UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04852

Victory Portfolios

(Exact name of registrant as specified in charter)

| 4900 Tiedeman Road, 4th Floor, Brooklyn, Ohio | 44144 |

| (Address of principal executive offices) | (Zip code) |

Citi Fund Services Ohio, Inc., 4400 Easton Commons, Suite 200, Columbus, Ohio 43219

(Name and address of agent for service)

Registrant’s telephone number, including area code: 800-539-3863

Date of fiscal year end: December 31

Date of reporting period: December 31, 2022

Item 1. Reports to Stockholders.

December 31, 2022

Annual Report

Victory RS Partners Fund

Victory RS Value Fund

Victory RS Large Cap Alpha Fund

Victory RS Investors Fund

Victory Global Energy Transition Fund

vcm.com

News, Information And Education 24 Hours A Day, 7 Days A Week

The Victory Capital website gives fund shareholders, prospective shareholders, and investment professionals a convenient way to access fund information, get guidance, and track fund performance anywhere they can access the Internet. The site includes:

• Detailed performance records

• Daily share prices

• The latest fund news

• Investment resources to help you become a better investor

• A section dedicated to investment professionals

Whether you're a potential investor searching for the fund that matches your investment philosophy, a seasoned investor interested in planning tools, or an investment professional, vcm.com has what you seek. Visit us anytime. We're always open.

Victory Portfolios

TABLE OF CONTENTS

Shareholder Letter (Unaudited) | 3 | ||||||

| Managers' Commentary / Investment Overview (Unaudited) | 5 | ||||||

| Investment Objective and Portfolio Holdings (Unaudited) | 19 | ||||||

Schedules of Portfolio Investments | |||||||

Victory RS Partners Fund | 24 | ||||||

Victory RS Value Fund | 27 | ||||||

Victory RS Large Cap Alpha Fund | 29 | ||||||

Victory RS Investors Fund | 31 | ||||||

Victory Global Energy Transition Fund | 33 | ||||||

Financial Statements | |||||||

Statements of Assets and Liabilities | 35 | ||||||

Statements of Operations | 37 | ||||||

Statements of Changes in Net Assets | 39 | ||||||

Financial Highlights | 44 | ||||||

Notes to Financial Statements | 64 | ||||||

| Report of Independent Registered Public Accounting Firm | 77 | ||||||

Supplemental Information (Unaudited) | 78 | ||||||

Trustee and Officer Information | 78 | ||||||

Proxy Voting and Portfolio Holdings Information | 81 | ||||||

Expense Examples | 81 | ||||||

Additional Federal Income Tax Information | 83 | ||||||

Advisory Contract Approval | 84 | ||||||

Privacy Policy (inside back cover) | |||||||

1

IRA DISTRIBUTION WITHHOLDING DISCLOSURE

We generally must withhold federal income tax at a rate of 10% of the taxable portion of your distribution and, if you live in a state that requires state income tax withholding, at your state's tax rate. However, you may elect not to have withholding apply or to have income tax withheld at a higher rate. Any withholding election that you make will apply to any subsequent distribution unless and until you change or revoke the election. If you wish to make a withholding election, or change or revoke a prior withholding election, call 800-539-3863 (800-235-8396 for Member Class) and form W-4P (OMB No. 1545-0074 withholding certificate for pension or annuity payments) will be electronically sent.

If you do not have a withholding election in place by the date of a distribution, federal income tax will be withheld from the taxable portion of your distribution at a rate of 10%. If you must pay estimated taxes, you may be subject to estimated tax penalties if your estimated tax payments are not sufficient and sufficient tax is not withheld from your distribution.

For more specific information, please consult your tax adviser.

The Funds are distributed by Victory Capital Services, Inc. Victory Capital Management Inc. is the investment adviser to the Funds and receives fees from the Funds for performing services for the Funds.

This report is not authorized for distribution to prospective investors unless preceded or accompanied by a current prospectus of the Victory Funds.

For additional information about any Victory Fund, including fees, expenses, and risks, view our prospectus online at vcm.com or call 800-539-3863 (800-235-8396 for Member Class). Read it carefully before you invest or send money.

