Shareholders Annual Meeting

April 25, 2013

Bryn Mawr Bank Corporation

NASDAQ: BMTC

Strong—Stable—Secure

Safe Harbor

This presentation contains statements which, to the extent that they are not recitations of historical fact may constitute forward-looking statements for purposes of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended.

Please see the section titled Safe Harbor begins on slide 32 for more information regarding these types of statements.

The information contained in this presentation is correct only as of April 25, 2013. Our business, financial condition, results of operations and prospects may have changed since that date, and we do not undertake to update such information.

1

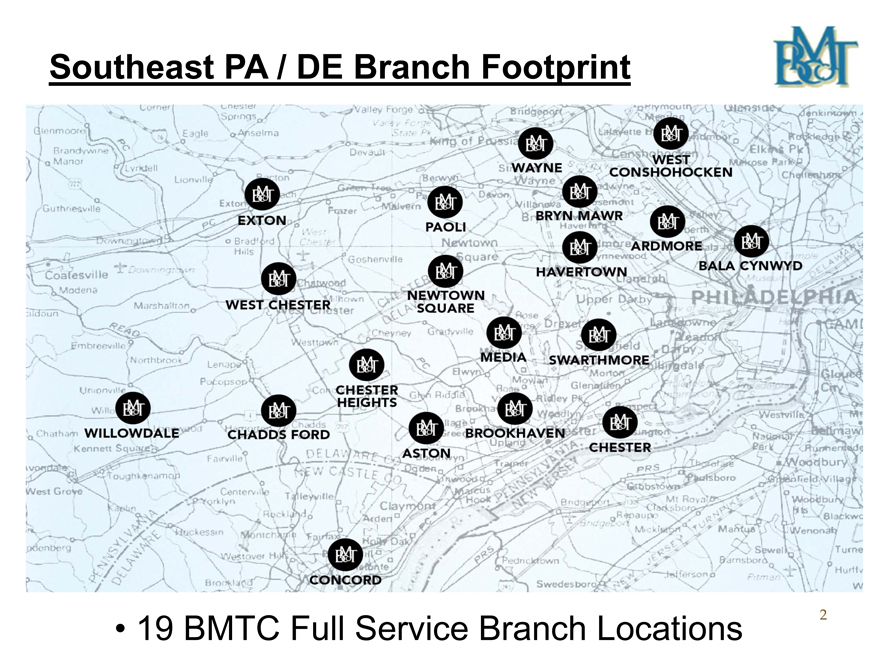

Southeast PA / DE Branch Footprint

• 19 BMTC Full Service Branch Locations

2

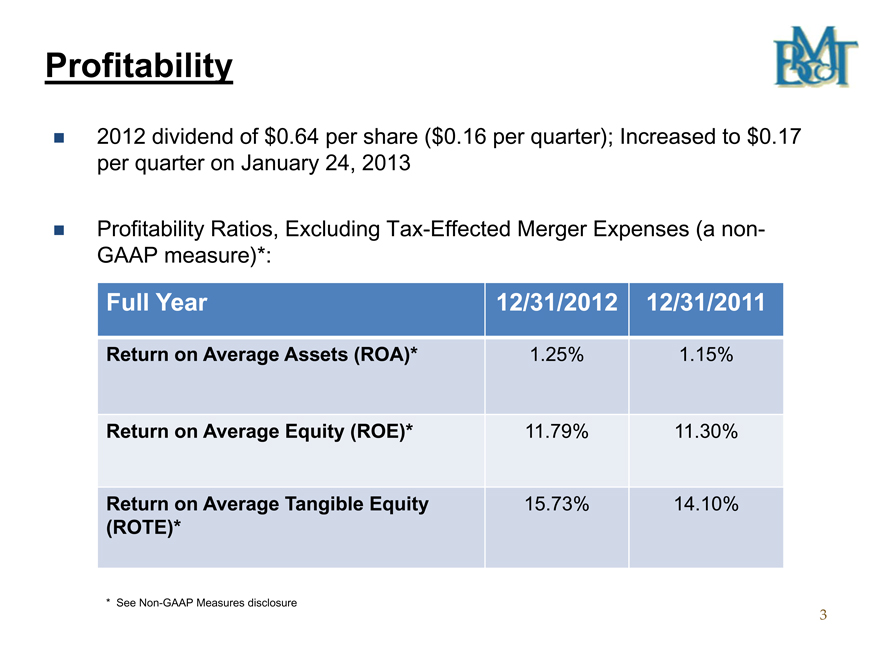

Profitability

2012 dividend of $0.64 per share ($0.16 per quarter); Increased to $0.17 per quarter on January 24, 2013

Profitability Ratios, Excluding Tax-Effected Merger Expenses (a non-GAAP measure)*:

