UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-04521

| T. Rowe Price State Tax-Free Funds, Inc. |

|

| (Exact name of registrant as specified in charter) |

| |

| 100 East Pratt Street, Baltimore, MD 21202 |

|

| (Address of principal executive offices) |

| |

| David Oestreicher |

| 100 East Pratt Street, Baltimore, MD 21202 |

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (410) 345-2000

Date of fiscal year end: February 28

Date of reporting period: February 28, 2022

Item 1. Reports to Shareholders

(a) Report pursuant to Rule 30e-1.

| Maryland Tax-Free Bond Fund | February 28, 2022 |

| MDXBX | Investor Class |

| TFBIX | I Class |

| T. ROWE PRICE Maryland Tax-Free Funds |

|

HIGHLIGHTS

| ■ | After delivering strong results in 2021, municipal bonds faced headwinds in early 2022 as Treasury yields moved higher, leading to negative results for the tax-free bond sector during the reporting period. |

| | |

| ■ | The Maryland Tax-Free Bond Fund and the Maryland Short-Term Tax-Free Bond Fund outperformed their Lipper peer group averages over the 12-month period. The Maryland Tax-Free Money Fund produced roughly flat returns amid very low money market rates. |

| | |

| ■ | Maryland is rated AAA with a stable outlook by all three of the major credit rating agencies. |

| | |

| ■ | We believe that strong fiscal conditions at the state and local level should leave municipal bonds relatively well positioned for a challenging investment landscape. |

Log in to your account at troweprice.com for more information.

*Certain mutual fund accounts that are assessed an annual account service fee can also save money by switching to e-delivery.

Market Commentary

Dear Shareholder

Major stock and bond indexes produced mixed results during your fund’s fiscal year, the 12-month period ended February 28, 2022. Strong corporate earnings growth and a recovering economy contended with worries about inflation, new coronavirus variants, expectations of aggressive central bank tightening, and escalating geopolitical tensions.

Financial markets entered the period on an upbeat note, as the U.S. Congress expanded its coronavirus relief efforts with the passage of the $1.9 trillion American Rescue Plan Act in March. Record levels of fiscal stimulus, combined with an accelerating global vaccine rollout, helped propel a robust economic recovery and a rise in equity indexes. Weekly jobless claims declined steadily to new pandemic-era lows during the second quarter of 2021. The improved labor market and renewed stimulus efforts were reflected in higher consumer spending. A robust increase in corporate earnings growth also drove markets for much of 2021. However, earnings tailwinds showed signs of fading heading into 2022, as certain high-profile companies issued weaker-than-expected earnings reports or financial projections.

Concerns over inflation began to intensify in the latter half of the period. Persistent supply chain problems, including soaring shipping costs, raised prices for both raw materials and finished goods, while the release of pent-up demand for travel, recreation, and other services also pushed prices higher. In the U.S., consumer prices rose by 7.5% in the 12-month period ended in January 2022, the most since 1982.

Meanwhile, central banks began to move away from the extremely accommodative policies they instituted in response to the initial wave of the coronavirus. Federal Reserve officials began tapering the central bank’s purchases of Treasuries and agency mortgage-backed securities in November, and markets priced in a much more aggressive pace of rate hikes than previously expected as inflation remained elevated.

Markets were caught by surprise at the end of the period when Russia launched a large-scale military offensive into Ukraine. Amid the humanitarian crisis caused by the invasion, global equity markets moved sharply lower. Defensive stocks outperformed amid a flight to safety, while energy prices and market volatility spiked. Financials and other cyclicals dependent on a healthy economy underperformed.

In the fixed income market, domestic bond returns were broadly negative over the course of the period, as yields rose across the Treasury yield curve—especially in the intermediate-term portion of the curve—amid expectations of aggressive monetary tightening. (Bond yields and prices move in opposite directions.) Municipal bonds finished the 12-month period with negative results but held up better than Treasuries and the broader U.S. investment-grade taxable bond market, as demand for tax-free income remained strong, new supply was manageable, and state and local governments benefited from an influx of federal cash and stronger-than-expected tax revenues. However, the sector faced headwinds in early 2022 as Treasury yields increased and fund flows turned negative.

Looking ahead, the geopolitical turmoil in Ukraine has understandably raised investor and humanitarian concerns around the globe and increased market volatility and uncertainty. In light of the tragic events unfolding in Ukraine, we believe volatility in the market is likely to continue. Supply chain issues and inflation pressures are also likely to persist for longer, complicating the already difficult task of central banks trying to tackle price pressures and engineer a soft landing. Past performance of markets shows that the beginning of a policy rate-hiking cycle does not necessarily derail the U.S. stock or bond markets, nor the U.S. dollar. However, this past performance does not guarantee that those markets will perform well at the beginning of the next hiking cycle.

On the positive side, we believe that household wealth gains, pent-up consumer demand, and a potential boom in capital expenditures could sustain growth even as monetary policy turns less supportive. In this environment, our investment teams will remain focused on using fundamental research to identify companies that we believe can add value to your portfolio over the long term.

Thank you for your continued confidence in T. Rowe Price.

Sincerely,

Robert Sharps

President and CEO

Management’s Discussion of Fund Performance

MARYLAND TAX-FREE MONEY FUND

INVESTMENT OBJECTIVE

The fund seeks to provide preservation of capital, liquidity, and, consistent with these objectives, the highest level of income exempt from federal and Maryland state and local income taxes.

FUND COMMENTARY

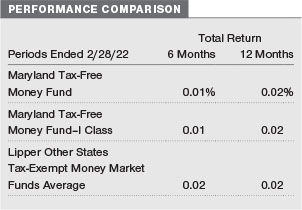

How did the fund perform in the past 12 months?

The Maryland Tax-Free Money Fund returned 0.02% in the 12 months ended February 28, 2022, performing in line with its peer group, the Lipper Other States Tax-Exempt Money Market Funds Average, which also returned 0.02%. (Returns for I Class shares may vary slightly, reflecting their different fee structure. Past performance cannot guarantee future results.)

What factors influenced the fund’s performance?

Yields began to increase over the past six months as investors priced in a more aggressive response by the Federal Reserve to the challenges posed by persistently high inflation. However, during the fund’s reporting period, the Fed kept the federal funds target rate in a range from 0.00% to 0.25%, which helped keep the interest rates available to money market investors at very low levels.

Technical factors had a mixed impact on yields during the period. Tax-exempt supply remained constrained as taxable municipal issuance increased. However, there were outflows from tax-exempt money funds, and demand for municipal money market securities from separately managed accounts and municipal bond funds weakened late in the period, contributing to a cheapening of some securities in our portfolio.

Variable rate demand note (VRDN) yields averaged 0.07% since our last report six months ago, compared with a 0.04% average for the prior six-month reporting period. Longer rates increased 76 basis points (0.76 percentage point) over the most recent six months, with one-year maturities trading around 0.84% at the end of the reporting period. The top-yielding securities in the portfolio included our positions in housing and health care VRDNs.

How is the fund positioned?

VRDNs, which are very short-maturity (one to seven day) securities, represented the portfolio’s largest position in absolute terms at the end of the period. These securities can quickly reprice during a period of rising rates, which should be beneficial for the fund.

The portfolio’s weighted average maturity (WAM) fluctuated during the period as we adjusted to changing market conditions. Later in the period, we added longer-maturity securities that have already priced in expectations for future rate hikes, and the WAM finished higher than it was six months ago.

