UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

10-K

(Mark one)

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2021 |

| ☐ | TRANSITION REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number

001-31895

ODYSSEY MARINE EXPLORATION, INC.

(Exact name of registrant as specified in its charter)

Nevada | 84-1018684 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

205 S. Hoover Blvd, Suite 210, Tampa FL 33609

(Address and zip code of principal executive offices)

(813)

876-1776

(Registrant’s telephone number including area code)

Securities registered pursuant Section 12(b) of the Act:

Common Stock, $.0001 par value | OMEX | NASDAQ Capital Market | ||

(Title of each class) | (Trading symbol) | (Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Act. Yes ☐ No ☒

Indicate by mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☒ No ☐Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, a smaller reporting company, or emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule12b-2

of the Exchange Act. (Check one):| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal controls over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule

12b-2

of the Act). Yes ☐ No ☒The aggregate market value of the 12.3 million shares of voting stock held by

non-affiliates

of Odyssey Marine Exploration, Inc. as of June 30, 2021, was approximately $78.2 million. As of March 8, 2022, the Registrant had 14,349,363 shares of Common Stock outstanding.DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this Form

10-K

is incorporated by reference to the Company’s Definitive Proxy Statement for the Registrant’s Annual Meeting of Stockholders to be held on June 13, 2022.

TABLE OF CONTENTS

Page | ||||||

Item 1. | 1 | |||||

Item 1A. | 7 | |||||

Item 1B. | 12 | |||||

Item 2. | 12 | |||||

Item 3. | 19 | |||||

Item 4. | 19 | |||||

Item 5. | 20 | |||||

Item 6. | 20 | |||||

Item 7. | 20 | |||||

Item 7A. | 34 | |||||

Item 8. | 34 | |||||

Item 9. | 34 | |||||

Item 9A. | 34 | |||||

Item 9B. | 35 | |||||

Item 9C. | 35 | |||||

Item 10. | 35 | |||||

Item 11. | 35 | |||||

Item 12. | 35 | |||||

Item 13. | 35 | |||||

Item 14. | 35 | |||||

Item 15. | 36 | |||||

| 80 | ||||||

| 81 | ||||||

As used in this Annual Report on Form

10-K,

“we,” “us,” “our company” and “Odyssey” mean Odyssey Marine Exploration, Inc. and our subsidiaries, unless the context indicates otherwise.PART I

This Annual Report on Form

10-K

contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Act of 1934, as amended. The statements regarding Odyssey Marine Exploration, Inc. and its subsidiaries contained in this report that are not historical in nature, particularly those that utilize terminology such as “may,” “will,” “should,” “likely,” “expects,” “anticipates,” “estimates,” “believes,” “plans,” or comparable terminology, are forward-looking statements based on current expectations and assumptions, and entail various risks and uncertainties that could cause actual results to differ materially from those expressed in such forward-looking statements.Important factors known to us that could cause such material differences are identified in our “RISK FACTORS” in Item 1A and elsewhere in this report. Accordingly, readers of this Annual Report on Form

10-K

should consider these factors in evaluating an investment in our securities and are cautioned not to place undue reliance on the forward-looking statements contained herein. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information or future events unless otherwise specifically indicated, except as required by law.ITEM 1. | BUSINESS |

Overview

Odyssey Marine Exploration, Inc. discovers, validates and develops high-value seafloor resources in an environmentally responsible manner, providing access to critical resources that can transform societies and economies for generations to come.

The company has a diversified mineral portfolio that includes projects controlled by us and other projects in which we are a minority owner and service provider. In addition, our team is continually working to add new projects to the portfolio by identifying potential new assets through a proprietary Global Prospectivity Program leading to the acquisition of appropriate rights. Our development focus is on projects that can meet stringent standards for environmental responsibility and sustainability while unlocking benefits for the host country. Environmental protection remains at the forefront of the strategic and tactical decision-making processes in all our work.

Each project in the portfolio is advanced along a defined development path, decreasing risk and increasing value along the way. These steps may include, but are not limited to, verification and quantification of the mineral asset, collection of baseline environmental data essential for environmental permitting, environmental impact studies and reports, design and verification of extraction systems and definition and verification of commercial programs. Odyssey may elect to sell equity in individual projects to fund continued advancement of the project.

For nearly 30 years, we have deployed cutting-edge ocean technology and processes at depths up to 6,000 meters, under the direction of some of the industry’s most skilled and successful ocean exploration professionals, scientists, and environmental specialists.

Importance of Seabed Mineral Exploration

There is growing global demand for critical mineral resources to power the green economy, feed the world’s growing population and provide vital infrastructure. Land based deposits of cobalt, manganese, rare earth minerals, phosphorite, gold, silver, copper and zinc are being depleted. As the worldwide population continues to grow, it is necessary to explore additional and alternative sources of these much-needed materials.

Climate change and the global transition to a lower carbon economy presents opportunities for Odyssey given the increased demand for raw materials for the future green economy including those that will be required for renewable energy generation and storage. Furthermore, as the worldwide population continues to grow, it is necessary to explore additional and alternative sources of these much-needed materials.

Subsea mineral deposits can provide these critical resources with less social and environmental impact. We have the expertise and technology to find and access these deposits and to prepare the project for extraction in an economically feasible and environmentally sensitive way.

1

Benefits of Ocean Mineral Resource Development

Some of the benefits of ocean mineral resource development include:

| • | Infrastructure Expense: No site-specific infrastructure and generally low capital expenditures – ship-based extraction systems provide the ability to redeploy, repurpose or increase equipment productivity through cost/tonne or ship charter financing options. |

| • | Overburden: Little overburden to be removed in most proposed seafloor mining projects which contributes to operational efficiencies. |

| • | Flexibility: Extraction ships can move to different types of deposits/minerals to suit market conditions without infrastructure loss at minimal costs. |

| • | Social Displacement: No people are displaced, no disruption of society or property. |

| • | Environmental Impact: Seafloor mining can be done responsibly with limited biological impact and a manageable carbon footprint. No forested lands will be impacted, and freshwater systems are not affected. Seafloor dredging, aggregate and diamond mining have been carried out for many years in shallow waters around the world and with appropriate mitigation programs have posed minimal adverse impact to marine ecosystems. |

| • | Shipping logistics are efficient as ore and materials are extracted and moved directly to bulk carriers, lowering the number of steps in the delivery process thus reducing costs. |

Considering the benefits of subsea mineral resource extraction, we are convinced that in the future, ocean mining will be the best practice for responsible provision of critical resources required worldwide. Odyssey is taking the lead in preparing for this future through the validation and development of environmentally and socially responsible seafloor mineral projects.

Mineral and Offshore Services

We provide specialized mineral exploration, project development and marine services to clients (subsidiary companies, other companies and/or governments). As our business is focused on the development of a diversified portfolio of subsea resources, we may elect to receive equity for the provision of our services on select mineral projects. We have an extensive history conducting deep-ocean projects down to 6,000 meters in depth including deep-ocean resource explorations, ship and airplane wreck explorations, archaeological recovery and conservation and insurance documentation and applying this experience and expertise to advance our project portfolio.

Operational Projects and Status

We focus on projects that can meet stringent standards for environmental responsibility while unlocking benefits for the host community and country.

