UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☒ | Definitive Proxy Statement |

| ☐ | Definitive Additional Materials |

| ☐ | Soliciting Material Pursuant to §240.14a-12 |

Farmers & Merchants Bancorp

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check all boxes that apply):

| ☒ | No fee required. |

| ☐ | Fee paid previously with preliminary materials. |

| ☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11. |

FARMERS & MERCHANTS BANCORP, INC.

307 North Defiance St.

Archbold, Ohio 43502

(419) 446-2501

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS

TO BE HELD APRIL 29, 2024

To Our Shareholders:

NOTICE IS HEREBY GIVEN that the Annual Meeting of Shareholders of Farmers & Merchants Bancorp, Inc., an Ohio corporation (the “Company”), will be held virtually on April 29, 2024, at 1:30 P.M., Eastern Daylight Savings Time, for the following purposes:

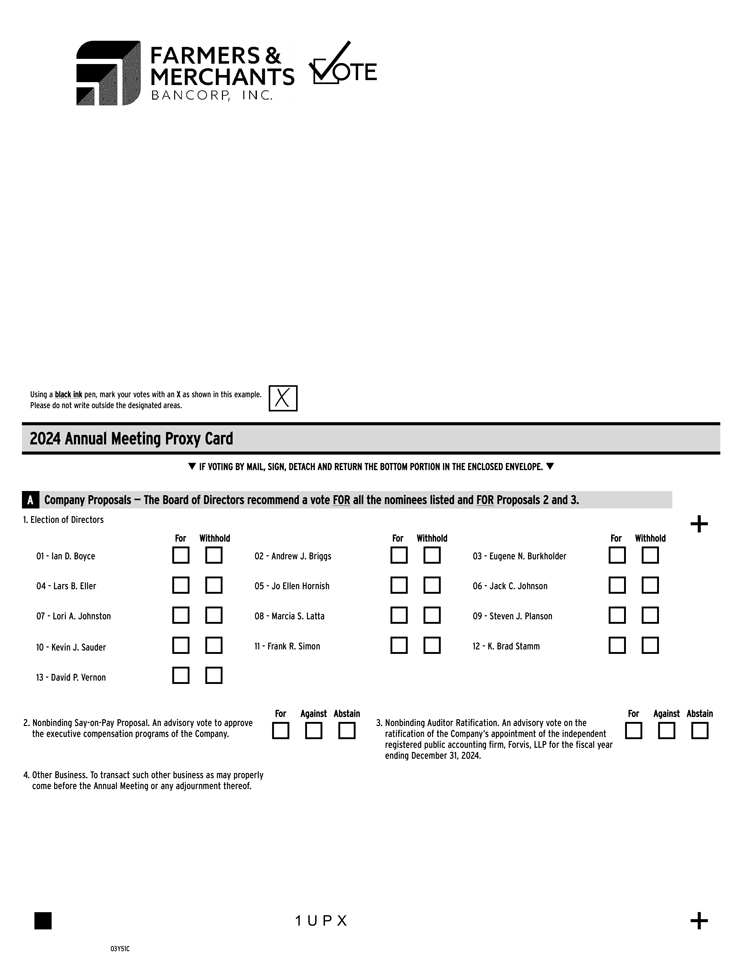

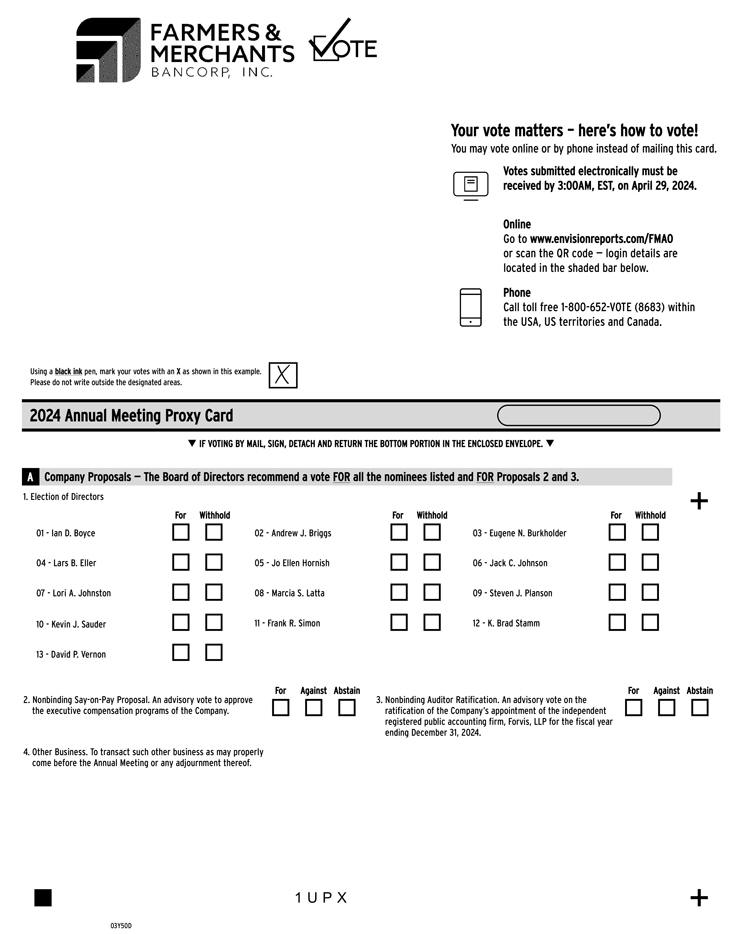

| 1. | Election of Directors. To elect the following thirteen nominees to the Board of Directors to serve until the Annual Meeting of Shareholders in 2025: |

Ian D. Boyce | Jack C. Johnson | Kevin J. Sauder | ||

Andrew J. Briggs | Lori A. Johnston | Frank R. Simon | ||

Eugene N. Burkholder | Marcia S. Latta | K. Brad Stamm | ||

Lars B. Eller | Steven J. Planson | David P. Vernon | ||

Jo Ellen Hornish |

| 2. | Nonbinding Say-on-Pay Proposal. An advisory vote to approve the executive compensation programs of the Company. |

| 3. | Nonbinding Auditor Ratification. An advisory vote on the ratification of the Company’s appointment of the independent registered public accounting firm, FORVIS, LLP for the fiscal year ending December 31, 2024. |

| 4. | Other Business. To transact such other business as may properly come before the Annual Meeting or any adjournment thereof. |

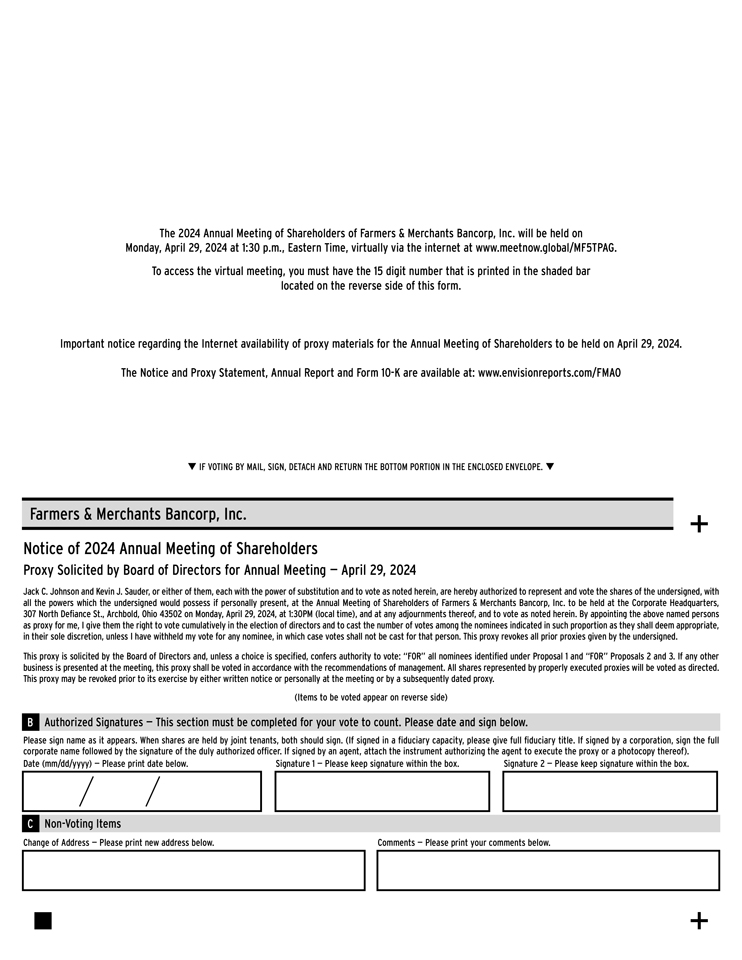

This year, the Annual Meeting will be hosted as a completely virtual meeting of shareholders, which will be conducted solely online via live webcast. Shareholders will be able to participate in the Annual Meeting online, vote your shares electronically and submit questions prior and during the Annual Meeting by visiting www.meetnow.global/MF5TPAG at the meeting date and time described in the accompanying proxy statement. There is no physical location for the Annual Meeting. The Board of Directors has fixed the close of business on March 5, 2024 as the voting record date for determination of shareholders who are entitled to notice of and to vote at the Annual Meeting.