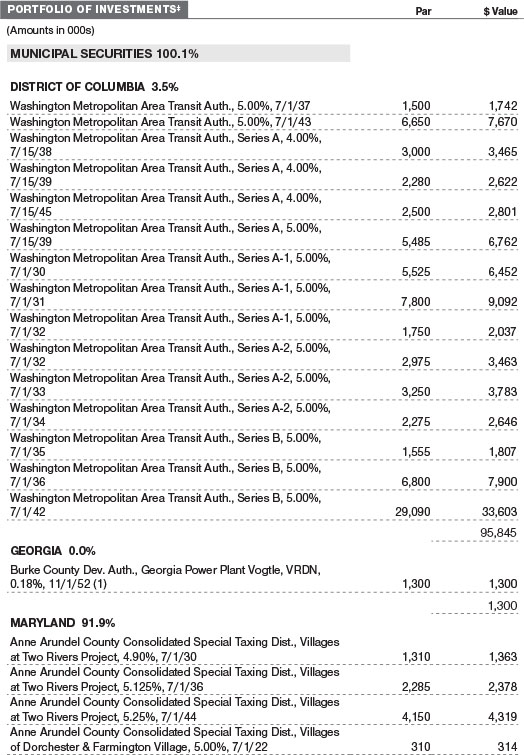

Credit quality continues to play a significant part in our security selection. At the end of the period, our largest sector allocations were to health care and housing revenue debt as well as local general obligation (GO) securities. Some prominent positions in the portfolio included Howard Hughes Medical Institute, Baltimore County, and Montgomery County. (Please refer to the portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

What is portfolio management’s outlook?

We believe yields will increase for municipal money market investors in 2022 as the Fed begins to raise rates to address high inflation. In this environment, we are pursuing a strategy that will allow the fund to quickly respond to a change in interest rate sentiment, an increase in issuance, or a changing pattern of cash flows into or out of the municipal money market. We believe the fund’s positioning in VRDNs and commercial paper is appropriate in this environment.

As always, we remain committed to managing a high-quality, diversified portfolio focused on liquidity and stability of principal, which we deem of utmost importance to our shareholders.

MARYLAND SHORT-TERM TAX-FREE BOND FUND

INVESTMENT OBJECTIVE

The fund seeks to provide the highest level of income exempt from federal and Maryland state and local income taxes consistent with modest fluctuation in principal value.

FUND COMMENTARY

How did the fund perform in the past 12 months?

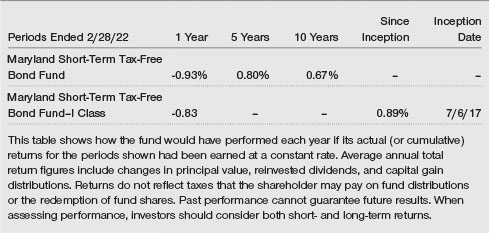

The Maryland Short-Term Tax-Free Bond Fund returned -0.93% for the 12 months ended February 28, 2022, outperforming the Lipper Short Municipal Debt Funds Average, which returned -0.97%. (Returns for I Class shares varied slightly, reflecting their different fee structure. Past performance cannot guarantee future results.)

What factors influenced the fund’s performance?

Shorter-maturity municipal bonds underperformed longer-term municipals during the 12-month period. Investors sought out higher-yielding securities, and bonds with shorter maturities were pressured as the Federal Reserve became more hawkish amid high inflation.

Within the portfolio, security selection in the revenue sector was the largest contributor to relative results versus the national benchmark. The portfolio’s holdings in segments that were hit hard early in the pandemic, such as some continuing care retirement communities and dedicated tax securities, outperformed. Bonds from the Baltimore Convention Center performed well for the portfolio. The fund also benefited from an overall overweight to the revenue sector as well as allocations within the sector, including an overweight to student housing.

Interest rate management aided results. The portfolio’s duration posture was slightly shorter than the national benchmark and our peers, which helped as rates increased during the period, and an underweight in bonds with two-year maturities was beneficial as yields in that portion of the curve increased meaningfully.

There were few significant detractors from relative results during the period; however, security selection in local general obligation (GO) bonds modestly weighed on returns.

How is the fund positioned?

We continued to favor revenue bonds over GO debt in the portfolio, reflecting our preference for bonds backed by dedicated revenue streams, which typically offer higher yields than other areas of the municipal market.

Within the revenue sector, the health care segment represents our largest position in absolute terms and relative to the benchmark. We believe our balance-sheet-first approach to investing in the segment allows our credit research team to locate strong underlying credits at attractive risk-adjusted yields. We also maintained large positions in special tax and education bonds.

While our preference for revenue bonds over GOs remains intact, it has been challenging to find opportunities in revenue debt in Maryland in the short- to intermediate-term municipal market. As a result, local GO bonds continued to be one of the fund’s largest allocations at the sector level at the end of the period. Notable purchases during the period included bonds issued for the University of Maryland Medical Center, Homewood Retirement Centers, and Baltimore County. (Please refer to the portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

The fund remains a high-quality portfolio, with about 60% of its assets invested in AAA or AA securities.

What is portfolio management’s outlook?

Accelerating inflation and geopolitical turmoil have amplified risks to the global economy, sparking a series of volatile moves across asset classes. The municipal bond market has not been immune to these macro developments, evidenced by its rates-driven sell-off at the beginning of this year and subsequent price swings.

In this environment, moderate new issuance has helped alleviate pressures from municipal fund outflows industrywide, but we believe that primary market activity could increase this spring. Although we see potential for technical headwinds to persist over the near term and anticipate additional bouts of interest rate volatility in 2022, we feel that strong fiscal conditions for states and localities leave municipal bonds better positioned for a tenuous investment landscape than most fixed income sectors.

News surrounding the Russia-Ukraine crisis, inflation, and monetary policy will likely dominate headlines in the coming months, and while we will continue to closely monitor these and other macroeconomic factors, we remain as focused as ever on bottom-up credit analysis. In our view, the recent downturn in the tax-exempt bond market has introduced compelling entry points in several segments, and we are maintaining liquidity to potentially take advantage of further pricing inefficiencies should they arise.

Ultimately, we will stay risk aware and disciplined in our fundamental, research-driven approach, which we believe will continue to serve our shareholders well.

MARYLAND TAX-FREE BOND FUND

INVESTMENT OBJECTIVE

The fund seeks to provide, consistent with prudent portfolio management, the highest level of income exempt from federal and Maryland state and local income taxes by investing primarily in investment-grade Maryland municipal bonds.

FUND COMMENTARY

How did the fund perform in the past 12 months?

The Maryland Tax-Free Bond Fund returned 0.81% for the 12 months ended February 28, 2022, outperforming the Lipper Maryland Municipal Debt Funds Average, which returned -0.22%. (Returns for I Class shares may vary slightly, reflecting their different fee structure. Past performance cannot guarantee future results.)

What factors influenced the fund’s performance?

After delivering strong results in 2021, municipal bonds faced headwinds in early 2022 as Treasury yields moved higher, leading to negative results for the tax-free bond sector during the reporting period. Despite the challenging environment, your fund produced positive results for the 12-month period.

Within the portfolio, security selection in the revenue sector was the largest contributor to relative results versus the national benchmark. The portfolio’s holdings in hospitals and industrial revenue outperformed, and Purple Line Light Rail Project bonds were a solid contributor during the period. Our allocation decisions within the revenue sector were also beneficial. An overweight to continuing care retirement communities and student housing helped returns. (Please refer to the portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

Our positions in bonds issued by the Commonwealth of Puerto Rico also added value. Puerto Rico securities outperformed as the commonwealth continued to make progress on restructuring its general obligation (GO) debt during the period.

Interest rate management had a positive overall impact on returns. Our overweight position in longer maturities was beneficial for the portfolio as yield increases were more pronounced in the front end of the curve. However, the fund’s average duration was slightly longer than that of the national benchmark, which was a modest detractor as yields rose over the past year.

