UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File No.: 811-04809

Liberty All-Star Equity Fund

(Exact name of registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

Alex Marks

ALPS Fund Services, Inc.

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: December 31

Date of reporting period: January 1 - December 31, 2014

Item 1. Report of Shareholders.

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 1 |

PRESIDENT’S LETTER (UNAUDITED) | | | |

| | |

Fellow Shareholders: | | February 2015 |

Although roiled by periodic sell-offs, U.S. equity markets rose once again in 2014, as the S&P 500® Index and the widely followed Dow Jones Industrial Average (DJIA) posted numerous record highs throughout the year. The S&P 500 returned 13.69 percent while the DJIA gained 10.04 percent. The technology-focused NASDAQ Composite Index returned 14.75 percent.

The S&P 500 Index recorded positive returns each quarter in 2014, with the first and third quarters in the range of 1 percent-plus while the second and fourth quarters were in the mid-single digits. The U.S. economy was the main source of strength for equities. An abnormally harsh winter caused gross domestic product (GDP) to decline 2.1 percent in the first quarter. Growth was strong in the second and third quarters, however, when GDP rose 4.6 percent and 5.0 percent, respectively. The employment picture in the U.S. also brightened. Except for January, which was distorted by the weather, every month in 2014 was marked by the creation of more than 200,000 non-farm jobs. The ongoing job growth meant that by May all of the 8.7 million jobs lost during the Great Recession had finally been recouped. Throughout the fiscal year, the Federal Reserve (Fed) kept short-term interest rates at record low levels, even as it continued to wind down its program of quantitative easing (QE), first launched in December 2008. In October, the Fed ended the program altogether. Another powerful theme running throughout the year was the industrial renaissance in the U.S., as auto, capital equipment and energy output gained strength. U.S. energy production stood out as a growth driver, as hydraulic fracturing methodologies unlocked previously inaccessible or economically impractical oil and gas deposits. The price of oil began a gradual descent at mid-year, a move that accelerated in the fourth quarter. From a peak of $106 per barrel in June, the price of West Texas Intermediate (WTI) crude fell to an average of $59 per barrel in December (and continued to slide in early 2015).

The steep, rapid decline in the price of oil was interpreted by many to be a sign of slowing economic growth

worldwide and investors responded by selling equities in one of the several sell-offs that made 2014 a positive, but choppy year. Fears of higher interest rates and geopolitical tensions, chiefly in Ukraine, fueled a retrenchment in the first quarter. A significant sell-off in biotechnology, information technology and social networking stocks hit the NASDAQ Composite in April. And falling oil prices led to a one-week decline of 3.1 percent in the S&P 500 in early October.

One characteristic of the 2014 investment environment that warrants comment was how challenging it was for active managers and actively managed funds. According to data provider Lipper, 2014 was the worst year for active managers relative to the market in three decades, while data from research firm Morningstar indicates that less than 20 percent of U.S. equity fund managers beat their benchmark. As Liberty All-Star® Equity Fund is actively managed, we asked the Fund’s five investment managers to comment on this in our annual Manager Roundtable, which begins on page 9 of this report. We recommend their thoughts and insights to you.

Liberty All-Star® Equity Fund

After strongly outperforming the market in 2013, Liberty All-Star® Equity Fund returns lagged in 2014. The Fund returned 8.87 percent with shares valued at net asset value (NAV) with dividends reinvested and 6.98 percent with shares valued at market price with dividends reinvested. (Fund returns are net of fees.) The Lipper Large-Cap Core Mutual Fund Average returned 11.32 percent. The Fund posted positive returns for three quarters, but experienced a negative return of -1.38 percent in the third quarter, hurt in part by the sell-off in energy stocks. The discount at which Fund shares traded relative to their underlying NAV widened compared with 2013, ranging from a low of -10.5 percent to a high of -13.6 percent.

Looking longer term, the Fund’s average annual returns are in-line with most indices, as they lag the S&P 500 by just 42 basis points for the trailing three-year period (with

| | |

www.all-starfunds.com | | USA |

| | | | |

| 2 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | PRESIDENT’S LETTER (UNAUDITED) |

| | | | |

shares valued at market price with dividends reinvested) and are ahead of the Lipper average by 87 basis points for the same period. By the same measure, the Fund trails the S&P 500 for the past five years, but once again is ahead of the Lipper.

As previously discussed, it had been a challenging environment for active managers’ relative performance during 2014 and, actually, for most years subsequent to the 2008 financial crisis. The massive liquidity provided by the Federal Reserve in response to the crisis certainly pushed stock indices to record highs and interest rates to record lows. It has, however, been a challenging period for active managers, as the transmission mechanism for that liquidity into domestic stocks has been largely through index funds and index exchange-traded funds (ETFs) rather than actively managed products. Looking longer term, there are also periods when active managers, on balance, have outperformed stock indices, which points to the cyclical nature of those performance patterns. The last such period was from 2000-2007, a time frame beginning after the bursting of the technology bubble and, coincidentally, was approximately the same duration as the current post-crisis period. It is worth noting that for the past 15 years, from January 1, 2000, to December 31, 2014, the Fund’s NAV reinvested return after fund expenses exceeds both the Lipper average and the S&P 500. No one can predict the timing of when or for how long active managers generally out- or underperform stock indices, but viewing active managers’ relative performance in the context of a combined cycle is relevant.

Fund distributions totaled $0.39 per share in 2014. As shareholders may recall, the Fund’s distribution policy has been in place since 1988 and is a major component of the Fund’s total return. These distributions add up to $24.66 since 1987 (the Fund’s first full calendar year of operations). We continue to emphasize that shareholders should include these distributions when determining the return on their investment in the Fund.

One of the key principles on which the Fund was founded is multi-management, or the practice of allocating the Fund’s assets to carefully selected investment managers

representing both value and growth styles of investing. Thus, we are once again offering insights into the managers’ thinking through the previously mentioned roundtable discussion, and invite shareholders to read the managers’ comments.

In a difficult environment for active managers, the Fund lagged key benchmarks in 2014. After a strong 2013, however, the Fund’s market price returns over the past two years average 19.52 percent. If the start of the year is any indicator, 2015 may be highly volatile. We are confident in the Fund’s five investment managers’ ability to navigate whatever market conditions prevail in the year ahead. For our part, we will continue to manage the Fund with our sights set on rewarding long-term returns for shareholders.

Sincerely,

William R. Parmentier, Jr.

President and Chief Executive Officer

Liberty All-Star® Equity Fund

| | | | | | |

ANNUAL REPORT | |

| | DECEMBER 31, 2014 | | |

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 3 |

PRESIDENT’S LETTER (UNAUDITED) | | | |

| | | | | | | | | | | | | | |

| |

FUND STATISTICS AND SHORT-TERM PERFORMANCE PERIODS ENDED DECEMBER 31, 2014 | | | |

| |

FUND STATISTICS: | | | |

| | | | |

Net Asset Value (NAV) | | | | | | | $6.84 | | | | | | | |

Market Price | | | | | | | $5.98 | | | | | | | |

Discount | | | | | | | -12.6% | | | | | | | |

| | | | |

| | | Quarter | | | | | | 2014 | | | |

Distributions* | | | $0.09 | | | | | | | | $0.39 | | | |

Market Price Trading Range | | | $5.22 to $6.09 | | | | | | | | $5.22 to $6.09 | | | |

Premium/(Discount) Range | | | -11.8% to -13.6% | | | | | | | | -10.5% to -13.6% | | | |

| | | | |

PERFORMANCE: | | | | | | | | | | | | | | |

| | | | |

Shares Valued at NAV with Dividends Reinvested | | | 4.30% | | | | | | | | 8.87% | | | |

Shares Valued at Market Price with Dividends Reinvested | | | 4.16% | | | | | | | | 6.98% | | | |

Dow Jones Industrial Average | | | 5.20% | | | | | | | | 10.04% | | | |

NASDAQ Composite Index | | | 5.70% | | | | | | | | 14.75% | | | |

Lipper Large-Cap Core Mutual Fund Average | | | 4.27% | | | | | | | | 11.32% | | | |

S&P 500® Index | | | 4.93% | | | | | | | | 13.69% | | | |

| | | | | | | | | | | | | | | | | | | | |

| |

LONG-TERM PERFORMANCE SUMMARY AND DISTRIBUTIONS PERIODS ENDED

DECEMBER 31, 2014 | | ANNUALIZED RATES OF RETURN | |

| 3 YEARS | | | 5 YEARS | | | 10 YEARS | | | 15 YEARS | | | 25 YEARS | |

| | | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Distributions | | | $1.06 | | | | $1.71 | | | | $5.32 | | | | $10.49 | | | | $21.89 | |

Shares Valued at NAV with Dividends Reinvested | | | 18.67% | | | | 12.84% | | | | 5.95% | | | | 4.80% | | | | 9.21% | |

Shares Valued at Market Price with Dividends Reinvested | | | 19.99% | | | | 14.08% | | | | 4.25% | | | | 5.51% | | | | 9.28% | |

Dow Jones Industrial Average | | | 16.29% | | | | 14.22% | | | | 7.91% | | | | 5.44% | | | | 10.42% | |

Lipper Large-Cap Core Mutual Fund Average | | | 19.12% | | | | 13.90% | | | | 7.05% | | | | 4.29% | | | | 9.21% | |

NASDAQ Composite Index | | | 23.60% | | | | 17.19% | | | | 9.17% | | | | 1.82% | | | | 10.18% | |

S&P 500® Index | | | 20.41% | | | | 15.45% | | | | 7.67% | | | | 4.24% | | | | 9.62% | |

| * | All 2014 distributions consist of ordinary dividends and long-term capital gains. A breakdown of each 2014 distribution for federal income tax purposes can be found in the table on page 39. |

Returns for the Fund are total returns, which include dividends. Performance returns are net of management fees and other Fund expenses.