The information in this report is based on data obtained from recognized services and sources and is believed to be reliable. Any opinions, projections, or recommendations in this report are subject to change without notice and are not intended as individual investment advice. Past investment performance of the Funds, markets or securities mentioned herein should not be considered to be indicative of future results.

• NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

Call Victory at:

800-539-FUND (800-539-3863)

800-235-8396 for Member Class

Visit our website at:

vcm.com

2

Victory Funds Letter to Shareholders

(Unaudited)

Dear Shareholder,

Our most recent annual reporting period ending December 31, 2022, was filled with epic challenges. Even the most seasoned investors who have been through more than one economic cycle have not witnessed financial markets like this in a long time, if ever.

Consider what transpired and how the investing backdrop changed so abruptly. The year began well enough with ample liquidity and an encouraging outlook for corporate profits. But that optimism faded early and was punctuated by the start of a terrible war in Eastern Europe. This fueled rising energy prices and intensified an inflation problem that was proving to be more than "transitory."

The inflation data was particularly troublesome and surprised many with some of the highest readings since the 1970s. In response, the U.S. Federal Reserve (the "Fed") pivoted to a far more restrictive monetary policy than anyone anticipated. Over the course of 2022, the Fed boosted the Fed funds interest rate on seven different occasions by a total of 4.5 percentage points. And if that wasn't enough, zero-Covid policies in China further exacerbated supply chain issues and dampened the outlook for global growth.

As one might expect, all of these obstacles ratcheted up volatility across financial markets. Broad market stock indices pulled back substantially around the world. The S&P 500® Index, the bell-weather proxy for our domestic stock market, delivered a negative total return of more than 18% for our annual reporting period.

Perhaps what made 2022 even more difficult was the performance of fixed income markets, which normally are considered a safe haven in times of equity turmoil. But not this past year. In fact, the Bloomberg US Aggregate Bond Index—a proxy for a diversified fixed income portfolio and one that many investors and institutions follow closely—delivered a negative total return of approximately 13%, its worst annual performance since the 1970s. That's not exactly the offset to equity performance that many investors were expecting from bonds.

It was a tough year, and we fully acknowledge that the steady drumbeat of bad news and bouts of stomach-churning volatility can take a toll on investors' psyche. Nobody likes opening their account statements during declining markets; and even when markets snap back sharply (as happened this past July and October), investors often wonder if they have missed an opportunity.

Through all of the challenges in our most recent annual reporting period, we are reminded of two enduring realities: 1) financial markets are dynamic and apt to change abruptly; 2) it's vital that we remain calm and rational whenever faced with those inevitable bouts of turmoil.

Fortunately, we think that investors can take comfort knowing that all of our independent investment franchises have experience managing portfolios through a wide variety of market environments. Our investment professionals remain calm during turbulent financial markets, and we think it's imperative that investors do the same.

3

We still believe that a long-term plan, a well-diversified portfolio across asset classes and investment types, and a clear understanding of individual risk tolerances are the key ingredients for staying the course and progressing on investment goals. Moreover, all our investment professionals continually monitor the environment and work hard to position portfolios opportunistically no matter what the markets bring. Remember, turmoil can also create opportunity.

On the following pages you will find information relating to your Victory Funds investment. If you have any questions, we encourage you to contact your financial advisor. If you invest with us directly, you may call 800-539-3863 (800-235-8396 for Member Class) or visit our website at vcm.com.

From all of us here at Victory Capital, thank you for your ongoing confidence and for letting us help you work toward your investment goals.

Christopher K. Dyer, CFA

President,

Victory Funds

4

Victory RS Partners Fund

Managers' Commentary

(Unaudited)

What were the market conditions during the reporting period?

The fourth quarter of 2022 certainly began well enough, even as the year ended on a downbeat. Financial markets had been languishing all year and were in the doldrums as summer ended, but most segments of the equity market bounced back sharply in October and November thanks to better-than-expected earnings and signs that inflation may have peaked. Value stocks led the way, with the Russell 1000® Value Index up 10.25% in October and an additional 6.25% in November, while the Russell 2000® Value Index was up 12.59% in October and 3.06% in November. Unfortunately, that euphoria was short-lived.