Our subsea project portfolio contains multiple projects in various stages of development throughout the world and across different mineral resources. We are regularly adding new projects through the development of new deposits, acquisition of mineral rights/deposits and through a leveraged contracting model, which allows the company to earn equity in

deep-sea

mineral projects.With respect to mineral deposits, Subpart 1300 of Regulations

S-K

outlines the Securities and Exchange Commission’s basic mining disclosure policy and what information may be disclosed in public filings. The SEC has adopted amendments to the property disclosure requirements for mining registrants that must be complied with for the full fiscal year beginning on or after January 1, 2021, See Item 2 Properties.Although Odyssey has a variety of projects in various stages of development, only projects with material operational activity in the past 12 months are included below.

ExO Phosphate Project:

The “Exploraciones Oceanicas” Phosphate Project is a rich deposit of phosphate sands located

70-90

meters deep within Mexico’s Exclusive Economic Zone. This deposit contains a large amount of high-grade phosphate rock that can be extracted on a financially attractive basis (essentially a standard dredging operation). The product will be attractive to Mexican and other world producers of fertilizers and can provide important benefits to Mexico’s agricultural development.2

The deposit lies within an exclusive mining concession licensed to the Mexican company Exploraciones Oceánicas S. de R.L. de CV (“ExO”). Oceanica Resources, S. de R.L., a Panamanian company (“Oceanica”) owns 99.99% of ExO, and Odyssey owns 56.29% of Oceanica through Odyssey Marine Enterprises, Ltd., a wholly owned Bahamian company (“Enterprises”).

In 2012, ExO was granted a

50-year

mining license by Mexico (extendable for another 50 years at ExO’s option) for the deposit that lies25-40

km offshore in Baja California Sur. AnNI 43-101 compliant

report was completed on the deposit in 2014 and has been periodically updated.We spent more than three years preparing an environmentally sustainable development plan with the assistance of experts in marine dredging and leading environmental scientists from around the world. Key features of the environmental plan included:

| • | No chemicals would be used in the dredging process or released into the sea. |

| • | A specialized return down pipe that exceeds international best practices to manage the return of dredged sands close to the seabed, limiting plume or impact to the water column and marine ecosystem (including primary production). |

| • | The seabed would be restored after dredging in such a way as to promote rapid regeneration of seabed organisms in dredged areas. |

| • | Ecotoxicology tests demonstrated that the dredging and return of sediment to the seabed would not have toxic effects on organisms. |

| • | Sound propagation studies concluded that noise levels generated during dredging would be similar to whale-watching vessels, merchant ships and fisherman’s ships that already regularly transit this area, proving the system is not a threat to marine mammals. |

| • | Dredging limited to less than one square kilometre each year, which means the project would operate in only a tiny proportion of the concession area each year. |

| • | Proven turtle protection measures were incorporated, even though the deposit and the dredging activity are much deeper and colder than where turtles feed and live, making material harm to the species highly remote. |

| • | There will be no material impact on local fisheries as fishermen have historically avoided the water column directly above the deposit due to the naturally low occurrence of fish there. |

| • | The project would not be visible from the shoreline and would not impact tourism or coastal activities. |

| • | Precautionary mitigation measures were incorporated into the development plan in line with best-practice global operational standards. |

| • | The technology proposed to recover the phosphate sands has been safely used in Mexican waters for over 20 years on more than 200 projects. |

Notwithstanding the factors stated above, in April 2016 the Mexican Ministry of the Environment and Natural Resources (SEMARNAT) unlawfully rejected the permission to move forward with the project.

ExO challenged the decision in Mexican Federal court and in March 2018, the Tribunal Federal de Justicia Administrativa (TFJA), an

11-judge

panel, ruled unanimously that SEMARNAT denied the application in violation of Mexican law and ordered the agency tore-take

their decision. Just prior to the change in administration later in 2018, SEMARNAT denied the permit a second time in defiance of the court. ExO is once again challenging the unlawful decision of the Peña Nieto administration before the TFJA. In addition, in April 2019, we filed a NAFTA Claim against Mexico to protect our shareholders’ interests and significant investment in the project.Our claim seeks compensation of over $2 billion on the basis that SEMARNAT’s wrongful repeated denial of authorization has destroyed the value of our investment in the country and is in violation of the following provisions of NAFTA:

| • | Article 1102. National Treatment. |

| • | Article 1105. Minimum Standard of Treatment; and |

| • | Article 1110. Expropriation and Compensation. |

We filed First Memorial in the NAFTA case in September 2020. It is supported by documentary evidence and 20 expert reports and witness statements. In summary, this evidence includes:

| • | MERITS: Testimony from independent environmental experts that the environmental impact of ExO’s phosphate project is minimal and readily mitigated by the mitigation measures proposed by ExO. Witnesses also testified that |

3

Mexico’s denial of environmental approval by the prior administration was politically motivated and not justified on environmental grounds, and that Mexico granted environmental permits to similar dredging projects in areas that are considered more environmentally sensitive than ExO’s project location. |

| • | RESOURCE: An independent certified marine geologist testified as to the size and character of the resource. |

| • | OPERATIONAL VIABILITY: Engineering experts testified that the project uses established dredging and processing technology, and the project’s anticipated CAPEX and OPEX was reasonable. |

| • | VALUE: A phosphate market analyst testified that the project’s projected CAPEX and OPEX would make the project one of the lowest cost phosphate rock resources in the world, and damages experts testified the project would be commercially viable and profitable. |

Odyssey filed its First Memorial in the case on September 4, 2020. Mexico filed its Counter-Memorial on February 23, 2021. On June 29, 2021, we filed our reply to Mexico’s Counter-Memorial. Odyssey’s filings are available at www.odysseymarine.com/nafta. Mexico filed their Rejoinder on October 19, 2021. All filings are available on the ICSID website. The NAFTA’s Tribunal hearing took place from January 24 – January 29, 2022. After this evidentiary phase is closed by the Tribunal, deliberations will begin. Odyssey cannot predict the length of these deliberations or when a ruling will be issued, but we remain confident in the merits of our case.

On June 14, 2019, Odyssey executed an agreement that provided up to $6.5 million in funding for prior, current and future costs of the NAFTA action. On January 31, 2020, this agreement was amended and restated, as a result of which the availability increased to $10.0 million. In December 2020, Odyssey announced it secured an additional $10 million from the funder to aid in our NAFTA case. On June 14, 2021, the funder agreed to fund up to an additional $5.0 million for litigation costs. The funder will not have any right of recourse against us unless the environmental permit is awarded or if proceeds are received (See NOTE H – LOANS PAYABLE – Litigation Financing).

LIHIR Gold Project:

The exploration license for the Lihir Gold Project covers a subsea area that contains at least five prospective gold exploration targets in two different mineralization types: seamount-related epithermal and modern placer gold. Two subaqueous debris fields within the area are adjacent to the terrestrial Ladolam Gold Mine and are believed to have originated from the same volcanogenic source. The resource lies

500-2,000

meters deep in the Papua New Guinea Exclusive Economic Zone off the coast of Lihir Island, adjacent to the location of one of the world’s largest know terrestrial gold deposits. We have an indirect 85.6% interest in Bismarck Mining Corporation, Ltd, the Papua New Guinea company that holds the exploration license for the project.Previous exploration expeditions in the license area, including a survey conducted by Odyssey, indicate a polymetallic resource with commercially viable gold content likely exists.

