flow provide flexibility in

volatile markets – No need to

issue equity

Meeting

Commitments

Delivering Value: Today and Tomorrow

20

Operational excellence, financial strength and disciplined investment…

… position us well in today’s market.

Low payout ratio and strong balance sheet provide support

Is dividend secure?

Strong balance sheet, credit metrics and liquidity

What is the impact of

credit market stress?

Strong cash flow well in excess of PSE&G’s equity

requirements

Do you need equity?

Carbon friendly

Federal and State Policy initiatives support capital plans

How is PSEG affected

by policy changes?

Multi-year hedging profile supported by core assets

Asset balance dampens relative fuel price volatility

Capacity markets provide stability

What’s the impact of

commodity volatility?

PSE&G current/pending rate needs equal 2-4% impact

BGS supply generally priced at market

What is impact on

customer from capital

programs?

PSEG Position

Market’s Questions

Delivering Value: Today and Tomorrow

21

PSE&G - Review and Outlook

We make things work for you.

Ralph LaRossa

President and Chief Operating Officer, PSE&G

Earnings targets met

Transmission formula rate

treatment received from

FERC

Strong O&M control

Reduced Distribution capital

expenditures

National ReliabilityOne

Award winner

Earnings on track to meet

2009 guidance

Distribution base rate case

filing mid-2009 to address

capital and O&M recovery

Transmission investment

increasing

New customer information

system to go-live end of 1st

quarter

Active participant in shaping

State energy policy

Prepared to meet NJ’s

stimulus and energy goals

Resolve Distribution base

rate case by mid-2010

Investment program

responsive to NJ’s

economic and energy-

related goals

Transmission formula rates

provide current return on

invested capital

Earnings growth in line with

capital investment

Continue to lead the nation

in electric reliability

PSE&G – Delivering Value: Today and Tomorrow

Delivering

Value Today

Positioned for

the Future

Meeting

Commitments

Delivering Value: Today and Tomorrow

23

PSE&G met earnings targets…

… through fair rate treatment and diligent O&M management.

2007 Operating

Earnings*

Sales

Weather

O&M

Depreciation,

Interest and

Other

Taxes

2008 Operating

Earnings*

$350M

$370M

Guidance

Range

$330M

$350M

Guidance

Range

$376M

($21M)

($7M)

$10M

($9M)

$11M

$360M

*See page 139 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings

Delivering Value: Today and Tomorrow

24

Regulatory decisions…

PSE&G’s revenues fall under the regulatory jurisdiction of:

NJ Board of Public Utilities (BPU)

Commission has jurisdiction over Electric and Gas Distribution and

Energy Master Plan investments

Anticipate filing Electric and Gas base rate case in mid-2009

Last base rate case resulted in settlement effective November 2006

Federal Energy Regulatory Commission (FERC)

Commission has jurisdiction over Electric Transmission revenues

Formula rate treatment for Transmission effective on October 1,

2008 with true-up adjustments for operating and maintenance

expense and capital on annual basis

Allowed ROE of 11.68%

Additional incentive of 1.25% ROE for Susquehanna-to-Roseland

investment

… have provided PSE&G the opportunity to earn a fair return.

Delivering Value: Today and Tomorrow

25

PSE&G refocused its investments in late 2008 in response to the 4th quarter market stress.

PSE&G’s current investment plan…

34%

51%

15%

0%

30%

1%

20%

49%

32%

17%

1%

50%

… provides for growth in rate base of 9% which drives solid growth

in earnings from 2009 – 2011 of 13% - 14%.

PSE&G Rate Base

28%

25%

1%

46%

Electric Transmission

Electric Distribution

Gas Distribution

Energy Master Plan

2008

Rate Base $6.9B

Equity Ratio ~ 50%

2009

Rate Base $7.4B

Equity Ratio ~ 51%*

2010

Rate Base $8.0B

Equity Ratio ~ 51%*

2011

Rate Base $8.8B

Equity Ratio ~ 51%*

*Pending regulatory approval

Delivering Value: Today and Tomorrow

26

0

100

200

300

400

500

600

2007

2008

2009

2010

2011

Reliability Performance Metrics compared to

Peer Panel have been Top Quartile since:

National ReliabilityOne

Award winner three of

the last four years

… and focusing investment to achieve top quartile reliability performance.

PSE&G Base* O&M

2004

CAIDI

2006

Damages per Locate 1,000 Requests

2000

Leak Response Rate

2003

Gas Leak Reports per Mile

2004

MAIFI (Excluding Major Storms)

2000

SAIFI (Excluding Major Storms)

CAGR

2007 – 2011: 0.6%

2008 – 2011: 2.0%

PSE&G manages O&M growth by capturing productivity gains…

*Excludes pension, EMP and revenue generating expenses

Delivering Value: Today and Tomorrow

27

2008 Operating

Earnings*

Weather

Transmission

Pension

Depreciation,

Interest and Other

2009 Guidance

$360M

$5 - 10M

$320 –

$345M

$10 - 15M

… increasing pension, depreciation and interest costs.

($40 - 35M)

($15 - 5M)

In 2009, controlling O&M will mitigate the effects of…

*See page 139 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings

Delivering Value: Today and Tomorrow

28

PSE&G – Business Drivers

Operational excellence and effective cost

management

Distribution rate case should improve

2009 ROE’s of 8.0% - 8.8% to 9.0% - 9.5%

Addresses capital investment, O&M and

sales losses

1% change in Distribution rate case ROE for

2010 = ~$21M change in earnings

Transmission Investment under formula

rates. ROE ~ 11.7%

Capital Stimulus could provide an

additional 25 – 50 basis points to ROE

Energy Master Plan investments for

Energy Efficiency and Renewables could

provide an additional 5 – 10 basis points

to ROE if approved as planned.

A ±1% deviation in sales would result in a

±$15M change to margin revenues

$320 – $345M

2009 Guidance

2010+ Drivers

Delivering Value: Today and Tomorrow

29

PSE&G has been working with key stakeholders…

Federal

Collaborated with EEI and NRDC on key energy positions for

the American Recovery and Reinvestment Act of 2009

State

Worked with the Governor’s office and the New Jersey BPU to

craft programs that would create jobs and stimulate the New

Jersey economy

Worked with solar developers and the New Jersey BPU on

“Solar 4 All” program that will help the state meet aggressive

requirements for renewable portfolio standards

Working with key legislators on Rate Stabilization legislation

that will correct deficiencies in the current rate making process

Federal and State

Secured additional LIHEAP and NJ SHARES funding to assist

customers with energy bills

… to guide rulemaking.

Delivering Value: Today and Tomorrow

30

2008 Regulatory Activities

A.

Solar Loan Program

($105M)

Approved April 2008

Up to 30MW

B.

Demand Response

($63M)

Filed August 2008. Decision

pending

Reduce demand by residential

and small commercial

customers by 150MW

C.

Carbon Abatement

Program ($47M)

Approved December 2008

Provides energy efficiency

programs

A

C

B

2009 Regulatory Activities

D.

Capital Economic Stimulus Infrastructure Investment

Program ($700M)

Filed January 2009, expected BPU decision in April 2009

Accelerate capital investments to promote economic stimulus and

promote job growth in NJ

E.

Solar Loan Program – Phase II

To be filed March 2009

F.

File Electric and Gas Distribution

base rate case

To be filed mid-2009

G.

Energy Efficiency Economic Stimulus Program

($200M)

Filed January 2009, expected BPU decision by mid-year 2009

Promote job growth and stimulate NJ economy via energy

efficiency expenditures

H.

Solar 4 All ($800M)

Filed February 2009, expected BPU decision by August 2009

120MW of utility-owned solar generation

D

E

G

H

I

2010 Regulatory Activities

I.