With the potential for continued rates volatility, we believe a neutral duration position is appropriate, and the portfolio’s positions in higher-coupon securities should offer some protection from downside risks if rates move higher.

How is the fund positioned?

Within the revenue sector, health care remained our largest allocation and represented 24% of the fund’s net assets. Nonprofit hospitals had built up solid balance sheets before the coronavirus crisis and have since received significant federal aid, which we believe will provide financial stability going forward. We are focused on hospital systems with strong management teams that are able to keep costs down while maintaining operational excellence amid the challenges created by staff shortages and increasing labor costs.

The fund maintained significant allocations to revenue bonds in the education and transportation sectors as well as local GO debt. We also believe student housing is an attractive segment, and our purchases during the period included student housing bonds issued for Morgan State University.

We added to our position in bonds from Puerto Rico as the fundamental backdrop for the island’s debt has continued to improve.

About 47% of the portfolio consisted of AAA and AA rated bonds at period-end, but we continue to overweight A and BBB rated debt. We believe these lower-rated investment-grade segments are an area where our credit research team can help us find appropriate investment opportunities that offer incremental risk-adjusted yield. We also maintain a position in below investment-grade and unrated bonds.

Maryland’s credit rating—AAA with a stable outlook from all three major rating agencies—was unchanged during the period. Governor Larry Hogan introduced a $58 billion budget in January that commits an additional $2.4 billion to the state’s rainy-day fund and will leave the state with a structural surplus of $1.3 billion in the following years.

Maryland has a long history of responsible stewardship and prudent financial management, but, unfavorably, the state’s pension system was only funded at 71% on an actuarial basis (according to CreditScope data for 2020, the most recent data available). Maryland is currently funding its actuarially required contribution, but this has not always been the case. Although net pension liability growth has slowed, Maryland still faces heavy unfunded liabilities for its pension plans compared with other AAA rated states. We are closely monitoring Maryland’s progress in this regard.

What is portfolio management’s outlook?

Accelerating inflation and geopolitical turmoil have amplified risks to the global economy, sparking a series of volatile moves across asset classes. The municipal bond market has not been immune to these macro developments, evidenced by its rates-driven sell-off at the beginning of this year and subsequent price swings.

In this environment, moderate new issuance has helped alleviate pressures from municipal fund outflows industrywide, but we believe that primary market activity could increase this spring. Although we see potential for technical headwinds to persist over the near term and anticipate additional bouts of interest rate volatility in 2022, we feel that strong fiscal conditions for states and localities leave municipal bonds better positioned for a tenuous investment landscape than most fixed income sectors.

News surrounding the Russia-Ukraine crisis, inflation, and monetary policy will likely dominate headlines in the coming months, and while we will continue to closely monitor these and other macroeconomic factors, we remain as focused as ever on bottom-up credit analysis. In our view, the recent downturn in the tax-exempt bond market has introduced compelling entry points in several segments, and we are maintaining liquidity to potentially take advantage of further pricing inefficiencies should they arise.

Ultimately, we will stay risk aware and disciplined in our fundamental, research-driven approach, which we believe will continue to serve our shareholders well.

The views expressed reflect the opinions of T. Rowe Price as of the date of this report and are subject to change based on changes in market, economic, or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

RISKS OF INVESTING IN A RETAIL MONEY MARKET FUND

You could lose money by investing in the Fund. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. The Fund may impose a fee upon the sale of your shares or may temporarily suspend your ability to sell shares if the Fund’s liquidity falls below required minimums because of market conditions or other factors. An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and you should not expect that the sponsor will provide financial support to the Fund at any time.

RISKS OF INVESTING IN FIXED INCOME SECURITIES

Bonds are subject to interest rate risk (the decline in bond prices that usually accompanies a rise in interest rates) and credit risk (the chance that any fund holding could have its credit rating downgraded or that a bond issuer will default by failing to make timely payments of interest or principal), potentially reducing the fund’s income level and share price. The fund is less diversified than one investing nationally. Some income may be subject to state and local taxes and the federal alternative minimum tax.

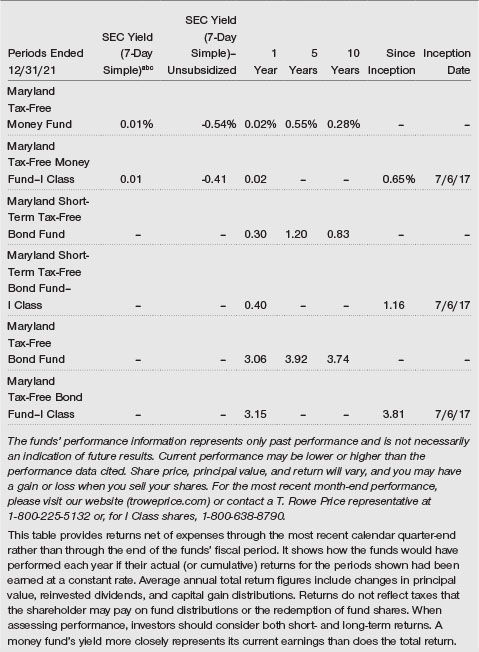

BENCHMARK INFORMATION

Note: Bloomberg®, the Bloomberg 1–3 Year Municipal Bond Index, and the Bloomberg Municipal Bond Index are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by T. Rowe Price. Bloomberg is not affiliated with T. Rowe Price, and Bloomberg does not approve, endorse, review, or recommend its products. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to its products.

Portions of the mutual fund information contained in this report were supplied by Lipper, a Refinitiv Company, subject to the following: Copyright 2022 © Refinitiv. All rights reserved. Any copying, republication or redistribution of Lipper content is expressly prohibited without the prior written consent of Lipper. Lipper shall not be liable for any errors or delays in the content, or for any actions taken in reliance thereon.

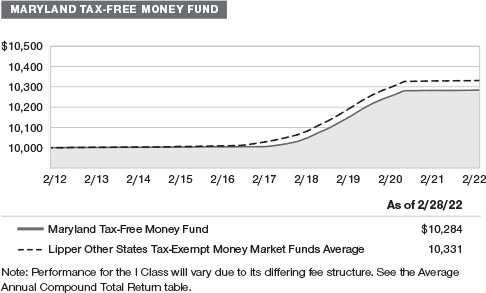

GROWTH OF $10,000

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which include a broad-based market index and may also include a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

AVERAGE ANNUAL COMPOUND TOTAL RETURN

GROWTH OF $10,000

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which include a broad-based market index and may also include a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

AVERAGE ANNUAL COMPOUND TOTAL RETURN

GROWTH OF $10,000

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which include a broad-based market index and may also include a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

AVERAGE ANNUAL COMPOUND TOTAL RETURN

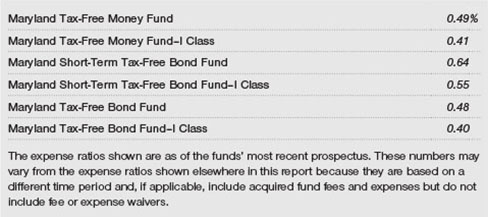

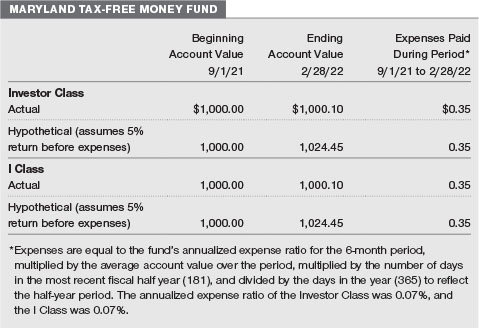

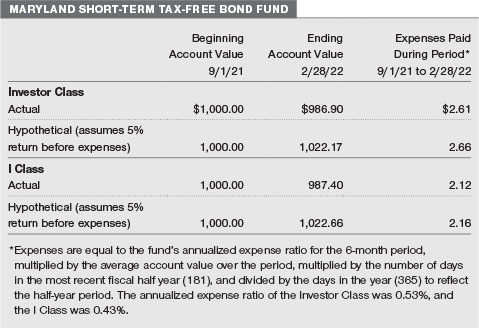

EXPENSE RATIOS

FUND EXPENSE EXAMPLE

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, such as redemption fees or sales loads, and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

Please note that the fund has two share classes: The original share class (Investor Class) charges no distribution and service (12b-1) fee, and the I Class shares are also available to institutionally oriented clients and impose no 12b-1 or administrative fee payment. Each share class is presented separately in the table.

