Exhibit (a)(l)(K)

| Gregory M. Shepard |

| 7028 Portmarnock Place |

| Bradenton, Florida 34202 |

April 10, 2013

Mr. Donald H. Nikolaus

President & Chief Executive Officer

Donegal Group, Inc.

1195 River Road

Marietta, Pennsylvania 17547

| Re: | Request for Explanation of Extraordinarily High Level of Option Grants |

Dear Mr. Nikolaus:

As you know, I have been a longstanding shareholder of Donegal Group, Inc. (“Donegal”) and currently hold 3,602,900 shares of Class A and 397,100 shares of Class B stock.

I am very disappointed that you have continued to issue options, especially to yourself and the other executives and directors, including Donegal Mutual Insurance Company directors, in such an outrageously high manner in comparison to even the industry peer companies identified by Donegal. These option grants are potentially highly dilutive to the shareholders.

I would like you to explain to the shareholders at the upcoming Annual Meeting on April 18, 2013, why you believe this was in the shareholders’ best interest, given the dismal price performance of Donegal’s Class A shares and Class B shares over the last seven years.

I attach an analysis that was compiled based on publicly available data by Duff & Phelps. I ask you to distribute this letter to the shareholders at the annual meeting and to discuss and justify your actions.

| Very truly yours, | |

| /s/ Gregory M. Shepard | |

| Gregory M. Shepard |

| To:Gregory M. Shepard |

| From:Duff & Phelps, LLC | |

| Subject:Analysis of Options Grants of Donegal Group, Inc, | |

| Date:April 10, 2013 | |

Dear Mr. Shepard:

We were engaged to perform an analysis of the option grants made by Donegal Group (“Donegal”). Listed below is a summary of our findings. Please refer to the attached appendix which has schedules supporting our analysis.

