Table of Contents

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON AUGUST 2, 2004.

SECURITIES ACT FILE NO. 333-

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933 x

PRE-EFFECTIVE AMENDMENT NO. ¨

POST-EFFECTIVE AMENDMENT NO. ¨

SCUDDER ADVISOR FUNDS

(EXACT NAME OF REGISTRANT AS SPECIFIED IN CHARTER)

One South Street, Baltimore, MD 21202

(ADDRESS OF PRINCIPAL EXECUTIVE OFFICES) (ZIP CODE)

410-895-5000

(REGISTRANT’S AREA CODE AND TELEPHONE NUMBER)

John Millette, Secretary

Scudder Advisor Funds

One South Street, Baltimore, MD 21202

(NAME AND ADDRESS OF AGENT FOR SERVICE)

WITH COPIES TO:

| Burton M. Leibert, Esq. | Cathy G. O’Kelly, Esq. | |

Mary C. Carty, Esq. | David A. Sturms, Esq. | |

Willkie Farr & Gallagher LLP | Vedder, Price, Kaufman & Kammholz, P.C. | |

787 Seventh Avenue | 222 North LaSalle Street | |

New York, New York 10019-6099 | Chicago, Illinois 60601 |

APPROXIMATE DATE OF PROPOSED PUBLIC OFFERING: As soon as practicable after the effective date of this Registration Statement.

TITLE OF SECURITIES BEING REGISTERED:

Shares of Beneficial Interest ($0.001 par value) of the Registrant

The Registrant has registered an indefinite amount of securities under the Securities Act of 1933, as amended, pursuant to Section 24(f) under the Investment Company Act of 1940, as amended; accordingly, no fee is payable herewith because of reliance upon Section 24(f).

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

SCUDDER DYNAMIC GROWTH FUND |

Q&A

Q What is happening?

A Deutsche Asset Management has initiated a program to reorganize and combine selected funds within the Scudder fund family.

Q What issue am I being asked to vote on?

A You are being asked to vote on a proposal to merge Scudder Dynamic Growth Fund into Scudder Mid Cap Growth Fund. The funds are managed by largely the same portfolio management team, have similar investment objectives and seek to achieve their objectives through similar types of investments. Both funds invest in stocks of medium-sized companies, although Scudder Dynamic Growth Fund may invest a larger percentage of its assets in smaller-sized companies.

After carefully reviewing the proposal, your fund’s Board has determined that this action is in the best interest of the fund. The Board [unanimously] recommends that you vote “FOR” this proposal.

Q Why has this proposal been made for my fund?

A As discussed in the enclosed Prospectus/Proxy Statement, the combination of the two funds is the consolidation of similar funds that are categorized in the same peer group, compete in the same distribution channels and are managed by largely the same portfolio management team. The merger is intended to create a more streamlined line-up of Scudder funds, which Deutsche Asset Management believes may help enhance investment performance and increase the efficiency of Deutsche Asset Management’s operations. The merger may also result in greater cost efficiencies and the potential for economies of scale for the combined fund and its shareholders.

Q Will I have to pay taxes as a result of the merger?

A The merger is expected to be a tax-free transaction, and will not take place unless special tax counsel provides an opinion to that effect. As a result of the merger, however,

Table of Contents

Q&A continued

your fund may lose the benefit of certain tax losses that could have been used to offset or defer future gains.

If you choose to redeem or exchange your shares before or after the merger, the redemption or exchange will generate taxable gain or loss; therefore, you should consult a tax advisor before doing so. Of course, you may also be subject to capital gains or losses as a result of the normal operations of your fund whether or not the transaction occurs.

Q Upon merger, will I own the same number of shares?

A The aggregate value of your shares will not change as a result of the transaction. It is likely that the number of shares you own will change as a result of the transaction because your shares will be exchanged at the net asset value per share of Scudder Mid Cap Growth Fund, which will probably be different from the net asset value per share of Scudder Dynamic Growth Fund.

Q Will any fund pay for the proxy solicitation and legal costs associated with this solicitation?

A No. Deutsche Asset Management will bear these costs.

Q When would the merger take place?

A If approved, the merger would occur on or about November 15, 2004 or as soon as reasonably practicable after shareholder approval is obtained. Shortly after completion of the merger, shareholders whose accounts are affected by the merger will receive a confirmation statement reflecting their new account number and number of shares owned.

Q How can I vote?

A You can vote in any one of four ways:

| n | Through the internet by going to the website listed on your proxy card; |

| n | By telephone, with a toll-free call to the number listed on your proxy card; |

| n | By mail, by sending the enclosed proxy card, signed and dated, to us in the enclosed envelope; or |

| n | In person, by attending the special meeting. |

We encourage you to vote over the internet or by telephone, using the voting control number that appears on your proxy card. Whichever method you choose, please take the time to read the full text of the proxy statement before you vote.

2

Table of Contents

Q If I send my proxy in now as requested, can I change my vote later?

A You may revoke your proxy at any time before it is voted by: (1) sending a written revocation to the Secretary of the fund as explained in the proxy statement; or (2) forwarding a later-dated proxy that is received by the fund at or prior to the special meeting; or (3) attending the special meeting and voting in person. Even if you plan to attend the special meeting, we ask that you return the enclosed proxy. This will help us ensure that an adequate number of shares are present for the special meeting to be held.

Q Will I be able to continue to track my fund’s performance in the newspaper, on the Internet or through the voice response system (ScudderACCESS)?

A Yes. You will be able to continue to track your fund’s performance through all these means.

Q What is the Board’s recommendation?

A Your fund’s Board [unanimously] recommends that all shareholders vote “FOR” the approval of the merger.

Q Whom should I call for additional information about this Prospectus/Proxy Statement?

A Please call Georgeson Shareholder Communications Inc., your fund’s proxy solicitor, at 1-888-288-5518.

Q&A continued

3

Table of Contents

A Message from the Fund’s Chief Executive Officer

, 2004

Dear Shareholder:

I am writing to you to ask for your vote on an important matter that affects your investment in Scudder Dynamic Growth Fund (“Dynamic Growth Fund”). While you are, of course, welcome to join us at the Dynamic Growth Fund shareholders’ meeting, most shareholders cast their vote by filling out and signing the enclosed proxy card, or by voting by telephone or through the Internet.

We are asking for your vote on the following matter:

Approval of a proposed merger of Dynamic Growth Fund into Scudder Mid Cap Growth Fund (“Mid Cap Growth Fund”). In this merger, your shares of Dynamic Growth Fund would, in effect, be exchanged, on a tax-free basis, for shares of Mid Cap Growth Fund with an equal net asset value.

The proposed merger is part of a program initiated by Deutsche Asset Management. This program is intended to provide a more streamlined selection of investment options that is consistent with the changing needs of investors. If approved by fund shareholders, this program will enable Deustche Asset Management to:

| • | Eliminate redundancies within the Scudder fund family by reorganizing and combining certain funds; and |

| • | Focus its investment resources on a core set of mutual funds that best meet investor needs. |

In determining to recommend approval of the merger, the Trustees of Dynamic Growth Fund considered the following factors, among others:

| • | Deutsche Asset Management’s overall program to reorganize and combine selected funds within the Scudder fund family gives the portfolio management team the opportunity to focus its efforts on managing the combined Fund and offers a uniform distribution platform for the combined Fund; |

| • | Dynamic Growth Fund shareholders will have the opportunity to continue to invest in a substantially larger Fund with similar investment policies; |

| • | shareholders will have the potential for economies of scale; |

| • | Deutsche Asset Management’s agreement to pay all costs associated with the merger; and |

| • | the merger would be a tax-free reorganization for the shareholders. |

The investment objective and policies of Dynamic Growth Fund are similar to those of Mid Cap Growth Fund.

Table of Contents

If the merger is approved, the Board expects that the proposed changes will take effect during the fourth calendar quarter of this year.

Included in this booklet is information about the upcoming shareholders’ meeting:

| • | A Notice of a Special Meeting of Shareholders, which summarizes the issue for which you are being asked to provide voting instructions; |

| • | A Prospectus/Proxy Statement, which provides detailed information on Mid Cap Growth Fund, the specific proposal being considered at the shareholders’ meeting, and why the proposal is being made. |

Whether or not you plan to be present at the meeting, we need your vote. We urge you to review the enclosed materials thoroughly. Once you’ve determined how you would like your interests to be represented, please promptly complete, sign, date and return the enclosed proxy card, vote by telephone or record your voting instructions on the Internet. A postage-paid envelope is enclosed for mailing, and telephone and Internet voting instructions are listed at the top of your proxy card.

I’m sure that you, like most people, lead a busy life and are tempted to put this proxy aside for another day. Please don’t. Your prompt return of the enclosed proxy card(s) (or your voting by telephone or through the Internet) may save the necessity and expense of further solicitations.