Full Year 12/31/2012 12/31/2011

Return on Average Assets (ROA)* 1.25% 1.15%

Return on Average Equity (ROE)* 11.79% 11.30%

Return on Average Tangible Equity 15.73% 14.10%

(ROTE)*

* See Non-GAAP Measures disclosure

3

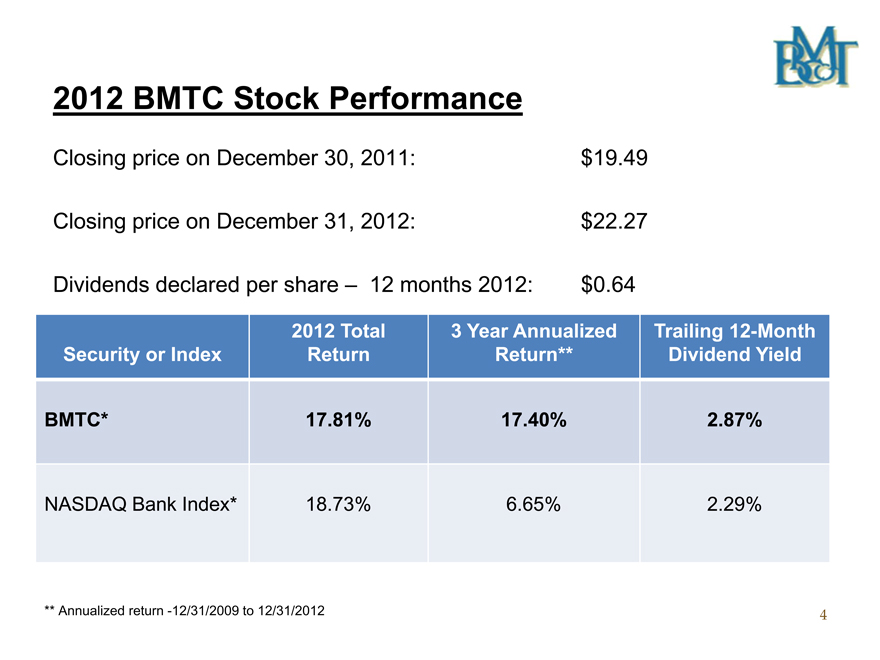

2012 BMTC Stock Performance

Closing price on December 30, 2011: $19.49 Closing price on December 31, 2012: $22.27 Dividends declared per share 12 months 2012: $0.64

2012 Total 3 Year Annualized Trailing 12-Month

Security or Index Return Return** Dividend Yield

BMTC* 17.81% 17.40% 2.87%

NASDAQ Bank Index* 18.73% 6.65% 2.29%

** Annualized return -12/31/2009 to 12/31/2012

4

Growth Initiatives

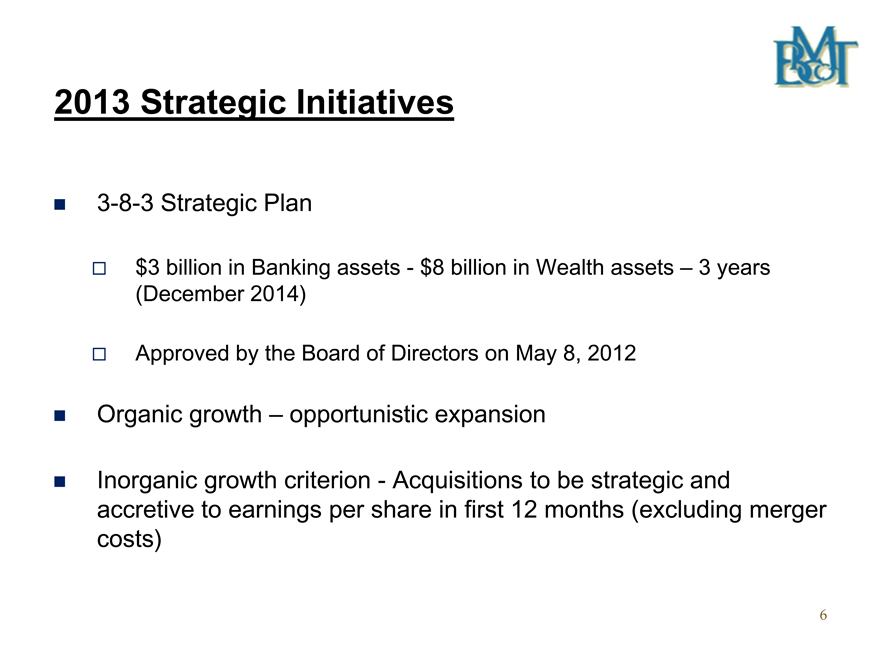

2013 Strategic Initiatives

3-8-3 Strategic Plan

$3 billion in Banking assets—$8 billion in Wealth assets – 3 years (December 2014)

