UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-4946

THOMPSON IM FUNDS, INC.

(Exact name of registrant as specified in charter)

918 Deming Way

Madison, Wisconsin 53717

(Address of principal executive offices)--(Zip code)

Jason L. Stephens

Chief Executive Officer

Thompson IM Funds, Inc.

918 Deming Way

Madison, Wisconsin 53717

(Name and address of agent for service)

With a copy to:

Matthew C. Vogel, Esq.

Quarles & Brady LLP

411 East Wisconsin Avenue

Milwaukee, Wisconsin 53202

Registrant's telephone number, including area code: (608) 827-5700

Date of fiscal year end: November 30, 2018

Date of reporting period: November 30, 2018

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, N.W., Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Report to Stockholders.

THOMPSON IM FUNDS, INC.

ANNUAL REPORT TO SHAREHOLDERS

NOTE ON FORWARD-LOOKING STATEMENTS

The matters discussed in this report may constitute forward-looking statements. These include any Advisor or portfolio manager predictions, assessments, analyses or outlooks for individual securities, industries, investment styles, market sectors, interest rates, economic trends and/or markets. These statements involve risks and uncertainties. In addition to the general risks described for each Fund in its current Prospectus, other factors bearing on these reports include the accuracy of the Advisor’s or portfolio manager’s forecasts and predictions, the appropriateness of the investment strategies designed by the Advisor or portfolio manager and the ability of the Advisor or portfolio manager to implement its strategies efficiently and successfully. Any one or more of these factors, as well as other risks affecting the securities markets generally, could cause the actual results of any Fund to differ materially as compared to its benchmarks.

THOMPSON IM FUNDS, INC.

ANNUAL REPORT TO SHAREHOLDERS

November 30, 2018

CONTENTS

| | | Page(s) |

| LargeCap Fund | | |

| Investment review | | 2-4 |

| Schedule of investments | | 5-8 |

| |

| MidCap Fund | | |

| Investment review | | 9-11 |

| Schedule of investments | | 12-15 |

| |

| Bond Fund | | |

| Investment review | | 16-18 |

| Schedule of investments | | 19-33 |

| |

| Fund Expense Examples | | 34 |

| |

| Financial Statements | | |

| Statements of assets and liabilities | | 35 |

| Statements of operations | | 36 |

| Statements of changes in net assets | | 37 |

| Notes to financial statements | | 38-44 |

| Financial highlights | | 45-47 |

| |

| Report of Independent Registered Public Accounting Firm | | 48 |

| |

| Directors and Officers | | 49-50 |

| |

| Additional Information | | 51-54 |

This report contains information for existing shareholders of Thompson IM Funds, Inc. It

does not constitute an offer to sell. This Annual Report is authorized for distribution to prospective investors

only when preceded or accompanied by a Fund Prospectus, which contains information about

the Funds’ objectives and policies, risks, management, expenses and other information.

A Prospectus can be obtained by calling 1-800-999-0887.

Please read your Prospectus carefully.

1

| LARGECAP FUND INVESTMENT REVIEW(Unaudited) |

| November 30, 2018 |

Portfolio Managers

James T. Evans, CFA

Jason L. Stephens, CFA

Performance

The LargeCap Fund produced a total return of 1.72% for the fiscal year ended November 30, 2018, as compared to its benchmark, the S&P 500 Index, which returned 6.27%.

| Comparison of Change in Value of a Hypothetical $10,000 Investment |

|

| Average Annual Total Returns |

| Through 11/30/18 |

| | 1 Year | | 3 Year | | 5 Year | | 10 Year |

| Thompson LargeCap Fund | | 1.72% | | 10.23% | | 8.08% | | 13.54% |

| S&P 500 Index | | 6.27% | | 12.16% | | 11.12% | | 14.32% |

Gross Expense Ratio as of 03/31/18 was 1.22%.

Net Expense Ratio after reimbursement as of 12/01/18 was 1.03%.*

| * | The Advisor has contractually agreed to waive management fees and/or reimburse expenses incurred by the LargeCap Fund through March 31, 2020, so that the annual operating expenses of the Fund do not exceed 1.03% of its average daily net assets. Net expense ratios are current as of the most recent Prospectus and are applicable to investors. |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 1-800-999-0887 or visiting www.thompsonim.com.

Results include the reinvestment of all dividends and capital gains distributions. Investment performance reflects all fee waivers that may be in effect. In the absence of such waivers, total return would be reduced. The performance information reflected in the graph and the table above does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares, nor does it imply future performance. The S&P 500 Index is an unmanaged index commonly used to measure the performance of U.S. stocks. You cannot directly invest in an index.

The S&P 500 Index is a product of S&P Dow Jones Indices LLC and has been licensed for use by Thompson Investment Management, Inc. S&P®and S&P 500®are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”). The Thompson IM Funds are not sponsored, endorsed, sold or promoted by S&P Dow Jones Indices LLC, Dow Jones, S&P or their respective affiliates, and none of S&P Dow Jones Indices LLC, Dow Jones, S&P nor their respective affiliates makes any representation regarding the advisability of investing in such products.

See Notes to Financial Statements.

2

| LARGECAP FUND INVESTMENT REVIEW(Unaudited) (Continued) |

| November 30, 2018 |

Management Commentary

The Fund’s lag relative to its benchmark for the fiscal year was primarily driven by underperformance in the Consumer Discretionary, Financial and Industrial sectors. While some of the discrepancy can be attributed to poor security selection, we believe that a broader trend was at play. Specifically, one segment of the market seemed to be discounting the possibility of an impending recession while another did not. Many of the Fund’s holdings recorded record earnings during the year, yet their stock prices remain mired in a sideways or worse pattern. In other words, the market appeared to be assuming said earnings will not be sustainable. Short of a recession, we do not believe this to be the case.

We’ve seen this divergence between growth and value stocks before, but the differential over recent time periods has been particularly acute. In fact, the S&P 500 Growth Index outperformed the S&P 500 Value Index by 7.8% during the fiscal year and by 22.45% over the previous two fiscal years. While our “Growth at a Reasonable Price” strategy generally leads us to invest in a blend of growth and value stocks, over different points in the economic cycle the Fund typically drifts more in one direction or the other. Coming out of the financial crisis, many great companies saw their stock prices depressed notwithstanding their growth prospects. Thus, the Fund tilted slightly to the growth side at the time based on the abundance of attractive opportunities we found. In the last few years we have tilted more towards the value side, as many of the best growth companies appreciated to what we believed were unrealistic earnings multiples and were in our opinion no longer attractive.

Even though our current value bias has cost the Fund relative performance over the past fiscal year, we believe it remains the best option for shareholders going forward based on the existing set of opportunities. Many quality firms with strong free cash flow and growing earnings have been trading at a discount to the S&P 500 index’s price-to-earnings (P/E) ratio. While a few of these firms may ultimately turn out to be unforeseen value traps, our view is that the majority should prosper as long as the economy can avoid a recession. If our belief that a recession is not imminent proves to be false, we expect the high-flying growth names that have led the market will likely suffer the greatest relative hit to their stock prices. Either way, it suggests to us that the current fund positioning is the best one for shareholders going forward.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice.

Mutual fund investing involves risk. Principal loss is possible. Investments in smaller companies involve additional risks such as limited liquidity and greater volatility. Investments in American Depositary Receipts (“ADRs”) are subject to some extent to the risks associated with directly investing in securities of foreign issuers, including the risk of changes in currency exchange rates, expropriation or nationalization of assets, and the impact of political, diplomatic, or social events. Investments in real estate securities may involve greater risk and volatility including greater exposure to economic downturns and changes in real estate values, rents, property taxes, and tax and other laws. A real estate investment trust’s (REIT’s) share price may decline because of adverse developments affecting the real estate industry.

Please refer to the Schedule of Investments on page 5 of this report for holdings information. The management commentary above as well as Fund holdings and asset/sector allocations should not be considered a recommendation to buy or sell any security. In addition, please note that Fund holdings and asset/sector allocations are subject to change.

Free Cash Flow is a measure of financial performance calculated as operating cash flow minus capital expenditures. Free cash flow (FCF) represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base.

Price-To-Earnings (P/E) Ratio is a valuation ratio of a company’s current share price compared to its per-share earnings. Divide market value of a share by the earnings per share.

S&P 500 Growth Index is a market capitalization weighted index. It consists of stocks within the S&P 500 Index that exhibit strong growth characteristics - sales growth, the ratio of earnings change to price, and momentum.

S&P 500 Value Index is a market capitalization weighted index. It consists of stocks within the S&P 500 Index that exhibit strong value characteristics - the ratios of book value, earnings, and sales to price.

Earnings Growth is a measure of growth in a company’s net income over a specific period, often one year. It is not a prediction of the Fund’s future returns.

See Notes to Financial Statements.

3

| LARGECAP FUND INVESTMENT REVIEW(Unaudited) (Continued) |

| November 30, 2018 |

| Sector Weightings at 11/30/18 |

| % of Total Investments |

| |

|

| Top 10 Equity Holdings at 11/30/18 |

| | | | % of Fund’s |

| Company | | Industry | | Net Assets |

| Alphabet, Inc. Class A | | Interactive Media & Services | | 3.26% |

| Microsoft Corp. | | Software | | 2.99% |

| Exxon Mobil Corp. | | Oil, Gas & Consumable Fuels | | 2.49% |

| The Walt Disney Co. | | Entertainment | | 2.36% |

| Hanger, Inc. | | Health Care Providers & Services | | 2.30% |

| Bank of America Corp. | | Banks | | 2.27% |

| CBS Corp. Class B | | Media | | 2.27% |

| JPMorgan Chase & Co. | | Banks | | 2.10% |

| Cisco Systems, Inc. | | Communications Equipment | | 2.06% |

| Pfizer Inc. | | Pharmaceuticals | | 2.01% |

As of November 30, 2018, 99.8% of the Fund’s net assets were in equity and short-term investments.

See Notes to Financial Statements.