Sentiment soured once again in December as investors began to digest how hawkish the U.S. Federal Reserve (the "Fed") really intended to be, given its repeated statements that it would not stop hiking the Fed funds interest rate until inflation was well in check irrespective of the impact to the broader economy. Some investors and corporate leaders began to question whether Fed Chair Jerome Powell was up to the task of maintaining an economic environment supportive of corporate growth while still taming inflation.

These growing concerns turned into a full-fledged market sell-off in December, with the Russell 1000® Value Index shedding 4.03% and the Russell 2000® Value Index falling 6.56%. This reflected some poor earnings guidance by corporations and ongoing hawkish comments by Chairman Powell. In fact, the Chairman bluntly told market participants, "Fed hikes and volatility have been central themes of 2022, and investors should expect both — along with hits to corporate earnings — as we enter the new year." On top of that, he braced investors for the possibility of a recession in 2023. All this economic uncertainty merely exacerbated the interest rate backdrop and highlighted the difficulties facing the Fed in carrying out its dual monetary policy goals.

Yet despite the volatility and challenges in the fourth quarter, it was not all bad news as we closed out 2022. For starters, we believe the worst inflation numbers are behind us. Demand for goods has decreased, as evidenced by higher inventories among retailers and a continued decline in energy prices globally. This should eventually provide some relief for battered markets. There are even reasons for optimism within certain sectors of the economy (and individual companies). Chief among these is the fact that select corporate operations (and earnings) have come in better than expected, which means the market decline has improved valuations and may be creating a more favorable risk-reward tradeoff going forward.

In terms of the overall numbers for our area of focus — domestic value-oriented strategies — the Russell 3000® Value Index was up 12.18% during the fourth quarter and was down 7.98% for the full year. In terms of market capitalizations, small-cap value stocks, as represented by the Russell 2000® Value Index (the "Index"), declined 14.48% for the year. The Russell Midcap® Value Index declined by 12.03% for the full year, while large-cap value stocks, as represented by the Russell 1000® Value Index, posted an annual decline of 7.54%.

Looking ahead, many investors are not only wondering just how restrictive monetary policy will become, but also how healthy the economy really is. Of course, nobody can answer these questions with absolute certainty, but we can definitively say that the current investment landscape continues to be polarizing, and we would not be surprised to see further bouts of elevated volatility in 2023.

5

Victory RS Partners Fund

Managers' Commentary (continued)

How did Victory RS Partners Fund (the "Fund") perform during the reporting period?

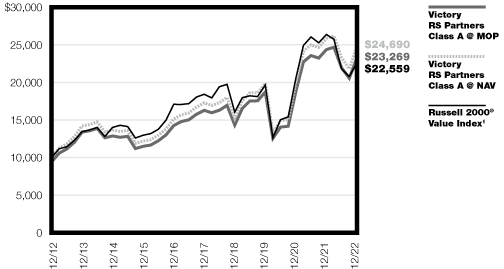

The Fund returned -4.54% (Class A at net asset value) for the fiscal year ended December 31, 2022, outperforming the Index, which returned -14.48% for the reporting period.

What strategies did you employ during the reporting period?

The Fund outperformed the Index primarily through stock selection in the Financials and Industrials sectors. Our focus on businesses that have the potential for long-term value creation while limiting our downside paid off during 2022. For the year, the stocks that provided positive contribution tended to be undergoing a unique structural change, but also holding a competitive advantage. Within the Financials sector, Globe Life, Inc. and White Mountains Insurance Group Ltd. were significant positive contributors to performance. The Industrials sector provided other names that benefitted the portfolio. Meritor, Inc. and Fluor Corp. led performance. Where we struggled was in a couple of our holdings in the Technology sector. NCR Corp. saw its share price fall as supply chain issues, coupled with uncertainty surrounding the company's strategic review, pressured the share price. Euronet Worldwide, Inc. continued to experience pressure on the travel segment of its ATM business, which impacted the share price. At the end of the day, we managed to outperform the Index in 2022, and we remain confident in our process and feel it will provide us with the discipline which leads to longer-term performance which will benefit our investors over time.