Approved by the Board of Directors on May 8, 2012

Organic growth – opportunistic expansion

Inorganic growth criterion—Acquisitions to be strategic and accretive to earnings per share in first 12 months (excluding merger costs)

6

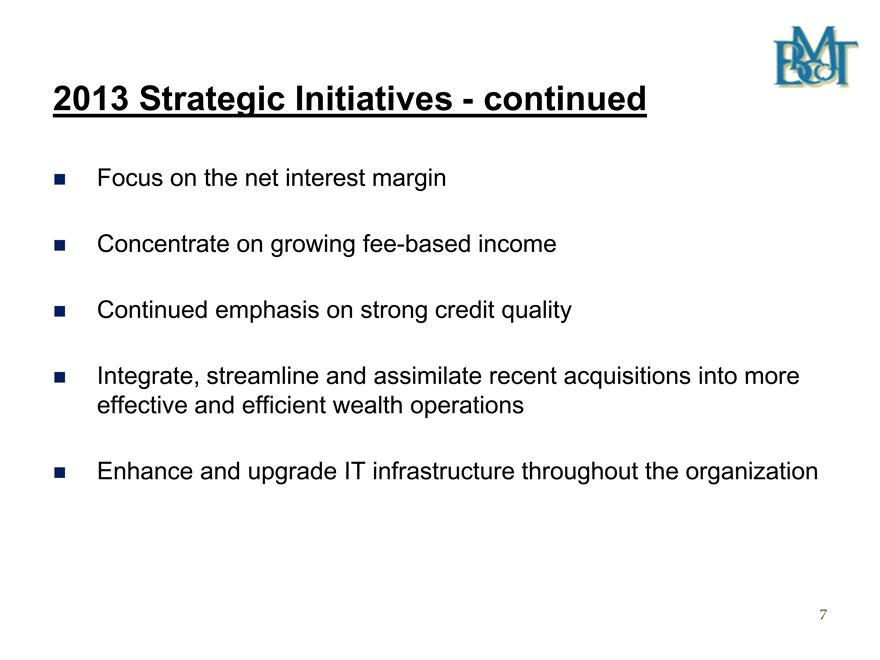

2013 Strategic Initiatives—continued

Focus on the net interest margin

Concentrate on growing fee-based income

Continued emphasis on strong credit quality

Integrate, streamline and assimilate recent acquisitions into more effective and efficient wealth operations

Enhance and upgrade IT infrastructure throughout the organization

7

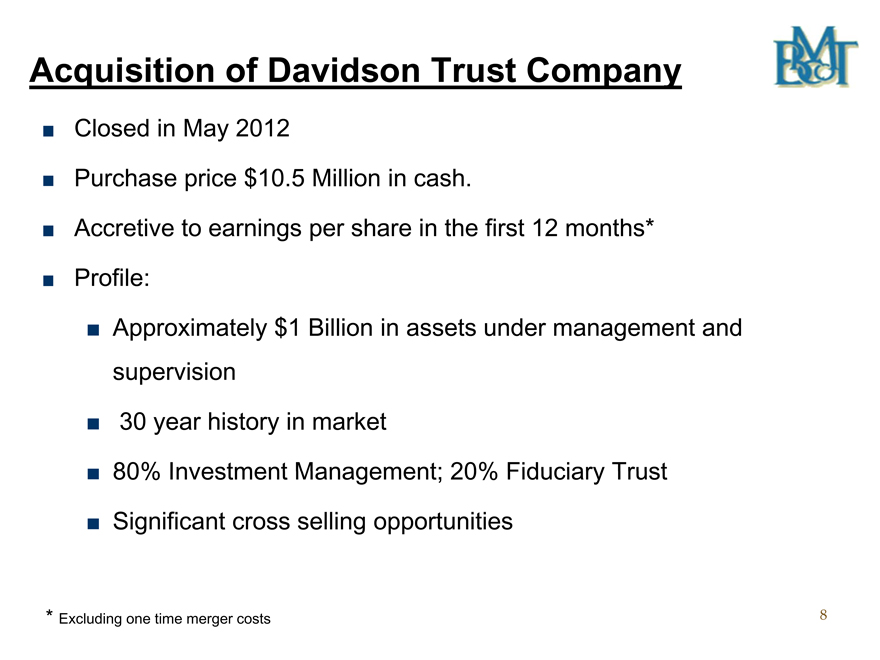

Acquisition of Davidson Trust Company

Closed in May 2012

Purchase price $10.5 Million in cash.