Figures shown for the Lipper Large-Cap Core Mutual Fund Average are based on open-end mutual funds’ total returns, which include dividends, and are net of Fund expenses. Figures shown for the unmanaged Dow Jones Industrial Average, NASDAQ Composite Index and the S&P 500® Index are total returns, including dividends. A description of the Lipper benchmark and the market indices can be found on page 39.

Past performance cannot predict future results. Performance will fluctuate with market conditions. Current performance may be lower or higher than the performance data shown. Performance information does not reflect the deduction of taxes that shareholders would pay on Fund distributions or the sale of Fund shares. An investment in the Fund involves risk, including loss of principal.

Closed-end funds raise money in an initial public offering and shares are listed and traded on an exchange. Open-end mutual funds continuously issue and redeem shares at net asset value. Shares of closed-end funds frequently trade at a discount to net asset value. The price of the Fund’s shares is determined by a number of factors, several of which are beyond the control of the Fund. Therefore, the Fund cannot predict whether its shares will trade at, below or above net asset value.

| | |

www.all-starfunds.com | | USA |

| | | | |

| 4 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | UNIQUE FUND ATTRIBUTES (UNAUDITED) |

| | | | |

| | | | | | | | |

| | | | | |

| | | | | Unique Attributes of Liberty All-Star® Equity Fund | | | | |

| | | | | |

| | | | | Several attributes help to make the Fund a core equity holding for investors seeking diversification, income and the potential for long-term appreciation. | | | | |

| | | | | | | | | |

| | | | | | |

| |

| | Multi-management for Individual Investors | | |

| |

| | |

| | | |

| | | | Liberty All-Star® Equity Fund is multi-managed, an investment discipline that is followed by large institutional investors to diversify their portfolios. In 1986, Liberty All-Star® Equity Fund became the first closed-end fund to bring multi-management to individual investors. | | |

| | | |

| |

| | Real-time Trading and Liquidity | | |

| |

| | |

| | | |

| | | | The Fund has a fixed number of shares that trade on the New York Stock Exchange and other exchanges. Share pricing is continuous—not just end-of-day, as it is with open-end mutual funds. In addition, Fund shares offer immediate liquidity and there are no annual sales fees. | | |

| | | | | | |

ANNUAL REPORT | |

| | DECEMBER 31, 2014 | | |

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 5 |

UNIQUE FUND ATTRIBUTES (UNAUDITED) | | | |

| | | | |

| | Access to Institutional Managers | | |

|

|

| | |

| | The Fund’s investment managers invest primarily for pension funds, endowments, foundations and other institutions. Because institutional managers are closely monitored by their clients, they tend to be more disciplined and consistent in their investment process. | | |

| | |

| | Monitoring and Rebalancing | | |

|

|

| | |

| | ALPS Advisors continuously monitors these investment managers to ensure that they are performing as expected and adhering to their style and strategy, and will replace managers when warranted. Periodic rebalancing maintains the Fund’s structural integrity and is a well-recognized investment discipline. | | |

| | |

| | Alignment and Objectivity | | |

|

|

| | |

| | Alignment with shareholders’ best interests and objective decision-making help to ensure that the Fund is managed openly and equitably. In addition, the Fund is governed by a Board of Trustees that is elected by and responsible to shareholders. | | |

| | |

| | Distribution Policy | | |

|

|

| | |

| | Since 1988, the Fund has followed a policy of paying annual distributions on its shares at a rate that approximates historical equity market returns. The current annual distribution rate is 6 percent of the Fund’s net asset value (paid quarterly at 1.5 percent per quarter), providing a systematic mechanism for distributing funds to shareholders. | | |

| | |

www.all-starfunds.com | | USA |

| | | | |

| 6 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | | INVESTMENT MANAGERS/PORTFOLIO CHARACTERISTICS (UNAUDITED) |

| | | | |

THE FUND’S ASSETS ARE APPROXIMATELY EQUALLY DISTRIBUTED AMONG THREE VALUE MANAGERS AND TWO GROWTH MANAGERS:

MANAGERS’ DIFFERING INVESTMENT STRATEGIES ARE REFLECTED IN PORTFOLIO CHARACTERISTICS

The portfolio characteristics table below is a regular feature of the Fund’s shareholder reports. It serves as a useful tool for understanding the value of a multi-managed portfolio. The characteristics are different for each of the Fund’s five investment managers. These differences are a reflection of the fact that each pursues a different investment style. The shaded column highlights the characteristics of the Fund as a whole, while the final column shows portfolio characteristics for the S&P 500® Index.

| | | | | | | | | | | | | | | | | | |

| | | | INVESTMENT STYLE SPECTRUM | | | | | | | | | | | | |

| PORTFOLIO CHARACTERISTICS AS OF DECEMBER 31, 2014 | | VALUE | | | | GROWTH | | | | | | | | |

| |

| | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | |

| | | Schneider | | Pzena | | Matrix | | Cornerstone | | TCW | | Total Fund | | S&P

500® Index | | |

| | | | | | | | |

Number of Holdings | | 36 | | 41 | | 35 | | 43 | | 31 | | 158* | | 502 | | |

| | | | | | | | |

Percent of Holdings in Top 10 | | 55% | | 36% | | 36% | | 39% | | 44% | | 17% | | 18% | | |

| | | | | | | | |

Weighted Average Market Capitalization (billions) | | $44 | | $86 | | $106 | | $67 | | $64 | | $74 | | $131 | | |

| | | | | | | | |

Average Five-Year Earnings Per Share Growth | | 5% | | 13% | | 17% | | 25% | | 19% | | 18% | | 15% | | |

| | | | | | | | |

Dividend Yield | | 1.5% | | 1.9% | | 2.1% | | 0.7% | | 0.6% | | 1.4% | | 2.0% | | |

| | | | | | | | |

Price/Earnings Ratio** | | 15x | | 13x | | 17x | | 25x | | 33x | | 18x | | 19x | | |

| | | | | | | | |

Price/Book Value Ratio | | 1.4x | | 2.0x | | 2.1x | | 4.0x | | 5.7x | | 2.6x | | 3.0x | | |

| * | Certain holdings are held by more than one manager. |

| ** | Excludes negative earnings. |

| | | | | | |

ANNUAL REPORT | |

| | DECEMBER 31, 2014 | | |

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 7 |

INVESTMENT GROWTH (UNAUDITED) | | | |

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT

The graph below illustrates the growth of a hypothetical $10,000 investment assuming the purchase of shares of beneficial interest at the closing market price (NYSE: USA) of $6.00 on December 31, 1987, and tracking its progress through December 31, 2014. For certain information, it also assumes that a shareholder exercised all primary rights in the Fund’s rights offerings (see below). This graph covers the period since the Fund commenced its 10 percent distribution policy in 1988. Effective with the 2009 second quarter distribution, the annual distribution rate was changed from 10 percent to 6 percent.

| | |

| | The growth of the investment assuming all distributions were received in cash and not reinvested back into the Fund. The value of the investment under this scenario grew to $50,217 (including the December 31, 2014 value of the original investment of $9,967 plus distributions during the period of $39,133 and tax credits on retained capital gains of $1,117). |

| |

| | The additional value realized through reinvestment of all distributions and tax credits. The value of the investment under this scenario grew to $145,963. |

| |

| | The additional value realized through full participation in all the rights offerings under the terms of each offering. The value of the investment under this scenario grew to $210,287 excluding the cost to fully participate in all the rights offerings under the terms of each offering which was $49,966. |

Past performance cannot predict future results. Performance will fluctuate with changes in market conditions. Current performance may be lower or higher than the performance data shown. Performance information does not reflect the deduction of taxes that shareholders would pay on Fund distributions or the sale of Fund shares. An investment in the Fund involves risk, including loss of principal.