We continue to believe that the current environment is creating potential pockets of opportunity for astute, long-term investors. Our experience has taught us that any tumultuous market backdrop (and the subsequent short-term price dislocations) can be an advantage for active managers. Our team continues to seek and identify companies that share two vital traits: a trend of improving their ROIC (return on invested capital), and stock prices trading at what we perceive as a deep discount to intrinsic value. We believe that allocating to these types of companies is a means to generate attractive risk-adjusted returns over longer time periods, and this continues to be a primary focus for us.

6

Victory RS Partners Fund

Investment Overview

(Unaudited)

Average Annual Total Return

Year Ended December 31, 2022

Class A | Class R | Class Y | Member Class | ||||||||||||||||||||||||

INCEPTION DATE | 7/12/95 | 10/13/06 | 5/1/07 | 11/2/20 | |||||||||||||||||||||||

| Net Asset Value | Maximum Offering Price | Net Asset Value | Net Asset Value | Net Asset Value | Russell 2000® Value Index1 | ||||||||||||||||||||||

One Year | –4.54 | % | –10.04 | % | –4.86 | % | –4.23 | % | –4.36 | % | –14.48 | % | |||||||||||||||

Five Year | 7.40 | % | 6.13 | % | �� | 7.01 | % | 7.75 | % | N/A | 4.13 | % | |||||||||||||||

Ten Year | 9.46 | % | 8.81 | % | 9.07 | % | 9.82 | % | N/A | 8.48 | % | ||||||||||||||||

Since Inception | N/A | N/A | N/A | N/A | 22.68 | % | N/A | ||||||||||||||||||||

The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month's end, please visit vcm.com.

The maximum offering price figures reflect a maximum sales charge of 5.75% for Class A. Net Asset Value does not reflect sales charges. Total return measures the price change in a share assuming the reinvestment of all net investment income and realized capital gain distributions, if any. The total returns quoted do not reflect adjustments made to the enclosed financial statements in accordance with U.S. Generally Accepted Accounting Principles or the deduction of taxes that a shareholder would pay on net investment income and realized capital gain distributions, including reinvested distributions, or redemptions of shares. The total return figures set forth above include all waivers of fees. Without such fee waivers, the total returns would have been lower.

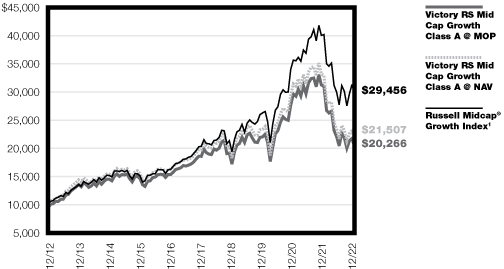

Victory RS Partners Fund — Growth of $10,000

1The Russell 2000® Value Index is an unmanaged index that measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000® companies with lower price-to-book ratios and lower forecasted growth values. Index results assume the reinvestment of dividends paid on the stocks constituting the index. This index does not include the effect of sales charges, commissions, expenses, or taxes, is not representative of the Fund, and it is not possible to invest directly in an index.

The graph reflects investment of growth of a hypothetical $10,000 investment in the Fund.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares.

Past performance is not indicative of future results.

7

Victory RS Value Fund

Managers' Commentary

(Unaudited)

What were the market conditions during the reporting period?

The fourth quarter of 2022 certainly began well enough, even as the year ended on a downbeat. Financial markets had been languishing all year and were in the doldrums as summer ended, but most segments of the equity market bounced back sharply in October and November thanks to better-than-expected earnings and signs that inflation may have peaked. Value stocks led the way, with the Russell 1000® Value Index up 10.25% in October and an additional 6.25% in November, while the Russell 2000® Value Index was up 12.59% in October and 3.06% in November. Unfortunately, that euphoria was short-lived.

Sentiment soured once again in December as investors began to digest how hawkish the U.S. Federal Reserve (the "Fed") really intended to be, given its repeated statements that it would not stop hiking the Fed funds interest rate until inflation was well in check irrespective of the impact to the broader economy. Some investors and corporate leaders began to question whether Fed Chair Jerome Powell was up to the task of maintaining an economic environment supportive of corporate growth while still taming inflation.