4

| LARGECAP FUND SCHEDULE OF INVESTMENTS |

| November 30, 2018 |

| | Shares | | Value |

| COMMON STOCKS - 99.7% | | | | $121,374,631 |

| (COST $126,080,464) | | | | |

| |

| Communication Services - 10.6% | | | | 12,903,114 |

| Entertainment - 3.3% | | | | |

| The Walt Disney Co. | | 24,850 | | 2,869,926 |

| Viacom Inc. Class B | | 37,775 | | 1,165,737 |

| Interactive Media & Services - 5.0% | | | | |

| Alphabet Inc. Class A (a) | | 3,575 | | 3,966,999 |

| Facebook, Inc. Class A (a) | | 15,200 | | 2,137,272 |

| Media - 2.3% | | | | |

| CBS Corp. Class B | | 51,000 | | 2,763,180 |

| |

| Consumer Discretionary - 11.1% | | | | 13,544,888 |

| Automobiles - 1.0% | | | | |

| Harley-Davidson, Inc. | | 28,400 | | 1,201,036 |

| Distributors - 1.0% | | | | |

| LKQ Corp. (a) | | 45,225 | | 1,259,064 |

| Hotels, Restaurants & Leisure - 1.4% | | | | |

| Starbucks Corp. | | 25,975 | | 1,733,052 |

| Household Durables - 1.1% | | | | |

| TopBuild Corp. (a) | | 26,352 | | 1,342,634 |

| Internet & Direct Marketing Retail - 2.0% | | | | |

| eBay Inc. (a) | | 81,895 | | 2,444,566 |

| Leisure Products - 0.9% | | | | |

| Brunswick Corp. | | 19,700 | | 1,044,888 |

| Multiline Retail - 0.8% | | | | |

| Target Corp. | | 14,060 | | 997,698 |

| Specialty Retail - 1.9% | | | | |

| Bed Bath & Beyond Inc. | | 82,600 | | 1,063,888 |

| Lumber Liquidators Holdings, Inc. (a) | | 100,175 | | 1,265,210 |

| Textiles, Apparel & Luxury Goods - 1.0% | | | | |

| Hanesbrands, Inc. | | 74,975 | | 1,192,852 |

| |

| Consumer Staples - 4.3% | | | | 5,188,435 |

| Food & Staples Retailing - 2.0% | | | | |

| Walgreens Boots Alliance, Inc. | | 28,825 | | 2,440,613 |

| Household Products - 2.3% | | | | |

| Kimberly-Clark Corp. | | 13,168 | | 1,519,192 |

| The Procter & Gamble Co. | | 13,000 | | 1,228,630 |

| |

| Energy - 6.8% | | | | 8,308,116 |

| Energy Equipment & Services - 0.9% | | | | |

| Schlumberger Ltd. | | 24,144 | | 1,088,894 |

| Oil, Gas & Consumable Fuels - 5.9% | | | | |

| Chevron Corp. | | 10,170 | | 1,209,620 |

| Devon Energy Corp. | | 45,025 | | 1,217,026 |

| EOG Resources, Inc. | | 8,500 | | 878,135 |

| Exxon Mobil Corp. | | 38,070 | | 3,026,565 |

| Noble Energy, Inc. | | 37,400 | | 887,876 |

See Notes to Financial Statements.

5

| LARGECAP FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | Shares | | Value |

| COMMON STOCKS(continued) | | | | |

| |

| Financials - 15.2% | | | | $18,459,562 |

| Banks - 9.5% | | | | |

| Bank of America Corp. | | 97,500 | | 2,769,000 |

| CIT Group Inc. | | 32,275 | | 1,498,528 |

| Citigroup Inc. | | 37,530 | | 2,431,569 |

| JPMorgan Chase & Co. | | 22,955 | | 2,552,366 |

| PNC Financial Services Group, Inc. | | 6,795 | | 922,625 |

| SunTrust Banks, Inc. | | 10,450 | | 655,111 |

| Zions Bancorporation, N.A. | | 14,525 | | 706,787 |

| Capital Markets - 4.2% | | | | |

| Northern Trust Corp. | | 18,635 | | 1,849,151 |

| State Street Corp. | | 30,225 | | 2,207,029 |

| The Goldman Sachs Group, Inc. | | 5,550 | | 1,058,330 |

| Consumer Finance - 0.5% | | | | |

| Discover Financial Services | | 8,820 | | 628,866 |

| Insurance - 1.0% | | | | |

| Fidelity National Financial, Inc. | | 35,125 | | 1,180,200 |

| |

| Health Care - 20.4% | | | | 24,744,034 |

| Biotechnology - 6.8% | | | | |

| AbbVie Inc. | | 21,525 | | 2,029,162 |

| Amgen Inc. | | 5,975 | | 1,244,294 |

| Celgene Corp. (a) | | 32,875 | | 2,374,232 |

| Exact Sciences Corp. (a) | | 29,500 | | 2,300,410 |

| MiMedx Group Inc. (a) | | 89,500 | | 269,395 |

| Health Care Equipment & Supplies - 1.3% | | | | |

| Abbott Laboratories | | 21,000 | | 1,555,050 |

| Health Care Providers & Services - 8.3% | | | | |

| Cigna Corp. | | 6,000 | | 1,340,280 |

| CVS Health Corp. | | 26,800 | | 2,149,360 |

| Hanger, Inc. (a) | | 139,475 | | 2,793,684 |

| HCA Healthcare, Inc. | | 9,800 | | 1,411,102 |

| McKesson Corp. | | 18,960 | | 2,360,520 |

| Pharmaceuticals - 4.0% | | | | |

| Johnson & Johnson | | 8,410 | | 1,235,429 |

| Merck & Co., Inc. | | 15,500 | | 1,229,770 |

| Pfizer Inc. | | 53,025 | | 2,451,346 |

| |

| Industrials - 8.5% | | | | 10,492,593 |

| Air Freight & Logistics - 1.3% | | | | |

| FedEx Corp. | | 6,975 | | 1,597,275 |

| Airlines - 0.8% | | | | |

| Delta Air Lines, Inc. | | 17,000 | | 1,032,070 |

| Building Products - 3.3% | | | | |

| Johnson Controls Int’l. PLC | | 55,741 | | 1,938,672 |

| Masco Corp. | | 67,075 | | 2,125,607 |

See Notes to Financial Statements.

6

| LARGECAP FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | Shares | | Value |

| COMMON STOCKS(continued) | | | | |

| |

| Industrials (continued) | | | | |

| Electrical Equipment - 0.9% | | | | |

| ABB Ltd. ADR | | 54,175 | | $1,098,669 |

| Industrial Conglomerates - 1.4% | | | | |

| General Electric Co. | | 233,025 | | 1,747,687 |

| Trading Companies & Distributors - 0.8% | | | | |

| HD Supply Holdings, Inc. (a) | | 23,875 | | 952,613 |

| |

| Information Technology - 21.4% | | | | 26,078,408 |

| Communications Equipment - 3.4% | | | | |

| Cisco Systems, Inc. | | 52,260 | | 2,501,686 |

| Lumentum Holdings Inc. (a) | | 13,700 | | 609,239 |

| Viavi Solutions Inc. (a) | | 105,735 | | 1,072,153 |

| Electronic Equipment, Instruments & Components - 2.0% | | | | |

| Corning Inc. | | 48,925 | | 1,576,363 |

| II-VI Inc. (a) | | 16,500 | | 617,430 |

| Maxwell Technologies, Inc. (a) | | 93,997 | | 235,932 |

| IT Services - 3.0% | | | | |

| Alliance Data Systems Corp. | | 10,750 | | 2,153,870 |

| PayPal Holdings, Inc. (a) | | 10,570 | | 907,012 |

| Visa Inc. Class A | | 4,300 | | 609,353 |

| Semiconductors & Semiconductor Equipment - 6.8% | | | | |

| Infineon Technologies A.G. ADR | | 87,050 | | 1,845,460 |

| Intel Corp. | | 31,600 | | 1,558,196 |

| Maxim Integrated Products, Inc. | | 24,755 | | 1,384,300 |

| NXP Semiconductors N.V. | | 16,000 | | 1,333,920 |

| Qualcomm Inc. | | 37,330 | | 2,174,846 |

| Software - 4.7% | | | | |

| Microsoft Corp. | | 32,801 | | 3,637,303 |

| Oracle Corp. | | 42,475 | | 2,071,081 |

| Technology Hardware, Storage & Peripherals - 1.5% | | | | |

| Apple Inc. | | 10,025 | | 1,790,264 |

| |

| Materials - 1.4% | | | | 1,655,481 |

| Metals & Mining - 1.4% | | | | |

| Freeport-McMoRan Inc. | | 138,650 | | 1,655,481 |

See Notes to Financial Statements.

7

| LARGECAP FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | Shares | | Value |

| SHORT-TERM INVESTMENTS - 0.1% | | | | $100,000 |

| (COST $100,000) | | | | |

| | | | | |

| Money Market Funds - 0.1% | | | | 100,000 |

| First American Gov’t. Obligations Fund Class X, 2.131% (b) | | 100,000 | | 100,000 |

| | | | | |

| TOTAL INVESTMENTS - 99.8% (COST $126,180,464) | | | | 121,474,631 |

| | | | | |

| NET OTHER ASSETS AND LIABILITIES - 0.2% | | | | 242,420 |

| | | | | |

| NET ASSETS - 100.0% | | | | $121,717,051 |

| (a) | Non-income producing security. |

| (b) | Represents the 7-day yield at November 30, 2018. |

| Abbreviations: |

| ADR | | American Depositary Receipt |

| A.G. | | Aktiengesellschaft is the German term for a public limited liability corporation. |

| N.V. | | Naamloze Vennootschap is the Dutch term for a public limited liability corporation. |

| PLC | | Public Limited Company |

The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of MSCI Inc. (“MSCI”) and Standard & Poor’s Financial Services LLC (“S&P”) and is licensed for use by Thompson Investment Management, Inc. Neither MSCI, S&P, nor any other party involved in making or compiling the GICS or any GICS classifications makes any warranties with respect thereto or the results to be obtained by the use thereof, and no such party shall have any liability whatsoever with respect thereto.

See Notes to Financial Statements.

8

| MIDCAP FUND INVESTMENT REVIEW(Unaudited) |

| November 30, 2018 |

Portfolio Managers

James T. Evans, CFA

Jason L. Stephens, CFA

Performance

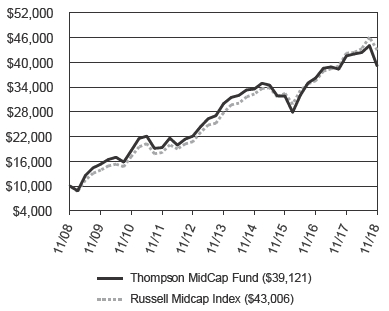

The MidCap Fund produced a total return of -5.85% for the fiscal year ended November 30, 2018, as compared to its benchmark, the Russell Midcap Index, which returned 1.89%.

| Comparison of Change in Value of a Hypothetical $10,000 Investment |

|

| Average Annual Total Returns |

| Through 11/30/18 |

| | 1 Year | | 3 Year | | 5 Year | | 10 Year |

| Thompson MidCap Fund | | -5.85% | | 7.14% | | 5.47% | | 14.62% |

| Russell Midcap Index | | 1.89% | | 9.84% | | 9.14% | | 15.71% |

Gross Expense Ratio as of 03/31/18 was 1.44%.

Net Expense Ratio after reimbursement as of 03/31/18 was 1.15%.*

| * | The Advisor has contractually agreed to waive management fees and/or reimburse expenses incurred by the MidCap Fund through March 31, 2020, so that the annual operating expenses of the Fund do not exceed 1.15% of its average daily net assets. Net expense ratios are current as of the most recent Prospectus and are applicable to investors. |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 1-800-999-0887 or visiting www.thompsonim.com.