Your vote is important to us. We appreciate the time and consideration I am sure you will give this important matter. If you have questions about the proposal, please call Dynamic Growth Fund’s proxy solicitor at 1-888-288-5518 or contact your financial advisor. Thank you for your continued support of Scudder Investments.

Sincerely yours,

Julian F. Sluyters

Chief Executive Officer

Scudder Dynamic Growth Fund

ii

Table of Contents

NOTICE OF A SPECIAL MEETING OF SHAREHOLDERS

This is the formal agenda for your fund’s shareholder meeting. It tells you what matters will be voted on and the time and place of the meeting in the event you choose to attend in person.

To the Shareholders of Scudder Dynamic Growth Fund:

A Special Meeting of Shareholders of Scudder Dynamic Growth Fund (“Dynamic Growth Fund”) will be held on November 4, 2004 at 4:00 p.m. Eastern time at One South Street, Baltimore, Maryland 21202 (the “Meeting”), to consider the following (the “Proposal”):

| Proposal: | Approving an Agreement and Plan of Reorganization and the transactions it contemplates, including the transfer of all of the assets of Scudder Dynamic Growth Fund to Scudder Mid Cap Growth Fund in exchange for the issuance and delivery of shares of Scudder Mid Cap Growth Fund and the assumption by Scudder Mid Cap Growth Fund of all liabilities of Scudder Dynamic Growth Fund, and the distribution of such shares, on a tax-free basis, to the shareholders of Scudder Dynamic Growth Fund in complete termination and liquidation of Scudder Dynamic Growth Fund. |

The persons named as proxies will vote in their discretion on any other business that may properly come before the Meeting or any adjournments or postponements thereof.

Holders of record of shares of Dynamic Growth Fund at the close of business on August 18, 2004 are entitled to vote at the Meeting and at any adjournments or postponements thereof.

In the event that the necessary quorum to transact business or the vote required to approve the merger is not obtained at the Meeting, the persons named as proxies may propose one or more adjournments of the Meeting in accordance with applicable law to permit such further solicitation of proxies as may be deemed necessary or advisable. Any such adjournment as to a matter will require the affirmative vote of the holders of a majority of Dynamic Growth Fund’s shares present in person or by proxy at the Meeting. The persons named as proxies will vote FOR any such adjournment those proxies which they are entitled to vote in favor of the Proposal and will vote AGAINST any such adjournment those proxies to be voted against the Proposal.

By order of the Trustees

John Millette

Secretary

, 2004

WE URGE YOU TO MARK, SIGN, DATE AND MAIL THE ENCLOSED PROXY IN THE POSTAGE-PAID ENVELOPE PROVIDED OR RECORD YOUR VOTING INSTRUCTIONS BY TELEPHONE OR VIA THE INTERNET SO THAT YOU WILL BE REPRESENTED AT THE MEETING.

Table of Contents

INSTRUCTIONS FOR SIGNING PROXY CARDS

The following general rules for signing proxy cards may be of assistance to you and avoid the time and expense involved in validating your vote if you fail to sign your proxy card properly.

| 1. | Individual Accounts: Sign your name exactly as it appears in the registration on the proxy card. |

| 2. | Joint Accounts: Either party may sign, but the name of the party signing should conform exactly to the name shown in the registration on the proxy card. |

| 3. | All Other Accounts: The capacity of the individual signing the proxy card should be indicated unless it is reflected in the form of registration. For example: |

Registration | Valid Signature | |

Corporate Accounts | ||

(1) ABC Corp. | ABC Corp. John Doe, Treasurer | |

(2) ABC Corp. | John Doe, Treasurer | |

(3) ABC Corp. | John Doe | |

(4) ABC Corp. Profit Sharing Plan | John Doe, Trustee | |

Partnership Accounts | ||

(1) The XYZ Partnership | Jane B. Smith, Partner | |

(2) Smith and Jones, | Jane B. Smith, General Partner | |

Trust Accounts | ||

(1) ABC Trust Account | Jane B. Doe, Trustee | |

(2) Jane B. Doe, Trustee u/t/d 12/28/78 | Jane B. Doe | |

Custodial or Estate Accounts | ||

(1) John B. Smith, Cust. f/b/o John B. Smith Jr. UGMA/UTMA | John B. Smith | |

(2) Estate of John B. Smith | John B. Smith, Jr., Executor | |

Table of Contents

IMPORTANT INFORMATION

FOR SHAREHOLDERS OF

SCUDDER DYNAMIC GROWTH FUND

This document contains a prospectus/proxy statement and a proxy card. A proxy card is, in essence, a ballot. When you vote your proxy, it tells us how to vote on your behalf on an important issue relating to your fund. If you complete and sign the proxy (or tell us how you want to vote by voting by telephone or through the Internet), we’ll vote exactly as you tell us. If you simply sign the proxy, we’ll vote it in accordance with the Trustees’ recommendation on page .

We urge you to review the Prospectus/Proxy Statement carefully, and either fill out your proxy card and return it to us through the mail (in the postage paid envelope provided), vote by telephone or record your voting instructions through the Internet. You may receive more than one proxy card since several shareholder meetings are being held as part of the broader restructuring program of the Scudder fund family. If so, please vote each one. Your prompt return of the enclosed proxy card(s) (or voting by telephone or through the Internet) may save the necessity and expense of further solicitations.

We want to know how you would like to vote and welcome your comments. Please take a few minutes to read these materials and return your proxy to us.

Table of Contents

| Page | ||

| ii | ||

| iv | ||

| 1 | ||

| 3 | ||

| 9 | ||

| 16 | ||

| 17 | ||

| 24 | ||

Regulatory and Litigation Matters | 28 | |

| A-1 | ||

Proxy card enclosed.

If you have any questions, please call Georgeson Shareholder Communications Inc., Scudder Dynamic Growth Fund’s proxy solicitor, at 1-888-288-5518 or contact your financial advisor.

i

Table of Contents

, 2004

Acquisition of the assets of: | By and in exchange for shares of: | |

Scudder Dynamic Growth Fund a series of Scudder Dynamic Growth Fund | Scudder Mid Cap Growth Fund a series of Scudder Advisor Funds | |

222 S. Riverside Plaza Chicago, IL 60606 (617) 295-2572 | One South Street Baltimore, MD 21202 (410) 895-5000 | |

This Prospectus/Proxy Statement is being furnished in connection with the proposed merger of Scudder Dynamic Growth Fund (“Dynamic Growth Fund”) into Scudder Mid Cap Growth Fund (“Mid Cap Growth Fund”). Dynamic Growth Fund and Mid Cap Growth Fund are referred to in this Prospectus/Proxy Statement collectively as the “Funds,” and each is referred to herein individually as a “Fund.” As a result of the proposed merger, each shareholder of Dynamic Growth Fund will receive that number of full and fractional shares of the corresponding class of Mid Cap Growth Fund equal in aggregate value as of the date of the merger to the total value of such shareholder’s Dynamic Growth Fund shares.

This Prospectus/Proxy Statement is being mailed on or about September 7, 2004. It explains concisely what you should know before voting on the matter described in this Prospectus/Proxy Statement or investing in Mid Cap Growth Fund, a diversified series of an open-end management investment company. Please read it carefully and keep it for future reference.

The securities offered by this Prospectus/Proxy Statement have not been approved or disapproved by the SEC, nor has the SEC passed upon the accuracy or adequacy of this Prospectus/Proxy Statement. Any representation to the contrary is a criminal offense.

The following documents have been filed with the Securities and Exchange Commission (“SEC”) and are incorporated into this Prospectus/Proxy Statement by reference:

| • | Mid Cap Growth Fund’s Class A, B, C and R prospectus and Institutional Class prospectus, each dated February 1, 2004, each as supplemented from time to time, the applicable copy of which is included with this Prospectus/Proxy Statement; |

| • | Dynamic Growth Fund’s Class A, B and C prospectus dated December 1, 2003, and Institutional Class supplement dated December 1, 2003, each as supplemented from time to time; |

| • | The audited financial statements and related Independent Registered Public Accounting Firm’s report for Dynamic Growth Fund contained in the annual report for the fiscal year ended September 30, 2003 and financial statements contained in the semi-annual report for the semi-annual period ended March 31, |

1

Table of Contents

2004. Mid Cap Growth Fund’s annual report for the fiscal year ended September 30, 2003 and semi-annual report for the semi-annual period ended March 31, 2004. The semi-annual report of Mid Cap Growth Fund accompanies this Prospectus/Proxy Statement; and |

| • | the statement of additional information relating to the proposed merger, dated , 2004 (the “Merger SAI”). |

Shareholders may receive free copies of the Funds’ annual reports, either Fund’s Prospectuses or statements of additional information and/or the Merger SAI, request other information about a Fund, or make shareholder inquiries by contacting their financial advisor or by calling the corresponding Fund at the phone number listed above.