Actual Expenses

The first line of the following table (Actual) provides information about actual account values and expenses based on the fund’s actual returns. You may use the information on this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number on the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (Hypothetical) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Note: T. Rowe Price charges an annual account service fee of $20, generally for accounts with less than $10,000. The fee is waived for any investor whose T. Rowe Price mutual fund accounts total $50,000 or more; accounts electing to receive electronic delivery of account statements, transaction confirmations, prospectuses, and shareholder reports; or accounts of an investor who is a T. Rowe Price Personal Services or Enhanced Personal Services client (enrollment in these programs generally requires T. Rowe Price assets of at least $250,000). This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

QUARTER-END RETURNS

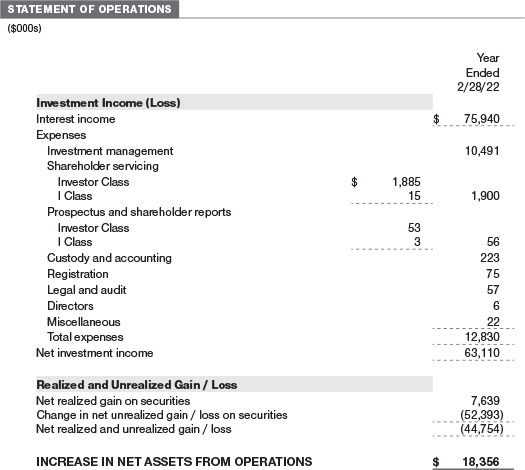

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

February 28, 2022

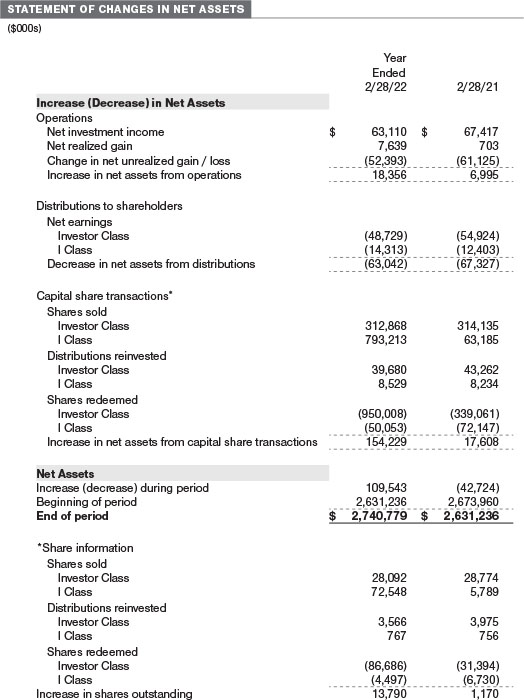

The accompanying notes are an integral part of these financial statements.

February 28, 2022

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

| NOTES TO FINANCIAL STATEMENTS |

T. Rowe Price State Tax-Free Funds, Inc. (the corporation) is registered under the Investment Company Act of 1940 (the 1940 Act). The Maryland Tax-Free Bond Fund (the fund) is a nondiversified, open-end management investment company established by the corporation. The fund seeks to provide, consistent with prudent portfolio management, the highest level of income exempt from federal and Maryland state and local income taxes by investing primarily in investment-grade Maryland municipal bonds. The fund has two classes of shares: the Maryland Tax-Free Bond Fund (Investor Class) and the Maryland Tax-Free Bond Fund–I Class (I Class). I Class shares require a $500,000 initial investment minimum, although the minimum generally is waived or reduced for financial intermediaries, eligible retirement plans, and certain other accounts. Prior to November 15, 2021, the initial investment minimum was $1 million and was generally waived for financial intermediaries, eligible retirement plans, and other certain accounts. As a result of the reduction in the I Class minimum, certain assets transferred from the Investor Class to the I Class. This transfer of shares from Investor Class to I Class is reflected in the Statement of Changes in Net Assets within the Capital shares transactions as Shares redeemed and Shares sold, respectively. Each class has exclusive voting rights on matters related solely to that class; separate voting rights on matters that relate to both classes; and, in all other respects, the same rights and obligations as the other class.

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

Basis of Preparation The fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 (ASC 946). The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (GAAP), including, but not limited to, ASC 946. GAAP requires the use of estimates made by management. Management believes that estimates and valuations are appropriate; however, actual results may differ from those estimates, and the valuations reflected in the accompanying financial statements may differ from the value ultimately realized upon sale or maturity.

Investment Transactions, Investment Income, and Distributions Investment transactions are accounted for on the trade date basis. Income and expenses are recorded on the accrual basis. Realized gains and losses are reported on the identified cost basis. Premiums and discounts on debt securities are amortized for financial reporting purposes. Income tax-related interest and penalties, if incurred, are recorded as income tax expense. Non-cash dividends, if any, are recorded at the fair market value of the asset received. Distributions to shareholders are recorded on the ex-dividend date. Income distributions are declared by each class daily and paid monthly. A capital gain distribution may also be declared and paid by the fund annually.

Class Accounting Shareholder servicing, prospectus, and shareholder report expenses incurred by each class are charged directly to the class to which they relate. Expenses common to all classes and investment income are allocated to the classes based upon the relative daily net assets of each class’s settled shares; realized and unrealized gains and losses are allocated based upon the relative daily net assets of each class’s outstanding shares.

Capital Transactions Each investor’s interest in the net assets of the fund is represented by fund shares. The fund’s net asset value (NAV) per share is computed at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day the NYSE is open for business. However, the NAV per share may be calculated at a time other than the normal close of the NYSE if trading on the NYSE is restricted, if the NYSE closes earlier, or as may be permitted by the SEC. Purchases and redemptions of fund shares are transacted at the next-computed NAV per share, after receipt of the transaction order by T. Rowe Price Associates, Inc., or its agents.

New Accounting Guidance In March 2020, the FASB issued Accounting Standards Update (ASU), ASU 2020–04, Reference Rate Reform (Topic 848) – Facilitation of the Effects of Reference Rate Reform on Financial Reporting, which provides optional, temporary relief with respect to the financial reporting of contracts subject to certain types of modifications due to the planned discontinuation of the London Interbank Offered Rate (LIBOR) and other interbank-offered based reference rates as of the end of 2021. In March 2021, the administrator for LIBOR announced the extension of the publication of a majority of the USD LIBOR settings to June 30, 2023. Management expects that the adoption of the guidance will not have a material impact on the fund’s financial statements.

Indemnification In the normal course of business, the fund may provide indemnification in connection with its officers and directors, service providers, and/or private company investments. The fund’s maximum exposure under these arrangements is unknown; however, the risk of material loss is currently considered to be remote.

