Exhibit 99.1

For immediate release

December 13, 2007 ; (publié également en français)

Petro-Canada’s Capital Program Up 28% Over 2007; Continued Focus on Long-Life Projects

Highlights

| · | $5.3 billion capital program planned: focus on long-life projects that provide sustainable cash flow |

| · | Upstream production guidance range for 2008 of 390,000 barrels of oil equivalent per day (boe/d) to 420,000 boe/d |

Calgary– Petro-Canada’s Board of Directors today approved a capital and exploration expenditure program totalling $5.3 billion for 2008, an increase of 28% compared with the program in 2007.

The 2008 capital program includes $3.6 billion directed to growth projects, exploration and new venture developments, a 50% increase in this category compared with 2007. In addition, Petro-Canada expects to invest $1.2 billion to replace reserves in core areas, $430 million to enhance existing assets and to improve profitability in the base business, and $105 million to comply with new regulations. The 2008 capital expenditure program is expected to be funded primarily from cash flow and additional debt as required.

“The step up in our capital program for 2008 begins to fund the next large projects in our portfolio of opportunities,” said Ron Brenneman, president and chief executive officer. “These are high quality, long-life projects consistent with our business strategy to deliver profitable growth.”

Petro-Canada’s upstream production is expected to decrease slightly in 2008 and be in the range of 390,000 boe/d to 420,000 boe/d. In 2008, natural declines in East Coast Canada and Western Canada are expected to be partially offset by additional volumes from the full-year impact of Buzzard and Saxon in the North Sea, as well as higher planned Oil Sands production. Production for the full year of 2007 is expected to be at the high end of the range of 400,000 boe/d to 420,000 boe/d, in line with previous guidance.

“In 2007, we took our base rate of production to a new level, and we will see that again when our next big upstream projects come on,” said Brenneman. “In the meantime, our two refining conversion projects will boost earnings and cash flow significantly in the near term.”

The increased level of capital spending contemplated is consistent with the Company’s priority of investing in attractive projects to create shareholder value. As the Company looks beyond 2008, spending on the next large projects will likely result in annual capital expenditures exceeding operating cash flow. Additional funding requirements are expected to be met by external financing. As financial leverage is expected to increase over time, it will be managed in the context of Petro-Canada’s target ranges.

Petro-Canada is one of Canada’s largest oil and gas companies, operating in both the upstream and downstream sectors of the industry in Canada and internationally. The Company creates value by responsibly developing energy resources and providing world class petroleum products and services. Petro-Canada is proud to be a National Partner to the Vancouver 2010 Olympic and Paralympic Winter Games. Petro-Canada’s common shares trade on the Toronto Stock Exchange (TSX) under the symbol PCA and on the New York Stock Exchange (NYSE) under the symbol PCZ.

Read the full text of "Petro-Canada’s Capital Program Up 28% Over 2007; Continued Focus on Long-Life Projects" release at http://www.petro-canada.ca/en/investors/93.aspx.

Petro-Canada will hold a conference call to discuss the 2008 outlook with investors on Thursday, December 13, 2007 at 5:30 p.m. Eastern Standard Time (EST). To participate, please call 1-866-898-9626 (toll-free in North America), 00-800-8989-6323 (toll-free internationally), or 416-340-2216 at 5:25 p.m. Media are invited to listen to the call by dialing 1-866-540-8136 (toll-free in North America) or 416-340-8010. Media are invited to ask questions at the end of the call. A live audio webcast of the conference call will be available on Petro-Canada's website at http://www.petro-canada.ca/en/investors/93.aspx on December 13, 2007 at 5:30 p.m. EST. Those who are unable to listen to the call live may listen to a recording of the call approximately one hour after its completion by calling 1-800-408-3053 (toll-free in North America) or 416-695-5800 (passcode number 3242534#). Approximately one hour after the call, a recording will be available on Petro-Canada’s website.