Resolve Electric and

Gas Distribution

base rate case

Normal BPU schedule would

have resolution of rate

proceeding by mid-2010

2011 will be first full year of

rate relief

2008

2009

2010

May

Dec

Dec

Jan

Jan

Jun

F

… with a manageable rate increase of 2% - 4% to customers.

$215M Filed

PSE&G is well positioned to respond to NJ’s needs…

Delivering Value: Today and Tomorrow

31

0

100

200

300

400

500

600

700

800

2009

2010

2011

Capital Infrastructure Stimulus

Energy Efficiency Stimulus

Solar II

Solar 4 All

… have potential to add 10% - 15% a year to earnings through 2011.

PSE&G Annual Potential Capital Investments

Rate Base Including Potential Investments

31%

4%

18%

47%

28%

22%

5%

45%

Electric Transmission

Electric Distribution

Gas Distribution

Energy Master Plan

$9.8B

$8.8B

2011

2010

An additional ~$1.4B of

investments to be added

2009-2011 if appropriate

regulatory treatment is

received

Filed positions:

10.3% ROE

51% Equity Ratio

PSE&G’s additional investment proposals …

Delivering Value: Today and Tomorrow

32

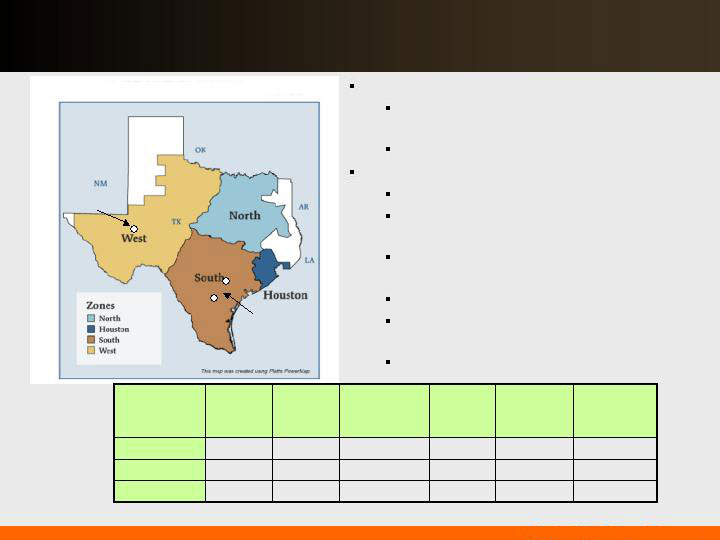

Projects to NY

Neptune HVDC project (685 MW)

Sayreville to Long Island

Linden VFT project (330 MW) Linden

to Staten Island

Bergen O66 project (670 MW)

Bergen to ConEd’s West 49th St

Roseland U2-046 HVDC project

(660MW) to ConEd’s West 49th St

Deans U2-047 HVDC project

(660MW) to Long Island

The Linden VFT project U2-077 (300

MW) Linden to NY

Bergen U2-100 project (1,000 MW)

connecting Bergen to NY

Projects to NJ

PSE&G’s evaluation of

the proposed backbone

Transmission projects:

Susquehanna -

Roseland

AEP Interstate-765

project into Deans

MidAtlantic Power

Pathway project into

Salem

As a result NJ will need new generation, DSM or additional

transmission imports.

Total Import

Capability

~ 5,000 MW

Total Export

Capability

~ 4,300 MW

2009-2019 NJ Summer Peak

Growth Rate = 1.7%

Sources: Imports: PSE&G Estimates; Exports: PJM 2008 RTEP; Load Growth: PJM 2009 Load Forecast Report

NJ’s load is expected to grow 3,800MW by 2019, with net imports

increasing ~700MW.

Delivering Value: Today and Tomorrow

33

Transmission Growth

PJM approved the $750M Susquehanna to

Roseland line in October 2007

Siting and permitting process underway

Incentives approved by FERC:

ROE: 12.93% (125 basis point adder)

100% CWIP in Rate Base

FERC approval of Sub-Transmission to

Transmission system reliability investments

represents about $340M through 2011, post-2011

~$60M per year

Other approved RTEP projects ~$250M also

contribute meaningfully to improved reliability and

earnings growth

PJM approved the Branchburg-Roseland-Hudson

line in November 2008. Additional 500 kV

investments brings potential capital expenditures to

approximately $1.0 -1.5B

These opportunities will require substantial deployment of capital with siting

and permitting as the major challenges.

Branchburg

Roseland

Jefferson

New Freedom

Smithburg

Deans

MAPP

Hope Creek

Salem

Project

I-765

Interstate

Project

PSE&G implemented fully-forecasted formula rates with an 11.68%

base ROE, which provides attractive current return on investments.

Delivering Value: Today and Tomorrow

34

18.5

0

2

4

6

8

10

12

14

16

18

20

PSE&G

Average

2011

Based on tariff rates in effect in Nov 2008, does not include effects of the BGSS decreases effective Jan 1, 2009 and March 1, 2009.

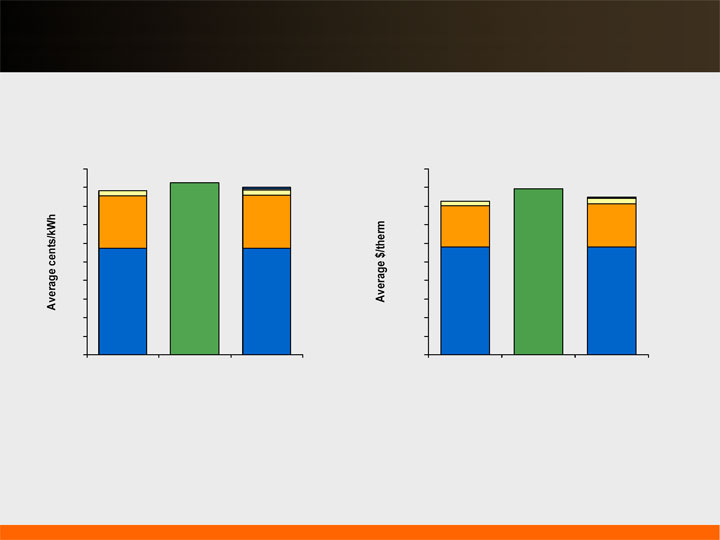

… produces superior value to our electric and gas customers.

Electricity

(500kWh/month bill)

BGS

Delivery

Clauses

17.7

1.79

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

PSE&G

Average

2011

Gas

(100 therm/month bill)

BGSS

Delivery

Clauses

1.65

Source: Rates from PSE&G, NYPSC and PAPUC

1.70

BGSS

Delivery *

Clauses

BGS***

Delivery *

Clauses

Potential

Investments**

18.1

* Includes base rate increases

** Includes NJ stimulus filing (Capital and EEE), Solar 4 All and Solar II

Potential

Investments**

*** Assumes BGS/BGSS pricing remains constant

Combining operational excellence with prices comparable to

regional competitors …

Delivering Value: Today and Tomorrow

35

Earnings targets met

Transmission formula rate

treatment received from

FERC

Strong O&M control

Reduced Distribution capital

expenditures

National ReliabilityOne

Award winner

Earnings on track to meet

2009 guidance

Distribution base rate case

filing mid-2009 to address

capital and O&M recovery

Transmission investment

increasing

New customer information

system to go-live end of 1st

quarter

Active participant in shaping

State energy policy

Prepared to meet NJ’s

stimulus and energy goals

Resolve Distribution base

rate case by mid-2010

Investment program

responsive to NJ’s

economic and energy-

related goals

Transmission formula rates

provide current return on

invested capital

Earnings growth in line with

capital investment

Continue to lead the nation

in electric reliability

PSE&G – Delivering Value: Today and Tomorrow

Delivering

Value Today

Positioned for

the Future

Meeting

Commitments

Delivering Value: Today and Tomorrow

36

We make things work for you.