| | |

www.all-starfunds.com | | USA |

| | | | |

| 8 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | TABLE OF DISTRIBUTIONS AND RIGHTS OFFERINGS (UNAUDITED) |

| | | | |

| | | | | | | | | | | | | | |

| | | | | |

| | | | | | | RIGHTS OFFERINGS | | | | |

| | | YEAR | | PER SHARE

DISTRIBUTIONS | | MONTH

COMPLETED | | SHARES NEEDED TO PURCHASE

ONE ADDITIONAL SHARE | | SUBSCRIPTION

PRICE | | TAX CREDITS* | | |

| | | 1988 | | $0.64 | | | | | | | | | | |

| | | 1989 | | 0.95 | | | | | | | | | | |

| | | 1990 | | 0.90 | | | | | | | | | | |

| | | 1991 | | 1.02 | | | | | | | | | | |

| | | 1992 | | 1.07 | | April | | 10 | | $10.05 | | | | |

| | | 1993 | | 1.07 | | October | | 15 | | 10.41 | | $0.18 | | |

| | | 1994 | | 1.00 | | September | | 15 | | 9.14 | | | | |

| | | 1995 | | 1.04 | | | | | | | | | | |

| | | 1996 | | 1.18 | | | | | | | | 0.13 | | |

| | | 1997 | | 1.33 | | | | | | | | 0.36 | | |

| | | 1998 | | 1.40 | | April | | 20 | | 12.83 | | | | |

| | | 1999 | | 1.39 | | | | | | | | | | |

| | | 2000 | | 1.42 | | | | | | | | | | |

| | | 2001 | | 1.20 | | | | | | | | | | |

| | | 2002 | | 0.88 | | May | | 10 | | 8.99 | | | | |

| | | 2003 | | 0.78 | | | | | | | | | | |

| | | 2004 | | 0.89 | | July | | 10** | | 8.34 | | | | |

| | | 2005 | | 0.87 | | | | | | | | | | |

| | | 2006 | | 0.88 | | | | | | | | | | |

| | | 2007 | | 0.90 | | December | | 10 | | 6.51 | | | | |

| | | 2008 | | 0.65 | | | | | | | | | | |

| | | 2009*** | | 0.31 | | | | | | | | | | |

| | | 2010 | | 0.31 | | | | | | | | | | |

| | | 2011 | | 0.34 | | | | | | | | | | |

| | | 2012 | | 0.32 | | | | | | | | | | |

| | | 2013 | | 0.35 | | | | | | | | | | |

| | | 2014 | | 0.39 | | | | | | | | | | |

| | Total | | $23.48 | | | | | | | | | | |

| * | The Fund’s net investment income and net realized capital gains exceeded the amount to be distributed under the Fund’s distribution policy. In each case, the Fund elected to pay taxes on the undistributed income and passed through a proportionate tax credit to shareholders. |

| ** | The number of shares offered was increased by an additional 25% to cover a portion of the over-subscription requests. |

| *** | Effective with the second quarter distribution, the annual distribution rate was changed from 10 percent to 6 percent. |

DISTRIBUTION POLICY

The current policy is to pay distributions on its shares totaling approximately 6 percent of its net asset value per year, payable in four quarterly installments of 1.5% of the Fund’s net asset value at the close of the New York Stock Exchange on the Friday prior to each quarterly declaration date. Sources of distributions to shareholders may include ordinary dividends, long-term capital gains and return of capital. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the Fund’s investment experience during the remainder of its fiscal year and may be subject to changes based on tax regulations. If a distribution includes anything other than net investment income, the Fund provides a Section 19(a) notice of the best estimate of its distribution sources at that time. These estimates may not match the final tax characterization (for the full year’s distributions) contained in shareholders’ 1099-DIV forms after the end of the year. If the Fund’s net investment income and net realized capital gains for any year exceed the amount distributed under the distribution policy, the Fund may, in its discretion, retain and not distribute capital gains and pay income tax thereon to the extent of such excess.

| | | | | | |

ANNUAL REPORT | |

| | DECEMBER 31, 2014 | | |

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 9 |

MANAGER ROUNDTABLE (UNAUDITED) | | | |

Manager Roundtable

Periods of volatility—brief, but extreme—appeared periodically throughout 2014, the final spasm being driven by sharp declines in the price of oil and its implications for slowing economic growth around the world. How do the Fund’s investment managers view this, and what do they think it portends for 2015? Almost uniformly, their response is to invest in high conviction stocks—quality names with sound fundamentals and competitive business models—at those times when volatility creates buying opportunities.

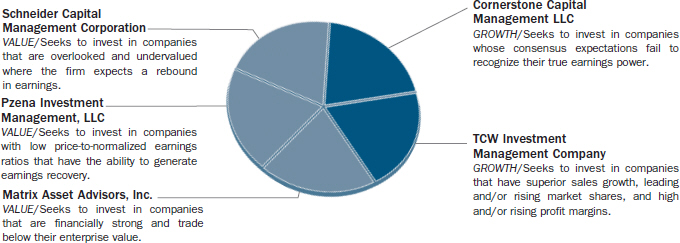

Liberty All-Star® Equity Fund’s five investment managers represent long experience, deep knowledge, a proven track record and, given that they represent both growth and value styles of investing, a broad point of view on the stock market and equity investing generally. Thus, once again, we are grateful to be able to call upon this resource to provide Fund shareholders with commentary and insight. The Fund’s Investment Advisor, ALPS Advisors, serves as moderator of the roundtable. Participating investment management firms, the portfolio manager for each, and their respective styles and strategies are:

CORNERSTONE CAPITAL MANAGEMENT LLC

Portfolio Manager/Thomas G. Kamp, CFA

President and Chief Investment Officer

Investment Style/Growth – Cornerstone’s portfolio is focused on stocks in which its research has identified Perception Gaps (underappreciated opportunities) for growth in the key metrics that drive the financial statements of the company. Stock selection is further based on the fundamentals of revenue, earnings, cash flow, and management depth and credibility.

MATRIX ASSET ADVISORS, INC.

Portfolio Manager/David A. Katz, CFA

President and Chief Executive Officer

Investment Style/Value – Matrix follows an opportunistic value-oriented investment philosophy. Matrix believes that value can be found in all sectors of the economy, and thus looks for investment opportunities beyond traditional value industries.

PZENA INVESTMENT MANAGEMENT, LLC

Portfolio Managers:

Richard S. Pzena, Founder and Co-Chief Investment Officer John P. Goetz, Managing Principal and Co-Chief Investment Officer Benjamin S. Silver, CFA, Principal and Co-Director of Research Investment Style/Value – Pzena uses fundamental research and a disciplined process to identify good companies with a sustainable business advantage that the firm believes are undervalued on the basis of current price to an estimated normal level of earnings.

SCHNEIDER CAPITAL MANAGEMENT CORPORATION

Portfolio Manager/Arnold C. Schneider, III, CFA

President and Chief Investment Officer

Investment Style/Value – The firm practices a disciplined, fundamental approach to add value over time. Research focuses on uncovering new ideas and owning undervalued stocks before they experience a rebound in earnings and come to the attention of other investors.

TCW INVESTMENT MANAGEMENT COMPANY

Portfolio Manager/Craig C. Blum, CFA

Managing Director

Investment Style/Growth – TCW seeks to invest in companies that have superior sales growth, leading and/ or rising market shares, and high and/or rising profit margins. TCW’s concentrated growth equity strategy seeks companies with distinct advantages in their business model.

There can be several interpretations of the volatility that hit equity markets in the fourth quarter: Sell-offs in late September/early October—principally taken down by economically sensitive sectors—and in December with the further collapse in world oil prices and its implications for slower growth around the world. But rallies followed both pull-backs. Based on your investment style and strategy, what’s your analysis of these scenarios and their implications for 2015? Let’s start with the growth style managers and hear first from Tom Kamp.

Kamp (Cornerstone – Growth): The upward movement in the market over the last two and a quarter years came with remarkably little volatility. However, we believe the long period of low volatility has ended. We expect the normal “to and fro” of the market to return now that the unprecedented

| | |

volatility- dampening influence of Quantitative Easing (QE) has been removed against the backdrop of a slow growth economy and rising global fiscal and monetary crosscurrents. We expect the market to be choppier as sentiment and fundamentals react to geopolitical, economic and company-specific data. This change is welcomed since our process thrives on the | | “We expect the market to be choppier [in reaction to] to geopolitical, economic and company-specific data. This is welcomed since our process thrives on short-term dislocations in high conviction stock ideas...” Tom Kamp (Cornerstone –Growth) |

short-term dislocations in high conviction stock ideas that normally exist.

| | |

www.all-starfunds.com | | USA |

| | | | |

| 10 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | | MANAGER ROUNDTABLE (UNAUDITED) |

| | | | |

After the significant upward movement in the equity market over the last six years, accompanied by significant valuation expansion, it is not likely that the equity market will have a strong return in the coming year. However, against a backdrop of near zero interest rates that have nowhere to go but up, the alternatives are not good. Barring a geopolitical crisis with Russia, our current expectation is for a 6 percent total return for the S&P 500 Index in 2015. This expectation is in-line with the current expectation of earnings growth. Current earnings expectations are probably still a bit high considering that energy sector earnings expectations need to fall somewhat further to reflect the current forward oil price curve. Offsetting this expected decline is a 1.9 percent dividend yield on the S&P 500. Therefore, if the valuation multiple of 16.4 times the next 12 months’ earnings per share is maintained, we may see something close to a 6 percent total return for the market in 2015.

| | |

Blum (TCW – Growth): The sell-off in oil was abrupt and far greater than most had imagined possible over a year ago. This has many possible ramifications. Most obviously, lower oil prices will lead to reduced revenue for oil-producing nations, i.e., Russia and Saudi Arabia, and, as investment | | “As we enter 2015, we expect higher volatility and, thus, more opportunities to add to our portfolio of companies with pricing power, resilient business models and growing end markets.” Craig Blum (TCW – Growth) |

in oil drilling potentially declines, earnings for oil service companies will be pressured. The U.S. dollar will likely continue to strengthen, becoming a potential headwind for many multinational corporations, particularly in the technology sector. Encouragingly, the oil price drop equates to cheaper gasoline prices, which should act as a massive tax break for the U.S. consumer. As we enter 2015, we expect higher volatility and, thus, more opportunities to add to our portfolio of companies with pricing power, resilient business models and growing end markets.

Let’s get the value perspective. David Katz, what is your view?

Katz (Matrix – Value): After a multi-year period of little downside volatility, the market returned to a more normal environment of generally favorable returns mixed with periodic macro- or fear-driven sell-offs. Ultimately, favorable fundamentals enabled stock prices to trade higher and overwhelm these pull-backs.