Like shares of Dynamic Growth Fund, shares of Mid Cap Growth Fund are not deposits or obligations of, or guaranteed or endorsed by, any financial institution, are not insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other agency, and involve risk, including the possible loss of the principal amount invested.

This document will give you the information you need to vote on the proposal. Much of the information is required disclosure under rules of the SEC; some of it is technical. If there is anything you don’t understand, please contact Georgeson Shareholder Communications Inc., Dynamic Growth Fund’s proxy solicitor, at 1-888-288-5518, or contact your financial advisor.

You may review and copy information about the Funds at the SEC’s public reference room at 450 Fifth Street, NW, Washington, D.C. You may call the SEC at 1-202-942-8090 for information about the operation of the public reference room. You may also review and copy information about the Funds at the SEC’s public reference facilities located at 233 Broadway, New York, NY (1-646-428-1500) and 175 W. Jackson Boulevard, Suite 900, Chicago, IL (1-312-353-7390). You may obtain copies of this information, with payment of a duplication fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Branch, Officer of Consumer Affairs and Information Services, Securities and Exchange Commission, Washington, D.C. 20549-0102. You may also access reports and other information about the Funds on the EDGAR database on the SEC’s Internet site at http://www.sec.gov.

2

Table of Contents

The responses to the questions that follow provide an overview of key points typically of concern to shareholders considering a proposed merger between mutual funds. These responses are qualified in their entirety by the remainder of this Prospectus/Proxy Statement, which you should read carefully because it contains additional information and further details regarding the proposed merger.

| What | is being proposed? |

The Trustees of Scudder Dynamic Growth Fund (the “Trust”), of which Dynamic Growth Fund is the sole series, are recommending that shareholders approve the transactions contemplated by the Agreement and Plan of Reorganization (as described below), which we refer to as a merger of Dynamic Growth Fund into Mid Cap Growth Fund. If approved by shareholders, all of the assets of Dynamic Growth Fund will be transferred to Mid Cap Growth Fund solely in exchange for the issuance and delivery to Dynamic Growth Fund of shares of Mid Cap Growth Fund (“Merger Shares”) with a value equal to the value of Dynamic Growth Fund’s assets net of liabilities and for the assumption by Mid Cap Growth Fund of all liabilities of Dynamic Growth Fund. Immediately following the transfer, the appropriate class of Merger Shares received by Dynamic Growth Fund will be distributed pro rata to each of its shareholders of record.

Deutsche Asset Management proposed this combination as part of its overall product rationalization program to reorganize and combine selected funds within the Scudder fund family. The Scudder fund family is made up of a group of funds that were managed by different investment advisors over the years and that have come together as a result of various corporate transactions that have taken place over time. As a result of these corporate transactions, there are a number of redundant funds within the Scudder fund family. In addition, the funds in the Scudder fund family do not currently have the same share class structure. Deutsche Asset Management’s overall program is designed to reorganize and combine funds in order to, among other reasons, eliminate redundant funds. Deutsche Asset Management’s program is also designed to expand product offerings across more share classes and adjust or eliminate share classes in order to implement the same share class structure across the Scudder fund family. Deutsche Asset Management believes this program may help enhance investment performance and increase the efficiency of its operations.

| What | will happen to my shares of Dynamic Growth Fund as a result of the merger? |

Your shares of Dynamic Growth Fund will, in effect, be exchanged on a tax-free basis for shares of the same class of Mid Cap Growth Fund with an equal aggregate net asset value on the date of the merger.

| Why | have the Trustees of the Trust recommended that I approve the merger? |

The Trustees considered the following factors in determining to recommend that shareholders of Dynamic Growth Fund approve the merger:

| • | Deutsche Asset Management’s overall program to reorganize and combine selected funds in the Scudder fund family as described above. |

| • | The merger offers Dynamic Growth Fund shareholders the opportunity to continue to invest in a substantially larger fund with similar investment policies. Deutsche Investment Management Americas Inc. (“DeIM”), Dynamic Growth |

3

Table of Contents

Fund’s investment advisor, has advised the Trustees that Dynamic Growth Fund and Mid Cap Growth Fund have similar investment objectives, policies and strategies. In addition, DeIM has advised the Trustees that both Funds have the same lead portfolio manager and two other portfolio managers in common. |

| • | The merger is intended to create a more streamlined line-up of Scudder funds, which Deutsche Asset Management believes may help enhance investment performance and increase the efficiency of Deutsche Asset Management’s operations. The merger may also result in greater cost efficiencies and the potential for economies of scale for the combined fund and its shareholders. |

| • | Deutsche Asset Management’s agreement to pay all costs associated with the merger. |

| • | The merger is structured as a tax-free reorganization for federal income tax purposes. Shareholders are not expected to recognize any gain or loss for federal income tax purposes directly as a result of the merger. |

[The Trustees of the Trust have concluded that: (1) the merger is in the best interests of Dynamic Growth Fund, and (2) the interests of the existing shareholders of Dynamic Growth Fund will not be diluted as a result of the merger. Accordingly, the Trustees [unanimously] recommend that shareholders approve the Agreement and Plan of Reorganization effecting the merger.]

How do the investment goals, policies and restrictions of the two Funds compare?

As noted and further described under “Investment Strategies and Risk Factors,” the investment objectives, policies and restrictions of the Funds are similar. The investment goal of Dynamic Growth Fund is maximum appreciation on investors’ capital. To pursue its investment goal, under normal market conditions, Dynamic Growth Fund invests at least 65% of its total assets in stocks whose market capitalizations are $8.5 billion or less. Dynamic Growth Fund seeks to invest in small to medium-sized companies that may benefit from technological advances, new marketing methods and economic and demographic changes.

The investment goal of Mid Cap Growth Fund is long-term capital growth. To pursue its investment goal, under normal market conditions, Mid Cap Growth Fund invests at least 80% of its assets, determined at the time of purchase, in companies with market caps within the market capitalization range of the Russell Mid Cap Growth Index ($1.3 to $13.25 billion as of June 30, 2004) or securities with equity characteristics that provide exposure to those companies. Mid Cap Growth Fund invests primarily in equity securities of medium-sized growth-oriented companies.

The most significant difference in the way the Funds are managed is that Mid Cap Growth Fund is required to invest at least 80% of its assets in mid cap companies, while Dynamic Growth Fund may invest in both small and mid cap companies as long as at least 65% of its assets are invested in stocks whose market capitalizations are $8.5 billion or less.

Please also see “Investment Strategies and Risk Factors” below for a more detailed comparison of the Funds’ investment policies and restrictions.

The following table sets forth a summary of the composition of the investment portfolio of each Fund as of March 31, 2004, and of Mid Cap Growth Fund on a pro forma combined basis, giving effect to the proposed merger:

4

Table of Contents

Portfolio Composition (March 31, 2004)

| Average Market Capitalization (000) | ||

Dynamic Growth Fund | 3,656 | |

Mid Cap Growth Fund | 3,515 | |

Mid Cap Growth Fund—Pro Forma Combined1 | 3,555 |

| 1 | Reflects the blended characteristics of Dynamic Growth Fund and Mid Cap Growth Fund as of March 31, 2004. The portfolio composition and characteristics of the merged fund will change consistent with its stated investment objectives and policies. |

How do the management fees and other expenses of the two Funds compare, and what are they estimated to be following the merger?

The following tables summarize the fees and expenses you may pay when investing in the Funds, the expenses that each Fund incurred for the twelve months ended March 31, 2004, and the pro forma expenses of Mid Cap Growth Fund assuming consummation of the merger and a new management fee schedule as of that date. The management fee for Dynamic Growth Fund is performance-based and payable at an annual rate of 0.65% of average daily net assets. The fee is then adjusted upward or downward by a maximum of 0.30% based upon the performance of the Fund’s Class A shares of beneficial interest compared with the performance of the S&P 500 Stock Index. The total adjusted fee on an annual basis can range from 0.35% to 0.95% of average daily net assets. The management fee for Mid Cap Growth Fund is 0.65% of average daily net assets for the first $500 million in assets, 0.625% of average daily net assets on the next $1 billion in assets, 0.60% of average daily net assets on the next $1 billion in assets, 0.55% of average daily net assets on the next $10 billion in assets and 0.51% of average daily net assets on assets exceeding $12.5 billion. Mid Cap Growth’s management fee does not include any adjustments based on performance. As a result, if the merger is approved, the resulting management fee will not have a performance fee adjustment. As shown below, the merger is expected to result in decreased total expenses for shareholders of both Funds. However, there can be no assurance that the merger will result in expense savings.