By Order of the Board of Directors

|

|

Melinda L. Gies Board Administrator/Corporate Secretary |

March 15, 2024

Archbold, Ohio

PROXY STATEMENT

FARMERS & MERCHANTS BANCORP, INC.

307 North Defiance Street

Archbold, Ohio 43502

2024 ANNUAL MEETING OF SHAREHOLDERS

April 29, 2024

GENERAL INFORMATION

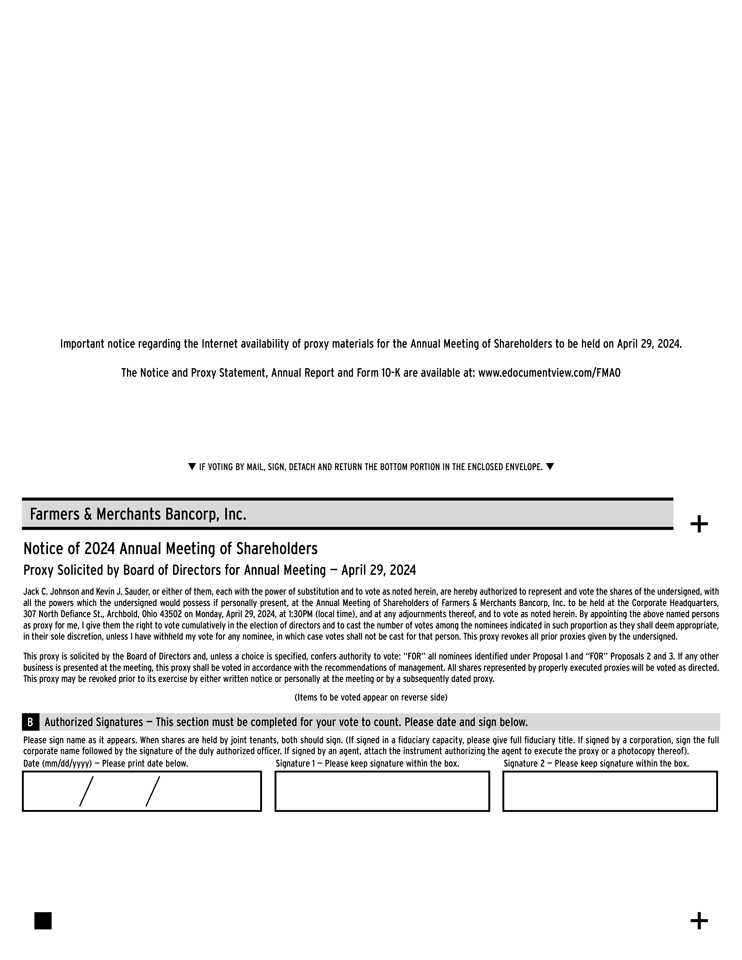

This Proxy Statement is being furnished in connection with the solicitation of proxies by the Board of Directors of Farmers & Merchants Bancorp, Inc., an Ohio corporation (“Company”), to be used at the Annual Meeting of Shareholders of the Company, to be held on Monday, April 29, 2024, at 1:30 PM EST, and at any adjournment thereof, for the purposes set forth in the Notice of Annual Meeting of Shareholders. This year’s Annual Meeting will be hosted as a completely virtual meeting, which will be conducted solely online via live webcast at www.meetnow.global/MF5TPAG. Shareholders will be able to participate in the Annual Meeting by accessing online, voting their shares electronically and submitting questions prior to and online during the meeting. To participate in the live webcast of the Annual Meeting, you will need your secure 15-Digit Control Number, which is provided on your proxy card, to enter the meeting.

The Company will send a single annual report, 10-K and proxy statement to multiple shareholders of record that share the same address, unless we receive instructions to the contrary. However, each shareholder of record will continue to receive a separate proxy card. This practice, known as “householding,” is designed to reduce our printing and postage costs. If you wish to receive a separate annual report, 10-K and proxy statement, you may request it by writing to us at Farmers & Merchants Bancorp, Inc., Attention: Investor Relations, 307 North Defiance Street, Archbold, Ohio 43502. If you wish to discontinue householding entirely, you may contact Investor Relations by calling 419-446-2501 or by forwarding a written request addressed to the address above. If you receive multiple copies of the annual report, 10-K and proxy statement, you may request householding by contacting the Company as noted above. If your shares are held in street name through a bank, broker, or other holder of record, you may request householding by contacting that bank, broker, or other holder of record. In addition, the Company also makes available copies of these materials electronically, as described in the section which immediately follows.

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR THE

ANNUAL MEETING TO BE HELD ON APRIL 29, 2024

The proxy statement and annual report to security holders are available at:

www.envisionreports.com/FMAO

The following items are available at the specified web site:

| ● | The proxy statement being issued in connection with the 2024 Annual Meeting of Shareholders; |

| ● | The Company’s 2023 Annual Report to Shareholders; |

| ● | The form of proxy for use in connection with the 2024 Annual Meeting of Shareholders; and |

| ● | The Company’s 2023 10-K Report. |

1

The Proxy Statement, Proxy Card and Farmers & Merchants Bancorp, Inc. 2023 Annual Report will be mailed to shareholders commencing on or about March 15, 2024.

VIRTUAL MEETING INFORMATION

We will be hosting the Annual Meeting live via the internet. Shareholders will be able to participate in the Annual Meeting online via live webcast. Provided below is the summary of the information that you will need to participate in the Annual Meeting.

| ● | Shareholders can participate in the Annual Meeting via live webcast over the internet at www.meetnow.global/MF5TPAG. |

| ● | The online meeting will begin promptly at 1:30 P.M. EST on April 29, 2024. On the day of the Annual Meeting, we recommend that you access the meeting prior to the start time leaving ample time for the check in. Please follow the registration instructions as outlined in this proxy statement. |

| ● | You will need your secure 15-Digit Control Number, which is provided on your proxy card, to enter the Annual Meeting. |

| ● | You may submit questions for the meeting in advance at www.meetnow.global/MF5TPAG. Shareholders will also have the ability to vote and submit live questions during the Annual Meeting webcast at www.meetnow.global/MF5TPAG. Questions related directly to the Annual Meeting will be answered during our virtual meeting, subject to time constraints. Any questions pertinent to meeting matters that cannot be answered during the meeting due to time constraints will be posted online and answered on our website at www.fm.bank under the “Investors” tab. The questions and answers will be available as soon as practical after the meeting and will remain available until one week after the posting. |

| ● | Instructions on how to participate in the live webcast, including how to verify stock ownership and vote your shares electronically during the Annual Meeting, are available at www.envisionreports.com/FMAO. |

| ● | Webcast replay of the Annual Meeting will be available until April 29, 2025. |

Your Vote Is Important

If you hold stock directly in your own name: Whether or not you plan to participate at the Annual Meeting and are a shareholder of record, follow the voting instructions enclosed for internet or telephone voting. Or if you prefer to do so, please complete, sign, and date the enclosed proxy and return it promptly in the envelope provided.

If you hold stock in a brokerage account, IRA, 401(k) plan, or trust account:

With respect to a limited number of proposals, your broker or bank is permitted to vote your shares even when you have not provided instructions on how you would like your shares to be voted. The New York Stock Exchange and the rules of the SEC govern how shares held in brokerage or other accounts may be “discretionarily voted” by brokers and banks in the absence of voting instructions from the actual owner. Under these rules, if you do not direct your broker or bank on how to vote your shares on Proposal One, your shares will remain un-voted on such proposal.

Therefore, if you hold shares in one or more accounts, it is very important that you direct your broker or bank on how to vote your shares for all proposals. Most banks and brokerage firms permit shareholders to direct their votes via the internet or by telephone. Your broker or bank will provide you with instructions for how to direct the voting of your shares.

2

If you would like to vote your shares electronically during the meeting, shareholders of record date can participate in the Annual Meeting via live webcast and entitled to vote electronically over the internet at www.meetnow.global/MF5TPAG.

In accordance with company policy, proxy cards, ballots and voting instructions that identify individual shareholders will be kept confidential. Exceptions to this policy, however, may be necessary in limited instances to comply with applicable legal requirements and in the event of a contested proxy solicitation, to verify the validity of proxies presented by any person and the results of the voting.

MEETING INFORMATION

The Board of Directors has fixed the close of business on March 5, 2024, as the record date for the determination of shareholders who are entitled to notice of and to vote at the meeting. Subject to your right to vote cumulatively in the election of directors, if properly implemented, you are entitled to one vote for each share of common stock you held on the record date, including shares:

| ● | held directly in your name; and/or |

| ● | held for you in an account with a broker, bank, or other nominee (shares held in “street name”). |

How many shares must be present to hold the meeting?

The Company’s Code of Regulations provides that thirty-three and one-third percent (33 1/3%) of the Company’s shares entitled to vote be present in person or by proxy at any meeting shall constitute a quorum for purposes of holding the meeting and conducting business. As of January 1, 2024, there were 13,664,641 shares of the Company’s common stock, without par value (“Common Stock”) outstanding, of which 151,350 shares are subject to restricted stock grants, the holders of which shares are entitled to vote such shares. Each of the holders of the outstanding shares and restricted stock grants totaling 13,664,641 shares are entitled to one vote per share, subject to the right to vote cumulatively in the election of directors, if properly implemented. Your shares are counted as present at the meeting if you:

| ● | participate in the Annual Meeting via live webcast and vote electronically over the internet at www.meetnow.global/MF5TPAG; or |

| ● | have properly submitted a proxy card or have voted electronically or by telephone prior to the meeting. |

Abstentions and broker non-votes are counted for purposes of determining the presence or absence of a quorum for the transaction of business at the meeting.