In August 2021, Papua New Guinea (PNG) issued a permit extension allowing Odyssey to continue with our exploration program. We have developed an exploration program for the Lihir Gold Project to validate and quantify the precious and base metal content of the prospective resource. The Company met with local regulatory authorities, specialists in local mining, environmental legal experts, and logistics support service companies in PNG to establish baseline business functions essential for a successful program to support upcoming marine exploration operations in the license area. This offshore work began in late 2021 and will continue, provided there are no constraints from the

COVID-19

pandemic or other unexpected impediments. Bismarck and Odyssey value the environment and respect the interests and people of Papua New Guinea and Lihir and are committed to transparent sharing of all environmental data collected during the exploration program.Offshore survey and mapping operations commenced in December 2021 in the Papua New Guinea, Lihir license area. Raw data is being processed to produce a report and full analysis. The goals of this work include producing a high-resolution acoustic terrain model of the seafloor in the area, as well as acquiring acoustic images of subseafloor sediments and lithology. This will provide a basis for characterizing the geologic setting of the area and essentially creating a “snapshot” of the environment. These activities will help us to further characterize the value of this project and allow informed decision making on how to proceed with environmentally sensitive direct geologic sampling.

Odyssey’s multi-year exploration program will focus on robust environmental surveys and studies that will accrue to environmental permitting in compliance with PNG’s requirements as well as the development of an EIA (Environmental Impact Assessment). During the exploration phase, steps to validate and quantify the precious and base metal content of the prospective resource will also be carried out. Once completed, if the data shows extraction can be carried out responsibly, Odyssey will apply for a Mining License.

4

Further development of this project is dependent on the characterization of any present resources during exploration and license approvals.

CIC Project:

Odyssey is a member of the CIC Consortium, which is seeking an exploration license in an island nation’s Exclusive Economic Zone. The CIC Consortium was founded and is led by Odyssey

co-founder

and former CEO, Greg Stemm, and includes Royal Boskalis Westminster NV and Odyssey Marine Exploration.In December 2021, the Cook Islands Seabed Minerals Authority’s (SBMA) Licensing Panel evaluated three applications and announced that CIC LIMITED (CIC) met the qualification criteria for an exploration license. On February 23, 2022, CIC was awarded a five-year exploration license by the Cook Islands

Through a wholly owned subsidiary, we have earned and now hold approximately 13.4% of the current outstanding equity units of CIC. We have the ability to earn up to 20.0 million equity units over the next several calendar years, which represents an approximate 16.0% interest in CIC based on the currently outstanding equity units. This means we can earn approximately 3.5 million additional equity units in CIC. We achieved our current equity position through the provision of services related to resource assessment, project planning, research and project management. We receive cash and equity for services rendered to this venture, see NOTE G.

Antigua and Barbuda:

In September 2021, Odyssey entered into a Memorandum of Understanding (MoU) with the Government of Antigua and Barbuda to determine the feasibility of a sustainable seabed mineral resource program from highly prospective areas in their Exclusive Economic Zone. There is a high probability for polymetallic nodule formation based on legacy data, regional analysis and seafloor conditions which are similar to and adjacent to our target area. Development of an exploration program, which will be the basis for a definitive agreement between the parties, is in late-stage development. Additional information will be released upon execution of the definitive agreement, which is expected in the coming months.

Brazilian Phosphate Project:

Odyssey reached an exclusive agreement early in 2022 with BlueSea Minerals, Ltd. and BlueSea Minerals Brasil Ltda, (collectively BlueSea Group) to create a new joint venture (JV) company in which Odyssey will own a 75% interest. The new company will have exclusive rights to 19 highly prospective phosphate areas in the Exclusive Economic Zone (EEZ) of Brazil. Legacy data and desktop research indicate high-grade phosphate deposits in the concession areas.

Pending execution of the definitive agreement, Odyssey will manage the overall Brazilian Phosphate Project development and BlueSea Group will manage business operations in Brazil. A related party to BlueSea Group, SeaSeep, a Brazilian entity, will provide marine operations services, supervised by Odyssey.

The 19 licenses to be developed by the JV include 366 square kilometres of seabed in the Brazilian EEZ. The geological setting of these licenses is similar to the geology Odyssey identified off the coast of Mexico, which is now known as the ExO Phosphate deposit (“ExO”). The NI

43-101

for the ExO deposit estimated 588 million tonnes of high-grade resource, even though the NI43-101

only considered 206.5 square kilometres of the 1147 square kilometres covered by the ExO mining concession. Even based on 2016 phosphate pricing, the ExO project had extremely compelling economics that demonstrated that ExO could have been one of the lowest cost producers in the world. Since then, phosphate prices have surged and the need for phosphate to combat world hunger continues to grow. It is anticipated that the Brazilian deposits can be dredged with the standard technology and engineering solutions already identified for the ExO Project, which will allow the phosphate to be recovered in an environmentally responsible manner without the addition of any chemicals into the sea.Legal and Political Issues

Odyssey works with several leading international maritime lawyers and policy experts to constantly monitor international legal initiatives that might affect our projects.

To the extent that we engage in mineral exploration or marine activities in the territorial, contiguous or exclusive economic zones of countries, we work to comply with verifiable applicable regulations and treaties.

5

We believe there will be increased interest in the recovery of subsea minerals throughout the oceans of the world. We are uniquely qualified to provide governments and international agencies with knowledge and skills to help manage these resources.

Related to mineral exploration, we evaluate the political climate and specific legal requirements of any areas in which we are working. We may partner with third parties who have unique industry experience in specific geographical areas to assist with navigation of the regulatory landscape.

Competition

We conduct mineral exploration on both shallow and

deep-sea

terrains. There are several companies that publicly identify themselves as engaged in aspects of deep-ocean mineral exploration or mining, including DSMF (OTCM:NUSMF), Neptune Minerals, Deep Green Resources, Inc., which recently combined with the Sustainable Opportunities Acquisition Corporation to go public as The Metals Company (NASDAQ:TMC), GSR, and Chatham Rock Phosphate, Ltd. (CRP.NZ), as well as countries that are evaluating options to mine deep-ocean mineralized materials. As our mineral exploration business plan includes partnering with others in the industry, we view these entities as potential partners rather than pure competitors. As mineral rights are generally granted on an exclusive basis for a specific area or tenement, once licenses are granted, we do not anticipate any competitive intrusion on those areas. It is possible that one of these companies or some currently unknown group may secure licenses on an area desired by us or one of our partners; but since exploration work does not start until licenses are secured, we do not believe that competition from one or more of these entities, known or unknown, would materially affect our operating plan or alter our current business strategy. For offshore mineral exploration, there are providers of vessels and equipment that could be competitors or partners for certain projects. These companies generally service the oil, gas and telecom industries with survey capabilities. We view these companies as potential strategic partners or services providers for our projects.Cost of Environmental Compliance

With the exception of marine operations, our general business operations do not expose us to environmental risks or hazards. We carry insurance that provides a layer of protection in the event of an environmental exposure resulting from the operation of vessels we may utilize. The cost of such coverage is not material on an annual basis. Our seabed mineral business is currently in the exploration and validation phase and has thus not exposed us to any significant environmental risks or hazards, other than those which are standard to basic marine operations.

Executive Officers of the Registrant

The names, ages and positions of all the executive officers of the Company as of March 1, 2022, are listed below.

Mark D. Gordon (age 61) has served as Chief Executive Officer since October 1, 2014, and was appointed to the Board of Directors in January 2008. Mr. Gordon also served as President from October 2007 to June 2019, when he was appointed Chairman of the Board. Previously, Mr. Gordon served as Chief Operating Officer since October 2007 and as Executive Vice President of Sales and Business Development since January 2007 after joining Odyssey as Director of Business Development in June 2005. Prior to joining Odyssey, Mr. Gordon owned and managed four different ventures.