Shareholder Fees (fees paid directly from your investment)

| Class A | Class B | Class C | Institutional Class | ||||||||

Maximum Sales Charge (Load) | |||||||||||

Imposed on Purchases | |||||||||||

Dynamic Growth Fund | 5.75 | % | None | None | None | ||||||

Mid Cap Growth Fund | 5.75 | % | None | None | None | ||||||

Maximum Contingent Deferred Sales Charge (Load) (as a percentage of redemption proceeds) | |||||||||||

Dynamic Growth Fund | None1 | 4.00 | % | 1.00 | % | None | |||||

Mid Cap Growth Fund | None1 | 4.00 | % | 1.00 | % | None |

5

Table of Contents

Annual Fund Operating Expenses

(expenses that are deducted from Fund assets)

| Management Fees | Distribution/ (12b-1) Fees2 | Other Expenses3 | Total Operating | Less Expense Waiver/ Reimbursement | Net Annual Fund Operating Expenses | |||||||||||||

Dynamic Growth Fund | ||||||||||||||||||

Class A | 0.76 | % | 0.24 | % | 0.39 | % | 1.39 | % | 0.00 | %4 | 1.39 | %4 | ||||||

Class B | 0.76 | % | 0.98 | % | 0.91 | % | 2.65 | % | 0.16 | %4 | 2.49 | %4 | ||||||

Class C | 0.76 | % | 0.99 | % | 0.78 | % | 2.53 | % | 0.03 | %4 | 2.50 | %4 | ||||||

Institutional Class | 0.76 | % | None | 1.49 | % | 2.25 | % | 1.24 | 4 | 1.01 | %4 | |||||||

Mid Cap Growth Fund | ||||||||||||||||||

Class A | 0.65 | % | 0.25 | % | 0.43 | % | 1.33 | % | 0.08 | %5 | 1.25 | %5 | ||||||

Class B | 0.65 | % | 1.00 | % | 0.43 | % | 2.08 | % | 0.08 | %5 | 2.00 | %5 | ||||||

Class C | 0.65 | % | 1.00 | % | 0.43 | % | 2.08 | % | 0.08 | %5 | 2.00 | %5 | ||||||

Institutional Class | 0.65 | % | None | 0.43 | % | 1.08 | % | 0.08 | %5 | 1.00 | %5 | |||||||

Mid Cap Growth Fund (Pro forma combined) | ||||||||||||||||||

Class A | 0.64 | %6 | 0.25 | % | 0.44 | % | 1.33 | % | 0.08 | % | 1.25 | %7 | ||||||

Class B | 0.64 | %6 | 1.00 | % | 0.44 | % | 2.08 | % | 0.08 | % | 2.00 | %7 | ||||||

Class C | 0.64 | %6 | 1.00 | % | 0.44 | % | 2.08 | % | 0.08 | % | 2.00 | %7 | ||||||

Institutional Class | 0.64 | %6 | None | 0.44 | % | 1.08 | % | 0.08 | % | 1.00 | %7 |

| 1 | The redemption of shares purchased at net asset value under the Large Order NAV Purchase Privilege may be subject to a contingent deferred sales charge of 1.00% if redeemed within 12 months of purchase and 0.50% if redeemed within 12 to 18 months following purchase. Please see the applicable Fund’s Prospectus for more details. |

| 2 | Includes a shareholder servicing fee for Class B and C shares of up to 0.25%. |

| 3 | Restated and estimated to reflect the termination of the fixed administrative fee. |

| 4 | Through September 30, 2005, Dynamic Growth Fund’s investment advisor has contractually agreed to waive all or a portion of its management fee and reimburse or pay operating expenses of each Fund to the extent necessary to maintain total operating expenses at 1.50% for Class A, Class B and Class C shares and 1.00% for Institutional Class shares, excluding certain expenses such as Rule 12b-1 and/or service fees, extraordinary expenses, taxes, brokerage, interest and trustee and trustee counsel fees, and organizational and offering expenses. |

| 5 | Through , Mid Cap Growth Fund’s investment advisor and administrator have contractually agreed to waive their fees or reimburse expenses so that total operating expenses will not exceed 1.25% for Class A shares, 2.00% for Class B and C shares and 1.00% for Institutional Class shares. |

6

Table of Contents

| 6 | Subject to Board approval on August 8, 2004. |

| 7 | Through , 2007, Mid Cap Growth Fund’s investment advisor and administrator have contractually agreed to waive their fees or reimburse expenses so that total operating expenses will not exceed 1.00% for Class A, B, C and Institutional Class shares, excluding certain expenses such as Rule 12b-1 and/or service fees, extraordinary expenses, taxes, brokerage, interest and trustee and trustee counsel fees, and organizational and offering expenses. |

The tables are provided to help you understand the expenses of investing in the Funds and your share of the operating expenses that each Fund incurs and that Deutsche Asset Management, Inc. (“DeAM”) expects the combined Fund to incur in the first year following the merger.

Examples

These examples translate the expenses shown in the preceding table into dollar amounts. Based on the costs above, this examples help you compare the costs of investing in the Funds. The examples make certain assumptions. They assume that the expenses above remain the same. They also assume that you invest $10,000 in a Fund, earned 5% annual returns, and reinvested all dividends and distributions. This is only an example; actual expenses will be different.

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||

Dynamic Growth Fund | ||||||||||||

Class A | $ | 708 | $ | 989 | $ | 1,291 | $ | 2,146 | ||||

Class B* 1 | $ | 652 | $ | 1,108 | $ | 1,591 | $ | 2,380 | ||||

Class C* 1 | $ | 353 | $ | 783 | $ | 1,341 | $ | 2,859 | ||||

Institutional Class 1 | $ | 103 | $ | 584 | $ | 1,091 | $ | 2,488 | ||||

Class B** 1 | $ | 252 | $ | 808 | $ | 1,391 | $ | 2,380 | ||||

Class C** 1 | $ | 253 | $ | 783 | $ | 1,341 | $ | 2,859 | ||||

Mid Cap Growth Fund | ||||||||||||

Class A 1 | $ | 695 | $ | 966 | $ | 1,257 | $ | 2,083 | ||||

Class B* 1 | $ | 603 | $ | 945 | $ | 1,313 | $ | 2,041 | ||||

Class C* 1 | $ | 303 | $ | 645 | $ | 1,113 | $ | 2,409 | ||||

Institutional Class 1 | $ | 102 | $ | 337 | $ | 590 | $ | 1,315 | ||||

Class B** 1 | $ | 203 | $ | 645 | $ | 1,113 | $ | 2,041 | ||||

Class C** 1 | $ | 203 | $ | 645 | $ | 1,113 | $ | 2,409 | ||||

Mid Cap Growth Fund (Pro forma combined) | ||||||||||||

Class A 2 | �� | $ | 695 | $ | 950 | $ | 1,240 | $ | 2,065 | |||

Class B* 2 | $ | 603 | $ | 928 | $ | 1,296 | $ | 2,023 | ||||

Class C* 2 | $ | 303 | $ | 628 | $ | 1,096 | $ | 2,391 | ||||

Institutional Class 2 | $ | 102 | $ | 319 | $ | 572 | $ | 1,297 | ||||

Class B** 2 | $ | 203 | $ | 628 | $ | 1,096 | $ | 2,023 | ||||

Class C** 2 | $ | 203 | $ | 628 | $ | 1,096 | $ | 2,391 | ||||

| (1) | Includes one year of capped expenses in each period. |

| (2) | Includes three years of capped expenses in each period. |

| * | Assumes you sold your shares at the end of each period. |

| ** | Assumes you kept your shares. |

7

Table of Contents

What are the federal income tax consequences of the proposed merger?

For federal income tax purposes, generally no gain or loss is expected to be recognized by Dynamic Growth Fund or its shareholders as a direct result of the merger. For a discussion of taxes that you may incur indirectly as a result of the merger (e.g., due to differences in the Funds’ portfolio turnover rates and net investment income), please see “Information about the Proposed Merger — Federal Income Tax Consequences” below.

Will my dividends be affected by the merger?

The merger will not result in a change in dividend policy.

Do the procedures for purchasing, redeeming and exchanging shares of the two Funds differ?

The procedures for purchasing and redeeming Class A, B and C shares of each Fund, and for exchanging shares of each Fund for shares of other Scudder funds, are identical. The investment minimum for Mid Cap Growth Fund’s Institutional Class shares is $1 million. This investment minimum will be waived for all existing Dynamic Growth Fund Institutional Class shareholders. Institutional Class shareholders of Dynamic Growth Fund may only exchange their shares for (i) shares of Scudder Money Funds—Scudder Money Market Fund if they have purchased shares because they are participants in tax-exempt retirement plans of DeIM and its affiliates and (ii) Institutional Class shares of other Scudder funds, while Institutional Class shareholders of Mid Cap Growth Fund do not have these restrictions on exchanges.

How will I be notified of the outcome of the merger?