What proposals will be voted on at the meeting?

There are three proposals scheduled to be voted on at the meeting which include: (i) the election of thirteen members to serve on the Company Board of Directors; (ii) an advisory vote on Say-on-Pay to consider the executive compensation programs of the Company; and (iii) an advisory vote on the selection of our independent registered accounting firm, which gives you the opportunity to endorse or not endorse the Company’s appointment of the independent registered public accounting firm.

Who is requesting my vote?

The solicitation of proxies on the enclosed form is made on behalf of the Board of Directors of the Company and will be conducted primarily through the mail. Please vote by telephone or the internet. Or mail your completed proxy in the envelope included with these proxy materials. In addition to the use of the mail, members of the Board of Directors and certain officers and employees of the Company or its subsidiary may solicit the return of proxies by telephone, facsimile, and other electronic media or through personal contact. The directors, officers and employees that participate in such solicitation will not receive additional compensation for such efforts but will be reimbursed for out-of-pocket expenses. The cost of preparing, assembling, and mailing this Proxy Statement, the Notice of Meeting and the enclosed proxy will be borne by the Company.

3

REQUIRED VOTE

You are entitled to cast one vote for each share owned. Below are specifics regarding the vote requirement for each proposal:

Proposal One:

Directors will be elected by a plurality of the votes cast at the Annual Meeting. This means that the thirteen nominees who receive the largest number of “FOR” votes cast will be elected as directors.

The laws of Ohio, under which the Company is incorporated, and the Company’s Articles of Incorporation provide that if notice in writing is given by any shareholder to the President, Vice President or the Secretary of the Company not less than 48 hours before the time fixed for holding a meeting of shareholders for the purpose of electing directors, that they desire that the voting at that election shall be cumulative, and if an announcement of the giving of such notice is made upon the convening of the meeting by the Chairman or Secretary or by or on behalf of the shareholder giving such notice, each shareholder shall have the right to cumulate such voting power as they possess in voting for directors. Cumulative voting rights allow shareholders to vote the number of shares owned by them times the number of directors to be elected and to cast such votes for one nominee or to allocate such votes among nominees as they deem appropriate. Shareholders will not be entitled to exercise cumulative voting unless at least one shareholder properly notifies the Company of their desire to implement cumulative voting at the Annual Meeting. The Company is soliciting the discretionary authority to cumulate votes represented by proxy, if such cumulative voting rights are exercised.

Proposal Two:

Proposal Two, commonly known as a “Say-on-Pay” proposal, gives you as a shareholder the opportunity to endorse or not endorse our executive compensation programs. The affirmative vote of a majority of the votes cast by the holders of the Company’s common stock is required to approve Proposal Two, a nonbinding advisory vote on executive compensation.

Proposal Three:

Proposal Three, the affirmative vote of a majority of the votes cast by the holders of the Company’s common stock is required to approve Proposal Three, a non-binding advisory vote on the appointment of the independent registered public accounting firm.

Because the proposal to approve and ratify the appointment of FORVIS, LLP as our independent registered public accounting firm is advisory, it will not be binding upon the Board. However, the Audit Committee may re-consider its selection of FORVIS, LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2024.

What are the effects of abstentions and broker non-votes on each proposal?

If you hold your shares in a trust or brokerage account (sometimes referred to as holding shares in “street name”) please note that your bank or brokerage firm has “no discretionary” voting authority with respect to Proposals One through Two and therefore cannot vote on such proposals in the absence of your instructions. As a result, unless you direct your broker on how to vote your shares with respect to those proposals, your shares will remain un-voted on Proposals One and Two. Proposal Three is considered a “discretionary” item, so your brokerage firm may vote in its discretion on your behalf if you do not furnish voting instructions.

Furthermore, shares held in street name for which no voting instructions have been provided by the beneficial owner (and which are not voted by the broker pursuant to discretionary voting authority) are generally referred to as “broker non-votes”. Although abstentions and broker non-votes will be counted for purposes of determining the presence of a quorum, they are not considered votes cast. As a consequence, abstentions and broker non-votes will not impact the outcome of either proposal.

4

How can I participate in the Annual Meeting with the ability to ask a question and/or vote?

No physical meeting of shareholders will be held this year. The Annual Meeting will be a completely virtual meeting, which will be conducted exclusively by webcast. You are entitled to participate in the Annual Meeting only if, as of the Record Date, you were either: (A) a shareholder of record of the Company (a “Record Holder”) holding shares registered in your name; or (B) a “beneficial holder” holding shares through a brokerage or retirement account and have been issued a valid legal proxy to vote your shares by the applicable bank or broker (a “Beneficial Holder”). A Record Holder will receive a form of proxy directly from the Company, while a Beneficial Holder will generally receive a “voting instruction form” from their brokerage or other financial institution requesting direction on how to vote the shares on their behalf.

As a Record Holder, you will be able to participate in the Annual Meeting online, ask a question and vote by visiting www.meetnow.global/MF5TPAG and follow the instructions on your Notice, proxy card, or on the instructions that accompanied your proxy materials.

If you are a Beneficial Holder and want to participate in the Annual Meeting online by webcast with the ability to ask a question and/or vote, if you choose to do so, register to participate in advance of the Annual meeting.

To register in advance of the Annual Meeting, submit proof to Computershare of your legal proxy power from your broker or bank reflecting your holdings along with your name and email address. Requests for advance registration must be labeled as “Legal Proxy” and be received no later than 5:00 PM EST, on April 24, 2024. Requests for advance registration should be directed to us at the following:

By email: | Forward the email from your broker granting you a Legal Proxy, or attach an image of your Legal Proxy, to legalproxy@computershare.com

(You will receive a confirmation of your registration by email after we receive your registration materials.)

| |

By mail: | Computershare Farmers & Merchants Bancorp Inc. Legal Proxy P.O. Box 43101 Providence, RI 02940-3000 |

For Beneficial Owners, it will also be possible to register online the day of the Annual Meeting using the secure 15-DIGIT Control Number received with the voting instruction form. Please note, however, that this option is intended to be provided as a convenience to Beneficial Holders only, and there is no guarantee this option will be available for every type of Beneficial Holder voting control number. The inability to provide this option to any or all Beneficial Holders shall in no way impact the validity of the Annual Meeting.

To safely ensure your ability to participate at the Annual Meeting, Beneficial Holders are advised to register in advance of the Annual Meeting.

Please go to www.meetnow.global/MF5TPAG for more information on the available options and registration instructions.

The online meeting will begin promptly at 1:30 PM EST. We encourage you to access the meeting prior to the start time leaving ample time for the check in. Please follow the registration instructions as outlined in this proxy statement.

5

Do I need to register to participate in the Annual Meeting virtually?

Registration is only required if you are a Beneficial Holder, as set forth above. In addition, regardless of whether you intend to participate in this year’s virtual Annual Meeting, you may direct your vote prior to the Annual Meeting.

How do I vote my shares?

| ● | By Internet – You may vote by internet by using your secure 15-Digit Control Number, which is provided on your proxy card. Please go to the following web site, follow the instructions given, and enter the requested information at: www.envisionreports.com/FMAO |

| ● | By Phone – You may vote by phone by calling 1-800-652-VOTE (8683) by using your secure 15-Digit Control Number, which is provided on your proxy card, and follow the instructions given. |

| ● | By Mail – You may vote by mail by signing and dating your proxy card and mailing it in the envelope provided. You should sign your name exactly as it appears on the proxy card. If you are signing in a representative capacity (for example as guardian, trustee, custodian, attorney, or officer of a corporation), you should indicate your name and title or capacity. |

Your vote by phone or internet is valid as authorized by the Ohio General Corporation Law. For shares held in “street name” by Beneficial Owners, you should follow the voting instructions provided by your broker or nominee. You may complete and mail a voting instruction card to your broker or nominee or, in some cases, submit voting instructions by telephone or the internet. If you provide specific voting instructions by mail, telephone, or internet, your broker or nominee will vote your shares as you have directed. Under NYSE Rule 452, brokers will no longer be allowed to vote uninstructed shares in regard to the election of directors.

Online voting will also be available during the Annual Meeting, but Record Holders and Beneficial Holders are both strongly encouraged to submit their proxy or voting instructions in advance of the Annual Meeting.

How will my shares be voted?

Your proxy, if properly submitted and not revoked prior to its use, will be voted in accordance with the instructions you give. Properly submitted proxies that do not contain voting instructions and that are not “broker non-votes” will be voted (1) FOR the director nominees identified in Proposal One herein; (2) FOR Nonbinding Say-on-Proposal; (3) FOR the ratification of the appointment of FORVIS, LLP as our independent registered public accounting firm for 2024 and (4) in accordance with the best judgment of the persons appointed as proxies upon the transaction of such other business as may properly come before the Annual Meeting.

May I revoke my proxy?

