Exhibit 4.5

Management’s Discussion and Analysis

For the three months ended March 31, 2013

New Gold Inc.

TABLE OF CONTENTS

| 1 | EXECUTIVE SUMMARY | ||

| 2 | FINANCIAL AND OPERATING HIGHLIGHTS | ||

| 3 | Financial highlights | ||

| 4 | Operating highlights | ||

| 5 | Development and exploration highlights | ||

| 5 | Corporate developments | ||

| 5 | OUTLOOK FOR 2013 | ||

| 6 | KEY PERFORMANCE DRIVERS AND ECONOMIC OUTLOOK | ||

| 6 | Key performance drivers | ||

| 7 | Economic outlook | ||

| 8 | CORPORATE SOCIAL RESPONSIBILITY | ||

| 9 | FINANCIAL AND OPERATING RESULTS | ||

| 9 | Summary of quarterly and year to date financial and operating results | ||

| 12 | Review of operating mines | ||

| 17 | DEVELOPMENT AND EXPLORATION REVIEW | ||

| 20 | FINANCIAL CONDITION REVIEW | ||

| 20 | Balance sheet review | ||

| 22 | Liquidity and cash flow | ||

| 22 | Commitments | ||

| 22 | Contingencies | ||

| 23 | Contractual obligations | ||

| 23 | Related party transactions | ||

| 23 | Off-balance sheet arrangements | ||

| 23 | Outstanding shares | ||

| 23 | NON-GAAP FINANCIAL PERFORMANCE MEASURES | ||

| 26 | ENTERPRISE RISK MANAGEMENT | ||

| 26 | General risks | ||

| 26 | Financial risk management | ||

| 30 | CRITICAL ACCOUNTING POLICIES, ESTIMATES AND ACCOUNTING CHANGES | ||

| 34 | CONTROLS AND PROCEDURES | ||

| 35 | CAUTIONARY NOTES | ||

Management’s Discussion and Analysis

For the three months ended March 31, 2013

The following Management’s Discussion and Analysis (“MD&A”) provides information that management believes is relevant to an assessment and understanding of the consolidated financial condition and results of operations of New Gold Inc. and its subsidiaries (“New Gold” or the “Company”), including its predecessor entities. This MD&A should be read in conjunction with New Gold’s unaudited condensed consolidated financial statements for the three months ended March 31, 2013 and 2012 and related notes which are prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). This MD&A contains forward-looking statements that are subject to risk factors set out in a cautionary note contained in this MD&A. The reader is cautioned not to place undue reliance on forward-looking statements. All figures are in United States dollars and tabular amounts are in millions, unless otherwise noted. This MD&A has been prepared as at May 1, 2013. Additional information relating to the Company, including the Company’s Annual Information Form, is available on SEDAR at www.sedar.com.

EXECUTIVE SUMMARY

New Gold is an intermediate gold producer with operating mines in Canada, Mexico, the United States and Australia and development projects in Canada and Chile. With a strong liquidity position, simplified balance sheet and an experienced management and board of directors, the Company has a solid platform to continue to execute its growth strategy. During the first quarter of 2013, the New Afton Mine in Canada (“New Afton”), the Cerro San Pedro Mine in Mexico (“Cerro San Pedro”), the Mesquite Mine in the United States (“Mesquite”) and the Peak Mines in Australia (“Peak Mines”) combined to produce 94,695 ounces of gold.

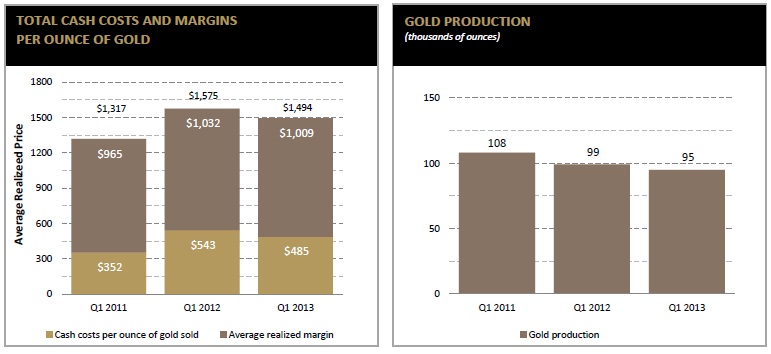

New Gold’s production costs remain very competitive when compared to the broader gold mining industry and provide the Company with strong margins. In the first quarter of 2013, New Gold achieved total cash costs(1) of $485 per ounce of gold sold and an average realized gold price(1) of $1,494 per ounce, resulting in a margin(1) per ounce of $1,009 . This compares to a margin per ounce of $1,032 in the first quarter of 2012. New Gold has been able to maintain its costs well below the industry average as the Company also produces silver and copper as by-product metals, which have historically moved in line with, and acted as an offset to, some of the input cost pressures faced by the mining industry. Consistent with New Gold’s plan, operations are expected to have progressively stronger quarters throughout 2013 leading to increased gold production and operating cash flow, with steadily declining cash costs. New Gold remains in line to meet production and cash cost guidance for 2013.

Subsequent to quarter-end, on April 4, 2013, New Gold announced a Mineral Resource update at its Blackwater Project. This Blackwater resource update, which will be used for the project’s Feasibility Study, has been updated to include 89 additional holes totaling 22,220 metres, including further infill drilling and more refined geologic and geostatistical modeling. Key highlights of the update are:

| · | Measured and Indicated(2) gold resources for direct processing increased to 8.6 million ounces at 0.88 grams per tonne |

| · | Measured gold resources increased by 44% to 3.9 million ounces at 1.04 grams per tonne |

During the quarter, a Mineral Resource update was also announced at New Afton as part of the year-end resource update which resulted in the New Afton mine life being extended by two years from 12 to 14 years. In addition, the C-Zone resource, which lies immediately down plunge of the block of mineralization currently being mined, has been updated at May 1, 2013, to incorporate the drilling that was completed through the end of February 2013. The C-Zone update reflects positive increases to the gold and copper resource at more favourable grades. The objective of the C-Zone exploration drilling is to add to the mine’s life while, at the same time, New Gold continues to evaluate opportunities to increase the throughput rate beyond the nameplate capacity of 11,000 tonnes per day.

New Gold continues to build on its successful portfolio which now consists of four operating mines and two development projects, all located in jurisdictions that are considered favourable to mining activities.

| 1. | We use certain non-GAAP financial performance measures throughout our MD&A. For a detailed description of each of the non-GAAP measures used in this MD&A, please see the discussion under “Non-GAAP Financial Performance Measures” of this MD&A. |

| 2. | Notes to Mineral Resources Estimates are on page 18 of this MD&A. |

1

FINANCIAL AND OPERATING HIGHLIGHTS

| Three months ended March 31 | ||||

| (in millions of U.S. dollars, except where noted) | 2013 | 2012 | ||

| Operating information: | ||||

| Gold (ounces): | ||||

Produced (1) | 94,695 | 99,274 | ||

Sold (1) | 95,181 | 93,676 | ||

| Silver (ounces): | ||||

Produced (1) | 358,905 | 456,584 | ||

Sold (1) | 360,913 | 439,141 | ||

| Copper (thousands of pounds): | ||||

Produced (1) | 15,998 | 3,683 | ||

Sold (1) | 15,867 | 1,780 | ||

Average realized price (2): | ||||

| Gold ($/ounce) | 1,494 | 1,575 | ||

| Silver ($/ounce) | 29.51 | 32.70 | ||

| Copper ($/pound) | 3.44 | 4.14 | ||

Total cash costs per gold ounce sold (2) (3) | 485 | 543 | ||

Average realized margin (2) ($/ounce) | 1,009 | 1,032 | ||

Financial Information: | ||||

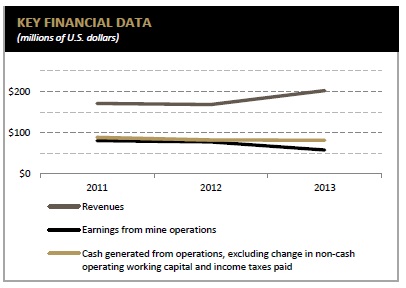

| Revenues | 201.8 | 168.8 | ||

| Earnings from mine operations | 57.8 | 77.7 | ||

| Net earnings | 36.3 | 33.5 | ||

Adjusted net earnings (1) | 20.6 | 44.2 | ||

| Cash generated from operations | 68.2 | 66.1 | ||

| Net cash generated from continuing operations | 58.5 | 36.7 | ||

| Capital expenditures | 76.4 | 110.1 | ||

| Total assets | 4,302.2 | 3,293.0 | ||

| Cash and cash equivalents | 672.4 | 235.7 | ||

| Long-term debt | 854.3 | 262.3 | ||

| Share Data: | ||||

| Earnings per share from continuing operations: | ||||

| Basic | 0.08 | 0.07 | ||

| Diluted | 0.08 | 0.07 | ||

Adjusted net earnings per basic share (1) | 0.04 | 0.10 | ||

| Share price as at March 31 (TSX – Canadian dollars) | 9.24 | 9.85 | ||

| Weighted average outstanding shares (basic) (millions) | 476 | 461 | ||

| 1. | Production is shown on a total contained basis while sales are shown on a net payable basis, including final product inventory and smelter payable adjustments, where applicable. |

| 2. | We use certain non-GAAP financial performance measures throughout our MD&A. Total cash costs per gold ounce sold, average realized price, average realized margin, operating margin, adjusted net earnings, adjusted net earnings per share and cash generated from operations, excluding working capital changes and income taxes paid, are non-GAAP financial performance measures with no standard meaning under IFRS. For further information and a detailed reconciliation, please refer to the “Non-GAAP Financial Performance Measures” section of this MD&A. |

| 3. | The calculation of total cash costs per gold ounce sold is net of by-product silver and copper revenues. If silver and copper revenues were treated as co-products, co-product total cash costs for the three months ended March 31, 2013 would be $793 per ounce of gold (2012 - $672), $16.45 per ounce of silver (2012 - $13.97); and $1.96 per pound of copper (2012 - $2.09). |

