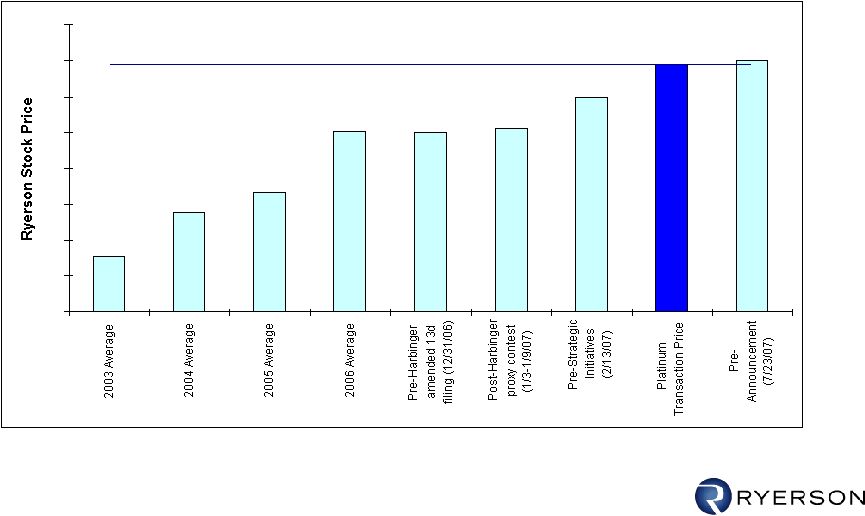

18 Proxy Solicitation Important Information In connection with its proposed merger with an affiliate of Platinum Equity, LLC, Ryerson plans to file with the Securities and Exchange Commission (the “SEC”) a preliminary proxy statement and a definitive proxy statement. The definitive proxy statement will be mailed to stockholders of Ryerson. Stockholders of Ryerson are urged to read the proxy statement relating to the merger and other relevant materials when they become available because they will contain important information about the merger and Ryerson. Security holders may obtain a free copy of the proxy statement and any other relevant documents (when available) that Ryerson files with the SEC at the SEC’s web site at http://www.sec.gov. The definitive proxy statement and these other documents may be accessed at www.ryerson.com or obtained free from Ryerson by directing a request to Ryerson Inc., ATTN: Investor Relations, 2621 West 15th Place, Chicago, IL 60608. Certain Information Regarding Participants Ryerson, its directors and executive officers may be deemed to be participants in the solicitation of the Company’s security holders in connection with the proposed merger. Security holders may obtain information regarding the names, affiliations and interests of such individuals in the Company’s proxy statement in connection with its 2007 annual meeting of stockholders, which was filed with the SEC on July 31, 2007. To the extent holdings of the Company’s equity securities have changed since the amounts reflected in such proxy statement, such changes have been reflected on Statements of Change in Ownership on Form 4 filed with the SEC. |