Exhibit 13.1

Commission File No. 0-15261

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES AND EXCHANGE ACT OF 1934

For the Year Ended December 31, 2009

BRYN MAWR BANK CORPORATION

BRYN MAWR

BANK CORPORATION

2009 ANNUAL REPORT

Strong. Stable. Secure.

Investing for Growth

A rich tradition of investing in our franchise and our future. Recent investments over the last five years have included: January 2004 — Opened the Newtown Square office. February 2005 — Formed mortgage joint venture with Keller Williams. March 2005 — Opened the Exton office. September 2006 — Established Bryn Mawr Leasing Company. January 2007 — Opened the Ardmore office. May 2007 — Formed the Private Banking Group. June 2008 — Major renovations of the Wayne office. July 2008 — Acquired Lau Associates LLC, Wilmington, DE. November 2008 — Established The Bryn Mawr Trust Company of Delaware in Wilmington, DE. January 2009 — Opened the West Chester Regional Banking Center. May 2009 — Established BMT Asset Management. November 2009 — Signed agreement to acquire First Keystone Financial. December 2009 — Major renovations of the Paoli office.

ANNUAL MEETING The Annual Meeting of Shareholders of Bryn Mawr Bank Corporation will be held at Saint Davids Golf Club, 845 Radnor Street Road, Wayne, PA 19087, on Wednesday, April 28, 2010, at 11:00 a.m.

STOCK LISTING Bryn Mawr Bank Corporation common stock is traded over-the-counter and is listed on the NASDAQ Global Market under the symbol BMTC.

FORM 10-K A copy of the Corporation’s Form 10-K, including financial statement schedules as filed with the Securities and Exchange Commission, is available on our website www.bmtc.com or upon written request to the Corporate Secretary, Bryn Mawr Bank Corporation, 801 Lancaster Avenue, Bryn Mawr, Pennsylvania 19010.

EQUAL EMPLOYMENT OPPORTUNITY The Corporation continues its commitment to equal opportunity employment and does not discriminate against minorities or women with respect to recruitment, hiring, training, or promotion. It is the policy of the Corporation to comply voluntarily with the practices of Affirmative Action.

This discussion contains forward-looking statements. Please see the section entitled “Special Cautionary Notice Regarding Forward Looking Statements” in the enclosed Annual Report to Shareholders, and the section entitled “Risk Factors” in the enclosed Form 10-K, for discussions of the risks, uncertainties and assumptions associated with these statements.

2009 Annual Report

Financial highlights

CONSOLIDATED FINANCIAL HIGHLIGHTS

dollars in thousands, except per share data

| | | | | | | | | | | | | | | |

| | | 2009 | | | 2008 | | | CHANGE | |

FOR THE YEAR | | | | | | | | | | | | | | | |

Net interest income | | $ | 40,793 | | | $ | 37,138 | | | $ | 3,655 | | | 9.8 | % |

Net interest income after loan and lease loss provision | | | 33,909 | | | | 31,542 | | | | 2,367 | | | 7.5 | % |

Non-interest income | | | 28,470 | | | | 21,472 | | | | 6,998 | | | 32.6 | % |

Non-interest expenses | | | 46,542 | | | | 38,676 | | | | 7,866 | | | 20.3 | % |

Income taxes | | | 5,500 | | | | 5,013 | | | | 487 | | | 9.7 | % |

Net income | | | 10,337 | | | | 9,325 | | | | 1,012 | | | 10.9 | % |

AT YEAR-END | | | | | | | | | | | | | | | |

Total assets | | $ | 1,238,821 | | | $ | 1,151,346 | | | $ | 87,475 | | | 7.6 | % |

Total portfolio loans and leases | | | 885,739 | | | | 899,577 | | | | (13,838 | ) | | -1.5 | % |

Total deposits | | | 937,887 | | | | 869,490 | | | | 68,397 | | | 7.9 | % |

Shareholders’ equity | | | 103,936 | | | | 92,413 | | | | 11,523 | | | 12.5 | % |

Tangible common equity | | | 92,214 | | | | 82,055 | | | | 10,159 | | | 12.4 | % |

Wealth assets under management, administration and supervision | | | 2,871,143 | | | | 2,146,399 | | | | 724,744 | | | 33.8 | % |

PER COMMON SHARE | | | | | | | | | | | | | | | |

Basic earnings per common share | | $ | 1.18 | | | $ | 1.09 | | | $ | 0.09 | | | 8.3 | % |

Diluted earnings per common share | | | 1.18 | | | | 1.08 | | | | 0.10 | | | 9.3 | % |

Dividends declared | | | 0.56 | | | | 0.54 | | | | 0.02 | | | 3.7 | % |

Book value | | | 11.72 | | | | 10.76 | | | | 0.96 | | | 8.9 | % |

Tangible book value | | | 10.40 | | | | 9.55 | | | | 0.85 | | | 8.9 | % |

Closing price | | | 15.09 | | | | 20.10 | | | | (5.01 | ) | | -24.9 | % |

SELECTED RATIOS | | | | | | | | | | | | | | | |

Return on average assets | | | 0.88 | % | | | 0.89 | % | | | | | | | |

Return on average shareholders’ equity | | | 10.55 | % | | | 10.01 | % | | | | | | | |

Tax equivalent net interest margin | | | 3.70 | % | | | 3.84 | % | | | | | | | |

Allowance for loan & lease losses as a % of loans & leases | | | 1.18 | % | | | 1.15 | % | | | | | | | |

Tangible common equity to tangible assets | | | 7.51 | % | | | 7.13 | % | | | | | | | |

1

Letter to shareholders

Dear Shareholders and Friends,

While almost all financial institutions had sharp declines in income and many registered losses, I’m pleased to report that Bryn Mawr Bank Corporation, and our chief subsidiary, The Bryn Mawr Trust Company, had an increase in earnings of 10.9% and remained one of the most profitable banks in the nation.

Let’s review some of the highlights of this past year.

| • | | The biggest news in 2009 was the signing of a definitive agreement to purchase First Keystone Financial, Inc. of Media, Pennsylvania. First Keystone has a long and rich history in Delaware County, and has deep relationships with its clients. With an expected closing by this July, Bryn Mawr Trust will now be the largest community bank in the western suburbs of Philadelphia, with 17 full-service branch locations and approximately $1.7 billion in banking assets. |

| • | | Our Wealth Management Division saw its assets under management and supervision grow sharply from $1.9 billion, in March 2009, to just under $2.9 billion by year’s end. Lau Associates, the high-end financial planning and investment management firm in Wilmington, Delaware which we acquired in 2008, continued to play an important role in our wealth growth strategy. |

2

2009 Annual Report

| • | | Our new Bryn Mawr Trust Company of Delaware gathered over $400 million of new wealth assets during the year. We are projecting sustained growth with this important initiative, which takes advantage of the special trust statutes available in only Delaware and few other states. |

| • | | During the year, we started BMT Asset Management, which replaced our existing brokerage business. Professionals from UBS, Morgan Stanley, and other investment firms have been recruited, and we have attracted well over $100 million of new wealth assets to manage. |

| • | | In January of 2009, we opened a large regional banking office in West Chester, staffed not only with an experienced team of retail bankers, but also with a business lending group and a wealth officer. With over $21 million of new deposits, we have far exceeded our original projections. When we conclude the merger with First Keystone Bank, we will have five offices in Chester County, still one of the fastest growing areas in Pennsylvania. |

| • | | BMT Mortgage Company had a stellar year as low interest rates created an active re-financing market. Over $250 million of new mortgage loans were closed, most of which were sold to Fannie Mae while we retained the servicing of these loans. At the end of 2009, we were servicing over half a billion dollars of loans for Fannie Mae. |

Despite this strong record of accomplishments in 2009, we have many challenges ahead of us. Although we expect business conditions to remain difficult, the Bank is prepared. Bryn Mawr Trust is well-capitalized, profitable, and uniquely well-positioned to serve our wealth and banking clients. We have clearly defined goals and strategies to grow the Bank and to remain highly profitable.

The Board of Directors, the management team, and I thank you for your support of the Bank this past year. In a difficult environment we have performed well. We are hopeful that through our continued growth in profitability, banking assets, and wealth assets that our stock price will show improvement in 2010.

As always, please feel free to call me with any questions or comments. My direct phone line is610-581-4800. Thank you.

Best wishes,

Ted Peters

Chairman and Chief Executive Officer

3

Year in review

“The current economic turmoil has given us a wonderful opportunity to increase our market share and to geographically expand our franchise.” – TED PETERS

In 2009, the financial services industry was in crisis and faced many significant problems and challenges. It would have been hard for anyone to imagine that there would be opportunities for success amidst all of this turmoil. However, there were opportunities for success, and the Bryn Mawr Trust team was able to recognize and capitalize on many of them. As a result, while many other institutions struggled, we had a very successful year. We are pleased to share with you some of our most significant accomplishments.

Seizing Opportunities

The Wealth Management Division had a fantastic year, with assets growing 33.8% from year-end 2008. While the entire Division contributed to this outstanding performance, a big part of the success was the result of two new initiatives which generated significant growth. The BMT Asset Management unit was formed in the second quarter of 2009, by hiring well-known, experienced investment professionals who developed significant new investment relationships of approximately $100 million in a very short period of time. We made additions to this staff in the fourth quarter and we are very excited about their future growth potential. In its first full year of operation, The Bryn Mawr Trust Company of Delaware grew to more than $400 million in wealth assets. This subsidiary allows us to serve as a corporate fiduciary under Delaware statutes, a significant competitive advantage, and we expect it to be a meaningful contributor to our long-term growth.