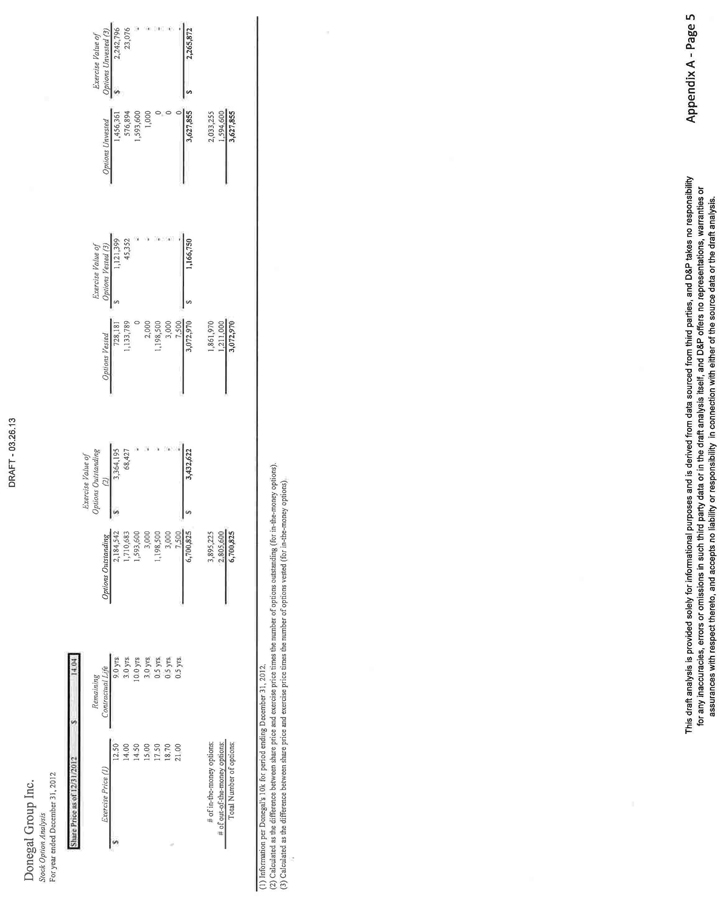

I. Current Options

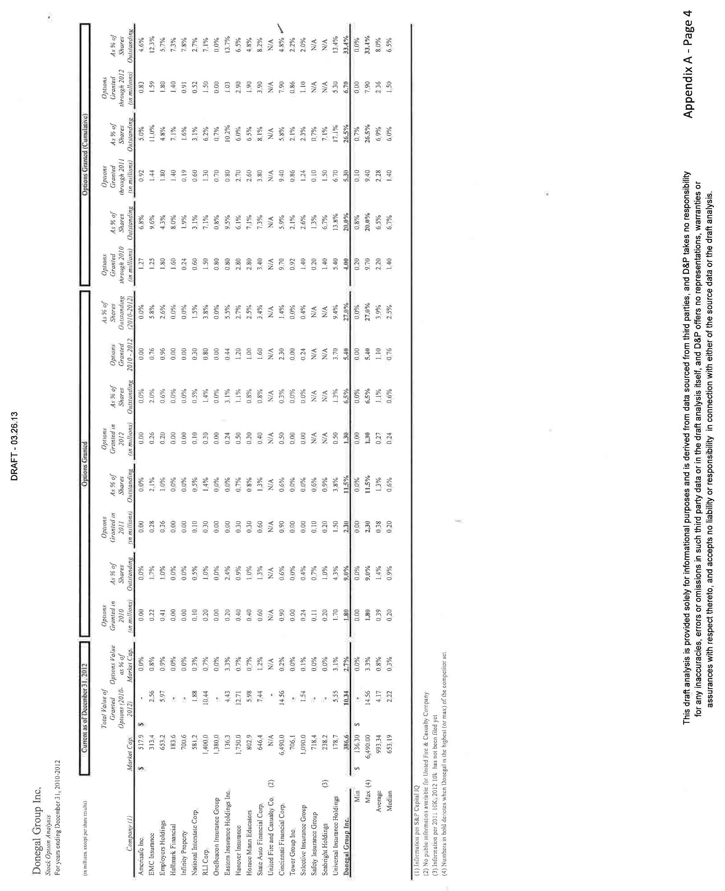

| - | Donegal has 3.1 million Vested options as of 12/31/2012, which is in the upper quartile of the group of selected guideline public companies (“GPCs”) |

| - | Donegal has 3.6 million Unvested options as of 12/31/2012, which is the highest number in the group of selected GPCs |

| - | The number of Donegal’s in-the-money options is equal to 3.9 million, which equates to a $3.4 million liability, if exercised |

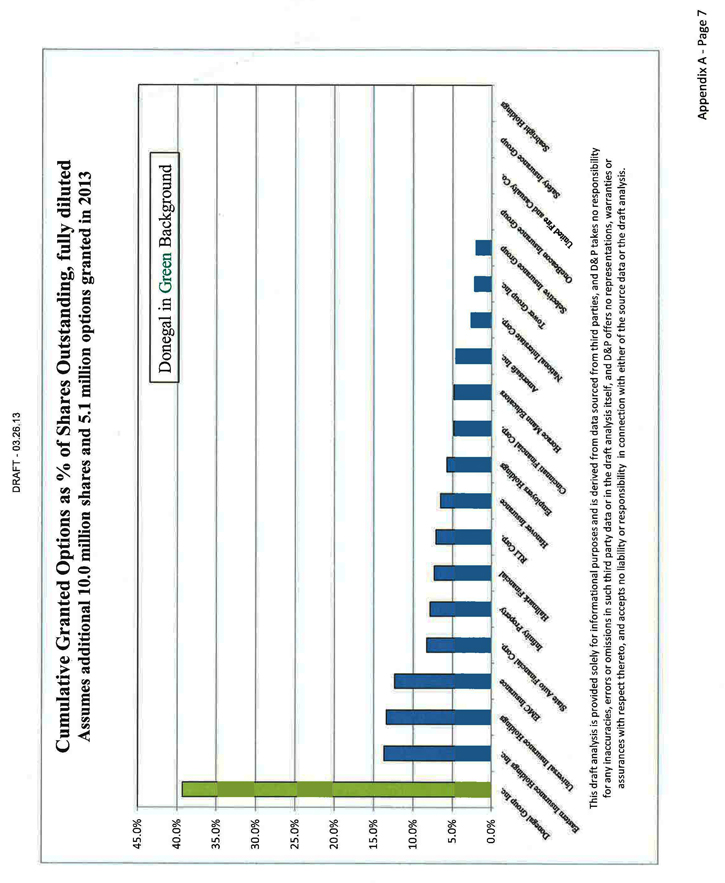

| - | Relative to GPC, Donegal: |

| o | has the highest number of Options Granted with 1.8 million, 2.3 million and 1.3 million, in 2010, 2011 and 2012, respectively |