2

FINANCIAL HIGHLIGHTS

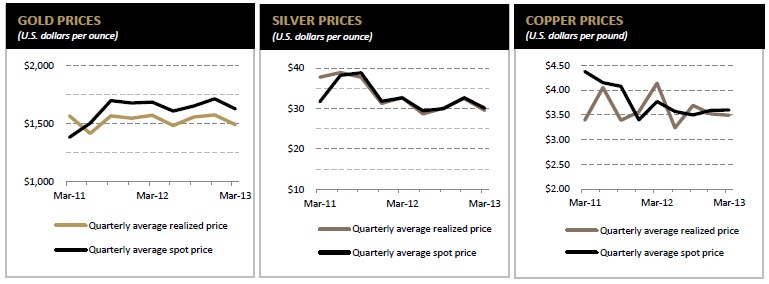

• Revenues were $201.8 million for the first quarter of 2013, an increase of 20% over $168.8 million in the prior year. The increase was driven primarily by higher sales of gold and copper compared to the prior year, positively impacted by a full quarter of commercial production at New Afton. The benefit from increased sales volume was offset by a decrease in the average realized price of gold, silver and copper. The average realized price for gold in the first quarter of 2013 was $1,494 per ounce of gold compared to $1,575 per ounce in the prior year. The average realized price of copper and silver decreased from $4.14 per pound of copper and $32.70 per ounce of silver in 2012 to $3.44 per pound of copper and $29.51 per ounce of silver in 2013.

• Net cash generated from operations in the first quarter of 2013 was $58.5 million, a 59% increase compared to $36.7 million in the prior year. This increase was primarily driven by New Afton now being a meaningful contributor to the Company’s cash flow generation and lower income taxes paid than in the prior year period. In the first quarter of 2012, the New Gold made $7.1 million in income tax payments that related to 2011. There were no similar payments made in 2013.

• Earnings from mine operations were $57.8 million for the first quarter of 2013 compared to $77.7 million in the same prior year period. The benefits of increased earnings from mine operations from New Afton and the Peak Mines were more than offset by decreases at Cerro San Pedro and Mesquite due to planned mining of lower grade ore at the Company’s two open pit operations. Additionally, non-cash depreciation and depletion expense increased to $37.9 million in the first quarter of 2013 from $18.8 million in the first quarter of 2012, reflecting the addition of the New Afton initial capital cost to the depreciable pools of assets.

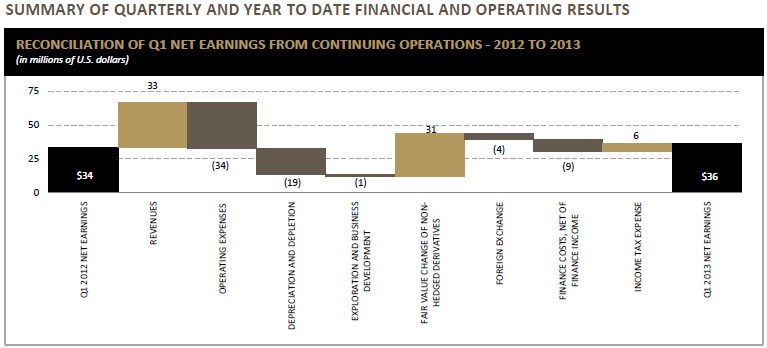

• Net earnings from continuing operations for the first quarter of 2013 were $36.3 million or $0.08 per basic share, compared to $33.5 million or $0.07 per basic share in the same period in 2012. The increase is primarily due to the impact of non-operating “Other gains and losses”, where a gain of $15.8 million was recorded for the first quarter of 2013 relative to a loss of $12.1 million in 2012. The gain includes a non-cash gain on non-hedged derivatives of $22.6 million which related fully to the mark to market of the share purchase warrant liability. This benefit was offset by lower earnings from mine operations resulting from the planned mining of lower grade ore at Mesquite and Cerro San Pedro.

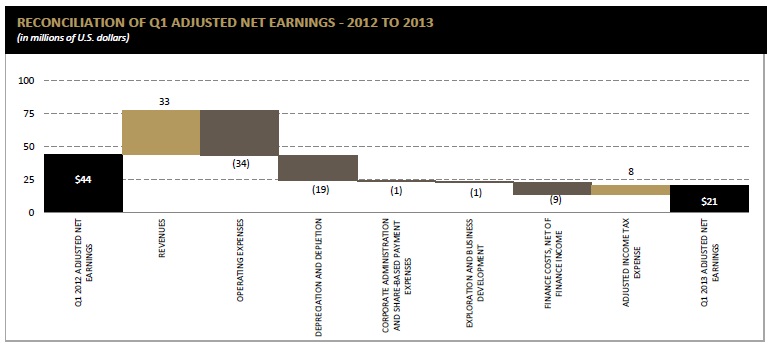

• Adjusted net earnings for the first quarter of 2013 were $20.6 million or $0.04 per basic share, relative to $44.2 million or $0.10 per basic share in the prior year period. In addition to the planned mining of lower grade ore, adjusted net earnings were impacted by a combination of a $19.1 million increase in non-cash depreciation and depletion expense as well as a $9.4 million increase in interest expense.

• Cash and cash equivalents were $672.4 million at March 31, 2013 compared to $687.8 million at December 31, 2012.

| 3. | We use certain non-GAAP financial performance measures throughout our MD&A. For a detailed description of each of the non-GAAP measures used in this MD&A, please see the discussion under “Non-GAAP Financial Performance Measures” of this MD&A. |

3

OPERATING HIGHLIGHTS

• Total cash costs per ounce sold for the first quarter of 2013, net of by-product sales, were $485 per ounce, a decrease of $58 per ounce compared to $543 per ounce in the same period in 2012. The decrease in the Company’s cash costs was primarily driven by increased copper sales volumes which were partially offset by a combination of lower realized copper prices, lower silver sales volumes and realized prices as well as the scheduled mining of lower grade ore. New Gold’s total cash costs per ounce are expected to steadily decline throughout the remainder of 2013.

• Gold production for the first quarter of 2013 was 94,695 ounces, compared to 99,274 ounces in the same prior year period. Production increases from New Afton now being part of New Gold’s operating portfolio and higher gold grades at the Peak Mines were offset by lower production at Cerro San Pedro and Mesquite due to planned mining of lower grade ore. Per the Company’s plan, gold grades and production are expected to increase during the remainder of the year.

• Copper production for the first quarter of 2013 was 16.0 million pounds, an increase of 332% compared to 3.7 million pounds in the same prior year period. This increase was due to the addition of New Afton in the first quarter of 2013 and a 14% increase in copper production at Peak Mines, reflecting an increase in ore tonnes processed and copper recoveries.

• Gold sales in the first quarter of 2013 were 95,181 ounces, up 2% from 93,676 ounces in the same period in 2012. Though production levels were lower than in the prior year period, gold sales were benefitted through a reduction in inventory in 2013 relative to an increase in 2012.

• The average realized margin for the first quarter of 2013 was $1,009 per ounce, consistent with $1,032 in the same prior year period.

4

DEVELOPMENT AND EXPLORATION HIGHLIGHTS

• Subsequent to quarter-end, New Gold updated its mineral resource estimate for Blackwater which resulted in an increase in the Measured and Indicated gold Mineral Resource to 9.5 million ounces from 8.1 million ounces at the end of 2012. The updated Mineral Resource includes 0.9 million gold ounces of lower grade Measured and Indicated Resources suitable for stockpiling and processing toward the end of the project’s currently envisioned mine life. The Mineral Resource estimate will be incorporated into the feasibility study currently in progress and scheduled for completion in late 2013. Notes to the Mineral Resource Estimates are on page 18 of this MD&A.

• Subsequent to quarter-end, an update to the New Afton C-Zone mineral resource estimate reflects an over 300% increase in gold ounces and copper pounds at improved grade. Measured and Indicated gold and copper Resources increased to 0.3 million ounces and 211 million pounds respectively. Measured and Indicated gold and copper grades increased to 0.77 grams per tonne gold and 0.77% copper from 0.62 grams per tonne and 0.68% copper. The Inferred gold and copper Resources increased by over 30% to 0.4 million ounces and 301 million pounds.