Christopher E. Jones (age 48) has served as Chief Financial Officer since June 15, 2021. Prior to joining Odyssey, Mr. Jones served as Vice President of Corporate Finance at Mohegan Gaming & Entertainment (MGE) since 2017; Managing Director at Buckingham Research Group from 2016 to 2017; Managing Director at Union Gaming from 2014 to 2016 and Managing Director at Telsey Advisory Group (TAG) from 2008 to 2014. He has also held positions at Oppenheimer & Company, Merrill Lynch and Lehman Brothers.

Jay A. Nudi, CPA (age 58) has served as Principal Accounting Officer since January 2006 and Treasurer since May 2010. Previously, Mr. Nudi served as the Chief Financial Officer from 2016 to 2021. Mr. Nudi joined the Company in May 2005 in the Corporate Controller capacity. Prior to joining Odyssey, Mr. Nudi served as Controller for The Axis Group in Atlanta (2003 to 2004).

John D. Longley, Jr. (age 55) has served as Chief Operating Officer since October 1, 2014 and was appointed President on June 3, 2019. Previously Mr. Longley served as Executive Vice President of Sales and Business Development since February 2012. Mr. Longley was originally the Director of Sales and Business Operations when he joined the Company in May 2006. Prior to joining Odyssey, Mr. Longley served as Vice President of Sales and Marketing for Public Imagery from 2003 to 2005 and Director of Retail Marketing for Office Depot North American stores from 1998 to 2003.

6

Laura L. Barton (age 59) was appointed as Chief Business Officer in March 2021 and was elected to the Board of Directors in June 2019 and has served as Corporate Secretary since June 2015. She formerly served as Vice President and Director of Corporate Communications from November 2007 to June 2012 and Executive Vice President and Director of Communications from 2012 until 2021. Ms. Barton previously served as Director of Corporate Communications and Marketing for Odyssey since July 2003. Ms. Barton was previously President of LLB Communications, a marketing and communications consulting company whose customers included a variety of television networks, stations and distributors and the Company (1994 to 2003).

Human Capital Management

As of December 31, 2021, we had 13 full-time employees, most working from our corporate offices in Tampa, Florida. Additionally, we contract with specialized technicians to perform technical marine survey and recovery operations and from time to time hire subcontractors and consultants to perform specific services.

Odyssey has historically experienced low voluntary employee turnover. We believe this is a testament to our culture of treating our employees well, providing them with the tools and flexibility to be productive, and maintaining an environment of mutual trust and respect. We offer competitive compensation and generous health benefits and flexible work schedules which in turn helps foster employee loyalty.

As the company continues to grow, we recognize our continued success will depend on our ability to recruit, develop and retain skilled employees, including those from younger generations, whose backgrounds and skills will be critical to drive innovation and meet future challenges. Enhancing gender and racial/ethnic diversity in management and our broader workforce is among Odyssey’s priorities for the coming years.

Internet Access

Odyssey’s Forms. They may be accessed as follows:(Investors/Financial Information Link).

10-K,

10-Q,

8-K

and all amendments to those reports are available without charge through Odyssey’s web site on the Internet as soon as reasonably practicable after they are electronically filed with, or furnished to, the Securities and Exchange Commission,www.sec.gov

www.odysseymarine.com

ITEM 1A. | RISK FACTORS |

You should carefully consider the following factors, in addition to the other information in this Annual Report on

Form 10-K,

in evaluating our company and our business. Our business, operations and financial condition are subject to various risks. The material risks are described below and should be carefully considered in evaluating Odyssey or any investment decision relating to our securities. This section is intended only as a summary of the principal risks. If any of the following risks actually occur, our business, operating results, or financial results could suffer. If this occurs, the trading price of our common stock could decline, and you could lose all or part of the money you paid to buy our common stock.Our business involves a high degree of risk.

An investment in Odyssey is extremely speculative and of exceptionally high risk. With respect to mineral exploration projects, there are uncertainties with respect to the quality and quantity of the material and their economic feasibility, the price we can obtain for the sale of the deposit or the ore extracted from the deposit, the granting of the necessary permits to operate, environmental safety, technology for extraction and processing, distribution of the eventual ore product, and funding of necessary equipment and facilities. In projects where Odyssey takes a minority ownership position in the company holding the mining rights, there may be uncertainty as to that company’s ability to move the project forward.

The research and data we use may not be reliable.

The success of a mineral project is dependent to a substantial degree upon the research and data we or the contracting party have obtained. By its very nature, research and data regarding mineral deposits can be imprecise, incomplete, outdated, and unreliable. For mineral exploration, data is collected based on a sampling technique and available data may not be representative of the entire ore body or tenement area. Prior to conducting

off-shore

exploration, we typically conducton-shore

research. There is no guarantee that the models and research conducted onshore will be representative of actual results on the seafloor. Offshore exploration typically requires significant expenditures, with no guarantee that the results will be useful or financially rewarding.7

Operations may be affected by natural hazards.

Underwater exploration and recovery operations are inherently difficult and dangerous and may be delayed or suspended by weather, sea conditions or other natural hazards. Further, such operations may be undertaken more safely during certain months of the year than others. We cannot guarantee that we, or the entities we are affiliated with, will be able to conduct exploration, sampling or extractions operations during favorable periods. In addition, even though sea conditions in a particular search location may be somewhat predictable, the possibility exists that unexpected conditions may occur that adversely affect our operations. It is also possible that natural hazards may prevent or significantly delay operations. Seabed mineral extraction work may be subject to interruptions resulting from storms that adversely affect the extraction operations or the ports of delivery. Project planning considers these risks.

We may be unable to establish our rights to resources or items we discover or recover.

We may discover potentially valuable seabed mineral deposits, but we may be unable to get title to the deposits or get the necessary governmental permits to commercially extract the minerals. Mineral deposits may be in controlled waters where the policies and laws of a certain government may change abruptly, thereby adversely affecting our ability to operate in those zones. We have a process for evaluating this risk in our proprietary Global Prospectivity Program.

The market for any objects or minerals we recover is uncertain.

During the time between when a mineral deposit is discovered and the first extracted minerals are sold, world and local prices for the mineral may fluctuate drastically and thereby adversely affect the economics of the mineral project.

We could experience delays in the disposition or sale of minerals or recovered objects.

It may take significant time between when a mineral deposit is discovered and the first extracted minerals are sold. Stakes in the mineral deposits can potentially be sold at an earlier date, but there is no guarantee that there will be readily available buyers at favorable competitive prices.

Legal, political or civil issues could interfere with our marine operations.

Legal, political or civil issues of governments throughout the world could restrict access to our operational marine sites or interfere with our marine operations or rights to seabed mineral deposits. In many countries, the legislation covering ocean exploration lacks clarity or certainty. As a result, when we are conducting projects in certain areas of the world for our own account or on our behalf of a contracting party, we may be subjected to unexpected delays, requests, and outcomes as we work with local governments to define and obtain the necessary permits and to assert our claims over assets on the seafloor bottom. Our vessel, equipment, personnel and or cargo could be seized or detained by government authorities. We may have to work with different units of a government, and there may be a change of government representatives over time. This may result in unexpected changes or interpretations in government contracts and legislation.

We may be unable to get permission to conduct exploration, excavation, or extraction operations.

It is possible we will not be successful in obtaining the necessary permits to conduct exploration or excavation and extraction operations. In addition, permits we obtain may be revoked or not honored by the entities that issued them. In addition, certain governments may develop new permit requirements that could delay new operations or interrupt existing operations.