Accretive to earnings per share in the first 12 months*

Profile:

Approximately $1 Billion in assets under management and supervision

30 year history in market

80% Investment Management; 20% Fiduciary Trust Significant cross selling opportunities

* Excluding one time merger costs

8

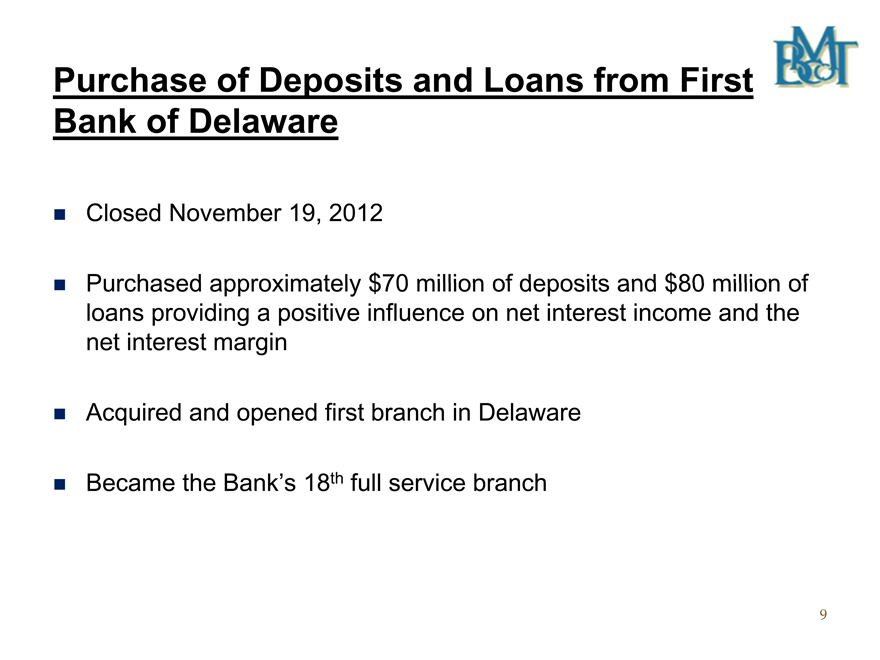

Purchase of Deposits and Loans from First Bank of Delaware

Closed November 19, 2012

Purchased approximately $70 million of deposits and $80 million of loans providing a positive influence on net interest income and the net interest margin

Acquired and opened first branch in Delaware

Became the Bank’s 18th full service branch

9

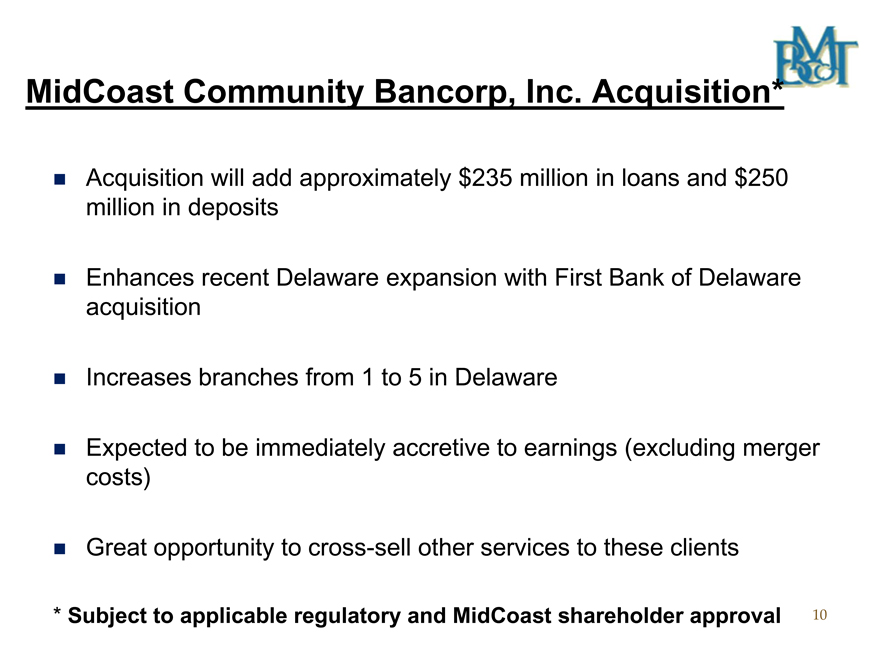

MidCoast Community Bancorp, Inc. Acquisition*

Acquisition will add approximately $235 million in loans and $250 million in deposits

Enhances recent Delaware expansion with First Bank of Delaware acquisition

Increases branches from 1 to 5 in Delaware

Expected to be immediately accretive to earnings (excluding merger costs)

