Exhibit 99.2

OPERATIONAL AND FINANCIAL HIGHLIGHTS

OPERATIONAL HIGHLIGHTS

All dollar figures are in United States dollars and tabular dollar amounts are in millions, unless otherwise noted.

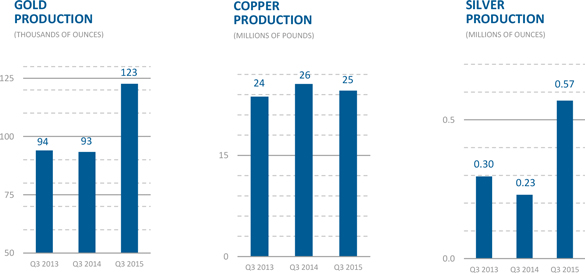

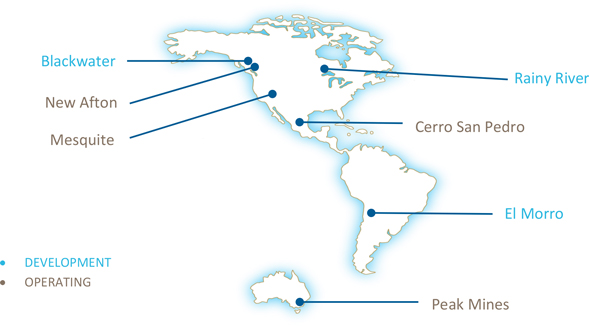

New Gold Inc. (“New Gold” or the “Company”) is an intermediate gold producer with operating mines in Canada, the United States, Australia and Mexico and development projects in Canada and Chile. For the nine months ended September 30, 2015, the New Afton Mine in Canada (“New Afton”), the Mesquite Mine in the United States (“Mesquite”), Peak Mines in Australia (“Peak Mines”) and the Cerro San Pedro Mine in Mexico (“Cerro San Pedro”) combined to produce 303,999 gold ounces, 71.1 million pounds of copper and 1.4 million silver ounces, building on the Company’s solid start to the year. During the third quarter of 2015 the Company’s mine sites produced 122,580 gold ounces, 24.6 million pounds of copper and 0.6 million silver ounces.

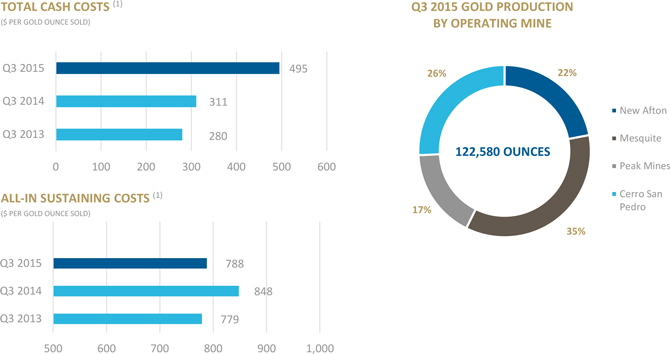

New Gold’s production costs remained competitive compared to the broader gold mining space as New Gold had total cash costs(1) of $495 per gold ounce sold and all-in sustaining costs(1) of $788 per gold ounce sold in the third quarter of 2015.We believe New Gold continues to further establish itself as one of the lowest cost producers in the industry.

| 1 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

FINANCIAL HIGHLIGHTS

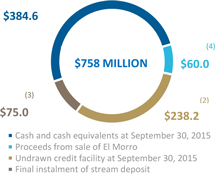

New Gold maintains a strong liquidity position with total liquidity of $758 million as of September 30, 2015 comprised of $385 million in cash and cash equivalents and $238 million available for drawdown under the Company’s $300 million revolving credit facility. In addition New Gold will receive the final $75 million of the deposit under the stream agreement when the applicable conditions precedent are satisfied, which is expected in mid-2016 and $60 million of after tax proceeds from the sale of El Morro which is expected to close in the fourth quarter of 2015.

|  |

| 1. | The Company uses certain non-GAAP financial performance measures throughout this Management’s Discussion & Analysis (“MD&A”). For a detailed description of each of the non-GAAP measures used in the MD&A and a detailed reconciliation, please refer to the “Non-GAAP Financial Performance Measures” section of the MD&A. |

| 2. | Of the $300 million credit facility, $61.8 million is utilized for letters of credit as at September 30, 2015. |

| 3. | The first installment of $100 million was paid to New Gold on July 20th and payment for the second installment of $75 million is subject to certain conditions. Refer to the “Corporate Developments” section of this MD&A for more information. |

| 4. | New Gold announced the sale of its interest in El Morro for $60.0 million cash (net of tax), a 4% gold stream from the El Morro property and the cancellation of New Gold’s carried funding loan. Refer to the “Corporate Developments” section of this MD&A for more information. |

| 5. | Net cash from operations and net cash generated from operations before working capital changes in Q3 2013 excludes $17.8 million of Rainy River acquisition expenses paid. |

Three months ended September 30 | Nine months ended September 30 | |||

| (in millions of U.S. dollars, except where noted) | 2015 | 2014 | 2015 | 2014 |

| Operating information | ||||

| Gold production (ounces) | 122,580 | 93,367 | 303,999 | 274,144 |

| Gold sales (ounces) | 115,695 | 88,168 | 295,847 | 266,956 |

| Average realized price ($/ounce)(1) | $1,117 | $1,236 | $1,174 | $1,283 |

| Total cash costs per gold ounce sold ($/ounce)(1) | $495 | $311 | $464 | $272 |

| All-in sustaining costs per gold ounce sold ($/ounce)(1) | $788 | $848 | $895 | $754 |

| Financial Information | ||||

| Revenues | $177.3 | $169.3 | $513.9 | $537.9 |

| Net earnings (loss) | (157.8) | (59.6) | (191.9) | (45.2) |

| Adjusted net (loss) earnings(1) | (8.5) | 5.4 | (13.9) | 31.8 |

| Net cash generated from operations | 51.0 | 58.2 | 177.7 | 198.9 |

| Net cash generated from operations before changes in non-cash working capital(1) | 58.4 | 78.6 | 188.5 | 240.6 |

| Cash and cash equivalents | 384.6 | 416.1 | 384.6 | 416.1 |

| Capital expenditures (sustaining and growth) | 76.7 | 73.7 | 219.8 | 190.6 |

| Share Data | ||||

| Earnings (loss) per basic share ($) | (0.31) | (0.12) | (0.38) | (0.09) |

| Adjusted net (loss) earnings per basic share(1)($) | (0.02) | 0.01 | (0.03) | 0.06 |

| 2 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Contents

| OPERATIONAL HIGHLIGHTS | 1 |

| FINANCIAL HIGHLIGHTS | 2 |

| OUR BUSINESS | 4 |

| OPERATING AND FINANCIAL HIGHLIGHTS | 5 |

| CORPORATE DEVELOPMENTS | 9 |

| CORPORATE SOCIAL RESPONSIBILITY | 11 |

| OUTLOOK FOR 2015 | 13 |

| KEY PERFORMANCE DRIVERS | 13 |

| FINANCIAL RESULTS | 16 |

| REVIEW OF OPERATING MINES | 24 |

| DEVELOPMENT AND EXPLORATION REVIEW | 36 |

| FINANCIAL CONDITION REVIEW | 40 |

| NON-GAAP FINANCIAL PERFORMANCE MEASURES | 47 |

| ENTERPRISE RISK MANAGEMENT | 58 |

| CRITICAL JUDGMENTS AND ESTIMATION UNCERTAINTIES | 65 |

| CONTROLS AND PROCEDURES | 69 |

| CAUTIONARY NOTES | 70 |

| 3 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the three and nine months ended September 30, 2015

The following Management’s Discussion and Analysis (“MD&A”) provides information that management believes is relevant to an assessment and understanding of the consolidated financial condition and results of operations of New Gold Inc. and its subsidiaries (“New Gold” or the “Company”). This MD&A should be read in conjunction with New Gold’s unaudited condensed consolidated financial statements for the three and nine months ended September 30, 2015 and 2014 and related notes which are prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). The MD&A should also be read in conjunction with our audited annual financial statements for the year ended December 31, 2014 and the related Management’s Discussion and Analysis. This MD&A contains forward-looking statements that are subject to risks and uncertainties, as discussed in a cautionary note contained in this MD&A. The reader is cautioned not to place undue reliance on forward-looking statements. This MD&A has been prepared as at October 28, 2015. Additional information relating to the Company, including the Company’s Annual Information Form, is available on SEDAR at www.sedar.com.

OUR BUSINESS

New Gold is an intermediate gold producer with operating mines in Canada, the United States, Australia and Mexico and development projects in Canada and Chile. The Company’s principal operating assets consist of the New Afton gold-copper mine in Canada, the Mesquite gold mine in the United States, the Peak Mines gold-copper mine in Australia and the Cerro San Pedro gold-silver mine in Mexico. In addition, New Gold’s principal development projects are its 100% owned Rainy River (“Rainy River”) and Blackwater (“Blackwater”) projects, both in Canada. In August 2015, New Gold announced that it had entered into an agreement to sell its 30% interest of the El Morro (“El Morro”) project in Chile.