Results include the reinvestment of all dividends and capital gains distributions. Investment performance reflects all fee waivers that may be in effect. In the absence of such waivers, total return would be reduced. The performance information reflected in the graph and the table above does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares, nor does it imply future performance. The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000 Index based on total market capitalization. You cannot directly invest in an index.

FTSE Russell is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. “FTSE®” and “Russell®” are trademarks of the London Stock Exchange Group.

See Notes to Financial Statements.

9

| MIDCAP FUND INVESTMENT REVIEW(Unaudited) (Continued) |

| November 30, 2018 |

Management Commentary

The Fund’s lag for the fiscal year was primarily driven by underperformance in the Consumer Discretionary, Information Technology and Financials sectors. Historically, the Fund’s “big losers” from an individual security perspective have tended to be offset by its “big winners” over time. While we did benefit this fiscal year from some outsized performers like Hanger and Exact Sciences, we didn’t have enough of them to offset big losers like REV Group and Accelerate Diagnostics. In the long run, we would expect our batting average at each extreme typically to be more balanced, as it has been in the past. We believe that the larger reason for the Fund’s divergence from its benchmark is more likely related to an increase in investor uncertainty with respect to the future economic growth prospects of the U.S. economy.

For example, the Fund’s investments in the Financials sector lagged those of its benchmark by -1.05% during the period. There were no “big losers” in this sector among the stocks held by the Fund. The problem was instead that the Fund favored banks over other financial companies, and bank stocks have not recently kept up with our perception of their underlying economic performance. Additionally, investments in other sectors that benefit from housing turnover also underperformed. While the housing sector has shown signs of slowing, we believe it’s premature to infer that a sharp downturn is imminent, though stock performance would suggest otherwise. Many other pro-cyclical industries are performing poorly, as well.

Investor enthusiasm driven by tax cuts seems to have been replaced by anxiety related to Federal Reserve interest rate policy and the potential for a trade war with China. While trade policy is important, we do believe that investors have potentially been overreacting. Many investors tend to fight the last battle, which in this case means selling the financial-and housing-related stocks that were central to the Great Recession. Today we believe bank balance sheets are on the whole as strong as ever, and that the housing sector is actually likely undersupplied. Whatever problem emerges as the source of the next bear market, we believe it will be somewhere else.

The potential for a recession increases when the benefits from recent tax cuts wear off in the second half of 2019. For now, we believe the odds of a material slowdown are still low. However, an exogenous event or policy error (such as a trade war) could change this outlook. While we have still maintained a slightly pro-cyclical tilt in the Fund, we will continue to take these factors into account as they relate to the fundamental prospects of the companies in which we invest, and make adjustments to the portfolio as our outlook changes.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice.

Mutual fund investing involves risk. Principal loss is possible. Midcap companies tend to have more limited liquidity and greater volatility than large-capitalization companies. Investments in American Depositary Receipts (“ADRs”) are subject to some extent to the risks associated with directly investing in securities of foreign issuers, including the risk of changes in currency exchange rates, expropriation or nationalization of assets, and the impact of political, diplomatic, or social events. Investments in real estate securities may involve greater risk and volatility including greater exposure to economic downturns and changes in real estate values, rents, property taxes, and tax and other laws. A real estate investment trust’s (REIT’s) share price may decline because of adverse developments affecting the real estate industry.

Please refer to the Schedule of Investments on page 12 of this report for holdings information. The management commentary above as well as Fund holdings and asset/sector allocations should not be considered a recommendation to buy or sell any security. In addition, please note that Fund holdings and asset/sector allocations are subject to change.

Earnings Growth is a measure of growth in a company’s net income over a specific period, often one year. It is not a prediction of the Fund’s future returns.

See Notes to Financial Statements.

10

| MIDCAP FUND INVESTMENT REVIEW(Unaudited) (Continued) |

| November 30, 2018 |

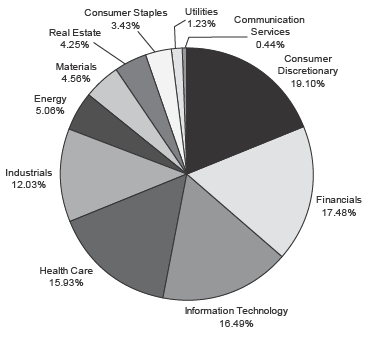

| Sector Weightings at 11/30/18 |

| % of Total Investments |

|

| Top 10 Equity Holdings at 11/30/18 |

| | % of Fund’s |

| Company | Industry | Net Assets |

| Hanger, Inc. | Health Care Providers & Services | 3.94% |

| Newell Brands, Inc. | Household Durables | 2.40% |

| Alliance Data Systems Corp. | IT Services | 2.17% |

| Exact Sciences Corp. | Biotechnology | 2.13% |

| CIT Group Inc. | Banks | 2.11% |

| Northern Trust Corp. | Capital Markets | 1.92% |

| Masco Corp. | Building Products | 1.83% |

| First Horizon National Corp. | Banks | 1.82% |

| Associated Banc-Corp | Banks | 1.77% |

| LKQ Corp. | Distributors | 1.77% |

As of November 30, 2018, 100.0%, of the Fund’s net assets were in equity and short-term investments.

See Notes to Financial Statements.

11

| MIDCAP FUND SCHEDULE OF INVESTMENTS |

| November 30, 2018 |

| | | | Shares | | Value |

| COMMON STOCKS - 100.0% | | | | $ | 45,008,308 |

| (COST $42,218,838) | | | | | |

| |

| Communication Services - 0.4% | | | | | 198,503 |

| Entertainment - 0.4% | | | | | |

| Take-Two Interactive Software, Inc. (a) | | 1,810 | | | 198,503 |

| |

| Consumer Discretionary - 19.1% | | | | | 8,598,912 |

| Automobiles - 1.1% | | | | | |

| Harley-Davidson, Inc. | | 11,875 | | | 502,194 |

| Distributors - 1.8% | | | | | |

| LKQ Corp. (a) | | 28,645 | | | 797,477 |

| Hotels, Restaurants & Leisure - 0.7% | | | | | |

| Extended Stay America, Inc. | | 17,800 | | | 323,960 |

| Household Durables - 5.7% | | | | | |

| D.R. Horton, Inc. | | 12,325 | | | 458,737 |

| Newell Brands, Inc. | | 46,231 | | | 1,081,805 |

| PulteGroup Inc. | | 20,075 | | | 532,389 |

| TopBuild Corp. (a) | | 9,640 | | | 491,158 |

| Leisure Products - 2.2% | | | | | |

| Brunswick Corp. | | 10,675 | | | 566,202 |

| Mattel, Inc. (a) | | 31,550 | | | 438,545 |

| Specialty Retail - 4.3% | | | | | |

| Bed Bath & Beyond Inc. | | 38,250 | | | 492,660 |

| Lumber Liquidators Holdings, Inc. (a) | | 47,475 | | | 599,609 |

| Party City Holdco Inc. (a) | | 43,000 | | | 513,850 |

| Urban Outfitters, Inc. (a) | | 8,375 | | | 319,004 |

| Textiles, Apparel & Luxury Goods - 3.3% | | | | | |

| Hanesbrands, Inc. | | 49,365 | | | 785,397 |

| Skechers U.S.A., Inc. Class A (a) | | 25,775 | | | 695,925 |

| |

| Consumer Staples - 3.4% | | | | | 1,546,070 |

| Beverages - 1.4% | | | | | |

| Molson Coors Brewing Co. Class B | | 9,575 | | | 629,748 |

| Food Products - 2.0% | | | | | |

| The Hain Celestial Group, Inc. (a) | | 14,075 | | | 291,352 |

| The J. M. Smucker Co. | | 5,980 | | | 624,970 |

| |

| Energy - 5.1% | | | | | 2,276,835 |

| Energy Equipment & Services - 1.4% | | | | | |

| Helmerich & Payne, Inc. | | 3,510 | | | 212,706 |

| TechnipFMC PLC | | 17,125 | | | 395,416 |

| Oil, Gas & Consumable Fuels - 3.7% | | | | | |

| Cameco Corp. | | 19,750 | | | 234,630 |

| Devon Energy Corp. | | 10,250 | | | 277,058 |

| Noble Energy, Inc. | | 26,675 | | | 633,265 |

| Pioneer Natural Resources Co. | | 1,475 | | | 217,931 |

| Southwestern Energy Co. (a) | | 63,450 | | | 305,829 |

See Notes to Financial Statements.

12

| MIDCAP FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | | | Shares | | Value |

| COMMON STOCKS(continued) | | | | | |

| |

| Financials - 17.5% | | | | $ | 7,862,370 |

| Banks - 9.1% | | | | | |

| Associated Banc-Corp | | 34,443 | | | 798,044 |

| CIT Group Inc. | | 20,480 | | | 950,886 |

| First Horizon National Corp. | | 49,645 | | | 818,646 |

| Regions Financial Corp. | | 16,035 | | | 263,776 |

| SunTrust Banks, Inc. | | 8,520 | | | 534,119 |

| Zions Bancorporation, N.A. | | 14,635 | | | 712,139 |

| Capital Markets - 4.0% | | | | | |

| Eaton Vance Corp. | | 12,470 | | | 507,903 |

| Northern Trust Corp. | | 8,730 | | | 866,278 |

| State Street Corp. | | 5,975 | | | 436,295 |

| Consumer Finance - 1.2% | | | | | |

| Discover Financial Services | | 7,404 | | | 527,905 |

| Insurance - 2.1% | | | | | |

| Fidelity National Financial, Inc. | | 17,525 | | | 588,840 |

| Unum Group | | 9,580 | | | 344,018 |

| Thrifts & Mortgage Finance - 1.1% | | | | | |

| Flagstar Bancorp, Inc. (a) | | 15,825 | | | 513,521 |

| |

| Health Care - 15.9% | | | | | 7,170,067 |

| Biotechnology - 3.2% | | | | | |

| Exact Sciences Corp. (a) | | 12,300 | | | 959,154 |

| MiMedx Group Inc. (a) | | 92,375 | | | 278,049 |

| Xencor, Inc. (a) | | 4,800 | | | 201,648 |

| Health Care Equipment & Supplies - 1.2% | | | | | |

| Hologic, Inc. (a) | | 12,425 | | | 551,794 |

| Health Care Providers & Services - 8.3% | | | | | |

| Acadia Healthcare Co., Inc. (a) | | 15,675 | | | 532,480 |

| Hanger, Inc. (a) | | 88,594 | | | 1,774,538 |

| Henry Schein, Inc. (a) | | 3,575 | | | 318,890 |

| McKesson Corp. | | 2,665 | | | 331,792 |

| Patterson Cos., Inc. | | 10,980 | | | 278,563 |

| Premier, Inc. Class A (a) | | 13,075 | | | 518,554 |

| Life Sciences Tools & Services - 1.5% | | | | | |

| Accelerate Diagnostics, Inc. (a) | | 44,500 | | | 657,265 |

| Pharmaceuticals - 1.7% | | | | | |

| Jazz Pharmaceuticals PLC (a) | | 5,075 | | | 767,340 |

| |

| Industrials - 12.0% | | | | | 5,415,932 |

| Building Products - 2.8% | | | | | |

| A.O. Smith Corp. | | 9,700 | | | 459,586 |

| Masco Corp. | | 25,950 | | | 822,356 |

| Commercial Services & Supplies - 0.5% | | | | | |

| Hudson Technologies, Inc. (a) | | 225,325 | | | 245,604 |

| Electrical Equipment - 1.2% | | | | | |

| Regal Beloit Corp. | | 7,030 | | | 549,605 |

See Notes to Financial Statements.