Changes in our business strategy or restructuring of our businesses may increase our costs or otherwise affect the profitability of our businesses.

As changes in our business environment occur, we may need to adjust our business strategies to meet these changes or we may otherwise find it necessary to restructure our operations or particular businesses or assets. When these changes or events occur, we may incur costs to change our business strategy and may need to write down the value of assets or sell certain assets. In any of these events our costs may increase, and we may have significant charges associated with the write-down of assets. Discontinuing the use of a multi-year charter of a ship may result in large

one-time

costs to cover any penalties or charges to put the ship back into its original condition.8

We may be unsuccessful in raising the necessary capital to fund operations and capital expenditures.

Our ability to generate cash inflows is dependent upon our ability to provide mineral exploration and development services to our subsidiaries and other subsea mineral companies or monetize mineral rights. However, we cannot guarantee that the sales and other cash sources will generate sufficient cash inflows to meet our overall cash requirements. If cash inflows are not sufficient to meet our business requirements, we will be required to raise additional capital through other financing activities. While we have been successful in raising the necessary funds in the past, there can be no assurance we can continue to do so in the future.

We depend on key employees and face competition in hiring and retaining qualified employees.

Our employees are vital to our success, and our key management and other employees are difficult to replace. We currently do not have employment contracts with the majority of our key employees. We may not be able to retain highly qualified employees in the future which could adversely affect our business.

We may continue to experience significant losses from operations.

We have experienced a net loss in every fiscal year since our inception except for 2004. Our net losses were $10.0 million in 2021, $14.8 million in 2020 and $10.4 million in 2019. Even if we do generate operating income in one or more quarters in the future, subsequent developments in our industry, customer base, business or cost structure or an event such as significant litigation or a significant transaction may cause us to again experience operating losses. We may not become profitable for the long-term, or even for any quarter.

Technological obsolescence of our marine assets or failure of critical equipment could put a strain on our capital requirements or operational capabilities.

We employtechnology including side-scan sonar, magnetometers, ROVs, and other advanced science and technology to perform seabed mineral exploration and to locate and recover shipwrecks at depths previously unreachable in an economically feasible manner. Although we try to maintain

state-of-the-art

back-ups

on critical equipment and components, equipment failures may require us to delay or suspend operations. Also, while we endeavor to keep marine equipment in excellent working condition and current with all available upgrades, technological advances in new equipment may provide superior efficiencies compared to the capabilities of our existing equipment, and this could require us to purchase new equipment which would require additional capital.We may not be able to contract with clients or customers for marine services or syndicated projects.

In the past, from time to time, we have earned revenue by chartering out vessels, equipment and crew and providing marine services to clients or customers. Even if we do contract out our services, the revenue may not be sufficient to cover administrative overhead costs. While the operational results of these syndicated projects are generally successful, the clients or customers may not be willing or financially able to continue with syndicated projects of this type in the future. Failure to secure such revenue producing contracts in the future may have a material adverse impact on our revenue and operating cash flows. We may take payment for these services in the form of cash, equity in the client’s company, or a financial interest in the tenement areas.

The issuance of shares at conversion prices lower than the market price at the time of conversion and the sale of such shares could adversely affect the price of our common stock.

Some of our outstanding shares may have been acquired from time to time upon conversion of convertible notes at conversion prices that are lower than the market price of our common stock at the time of conversion. In the past, Odyssey has issued debt obligations that could be converted into common shares at prices below the current market price. Conversion of the notes at conversion prices that are lower than the market price at the time of conversion and the sale of the shares issued upon conversion could have an adverse effect upon the market price of our common stock.

9

Investments in subsea mineral exploration companies may prove unsuccessful.

We have invested in marine mineral companies that to date are still in the exploration phase and have not begun to earn revenue from operations. We may or may not have control or input on the future development of these businesses. There can be no assurance that these companies will achieve profitability or otherwise be successful in capitalizing on the mineralized materials they intend to exploit.

We may be subject to short selling strategies

Short sellers of our stock may be manipulative and may attempt to drive down the market price of our common stock. Short selling is the practice of selling securities that the seller does not own but rather has, supposedly, borrowed from a third party with the intention of buying identical securities back at a later date to return to the lender. The short seller hopes to profit from a decline in the value of the securities between the sale of the borrowed securities and the purchase of the replacement shares, as the short seller expects to pay less in that purchase than it received in the sale. As it is therefore in the short seller’s best interests for the price of the stock to decline, many short sellers (sometime known as “disclosed shorts”) publish, or arrange for the publication of, negative opinions regarding the relevant issuer and its business prospects to create negative market momentum and generate profits for themselves after selling a stock short. Although traditionally these disclosed shorts were limited in their ability to access mainstream business media or to otherwise create negative market rumors, the rise of the Internet and technological advancements regarding document creation, videotaping and publication by weblog (“blogging”) have allowed many disclosed shorts to publicly attack a company’s credibility, strategy and veracity by means of

so-called

“research reports” that mimic the type of investment analysis performed by large Wall Street firms and independent research analysts. These short attacks have, in the past, led to selling of shares in the market, on occasion in large scale and broad base. Issuers who have limited trading volumes and are susceptible to higher volatility levels thanlarge-cap

stocks, can be particularly vulnerable to such short seller attacks. These short seller publications are not regulated by any governmental, self-regulatory organization or other official authority in the U.S., are not subject to certification requirements imposed by the Securities and Exchange Commission and, accordingly, the opinions they express may be based on distortions or omissions of actual facts or, in some cases, fabrications of facts. In light of the limited risks involved in publishing such information, and the enormous profit that can be made from running just one successful short attack, unless the short sellers become subject to significant penalties, it is more likely than not that disclosed short sellers will continue to issue such reports.Some of our equipment or assets could be seized or we may be forced to sell certain assets.

We have pledged certain assets, such as equipment and shares of subsidiaries, as collateral under our loan agreements. Some suppliers have the ability to seize some of our assets if we do not make timely payments for the services, supplies, or equipment that they have provided to us. If we were unable to make payments on these obligations, the lender or supplier may seize the asset or force the sale of the asset. The loss of such assets could adversely affect our operations. The sale of the asset may be done in a manner and under circumstances that do not provide the highest cash value for the sale of the asset.

We could be delisted from the NASDAQ Capital Market.

Our common stock is listed on the NASDAQ Capital Market, which imposes, among other requirements, a minimum bid requirement. The closing bid price for our common stock must remain at or above $1.00 per share to comply with NASDAQ’s minimum bid requirement for continued listing. If the closing bid price for our common stock is less than $1.00 per share for 30 consecutive business days, NASDAQ may send us a notice stating we will be provided a period of 180 days to regain compliance with the minimum bid requirement or else NASDAQ may make a determination to delist our common stock. Another requirement for continued listing on the NASDAQ Capital Market is to maintain our market capitalization above $35.0 million.