You may revoke your proxy at any time before it is exercised by (i) filing written notice of revocation to be received prior to voting at the Annual Meeting and directed to Ms. Marilyn Johnson, Inspector of Elections of Farmers & Merchants Bancorp, Inc., 307 N. Defiance Street, Archbold, Ohio 43502; (ii) submitting a valid proxy bearing a later date that is received prior to voting at the Annual Meeting; or (iii) participating in the Annual Meeting online and giving notice of revocation to the Inspector of Elections.

How many shares are owned by Directors and Executive Officers?

All directors and named executive officers of the Company as a group (comprised of 16 individuals), beneficially held 1,077,896 shares of the Company’s common stock as of January 1, 2024, representing 7.89% of the outstanding common stock of the Company.

6

PROPOSAL ONE

Election of Directors and Information Concerning Directors and Officers

Pursuant to the Code of Regulations of Farmers & Merchants Bancorp, Inc. the number of directors is currently set at thirteen. Set forth below, as of the record date, is information concerning the nominees for election to the Board of Directors. The following persons have been nominated as directors by the Board of Directors upon the recommendation of the Company’s Corporate Governance and Nominating Committee to serve until the Annual Meeting of Shareholders in 2025:

There are no family relationships among any of the directors, nominees for election as directors and executive officers of the Company. In addition, no member of the Board of Directors serves on the Board of any other company which has a class of securities registered with the Securities and Exchange Commission.

While it is contemplated that all nominees will stand for election, and the nominees have confirmed this with the Company, if one or more of the nominees at the time of the Annual Meeting should be unavailable or unable to serve as a candidate for election as a director of the Company, the proxies reserve full discretion to vote the common shares represented by the proxies for the election of the remaining nominees and any substitute nominee(s) designated by the Board of Directors. The Board of Directors knows of no reason why any of the aforementioned persons will be unavailable or unable to serve if elected to the Board. The attached form of proxy grants to the persons listed in such proxy the right to vote shares cumulatively in the election of directors if a shareholder properly implements cumulative voting.

7

| Name | Age | Principal Occupation or Employment for Past Five Years | Year First Became Director | |||||||

Ian D. Boyce | 56 | Founding Member and Managing Partner Dickmeyer Boyce Financial Management | 2024 | |||||||

Andrew J. Briggs | 69 | Retired and former Chairman of Limberlost Bancshares, Inc. and President of its wholly-owned subsidiary Bank of Geneva | 2019 | |||||||

Eugene N. Burkholder | 71 | President, Falor Farm Center, Inc. | 2012 | |||||||

Lars B. Eller | 57 | President and CEO of the Company and The Farmers & Merchants State Bank | 2018 | |||||||

Jo Ellen Hornish | 70 | CEO, Hornish Bros, Inc. / Fountain City Leasing, Inc. / Advantage Powder Coating, Inc. | 2013 | |||||||

Jack C. Johnson | 71 | President, Hawk’s Clothing, Inc. | 1991 | |||||||

Lori A. Johnston | 62 | President, ProMedica Insurance Corporation | 2020 | |||||||

Dr. Marcia S. Latta | 62 | Vice President of University Advancement, The University of Findlay | 2009 | |||||||

Steven J. Planson | 64 | President, Planson Farms, Inc. | 2008 | |||||||

Kevin J. Sauder | 63 | President, Chief Executive Officer, Sauder Woodworking Co. | 2004 | |||||||

Frank R. Simon | 54 | Founder & Managing Member / Attorney Simon PLC Attorneys & Counselors | 2021 | |||||||

Dr. K. Brad Stamm | 71 | President and Educational Consultant of Stamm Management Group | 2016 | |||||||

David P. Vernon | 57 | Owner, Licensed Funeral Director & Embalmer Vernon Family Funeral Homes | 2021 | |||||||

The Board of Directors Recommends That You Vote “FOR” The Thirteen

Nominees Aforementioned As Directors Of The Company.

Proxies in the form solicited hereby, which are properly executed and returned to the Company will be voted in favor of each nominee for election to the Board of Directors unless otherwise instructed by the shareholder. Directors will be elected by a plurality of the votes cast at the Annual Meeting. This means that the thirteen nominees with the largest number of “FOR” votes cast will be elected as directors. Abstentions from voting and broker non-votes, if any, on Proposal One will have no effect on outcome of the election of Directors.

8

The following table sets forth certain information with respect to the named executive officers of the Company and the Bank. Executive officers of the Company are appointed annually at the organizational meeting of the Company’s Board of Directors.

| Name | Age | Officer Since | Positions and Offices Held With Company and the Bank & Principal Occupation Held Past Five Years | |||

Lars B. Eller | 57 | 2018 | President and CEO (“PEO”) (1) | |||

Barbara J. Britenriker | 62 | 1992 | Executive Vice President and Chief Financial Officer (“PFO”) (1) and Chief Retail Banking Officer (2) | |||

Rex D. Rice | 65 | 1984 | Executive Vice President and Chief Lending Officer (3) | |||

Benét S. Rupp | 58 | 2019 | Executive Vice President and Chief Administrative Officer (4) | |||

| (1) | The designation PEO means principal executive officer and PFO means principal financial officer under the rules of the SEC. |

| (2) | Ms. Britenriker was Executive Vice President and Chief Financial Officer of the Company. Ms. Britenriker served as Executive Vice President and Chief Retail Banking Officer of the Bank from January 7, 2019 to October 16, 2023 and resumed the position of Executive Vice President and Chief Financial Officer of the Bank on October 16, 2023. |

| (3) | Mr. Rice was appointed to serve as the Chief Lending Officer of the Bank on February 1, 2020. |

| (4) | Ms. Rupp joined the Company in June 2019 and was the Sr. Vice President and Chief People Officer until August 23, 2022. Ms. Rupp was appointed to serve as the Executive Vice President and Chief Administrative Officer of the Bank on August 23, 2022. |

Security Ownership of Certain Beneficial Owners and Named Executive Officers

As of January 1, 2024, the following person was the only shareholder known to the Company to be the beneficial owner of more than 5% of the Company’s outstanding common shares.

Name and Address of Beneficial Owner | Amount of Shares of Common Stock Beneficially Owned | Percent of Total | ||

Andrew J. Briggs 307 N. Defiance Street Archbold, Ohio 43502 | 711,107 | 5.20% |

9

The following table sets forth the number of shares of common stock beneficially owned on December 31, 2023 by each director and nominee, and all directors and named executive officers as a group.

| Beneficial Ownership of Nominees for Director and Named Executive Officers | Amount of Shares of Common Stock Beneficially Owned | Percent of Total | ||||||

Directors: | ||||||||

Ian D. Boyce | 0 | 0.00% | ||||||

Andrew J. Briggs | 711,107 | (1) | 5.20% | |||||

Eugene N. Burkholder | 24,909 | 0.18% | ||||||

Lars B. Eller | 20,678 | (2) | 0.15% | |||||

Jo Ellen Hornish | 36,406 | (3) | 0.27% | |||||

Jack C. Johnson | 5,139 | 0.04% | ||||||

Lori A. Johnston | 1,293 | 0.01% | ||||||

Marcia S. Latta | 6,423 | 0.05% | ||||||

Steven J. Planson | 19,550 | (4) | 0.14% | |||||

Kevin J. Sauder | 5,719 | 0.04% | ||||||

Frank R. Simon | 1,142 | 0.01% | ||||||

K. Brad Stamm | 143,194 | (5) | 1.05% | |||||

David P. Vernon | 44,415 | (6) | 0.33% | |||||

Named Executive Officers (other than Mr. Eller who is noted above): |

| |||||||

Barbara J. Britenriker | 28,552 | (7) | 0.21% | |||||

Rex D. Rice | 23,608 | (8) | 0.17% | |||||

Benét S. Rupp | 5,761 | (9) | 0.00% | |||||

Directors and Executive Officers as a Group |

| |||||||

(16 persons) | 1,077,896 | 7.89% | ||||||

| (1) | Mr. Briggs is a beneficial owner of 5.20% of the Company’s outstanding FMAO common stock. This includes 206,402 shares of common stock owned individually by Mr. Briggs, 3,660 shares of common stock owned jointly with Mr. Brigg’s spouse, and 457,500 shares of common stock held by family trusts of which Mr. Briggs is the trustee. |

| (2) | Includes 11,800 shares representing restricted stock awards issued pursuant to the Company’s Long-Term Incentive Plan, 3,000 shares which will vest on 8/17/2024, 4,000 shares which will vest on 8/23/2025, and 4,800 shares which will vest on 3/01/2026. |

| (3) | Includes 36,406 shares of common stock owned jointly with Ms. Hornish’s spouse. |

| (4) | Includes 3,641 shares of common stock owned jointly with Mr. Planson’s spouse, 2,903 shares of common stock owned individually by Mr. Planson’s spouse, 9,036 shares of common stock held individually, and 3,970 shares of common stock held in his individual trust. |

| (5) | Includes 11,960 shares of common stock owned by Mr. Stamm’s spouse, 22,880 shares of common stock of which he is the custodian, 9,592 shares of common stock owned in trusts of which Mr. Stamm is co-trustee, and 98,762 shares of common stock held individually in his individual trust. |

| (6) | Includes 4,894 shares of common stock held individually and 39,521 shares of common stock owned jointly with Mr. Vernon’s spouse. |

| (7) | Includes 1,215 shares of common stock owned individually by Ms. Britenriker, 21,237 shares of common stock owned jointly with Ms. Britenriker’s spouse and 6,100 shares representing restricted stock awards issued pursuant to the Company’s Long-Term Incentive Plan, 2,000 shares which will vest on 8/17/2024, 2,000 shares which will vest on 8/23/2025, and 2,100 shares which will vest on 3/01/2026. |

| (8) | Includes 19,308 shares of common stock owned jointly with Mr. Rice’s spouse, 4,300 shares representing restricted stock awards issued pursuant to the Company’s Long-Term Incentive Plan, 1,200 shares which will vest on 8/17/2024, 1,200 shares which will vest on 8/23/2025, and 1,900 shares which will vest on 3/01/2026. |

| (9) | Includes 1,362 shares of common stock owned individually by Ms. Rupp and 4,400 shares representing restricted stock awards issued pursuant to the Company’s Long-Term Incentive Plan, 1,000 shares which will vest on 8/17/2024, 1,500 shares which will vest on 8/23/2025, and 1,900 shares which will best on 3/01/2026. |

10

Committees of the Board of Directors

The following table summarizes the membership of the Board of Directors as of December 31, 2023, each of its committees, and the number of times each met during 2023.