New Gold’s operating portfolio is diverse both geographically and in the range of commodities that its operations produce. The assets produce gold with copper and silver by-products at total cash costs and all-in sustaining costs below the industry average. With a strong liquidity position, a simplified balance sheet and an experienced management and Board of Directors, the Company has a solid platform to continue to execute its growth strategy, both organically and through value-enhancing accretive acquisitions, to further establish itself as an industry leading intermediate gold producer.

| 4 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

OPERATING AND FINANCIAL HIGHLIGHTS

OPERATING HIGHLIGHTS

Three months ended September 30 | Nine months ended September 30 | |||

| (in millions of U.S. dollars, except where noted) | 2015 | 2014 | 2015 | 2014 |

| Operating information | ||||

| Gold (ounces): | ||||

| Produced(1) | 122,580 | 93,367 | 303,999 | 274,144 |

| Sold(1) | 115,695 | 88,168 | 295,847 | 266,956 |

| Silver (millions of ounces): | ||||

| Produced(1) | 0.6 | 0.2 | 1.4 | 1.1 |

| Sold(1) | 0.5 | 0.2 | 1.3 | 1.1 |

| Copper (millions of pounds): | ||||

| Produced(1) | 24.6 | 25.6 | 71.1 | 77.0 |

| Sold(1) | 21.6 | 22.7 | 67.4 | 72.2 |

| Average realized price(2): | ||||

| Gold ($/ounce) | 1,117 | 1,236 | 1,174 | 1,283 |

| Silver ($/ounce) | 14.72 | 19.66 | 15.72 | 19.90 |

| Copper ($/pound) | 2.23 | 3.11 | 2.52 | 3.06 |

| Total cash costs per gold ounce sold(2)(3) | 495 | 311 | 464 | 272 |

| All-in sustaining costs per gold ounce sold (2)(3) | 788 | 848 | 895 | 754 |

Total cash costs per gold ounce sold on a co-product basis (2)(3) | 662 | 666 | 693 | 668 |

All-in sustaining costs per gold ounce sold on a co-product basis(2)(3) | 867 | 983 | 972 | 951 |

| 1. | Production is shown on a total contained basis while sales are shown on a net payable basis, including final product inventory and smelter payable adjustments, where applicable. |

| 2. | The Company uses certain non-GAAP financial performance measures throughout this MD&A. Average realized price, total cash costs and all-in sustaining costs per gold ounce sold and total cash costs and all-in sustaining costs on a co-product basis are non-GAAP financial performance measures with no standard meaning under IFRS. For further information and a detailed reconciliation, please refer to the “Non-GAAP Financial Performance Measures” section of this MD&A. |

| 3. | The calculation of total cash costs and all-in sustaining costs per gold ounce sold is net of by-product silver and copper revenues. Total cash costs and all-in sustaining costs on a co-product basis remove the impact of other metal sales that are produced as a by-product of our gold production and apportions the cash costs to each metal produced on a percentage of revenue basis. If silver and copper revenues were treated as co-products, co-product total cash costs for the three months ended September 30, 2015 would be $8.56per silver ounce (2014 – $10.54) and $1.49per pound of copper (2014 -$1.83) and co-product all-in sustaining costs for the three months ended September 30, 2015 would be $11.25per silver ounce (2014 - $15.59) and $1.89per pound of copper (2014 - $2.63). For the nine months ended September 30, 2015 co-product total cash costs would be $9.11per silver ounce (2014 - $10.15) and $1.64per pound of copper (2014 - $1.73) and co-product all-in sustaining costs for the nine months ended September 30, 2015 would be $12.83per silver ounce (2014 -$14.53) and $2.24per pound of copper (2014 - $2.41). |

| 5 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Gold production for thethird quarter of 2015 increased by 31% compared to the prior-year period with 122,580 gold ounces produced compared to 93,367 ounces. The significant increase in quarterly gold production was a result of higher production at New Afton, Mesquite and Cerro San Pedro which more than offsetting a decrease in production at the Peak Mines. Production increases at Mesquite were driven by more than twice the number of ore tonnes being mined and placed on the leach pad and faster process recoveries resulting from the Company’s investment in the leach pad expansion. These factors combined to deliver Mesquite’s highest quarterly production since the first quarter of 2012. Production at Cerro San Pedro benefitted from a significant increase in ore tonnes mined and placed on the leach pad coupled with higher gold grade as Cerro San Pedro is fully mining the final phase of ore. Production at New Afton increased relative to the prior-year period due to a 5% increase in throughput with gold grade and recovery remaining consistent. Third quarter gold production at the Peak Mines increased relative to the second quarter as planned, however, was below that of the prior-year period. Lower production at Peak Mines compared to the prior-year period was due to the combined impact of lower tonnes processed as well as lower gold grade, arising from the previously disclosed geotechnical challenges in the main stoping area of the Perseverance ore body. Since that time, there has been reduced accessibility to the Perseverence ore body and a decrease in tonnes mined and processed from this area as there was an increased focus on rehabilitation and remediation.

Despite the challenges at Peak, production for the nine months ended September 30, 2015 increased with 303,999 gold ounces produced compared to production of 274,144 gold ounces in the prior-year period. Production during the first nine months ended September 30, 2015 was positively impacted by the increase in ore tonnes mined at Mesquite and Cerro San Pedro. New Afton had a moderate decrease in production for the first nine months of 2015 compared to the prior-year period due lower gold grade and recovery, which was partially offset by higher throughput. As the mill expansion was completed on schedule in mid-2015, gold recovery in the early part of 2015 was lower than the prior year as throughput was increased. Since the completion of the mill expansion, gold recovery has increased by 3% relative to the first quarter of 2015. The decrease in gold production at the Peak Mines was attributable to a 12% decrease in throughput and lower gold grade, with both primarily related to the geotechnical challenges at Perseverance.

Gold sales for the third quarter of 2015 were 115,695 ounces, compared to 88,168 ounces in the prior-year period.In the nine months ended September 30, 2015, 295,847 ounces of gold were sold compared to 266,956 ounces in the prior-year period. Timing of sales at the end of the quarter resulted in a difference between ounces sold and ounces produced.

Copper production for the third quarter of 2015 was 24.6 million pounds compared to 25.6 million pounds in the prior-year period.New Afton’s quarterly copper production was in line with the third quarter of 2014. The combination of the 5% increase in throughput and a 1% increase in copper recovery, resulting from the successful mill expansion project, offset a decrease in copper grade. Copper production for thenine months ended September 30, 2015 was 71.1 million pounds compared to 77.0 million pounds produced in the prior-yearperiod. Copper production decreased at New Afton where the combination of lower gold grade and recovery was only partially offset by higher throughput and at Peak Mines due to lower throughput and copper recovery.

Copper sales were 21.6 million pounds for the third quarter of 2015 compared to 22.7 million pounds in the prior-year period. Copper sales volumes were lower than the prior-year period primarily due to lower production. Copper sales were 67.4 million pounds for the nine months ended September 30, 2015 compared to 72.2 million pounds in the prior-year period. Timing of sales at the end of the quarter resulted in a difference between ounces sold and ounces produced.

Silver production in the third quarter of 2015 increased to 0.6 million ounces from the prior-year period production of 0.2 million ounces.Silver production at Cerro San Pedro benefitted from the additional ore tonnes placed on the leach pad in third quarter as well as prior quarters as the leach recovery cycle for silver is longer than for gold. Silver production for the nine months ended September 30, 2015 was 1.4 million ounces consistent with prior year production of 1.1 million ounces. This increase was primarily attributed to the third quarter of 2015.

| 6 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Total cash costs per gold ounce sold for the third quarter of 2015, net of by-product sales, were $495 per ounce compared to $311 per ounce in the prior-year period.The increase in cash costs was primarily driven by lower copper by-product revenue from lower average realized copper prices. This was partially offset by weakening foreign currency exchange rates in certain jurisdictions where the Company operates, relative to the U.S. dollar. Total cash costs per gold ounce sold, net of by-product sales, were $464 per ounce for the nine months ended September 30, 2015, compared to $272 per ounce in the prior-year period.

All-in sustaining costs per gold ounce sold for the third quarter of 2015 were $788 per ounce compared to $848 per ounce in the prior-year period.Despite the increase in total cash costs, all-in sustaining costs decreased driven by reduced sustaining capital expenditures compared to the prior-year period. In the prior-year period Mesquite purchased four new haul trucks. In addition, a decrease in corporate administration and exploration expenses futher reduced all-in sustaining costs. All-in sustaining costs per gold ounce sold were $895 per ounce for the nine months ended September 30, 2015, compared to $754 per ounce in the prior-year period.