LEGAL NOTICE – FORWARD-LOOKING INFORMATION

This release contains forward-looking information. You can usually identify this information by such words as "plan,""anticipate,""forecast,""believe,""target,""intend,""expect,""estimate,""budget," or other similar wording suggesting future outcomes or statements about an outlook. Below are examples of references to forward-looking information:

· business strategies and goals · future investment decisions · outlook (including operational updates and strategic milestones) · future capital, exploration and other expenditures · future resource purchases and sales · construction and repair activities · turnarounds at refineries and other facilities · anticipated refining margins · future oil and gas production levels and the sources of their growth · project development, and expansion schedules and results · future exploration activities and results, and dates by which certain areas may be developed or may come on-stream | · retail throughputs · pre-production and operating costs · reserves and resources estimates · royalties and taxes payable · production life-of-field estimates · natural gas export capacity · future financing and capital activities (including purchases of Petro-Canada common shares under the Company's normal course issuer bid (NCIB) program) · contingent liabilities (including potential exposure to losses related to retail licensee

agreements) · environmental matters · future regulatory approvals |

Such forward-looking information is subject to known and unknown risks and uncertainties. Other factors may cause actual results, levels of activity and achievements to differ materially from those expressed or implied by such information. Such factors include, but are not limited to:

· industry capacity · imprecise reserves estimates of recoverable quantities of oil, natural gas and liquids from resource plays, and other sources not currently classified as reserves · the effects of weather and climate conditions · the results of exploration and development drilling, and related activities · the ability of suppliers to meet commitments · decisions or approvals from administrative tribunals · risks attendant with domestic and international oil and gas operations · expected rates of return | · general economic, market and business conditions · competitive action by other companies · fluctuations in oil and gas prices · refining and marketing margins · the ability to produce and transport crude oil and natural gas to markets · fluctuations in interest rates and foreign currency exchange rates · actions by governmental authorities (including changes in taxes, royalty rates and

resource-use strategies) · changes in environmental and other regulations · international political events · nature and scope of actions by stakeholders and/or the general public |

Many of these and other similar factors are beyond the control of Petro-Canada. Petro-Canada discusses these factors in greater detail in filings with the Canadian provincial securities commissions and the United States (U.S.) Securities and Exchange Commission (SEC).

We caution readers that this list of important factors affecting forward-looking information is not exhaustive. Furthermore, the forward-looking information in this release is made as of December 13, 2007 and, except as required by applicable law, Petro-Canada does not update it publicly or revise it. This cautionary statement expressly qualifies the forward-looking information in this release.

Petro-Canada disclosure of reserves

Petro-Canada's qualified reserves evaluators prepare the reserves estimates the Company uses. The Canadian provincial securities commissions do not consider our reserves staff and management as independent of the Company. Petro-Canada has obtained an exemption from certain Canadian reserves disclosure requirements that allow the Company to make disclosure in accordance with SEC standards. This exemption allows comparisons with U.S. and other international issuers.

As a result, Petro-Canada formally discloses its reserves data and other oil and gas data using U.S. requirements and practices, and these may differ from Canadian domestic standards and practices. Note that when we use the term boe in this release, it may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet (Mcf) to one barrel (bbl) is based on an energy equivalency conversion method. This method primarily applies at the burner tip and does not represent a value equivalency at the wellhead.

To disclose reserves in SEC filings, oil and gas companies must prove they are economically and legally producible under existing economic and operating conditions. Proof comes from actual production or conclusive formation tests. The use of terms such as "probable," "possible," "recoverable," or "potential reserves and resources" in this release does not meet the SEC guidelines for SEC filings.

The table below describes the industry definitions that we currently use:

Definitions Petro-Canada uses | Reference |

| Proved oil and gas reserves (includes both proved developed and proved undeveloped) | U.S. SEC reserves definition (Accounting Rules Regulation S-X 210.4-10, U.S. Financial Accounting Standards Board Statement No.-69) |

| Unproved reserves, probable and possible reserves | CIM (Petroleum Society) definitions (Canadian Oil and Gas Evaluation Handbook, Vol. 1 Section 5) |

| Contingent and prospective resources | Society of Petroleum Engineers, World Petroleum Congress and American Association of Petroleum Geologists definitions (approved February 2000) |

There is no certainty that it will be economically viable or technically feasible to produce any portion of the resources. For use in this release, "total resources" means reserves plus resources.

