As filed with the Securities and Exchange Commission on January 13, 2023 Registration No. 333-264350

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

POST-EFFECTIVE AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

Allianz Life Insurance Company of New York

(Exact name of Registrant as specified in its charter)

New York (State or other jurisdiction of incorporation or organization) | 6311 (Primary Standard Industrial Classification Code Number) | 13-3191369 (I.R.S. Employer Identification No.) |

1633 Broadway, 42nd Floor,

New York, New York 10019

(212) 586-7733

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Erik T. Nelson, Esq.

Allianz Life Insurance Company of North America

5701 Golden Hills Drive Minneapolis, MN 55416

(763) 765-7453

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated filer [ ]

Non-accelerated filer [X] Smaller reporting company[ ]

(Do not check if a smaller reporting company)

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

PART I PROSPECTUS

ALLIANZ Index Advantage® New York VARIABLE ANNUITY CONTRACT issued on or before December 31, 2022

Issued by Allianz Life of NY Variable Account C and Allianz Life Insurance Company of New York (Allianz Life of New York, we, us, our)

THE CONTRACT IS NO LONGER OFFERED FOR SALE TO NEW INVESTORS. We continue to administer the in force Contracts. |

The variable annuity described in this prospectus is an individual flexible purchase payment index-linked variable deferred annuity contract (Contract). This prospectus describes the Contract between you, the Owner, and Allianz Life of New York.

The Contract allows you to allocate your money (Purchase Payments) and any earnings among the Contract’s investment options (Allocation Options), which currently include index-linked investment options (Index Options) and variable investment options (Variable Options).

•

Index Options. Each Index Option is tied (or linked) to the performance of a specific market Index for a defined time period (Index Year). Each Index Option has a Buffer downside feature that provides limited protection against any negative Index rate of return (Index Return) that may be credited to your investment for an Index Year. Each Index Option also has a Capped upside feature that puts an upper limit on positive Index Return that may be credited for an Index Year.

•

Variable Options. The Variable Options performance is based on the securities in which they invest.

We expect to add or remove Variable Options, and to add Index Options, from time to time. We currently offer the following Index Options: Index Protection NY Strategy with 30% Buffer and 1.50% minimum Cap; and Index Performance Strategy with 10% Buffer and 1.50% minimum Cap.

Index-linked and variable annuity contracts are complex insurance and investment vehicles. You may lose money, including your principal investment and previously credited earnings. Contract fees and expenses could cause your losses to be greater than the downside protection of the Index Options. Your losses may be significant. Be sure to ask your Financial Professional about the Contract’s features, benefits, risks, fees and expenses, whether the Contract is appropriate for you based upon your financial situation and objectives. The Contract’s risks are described in Risk Factors on page 15 of this prospectus.

Before the end of an Index Year, if you take any type of withdrawal, execute the Performance Lock feature, begin Annuity Payments, or if we pay a death benefit or deduct a fee or expense, we base the transaction on the interim value of your Index Option investment, which includes the Daily Adjustment. The Daily Adjustment fluctuates daily, positively or negatively. The Daily Adjustment could reflect significantly less gain, or more loss than we would apply to an Index Option at the end of an Index Year.

If you have an investment advisor and choose to pay financial adviser fees from this Contract, the deduction of this financial adviser fee is in addition to this Contract’s fees and expenses, and the deduction is treated the same as any other withdrawal under the Contract. As such, withdrawals to pay financial adviser fees will be subject to withdrawal charges, will reduce the Contract Value and Guaranteed Death Benefit Value (perhaps significantly), and may be subject to federal and state income taxes (including a 10% additional federal tax). A six-year withdrawal charge period applies to the initial and any additional Purchase Payment. Please consult with your Financial Professional before requesting us to pay financial adviser fees from this Contract rather than from other assets you may have.

All guarantees under the Contract, including index-linked returns (Performance Credits), are the obligations of Allianz Life of New York and are subject to our claims-paying ability and financial strength.

Please read this prospectus before investing and keep it for future reference. The prospectus describes all material rights and obligations of purchasers under the Contract. It contains important information about the Contract and Allianz Life of New York that you ought to know before investing. Availability of Index Options may vary by financial intermediary. You can obtain information on which Index Options are available to you by calling (800) 624-0197, or from your Financial Professional. This prospectus is offered only in New York. This prospectus is not offered in any state, country, or jurisdiction in which we are not authorized to sell the Contracts. You should rely only on the information contained in this prospectus. We have not authorized anyone to give you different information.

The Securities and Exchange Commission (SEC) has not approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense. An investment in this

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

Contract is not a deposit of a bank or financial institution and is not federally insured or guaranteed by the Federal Deposit Insurance Corporation or any other federal government agency. An investment in this Contract involves investment risk including the possible loss of principal.

This prospectus is not intended to constitute a suitability recommendation or fiduciary advice.

Additional information about certain investment products, including variable annuities, has been prepared by the Securities & Exchange Commission’s (SEC) staff and is available at investor.gov.

Dated: May 1, 2023

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

GlossaryThis prospectus is written in plain English. However, there are some technical words or terms that are capitalized and are used as defined terms throughout the prospectus. For your convenience, we included this glossary to define these terms.

Accumulation Phase – the first phase of your Contract before you request Annuity Payments. The Accumulation Phase begins on the Issue Date.

Allocation Options – the Variable Options and Index Options available to you under the Contract.

Annuitant – the individual upon whose life we base the Annuity Payments. Subject to our approval, the Owner designates the Annuitant, and can add a joint Annuitant for the Annuity Phase. There are restrictions on who can become an Annuitant.

Annuity Date – the date we begin making Annuity Payments to the Payee from the Contract. The earliest available Annuity Date is 13 months after the Issue Date, and the latest possible Annuity Date is either age 90 or age 100 depending on the requirements of the Financial Professional you purchased your Contract through.

Annuity Options – the annuity income options available to you under the Contract.

Annuity Payments – payments made by us to the Payee pursuant to the chosen Annuity Option.

Annuity Phase – the phase the Contract is in once Annuity Payments begin.

Beneficiary – the person(s) or entity the Owner designates to receive any death benefit, unless otherwise required by the Contract or applicable law.

Buffer – for each Index Option, this is the negative Index Return that we absorb before applying a negative Performance Credit. The Buffers are 10% or 30%, and do not change.

Business Day – each day on which the New York Stock Exchange is open for trading. Allianz Life of New York is open for business on each day that the New York Stock Exchange is open. Our Business Day ends when regular trading on the New York Stock Exchange closes, which is usually at 4:00 p.m. Eastern Time.

Cap – for any Index Option, this is the upper limit on positive Index performance and the maximum potential Performance Credit for an Index Option. We set a Cap for each Index Option on the Index Effective Date and each Index Anniversary. The Caps applicable to your Contract are shown on the Index Options Statement.

Charge Base – the Contract Value on the preceding Quarterly Contract Anniversary (or the initial Purchase Payment received on the Issue Date if this is before the first Quarterly Contract Anniversary), increased by the dollar amount of subsequent Purchase Payments, and reduced proportionately for subsequent withdrawals you take or financial adviser fees that you choose to have us pay from this Contract (including any withdrawal charge) and deductions we make for Contract fees and expenses. All withdrawals you take reduce the Charge Base, even Penalty-Free Withdrawals. We use the Charge Base to determine the next product fee we deduct.

Contract – the individual flexible purchase payment index-linked and variable deferred annuity contract described by this prospectus. The Contract may also be referred to as a registered index-linked annuity, or “RILA”.