We would not read too much into this return to more typical volatility. Over the last 30-plus years, bouts of market volatility ebbed and flowed around the “hysteria du jour.” All have subsequently been resolved, and stocks have ultimately traded higher, achieving healthy returns

for investors over time. We expect this recently greater volatility to continue in 2015, sparked by concerns about the Fed raising interest rates, international economic growth and geopolitical uncertainty. In the end though, fundamentals and valuations will drive stock prices, similar to the fourth quarter of 2014. We believe these latter considerations are generally favorable and should allow for positive stock returns.

While these scares are unsettling, they create investment opportunities for a disciplined and seasoned investor. We attempt to take advantage of these sell-offs by buying into stocks or sectors where the decline is overdone, and where there is compelling upside potential when the dust settles.

Pzena (Pzena – Value): Resilience of the U.S. economy, as witnessed by strong GDP and employment growth, helped U.S. markets recover from bouts of uncertainty driven by questionable economic prospects outside the U.S. during 2014. Inevitably, markets will continue to react to economic and geopolitical news in the coming year, but our advice is to stick to a valuation-based investment approach that filters out the day-to-day noise and focuses on the long-term prospects of a company based on the strength of its underlying business franchise. Volatility has increased from abnormally low levels, and our experience has shown that investors tend to overreact to near-term events, thereby creating opportunities to invest in leading businesses at a fraction of their underlying value. We see these types of opportunities today in financial services, mature technology and energy companies, which make up the bulk of our portfolio’s exposures.

Schneider (Schneider Capital Management – Value): The sharp market movements in the latter portion of 2014 were symptomatic of investors’ shortened investment horizons. The resulting volatility caused some stock prices to move, either up or down, more than the underlying fundamentals support. However, low oil prices have widened overall credit spreads markedly in the second half of the year, which is a modest negative for equities and will likely lead to more episodes like these. Additionally, these oil prices have unleashed powerful geopolitical strains that will add to volatility.

As deep-value investors, we are constantly in search of stocks where our research indicates that a company is selling well below what we believe to be its true intrinsic value and where earnings will be improving in the next 12 months. Market volatility creates opportunities to purchase such stocks at temporarily lowered prices or, in some cases, to sell stocks at shorter-lived elevated prices.

| | | | | | |

ANNUAL REPORT | |

| | DECEMBER 31, 2014 | | |

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 11 |

MANAGER ROUNDTABLE (UNAUDITED) | | | |

Thank you very much. A question for the value style managers: The fact that you base buy/sell decisions on stock-by-stock bottom-up analysis notwithstanding, we would still like to inquire whether you believe the sell-off in the energy sector creates buying opportunities, or whether you view the decline in energy prices as more of a secular phenomenon that is likely to persist for some time to come. Let’s start with Arnie Schneider.

Schneider (Schneider Capital Management – Value): The market’s dramatic reaction to the short-term collapse in energy prices has created some very compelling investment opportunities in oil, gas and other energy-related companies that we believe offer significant upside potential.

At current prices, the industry cannot remotely begin to economically offset its 5 percent supply curve decline. We continue to maintain our long-term economic view of $90 per barrel for West Texas Intermediate crude, but expect the recovery to take a few years. In the interim, the modest 4 percent current spare capacity of nearly 4 million barrels per day will begin to dissipate as U.S. production growth slows and global demand increases.

The Saudis have remained steadfast in their statements and actions that they will not cut production to support prices. While they have the financial wherewithal to survive with oil at or below $60 per barrel for possibly five years, many other oil producing countries, especially Venezuela, Iran, Nigeria and Russia, require oil at or above $100 per barrel to keep their fragile economies going.

| | |

Katz (Matrix – Value): We believe this historic sell-off in oil prices has become overextended and that prices are far too low for the longer term. While short-term prices can be irrational, we believe simple supply/demand economics will kick in. Supply will fall as it becomes less attractive to drill, and demand will rise as consumers, businesses and | | “We believe this historic sell-off in oil prices has become overextended and that prices are far too low for the longer term. While short-term prices can be irrational, we believe simple supply/ demand economics will kick in.” David Katz (Matrix– Value) |

oil-consuming economies see a major expense falling sharply. We are already seeing this play out: New well permits are down significantly, capital expenditure programs for many drillers have been slashed by billions of dollars, consumers are driving more and new SUV and truck sales are growing. In addition, many OPEC nations have a strong incentive to see higher prices, and we think OPEC might change its current course over the next few months in a manner aimed at achieving that objective. Ultimately, we think the microeconomics of energy production argue for an oil price closer to $80 plus, and we expect movement toward that level during 2015.

After the recent sell-off, we believe that many energy stocks are selling at very attractive valuations. We hold very high quality, production-related companies that are well-situated to navigate these very low prices and their stock prices should be significantly higher in the more normal environment we foresee over the coming year. As we get greater clarity on the timing of oil’s recovery—and/ or believe catalysts are in place to realize value sooner—we might add to positions or add names in other areas of the sector.

Pzena (Pzena – Value): It is our belief that the market dynamic that led to the recent collapse in oil prices and ensuing sell-off in the energy sector is straightforward: consistently high oil prices attracted capital investment that stimulated production that has resulted in the supply of oil exceeding demand. Although we believe that oil prices should ultimately normalize at higher levels, it will take time for the market to stabilize and there are structural reasons why supply is not likely to be curtailed in the near future. As a result, there remains downside risk to both the oil price and to related equities in the near term. The bulk of our investments in the energy sector are in the integrated oil companies that have strong balance sheets and diversified business models that can also benefit should weaker players exit the market. Although our original investment thesis on the integrateds was not based on a forecast of high oil prices, we believe our holdings are attractive even if oil prices remain low for an extended period. Our research will continue to focus on businesses across the energy sector that have downside protection and are attractively valued based on a range of oil prices.

Now, a question for the growth style managers: The recent sell-off in equities spread way beyond the energy sector owing to its implications for slower economies around the world and, in some cases, outright deflation. Shouldn’t that have favorable implications for the stocks of companies that have strong positions in high growth markets? Or are investors saying that their growth will be impacted as well? Craig Blum, will you start us off?

Blum (TCW – Growth): Global central banks have been pumping money into the system for years, yet deflation has become the bigger risk of late given the precipitous drop in the price of oil. QE tapering concluded late last year and interest rates should arguably be higher, but the world is flush with cash and searching for yield with a backdrop of slower global growth, falling inflation and low liquidity. There are risks and we expect some

| | |

www.all-starfunds.com | | USA |

| | | | |

| 12 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | MANAGER ROUNDTABLE (UNAUDITED) |

| | | | |

volatility but note that the fundamentals for a majority of our companies are very strong. We view the recent volatility as a net positive for our concentrated portfolio of companies with defensible business models, pricing power, best of breed management teams and growing end markets.

Kamp (Cornerstone – Growth): The recent sell-off reflected fears that growth expectations—for revenue, earnings and cash flow—would have to be revised downward. Some industries and companies were affected more than others, however, because some are more likely to be impacted than others. The tension in the market is one of trying to determine when the negative estimate revisions are fully reflected in a given stock. Until those estimates have bottomed, the greatest risk exists in the stocks of those companies with the largest negative revisions. These stocks are often the fastest growers. Safety can be found in the stocks of less affected companies that can plow through the economic difficulty due to any of a variety of factors. Once the estimates have bottomed, however, investors will most highly prize those companies that can generate superior earnings growth in a slow growth environment, especially in one accompanied by low interest rates. Such is the focus of our research.

Two thousand fourteen was a challenging year for active managers, active management referring to investment funds for which a portfolio manager or team makes decisions about which stocks and in what weight will be held. The opposite is passive management or indexing, in which portfolio holdings mirror the components of a market index. From your perspective, why was 2014 such a difficult year for active managers? Let’s stay with the growth managers and invite Tom Kamp to go first.

Kamp (Cornerstone – Growth): The S&P 500 beat the expectations of many investors for a low double-digit return, in-line with earnings growth. Although I don’t have the data to support this statement, I suspect that most managers underperformed the most in the first quarter, which continued the momentum-driven market environment of valuation expansion that we saw in 2013. The subsequent quarters provided greater volatility, which benefits active managers with superior research-based insights.

It is also worth mentioning that the large size of Apple Computer in the benchmark makes it very difficult for active managers to take a positive active weight. This stock represents 6.24 percent of the Russell 1000®

Growth Index. Few managers had a positive active weight in this stock, which was a superb performer in 2014.

Craig Blum, what about TCW’s thoughts?

Blum (TCW – Growth): First, six years of QE has led to asset reflation and a global thirst for yield; currently about one-third of the stocks in the S&P 500 carry dividend yields greater than 10-year U.S. Treasuries. Second, interest rates have plummeted, boosting the performance of stocks seen as bond proxies, a majority of which come from the utility, telecom and consumer staples sectors. It is very unusual for defensive stocks to lead an advance in the S&P 500 of more than 14 percent. Third, although much has been made of stock correlations coming down, which is true, most people are unaware that during the majority of 2014 the delta, or difference, between the top and bottom decile performing stocks within the S&P 500 was near the lowest it has been in over 25 years, according to a study by Bank of America Merrill Lynch. This means there is little investor differentiation between the quality and business model advantages of companies. Lastly, and probably most obviously, as money has more moved to passive investing, the stocks in these market-cap weighted indices are unnaturally bid up.