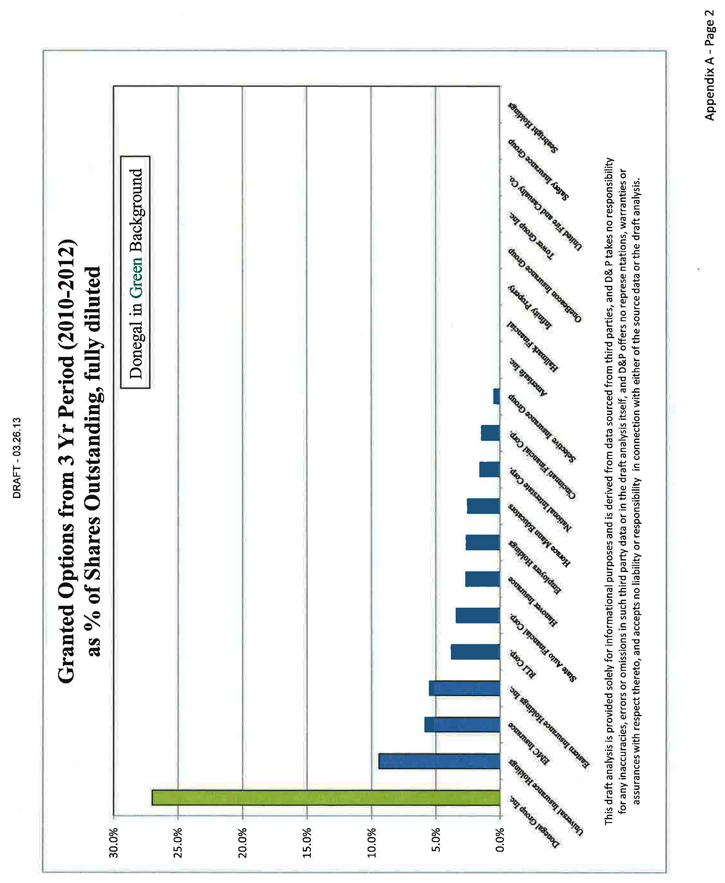

| o | has the highest number of Options Granted in relation to Total Number of Shares Outstanding, with 9.0%, 11.5% and 6.5% in 2010, 2011 and 2012, respectively, all of which are at least 6.0x the average of the GPCs |

| o | has the highest number of Options Granted from 2010-2012 in relation to Total Shares Outstanding at 27.0% |

This analysis is provided solely for informational purposes and is derived from data sourced from third parties, and D&P takes no responsibility for any inaccuracies, errors or omissions in such third party data or in the analysis itself, and D&P offers no representations, warranties or assurances with respect thereto, and accepts no liability or responsibility in connection with either of the source data or the analysis.