These growing concerns turned into a full-fledged market sell-off in December, with the Russell 1000® Value Index shedding 4.03% and the Russell 2000® Value Index falling 6.56%. This reflected some poor earnings guidance by corporations and ongoing hawkish comments by Chairman Powell. In fact, the Chairman bluntly told market participants, "Fed hikes and volatility have been central themes of 2022, and investors should expect both — along with hits to corporate earnings — as we enter the new year." On top of that, he braced investors for the possibility of a recession in 2023. All this economic uncertainty merely exacerbated the interest rate backdrop and highlighted the difficulties facing the Fed in carrying out its dual monetary policy goals.

Yet despite the volatility and challenges in the fourth quarter, it was not all bad news as we closed out 2022. For starters, we believe the worst inflation numbers are behind us. Demand for goods has decreased, as evidenced by higher inventories among retailers and a continued decline in energy prices globally. This should eventually provide some relief for battered markets. There are even reasons for optimism within certain sectors of the economy (and individual companies). Chief among these is the fact that select corporate operations (and earnings) have come in better than expected, which means the market decline has improved valuations and may be creating a more favorable risk-reward tradeoff going forward.

In terms of the overall numbers for our area of focus — domestic value-oriented strategies — the Russell 3000® Value Index was up 12.18% during the fourth quarter and was down 7.98% for the full year. In terms of market capitalizations, small-cap value stocks, as represented by the Russell 2000® Value Index, declined 14.48% for the year. The Russell Midcap® Value Index (the "Index") declined by 12.03% for the full year, while large-cap value stocks, as represented by the Russell 1000® Value Index, posted an annual decline of 7.54%.

Looking ahead, many investors are not only wondering just how restrictive monetary policy will become, but also how healthy the economy really is. Of course, nobody can answer these questions with absolute certainty, but we can definitively say that the current investment landscape continues to be polarizing, and we would not be surprised to see further bouts of elevated volatility in 2023.

8

Victory RS Value Fund

Managers' Commentary (continued)

How did Victory RS Value Fund (the "Fund") perform during the reporting period?

The Fund returned -2.97% (Class A at net asset value) for the fiscal year ended December 31, 2022, outperforming the Index, which returned -12.03% for the reporting period.

What strategies did you employ during the reporting period?

The Fund outperformed the Index primarily through stock selection in the Financials and Industrials sectors. Our focus on businesses that have the potential for long-term value creation while limiting our downside paid off during 2022. For the year, the stocks that provided positive contribution tended to be undergoing a unique structural change, but also holding a competitive advantage. Within the Financials sector, Globe Life, Inc. and Progressive Corp. were significant positive contributors to performance. The Industrials sector provided other names that benefitted the portfolio. Fluor Corp. and Curtiss-Wright Corp. led performance. Where we struggled was in a couple of our holdings in the Technology sector. NCR Corp. saw its share price fall as supply chain issues, coupled with uncertainty surrounding the company's strategic review, pressured the share price. Euronet Worldwide, Inc. continued to experience pressure on the travel segment of its ATM business, which impacted the share price. At the end of the day, we managed to outperform the Index in 2022, and we remain confident in our process and feel it will provide us with the discipline which leads to longer-term performance, which will benefit our investors over time.

We continue to believe that the current environment is creating potential pockets of opportunity for astute, long-term investors. Our experience has taught us that any tumultuous market backdrop (and the subsequent short-term price dislocations) can be an advantage for active managers. Our team continues to seek and identify companies that share two vital traits: a trend of improving their ROIC (return on invested capital), and stock prices trading at what we perceive as a deep discount to intrinsic value. We believe that allocating to these types of companies is a means to generate attractive risk-adjusted returns over longer time periods, and this continues to be a primary focus for us.