13

| MIDCAP FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | | Shares | | Value |

| COMMON STOCKS(continued) | | | | |

| |

| Industrials (continued) | | | | |

| Machinery - 5.9% | | | | |

| Ingersoll-Rand PLC | | 5,625 | | $582,300 |

| Kornit Digital Ltd. (a) | | 14,250 | | 328,035 |

| Mueller Water Products, Inc. Class A | | 30,525 | | 321,428 |

| REV Group, Inc. | | 40,050 | | 488,610 |

| SPX Corp. (a) | | 7,650 | | 226,287 |

| SPX Flow, Inc. (a) | | 18,515 | | 694,868 |

| Trading Companies & Distributors - 1.6% | | | | |

| HD Supply Holdings, Inc. (a) | | 17,475 | | 697,253 |

| |

| Information Technology - 16.6% | | | | 7,422,035 |

| Communications Equipment - 2.1% | | | | |

| Lumentum Holdings Inc. (a) | | 8,000 | | 355,760 |

| Viavi Solutions Inc. (a) | | 56,231 | | 570,182 |

| Electronic Equipment, Instruments & Components - 1.6% | | | | |

| II-VI Inc. (a) | | 15,400 | | 576,268 |

| Maxwell Technologies, Inc. (a) | | 49,997 | | 125,492 |

| IT Services - 3.6% | | | | |

| Alliance Data Systems Corp. | | 4,870 | | 975,753 |

| Black Knight, Inc. (a) | | 6,735 | | 305,365 |

| Fiserv, Inc. (a) | | 4,138 | | 327,440 |

| Semiconductors & Semiconductor Equipment - 6.3% | | | | |

| Cypress Semiconductor Corp. | | 34,500 | | 479,550 |

| Infineon Technologies A.G. ADR | | 29,225 | | 619,570 |

| Marvell Technology Group Ltd. | | 34,304 | | 552,637 |

| Maxim Integrated Products, Inc. | | 8,066 | | 451,051 |

| NXP Semiconductors N.V. | | 9,000 | | 750,330 |

| Technology Hardware, Storage & Peripherals - 3.0% | | | | |

| CPI Card Group Inc. (a) | | 150,397 | | 458,711 |

| Electronics for Imaging, Inc. (a) | | 23,050 | | 638,024 |

| Pure Storage, Inc. Class A (a) | | 12,475 | | 235,902 |

| |

| Materials - 4.6% | | | | 2,051,445 |

| Chemicals - 1.3% | | | | |

| Ecolab Inc. | | 2,105 | | 337,831 |

| Int’l. Flavors & Fragrances Inc. | | 1,535 | | 217,402 |

| Containers & Packaging - 1.6% | | | | |

| AptarGroup, Inc. | | 2,100 | | 218,505 |

| Crown Holdings, Inc. (a) | | 10,000 | | 512,800 |

| Metals & Mining - 1.7% | | | | |

| Freeport-McMoRan Inc. | | 54,670 | | 652,760 |

| Lundin Mining Corp. | | 25,900 | | 112,147 |

See Notes to Financial Statements.

14

| MIDCAP FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | | Shares | | Value |

| COMMON STOCKS(continued) | | | | |

| |

| Real Estate - 4.2% | | | | $1,913,724 |

| Equity Real Estate Investment - 3.2% | | | | |

| DiamondRock Hospitality Co. | | 42,600 | | 449,004 |

| Host Hotels & Resorts Inc. | | 23,335 | | 443,365 |

| Kimco Realty Corp. | | 34,550 | | 564,893 |

| Real Estate Management & Development - 1.0% | | | | |

| Realogy Holdings Corp. | | 23,700 | | 456,462 |

| |

| Utilities - 1.2% | | | | 552,415 |

| Electric Utilities - 0.5% | | | | |

| Xcel Energy, Inc. | | 4,350 | | 228,158 |

| Multi-Utilities - 0.7% | | | | |

| MDU Resources Group, Inc. | | 12,250 | | 324,257 |

| |

| SHORT-TERM INVESTMENTS - 0.0%^ | | | | 3,925 |

| (COST $3,925) | | | | |

| |

| Money Market Funds - 0.0%^ | | | | 3,925 |

| First American Gov’t. Obligations Fund Class X, 2.131% (b) | | 3,925 | | 3,925 |

| |

| TOTAL INVESTMENTS - 100.0% (COST $42,222,763) | | | | 45,012,233 |

| |

| NET OTHER ASSETS AND LIABILITIES - 0.0%^ | | | | 16,983 |

| |

| NET ASSETS - 100.0% | | | | $45,029,216 |

| (a) | Non-income producing security. |

| (b) | Represents the 7-day yield at November 30, 2018. |

| ^ | Rounds to 0.0%. |

| Abbreviations: |

| ADR | American Depositary Receipt |

| A.G. | Aktiengesellschaft is the German term for a public limited liability corporation. |

| N.V. | Naamloze Vennootschap is the Dutch term for a public limited liability corporation. |

| PLC | Public Limited Company |

The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of MSCI Inc. (“MSCI”) and Standard & Poor’s Financial Services LLC (“S&P”) and is licensed for use by Thompson Investment Management, Inc. Neither MSCI, S&P, nor any other party involved in making or compiling the GICS or any GICS classifications makes any warranties with respect thereto or the results to be obtained by the use thereof, and no such party shall have any liability whatsoever with respect thereto.

See Notes to Financial Statements.

15

| BOND FUND INVESTMENT REVIEW(Unaudited) |

| November 30, 2018 |

Portfolio Managers

James T. Evans, CFA

Jason L. Stephens, CFA

Performance

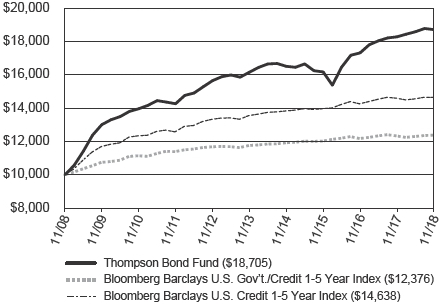

The Bond Fund produced a total return of 2.37% for the fiscal year ended November 30, 2018, as compared to its benchmark, the Bloomberg Barclays U.S. Government/Credit 1-5 Year Index, which returned 0.36%, and as compared to the Bloomberg Barclays U.S. Credit 1-5 Year Index, which returned 0.31%.

| Comparison of Change in Value of a Hypothetical $10,000 Investment |

|

| Average Annual Total Returns |

| Through 11/30/18 |

| | 1 Year | | 3 Year | | 5 Year | | 10 Year |

| Thompson Bond Fund | | | 2.37% | | | | 4.98% | | | | 2.98% | | | | 6.46% | |

| Bloomberg Barclays U.S. Gov’t./Credit 1-5 Year Index | | | 0.36% | | | | 0.98% | | | | 1.03% | | | | 2.16% | |

| Bloomberg Barclays U.S. Credit 1-5 Year Index | | | 0.31% | | | | 1.58% | | | | 1.55% | | | | 3.88% | |

| Gross Expense Ratio as of 03/31/18 was 0.71%. | 30-Day SEC Yield as of 11/30/18 was 3.72%. |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 1-800-999-0887 or visiting www.thompsonim.com.

Results include the reinvestment of all dividends and capital gains distributions. Investment performance reflects all fee waivers that may have been in effect. In the absence of such waivers, total return would have been reduced. The performance information reflected in the graph and the table above does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares, nor does it imply future performance. The Bloomberg Barclays U.S. Government/Credit 1-5 Year Index is a market-value-weighted index of all investment-grade bonds with maturities of more than one year and less than 5 years. The Bloomberg Barclays U.S. Credit 1-5 Year Index is a market-value-weighted index which includes virtually every major investment-grade rated corporate bond with 1-5 years remaining until maturity that serves as a supplementary benchmark. You cannot directly invest in an index.

Bloomberg®is a trademark and service mark of Bloomberg Finance L.P. Barclays®is a trademark and service mark of Barclays Bank PLC.

See Notes to Financial Statements.

16

| BOND FUND INVESTMENT REVIEW(Unaudited) (Continued) |

| November 30, 2018 |

Management Commentary

The fiscal year was a difficult one for many fixed income strategies. Five year or less Treasury yields rose between 67 and 118 basis points depending on the maturity, depressing overall returns as prices fell to compensate. Corporate bonds weren’t much better, as spreads widened by 42 basis points on 10-year BBB-rated securities during the period, countering much of the extra income that an investor would normally expect to receive by holding the riskier asset class. As a result, the Fund’s primary and supplementary benchmarks were only able to eke out small gains for the year after spending most of the fiscal year before early August in negative territory. So while the Fund’s 2.37% return for the fiscal year may not be the largest annual return generated for shareholders over the past decade, it’s one that we are particularly proud of given the circumstances.

During the fiscal year, the Fund’s corporate bond overweight coupled with an allocation to asset-backed and commercial mortgage bonds gave the Fund extra income relative to its benchmarks. While these positions were an important component of the Fund’s outperformance, merely concluding that the corporate position was the dominant factor behind the Fund’s performance does not tell the full story. After all, absent extraordinary issue selection, a corporate overweight coupled with a duration of 2-3 years would likely have generated performance somewhat similar to the 0.31% return of the Bloomberg Barclays U.S. Credit 1-5 Year Index.

The key in our opinion to the Fund’s relative success during the period was instead a combination of the shape of the yield curve coupled with a low Fund duration. Because the yield curve for non-government bonds was relatively flat, we were able to buy bonds in the 1-2 year maturity timeframe and earn income that was only modestly below yields available on longer-maturity bonds. At the same time, the short duration helped to reduce both interest-rate and spread-widening risk that hurt many of our peers and the benchmarks. This is because the change in price of a corporate bond from wider spreads is roughly equal to the combination of the change in the spread times the duration of said bond. By keeping the duration small, we were able to reduce the overall impact of a given change in spreads.