Value managers, let’s hear from you on this question. David Katz, please lead off.

Katz (Matrix – Value): The past year was a difficult one for active managers, with a number of crosscurrents that rendered fundamental stock selection for both growth and value less effective over the period. Some of these factors follow:

While it was a “risk-on” year for stocks, the lower risk sectors, such as utilities and consumer staples, had the best returns. Both generally have a low revenue and earnings growth outlook, yet are selling at the upper ends of their historical valuation parameters. The valuations and fundamentals of these groups were unattractive to both value and growth investors, and their underweights hurt relative returns. Conversely, certain groups with very attractive valuation metrics, like energy and industrials, had a difficult period, which resulted in the cheap getting cheaper. This also hurt relative returns. Next, owning small and mid-sized companies likely hurt returns as these capitalizations lagged the major indices. Finally, specific industries like social media and biotech started the year selling at very rich valuations. Many extended their gains to levels that value investors found questionable but where growth investors thought there were more attractive alternatives.

| | | | | | |

ANNUAL REPORT | |

| | DECEMBER 31, 2014 | | |

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 13 |

MANAGER ROUNDTABLE (UNAUDITED) | | | |

The silver lining to the difficult 2014 environment is that it has further stretched some valuations to extremes. As in previous cycles, we believe this phenomenon has set the stage for active managers to produce very attractive returns in the upcoming year.

| | |

Pzena (Pzena – Value): There were two factors that we believe contributed to making 2014 a challenging year for active managers: the decline in interest rates from already low levels at the beginning of the year and the collapse in oil prices. Conventional wisdom at the outset of 2014 anticipated higher interest rates as the Federal Reserve’s quantitative | | “...two factors contributed to making 2014 a challenging year for active managers: the decline in interest rates from already low levels at the beginning of the year and the collapse in oil prices.” Rich Pzena (Pzena – Value) |

easing program wound down and the U.S. economy continued its gradual improvement. Instead, interest rates on 10-year treasuries fell from 3.0 percent to 2.2 percent, creating challenges for managers underexposed to stocks that typically do well in falling interest rate environments.

After three years of relatively stable prices, oil plunged 48 percent from $110 to $57 per barrel for Brent crude during the year as increases in the supply of oil outpaced slowing demand growth. As a result, energy was the worst performing sector for 2014, which may have also created challenges for active managers overexposed to this sector.

Schneider (Schneider Capital Management – Value):

| | |

In general, 2014 was a year in which managers that looked more like their benchmark did much better than those who were different than their benchmark. Investors demonstrated risk-averse tendencies, gravitating to stocks that quickly returned capital to shareholders via dividends or share repurchases. | | “In general, 2014 was a year in which managers that looked more like their benchmark did much better than those who were different than their benchmark.” Arnie Schneider (Schneider Capital Management – Value) |

The largest, mega-capitalization stocks were among the best performers, and diversification, especially in regard to sector weights, i.e., overweights or underweights, was a detriment to performance. The perceived “safe” sectors of health care, utilities and consumer staples performed much better than the broad market.

High active share1 was a drag on returns as the benchmark names tended to outperform non-benchmark names. Lastly, a lack of exposure to the top performing stocks in the indexes was a drag on returns for most active managers.

What is a stock in the portion of the Liberty All-Star Equity Fund that you manage that did especially well for you in 2014, and what is a stock whose prospects you like for 2015? Arnie Schneider, please go first for the value managers.

Schneider (Schneider Capital Management – Value): Our position in Marriott International helped performance in 2014. Strong demand and continued low supply drove revenue and margin improvement for Marriott and the hotel industry. The outlook for growth in rooms carrying Marriott brands also improved in 2014, driven by new hotels (primarily in international markets) as well as brand conversions and acquisitions of smaller brands. Marriott also continued to use growing free cash flow to reduce the share count.

We expect Citigroup to be a strong performer in 2015. Last year Citigroup was hurt by litigation and repositioning charges, a weak trading environment and its qualitative failure of the Fed stress test despite strong capital levels. We expect Citigroup to pass the stress test and begin share repurchases in 2015, as already strong capital ratios have continued to improve. Additionally, the completed repositioning or exiting of several underperforming businesses will drive significantly improved operating efficiency and earnings in 2015 and beyond.

Katz (Matrix – Value): One strong performer was Teva Pharmaceutical, which benefited from many positive factors, including investor and board activism, to drive shareholder value, favorable fundamentals and significant multiple expansion. After years of underperformance, Teva’s board reacted to shareholder pressure and named a new CEO charged with increasing value through stringent cost controls and aggressive portfolio repositioning. The company also had a number of favorable clinical and legal developments benefiting its flagship product, Copaxone. Consequently, the stock saw significant appreciation. While it was one of our top 2014 performers, it is still attractively valued and should continue its gains this year.

Qualcomm is particularly well positioned for 2015. It is the premier wireless communication equipment player worldwide, and a significant beneficiary of the continued rollout of smartphones. The company’s technological superiority and the global growth of the end market led

| 1 | High active share is an investment term that emerged from an academic study at Yale University. Active share relates to the difference between a manager’s portfolio holdings and those in the relevant benchmark. The greater the difference, the higher the active share. |

| | |

www.all-starfunds.com | | USA |

| | | | |

| 14 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | MANAGER ROUNDTABLE (UNAUDITED) |

| | | | |

to a decade-plus of strong revenue growth, double-digit earnings growth and massive free cash flow generation, accumulating to nearly $19 a share in net cash as of September 30, 2014. While Qualcomm’s dominant position and long-term outlook continue to be very favorable, the stock was only modestly higher last year, lagging the market and its peers. As a result of short-term setbacks, the stock didn’t participate in the technology sector’s strong gains in 2014 and sells at a modest 14.2 times 2015 earnings. Management is very shareholder oriented and has been aggressively both growing its dividend, currently at 2.3 percent, and executing a multi-billion dollar share repurchase program. We expect that business will continue to grow and that China’s regulatory investigation of the company’s pricing will be resolved. While we anticipate considerable fines and concessions to settle the dispute, we believe that the stock is poised for a meaningful move higher as these overhangs dissipate and the company delivers strong and growing earnings and cash flows.

Pzena (Pzena – Value): Hewlett-Packard (symbol: HPQ), a global leader in technology products and services, advanced 46 percent during the year as investors realized their fears of this strong franchises’ demise had been overblown. In addition, an increase in corporate spending on PCs helped the company deliver consensus-beating earnings results. Although we have harvested some profits, HPQ remains an attractive opportunity. Regarding opportunities heading into 2015, we believe the global banks, such as Bank of America, Citigroup and JPMorgan, represent some of the best risk/reward opportunities in our investment universe today. Although investors are focused on regulatory and legal uncertainties, we believe there is a real case for significant earnings upside through normalization of interest rates, securities trading activity and expense rationalization. Coupled with depressed valuations, we see these as compelling investment opportunities.

Craig Blum and Tom Kamp, wrap it up for us with insights into your growth portfolios.

Blum (TCW – Growth): Allergan, which we first purchased in December 2008, was our best performing stock in 2014. We were initially attracted to the company’s cash flow generation and strong portfolio of therapeutic products. In April, Valeant Pharmaceuticals (with Pershing Square in its corner) made an unsolicited bid for the company, valuing it at $47 billion. Seven months later, Actavis entered into an agreement to purchase Allergan for about $66 billion. For 2015 and beyond, we are particularly constructive on Illumina, the market leader in the rapidly growing end market of next generation

gene sequencing. Illumina’s technology is widely used in genetic research and increasingly used for broader functions, such as drug discovery, clinical diagnostics, forensics, agbio and personalized medicine. The pace of innovation in the industry has been staggering: 13 years ago, the sequencing cost per genome was about $100 million. Today, with Illumina’s HiSeqX, the human genome can now be sequenced in under three hours for about $1,000 per genome.

Kamp (Cornerstone – Growth): One of the top performing stocks in the portfolio was Gilead Sciences. We successfully traded around a core position in this name, driven by the fundamentals as we understood them throughout the year. We began the year with a modest position as a result of a trim in late 2013 as the reward-to-risk ratio declined in anticipation of the launch of the company’s blockbuster drug for Hepatitis C, Sovaldi. We used the pull-back in April and May that hit many biotech/pharma stocks and the fears that doctors would hold off treatment in advance of the anticipated all-oral version of the drug to add to our Gilead holdings. As the stock recovered to record levels, we trimmed and ultimately exited in early September, very close to the top in the stock’s price. We exited since the stock price was full relative to each of our valuation methodologies and competition from another company, Abbvie, was coming. Once the competitive product was announced and pharma benefits company Express Scripps signed Abbvie to an exclusive arrangement, Gilead’s stock price sank almost 20 percent. We used that weakness to re-enter the stock since we believed the reaction was overdone.

One of the stocks that we are most excited about is Affiliated Managers Group, Inc. (symbol: AMG), a global asset management company that invests in leading boutique investment management firms. We purchased AMG on a pullback in the company’s valuation in December caused by a slowing in net inflows, a slower rate of acquisitions and a choppy equity market. While net inflows have slowed somewhat, inflows remain well above peer levels. Management recently indicated that the acquisition pipeline is strong, setting up 2015 for a big year. Emerging catalysts of share repurchases and a structurally declining tax rate are also underappreciated by the market. As a result, we believe that AMG should regain its historical average relative market multiple of 1.1 to 1.2x versus its current multiple of 0.9x. With a high reward–risk-ratio, AMG is very attractive to us.