Professionals in the Wealth Management Division have long been sought out for their advice, opinions and comments on a variety of wealth and financial management topics. That trend continued in 2009, and our professionals were interviewed extensively by the news media including:The Wall Street Journal, FOX Business News, CNBC, Bloomberg News,The Philadelphia Inquirer, The American Banker and thePhiladelphia Business Journal.

Our strong brand enabled us to attract many new clients in 2009. To increase our brand awareness and promote our Wealth Management capabilities, we launched a mass media campaign using radio, print and outdoor advertising. We were very satisfied with our promotional efforts and intend to continue these strategies in 2010.

Above: Wealth Management Division, 10 S. Bryn Mawr Avenue, Bryn Mawr, PA; Opposite page (left to right): Francis J. Leto, Executive V.P., Wealth Management Division, Karin Kinney, Senior V.P., Philanthropic Services Group; Richard K. Cobb, Jr., Senior V.P., BMT Asset Management, Drew Camerota, Senior V.P., BMT Asset Management, Bill Thorkelson, Senior V.P., Investment Management, Charles F. Ward, Senior V.P., BMT Asset Management.

4

2009 Annual Report

Once again, Retail Banking had another strong year, growing our deposits by almost 8.0% over the prior year. The branch banking staff concentrated their selling efforts on generating small business accounts, cash management sales and deep consumer banking relationships. Consumer banking promotions required new checking accounts with direct deposit, online banking and eStatements in order to qualify for the promotional offers. Our solid reputation was a great benefit as many clients, concerned with the financial crisis, chose to develop a relationship with a “Strong, Stable and Secure” financial institution.

The new West Chester Regional Banking Center, which opened in January 2009, contributed to our strong deposit growth with over $21 million in deposits at year end. To strengthen our ties with the business community, we announced the formation of a Business Advisory Board for Chester County in June 2009. Advisory Board members will meet with senior managers from the Bank on emerging trends, issues and opportunities to enhance Bryn Mawr Trust’s well-established role as a leading business and community partner. The board is comprised of leaders from the area’s business and professional community, including; Anthony Giannascoli, Esq., Giannascoli & Associates, PC, Kevin Holleran, Esq., Gawthrop Greenwood, PC, Senya D. Isayeff, Alliance Environmental Systems, Inc., Valerie Jester, Brandywine Capital Associates, Inc., James MacFadden, Century 21 Alliance, Mary Ellen “Mell” Josephs, Executive Director, Student Services, Inc., West Chester University, Eugene Steger, Esq. and CPA, Steger Gowie & Company, Inc. and the Hon. Richard B. Yoder, Immediate Past Mayor of West Chester, Pennsylvania.

The BMT Mortgage Company was a very busy place to be in 2009 as sustained low interest rates created a very beneficial environment for refinancing activity. Revenues for this unit were more than four times 2008 revenues. The Consumer Lending department also saw solid growth, with home equity loans and lines, in our local market area, up more than 15.0% from the prior year.

While many banks stopped making loans, we continued to lend, helping businesses grow and expand. However, overall growth in commercial lending was relatively flat as a result of our desire to limit exposure to certain types of commercial loans. A significant challenge for our lenders was to protect the margin and preserve asset quality, and they did an outstanding job. Our business model, emphasizing risk management and a disciplined approach to growing the Corporation, has served us well, particularly in this difficult financial climate.

5

Community Giving, Activities and Events

As a Community Bank, we truly understand the need to be a part of and support the communities we serve. In good times and bad, we have a tradition of generously supporting a wide variety of charitable, educational, cultural and civic organizations. The entire team finds it very rewarding that we are able to support these worthwhile activities and organizations.

This page, left to right: Kristin M. Green, V.P., Retail Banking, Alison E. Gers, Executive V.P., Retail Banking, Operations, IT and Marketing, Stephen P. Novak, Senior V.P., Retail Banking; Robert J. Ricciardi, Executive V.P. and Chief Credit Policy Officer.

We were especially pleased this year to have been awarded the Regional Community Service Award by the Pennsylvania Association of Community Bankers (PACB). Each year the PACB recognizes community banks for outstanding community activities and support. Bryn Mawr Trust was recognized for establishing the Linda Kahley Ovarian Cancer Walk, to honor the memory of Linda Kahley, a thirty-seven year employee.

Bryn Mawr Trust is committed to making a positive difference in the communities we serve.

Recognizing an Outstanding Career

After nearly 39 years at Bryn Mawr Trust, our distinguished colleague Robert J. Ricciardi has announced his retirement. After his graduation from Villanova University in 1971, Bob started his career as a management trainee in the mortgage department. It didn’t take long for management to recognize Bob’s talent and potential as he was promoted to Loan Officer in December 1972. This was the first of many 1972. This was the first of many promotions for Bob, who is currently Executive Vice President, Chief Credit Policy Officer and Corporate Secretary.

Bob has managed many different functions during his career, including; commercial lending, real estate lending, community banking, human resources, facilities, risk management, the Bank’s title insurance subsidiary, Insurance Counsellors of Bryn Mawr, Inc. and corporate services.

Over the last several years, Bob has also had oversight over branch site acquisitions, construction of new branches and renovation projects for our existing branches and facilities. Bob will continue to provide expertise in this area as a consultant to the Bank.

6

2009 Annual Report

Despite a very heavy workload, Bob also found time to volunteer for many different organizations. He is currently a board member for East Whiteland Township Park and Recreation Board, and is a Trustee of the Hospice and Homecare Foundation, which is part of the Jefferson Home Care Network. He is also a former board member of the Main Line Chamber of Commerce.

When asked about accomplishments at Bryn Mawr Trust that he is most proud of Bob said, “There are many things I’m proud of, but I think the thing I’m most proud of is the number of talented people I’ve hired and worked with over the years who have made Bryn Mawr Trust the outstanding organization it is today”. Bob, we’re proud that you chose to spend your career with us! Bob’s future plans include spending more time with his wife Nancy, his children, five grandchildren, and golf at St. Davids Golf Club. Best wishes from all of us.

This page, left to right: Martin F. Gallagher, Jr., Senior V.P., Commercial Lending, Regina Kemery, Senior V.P., Consumer Lending, Joseph G. Keefer, Executive V.P. and Chief Lending Officer; Myron H. Headen, Senior V.P., BMT Mortgage Company, Thomas DiBiase, V.P., BMT Mortgage Company, Robert J. McLaughlin IV, Senior V.P., BMT Mortgage Company.

Investing in Facilities

In December, we completed major renovations to our Paoli Branch. The remodeling project significantly improved the appearance and functionality of the branch and makes it a much more inviting place to do business. We invite you to visit the branch located at 39 West Lancaster Avenue, Paoli, PA, and see for yourself just how great it looks.

Investing in our Future

In November 2009, we announced our agreement to acquire First Keystone Financial, Inc. and its main operating subsidiary First Keystone Bank. We are very excited that they have agreed to join Bryn Mawr Trust. First Keystone has a rich history of providing exceptional client service and we feel that our combined organization will have many opportunities to grow market share. The proposed merger is subject to regulatory approval and other conditions. For additional details please review the enclosed Annual Report to Shareholders.

Despite the unprecedented financial turmoil our team came together to uncover opportunities for us to succeed and grow. Management, staff, and the Board of Directors are very pleased with our 2009 accomplishments and thank you for your continued support.

Bryn Mawr Trust

Strong. Stable. Secure.

7

CORPORATE INFORMATION

CORPORATE HEADQUARTERS

801 Lancaster Avenue,

Bryn Mawr, PA 19010

610-525-1700¢

www.bmtc.com

DIRECTORS

Thomas L. Bennett,

Private Investor, Director and Trustee of the

Delaware Investments Family of Funds

Andrea F. Gilbert,

President, Bryn Mawr Hospital

Wendell F. Holland,

Partner, Saul Ewing LLP

Scott M. Jenkins,

President, S.M. Jenkins & Co.

David E. Lees,

Senior Partner, myCIO Wealth Partners, LLC

Francis J. Leto,

Executive Vice President, Wealth Management

Britton H. Murdoch,

CEO, City Line Motors;

Managing Director, Strattech Partners

Frederick C. “Ted” Peters II,

Chairman, President & Chief Executive Officer,

Bryn Mawr Bank Corporation and

The Bryn Mawr Trust Company

B. Loyall Taylor, Jr.,

President, Taylor Gifts, Inc.

MARKET MAKERS

Boenning & Scattergood, Inc.

Citigroup Global Markets Holdings Inc.

Deutsche Bank Securities Inc.

FTN Equity Capital Markets Corp.

Janney Montgomery Scott LLC

Keefe, Bruyette & Woods, Inc.

Morgan Stanley & Co., Inc.

Ryan Beck & Co., Inc.

Sandler O’Neill & Partners, L.P.

Sterne, Agee & Leach, Inc.

Stifel, Nicolaus & Co.