Memo re: Donegal

Page 2 of 3

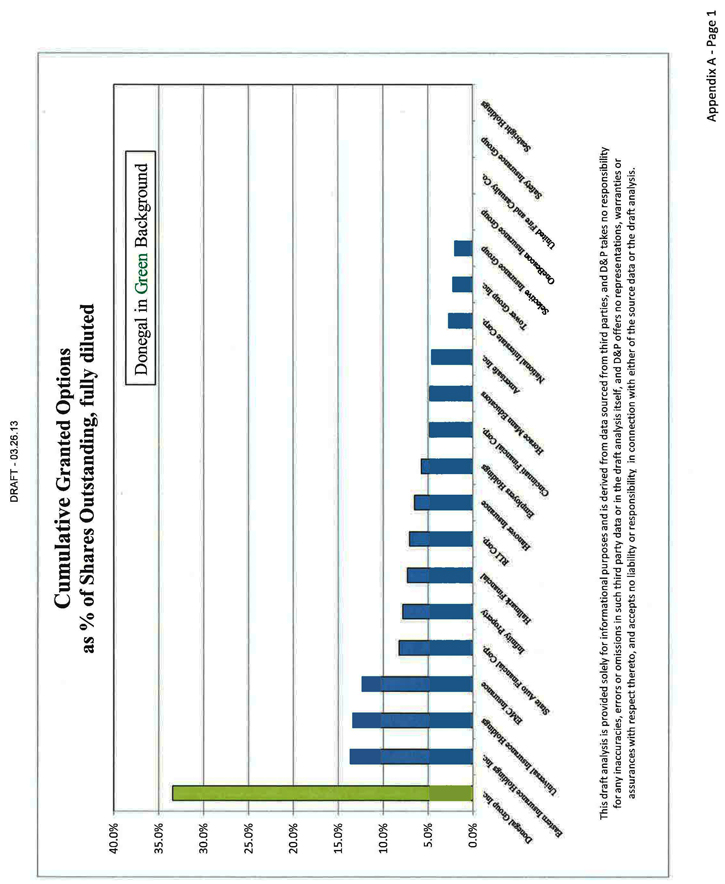

| o | has the highest number of Options Granted (Cumulative) in relation to the Total Number of Shares Outstanding, with 20.0%, 26.5% and 33.4% in 2010, 2011 and 2012 |

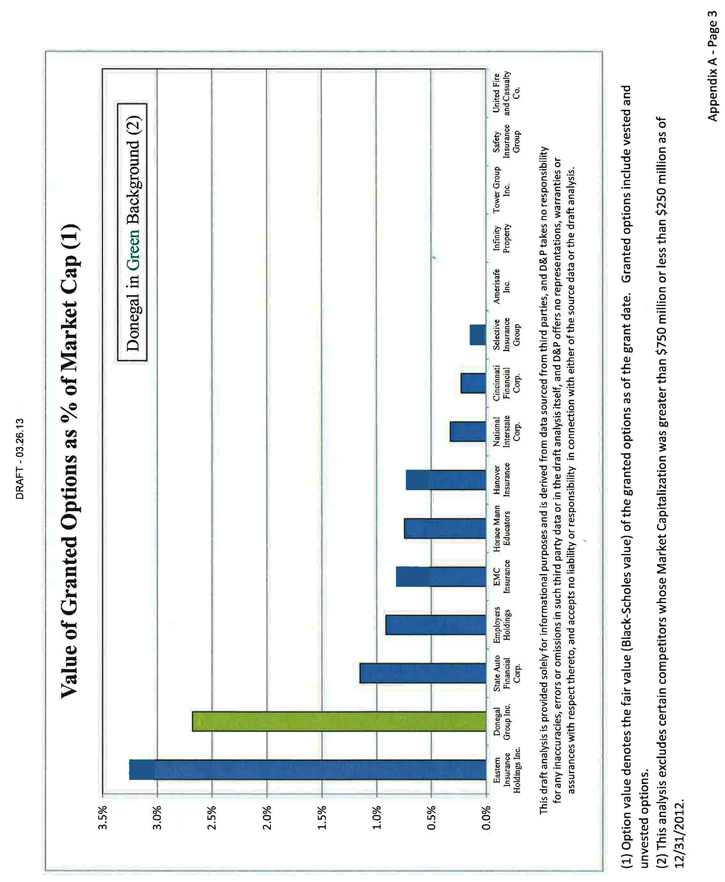

| o | is the highest in Option Value (calculated as Fair Value as of the date of grant) for all options granted from 2010-2012 as % of Market Capitalization (2.7%)1 |

| o | is the highest in its group of GPCs in Total Value of Options at Grant Date in 2012, with $10.3 million in value 2 |

| o | is in the top of the upper quartile in its group of GPCs in Options Granted (Cumulative), with 4.0 million, 5.3 million and 6.70 million options outstanding in 2010, 2011 and 2012, respectively. |