Great opportunity to cross-sell other services to these clients

* Subject to applicable regulatory and MidCoast shareholder approval 10

10

Financial Review

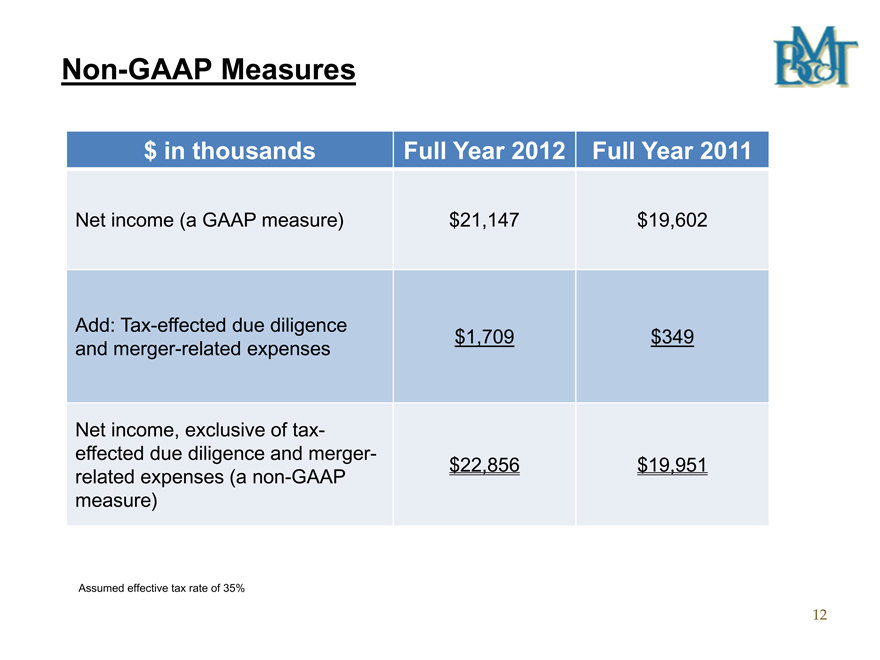

Non-GAAP Measures

$ in thousands Full Year 2012 Full Year 2011

Net income (a GAAP measure) $21,147 $19,602

Add: Tax-effected due diligence

and merger-related expenses $1,709 $349

Net income, exclusive of tax-

effected due diligence and merger-

related expenses (a non-GAAP $22,856 $19,951

measure)

Assumed effective tax rate of 35%

12

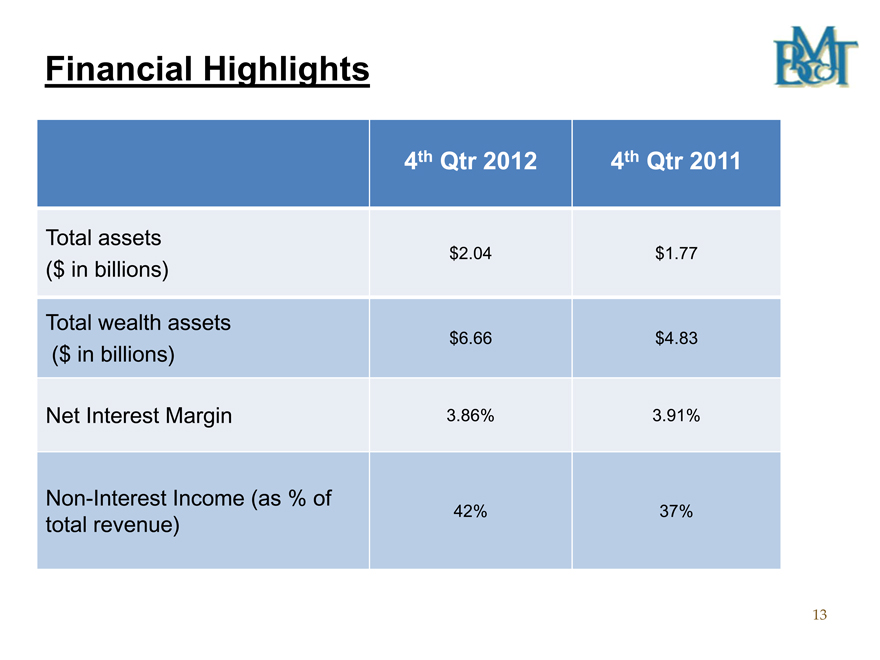

Financial Highlights

4th Qtr 2012 4th Qtr 2011

Total assets

$ 2.04 $ 1.77

($ in billions)