Looking forward, we like how the Fund is positioned. The SEC yield of the Fund as of the end of the fiscal year was 3.72%, suggesting that the Fund’s holdings are likely to provide a competitive return for shareholders going forward. We continue to find bargains in the 1-2 year space and see little reason at this time to purchase longer maturities except for the occasional exceptional bond. At some point it very likely will make sense to extend, once the yield curve is steeper than today, either due to long-term rates having risen or because the Federal Reserve has begun a rate-cutting cycle to fight a recession. If we were to extend we would probably concurrently increase the Fund’s allocation to government securities in an effort to reduce the portfolio’s credit risk. However, neither scenario appears imminent to us. Thus, as we look ahead to the next fiscal year we will likely continue with the strategy that served us so well over the past year.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice.

Mutual fund investing involves risk. Principal loss is possible. Investments in debt securities typically decrease in value when interest rates rise. The risk is usually greater for longer-term debt securities. Investments in bonds of foreign issuers involve greater volatility, political and economic risks, and differences in accounting methods. Investment by the Fund in lower-rated and non-rated securities presents a greater risk of loss to principal and interest than higher-rated securities.

Please refer to the Schedule of Investments on page 19 of this report for holdings information. The management commentary above as well as Fund holdings should not be considered a recommendation to buy or sell any security. In addition, please note that Fund holdings are subject to change.

The federal government guarantees interest payments from government securities while dividend payments carry no such guarantee. Government securities, if held to maturity, guarantee the timely payment of principal and interest.

Basis Points is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. The basis point is commonly used for calculating changes in interest rates, equity indexes and the yield of a fixed-income security.

Duration is a commonly used measure of the potential volatility of the price of a debt security, or the aggregate market value of a portfolio of debt securities, prior to maturity. Securities with a longer duration generally have more volatile prices than securities of comparable quality with a shorter duration.

SEC Yield is a standardized yield computed by dividing the net investment income per share earned during the 30-day period prior to quarter-end and was created to allow for fairer comparisons among bond funds.

Spread is the percentage point difference between yields of various classes of bonds compared to treasury bonds.

Yield is the income earned from a bond, which takes into account the sum of the interest payment, the redemption value at the bond’s maturity, and the initial purchase price of the bond.

Yield Curve is a line that plots the interest rates, at a set point in time, of bonds having equal credit quality but differing maturity dates.

Credit Ratings are provided by Standard & Poor’s, who assign a rating based on their analysis of the issuer’s creditworthiness. The highest rating given is AAA and the lowest is C.

See Notes to Financial Statements.

17

| BOND FUND INVESTMENT REVIEW(Unaudited) (Continued) |

| November 30, 2018 |

The purpose of Moody’s ratings is to provide investors with a simple system of gradation by which relative creditworthiness of securities may be noted. Gradations of creditworthiness are indicated by rating symbols, with each symbol representing a group in which the credit characteristics are broadly the same. The highest rating assigned by Moody’s is AAA and the lowest is C.

Although the makeup of the Bond Fund’s portfolio is constantly changing, as of November 30, 2018, 74.60% of the Fund’s portfolio was invested in corporate bonds. Due to prevailing market conditions, the composition of the Fund’s portfolio as of that date was consistent with the composition of the Fund’s portfolio over the past 5 years. In addition, as of that date 64.91% of the Fund’s portfolio was invested in securities rated BBB by Standard & Poor’s, while an additional 4.09% of the Fund’s portfolio was rated below investment-grade and 16.67% of the Fund’s portfolio was not rated by Standard & Poor’s. For portfolio information current as of the most recent quarter-end, please call 1-800-999-0887 or visit our website at www.thompsonim.com. Compared to a portfolio that is more evenly allocated between government and corporate bonds, a portfolio that is heavily allocated to corporate bonds may provide higher returns but is also subject to greater levels of credit and liquidity risk and to greater price fluctuations. A portfolio that is significantly allocated to bonds having lower and below-investment-grade ratings may also be subject to greater levels of credit and liquidity risk and experience greater price fluctuations than a portfolio comprised of higher-rated investment-grade bonds.

| Asset Allocation at 11/30/18 |

| (Includes cash equivalents) |

| % of Total Investments |

| Corporate Bonds | 74.60% |

| Asset-Backed Securities | 11.00% |

| U.S. Government & Agency Securities | 5.25% |

| Commercial Mortgage-Backed Securities | 3.55% |

| Taxable Municipal Bonds | 3.09% |

| Sovereign Bonds | 1.52% |

| Commercial Paper | 0.68% |

| Tax-Exempt Municipal Bonds | 0.17% |

| U.S. Government Agency Mortgage-Backed Securities | 0.07% |

| Residential Mortgage-Backed Securities | 0.07% |

| 100.00% |

| |

| Quality Composition at 11/30/18^ |

| (Includes cash equivalents) |

| % of Total Investments |

| U.S. Government & Agency Issues | 5.32% |

| AAA | 0.47% |

| AA | 1.65% |

| A | 12.30% |

| BBB | 73.46% |

| BB and Below | 6.47% |

| Not Rated | 0.33% |

| 100.00% |

| ^ | The Bond Fund’s quality composition is calculated using ratings from Standard & Poor’s. If Standard & Poor’s does not rate a holding then Moody’s is used. If Standard & Poor’s and Moody’s do not rate a holding then Fitch is used. For certain securities that are not rated by any of these three agencies, credit ratings from other Nationally Recognized Statistical Credit Rating Organizations (NRSRO) agencies may be used. Not rated category includes holdings that are not rated by any NRSRO. All ratings are as of 11/30/18. |

| Top 10 Bond Holdings by Issuer at 11/30/18 |

| % of Fund’s Net Assets |

| XL Group PLC | 2.20% |

| MBIA Inc. | 1.98% |

| Barclays PLC | 1.93% |

| County of Racine WI Anticipation Notes | 1.71% |

| Fannie Mae | 1.70% |

| Ford Motor Credit Co. LLC | 1.67% |

| General Electric Co. | 1.41% |

| Becton Dickinson and Co. | 1.30% |

| First Tennessee Bank N.A. | 1.23% |

| Federal Home Loan Banks | 1.21% |

See Notes to Financial Statements.

18

| BOND FUND SCHEDULE OF INVESTMENTS |

| November 30, 2018 |

| | | Rate (%) | | Maturity Date | | Principal Amount | | | Value |

| BONDS - 97.6% | | | | | | | | $ | 3,569,807,362 |

| | (COST $3,629,856,593) | | | | | | | | | |

| |

| Asset-Backed Securities - 10.9% | | | | | | | | | 398,358,070 |

| Air Canada, Series 2013-1B (h) | | 5.375 | | 11/15/22 | | 7,795,721 | | | 7,941,890 |

| Air Canada, Series 2015-1B (h) | | 3.875 | | 09/15/24 | | 1,944,723 | | | 1,898,574 |

| Air Canada, Series 2015-2B (h) | | 5.000 | | 06/15/25 | | 4,668,520 | | | 4,715,206 |

| Airspeed Ltd., Series 2007-1A G1 (1 month LIBOR + 0.270%, | | | | | | | | | |

| floor 0.000%) (c)(h) | | 2.577 | | 06/15/32 | | 2,528,344 | | | 2,428,910 |

| America West Airlines, Series 1999-1 | | 7.930 | | 07/02/20 | | 1,632,290 | | | 1,638,983 |

| America West Airlines, Series 2000-1 | | 8.057 | | 01/02/22 | | 18,936 | | | 19,958 |

| America West Airlines, Series 2001-1 | | 7.100 | | 10/02/22 | | 3,296,396 | | | 3,436,492 |

| American Airlines, Series 2013-2 A | | 4.950 | | 07/15/24 | | 431,826 | | | 440,985 |

| American Airlines, Series 2015-1 B | | 3.700 | | 11/01/24 | | 2,733,715 | | | 2,655,257 |

| American Airlines, Series 2015-2 B | | 4.400 | | 03/22/25 | | 5,123,666 | | | 5,065,256 |

| Applebee’s Funding LLC / IHOP Funding LLC, Series 2014-1 A2 (h) | | 4.277 | | 09/05/44 | | 39,658,410 | | | 39,196,405 |

| British Airways PLC, Series 2013-1 B (h) | | 5.625 | | 12/20/21 | | 14,721,505 | | | 14,958,521 |

| British Airways PLC, Series 2013-1 B (h) | | 5.625 | | 12/20/21 | | 30,663 | | | 31,156 |

| Business Jet Securities, LLC, Series 2018-1 A (h) | | 4.335 | | 02/15/33 | | 7,251,485 | | | 7,240,540 |

| Business Jet Securities, LLC, Series 2018-1 B (h) | | 6.048 | | 02/15/33 | | 1,044,138 | | | 1,068,583 |

| Cajun Global LLC, Series 2017-1A A2 (h) | | 6.500 | | 08/20/47 | | 9,550,000 | | | 9,726,484 |

| CAL Funding II Ltd., Series 2012-1A A (h) | | 3.470 | | 10/25/27 | | 1,094,708 | | | 1,081,779 |

| CAL Funding II Ltd., Series 2013-1A A (h) | | 3.350 | | 03/27/28 | | 2,812,333 | | | 2,779,520 |

| Castle Aircraft Securitization Trust, Series 2015-1A A (h) | | 4.703 | | 12/15/40 | | 775,845 | | | 779,678 |

| Continental Airlines, Series 1999-2 A-1 | | 7.256 | | 09/15/21 | | 12,059 | | | 12,293 |

| Continental Airlines, Series 1999-2 C | | 6.236 | | 09/15/21 | | 391,930 | | | 397,809 |

| Continental Airlines, Series 2010-1 B | | 6.000 | | 07/12/20 | | 1,368,485 | | | 1,372,317 |

| Continental Airlines, Series 2012-1 B | | 6.250 | | 10/11/21 | | 4,498,622 | | | 4,597,592 |

| Continental Airlines, Series 2012-2 B | | 5.500 | | 04/29/22 | | 7,343,535 | | | 7,490,406 |

| Cronos Containers Program I Ltd., Series 2013-1A A (h) | | 3.080 | | 04/18/28 | | 5,341,958 | | | 5,256,519 |

| Cronos Containers Program I Ltd., Series 2014-1A A (h) | | 3.040 | | 08/18/29 | | 1,046,729 | | | 1,027,938 |

| Delta Air Lines, Series 2007-1 B | | 8.021 | | 02/10/24 | | 1,648,290 | | | 1,804,927 |

| Delta Air Lines, Series 2012-1B (h) | | 6.875 | | 11/07/20 | | 456,139 | | | 462,525 |

| Doric Nimrod Air Alpha, Series 2013-1 B (h) | | 6.125 | | 11/30/21 | | 9,304,892 | | | 9,444,465 |

| Doric Nimrod Air Alpha, Series 2013-1 B (h) | | 6.125 | | 11/30/21 | | 1,516,165 | | | 1,538,907 |