FINANCIAL HIGHLIGHTS

Three months ended September 30 | Nine months ended September 30 | |||

| (in millions of U.S. dollars, except where noted) | 2015 | 2014 | 2015 | 2014 |

| FINANCIAL INFORMATION | ||||

| Revenues | 177.3 | 169.3 | 513.9 | 537.9 |

| Operating margin(1) | 71.9 | 75.1 | 210.7 | 249.9 |

| Earnings from mine operations | 11.1 | 21.4 | 44.1 | 91.9 |

| Net earnings (loss) | (157.8) | (59.6) | (191.9) | (45.2) |

| Adjusted net (loss) earnings(1) | (8.5) | 5.4 | (13.9) | 31.8 |

| Net cash generated from operations | 51.0 | 58.2 | 177.7 | 198.9 |

| Net cash generated from operations before changes in non-cash operating working capital(1) | 58.4 | 78.6 | 188.5 | 240.6 |

| Capital expenditures (sustaining capital) (1) | 24.5 | 36.5 | 97.9 | 90.6 |

| Capital expenditures (growth capital) (1) | 52.2 | 37.2 | 121.9 | 100.1 |

| Total assets | 3,919.8 | 4,250.7 | 3,919.8 | 4,250.7 |

| Cash and cash equivalents | 384.6 | 416.1 | 384.6 | 416.1 |

| Long-term debt | 787.1 | 871.9 | 787.1 | 871.9 |

| Share Data | ||||

| Earnings (loss) per share: | ||||

| Basic ($) | (0.31) | (0.12) | (0.38) | (0.09) |

| Diluted ($) | (0.31) | (0.12) | (0.38) | (0.09) |

| Adjusted net (loss) earnings per basic share ($)(1) | (0.02) | 0.01 | (0.03) | 0.06 |

| Share price as at September 30 (TSX – Canadian dollars) | 3.01 | 5.67 | 3.01 | 5.67 |

| Weighted average outstanding shares (basic) (millions) | 509.1 | 503.9 | 508.9 | 503.7 |

| 1. | The Company uses certain non-GAAP financial performance measures throughout this MD&A. Operating margin, adjusted net (loss) earnings, adjusted net (loss) earnings per basic share and net cash generated from operations before changes in non-cash operating working capital are non-GAAP financial performance measures with no standard meaning under IFRS. For further information and a detailed reconciliation, please refer to the “Non-GAAP Financial Performance Measures” section of this MD&A. |

| 7 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

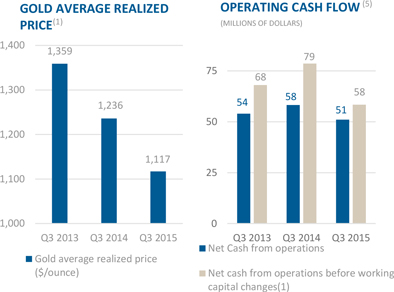

Revenue was $177.3 million for the third quarter of 2015, compared to $169.3 million in the prior-year period. The benefit from increased gold sales was partially offset by lower average realized commodity prices compared to the prior-year period for all metals. The average realized prices for the third quarter of 2015 were $1,117 per gold ounce, $2.23 per pound of copper and $14.72 per silver ounce, compared to $1,236 per gold ounce, $3.11 per pound of copper and $19.66 per silver ounce in the prior-year period.

Revenue was $513.9 million for the nine months ended September 30, 2015, compared to $537.9 million in the prior-year period.Revenues were impacted by the combination of lower realized metal prices and copper sales volumes which was only partially offset by higher gold sales volumes relative to the prior-year period.The average realized prices for the nine months ended September 30, 2015 were $1,174 per gold ounce, $2.52 per pound of copper and $15.72 per silver ounce, compared to $1,283 per gold ounce, $3.06 per pound of copper and $19.90 per silver ounce in the prior-year period.

Earnings from mine operations were $11.1 million for the third quarter of 2015, compared to $21.4 million in the prior-year period.The decrease in earnings from mine operations was attributed primarily to lower average realized prices which was only partially offset by increased gold sales. The Company’s total production expenses (operating expenses before production expenses capitalized and change in inventory and work-in-progress as per note 3 of the Company’s unaudited condensed consolidated financial statements for the three and nine months ended September 30, 2015 and 2014) have decreased to $118.7 million from $130.4 million in the prior-year period. The increased mining activity at each of New Afton, Mesquite and Peak Mines was offset by the combined benefit of the depreciation of the Canadian and Australian dollars relative to the U.S. dollar. Depreciation and depletion was in line with the prior-year period.

Earnings from mine operations were $44.1 million for the nine months ended September 30, 2015, compared to $91.9 million in the prior-year period. Consistent with the third quarter of 2015, the decrease in earnings from mine operations was attributed primarily to loweraverage realized metal prices, which was only partially offset by increased gold and silver sales. The Company’s total production expenses (operating expenses before production expenses capitalized and change in inventory and work-in-progress as per note 3 of the Company’s unaudited condensed consolidated financial statements for the three and nine months ended September 30, 2015 and 2014) have decreased to $359.2 million from $380.7 million in the prior-year period. The increased mining activity at each of New Afton, Mesquite and Peak Mines, were offset by the combined benefit of the depreciation of the Canadian and Australian dollars relative to the U.S. dollar.

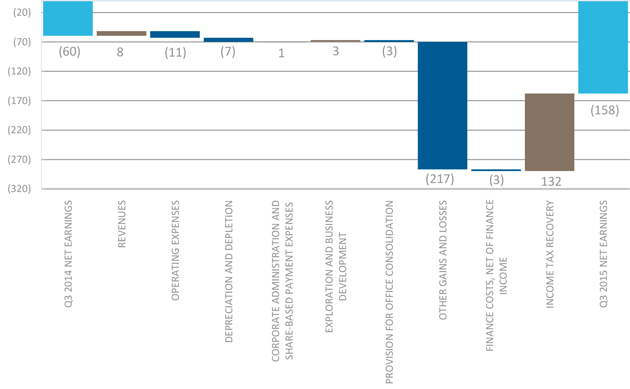

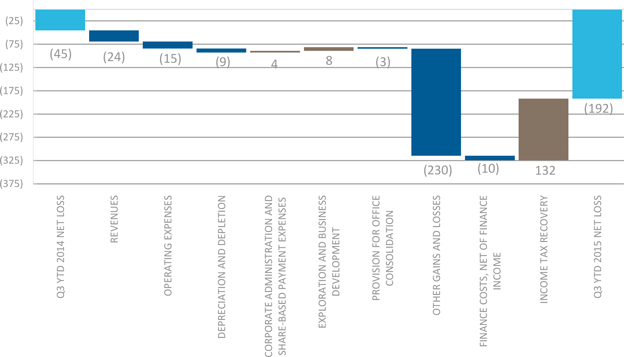

Net loss was $157.8 million or $0.31 per basic share for the third quarter of 2015, compared to $59.6 million or $0.12 per basic share in the prior-year period. The net loss was impacted by the change in earnings from mine operations as noted above and the impact of items included in non-operating “Other gains and losses”, where a loss of $230.7 million was recorded for the third quarter of 2015, compared to a loss of $13.8 million in the prior-year period.

During the three months ended September 30, 2015 an impairment loss on reclassification of the El Morro project as held for sale of $100.5 million ($182.0 million included in other gains and losses less associated tax recovery of $81.5 million) was included in net loss. On August 27, 2015 the Company announced the sale of the El Morro project. The El Morro project met the criteria for classification as held for sale and was revalued at its fair value less costs to sell. Additionally, during the three months ended September 30, 2015 the Company entered into a $175 million streaming agreement which was classified as a derivative liability. The Company had an unrealized loss on the revaluation of the derivative instrument at September 30, 2015 of $3.2 million and incurred transaction costs of $2.6 million related to the streaming agreement, both of which are included in other gains and losses. Please refer to the “Corporate Developments” section of this MD&A for further details on these transactions.

| 8 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Other gains and losses also included a foreign exchange loss of $40.8 million and $72.6 million for the three and nine months ended September 30, 2015. The foreign exchange loss is primarily due to the foreign exchange loss in relation to the tax basis of the non-monetary assets and liabilities denominated in currencies other than the U.S. dollar. Additionally, the Company had an unrealized loss of $1.7 million and a gain of $9.8 million for the three and nine months ended September 30, 2015 on the mark-to-market of share purchase warrants.

The increase in finance costs in the period was attributable to the reduction in capitalized interest allocated to development projects. The Company also recognized a provision for the relocation, severance and career transition costs, related to the Company’s plans to consolidate its head office in the three months ended September 30, 2015 of $3.0 million. These costs were offset by lower exploration and corporate administrative costs.

The Company’s net loss for the nine months ended September 30, 2015 was $191.9 million or $0.38 per basic share, compared to net loss of $45.2 million or $0.09 per basic share in the prior-year period.

The adjusted net loss for the third quarter of 2015 was $8.5 million or $0.02 per basic share, compared to adjusted net earnings of $5.4 million or $0.01 per basic share in the prior-year period. Adjusted net loss was impacted by the change in earnings from mine operations, as noted above, and increased finance costs as capitalized interest is no longer applied to the Blackwater project. These changes were partially offset by decreased corporate administration and exploration costs. Adjusted net loss for the nine months ended September 30, 2015 was $13.9 million or $0.03 per basic share, compared to adjusted net earnings of $31.8 million or $0.06 per basic share in the prior-year period.

Net cash generated from operations for the third quarter of 2015 was $51.0 million, decreasing from the prior-year period of $58.2 million. The negative impact to cash flow due to lower metal prices and decrease in income tax refund was partially offset by a decrease in corporate administration and exploration and business development expenses. Net cash generated from operations for the nine months ended September 30, 2015 was $177.7 million compared to $198.9 million in the prior-year period.