CORPORATE DEVELOPMENTS

The Company continues to pursue disciplined growth both through organic initiatives and potential mergers and acquisitions. The Company came together through two accretive business combinations in mid-2008 and mid-2009. Since the middle of 2009, New Gold has been successful in enhancing the value of its portfolio of assets, while also continuously looking for compelling external growth opportunities. The Company continues to evaluate assets in favourable jurisdictions and where the asset has the potential to provide New Gold shareholders with meaningful gold production, cash flow and exploration potential, while ensuring that any potential acquisition is accretive on key per share metrics. The Company strives to maintain a strong financial position by continually reviewing strategic alternatives with the view to maximizing shareholder value. In short, New Gold strives to pursue corporate development initiatives that will leave the Company and its shareholders in a fundamentally stronger position.

OUTLOOK FOR 2013

New Gold is pleased to reiterate its guidance for 2013 which is scheduled to provide shareholders with increased gold production at lower cost when compared to 2012:

2013 PRODUCTION AND COST GUIDANCE

| Gold | Silver | Copper | Total cash costs | |

| (thousands of ounces) | (millions of ounces) | (millions of pounds) | (per ounce) | |

| Mesquite | 130 - 140 | - | - | $830 - $850 |

| Cerro San Pedro | 140 - 150 | 1.4 - 1.6 | - | $375 - $395 |

| Peak Mines | 95 - 105 | - | 12 - 14 | $670 - $690 |

| New Afton | 75 - 85 | - | 66 - 74 | $(1,410) - $(1,390) |

| Total | 440-480 | 1.4 - 1.6 | 78 - 88 | $265 - $285 |

New Gold’s copper and silver by-product revenue continues to provide an effective natural hedge against the various cost pressures being faced by the broader industry which allows the Company to deliver lower costs.

Assumptions used in the 2013 guidance include gold, silver and copper prices of $1,600 per ounce, $30.00 per ounce and $3.50 per pound and Canadian dollar, Australian dollar and Mexican peso exchange rates of $1.00, $1.00 and $13.00 to the U.S. dollar. The diesel price assumed for 2013 is $3.70 per gallon. Realized commodity prices and average foreign exchange rates were in line with these assumptions during the first quarter, however, prices of gold, silver and copper have declined below the assumed levels in recent weeks. Though the Company’s cash costs would be negatively impacted should copper and silver prices remain below the assumed prices, other cost-related factors, such as declining oil prices, lower explosive and cyanide costs as well as the depreciation of the Canadian dollar, would benefit costs.

5

KEY PERFORMANCE DRIVERS AND ECONOMIC OUTLOOK

KEY PERFORMANCE DRIVERS

There are a range of key performance drivers that are critical to the successful implementation of New Gold’s strategy and the achievement of its goals. The key internal drivers are production volumes and costs. The key external drivers are spot prices of gold, silver and copper, as well as foreign exchange rates.

Production Volumes and Costs

New Gold has demonstrated a history of achieving guidance with respect to production volumes and costs. New Gold’s portfolio of operating mines achieved another solid production quarter, with 94,695 ounces of gold production in the first quarter of 2013.

Total cash costs per ounce sold for the quarter, net of by-products sales, of $485 are below the industry average.

New Gold’s outlook is to increase gold production in 2013 by approximately 12% and total cash costs per ounce sold are forecast to decrease by approximately $145 per ounce compared to the 2012 level at budgeted prices.

Commodity Prices

Gold prices

The price of gold is the largest single factor affecting New Gold’s profitability and operating cash flows. As such, the current and future financial performance of the Company will be closely related to the prevailing price of gold.

The gold price ended the quarter almost 5% lower than at the end of 2012. In April 2013 the gold price fell more significantly to a low of $1,322 per ounce on concerns that governments facing economic difficulties may consider selling part of their gold reserves, before recovering to some extent to above $1,400 per ounce as physical demand and renewed investor interest resulted in a rebound. In spite of the recent decline in prices, interest rates continue at historically low rates and are likely to remain so for the foreseeable future in the face of slow-moving economic recovery, and there are numerous political and economic risks on the horizon, all of which are traditionally positive factors for gold.

During the first quarter of 2013, the London PM fix gold price averaged $1,630 per ounce compared to $1,689 per ounce during the first quarter of 2012.

6

Copper and silver prices

Copper declined during the quarter by approximately 5%, and then fell further during the first part of April as part of the commodity sell-off that also affected gold and silver. The copper London Metals Exchange price averaged $3.60 per pound during the quarter compared to $3.77 per pound during the first quarter of 2012.

During the first quarter of 2013, silver had an average London PM fix price of $30.08 per ounce, compared to the first quarter of 2012 during which silver averaged $32.62 per ounce..

Foreign Exchange Rates

The Company operates in Canada, Mexico, the United States, Australia and Chile. As a result, the Company has foreign currency exposure with respect to items not denominated in U.S. dollars.

New Gold’s operating results and cash flows are influenced by changes in various exchange rates against the U.S. dollar. We have exposure to the Canadian dollar through New Afton and Blackwater, as well as through our corporate administration costs. We also have exposure to the Mexican peso through Cerro San Pedro, and to the Australian dollar through our Peak Mines operations.

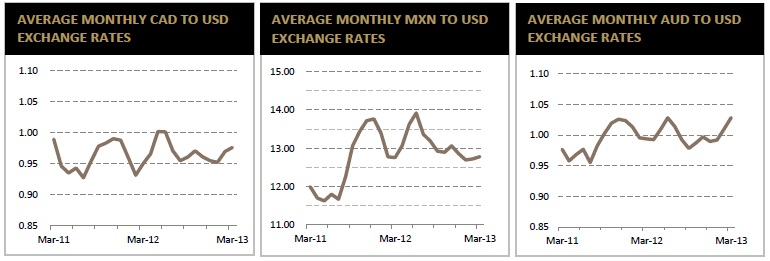

The Canadian dollar fell from slightly above parity at the end of 2012 to end the first quarter approximately 2.5% lower. A weaker Canadian dollar reduces costs in U.S. dollar terms at the Company’s Canadian operations.

The Mexican peso increased in strength during the quarter compared with the U.S. dollar. A significant proportion of costs at Cerro San Pedro are incurred in U.S. dollars and, as such, the movement in the Mexican peso exchange rate was not a significant driver of U.S. dollar-denominated costs.

The Australian dollar stayed above parity for the duration of the quarter, initially declining before regaining most of its strength before the end of the period.

For an analysis of the impact of foreign exchange fluctuations on operating costs in 2013 relative to 2012, refer to the ‘Review of Operating Mines’ sections for New Afton, Cerro San Pedro and Peak Mines for details.

ECONOMIC OUTLOOK

In early 2013 equity indices continued to do well for the most part, with the MSCI All-Country World Index climbing by almost 6% and the S&P 500 Index reaching new highs and ending the quarter up by more than 10%. However the global recovery continued to be hampered by uncoordinated policy decisions and by unexpected economic events. Global focus shifted to Cyprus, responsible for approximately 0.2% of Eurozone GDP but sufficient to threaten the destabilization of the rest of the currency union as efforts were made to bail out the country’s overextended banking sector while balancing various creditor interests. Ultimately this led to a sell-off in gold early in the second quarter of 2013 as concerns grew that struggling governments would instruct their central banks to sell gold to generate funds.

However, buying interest has emerged at these new lower gold price levels, and uncertainty, volatility and an ongoing ultra-low interest rate environment should provide positive encouragement for gold investors.

Economic events can have significant effects on the gold price, via currency rate fluctuations, the relative strength of the U.S. dollar, supply of and demand for gold and macroeconomic factors such as the level of interest rates and inflation expectations. Management anticipates that the long term economic environment should remain positive with respect to precious metals and for gold in particular, and believes the prospects for the business are favourable. The Company has not hedged foreign exchange rates and metal prices with the exception of the gold hedge mandated by Mesquite’s 2008 project financing. New Gold’s growth plan is focused on organic and acquisition-led growth, and the Company plans to remain flexible in the current environment to be able to respond to opportunities as they arise.

7

CORPORATE SOCIAL RESPONSIBILITY

New Gold is committed to excellence in corporate social responsibility. We consider our ability to make a lasting and positive contribution toward sustainable development through the protection of the health and well-being of our people and our host communities, environmental stewardship and community engagement and development, a key driver to achieving a productive and profitable business.

As a partner of the United Nations Global Compact, New Gold’s policies and practices are guided by its principles on Human Rights, Labour, Environment and Anti-corruption. As a member of the Mining Association of Canada (“MAC”), our Canadian operations adhere closely to the principles of MAC’s Towards Sustainable Mining program.

New Gold’s corporate social responsibility objectives include promoting and protecting the welfare of our employees through safety-first work practices, upholding fair employment practices and encouraging a diverse workforce, where people are treated with respect and are supported to realize their full potential. At New Gold, we believe that our people are our most valued assets regardless of gender, race, cultural background, age or religion. We strive to create a culture of inclusiveness that begins at the top and which is reflected in our hiring, promotion and overall human resources practices. We encourage tolerance and acceptance in worker-to-worker relationships. In each of our host communities we are recognized as an employer of choice as a result of our competitive wages, competitive benefits and our policies of recognizing and rewarding employee performance and promoting from within.