| Doric Nimrod Air Finance Alpha Ltd., Series 2012-1 B (h) | | 6.500 | | 05/30/21 | | 2,338,501 | | | 2,352,422 |

| ECAF I Ltd., Series 2015-1A A2 (h) | | 4.947 | | 06/15/40 | | 3,864,053 | | | 3,941,379 |

| ECAF I Ltd., Series 2015-1A B1 (h) | | 5.802 | | 06/15/40 | | 19,081,000 | | | 19,021,274 |

| Element Rail Leasing LLC, Series 2014-1A B1 (h) | | 4.406 | | 04/19/44 | | 10,158,750 | | | 10,123,544 |

| Element Rail Leasing LLC, Series 2015-1A B1 (h) | | 4.175 | | 02/19/45 | | 16,917,000 | | | 16,341,282 |

| EngenCap ABS Trust, Series 2016-1 A (h) | | 3.670 | | 12/21/26 | | 23,281,248 | | | 22,466,404 |

| FPL Energy Caithness Funding Corp. (h) | | 7.645 | | 12/31/18 | | 964,237 | | | 966,647 |

| FRS LLC, Series 2013-1A B (h) | | 3.960 | | 04/15/43 | | 1,594,874 | | | 1,588,580 |

| Global Container Assets Ltd., Series 2015-1A A1 (h) | | 2.100 | | 02/05/30 | | 589,048 | | | 587,859 |

| Global SC Finance II SRL (SEACO), Series 2013-1A A (h) | | 2.980 | | 04/17/28 | | 7,950,000 | | | 7,780,617 |

| Global SC Finance II SRL (SEACO), Series 2014-1A A1 (h) | | 3.190 | | 07/17/29 | | 4,624,000 | | | 4,522,566 |

| Harley Marine Financing LLC, Series 2018-1A A2 (h) | | 5.682 | | 05/15/43 | | 14,775,000 | | | 13,736,318 |

| HP Communities LLC (h) | | 5.320 | | 03/15/23 | | 271,471 | | | 277,309 |

| Icon Brand Holdings LLC, Series 2012-1A A (h) | | 4.229 | | 01/25/43 | | 8,229,185 | | | 7,419,891 |

| Latam Airlines Group, Series 2015-1 B | | 4.500 | | 08/15/25 | | 4,285,412 | | | 4,107,568 |

| Merlin Aviation Holdings D.A.C., Series 2016-1 A (h) | | 4.500 | | 12/15/32 | | 12,146,813 | | | 12,246,652 |

See Notes to Financial Statements.

19

| BOND FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | | Rate (%) | | Maturity Date | | Principal Amount | | Value |

| BONDS(continued) | | | | | | | | |

| |

| Asset-Backed Securities (continued) | | | | | | | | |

| | Merlin Aviation Holdings D.A.C., Series 2016-1 B (h) | | 6.500 | | 12/15/32 | | 1,333,735 | | $1,346,679 |

| METAL LLC, Series 2017-1 A (h) | | 4.581 | | 10/15/42 | | 13,541,324 | | 13,468,603 |

| METAL LLC, Series 2017-1 B (h) | | 6.500 | | 10/15/42 | | 20,763,364 | | 21,085,661 |

| Northwest Airlines, Series 1999-2 A | | 7.575 | | 09/01/20 | | 102,082 | | 103,103 |

| Northwest Airlines, Series 2000-1 G (d) | | 7.150 | | 04/01/21 | | 6,721 | | 6,709 |

| Northwest Airlines, Series 2002-1 G-2 | | 6.264 | | 05/20/23 | | 1,051,671 | | 1,069,654 |

| Prudential Securities Structured Assets, Inc., Series 1998-1 A | | | | | | | | |

| (1 month LIBOR + 0.420%, floor 0.000%) (c)(h) | | 2.727 | | 03/02/25 | | 10,548,703 | | 9,849,851 |

| SBA Tower Trust, Series 2014-1A C (h) | | 2.898 | | 10/15/44 | | 1,301,000 | | 1,295,842 |

| Spirit Master Funding, LLC, Series 2014-2A A (h) | | 5.760 | | 03/20/41 | | 16,716,601 | | 17,148,576 |

| Spirit Master Funding, LLC, Series 2014-4A A1 (h) | | 3.501 | | 01/20/45 | | 4,853,256 | | 4,821,567 |

| Spirit Master Funding, LLC, Series 2017-1A B (h) | | 5.490 | | 12/20/47 | | 5,000,000 | | 5,033,944 |

| TAL Advantage V LLC, Series 2014-1A B (h) | | 4.100 | | 02/22/39 | | 2,939,998 | | 2,898,214 |

| TAL Advantage V LLC, Series 2014-2A A2 (h) | | 3.330 | | 05/20/39 | | 2,245,833 | | 2,226,628 |

| Textainer Marine Containers V Ltd., Series 2017-1A B (h) | | 4.850 | | 05/20/42 | | 1,629,784 | | 1,613,595 |

| TGIF Funding LLC, Series 2017-1A A2 (h) | | 6.202 | | 04/30/47 | | 29,100,000 | | 29,048,493 |

| United Air Lines, Series 2013-1 B | | 5.375 | | 02/15/23 | | 1,582,681 | | 1,609,794 |

| US Airways, Series 1999-1 A | | 8.360 | | 07/20/20 | | 3,551 | | 3,587 |

| US Airways, Series 2001-1 G | | 7.076 | | 09/20/22 | | 360,531 | | 377,404 |

| US Airways, Series 2012-1 B | | 8.000 | | 04/01/21 | | 16,677,556 | | 17,206,735 |

| US Airways, Series 2013-1B | | 5.375 | | 05/15/23 | | 76,850 | | 78,751 |

| Virgin Australia Trust, Series 2013-1 A (h) | | 5.000 | | 04/23/25 | | 73,348 | | 74,493 |

| |

| Commercial Mortgage-Backed Securities - 3.4% | | | | | | | | 128,383,280 |

| CG-CCRE Commercial Mortgage Trust, Series 2014-FL1 D | | | | | | | | |

| (1 month LIBOR + 2.750%, floor 2.750%) (c)(h) | | 5.057 | | 06/15/31 | | 12,000,000 | | 11,970,865 |

| COMM Mortgage Trust, Series 2012-CR1 D (c)(h) | | 5.321 | | 05/15/45 | | 4,774,000 | | 4,752,311 |

| COMM Mortgage Trust, Series 2012-CR3 E (c)(h) | | 4.753 | | 10/15/45 | | 5,000,000 | | 4,477,291 |

| COMM Mortgage Trust, Series 2013-CR9 D (c)(h) | | 4.257 | | 07/10/45 | | 4,898,000 | | 4,141,335 |

| COMM Mortgage Trust, Series 2014-CC17 D (c)(h) | | 4.801 | | 05/10/47 | | 5,210,000 | | 4,901,947 |

| GS Mortgage Securities Trust, Series 2010-C1 E (h) | | 4.000 | | 08/10/43 | | 17,741,000 | | 16,872,417 |

| J.P. Morgan Chase Commercial Mortgage Securities Trust, | | | | | | | | |

| Series 2014-C20 D (c)(h) | | 4.571 | | 07/15/47 | | 5,000,000 | | 4,408,782 |

| J.P. Morgan Chase Commercial Mortgage Securities Trust, | | | | | | | | |

| Series 2014-C22 D (c)(h) | | 4.558 | | 09/15/47 | | 4,966,000 | | 4,191,696 |

| Morgan Stanley Bank of America Merrill Lynch Trust, | | | | | | | | |

| Series 2014-C18 D (h) | | 3.389 | | 10/15/47 | | 5,000,000 | | 4,047,264 |

| Morgan Stanley Bank of America Merrill Lynch Trust, | | | | | | | | |

| Series 2015-C22 D (c)(h) | | 4.237 | | 04/15/48 | | 5,000,000 | | 4,333,549 |

| Morgan Stanley Capital I Trust, Series 2011-C2 D (c)(h) | | 5.485 | | 06/15/44 | | 1,000,000 | | 990,796 |

| OBP Depositor LLC Trust, Series 2010-OBP A (h) | | 4.646 | | 07/15/45 | | 8,939,000 | | 9,064,324 |

| Palisades Center Trust, Series 2016-PLSD B (h) | | 3.357 | | 04/13/33 | | 4,500,000 | | 4,426,794 |

| TRU Trust, Series 2016-1 A (1 month LIBOR + 2.250%, | | | | | | | | |

| floor 1.750%) (c)(h) | | 4.557 | | 11/15/30 | | 5,631,561 | | 5,632,065 |

| TRU Trust, Series 2016-1 B (1 month LIBOR + 3.150%, | | | | | | | | |

| floor 2.750%) (c)(h) | | 5.457 | | 11/15/30 | | 14,600,000 | | 14,618,507 |

| TRU Trust, Series 2016-1 C (1 month LIBOR + 4.000%, | | | | | | | | |

| floor 4.000%) (c)(h) | | 6.307 | | 11/15/30 | | 14,575,000 | | 14,353,313 |

See Notes to Financial Statements.

20

| BOND FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | | Rate (%) | | Maturity Date | | Principal Amount | | Value |

| BONDS(continued) | | | | | | | | |

| |

| Commercial Mortgage-Backed Securities (continued) | | | | | | | | |

| UBS-Barclays Commercial Mortgage Trust, Series 2012-C4 D (c)(h) | | 4.481 | | 12/10/45 | | 5,000,000 | | $4,621,427 |

| Wells Fargo Commercial Mortgage Trust, Series 2014-LC16 D (h) | | 3.938 | | 08/15/50 | | 7,072,000 | | 5,789,143 |

| WFRBS Commercial Mortgage Trust, Series 2011-C4 E (c)(h) | | 5.231 | | 06/15/44 | | 5,000,000 | | 4,789,454 |

| |

| Corporate Bonds - 73.9% | | | | | | | | 2,700,701,782 |

| | Actavis Funding SCS | | 2.450 | | 06/15/19 | | 6,259,000 | | 6,240,226 |

| Acuity Brands Lighting, Inc. | | 6.000 | | 12/15/19 | | 310,000 | | 317,784 |

| AerCap Ireland Capital Ltd. / AerCap Global Aviation Trust | | 3.750 | | 05/15/19 | | 500,000 | | 500,373 |

| AerCap Ireland Capital Ltd. / AerCap Global Aviation Trust | | 4.625 | | 10/30/20 | | 580,000 | | 583,271 |

| AerCap Ireland Capital Ltd. / AerCap Global Aviation Trust | | 4.500 | | 05/15/21 | | 10,401,000 | | 10,457,694 |