Contract Anniversary – a twelve-month anniversary of the Issue Date or any subsequent Contract Anniversary.

Contract Value – the value of your Purchase Payments based on the returns of your selected Allocation Options reduced for previously assessed Contract fees and expenses, and withdrawals. On any Business Day, your Contract Value is the sum of your Index Option Value(s) and Variable Account Value. The Variable Account Value component of the Contract Value fluctuates each Business Day that money is held in a Variable Option. The Index Option Value component of the Contract Value is adjusted on each Index Anniversary to reflect Performance Credits, which can be negative. A negative Performance Credit means that you can lose principal and previous earnings. The Index Option Values also reflect the Daily Adjustment on every Business Day other than the Index Effective Date or an Index Anniversary. All withdrawals you take reduce Contract Value dollar for dollar, even Penalty-Free Withdrawals, and financial adviser fees that you choose to have us pay from this Contract. Contract Value is also reduced dollar for dollar for deductions we make for Contract fees and expenses. However, Contract Value does not reflect future fees and expenses we would apply on liquidation.

Contract Year – any period of twelve months beginning on the Issue Date or a subsequent Contract Anniversary.

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

Crediting Method – a method we use to calculate annual Performance Credits if you allocate Purchase Payments or transfer Contract Value to an Index Option.

Daily Adjustment – how we calculate Index Option Values on days other than the Index Effective Date or an Index Anniversary for each Index Option as discussed in section 4, Valuing Your Contract – Daily Adjustment; and Appendix B. The Daily Adjustment approximates the Index Option Value that will be available on the next Index Anniversary. It is the estimated present value of the future Performance Credit that we will apply on the next Index Anniversary.

Determining Life (Lives) – the person(s) designated at Contract issue and named in the Contract on whose life we base the guaranteed Traditional Death Benefit.

Financial Professional – the person who advises you regarding the Contract.

Good Order – a request is in “Good Order” if it contains all of the information we require to process the request. If we require information to be provided in writing, “Good Order” also includes providing information on the correct form, with any required certifications, guarantees and/or signatures, and received at our Service Center after delivery to the correct mailing, email, or website address, which are all listed at the back of this prospectus. If you have questions about the information we require, or whether you can submit certain information by fax, email or over the web, please contact our Service Center. If you send information by email or upload it to our website, we send you a confirmation number that includes the date and time we received your information.

Guaranteed Death Benefit Value – the guaranteed value that is available to your Beneficiary(s) on the first death of any Determining Life during the Accumulation Phase. The Guaranteed Death Benefit Value is total Purchase Payments reduced proportionately for withdrawals you take (including any withdrawal charge). All withdrawals you take reduce the Guaranteed Death Benefit Value, even Penalty-Free Withdrawals, and any financial adviser fees that you choose to have us pay from this Contract. However, we do not reduce the Guaranteed Death Benefit Value for deductions we make for Contract fees and expenses.

Index (Indexes) – one (or more) of the nationally recognized third-party broad based equity securities price return Indexes available to you under your Contract. The Indexes are described in Appendix A.

Index Anniversary – a twelve-month anniversary of the Index Effective Date or any subsequent Index Anniversary. It is the date we apply Performance Credits. If an Index Anniversary does not occur on a Business Day, we consider it to occur on the next Business Day for the purposes of determining Index Values and Index Returns, applying Performance Credits, and setting the Caps.

Index Effective Date – the first day we allocate assets to an Index Option. You selected the Index Effective Date when you purchased the Contract. The Index Effective Date is stated on the Index Options Statement and starts the first Index Year.

Index Option – the index-linked investments available to you under the Contract. Each Index Option is the combination of an Index, a Crediting Method, and a Buffer amount.

Index Option Base – an amount we use to calculate Performance Credits and the Daily Adjustment. The Index Option Base is initially equal to the amounts you allocate to an Index Option. We reduce the Index Option Base proportionately for withdrawals you take and any financial adviser fees that you choose to have us pay from this Contract (including any withdrawal charge), and deductions we make for Contract fees and expenses; we increase/decrease it by the dollar amount of additional Purchase Payments allocated to, transfers into or out of the Index Option; and any Performance Credits.

Index Option Value – on any Business Day, it is equal to the portion of your Contract Value in a particular Index Option. We establish an Index Option Value for each Index Option you select. Each Index Option Value includes any Performance Credits from previous Index Anniversaries and reflects proportional reductions for previous partial withdrawals you take and any financial adviser fees that you choose to have us pay from this Contract (including any withdrawal charge), and previous deductions we made for Contract fees and expenses. On each Business Day during the Index Year other than the Index Effective Date or an Index Anniversary, the Index Option Values also include an increase/decrease from the Daily Adjustment.

Index Options Statement – the account statement we mail to you on the Index Effective Date and each Index Anniversary thereafter. On the Index Effective Date, the statement showed the initial Index Values, Caps for the Index Options you selected. On each Index Anniversary, the statement shows the new Index Values, Performance Credits received, and renewal Caps that are effective for the next year for the Index Options you selected. The Index Options Statement also shows the applicable Buffer for your selected Index Option(s).

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

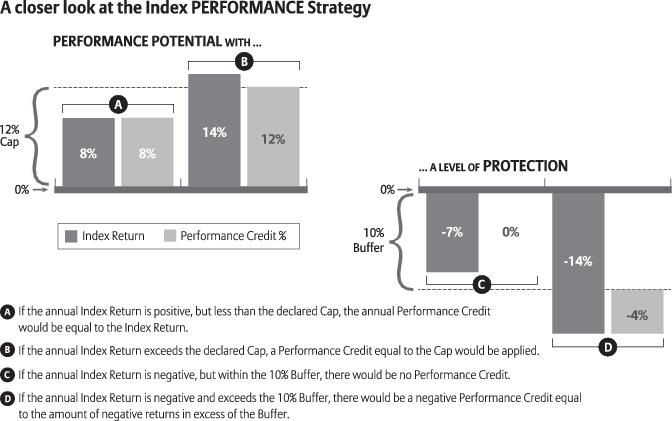

Index Performance Strategy – one of the Crediting Methods described in section 4, Valuing Your Contract. The Index Performance Strategy calculates Performance Credits based on Index Returns subject to a Cap and 10% Buffer. You can receive negative Performance Credits, which means you can lose principal and previous earnings. The Index Performance Strategy provides the highest potential returns. Its Caps will generally be greater than the Index Protection NY Strategy Caps. The Index Performance Strategy is more sensitive to large negative market movements because small negative market movements are absorbed by the 10% Buffer.

Index Protection NY Strategy – one of the Crediting Methods described in section 4, Valuing Your Contract. The Index Protection NY Strategy calculates Performance Credits based on Index Returns subject to a Cap and 30% Buffer. You can receive negative Performance Credits under this Crediting Method, which means you can lose principal and previous earnings. The Index Protection NY Strategy provides more protection than the Index Performance Strategy. It generally has higher Buffers in exchange for lower Caps.

Index Return – the percentage change in Index Value from the Index Effective Date or an Index Anniversary to the next Index Anniversary, which we use to determine the Performance Credits. The Index Return is an Index’s current Index Value, minus its Index Value on the last Index Anniversary (or the Index Effective Date if this is the first Index Anniversary), divided by its Index Value on the last Index Anniversary (or the Index Effective Date if this is the first Index Anniversary).

Index Value – an Index’s closing market price at the end of the Business Day on the Index Effective Date and each Index Anniversary as provided by Bloomberg or another market source if Bloomberg is not available.