Many thanks to all for sharing excellent insights into your investment philosophy and for perspective that may be useful to individual investors.

| | | | | | |

ANNUAL REPORT | |

| | DECEMBER 31, 2014 | | |

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 15 |

TOP 20 HOLDINGS AND ECONOMIC SECTORS (UNAUDITED) | | | |

as of December 31, 2014

| | | | | | |

| | | |

| | | TOP 20 HOLDINGS * | | PERCENT OF NET ASSETS | | |

| | | |

| | | JPMorgan Chase & Co. | | 2.18% | | |

| | | |

| | | Salesforce.com, Inc. | | 2.05 | | |

| | | |

| | | State Street Corp. | | 1.96 | | |

| | | |

| | | Citigroup, Inc. | | 1.81 | | |

| | | |

| | | Google, Inc., Class A & C | | 1.74 | | |

| | | |

| | | Visa, Inc., Class A | | 1.73 | | |

| | | |

| | | Starbucks Corp. | | 1.57 | | |

| | | |

| | | SunTrust Banks, Inc. | | 1.52 | | |

| | | |

| | | Hewlett-Packard Co. | | 1.50 | | |

| | | |

| | | American International Group, Inc. | | 1.40 | | |

| | | |

| | | MetLife, Inc. | | 1.35 | | |

| | | |

| | | Precision Castparts Corp. | | 1.34 | | |

| | | |

| | | QUALCOMM, Inc. | | 1.27 | | |

| | | |

| | | Facebook, Inc., Class A | | 1.23 | | |

| | | |

| | | Marriott International, Inc., Class A | | 1.23 | | |

| | | |

| | | Microsoft Corp. | | 1.19 | | |

| | | |

| | | Bank of America Corp. | | 1.18 | | |

| | | |

| | | Morgan Stanley | | 1.13 | | |

| | | |

| | | Schlumberger Ltd. | | 1.13 | | |

| | | |

| | | Amazon.com, Inc. | | 0.98 | | |

| | | |

| | | | 29.49% | | |

| | | | | | |

| | | |

| | | ECONOMIC SECTORS * | | PERCENT OF NET ASSETS | | |

| | | |

| | | Financials | | 28.49% | | |

| | | |

| | | Information Technology | | 20.16 | | |

| | | |

| | | Consumer Discretionary | | 16.38 | | |

| | | |

| | | Health Care | | 11.88 | | |

| | | |

| | | Energy | | 10.40 | | |

| | | |

| | | Industrials | | 6.12 | | |

| | | |

| | | Consumer Staples | | 3.66 | | |

| | | |

| | | Materials | | 0.57 | | |

| | | |

| | | Utilities | | 0.08 | | |

| | | |

| | | Other Net Assets | | 2.26 | | |

| | | |

| | | | 100.00% | | |

| |

| | * Because the Fund is actively managed, there can be no guarantee that the Fund will continue to hold securities of the indicated issuers and sectors in the future. |

| | |

www.all-starfunds.com | | USA |

| | | | |

| 16 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | MAJOR STOCK CHANGES IN THE QUARTER (UNAUDITED) |

December 31, 2014 |

The following are the major ($5 million or more) stock changes—both purchases and sales—that were made in the Fund’s portfolio during the fourth quarter of 2014.

| | | | | | | | | | |

| | | SHARES | | |

| SECURITY NAME | | PURCHASES (SALES) | | HELD AS OF 12/31/14 | | |

PURCHASES | | | | | | | | | | |

EOG Resources, Inc. | | 61,848 | | | | 61,848 | | | | |

| | | | | |

Facebook, Inc., Class A | | 70,689 | | | | 193,715 | | | | |

| | | | | |

Ford Motor Co. | | 326,400 | | | | 326,400 | | | | |

| | | | | |

Gilead Sciences, Inc. | | 56,903 | | | | 69,403 | | | | |

| | | | | |

Las Vegas Sands Corp. | | 84,678 | | | | 84,678 | | | | |

| | | | | |

Stanley Black & Decker, Inc. | | 52,875 | | | | 52,875 | | | | |

| | | | | |

State Street Corp. | | 75,176 | | | | 302,276 | | | | |

| | | | | |

WPX Energy, Inc. | | 610,965 | | | | 610,965 | | | | |

SALES | | | | | | | | | | |

Bank of America Corp. | | (466,540) | | | | 807,524 | | | | |

| | | | | |

Becton, Dickinson & Co. | | (43,350) | | | | 0 | | | | |

| | | | | |

CME Group, Inc. | | (72,045) | | | | 0 | | | | |

| | | | | |

General Motors Co. | | (157,600) | | | | 0 | | | | |

| | | | | |

Schlumberger Ltd. | | (86,523) | | | | 161,815 | | | | |

| | | | | | |

ANNUAL REPORT | |

| | DECEMBER 31, 2014 | | |

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 17 |

SCHEDULE OF INVESTMENTS | | | |

as of December 31, 2014

| | | | | | | | | | | | | | |

COMMON STOCKS (97.74%) | | | SHARES | | | | | | MARKET VALUE | | | |

| | | | |

u CONSUMER DISCRETIONARY (16.38%) | | | | | | | | | | | | |

| | Auto Components (1.08%) | | | | | | | | | | | | |

| | Delphi Automotive PLC | | | 14,411 | | | | | $ | 1,047,968 | | | |

| | Johnson Controls, Inc. | | | 150,000 | | | | | | 7,251,000 | | | |

| | TRW Automotive Holdings Corp.(a) | | | 48,400 | | | | | | 4,977,940 | | | |

| | | | | | | | | | | 13,276,908 | | | |

| | | | | |

| | Automobiles (0.57%) | | | | | | | | | | | | |

| | Ford Motor Co. | | | 326,400 | | | | | | 5,059,200 | | | |

| | Tesla Motors, Inc.(a) | | | 8,880 | | | | | | 1,975,001 | | | |

| | | | | | | | | | | 7,034,201 | | | |

| | | | | |

| | Hotels, Restaurants & Leisure (5.12%) | | | | | | | | | | | | |

| | Carnival Corp. | | | 247,850 | | | | | | 11,235,041 | | | |

| | Chipotle Mexican Grill, Inc.(a) | | | 9,390 | | | | | | 6,427,549 | | | |

| | Las Vegas Sands Corp. | | | 84,678 | | | | | | 4,924,872 | | | |

| | Marriott International, Inc., Class A | | | 193,281 | | | | | | 15,081,716 | | | |

| | McDonald’s Corp. | | | 62,000 | | | | | | 5,809,400 | | | |

| | Starbucks Corp. | | | 233,682 | | | | | | 19,173,608 | | | |

| | | | | | | | | | | 62,652,186 | | | |

| | | | | |

| | Household Durables (2.08%) | | | | | | | | | | | | |

| | Lennar Corp., Class A | | | 173,040 | | | | | | 7,753,922 | | | |

| | PulteGroup, Inc. | | | 271,088 | | | | | | 5,817,549 | | | |

| | Taylor Morrison Home Corp., Class A(a) | | | 71,159 | | | | | | 1,344,194 | | | |

| | Toll Brothers, Inc.(a) | | | 307,516 | | | | | | 10,538,573 | | | |

| | | | | | | | | | | 25,454,238 | | | |

| | | | | |

| | Internet & Catalog Retail (1.75%) | | | | | | | | | | | | |

| | Amazon.com, Inc.(a) | | | 38,506 | | | | | | 11,950,337 | | | |

| | priceline.com, Inc.(a) | | | 8,350 | | | | | | 9,520,754 | | | |

| | | | | | | | | | | 21,471,091 | | | |

| | | | | |

| | Media (3.00%) | | | | | | | | | | | | |

| | CBS Corp., Class B | | | 59,019 | | | | | | 3,266,111 | | | |

| | Comcast Corp., Class A | | | 113,109 | | | | | | 6,561,453 | | | |

| | The Interpublic Group of Cos., Inc. | | | 128,075 | | | | | | 2,660,118 | | | |

| | News Corp., Class A(a) | | | 305,600 | | | | | | 4,794,864 | | | |

| | News Corp., Class B(a) | | | 112,445 | | | | | | 1,695,671 | | | |

| | Omnicom Group, Inc. | | | 93,825 | | | | | | 7,268,623 | | | |

| | Time Warner Cable, Inc. | | | 21,324 | | | | | | 3,242,527 | | | |

| | The Walt Disney Co. | | | 76,999 | | | | | | 7,252,536 | | | |

| | | | | | | | | | | 36,741,903 | | | |

| | | | | |

| | Multi-Line Retail (0.41%) | | | | | | | | | | | | |

| | Dollar General Corp.(a) | | | 70,563 | | | | | | 4,988,804 | | | |

| | | | | |

| | Specialty Retail (1.90%) | | | | | | | | | | | | |

| | The Home Depot, Inc. | | | 60,760 | | | | | | 6,377,977 | | | |

| | Office Depot, Inc.(a) | | | 482,550 | | | | | | 4,137,866 | | | |

See Notes to Schedule of Investments and Financial Statements.