If the proposed merger is approved by shareholders, you will receive confirmation after the reorganization is completed, indicating your new account number, the number of Merger Shares you are receiving and the procedures for surrendering your certificates, if you have any. Otherwise, you will be notified in the next annual report of Dynamic Growth Fund.

Will the number of shares I own change?

The number of shares you own will most likely change, but the total value of the shares of Mid Cap Growth Fund you receive will equal the total value of the shares of

8

Table of Contents

Dynamic Growth Fund that you hold at the time of the merger. Even though the net asset value per share of each Fund is likely to be different, the total value of each shareholder’s holdings will not change as a result of the merger.

What percentage of shareholders’ votes is required to approve the merger?

Approval of the merger will require the “yes” vote of the holders of a majority of the outstanding shares of Dynamic Growth Fund.

The Trustees of the Trust believe that the proposed merger is in the best interests of Dynamic Growth Fund. Accordingly, the Trustees [unanimously] recommend that shareholders vote “FOR” approval of the proposed merger.

INVESTMENT STRATEGIES AND RISK FACTORS

What are the main investment strategies and related risks of Dynamic Growth Fund and how do they compare with those of Mid Cap Growth Fund?

Investment Objectives and Strategies. Dynamic Growth Fund and Mid Cap Growth Fund have similar investment objectives, policies and restrictions. Both Funds are managed by the same lead portfolio manager and have two other portfolio managers in common. The investment goal of Dynamic Growth Fund is maximum appreciation on investors’ capital. To pursue its investment goal, under normal market conditions, Dynamic Growth Fund invests at least 65% of its total assets in stocks whose market capitalizations are $8.5 billion or less. Dynamic Growth Fund seeks to invest in small to medium-sized companies that may benefit from technological advances, new marketing methods and economic and demographic changes.

The investment goal of Mid Cap Growth Fund is long-term capital growth. To pursue its investment goal, under normal market conditions, Mid Cap Growth Fund invests at least 80% of its total assets, determined at the time of purchase, in companies with market caps within the market capitalization range of the Russell Mid Cap Growth Index or securities with equity characteristics that provide exposure to those companies. Mid Cap Growth Fund invests primarily in equity securities of medium-sized growth-oriented companies.

The Funds have each adopted certain fundamental and non-fundamental investment policies. Each Fund has substantially similar investment policies. Each Fund may invest in foreign securities. Dynamic Growth Fund may invest up to 25% of its total assets in foreign securities, but Mid Cap Growth may only invest up to 20% of its total assets in foreign securities.

The most significant difference in the way the Funds are managed is that Mid Cap Growth Fund is required to invest at least 80% of its assets in mid cap companies, while Dynamic Growth Fund may invest in both small and mid cap companies as long as at least 65% of its assets are invested in stocks whose market capitalizations are $8.5 billion or less.

For a more detailed description of the investment techniques used by the Dynamic Growth Fund and the Mid Cap Growth Fund, please see each Fund’s Prospectus and SAI.

9

Table of Contents

Primary Risks.

Mid Cap Growth Fund

As with any stock mutual fund, you may lose money by investing in Mid Cap Growth Fund. Certain risks associated with an investment in Mid Cap Growth Fund are summarized below. Subject to limited exceptions, the risks of an investment in Mid Cap Growth Fund are substantially similar to the risks of an investment in Dynamic Growth Fund. More detailed descriptions of the risks associated with an investment in Mid Cap Growth Fund can be found in the Fund’s Prospectus and SAI.

The value of your investment in Mid Cap Growth Fund will change with changes in the values of the investments held by Mid Cap Growth Fund. A wide array of factors can affect those values. In this summary, we describe the principal risks that may affect Mid Cap Growth Fund’s investments as a whole. Mid Cap Growth Fund could be subject to additional principal risks because the types of investments it makes can change over time.

There are several risk factors that could hurt Mid Cap Growth Fund’s performance, cause you to lose money or cause Mid Cap Growth Fund’s performance to trail that of other investments.

Stock Market Risk. As with most stock funds, one of the most important factors with Mid Cap Growth Fund is how stock markets perform – in this case, the medium-sized capitalization portion of the US stock market. When stock prices fall, you should expect the value of your investment to fall as well. Because a stock represents ownership in its issuer, stock prices can be hurt by poor management, shrinking product demand and other business risks. These may affect single companies as well as groups of companies. In addition, movements in financial markets may adversely affect a stock’s price regardless of how well the company performs. The market as a whole may not favor the types of investments the Fund makes and the Fund may not be able to get an attractive price for them.

Security Selection Risk. A risk that pervades all investing is the risk that the securities the managers have selected will not perform to expectations. The managers could be incorrect in their analysis of companies, sectors, economic trends or other matters.

Medium-Sized Company Risk. Medium-sized company stocks tend to experience steeper price fluctuations—down as well as up—than stocks of larger companies. A shortage of reliable information—the same information gap that creates opportunity—can also pose added risk. Industry-wide reversals may have a greater impact on medium-sized companies, since they lack a large company’s financial resources. Medium-sized company stocks are typically less liquid than large company stocks: when things are going poorly, it is harder to find a buyer for a medium-sized company’s shares.

Foreign Securities Risk. Foreign securities may be more volatile than their US counterparts, for reasons such as currency fluctuations and political and economic uncertainty.

10

Table of Contents

Pricing Risk. At times, market conditions might make it hard to value some investments. For example, if the Fund has valued its securities too highly, you may end up paying too much for Fund shares when you buy into the Fund. If the Fund underestimates the prices of its securities, you may not receive the full value for your Fund shares when you sell.

Securities Lending Risk. Any loss in the market price of securities loaned by the Fund that occurs during the term of the loan would be borne by the Fund and would adversely affect the Fund’s performance. Also, there may be delays in recovery of securities loaned or even a loss of rights in the collateral should the borrower of the securities fail financially while the loan is outstanding. However, loans will be made only to borrowers selected by the Fund’s delegate after a review of relevant facts and circumstances, including the creditworthiness of the borrower.

Another factor that could affect performance:

| • | derivatives risk—derivatives could produce disproportionate losses due to a variety of factors, including the unwillingness or inability of the counterparty to meet its obligations or unexpected price as interest rate movements. |

Dynamic Growth Fund

In addition to stock market risk described above, Dynamic Growth Fund also has as its principal risk factors growth investing risk and industry risk.

Growth Investing Risk. Since growth companies usually reinvest a large portion of earnings in their own businesses, growth stocks may lack the dividends associated with value stocks that might otherwise cushion their decline in a falling market. Earnings disappointments in growth stocks often result in sharp price declines because investors buy these stocks because of their potential for superior earnings growth. Growth stocks may also be out of favor for certain periods in relation to value stocks.

Industry Risk. While the Fund does not concentrate in any industry, to the extent that the Fund has exposure to a given industry or sector, any factors affecting that industry or sector could affect the value of portfolio securities. For example, manufacturers of consumer goods could be hurt by a rise in unemployment, or technology companies could be hurt by such factors as market saturation, price competition and rapid obsolescence.

Other factors that could affect the Fund’s performance include:

| • | the managers could be incorrect in their analysis of industries, companies, economic trends, the relative attractiveness of different sizes of stocks, geographical trends or other factors |

| • | foreign securities risk (see above) |

| • | derivatives risk (see above) |

Performance Information. The following information provides some indication of the risks of investing in the Funds. The bar charts show year-to-year changes in Fund performance. The table following the charts compares the Funds’ performance to each other’s and to that of a broad measure of market performance.

11

Table of Contents

The bar charts show how the performance for each Fund’s Class A shares has varied from year to year, which may give some idea of risk. The bar charts do not reflect sales loads; if they did, total returns would be lower. The table shows how each Fund’s performance compares with a broad-based market index (which, unlike a Fund, does not have any fees or expenses). The performance of the Dynamic Growth Fund is compared to the Russell Mid Cap Growth Index and the performance of the Mid Cap Growth Fund is compared to the S&P Mid Cap 400 Index and to the Russell Mid Cap Growth Index. The table includes the effects of maximum sales loads. The performance of the Funds and the indexes varies over time. All figures assume reinvestment of dividends and distributions (in the case of after-tax returns, reinvested net of assumed tax rates.) For Mid Cap Growth Fund, the inception date for Class A, B and C shares was June 28, 2002. The performance figures for Class A, B and C shares before their inception date are based on the historical performance of the fund’s original share class (Investment Class), adjusted to reflect both the higher gross total annual operating expenses and current applicable sales charges of Classes A, B and C. For Dynamic Growth Fund, the inception date for Class B and C shares is May 31, 1994. Performance figures for periods prior to that date are based on the historical performance of the Fund’s original share class (Class A), adjusted to reflect the higher gross total annual operating expenses and the current applicable sales charges of Classes B and C. The table shows returns on a before-tax and after-tax basis. After-tax returns are shown for Class A only and will vary for other classes. After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s situation and may differ from those shown in the table.