UBS Securities LLC

For a complete list visit our website at

www.bmtc.com

INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

KPMG LLP,

1601 Market Street,

Philadelphia, PA 19103

LEGAL COUNSEL

McElroy, Deutsch, Mulvaney & Carpenter, LLP

One Penn Center at Suburban Station

1617 John F. Kennedy Boulevard,

Suite 1500,

Philadelphia, PA 19103

Stradley Ronon Stevens & Young, LLP

2005 Market Street,

Suite 2600,

Philadelphia, PA 19103-7098

BRYN MAWR BANK CORPORATION

Frederick C. “Ted” Peters II,

Chairman, President & Chief Executive Officer

Geoffrey L. Halberstadt,

Corporate Secretary (effective 3/31/10)

J. Duncan Smith, CPA,

Treasurer and Assistant Secretary

Francis J. Leto,

Vice President (effective 3/31/10)

PRINCIPAL SUBSIDIARY

The Bryn Mawr Trust Company

A Subsidiary of Bryn Mawr Bank Corporation

EXECUTIVE MANAGEMENT

Frederick C. “Ted” Peters II,

Chairman, President & Chief Executive Officer

Alison E. Gers,

Executive Vice President, Retail Banking,

Central Sales, Marketing, Information Systems

& Operations

Joseph G. Keefer,

Executive Vice President and Chief Lending Officer

Francis J. Leto,

Executive Vice President, Wealth Management

Robert J. Ricciardi,

Executive Vice President, Chief Credit Policy

Officer and Corporate Secretary

J. Duncan Smith, CPA,

Executive Vice President and Chief Financial Officer

Matthew G. Waschull, CTFA®, AEP®,

President and Treasurer, The Bryn Mawr

Trust Company of Delaware

BRANCH OFFICES

50 West Lancaster Avenue,

Ardmore, PA 19003

801 Lancaster Avenue,

Bryn Mawr, PA 19010

237 North Pottstown Pike,

Exton, PA 19341

18 West Eagle Road,

Havertown, PA 19083

3601 West Chester Pike,

Newtown Square, PA 19073

39 West Lancaster Avenue,

Paoli, PA 19301

330 East Lancaster Avenue,

Wayne, PA 19087

849 Paoli Pike,

West Chester, PA 19380

One Tower Bridge,

West Conshohocken, PA 19428

WEALTH MANAGEMENT DIVISION

10 South Bryn Mawr Avenue,

Bryn Mawr, PA 19010

LIFE CARE COMMUNITY OFFICES

Beaumont at Bryn Mawr Retirement Community,

Bryn Mawr, PA

Bellingham Retirement Living,

West Chester, PA

Martins Run Life Care Community,

Media, PA

Rosemont Presbyterian Village,

Rosemont, PA

The Quadrangle,

Haverford, PA

Waverly Heights,

Gladwyne, PA

White Horse Village,

Newtown Square, PA

OTHER SUBSIDIARIES AND FINANCIAL SERVICES

BMT Leasing, Inc.

A Subsidiary of The Bryn Mawr Trust Company,

Bryn Mawr, PA

Joseph G. Keefer, Chairman;

James A. Zelinskie, Jr., President

BMT Mortgage Company

A Division of The Bryn Mawr Trust Company,

Bryn Mawr, PA

Myron H. Headen, President

BMT Mortgage Services, Inc.

A Subsidiary of The Bryn Mawr Trust Company,

Bryn Mawr, PA

Joseph G. Keefer, Chairman;

Myron H. Headen, President

BMT Settlement Services, Inc.

A Subsidiary of The Bryn Mawr Trust Company,

Bryn Mawr, PA

Joseph G. Keefer, Chairman;

Myron H. Headen, President

The Bryn Mawr Trust Company of Delaware

A Subsidiary of Bryn Mawr Bank Corporation,

Wilmington, DE

Matthew G. Waschull, CTFA®, AEP®, President and Treasurer

Insurance Counsellors of Bryn Mawr, Inc.

A Subsidiary of The Bryn Mawr Trust Company,

Bryn Mawr, PA

Thomas F. Drennan, President

Lau Associates LLC

A Subsidiary of Bryn Mawr Bank Corporation,

Wilmington, DE

Judith W. Lau, CFP®, President

REG ISTRAR & TRANSFER AGENT

BNY Mellon Shareowner Services

PO Box 358015,

Pittsburgh, PA 15252-8015

www.bnymellon.com/shareowner/isd

8

2009 Annual Report

| | |

SELECTED FINANCIAL DATA | | 1 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | | 2 |

MANAGEMENT’S REPORT OF INTERNAL CONTROL OVER FINANCIAL REPORTING | | 23 |

REPORTS OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | 24 |

CONSOLIDATED BALANCE SHEETS | | 26 |

CONSOLIDATED STATEMENTS OF INCOME | | 27 |

CONSOLIDATED STATEMENTS OF CASH FLOWS | | 28 |

CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY | | 30 |

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS | | 31 |

PRICE RANGE OF SHARES | | 56 |

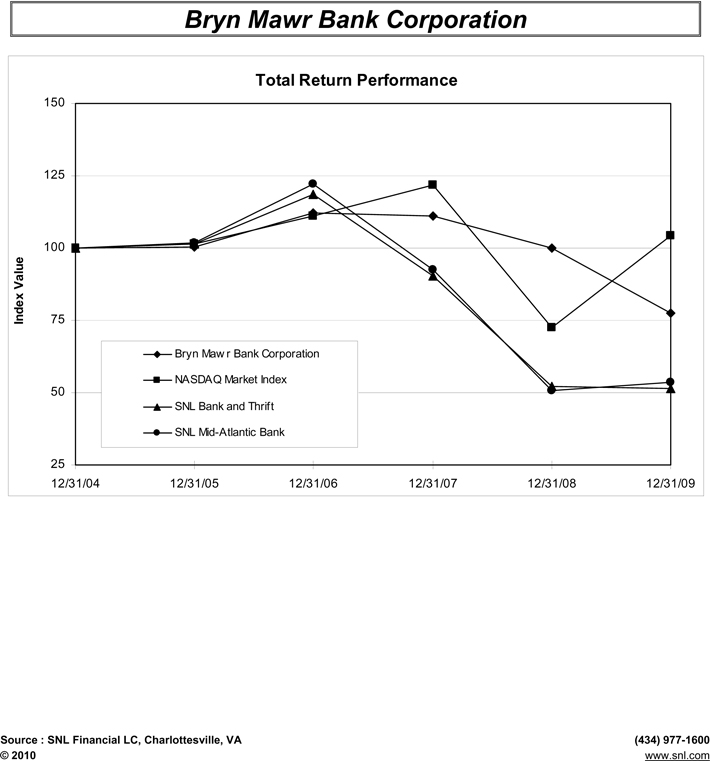

COMPARATIVE DATA PERFORMANCE | | 57 |

Exhibit 13.1

Selected Financial Data

| | | | | | | | | | | | | | | | | | | | |

| For the years ended December 31, | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

| | | (dollars in thousands, except for per share data) | |

Interest income | | $ | 56,892 | | | $ | 57,934 | | | $ | 54,218 | | | $ | 45,906 | | | $ | 37,908 | |

Interest expense | | | 16,099 | | | | 20,796 | | | | 19,976 | | | | 12,607 | | | | 6,600 | |

| | | | | | | | | | | | | | | | | | | | |

Net interest income | | | 40,793 | | | | 37,138 | | | | 34,242 | | | | 33,299 | | | | 31,308 | |

Provision for loan and lease losses | | | 6,884 | | | | 5,596 | | | | 891 | | | | 832 | | | | 762 | |

| | | | | | | | | | | | | | | | | | | | |

Net interest income after loan loss provision | | | 33,909 | | | | 31,542 | | | | 33,351 | | | | 32,467 | | | | 30,546 | |

Non-interest income | | | 28,470 | | | | 21,472 | | | | 21,781 | | | | 18,361 | | | | 18,305 | |

Non-interest expense | | | 46,542 | | | | 38,676 | | | | 34,959 | | | | 31,423 | | | | 31,573 | |

| | | | | | | | | | | | | | | | | | | | |

Income before income taxes | | | 15,837 | | | | 14,338 | | | | 20,173 | | | | 19,405 | | | | 17,278 | |

Applicable income taxes | | | 5,500 | | | | 5,013 | | | | 6,573 | | | | 6,689 | | | | 5,928 | |

| | | | | | | | | | | | | | | | | | | | |

Net Income | | $ | 10,337 | | | $ | 9,325 | | | $ | 13,600 | | | $ | 12,716 | | | $ | 11,350 | |

| | | | | | | | | | | | | | | | | | | | |

Per share data: | | | | | | | | | | | | | | | | | | | | |

Earnings per common share: | | | | | | | | | | | | | | | | | | | | |

Basic | | $ | 1.18 | | | $ | 1.09 | | | $ | 1.59 | | | $ | 1.48 | | | $ | 1.33 | |

Diluted | | $ | 1.18 | | | $ | 1.08 | | | $ | 1.58 | | | $ | 1.46 | | | $ | 1.31 | |

| | | | | |

Dividends declared | | $ | 0.56 | | | $ | 0.54 | | | $ | 0.50 | | | $ | 0.46 | | | $ | 0.42 | |

| | | | | |

Weighted-average shares outstanding | | | 8,732,004 | | | | 8,566,938 | | | | 8,539,904 | | | | 8,578,050 | | | | 8,563,027 | |