PSEG Energy Holdings -

Review and Outlook

Stephen Byrd

President and Chief Operating Officer, PSEG Energy Holdings

PSEG Energy Holdings – Delivering Value: Today and Tomorrow

Exceeded earnings

targets

Strong 2008 Texas

performance well

above expectations

Stable earnings from

US contracted

generation assets

Sale of international

assets yielded $1.5B over

2007-2008

Proactively reserved for

potential LILO/SILO

liability

Earnings on track to meet

2009 guidance

Achieving predictable

performance from

contracted US generation

assets

Improving Texas

operations via asset

management agreement

with PSEG Power

Redeemed approximately

$280M of Texas project

debt in the first quarter of

2009

Managing risk by limiting

growth in lease tax liability

Sufficient liquidity and

credit strength to fund

potential LILO/SILO liability

through cash, asset value

and debt capacity

Exploring opportunities to

optimize other U.S. assets

Pursuing attractive

renewable generation

opportunities

Compressed Air

Energy Storage

(CAES)

Solar

Offshore Wind

Meeting

Commitments

Delivering

Value Today

Positioned for

the Future

Delivering Value: Today and Tomorrow

38

PSEG Energy Holdings will continue to maximize the value of its

investment portfolio, …

PSEG Energy Holdings operates through two

primary subsidiaries:

PSEG Global

Owns approximately 2,400 MW of

domestic generation capacity

2,000 MW merchant CC in TX

400 MW contracted in CA, HI, NH

Small remaining international

investments with a total book value of

under $25M

Pursues unregulated renewables

opportunities: CAES, solar and

offshore wind

PSEG Resources

Generates earnings and cash from

lease investments (primarily in

energy-related assets)

Continues to opportunistically

monetize investments as appropriate

… while identifying opportunities for growth driven by climate change.

PSEG Energy Holdings

2009 Operating Earnings Guidance

$0 – $20M

TOTAL

($10 – 20)

PSEG Resources

$15 – $35

PSEG Texas

($5) – $5

PSEG Global

(excluding Texas)

2009 Operating Earnings Guidance

Delivering Value: Today and Tomorrow

39

By reducing its investment in international assets …

… Holdings has decreased its risk profile and improved its

business focus.

$0.4

$0.5

$0.5

$0.8

$2.2

$1.4

$0.1

2004

2006

2008

2009 Projected*

PSEG Global Invested Capital

($ Billions)

$2.6B

$1.9B

$0.6B

$0.8B

*Investment Includes redemption of Texas debt in February 2009

International

Domestic

Delivering Value: Today and Tomorrow

40

Texas assets are the major driver of PSEG Global’s business

results.

PSEG Texas projected EBITDA reflects higher maintenance costs and

market uncertainty.

Strong 2008 performance from favorable market in Spring 2008

Looking ahead to 2009:

Uncertainty on gross margin impact from new wind additions

Operations and maintenance costs approximately $20M higher in 2009 than 2007 as

plants enter periods of major maintenance

Longer-term:

Continued uncertainty from wind

Positive impact from transmission build-up and potential unit mothballing by other

generators

70 – 80

35 – 45%

140 – 150

16%

4.5 - 5.5

2009

PSEG

Market

214

162

$186

Gross

Margin ($M)

147

47.9%

14%

9.0

2008

104

48.7%

15%

6.9

2007

$130

54.4%

16%

$6.7

2006

EBITDA*

($M)

Capacity

Factors

Reserve

Margin

Nat. Gas

Henry Hub Spot

($/mmBtu)

*Excluding Mark-to-Market Accounting effects

Delivering Value: Today and Tomorrow

41

Global continues to focus on monetizing non-core assets …

International Assets:

Total book value of $24M in India and Venezuela

Other Domestic Assets:

GWF Energy (CA) – 363 MW (60% Ownership)

GWF & Hanford (CA) – 132 MW (50% Ownership)

Kalaeloa (HI) – 208 MW (50% Ownership)

Bridgewater (NH) – 16 MW (40% Ownership)

Conemaugh (PA) – 15 MW (4% Ownership)

Renewables:

Compressed Air Energy Storage (Energy Storage & Power joint venture):

Technology can be used to optimize an intermittent renewable energy source, such

as wind, by storing energy at night and releasing this stored energy during the day

when customers need power

Offshore Wind:

In October 2008, the New Jersey Office of Clean Energy (OCE) awarded a $4M

grant to a PSEG Global joint venture in order to advance the development of a

350 MW wind farm approximately 16 miles off the shore of southern New Jersey

Solar:

Ongoing additional opportunity evaluation and investment

… while enhancing the performance of domestic assets and

identifying opportunities for renewable growth.

Net other domestic owned

capacity: 395 MW;

Book value: $162M

Delivering Value: Today and Tomorrow

42

Resources is focused on managing its current investment

portfolio.

Net Investment in lease portfolio of $0.3B

Book investment of $2.3B less deferred taxes of $2.0B

Assuming 100% litigation loss, the lease portfolio would generate $2.1B of

after-tax cash over the remaining life of the portfolio

Net present value of after tax cash flow using 8% discount rate would be

approximately $800M

17

8

LILO/SILO Lease Termination Revenue

(54)

(43)

IRS LILO/SILO Interest**

48

51

Non-LILO/SILO Lease Revenue

2

27

LILO/SILO Lease Revenue

13

43

Total Lease Related

(22)

20

After Tax Earnings

(35)

2009 Forecast

($ Millions)

2008*

($ Millions)

PSEG Resources Earnings

(23)

Interest, G&A, Taxes & Other

*Normalized to exclude June LILO/SILO accounting adjustment.

**IRS Interest accrued for LILO/SILO tax deficit.

2009 earnings reflect reduced LILO/SILO lease income pending IRS

resolution.

PSEG Resources Lease Portfolio Overview

Delivering Value: Today and Tomorrow

43

Resources continues to monitor its tax risks …

June 2008 results included after tax charges of $490M:

$135M interest reserve

$355M reduced return due to cash flow timing

This charge will be reversed into income over the remaining terms of the

affected leases

Charge represents reserve against approximately 85% of potential

estimated liability

As of 12/31/08, $180M deposited with IRS

The forecast of cash available assumes interest payments to IRS to limit

growth in liability

PSEG anticipates paying between $500 - $920M for the tax years 1997 -

2003 to the IRS.

PSEG will then file for refund and commence litigation to recover these

amounts

… and maintains a flexible plan to handle the uncertainty.