Our failure to maintain compliance with the above-mentioned and other NASDAQ continued listing requirements may lead to the delisting of our common from the NASDAQ Capital Market. Delisting from the NASDAQ Capital Market could make trading our common stock more difficult for investors, potentially leading to declines in our share price and liquidity. If our common stock is delisted by NASDAQ, our common stock may be eligible to trade on anquotation system, where an investor may find it more difficult to sell our stock or obtain accurate quotations as to the market value of our common stock. We cannot assure you that our common stock, if delisted from the NASDAQ Capital Market, will be listed on another national securities exchange or quoted on an

over-the-counter

over-the

counter quotation system.Our insurance coverage may be inadequate to cover all of our business risks

Although we seek to obtain insurance for some of our main operational risks, there is no guarantee that the insurance policies that we have are sufficient, that they will be in place when needed, that we will be able to obtain insurance coverage

10

when desired, that insurance will be available on commercially attractive terms, or that we will be able to anticipate the risks that need to be insured. For example, although we may be able to obtain War Risk coverage for a project at a specific date and location, such insurance may be unavailable at other times and locations. Although we may be able to insure our marine assets for certain risks such as certain possible loss or damage scenarios, we may lack insurance to cover against government seizure or detention of our certain marine assets. Permanent loss or temporary loss of our marine assets and the associated business interruption without commensurate compensation from an insurance policy could severely impact the financial results and operational capabilities of the company.

We may be exposed to cyber security risks.

We depend on information technology networks and systems to process, transmit and store electronic information and to communicate among our locations around the world and among ourselves within our company. Additionally, one of our significant responsibilities is to maintain the security and privacy of our confidential and proprietary information and the personal data of our employees. Our information systems, and those of our service and support providers, are vulnerable to an increasing threat of continually evolving cybersecurity risks. Computer viruses, hackers and other external hazards, as well as improper or inadvertent staff behavior could expose confidential company and personal data systems and information to security breaches. Techniques used to obtain unauthorized access or cause system interruption change frequently and may not immediately produce signs of intrusion. As a result, we may be unable to anticipate these incidents or techniques, timely discover them, or implement adequate preventative measures. With respect to our commercial arrangements with service and support providers, we have processes designed to require third-party IT outsourcing, offsite storage and other vendors to agree to maintain certain standards with respect to the storage, protection and transfer of confidential, personal and proprietary information. However, we remain at risk of a data breach due to the intentional or unintentional

non-compliance

by a vendor’s employee or agent, the breakdown of a vendor’s data protection processes, or a cyber-attack on a vendor’s information systems or our information systems.Mining exploration, development and operating have inherent risks.

Mining operations generally involve a high degree of risk. The financing, exploration, development and mining of any of our properties is furthermore subject to a number of macroeconomic, legal and social factors, including commodity prices, laws and regulations, political conditions, currency fluctuations, the ability to hire and retain qualified people, the inability to obtain suitable and adequate machinery, equipment or labor and obtaining necessary services in the jurisdictions in which we may operate. Unfavorable changes to these and other factors have the potential to negatively affect our operations and business. Major expenses may be required to locate and establish mineral reserves and resources, to develop processes and to construct mining and processing facilities at a particular site. Mining, processing, development and exploration activities depend, to one degree or another, on adequate infrastructure. Unusual or infrequent weather phenomena, sabotage, government or other interference could adversely affect our operations, financial condition and results of operations. It is impossible to ensure that the exploration or development programs planned by us will result in a profitable commercial mining operation. Whether precious or base metal or mineral deposit will be commercially viable depends on a number of factors, some of which are: the particular attributes of the deposit, such as the quantity and quality of mineralization ; mineral prices, which are highly cyclical; and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in not receiving an adequate return on invested capital. There is no certainty that the expenditures to be made by us towards the exploration and evaluation of our projects will result in discoveries or production of commercial quantities of the minerals. In addition, once in production, mineral reserves are finite and there can be no assurance that we will be able to locate additional reserves as its existing reserves are depleted.

We are subject to significant governmental regulations, which affect our operations and costs of conducting our business.

Our exploration operations are subject to government legislation, policies and controls relating to prospecting, development, production, environmental protection, mining taxes and labor standards. In order for us to carry out our activities, various licenses and permits must be obtained and kept current. There is no guarantee that the Company’s licenses and permits will be granted, or that once granted will be maintained and extended. In addition, the terms and conditions of such licenses or permits could be changed and there can be no assurances that any application to renew any existing licenses will be approved. There can be no assurance that all permits that we require will be obtainable on reasonable terms, or at all. Delays or a failure to obtain such permits, or a failure to comply with the terms of any such permits that we have obtained, could have a material adverse impact on our operations. We may be required to contribute to the cost of providing the required infrastructure to facilitate the development of our properties and will also have to obtain and comply with permits and licenses that may contain

11

specific conditions concerning operating procedures, water use, waste disposal, spills, environmental studies and financial assurances. There can be no assurance that we will be able to comply with any such conditions and

non-compliance

with such conditions may result in the loss of certain of our permits and licenses on properties, which may have a material adverse effect on us. Future taxation of mining operators cannot be predicted with certainty so planning must be undertaken using present conditions and best estimates of any potential future changes. There is no certainty that such planning will be effective to mitigate adverse consequences of future taxation on us.We may not be able to obtain all required permits and licenses to place any of our properties into production.

Our current and future operations, including development activities and commencement of production, if warranted, require permits from governmental authorities and such operations are and will be governed by laws and regulations governing prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, toxic substances, environmental protection, mine safety and other matters. Companies engaged in mineral property exploration and the development or operation of mines and related facilities generally experience increased costs, and delays in production and other schedules as a result of the need to comply with applicable laws, regulations and permits. We cannot predict if all permits which we may require for continued exploration, development or construction of mining facilities and conduct of mining operations will be obtainable on reasonable terms, if at all. Costs related to applying for and obtaining permits and licenses may be prohibitive and could delay our planned exploration and development activities. Failure to comply with applicable laws, regulations and permitting requirements may result in enforcement actions, including orders issued by regulatory or judicial authorities causing operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment, or remedial actions. Parties engaged in mining operations may be required to compensate those suffering loss or damage by reason of the mining activities and may have civil or criminal fines or penalties imposed for violations of applicable laws or regulations. Amendments to current laws, regulations and permits governing operations and activities of mining companies, or more stringent implementation thereof, could have a material adverse impact on our operations and cause increases in capital expenditures or production costs or reduction in levels of production at producing properties or require abandonment or delays in development of new mining properties

Calculations of mineral resources and mineral reserves are estimates only and subject to uncertainty.

The estimating of mineral resources and mineral reserves is an imprecise process and the accuracy of such estimates is a function of the quantity and quality of available data, the assumptions used and judgments made in interpreting engineering and geological information and estimating future capital and operating costs. There is significant uncertainty in any reserve or resource estimate, and the economic results of mining a mineral deposit may differ materially from the estimates as additional data are developed or interpretations change.

Estimated mineral resources and mineral reserves may be materially affected by other factors.

In addition to uncertainties inherent in estimating mineral resources and mineral reserves, other factors may adversely affect estimated mineral resources and mineral reserves. Such factors may include but are not limited to metallurgical, environmental, permitting, legal, title, taxation, socio-economic, marketing, political, gold prices, and capital and operating costs. Any of these or other adverse factors may reduce or eliminate estimated mineral reserves and mineral resources and could have a material adverse effect on our business, prospects, results of operations, cash flows, financial condition and corporate reputation.

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

ITEM 2. | PROPERTIES |

Corporate Office

We maintain our corporate offices in Tampa, Florida where we lease approximately 6,000 square feet of office space. We currently do not own any buildings or land. We believe our current leased facility is sufficient for our foreseeable needs.