SEC regulations do not define proved reserves from our oil sands mining operations as an oil and gas activity. These reserves are classified as a mining activity and are estimated in accordance with SEC Industry Guide 7. For internal management purposes, Petro-Canada views these reserves and their development as part of the Company’s total exploration and production operations.

Throughout this release, total Company reserves, total Company production, total Company reserves replacement and total Company reserves life index (RLI) on a before royalty basis are calculated using the sum of all oil and gas activities, and all oil sands mining activities. Before royalties, oil sands mining 2006 year-end proved reserves were 345 million barrels (MMbbls) and oil sands mining annual 2006 production was 11 MMbbls.

For more information, please contact:

| INVESTOR AND ANALYST INQUIRIES | MEDIA AND GENERAL INQUIRIES |

| | |

Ken Hall Investor Relations 403-296-7859 e-mail: investor@petro-canada.ca | Michelle Harries Corporate Communications 403-296-3648 e-mail: corpcomm@petro-canada.ca |

| | |

Pamela Tisdale Investor Relations 403-296-4423 e-mail: investor@petro-canada.ca | |

| | |

| www.petro-canada.ca |

OUTLOOK – CAPITAL EXPENDITURES

Long-Term Investment Profile

Petro-Canada’s capital program anticipates a number of major projects over the next several years, adding significantly to earnings and cash flow.

Over the past number of years, Petro-Canada has been building a suite of investment opportunities to add significantly to earnings and cash flow going forward. In the upstream, most of these opportunities are long-life projects with plateau production for 10 years or more. In the Downstream, the Edmonton refinery conversion project (RCP) will enable the refinery to run 100% oil sands-based feedstock. The project has been sanctioned and is under construction. The remainder of the projects are expected to be sanctioned once sufficient front-end engineering and design (FEED) work has been completed. The increased level of capital spending contemplated is consistent with the Company’s priority of investing in attractive projects to create shareholder value. As the Company looks beyond 2008, spending on future large projects will likely result in annual capital expenditures exceeding operating cash flow. The Company anticipates that additional funding requirements will be met by external financing. As financial leverage is expected to increase over time, it will be managed in the context of Petro-Canada’s target ranges. The Company has the flexibility to pace the projects and will continue to manage the cash returned to shareholders with an eye to creating the most value.

Major Project | Capital Cost Estimate | Target On-Stream Date |

| | (millions of Canadian dollars) | |

| Edmonton Refinery Conversion | 2,200 | 2008 |

| Montreal Refinery Coker | 1,000 | 2010 |

| Syria Gas Development | 600 – 800 | 2010 |

| MacKay River Expansion | 1,000 – 1,200 | 2011 |

| Fort Hills – Phase I | 8,500 | 2011 |

| Libyan Concession Development | 5,000 | 2012 |

Capital Expenditures by Priorities

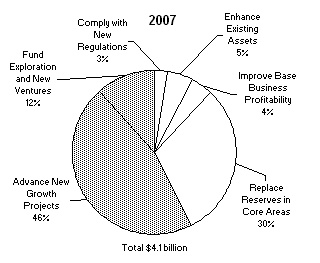

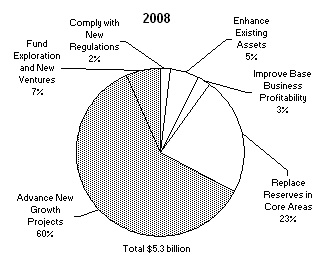

In 2008, spending on new growth projects is expected to increase. Two-thirds of planned capital expenditures support delivering profitable new growth and funding exploration and new ventures. This is up by more than $1 billion compared with the same categories in 2007. The remaining one-third of the 2008 planned capital expenditures is directed toward replacing reserves in core areas, enhancing existing assets, improving base business profitability and complying with new regulations.