We are committed to preserving the long-term health and viability of the natural environments affected by our operations. Wherever New Gold operates – in all stages of mining activity, from early exploration and planning, to commercial mining operations through to eventual closure – we are committed to excellence in environmental management. From the earliest site investigations, we carry out comprehensive environmental studies to establish baseline measurements for flora, fauna, land, air and water. During operations we promote the efficient use of resources, work to minimize environmental impacts and maintain robust monitoring programs, including groundwater and air quality. We implement progressive reclamation and re-vegetation activities throughout the life of our operations. After mining activities are complete, our objective is to restore the land to a level of productivity equivalent to its pre-mining capacity. We continually seek new strategies for enhancing our environmental performance including programs to improve energy efficiency, reduce our carbon footprint and minimize our use of water and other resources.

We are committed to establishing relationships based on mutual benefit and active participation with our host communities to contribute to healthy communities and sustainable community development. Wherever our operations interact with indigenous peoples, we endeavor to understand and respect traditional values, customs and culture. We take meaningful action to serve their development needs and priorities through collaborative agreements aimed at creating jobs, training and lasting socio-economic benefits. We foster open communication with local residents and community leaders and strive to be a full partner in the long-term sustainability of the communities and regions in which we operate. We believe that only by thoroughly understanding the people, their histories, and their needs and plans, can we engage in a meaningful development process that will contribute to their cultural and economic health and welfare.

8

FINANCIAL AND OPERATING RESULTS

Production

New Gold’s consolidated gold production during the first quarter of 2013 was 94,695 ounces compared to 99,274 ounces in 2012. Despite the contribution from New Afton, which was still in the development stage throughout the first half of 2012, and increased gold production at the Peak Mines, production increases were largely offset by the decreases at the Mesquite Mine and Cerro San Pedro. Peak Mine’s gold production increased 33% reflecting increases in ore grade and improved mill recoveries. At Cerro San Pedro and Mesquite, planned mine sequencing resulted in below reserve grade ore being placed on the leach pads which led to production being below that of the first quarter of 2012 when grades closer to reserve grade were mined. Per the Company’s plans, gold grades and production are scheduled to increase during the balance of the year. In addition, at Mesquite, the two haul trucks the Company had planned to add to the fleet are now in operation. These trucks should enable Mesquite to increase the mining rate and ore tonnes placed on the leach pad.

New Gold’s consolidated copper production during the first quarter increased to 16.0 million pounds from 3.7 million pounds in the same period of the prior year. The increase was largely attributable to a full quarter of production from New Afton, though Peak Mines also increased copper production during the quarter. The increased production at Peak Mines was due to continued mill recovery improvements, which were partially offset by lower copper grades.

As expected, silver production at Cerro San Pedro decreased during the first quarter with 358,905 ounces in 2013 relative to 456,584 ounces in 2012, due primarily to planned mining of lower silver grades.

Revenues

Revenues were $201.8 million for the first quarter of 2013, an increase of 20% compared to $168.8 million in the same period in 2012. The $33.0 million revenue increase is driven primarily by higher gold and copper sales volumes relative to the same prior year period. Gold sales in the first quarter of 2013 were 95,181 ounces, relative to 93,676 ounces in the first quarter of 2012, as inventory movements impacted the relative periods. Copper sales were 15.9 million pounds, relative to 1.8 million pounds in the same prior year period as New Afton was still in the development stage in the first quarter of 2012. Sales of silver decreased to 360,913 ounces from 439,141 ounces in the same prior year period, in line with production. These increases in sales volumes were partly offset by lower average realized prices across all metals.

Operating expenses

Operating expenses increased from $72.3 million in the first quarter of 2012 to $106.1 million in 2013, impacted largely by New Afton’s full quarter of production. Gross operating costs for New Afton in the first quarter of 2013 were $26.6 million, for which there is no prior year comparative as New Afton was still in the development stage in the first half of 2012.

Depreciation and depletion

Depreciation and depletion for the first quarter of 2013 was $37.9 million compared to $18.8 million for the same prior year period, again primarily as a result of New Afton’s full quarter of commercial production. Depreciation and depletion for New Afton was $18.4 million, for which there is no prior year comparative as New Afton was still in the development stage in the first half of 2012.

9

Earnings from mine operations

For the three months ended March 31, 2013, New Gold had earnings from mine operations of $57.8 million compared with $77.7 million in the same prior year period. The benefits of increased earnings from mine operations from New Afton and the Peak Mines were more than offset by decreases at Cerro San Pedro and Mesquite due to planned mining of lower grade ore. In addition, with New Afton now forming part of the Company’s depreciable asset base, the non-cash depreciation and depletion expense increased by $19.1 million when compared to the same period of the prior year.

Corporate administration costs

Corporate administration costs were $7.3 million in the first quarter of 2013 compared to $6.7 million incurred in the same prior year period.

Share-based compensation costs

Share-based compensation costs were $2.5 million and $2.4 million in the first quarter of 2013 and 2012, respectively.

Exploration and business development

Exploration costs were $4.0 million in the first quarter of 2013 compared with $2.8 million for the same prior year period. New Afton incurred $1.9 million in exploration expense for the quarter, compared to $nil in the prior period, as the C-Zone exploration program continued in the first quarter of 2013, with the objective of adding to the Mineral Resource immediately at the base of the current Reserve block and further delineating the C-Zone which lies immediately down plunge of the current New Afton Reserve.

Hedging

For the quarter ended March 31, 2013, Mesquite had realized losses of $10.8 million within revenues for settlement of gold hedge contracts during the quarter totalling 16,500 ounces. As a result of the decrease in the spot price of gold from $1,658 per ounce to $1,598 per ounce between December 31, 2012 and March 31, 2013, Mesquite recognized $9.1 million of pre-tax unrealized gains in the mark-to-market of remaining contracts within other comprehensive income.

Other gains and losses

The following other gains and losses are all added back for the purposes of adjusted net earnings:

Non-hedged derivatives

For the quarter ended March 31, 2013, the Company recorded a gain of $22.6 million relating to the share purchase warrants. This compares to a loss of $7.6 million in the same prior year quarter. As the share purchase warrants are denominated in Canadian dollars, but the Company’s functional currency is the U.S. dollar, it is a requirement under IFRS to account for them as a liability. The fair value of this liability is assessed at each reporting period. As the traded value of the New Gold share purchase warrants increases or decreases, a related loss or gain on the mark-to-market of the liability is reflected on the financial statements.

In the first quarter of 2012, the Company recorded a gain of $2.7 million relating to the equity conversion option of its previously held Debentures, as well as a loss of $3.7 million relating to the change in fair value of the early redemption option embedded in the Company's previously held Senior Secured Notes. As both the Debentures and Senior Secured Notes were redeemed in 2012, there is no figure for the first quarter of 2013.

Foreign exchange

The Company recognized a foreign exchange loss of $5.6 million for the quarter ended March 31, 2013 compared to a loss of $1.5 million in the same prior year quarter. Foreign exchange gains and losses arise due to the fact that the Company operates in Canada, Australia, Mexico, Chile and the United States and, as a result, has foreign currency exposure with respect to items not denominated in U.S. dollars.

Ineffectiveness of hedge instruments

For the quarter ended March 31, 2013, a loss of $0.5 million was recorded reflecting the ineffective portion of the gold hedge. This compares to a loss of $0.2 million for the same prior year period.

Income tax

Income and mining tax expense in the first quarter of 2013 was $12.4 million compared to $18.3 million in the same prior year period, reflecting an effective tax rate of 25% for the first quarter of 2013 compared to 35% in 2012.

On an adjusted net earnings basis, the adjusted effective tax rate in the first quarter of 2013 was 37% compared to 31% in the same prior year period. The adjusted effective tax rates exclude the impact of changes in the recognition of deferred tax assets, specifically fair value changes in share purchase warrants and convertible debentures, as well as the impact of adjustments to uncertain tax positions. The adjusted effective tax rate has increased compared to the same prior year period due to the geographic mix as a higher proportion of profits earned in the first quarter of 2013 are in higher tax jurisdictions. The profit mix will change as the year progresses and the annual adjusted effective tax rate is expected to be lower than the first quarter rate.

10

Net earnings from continuing operations

For the quarter ended March 31, 2013, New Gold had net earnings from continuing operations of $36.3 million, or $0.08 per basic share. This compares with net earnings from continuing operations of $33.5 million, or $0.07 per basic share in the same prior year period.

Adjusted net earnings

For the three months ended March 31, 2013, adjusted net earnings from continuing operations were $20.6 million or $0.04 per basic share, a decrease from $44.2 million or $0.10 per basic share in the prior year period.

Net earnings have been adjusted, including the associated tax impact, for the group of costs in “Other gains and losses” on the condensed consolidated income statement. Key entries in this grouping are the fair value changes for share purchase warrants and convertible debt. Additionally, foreign exchange gain or loss and other non-recurring items are adjusted. Adjusting for these items provides an additional measure to evaluate the underlying operating performance of the Company as a whole for the reporting periods presented. The prior period tax is also adjusted for the foreign exchange impact of deferred tax on non-monetary assets.

See “Non-GAAP Financial Performance Measures” for reconciliation of net earnings to adjusted net earnings.