Dilutive potential common shares | | | 16,719 | | | | 34,233 | | | | 93,638 | | | | 113,579 | | | | 101,200 | |

| | | | | | | | | | | | | | | | | | | | |

Adjusted weighted-average shares | | | 8,748,723 | | | | 8,601,171 | | | | 8,633,542 | | | | 8,691,629 | | | | 8,664,227 | |

| | | | | |

Selected financial ratios: | | | | | | | | | | | | | | | | | | | | |

Tax equivalent net interest margin | | | 3.70 | % | | | 3.84 | % | | | 4.37 | % | | | 4.90 | % | | | 5.05 | % |

Net income/average total assets (“ROA”) | | | 0.88 | % | | | 0.89 | % | | | 1.59 | % | | | 1.72 | % | | | 1.66 | % |

Net income/average shareholders’ equity (“ROE”) | | | 10.55 | % | | | 10.01 | % | | | 15.87 | % | | | 15.71 | % | | | 15.50 | % |

Tier 1 Capital to Risk Weighted Assets | | | 9.41 | % | | | 8.81 | % | | | 10.40 | % | | | 11.38 | % | | | 11.38 | % |

Total Regulatory Capital to Risk Weighted Assets | | | 12.53 | % | | | 11.29 | % | | | 11.31 | % | | | 12.46 | % | | | 12.46 | % |

Dividends declared per share to net income per basic common share | | | 47.5 | % | | | 49.5 | % | | | 31.4 | % | | | 31.1 | % | | | 31.6 | % |

| | | | | |

| At December 31, | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

Total assets | | $ | 1,238,821 | | | $ | 1,151,346 | | | $ | 1,002,096 | | | $ | 826,817 | | | $ | 727,383 | |

Earning assets | | | 1,164,617 | | | | 1,061,139 | | | | 874,661 | | | | 733,781 | | | | 664,073 | |

Portfolio loans and leases | | | 885,739 | | | | 899,577 | | | | 802,925 | | | | 681,291 | | | | 595,165 | |

Deposits | | | 937,887 | | | | 869,490 | | | | 849,528 | | | | 714,489 | | | | 636,260 | |

Shareholders’ equity | | | 103,936 | | | | 92,413 | | | | 90,351 | | | | 82,092 | | | | 77,222 | |

Ratio of tangible common equity to tangible assets | | | 7.51 | % | | | 7.13 | % | | | 9.02 | % | | | 9.97 | % | | | 10.66 | % |

Ratio of equity to assets | | | 8.39 | % | | | 8.03 | % | | | 9.02 | % | | | 9.97 | % | | | 10.66 | % |

Loans serviced for others | | | 514,875 | | | | 350,199 | | | | 357,363 | | | | 382,141 | | | | 417,649 | |

Assets under management, administration & supervision1 | | | 2,871,143 | | | | 2,146,399 | | | | 2,277,091 | | | | 2,178,777 | | | | 2,042,613 | |

Book value per share | | $ | 11.72 | | | $ | 10.76 | | | $ | 10.60 | | | $ | 9.59 | | | $ | 9.03 | |

Tangible book value per share | | $ | 10.40 | | | $ | 9.55 | | | $ | 10.60 | | | $ | 9.59 | | | $ | 9.03 | |

Allowance as a percentage of portfolio loans and leases | | | 1.18 | % | | | 1.15 | % | | | 1.01 | % | | | 1.19 | % | | | 1.24 | % |

Non-performing loans and leases as a percentage of total loans and leases | | | 0.78 | % | | | 0.65 | % | | | 0.25 | % | | | 0.12 | % | | | 0.07 | % |

| 1 | Excludes assets under management from an institutional client for 2007, 2006 and 2005. |

1

Management’s Discussion and Analysis of Financial Condition and Results of Operations

BRIEF HISTORYOFTHE CORPORATION

The Bryn Mawr Trust Company (the “Bank” or “BMTC”) received its Pennsylvania banking charter in 1889 and is a member of the Federal Reserve System. In 1986, Bryn Mawr Bank Corporation (the “Corporation” or “BMBC”) was formed and on January 2, 1987, the Bank became a wholly-owned subsidiary of the Corporation. The Bank and Corporation are headquartered in Bryn Mawr, PA, a western suburb of Philadelphia, PA. The Corporation and its subsidiaries offer a full range of personal and business banking services, consumer and commercial loans, equipment leasing, mortgages, insurance and wealth management services, including investment management, trust and estate administration, retirement planning, custody services, and tax planning and preparation from nine full-service branches and seven limited-hour retirement community offices throughout Montgomery, Delaware and Chester counties. The Corporation trades on the NASDAQ Global Market (“NASDAQ”) under the symbol BMTC.

The goal of the Corporation is to become the preeminent community bank and wealth management organization in the Philadelphia area.

The Corporation operates in a highly competitive market area that includes local, national and regional banks as competitors along with savings banks, credit unions, insurance companies, trust companies, registered investment advisors and mutual fund families. The Corporation and its subsidiaries are regulated by many regulatory agencies including the Securities and Exchange Commission (“SEC”), NASDAQ, Federal Deposit Insurance Corporation (“FDIC”), the Federal Reserve and the Pennsylvania Department of Banking.

FIRST KEYSTONE FINANCIAL, INC.

On November 3, 2009, the Corporation announced that it had entered into a definitive Agreement and Plan of Merger (the “Agreement”) to acquire First Keystone Financial, Inc. and its subsidiaries (collectively, “First Keystone” or “FKF”), a Pennsylvania chartered savings and loan holding company headquartered in Media, PA, in a stock and cash transaction. In accordance with the terms of the Agreement, the acquisition is to be effected pursuant to a merger of First Keystone Financial, Inc. with and into the Corporation, and a two-step merger of First Keystone Bank with and into the Bank (collectively, the “Transaction”). At December 31, 2009 First Keystone had total assets of approximately $500 million and operated eight full-service branches, primarily in Delaware County, PA.

The Agreement provides for a per share merger consideration in the form of cash and common stock of the Corporation. The per share merger consideration may be adjusted based on the level of First Keystone’s “Delinquencies” at the month-end preceding the closing date of the Transaction. “Delinquencies” are defined in the Agreement as all loans delinquent thirty days or more, non-accruing loans, other real estate owned, troubled debt restructurings and the aggregate amount of loans charged-off between October 31, 2008 and the month-end preceding the closing date in excess of $2.5 million. “Administrative Delinquencies” as defined in the Agreement are excluded from this definition. The per share merger consideration and adjustment levels are as follows:

| | | | | | | | |

FKF Delinquencies at Month-End Preceding Closing | | Adjusted

Amount of

BMBC Stock

to be

Received

for Each

FKF Share | | Adjusted Per

Share Cash

Consideration

for Each

FKF Share | | Deal Value

with

BMTC Stock

Valued at

$16.00 per

Share*

(in millions) |

| | | |

Less than $10.5 million | | 0.6973 | | $ | 2.06 | | $ | 32.156 |

| | | |

$10.5 – $12.5 million | | 0.6834 | | $ | 2.02 | | $ | 31.518 |

| | | |

$12.5 – $14.5 million | | 0.6718 | | $ | 1.98 | | $ | 30.969 |

| | | |

$14.5 – $16.5 million | | 0.6589 | | $ | 1.95 | | $ | 30.393 |

| | | |

$16.5 million or more | | 0.6485 | | $ | 1.92 | | $ | 29.916 |

| * | Calculated as the sum of (a) the product of the number of shares of First Keystone Financial, Inc. common stock outstanding, multiplied by the adjusted amount of BMBC stock to be received for such shares, multiplied by the per share market price of BMBC common stock, as listed on the NASDAQ Global Market, plus (b) the product of the number of shares of First Keystone Financial, Inc. common stock outstanding multiplied by the per share cash consideration. Numbers in this column are provided as an example of what the deal value would be assuming the market price of BMBC common stock is $16.00 per share, and the number of First Keystone Financial, Inc. shares outstanding does not change. As the price of BMBC common stock fluctuates, or the number of First Keystone Financial, Inc.’s shares outstanding changes, the deal value will also change. |

The Agreement also provides that all options to purchase First Keystone stock which are outstanding and unexercised immediately prior to the closing (“Continuing Options”) under FKF’s Amended and Restated 1995 Stock Option Plan and Amended and Restated 1998 Stock Option Plan, in each case as amended, shall, subject to certain conditions and regulatory approvals, become fully vested, to the extent not already fully vested, and exercisable and be converted into fully vested and exercisable options to purchase shares of the Corporation’s stock. The number of shares of the Corporation’s stock to be subject to the Continuing Options will be equal to 0.8204 (“Option Exchange Ratio”) multiplied by the number of shares of First Keystone stock subject to the Continuing Options, subject to rounding. The exercise price per share of

2

the Corporation’s stock under the Continuing Options will be equal to the exercise price per share of First Keystone stock under the Continuing Options divided by the Option Exchange Ratio, subject to rounding. In the event that the per share Merger Consideration is adjusted as described above, the option exchange ration will also reflect a corresponding adjustment.

The closing of the Transaction is subject to approval by the Pennsylvania Department of Banking, the Office of Thrift Supervision and the Federal Reserve. Regulatory applications have been filed with these agencies and are under review. On March 2, 2010, First Keystone held a shareholder meeting to approve the Transaction. There were 2,432,998 shares of First Keystone common stock eligible to be voted at the meeting and 1,984,657 shares represented in person or by proxy. The shareholders approved the Transaction with more than 81% of the issued and outstanding shares voting in favor.