NOTE 2 - VALUATION

Fair Value The fund’s financial instruments are valued at the close of the NYSE and are reported at fair value, which GAAP defines as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The T. Rowe Price Valuation Committee (the Valuation Committee) is an internal committee that has been delegated certain responsibilities by the fund’s Board of Directors (the Board) to ensure that financial instruments are appropriately priced at fair value in accordance with GAAP and the 1940 Act. Subject to oversight by the Board, the Valuation Committee develops and oversees pricing-related policies and procedures and approves all fair value determinations. Specifically, the Valuation Committee establishes policies and procedures used in valuing financial instruments, including those which cannot be valued in accordance with normal procedures or using pricing vendors; determines pricing techniques, sources, and persons eligible to effect fair value pricing actions; evaluates the services and performance of the pricing vendors; oversees the pricing process to ensure policies and procedures are being followed; and provides guidance on internal controls and valuation-related matters. The Valuation Committee provides periodic reporting to the Board on valuation matters.

Various valuation techniques and inputs are used to determine the fair value of financial instruments. GAAP establishes the following fair value hierarchy that categorizes the inputs used to measure fair value:

Level 1 – quoted prices (unadjusted) in active markets for identical financial instruments that the fund can access at the reporting date

Level 2 – inputs other than Level 1 quoted prices that are observable, either directly or indirectly (including, but not limited to, quoted prices for similar financial instruments in active markets, quoted prices for identical or similar financial instruments in inactive markets, interest rates and yield curves, implied volatilities, and credit spreads)

Level 3 – unobservable inputs (including the fund’s own assumptions in determining fair value)

Observable inputs are developed using market data, such as publicly available information about actual events or transactions, and reflect the assumptions that market participants would use to price the financial instrument. Unobservable inputs are those for which market data are not available and are developed using the best information available about the assumptions that market participants would use to price the financial instrument. GAAP requires valuation techniques to maximize the use of relevant observable inputs and minimize the use of unobservable inputs. When multiple inputs are used to derive fair value, the financial instrument is assigned to the level within the fair value hierarchy based on the lowest-level input that is significant to the fair value of the financial instrument. Input levels are not necessarily an indication of the risk or liquidity associated with financial instruments at that level but rather the degree of judgment used in determining those values.

Valuation Techniques Debt securities generally are traded in the over-the-counter (OTC) market and are valued at prices furnished by independent pricing services or by broker dealers who make markets in such securities. When valuing securities, the independent pricing services consider the yield or price of bonds of comparable quality, coupon, maturity, and type, as well as prices quoted by dealers who make markets in such securities.

Assets and liabilities other than financial instruments, including short-term receivables and payables, are carried at cost, or estimated realizable value, if less, which approximates fair value.

Investments for which market quotations or market-based valuations are not readily available or deemed unreliable are valued at fair value as determined in good faith by the Valuation Committee, in accordance with fair valuation policies and procedures. The objective of any fair value pricing determination is to arrive at a price that could reasonably be expected from a current sale. Financial instruments fair valued by the Valuation Committee are primarily private placements, restricted securities, warrants, rights, and other securities that are not publicly traded. Factors used in determining fair value vary by type of investment and may include market or investment specific considerations. The Valuation Committee typically will afford greatest weight to actual prices in arm’s length transactions, to the extent they represent orderly transactions between market participants, transaction information can be reliably obtained, and prices are deemed representative of fair value. However, the Valuation Committee may also consider other valuation methods such as market-based valuation multiples; a discount or premium from market value of a similar, freely traded security of the same issuer; discounted cash flows; yield to maturity; or some combination. Fair value determinations are reviewed on a regular basis and updated as information becomes available, including actual purchase and sale transactions of the investment. Because any fair value determination involves a significant amount of judgment, there is a degree of subjectivity inherent in such pricing decisions, and fair value prices determined by the Valuation Committee could differ from those of other market participants.

Valuation Inputs On February 28, 2022, all of the fund’s financial instruments were classified as Level 2, based on the inputs used to determine their fair values.

NOTE 3 - OTHER INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks and/or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

Noninvestment-Grade Debt The fund invests, either directly or through its investment in other T. Rowe Price funds, in noninvestment-grade debt, including “high yield” or “junk” bonds or leveraged loans. Noninvestment-grade debt issuers are more likely to suffer an adverse change in financial condition that would result in the inability to meet a financial obligation. The noninvestment-grade debt market may experience sudden and sharp price swings due to a variety of factors that may decrease the ability of issuers to make principal and interest payments and adversely affect the liquidity or value, or both, of such securities. Accordingly, securities issued by such companies carry a higher risk of default and should be considered speculative.

Restricted Securities The fund invests in securities that are subject to legal or contractual restrictions on resale. Prompt sale of such securities at an acceptable price may be difficult and may involve substantial delays and additional costs.

When-Issued Securities The fund enters into when-issued purchase or sale commitments, pursuant to which it agrees to purchase or sell, respectively, an authorized but not yet issued security for a fixed unit price, with payment and delivery not due until issuance of the security on a scheduled future date. When-issued securities may be new securities or securities issued through a corporate action, such as a reorganization or restructuring. Until settlement, the fund maintains liquid assets sufficient to settle its commitment to purchase a when-issued security or, in the case of a sale commitment, the fund maintains an entitlement to the security to be sold. Amounts realized on when-issued transactions are included in realized gain/loss on securities in the accompanying financial statements.

LIBOR Transition The fund may invest in instruments that are tied to reference rates, including LIBOR. Over the course of the last several years, global regulators have indicated an intent to phase out the use of LIBOR and similar interbank offered rates (IBOR). While publication for most LIBOR currencies and lesser-used USD LIBOR settings ceased immediately after December 31, 2021, remaining USD LIBOR settings will continue to be published until June 30, 2023. There remains uncertainty regarding the future utilization of LIBOR and the nature of any replacement rate. Any potential effects of the transition away from LIBOR on the fund, or on certain instruments in which the fund invests, cannot yet be determined. The transition process may result in, among other things, an increase in volatility or illiquidity of markets for instruments that currently rely on LIBOR, a reduction in the value of certain instruments held by the fund, or a reduction in the effectiveness of related fund transactions such as hedges. Any such effects could have an adverse impact on the fund’s performance.

Other Purchases and sales of portfolio securities other than short-term securities aggregated $587,821,000 and $354,013,000, respectively, for the year ended February 28, 2022.

NOTE 4 - FEDERAL INCOME TAXES

Generally, no provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its income and gains. Distributions determined in accordance with federal income tax regulations may differ in amount or character from net investment income and realized gains for financial reporting purposes.

The fund files U.S. federal, state, and local tax returns as required. The fund’s tax returns are subject to examination by the relevant tax authorities until expiration of the applicable statute of limitations, which is generally three years after the filing of the tax return but which can be extended to six years in certain circumstances. Tax returns for open years have incorporated no uncertain tax positions that require a provision for income taxes.

Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences. The permanent book/tax adjustments have no impact on results of operations or net assets and relate primarily to a tax practice that treats a portion of the proceeds from each redemption of capital shares as a distribution of taxable net investment income or realized capital gain and differences between book/tax amortization policies. For the year ended February 28, 2022, the following reclassification was recorded:

Distributions during the years ended February 28, 2022 and February 28, 2021, totaled $63,042,000 and $67,327,000, respectively, and were characterized as tax-exempt income for tax purposes. At February 28, 2022, the tax-basis cost of investments and components of net assets were as follows:

During the year ended February 28, 2022, the fund utilized $350,000 of capital loss carryforwards.

NOTE 5 - RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price Associates, Inc. (Price Associates), a wholly owned subsidiary of T. Rowe Price Group, Inc. (Price Group). The investment management agreement between the fund and Price Associates provides for an annual investment management fee, which is computed daily and paid monthly. The fee consists of an individual fund fee, equal to 0.10% of the fund’s average daily net assets, and a group fee. The group fee rate is calculated based on the combined net assets of certain mutual funds sponsored by Price Associates (the group) applied to a graduated fee schedule, with rates ranging from 0.48% for the first $1 billion of assets to 0.260% for assets in excess of $845 billion. The fund’s group fee is determined by applying the group fee rate to the fund’s average daily net assets. The fee is computed daily and paid monthly. At February 28, 2022, the effective annual group fee rate was 0.28%.