Delivering Value: Today and Tomorrow

44

PSEG Energy Holdings – 2008 Earnings Drivers

2007

Operating

Earnings*

Global’s Lost

Income on

Asset Sales

Resources’

Lease Income

& LILO/SILO

Interest

Interest

Expense

Taxes

Texas Margin

Texas Mark to

Market Impact

2008

Operating

Earnings*

2008 MTM

2008

Operating

Earnings

without MTM

$99M

($65M)

($21M)

$34M

$18M

$26M

$123M

$101M

($14M)

$2M

Holdings 2007 vs 2008 Operating Earnings

*See page 139 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings

Delivering Value: Today and Tomorrow

45

2008 Operating

Earnings

without MTM

Texas Margin

and Major

Maintenance

Texas Project

Financing Paid

Off

Interest & Other

Global Taxes

Resources

Lease Income &

LILO/SILO

Interest

Resources

Interest, G&A,

Other & Taxes

2009 Guidance

PSEG Energy Holdings – 2009 Earnings Drivers

$99M

$0 – 20M

($50 - 40M)

($4 - 2M)

$17M

($20 - 16M)

($31 - 29M)

($11 - 9M)

Holdings 2008 Operating Earnings vs 2009 Guidance

Delivering Value: Today and Tomorrow

46

PSEG Energy Holdings – Business Drivers

$0 – 20M

2009 Guidance

2010+ Drivers

Sale of remaining international assets

(Book value $24M)

Continued defense of LILO/SILO lease

position with improved return post-

resolution

Focused management of domestic

contracted generation portfolio

Support of 2009 joint venture Energy

Storage & Power in efforts to license

CAES 2 technology

Pursuit of renewable development with

focus on Solar and Offshore Wind

Texas Spark Spread change of

±$5/MWh at market – impact of

approximately $0.03/share

Delivering Value: Today and Tomorrow

47

PSEG Energy Holdings — Delivering Value: Today and Tomorrow

Exceeded earnings

targets

Strong 2008 Texas

performance well

above expectations

Stable earnings from

US contracted

generation assets

Sale of international

assets yielded $1.5B over

2007-2008

Proactively reserved for

potential LILO/SILO

liability

Earnings on track to meet

2009 guidance

Achieving predictable

performance from

contracted US generation

assets

Improving Texas

operations via asset

management agreement

with PSEG Power

Redeemed approximately

$280M of Texas project

debt in the first quarter of

2009

Managing risk by limiting

growth in lease tax liability

Sufficient liquidity and

credit strength to fund

potential LILO/SILO liability

through cash, asset value

and debt capacity

Exploring opportunities to

optimize other U.S. assets

Pursuing attractive

renewable generation

opportunities

Compressed Air

Energy Storage

(CAES)

Solar

Offshore Wind

Meeting

Commitments

Delivering

Value Today

Positioned for

the Future

Delivering Value: Today and Tomorrow

48

We make things work for you.

PSEG Power – Overview

Bill Levis

President and Chief Operating Officer, PSEG Power

Delivering

Value Today

Positioned for

the Future

Meeting

Commitments

Achieved earnings targets

Improved operating

performance of generation

fleet

Environmental

commitments met

$1 Billion capital expense

on budget, met specs

Disciplined hedging

strategies have managed

earnings volatility and

reduced risk

On target to meet 2009

earnings guidance of

$1,210M to $1,285M

Continued Operational

Excellence Model (OEM)

implementation with

demonstrated

improvements at Fossil

Sustained, strong nuclear

performance

Successful multi-year

hedging strategy

supported by BGS, RPM in

liquid markets

Effective management of

costs and capital programs

to drive value

Low-cost, baseload

nuclear fleet benefits in

carbon constrained world

BET installation improves

operating capability of coal

fleet and enables a wide

variety of coals

Expansion opportunities

through existing

experience and

infrastructure, including

peaker bids

Strong free cash flow

PSEG Power - Delivering Value: Today and Tomorrow

Delivering Value: Today and Tomorrow

50

Low-cost portfolio

Regional focus in competitive, liquid

markets

Assets favorably located near

customers/load centers

Many units east of PJM

constraints

Southern NEPOOL/ Connecticut

Market knowledge and experience

to maximize the value of our assets

… with low cost plants, in good locations, within solid markets.

Power’s assets support commitments in a dynamic environment…

18%

45 %

9 %

27 %

Fuel Diversity

Coal

Gas

Oil

Nuclear

Pumped

Storage

1%

Energy Produced – 2008

53%

23%

23%

Pumped Storage

& Oil 1%

Nuclear

Coal

Gas

Total GWh: 55,300

Total MW: 13,576

Delivering Value: Today and Tomorrow

51

… of serving full requirement load contracts, while maintaining

optionality under a variety of conditions.

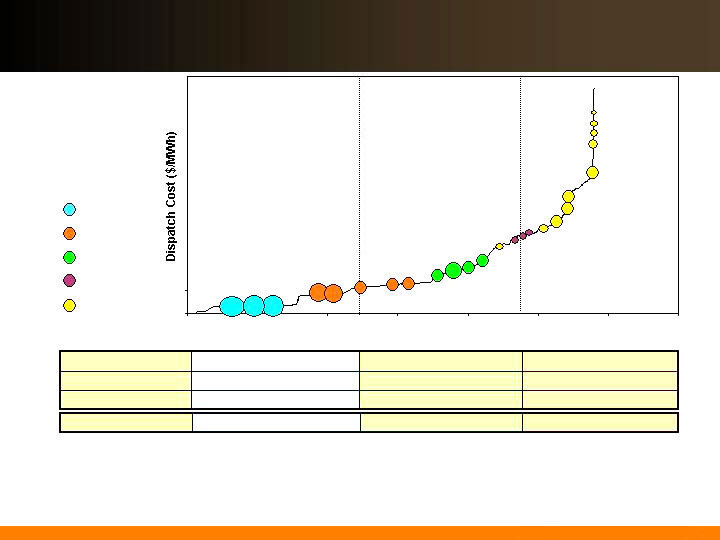

Power’s assets along the dispatch curve reduce the risk…

X

X

Ancillary Revenue

X

X

X

X

Capacity Revenue

X

X

Energy Revenue

X

X

Dual Fuel

Baseload units

Load following units

Peaking units

Illustrative

Salem

Hope

Creek

Keystone

Conemaugh

Hudson 2

Linden 1,2

Burlington 8-9-11

Edison 1-2-3

Essex 10-11-12

Bergen 1

Sewaren 1-4

Hudson 1

Mercer1, 2

Bergen 2

Sewaren 6

Mercer 3

Kearny 10-11

Linden 5-8 / Essex 9

Burlington 12 / Kearny 12

Peach

Bottom

Bridgeport

New

Haven

Nuclear

Coal

Combined Cycle

Steam

Peaking

BEC

Yards

Creek

National Park

Delivering Value: Today and Tomorrow

52

Nuclear has successfully transitioned to independent operations…

Industrial Safety Excellence

Lowest OSHA recordable rate ever

Equipment Reliability Excellence

Highest output ever, highest summer output ever

Forced Loss Rate improvement

Highest capacity factor of any unit in the country for Hope Creek

Refueling Outage Excellence

57 days – second fastest steam generator outage in industry

New industry standard on dose

Salem fall outage was the first PWR to complete Reactor Vessel Nozzle weld mitigation

requirements, and was completed within 18 hours of top quartile for standard outage

Strengthened Nuclear Fundamentals

Maintained site focus on Excellence – ensured organization focus on behaviors, highlighted nuclear safety culture principles weekly, strengthened industry peer group contacts and interaction.

Strengthened Stakeholder Confidence

Hope Creek Extended Power Uprate (EPU) – 150 MW

Successful NRC/FEMA graded emergency planning exercise

Successful NRC Force-on-Force evaluation

Withdrawal of National Guard and State Police

… and had a year of numerous accomplishments in 2008.

Delivering Value: Today and Tomorrow

53

Our nuclear performance has continued to improve…

79

80

97

94

92

97

96

96

97

96

97

2004

2005

2006

2007

2008

2009 Target

24.7

27.3

29.1

28.4

29.3

29.8

2004

2005

2006

2007

2008

2009 Target

INPO Index ( )

Highest capacity factor in the industry for Hope

Creek in 2008

Highest Nuclear output in Power’s history

2008 INPO Index for NJ Units of 92 would have

been 97, excluding planned Salem steam

generator replacement

Nuclear Generation Output ( )

(000’s GWH)

Forced Loss Rate ( )

(%)

3.1

2.1

0.6

0.7

0.6

0.6

0.6

0.6

1.0

11.1

0.7

2004

2005

2006

2007

2008

2009 Target

… as we maintain our relentless drive for excellence.