The closing of the Transaction remains subject to certain conditions more fully described in the Agreement, including, without limitation, governmental filings and regulatory approvals and expiration of applicable waiting periods, accuracy of specified representations and warranties of both parties, the absence of a material adverse effect, and obtaining material permits and authorizations for the lawful consummation of the Transaction. Upon completion of the Transaction, the Corporation and the Bank expect to be able to more efficiently leverage resources and deliver high quality products and services to the marketplace. Increasing the Corporation’s presence in Delaware and Chester Counties has been a strategic goal, and this Transaction is an important component of that strategic plan.

For further information with respect to the Agreement, please review the Proxy Statement / Prospectus which was filed with the SEC on January 25, 2010 in accordance with Rule 424(b) of the Securities Act of 1933, as amended (the “Securities Act”).

RESULTSOF OPERATIONS

The following is Corporation’s discussion and analysis of the significant changes in the results of operations, capital resources and liquidity presented in the accompanying consolidated financial statements. The Corporation’s consolidated financial condition and results of operations consist almost entirely of the Bank’s financial condition and results of operations. Current performance does not guarantee, and may not be indicative of similar performance in the future.

CRITICAL ACCOUNTING POLICIES, JUDGMENTSAND ESTIMATES

The accounting and reporting policies of the Corporation and its subsidiaries conform with accounting principles generally accepted in the United States of America applicable to the financial services industry (Generally Accepted Accounting Principles “GAAP”). All inter-company transactions are eliminated in consolidation and certain reclassifications are made when necessary to conform the previous year’s financial statements to the current year’s presentation. In preparing the consolidated financial statements, Corporation is required to make estimates and assumptions that affect the reported amount of assets and liabilities as of the dates of the balance sheets and revenues and expenditures for the periods presented. Therefore, actual results could differ from these estimates.

The allowance for loan and lease losses involves a higher degree of judgment and complexity than other significant accounting policies. The allowance for loan and lease losses is calculated with the objective of maintaining a reserve level believed by the Corporation to be sufficient to absorb estimated probable credit losses. The Corporation’s determination of the adequacy of the allowance is based on periodic evaluations of the loan and lease portfolio and other relevant factors. However, this evaluation is inherently subjective as it requires material estimates, including, among others, expected default probabilities, expected loan commitment usage, the amounts and timing of expected future cash flows on impaired loans and leases, value of collateral, estimated losses on consumer loans and residential mortgages and general amounts for historical loss experience. The process also considers economic conditions, international events, and inherent risks in the loan and lease portfolio. All of these factors may be susceptible to significant change. To the extent actual outcomes differ from the Corporation’s estimates, additional provisions for loan and lease losses may be required that would adversely impact earnings in future periods. See the section of this document titled Asset Quality and Analysis of Credit Risk for additional information.

Other significant accounting policies are presented in Note 1 in the accompanying financial statements. The Corporation’s Summary of Significant Accounting Policies has not substantively changed any aspect of its overall approach in the application of the foregoing policies.

OVERVIEWOF GENERAL ECONOMIC, REGULATORYAND GOVERNMENTAL ENVIRONMENT

During 2009, the global and U.S. economies experienced a dramatic swing, beginning the year in a recessionary environment which then began to stabilize in the latter part of 2009.

3

Dramatic declines in the housing market during the past year, as home prices fell and foreclosures and unemployment increased, resulted in significant write-downs of asset values by financial institutions, including government-sponsored entities and major commercial and investment banks.

The drop in real estate values negatively impacted residential real estate builder and development business nationwide. As the U.S. economy entered a recession in 2008 which carried over into 2009, financial institutions faced higher credit losses from distressed real estate values and borrower defaults which resulted in reduced capital levels. In addition, investment securities backed by residential and commercial real estate were reflecting substantial unrealized losses due to a lack of liquidity in the financial markets and anticipated credit losses. Some financial institutions were forced into liquidation or were merged with stronger institutions as losses increased and the amounts of available funding and capital levels lessened. As of December 31, 2009, the Bryn Mawr Bank Corporation (the “Corporation” and “BMBC”) and The Bryn Mawr Trust Company (“BMTC” and the “Bank”) are “well capitalized” by regulatory standards and are in a position to acquire new customers from weaker financial institutions.

In 2008 the Emergency Economic Stabilization Act of 2008 (“EESA”) was signed into law on October 3, 2008. The EESA authorizes the U.S. Treasury the ability to provide funds to restore liquidity and stability to the U.S. financial system. Two of the specific programs, the Troubled Asset Relief Program (“TARP”) and the Temporary Liquidity Guarantee Program (“TLGP”) are described in further detail below from their onset with relevant updates.

The TARP program under which the Treasury purchases equity stakes in certain banks and thrifts. The Treasury’s initial effort was to make available $250 billion of capital to U.S. financial institutions in the form of preferred stock (from the $700 billion authorized by the EESA). In conjunction with the purchase of preferred stock, the Treasury receives warrants to purchase common stock with an aggregate market price equal to 15% of the preferred investment.

As financial systems have stabilized, many larger financial institutions have begun to repay TARP funds early, as Federal Reserve stress tests performed on these institutions showed no additional need for capital. The Corporation elected not to participate in the program due to its “well capitalized” regulatory capital position and the ever changing conditions of the TARP program.

The systemic risk exception to the Federal Deposit Insurance Corporation (“FDIC”) Act, enables the FDIC to temporarily provide a 100% guarantee of the senior unsecured debt of all FDIC-insured institutions and their holding companies, as well as deposits in noninterest-bearing transaction deposit accounts under the TLGP through December 31, 2009. Pursuant to this program, all insured depository institutions automatically participated in the TLGP for 30 days following the announcement of the program without charge and thereafter, unless the institution opted out, at a cost of 75 basis points per annum for senior unsecured debt and 10 basis points per annum for noninterest-bearing transaction deposits.

On August 26, 2009 the FDIC extended the TLGP until June 30, 2010. This program will continue to provide depositors with unlimited coverage for non-interest bearing transaction accounts at participating FDIC-insured institutions. The unlimited coverage applies to all personal and business checking deposit accounts that do not earn interest, including DDA accounts, low interest NOW accounts and IOLTA accounts. BMTC chose to continue its participation in the TLGP and, thus, did not opt out.

On May 22, 2009 the FDIC adopted a final rule imposing a five basis point emergency special assessment on each insured depository institution’s assets less Tier I capital as of June 30, 2009, payable September 30, 2009. The Corporation’s special assessment was $540 thousand.

On November 12, 2009 the FDIC announced it will require insured institutions to prepay their estimated quarterly risk-based assessments for the fourth quarter of 2009 and for all of 2010, 2011 and 2012. The prepaid assessment for these periods was collected on December 30, 2009. The Corporation’s prepayment was $4.5 million.

The FDIC announced on October 3, 2008 that deposits held at FDIC-insured institutions are insured up to at least $250 thousand per depositor until December 31, 2009. On May 20, 2009 the FDIC announced an extension of this program until December 31, 2013.

The Federal Home Loan Bank of Pittsburgh (“FHLB-P”) has continued its voluntary suspension of dividend payments and the repurchase of excess capital stock originally announced on December 23, 2008. The FHLB-P expects that its ability to pay dividends and add to retained earnings will be significantly curtailed due to low short-term interest rates, an increased cost of maintaining liquidity and constrained access to debt markets at attractive rates. Capital stock repurchases from member banks will be reviewed on a quarterly basis, but no repurchase will take place until advised. As of December 31, 2009, the Corporation held $7.9 million of FHLB-P capital stock and is monitoring the situation closely as are other FHLB-P member banks. The FHLB-P is the primary source of liquidity for the Corporation, but it can also use other alternatives available to the Corporation that include the Federal Reserve and wholesale certificates of deposit.

Throughout 2009 the economy remained weak though improvements are occurring. A drawn-out economic recovery could have an adverse effect on the Corporation’s revenues, capital, liquidity and profitability. However, the Corporation is confident that its disciplined strategies to maintain a strong

4

financial position and build the brand name put it in a good position to weather the financial downturn and take advantage of opportunities as they arise.

EXECUTIVE OVERVIEW

2009 Compared to 2008

The Corporation’s 2009 diluted earnings per share increased $0.10 per share to $1.18 per share or 9.3% compared to $1.08 per share in 2008, and net income for the year ended December 31, 2009 of $10.3 million increased 10.9% or $1.0 million, compared to $9.3 million last year. Return on average equity (ROE) and return on average assets (ROA) for the year ended December 31, 2009 were 10.22% and 0.87%, compared with ROE and ROA of 10.01% and 0.89%, respectively, in 2008.

During 2009, the Corporation made progress on several of its growth initiatives including the announcement on November 3, 2009 to acquire First Keystone Financial, Inc. as discussed earlier in this document.

Additionally, on January 2, 2009, the Corporation opened its West Chester Regional Banking Center which enabled the Corporation’s wealth management and banking services to be introduced into another affluent market with good growth potential while further diversifying its asset base and client accounts.

Rounding out 2009, the Corporation established BMT Asset Management, a department within the Wealth Management Division of the Bank, filed a Shelf Registration Statement on Form S-3 and established a Dividend Reinvestment and Stock Purchased Plan (“DRIP”).