Index Year – a twelve-month period beginning on the Index Effective Date or a subsequent Index Anniversary.

Issue Date – the date we issued the Contract. The Issue Date is stated in your Contract and starts your first Contract Year. Contract Anniversaries and Contract Years are measured from the Issue Date.

Joint Owners – the two person(s) designated at Contract issue and named in the Contract who may exercise all rights granted by the Contract.

Lock Date – this is the Business Day we execute a Performance Lock and capture an Index Option Value (which includes the Daily Adjustment) before the Index Anniversary.

Non-Qualified Contract – a Contract that is not purchased under a pension or retirement plan that qualifies for special tax treatment under sections of the Code.

Owner – “you,” “your” and “yours.” The person(s) or entity designated at Contract issue and named in the Contract who may exercise all rights granted by the Contract.

Payee – the person or entity who receives Annuity Payments during the Annuity Phase.

Penalty-Free Withdrawals – withdrawals you take that are not subject to a withdrawal charge. Penalty-Free Withdrawals include withdrawals you take under the free withdrawal privilege or waiver of withdrawal charge benefit, and RMD payments you take under our minimum distribution program.

Performance Credit – the return you receive on an Index Anniversary from the Index Options. We base Performance Credits on Index Values and Index Returns up to the Cap if returns are positive, or after application of the Buffer if returns are negative. If Performance Credits are negative, you can lose principal and previous earnings.

Performance Lock – a feature that allows you to capture the current Index Option Value during the Index Year. A Performance Lock applies to the total Index Option Value in an Index Option, and not just a portion of that Index Option Value. After the Lock Date, Daily Adjustments do not apply to a locked Index Option for the remainder of the Index Year and the locked Index Option Value will not receive a Performance Credit.

Proxy Investment – provides a current estimate of what the Performance Credit will be on the next Index Anniversary taking into account any applicable Buffer and Cap. We use the Proxy Investment to calculate the Daily Adjustment on Business Days other than the Index Effective Date or an Index Anniversary. For more information, see Appendix B.

Proxy Value – the hypothetical value of the Proxy Investment used to calculate the Daily Adjustment as discussed in Appendix B.

Purchase Payment – the money you put into the Contract.

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

Qualified Contract – a Contract purchased under a pension or retirement plan that qualifies for special tax treatment under sections of the Code (for example, 401(a) and 401(k) plans), Individual Retirement Annuities (IRAs), or Tax-Sheltered Annuities (referred to as TSA contracts).

Quarterly Contract Anniversary – the day that occurs three calendar months after the Issue Date or any subsequent Quarterly Contract Anniversary.

Separate Account – Allianz Life of NY Variable Account C is the Separate Account that issued the variable investment portion of your Contract. It is a separate investment account of Allianz Life of New York. The Separate Account holds the Variable Options that underlie the Contracts. The Separate Account is divided into subaccounts, each of which invests exclusively in a single Variable Option. The Separate Account is registered with the SEC as a unit investment trust, and may be referred to as the Registered Separate Account.

Service Center – the area of our company that provides Contract maintenance and routine customer service. Our Service Center address and telephone number are listed at the back of this prospectus. The address for mailing checks for Purchase Payments may be different and is also listed at the back of this prospectus.

Traditional Death Benefit – the guaranteed death benefit automatically provided by the Contract for no additional fee described in section 10.

Valid Claim – the documents we require to be received in Good Order at our Service Center before we pay any death claim. This includes the death benefit payment option, due proof of death, and any required governmental forms. Due proof of death includes a certified copy of the death certificate, a decree of court of competent jurisdiction as to the finding of death, or any other proof satisfactory to us.

Variable Account Value – on any Business Day it is equal to the portion of your Contract Value in your selected Variable Options. The Variable Account Value increases and decreases based on your selected Variable Options’ performance and reflects deduction of the Variable Option operating expenses, and previous deductions we made for Contract fees and expenses.

Variable Options – the variable investments available to you under the Contract. Variable Option performance is based on the securities in which they invest.

Withdrawal Charge Basis – the total amount under your Contract that is subject to a withdrawal charge as discussed in section 6, Expenses – Withdrawal Charge.

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

Important Information You Should Consider About the Contract | | |

Charges for Early Withdrawals | If you withdraw money from the Contract within six years of your last Purchase Payment, you will be assessed a withdrawal charge of up to 8.5% of the Purchase Payment withdrawn, declining to 0% over that time period. For example, if you invest $100,000 in the Contract and make an early withdrawal, you could pay a withdrawal charge of up to $8,500. In addition, if you take a full or partial withdrawal (including financial adviser fees that you choose to have us pay from this Contract) from an Index Option on a date other than the Index Effective Date or an Index Anniversary, a Daily Adjustment will apply to the Index Option Value available for withdrawal. The Daily Adjustment also applies if before the Index Anniversary you execute a Performance Lock, annuitize the Contract, we pay a death benefit, or we deduct Contract fees and expenses. The Daily Adjustment may be positive, negative, or equal to zero. A negative Daily Adjustment will result in loss. In extreme circumstances, a negative Daily Adjustment could result in a loss beyond the protection of the 10% or 30% Buffer, but it cannot result in a total loss of -100%. | Fee Tables 4. Valuing Your Contract – Daily Adjustment 6. Expenses – Withdrawal Charge Appendix B – Daily Adjustment |

| In addition to withdrawal charges, and Daily Adjustments that may apply to withdrawals and other transactions from the Index Options, we will also charge you a fee of $25 per transfer after you exceed 12 transfers between Variable Options in a Contract Year. | Fee Tables 6. Expenses – Transfer Fee |

Ongoing Fees and Expenses (annual charges) | The table below describes the fees and expenses that you may pay each year, depending on the options you choose. Please refer to your Contract specifications page for information about the specific fees you will pay each year based on the options you have elected. These ongoing fees and expenses do not reflect any financial adviser fees paid to a Financial Professional from your Contract Value or other assets of the Owner. If such charges were reflected, these ongoing fees and expenses would be higher. [To be updated by amendment] | Fee Tables 6. Expenses Appendix G – Variable Options Under the Contract |

| | |

| | |

(Variable Option fees and expenses) | | |

| Optional Benefits Available for an Additional Charge (for a single optional benefit, if elected) | | | |

| As a percentage of the Charge Base, plus an amount attributable to the contract maintenance charge. | |

| As a percentage of the Variable Option’s average daily net assets. | |

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

| | |

| Because your Contract is customizable, the choices you make affect how much you will pay. To help you understand the cost of owning your Contract, the following table shows the lowest and highest cost you could pay each year, based on current charges. This estimate assumes that you do not take withdrawals from the Contract, which if taken from the Index Options could result in substantial losses due to the application of negative Daily Adjustments. [To be updated by amendment] | |

| Lowest Annual Cost: $1,753 | Highest Annual Cost: $1,803 | |

| Assumes: •Investment of $100,000 •Least expensive Variable Option fees and expenses •5% annual appreciation •No additional Purchase Payments, transfers, or withdrawals •No financial adviser fees | Assumes: •Investment of $100,000 •Most expensive Variable Option fees and expenses •5% annual appreciation •No additional Purchase Payments, transfers, or withdrawals •No financial adviser fees | |

| | |

| You can lose money by investing in the Contract, including loss of principal and previous earnings. | |