Capital Investment Priorities (millions of Canadian dollars) | 2007 Outlook As at July 26, 2007 (1) | 2008 Outlook As at Dec. 13, 2007 | 2008 Highlights |

| Comply with new regulations | $ 105 | $ 105 | Spending on regulatory projects at Downstream facilities and investment at Syncrude to reduce sulphur emissions |

| Enhance existing assets | 210 | 290 | Improving reliability at Downstream, Oil Sands and North American Natural Gas facilities |

| Improve base business profitability | 180 | 140 | Developing the retail/wholesale marketing networks and increasing refinery yield |

| Replace reserves in core areas | 1,250 | 1,195 | Investing for immediate impact across the four upstream businesses |

| Advance new growth projects | 1,890 | 3,205 | Investing in medium-term growth projects, such as preliminary engineering and design for Fort Hills, developing the Libyan concessions, converting the Edmonton refinery to run oil sands feedstocks, preparing for the potential new coker at the Montreal refinery, developing the Ebla project in Syria and preliminary engineering and design for the MacKay River expansion project |

| Fund exploration and new ventures for long-term growth | 480 | 350 | Investing in exploration activity in International, Alaska and the Mackenzie Delta/Corridor |

Total continuing operations | $4,115 | $5,285 | |

| (1) | 2007 Outlook amounts have been re-categorized to align with the 2008 Outlook presentation |

Capital Expenditures by Business

Spending reflects quality investment opportunities in the upstream and downstream sectors. Of note in 2008, Petro-Canada plans to direct additional funds to Oil Sands to complete the FEED for the Fort Hills project, to East Coast Canada to develop the White Rose extensions, and to International for development of the Libyan concessions, advancing the Ebla project in Syria and for a balanced exploration program. In the Downstream, capital spending is expected to decrease as the Company completes the Edmonton RCP, which is expected to come on-stream in the fourth quarter of 2008. This is partially offset by investing to advance the potential Montreal coker.

Capital Investment by Business Unit | 2007 Outlook | | | 2008 Outlook | |

(millions of Canadian dollars) | As at July 26, 2007 | | | As at December 13, 2007 | |

Upstream | | | | | |

| North American Natural Gas | | | | | |

Western Canada | $ | 540 | | | $ | 415 | |

U.S. Rockies | | 130 | | | | 190 | |

North of 60 | | 155 | | | | 70 | |

| Oil Sands | | | | | | | |

Fort Hills | | 270 | | | | 1,165 | |

MacKay River | | 260 | | | | 240 | |

Syncrude | | 75 | | | | 80 | |

Other leases | | 15 | | | | 35 | |

International & Offshore | | | | | | | |

East Coast Canada | | 205 | | | | 295 | |

International | | | | | | | |

North Sea | | 440 | | | | 360 | |

Libya/Syria | | 215 | | | | 985 | |

Trinidad and Tobago | | 315 | | | | 290 | |

| | | 2,620 | | | | 4,125 | |

Downstream | | | | | | | |

| Refining and Supply | | 1,285 | | | | 950 | |

| Sales and Marketing | | 150 | | | | 150 | |

| Lubricants | | 30 | | | | 25 | |

| | | 1,465 | | | | 1,125 | |

Shared Services | | 30 | | | | 35 | |

Total continuing operations | $ | 4,115 | | | $ | 5,285 | |

OUTLOOK – CONSOLIDATED PRODUCTION

Upstream production is expected to decrease slightly in 2008, primarily due to natural declines in East Coast Canada and Western Canada. Offsetting these decreases are additional volumes from the full-year impact of Buzzard and Saxon in the North Sea and higher planned Oil Sands production. Production is expected to average in the range of 390,000 boe/d to 420,000 boe/d in 2008.

Factors that may impact production during 2008 include reservoir performance, drilling results, facility reliability and the successful execution of planned turnarounds.

| | 2007 Outlook (+/-) | 2008 Outlook (+/-) |

(thousands of boe/d) | As at July 26, 2007 | As at December 13, 2007 |

North American Natural Gas | | |

| Natural gas | 97 | 93 |

| Liquids | 13 | 12 |

Oil Sands | | |

| Syncrude | 34 | 35 |

| MacKay River | 24 | 25 |

International & Offshore | | |

East Coast Canada | 95 | 85 |

International | | |

North Sea | 90 | 93 |

Other International | 57 | 57 |

Total continuing operations | 400 – 420 | 390 – 420 |

North American Natural Gas

Lower capital spending is expected to result in production declines of around 5%. The business is shifting away from new exploration in Western Canada, with a greater focus in the U.S. Rockies in the short term and North of 60 in the long term.