Board | Audit Committee | Compensation Committee | Corporate Governance And Nominating Committee | Enterprise Risk Management Committee | ||||||

Ian D. Boyce | Member | Member | ||||||||

Andrew J. Briggs | Member | Member | ||||||||

Eugene N. Burkholder | Member | Chair | ||||||||

Lars B. Eller | Member | |||||||||

Jo Ellen Hornish | Member | Member | Member | |||||||

Jack C. Johnson | Chair | Member | Member | Member | ||||||

Lori A. Johnston | Member | Chair | ||||||||

Marcia S. Latta | Member | Member | Chair | |||||||

Steven J. Planson | Member | Member | Member | |||||||

Kevin J. Sauder | Member | Chair | Member | |||||||

Frank R. Simon | Member | Member | Member | |||||||

K. Brad Stamm | Member | Member | Member | |||||||

David P. Vernon | Member | Member | Member | |||||||

Number of Meetings in 2023 | 7 | 6 | 3 | 5 | 5 | |||||

The Directors of Farmers & Merchants Bancorp, Inc. are also the Directors of The Farmers & Merchants State Bank (the “Bank”), the primary operating subsidiary of the Company. The Company’s Board of Directors met 7 times during 2023 whereas the Board of Directors of the Bank met 14 times in 2023. The Company’s Board of Directors also has each of the following duly constituted committees: Compensation Committee; Corporate Governance and Nominating Committee; Audit Committee, and Enterprise Risk Management Committee.

During 2023, each director attended 100% of the total meetings of the Board and the committees on which they served (held during the period that each served as a director) of the Company and The Farmers & Merchants State Bank.

The Compensation Committee is responsible for establishing salary levels and benefits for the executive officers of the Company. In determining the compensation of the executive officers of the Bank, the Bank has sought to create a compensation program that relates compensation to financial performance, recognizes individual contributions and achievements, and attracts and retains outstanding executive officers.

The Company has a Corporate Governance and Nominating Committee, which is responsible for recommendations to the full Board of Directors of candidates to serve as Director of the Company and the Bank, and to suggest any proposed amendments to the Company’s Articles of Incorporation, Code of Regulations, and other corporate governance policies.

The Company also has an Audit Committee established in accordance with 15 U.S.C. 78c (a) (58) (A). The primary function of the Audit Committee is to review the adequacy of the Company’s system of internal controls, to oversee the scope and adequacy of the work of the Company’s independent public accountants, and to approve and engage a firm of accountants to serve as the Company’s independent public accountants.

The primary function of the Enterprise Risk Management Committee is to advise the Board of Directors regarding the enterprise risk management framework of the Company and to provide oversight to assist the Board of Directors in supervising enterprise risk management activities. The Committee reviews and defines risk exposure limits for each risk category while taking into consideration strategic goals and objectives and current market conditions.

11

Corporate Governance

On May 10, 2017, the Company began listing on the NASDAQ Stock Exchange and became subject to the NASDAQ Capital Market listing standards and corporate governance requirements and complies with all of the corporate governance requirements applicable to it as a NASDAQ listed security. In addition to the NASDAQ requirements, the Company is subject to and complies with the applicable governance requirements of the Sarbanes-Oxley Act of 2002.

In consideration of the size, complexity, and nature of the Company’s business, the Board of Directors, Corporate Governance and Nominating Committee have chosen to establish separate positions for the President and the Board Chairman in order to maintain a separation of power and duties to further strengthen the governance structure. The Board Chairman is a non-employee, director who is not directly involved with the daily operations of the Company. Thus, the Board Chairman is able to focus attention on corporate structure and future strategic direction. The Board Chairman serves as the leader of the Board of Directors, presiding over full board meetings and ensuring full accountability for the shareholders’ interests. Effectively monitoring the decisions and actions of management is one of the primary roles of the Board of Directors. The President and Chief Executive Officer is a bank insider providing management and leadership for ongoing operations of the Company, as well as the Company’s wholly-owned subsidiary, The Farmers & Merchants State Bank, who is also accountable to the Board of Directors. Succession plans exist for the Board Chairman and President and Chief Executive Officer, as well as Vice Chairman of the Board, and all Executive Officers of the Bank.

Director Independence

The Corporate Governance and Nominating Committee of the Board of Directors of the Company undertakes a review of director independence annually and reports on its findings to the full Board in connection with its recommendation of nominees for election to the Board of Directors.

Based upon the review and report of the Corporate Governance and Nominating Committee, the Board of Directors has determined that, (A) all directors have met the independence standards of the NASDAQ Marketplace Rules; and (B) no directors have any relationship which, in the opinion of the Board, would interfere with the exercise of independent judgment in carrying out the responsibilities of a director, with the exceptions of, Mr. Eller, the current President and Chief Executive Officer of the Company and the Bank, and Mr. Briggs, the former First Senior Vice President of Business Development/Indiana of the Bank, who retired in December of 2022, who are both deemed not to be independent. In addition, the members of each of the Compensation Committee, the Corporate Governance and Nominating Committee, and the Audit Committee were determined to be, and under the terms of the respective charters, will continue to be “independent” pursuant to standards adopted by NASDAQ for such committees.

Committee Charters

The Board of Directors has adopted charters for the Audit Committee, the Compensation Committee, the Enterprise Risk Management Committee, and the Corporate Governance and Nominating Committee. Copies of the charters for each of these committees are available on the Bank’s website (www.fm.bank) and are available upon request from the Company. Shareholders desiring a paper copy of one or all of the charters should address written requests to Ms. Melinda L. Gies, Board Administrator/Corporate Secretary of Farmers & Merchants Bancorp, Inc., 307 North Defiance Street, Archbold, Ohio 43502.

Code of Conduct and Ethics

The Board of Directors has adopted a Code of Business Conduct and Ethics (the “Code”). The Code applies to all officers, directors and employees of the Company and the Bank. The administration of the Code has been delegated to the Audit Committee of the Board of Directors, a committee comprised entirely of independent directors. The Code addresses topics such as compliance with laws and regulations, honest and ethical conduct, conflicts of interest, confidentiality and protection of Company assets, fair dealing, and accurate and timely periodic reports, and also provides for enforcement mechanisms. The Board and management of the Company intend to continue to monitor not only the developing legal requirements in this area, but also the best practices of comparable companies, to assure that the Company maintains sound corporate governance practices in the future.

12

A copy of the Company’s Code is available on the website of the Bank (www.fm.bank). In addition, a copy of the Code is available to any shareholder free of charge upon request. Shareholders desiring a copy of the Code should address written requests to Ms. Melinda L. Gies, Board Administrator/Corporate Secretary of Farmers & Merchants Bancorp, Inc., 307 North Defiance Street, Archbold, Ohio 43502, and are asked to mark Code of Business Conduct and Ethics on the outside of the envelope containing the request.

Nominations for Members of the Board of Directors

As noted above under “Corporate Governance,” the Company has a Corporate Governance and Nominating Committee. The current members of the committee all are independent directors. The Corporate Governance and Nominating Committee has developed a policy regarding the consideration of nominations for directors by shareholders. The policy is posted on the Bank’s website for review by shareholders. As outlined in its policy, the Corporate Governance and Nominating Committee will consider nominations from shareholders, although it does not actively solicit such nomination recommendations. Proposed nominations should be addressed to Chairman of the Corporate Governance and Nominating Committee of Farmers & Merchants Bancorp, Inc., 307 North Defiance Street, Archbold, Ohio 43502. Such nominations must include a description of the specific qualifications the candidate possesses and a discussion as to the effect on the composition and effectiveness of the Board. The identification and evaluation of all candidates for nomination to the Board of Directors are undertaken on an ad hoc basis within the context of the Company’s strategic initiatives, at the time a vacancy occurs on the Board, or as anticipated retirement dates approach. In evaluating all candidates, including candidates recommended for nomination by shareholders, the Committee considers a variety of factors, including the candidate’s integrity, independence, qualifications, skills, occupation, experience (including experiences in finance and banking), familiarity with accounting rules and practices, and compatibility with existing members of the Board. In addition, attributes such as place of residence and geographic markets represented, age, gender, ethnicity, race, involvement and visibility in the counties and communities represented by the Company’s current and future geographic footprint, and relationships with the Company and the Bank are given consideration. A candidate’s occupation and experience are given high importance. Other than the foregoing, there are no stated minimum criteria for nominees, although the Committee may consider such other factors as it may deem at the time to be in the best interest of the Company and its shareholders, which factors may change from time to time.