Cash and cash equivalents were $384.6 million as at September 30, 2015 compared to $370.5 million as at December 31, 2014.Net cash generated from operations in the period of $177.7 million was offset by cash used in investing activities of $217.9 million (which includes $97.9 million of sustaining capital expenditures and $121.9 million of growth capital expenditure), cash generated by financing activities of $71.5 million and $17.2 million used by the impact of foreign exchange on cash and cash equivalents.

On July 20, 2015 the Company announced that it entered into a $175 million streaming transaction with RGLD Gold AG, a wholly-owned subsidiary of Royal Gold Inc. (“Royal Gold”), which provides New Gold with further financial flexibility. Under the terms of the agreement, Royal Gold will provide New Gold with a deposit of $175 million, to be used for the ongoing development of the Company’s Rainy River project, in exchange for a percentage of the annual gold and silver production from the project. Royal Gold paid the first $100 million of the deposit concurrent with the entering into the transaction. The remaining $75 million will be paid when 60% of the estimated Rainy River project development capital has been spent (subject to customary conditions precedent), which is expected to be in mid-2016.

CORPORATE DEVELOPMENTS

New Gold’s strategy is to continue strong operational execution at its current assets while pursuing disciplined growth both through organic initiatives and value-enhancing mergers and acquisitions. Since the middle of 2009, New Gold has successfully enhanced the value of its portfolio of assets, while also continually looking for compelling external growth opportunities. The Company continues to evaluate assets in favourable jurisdictions where the asset has the potential to provide New Gold shareholders with meaningful gold production, cash flow and exploration potential, while ensuring that any potential acquisition is accretive on key per share metrics. The Company strives to maintain a strong financial position while continually reviewing strategic alternatives with the view of maximizing shareholder value. New Gold’s objective is to pursue corporate development initiatives that will leave the Company and its shareholders in a fundamentally stronger position.

| 9 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

On July 20, 2015 New Gold announced that the Company had entered into a $175 million streaming agreement with Royal Gold. Under the terms of the agreement, Royal Gold will provide New Gold with a deposit of $175 million, to be used for the ongoing development of the Company’s Rainy River project, in exchange for a percentage of the annual gold and silver production from the project.

Streaming agreement Highlights Include: Upfront Deposit · Royal Gold to provide New Gold with a $175 million deposit for the development of the Company’s o $100 million paid at signing with the remaining $75 million to be paid when 60% of the Project development capital has been spent (subject to customary conditions precedent); expected to be in mid-2016 Gold and Silver Stream Percentage · New Gold to deliver 6.50% of the Project’s gold production up to a total of 230,000 ounces of gold, and 3.25% of the Project’s gold production thereafter · New Gold to deliver 60% of the Project’s silver production up to a total of 3.1 million ounces of silver, and 30% of the Project’s silver production thereafter Ongoing Cash Purchase Price · In addition to the upfront deposit, Royal Gold to pay 25% of the spot gold or silver price at the time each ounce of gold or silver is delivered under the stream |

The gold and silver stream will cover future production from New Gold’s current Rainy River land package, plus an additional two-kilometre area of interest, but excluding any potential future mineralization discovered on New Gold’s Offlake exploration claims located to the northeast of the Rainy River deposit.

| 10 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

On August 27, 2015 New Gold announced the sale of its interest in El Morro to a subsidiary of Goldcorp Inc. (“Goldcorp”) for $90 million cash (pre-tax), a 4% gold stream from the El Morro property and the cancellation of New Gold’s $94 million carried funding loan. The transaction provides New Gold with increased financial flexibility, strengthens the balance sheet and enables the company to maintain exposure to El Morro’s current gold reserves and ongoing exploration potential.

KEY TRANSACTION HIGHLIGHTS

$90 million cash consideration · $90 million, less applicable withholding taxes, to be paid at closing of the Transaction, expected to be in the fourth quarter of 2015 4% stream on gold production from the El Morro property · 4% stream on life-of-project gold production from the 417 square kilometre El Morro property · El Morro’s currently estimated gold mineral reserves – 599 million tonnes at an average gold grade of 0.46 grams per tonne, totalling 8.9 million ounces · New Gold to pay fixed $400 per ounce on the first 217,000 ounces of gold delivered as part of the stream $94 million carried funding loan cancelled · New Gold will no longer be obligated to repay the $94 million in debt that Goldcorp (and previous joint venture partners) funded on the Company’s behalf |

In conjunction with the transaction, Goldcorp and Teck Resources Limited (“Teck”) also announced that they plan to combine their respective El Morro and Relincho projects into a 50/50 joint venture with the interim name of Project Corridor.

Based on the results of the Project Corridor Preliminary Economic Assessment, when ore is sourced from El Morro, gold production is expected to average over 400,000 ounces per year which would enable New Gold to purchase over 16,000 ounces of gold per year at $400 per ounce.

The cash purchase price for gold delivered under the stream is fixed at $400 per ounce for the first 217,000 ounces of gold, where 217,000 ounces reflects 4% of El Morro’s currently estimated recoverable gold production. Thereafter, the cash purchase price will be $400 per ounce plus an annual 1% inflation adjustment.

Goldcorp and Teck are expecting to commence a Pre-Feasibility Study in early 2016 which should be completed 12 to 18 months thereafter. Closing of the Transaction is conditional upon the closing of the El Morro-Relincho joint venture between Goldcorp and Teck as well as other customary conditions. The Transaction is expected to close in the fourth quarter of 2015.

CORPORATE SOCIAL RESPONSIBILITY

New Gold is committed to excellence in corporate social responsibility. The Company considers its ability to make a lasting and positive contribution toward sustainable development a key driver to achieving a productive and profitable business. New Gold aims to achieve these objectives through the protection of the health and well-being of its people and host communities as well as industry leading practices in the areas of environmental stewardship and community engagement and development. The Company is proud to have been listed in the Maclean’s/Sustainalytics – Top 50 Socially Responsible Corporations in Canada and in the “Future 40 Most Responsible Corporate Leaders in Canada” by Corporate Knights for the second consecutive year.

| 11 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Environmental and community Highlights for Q3 2015 · A review of “Top Five” environmental and social risks and associated controls for the New Afton Mine and Peak Mines was carried out · Cerro San Pedro completed the 2015 reforestation campaign in the community of Monte Caldera, which involved environmental education activities and the work of 500 volunteers including community members and mineworkers, who planted 5,000 trees · An Independent Tailings Review Board has been established and is set to review the technical aspects of Tailings Storage Facility at New Afton in the fourth quarter of 2015 · Peak held the Annual Community Engagement meeting with the presentations of key mine personnel · Rainy River continues to inform and work with local communities and First Nations partners during the construction period of the mine |

As a participant and supporter of the United Nations Global Compact, New Gold’s policies and practices are guided by its principles with reference to human rights, labour, environmental stewardship and anti-corruption. As a member of the Mining Association of Canada (“MAC”), New Gold’s operations adopt the MAC’s Towards Sustainable Mining protocols.

New Gold’s corporate social responsibility objectives include promoting and protecting the welfare of its employees through safety-first work practices, upholding fair employment practices and encouraging a diverse workforce, where people are treated with respect and are supported to realize their full potential. New Gold believes that its people are its most valued assets. The Company strives to create a culture of inclusiveness that begins at the top and is reflected in its hiring, promotion and overall human resources practices. New Gold encourages tolerance and acceptance in worker-to-worker relationships. In each of its host communities, the Company strives to be an employer of choice through the provision of competitive wages and benefits, and through the implementation of policies of recognizing and rewarding employee performance and promoting from within wherever possible.

The Company is committed to preserving the long-term health and viability of the natural environments that host its operations. Wherever New Gold operates – in all stages of mining activity, from early exploration and planning, to commercial mining operations through to eventual closure – the Company is committed to excellence in environmental management. From the earliest site investigations, New Gold carries out comprehensive environmental studies to establish baseline measurements for flora, fauna, earth, air and water. During operations the Company promotes the efficient use of raw materials and resources, work to minimize environmental impacts and maintain robust monitoring programs. After mining activities are complete, New Gold’s objective is to restore the land to a level of productivity equivalent to its pre-mining capacity or to an alternative land use determined through consultation with local stakeholders.

New Gold is committed to establishing relationships based on mutual benefit and active participation with its host communities to contribute to healthy and sustainable communities. Wherever the Company’s operations interact with Indigenous peoples, New Gold promotes understanding of, and respect for traditional values, customs and culture and takes meaningful action to consider their interests through collaborative agreements aimed at creating jobs, training and lasting socio-economic benefits. New Gold aims to foster open communication with local residents and community leaders and strive to partner in the long-term sustainability of those communities. The Company believes that by thoroughly understanding the people, their histories, and their needs and aspirations, we can engage in a meaningful and sustainable development process.

| 12 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

OUTLOOK FOR 2015

Consistent with the Company’s February 2015 guidance for the year, production was planned to be weighted to the second half of 2015 and New Gold’s four operations began to deliver this higher production in the third quarter. As the Company has produced over 300,000 ounces of gold through the first nine months of the year and expects a strong fourth quarter, full-year gold production continues to have the potential to be toward the high end of the original guidance range of 390,000 to 430,000 ounces. Consolidated copper production is expected to be at the low end of the guidance range of 100 to 112 million pounds and consolidated silver production is expected to be in line with guidance at 1.75 to 1.95 million ounces.