Not a Short-Term Investment | • This Contract is not a short-term investment and is not appropriate if you need ready access to cash. • Considering the benefits of tax deferral and long-term income, the Contract is generally more beneficial to investors with a long investment time horizon. • If within six years after we receive a Purchase Payment you take a full or partial withdrawal (including financial adviser fees that you choose to have us pay from this Contract), withdrawal charges will apply. A withdrawal charge will reduce your Contract Value or the amount of money that you actually receive. Withdrawals may reduce or end Contract guarantees. • Withdrawals are subject to income taxes, including a 10% additional federal tax that may apply to withdrawals taken before age 59 1∕2. • Amounts invested in an Index Option must be held in the Index Option for a full Index Year before they can receive a Performance Credit. We apply a Daily Adjustment if before the Index Anniversary you take a full or partial withdrawal (including financial adviser fees that you choose to have us pay from this Contract), annuitize the Contract, execute a Performance Lock, we pay a death benefit, or we deduct Contract fees and expenses. For more information see section 4, Valuing Your Contract - Daily Adjustment; and Appendix B – Daily Adjustment. • The Traditional Death Benefit may not be modified, but it will terminate if you take withdrawals that reduce both the Contract Value and Guaranteed Death Benefit Value to zero. Withdrawals may reduce the Traditional Death Benefit’s Guaranteed Death Benefit Value by more than the value withdrawn and could end the Traditional Death Benefit. | Risk Factors 4. Valuing Your Contract 10. Death Benefit Appendix B – Daily Adjustment |

Risks Associated with Investment Options | • An investment in the Contract is subject to the risk of poor investment performance and can vary depending on the performance of the Variable Options and the Index Options available under the Contract. • Each Variable Option and Index Option has its own unique risks. • You should review each Variable Option’s prospectus and disclosures, including risk factors, for each Index Option before making an investment decision. | |

| An investment in the Contract is subject to the risks related to us. All obligations, guarantees or benefits of the Contract are the obligations of Allianz Life of New York and are subject to our claims-paying ability and financial strength. More information about Allianz Life of New York, including our financial strength ratings, is available upon request by visiting allianzlife.com/new-york/about/why-allianz, or contacting us at (800) 624-0197. | |

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

| | |

| • Certain Index Options may not be available under your Contract. • The first 12 transfers between Variable Options every Contract Year are free. After that, we deduct a $25 transfer fee for each additional transfer. Your transfers between the Variable Options are also subject to policies designed to deter excessively frequent transfers and market timing. • We only allow assets to move into the Index Options on the Index Effective Date and on subsequent Index Anniversaries as discussed in section 3, Purchase Payments – Allocation of Purchase Payments and Contract Value Transfers. • You can transfer Index Option Value only on an Index Anniversary. • We reserve the right to close or substitute the Variable Options, and to substitute Indexes. We can also decline a Purchase Payment if it does not meet the requirements set out in section 3, Purchase Payments – Purchase Payment Requirements. | Risk Factors 3. Purchase Payments 4. Valuing Your Contract 5. Variable Options 6. Expenses – Transfer Fee Appendix A – Available Indexes |

| The Contract does not offer any Optional Benefits. | |

| | |

| • Consult with a tax professional to determine the tax implications of an investment in and withdrawals from or payments received under the Contract. • If you purchased the Contract through a tax-qualified plan or individual retirement account (IRA), you do not get any additional tax benefit under the Contract. • Earnings under the Contract may be taxed at ordinary income rates when withdrawn, and you may have to pay a 10% additional federal tax if you take a full or partial withdrawal before age 59 1∕2. | |

| | |

Investment Professional Compensation | Your Financial Professional may receive compensation for selling this Contract to you, in the form of commissions, additional cash benefits (e.g., cash bonuses), and non-cash compensation. We and/or our wholly owned subsidiary distributor may also make marketing support payments to certain selling firms for marketing services and costs associated with Contract sales. This conflict of interest may influence your Financial Professional to recommend this Contract over another investment for which the Financial Professional is not compensated or compensated less. | 12. Other Information – Distribution |

| Some Financial Professionals may have a financial incentive to offer you a new contract in place of the one you already own. You should only exchange your contract if you determine, after comparing the features, fees, and risks of both contracts, that it is better for you to purchase the new contract rather than continue to own your existing contract. | 12. Other Information – Distribution |

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

Overview of the ContractWhat Is the Purpose of the Contract?

The Allianz Index Advantage® New York is a product that offers Index Options and Variable Options and allows you to defer taking regular fixed periodic payments (Annuity Payments) to a future date. Under the Contract, you make one or more Purchase Payments. Purchase Payments you allocate to the Index Options are first invested for a limited time in the AZL Government Money Market Fund and then transferred to the Index Option(s) that you select for investment. Depending on several factors (e.g., Allocation Options you select, market conditions, and timing of any withdrawals), your Contract can gain or lose value. When you are ready to receive a guaranteed stream of income under your Contract, you can annuitize your accumulated assets and begin receiving Annuity Payments from us based on the payout option you select (Annuity Options). The Contract includes for no additional charge a standard death benefit (the Traditional Death Benefit) that helps to financially protect your beneficiaries.

We designed the Contract for people who are looking for a death benefit for a period of time, and a level of protection for your principal investment while providing potentially higher returns than are available on traditional fixed annuities. In addition, you should have a long investment time horizon and your financial goals should be otherwise consistent with the terms and conditions of the Contract. This Contract is not intended for someone who is seeking complete protection from downside risk, seeking unlimited investment potential, or expecting to take withdrawals that will not be subject to withdrawal charges or Daily Adjustments (i.e., a person that does not need access to Contract Value within six years after we receive a Purchase Payment, or before an Index Anniversary).

Product features may not be available to all Contracts as stated in Appendix F - Material Contract Variations by Issue Date. Availability of Index Options may vary by financial intermediary. You can obtain information on which Index Options are available to you by calling (800) 624-0197, or from your Financial Professional.

What Are the Phases of the Contract?

The Contract has two phases: (1) an Accumulation Phase, and (2) an Annuity Phase.

•

Accumulation Phase. This is the first phase of your Contract, and it begins on the Issue Date. During the Accumulation Phase, your money is invested under the Contract on a tax-deferred basis. Tax deferral may not be available for certain non-individually owned contracts. Tax deferral means you are not taxed on any earnings or appreciation on the assets in your Contract until you take money out of your Contract. In addition, during this phase, you can make additional Purchase Payments, you can take withdrawals, and if you die we pay a death benefit to your named Beneficiary(s).

Your Contract Value may fluctuate up or down during the Accumulation Phase based on the performance of your selected Allocation Options.

−

Index Options. You may allocate your Purchase Payments to any or all of the Index Options available under your Contract. There are currently 8 Index Options based on different combinations of two credit calculation methods (Crediting Methods), and four nationally recognized third-party broad based equity securities price return Indexes. Each Index Option is the combination of an Index, a Crediting Method, and a Buffer amount.

Currently Available Crediting Methods and Buffers | Currently Available Indexes | Positive Index Performance Participation Limit |

Index Protection NY Strategy with 30% Buffer | • S&P 500® Index • Russell 2000® Index • Nasdaq-100® Index • EURO STOXX 50® | |

Index Performance Strategy with 10% Buffer | • S&P 500® Index • Russell 2000® Index • Nasdaq-100® Index • EURO STOXX 50® | |

Your initial and renewal Caps are stated in your Index Options Statement, which is the account statement we mail to you on the Index Effective Date and each Index Anniversary. The Index Options Statement also includes the Index

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

Values on the previous and current Index Anniversary. We use these Index Values to determine Index Returns and Performance Credits. More detailed information about the Index Options is included in section 4, Valuing Your Contract.