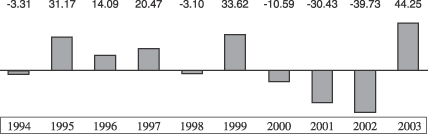

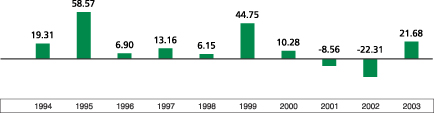

Calendar Year Total Returns for Class A Shares

Dynamic Growth Fund*

| * | On October 15, 2001, the fund changed its name from Scudder Small Capitalization Equity Fund to Scudder Dynamic Growth Fund. At the same time, the fund changed its investment strategy to invest at least 65% of total assets in companies whose market capitalizations are $8.5 billion or less. Previously, the fund invested at least 65% of total assets in small capitalization stocks similar in size to those comprising the Russell 2000 Index. Consequently, the fund’s performance prior to that date may have been different if the current investment strategy had been in place. |

For the periods included in the chart:

Best Quarter: 32.09%; Q4 1999

Worst Quarter: –32.96%, Q3 2001

12

Table of Contents

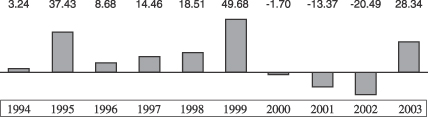

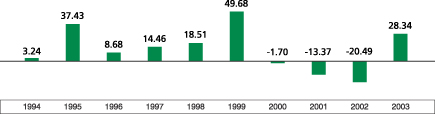

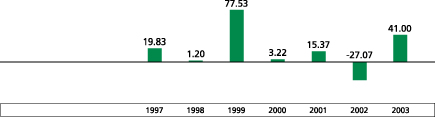

Mid Cap Growth Fund

For the periods included in the chart:

Best Quarter: 29.95%; Q4 1999

Worst Quarter: –19.58%, Q3 1998

Class A year-to-date performance through June 30, 2004 was -1.84% for Dynamic Growth Fund and 0.48% for Mid Cap Growth Fund.

Average Annual Total Returns (for periods ending 12/31/03)

| 1 year | 5 years | 10 years or since inception* | |||||||

Dynamic Growth Fund | |||||||||

Class A (Return before Taxes) | 35.95 | % | –7.39 | % | 1.41 | % | |||

Class A (Return after Taxes on Distributions) | 35.95 | % | –8.57 | % | –0.74 | % | |||

Class A (Return after Taxes on Distributions and Sale of Fund Shares) | 23.37 | % | –6.11 | % | 0.57 | % | |||

Class B (Return before Taxes) | 40.08 | % | –7.41 | % | 0.89 | % | |||

Class C (Return before Taxes) | 43.00 | % | –7.00 | % | 1.12 | % | |||

Institutional Class | 44.96 | % | –5.78 | % | 1.54 | % | |||

Index** (Reflects no deductions for fees, expenses or taxes) | 42.71 | % | 2.01 | % | 9.40 | % | |||

Mid Cap Growth Fund | |||||||||

Class A (Return before Taxes) | 20.96 | % | 4.16 | % | 9.87 | % | |||

Class A (Return after Taxes on Distributions) | 20.96 | % | –4.06 | % | –2.05 | % | |||

Class A (Return after Taxes on Distributions and Sale of Fund Shares) | 11.61 | % | –3.98 | % | –2.16 | % | |||

Class B (Return before Taxes) | 24.42 | % | 4.26 | % | 9.47 | % | |||

Class C (Return before Taxes) | 27.42 | % | 4.43 | % | 9.47 | % | |||

Institutional Class (Return before Taxes)*** | 28.67 | % | 5.66 | % | 10.82 | % | |||

Index**** (Reflects no deductions for fees, | 35.62 | % | 9.21 | % | 13.93 | % | |||

Index** (Reflects no deductions for fees, | 42.71 | % | 2.01 | % | 9.40 | % |

| * | Institutional Class of Dynamic Growth Fund commenced operations on July 3, 1995. Index comparison begins on June 20, 1995. Institutional Class shares are not subject to a sales charge. |

13

Table of Contents

| ** | The Russell Mid Cap Growth Index is an unmanaged capitalization-weighted index of medium and medium/small companies in the Russell Index chosen for their growth orientation. Effective on or about August 20, 2004, the Russell Mid Cap Growth Index replaced the S&P Mid Cap 400 Index as Mid Cap Growth Fund’s benchmark index because the advisor believes that it is more appropriate to measure the fund’s performance against the Russell Mid Cap Growth Index as it more accurately reflects the fund’s investment strategy. |

| *** | As of the close of business on August 31, 2000, Scudder Equity Appreciation Fund—Institutional Class became Scudder Mid Cap Fund—Institutional Class. Scudder Equity Appreciation Fund—Institutional Class was managed by the same investment management team with the same objective, policies and strategies as Scudder Mid Cap Fund. Performance for the period prior to August 31, 2000 reflects the performance of Scudder Equity Appreciation Fund—Institutional Class. |

| **** | The S&P Mid Cap 400 Index is an unmanaged index that tracks the stock movement of 400 mid-sized companies. |

Current performance may be higher or lower than the performance data quoted above. For more recent performance information, call your financial representative or call (800) 621-1048 or visit the Scudder website at www.scudder.com.

14

Table of Contents

Capitalization. The following table shows the capitalization of each Fund as of March 31, 2004, and of the Mid Cap Growth Fund on a pro forma combined basis, giving effect to the proposed acquisition of assets at net asset value as of that date1:

| (Unaudited) | |||||||||||||

| Scudder Mid Cap Growth Fund | Scudder Dynamic Growth Fund | Pro Forma Adjustments | Pro Forma Combined | ||||||||||

Net Assets | |||||||||||||

Class A | $ | 251,208,765 | $ | 223,858,184 | $ | $ | 475,066,949 | ||||||

Class B | 9,098,577 | 32,679,806 | 41,778,383 | ||||||||||

Class C | 7,617,266 | 10,617,849 | 18,235,115 | ||||||||||

Class I2 | — | 240,120 | (240,120 | ) | — | ||||||||

Investment Class | 43,174,425 | — | 43,174,425 | ||||||||||

Class R | 319,093 | — | 319,093 | ||||||||||

Institutional Class | 358,692,630 | — | 240,120 | 358,932,750 | |||||||||

Total Net Assets | $ | 670,110,756 | $ | 267,395,959 | $ | — | $ | 937,506,715 | |||||

Shares Outstanding | |||||||||||||

Class A | 19,937,440 | 68,926,673 | (51,160,150 | ) | 37,703,963 | ||||||||

Class B | 731,900 | 11,775,386 | (9,146,279 | ) | 3,361,007 | ||||||||

Class C | 612,778 | 3,740,624 | (2,886,412 | ) | 1,466,990 | ||||||||

Class I | — | 69,730 | (69,730 | ) | — | ||||||||

Investment Class | 3,425,192 | — | 3,425,192 | ||||||||||

Class R | 25,349 | — | 25,349 | ||||||||||

Institutional Class | 28,202,197 | — | 18,877 | 28,221,074 | |||||||||

Net Asset Value per Share | |||||||||||||

Class A | $ | 12.60 | $ | 3.25 | $ | 12.60 | |||||||

Class B | $ | 12.43 | $ | 2.78 | $ | 12.43 | |||||||

Class C | $ | 12.43 | $ | 2.84 | $ | 12.43 | |||||||

Class I | $ | — | $ | 3.44 | $ | — | |||||||

Investment Class | $ | 12.60 | $ | — | $ | 12.60 | |||||||

Class R | $ | 12.59 | $ | — | $ | 12.59 | |||||||

Institutional Class | $ | 12.72 | $ | — | $ | 12.72 | |||||||

| 1) | Assumes the Reorganization had been consummated on March 31, 2004, and is for information purposes only. No assurance can be given as to how many shares of the Scudder Mid Cap Growth Fund will be received by the shareholders of the Scudder Dynamic Growth Fund on the date the Reorganization takes place, and the foregoing should not be relied upon to reflect the number of shares of the Scudder Mid Cap Growth Fund that actually will be received on or after such date. |

| 2) | The “Class I” shares of Dynamic Growth Fund were renamed “Institutional Class” shares on August 13, 2004. |

Unaudited pro forma combined financial statements of the Funds as of March 31, 2004, and for the twelve-month period then ended, are included in the Merger SAI. Because the Agreement provides that Mid Cap Growth Fund will be the surviving Fund following the merger and because Mid Cap Growth Fund’s investment objective and policies will remain unchanged, the pro forma combining financial statements reflect the transfer of the assets and liabilities of Dynamic Growth Fund to Mid Cap Growth

15

Table of Contents

Fund as contemplated by the Agreement and Plan of Reorganization between the Funds, dated as of , 2004 (the “Agreement”).