New Gold’s 2015 all-in sustaining costs guidance of $745 to $785 per ounce, including total cash costs of $340 to $380 per ounce was set in February of 2015. The company’s cost guidance was based on assumptions of $2.75 per pound of copper and $16.00 per ounce of silver and foreign exchange rates for the Canadian dollar, Australian dollar and Mexican peso of $1.25, $1.25 and $15.00 to the U.S. dollar, respectively.

For the nine months ended September 30, 2015, New Gold’s all-in sustaining costs were $895 per ounce, including total cash costs of $464 per ounce. All-in sustaining costs and total cash costs per ounce are tracking above guidance due to the combined impact of by-product commodity prices being lower than those assumed at the beginning of 2015, copper production being at the low end of guidance and a higher percentage of the company’s gold production coming from Mesquite, which is scheduled to have an above average cost year in 2015.

The Company’s fourth quarter all-in sustaining costs are expected to be lower than the year-to-date costs driven by the combined benefit of higher gold and copper sales volumes. As a result, the 2015 full-year all-in sustaining costs and total cash costs per ounce are expected to decrease relative to those achieved through the first nine months of the year.

At the end of the second quarter, the Company indicated that based on spot commodity prices and foreign exchange rates at that time, full-year costs were expected to be higher than the guidance provided at the beginning of 2015. Since that time, copper prices have decreased further, while foreign exchange rates have remained in line. As a result, New Gold expects full-year all-in sustaining costs of $840 to $860 per ounce, including total cash costs of $430 to $450 per ounce.

KEY PERFORMANCE DRIVERS

There is a range of key performance drivers that are critical to the successful implementation of New Gold’s strategy and the achievement of its goals. The key internal drivers are production volumes and costs. The key external drivers are spot prices of gold, copper and silver, as well as foreign exchange rates.

Production Volumes and Costs

New Gold’s portfolio of operating mines produced 122,580 gold ounces during the third quarter of 2015 and 303,999 gold ounces for the nine months ended September 30, 2015.

Total cash costs and all-in sustaining costs for the third quarter, net of by-product sales, were $495 and $788 per gold ounce sold, respectively. For the nine months ended September 30, 2015 total cash costs and all-in sustaining costs, net of by-product sales, were $464 and $895 per gold ounce sold, respectively.

New Gold continues to deliver against guidance with respect to the key internal drivers.

| 13 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Commodity Prices

Gold Prices

The price of gold is the largest single factor affecting New Gold’s profitability and operating cash flows. As such, the current and future financial performance of the Company is expected to be closely related to the prevailing price of gold.

For the third quarter of 2015, New Gold achieved an average realized gold price of $1,117 per ounce compared to the London PM fix average gold price of $1,124 per ounce. For the nine months ended September 30, 2015, New Gold achieved an average realized gold price of $1,174 per ounce compared to the London PM fix average gold price of $1,179 per ounce.

The gold price has widened its recent trading range as the US Federal Reserve debates the likely timing for tightening monetary policy, but as interest rates remain low and the global economy continues to experience challenges, the fundamentals that support the gold price remain in place. As a lower cost producer, we believe New Gold is in a strong position to operate both in a low gold price environment and to take advantage of higher gold prices through our existing operations and growth projects.

Copper Prices

For the third quarter of 2015, New Gold’s average realized copper price was $2.23 per pound compared to the average London Metals Exchange copper price of $2.38 per pound. For the nine months ended September 30, 2015, New Gold achieved an average realized copper price of $2.52 per pound compared to the average London Metals Exchange copper price of $2.59 per pound. The realized copper price was further than usual from the market price during the third quarter due to an increasingly volatile copper market, and to variations in quotational period prices paid to customers.

Silver Prices

For the third quarter of 2015, New Gold had an average realized silver price of $14.72 per ounce compared to an average London PM fix price of $14.91 per ounce. For the nine months ended September 30, 2015, New Gold had an average realized silver price of $15.72 per ounce compared to an average London PM fix price of $16.01 per ounce.

Foreign Exchange Rates

The Company operates in Canada, the United States, Australia, Mexico and Chile, while revenues are predominantly generated in U.S. dollars. As a result, the Company has foreign currency exposure with respect to costs not denominated in U.S. dollars. New Gold’s operating results and cash flows are influenced by changes in various exchange rates against the U.S. dollar. The Company has exposure to the Canadian dollar through New Afton, Rainy River and Blackwater, as well as through corporate administration costs. The Company also has exposure to the Australian dollar through Peak Mines, and to the Mexican peso through Cerro San Pedro.

| 14 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

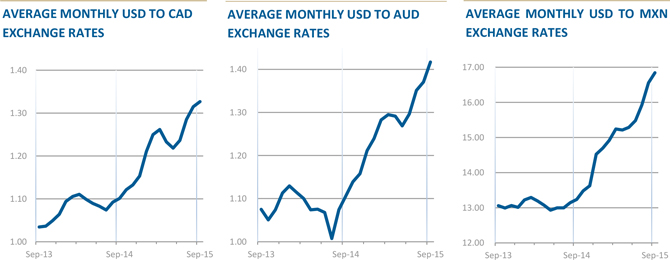

The Canadian dollar weakened against the U.S. dollar by approximately 6% in the third quarter of 2015 and weakened by approximately 12% during the nine months ended September 30, 2015. A weaker Canadian dollar decreases costs in U.S. dollar terms at the Company’s Canadian operations, as well as capital costs at the Company’s Canadian development properties.

The Australian dollar weakened against the U.S. dollar by approximately 7% in the third quarter of 2015 and weakened by approximately 15% during the nine months ended September 30, 2015. A weaker Australian dollar decreases costs in U.S. dollar terms at the Company’s Australian operation, Peak Mines.

The Mexican peso weakened against the U.S. dollar by approximately 7% in the third quarter of 2015 and weakened by approximately 15% during the nine months ended September 30, 2015. A significant portion of costs at Cerro San Pedro are incurred in U.S. dollars and, as such, the movement in the Mexican peso exchange rate is not significant driver of U.S.dollar-denominated costs.

For an analysis of the impact of foreign exchange fluctuations on operating costs during third quarter of 2015 and the nine months ended September 30, 2015 relative to the prior-year periods, refer to the “Review of Operating Mines” sections for New Afton, Peak Mines and Cerro San Pedro for details.

Economic Outlook

The gold price declined by approximately5% during the quarter, although it has performed well since the end of the quarter amid significant volatility. As attention has finally shifted from the Greek crisis, the Federal Reserve has returned to its position as the main driver of gold price movements, with the market carefully watching the flow of Fed commentary and US economic data to try to determine if rates will rise in 2015 or defer until next year. Regardless of this timing, aggregate global inflation and interest rates are likely to remain low for the foreseeable future. As a low cost producer with a pipeline of development projects, New Gold believes it is particularly well positioned both to operate in a lower gold price environment and to take advantage of higher prices in the gold market.

| 15 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Economic events can have significant effects on the price of gold, through currency rate fluctuations, the relative strength of the U.S. dollar, supply of and demand for gold, and macroeconomic factors such as interest rates and inflation expectations. Management anticipates that the long-term economic environment should provide support for precious metals and for gold in particular, and believes the prospects for the business are favourable. New Gold’s growth plan is focused on organic and acquisition-led growth, and the Company plans to remain flexible in the current environment to be able to respond to opportunities as they arise.

FINANCIAL RESULTS

Summary of Quarterly Financial Results

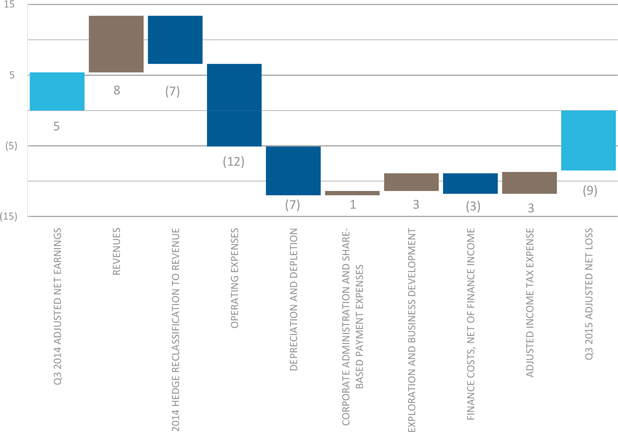

RECONCILIATON OF THIRD QUARTER NET EARNINGS – 2014 TO 2015

(in millions of U.S. dollars)

Revenue

Revenue was $177.3 million for the third quarter of 2015, compared to $169.3 million in the prior-year period. The benefit from increased gold sales was partially offset by lower copper sales as well as lower average realized commodity prices compared to the prior-year period. A detailed discussion of production is included in the “Operating Highlights” section of this MD&A. The average realized prices for the third quarter of 2015 were $1,117 per gold ounce, $2.23 per pound of copper and $14.72 per silver ounce, compared to $1,236 per gold ounce, $3.11 per pound of copper and $19.66 per silver ounce in the prior-year period. Additionally, revenue in the prior-year period was impacted by the reclassification of the loss on the monetization of the hedge of $6.8 million.