−

Variable Options. You can allocate your Purchase Payments to any or all of the Variable Options available under your Contract. We only allow assets to move into the Index Options on the Index Effective Date and on subsequent Index Anniversaries. As a result, we hold Purchase Payments you allocate to the Index Options in the AZL Government Money Market Fund until we transfer them to the Index Options in accordance with your instructions. The Variable Options are underlying mutual funds with their own investment objectives, strategies, and risks. For more information, please see Appendix G - Variable Options Available Under the Contract.

•

Annuity Phase. If you request Annuity Payments, the Accumulation Phase ends and the Annuity Phase begins. Annuity Payments are fixed payments we make based on the Annuity Option you select and your Contract Value (which reflects any previously deducted Contract fees and expenses) less final product fee. Annuity Payments can provide a guaranteed lifetime fixed income stream with certain tax advantages. We designed the Annuity Payments for Owners who no longer need immediate access to Contract Value to meet their short-term income needs.

During the Annuity Phase, you will receive a stream of regular income in the form of Annuity Payments. You will be unable to take withdrawals upon demand, the Traditional Death Benefit ends, and no amounts will be payable upon death during the Annuity Phase unless your Annuity Option provides otherwise.

What Are the Contract’s Primary Features?

•

Accessing Your Money. During the Accumulation Phase, you can surrender (take a full withdrawal) the Contract or take partial withdrawals. Withdrawals may be subject to a withdrawal charge, negative Daily Adjustments, and income taxes, including a 10% additional federal tax if taken before age 59 1∕2.

•

Additional Purchase Payments. Subject to the limitations described in this prospectus, we continue to accept additional Purchase Payments under the Contracts during the Accumulation Phase. We only allow additional Purchase Payments to move into Index Options on Index Anniversaries. As a result, we hold Purchase Payments you allocate to the Index Options that we receive on days other than an Index Anniversary in the AZL Government Money Market Fund and such Purchase Payments are not available to receive Performance Credits until we transfer them to your selected Index Options. We do not allow assets to move into an established Index Option until the Index Anniversary.

•

Death Benefit. The Contract’s death benefit is paid upon the first death of any Determining Life during the Accumulation Phase. The Contract includes for no additional charge a standard death benefit (the Traditional Death Benefit). The death benefit equals the greater of Contract Value, or the Guaranteed Death Benefit Value (which is based on Purchase Payments).

•

Withdrawal Charge Waivers. Under the free withdrawal privilege, you may withdraw up to 10% of your total Purchase Payments each Contract Year during the Accumulation Phase without incurring a withdrawal charge. Upon a full withdrawal, the free withdrawal privilege is not available to you. We do not apply a withdrawal charge to deductions we make for Contract fees or expenses. The waiver of withdrawal charge benefit allows you to take a withdrawal after the first Contract Year without incurring a withdrawal charge if you are confined to a nursing home for a period of at least 90 consecutive days. Also, if you own an IRA or Simplified Employee Pension (SEP) IRA Contract, payments you take under our minimum distribution program (RMD payments) are not subject to a withdrawal charge. Withdrawals under these waivers are still subject to income taxes (including tax penalties if you are younger than age 59 1∕2) and may reduce Contract benefits (perhaps significantly).

•

Deduction of Financial Adviser Fees. If you have a financial adviser and want to pay their financial adviser fees from this Contract, you can instruct us to withdraw the fee from your Contract and pay it to your Financial Professional or Financial Professional’s firm as instructed. The deduction of financial adviser fees is in addition to this Contract’s fees and expenses, and the deduction is treated the same as any other withdrawal under the Contract. As such, withdrawals to pay financial adviser fees will be subject to withdrawal charges, will reduce the Contract Value and Guaranteed Death Benefit Value (perhaps significantly), and may be subject to income taxes (including a 10% additional federal tax if you are younger than age 59 1∕2). Please consult with your Financial Professional before requesting us to pay financial adviser fees from this Contract rather than from other assets you may have.

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

Fee TablesThe following tables describe the fees and expenses that you will pay when buying, owning, and surrendering or making withdrawals from the Contract. Please refer to your Contract specifications page for information about the specific fees you will pay each year. These tables do not reflect any financial adviser fees that you pay from your other assets, or that you choose to have us pay from this Contract. If financial adviser fees were reflected, fees and expenses would be higher.

The first table describes the fees and expenses that you will pay at the time that you buy the Contract, surrender or make withdrawals from the Contract, or transfer Contract Value between investment options. State premium taxes may also be deducted.

Transaction Expenses

Withdrawal Charge During Your Contract’s First Phase, the Accumulation Phase(1)

(as a percentage of each Purchase Payment withdrawn)(2)

Number of Complete Years Since Purchase Payment | |

| |

| |

| |

| |

| |

| |

| |

| |

(for each transfer between Variable Options after twelve in a Contract Year) | |

| Index Protection NY Strategy and Index Performance Strategy |

Daily Adjustment Maximum Potential Loss | |

(as a percentage of Index Option Value, applies for distributions from an Index Option before any Index Anniversary)(4) | |

(1)

The Contract provides a free withdrawal privilege that allows you to withdraw 10% of your total Purchase Payments annually without incurring a withdrawal charge, as discussed in section 7, Access to Your Money – Free Withdrawal Privilege.

(2)

The Withdrawal Charge Basis is the total amount under your Contract that is subject to a withdrawal charge, as discussed in section 6, Expenses – Withdrawal Charge.

(3)

We count all transfers made in the same Business Day as one transfer, as discussed in section 6, Expenses – Transfer Fee. The transfer fee does not apply to transfers to or from the Index Options and these transfers do not count against your free transfers. Transfers are subject to the policies discussed in section 5, Variable Options – Excessive Trading and Market Timing.

(4)

This shows the maximum potential loss due to the application of the Daily Adjustment (e.g., maximum loss could occur if there is a total distribution within an Index Year at a time when the Index price has declined to zero). The Daily Adjustment could result in a loss beyond the protection of the 10% or 30% Buffer. The Daily Adjustment applies if before an Index Anniversary you take a full or partial withdrawal (including any financial adviser fees that you choose to have us pay from this Contract), execute a Performance Lock, annuitize the Contract, we pay a death benefit, or when we deduct Contract fees or expenses. The actual Daily Adjustment calculation is determined by a formula described in Appendix B.

The next table describes the fees and expenses that you will pay each year during the time that you own the Contract (not including Variable Option fees and expenses).

Annual Contract Expenses

Administrative Expenses (or contract maintenance charge)(1) (per year) | |

Base Contract Expenses(2) (as a percentage of the Charge Base) | |

(1)

Referred to as the “contract maintenance charge” in the Contract and elsewhere in this prospectus. Waived if the Contract Value is at least $100,000. Also waived during the Annuity Phase. See the section 6, Expenses – Contract Maintenance Charge (Administrative Expenses).

(2)

Referred to as the “product fee” in the Contract and elsewhere in this prospectus. See section 6, Expenses – Base Contract Expenses (Product Fee).

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

The next table shows the minimum and maximum total operating expenses charged by the Variable Options that you may pay periodically during the time that you own the Contract. A complete list of Variable Options available under the Contract, including their annual expenses, may be found in Appendix G – Variable Options Available Under the Contract.