OTHER COMPARISONS BETWEEN THE FUNDS

Investment advisors. DeAM is the investment advisor for Mid Cap Growth Fund and DeIM is the investment advisor for Dynamic Growth Fund. Each advisor makes investment decisions for the applicable Fund, buys and sells securities for the Fund and conducts the research that leads to the purchase and sale decisions. Each advisor is a wholly owned subsidiary of Deutsche Bank AG. Deutsche Bank AG is a major global banking institution that is engaged in a wide range of financial services, including investment management, mutual fund, retail, private and commercial banking, investment banking and insurance. The Funds have the same lead portfolio manager and two other portfolio managers in common.

The management fee for Dynamic Growth Fund is performance-based and payable at an annual rate of 0.65% of average daily net assets. The fee is then adjusted upward or downward by a maximum of 0.30% based upon the performance of the Fund’s Class A shares of beneficial interest compared with the performance of the S&P 500 Stock Index. The total adjusted fee on an annual basis can range from 0.35% to 0.95% of average daily net assets. The management fee for Mid Cap Growth Fund is 0.65% of average daily net assets on the first $500 million in assets, 0.625% of average daily net assets on the next $1 billion in assets, 0.60% of average daily net assets on the next $1 billion in assets, 0.55% of average daily net assets on the next $10 billion in assets and 0.51% of average daily net assets on assets exceeding $12.5 billion. Mid Cap Growth Fund’s management fee does not include any adjustments based on performance. If the merger is approved, the resulting management fee will not have a performance fee adjustment.

Distribution and Service Fees. Pursuant to separate Underwriting and Distribution Services Agreements, Scudder Distributors, Inc. (“SDI”), 222 South Riverside Plaza, Chicago, Illinois 60606, an affiliate of each Fund’s investment advisor, is the principal underwriter and distributor for the Class A, Class B and Class C shares of each Fund and acts as agent of each Fund in the continuing offer of such shares. Mid Cap Growth Fund has adopted distribution plans on behalf of the Class A, B and C shares in accordance with Rule 12b-1 under the Investment Company Act of 1940, as amended (the “1940 Act”), that are substantially similar to the distribution plans for Class B and C shares, and the service plan for Class A shares of Dynamic Growth Fund.

Pursuant to the Services Agreement with Mid Cap Growth Fund, which is substantially identical to the services agreement for Class B and C shares of Dynamic Growth Fund, SDI receives a shareholder services fee of up to 0.25% per year with respect to the Class A, B and C shares of Mid Cap Growth Fund. SDI uses the fee to compensate financial services firms for providing personal services and maintaining accounts for their customers that hold these classes of shares of Mid Cap Growth Fund, and may retain any portion of the fee not paid to such firms to compensate itself for administrative functions performed for the Fund. All amounts are payable monthly and are based on the average daily net assets of each Fund attributable to the relevant class of shares. Mid Cap Growth Fund’s 12b-1 and service fee structure will remain in effect following the merger.

16

Table of Contents

Trustees and Officers. The Trustees of the Trust are different from those of Scudder Advisor Funds, of which Mid Cap Growth Fund is a series. As described in the Mid Cap Growth Fund’s SAI, which is available upon request, the following individuals comprise the Board of Trustees of Scudder Advisor Funds:

Richard R. Burt

S. Leland Dill

Martin J. Gruber

Joseph R. Hardiman

Richard J. Herring

Graham E. Jones

Rebecca W. Rimel

Philip Saunders, Jr.

William N. Searcy

Robert H. Wadsworth

In addition, certain officers of Dynamic Growth Fund are different from those of Mid Cap Growth Fund.

Service Providers. State Street Bank and Trust Company (“SSB”) serves as the custodian for both Funds. Scudder Investments Service Company (“SISC”) serves as transfer agent for Mid Cap Growth, and although SSB serves as Dynamic Growth Fund’s transfer agent, SSB has contracted with SISC to perform all of SSB’s duties as transfer agent. The Investment Company Capital Corporation is the administrator for Mid Cap Growth Fund, while SDI serves as the administrator for Dynamic Growth Fund. Dynamic Growth Fund’s Independent Registered Public Accounting Firm is Ernst & Young LLP and Mid Cap Growth Fund’s Independent Registered Public Accounting Firm is PricewaterhouseCoopers LLP.

Fund Accounting Fees. For Mid Cap Growth Fund, the fund accounting fees are paid by the administrator from the fees collected in the administration fee. For Dynamic Growth Fund, its advisor pays the fund accounting costs from fees collected in the management fee. If the merger is approved, fund accounting fees will continue to be paid by the administrator out of fees collected from the administration fee.

Charter Documents. Each Fund is a series of a Massachusetts business trust. There are no significant differences between the Fund’s organizational documents with respect to the rights of shareholders contained therein.

INFORMATION ABOUT THE PROPOSED MERGER

General. The shareholders of Dynamic Growth Fund are being asked to approve a merger between Dynamic Growth Fund and Mid Cap Growth Fund pursuant to the Agreement, a copy of which is attached to this Prospectus/Proxy Statement as Appendix A.

The merger is structured as a transfer of all of the assets of Dynamic Growth Fund to Mid Cap Growth Fund in exchange for the assumption by Mid Cap Growth Fund of all of the liabilities of Dynamic Growth Fund and for the issuance and delivery to Dynamic Growth Fund of Merger Shares of Mid Cap Growth Fund equal in aggregate value to the net value of the assets transferred to Mid Cap Growth Fund.

17

Table of Contents

After receipt of the Merger Shares, Dynamic Growth Fund will distribute them to its shareholders, in proportion to their existing shareholdings, in complete liquidation of Dynamic Growth Fund, and the legal existence of Dynamic Growth Fund as a series and as a trust will be terminated. Each shareholder of Dynamic Growth Fund will receive a number of full and fractional Merger Shares of the same class(es) as, and equal in value at the date of the exchange to the aggregate value of, the shareholder’s Dynamic Growth Fund shares.

Prior to the date of the transfer, Dynamic Growth Fund will declare a distribution to shareholders which, together with all previous distributions, will have the effect of distributing to shareholders all of its investment company income (computed without regard to the deduction for dividends paid) and net realized capital gains, if any, through the date of the transfer.

The Trustees of the Trust have voted [unanimously] to approve the Agreement and the proposed merger and to recommend that shareholders also approve the merger. The actions contemplated by the Agreement and the related matters described therein will be consummated only if approved by the affirmative vote of a majority of the outstanding voting securities of Dynamic Growth Fund.

In the event that the merger does not receive the required shareholder approval, Dynamic Growth Fund will continue to be managed as a separate Fund in accordance with its current investment objective and policies, and the Trustees of the Trust may consider such alternatives as may be in the best interests of the Fund’s shareholders.

Background and Trustees’ Considerations Relating to the Proposed Merger. Deutsche Asset Management discussed the proposed merger with the Trustees of the Trust at a meeting held on February 13, 2004. The merger was presented to the Trustees and considered by them as part of a broader program initiated by Deutsche Asset Management to consolidate its mutual fund lineup. This initiative includes the following major components:

| (i) | The merger of selected funds within the Scudder fund family having similar investment objectives and policies; |

| (ii) | The liquidation of certain small funds which have not achieved market acceptance and which are unlikely to reach an efficient operating size; and |

| (iii) | The creation of new classes of shares of each fund into which a Scudder fund is merging in order to allow current Scudder fund shareholders to continue holding a class of shares with similar rights, privileges and expense structures as they currently possess. |

The Trustees of the Trust, including all Trustees who are not “interested persons” of the Fund (as defined by the 1940 Act), conducted a thorough review of the potential implications of this program for Dynamic Growth Fund as well as the various other funds for which they serve as trustees or directors. They were assisted in this review by their independent legal counsel. Following the February 13, 2004 meeting, the Trustees met on several occasions to review and discuss this program both among themselves and with representatives of Deutsche Asset Management. In the course of their review, the Trustees requested and received substantial additional information and suggested numerous changes to Deutsche Asset Management’s program, many of which were accepted.

18

Table of Contents

Following the conclusion of this process, the Trustees of the Trust, the independent trustees/directors of other funds involved and Deutsche Asset Management reached general agreement on the elements of a restructuring plan as it affects shareholders of various funds and, where required, agreed to submit elements of the plan for approval to shareholders of those funds.

[On August , 2004, the Trustees of the Trust, including [all] Trustees who are not “interested persons” of the Fund (as defined by the 1940 Act), approved the terms of the merger. The Trustees also [unanimously] agreed to recommend that the merger be approved by the Fund’s shareholders. In making this determination, the Trustees examined all factors that they considered relevant, including information regarding comparative expense ratios, management fees and the tax consequences of the merger to Dynamic Growth Fund and its shareholders.