Operating expenses

Operating expenses for the third quarter of 2015 were higher than the prior-year period at $105.4 million compared to $94.2 million, primarily driven by increase in metal production and a reduction in capitalized production expenses. The Company’s total production costs (operating expenses before production expenses capitalized and change in inventory and work-in-progress as per note 3 of the Company’s unaudited condensed consolidated financial statements for the three and nine months ended September 30, 2015 and 2014) have decreased to $118.7 million from $130.4 million in the prior-year period. The increased mining activity at New Afton and Mesquite along with the rehabilitation work at Peak Mines, were offset by the combined benefit of the depreciation of the Canadian and Australian dollars relative to the U.S. dollar. Refer to the “Review of Operating Mines” section of this MD&A for more details.

| 16 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Depreciation and depletion

Depreciation and depletion for the third quarter of 2015 increased compared to the prior-year period at $60.8 million compared to $53.7 million, as a result of increase gold and silver production.

Earnings from mine operations

Earnings from mine operations for the third quarter of 2015 were $11.1 million compared with $21.4 million in the prior-year period. The decrease in earnings from mine operations was due to lower average realized priceswhich was partially offset by increased gold and silver sales and higher depreciation and depletion expense.

Corporate administration

Corporate administration costs were $5.2 million in the third quarter of 2015 compared to $6.0 million incurred in the prior-year period. These costs were positively impacted by the weaker Canadian dollar.

During the three months ended September 30, 2015 the Company recognized a provision for the relocation, severance and career transition costs related to the Company’s plans to consolidate its head office, in the three months ended September 30, 2015 of $3.0 million.

Share-based compensation

Share-based compensation costs were $1.7 million in the third quarter of 2015 consistent with $1.5 million in the prior-year period.

Exploration and business development

Exploration and business development expense was $2.5 million in the third quarter of 2015 compared to $5.0 million for the prior-year period. The decrease is due to the Company receiving a refundable tax credit of $0.6 million at Blackwater related to the British Columbia Mining Exploration Tax Credit, reduced exploration activity at Blackwater compared to the prior-year period and timing of the infill drilling program at Mesquite. Expensed exploration in the current period was primarily incurred at Peak Mines and the Blackwater project. The prior-year period included expensed exploration costs at Mesquite, Peak Mines and the Blackwater project.

Capitalized exploration costs were of $0.8 million in the third quarter of 2015 compared to $4.4 million in the prior-year period. Capitalized exploration was incurred at Rainy River and Peak Mines in the current period and Rainy River, Peak Mines and New Afton in the prior-year period.

Other gains and losses

The following other gains and losses are all added back for the purposes of adjusted net earnings:

Non-hedged derivatives

In the third quarter of 2015, the Company recorded a loss of $1.7 million related to the mark-to-market of the share purchase warrants. This compares to a gain of $9.2 million in the prior-year period. The Company’s functional currency is the U.S. dollar, however, the share purchase warrants are denominated in Canadian dollars and are therefore treated as a derivative liability under IFRS. As the traded value of the New Gold share purchase warrants increases or decreases, a related loss or gain on the mark-to-market of the liability is reflected in earnings.

| 17 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Impairment loss on reclassification of the El Morro project as held for sale

During the three months ended September 30, 2015 the Company announced the sale of the El Morro project. The El Morro project met the criteria for classification as held for sale was revalued at its fair value less costs to sell. Included in net loss is an impairment loss of $100.5 million ($182.0 million included in other gains and losses less associated tax recovery of $81.5 million) on the revaluation.

Gold stream obligation

During the three months ended September 30, 2015 the Company entered into a $175 million streaming agreement which was classified as a derivative liability. The derivative liability is revalued at each period end with adjustments as a result of changes in the Company’s own credit risk recorded in the statement of other comprehensive income. Gains and losses related to changes in the risk free interest rate, expected ounces to be delivered, future metal prices and accretion due to the passage of time are recorded in other gains and losses. The Company had an unrealized loss on the revaluation of the derivative instrument at September 30, 2015 of $3.2 million included within other gains and losses. An unrealized gain of $15.0 million has been included within other comprehensive income related to the change in the risk adjusted discount rate used to value this obligation. The Company also incurred transaction costs of $2.6 million related to the streaming agreement, which are included in other gains and losses. Please refer to the “Corporate Developments” section of this MD&A for further details on these transactions.

Foreign exchange

In the third quarter of 2015, the Company recognized a foreign exchange loss of $40.8 million compared to a loss of $23.1 million in the prior-year period. The foreign exchange loss is primarily due to the Company recognizing a foreign exchange gain in relation to the tax basis of the non-monetary assets and liabilities denominated in currencies other than the U.S. dollar.

Income tax

Income and mining tax recovery in the third quarter of 2015 was $83.8 million compared to an expense of $48.1 million in the prior-year period, reflecting an effective tax rate of 35% for the third quarter of 2015 compared to 418% in the prior-year period. The primary reason for a lower unadjusted effective tax rate is the impact of lower Chilean income tax rate of 22.5% applicable on asset held for sale as against 35% in the prior periods. In addition, the unadjusted effective tax rate was also lower due to impact of foreign exchange movements on the deferred tax related to non-monetary assets and liabilities that have no tax basis. In the third quarter of 2015 the Company recorded a foreign exchange expense of $40.0 million on the deferred tax related to foreign exchange on non-monetary assets and liabilities as compared to $23.0 million in the same prior-year period with no associated tax impact. In the prior-year period the Company recognized a $48.3 million tax expense related to the change in the tax rate used in Chile from 20% to 35% due to the enactment of new legislation on September 26, 2014.

On an adjusted net earnings basis, the effective tax rate for the third quarter of 2015 was 7% compared to 41% in the prior-year period. The adjusted effective tax rate excludes the impact of foreign exchange, the impairment loss on reclassification of the El Morro project as held for sale, the gold stream obligation transaction costs, the loss on revaluation of the gold stream obligation at the period end, the provision for office consolidation, the hedge settlement in the prior-year period, and any associated changes in the recognition of deferred tax assets. The lower adjusted effective tax rate reflects the greater impact of permanent differences over adjusted net loss compared net earnings in the prior period.

Net loss

For the third quarter of 2015, New Gold had a net loss of $157.8 million, or $0.31 per basic share compared with $59.6 million, or $0.12 per basic share in the prior-year period.

| 18 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Adjusted net loss

For the third quarter of 2015, the adjusted net loss was $8.5 million or $0.02 per basic share, compared to adjusted net earnings of $5.4 million or $0.01 per basic share in the prior-year period.

RECONCILIATON OF THIRD QUARTER ADJUSTED NET LOSS – 2014 TO 2015

(in millions of U.S. dollars)

Net loss has been adjusted, including the associated tax impact, for costs in “Other gains and losses” on the condensed consolidated income statement. Key entries in this grouping are: impairment loss on reclassification of the El Morro project as held for sale; the fair value changes for the gold stream obligation and share purchase warrants; gold stream obligation transaction costs; foreign exchange gain or loss; and other non-recurring items. Net loss is also adjusted for inventory net realizable value provisions. Other adjustments to net loss in the prior-year period include the non-cash loss incurred on the monetization of the Company’s legacy hedge position as it is realized into income over the original term of the hedge contract, which is included in revenue.

See “Non-GAAP Financial Performance Measures” for reconciliation of the net loss to adjusted net earnings.

| 19 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Key Quarterly Operating and Financial Information

Selected financial and operating information for the current and previous quarters is as follows:

| |||||||||||||

(in millions of U.S. dollars, except where noted) | Q3 2015 | Q2 2015 | Q1 2015 | Q4 2014 | Q3 2014 | Q2 2014 | Q1 2014 | Q4 2013 | Q3 2013 | ||||

| Operating information | |||||||||||||

| Gold production (ounces) | 122,580 | 86,442 | 94,977 | 105,992 | 93,367 | 89,460 | 91,317 | 106,520 | 94,038 | ||||

| Gold sales (ounces) | 115,695 | 87,754 | 92,398 | 104,224 | 88,168 | 84,736 | 94,052 | 104,523 | 94,082 | ||||

| Revenues | 177.3 | 167.7 | 168.9 | 188.1 | 169.3 | 178.1 | 190.5 | 198.4 | 196.0 | ||||

| Net earnings (loss) | (157.8) | 9.4 | (43.8) | (431.9) | (59.6) | 16.2 | (1.8) | (254.7) | 12.2 | ||||

| Per share: | |||||||||||||

| Basic | (0.31) | 0.02 | (0.09) | (0.86) | (0.12) | 0.03 | 0.00 | (0.51) | 0.02 | ||||

| Diluted | (0.31) | 0.02 | (0.09) | (0.86) | (0.12) | 0.03 | 0.00 | (0.51) | 0.02 | ||||

| Adjusted net (loss) earnings | (8.5) | (1.3) | (4.9) | 13.4 | 5.4 | 8.2 | 18.2 | 16.7 | 20.0 | ||||

| Per share: | |||||||||||||

| Basic | (0.02) | (0.00) | (0.01) | 0.03 | 0.01 | 0.02 | 0.04 | 0.04 | 0.04 | ||||

| Diluted | (0.02) | (0.00) | (0.01) | 0.03 | 0.01 | 0.02 | 0.04 | 0.03 | 0.04 | ||||

A detailed discussion of production is included in the “Operating Highlights” section of this MD&A.