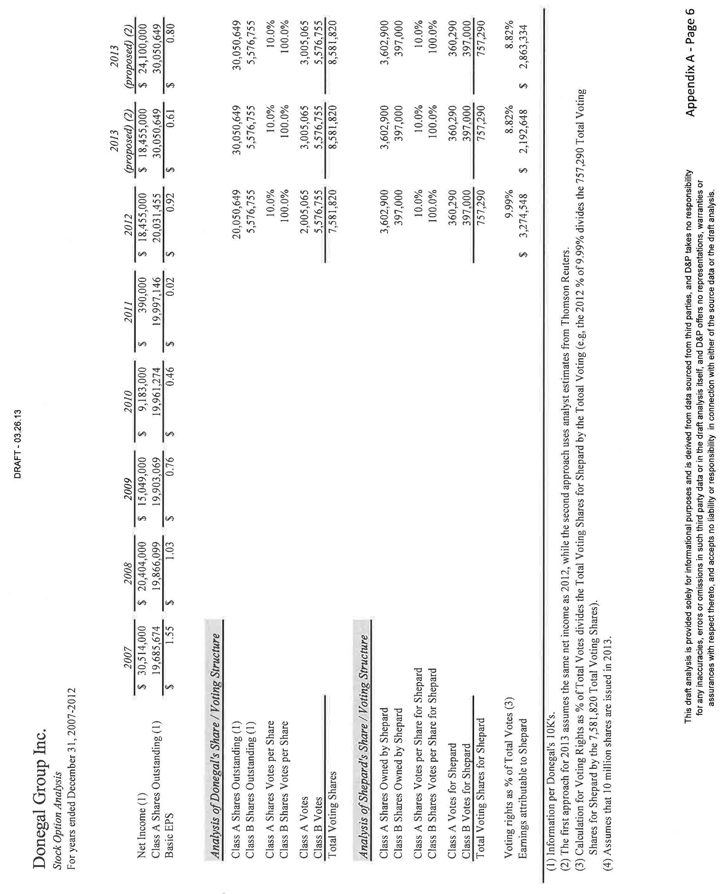

II. Earnings Dilution

| - | The analysis in Section II assumes that the additional 10 million shares are authorized and issued in 2013. |

| - | We assume two different Net Income Forecasts for 2013. |

| o | If we assume that 2013 Net Income remains unchanged from 2012 at $18.5: |

| ■ | The increase in Class A Shares Outstanding would dilute EPS from $0.91 in 2012 to $0.61 in 2013 |

| ■ | This increase in Class A Shares Outstanding would also result in decreased earnings attributable to Mr. Shepherd from $3.27 million in 2012 to $2.19 million in 2013 |

| o | If we assume that 2013 Net Income increased to $24.1 million (based on a forecast from Thomson Reuters): |

| ■ | Theincrease in Total Number of Class A Shares Outstanding would dilute EPS from $0.91 in 2012 to $0.79 in 2013 |

| 1 | This analysis excludes certain competitors whose Market Capitalization was less than $250 million or greater than $750 million as of 12/31/2012. |

| 2 | Id. |

This analysis is provided solely for informational purposes and is derived from data sourced from third parties, and D&P takes no responsibility for any inaccuracies, errors or omissions in such third party data or in the analysis itself, and D&P offers no representations, warranties or assurances with respect thereto, and accepts no liability or responsibility in connection with either of the source data or the analysis.

Memo re: Donegal

Page 3 of 3

| ■ | This increase in Class A Shares Outstanding would also result in decreased earnings attributable to Mr. Shepherd from $3.27 million in 2012 to $2.86 million in 2013 |

III. Voting Dilution

| - | If the 10 million additional authorized shares are issued in 2013: |

| o | The number of Total Number of Class A Shares Outstanding increases to 30.05 million (approximately 50% increase) |

| o | The increase in Class A Shares Outstanding dilutes Mr. Shepherd’s voting rights from 9.99% in 2012 to 8.8% in 2013 |

| o | This increase in Class A Shares Outstanding would also dilute the voting rights of the average shareholder by roughly 11.6% (1 less 2012 Voting Shares of 7.58 million divided by 2013 Voting Shares of 8.58 million) |

This analysis is provided solely for informational purposes and is derived from data sourced from third parties, and D&P takes no responsibility for any inaccuracies, errors or omissions in such third party data or in the analysis itself, and D&P offers no representations, warranties or assurances with respect thereto, and accepts no liability or responsibility in connection with either of the source data or the analysis.