| | |

www.all-starfunds.com | | USA |

| | | | |

| 18 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | SCHEDULE OF INVESTMENTS |

| | as of December 31, 2014 |

| | | | | | | | | | | | | | |

| COMMON STOCKS (continued) | | SHARES | | | | | MARKET VALUE | | | |

| | | | | |

| | Specialty Retail (1.90%) (continued) | | | | | | | | | | | | |

| | Staples, Inc. | | | 367,550 | | | | | $ | 6,660,006 | | | |

| | Tiffany & Co. | | | 57,315 | | | | | | 6,124,681 | | | |

| | | | | | | | | | | 23,300,530 | | | |

| | | | | |

| | Textiles, Apparel & Luxury Goods (0.47%) | | | | | | | | | | | | |

| | NIKE, Inc., Class B | | | 59,396 | | | | | | 5,710,925 | | | |

| | | | |

u CONSUMER STAPLES (3.66%) | | | | | | | | | | | | |

| | Beverages (0.88%) | | | | | | | | | | | | |

| | Diageo PLC(b) | | | 23,316 | | | | | | 2,660,123 | | | |

| | PepsiCo, Inc. | | | 61,500 | | | | | | 5,815,440 | | | |

| | SABMiller PLC(b) | | | 45,418 | | | | | | 2,341,752 | | | |

| | | | | | | | | | | 10,817,315 | | | |

| | | | | |

| | Food & Staples Retailing (1.06%) | | | | | | | | | | | | |

| | Costco Wholesale Corp. | | | 44,775 | | | | | | 6,346,856 | | | |

| | CVS Health Corp. | | | 68,500 | | | | | | 6,597,235 | | | |

| | | | | | | | | | | 12,944,091 | | | |

| | | | | |

| | Food Products (0.59%) | | | | | | | | | | | | |

| | Mead Johnson Nutrition Co. | | | 71,900 | | | | | | 7,228,826 | | | |

| | | | | |

| | Household Products (0.67%) | | | | | | | | | | | | |

| | The Procter & Gamble Co. | | | 90,500 | | | | | | 8,243,645 | | | |

| | | | | |

| | Personal Products (0.46%) | | | | | | | | | | | | |

| | The Estee Lauder Cos., Inc., Class A | | | 73,074 | | | | | | 5,568,239 | | | |

| | | | |

u ENERGY (10.40%) | | | | | | | | | | | | |

| | Energy Equipment & Services (2.45%) | | | | | | | | | | | | |

| | Baker Hughes, Inc. | | | 66,300 | | | | | | 3,717,441 | | | |

| | Oceaneering International, Inc. | | | 60,775 | | | | | | 3,574,178 | | | |

| | Schlumberger Ltd. | | | 161,815 | | | | | | 13,820,619 | | | |

| | Weatherford International Ltd.(a) | | | 781,088 | | | | | | 8,943,457 | | | |

| | | | | | | | | | | 30,055,695 | | | |

| | | | | |

| | Oil, Gas & Consumable Fuels (7.95%) | | | | | | | | | | | | |

| | Anadarko Petroleum Corp. | | | 63,929 | | | | | | 5,274,143 | | | |

| | Arch Coal, Inc.(c) | | | 1,565,642 | | | | | | 2,786,843 | | | |

| | BP PLC(b) | | | 244,300 | | | | | | 9,312,724 | | | |

| | Chesapeake Energy Corp. | | | 518,266 | | | | | | 10,142,466 | | | |

| | Chevron Corp. | | | 58,000 | | | | | | 6,506,440 | | | |

| | Cobalt International Energy, Inc.(a) | | | 172,093 | | | | | | 1,529,907 | | | |

| | ConocoPhillips | | | 86,500 | | | | | | 5,973,690 | | | |

| | Devon Energy Corp. | | | 163,230 | | | | | | 9,991,308 | | | |

| | EOG Resources, Inc. | | | 61,848 | | | | | | 5,694,345 | | | |

| | Exxon Mobil Corp. | | | 44,775 | | | | | | 4,139,449 | | | |

See Notes to Schedule of Investments and Financial Statements.

| | | | | | |

ANNUAL REPORT | |

| | DECEMBER 31, 2014 | | |

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 19 |

SCHEDULE OF INVESTMENTS | | | |

as of December 31, 2014 | | | | |

| | | | | | | | | | |

| COMMON STOCKS (continued) | | SHARES | | | MARKET VALUE | |

| | | |

| | Oil, Gas & Consumable Fuels (7.95%) (continued) | | | | | | | | |

| | Murphy Oil Corp. | | | 94,175 | | | $ | 4,757,721 | |

| | Occidental Petroleum Corp. | | | 85,000 | | | | 6,851,850 | |

| | Peabody Energy Corp.(c) | | | 897,320 | | | | 6,945,257 | |

| | Royal Dutch Shell PLC, Class A(b) | | | 154,493 | | | | 10,343,306 | |

| | WPX Energy, Inc.(a) | | | 610,965 | | | | 7,105,523 | |

| | | | | | | | | 97,354,972 | |

| | |

u FINANCIALS (28.49%) | | | | | | | | |

| | Banks (0.37%) | | | | | | | | |

| | First Niagara Financial Group, Inc. | | | 539,370 | | | | 4,546,889 | |

| | | |

| | Capital Markets (6.03%) | | | | | | | | |

| | Affiliated Managers Group, Inc.(a) | | | 24,375 | | | | 5,173,350 | |

| | Ameriprise Financial, Inc. | | | 34,980 | | | | 4,626,105 | |

| | The Charles Schwab Corp. | | | 262,600 | | | | 7,927,894 | |

| | Franklin Resources, Inc. | | | 85,600 | | | | 4,739,672 | |

| | The Goldman Sachs Group, Inc. | | | 37,450 | | | | 7,258,934 | |

| | Morgan Stanley | | | 357,175 | | | | 13,858,390 | |

| | State Street Corp. | | | 305,276 | | | | 23,964,166 | |

| | UBS Group AG(a) | | | 370,400 | | | | 6,315,320 | |

| | | | | | | | | 73,863,831 | |

| | | |

| | Commercial Banks (5.07%) | | | | | | | | |

| | Barclays PLC(b) | | | 261,781 | | | | 3,929,333 | |

| | BB&T Corp. | | | 205,000 | | | | 7,972,450 | |

| | Comerica, Inc. | | | 70,225 | | | | 3,289,339 | |

| | First Republic Bank | | | 102,030 | | | | 5,317,803 | |

| | The PNC Financial Services Group, Inc. | | | 70,666 | | | | 6,446,859 | |

| | Regions Financial Corp. | | | 651,453 | | | | 6,879,344 | |

| | SunTrust Banks, Inc. | | | 444,978 | | | | 18,644,578 | |

| | Wells Fargo & Co. | | | 176,000 | | | | 9,648,320 | |

| | | | | | | | | 62,128,026 | |

| | | |

| | Consumer Finance (2.73%) | | | | | | | | |

| | American Express Co. | | | 42,500 | | | | 3,954,200 | |

| | Capital One Financial Corp. | | | 101,000 | | | | 8,337,550 | |

| | Visa, Inc., Class A | | | 80,561 | | | | 21,123,094 | |

| | | | | | | | | 33,414,844 | |

| | | |

| | Diversified Financial Services (5.99%) | | | | | | | | |

| | Bank of America Corp. | | | 807,524 | | | | 14,446,604 | |

| | Citigroup, Inc. | | | 408,754 | | | | 22,117,679 | |

| | JPMorgan Chase & Co. | | | 426,500 | | | | 26,690,370 | |

| | Voya Financial, Inc. | | | 239,370 | | | | 10,144,501 | |

| | | | | | | | | 73,399,154 | |

| | | |

| | Insurance (6.79%) | | | | | | | | |

| | ACE Ltd. | | | 84,900 | | | | 9,753,312 | |

| | The Allstate Corp. | | | 68,807 | | | | 4,833,692 | |

See Notes to Schedule of Investments and Financial Statements.

| | |

www.all-starfunds.com | | USA |

| | | | |

| 20 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | SCHEDULE OF INVESTMENTS |

| | | | as of December 31, 2014 |

| | | | | | | | | | |

| COMMON STOCKS (continued) | | SHARES | | | MARKET VALUE | |

| | | |

| | Insurance (6.79%) (continued) | | | | | | | | |

| | American International Group, Inc. | | | 305,531 | | | $ | 17,112,791 | |

| | Assured Guaranty Ltd. | | | 246,096 | | | | 6,396,035 | |

| | Axis Capital Holdings Ltd. | | | 156,000 | | | | 7,970,040 | |

| | First American Financial Corp. | | | 110,452 | | | | 3,744,323 | |

| | Genworth Financial, Inc., Class A(a) | | | 207,100 | | | | 1,760,350 | |

| | The Hartford Financial Services Group, Inc. | | | 238,295 | | | | 9,934,519 | |

| | MetLife, Inc. | | | 304,725 | | | | 16,482,575 | |

| | Willis Group Holdings PLC | | | 115,350 | | | | 5,168,833 | |

| | | | | | | | | 83,156,470 | |

| | | |

| | Real Estate Investment Trusts (1.25%) | | | | | | | | |

| | American Tower Corp. | | | 118,260 | | | | 11,690,001 | |

| | NorthStar Realty Finance Corp. | | | 170,314 | | | | 2,994,120 | |

| | Paramount Group, Inc.(a) | | | 31,582 | | | | 587,110 | |

| | | | | | | | | 15,271,231 | |

| | | |

| | Real Estate Management & Development (0.26%) | | | | | | | | |

| | Forest City Enterprises, Inc., Class A(a) | | | 147,310 | | | | 3,137,703 | |