NJ Units

1st Quartile

NJ Units

1st Quartile

Delivering Value: Today and Tomorrow

54

Salem’s benchmarking against the industry assures a constant

striving for excellence…

… and Salem has closed gaps even with 2008 results impacted by a planned

steam generator outage.

Indicator

Unit

2004

2005

2006

2007

2008

2009 PROJ

1

2

Industrial Safety (OSHA)

1

2

1

2

1

2

Safety System Reliability

1

2

1

2

1

2

1

2

1

2

1

2

1

2

Production Cost

Fuel Reliability (annual value)

CM Backlogs (annual value)

1

2

Forced Outages (annual value)

Significant Events

Emergency Diesel Generators (3-year avg)

Auxiliary Feedwater (3-year avg)

Safety Injection (3-year avg)

Chemistry Performance/Effectiveness Index

Capacity Factor

Forced Loss Rate

Refueling Outage Duration (annual value)

INPO Index (not an average)

Collective Radiation Exposure

Unplanned Scram Rate (per 7000 hrs)

Key

N/A

4th Quartile

3rd Quartile

2nd Quartile

1st Quartile

Delivering Value: Today and Tomorrow

55

Hope Creek’s performance against its peers has greatly improved…

… and has set top quartile performance goals across the board for

2009.

Indicator

2004

2005

2006

2007

2008

2009 PROJ

INPO Index (not an average)

Industrial Safety (OSHA)

Collective Radiation Exposure

Unplanned Scram Rate (per 7000 hrs)

Significant Events

Safety System Reliability

Emergency Diesel Generators (3-year avg)

Residual Heat Removal (3-year avg)

High Pressure Coolant Injection (3-year avg)

Chemistry Performance/Effectiveness Index (18 month)

Capacity Factor

Forced Loss Rate

Refueling Outage Duration (annual value)

Production Cost

Fuel Reliability (annual value)

CM Backlogs (annual value)

Forced Outages (annual value)

Key

4th Quartile

3rd Quartile

2nd Quartile

1st Quartile

Delivering Value: Today and Tomorrow

56

Fossil met most 2008 objectives…

Capture value through Operational Excellence Model implementation

Achieved record output in 2008

Achieved record summer output in 2008

Hudson / Mercer back end technology implementation

Completed Mercer 1&2 baghouse installation, also completed first full year

Bridgeport Harbor – baghouse operations

Met all Consent Decree milestones

Early benefit from balance of plant work at Hudson

Outage planning and execution, seasonal readiness

Total planned outage days completed ahead of schedule

Shortened peaking outage durations (Spare LM6000)

Integrate operation with growth opportunities

Transitioned management of Texas operations into Fossil

Won Request For Proposal (RFP) for peaker at New Haven

Opacity Controls

Decrease in opacity events by 62% since 2006 and by 35% from 2007 to 2008

… and continues to improve through implementation of the

Operational Excellence Model.

Delivering Value: Today and Tomorrow

57

Power’s coal capacity is an area identified for improvement…

Outages related to the installation

of BET have reduced output in

2007 – 2009

Continued drive to enhance our

environmental footprint

Output ( )

(000’s GWh)

15.3

14.9

13.1

13.0

13.0

2005

2006

2007

2008

2009 Target

Forced Outage Rate ( )

(% EFORD)

11.1

11.3

7.9

8.4

6.0

2005

2006

2007

2008

2009 Target

SO

2

and NOx Rates ( )

(lb/mmbtu)

1.12

1.01

0.91

0.96

0.73

0.34

0.29

0.20

0.21

0.16

2005

2006

2007

2008

2009 Target

… and BET and major capital improvements will prepare us for the

future.

SO2

NOx

Delivering Value: Today and Tomorrow

58

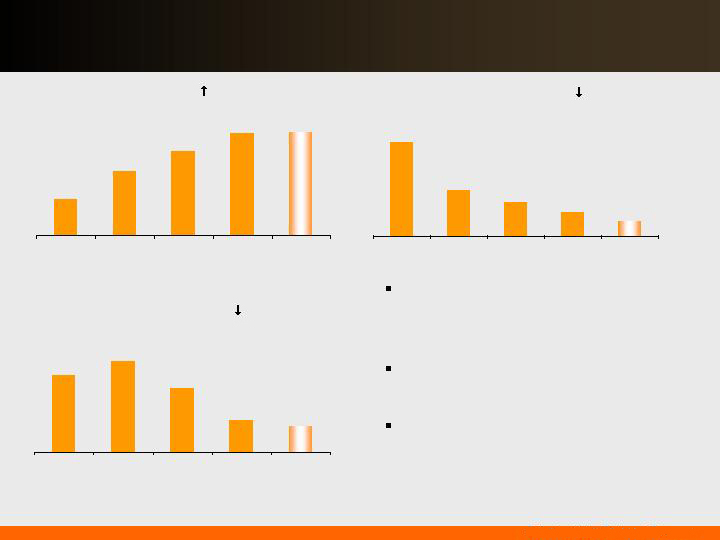

Power’s Combined Cycle capacity has shown significant

improvement…

Output has shown continued upward

trend based on market dynamics

and operational excellence model

Approaching top quartile forced

outage rate

Benefits from heat rate improvement

program

Output ( )

(000’s GWh)

12.2

12.1

9.9

7.6

4.3

2005

2006

2007

2008

2009 Target

Forced Outage Rate ( )

(% EFORD)

7.0

3.4

2.5

1.8

1.1

2005

2006

2007

2008

2009 Target

Period Heat Rate ( )

(mmbtu/kwh)

7,847

7,928

7,768

7,587

7,552

2005

2006

2007

2008

2009 Target

… benefiting from operating enhancements and market dynamics.

*

*

*

*

*Includes Texas

Delivering Value: Today and Tomorrow 59

Performance has improved for Power’s peaking fleet…

Peaking start success results in

opportunities in ancillary and

real time markets

Significant improvements driven by

investments in the facilities

Peaking provides flexibility in serving

load and managing needs of a diverse

market

Start Success ( )

97

99

97

99

99

2005

2006

2007

2008

2009 Target

Forced Outage Rate ( )

(% EFORD)

17.2

22.8

18.9

12.7

8.0

2005

2006

2007

2008

2009 Target

Equivalent Availability ( )

86

76

77

91

93

2005

2006

2007

2008

2009 Target

… and will be increasingly relied upon as markets tighten.

Delivering Value: Today and Tomorrow 60

The mission of the units in the peaking fleet varies by type of unit…

… with a balance of opportunities in energy, capacity and ancillary

products.

Gross Margin Contribution From All Peaking Units

Peaking provides optionality

Value of peaking units should increase

with increase in renewables

Peaking helps in serving BGS product

Energy Units

Technology

Capacity

Energy

Capacity

Ancillary

Forced Outage Rate

# Starts

Burlington 12

LM 6000

168

X

X

X

Kearny 12

LM 6000

175

X

X

X

Essex 9

GE 7 EA

81

X

X

X

Linden 5,6,7,8

GE 7 EA

336

X

X

X

760

4%

4,351

Ancillary Units

Edison 1, 2, 3

FT4

504

X

X

Essex 10, 11, 12

FT4

536

X

X

Burlington 9, 11

FT4

364

X

X

1,404

11%

7,402

Capacity Units

Kearny 10 ,11

FT4

250

X

Sewaren 6

FT4

105

X

Mercer 3

FT4

115

X

Salem 3

FT4

22

X

Bridgeport Harbor 4, Kearny 9

FT4

36

X

National Park, Bergen 3, Burlington 8

FT4

63

X

591

29%

176

Energy

Capacity

Ancillary

Delivering Value: Today and Tomorrow 61

Benchmarking has helped Fossil identify areas for improvement…

Units by Groups: Coal: Hudson 2, Mercer 1&2 and Bridgeport 3 CC: Bergen 1&2 BEC, Linden 1&2 and *Texas (starting in 2008) ; Peaking: CT units

… and through the Operational Excellence Model we intend to close the

gaps for a potential $50M - $75M gain in gross margin.