Effective September 1, 2021, the Investor Class is subject to a contractual expense limitation through the expense limitation date indicated in the table below. During the limitation period, Price Associates is required to waive its management fee and pay the fund for any expenses (excluding interest; expenses related to borrowings, taxes, and brokerage; and other non-recurring expenses permitted by the investment management agreement) that would otherwise cause the fund’s ratio of annualized total expenses to average net assets (net expense ratio) to exceed its expense limitation. The fund is required to repay Price Associates for expenses previously waived/paid to the extent its net assets grow or expenses decline sufficiently to allow repayment without causing the fund’s net expense ratio (after the repayment is taken into account) to exceed the lesser of: (1) the expense limitation in place at the time such amounts were waived; or (2) the fund’s current expense limitation. However, no repayment will be made more than three years after the date of a payment or waiver.

The I Class is also subject to an operating expense limitation (I Class Limit) pursuant to which Price Associates is contractually required to pay all operating expenses of the I Class, excluding management fees; interest; expenses related to borrowings, taxes, and brokerage; and other non-recurring expenses permitted by the investment management agreement, to the extent such operating expenses, on an annualized basis, exceed the I Class Limit. This agreement will continue through the expense limitation date indicated in the table below, and may be renewed, revised, or revoked only with approval of the fund’s Board. The I Class is required to repay Price Associates for expenses previously paid to the extent the class’s net assets grow or expenses decline sufficiently to allow repayment without causing the class’s operating expenses (after the repayment is taken into account) to exceed the lesser of: (1) the I Class Limit in place at the time such amounts were paid; or (2) the current I Class Limit. However, no repayment will be made more than three years after the date of a payment or waiver.

In addition, the fund has entered into service agreements with Price Associates and a wholly owned subsidiary of Price Associates, each an affiliate of the fund (collectively, Price). Price Associates provides certain accounting and administrative services to the fund. T. Rowe Price Services, Inc. provides shareholder and administrative services in its capacity as the fund’s transfer and dividend-disbursing agent. For the year ended February 28, 2022, expenses incurred pursuant to these service agreements were $89,000 for Price Associates and $501,000 for T. Rowe Price Services, Inc. All amounts due to and due from Price, exclusive of investment management fees payable, are presented net on the accompanying Statement of Assets and Liabilities.

The fund may participate in securities purchase and sale transactions with other funds or accounts advised by Price Associates (cross trades), in accordance with procedures adopted by the fund’s Board and Securities and Exchange Commission rules, which require, among other things, that such purchase and sale cross trades be effected at the independent current market price of the security. Purchases and sales cross trades aggregated $15,130,000 and $28,155,000, respectively, with net realized gain of $0 for the year ended February 28, 2022.

NOTE 6 - OTHER MATTERS

Unpredictable events such as environmental or natural disasters, war, terrorism, pandemics, outbreaks of infectious diseases, and similar public health threats may significantly affect the economy and the markets and issuers in which a fund invests. Certain events may cause instability across global markets, including reduced liquidity and disruptions in trading markets, while some events may affect certain geographic regions, countries, sectors, and industries more significantly than others, and exacerbate other pre-existing political, social, and economic risks. Since 2020, a novel strain of coronavirus (COVID-19) has resulted in disruptions to global business activity and caused significant volatility and declines in global financial markets. In February 2022, Russian forces entered Ukraine and commenced an armed conflict. Economic sanctions have since been imposed on Russia and certain of its citizens, including the exclusion of Russia from the SWIFT global payments network. As a result, Russia’s central bank closed the country’s stock market on February 28, 2022, and Russian-related stocks and debt have since suffered significant declines in value. The duration of the coronavirus outbreak and the Russian-Ukraine conflict, and their effects on the financial markets, cannot be determined with certainty. The fund’s performance could be negatively impacted if the value of a portfolio holding were harmed by these and such other events. Management is actively monitoring these events.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors of T. Rowe Price State Tax-Free Funds, Inc. and

Shareholders of T. Rowe Price Maryland Tax-Free Bond Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of T. Rowe Price Maryland Tax-Free Bond Fund (one of the funds constituting T. Rowe Price State Tax-Free Funds, Inc., referred to hereafter as the “Fund”) as of February 28, 2022, the related statement of operations for the year ended February 28, 2022, the statement of changes in net assets for each of the two years in the period ended February 28, 2022, including the related notes, and the financial highlights for each of the periods indicated therein (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of February 28, 2022, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period ended February 28, 2022 and the financial highlights for each of the periods indicated therein, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits of these financial statements in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of February 28, 2022 by correspondence with the custodian and brokers; when replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Baltimore, Maryland

April 19, 2022

We have served as the auditor of one or more investment companies in the T. Rowe Price group of investment companies since 1973.

TAX INFORMATION (UNAUDITED) FOR THE TAX YEAR ENDED 2/28/22

We are providing this information as required by the Internal Revenue Code. The amounts shown may differ from those elsewhere in this report because of differences between tax and financial reporting requirements.

The fund’s distributions to shareholders included:

| ■ | $178,000 from short-term capital gains |

| | |

| ■ | $1,042,000 from long-term capital gains, subject to a long-term capital gains tax rate of not greater than 20% |

| | |

| ■ | $63,192,000 which qualified as exempt-interest dividends. |

INFORMATION ON PROXY VOTING POLICIES, PROCEDURES, AND RECORDS

A description of the policies and procedures used by T. Rowe Price funds to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information. You may request this document by calling 1-800-225-5132 or by accessing the SEC’s website, sec.gov.

The description of our proxy voting policies and procedures is also available on our corporate website. To access it, please visit the following Web page:

https://www.troweprice.com/corporate/en/utility/policies.html

Scroll down to the section near the bottom of the page that says, “Proxy Voting Policies.” Click on the Proxy Voting Policies link in the shaded box.

Each fund’s most recent annual proxy voting record is available on our website and through the SEC’s website. To access it through T. Rowe Price, visit the website location shown above, and scroll down to the section near the bottom of the page that says, “Proxy Voting Records.” Click on the Proxy Voting Records link in the shaded box.

HOW TO OBTAIN QUARTERLY PORTFOLIO HOLDINGS

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission (SEC) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The fund’s reports on Form N-PORT are available electronically on the SEC’s website (sec.gov). In addition, most T. Rowe Price funds disclose their first and third fiscal quarter-end holdings on troweprice.com.

ABOUT THE FUND’S DIRECTORS AND OFFICERS

Your fund is overseen by a Board of Directors (Board) that meets regularly to review a wide variety of matters affecting or potentially affecting the fund, including performance, investment programs, compliance matters, advisory fees and expenses, service providers, and business and regulatory affairs. The Board elects the fund’s officers, who are listed in the final table. At least 75% of the Board’s members are considered to be independent (i.e., not “interested persons” as defined in Section 2(a)(19) of the 1940 Act) of the Price Funds, T. Rowe Price Associates, Inc. (T. Rowe Price), and its affiliates; “interested” directors and officers are employees of T. Rowe Price. The business address of each director and officer is 100 East Pratt Street, Baltimore, Maryland 21202. The Statement of Additional Information includes additional information about the fund directors and is available without charge by calling a T. Rowe Price representative at 1-800-638-5660.