The planned capital program for North American Natural Gas is approximately $675 million in 2008, down from forecast 2007 spending levels. Approximately $415 million is planned for the replacement of reserves in core areas of Western Canada, down 23% from the estimate for 2007 of $540 million. Lower capital spending reflects the maturity of the basin and increasing royalty rates. Investment in unconventional growth opportunities in the U.S. Rockies is estimated to be $190 million. Exploration and new venture investments of approximately $70 million are expected to be spent to develop longer term supply opportunities in the frontier areas of Alaska and the Mackenzie Delta/Corridor. The Company plans to test some of its frontier exploration prospects by participating in two exploration wells in the Alaska Foothills and one exploration well in the Mackenzie Corridor in 2008.

North American Natural Gas production is expected to decline around 5% to 105,000 boe/d, compared with estimated production of 110,000 boe/d in 2007. Declines in conventional production in Western Canada are forecast to be partially offset by additional annual average U.S. Rockies volumes. U.S. Rockies production is expected to remain steady at the current rate of 95 million cubic feet equivalent/day (MMcfe/d) of natural gas through 2008.

Oil Sands

Increased capital spending in 2008 reflects FEED work for Fort Hills and the MacKay River expansion.

A capital program of about $1,520 million is planned for Oil Sands in 2008. Capital for new growth opportunities of approximately $1,311 million includes funding FEED for the Fort Hills project (forecast to be $1,165 million) and the MacKay River expansion (forecast to be $90 million). The time frame for the completion of FEED for the MacKay River expansion project has been extended by one year to evaluate opportunities for integration with the Fort Hills project and to pursue cost-saving opportunities associated with utilizing an international engineering, procurement and construction contractor. Spending to enhance existing operations and comply with regulations at Syncrude is budgeted to be $62 million. Enhancing existing operations and improving base business profitability at MacKay River is expected to be approximately $85 million. Investment of $62 million is planned for the replacement of reserves through ongoing pad development at MacKay River.

In 2008, production from Oil Sands is expected to be 60,000 boe/d, compared with estimated production of 58,000 boe/d in 2007. Higher expected production in 2008 is due to higher volumes anticipated at Syncrude and MacKay River. Syncrude’s 2008 forecast production takes into account a planned 45-day Coker 8-1 turnaround starting in March and a planned 53-day hydrogen plant turnaround starting in August. At MacKay River, a major five-year 10- to 15-day planned turnaround is scheduled for May 2008.

International & Offshore

In the first quarter of 2007, the Company combined its East Coast Canada and International businesses under one management structure. This change leverages and grows the capabilities of similar operations. The combined East Coast Canada and International operations are now referred to as International & Offshore.

East Coast Canada

Lower production planned for 2008 reflects anticipated natural declines, while capital spending increases for future developments.

The planned capital program in 2008 for East Coast Canada will be about $295 million. Capital in 2008 is forecast to be spent primarily on advancing the White Rose extension developments and drilling to replace reserves at Hibernia and White Rose.

East Coast Canada production is expected to be 85,000 boe/d in 2008, compared with an estimate of 95,000 boe/d in 2007. The 2008 production estimate reflects natural declines at Hibernia and Terra Nova, while White Rose volumes are planned to come off plateau. Terra Nova and White Rose have planned maintenance turnarounds of 16 days each in the summer of 2008. There is no major turnaround planned for Hibernia in 2008.

International

International is delivering near-term growth in the North Sea and building a portfolio of longer term growth opportunities through exploration and business development.

In 2008, a capital budget of approximately $1,635 million is planned for International. Investment to replace reserves in core areas is expected to be approximately $366 million, primarily for ongoing development drilling at Buzzard, Guillemot West and on the producing fields in Trinidad and Tobago. About $986 million will be invested in new growth projects, with a focus on advancing the development of the Libyan concessions and for front-end engineering and preliminary drilling at the Ebla project in Syria. It is expected that approximately $283 million will be allocated to exploration.