2004

2005

2006

2007

2008

2009 PROJ

Maintenance Outage Hours

Maintenance Outage Hours

Maintenance Outage Hours

Indicator

Equivalent Availability

Forced Outage Rate (EFORd)

Equivalent Derate Hours

Forced Outage Occurences

Planned Outage Hours

FOR

Equivalent Availability

Forced Outage Rate (EFORd)

Equivalent Derate Hours

Forced Outage Occurences

Planned Outage Hours

FOR

Equivalent Availability

Forced Outage Rate (EFORd)

Equivalent Derate Hours

Forced Outage Occurences

Planned Outage Hours

FOR

Key

4th Quartile

3rd Quartile

2nd Quartile

1st Quartile

Delivering Value: Today and Tomorrow 62

2009 Objectives…

Successful Summer Run

Mercer/Hudson BET

Effective Cost Management

Streamline Outages

Continue OEM Implementation

Industrial Safety Excellence

Equipment Reliability

Excellence

Refueling Outage Excellence

Developing Our People

Effective Cost Management

… will focus our actions to help us achieve our goals.

Nuclear 2009 Objectives

Fossil 2009 Objectives

Delivering Value: Today and Tomorrow 63

The value of Power’s nuclear fleet…

Uprates

Peach Bottom 2 and 3 anticipate incremental 32 MW through

steam path retrofit

Potential for significant uprates remain for the future

License Renewal

Licenses at Peach Bottom 2 and 3 have been renewed

through 2033 and 2034 (respectively)

Power anticipates filing license renewal in the third quarter of

2009 for Salem 1, Salem 2 and Hope Creek

New Nuclear

Power’s Southern New Jersey site is a strong location for a new

nuclear unit

Power currently preparing Early Site Permit application for

submission in the second quarter of 2010

… can be improved through uprates, license renewal, and expansion.

Delivering Value: Today and Tomorrow 64

Our capital investment program …

Capex Planned

No Additional Capex Planned

… reduces emissions and positions the company for success.

Hudson (NJ)

Mercer (NJ)

Keystone (PA)

Bridgeport (CT)

Conemaugh (PA)

SCR

SCR

SCR

Low NOx

No additional

2010

Burners

Capex

Scrubber

Scrubber

Scrubber

Ultra-low

Scrubber

2010

2009

2009

Sulfur Coal

Baghouse

Baghouse

Scrubber

Baghouse

Scrubber

2010

2008

(PA compliant)

2008

(PA compliant)

$700 - $750M

$220M

$160M

Capital Expenditures*

NO

x

SO

2

Mercury / Particulate

Forecasted Environmental

*Excludes IDC

Delivering Value: Today and Tomorrow

65

Fossil’s projected environmental capital spending declines over

time…

… and we anticipate higher output, lower emissions, and greater

flexibility in coal sources.

Coal Environmental Capital

Coal Emissions Output

Aggregate emissions will decline nearly 66%

after installation of the pollution control

equipment

The installation will allow for fuel flexibility in

future years

Fossil spending on BET reached a peak of $491

million in 2008

Fossil’s coal fleet will be well positioned by

2010, with a dramatic reduction in capital

spending on pollution control equipment

Coal - NOx

Coal – SO2

352

491

381

175

4

$0

$300

$600

2007

2008

2009

2010

2011

0

20,000

40,000

60,000

80,000

2007

2008

2009

2010

2011

Complete

To Go

Delivering Value: Today and Tomorrow

66

0

20

40

60

80

100

120

140

160

180

200

0

10

20

30

40

50

60

70

80

0

2

4

6

8

10

12

14

16

18

20

Source: EPA, EIA (2006 and 2007) and PSEG Projection

PSEG Projected NOX Emission Rate for 2011

versus 2007 400 U.S. Coal Plants

Conemaugh

Keystone

Bridgeport

Hudson Mercer

NOx

Keystone

Bridgeport

Conemaugh

Hudson Mercer

SO2

PSEG Projected SO2 Emission Rate for 2011

versus 2007 400 U.S. Coal Plants

Keystone

Hudson Mercer

Bridgeport

Conemaugh

Mercury

PSEG Projected HG Emission Rate for 2011

versus 2006 400 U.S. Coal Plants

Power’s coal assets are undergoing environmental upgrades…

… which will dramatically reduce emissions and prepare the units for the future.

Delivering Value: Today and Tomorrow

67

-

500

1,000

1,500

2,000

2,500

3,000

Power’s fleet is well positioned for carbon legislation…

… based on its low carbon footprint.

Sources: 2007 EIA 906920 (generation & emission); eGRID 2006 (PJM Interconnection Data)

CO2 Emission Rate (lbs/MWh) Ranking

(PJM Connected Power Plants)

Delivering Value: Today and Tomorrow

68

Power has demonstrated success in managing large capital

projects…

In Service

($millions)

Bridgeport Harbor 3 Baghouse

2007 160

Salem Steam Generator

2008 240

Hope Creek Uprate

2008 180

Mercer Baghouse

2008 260

Hudson Balance of Plant

2007 - 2008 115

~$1Billion

Near Term

Spent To Go

Keystone Scrubber

2009 111 27

Mercer Scrubber

2009 135 95

Hudson Scrubber/SCR/Baghouse

2010 291 438

$537 $560

… with projects placed in service and achieving/exceeding desired

results.

In Service

Date

In Service

Date

($millions)

Power’s annual capital

spend for sustainability

has averaged $200M -

$225M over recent years

Depreciation expense is

expected to increase from

2008 ($164M) to 2011

($280M)

Delivering Value: Today and Tomorrow

69

Fossil is well positioned for growth…

Site Development

Opportunities in upcoming PJM capacity auction

Connecticut Peakers

Deliver on successful RFP efforts

Compressed Air Energy Storage (CAES)

Enabling technology for renewables

Power’s experience will help in managing in a

changing environment

Integration of assets into the portfolio

Renewables in Texas

RECs in managing full requirements contracts

… leveraging our existing infrastructure and experience.

Delivering Value: Today and Tomorrow

70

PSEG Power – Market Overview

We make things work for you.

Joe Hopf

President, PSEG Energy Resources & Trade

While commodity markets have been turbulent …

Energy markets showed high

volatility in 2008

Capacity markets continue to

be effective

Hedging strategy designed to

enhance stability and visibility

of earnings

Gas asset optimization and

other products round out a

strong portfolio

… Power benefits from operating in liquid transparent markets.

Disciplined approach to

hedging — controls in place to

manage through volatile

markets

Hedging philosophy manages

risk to a range of outcomes

Range of Potential Results 2009 – 2011

(Illustrative)

2009 2010 2011

$

Delivering Value: Today and Tomorrow

72

Power’s hedging strategy secures pricing for near term output…

Sell expected nuclear and coal output forward over a two to three

year horizon

Contract fuel to balance position

Buy gas short-term as we sell output from gas units

Utilize liquid markets to manage risk - BGS provides foundation

Annual recontracting opportunity

3-year term mitigates volatility

BGS volume at maximum tranches is approximately 50% of

Power’s coal and nuclear output

Utilize with ancillaries services market and FTRs

… which mitigates the impact of market movements on earnings.