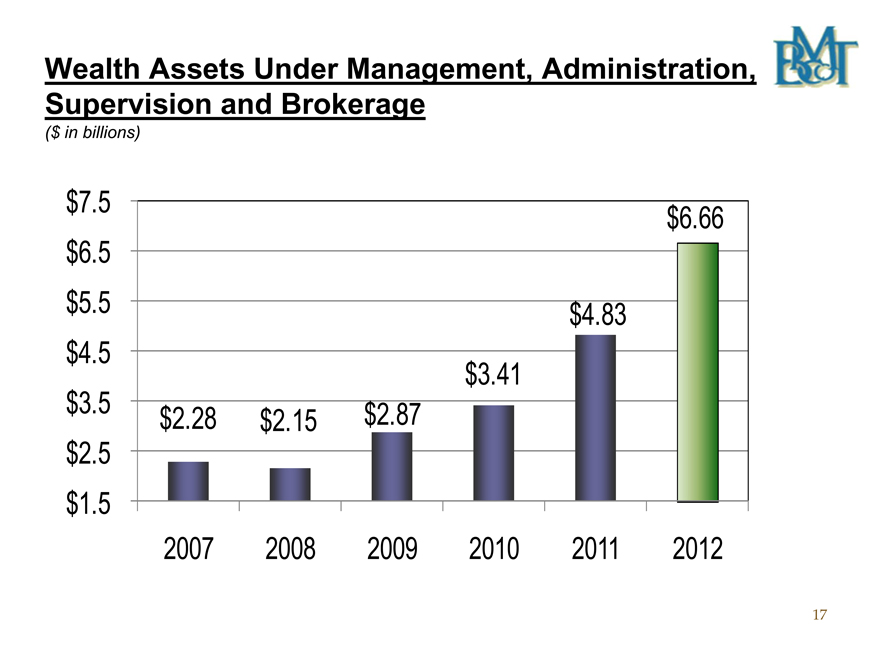

Total wealth assets

$ 6.66 $ 4.83

($ in billions)

Net Interest Margin 3.86% 3.91%

Non-Interest Income (as % of

total revenue) 42% 37%

13

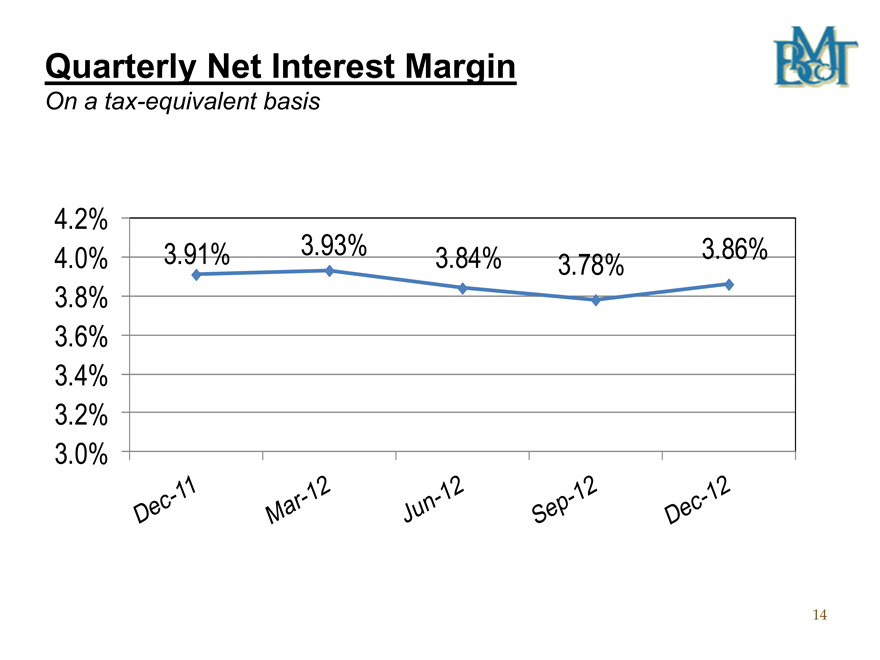

Quarterly Net Interest Margin

On a tax-equivalent basis

4.2%

4.0% 3.91% 3.93% 3.84% 3.78% 3.86%

3.8%

3.6%

34%.

3.2%

3.0%

14

Capital Considerations

Maintain a “well capitalized” capital position including a target tangible common equity to tangible asset ratio of 8.00%

Selectively add capital to maintain capital levels and fund asset growth and acquisitions

15

Wealth Division Review

Wealth Assets Under Management, Administration, Supervision and Brokerage

($ in billions)