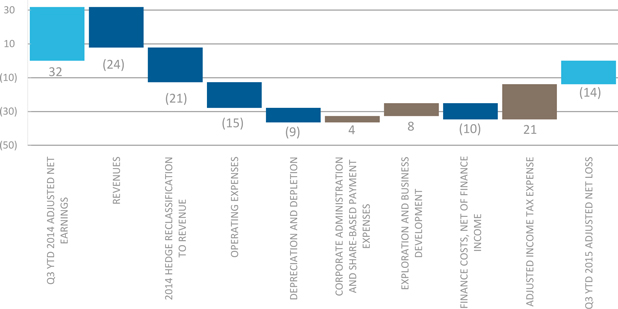

Summary of Year to Date Financial Results

RECONCILIATON OF YEAR TO DATE NET LOSS – 2014 TO 2015

(in millions of U.S. dollars)

| 20 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Revenue

Revenue for the nine months ended September 30, 2015 was $513.9 million compared to $537.9 million in the prior-year period. The decrease in revenue was primarily impacted by the decrease in commodity prices of all metals and lower copper sales volume, partially offset by an increase in gold sales volume. A detailed discussion of production is included in the “Operating Highlights” section of this MD&A. The average realized prices for the nine months ended September 30, 2015 were $1,174 per gold ounce, $2.52 per pound of copper and $15.72 per silver ounce, compared to $1,283 per gold ounce, $3.06 per pound of copper and $19.90 per silver ounce in the prior-year period. Additionally, revenue in the prior-year period was impacted by the reclassification of the loss on the monetization of the hedge of $20.5 million.

Operating expenses

Operating expenses were $303.2 million in the nine months ended September 30, 2015 compared to $288.0 million in the prior-year period, primarily driven by increase in metal production and a reduction in capitalized production expenses. The Company’s total production costs (operating expenses before production expenses capitalized and change in inventory and work-in-progress as per note 3 of the Company’s unaudited condensed consolidated financial statements for the three and nine months ended September 30, 2015 and 2014) have decreased to $359.2 million from $380.7 million in the prior-year period. The increased mining activity at New Afton and Mesquite along with the rehabilitation work at Peak Mines, were offset by the combined benefit of the depreciation of the Canadian and Australian dollars relative to the U.S. dollar. Refer to the “Review of Operating Mines” section of this MD&A for more details.

Depreciation and depletion

Depreciation and depletion increased in the nine months ended September 30, 2015 compared to the prior-year period to $166.6 million compared to $158.0 million, due to increased gold and silver production.

Earnings from mine operations

Earnings from mine operations were $44.1 million in the nine months ended September 30, 2015, compared to $91.9 million in the prior-year period. Earnings from mine operations were impacted by lower average realized priceswhich were only partially offset by the increased earnings associated with increased gold and silver sales.

Corporate administration

Corporate administration costs were $16.7 million in the nine months ended September 30, 2015, compared to $20.2 million in the prior-year period. These costs were positively impacted by the weaker Canadian dollar.

During the three months ended September 30, 2015 the Company recognized a provision of $3.0 million for the relocation, severance and career transition costs related to the Company’s plans to consolidate its head office.

Share-based compensation

Share-based compensation costs were $5.7 million in the nine months ended September 30, 2015, compared to $6.0 million in the prior-year period with the decrease representing a lower fair value for options granted.

Exploration and business development

Exploration and business development expense was $4.8 million in the nine months ended September 30, 2015, compared to $12.4 million in the prior-year period. The current period included a refundable tax credit of $1.5 million at Blackwater related to the British Columbia Mining Exploration Tax Credit and was also impacted by reduced exploration activity at Blackwater compared to the prior-year period and timing of the infill drilling program at Mesquite. Exploration expensed in the current period was primarily incurred at Peak Mines and the Blackwater project. The prior-year period included exploration expensed at Mesquite, Peak Mines and the Blackwater project. Exploration costs at Rainy River were capitalized to mineral interest in the current and prior-year periods.

| 21 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Capitalized exploration costs were of $3.9 million for the nine months ended September 30, 2015 compared to $16.3 million in the prior-year period. Capitalized exploration was incurred at Rainy River and Peak Mines in the current period and Rainy River, Peak Mines and New Afton in the prior-year period.

Other gains and losses

The following other gains and losses are all added back for the purposes of adjusted net earnings:

Non-hedged derivatives

For the nine months ended September 30, 2015, the Company recorded a gain of $9.8 million compared to a gain of $4.4 million in the prior-year period relating to share purchase warrants. The Company’s functional currency is the U.S. dollar, however, the share purchase warrants are denominated in Canadian dollars and are therefore treated as a derivative liability. As the traded value of the New Gold share purchase warrants increases or decreases, a related loss or gain on the mark-to-market of the liability is reflected in earnings.

Impairment loss on reclassification of the El Morro project as held for sale

During the three months ended September 30, 2015 the Company announced the sale of the El Morro project. The El Morro project met the criteria for classification as held for sale was revalued at its fair value less costs to sell. Included in net loss is an impairment loss of $100.5 million ($182.0 million included in other gains and losses less associated tax recovery of $81.5 million) on the revaluation.

Gold stream obligation

During the three months ended September 30, 2015 the Company entered into a $175 million streaming agreement which was classified as a derivative liability. The derivative liability is revalued at each period end with adjustments as a result of changes in the Company’s own credit risk recorded in the statement of other comprehensive income. Gains and losses related to changes in the risk free interest rate, expected ounces to be delivered, future metal prices and accretion due to the passage of time are recorded in other gains and losses. The Company had an unrealized loss on the revaluation of the derivative instrument at September 30, 2015 of $3.2 million included within other gains and losses. An unrealized gain of $15.0 million has been included within other comprehensive income related to the change in the risk adjusted discount rate used to value this obligation. The Company also incurred transaction costs of $2.6 million related to the streaming agreement, which are included in other gains and losses. Please refer to the “Corporate Developments” section of this MD&A for further details on these transactions.

Foreign exchange

For the nine months ended September 30, 2015, the Company recognized a foreign exchange loss of $72.6 million compared to a loss of $26.1 million in the prior-year period. Movements in foreign exchange are due to the revaluation of the monetary assets and liabilities at the balance sheet date and the depreciation of both the Canadian and Australian dollars compared to the U.S. dollar in the period.

Income tax

Income and mining tax recovery in the nine months ended September 30, 2015 was $76.1 million compared to $56.2 million in the prior-year period, reflecting an effective tax rate of 28% for the third quarter of 2015 compared to 511% in the prior-year period. The primary reason for a lower unadjusted effective tax rate is the impact of lower Chilean income tax rate of 22.5% applicable on the El Morro asset held for sale as against 35% in the prior periods. In addition, the unadjusted effective tax rate was also lower due to the impact of foreign exchange movements on the deferred tax related to non-monetary assets and liabilities. In the nine months ended September 30, 2015 the Company recorded a foreign exchange expense of $71.0 million on the deferred tax related to foreign exchange on non-monetary assets and liabilities as compared to $22.3 million in the same prior-year period with no associated tax impact. The effect on the tax rate is higher in the nine months ended September 30, 2015, primarily as a result of the stronger U.S. dollar. In the prior-year period the Company recognized a $48.3 million tax expense related to the change in the tax rate used in Chile from 20% to 35% due to the enactment of new legislation on September 26, 2014.

| 22 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

On an adjusted net (loss) earnings basis, the effective tax rate for the nine months ended September 30, 2015 was 3% compared to 40% in the prior-year period. The adjusted effective tax rate excludes the impact of foreign exchange, the impairment loss on the reclassification of the El Morro project as held for sale, the gold stream obligation transaction costs, the loss on revaluation of the gold stream obligation at the period end, the provision for office consolidation, the hedge settlement in the prior-year period, and any associated changes in the recognition of deferred tax assets. The lower adjusted effective tax rate reflects the greater impact of permanent differences over adjusted net loss compared net earnings in the prior period.

Net loss

For the nine months ended September 30, 2015, New Gold had a net loss of $191.9 million, or $0.38 per basic share. This compares with net loss of $45.2 million, or $0.09 per basic share in the prior-year period.

Adjusted net loss

For the nine months ended September 30, 2015, adjusted net loss was $13.9 million or $0.03 per basic share, compared to net earnings of $31.8 million or $0.06 per basic share in the prior-year period.