Annual Variable Option Expenses

[To be updated by amendment]

| | |

(expenses that are deducted from Variable Option assets, including management fees, distribution and/or service (12b-1) fees, and other expenses) | | |

Example

This Example is intended to help you compare the cost of investing in the Contract with the cost of investing in other variable annuity contracts. These costs include transaction expenses, annual Contract expenses, and annual Variable Option expenses. These costs do not include any financial adviser fees that you pay from your other assets, or that you choose to have us pay from this Contract.

The Example assumes that you invest $100,000 in the Contract for the time periods indicated. The Example also assumes that your investment has a 5% return each year. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

[To be updated by amendment]

(1)

If you surrender your Contract (take a full withdrawal) at the end of the applicable time period.

| | | | |

Maximum Variable Option expense | | | | |

Minimum Variable Option expense | | | | |

(2)

If you annuitize your Contract at the end of the applicable time period.

| | | | |

Maximum Variable Option expense | | | | |

Minimum Variable Option expense | | | | |

*

The earliest available Annuity Date is 13 months after the Issue Date.

(3)

If you do not surrender your Contract.

| | | | |

Maximum Variable Option expense | | | | |

Minimum Variable Option expense | | | | |

Risk FactorsThe Contract involves certain risks that you should understand before investing. You should carefully consider your income needs and risk tolerance to determine whether the Contract is appropriate for you. The level of risk you bear and your potential investment performance will differ depending on the Allocation Options you choose.

Liquidity Risks

We designed the Contract to be a long-term investment that you can use to help build and provide income for retirement. The Contract is not suitable for short-term investment.

If you need to take a full or partial withdrawal during the withdrawal charge period, or when we deduct any financial adviser fees that you choose to have us pay from this Contract, we deduct a withdrawal charge unless the withdrawal is a Penalty-Free Withdrawal. While Penalty-Free Withdrawals provide some liquidity, they are permitted in only limited amounts or in special circumstances. If you need to withdraw most or all of your Contract Value in a short period, you will

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

exceed the Penalty-Free Withdrawal amounts available to you and incur withdrawal charges. (For more information on the withdrawal charge, see the Fee Tables and section 6, Expenses – Withdrawal Charge.)

We calculate the withdrawal charge as a percentage of your Purchase Payments, not Contract Value. Consequently, if the Contract Value has declined since you made a Purchase Payment, it is possible the percentage of Contract Value withdrawn to cover the withdrawal charge would be greater than the withdrawal charge percentage. For example, assume you buy the Contract with a single Purchase Payment of $1,000. If your Contract Value in the 5th year is $800 and you take a full withdrawal a 5% withdrawal charge applies. The total withdrawal charge would be $50 (5% of $1,000). This results in you receiving $750.

In addition, upon a full withdrawal the free withdrawal privilege is not available to you, and we apply a withdrawal charge against Purchase Payments that are still within their withdrawal charge period, including amounts previously withdrawn under the free withdrawal privilege. On a full withdrawal your Withdrawal Charge Basis may be greater than your Contract Value because the following reduce your Contract Value, but do not reduce your Withdrawal Charge Basis: deductions we make for Contract fees or expenses; and/or poor performance.

Amounts withdrawn from this Contract may also be subject to federal and state income taxes, and a 10% additional federal tax if taken before age 59 1∕2.

We only apply Performance Credits to the Index Options once each Index Year on the Index Anniversary, rather than on a daily basis. In the interim, we calculate Index Option Values based on the Daily Adjustment. The Variable Options are not subject to the Daily Adjustment. Any assets removed from an Index Option during the Index Year for withdrawals you take (including Penalty-Free Withdrawals and any financial adviser fees that you choose to have us pay from this Contract), Annuity Payments, or deductions we make for Contract fees and expenses, or if we pay a death benefit, will not be eligible to receive a Performance Credit on the Index Anniversary. These removed assets will not receive the full benefit of the Index Value, Index Return, and the 10% or 30% Buffer that would have been available on the Index Anniversary, and losses could exceed the protection offered by the 10% or 30% Buffer. You will receive a Performance Credit only on the Index Option Value remaining in an Index Option on the Index Anniversary.

You can transfer Index Option Value to the Variable Options only on every sixth Index Anniversary, and you can transfer Index Option Value among the Index Options only on Index Anniversaries. At other times, you can only move assets out of an Index Option by taking a full or partial withdrawal, or entering the Annuity Phase. These restrictions may limit your ability to react to changes in market conditions. You should consider whether investing in an Index Option is consistent with your financial needs.

Risks of Investing in Securities

Returns on securities and securities Indexes can vary substantially, which may result in investment losses. The historical performance of the available Allocation Options does not guarantee future results. It is impossible to predict whether underlying investment values will fall or rise. Trading prices of the securities underlying the Allocation Options are influenced by economic, financial, regulatory, geographic, judicial, political and other complex and interrelated factors. These factors can affect capital markets generally and markets on which the underlying securities are traded and these factors can influence the performance of the underlying securities.

If you allocate Purchase Payments or transfer Contract Value to an Index Option, your returns depend on the performance of an Index although you are not directly invested in the Index. Because the S&P 500® Index, Russell 2000® Index, Nasdaq-100® Index and EURO STOXX 50® are each comprised of a collection of equity securities, in each case the value of the component securities is subject to market risk, or the risk that market fluctuations may cause the value of the component securities to go up or down, sometimes rapidly and unpredictably. In addition, the value of equity securities may decline for reasons directly related to the issuers of the securities.

S&P 500® Index. The S&P 500® Index is comprised of equity securities issued by large-capitalization U.S. companies. In general, large-capitalization companies may be unable to respond quickly to new competitive challenges, and also may not be able to attain the high growth rate of successful smaller companies.

Russell 2000® Index. The Russell 2000® Index is comprised of equity securities of small-capitalization U.S. companies. In general, the securities of small-capitalization companies may be more volatile and may involve more risk than the securities of larger companies.

Nasdaq-100® Index. The Nasdaq-100® Index is comprised of equity securities of the largest U.S. and non-U.S. companies listed on The Nasdaq Stock Market, including companies across all major industry groups except the financial industry. To

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

the extent that the Nasdaq-100® Index is comprised of securities issued by companies in a particular sector, that company’s securities may not perform as well as companies in other sectors or the market as a whole. Also, any component securities issued by non-U.S. companies (including related depositary receipts) are subject to the risks related to investments in foreign markets (e.g., increased price volatility; changing currency exchange rates; and greater political, regulatory, and economic uncertainty).

EURO STOXX 50®. EURO STOXX 50® is comprised of the equity securities of large-capitalization companies in the Eurozone. The securities comprising EURO STOXX 50® are subject to the risks related to investments in foreign markets (e.g., increased price volatility; changing currency exchange rates; and greater political, regulatory, and economic uncertainty), and are significantly affected by the European markets and actions of the European Union.