Quarterly financial and operating information

Selected financial and operating information for the current and previous quarters is as follows:

QUARTERLY FINANCIAL AND OPERATING INFORMATION

| (in millions of U.S. dollars, except per share amounts and where noted) | |||||||||

| Q1 2013 | Q4 2012 | Q3 2012 | Q2 2012 | Q1 2012 | Q4 2011 | Q3 2011 | Q2 2011 | Q1 2011 | |

| Gold sales (ounces) | 95,181 | 109,766 | 95,166 | 96,928 | 93,676 | 99,612 | 93,028 | 95,039 | 104,211 |

| Revenues | 201.8 | 250.9 | 195.5 | 176.1 | 168.8 | 177.6 | 175.5 | 171.6 | 171.2 |

| Net earnings (loss) from continuing operations | 36.3 | 123.9 | 17.8 | 23.7 | 33.5 | 35.0 | 40.7 | 78.6 | 24.7 |

| Per share: | |||||||||

| Basic | 0.08 | 0.26 | 0.04 | 0.05 | 0.07 | 0.08 | 0.09 | 0.19 | 0.06 |

| Diluted | 0.08 | 0.26 | 0.03 | 0.05 | 0.07 | 0.07 | 0.09 | 0.16 | 0.06 |

| Net earnings (loss) | 36.3 | 123.9 | 17.8 | 23.7 | 33.5 | 35.0 | 40.7 | 78.6 | 24.7 |

| Per share: | |||||||||

| Basic | 0.08 | 0.26 | 0.04 | 0.05 | 0.07 | 0.08 | 0.09 | 0.19 | 0.06 |

| Diluted | 0.08 | 0.26 | 0.03 | 0.05 | 0.07 | 0.07 | 0.09 | 0.16 | 0.06 |

| Adjusted net earnings | 20.6 | 49.7 | 42.6 | 45.8 | 44.2 | 42.2 | 49.5 | 49.8 | 47.9 |

| Per share: | |||||||||

| Basic | 0.04 | 0.11 | 0.09 | 0.10 | 0.10 | 0.09 | 0.11 | 0.12 | 0.12 |

| Diluted | 0.04 | 0.11 | 0.09 | 0.10 | 0.09 | 0.09 | 0.11 | 0.12 | 0.12 |

11

REVIEW OF OPERATING MINES

NEW AFTON MINE, BRITISH COLUMBIA, CANADA

A summary of New Afton’s operating results is provided below:

| Three months ended March 31 | ||||||

| (in millions of U.S. dollars, except where noted) | 2013 | 2012 | ||||

Operating information (1): | ||||||

| Ore mined (thousands of tonnes) | 754 | - | ||||

| Ore processed (thousands of tonnes) | 834 | - | ||||

| Average grade: | ||||||

| Gold (grams/tonne) | 0.67 | - | ||||

| Copper (%) | 0.79 | - | ||||

| Recovery rate (%): | ||||||

| Gold | 83.2 | - | ||||

| Copper | 81.3 | - | ||||

| Gold (ounces) | ||||||

Produced (2) | 14,936 | - | ||||

Sold (2) | 15,577 | - | ||||

| Copper (thousands of pounds) | ||||||

Produced (2) | 11,809 | - | ||||

Sold (2) | 12,069 | - | ||||

Average realized price (3): | ||||||

| Gold ($/ounce) | 1,591 | - | ||||

| Copper ($/pound) | 3.44 | - | ||||

Total cash costs per gold ounce sold (3)(4) | (770) | - | ||||

Financial Information (1): | ||||||

| Revenues | 63.4 | - | ||||

| Earnings from mine operations | 18.4 | - | ||||

| Capital expenditures | 42.0 | 74.4 | ||||

| 1. | There are no comparative figures for the first quarter of 2012 as New Afton reached commercial production on July 31, 2012. |

| 2. | Production is shown on a total contained basis while sales are shown on a net payable basis, including final product inventory and smelter payable adjustments, where applicable. |

| 3. | We use certain non-GAAP financial performance measures throughout our MD&A. Total cash costs per gold ounce sold, average realized price, average realized margin, adjusted net earnings, adjusted net earnings per share and cash generated from operations, excluding working capital changes and income taxes paid are non-GAAP financial performance measures with no standard meaning under IFRS. For further information and a detailed reconciliation, please refer to the “Non-GAAP Financial Performance Measures” section of this MD&A. |

| 4. | The calculation of total cash costs per ounce of gold is net of by-product copper revenue. If copper revenues were treated as a co-product, the average total cash costs at New Afton for the three months ended March 31, 2013 would be $721 per ounce of gold and $1.56 per pound of copper. |

Quarterly and Year to Date Operating Results

Production

In the first quarter of 2013, New Afton produced 14,936 ounces of gold and 11.8 million pounds of copper. There are no prior year comparatives as New Afton was still in the development stage throughout the first half of 2012. New Afton’s production increased in each consecutive month of the first quarter with further increases being seen in April. Production in early 2013 was impacted by the better-than-planned ramp up of the New Afton mill in the second half of 2012. As a result, the vast majority of New Afton’s ore stockpile was milled in 2012. Thus, the Company supplemented underground ore feed in January with remnant lower grade ore from the historical Afton open pit which also reduced the overall mill recoveries for the quarter. As planned, in late January, the installation of the permanent underground crusher was completed. This resulted in the underground mining rate steadily increasing to an average of 11,000 tonnes per day in March which compares to an average mining rate of 7,200 tonnes per day in the fourth quarter of 2012. As the New Afton mine and mill are now running at equivalent throughput rates, consistent with the operation’s 11,000 tonne per day nameplate capacity, and at planned gold and copper grades, the Company anticipates a steady increase in gold and copper production as the year progresses.

Revenue

Revenue in the first quarter of 2013 was $63.4 million compared to $nil in the prior year period. The average realized prices were $1,591 per ounce of gold and $3.44 per pound of copper. This is slightly lower than the average London PM fix gold price of $1,630 for the first quarter of 2013. The average London Metals Exchange copper price was $3.60 for the first quarter of 2013. Average realized prices were impacted by timing of sales.

12

Total cash costs

Total cash costs per ounce of gold sold, net of by-product sales is negative $770 per ounce for the first quarter of 2013. Consistent with planned increases in gold and copper production during the remaining quarters of 2013, New Afton’s cash costs are expected to decline over the balance of the year.

Earnings from mine operations

New Afton contributed $18.4 million to the Company’s earnings from mine operations for the three months ended March 31, 2013.

Capital expenditures

Capital expenditures for the first quarter of 2013 totaled $42.0 million relative to $74.4 million for the first quarter of 2012. Capital expenditures were significantly reduced in 2013 as New Afton entered into commercial production and reduced its development capital expenditure. Capital expenditures in 2013 are in excess of life of mine sustaining capital expenditure annual averages as the east cave is being developed and draw bell development remains accelerated in 2013. New Afton expects to develop an additional 37 draw bells in 2013. Additionally, some final construction expenditures were incurred in the first quarter of 2013, particularly related to the completion of the permanent underground crusher.

Exploration Project Review

In July 2012, New Gold initiated an exploration core drilling program to test the potential to expand the Main B-Zone Reserve currently being mined along strike and to expand the deeper C-Zone Mineral Resource located immediately below the B-Zone Reserve block. Total surface and underground exploration drilling during 2012 amounted to 17,072 metres in 34 holes. Seven of these 34 holes were incorporated into updated Mineral Resource and Reserve estimates completed on December 31, 2012 and reported previously.

Subsequent to quarter-end, the Company completed an updated Mineral Resource estimate for the C-Zone. The new Mineral Resource estimate incorporates the results for drilling which was completed in late 2012 and not included in the December 31, 2012 Mineral Resource estimate, as well as drilling completed through the end of February 2013.. The update reflects an increase by over 300% in gold ounces and copper pounds at improved grade. Measured and Indicated gold and copper Resources increased to 0.3 million ounces and 211 million pounds, respectively. Measured and Indicated gold and copper grades increased to 0.77 grams per tonne gold and 0.77% copper from 0.62 grams per tonne and 0.68% copper. The Inferred gold and copper Resources increased by over 30% to 0.4 million ounces and 301 million pounds.

The Company currently has three drills actively exploring the C-Zone and continues to target the completion of 30,000 metres of drilling in 2013. The Company also recently initiated a 17,000 metre program targeting extensions to the main reserve, with two surface core drills and one underground drill currently active. The objective of the C-Zone exploration drilling is to add to the mine’s life while, at the same time, New Gold continues to evaluate opportunities to increase the throughput rate beyond the nameplate capacity of 11,000 tonnes per day.