To maintain a wide-ranging mix of individuals, consideration is given to the depth and breadth of an individual’s business and civic experience in leadership positions, as well as their ties to the Company’s markets. Consideration has been given to the number of directors based on the board size of the nineteen peer bank holding companies as identified in the Compensation Discussion and Analysis for comparison of executive officer compensation. The Board of Directors conducted both an annual Self-Evaluation and Director Peer Evaluation during 2023. Attention is given to each director’s attendance at board meetings and committee meetings, as well as anticipated retirement dates and other events that might affect a director’s continued service. All current directors identified in Proposal One were deemed eligible for nomination in the ensuing year.

In June 2023, in consideration of upcoming retirement dates of directors, an additional seat was opened on the Board of Directors which increased the number of Board Directors to 13. This action was intended to bring on a new director and provide sufficient time to become familiar with the Company, Board of Director and Board Committee structure, and expected duties as a member of the Board of Directors.

The Corporate Governance and Nominating Committee will continue to assess and evaluate how the Board of Directors is functioning and whether additional board members are needed. Attention will also be given to anticipated retirement dates and other events that might affect a director’s continued service.

OUR BOARD COMPOSITION

The Company believes in the benefits diversity brings to the Board of Directors. The Corporate Governance and Nominating Committee developed a Board Diversity and Inclusion Policy which was adopted in November 2021 and is reviewed annually. This Policy conforms with NASDAQ rules issued to assure minimum levels of board diversity for all listed companies. The Board Diversity and Inclusion Policy recognizes that diversity of thought makes prudent business sense. Having a board composed of individuals

13

with gender, racial, and ethnic diversity, as well as skills, experience, backgrounds, and perspectives provides for:

| ● | the inclusion of different concepts and ideas that enhance decision-making; |

| ● | robust evaluation of opportunities, issues, and risks; |

| ● | broader relationships within a competitive foot print; |

| ● | heightened capacity for oversight and governance of the Company; and improved competitive advantage |

In consideration of board composition, diversity includes, but is not limited to, business and industry skills, experience, gender, ethnicity, and geography. In evaluating the current board composition, as well as potential candidates, based on their skills, experience, independence, and knowledge, it is the belief that the Board should also collectively reflect the diverse nature of the business environment in which the Company operates. In its evaluation of potential director nominees, the Corporate Governance and Nominating Committee gives significant consideration to racial, gender and ethnic diversity in conjunction with business and industry skills, leadership experience, geographic representation and the added value to the Company and its stakeholders. The Board of Directors aspires to attain levels of board composition in which females and underrepresented minorities are adequately represented. The Board Diversity and Inclusion Policy establishes a process to be followed by the Corporate Governance and Nominating Committee to attract female and racially diverse candidates who would enhance the balance of skills and background on the Board.

Based upon voluntary self-identification by each member of the Company’s Board of Directors, the diversity composition of the Board of Directors for the current year is disclosed as follows:

BOARD DIVERSITY MATRIX (AS OF DECEMBER 31, 2023)

| Total Number of Directors: 13 | ||||||||||||||||||||

| Female | Male | Non-Binary | Did Not Disclose Gender | |||||||||||||||||

Part I: GENDER IDENTITY | ||||||||||||||||||||

Directors | 3 | 10 | ||||||||||||||||||

Part II: DEMOGRAPHIC BACKGROUND | ||||||||||||||||||||

African American or Black | 1 | |||||||||||||||||||

Alaskan Native or Native American | 1 | |||||||||||||||||||

Asian | ||||||||||||||||||||

Hispanic or Latinx | ||||||||||||||||||||

Native Hawaiian or Pacific Islander | ||||||||||||||||||||

White | 2 | 9 | ||||||||||||||||||

Two or More Races or Ethnicities | ||||||||||||||||||||

LGBTQ+ | ||||||||||||||||||||

Did Not Disclose Demographic Background | 0 | 0 | ||||||||||||||||||

As currently comprised, the Board of Directors is a diverse group of individuals who are drawn from various market sectors and industry groups with a presence in the Company’s markets. Board members are individuals with leadership skills, extensive knowledge, and proven business and industry experience who reside in, serve, and represent the Company’s geographic footprint throughout the counties and communities served, as well as the broader region. Current board representation provides a background in accounting, auditing, agriculture, community banking, construction, economics, finance, financial planning, financial services, fund raising, funeral services, healthcare, law and legal services, manufacturing, retail, commercial, and education. The expertise of these individuals covers accounting and financial reporting; asset and wealth management; economics and economic analysis; corporate management and leadership; professional development; strategic planning; business acquisitions; marketing; education; human resources and employee relations; retail sales; small business operations; and family farm operations. In addition, gender and generational attributes further broaden the diversity of the full Board of Directors. What follows is a brief description of the experience and qualifications of each member of the Company’s Board of Directors.

14

Ian D. Boyce

| ||

| Mr. Boyce is a founding member and managing partner of Dickmeyer Boyce Financial Management, a Fee-Only Financial Planning and Wealth Management firm based in Fort Wayne, Indiana with an office in Milwaukee, Wisconsin. Established in 2002, Dickmeyer Boyce provides asset management, comprehensive financial planning and retirement advisory services to individuals, families, businesses, and foundations and has discretionary oversight of $300M in assets under management.

Mr. Boyce is a CERTIFIED FINANCIAL PLANNER™ practitioner and NAPFA-Registered Financial Advisor. In his role, he works directly with clients to provide financial planning and wealth management advice to families and high net worth individuals, and he is a frequent public speaker on financial topics. He specializes in planning for professionals and families in transition and has extensive experience in tax and estate planning, business management, and corporate finance. He holds a Bachelor of Arts degree in Zoology with a minor concentration in Economics from the University of Vermont. He also received an honorary doctorate in Humane Letters from the University of Vermont in 2015. His business experience and economic insight will help inform the board on issues related to small business and the consumer as well as business risk management issues. Mr. Boyce will serve on the Enterprise Risk Management Board Committee.

Mr. Boyce is also actively involved in a numerous professional, civic, and charitable organizations within his community. He currently serves as a Director / Board Member on several Boards including the Parkview Hospital Regional Medical Center (Current Board Chair), Parkview Health System Board, The University of St. Francis, and the Questa Education Foundation. Past service includes board chair for the University of Vermont Board of Trustees and Board Member of the Fort Wayne Community Foundation. | |

Andrew J. Briggs | ||

| Mr. Briggs was the former Chairman of Limberlost Bancshares, Inc. and President of its wholly-owned subsidiary Bank of Geneva. Upon completion of the merger on January 1, 2019 of Limberlost Bancshares, Inc. into Farmers & Merchants Bancorp, Inc., he was appointed to the Board of Directors of the Company and the Bank. With 40-plus years of banking experience, Mr. Briggs served as the First Senior Vice President for Business Development/Indiana of the Bank through 2022. He was the 2019 Chairman of the Indiana Bankers Association and is a member of the Indiana Bankers 40 Year Club. In August 2022, Mr. Briggs was a recipient of the Indiana Bankers Association Leadership in Banking Excellence Award.

In September 2019, Mr. Briggs was honored with the Sagamore of the Wabash award by Indiana Governor, Eric J. Holcomb. This award is given to exemplary Hoosiers in recognition of their distinguished service statewide. Actively involved in the community, Mr. Briggs is Treasurer of the Indiana State Museum, Corporate Secretary of Limberlost State Historic Site, a current Director and past Treasurer of the Northeast Indiana Regional Development Authority, Director of the READI Commission for Northeast Indiana Region, Treasurer of Adams County Economic Development Corporation, and Treasurer of the Adams Public Library System. Additionally, he is past President of the Geneva Town Council.

Mr. Briggs is a graduate of Ball State University. His extensive banking background and experience in corporate leadership enables him to provide knowledge and expertise to the Board regarding the banking industry, business development, and community development. Mr. Briggs serves on the Enterprise Risk Management Board Committee. | |

15

Eugene N. Burkholder

| ||

| Mr. Burkholder owns and manages Falor Farm Center, Inc., a large, independent agricultural retail fertilizer, chemical and seed company. His involvement with Falor Farm Center, Inc. spans over 35 years. He is part owner and member of Burkholder Farms, LLC, and owner of JRBC Properties, LLC. He is also a cash grain farmer. Through his business relationships, he is knowledgeable of the markets covering Fulton, Defiance, Lucas, Henry, and Wood Counties in Ohio and Lenawee County, Michigan. These are the same areas where the Company’s potential customer base is growing and expanding. His induction into the Fulton County Agricultural Hall of Fame in 2011 attests to the depth of his agricultural involvement. He is a current member of the Fulton County Agricultural Society and Ohio Agricultural Business Association.

With his involvement in multiple companies, he also brings an understanding of the concerns and operations of small business. He is a current member of NFIB (National Federation of Independent Businesses), the Ohio Chamber of Commerce and also serves on the Pike-Delta-York School’s Financial Advisory Board. Mr. Burkholder chairs the Enterprise Risk Management Committee and is also a member of the Executive Committee.