The COVID-19 pandemic has at times led to significant volatility and negative returns in the financial markets. These market conditions have impacted the performance of the Indexes to which the Index Options are linked, as well as securities held by the Variable Options. If these market conditions continue or reoccur, and depending on your individual circumstances (e.g., your selected Allocation Options and the timing of any Purchase Payments, transfers, or withdrawals), you may experience (perhaps significant) negative returns under the Contract. The COVID-19 pandemic has contributed to an uncertain and evolving economic environment. The impact of the COVID-19 pandemic and other interrelated factors (e.g., changes in interest rates, rising inflation, actions of governmental authorities) on the economic environment cannot be predicted with certainty, but they could negatively affect the returns of an Index and the level of Caps, and other product features, and the overall performance of your Contract. The military invasion of Ukraine initiated by Russia in February 2022 and the resulting response by the United States and other countries have led to economic disruptions, as well as increased volatility and uncertainty in the financial markets. It is not possible to predict the ultimate duration and scope of the conflict, or the future impact on U.S. and global economies and financial markets. The performance of the Indexes to which the Index Options are linked, as well as securities held by the AZL Government Money Market Fund, may be adversely affected. This risk could be higher for Indexes with exposure to European or Russian markets, including EURO STOXX 50®. Depending on your individual circumstances (e.g., your selected Index Options and the timing of any Purchase Payments, transfers, or withdrawals), you may experience (perhaps significant) negative returns under the Contract. You should consult with a Financial Professional about how the recent market conditions may impact your future investment decisions related to the Contract, such as purchasing the Contract or making Purchase Payments, transfers, or withdrawals, based on your individual circumstances. |

Risk of Negative Returns

The Variable Options do not provide any protection against negative returns. You can lose principal and previous earnings if you allocate Purchase Payments or transfer Contract Value to the Variable Options and such losses could be significant.

If you allocate Purchase Payments or transfer Contract Value to an Index Option, negative Index Returns may cause Performance Credits to be negative after application of the 10% or 30% Buffer. Ongoing deductions we make for Contract fees and expenses could also cause amounts available for withdrawal to be less than what you invested even if Index performance has been positive. You can lose principal and previous earnings if you allocate Purchase Payments or transfer Contract Value to the Index Options, and such losses could be significant. The maximum potential negative Performance Credit is based on the Buffer. If the Buffer is 10% the maximum negative Performance Credit is ‑90%, and if the Buffer is 30% the maximum negative Performance Credit is ‑70%. Such losses will be greater if you take a withdrawal (including any financial adviser fees that you choose to have us pay from this Contract) that is subject to a withdrawal charge, or is a deduction of Contract fees and expenses.

The Daily Adjustment is how we calculate Index Option Values on Business Days other than the Index Effective Date or an Index Anniversary. The Variable Options are not subject to the Daily Adjustment. The Daily Adjustment can affect the amounts available for withdrawal, Performance Locks, annuitization, payment of the death benefit, and the Contract Value used to determine the contract maintenance charge and Charge Base for the product fee. The Daily Adjustment can be less than the Cap even if the current Index return during an Index Year is greater than the Cap. In addition, even though the current Index return during an Index Year may be positive, the Daily Adjustment may be negative due to changes in Proxy Value inputs, such as volatility, dividend yield, and interest rate. The Daily Adjustment is generally negatively affected by:

•

interest rate decreases,

•

dividend rate increases,

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

•

poor market performance, and

•

increases in the expected volatility of Index prices.

If you take a withdrawal from an Index Option before the Index Anniversary, you could lose principal and previous earnings because of the Daily Adjustment even if Index performance is positive on that day or has been positive since the beginning of the Index Year. If the current Index return during the Index Year is negative, the Daily Adjustment could result in losses greater than the protection provided by the 10% or 30% Buffer. In extreme circumstances the Daily Adjustment could result in a loss beyond the protection of the Buffer, but it cannot result in a total loss of -100%. Such losses will be greater if the amount withdrawn (including any financial adviser fees that you choose to have us pay from this Contract) is also subject to a withdrawal charge, or is a deduction of Contract fees and expenses.

Managed Volatility Variable Option Risk

As described in more detail in the Variable Options’ prospectuses, certain Variable Options affiliated with us employ a managed volatility strategy that is intended to reduce the Variable Option’s overall volatility and downside risk. A Variable Option’s managed volatility strategy can negatively impact the value of your Contract and its benefits. During rising markets, the hedging strategies employed to manage volatility could result in your Contract Value rising less than would have been the case if you had been invested in a Variable Option without a managed volatility strategy. In addition, the cost of these hedging strategies may negatively impact performance. Variable Options that employ a managed volatility strategy are identified in Appendix G – Variable Options Available Under the Contract.

Risks Associated with Calculation of Performance Credits

We calculate Performance Credits each Index Year on the Index Anniversary. Because we calculate Index Returns only on a single date in time, you may experience negative or flat performance even though the Index you selected for a given Crediting Method experienced gains through some, or most, of the Index Year. If you allocate Purchase Payments or transfer Contract Value to the Index Options the Caps limit positive returns and could cause performance to be lower than it would otherwise have been if you invested in a mutual fund designed to track the performance of the applicable Index, or the Variable Options.

The Index Options do not directly participate in the returns of the Indexes or the Indexes’ component securities, and do not receive any dividends payable on these securities. Index returns would be higher if they included the dividends from the component securities. The past ten years of actual average of the annual Index returns without and with dividends would have been as follows:

[To be updated by amendment]

| January 1, 2012 through December 31, 2022 |

| | | | |

Returns without dividends | | | | |

| | | | |

Caps may be adjusted annually on the Index Anniversary and may vary significantly from year to year. Changes to Caps may significantly affect the amount of Performance Credit you receive. For more information, see the “Changes to Caps” discussion later in this section.

The Crediting Methods only capture Index Values on one day each year, so you will bear the risk that the Index Value might be abnormally low on these days.

Risks Associated with Performance Locks

If a Performance Lock is executed:

•

You will no longer participate in Index performance, positive or negative, for the remainder of the Index Year for the locked Index Option. This means that under no circumstances will your Index Option Value increase during the remainder of the Index Year for a locked Index Option, and you will start a new Index Option on the next Index Anniversary that occurs on or immediately after the Lock Date.

•

You will not receive a Performance Credit on any locked Index Option.

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

•

We use the Daily Adjustment calculated at the end of the current Business Day on the Lock Date to determine your locked Index Option Value. This means you will not be able to determine in advance your locked Index Option Value, and it may be higher or lower than it was at the point in time you requested a manual Performance Lock, or that your Index Option reached its target for an automatic Performance Lock. Through your account on our website you can request a Performance Lock based on upper and/or lower targets you set using Index Option Value returns.

•

If a Performance Lock is executed when your Daily Adjustment has declined, you will lock in any loss. It is possible that you would have realized less of a loss or no loss if the Performance Lock occurred at a later time, or if the Index Option was not locked.

We will not provide advice or notify you regarding whether you should execute a Performance Lock or the optimal time for doing so. We will not warn you if you execute a Performance Lock at a sub-optimal time. We are not responsible for any losses related to your decision whether or not to execute a Performance Lock. |

Substitution of an Index

There is no guarantee that the Indexes will be available during the entire time that you own your Contract. Once we add an Index to your Contract, we cannot remove it without simultaneously substituting it. If we substitute a new Index for an existing Index, the performance of the new Index may be different and this may affect your ability to receive positive Performance Credits. We may substitute a new Index for an existing Index if:

•

the Index is discontinued,

•

we are unable to use the Index because, for example, changes to an Index make it impractical or expensive to purchase derivative hedging instruments to hedge the Index, or we are not licensed to use the Index, or

•

the method of calculation of the Index Values changes substantially, resulting in significantly different Index Values and performance results. This could occur, for example, if an Index altered the types of securities tracked, or the weighting of different categories of securities.

If we add or substitute an Index, we first seek any required regulatory approval from the New York Department of Financial Services and then provide you with written notice. We also provide you with written notice if an Index changes its name. Index substitutions can occur either on an Index Anniversary or during an Index Year. If we substitute an Index during an Index Year we will combine the return of the previously available substituted Index from the prior Index Anniversary to the substitution date with the return of the new Index from the substitution date to the next Index Anniversary. If we substitute an Index during an Index Year:

•

we do not change the Charge Base we use to calculate the product fee, and

•

the Buffers and Caps for the substituted Index will apply to the new Index. We do not change the Buffers or Caps that were in effect on the prior Index Anniversary.