Production from the International business is expected to increase to 150,000 boe/d in 2008, compared with estimated production of 147,000 boe/d in 2007. The slight increase in production in 2008 reflects the full-year contributions from Buzzard and Saxon (a small North Sea development that started up in November 2007). These projects are expected to more than offset the 15% to 20% annual natural declines in the North Sea.

Exploration Summary

Petro-Canada’s 2008 exploration program is significant and reflects the Company’s success in building a sizable, balanced portfolio of prospects.

(millions of Canadian dollars) | 2008 Exploration and New Ventures | | 2008 General and Administrative, Geological and Geophysical

(including seismic) Exploration Expenses | | Total (1) | |

International, East Coast Canada, Alaska and Mackenzie Delta/Corridor | $ | 350 | | $ | 180 | | $ | 530 | |

(1) The total exploration budget is comprised of capital investments for exploration and new ventures plus general and administrative, and geological and geophysical (including seismic) exploration expenses.

Petro-Canada’s exploration budget of $530 million includes exploration spending for International, East Coast Canada, Alaska and the Mackenzie Delta/Corridor. Spending of about $373 million covers an expected program of up to 17 wells focused in the North Sea, Trinidad and Tobago, Syria and the Alaskan Foothills. In addition, a planned seismic program will be focused on Libya and Trinidad and Tobago.

Downstream

Capital investment is focused on growth and improving base business profitability. The Edmonton refinery conversion project (RCP) is expected to add net earnings and cash flow starting in late 2008.

A capital program of about $1,125 million for the Downstream is planned in 2008. The majority of capital spending is forecast for new growth project funding of $767 million. This capital will be directed toward completing the Edmonton RCP and advancing the potential 25,000 barrel per day (b/d) Montreal coker. The total project cost estimated for RCP has increased from $2.0 billion to $2.2 billion, reflecting labour cost pressures in Alberta. Final RCP costs will depend on the labour productivity the Company is able to achieve this winter. Approximately $136 million is forecast to be directed to the enhancement of existing operations. This includes reliability and safety improvements at Downstream facilities, as well as site enhancement within the wholesale and retail networks. A further $138 million is planned to be invested to improve the profitability of the Downstream’s base business. This includes a number of high return refining projects and continued development of the retail and wholesale network. Approximately $84 million is expected to be invested in regulatory compliance, relatively flat compared with the estimated $70 million invested in 2007.

In the third quarter of 2008, the Edmonton refinery is expected to commence a two-month planned turnaround to tie-in RCP and to complete routine maintenance on other units within the refinery. It is anticipated that this planned turnaround will reduce the annual average crude throughput and light oil yield by approximately 20,000 b/d. The Montreal refinery has planned turnarounds on secondary processing units in 2008. As with all planned Downstream turnarounds, supply arrangements will be made to meet market demand during these outages. Other planned maintenance activities at the Edmonton refinery and the Lubricants plant in Mississauga in 2008 are not expected to have a significant impact on throughput or yields.

Conference Call Details

Petro-Canada will hold a conference call to discuss the 2008 outlook with investors on Thursday, December 13, 2007 at 5:30 p.m. Eastern Standard Time (EST). To participate, please call 1-866-898-9626 (toll-free in North America), 00-800-8989-6323 (toll-free internationally), or 416-340-2216 at 5:25 p.m. Media are invited to listen to the call by dialing 1-866-540-8136 (toll-free in North America) or 416-340-8010. Media are invited to ask questions at the end of the call. A live audio webcast of the conference call will be available on Petro-Canada's website at http://www.petro-canada.ca/en/investors/93.aspx on December 13, 2007 at 5:30 p.m. EST. Those who are unable to listen to the call live may listen to a recording of the call approximately one hour after its completion by calling 1-800-408-3053 (toll-free in North America) or 416-695-5800 (passcode number 3242534#). Approximately one hour after the call, a recording will be available on Petro-Canada’s website.