| Aircastle Ltd. | | 6.250 | | 12/01/19 | | 16,744,000 | | 17,117,758 |

| Aircastle Ltd. | | 7.625 | | 04/15/20 | | 2,000,000 | | 2,093,603 |

| Aircastle Ltd. | | 5.125 | | 03/15/21 | | 9,562,000 | | 9,732,506 |

| Aircastle Ltd. | | 5.500 | | 02/15/22 | | 8,263,000 | | 8,475,349 |

| American Tower Corp. | | 3.400 | | 02/15/19 | | 2,375,000 | | 2,375,551 |

| Ameriprise Financial, Inc. | | 7.300 | | 06/28/19 | | 4,640,000 | | 4,745,782 |

| Amphenol Corp. | | 2.550 | | 01/30/19 | | 1,749,000 | | 1,747,159 |

| AmTrust Financial Services, Inc. | | 6.125 | | 08/15/23 | | 23,096,000 | | 21,789,923 |

| Anadarko Petroleum Corp. | | 8.700 | | 03/15/19 | | 2,874,000 | | 2,918,721 |

| Anadarko Petroleum Corp. | | 6.950 | | 06/15/19 | | 6,830,000 | | 6,940,045 |

| Andeavor Logistics LP / Tesoro Logistics Finance Corp. | | 6.250 | | 10/15/22 | | 36,112,000 | | 37,014,800 |

| Anheuser-Busch InBev Worldwide Inc. | | 6.875 | | 11/15/19 | | 990,000 | | 1,021,562 |

| Arbor Realty Trust, Inc. | | 5.625 | | 05/01/23 | | 12,500,000 | | 12,658,210 |

| ARC Properties Operating Partnership, L.P. | | 3.000 | | 02/06/19 | | 3,475,000 | | 3,473,251 |

| ArcelorMittal | | 5.125 | | 06/01/20 | | 2,805,000 | | 2,847,356 |

| Arconic Inc. | | 6.150 | | 08/15/20 | | 22,236,000 | | 22,901,523 |

| Arconic Inc. | | 5.400 | | 04/15/21 | | 7,102,000 | | 7,201,428 |

| Arrow Electronics, Inc. | | 6.000 | | 04/01/20 | | 3,600,000 | | 3,697,425 |

| Associated Banc-Corp | | 2.750 | | 11/15/19 | | 23,397,000 | | 23,266,802 |

| Assured Guaranty US Holdings Inc. (3 month LIBOR + 2.380%) (c) | | 4.714 | | 12/15/66 | | 24,129,000 | | 22,681,260 |

| AT&T Inc. | | 5.800 | | 02/15/19 | | 7,950,000 | | 7,995,077 |

| Australia & New Zealand Banking Group Ltd. | | 2.250 | | 06/13/19 | | 3,000,000 | | 2,986,621 |

| AutoNation, Inc. | | 5.500 | | 02/01/20 | | 16,099,000 | | 16,416,123 |

| Avery Dennison Corp. | | 5.375 | | 04/15/20 | | 1,401,000 | | 1,427,563 |

| Avon Products, Inc. (e) | | 6.600 | | 03/15/20 | | 500,000 | | 503,750 |

| AXIS Specialty Finance PLC | | 2.650 | | 04/01/19 | | 5,797,000 | | 5,783,082 |

| Bank of America Corp. | | 5.490 | | 03/15/19 | | 344,000 | | 346,202 |

| Bank of America Corp. (5.125% to 06/17/19, | | | | | | | | |

| then 3 month LIBOR + 3.387%) (c)(g) | | 5.125 | | 06/17/19 | | 6,753,000 | | 6,719,910 |

| Bank of America Corp. | | 6.750 | | 08/15/19 | | 150,000 | | 153,371 |

| Bank of America Corp. (5.200% to 06/01/23, | | | | | | | | |

| then 3 month LIBOR + 3.135%) (c)(g) | | 5.200 | | 06/01/23 | | 2,500,000 | | 2,435,000 |

| Bank of America Corp. (4.0 times (USISDA10 - USISDA02 - 0.250%), | | | | | | | | |

| floor 0.000%, cap 10.000%) (c) | | 0.000 | | 11/19/30 | | 671,000 | | 402,600 |

| Bank of the Ozarks, Inc. (5.500% to 07/01/21, | | | | | | | | |

| then 3 month LIBOR + 4.425%) (c) | | 5.500 | | 07/01/26 | | 19,475,000 | | 19,868,356 |

| Barclays Bank PLC (d) | | 2.250 | | 09/13/19 | | 15,000,000 | | 14,849,992 |

| Barclays Bank PLC (CPI YOY + 1.000%, floor 0.000%) (c) | | 3.699 | | 03/16/23 | | 4,435,000 | | 4,306,385 |

See Notes to Financial Statements.

21

| BOND FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | | Rate (%) | | Maturity Date | | Principal Amount | | Value |

| BONDS(continued) | | | | | | | | |

| |

| Corporate Bonds (continued) | | | | | | | | |

| | Barclays Bank PLC (3 month LIBOR + 0.650%, | | | | | | | | |

| floor 1.650%, cap 6.000%) (c) | | 3.232 | | 02/05/25 | | 15,000,000 | | $14,390,074 |

| Barclays Bank PLC (5.0 times (USISDA30 - USISDA05), | | | | | | | | |

| floor 0.000%, cap 10.000%) (c) | | 0.735 | | 04/30/29 | | 2,425,000 | | 1,857,550 |

| Barclays Bank PLC (8.0 times (USISDA30 - USISDA05 - 0.250%), | | | | | | | | |

| floor 0.000%, cap 8.000%) (c) | | 0.000 | | 08/28/29 | | 2,721,000 | | 1,901,968 |

| Barclays PLC | | 2.750 | | 11/08/19 | | 33,492,000 | | 33,149,645 |

| Barrick (PD) Australia Finance Pty. Ltd. | | 4.950 | | 01/15/20 | | 420,000 | | 426,660 |

| BCB Bancorp, Inc. (5.625% to 08/01/23, | | | | | | | | |

| then 3 month LIBOR + 2.720%) (c)(h) | | 5.625 | | 08/01/28 | | 8,000,000 | | 7,969,509 |

| Becton Dickinson and Co. | | 2.133 | | 06/06/19 | | 5,416,000 | | 5,384,629 |

| Becton Dickinson and Co. | | 2.675 | | 12/15/19 | | 16,919,000 | | 16,777,190 |

| Becton Dickinson and Co. (3 month LIBOR + 1.030%) (c) | | 3.353 | | 06/06/22 | | 25,355,000 | | 25,296,230 |

| Bemis Co., Inc. | | 6.800 | | 08/01/19 | | 1,186,000 | | 1,212,422 |

| BGC Partners Inc. (h) | | 5.375 | | 12/09/19 | | 1,500,000 | | 1,531,355 |

| BGC Partners Inc. | | 5.375 | | 12/09/19 | | 17,716,000 | | 18,086,318 |

| BHP Billiton Finance USA Ltd. (6.250% to 10/19/20, then USSW5 | | | | | | | | |

| +4.971% to 10/19/25, +5.221% to 10/19/40, then +5.971%) (c)(h) | | 6.250 | | 10/19/75 | | 7,951,000 | | 8,176,013 |

| BMW US Capital, LLC (h) | | 1.850 | | 09/15/21 | | 10,000,000 | | 9,506,406 |

| Boardwalk Pipelines, LP | | 5.750 | | 09/15/19 | | 2,945,000 | | 2,998,379 |

| BorgWarner, Inc. | | 8.000 | | 10/01/19 | | 3,907,000 | | 4,060,707 |

| Brambles USA, Inc. (h) | | 5.350 | | 04/01/20 | | 1,750,000 | | 1,787,232 |

| Braskem Finance Ltd. (h) | | 5.750 | | 04/15/21 | | 10,000,000 | | 10,260,500 |

| Braskem Finance Ltd. (h) | | 5.750 | | 04/15/21 | | 21,788,000 | | 22,355,577 |

| British Sky Broadcasting Group plc (h) | | 2.625 | | 09/16/19 | | 500,000 | | 496,685 |

| Brunswick Corp. (h) | | 4.625 | | 05/15/21 | | 10,828,000 | | 10,834,214 |

| Buckeye Partners, L.P. | | 5.500 | | 08/15/19 | | 5,965,000 | | 6,031,168 |

| Buckeye Partners, L.P. | | 4.875 | | 02/01/21 | | 822,000 | | 833,263 |

| CA, Inc. | | 5.375 | | 12/01/19 | | 8,606,000 | | 8,735,274 |

| Cabot Corp. | | 7.420 | | 12/11/18 | | 1,000,000 | | 1,000,667 |

| Cadence BanCorp (h) | | 4.875 | | 06/28/19 | | 3,500,000 | | 3,500,616 |

| Campbell Soup Co. | | 4.500 | | 02/15/19 | | 14,325,000 | | 14,356,229 |

| Campbell Soup Co. | | 8.875 | | 05/01/21 | | 3,750,000 | | 4,130,207 |

| Canadian Oil Sands Ltd. (h) | | 7.750 | | 05/15/19 | | 990,000 | | 1,006,555 |

| Capital Funding Bancorp, Inc. (h) | | 6.000 | | 12/01/23 | | 20,000,000 | | 20,123,512 |

| Capital One Bank USA N.A. | | 2.250 | | 02/13/19 | | 1,250,000 | | 1,247,736 |

| Capital One Bank USA N.A. | | 8.800 | | 07/15/19 | | 8,907,000 | | 9,192,636 |

| Capital One N.A. | | 2.400 | | 09/05/19 | | 2,217,000 | | 2,202,475 |

| Capital One N.A. | | 1.850 | | 09/13/19 | | 19,682,000 | | 19,463,151 |

| Carpenter Technology Corp. | | 5.200 | | 07/15/21 | | 3,500,000 | | 3,560,955 |

| CBL & Associates LP | | 5.250 | | 12/01/23 | | 7,075,000 | | 5,872,250 |

| CBL & Associates LP | | 4.600 | | 10/15/24 | | 5,889,000 | | 4,711,200 |

| Citigroup, Inc. | | 2.450 | | 01/10/20 | | 1,000,000 | | 989,386 |

| Citigroup, Inc. (4.0 times (USISDA10 - USISDA02 - 0.250%), | | | | | | | | |

| floor 0.000%, cap 10.000%) (c) | | 0.000 | | 11/19/30 | | 727,000 | | 462,954 |

| Citigroup, Inc. (5.0 times (USISDA30 - USISDA05), | | | | | | | | |

| floor 0.000%, cap 10.000%) (c) | | 0.330 | | 12/20/33 | | 1,485,000 | | 971,487 |

| Citizens Bank, N.A. | | 2.450 | | 12/04/19 | | 10,000,000 | | 9,913,141 |

| Citizens Bank, N.A. | | 2.250 | | 03/02/20 | | 3,668,000 | | 3,613,567 |

See Notes to Financial Statements.