Mr. Burkholder is familiar with the workings of the Bank as he previously served on the Bank’s Delta Advisory Board. He graduated from Ohio State University with a Bachelor of Science in Agronomy specializing in soil fertility. A graduate of Wauseon High School, he previously worked for Fulton County Soil & Water Conservation Society and taught Vocational Agriculture at Stryker Local Schools in Stryker, Ohio. | |

| Lars B. Eller | ||

| Mr. Eller joined The Farmers & Merchants State Bank as its President and Chief Executive Officer in September 2018. He was also appointed to the Board of Directors of Farmers & Merchants Bancorp, Inc. and The Farmers & Merchants State Bank in September 2018. He assumed the additional position of President and Chief Executive Officer of the Company on February 1, 2019 upon the retirement of the then current President and Chief Executive Officer.

Mr. Eller has a Master of Business Administration degree from McGill University in Montreal, Canada, and an undergraduate degree from Concordia University in Montreal, Canada. Prior to joining the Bank, he worked as a consultant for Cambridge Savings Bank. In 2013, he joined Royal Bank of America as Executive Vice President and Chief Retail Banking Officer. Royal Bank of America was a publicly held community bank based in Philadelphia, Pennsylvania which was acquired in 2017. Previous banking experience includes serving as Director of Sales and Marketing at Clarity Advantage Corporation; Senior Vice President of Retail Banking for TD Bank in Pennsylvania, Head of National Sales for U.S. Wealth Management at TD Bank, leadership roles at National City Bank in Cleveland, Youngstown, and Dayton; and starting his banking career with TD Bank Financial Group working his way through the ranks as a management trainee to an area manager.

Mr. Eller has extensive experience at both large national and regional banks, as well as community banks. He is able to provide knowledge and expertise to the Board regarding executive management, sales and marketing, retail banking, bank mergers and acquisitions, human resource management, executive officer compensation and incentives, strategic planning, and shareholder relations. He is a member of the Executive Committee. He is a Board Member of the Boy Scouts of America, is a member of the Jumpstart Toledo Business Growth Collaborative Investment Committee, the Bryan Rotary Club, Toledo Museum of Art Director Circle Crystal Member, and Board Member of the Ohio Bankers League and Board Member of the Parkview Bryan Hospital in Williams County, Ohio. | |

16

Jo Ellen Hornish

| ||

| Ms. Hornish is the President and CEO of several Defiance area companies. She oversees the day-to-day strategic and financial operations of Hornish Bros., Inc., Fountain City Leasing, Inc., Advantage Powder Coating, Inc., OneSource Diversified Services, Ltd., and Hornish Properties, LLC.

Purchased in 1984, Hornish Bros., Inc. is a primary carrier supplying logistical, trucking and warehouse services the past 38 years for the General Motors Powertrain plant in Defiance, as well as several other GM plants and their suppliers throughout the Midwest and Ontario. HBI has been recognized as an eight-time General Motors Worldwide Supplier of the Year. Ms. Hornish recently sold Hornish Bros., Inc. in November of 2023.

Fountain City Leasing, Inc. was established in 1981 and currently leases equipment and provides tractor and trailer repairs.

Advantage Powder Coating, Inc. was established to provide an environmentally friendly process to powder coat iron castings for the automotive community. With the transition to all aluminum at the General Motors plant in Defiance, they no longer powder coat; however, they continue to include other foundry related services.

OneSource Diversified Services, Ltd. supplies rental properties and buildings which provide services to the automotive community as well as other commercial companies.

Hornish Properties LLC is a holding company for farmland and real estate.

Born and raised in the Milwaukee, Wisconsin area, Ms. Hornish relocated to Northwest Ohio over 46 years ago and resides near Defiance, Ohio. Her memberships include the American Trucking Association, Ohio Trucking Association, and the Northern Ohio Minority Supplier Development Council. She was also a managing member of the former Sam Hornish Jr. Foundation which provided gifting to many local and national charities.

Due to her corporate leadership and involvement in the automotive and transportation industries, Ms. Hornish can provide guidance to the Board on corporate management and matters related to those industries. She currently serves on the Audit Committee and the Corporate Governance and Nominating Committee. | |

Jack C. Johnson

| ||

| Mr. Johnson has over 45 years’ experience in running an independent retail clothing business. His background and experience encompasses the various aspects of running a small retail business including accounting principles and practices, purchasing, retail sales, marketing, human resource management, and taxes. He brings valuable insight regarding small retail business operations; retail marketing and sales of products and services to consumers; and consumer buying habits and trends during various economic cycles. Prior to joining the Farmers & Merchants Bancorp, Inc. Board of Directors, Mr. Johnson served on the Bank’s Bryan Advisory Board. Mr. Johnson is Chairman of the Board of Directors and the Executive Committee and is a member of the Corporate Governance and Nominating Committee, the Compensation Committee, and the Enterprise Risk Management Committee.

Mr. Johnson graduated from Ohio State University with a Bachelor of Science degree in Business Administration specializing in marketing. A life-time resident of Williams County, Ohio, he is a member of the Bryan Chamber of Commerce and former board member representing the retail division. In addition, he is a member and former president of the Bryan Retail Merchants Association, a graduate of the Hagger | |

17

Business School, a member of the Men’s Apparel Guild of California, and a member of the Action Sports Retailing Group. Mr. Johnson is a former member of The Doneger Group, a fashion merchandising and consulting group providing apparel retailers with merchandising information and trend analysis for the apparel market segments. | ||

Lori A. Johnston

| ||

| Lori Johnston is the President of ProMedica Insurance Corporation, the insurance division of ProMedica Health System. In this role she oversees the medical, dental and workers compensation insurance plan with operations in Ohio, Michigan, Indiana, Kentucky, West Virginia, and Pennsylvania. ProMedica Insurance Corporation provides insurance products in the Medicare, Commercial, Health Exchange and Workers Compensation sectors. Prior to her role at ProMedica Insurance Corporation, Ms. Johnston has served in various executive roles with ProMedica since 1996, including Vice President and Senior Vice President of Finance (12 years); Chief Information Officer, overseeing all Information Technology for the health system including the implementation of ProMedica’s Electronic Health Record, Epic; and President of the ProMedica Physicians Group.

Before coming to ProMedica, Ms. Johnston was a Senior Manager at Ernst & Young where she served on the audit and healthcare consulting teams in Northern Ohio and Southeastern Michigan for thirteen years. She led and conducted audits and financial consulting projects. Ms. Johnston maintained an active CPA license from 1985 to 2010, which is currently inactive. Her extensive experience in corporate leadership and executive management enable her to provide knowledge and expertise to the Board regarding corporate management, corporate finance, strategic planning, organizational development, human resource management, and healthcare strategy. With an extensive accounting and financial background, Ms. Johnston is deemed the financial expert for the Board’s Audit Committee. As the financial expert, Ms. Johnston can provide significant insight regarding accounting principles and practices, auditing and risk management strategies, government regulations, internal controls, and procedures for financial reporting, as well as insight on audit committee functions. In addition to her professional work, she has spent time in Central America and the Philippines doing medical mission work.

Ms. Johnston is the current chairman of the Ohio Association of Health Plans and is a board member of the Health Plan Alliance. She has a Masters of Business Administration degree from the Fisher College of Business at the Ohio State University, and a Bachelor of Business Administration in Accounting degree from the University of Toledo. She serves on the boards of the Toledo Mud Hens and Toledo Walleye, Compassion Health Toledo, the St. Francis de Sales High School Foundation and the Advisory Council for the Area Office on Aging. She is currently chairing the Northwest Ohio Go Red for Women initiative and is on the fundraising cabinet for the Northwest Ohio YWCA. Ms. Johnston is originally from Henry County, Ohio and now resides in Lucas County, Ohio. | |

18

Marcia S. Latta, Ed.D

| ||

| Dr. Latta has a strong background in the fields of advancement and board governance with multiple organizations. She has been responsible for raising over $400 million for higher education and healthcare organizations. Dr. Latta also has decades of experience serving on four different organizations’ board governance committees, chairing three of them, serving as the lead staff person for multiple university trusteeship committees, and as an academic researcher and presenter on the subject. She consults with non-profit organizations through Latta Strategies.

Dr. Latta recently retired as Vice President for University Advancement at University of Findlay where she provided leadership for fundraising, alumni and parent relations, and the nationally-known Mazza Museum. Prior executive experience includes serving as Vice President for Advancement at DePauw University, as the Bowling Green State University Foundation’s Vice President where she oversaw the investments and grant awards of a $120 million Foundation, and Campaign Director for the BGSU Centennial Campaign. Marcia has prior experience as a CEO of a healthcare foundation. Early in her career she served as a congressional aide and also did volunteer work in Costa Rica.