9

Victory RS Value Fund

Investment Overview

(Unaudited)

Average Annual Total Return

Year Ended December 31, 2022

Class A | Class C | Class R | Class Y | ||||||||||||||||||||||||||||

INCEPTION DATE | 6/30/93 | 5/1/07 | 12/4/06 | 5/1/07 | |||||||||||||||||||||||||||

| Net Asset Value | Maximum Offering Price | Net Asset Value | Contingent Deferred Charges | Net Asset Value | Net Asset Value | Russell Midcap® Value Index1 | |||||||||||||||||||||||||

One Year | –2.97 | % | –8.56 | % | –3.71 | % | –4.61 | % | –3.38 | % | –2.71 | % | –12.03 | % | |||||||||||||||||

Five Year | 7.12 | % | 5.86 | % | 6.29 | % | 6.29 | % | 6.70 | % | 7.38 | % | 5.72 | % | |||||||||||||||||

Ten Year | 10.23 | % | 9.58 | % | 9.55 | % | 9.55 | % | 9.79 | % | 10.49 | % | 10.11 | % | |||||||||||||||||

The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month's end, please visit vcm.com.

The maximum offering price figures reflect a maximum sales charge of 5.75% for Class A. Class C is not subject to an initial sales charge, but is subject to a deferred sales charge of 1.00% on shares redeemed within one year of purchase. Net Asset Value does not reflect sales charges. Total return measures the price change in a share assuming the reinvestment of all net investment income and realized capital gain distributions, if any. The total returns quoted do not reflect adjustments made to the enclosed financial statements in accordance with U.S. Generally Accepted Accounting Principles or the deduction of taxes that a shareholder would pay on net investment income and realized capital gain distributions, including reinvested distributions, or redemptions of shares. The total return figures set forth above include all waivers of fees. Without such fee waivers, the total returns would have been lower.

Victory RS Value Fund — Growth of $10,000

1The Russell Midcap® Value Index is an unmanaged Index that measures the performance of the mid-cap value segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with relatively lower price-to-book ratios and lower forecasted growth values. Index results assume the reinvestment of dividends paid on the stocks constituting the index. This index does not include the effect of sales charges, commissions, expenses, or taxes, is not representative of the Fund, and it is not possible to invest directly in an index.

The graph reflects investment of growth of a hypothetical $10,000 investment in the Fund.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares.

Past performance is not indicative of future results.

10

Victory RS Large Cap Alpha Fund

Managers' Commentary

(Unaudited)

What were the market conditions during the reporting period?

The fourth quarter of 2022 certainly began well enough, even as the year ended on a downbeat. Financial markets had been languishing all year and were in the doldrums as summer ended, but most segments of the equity market bounced back sharply in October and November thanks to better-than-expected earnings and signs that inflation may have peaked. Value stocks led the way, with the Russell 1000® Value Index up 10.25% in October and an additional 6.25% in November, while the Russell 2000® Value Index was up 12.59% in October and 3.06% in November. Unfortunately, that euphoria was short-lived.

Sentiment soured once again in December as investors began to digest how hawkish the U.S. Federal Reserve (the "Fed") really intended to be, given its repeated statements that it would not stop hiking the Fed funds interest rate until inflation was well in check irrespective of the impact to the broader economy. Some investors and corporate leaders began to question whether Fed Chair Jerome Powell was up to the task of maintaining an economic environment supportive of corporate growth while still taming inflation.

These growing concerns turned into a full-fledged market sell-off in December, with the Russell 1000® Value Index shedding 4.03% and the Russell 2000® Value Index falling 6.56%. This reflected some poor earnings guidance by corporations and ongoing hawkish comments by Chairman Powell. In fact, the Chairman bluntly told market participants, "Fed hikes and volatility have been central themes of 2022, and investors should expect both — along with hits to corporate earnings — as we enter the new year." On top of that, he braced investors for the possibility of a recession in 2023. All this economic uncertainty merely exacerbated the interest rate backdrop and highlighted the difficulties facing the Fed in carrying out its dual monetary policy goals.

Yet despite the volatility and challenges in the fourth quarter, it was not all bad news as we closed out 2022. For starters, it really does seem to us that the worst inflation numbers are behind us. Demand for goods has decreased, as evidenced by higher inventories among retailers and a continued decline in energy prices globally. This should eventually provide some relief for battered markets. There are even reasons for optimism within certain sectors of the economy (and individual companies). Chief among these is the fact that select corporate operations (and earnings) have come in better than expected, which means the market decline has improved valuations and may be creating a more favorable risk-reward tradeoff going forward.