22

| BOND FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | | Rate (%) | | Maturity Date | | Principal Amount | | Value |

| BONDS(continued) | | | | | | | | |

| |

| Corporate Bonds (continued) | | | | | | | | |

| | Citizens Bank, N.A. (3 month LIBOR + 0.950%) (c) | | 3.336 | | 03/29/23 | | 10,000,000 | | $10,011,707 |

| CNH Industrial Capital LLC | | 3.375 | | 07/15/19 | | 9,221,000 | | 9,186,790 |

| CommonWealth REIT | | 5.875 | | 09/15/20 | | 6,412,000 | | 6,562,531 |

| Compass Bank | | 2.750 | | 09/29/19 | | 2,534,000 | | 2,522,082 |

| ConnectOne Bancorp, Inc. (5.200% to 02/01/23, | | | | | | | | |

| then 3 month LIBOR + 2.840%) (c) | | 5.200 | | 02/01/28 | | 1,935,000 | | 1,917,396 |

| Constellation Brands, Inc. | | 3.875 | | 11/15/19 | | 2,317,000 | | 2,321,183 |

| Continental Resources, Inc. | | 5.000 | | 09/15/22 | | 15,814,000 | | 15,810,764 |

| Controladora Mabe S.A. de C.V. (h) | | 7.875 | | 10/28/19 | | 10,000,000 | | 10,450,000 |

| County Bancorp, Inc. (5.875% to 06/01/23, | | | | | | | | |

| then 3 month LIBOR + 2.884%) (c) | | 5.875 | | 06/01/28 | | 7,500,000 | | 7,524,666 |

| CRB Group, Inc. (h) | | 6.250 | | 06/15/23 | | 5,000,000 | | 5,072,475 |

| Credit Suisse A.G. New York | | 5.400 | | 01/14/20 | | 18,903,000 | | 19,204,808 |

| CVS Health Corp. | | 2.250 | | 12/05/18 | | 14,994,000 | | 14,993,743 |

| D.R. Horton, Inc. | | 3.750 | | 03/01/19 | | 28,856,000 | | 28,849,459 |

| D.R. Horton, Inc. | | 4.000 | | 02/15/20 | | 271,000 | | 271,298 |

| Delphi Financial Group, Inc. | | 7.875 | | 01/31/20 | | 3,428,000 | | 3,587,178 |

| Deutsche Bank AG (3 month LIBOR + 1.450%) (c) | | 3.895 | | 01/18/19 | | 949,000 | | 949,395 |

| Deutsche Bank AG | | 2.500 | | 02/13/19 | | 12,981,000 | | 12,938,450 |

| Deutsche Bank AG | | 2.850 | | 05/10/19 | | 20,927,000 | | 20,801,520 |

| Deutsche Bank AG (3 month LIBOR + 1.910%) (c) | | 4.528 | | 05/10/19 | | 250,000 | | 250,000 |

| Deutsche Bank AG | | 3.150 | | 01/22/21 | | 250,000 | | 241,081 |

| Deutsche Bank AG | | 4.250 | | 10/14/21 | | 2,057,000 | | 2,006,599 |

| Deutsche Bank AG | | 4.250 | | 10/14/21 | | 313,000 | | 305,331 |

| Devon Energy Corp. | | 2.250 | | 12/15/18 | | 80,000 | | 79,986 |

| Devon Energy Corp. | | 6.300 | | 01/15/19 | | 172,000 | | 172,493 |

| Diamond 1 Finance Corp. / Diamond 2 Finance Corp. (h) | | 3.480 | | 06/01/19 | | 2,500,000 | | 2,494,621 |

| Digital Realty Trust, L.P. | | 5.875 | | 02/01/20 | | 304,000 | | 310,511 |

| Discover Bank | | 8.700 | | 11/18/19 | | 1,681,000 | | 1,758,341 |

| Discover Bank | | 7.000 | | 04/15/20 | | 4,450,000 | | 4,630,909 |

| Discover Financial Services | | 10.250 | | 07/15/19 | | 11,309,000 | | 11,749,144 |

| Dominion Gas Holdings, LLC | | 2.500 | | 12/15/19 | | 9,530,000 | | 9,435,197 |

| Dominion Resources, Inc. | | 1.875 | | 01/15/19 | | 1,250,000 | | 1,248,088 |

| Dominion Resources, Inc. | | 2.500 | | 12/01/19 | | 3,400,000 | | 3,366,393 |

| DPL Inc. | | 6.750 | | 10/01/19 | | 24,151,000 | | 24,452,888 |

| Dr Pepper Snapple Group, Inc. | | 2.600 | | 01/15/19 | | 5,000,000 | | 4,996,545 |

| Drawbridge Special Opportunities Fund L.P. (h) | | 5.000 | | 08/01/21 | | 15,000,000 | | 14,969,644 |

| Eagle Bancorp, Inc. (5.000% to 08/01/21, | | | | | | | | |

| then 3 month LIBOR + 3.850%) (c) | | 5.000 | | 08/01/26 | | 6,474,000 | | 6,483,565 |

| Eaton Corp. | | 6.950 | | 03/20/19 | | 340,000 | | 343,814 |

| Embraer Overseas Ltd. | | 6.375 | | 01/15/20 | | 13,540,000 | | 13,844,785 |

| Enable Midstream Partners, LP (b) | | 2.400 | | 05/15/19 | | 11,864,000 | | 11,792,090 |

| Enbridge Energy Partners, L.P. | | 9.875 | | 03/01/19 | | 3,010,000 | | 3,056,971 |

| Energy Transfer Partners, L.P. | | 9.700 | | 03/15/19 | | 10,549,000 | | 10,718,172 |

| Energy Transfer Partners, L.P. | | 9.000 | | 04/15/19 | | 2,817,000 | | 2,874,133 |

| EnLink Midstream Partners, LP | | 2.700 | | 04/01/19 | | 14,213,000 | | 14,105,682 |

| Enogex LLC (h) | | 6.250 | | 03/15/20 | | 1,295,000 | | 1,328,806 |

| Ensco PLC | | 8.000 | | 01/31/24 | | 12,306,000 | | 11,198,460 |

| Enstar Group Ltd. | | 4.500 | | 03/10/22 | | 25,056,000 | | 25,057,362 |

See Notes to Financial Statements.

23

| BOND FUND SCHEDULE OF INVESTMENTS(Continued) |

| November 30, 2018 |

| | | | Rate (%) | | Maturity Date | | Principal Amount | | Value |

| BONDS(continued) | | | | | | | | |

| |

| Corporate Bonds (continued) | | | | | | | | |

| Enterprise Products Operating LLC (3 month LIBOR + 2.7775%) (c) | | 5.099 | | 06/01/67 | | 8,538,000 | | $8,025,720 |

| Enterprise Products Operating LLC (5.250% to 08/16/27, | | | | | | | | |

| then 3 month LIBOR + 3.033%) (c) | | 5.250 | | 08/16/77 | | 6,666,000 | | 5,670,147 |

| Everest Reinsurance Holdings Inc. (3 month LIBOR + 2.385%) (c) | | 5.001 | | 05/01/67 | | 24,386,000 | | 23,166,700 |

| Exelon Generation Co., LLC | | 5.200 | | 10/01/19 | | 624,000 | | 633,679 |

| Exelon Generation Co., LLC | | 2.950 | | 01/15/20 | | 8,229,000 | | 8,176,618 |

| Express Scripts, Inc. | | 7.250 | | 06/15/19 | | 1,022,000 | | 1,042,912 |

| Exxon Mobil Corp. (3 month LIBOR + 0.780%) (c) | | 3.101 | | 03/01/19 | | 400,000 | | 400,683 |

| Fidelity Federal Bancorp (6.875% to 10/15/23, | | | | | | | | |

| then 3 month LIBOR + 3.790%) (c)(h) | | 6.875 | | 10/15/28 | | 6,500,000 | | 6,584,869 |

| Fifth Third Bancorp (4.900% to 09/30/19, | | | | | | | | |

| then 3 month LIBOR + 3.129%) (c)(g) | | 4.900 | | 09/30/19 | | 31,391,000 | | 30,920,135 |

| First Niagara Financial Group, Inc. | | 6.750 | | 03/19/20 | | 4,993,000 | | 5,191,394 |

| First Tennessee Bank N.A. | | 2.950 | | 12/01/19 | | 45,336,000 | | 45,081,268 |

| Flagstar Bancorp, Inc. | | 6.125 | | 07/15/21 | | 42,360,000 | | 44,058,679 |

| Flex Ltd. | | 4.625 | | 02/15/20 | | 5,650,000 | | 5,674,556 |

| Flushing Financial Corp. (5.250% to 12/15/21, | | | | | | | | |

| then 3 month LIBOR + 3.440%) (c) | | 5.250 | | 12/15/26 | | 730,000 | | 748,308 |

| FMC Corp. | | 5.200 | | 12/15/19 | | 5,000,000 | | 5,096,091 |

| Ford Motor Credit Co. LLC | | 2.375 | | 03/12/19 | | 1,155,000 | | 1,151,672 |

| Ford Motor Credit Co. LLC | | 2.262 | | 03/28/19 | | 5,562,000 | | 5,540,535 |

| Ford Motor Credit Co. LLC | | 2.021 | | 05/03/19 | | 1,000,000 | | 993,087 |

| Ford Motor Credit Co. LLC | | 1.897 | | 08/12/19 | | 15,170,000 | | 14,948,838 |

| Ford Motor Credit Co. LLC | | 2.597 | | 11/04/19 | | 37,480,000 | | 36,984,449 |

| Ford Motor Credit Co. LLC | | 2.681 | | 01/09/20 | | 946,000 | | 932,253 |

| Ford Motor Credit Co. LLC | | 8.125 | | 01/15/20 | | 500,000 | | 520,811 |

| FS Investment Corp. | | 4.000 | | 07/15/19 | | 4,402,000 | | 4,400,918 |

| GATX Corp. | | 2.500 | | 03/15/19 | | 11,908,000 | | 11,890,307 |

| GATX Corp. | | 2.600 | | 03/30/20 | | 3,291,000 | | 3,247,043 |

| General Electric Capital Corp. | | 5.100 | | 02/15/19 | | 522,000 | | 522,000 |

| General Electric Capital Corp. (3 month LIBOR + 1.000%) (c) | | 3.436 | | 04/15/23 | | 10,075,000 | | 9,017,125 |

| General Electric Capital Corp. (3 month LIBOR + 0.380%) (c) | | 2.962 | | 05/05/26 | | 5,148,000 | | 4,191,568 |

| General Electric Co. (5.000% to 01/21/21, | | | | | | | | |

| then 3 month LIBOR + 3.330%) (c)(g) | | 5.000 | | 01/21/21 | | 46,706,000 | | 37,131,270 |

| General Electric Co. / LJ VP Holdings LLC (h) | | 3.800 | | 06/18/19 | | 750,000 | | 746,025 |