BMT Asset Management was established through the hiring of experienced asset managers in the later part of June 2009 and has generated $86.6 million in assets under management at December 31, 2009.

The shelf registration was declared effective by the Securities and Exchange Commission (“SEC”) on June 17, 2009, and is intended to allow the Corporation to raise additional capital through offers and sales of registered securities consisting of common stock, warrants to purchase common stock, stock purchase contracts or units consisting of any combination of the foregoing securities.

On July 20, 2009 the Corporation filed a prospectus supplement with the SEC in order to take securities down from the Shelf Registration Statement in connection with the DRIP. The DRIP provides existing shareholders and new investors the opportunity to easily and conveniently increase their investment in the Corporation through reinvestment of dividends, new investments and requests for waivers.

The Corporation’s portfolio of loans and leases at December 31, 2009 of $885.7 million decreased 1.6% or $13.9 million from $899.6 million at December 31, 2008 balances.

The loan portfolio, excluding leases, declined marginally by 0.3% or $2.3 million to $838.0 million in 2009 compared with $840.3 million in 2008. The lease portfolio declined 19.5% or $11.6 million to $47.8 million from the December 31, 2008 balance of $59.4 million. The lease portfolio represents approximately 5.4% of total 2009 year-end portfolio loans and leases. The decline in the loan portfolio was concentrated in the construction and lease portfolios due to the Corporation’s decision to limit exposure to those sections of the portfolio.

Credit quality on the overall loan and lease portfolio remains stable as total non-performing loans and leases represents 78 basis points or $6.9 million of portfolio loans and leases at December 31, 2009. The Corporation believes the majority of these loans are adequately secured by collateral that can substantially liquidate the debt. This compares with 65 basis points or $5.8 million at December 31, 2008. The provision for loan and lease losses for the years ended December 31, 2009 and 2008 was $6.9 million and $5.6 million, respectively. At December 31, 2009, the allowance for loan and lease losses (“allowance”) of $10.4 million represented 1.18% of portfolio loans and leases compared with 1.15% at December 31, 2008. For additional information about asset quality and analysis of credit risk, see page 11 of this document.

Funding from wholesale sources, which includes wholesale deposits, subordinated debt and Federal Home Loan Bank of Pittsburg (“FHLB-P”) borrowings, at December 31, 2009 of approximately $255.6 million was $65.3 million lower than the $320.9 million at December 31, 2008. The increase in deposit activity during 2009 reduced the Corporation’s dependency on more expensive wholesale funding by approximately 8%.

The increase in the Corporation’s tax equivalent net interest income of $3.7 million or 9.8% for the year ended December 31, 2009 compared to the same period last year was due to an interest expense reduction of $5.4 million or 26.5%, growth in the investment portfolio and a higher than average interest rate on interest earning assets. The Corporation’s tax-equivalent net interest margin increased from 3.70% in 2008 to 3.84% in 2009.

For the year ended December 31, 2009, non-interest income was $28.5 million, a increase of $7.0 million or 32.6% from $21.5 million in 2008. The primary factors for this increase were the gains on the sale of residential mortgage loans, the gains on sale of investment securities and increased fees from the Wealth Management Division.

For the year ended December 31, 2009, non-interest expense was $46.5 million, an increase of $7.9 million or 20.3% over the $38.7 million in the same period last year. Personnel and

5

related support costs associated with new business initiatives including commissions on mortgage originations, the opening of the West Chester Regional Banking Center, costs associated with the Transaction with First Keystone and the FDIC insurance increase along with the FDIC one-time special assessment were the largest contributors to this increase.

2008 Compared to 2007

For the twelve months ended December 31, 2008, the Corporation earned $9.3 million or $1.08 per diluted share. The Corporation’s 2008 diluted earnings per share decreased $0.50 per share or 31.6% compared to $1.58 per share in 2007, and net income for the year ended December 31, 2008 decreased 31.6% or $4.3 million, compared to $13.6 million in 2007. Return on average equity (ROE) and return on average assets (ROA) for the year ended December 31, 2008 were 10.01% and 0.89%, respectively. ROE was 15.87% and ROA was 1.59% for the same period last year.

The Corporation elected not to participate in the United States Government’s TARP Program due to the Corporation’s regulatory capital status of “well capitalized” and the ever changing conditions of the TARP Program.

During 2008, the Corporation established The Bryn Mawr Trust Company of Delaware, a limited purpose trust company (“LPTC”) in the State of Delaware. Additionally, on July 15, 2008, the Corporation acquired Lau Associates, a Wilmington, Delaware, based investment advisory and financial planning firm.

The Corporation increased portfolio loans and leases in 2008 by 12.0% or $96.7 million compared with year-end 2007 balances by expanding banking relationships with local businesses, not-for-profit entities and high credit quality individuals.

The loan portfolio, excluding leases, grew 10.9% or $82.4 million to $840.3 million in 2008 compared with $757.8 million in 2007. This increase included home equity loans and lines, commercial and industrial loans and commercial mortgages. The lease portfolio grew 31.5% or $14.2 million to $59.3 in 2008 and now represents approximately 6.6% of total portfolio loans and leases. The lease portfolio, which is national in scope, did not perform well in 2008 as charge-offs were 6.24% of average leases. The Corporation made underwriting adjustments at the end of 2007 and has continued to “tighten” these standards in 2008 and early 2009.

Total non-performing loans and leases represents 65 basis points or $5.8 million of portfolio loans and leases at December 31, 2008. This compares with 25 basis points or $2.0 million at December 31, 2007. The provision for loan and lease losses for the years ended December 31, 2008 and 2007 was $5.6 million and $891 thousand, respectively, which was primarily due to the increased level of charge-offs in the lease portfolio. At December 31, 2008, the allowance for loan and lease losses (“allowance”) of $10.3 million represents 1.15% of portfolio loans and leases compared with 1.01% at December 31, 2007.

Funding from wholesale sources, which includes wholesale deposits, subordinated debt and FHLB-P borrowings, at December 31, 2008 of approximately $290.7 million was $115.9 million higher than the $174.8 million at December 31, 2007. The incremental wholesale funding was primarily used to fund $96.7 million of growth in the loan and lease portfolio and $60.0 million of growth in the Corporation’s investment portfolio.

The increase in the Corporation’s tax equivalent net interest income of $2.8 million or 8.2% for the year ended December 31, 2008 compared to the same period last year was due to the increase in loan and lease volume, and the growth in the investment portfolio, which more than offset the decrease in asset yields and higher funding costs. The Corporation’s tax-equivalent net interest margin declined from 4.37% in 2007 to 3.84% in 2008.

For the year ended December 31, 2008, non-interest income was $21.5 million, a decrease of $0.3 million or 1.4% from the $21.8 million in 2007. The primary factor for this decrease was a gain on the sale of real estate of $1.3 million in 2007. Partially offsetting this decrease were gains on sale of investments, interest rate floor income and increased Wealth Management Division revenue which is attributed to the acquisition of Lau Associates.

For the year ended December 31, 2008, non-interest expense was $38.7 million, an increase of $3.7 million or 10.6% over the $35.0 million in the same period last year. Personnel and related support costs associated with new business initiatives including the Lau Associates acquisition and the impairment of mortgage servicing rights were the largest contributors to this increase.

6

COMPONENTSOF NET INCOME

Net income is affected by five major elements:Net Interest Income, or the difference between interest income and loan fees earned on loans and investments and interest expense paid on deposits and borrowed funds;Provision For Loan and Lease Losses, or the amount added to the allowance for loan and lease losses to provide for estimated inherent losses on loans and leases;Non-Interest Income which is made up primarily of certain fees, wealth management revenue, residential mortgage activities and gains and losses from the sale of securities and other assets;Non-Interest Expense, which consists primarily of salaries, employee benefits and other operating expenses; andIncome Taxes. Each of these major elements will be reviewed in more detail in the following discussion.

NET INTEREST INCOME

Rate/Volume Analyses (Tax Equivalent Basis)*

The rate volume analysis in the table below analyzes changes in tax equivalent net interest income for the years 2009 compared to 2008 and 2008 compared to 2007 by its rate and volume components. The change in interest income/expense due to both volume and rate has been allocated to changes in volume.

| | | | | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, | |

| (dollars in thousands) | | 2009 Compared to 2008 | | | 2008 Compared to 2007 | |

| increase/(decrease) | | Volume | | | Rate | | | Total | | | Volume | | Rate | | | Total | |

Interest Income: | | | | | | | | | | | | | | | | | | | | | | | |

Interest-bearing deposits with banks | | $ | 127 | | | $ | (198 | ) | | $ | (71 | ) | | $ | 867 | | $ | (798 | ) | | $ | 69 | |

Money market funds | | | (123 | ) | | | (12 | ) | | | (135 | ) | | | 162 | | | (152 | ) | | | 10 | |

Federal funds sold | | | 193 | | | | (15 | ) | | | 178 | | | | 106 | | | (144 | ) | | | (38 | ) |

Investment securities available for sale | | | 2,531 | | | | (1,848 | ) | | | 683 | | | | 2,522 | | | (271 | ) | | | 2,251 | |

Loans and leases | | | 2,546 | | | | (4,121 | ) | | | (1,575 | ) | | | 7,820 | | | (6,463 | ) | | | 1,357 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Total interest income | | | 5,274 | | | | (6,194 | ) | | | (920 | ) | | | 11,477 | | | (7,828 | ) | | | 3,649 | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Interest expense: | | | | | | | | | | | | | | | | | | | | | | | |