In determining to recommend that the shareholders of Dynamic Growth Fund approve the merger, the Trustees considered, among other factors: (a) the fees and expense ratios of the Funds, including comparisons between the expenses of Dynamic Growth Fund and the estimated operating expense ratio of the combined Fund, and between the estimated operating expense ratio of the combined Fund and other mutual funds with similar investment objectives, and in particular noted that the combined Fund’s total operating expense ratio was anticipated to be lower than that of Dynamic Growth Fund currently; (b) the terms and conditions of the merger and whether the merger would result in the dilution of shareholder interests; (c) the compatibility of Dynamic Growth Fund’s and Mid Cap Growth Fund’s investment objectives, policies, restrictions and portfolios; (d) that the service features available to shareholders of each Fund were identical on a class level; (e) the costs to be borne by the combined Fund and DeAM as a result of the merger, and in particular that DeAM would bear all costs of the merger; (f) prospects for the combined Fund to attract additional assets; (g) the tax consequences of the merger on Dynamic Growth Fund and its shareholders and, in particular, that the merger would be a tax-free reorganization; and (h) the respective investment performances of the two Funds.

The Trustees also gave consideration to possible economies of scale that might be realized from the merger. The Trustees considered the impact of the merger on the total expenses to be borne by shareholders of Dynamic Growth Fund. The Trustees also considered that the merger would permit the shareholders of Dynamic Growth Fund to continue to pursue similar investment goals in a larger fund.

The Trustees also considered that the Dynamic Growth Fund has a management fee with a performance fee adjustment and that the Mid Cap Growth Fund does not. The Trustees noted that currently the base management fee for the Dynamic Growth Fund is the same as the current management fee for the Mid Cap Growth Fund, but that DeAM had agreed to add break-points to the management fee schedule of the Mid Cap Growth Fund for the two years following the merger. The Trustees also noted that the combined Fund will have a management fee with the same base as that of the Dynamic Growth Fund but that the management fee rate of the combined Fund will decline as assets of the Fund grow. Accordingly, the Trustees noted that while the Dynamic Growth Fund’s management fee decreased when the Dynamic Growth Fund underperformed the S&P 500 Stock Index, the combined Fund’s management fee will decrease as assets grow. The Trustees considered that the management fee of the combined Fund will generally be the same as that of the Dynamic Growth Fund when the Fund performs in line with

19

Table of Contents

the S&P 500 Stock Index. However, assuming the current level of assets of the combined Fund, the management fee of the combined Fund will generally be lower than that of the Dynamic Growth Fund when the Fund outperforms the S&P 500 Stock Index and will generally be higher than that of the Dynamic Growth Fund when the Fund underperforms the S&P 500 Stock Index.

The Trustees also considered the potential tax consequences to shareholders as a result of differences in the Funds’ realized or unrealized capital gains or losses and capital loss carry-forwards. Although the merger will be achieved on a federally tax-free basis (see “Federal Income Tax Consequences”), there are differences in the Funds’ unrealized gains or losses, tax loss carryovers and portfolio turnover rates which may affect the timing and amount of any future capital gain distributions paid to shareholders.

6/30/04 Gain (Loss) | 6/30/04 Unrealized Gain (Loss) as % of 6/30/04 Net Assets | 6/30/04 Loss Carryovers | 6/30/04 Loss Carryovers as % of 6/30/04 Net Assets | 6/30/04 Portfolio Turnover Rate | ||||||||||

Dynamic Growth Fund | $ | 35,424,782 | 14 | % | $ | 318,660,000 | 11 | % | % | |||||

Mid Cap Growth Fund | $ | 112,258,164 | 17 | % | $ | 70,496,000 | 127 | % | % | |||||

The Dynamic Growth Fund’s capital loss carryovers are larger than the Fund, and the Fund is losing assets, thus making it unlikely that the Fund’s carryovers will be able to be used in their entirety before they expire. To the extent it is prudent from an investment perspective, DeAM intends to realize gains in the Dynamic Growth Fund prior to the merger and apply capital loss carryovers against them for the benefit of current shareholders.

After the merger, the Dynamic Growth Fund’s capital loss carryovers will be available to Mid Cap Growth Fund to offset its capital gains, although the amount of these losses which may offset Mid Cap Growth Fund’s capital gains in any given year may be limited. As a result of this limitation, it is possible that Mid Cap Growth Fund may not be able to use these losses as rapidly as the Dynamic Growth Fund might have, and part or all of these losses may not be usable at all. The ability of Mid Cap Growth Fund or the Dynamic Growth Fund to absorb losses in the future depends on a variety of factors that cannot be known in advance, including the existence of capital gains against which these losses may be offset. Net capital losses of regulated investment companies generally expire at the end of the eighth taxable year after they arise, if not previously absorbed by that time; therefore, it is possible that some or all of these losses will expire unused. In addition, the benefits of any capital loss carryovers currently are available only to the shareholders of each Fund respectively. After the merger, however, these benefits will inure to all the shareholders of Mid Cap Growth Fund.

The Trustees considered the possibility that shareholders of the Dynamic Growth Fund in taxable accounts could incur indirect costs as a result of future capital gain distributions or the loss of current tax loss carryovers (shareholders in tax deferred retirement accounts are not affected). They concluded that such future tax

20

Table of Contents

consequences are not quantifiable or predictable due to uncertainties as to the amount of any actual future realization of capital gains or losses in view of future changes in portfolio values, and the differing consequences of future capital gain distributions to each shareholder whose tax liability (if any) is determined by the net effect of a multitude of considerations that are individual to that shareholder. Shareholders should, however, review their own tax situation to determine what potential effect, if any, the tax differences shown above may have on them.

Based on all of the foregoing, the Trustees concluded that Dynamic Growth Fund’s participation in the merger would be in the best interests of the Fund and would not dilute the interests of the Fund’s existing shareholders. The Trustees of the Trust, including the Trustees who are not “interested persons” of the Fund (as defined in the 1940 Act), [unanimously] recommend that shareholders of the Fund approve the Merger.]

Agreement and Plan of Reorganization. The proposed merger will be governed by the Agreement, a copy of which is attached as Appendix A. The Agreement provides that Scudder Advisor Funds, on behalf of Mid Cap Growth Fund, will acquire all of the assets of Dynamic Growth Fund in exchange for the assumption by Mid Cap Growth Fund of all of the liabilities of Dynamic Growth Fund and for the issuance of Merger Shares equal in value to the value of the transferred assets net of assumed liabilities. The Merger Shares will be issued on the next full business day (the “Exchange Date”) following the time as of which the Funds’ shares are valued for determining net asset value for the merger (4:00 pm, Eastern time, on November 12, 2004, or such other date and time as may be agreed upon by the parties). The following discussion of the Agreement is qualified in its entirety by the full text of the Agreement.

Dynamic Growth Fund will sell all of its assets to Mid Cap Growth Fund, and in exchange Mid Cap Growth Fund will assume all of the liabilities of Dynamic Growth Fund and deliver to Mid Cap Growth Fund a number of full and fractional Merger Shares of each class having an aggregate net asset value equal to the value of the assets of Dynamic Growth Fund attributable to shares of beneficial interest of the corresponding class of Dynamic Growth Fund less the value of the liabilities of Dynamic Growth Fund assumed by Mid Cap Growth Fund attributable to shares of beneficial interest of such class of Dynamic Growth Fund. Immediately following the Exchange Date, Dynamic Growth Fund will distribute pro rata to its shareholders of record as of the close of business on the Exchange Date the full and fractional Merger Shares received by Dynamic Growth Fund, with Merger Shares of each class being distributed to holders of shares of beneficial interest of the corresponding class of Dynamic Growth Fund. This distribution will be accomplished by the establishment of accounts on the share records of Mid Cap Growth Fund in the name of such Dynamic Growth Fund shareholders, each account representing the respective number of full and fractional Merger Shares of each class due the respective shareholder. New certificates for Merger Shares will not be issued.

The Trustees of the Trust and of Scudder Advisor Funds have each determined that the interests of their respective Fund’s shareholders will not be diluted as a result of the transactions contemplated by the Agreement, and the Trustees of the Trust and Scudder Advisor Funds have each determined that the proposed merger is in the best interests of their respective Fund.

21

Table of Contents

The consummation of the merger is subject to the conditions set forth in the Agreement. The Agreement may be terminated and the merger abandoned at any time, before or after approval by the shareholders, prior to the Exchange Date, by mutual consent of Mid Cap Growth Fund and Dynamic Growth Fund or, if any condition set forth in the Agreement has not been fulfilled and has not been waived by the party entitled to its benefits, by such party.