Delivering Value: Today and Tomorrow

73

2003

2004

2005

2006

2007

2008

2009

Increase in Full Requirements

Component Due to:

Increased Congestion (East/West Basis)

Increase in Capacity Markets/RPM

Volatility in Market Increases Risk

Premium

The recent successful completion of the seventh BGS auction...

Market Perspective – BGS Auction Results

… cushions the impact of volatile markets on customers.

Note: BGS prices reflect PSE&G Zone

Full Requirements

3 Year Average

Round the Clock

PJM West

Forward Energy

Price

$55.05

$65.41

~ $18

~ $21

$102.51

~ $32

$98.88

~ $41

~ $43

$111.50

~ $47

$103.72

$55.59

~ $21

Capacity

Load shape

Transmission

Congestion

Ancillary services

Risk premium

Green

$33 - $34

$36 - $37

$44 - $46

$67 - $70

$58-$60

$68 - $71

$56 - $58

*

*2009 RTC price was ~ $50/MWh at time of auction

Delivering Value: Today and Tomorrow

74

-

2,000

4,000

6,000

8,000

10,000

12,000

-

2,000

4,000

6,000

8,000

10,000

12,000

Power’s output is sold forward…

… through full requirement contracts and other hedging transactions.

2009 2010 2011

2009 2010 2011

Nuclear

Coal

CC

Steam / Pk

Existing Hedges

Existing Loads+ Hedges

Existing Loads+ Hedges + Potential Future BGS

Total Fleet On-Peak Average MW

Total Fleet Off-Peak Average MW

Delivering Value: Today and Tomorrow

75

Our hedging strategy has been effective in 2008 in volatile

markets…

$800

$900

$1,000

$1,100

$1,200

… resulting in strong 2008 results for Power.

$1,110

$1,010

Guidance

Range

$50

$70

$90

$110

$130

$150

2008 Average Monthly PJM West Energy Price

2008 Operating Earnings*

Jan

Dec

$1,050

*See page 139 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings

Delivering Value: Today and Tomorrow

76

Commodity prices have been volatile…

*Average of 2 historical months and 10 forward months

… but Power’s diverse asset portfolio and hedging strategy has

mitigated the effect of volatility, providing strong results.

$0

$5

$10

2004

2005

2006

2007

2008

2009

Fwd*

2010

Fwd

2011

Fwd

$0

$20

$40

$60

$80

$100

2004

2005

2006

2007

2008

2009

Fwd*

2010

Fwd

2011

Fwd

$0

$20

$40

$60

$80

$100

2004

2005

2006

2007

2008

2009

Fwd*

2010

Fwd

2011

Fwd

$0

$20

$40

$60

$80

$100

$120

2004

2005

2006

2007

2008

2009

Fwd *

2010

Fwd

2011

Fwd

Henry Hub NYMEX

($/MMBTU)

Western Hub RTC

($/MWh)

West Hub On Peak

($/MWh)

Central Appalachian Coal

($/Ton)

Note: Forward prices as of 2/6/09

Delivering Value: Today and Tomorrow

77

The effect of our hedging/forward sales strategy…

Power’s hedging strategy

secures pricing over a 2 - 3 year

future time horizon.

The 3 year BGS Auction period

has the effect of pulling forward

prices back.

… is to create a realized price that is a blend of prior and future pricing,

moderating volatility.

*PJM West Average of 2 historical months and 10 forward months as of 2/6/09

$0

$20

$40

$60

$80

$100

2004

2005

2006

2007

2008

2009 Fwd

2010 Fwd

2011 Fwd

PJM West

PS Zone vs PJM West Basis

2009 realized

price

*

Delivering Value: Today and Tomorrow

78

$10

$20

$30

$40

$50

$60

$70

2005

2006

2007

2008

2009

2010

2011

Annual Average

Historical Monthly

Forecast

Note: Forward prices as of 02/06/09

Spark spreads are in line with rising historical averages…

PJM Western Hub Spark Spread (On-Peak – Henry Hub * 7.5 Heat Rate)

PJM Western Hub Dark Spread (RTC – Central Appalachian Coal * 10 Heat Rate)

$0

$10

$20

$30

$40

$50

2005

2006

2007

2008

2009

2010

2011

… but near term dark spreads have declined as coal prices have risen.

Delivering Value: Today and Tomorrow

79

$50

$52

$54

$56

$58

$60

$62

$64

Power’s assets are well positioned…

… deriving higher prices based on locational value.

Historical 5-year Average PJM Energy Price

(Around the Clock)

Note: Reflects prices of original PJM load zones

Current plant locations,

site expansion capability

System Interface

New Haven

Bridgeport

Bethlehem Energy Center

(Albany)

Bergen

Kearny

Essex

Sewaren

Edison

Linden

Mercer

Burlington

National Park

Hudson

Conemaugh

Keystone

Peach Bottom

Hope Creek

Salem

Yards Creek

Delivering value: Today and Tomorrow

80

Expanded PJM Energy (000’s GWh)

0

300

600

900

Actual

2008 Forecast

2009 Forecast

Regional Energy Demand Growth (%)

-1%

0%

1%

2%

3%

4%

2009

2010

2011

2012

2013

PJM

EMAAC

New Jersey

PJM forecasts New Jersey to maintain a

higher demand growth rate than the

EMAAC region and the overall PJM

region off a lower 2008 base

The ultimate demand will be driven by

the economy, but Power’s assets are well

located to manage through difficult times

Electricity demand is anticipated to show

moderate declines

PJM’s January 2009 load forecast

reflects a 0.6% drop in demand from ’08

to ’09

The growth rate forecast is more bearish

than last year’s forecast for ’09 and ’10,

but higher starting in ’11, with absolute

load levels nearly recovered by ‘13

Electric load growth is affected by the economy …

… with Power well positioned during challenging times.

Delivering value: Today and Tomorrow

81

… Power expects to see continued strong margins from PJM’s

Reliability Pricing Model.

Through the new capacity construct, and pricing at auction

prices…

Power Capacity Receiving RPM

PJM Zones

2007 / 2008

2008 / 2009

2009 / 2010

2010 / 2011

2011 / 2012

Eastern MAAC*

$197.67

$148.80

$191.32

$174.29

$110.00

MAAC

---

---

$191.32 (a)

$174.29

$110.00

Rest of Pool

$40.80

$111.92

$102.04

$174.29

$110.00

* Majority of Power’s assets

(a) – includes APS

MW

Power Total Capacity

13,576

Less New England

(977)

Less New York

(747)

PJM Capacity

11,852

Less RMR (Hudson 1)

(355)

11,497

Less Forced Outage (EFORD)

(881)

Available PJM Capacity

10,616

Less Capacity Absorbed By BGS Pre-RPM

Less Bilateral Capacity Sales Pre-RPM

Equals Capacity Available to Receive RPM Pricing

PJM Capacity Available to Receive Auction Pricing

0

2,000

4,000

6,000

8,000

10,000

12,000

07/08

08/09

09/10

10/11

11/12

Delivering value: Today and Tomorrow

82

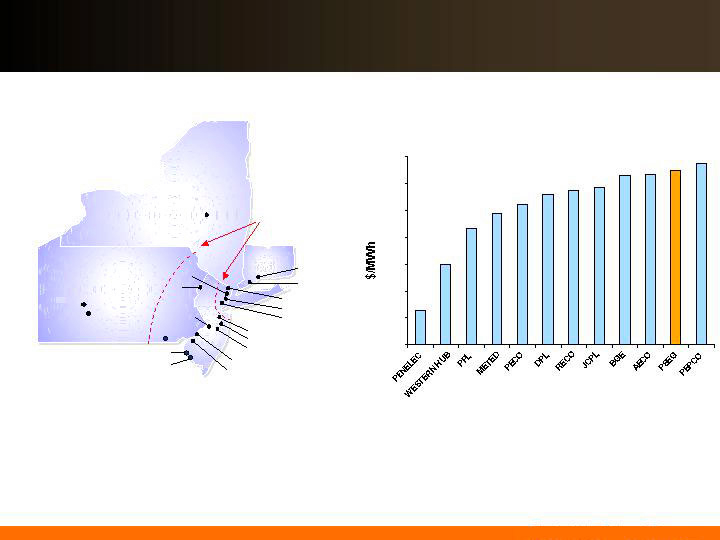

Capacity as an element of the overall pricing for BGS…

… contributed approximately $16/MWh to the 2009 BGS auction price.