New Afton C-Zone Mineral Resource Update – May 1, 2013 | |||||||

| Resource Category | Tonnes & Grade | Contained Metal | |||||

Tonnes 000’s | Gold g/t | Silver g/t | Copper % | Gold Koz | Silver Koz | Copper Mlbs | |

| Measured | 1,282 | 0.75 | 1.35 | 0.79 | 31 | 56 | 22 |

| Indicated | 11,205 | 0.78 | 1.52 | 0.77 | 280 | 548 | 189 |

| Total M&I | 12,486 | 0.77 | 1.50 | 0.77 | 311 | 602 | 211 |

| Inferred | 20,221 | 0.62 | 1.42 | 0.68 | 401 | 923 | 301 |

New Afton C-Zone Mineral Resource – December 31, 2012 | |||||||

| Resource Category | Tonnes & Grade | Contained Metal | |||||

Tonnes 000’s | Gold g/t | Silver g/t | Copper % | Gold Koz | Silver Koz | Copper Mlbs | |

| Measured | 400 | 0.60 | 1.30 | 0.73 | 8 | 20 | 6 |

| Indicated | 2,900 | 0.63 | 1.30 | 0.68 | 58 | 120 | 43 |

| Total M&I | 3,300 | 0.62 | 1.30 | 0.68 | 66 | 140 | 49 |

| Inferred | 13,600 | 0.70 | 1.50 | 0.76 | 307 | 670 | 228 |

| 1. | Mineral resources are reported above a 0.40% copper-equivalent cut-off grade based on metal prices of $1,400/ounce gold, $28.00/ounce silver and $3.25/pound copper, average metallurgical recoveries of 87.7% for gold, 73.5% for silver and 86.4% for copper and related smelter and refining charges. |

| 2. | Total contained metal calculated on the basis of tonnes multiplied by gold or silver grade divided by 31.10348 grams per troy ounce, and tonnes multiplied by copper percent grade and 2.2046 |

| 3. | Additional technical details regarding the New Afton project are available in the NI 43-101 Technical Report dated December 31, 2009 published on SEDAR. |

| 4. | As it is currently defined by exploration drilling, the C-Zone has a sub-vertical dip of 80° and a moderate southwesterly plunge. The zone measures approximately 800 metres along its lateral strike, 550 metres in the vertical dimension, and ranges from 10 to 100 metres in true width, averaging 50 metres in true width overall. |

13

CERRO SAN PEDRO MINE, SAN LUIS POTOSÍ, MEXICO

A summary of Cerro San Pedro’s operating results is provided below:

| Three months ended March 31 | |||||

| (in millions of U.S. dollars, except where noted) | 2013 | 2012 | |||

| Operating information: | |||||

| Ore mined (thousands of tonnes) | 3,434 | 4,016 | |||

| Waste mined (thousands of tonnes) | 3,532 | 4,530 | |||

| Ratio of waste to ore | 1.03 | 1.13 | |||

| Ore to leach pad (thousands of tonnes) | 3,434 | 4,016 | |||

| Average grade: | |||||

| Gold (grams/tonne) | 0.32 | 0.46 | |||

| Silver (grams/tonne) | 18.15 | 26.69 | |||

| Gold (ounces) | |||||

Produced (1) (2) | 26,387 | 33,984 | |||

Sold (1) | 26,468 | 32,771 | |||

| Silver (ounces) | |||||

Produced (1) (2) | 358,905 | 456,584 | |||

Sold (1) | 360,913 | 439,141 | |||

Average realized price (3): | |||||

| Gold ($/ounce) | 1,619 | 1,693 | |||

| Silver ($/ounce) | 29.51 | 32.70 | |||

Total cash costs per gold ounce sold (3)(4) | 495 | 233 | |||

Financial Information: | |||||

| Revenues | 53.5 | 69.9 | |||

| Earnings from mine operations | 22.6 | 40.0 | |||

| Capital expenditures | 3.1 | 2.9 | |||

| 1. | Production is shown on a total contained basis while sales are shown on a net payable basis, including final product inventory adjustments, where applicable. |

| 2. | Tonnes of ore processed each period does not necessarily correspond to ounces produced during the period, as there is a time delay between placing tonnes on the leach pad and pouring ounces of gold. |

| 3. | We use certain non-GAAP financial performance measures throughout our MD&A. Total cash costs per gold ounce sold, average realized price, average realized margin, operating margin, adjusted net earnings, adjusted net earnings per share and cash generated from operations, excluding working capital changes and income taxes paid, are non-GAAP financial performance measures with no standard meaning under IFRS. For further information and a detailed reconciliation, please refer to the “Non-GAAP Performance Measures” section of this MD&A. |

| 4. | The calculation of total cash costs per ounce of gold is net of by-product silver revenue. If the silver revenues were treated as a co-product, the average total cash costs at Cerro San Pedro for the three months ended March 31, 2013, would be $719 per ounce of gold (2012 - $533 ) and $13.10 per ounce of silver (2012 - $10.30 ). |

Quarterly and Year to Date Operating Results

Production

Gold production for the first quarter of 2013 was 26,387 ounces compared to 33,984 ounces produced in the same period in 2012. Silver production for the quarter was 358,905 ounces compared to 456,584 ounces produced in the same period in 2012. The decrease in gold and silver production is due to a combination of lower tonnes processed and planned mining of lower ore grades. The production profile of Cerro San Pedro in 2013 reflects improving gold and silver grades through the remainder of the year.

Revenue

Revenue for the first quarter of 2013 were $53.5 million compared to $69.9 million in the same prior year period due to lower ounces sold and lower average realized prices for both gold and silver. Consistent with production, gold sales for the first quarter of 2013 were 26,468 ounces relative to 32,771 ounces in the same prior year period. Silver sales also decreased, from 439,141 ounces in the first quarter of 2012 to 360,913 ounces in the same period in 2013. The average realized gold price during the first quarter of 2013 and 2012 was $1,619 and $1,693 per ounce, respectively which compares to the average London PM fix gold price of $1,630 and $1,689 per ounce, respectively. The average realized silver price per ounce during the first quarter of 2013 and 2012 were $29.51 and $32.70 per ounce, respectively. This compares to the average London fix silver price of $30.08 and $32.62 per ounce, respectively.

Total cash costs

Total cash costs per ounce of gold sold for the first quarter of 2013 of $495 per ounce were consistent with the Company’s quarterly plans and compared to $233 per ounce in the same prior year quarter. The increase in total cash costs when compared to the same period of 2012 is primarily driven by lower silver sales and prices negatively impacting by-product revenue, as well as the appreciation of the Mexican Peso and planned lower gold production. Per the 2013 mine plan, improving gold and silver ore grades should drive lower cash costs for the remainder of the year.

14

Earnings from mine operations

Cerro San Pedro generated $22.6 million in earnings from mine operations in the first quarter of 2013 compared to $40.0 million in the same period of the prior year.

Capital expenditures

Capital expenditures totalled $3.1 million and $2.9 million for the quarters ended March 31, 2013 and 2012, respectively. The projects in progress during the first quarter of 2013 are primarily targeting accelerated silver leaching.

Impact of Foreign Exchange on Operations

Cerro San Pedro was impacted by changes in the value of the Mexican peso against the U.S. dollar. The value of the Mexican peso increased from an average of 12.97 to the U.S. dollar in the first quarter of 2012 to 12.65 to the U.S. dollar in 2013. This had a positive impact of $15 per ounce of gold sold, which further contributed to the impact of the other factors described above.

MESQUITE MINE, CALIFORNIA, USA

A summary of Mesquite’s operating results is provided below:

| Three months ended March 31 | |||||

| (in millions of U.S. dollars, except where noted) | 2013 | 2012 | |||

| Operating information: | |||||

| Ore mined (thousands of tonnes) | 3,505 | 3,672 | |||

| Waste mined (thousands of tonnes) | 8,890 | 7,228 | |||

| Ratio of waste to ore | 2.54 | 1.97 | |||

| Ore to leach pad (thousands of tonnes) | 3,505 | 3,672 | |||

| Average grade: | |||||

| Gold (grams/tonne) | 0.32 | 0.59 | |||

| Gold (ounces) | |||||

Produced (1) (2) | 25,504 | 44,400 | |||

Sold (1) | 25,708 | 43,617 | |||

Average realized price (3): | |||||

Gold ($/ounce) (4) | 1,201 | 1,423 | |||

Total cash costs per gold ounce sold (3) | 879 | 628 | |||

Financial Information: | |||||

| Revenues | 30.9 | 62.0 | |||

| Earnings from mine operations | 3.1 | 27.5 | |||

| Capital expenditures | 3.4 | 1.6 | |||

| 1. | Production is shown on a total contained basis while sales are shown on a net payable basis, including final product inventory and smelter payable adjustments, where applicable. |

| 2. | Tonnes of ore processed each period does not necessarily correspond to ounces produced during the period, as there is a time delay between placing tonnes on the leach pad and pouring ounces of gold. |

| 3. | We use certain non-GAAP financial performance measures throughout our MD&A. Total cash costs per gold ounce sold, average realized price, average realized margin, operating margin, adjusted net earnings, adjusted net earnings per share and cash generated from operations, excluding working capital changes and income taxes paid, are non-GAAP financial performance measures with no standard meaning under IFRS. For further information and a detailed reconciliation, please refer to the “Non-GAAP Financial Performance Measures” section of this MD&A. |

| 4. | Average realized price per gold ounce for Mesquite includes realized gains and losses from gold hedge settlements. |

Quarterly and Year to Date Operating Results

Production

Gold production for the quarter ended March 31, 2013 was 25,504 ounces compared to 44,400 ounces produced in the same period in 2012. Production was lower in 2013 due to the mine plan moving through a phase of ore that was below reserve grade, or 0.32 grams per tonne. This compares to the first quarter of 2012 when ore grade was considerably higher at 0.59 grams per tonne. Similar to Cerro San Pedro, ore grade is expected to progressively improve through the remainder of 2013 resulting in increased production in later quarters of 2013.

Revenue

Revenue for the quarter ended March 31, 2013 was $30.9 million compared to $62.0 million in the same period last year due to negative variances in both volume and price. Consistent with production, gold ounces sold in the first quarter of 2013 were 25,708 ounces relative to 43,617 ounces in the prior year period, representing a point when Mesquite was mining above reserve grade ore. The average realized gold price during the first quarter of 2013 of $1,201 per ounce, including hedged gold ounce settlements at $801 per ounce, compared to $1,423 per ounce of gold sold in the same prior year period.