$7.5 $ 6.66

$ 6.5

$ 5.5 $ 4.83

$ 4.5

$ 3.41

$ 3.5 $ 2.28 $ 2.15 $ 2.87

$ 2.5

$ 1.5

2007 2008 2009 2010 2011 2012

17

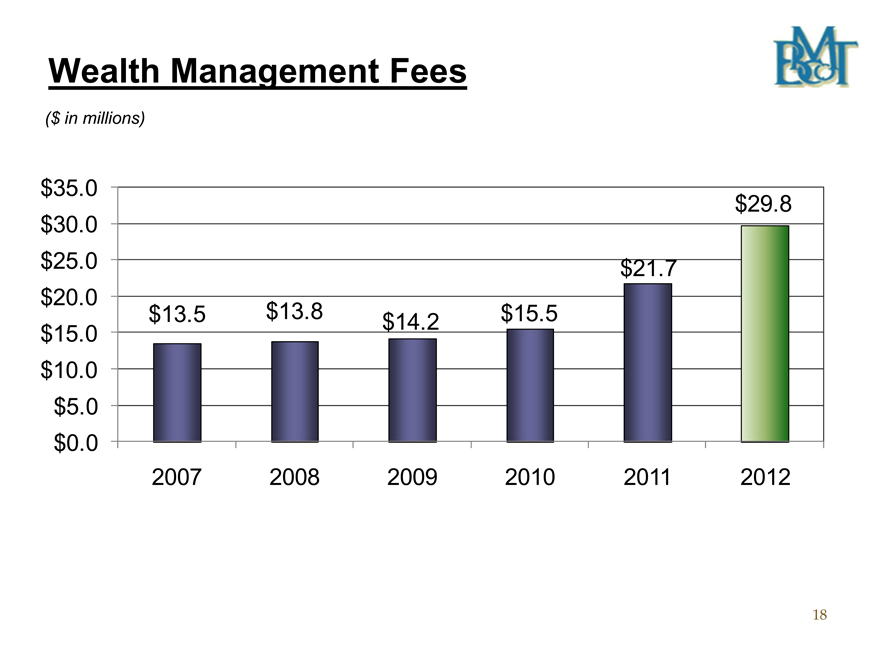

Wealth Management Fees

($ in millions)

$35.0 $29.8

$30.0

$25.0 $21.7

$20.0 $13.5 $13.8 $15.5

$15.0 $14.2

$10.0

$5.0

$0.0

2007 2008 2009 2010 2011 2012

18

Credit Review

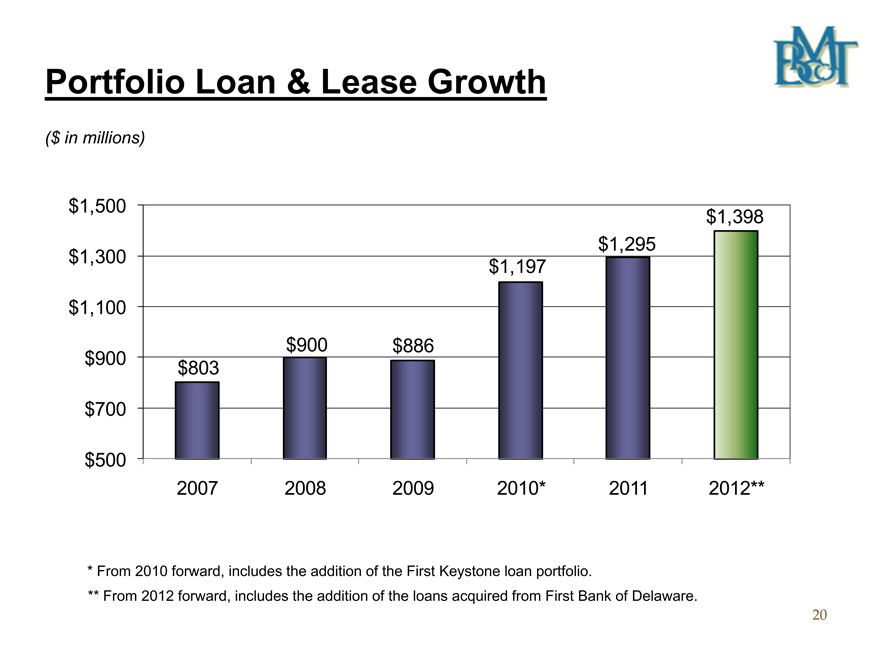

Portfolio Loan & Lease Growth

($ in millions)

$1,500 $1,398

$1,295

$1,300 $1,197

$1,100

$900 $886

$900 $803

$700

$500

2007 2008 2009 2010* 2011 2012**

* From 2010 forward, includes the addition of the First Keystone loan portfolio.

