Portions of this presentation contain forward-looking statements and involve risks and uncertainties that could materially affect

expected results of operations, liquidity, cash flows and business prospects. Factors that could cause results to differ

materially include, but are not limited to: global commodity pricing fluctuations; supply and demand considerations for

Occidental’s products; general domestic political and regulatory approval conditions; political events; not successfully

completing, or any material delay of, any development of new fields, expansion projects, capital expenditures, efficiency-

improvement projects, acquisitions or dispositions; potential failure to achieve expected production from existing and future oil

and gas development projects; exploration risks such as drilling unsuccessful wells; any general economic recession or

slowdown domestically or internationally; higher-than-expected costs; potential liability for remedial actions under existing or

future environmental regulations and litigation; potential liability resulting from pending or future litigation; general domestic and

international political conditions; potential disruption or interruption of Occidental’s production or manufacturing or damage to

facilities due to accidents, chemical releases, labor unrest, weather, natural disasters or insurgent activity; failure of risk

management; changes in law or regulations; or changes in tax rates. Finding and Development costs calculations inherently

compare costs and reserves from separate periods. The United States Securities and Exchange Commission (SEC) permits

oil and natural gas companies, in their SEC filings, to disclose only reserves anticipated to be economically producible, as of a

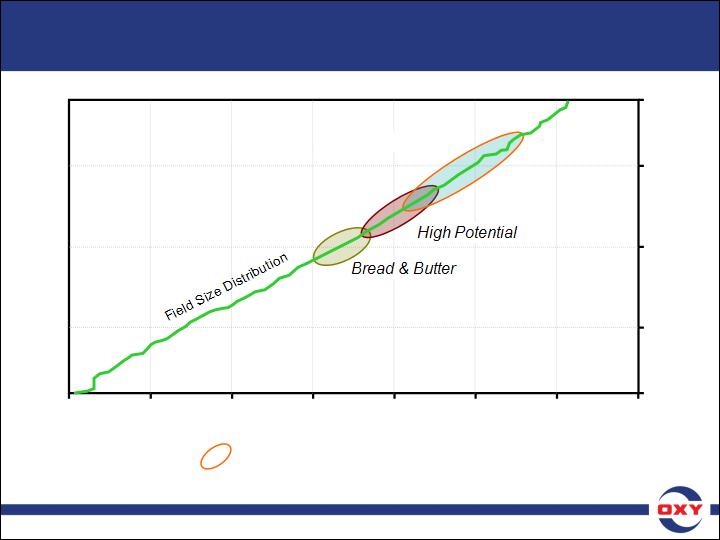

given date, by application of development projects to known accumulations. We use certain terms in this presentation, such as

resource potential, net risked reserves, de-risked, geologically viable, EUR (expected ultimate recovery), discovery volumes,

likely recoverable resources and oil in place, that the SEC’s guidelines strictly prohibit us from using in our SEC filings. These

terms represent our internal estimates of volumes of oil and gas that are not proved reserves but are potentially recoverable

through exploratory drilling or additional drilling or recovery techniques and are not intended to correspond to probable or

possible reserves as defined by SEC regulations. By their nature these estimates are more speculative than proved, probable

or possible reserves and subject to greater risk they will not be realized. You should not place undue reliance on these forward

-looking statements, which speak only as of the date of this presentation. Unless legally required, Occidental does not

undertake any obligation to update any forward-looking statements, as a result of new information, future events or otherwise.

U.S. investors are urged to consider carefully the disclosures in our 2010 Form 10-K, available through the following toll-free

number 1-888-OXYPETE (1-888-699-7383) or on the internet at http://www.oxy.com. You also can obtain a copy form the

SEC by calling 1-800-SEC-0330. We post or provide links to important information on our website including investor and

analyst presentations, certain board committee charters and information that SEC requires companies and certain of its officers

and directors to file or furnish. Such information may be found in the “Investor Relations” and “Social Responsibility” portions of

the website.

Cautionary Statement