Dr. Latta is a frequent presenter across the nation and internationally on development and board governance issues. Through her experience and education, she provides a strong understanding and commitment to leadership, board governance, corporate management, and public policy. She holds a Doctor of Education degree in leadership and policy studies from BGSU and has completed Harvard University’s School of Education’s Management and Leadership program. Dr. Latta chairs the Corporate Governance and Nominating Committee and also serves on the Compensation Committee. She is active in many civic and professional organizations including as a founding member of the Ohio State Parks Foundation Board, where she serves on the executive committee and chairs the governance committee, the Watterson Family Foundation, and the Bowling Green Community Foundation where she was the founding president. Prior board service includes the Toledo Zoo, Historic Sauder Village, and Ohio Citizens for the Arts. Marcia is former president of the Northwest Ohio Association of Fundraising Professionals which named her its Outstanding Fundraising Professional in 2009, and she was named a “Woman of Distinction” from the Western Ohio Girl Scouts in 2013. A former resident of Williams County, Ohio, she now resides in Wood County. | |

Steven J. Planson

| ||

| Mr. Planson has successfully managed a large family farm corporation for over 25 years with a primary focus on grain production and processing tomatoes. In addition, he is involved with a family trucking operation. Mr. Planson and his wife were previously named the Ohio Farm Bureau Federation’s Outstanding Young Couple in recognition of their farming operation accomplishments and leadership in the agricultural community. He is a past recipient of Red Gold Master Grower Awards for his tomato growing operation. His extensive farming background and practical experience provide significant insight regarding farm business management; agriculture finance; commodity sales and marketing; as well as the local farm economy and challenges to the farming industry. He also offers a valuable perspective on local and state government matters from his service as a Township Trustee. Mr. Planson is a member of the Audit Committee and the Enterprise Risk Management Committee.

Prior to joining the Farmers & Merchants Bancorp, Inc. Board of Directors, Mr. Planson served on the Bank’s Stryker Advisory Board. A life-time resident of Williams County, Ohio and graduate of Stryker High School, Stryker, Ohio, Mr. Planson has served as a Springfield Township Trustee in Williams County, Ohio for over 25 years. As a Township Trustee, he also served on the Springfield Township Zoning Board. He was a member | |

19

of the Stryker Farmers Exchange Board for 22 years, serving as president six of those years. Mr. Planson is an active member of the Williams County Farm Bureau, Stryker Heritage Council, Stryker Rotary Club, and Friends of Stryker Library. He is a former board member of the Williams County Farm Bureau, former trustee of the Campbell Soup Tomato Growers Association, and former member of the Stryker Chamber of Commerce. In 2011, Mr. Planson was the recipient of the Paul Harris Award by the Rotary Foundation. The Paul Harris Award recognizes individuals who have made contributions in promoting human philanthropic projects throughout the local community and around the world. | ||

Kevin J. Sauder

| ||

| Mr. Sauder has served as President/Chief Executive Officer since 2001 of Sauder Woodworking Company, a large privately-held, family-run corporation. The corporation, which is North America’s largest manufacturer of ready-to-assemble furniture, employs over 2,000 employees. Through its subsidiaries, Sauder Manufacturing and Progressive, Inc., serve the worship, education, health care, and assembled bedroom furniture markets. His extensive experience in executive management and corporate leadership enables him to provide knowledge and expertise to the Board regarding corporate management, corporate finance, product sales and marketing, and human resource management. His knowledge and expertise further enable him to assist the board on matters involving business acquisition, financial turnarounds, strategic planning, executive officer compensation and incentives, and shareholder relations. Mr. Sauder is Vice Chairman of the Board of Directors, Chairman of the Compensation Committee, a member of the Executive Committee and a member of the Corporate Governance and Nominating Committee.

Mr. Sauder has a Masters of Business Administration degree from Duke University, and an undergraduate degree from Miami University. A long-term resident of Fulton County, Ohio, Mr. Sauder is the past Chairman of the American Home Furnishings Alliance, and past Finance Committee Chair and Board Member of the ProMedica Health System. Mr. Sauder was the recipient of the prestigious 2023 American Home Furnishings Alliance (AHFA) Distinguished Service Award. This annual award is presented each year to an industry executive selected for their contribution to the home furnishings industry, to AHFA, and to the recipient’s local community. | |

Frank R. Simon

| ||

| Mr. Simon is the founding and Managing Member of Simon PLC Attorneys & Counselors whose practice areas include Receiverships; Litigation; Foreclosure; Collections; Creditors Rights; Workouts; Loan Documentation; Fraud and Negotiable Instrument Law; and Retail/Operations based Litigation. He is the primary point of contact for all matters at Simon PLC’s offices in Troy, Michigan, Arizona, Illinois, Florida, New York, Ohio, and Texas. The firm represents over 50 financial institutions and mid-size corporations.

As a court appointed Receiver, Mr. Simon has extensive experience in managing/operating ongoing business concerns of Receiverships/Assignment Estates and identifying, seizing, securing, and liquidating real and personal assets to satisfy creditors. He owns and manages several commercial properties in Michigan. His extensive experience in the practice of law, business management and operations, and corporate leadership enables him to provide knowledge and expertise to the Board of Directors on matters involving the law and legal interpretations, litigation strategies, the banking industry, business acquisition, financial turnarounds, collections, foreclosures, loan workouts, shareholder relations, as well as the current economic climate and market conditions in the State of Michigan. Mr. Simon is currently a | |

20

member of the Enterprise Risk Management Committee and the Corporate Governance and Nominating Committee.

Mr. Simon is a graduate of the University of Michigan and the University of Detroit School of Law receiving his Juris Doctor degree in 1995. He is admitted to practice as a member of the state bars of Michigan, District of Columbia, New York, and Illinois. In 2003, Mr. Simon completed a three-year program earning an additional graduate degree from the Graduate School of Banking at the University of Wisconsin-Madison. Mr. Simon is certified to document and conduct Small Business Administration 504 Loan Closings. He has also completed the Liquidations and Post Debenture Workout course through the National Association of Development Companies (NADCO) program. He serves as an Advisor to 10Core Law Society which provides access to housing literacy for underprivileged first-time home buyers. He is a member of the Detroit Athletic Club and a past Board Member of the YMCA of Metropolitan Detroit | ||

K. Brad Stamm

| ||

| Dr. Stamm presently serves as President and Educational Consultant of Stamm Management Group. Until his retirement in 2018, he served as Chair of the Division of Business at Cornerstone University in Grand Rapids, Michigan, where he also taught economics for nineteen years. Prior to that he was Chair of the Division of Business and Economics at Nyack College in New York with campuses both in Nyack and New York City. In addition, he teaches Economics for Grace College in Winona Lake, Indiana.

He received his undergraduate degree from Bowling Green State University with a Bachelor of Science degree in Business Administration and Economics, his MBA from Eastern University in St. David’s, Pennsylvania, his Ph.D. in Economics from Fordham University in New York City, and additional coursework at Gordon College and Florida State University. His academic specializations and certifications are in Applied Microeconomics, International Economics, Macroeconomic Theory, and Industrial Organization. Dr. Stamm has taught graduate courses several times in China and was a special lecturer in economics for six years at LCC International University in Klaipeda, Lithuania, and is a reviewer for the “Christian Business Academic Review.”

He has extensive experience in management, marketing, promotion, finance, and economic analysis. Dr. Stamm was a regular economic commentator on radio stations in West Michigan and periodically served as an Economic Analyst for West Michigan Television Stations. He has had several articles published in newspapers and business journals on topics related to economics along with his annual economic forecast. He is a member of the Audit and Enterprise Risk Management Committees.

Raised in Archbold, Ohio, he worked for several years in the community before moving to the East Coast where he was involved in concert promotion and production with large outdoor festivals in addition to marketing concerts for Radio City Music Hall, Jones Beach Theater, and Madison Square Garden. He and his family now reside in Ada, Michigan. His current memberships include the American Economic Association, the Association of Christian Economists, Omicron Delta Epsilon (the Graduate International Economics Honors Society), and Delta Mu Delta (Business Honor Society). Dr. Stamm is also a trustee of Pillar College in Newark, New Jersey and serves on the Advisory Committee of the Ron Blue Institute at Cornerstone University in Grand Rapids, Michigan. | |

21

David P. Vernon

| ||

| Mr. Vernon was a former member of the Board of Directors of Perpetual Federal Savings Bank of Urbana. Upon completion of the acquisition of Perpetual Federal Savings Bank of Urbana on October 1, 2021, he was appointed to the Board of Directors of the Company and the Bank.

Mr. Vernon is the President of Vernon Family Funeral Homes and Set-In-Stone Monuments with seven locations serving Champaign and Miami Counties in Ohio. Mr. Vernon and his family moved to Champaign County in 1999. In 2002, he acquired the first two funeral homes in Mechanicsburg and North Lewisburg, Ohio. In 2003, he added a funeral home located in Urbana. Most recently in 2023, he obtained the funeral homes in both St. Paris and Fletcher, Ohio. Vernon Family Funeral Homes offer a tradition of compassionate, family-centered funeral services.

His business ownership and experience in the funeral services industry, as well as his community involvement, enable him to provide knowledge and insight regarding business management and small business operations in the Champaign County footprint and surrounding area.

Born in Liverpool, England, he moved to the United States at a young age. Raised in Enon, Ohio, Mr. Vernon is a 1985 graduate of Greenon High School. He graduated from Wright State University in 1987 with an Associate’s Degree in Applied Sciences and the Cincinnati College of Mortuary Science in 1988 with a Bachelors in Mortuary Science. Mr. Vernon currently serves as President of the Champaign County Board of Health and is a Board Member of the Champaign Memorial Foundation, the Maple Grove Cemetery Board, and a member of the Mechanicsburg Lodge #113 F.&A.M. Mr Vernon currently serves on the Audit and Compensation Committees. | |

Shareholder Communication