Changes to Caps associated with the new Index, if any, may occur at the next regularly scheduled Index Anniversary or on later Index Anniversaries. Depending on the constitution of the substituted Index, the volatility of its investments, and our ability to hedge the Index’s performance, we may determine, in our discretion, to increase or decrease renewal Caps associated with the new Index. However, we would not implement any change to reflect this difference until the next Index Anniversary after the substitution. The substitution of an Index during an Index Year may result in an abnormally large change in the Daily Adjustment on the day we substitute the Index.

The selection of a substitution Index is in our discretion; however, it is anticipated that any substitute Index will be substantially similar to the Index it is replacing and we will substitute any equity Index with a broad-based equity index.

Changes to Caps

You can only transfer Index Option Value to a Variable Option on a sixth Index Anniversary. |

The 10% and 30% Buffers for the currently available Index Options do not change. However, if we add a new Index Option to your Contract, we establish the Buffer for it on the date we add the Index Option to your Contract. For a new Index Option the minimum Buffer is 5%.

We established the initial Caps on the Index Effective Date and they cannot change until the next Index Anniversary.We can change the renewal Caps for a Contract on each Index Anniversary subject to the guaranteed minimums, in our discretion. We will send you a letter at least 30 days before each Index Anniversary. This letter advises you that current Caps are expiring, and that renewal rates for the next Index Anniversary will be available for your review. The Index

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

Anniversary letter also reminds you of your opportunity to transfer Variable Account Value to the Index Options, or reallocate your Index Option Values on the upcoming Index Anniversary. On each Index Anniversary you have the option of remaining allocated to your current Index Options at the renewal Caps that we set on the next Index Anniversary, or transferring to another permitted Allocation Option, subject to the limitations on transfers from an Index Option to a Variable Option. At least seven calendar days before each Index Anniversary we publish renewal rates for your review in your account on our website, and on our public website at allianzlife.com/indexratesny, or call (800) 624-0197. If you do not review renewal change information when it is published, or take no action to transfer to another permitted Allocation Option, you will remain allocated to your current Index Options and will automatically become subject to the renewal Caps until the next Index Anniversary.

You risk the possibility that the renewal Caps you receive may be less than you would find acceptable. If you do not find the renewal rates acceptable, you must give us transfer instructions no later than the end of the Business Day on the Index Anniversary (or the next Business Day if the anniversary is a non-Business Day) or you will be subject to these renewal Caps for the next Index Year. Other than on a sixth Index Anniversary when you can transfer Index Option Value to the Variable Options, when your renewal rates change the only options available to you are to transfer Index Option Value between Index Options, or take a full withdrawal (which may be subject to a withdrawal charge).

Initial and Renewal Caps may vary significantly depending upon a variety of factors, including:

•

our hedging strategies and investment performance,

•

the availability of hedging instruments,

•

the amount of money available to us through Contract fees and expenses to purchase hedging instruments,

•

your Index Effective Date,

•

the level of interest rates,

•

utilization of Contract benefits by Owners, and

•

our profitability goals.

Due to a combination of factors, including potential changes in interest rates and other market conditions (e.g. rising inflation), the current economic environment is evolving. The future impact on initial and renewal Caps cannot be predicted with certainty. The effect of a change in interest rates or other market conditions may not be direct or immediate. There may be a lag in changes to Caps. Interest rates could increase. In a rising interest rate environment, increases in Caps, if any, may be substantially slower than increases in interest rates.

We manage our obligation to provide Performance Credits in part by trading call and put options, and other derivatives on the available Indexes. The costs of the call and put options and other derivatives vary based on market conditions, and we may adjust future renewal Caps to reflect these cost changes. The primary factor affecting the differences in the initial Caps for newly issued Contracts and renewal rates for existing Contracts is the difference in what we can earn from these investments for newly issued Contracts versus what we are earning on the investments that were made, and are being held to maturity, for existing Contracts. In some instances we may need to reduce initial and renewal Caps, or we may need to substitute an Index. You bear the risk that we may reduce Caps, which reduces your opportunity to receive positive Performance Credits.

Historical information on the Caps is provided in Appendix C. This information is for historical purposes only and is not a representation as to future Caps. |

Investment in Derivative Hedging Instruments

The Index Options are supported by bonds and other fixed income securities which are also used to support the Contract guarantees, cash, and derivative hedging instruments used to hedge the movements of the applicable Index.

At Contract issue, we invested a substantial majority of the initial Contract Value allocated to the Index Options in fixed income securities, with most of the remainder invested in derivative hedging instruments. The derivative hedging instruments are purchased to track and hedge Index movements and support our obligations with regard to the Index Options. The derivative hedging instruments we purchase include put options, call options, futures, swaps, and other derivatives.

The Index Options move assets in the unregistered separate account between a book value subaccount and a market value subaccount during the Index Year based on Index performance. We typically transfer assets between the subaccounts if

Allianz Index Advantage® New York Variable Annuity Prospectus – May 1, 2023

there is a 10% incremental change in year-to-date Index performance. For the Index Performance Strategy this starts at a -10% decrease in the market; for the Index Protection NY Strategy, this starts at a -30% decrease in the market. We monitor year-to-date Index performance daily and change allocations daily if needed based on this 10% increment. For more information on our unregistered separate account backing the Index Options, see section 12, Other Information – Our Unregistered Separate Account.

We currently limit our purchase of derivative hedging instruments to liquid securities. However, like many types of derivative hedging instruments, these securities may be volatile and their price may vary substantially. In addition, because we pay Performance Credits regardless of the performance of derivative hedging instruments we purchase, we may incur losses on hedging mismatches or errors in hedging. We may incur additional costs if the costs of our hedging program increase due to market conditions or other factors. Our overall experience with hedging securities may affect renewal Caps for existing Contracts.

Certain Variable Options may also invest in derivative securities. For more information on these investments, see the Variable Option prospectuses.

Risks of Deducting Financial Adviser Fees from the Contract

If you have an investment adviser and want to pay their financial adviser fees from this Contract, you can instruct us to withdraw the fee from your Contract and pay it to your adviser. Once authorized by you, the investment adviser requests each fee payment by submitting a letter of instruction that includes the fee amount. The deduction of financial adviser fees is in addition to this Contract’s fees and expenses, and the deduction is treated the same as any other withdrawal under the Contract. As such, withdrawals to pay financial adviser fees will be subject to withdrawal charges, will reduce the Contract Value and Guaranteed Death Benefit Value (perhaps significantly), and may be subject to income taxes (including a 10% additional federal tax if you are younger than age 59 1∕2). Please consult with your Financial Professional before requesting us to pay financial adviser fees from this Contract rather than from other assets you may have.

Our Financial Strength and Claims-Paying Ability

We make Annuity Payments, pay death benefits, and apply Performance Credits from our general account. Our general account assets are subject to claims by our creditors, and any payment we make from our general account is subject to our financial strength and claims-paying ability.

The assets in our unregistered separate account, Separate Account IANY are also subject to claims by our creditors. You can obtain information on our financial condition by reviewing our financial statements in this prospectus, and are also subject to our financial strength and claims paying ability. For more information see section 12, Other Information – Our Unregistered Separate Account.