In terms of the overall numbers for our area of focus — domestic value-oriented strategies — the Russell 3000® Value Index was up 12.18% during the fourth quarter and was down 7.98% for the full year. In terms of market capitalizations, small-cap value stocks, as represented by the Russell 2000® Value Index, declined 14.48% for the year. The Russell Midcap® Value Index declined by 12.03% for the full year, while large-cap value stocks, as represented by the Russell 1000® Value Index (the "Index"), posted an annual decline of 7.54%.

Looking ahead, many investors are not only wondering just how restrictive monetary policy will become, but also how healthy the economy really is. Of course, nobody can answer these questions with absolute certainty, but we can definitively say that the current investment landscape continues to be polarizing, and we would not be surprised to see further bouts of elevated volatility in 2023.

11

Victory RS Large Cap Alpha Fund

Managers' Commentary (continued)

How did Victory RS Large Cap Alpha Fund (the "Fund") perform during the reporting period?

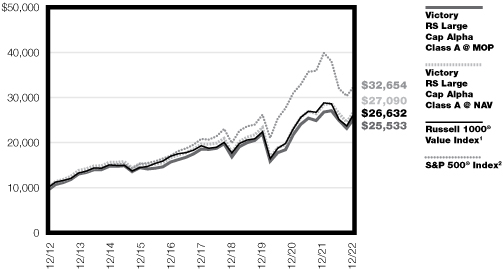

The Fund returned -4.62% (Class A at net asset value) for the fiscal year ended December 31, 2022, outperforming the Index, which returned -7.54% for the reporting period.

What strategies did you employ during the reporting period?

The Fund outperformed the Index primarily through stock selection in the Financials and Utilities sectors. Our focus on businesses that have the potential for long-term value creation while limiting our downside paid off during 2022. For the year, the stocks that provided positive contributions tended to be undergoing a unique structural change, but also holding a competitive advantage. Within the Financials sector, Fairfax Financial and The Progressive Corp. were significant positive contributors to performance. The Utilities sector provided other names that benefitted the portfolio. Constellation Energy and Vistra Corporation led performance. Where we struggled was in a couple of our holdings in the Materials sector. Sealed Air Corp. saw its share price fall as rising input costs impacted profitability. Similarly, PPG Industries, Inc. saw its margins impacted as price increases could not offset rising energy costs. At the end of the day, we managed to outperform the Index in 2022 and we remain confident in our process and feel it will provide us with the discipline which leads to longer-term performance which will benefit our investors over time.

We continue to believe that the current environment is creating potential pockets of opportunity for astute, long-term investors. Our experience has taught us that any tumultuous market backdrop (and the subsequent short-term price dislocations) can be an advantage for active managers. Our team continues to seek and identify companies that share two vital traits: a trend of improving their ROIC (return on invested capital), and stock prices trading at what we perceive as a deep discount to intrinsic value. We believe that allocating to these types of companies is a means to generate attractive risk-adjusted returns over longer time periods, and this continues to be a primary focus for us.

12

Victory RS Large Cap Alpha Fund

Investment Overview

(Unaudited)

Average Annual Total Return

Year Ended December 31, 2022

Class A | Class C | Class R | Class Y | ||||||||||||||||||||||||||||||||

INCEPTION DATE | 6/1/72 | 8/7/00 | 5/15/01 | 5/1/07 | |||||||||||||||||||||||||||||||

| Net Asset Value | Maximum Offering Price | Net Asset Value | Contingent Deferred Charges | Net Asset Value | Net Asset Value | Russell 1000® Value Index1 | S&P 500® Index2 | ||||||||||||||||||||||||||||

One Year | –4.62 | % | –10.11 | % | –5.39 | % | –6.24 | % | –4.97 | % | –4.43 | % | –7.54 | % | –18.11 | % | |||||||||||||||||||

Five Year | 6.60 | % | 5.35 | % | 5.75 | % | 5.75 | % | 6.21 | % | 6.82 | % | 6.67 | % | 9.42 | % | |||||||||||||||||||

Ten Year | 10.48 | % | 9.83 | % | 9.77 | % | 9.77 | % | 10.07 | % | 10.72 | % | 10.29 | % | 12.56 | % | |||||||||||||||||||

The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month's end, please visit vcm.com.