Savings, NOW and market rate accounts | | | 1,084 | | | | (1,632 | ) | | | (548 | ) | | | 628 | | | (1,044 | ) | | | (416 | ) |

Other wholesale deposits | | | 27 | | | | 10 | | | | 37 | | | | 111 | | | — | | | | 111 | |

Wholesale time deposits | | | (2,076 | ) | | | (1,338 | ) | | | (3,414 | ) | | | 2,099 | | | (1,637 | ) | | | 462 | |

Time deposits | | | (162 | ) | | | (1,985 | ) | | | (2,147 | ) | | | 355 | | | (2,226 | ) | | | (1,871 | ) |

Borrowed Funds | | | 1,221 | | | | 154 | | | | 1,375 | | | | 4,907 | | | (2,373 | ) | | | 2,534 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Total interest expense | | | 94 | | | | (4,791 | ) | | | (4,697 | ) | | | 8,100 | | | (7,280 | ) | | | 820 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Interest differential | | $ | 5,180 | | | $ | (1,403 | ) | | $ | 3,777 | | | $ | 3,377 | | $ | (548 | ) | | $ | 2,829 | |

| | | | | | | | | | | | | | | | | | | | | | | |

| * | The tax rate used in the calculation of the tax equivalent income is 35%. |

7

Analyses of Interest Rates and Interest Differential

The table below presents the major asset and liability categories on an average daily basis for the periods presented, along with tax-equivalent interest income and expense and key rates and yields:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | For the Year Ended December 31, | |

| | | 2009 | | | 2008 | | | 2007 | |

| (dollars in thousands) | | Average

Balance | | | Interest

Income/

Expense | | Average

Rates

Earned/

Paid | | | Average

Balance | | | Interest

Income/

Expense | | Average

Rates

Earned/

Paid | | | Average

Balance | | | Interest

Income/

Expense | | Average

Rates

Earned/

Paid | |

Assets: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest-bearing deposits with banks | | $ | 34,946 | | | $ | 74 | | 0.21 | % | | $ | 18,678 | | | $ | 145 | | 0.78 | % | | $ | 1,506 | | | $ | 76 | | 5.05 | % |

Federal funds sold | | | 548 | | | | 1 | | 0.18 | % | | | 5,616 | | | | 136 | | 2.42 | % | | | 3,496 | | | | 174 | | 4.98 | % |

Money market funds | | | 38,662 | | | | 197 | | 0.51 | % | | | 3,445 | | | | 19 | | 0.55 | % | | | 182 | | | | 9 | | 4.95 | % |

Investment securities: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Taxable | | | 129,780 | | | | 4,398 | | 3.39 | % | | | 86,940 | | | | 4,127 | | 4.75 | % | | | 39,510 | | | | 2,008 | | 5.08 | % |

Tax –Exempt | | | 17,818 | | | | 776 | | 4.36 | % | | | 7,538 | | | | 364 | | 4.83 | % | | | 5,029 | | | | 232 | | 4.61 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total investment securities(3) | | | 147,598 | | | | 5,174 | | 3.51 | % | | | 94,478 | | | | 4,491 | | 4.75 | % | | | 44,539 | | | | 2,240 | | 5.03 | % |

Loans and leases(1)(2) | | | 892,518 | | | | 51,835 | | 5.81 | % | | | 851,752 | | | | 53,410 | | 6.27 | % | | | 740,694 | | | | 52,053 | | 7.03 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total interest earning assets | | | 1,114,272 | | | | 57,281 | | 5.14 | % | | | 973,969 | | | | 58,201 | | 5.98 | % | | | 790,418 | | | | 54,552 | | 6.90 | % |

Cash and due from banks | | | 11,249 | | | | | | | | | | 15,780 | | | | | | | | | | 22,640 | | | | | | | |

Allowance for loan and lease losses | | | (10,421 | ) | | | | | | | | | (8,613 | ) | | | | | | | | | (8,463 | ) | | | | | | |

Other assets | | | 65,395 | | | | | | | | | | 64,542 | | | | | | | | | | 48,725 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 1,180,495 | | | | | | | | | $ | 1,045,678 | | | | | | | | | $ | 853,320 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Liabilities: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Savings, NOW, and market rate accounts | | $ | 408,523 | | | | 3,094 | | 0.76 | % | | $ | 325,291 | | | $ | 3,753 | | 1.15 | % | | $ | 280,371 | | | $ | 4,169 | | 1.49 | % |

Other wholesale deposits | | | 33,988 | | | | 148 | | 0.44 | % | | | 10,088 | | | | 111 | | 1.10 | % | | | — | | | | — | | — | |

Wholesale time deposits | | | 83,277 | | | | 2,084 | | 2.50 | % | | | 123,794 | | | | 5,498 | | 4.11 | % | | | 92,329 | | | | 4,925 | | 5.53 | % |

Time deposits | | | 190,071 | | | | 4,644 | | 2.44 | % | | | 194,739 | | | | 6,791 | | 3.49 | % | | | 187,044 | | | | 8,662 | | 4.63 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total interest-bearing deposits | | | 715,859 | | | | 9,970 | | 1.39 | % | | | 653,912 | | | | 16,042 | | 2.45 | % | | | 559,744 | | | | 17,756 | | 3.17 | % |

Subordinated debt | | | 20,260 | | | | 1,108 | | 5.47 | % | | | 5,934 | | | | 408 | | 6.88 | % | | | — | | | | — | | — | |

Mortgage payable | | | 1,450 | | | | 82 | | 5.66 | % | | | — | | | | — | | — | | | | — | | | | — | | — | |

Borrowed funds | | | 149,937 | | | | 4,939 | | 3.29 | % | | | 130,490 | | | | 4,346 | | 3.33 | % | | | 42,496 | | | | 2,220 | | 5.22 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total interest-bearing liabilities | | | 887,506 | | | | 16,099 | | 1.81 | % | | | 790,336 | | | | 20,796 | | 2.63 | % | | | 602,240 | | | | 19,976 | | 3.32 | % |

Non-interest-bearing deposits | | | 172,468 | | | | | | | | | | 143,924 | | | | | | | | | | 148,773 | | | | | | | |

Other liabilities | | | 22,502 | | | | | | | | | | 18,243 | | | | | | | | | | 16,622 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total non-interest-bearing liabilities | | | 194,970 | | | | | | | | | | 162,167 | | | | | | | | | | 165,395 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total liabilities | | | 1,082,476 | | | | | | | | | | 952,503 | | | | | | | | | | 767,635 | | | | | | | |

Shareholder’s equity | | | 98,019 | | | | | | | | | | 93,175 | | | | | | | | | | 85,685 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total liabilities and shareholders’ equity | | $ | 1,180,495 | | | | | | | | | $ | 1,045,678 | | | | | | | | | $ | 853,320 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net interest spread | | | | | | | | | 3.33 | % | | | | | | | | | 3.35 | % | | | | | | | | | 3.58 | % |

Effect of non-interest-bearing sources | | | | | | | | | 0.37 | % | | | | | | | | | 0.49 | % | | | | | | | | | 0.79 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net interest income/margin on earning assets | | | | | | $ | 41,182 | | 3.70 | % | | | | | | $ | 37,405 | | 3.84 | % | | | | | | $ | 34,576 | | 4.37 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Tax equivalent adjustment (tax rate 35%) | | | | | | $ | 389 | | 0.04 | % | | | | | | $ | 267 | | 0.03 | % | | | | | | $ | 334 | | 0.04 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Non-accrual loans have been included in average loan balances, but interest on non-accrual loans has not been included for purposes of determining interest income. Average loans and leases include portfolio loans, leases and loans held for sale. |

| (2) | Loans include portfolio loans and leases and loans held for sale. |

| (3) | Investment securities include trading and available for sale. |

Net Interest Income and Net Interest Margin 2009 Compared to 2008

Net interest income on a tax equivalent basis for the year ended December 31, 2009 of $41.2 million was $3.8 million or 10.1% higher than $37.4 million in 2008. This increase was substantially due to the reduction in interest expense of $4.7 million or 22.6%. Interest earning assets increased $140.3 million or 14.4% from 2008. However, the yield on earning assets, which offset the reduction in interest expense, decreased from 5.98% to 5.14% or 84 basis points from the same period. This is the result to the yields on loans decreasing 46 basis points to 5.81% due to the current rate environment and competitive pricing pressures. The yield on investments decreased 124 basis points as more short term liquid investments were purchased.

Average interest bearing liabilities increased $97.2 million or 12.3% from $790.3 million in 2008 to $887.5 million in 2009. This increase is mainly due to the increase in core deposits as wholesale deposits that matured were not replaced. Additionally, the Corporation increased subordinated debt by $14.3 million. The rate on interest bearing liabilities declined 82 basis points from 2.63% to 1.81% primarily due to

8

aggressive management of deposit pricing and the maturity of higher rate wholesale deposits. Despite the increase in the tax equivalent net interest income, the tax equivalent net interest margin on interest earning assets decreased 14 basis points to 3.70% from 3.84% during 2008.

Net Interest Income and Net Interest Margin 2008 Compared to 2007

Net interest income on a tax equivalent basis for the year ended December 31, 2008 of $37.4 million was 8.1% higher than $34.6 million in 2007. This increase was substantially rate driven. Average loan growth of $111.1 million or 15.0% and investment security growth of $50 million were able to offset rate decreases and the impact of funding with higher cost wholesale funds, which includes wholesale deposits, subordinated debt and borrowings.