*Excludes CTRs

$/MW-day

2009-2010 Auction

$191.32

2010-2011 Auction

$174.29

2011-2012 Auction

$110.00

Three Year Average ($/MW-day)

$158.54

Three Year Average ($/MW-day)

$158.54

MW per Tranche (varies by EDC)

~110

Days per Year

365

Capacity Cost per Tranche

$6,365,000

MW per Tranche (varies by EDC)

~110

Hours per Year

8,760

Load Factor (varies by EDC and demand)

~42%

MWh per Tranche

404,000

Capacity Cost per MWh

~$16

MWh per Tranche

Capacity Price per RPM Auction

Capacity Price per BGS Tranche

Delivering value: Today and Tomorrow

83

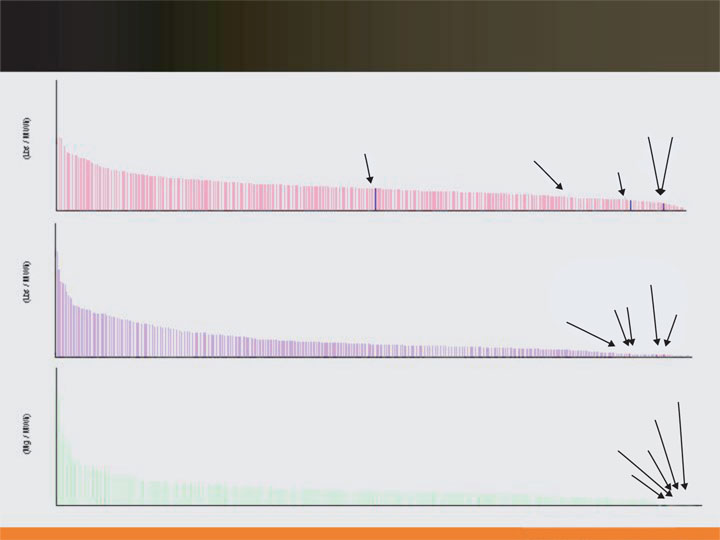

2,847

3,914

7,951

2,035

46,300

80,600

Prior FERC Approval of RPM

After FERC Approval of RPM

The market has responded to RPM …

… with proposals for additional capacity in the queue.

Resources Added Since RPM Began

(16,700 MW)

Proposed Generation in PJM Queue

(MW)

Net exports have decreased by nearly 3,000 MW

Withdrawn deactivation requests and

postponed/cancelled retirements have accounted

for nearly 4,000 MW

Almost 8,000 MW of new generation resources

DSM Resources have increased in each auction

RPM has prompted substantial generation

proposals, with over 34,000 MW added to the

queue since FERC approved RPM

Power has requested PJM study adding 1,000

MW, with the expectation of bidding 300 to 400

MW at our NJ sites in the next auction

Demand Resources

Increase in Generation

Retained Generation

Decrease in Net Exports

Delivering value: Today and Tomorrow

84

PJM is preparing for the 2012/2013 capacity auction…

The 6th RPM auction for capacity in PJM will take place in May 2009

Auction will cover the period of June 2012 – May 2013

Potential changes from prior auction include:

Update to Net Cost of New Entry from $171/MW-day to $286/MW-day

for the RTO ($62/kw-yr to $104/kw-yr)

Duquesne load participation

Locational Delivery Areas (LDAs) include PSEG zone/ PS North

Other issues

PJM issued planning parameters, including LDAs, on Feb 13

FERC expected to rule on proposed changes on March 27

… with a FERC decision anticipated in the near term.

Delivering Value: Today and Tomorrow

85

Gas Asset Optimization

Large wholesale provider to PSE&G and others

Storage capacity of 80 Bcf (in the Gulf and market regions)

Firm transportation of 1.1 Bcf/Day (on ten pipelines)

Off-system sales margins shared with residential customers

Commercial & Industrial customers (C&I) sales priced monthly at market

Storage spreads capture Summer/Winter price differential on C&I sales

Weather and price volatility drive results

Ancillary Services

Area regulation

Voltage regulation

Black start

Emissions Credits

… continuing to provide $100 to $200 million in margin.

Power has other attractive sources of revenues …

Delivering Value: Today and Tomorrow

86

RGGI

States

The Regional Greenhouse Initiative (RGGI)…

Cooperative effort by Northeast

states to design a regional cap-and-

trade program to reduce carbon

dioxide (CO2) emissions

Timeline

January 1, 2009 – Implementation

Quarterly auctions have been held

September 2008 clearing price

of $3.07/ton on 12.6M

allowances

December 2008 clearing price

of $3.38/ton on 31.5M

allowances

March 2009 auction for 32M

tons

Power’s anticipated CO2 emissions in

the RGGI regions is 15 – 16M tons

… is in place in the Northeast and may be a precursor to the

adoption of a national program.

ME

NY

DE

NH

VT

MA

NJ

RI

PA

MD

CT

Delivering Value: Today and Tomorrow

87

We make things work for you.

PSEG Power – Financial Overview

Daniel Cregg

Vice President, PSEG Power Finance

2007 Operating

Earnings*

Energy

Capacity

Cost

NDT and MTM

2008 Operating

Earnings*

2008 NDT and

MTM

2008 Operating

Earnings

without NDT

and MTM

… with the achievement of record earnings.

Power met its 2008 earnings commitment…

$949M

$1,107M

$80M

$134M

Operations

Uprates

BGS

Recontracting

Fuel

Full year

RPM

O&M

Depreciation

Other

($50M)

$57M

Power’s 2007 vs 2008 Operating Earnings

$1,050M

$1,850M EBITDA $2,170M

($63M)

*See page 139 for Items excluded from Income from Continuing Operations to reconcile to Operating Earnings

Delivering Value: Today and Tomorrow

89

Power’s results have also generated strong cash flow…

Cash from Operations

Strong cash flow from operations

Cash from Investing

Disciplined approach to investing

Near term conclusion of planned environmental build

Cash from Financing

Successful program to access retail markets yielded

approximately $210 million at 6% - 6.5%

… with benefits derived from many areas.

Cash from Operations

(↑)

($Million)

$600

$1,200

$1,800

2006

2007

2008

Delivering Value: Today and Tomorrow

90

2008 Operating

Earnings without

NDT and MTM

Energy

Capacity

Other Margin

Cost

2009 Guidance

… with visible sources of value to achieve this result.

Power’s commitment in 2009 reflects continued earnings

growth…

$1,107M

$1,210 -

$1,285M

$90 – 100M

($25 – 15M)

$88 – 133M

O&M (pension)

Depreciation

Other

($50 – 40M)

Power’s 2008 Operating Earnings vs 2009 Guidance