** From 2012 forward, includes the addition of the loans acquired from First Bank of Delaware.

20

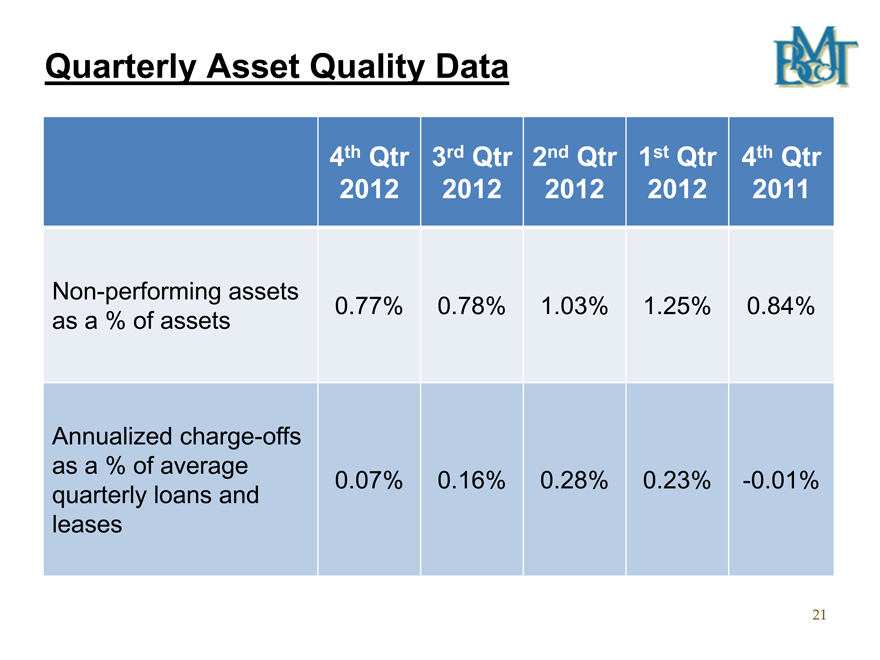

Quarterly Asset Quality Data

4th Qtr 3rd Qtr 2nd Qtr 1st Qtr 4th Qtr

2012 2012 2012 2012 2011

Non-performing assets 0.77% 0.78% 1.03% 1.25% 0.84%

as a % of assets

Annualized charge-offs

as a % of average

quarterly loans and 0.07% 0.16% 0.28% 0.23% -0.01%

leases

21

Summary

Outstanding franchise in a stable market

Focus on Wealth Services, Business Banking and Residential Mortgage

Diversified income base – non interest income 42% of total revenue for the twelve months ended December 21, 2012

Outstanding loan quality in a difficult economic environment

Sound business strategy, strong asset quality, well capitalized and solid risk management procedures serve as a foundation for potential strategic expansion

Focus on earnings per share growth

22

Important Information

On March 27, 2013, Bryn Mawr Bank Corporation (“BMBC”) and MidCoast Community Bancorp, Inc. (“MCBI”) entered into an Agreement and Plan of Merger pursuant to which MCBI will merge with and into BMBC (the “Merger”).

BMBC will file with the SEC a Registration Statement on Form S-4 concerning the Merger. The Registration Statement will include a prospectus for the offer and sale of BMBC common stock to MCBI shareholders as well as a proxy statement of MCBI for the solicitation of proxies from its shareholders for use at the meeting at which the Merger will be voted upon. The combined prospectus and proxy statement and other documents filed by BMBC with the SEC will contain important information about BMBC, MCBI, and the Merger. We urge investors and MCBI shareholders to read carefully the combined prospectus and proxy statement and other documents filed with the SEC, including any amendments or supplements also filed with the SEC. MCBI shareholders in particular should read the combined prospectus and proxy statement carefully before making a decision concerning the Merger. Investors and shareholders will be able to obtain a free copy of the combined prospectus and proxy statement – along with other filings containing information about BMBC – at the SEC’s website at http://www.sec.gov. Copies of the combined prospectus and proxy statement, and the filings with the SEC incorporated by reference in the combined prospectus and proxy statement, can also be obtained free of charge by directing a request to Bryn Mawr Bank Corporation, 801 Lancaster Avenue, Bryn Mawr, PA 19010, attention Geoffrey L. Halberstadt, Secretary, telephone (610) 581-4873.

MCBI, BMBC and certain of their directors and executive officers may, under the rules of the SEC, be deemed to be “participants” in the solicitation of proxies from shareholders in connection with the Merger. Information concerning the interests of the persons who may be considered “participants” in the solicitation as well as additional information concerning MCBI’s and BMBC’s directors and executive officers will be set forth in the combined prospectus and proxy statement relating to the Merger. Information concerning BMBC’s directors and executive officers is also set forth in BMBC’s proxy statement and annual report on Form 10-K (including any amendments thereto), previously filed with the SEC.

This communication shall not constitute an offer to sell or the solicitation of an offer to buy any securities nor shall there be any sale of securities in any jurisdiction in which the offer, solicitation, or sale is unlawful before registration or qualification of the securities under the securities laws of the jurisdiction. No offer of securities shall be made except by means of a prospectus satisfying the requirements of Section 10 of the Securities Act of 1933, as amended.

23