Average interest bearing liabilities increased by $188.1 million or 31.2% to $790.3 million during 2008 compared to $602.2 million during 2007. Wholesale deposits and borrowings were the primary factors contributing to the increase in average interest bearing liabilities. The change in average other deposit balances in 2008 was a nominal $1.6 million increase.

Despite the increase in tax equivalent net interest income due to increased loan, lease and investment balances, the tax equivalent net interest margin on interest earning assets decreased by 53 basis points from 4.37% during 2007 to 3.84% during 2008, due to lower rates on interest earning assets.

Net Interest Margin Over Last Five Quarters

The Corporation’s tax equivalent net interest margin increased 22 basis points to 3.85% in the fourth quarter of 2009 from 3.63% in the same period in 2008. The reduction in the earning asset yield of 64 basis points was due to prime rate decreases, the current rate environment and competitive pricing pressure.

The interest bearing liability cost decreased in the fourth quarter of 2009 to 1.45%, a decrease of 97 basis points from the fourth quarter of 2008. This reduction was due primarily to aggressive management of deposit pricing and the maturity of higher rate wholesale deposits during 2009.

The tax equivalent net interest margin and related components for the past five linked quarters are shown in the table below.

| | | | | | | | | | | | | | | | | |

| | | Year | | Earning

Asset

Yield | | | Interest

Bearing

Liability

Cost | | | Net

Interest

Spread | | | Effect of

Non-Interest

Bearing

Sources | | | Net

Interest

Margin | |

Tax Equivalent Net Interest Margin Last Five Quarters | |

| | | | | | |

4thQuarter | | 2009 | | 4.99 | % | | 1.45 | % | | 3.54 | % | | 0.31 | % | | 3.85 | % |

3rdQuarter | | 2009 | | 5.09 | % | | 1.73 | % | | 3.36 | % | | 0.36 | % | | 3.72 | % |

2ndQuarter | | 2009 | | 5.13 | % | | 1.94 | % | | 3.19 | % | | 0.40 | % | | 3.59 | % |

1stQuarter | | 2009 | | 5.37 | % | | 2.15 | % | | 3.22 | % | | 0.40 | % | | 3.62 | % |

4thQuarter | | 2008 | | 5.63 | % | | 2.42 | % | | 3.21 | % | | 0.42 | % | | 3.63 | % |

| | | | | | |

| | | Year | | Earning

Asset

Yield | | | Interest

Bearing

Liability

Cost | | | Net

Interest

Spread | | | Effect of

Non-Interest

Bearing

Sources | | | Net

Interest

Margin | |

Tax Equivalent Net Interest Margin Last Three Years | | | |

| | | | | | |

| | 2009 | | 5.14 | % | | 1.81 | % | | 3.33 | % | | 0.37 | % | | 3.70 | % |

| | 2008 | | 5.98 | % | | 2.63 | % | | 3.35 | % | | 0.49 | % | | 3.84 | % |

| | 2007 | | 6.90 | % | | 3.32 | % | | 3.58 | % | | 0.79 | % | | 4.37 | % |

Interest Rate Sensitivity

The Corporation actively manages its interest rate sensitivity position. The objectives of interest rate risk management are to control exposure of net interest income to risks associated with interest rate movements and to achieve sustainable growth in net interest income. The Corporation’s Asset Liability Committee (“ALCO”), using policies and procedures approved by the Corporation’s Board of Directors, is responsible for managing the interest rate sensitivity position. The Corporation manages interest rate sensitivity by changing the mix, pricing and re-pricing characteristics of its assets and liabilities, through the management of its investment portfolio, its offering of loan and selected deposit terms and through wholesale funding. Wholesale funding consists of multiple sources including borrowings from the FHLB-P, Federal Reserve Bank of Philadelphia discount window, certificates of deposit from institutional brokers, Certificate of Deposit Account Registry Service (“CDARS”), Insured Network Deposit (“IND”) Program, Institutional Deposit Corporation (“IDC”) and Pennsylvania Local Government Investment Trust (“PLGIT”).

The Corporation uses several tools to manage its interest rate risk including interest rate sensitivity analysis (a/k/a “GAP Analysis”), market value of portfolio equity analysis, interest rate simulations under various rate scenarios and tax equivalent net interest margin reports. The results of these reports are compared to limits established by the Corporation’s ALCO Policies and appropriate adjustments are made if the results are outside of established limits.

The following table demonstrates the annualized result of an interest rate simulation and the estimated effect that a parallel interest rate shift in the yield curve and subjective adjustments in deposit pricing might have on the Corporation’s projected net interest income over the next 12 months.

This simulation assumes that there is no growth in the balance sheet over the next twelve months. The changes to net interest income shown below are in compliance with the Corporation’s policy guidelines.

9

Summary of Interest Rate Simulation

| | | | | | | |

| | | December 31, 2009 | |

| (dollars in thousands) | | Estimated Change

In Net Interest

Income Over

Next 12 Months | |

Change in Interest Rates | | | | | | | |

+300 basis points | | $ | 2,980 | | | 6.86 | % |

+200 basis points | | $ | 1,725 | | | 3.97 | % |

+100 basis points | | $ | (632 | ) | | (1.45 | )% |

-100 basis points | | $ | (1,313 | ) | | (3.02 | )% |

The interest rate simulation above indicates that the Corporation’s balance sheet as of December 31, 2009 is asset sensitive, meaning that a 100 basis point increase or decrease in interest rates will have a negative impact on net interest income over the next 12 months. Assets will not reprice as quickly as deposits since Bryn Mawr Trust’s prime rate is 74 basis points higher than the Wall Street Journal prime rate and there are interest rate floors on approximately all home equity lines of credit. The interest rate simulation is an estimate based on assumptions, which are based in part on past behavior of customers, along with expectations of future behavior relative to interest rate changes.

Actual results may differ from the interest rate simulation for many reasons including market reactions, competitor responses, regulatory actions and/or customer behavior, especially in these uncertain economic times, which could cause an unexpected outcome that may translate into lower net interest income.

GAP Report

The interest sensitivity or “GAP” report identifies interest rate risk by showing repricing gaps in the bank’s balance sheet. All assets and liabilities are reflected based on behavioral sensitivity, which is usually the earliest of either: repricing, maturity, contractual amortization, prepayments or likely call dates. Non-maturity deposits such as NOW, Savings and money market accounts are spread over various time periods based on the expected sensitivity of these rates considering liquidity and investment preferences for the bank. Non-rate sensitive assets and liabilities are spread over time periods to reflect how the Corporation views the maturity of these funds.

Non-maturity deposits, demand deposits in particular, are recognized by the regulatory agencies to have different sensitivities to interest rate environments. Consequently, it is an accepted practice to spread non-maturity deposits over defined time periods in order to capture that sensitivity. Commercial demand deposits are often in the form of compensating balances, and fluctuate inversely to the level of interest rates; the maturity of those deposits is reported as having a shorter life than typical retail demand deposits. Additionally, the regulatory agencies have suggested distribution limits are for non-maturity deposits. However, the Corporation has taken a more conservative approach than these limits would imply by reporting them as having a shorter maturity. The following table presents the Corporation’s GAP Analysis as of December 31, 2009:

| | | | | | | | | | | | | | | | | | | | | | | | |

| (dollars in thousands) | | 0 to 90

Days | | | 91 to 365

Days | | | 1 - 5

Years | | | Over

5 Years | | | Non-Rate

Sensitive | | | Total | |

Assets: | | | | | | | | | | | | | | | | | | | | | | | | |

Interest-bearing deposits with banks | | $ | 58.5 | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | 58.5 | |

Money market funds | | | 9.2 | | | | — | | | | — | | | | — | | | | — | | | | 9.2 | |

Investment securities | | | 67.2 | | | | 37.9 | | | | 55.3 | | | | 47.8 | | | | — | | | | 208.2 | |

Loans and leases(1) | | | 369.7 | | | | 84.5 | | | | 374.4 | | | | 60.1 | | | | — | | | | 888.7 | |

Allowance | | | — | | | | — | | | | — | | | | — | | | | (10.4 | ) | | | (10.4 | ) |

Cash and due from banks | | | — | | | | — | | | | — | | | | — | | | | 11.7 | | | | 11.7 | |

Other assets | | | — | | | | — | | | | 0.6 | | | | 0.1 | | | | 72.2 | | | | 72.9 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 504.6 | | | $ | 122.4 | | | $ | 430.3 | | | $ | 108.0 | | | $ | 73.5 | | | $ | 1,238.8 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Liabilities and shareholders’ equity: | | | | | | | | | | | | | | | | | | | | | | | | |

Demand, non-interest-bearing | | $ | 79.2 | | | | 21.1 | | | | 112.6 | | | | — | | | | — | | | | 212.9 | |

Savings, NOW and market rate | | | 83.5 | | | | 73.4 | | | | 260.9 | | | | 65.1 | | | | — | | | | 482.9 | |

Time deposits | | | 97.7 | | | | 45.3 | | | | 10.7 | | | | 0.1 | | | | — | | | | 153.8 | |

Other wholesale deposits | | | 52.2 | | | | — | | | | — | | | | — | | | | — | | | | 52.2 | |