| | |

u HEALTH CARE (11.88%) | | | | | | | | |

| | Biotechnology (2.91%) | | | | | | | | |

| | Alexion Pharmaceuticals, Inc.(a) | | | 46,507 | | | | 8,605,190 | |

| | BioMarin Pharmaceutical, Inc.(a) | | | 79,045 | | | | 7,145,668 | |

| | Celgene Corp.(a) | | | 85,630 | | | | 9,578,572 | |

| | Gilead Sciences, Inc.(a) | | | 69,403 | | | | 6,541,927 | |

| | Pharmacyclics, Inc.(a) | | | 30,940 | | | | 3,782,724 | |

| | | | | | | | | 35,654,081 | |

| | | |

| | Health Care Equipment & Supplies (1.84%) | | | | | | | | |

| | Baxter International, Inc. | | | 69,025 | | | | 5,058,842 | |

| | Hologic, Inc.(a) | | | 336,400 | | | | 8,995,336 | |

| | Zimmer Holdings, Inc. | | | 74,500 | | | | 8,449,790 | |

| | | | | | | | | 22,503,968 | |

| | | |

| | Health Care Providers & Services (2.04%) | | | | | | | | |

| | Catamaran Corp.(a) | | | 206,150 | | | | 10,668,263 | |

| | Cigna Corp. | | | 80,500 | | | | 8,284,255 | |

| | Envision Healthcare Holdings, Inc.(a) | | | 98,163 | | | | 3,405,274 | |

| | Laboratory Corp. of America Holdings(a) | | | 24,025 | | | | 2,592,298 | |

| | | | | | | | | 24,950,090 | |

| | | |

| | Health Care Technology (1.52%) | | | | | | | | |

| | athenahealth, Inc.(a)(c) | | | 54,000 | | | | 7,867,800 | |

| | Cerner Corp.(a) | | | 166,668 | | | | 10,776,753 | |

| | | | | | | | | 18,644,553 | |

| | | |

| | Life Sciences Tools & Services (1.16%) | | | | | | | | |

| | Illumina, Inc.(a) | | | 42,700 | | | | 7,881,566 | |

| | Thermo Fisher Scientific, Inc. | | | 50,000 | | | | 6,264,500 | |

| | | | | | | | | 14,146,066 | |

See Notes to Schedule of Investments and Financial Statements.

| | | | | | |

ANNUAL REPORT | |

| | DECEMBER 31, 2014 | | |

| | | | |

LIBERTY ALL-STAR® EQUITY FUND | | | | 21 |

SCHEDULE OF INVESTMENTS | | | |

as of December 31, 2014 | | | | |

| | | | | | | | | | |

| COMMON STOCKS (continued) | | SHARES | | | MARKET VALUE | |

| | | |

| | Pharmaceuticals (2.41%) | | | | | | | | |

| | Abbott Laboratories | | | 107,925 | | | $ | 4,858,784 | |

| | Allergan, Inc. | | | 30,555 | | | | 6,495,687 | |

| | Johnson & Johnson | | | 66,500 | | | | 6,953,905 | |

| | Perrigo Co. PLC | | | 20,942 | | | | 3,500,665 | |

| | Teva Pharmaceutical Industries Ltd.(b) | | | 134,200 | | | | 7,717,842 | |

| | | | | | | | | 29,526,883 | |

| | |

uINDUSTRIALS (6.12%) | | | | | | | | |

| | Aerospace & Defense (1.94%) | | | | | | | | |

| | The Boeing Co. | | | 4,845 | | | | 629,753 | |

| | Bombardier, Inc., Class B | | | 872,993 | | | | 3,134,045 | |

| | Precision Castparts Corp. | | | 68,262 | | | | 16,442,950 | |

| | Textron, Inc. | | | 84,399 | | | | 3,554,042 | |

| | | | | | | | | 23,760,790 | |

| | | |

| | Building Products (0.49%) | | | | | | | | |

| | Masco Corp. | | | 238,725 | | | | 6,015,870 | |

| | | |

| | Electrical Equipment (0.72%) | | | | | | | | |

| | Eaton Corp. PLC | | | 129,000 | | | | 8,766,840 | |

| | | |

| | Machinery (1.43%) | | | | | | | | |

| | Caterpillar, Inc. | | | 62,000 | | | | 5,674,860 | |

| | Parker-Hannifin Corp. | | | 52,825 | | | | 6,811,784 | |

| | Stanley Black & Decker, Inc. | | | 52,875 | | | | 5,080,230 | |

| | | | | | | | | 17,566,874 | |

| | | |

| | Trading Companies & Distributors (1.23%) | | | | | | | | |

| | Fastenal Co. | | | 242,593 | | | | 11,537,723 | |

| | United Rentals, Inc.(a) | | | 33,961 | | | | 3,464,362 | |

| | | | | | | | | 15,002,085 | |

| | | |

| | Transportation Infrastructure (0.31%) | | | | | | | | |

| | Aegean Marine Petroleum Network, Inc. | | | 271,629 | | | | 3,808,238 | |

| | |

uINFORMATION TECHNOLOGY (20.16%) | | | | | | | | |

| | Communications Equipment (2.00%) | | | | | | | | |

| | Cisco Systems, Inc. | | | 319,000 | | | | 8,872,985 | |

| | QUALCOMM, Inc. | | | 209,400 | | | | 15,564,702 | |

| | | | | | | | | 24,437,687 | |

| | | |

| | Computers & Peripherals (2.12%) | | | | | | | | |

| | Hewlett-Packard Co. | | | 457,525 | | | | 18,360,478 | |

| | Stratasys Ltd.(a)(c) | | | 91,148 | | | | 7,575,311 | |

| | | | | | | | | 25,935,789 | |

| | | |

| | Electronic Equipment & Instruments (1.76%) | | | | | | | | |

| | Avnet, Inc. | | | 13,021 | | | | 560,163 | |

| | Corning, Inc. | | | 256,200 | | | | 5,874,666 | |

| | TE Connectivity Ltd. | | | 150,475 | | | | 9,517,544 | |

See Notes to Schedule of Investments and Financial Statements.

| | |

www.all-starfunds.com | | USA |

| | | | |

| 22 | | | | LIBERTY ALL-STAR® EQUITY FUND |

| | | SCHEDULE OF INVESTMENTS |

| | | | as of December 31, 2014 |

| | | | |

| | | | | | | | | | | | | | |

| COMMON STOCKS (continued) | | SHARES | | | | | MARKET VALUE | | | |

| | | | | |

| | Electronic Equipment & Instruments (1.76%) (continued) | | | | | | | | | | | | |

| | Trimble Navigation Ltd.(a) | | | 210,915 | | | | | $ | 5,597,684 | | | |

| | | | | | | | | | | 21,550,057 | | | |

| | Internet Software & Services (6.31%) | | | | | | | | | | | | |

| | Alibaba Group Holding Ltd.(a)(b) | | | 46,367 | | | | | | 4,819,386 | | | |

| | CoStar Group, Inc.(a) | | | 27,426 | | | | | | 5,036,237 | | | |

| | Equinix, Inc. | | | 33,006 | | | | | | 7,483,450 | | | |

| | Facebook, Inc., Class A(a) | | | 193,715 | | | | | | 15,113,644 | | | |

| | Google, Inc., Class A(a) | | | 18,227 | | | | | | 9,672,340 | | | |

| | Google, Inc., Class C(a) | | | 22,110 | | | | | | 11,638,704 | | | |

| | LinkedIn Corp., Class A(a) | | | 33,420 | | | | | | 7,676,908 | | | |

| | Mercadolibre, Inc. | | | 32,920 | | | | | | 4,202,897 | | | |

| | Rackspace Hosting, Inc.(a) | | | 249,141 | | | | | | 11,662,290 | | | |

| | | | | | | | | | | 77,305,856 | | | |

| | IT Services (0.38%) | | | | | | | | | | | | |

| | Teradata Corp.(a) | | | 106,000 | | | | | | 4,630,080 | | | |

| | | | | |

| | Semiconductors & Semiconductor Equipment (1.91%) | | | | | | | | | | | | |

| | ARM Holdings PLC(b) | | | 148,620 | | | | | | 6,881,106 | | | |

| | Intel Corp. | | | 218,275 | | | | | | 7,921,200 | | | |

| | Micron Technology, Inc.(a) | | | 244,061 | | | | | | 8,544,575 | | | |

| | | | | | | | | | | 23,346,881 | | | |

| | Software (5.68%) | | | | | | | | | | | | |

| | Microsoft Corp. | | | 314,775 | | | | | | 14,621,299 | | | |

| | Oracle Corp. | | | 191,025 | | | | | | 8,590,394 | | | |

| | Salesforce.com, Inc.(a) | | | 422,738 | | | | | | 25,072,591 | | | |

| | ServiceNow, Inc.(a) | | | 111,300 | | | | | | 7,551,705 | | | |

| | Splunk, Inc.(a) | | | 90,900 | | | | | | 5,358,555 | | | |

| | Symantec Corp. | | | 327,482 | | | | | | 8,401,550 | | | |

| | | | | | | | | | | 69,596,094 | | | |

u MATERIALS (0.57%) | | | | | | | | | | | | |

| | Chemicals (0.57%) | | | | | | | | | | | | |

| | EI du Pont de Nemours & Co. | | | 95,000 | | | | | | 7,024,300 | | | |

| | | | |