RECONCILIATON OF YEAR TO DATE ADJUSTED NET LOSS – 2014 TO 2015

(in millions of U.S. dollars)

The net loss has been adjusted, including the associated tax impact, for costs in “Other gains and losses” on the condensed consolidated income statement. Key entries in this grouping are: the impairment loss on the reclassification of the El Morro project as held for sale; the fair value changes for the gold stream obligation and share purchase warrants; gold stream obligation transaction costs; foreign exchange gain or loss; and other non-recurring items. Net loss is also adjusted for inventory net realizable value provisions. Other adjustments to net loss in the prior-year period include the non-cash loss incurred on the monetization of the Company’s legacy hedge position as it is realized into income over the original term of the hedge contract, which is included in revenue. See “Non-GAAP Financial Performance Measures” for reconciliation of the net loss to adjusted net earnings.

| 23 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

REVIEW OF OPERATING MINES

New Afton Mine, British Columbia, Canada The New Afton gold-copper mine is located near Kamloops, British Columbia, Canada. The mine is a large underground gold-copper deposit. New Afton’s property package consists of the nine square kilometre Afton mining lease which centers on the New Afton mine as well as 118 square kilometres of exploration licenses covering multiple mineral prospects within the historic Iron Mask mining district. At December 31, 2014, the mine had 0.8 million ounces of Proven and Probable gold Mineral Reserves and 781 million pounds of Proven and Probable copper Mineral Reserves, with 1.8 million ounces of Measured and Indicated gold Mineral Resources, exclusive of Mineral Reserves, and 1.4 billion pounds of Measured and Indicated copper Mineral Resources, exclusive of Mineral Reserves. A summary of New Afton’s operating results is provided below. |

AT-A-GLANCE 2015 GUIDANCE: Gold:105,000 - 115,000 ounces copper:85 - 95 million pounds Total cash costs/oz:($1,070) - ($1,030) ALL-IN SUSTAINING COSTS/OZ:($560) - ($520)

Q3 YTD 2015 Production: Gold:75,256 Ounces copper:60.9 million pounds Total cash costs/oz:($769) ALL-IN SUSTAINING COSTS/OZ:($203) |

Three months ended September 30 | Nine months ended September 30 | |||

| (in millions of U.S. dollars, except where noted) | 2015 | 2014 | 2015 | 2014 |

| Operating information | ||||

| Ore mined (thousands of tonnes) | 1,365 | 1,246 | 3,729 | 3,574 |

| Ore processed (thousands of tonnes) | 1,326 | 1,258 | 3,743 | 3,579 |

| Average grade: | ||||

| Gold (grams/tonne) | 0.76 | 0.76 | 0.76 | 0.82 |

| Copper (%) | 0.85 | 0.90 | 0.88 | 0.95 |

| Recovery rate (%): | ||||

| Gold | 82.9 | 83.0 | 82.0 | 84.2 |

| Copper | 85.9 | 84.7 | 83.5 | 85.6 |

| Gold (ounces): | ||||

| Produced(1) | 26,986 | 25,612 | 75,256 | 79,288 |

| Sold(1) | 23,860 | 24,668 | 70,985 | 76,225 |

| Copper (millions of pounds): | ||||

| Produced(1) | 21.4 | 21.1 | 60.9 | 64.1 |

| Sold(1) | 18.3 | 18.9 | 57.5 | 60.6 |

| Silver (millions of ounces): | ||||

| Produced(1) | 0.1 | 0.1 | 0.2 | 0.2 |

| Sold(1) | 0.1 | 0.1 | 0.2 | 0.2 |

| Average realized price (1)(2): | ||||

| Gold ($/ounce) | 1,115 | 1,159 | 1,189 | 1,277 |

| Copper ($/pound) | 2.22 | 3.13 | 2.52 | 3.06 |

| Silver ($/ounce) | 13.57 | 20.93 | 15.29 | 19.76 |

| Total cash costs per gold ounce sold ($/ounce)(2)(3) | (533) | (1,245) | (769) | (1,264) |

| All-in sustaining costs per gold ounce sold ($/ounce)(2)(3) | (20) | (700) | (203) | (680) |

| Total cash costs on a co-product basis(2)(3) | ||||

| Gold ($/ounce) | 471 | 383 | 476 | 413 |

| Copper ($/pound) | 0.94 | 1.04 | 1.01 | 0.99 |

| All-in sustaining costs on a co-product basis(2)(3) | ||||

| Gold ($/ounce) | 671 | 560 | 682 | 612 |

| Copper ($/pound) | 1.33 | 1.51 | 1.44 | 1.47 |

| 24 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

Three months ended September 30 | Nine months ended September 30 | |||

| (in millions of U.S. dollars, except where noted) | 2015 | 2014 | 2015 | 2014 |

| Financial Information: | ||||

| Revenues | 61.3 | 81.8 | 211.5 | 264.9 |

| Operating margin(2) | 39.4 | 59.4 | 139.0 | 193.8 |

| Earnings from mine operations | 4.8 | 28.0 | 37.3 | 97.0 |

| Capital expenditures (sustaining capital)(2) | 12.0 | 13.2 | 39.2 | 43.6 |

| Capital expenditures (growth capital) (2) | 1.4 | 8.4 | 14.7 | 20.6 |

| 1. | Production is shown on a total contained basis while sales are shown on a net payable basis, including final product inventory and smelter payable adjustments, where applicable. |

| 2. | We use certain non-GAAP financial performance measures throughout our MD&A. Total cash costs and all-in sustaining costs per gold ounce sold, total cash costs and all-in sustaining costs on a co-product basis, average realized price, operating margin, and capital expenditures (sustaining capital and growth capital) are non-GAAP financial performance measures with no standard meaning under IFRS. For further information and a detailed reconciliation, please refer to the “Non-GAAP Financial Performance Measures” section of this MD&A. |

| 3. | The calculation of total cash costs per gold ounce is net of by-product revenue while total cash costs and all-in sustaining costs on a co-product basis removes the impact of other metal sales that are produced as a by-product of our gold production and apportions the cash costs to each metal produced on a percentage of revenue basis. |

Year to date and Quarterly Operating Results

Production

In the third quarter of 2015, New Afton produced 26,986 gold ounces compared to 25,612 ounces in the prior-year period. The increase in quarterly production was driven by a 5% increase in throughput with gold grade and recovery remaining consistent. New Afton’s quarterly operating performance continued to benefit from the completion of the mill expansion in mid 2015. As a result of the incremental grinding capacity added to the mill circuit, gold recovery remained at 83% despite the increase in throughput.

Copper production in the third quarter of 2015 was 21.4 million pounds compared to 21.1 million pounds in the prior-year period. The combination of the 5% increase in throughput and a 1% increase in copper recovery, resulting from the successful mill expansion project, offset a decrease in copper grade.

For the nine months ended September 30, 2015, New Afton produced 75,256 gold ounces compared to 79,288 gold ounces in the prior-year period and produced 60.9 million pounds of copper compared to 64.1 million pounds of copper in the prior-year period. The decrease in gold production was due to the combination of lower gold grade and recovery, which was partially offset by higher throughput. As the mill expansion was completed on schedule in mid-2015, gold recovery in the early part of 2015 was lower than the prior year as throughput was increased. Since the completion of the mill expansion, gold recovery has increased by 3% relative to the first quarter of 2015.

Revenue

In the third quarter of 2015, revenue was $61.3 million compared to $81.8 million in the prior year impacted primarily by lower average realized commodity prices. The average realized gold price for the third quarter of 2015 was $1,115 per gold ounce compared to $1,159 per gold ounce in the prior-period and the London PM fix average of $1,124 per gold ounce. The average realized copper price for the third quarter of 2015 was $2.22 per pound of copper compared to $3.13 per pound of copper in the prior-year period and the London Metals exchange average copper price of $2.39 per pound. The average realized price in the three months ended September 30, 2015 was impacted by the final settlement of prior period sales in the third quarter of 2015 which settled at lower prices than they were marked to market at on June 30, 2015.

For the nine months ended September 30, 2015, revenue was $211.5 million compared to $264.9 million in the prior-year period due primarily to lower average realized commodity prices and lower metal sales. The average realized gold price for the nine months ended September 30, 2015 was $1,189 per gold ounce compared to $1,277 per gold ounce in the prior-year period and the London PM fix average of $1,179 per gold ounce. The average realized price in the nine months ended September 30, 2015 benefitted from the final settlement of 2014 sales in the first quarter of 2015 which settled at higher prices than they were marked to market at on December 31, 2014. The average realized copper price for the nine months ended September 30, 2015 was $2.52 per pound of copper compared to $3.06 per pound of copper in the prior-year period and the London Metals average exchange copper price of $2.59 per pound.

| 25 | WWW.NEWGOLD.COM TSX:NGD NYSE MKT:NGD |

At the end of the quarter, New Afton’s exposure to the impact of movements in market metal prices for provisionally priced contracts was 19,200 ounces of gold and 36.5 million pounds of copper. Exposure to these movements in market metal prices is reduced by 18,700 ounces of gold swaps and 24.9 million pounds of copper swaps outstanding at September 30, 2015, with settlement periods ranging from October 2015 to February 2016.

Earnings from mine operations

New Afton contributed $4.8 million to the Company’s earnings from mine operations in the third quarter of 2015, compared to $28.0 million for the prior-year period. For the nine months ended September 30, 2015, New Afton generated $37.3 million in earnings from mine operations compared to $97.0 million in the prior-year period. These differences were primarily driven by the impact of lower commodity prices, partially offset by the benefit of the weaker Canadian dollar on operating costs.

Total cash costs and all-in sustaining costs