12

Don Diego Phosphorite Project

Summary

We have one material mining project, the Don Diego Phosphorite Project, which is located in the Mexican Exclusive Economic Zone (the “Mexican EEZ”) offshore Baja California Sur, Mexico in the Pacific Ocean. The exclusive mining concessions for the Don Diego Phosphorite Project are held by Exploraciones Oceánicas S. de R.L. de CV (“ExO”), a Mexican company in which we hold, through other subsidiaries, a 56.3% interest. The Don Diego Phosphorite Project is classified as an exploration stage property because it currently has no mineral reserves disclosed. The primary concession (Don Diego West Phosphorite Deposit) was granted in 2012, and rights for the two additional adjacent concessions (Don Diego Norte and Don Diego Sur) were acquired in 2014.

Qualified Person

The scientific and technical disclosures about the Don Diego Phosphorite Project in this annual report on Form

10-K

have been reviewed and approved by Henry J. Lamb of Mineral Resource Associates. Mr. Lamb is a professional geologist with 40 years’ experience in the exploration, evaluation, development, maintenance, and operation of phosphate rock mines and beneficiation plants in multiple countries. Mr. Lamb is a “qualified person” as defined by RegulationS-K

Subpart 1300 and NI43-101.

For a description of the key assumptions, parameters and methods used to estimate mineral resources included in this Form10-K,

as well as data verification procedures and a general discussion of the extent to which the estimates may be affected by any known environmental, permitting, legal, title, taxation, socio-economic, marketing, political or other relevant factors, please review the43-101

Technical Report for the Don Diego Phosphorite Project attached as Exhibit 96.01 to this annual report on Form10-K.

Technical Report

The information that follows relating to the Don Diego Phosphorite Project is, for the most part, derived from, and, in some instances, may be extracted from, the

43-101

technical report entitled “Technical Report: Revised Assessment of the Don Diego West Phosphorite Deposit, Mexican Exclusive Economic Zone (EEZ)” (the “Don Diego Technical Report”), with an effective date of June 30, 2014. Readers should consult the Don Diego Technical Report to obtain further information regarding the Don Diego Phosphorite Project, which is available at www.sec.gov and attached as Exhibit 96.01 to this annual report on Form10-K.

The Don Diego Technical Report is not incorporated by reference into this annual report on Form10-K.

Following the submission of the 2014 Technical Report, additional samples from the newly acquired Don Diego Norte concession were analyzed by Mr. Lamb and results were provided to us. No analysis has been done on the Don Diego Sur concession. The NI43-101

Technical Report and additional updates pertaining to the Norte concession were completed using standard guidelines and protocols.Location and Brief Description

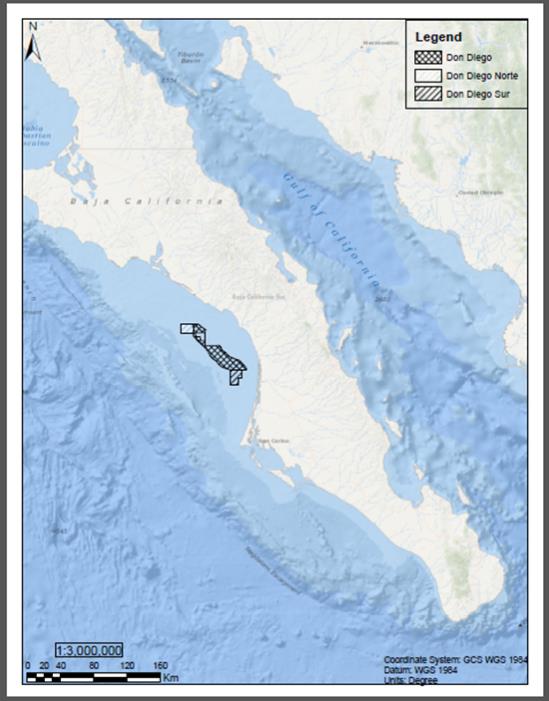

The Don Diego Phosphorite Project concession area is a sedimentary marine phosphorite deposit located in the Mexican EEZ offshore Baja California Sur, Mexico in the Pacific Ocean. The property is located using a multi-point polygonal property demarcation bounded by latitudes 26.1°, 25.60°, and longitudes

-112.12°,

-112.80°

WGS 1984. The property is roughly 20 to 45 kilometers from shore. Following is a map denoting the three concessions in Don Diego in relation to Baja California Sur, Mexico.13

Infrastructure and Access

There is no material infrastructure located on the property where the concessions are located. Access to the site is by

sea-going

vessels dispatched from various nearby ports of opportunity.Project engineering anticipates use of existing dredging technology to recover the phosphorite ore, including a trailer suction hopper dredger, and

on-site

mechanical beneficiation using a floating production and storage platform to produce phosphate rock concentrate.14

Description of Concessions

Total concessions encompass 1,147 km

2

of seafloor at a water depth of approximately 80 meters and consist of three concessions in total (see the previous map). The concessions were granted to ExO by the Mexican Secretary of Economy, General Coordination of Mining, and are valid for 50 years, with an option for a50-year

extension. The primary concession was granted in 2012, and rights for the other two concessions (Norte and Sur) were acquired thereafter in 2014. To commence further operations on the Don Diego Phosphorite Project, ExO must obtain approval of its Environmental and Social Impact Assessment (“ESAI”) from the Mexican Secretariat of Environment and Natural Resources. See ExO Phosphate Project in the above ITEM 1. BUSINESS for additional information.The property is subject to rents, fees and other payments to the Government of Mexico or its designated government ministry or agency. The anticipated annual obligations for each of the years in the three-year period ending December 31, 2024 are set forth in the table below.

Primary Concession

Year | Area (Hectares) | Annual Rent, MxN Pesos, owed semesterly | ||

| 2022 | 80,050.5 | 30,236,658 | ||

| 2023 | 80,050.5 | The above is based on 188.86 MxN per hectare per semester. 2023 will be a similar rate but increase by some inflationary factor e.g. increase the rate per hectare by about 5% | ||

| 2024 | 80,050.5 | The above is based on 188.86 MxN per hectare per semester. 2024 will be a similar rate but increase by some inflationary factor e.g. increase the rate per hectare by about 5% | ||

Norte Concession

Year | Area (Hectares) | Annual Rent, Mx Pesos, owed semesterly | ||

| 2022 | 14,300 | 3,069,352 | ||

| 2023 | 14,300 | Will be based on 107.32 MxN per hectare per semester, with an increase in this rate from inflation | ||

| 2024 | 14,300 | Will be based on 188.86 MxN per hectare per semester, with an increase in this rate from inflation | ||

Sur Concession

Year | Area (Hectares) | Annual Rent, Mx Pesos, owed semesterly | ||

| 2022 | 20,425 | 4,384,022 | ||

| 2023 | 20,425 | Will be based on 107.32 MxN per hectare per semester, with an increase in this rate from inflation | ||

| 2024 | 20,425 | Will be based on 188.86 MxN per hectare per semester, with an increase in this rate from inflation | ||

15

Work Completed

The Don Diego Phosphorite Project is in the exploration stage with sufficient data to confirm the geological continuity of the deposit and the estimation of measured, indicated and inferred resource tonnes of resource. ExO, through exploration operations conducted by Odyssey, explored the area, characterized the environmental baseline to enable drafting of the ESAI, and acquired approximately 200 vibracore samples for assay. These cores were split into over 800 individual strata core units each of approximately 1 meter length. The cores were assayed at Florida Industrial and Phosphate Research Institute in Bartow, Florida under the guidance of Mr. Lamb.