15

Total cash costs

Total cash costs per ounce of gold sold for the quarter ended March 31, 2013 were $879 per ounce, compared to $628 per ounce in the same prior year period. Mesquite’s total gross operating costs remained consistent with the prior year period with the mine benefitting from lower fuel and explosive costs. As such, the increase in total cash costs per ounce sold was primarily driven by the planned mining of lower grade ore resulting in costs being spread over a lower production base.

Earnings from mine operations

As a result of a lower average realized gold price and fewer ounces sold, Mesquite generated $3.1 million in earnings from mine operations for the quarter ended March 31, 2013, compared to $27.5 million in the same period in 2012.

Capital expenditures

Capital expenditures totalled $3.4 million and $1.6 million, for the quarters ended March 31, 2013 and 2012, respectively. The increase in 2013 was due to the scheduled component replacements on heavy equipment.

PEAK MINES, NEW SOUTH WALES, AUSTRALIA

A summary of Peak Mines’ operating results is provided below:

| Three months ended March 31 | |||||

| (in millions of U.S. dollars, except where noted) | 2013 | 2012 | |||

| Operating information: | |||||

| Ore mined (thousands of tonnes) | 156 | 172 | |||

| Ore processed (thousands of tonnes) | 201 | 184 | |||

| Average grade: | |||||

| Gold (grams/tonne) | 4.72 | 3.90 | |||

| Copper (%) | 1.03 | 1.10 | |||

| Recovery rate (%): | |||||

| Gold | 91.5 | 91.0 | |||

| Copper | 91.9 | 83.0 | |||

| Gold (ounces) | |||||

Produced (1) | 27,868 | 20,890 | |||

Sold (1) | 27,428 | 17,288 | |||

| Copper (thousands of pounds) | |||||

Produced (1) | 4,189 | 3,683 | |||

Sold (1) | 3,798 | 1,780 | |||

Average realized price (2): | |||||

| Gold ($/ounce) | 1,592 | 1,737 | |||

| Copper ($/pound) | 3.43 | 4.14 | |||

Total cash costs per gold ounce sold (2)(3) | 819 | 915 | |||

Financial Information: | |||||

| Revenues | 54.0 | 36.9 | |||

| Earnings from mine operations | 13.7 | 10.2 | |||

| Capital expenditures | 13.4 | 9.2 | |||

| 1. | Production is shown on a total contained basis while sales are shown on a net payable basis, including final product inventory and smelter payable adjustments, where applicable. |

| 2. | We use certain non-GAAP financial performance measures throughout our MD&A. Total cash costs per gold ounce sold, average realized price, average realized margin, adjusted net earnings, adjusted net earnings per share and cash generated from operations, excluding working capital changes and income taxes paid are non-GAAP financial performance measures with no standard meaning under IFRS. For further information and a detailed reconciliation, please refer to the “Non-GAAP Financial Performance Measures” section of this MD&A. |

| 3. | The calculation of total cash costs per ounce of gold is net of by-product copper revenue. If copper revenues were treated as a co-product, the average total cash costs at Peak Mines for the three months ended March 31, 2013 would be $990 per ounce of gold (2012 - $1,059 ) and $2.27 per pound of copper (2012 - $2.81 ). |

Quarterly and Year to Date Operating Results

Production

Peak Mines produced 27,868 ounces of gold and 4.2 million pounds of copper during first quarter of 2013 compared to 20,890 ounces of gold and 3.7 million pounds of copper for the same prior year period. Gold production benefitted from higher grade and improved recovery rates in the first quarter of 2013 relative to the prior year period, coupled with higher ore tonnes processed.

Revenue

Revenue for the three months ended March 31, 2013 was $54.0 million compared to $36.9 million in the same period in 2012. Although Peak Mines sold more gold ounces and copper pounds, these volume increases was partially offset by a decrease in both gold and copper average realized price relative to 2012. Gold ounces sold increased from 17,288 in 2012 to 27,428 in the current year, however, the average realized gold price was $1,592 per ounce compared to $1,737 per ounce in the same prior year period. This compares to the average London PM fix gold price of $1,630 and $1,689 per ounce for the three months ended March 31, 2013 and 2012, respectively. Copper sales were 3.8 million pounds compared to 1.8 million pounds in the prior year, however, copper prices were $3.43 per pound compared to $4.14 per pound in the prior year. The average London Metals Exchange copper price was $3.60 for three months ended March 31, 2013 and $3.77 for the same period in 2012.

16

Total cash costs

Total cash costs per ounce of gold sold for the first quarter of 2013 were $819 compared to $915 in the same period of 2012. This decrease in total cash costs was attributable to a combination of high copper by-product revenue, the depreciation of the Australian dollar and higher gold production.

Earnings from mine operations

For the first quarter of 2013, the higher sales volume of gold and copper resulted in Peak Mines generating $13.7 million in earnings from operations compared to $10.2 million in the same prior year period.

Capital expenditures

Capital expenditures totalled $13.4 million and $9.2 million for the quarter ended March 31, 2013 and 2012, respectively. Capital expenditures in the first quarter of 2013 were primarily associated with mine development and mobile fleet replacement, with the increase on prior year specifically related to scheduled loader and truck replacements.

Impact of Foreign Exchange on Operations

Peak Mines’ operations continue to be impacted by fluctuations in the valuation of the Australian dollar against the U.S. dollar. The value of the Australian dollar in the first quarter of 2013 averaged 0.96 against the U.S. dollar compared to 0.95 in the first quarter of 2012 resulting in a negative impact on cash costs of $33 per gold ounce sold.

Exploration Project Review

During the first quarter of 2013, the Company conducted 15,246 metres of underground exploration drilling to delineate additional Mineral Resources and Reserves at its Peak Mines operations. Approximately 50% of this total was drilled in the Perseverance deposit, 40% in the New Cobar deposit, and 10% in the Comstock exploration target zone. Additionally, a surface drilling program commenced at the Great Cobar deposit where a total of 1,723 metres of diamond drilling targeting extensions to the main lodes was completed. The Great Cobar mine was a significant historic producer of copper and gold in the region. Exploration to define new drill targets on Peak’s regional claim holdings also continued during the first quarter.

DEVELOPMENT AND EXPLORATION REVIEW

BLACKWATER PROJECT, BRITISH COLUMBIA, CANADA

Blackwater is a bulk-tonnage gold project located approximately 160 kilometres southwest of Prince George, a city of approximately 80,000, in central British Columbia, Canada, where New Gold already has an established presence through New Afton. The project property position covers over 1,000 km2 and is located near infrastructure. As at March 31, 2013, Blackwater had a resource estimate of 9.5 million ounces of Measured and Indicated gold Resources and an additional 0.38 million ounces of Inferred gold Resources. New Gold also owns a 100% interest in the Capoose mineral prospect, located approximately 25 kilometres from the Blackwater deposit. As at December 31, 2012 Mineral Resources at Capoose included 0.2 million ounces of gold at 0.43 grams per tonne and 9.5 million ounces of silver at 20.8 grams per tonne in the Indicated category and 0.6 million ounces gold at 0.29 grams per tonne and 47.8 million ounces silver at 23.2 grams per tonne in the Inferred category.

Project Review

The Blackwater project was further advanced during the first quarter. In addition to completing the previously announced Mineral Resource update, the team focused on progressing the environmental assessment reports, completing required condemnation drilling for proposed infrastructure sites and preparing for the regional exploration program on the Company’s 1,000 square kilometre land package.

Exploration activity at Blackwater during the first quarter of 2013 included the completion of 41 holes totaling 19,434 metres drilled. This total included 7,425 metres in 12 holes to explore potential extensions to the Blackwater resource at depth to further prove and potentially extend the high grade zones in the west and north-central portions of the deposit. Additionally, 2,131 metres in 5 holes were drilled for project engineering studies and 9,878 metres in 24 holes to test the mineral potential of areas selected for future operations facilities and infrastructure. The completion of these drilling campaigns concludes the resource delineation and development drilling work to be incorporated into the project feasibility study scheduled for completion in late 2013.

17

Project spending at Blackwater, including exploration and infrastructure-related expenditures, for the three months ended March 31, 2013 was $15.0 million compared to $27.5 for the prior year period.

Subsequent to quarter-end, the Company completed an updated Mineral Resource estimate for Blackwater (‘March 2013 Resource’) which will serve as the basis for the project’s feasibility study currently in progress. The Mineral Resource incorporates the results of an additional 89 infill holes totaling 21,959 metres completed during the latter half of the fourth quarter of 2012 in combination with more refined geologic and geostatistical modeling. The estimate is based on 1,002 core holes totaling 309,509 metres. Consistent with the Company’s plans to develop the project, the resource statement reflects the segregation of mineralized material that should be processed directly from which the Company plans to stockpile and process toward the end of the project’s currently envisioned mine life. The Company has utilized a dual cut-off strategy to reflect this segregation. All material grading above a gold-equivalent grade of 0.40 grams per tonne is considered for direct processing, while all material grading between a gold-equivalent cut-off of 0.30 and 0.40 grams per tonne is considered for stockpiling.