INDEPENDENT DIRECTORS(a)

Name

(Year of Birth)

Year Elected

[Number of T. Rowe Price

Portfolios Overseen] | | Principal Occupation(s) and Directorships of Public Companies and

Other Investment Companies During the Past Five Years |

| | | |

Teresa Bryce Bazemore

(1959)

2018

[204] | | President and Chief Executive Officer, Federal Home Loan Bank of San Francisco (2021 to present); President, Radian Guaranty (2008 to 2017); Chief Executive Officer, Bazemore Consulting LLC (2018 to 2021); Director, Chimera Investment Corporation (2017 to 2021); Director, First Industrial Realty Trust (2020 to present); Director, Federal Home Loan Bank of Pittsburgh (2017 to 2019) |

| | | |

Ronald J. Daniels

(1959)

2018

[204] | | President, The Johns Hopkins University(b) and Professor, Political Science Department, The Johns Hopkins University (2009 to present); Director, Lyndhurst Holdings (2015 to present); Director, BridgeBio Pharma, Inc. (2020 to present) |

| | | |

Bruce W. Duncan

(1951)

2013

[204] | | President, Chief Executive Officer, and Director, CyrusOne, Inc. (2020 to 2021); Chief Executive Officer and Director (2009 to 2016), Chair of the Board (2016 to 2020), and President (2009 to 2016), First Industrial Realty Trust, owner and operator of industrial properties; Chair of the Board (2005 to 2016) and Director (1999 to 2016), Starwood Hotels & Resorts, a hotel and leisure company; Member, Investment Company Institute Board of Governors (2017 to 2019); Member, Independent Directors Council Governing Board (2017 to 2019); Senior Advisor, KKR (2018 to present); Director, Boston Properties (2016 to present); Director, Marriott International, Inc. (2016 to 2020) |

| | | |

Robert J. Gerrard, Jr.

(1952)

2013

[204] | | Advisory Board Member, Pipeline Crisis/Winning Strategies, a collaborative working to improve opportunities for young African Americans (1997 to 2016); Chair of the Board, all funds (July 2018 to present) |

| | | |

Paul F. McBride

(1956)

2013

[204] | | Advisory Board Member, Vizzia Technologies (2015 to present); Board Member, Dunbar Armored (2012 to 2018) |

| | | |

Kellye L. Walker(c)

(1966)

2021

[204] | | Executive Vice President and Chief Legal Officer, Eastman Chemical Company (April 2020 to present); Executive Vice President and Chief Legal Officer, Huntington Ingalls Industries, Inc. (NYSE: HIl) (January 2015 to March 2020); Director, Lincoln Electric Company (October 2020 to present) |

| | | |

| (a)All information about the independent directors was current as of December 31, 2021, unless otherwise indicated, except for the number of portfolios overseen, which is current as of the date of this report. |

| (b)William J. Stromberg, nonexecutive chair of the Board and director of T. Rowe Price Group, Inc., the parent company of the Price Funds’ investment advisor, has served on the Board of Trustees of Johns Hopkins University since 2014. |

| (c)Effective November 8, 2021, Ms. Walker was appointed as independent director of the Price Funds. |

INTERESTED DIRECTORS(a)

Name

(Year of Birth)

Year Elected

[Number of T. Rowe Price

Portfolios Overseen] | | Principal Occupation(s) and Directorships of Public Companies and

Other Investment Companies During the Past Five Years |

| | | |

David Oestreicher

(1967)

2018

[204] | | General Counsel, Vice President, and Secretary, T. Rowe Price Group, Inc.; Chair of the Board, Chief Executive Officer, President, and Secretary, T. Rowe Price Trust Company; Director, Vice President, and Secretary, T. Rowe Price, T. Rowe Price Investment Services, Inc., T. Rowe Price Retirement Plan Services, Inc., and T. Rowe Price Services, Inc.; Director and Secretary, T. Rowe Price Investment Management, Inc. (Price Investment Management); Vice President and Secretary, T. Rowe Price International (Price International); Vice President, T. Rowe Price Hong Kong (Price Hong Kong), T. Rowe Price Japan (Price Japan), and T. Rowe Price Singapore (Price Singapore); Principal Executive Officer and Executive Vice President, all funds |

| | | |

Robert W. Sharps, CFA, CPA

(1971)

2019

[0] | | Director and Vice President, T. Rowe Price; Chief Executive Officer and President, T. Rowe Price Group, Inc.; Director, Price Investment Management; Vice President, T. Rowe Price Trust Company |

| | | |

Eric L. Veiel, CFA

(1972)

2022

[204] | | Director and Vice President, T. Rowe Price; Vice President, T. Rowe Price Group, Inc.; Vice President, T. Rowe Price Trust Company |

| | | |

| (a)All information about the interested directors was current as of January 1, 2022, unless otherwise indicated, except for the number of portfolios overseen, which is current as of the date of this report. |

OFFICERS

Name (Year of Birth)

Position Held With State Tax-Free Funds | | Principal Occupation(s) |

| | | |

Austin Applegate (1974)

Executive Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Colin T. Bando, CFA (1987)

Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Daniel Chihorek (1984)

Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc.; formerly, Vice President, Municipal Research Analyst, GW&K Investment Management (to 2018) |

| | | |

Davis Collins (1989)

Vice President | | Vice President, T. Rowe Price |

| | | |

M. Helena Condez (1962)

Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Alan S. Dupski, CPA (1982)

Principal Financial Officer, Vice President, and Treasurer | | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

| | | |

Sarah J. Engle (1979)

Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Stephanie A. Gentile, CFA (1956)

Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Gary J. Greb (1961)

Vice President | | Vice President, T. Rowe Price, Price International, and T. Rowe Price Trust Company |

| | | |

Charles B. Hill, CFA (1961)

Executive Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Dylan Jones, CFA (1971)

Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Michael Kane (1982)

Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc.; formerly, Research Analyst, GW&K Investments (to 2019) |

| | | |

Paul J. Krug, CPA (1964)

Vice President | | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

| | | |

Matthew T. Larkin (1983)

Assistant Vice President | | Assistant Vice President, T. Rowe Price |

| | | |

Alan D. Levenson, Ph.D. (1958)

Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

James T. Lynch, CFA (1983)

Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Konstantine B. Mallas (1963)

Executive Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

James M. Murphy, CFA (1967)

President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Mary Ann Picciotto, CPA (1973)

Chief Compliance Officer | | Chief Compliance Officer and Vice President, T. Rowe Price; Vice President, T. Rowe Price Group, Inc., and Price International; formerly, Head of Compliance, Invesco (to 2019) |

| | | |

Fran M. Pollack-Matz (1961)

Vice President and Secretary | | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., T. Rowe Price Investment Services, Inc., and T. Rowe Price Services, Inc. |

| | | |

Rachel Protzman (1988)

Assistant Vice President | | Assistant Vice President, T. Rowe Price |

| | | |

Shannon H. Rauser (1987)

Assistant Secretary | | Assistant Vice President, T. Rowe Price |

| | | |

Chen Shao (1980)

Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Douglas D. Spratley, CFA (1969)

Executive Vice President | | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

| | | |

Timothy G. Taylor, CFA (1975)

Executive Vice President | | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

| | | |

Megan Warren (1968)

Vice President | | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., T. Rowe Price Retirement Plan Services, Inc., T. Rowe Price Services, Inc., and T. Rowe Price Trust Company |

| | | |

| Unless otherwise noted, officers have been employees of T. Rowe Price or Price International for at least 5 years. |

Item 1. (b) Notice pursuant to Rule 30e-3.

Not applicable.

Item 2. Code of Ethics.