Previous Operations

The mineral concession granted by the Government of Mexico to ExO is believed to be the first for the subject property. Nearby concessions have been granted to Innophos Holdings, Inc. (“Innophos”) and PhosMex Corporation (“PhosMex”) that are adjacent to and are a window within the Don Diego mineral concession. Innophos may have conducted an exploration program on its adjacent property of an estimated 13,474 hectares. However, the details and any findings have not been distributed in the public domain. There is no evidence of significant mineral exploration activities within the concession area held by PhosMex.

Assessment Results

The Don Diego Technical Report describes the exploration program for the Don Diego Mineral Concession as the most detailed phosphorite production-based exploration program to be executed in the Offshore Baja California Phosphorite District. The exploration concept was to explore the area using known technologies applied to the marine environment to locate a suitable phosphorite deposit capable of sustaining the production of 3.0 to 3.5 million tonnes per year of phosphate rock concentrates with suitable chemical characteristics for the production of phosphoric acid using one of the established wet processes for a period of not less than 20 years.

The keys conclusions of the Don Diego Technical Report, which covered a portion of the original primary concession area granted in 2012 are:

| • | The Don Diego Mineral Concession contains an enriched, sedimentary marine phosphorite with the potential to yield a commercial phosphate rock concentrate using known procedures for mining (dredging) and mineral processing (washing, sizing, attrition, flotation and density separation). |

| • | The measured phosphorite resource for the Don Diego West Phosphorite Deposit is estimated at 106.9 million tonnes at 18.44% P 2 O5 contained within an area of 27.83 km2 . The average overburden thickness is 1.04 meters overlying an average of 2.75 meters of phosphorite. |

| • | The indicated phosphorite resource for the Don Diego West Phosphorite Deposit is estimated at 220.3 million ore tonnes at 18.71% P 2 O5 contained within an area of 55.49 km2 . The average overburden thickness is 1.16 meters overlying an average of 2.82 meters of phosphorite. |

| • | The inferred phosphorite resource for the Don Diego West Phosphorite Deposit is estimated at 166.4 million ore tonnes at 18.89% P 2 O5 contained within an area of 40.74 km2 . The average overburden thickness is 1.34 meters overlying an average of 2.97 meters of phosphorite. |

| • | The geologic boundaries of the Don Diego West Phosphorite Deposit appear to be open to the northwest, to the southeast, at depth and to the west. Future drilling results coupled with appropriate sampling and laboratory testing have the potential to further define the geologic continuity of the deposit and increase the mineral resource estimate. |

| • | Preliminary assaying and metallurgical testing of the core samples at approximately one-meter intervals indicates the potential to produce a phosphate rock concentrate at 28% to 30% P2 O5 with a favorable CaO/P2 O5 ratio of 1.5 to 1.55 and a Minor Element Ratio (MER) of 0.07 to 0.08. The chemical analysis suggests that the concentrate would be suitable for the production of phosphoric acid using the wet process methods. |

16

| • | Additional analysis was performed by the qualified person on the Norte concession. Conclusions were reported as below and are in addition to the Technical Report; the table reported in the Phosphorite Resources |

| • | The measured phosphorite resource for the Don Diego Norte Concession is estimated at 8 million tonnes at 14.95% P 2 O5 contained within an area of 2.25 km2 . The average overburden thickness is 0.89 meters overlying an average of 2.51 meters of phosphorite. |

| • | The indicated phosphorite resource for the Don Diego Norte Concession is estimated at 23.3 million ore tonnes at 15.04% P 2 O5 contained within an area of 6.58 km2 . The average overburden thickness is 0.89 meters overlying an average of 2.49 meters of phosphorite. |

| • | The inferred phosphorite resource for the Don Diego Norte Concession is estimated at 63.4 million ore tonnes at 14.94% P 2 O5 contained within an area of 17.89 km2 . The average overburden thickness is 0.87 meters overlying an average of 2.53 meters of phosphorite. |

Material Assumptions, Parameters, and Methods

The Don Diego Technical Report (Section 17.3) sets forth the material assumptions, parameters, and methods used to estimate phosphorite resources as follows:

| • | The category estimates are based on 199 drill holes representing 746.6 meters of drilling and 761 sample intervals. Based on laboratory physical and chemical tests results, the raw data was calculated for each sample interval (strata) and the quantity and quality of each component was reported. Detailed size distribution data was summarized into coarse waste (+20 mesh), flotation feed (-20+150 mesh) and fine waste(-150 mesh) and the estimated quantity and quality for each was reported. |

| • | Flotation tests have established certain parameters (concentrate %P 2 O5 and insol, tailings % P2 O5 and insol, and recovery factors) from a broad geographic range of sample locations at various depths and ore grades. These parameters were used to establish formulae for estimating the concentrate tonnes, % P2 O5 and insol for each strata containing an acceptable ore quantity and quality. [Based on critical physical and chemical characteristics that are directly correlated with Capital Investment and Operating Cost, each strata was classified as waste, marginal and mineable. Waste strata having a high Ore to Concentrate tonnage Ratio, a high Flotation Feed to Concentrate tonnage Ratio, or a low Concentrate P2 O5 content and lying above a marginal or mineable strata is identified as overburden. The overburden could be removed and discarded in anon-mineralized (sterile) area prior to mining and processing the underlying phosphorite strata. The marginal strata will have a lower economic value but when blended with the mineable strata in a well-defined mine plan could make a positive economic contribution. The mineral strata have favorable physical, chemical and economic characteristics. |

| • | The resource calculation procedure is based on the geologic data and laboratory testing of the core samples obtained from the drilling program, the reduction of the data into strata calculation reports and compilation of the marginal and mineable strata into mineable hole composites. |

| • | Using a conventional polygonal area of influence to weight each mineable hole, the measured, indicated and inferred phosphorite resources were calculated. The chemical characteristics are weight averaged with the tonnes as the weighting factor. |

| • | Measured resources are based on those holes within the transverse cross-sections where the distance between drill holes is approximately 500 meters and the geologic continuity along the primary axis is considered to be 500 meters. Thus, the area of influence is 0.25 km 2 . |

| • | Indicated resources have an area of influence for each drill hole equal to 1.0 km 2 (500 meters by 2,000 meters). The area of influence for the inferred resources is variable and typically extends midway between transect lines. |

| • | The resources have been estimated as if the final product is to be a feedstock for a wet process phosphoric acid plant to produce end product phosphoric acid for the fertilizer market. The resources are subject to modification based on the requirements of the end user process such as direct application or SSP (single superphosphate). |

17

Description of Sampling Methods

Piston Core and

One-Pass

Samples.one-pass

core barrel did not have liners; therefore, the material was hydraulically extruded into a core tray. For eachone-pass

core, the core was photographed and described. For both types of samples, visual descriptions used a10-power

hand lens and grain size card to determine grain size, sorting, roundness, presence of pelletal phosphorite, and shell fragment size. Colors were determined using Munsell soil color charts. Benthic infauna found within the samples were photographed, measured and identified. The archived core liner was capped and secured on both ends and labeled with appropriate identification. The archived piston core tubes, containing the undisturbed samples, were stored until returning to port (San Diego, California) where the samples were securely packaged, with a chain of custody identifying the contents of each package, and shipped by a commercial carrier to the Florida Industrial and Phosphate Research Institute (FIPR) laboratory in Bartow, Florida.Rossfelder Core Samples.

1.2-m

sections and point sampled. Visual descriptions used a10-power

hand lens and grain size card to determine grain size, sorting, roundness, presence of pelletal phosphorite, and shell fragment size. Colors were determined using Munsell soil color charts. Benthic infauna found within the samples were photographed, measured and identified. The1-m