Highlights of the updated Mineral Resource estimate include:

| · | Measured and Indicated gold resources for direct processing increased to 8.6 million ounces of gold at 0.88 grams per tonne and 57.5 million ounces of silver at 5.8 grams per tonne. | |||||||

| · | Measured gold resources increased by 44% to 3.9 million ounces at 1.04 grams per tonne. | |||||||

Blackwater March 2013 Mineral Resource Statement – March 31, 2013 | ||||||||

| Resource Category | Tonnes & Grade | Contained Metal | ||||||

Tonnes 000’s | Gold g/t | Silver g/t | Gold Moz | Silver Koz | ||||

| Measured & Indicated Resources | ||||||||

Direct processing material Measured | 116,955 | 1.04 | 5.6 | 3.90 | 21.06 | |||

| Indicated | 189,044 | 0.78 | 6.0 | 4.73 | 36.47 | |||

| M&I (direct processing) | 305,999 | 0.88 | 5.8 | 8.62 | 57.52 | |||

| Stockpile material | ||||||||

| Measured | 26,521 | 0.30 | 4.1 | 0.26 | 3.50 | |||

| Indicated | 64,382 | 0.30 | 4.4 | 0.62 | 9.11 | |||

| M&I (stockpile) | 90,904 | 0.30 | 4.3 | 0.87 | 12.60 | |||

| Total M&I | 396,903 | 0.74 | 5.5 | 9.50 | 70.13 | |||

| Inferred resources | ||||||||

| Inferred (direct processing) | 13,815 | 0.76 | 4.1 | 0.34 | 1.82 | |||

| Inferred (stockpile) | 3,785 | 0.31 | 3.6 | 0.04 | 0.44 | |||

| Total Inferred | 17,600 | 0.66 | 4.0 | 0.38 | 2.26 | |||

| 1. | Mineral resources are reported within a conceptual open pit shell based on metal prices of $1,400/oz gold and $28.00/oz silver and average metallurgical recoveries of 88.0% gold and 64.0% silver for oxide mineralization, 85.0% gold and 58.0% silver for transitional oxide/sulfide mineralization and 85.0% gold and 44.0% silver for sulfide mineralization. |

| 2. | Total contained metal calculated on the basis of Tonnes * Grade / 31.10348 grams per troy ounce. |

| 3. | Gold-equivalent cut-off grade estimates are based on $1,400/oz gold and $28.00/oz silver and average metal recoveries as described in Note 1 above |

| 4. | Direct processing material is defined as mineralization above a 0.40 g/t AuEq cut-off and likely to be mined and processed directly. |

| 5. | Stockpile material is defined as mineralization between a 0.30 g/t AuEq and a 0.40 AuEq cut-off that is suitable for stockpiling and future processing based on average metallurgical recoveries as described in Note 1 above. |

Mineral Resources are not Mineral Reserves and as such do not have demonstrated economic viability. This MD&A includes information on Blackwater which was outlined in the Preliminary Economic Assessment (“PEA”) Technical Report filed on October 10, 2012. New Gold has, since the date of the PEA, completed non-material updates of the Mineral Resource estimate for Blackwater. Although the PEA represents useful, accurate and reliable information based on the information available at the time of its publication, and provides an important indicator as to the economic potential of Blackwater, the PEA is based on Mineral Resource estimates with an effective date of July 27, 2012, which do not reflect drilling conducted since their effective date, and the PEA does not reflect the latest Mineral Resource estimate discussed in this MD&A. Certain assumptions used in the PEA, some of which relate to the July 27, 2012, Mineral Resource estimate may have changed from those used for the new Resource estimate, causing a variation of parameters. Moreover, the updated Mineral Resource estimate may impact how New Gold intends to develop the deposit, including pit outlines, production rates and mine life.

18

Feasibility Study Status

The Feasibility Study (“FS”) phase for Blackwater commenced in the first quarter. Highlights during this period include:

| · | Substantially completed the FS geological block model. |

| · | Substantially completed the FS metallurgical testwork program. |

| · | Awarded the FS plant design, project costing and FS Report compilation work to AMEC. |

| · | Completed mining studies for throughput selection and substantially completed study for trolley assisted haulage systems. |

| · | Confirmed the process flowsheet selection as Whole Ore Leach. |

| · | Confirmed plant capacity as 60,000 tonnes per day. |

| · | Completed second phase of geotechnical testing in the Tailings Storage Facility area, to significantly advance the design to minimize seepage. |

Work is ongoing to complete site layout design, finalize equipment sizing and establish the bases of estimate for the project. The feasibility study remains on track for completion in late 2013.

Other Project Highlights

Other highlights for Blackwater in the first quarter of 2013 include:

| · | Receipt of federal Environmental Impact Statement Guidelines and continuation of the provincial and federal environmental process. |

| · | Approval of amended multi-year area based exploration permits for 2013. |

| · | Initiation of discussions on Participation Agreements for construction and operation of the mine with key First Nations. |

| · | Advanced exploration target selection for Capoose and other prospective areas identified for reconnaissance drilling in 2013. |

EL MORRO PROJECT, ATACAMA REGION, CHILE

El Morro is an advanced stage gold-copper development project located in north-central Chile, Atacama Region, approximately 80 kilometres east of the city of Vallenar. El Morro is a world-class project with low expected cash costs and great organic growth potential. As at December 31, 2012, attributable to New Gold’s 30% share of the project are Proven and Probable gold Reserves of 2.9 million ounces and Proven and Probable copper Reserves of 2.1 billion pounds. The El Morro and La Fortuna deposits represent the two principal zones of gold-copper mineralization that have been identified to date. Future exploration efforts will also test the potential bulk-mineable gold and copper production below the bottom of the current La Fortuna open pit.

Under the terms of New Gold's agreement with Goldcorp Inc. ("Goldcorp"), Goldcorp is responsible for funding New Gold's 30% share of capital costs. The carried funding accrues interest at a fixed rate of 4.58%. New Gold will repay its share of capital plus accumulated interest out of 80% of its share of the project's cash flow with New Gold retaining 20% of its share of cash flow from the time production commences. Pursuant to the above agreement, New Gold has drawn down $71.3 million of carried funding at March 31, 2013. New Gold had no cash outlay in 2013. New Gold’s 30% of project spending, excluding interest, for the first quarter of 2013 and 2012 were $5.8 million and $7.2 million, respectively.

Project field work has been temporarily suspended following the April 27, 2012 ruling by the Supreme Court of Chile against approval of El Morro’s environmental permit. Based on the Supreme Court's announcement, El Morro suspended all project field work being executed under the terms of the environmental permit. Activities not subject to the environmental permit, including detailed engineering, design work and architectural planning, continue. Goldcorp is working closely with the Chilean Environmental Permitting Authority, the Servicio de Evalucion Ambiental, to address any perceived deficiencies in respect of the environmental permit. It is anticipated this consultation process could be completed by late 2013 with the expectation that the modified EIA should be approved shortly thereafter. Goldcorp is also focused on obtaining the project permits and optimizing project economics including sourcing of a long-term power supply. See the "Contingencies" section of this MD&A for more details.

19

FINANCIAL CONDITION REVIEW

SUMMARY BALANCE SHEET

| March 31 | December 31 | ||

| (in millions of U.S. dollars, except where noted) | 2013 | 2012 | |

| Cash and cash equivalents | 672.4 | 687.8 | |

| Deferred tax assets | 192.8 | 194.1 | |

| Other assets | 3,437.0 | 3,401.8 | |

| Total assets | 4,302.2 | 4,283.7 | |

| Derivative liabilities | 88.4 | 110.5 | |

| Reclamation and closure cost obligations | 67.0 | 68.5 | |

| Long-term debt | 854.3 | 847.8 | |

| Deferred tax liabilities | 336.4 | 322.9 | |

| Other liabilities | 226.0 | 257.5 | |

| Total liabilities | 1,572.1 | 1,607.2 | |

| Total equity | 2,730.1 | 2,676.5 |

BALANCE SHEET REVIEW

Assets

At March 31, 2013, New Gold held cash and cash equivalents of $672.4 million. This compares to $687.8 million held at December 31, 2012. The Company’s investment policy is to invest its surplus funds in permitted investments consisting of treasury bills, bonds, notes and other evidences of indebtedness of Canada, the U.S. or any of the Canadian Provinces with a minimum credit rating of R-1 mid from the Dominion Bond Rating Service (“DBRS”) or an equivalent rating from Standard & Poor’s and Moody’s and with maturities of twelve months or less at the original date of acquisition. In addition, the Company is permitted to invest in bankers’ acceptances and other evidences of indebtedness of certain financial institutions.

Gold hedge contracts

Under the terms of the term loan facility entered into by Western Mesquite Mines, Inc. (“WMMI”), as a condition precedent to drawdown of the loan, WMMI entered into a gold hedging program required by the banking syndicate. As such, WMMI executed gold forward sales contracts for 429,000 ounces of gold at a price of $801 per ounce. New Gold assumed the liability for the sales contracts on completion of the business combination with Western Goldfields Inc. in mid-2009. As at March 31, 2013, the remaining gold contracts represent a commitment of 5,500 ounces per month for 21 months with the last commitment deliverable in December 2014 for a total of 115,500 ounces.

The remaining contracts were marked to market as at March 31, 2013 using the March 31, 2013 gold forward curve, resulting in a cumulative unrealized pre-tax loss of $88.4 million that has been disclosed as a liability.

Reclamation and Closure Cost Obligations