The registrant has adopted a code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of this code of ethics is filed as an exhibit to this Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Directors has determined that Ms. Teresa Bryce Bazemore qualifies as an audit committee financial expert, as defined in Item 3 of Form N-CSR. Ms. Bazemore is considered independent for purposes of Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

(a) – (d) Aggregate fees billed for the last two fiscal years for professional services rendered to, or on behalf of, the registrant by the registrant’s principal accountant were as follows:

Audit fees include amounts related to the audit of the registrant’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. Audit-related fees include amounts reasonably related to the performance of the audit of the registrant’s financial statements and specifically include the issuance of a report on internal controls and, if applicable, agreed-upon procedures related to fund acquisitions. Tax fees include amounts related to services for tax compliance, tax planning, and tax advice. The nature of these services specifically includes the review of distribution calculations and the preparation of Federal, state, and excise tax returns. All other fees include the registrant’s pro-rata share of amounts for agreed-upon procedures in conjunction with service contract approvals by the registrant’s Board of Directors/Trustees.

(e)(1) The registrant’s audit committee has adopted a policy whereby audit and non-audit services performed by the registrant’s principal accountant for the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant require pre-approval in advance at regularly scheduled audit committee meetings. If such a service is required between regularly scheduled audit committee meetings, pre-approval may be authorized by one audit committee member with ratification at the next scheduled audit committee meeting. Waiver of pre-approval for audit or non-audit services requiring fees of a de minimis amount is not permitted.

(2) No services included in (b) – (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Less than 50 percent of the hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees.

(g) The aggregate fees billed for the most recent fiscal year and the preceding fiscal year by the registrant’s principal accountant for non-audit services rendered to the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant were $3,749,000 and $3,315,000, respectively.

(h) All non-audit services rendered in (g) above were pre-approved by the registrant’s audit committee. Accordingly, these services were considered by the registrant’s audit committee in maintaining the principal accountant’s independence.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

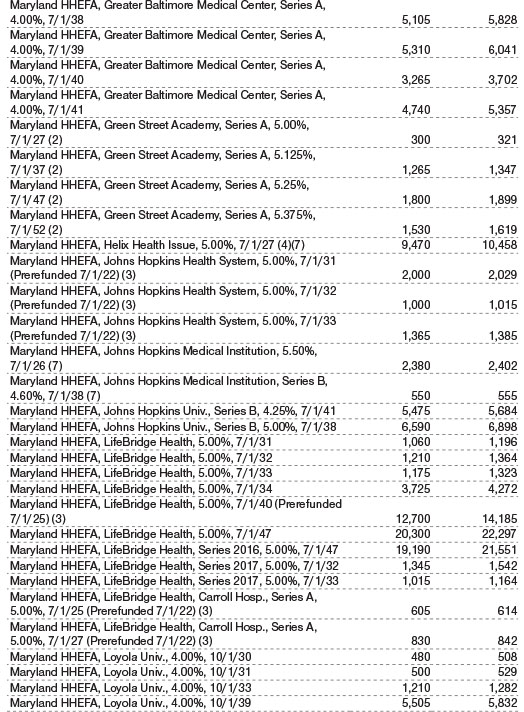

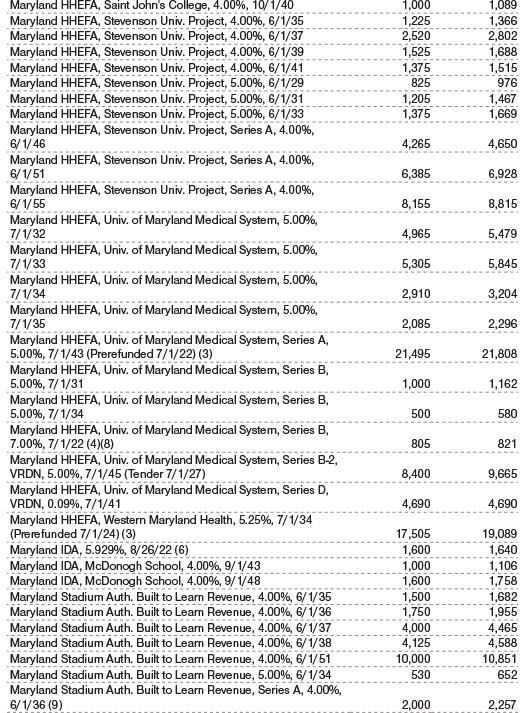

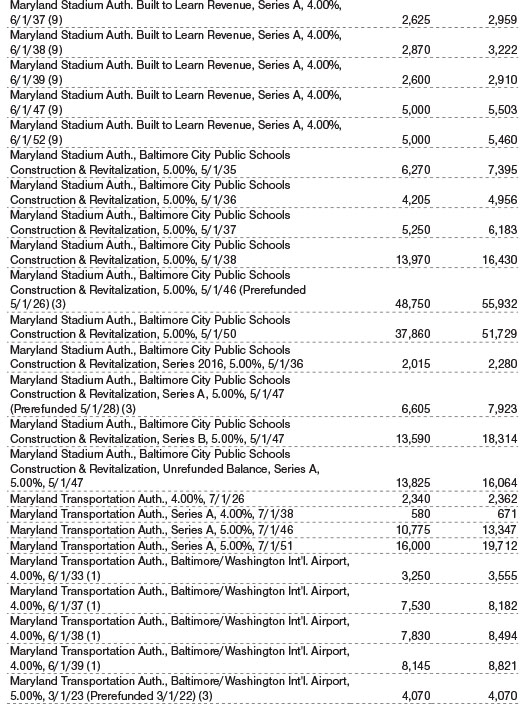

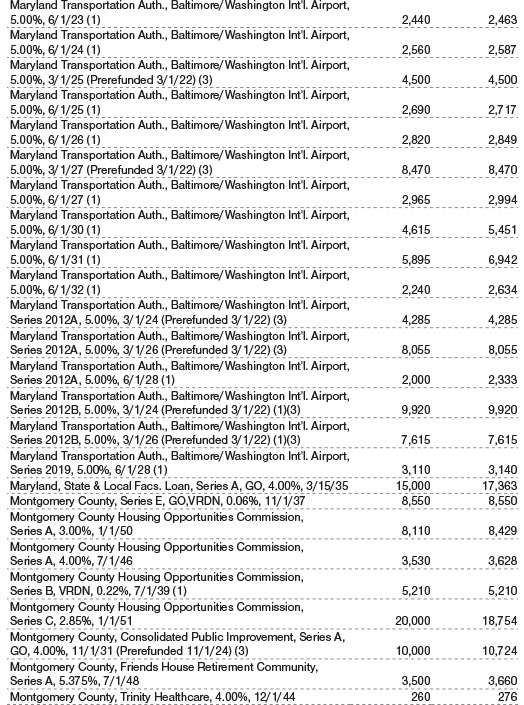

(a) Not applicable. The complete schedule of investments is included in Item 1 of this Form N-CSR.

(b) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

There has been no change to the procedures by which shareholders may recommend nominees to the registrant’s board of directors.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-CSR was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the period covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Disclosure of Securities Lending Activities for Closed-End Management Investment Companies.

Not applicable.

Item 13. Exhibits.

(a)(1) The registrant’s code of ethics pursuant to Item 2 of Form N-CSR is attached.

(2) Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

(3) Written solicitation to repurchase securities issued by closed-end companies: not applicable.

(b) A certification by the registrant’s principal executive officer and principal financial officer, pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(b) under the Investment Company Act of 1940, is attached.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

T. Rowe Price State Tax-Free Funds, Inc.

| By | | /s/ David Oestreicher |

| | | David Oestreicher |

| | | Principal Executive Officer |

| |

| Date | | April 19, 2022 | | | | |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By | | /s/ David Oestreicher |

| | | David Oestreicher |

| | | Principal Executive Officer |

| |

| Date | | April 19, 2022 | | | | |

| |

| |

| By | | /s/ Alan S. Dupski |

| | | Alan S. Dupski |

| | | Principal Financial Officer |

| |

| Date | | April 19, 2022 | | | | |