The maximum offering price figures reflect a maximum sales charge of 5.75% for Class A. Class C is not subject to an initial sales charge, but is subject to a deferred sales charge of 1.00% on shares redeemed within one year of purchase. Net Asset Value does not reflect sales charges. Total return measures the price change in a share assuming the reinvestment of all net investment income and realized capital gain distributions, if any. The total returns quoted do not reflect adjustments made to the enclosed financial statements in accordance with U.S. Generally Accepted Accounting Principles or the deduction of taxes that a shareholder would pay on net investment income and realized capital gain distributions, including reinvested distributions, or redemptions of shares. The total return figures set forth above include all waivers of fees. Without such fee waivers, the total returns would have been lower.

Victory RS Large Cap Alpha Fund — Growth of $10,000

1The Russell 1000® Value Index is made up of about 1,000 of the largest companies in the U.S. equity market. It represents top companies by market capitalization. It's made up of about 90% of the total market capitalization of all U.S. stocks. This index does not include the effect of sales charges, commissions, expenses, or taxes, is not representative of the Fund, and it is not possible to invest directly in an index.

2The S&P 500® Index is an unmanaged index comprised of 500 domestically traded common stocks, is weighted according to the market value of each common stock in the index, and includes reinvestment of dividends. This index does not include the effect of sales charges, commissions, expenses, or taxes, is not representative of the Fund, and it is not possible to invest directly in an index.

The graph reflects investment of growth of a hypothetical $10,000 investment in the Fund.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares.

Past performance is not indicative of future results.

13

Victory RS Investors Fund

Managers' Commentary

(Unaudited)

What were the market conditions during the reporting period?

The fourth quarter of 2022 certainly began well enough, even as the year ended on a downbeat. Financial markets had been languishing all year and were in the doldrums as summer ended, but most segments of the equity market bounced back sharply in October and November thanks to better-than-expected earnings and signs that inflation may have peaked. Value stocks led the way, with the Russell 1000® Value Index up 10.25% in October and an additional 6.25% in November, while the Russell 2000® Value Index was up 12.59% in October and 3.06% in November. Unfortunately, that euphoria was short-lived.

Sentiment soured once again in December as investors began to digest how hawkish the U.S. Federal Reserve (the "Fed") really intended to be, given its repeated statements that it would not stop hiking the Fed funds interest rate until inflation was well in check irrespective of the impact to the broader economy. Some investors and corporate leaders began to question whether Fed Chair Jerome Powell was up to the task of maintaining an economic environment supportive of corporate growth while still taming inflation.

These growing concerns turned into a full-fledged market sell-off in December, with the Russell 1000® Value Index shedding 4.03% and the Russell 2000® Value Index falling 6.56%. This reflected some poor earnings guidance by corporations and ongoing hawkish comments by Chairman Powell. In fact, the Chairman bluntly told market participants, "Fed hikes and volatility have been central themes of 2022, and investors should expect both — along with hits to corporate earnings — as we enter the new year." On top of that, he braced investors for the possibility of a recession in 2023. All this economic uncertainty merely exacerbated the interest rate backdrop and highlighted the difficulties facing the Fed in carrying out its dual monetary policy goals.

Yet despite the volatility and challenges in the fourth quarter, it was not all bad news as we closed out 2022. For starters, we believe the worst inflation numbers are behind us. Demand for goods has decreased, as evidenced by higher inventories among retailers and a continued decline in energy prices globally. This should eventually provide some relief for battered markets. There are even reasons for optimism within certain sectors of the economy (and individual companies). Chief among these is the fact that select corporate operations (and earnings) have come in better than expected, which means the market decline has improved valuations and may be creating a more favorable risk-reward tradeoff going forward.

In terms of the overall numbers for our area of focus — domestic value-oriented strategies — the Russell 3000® Value Index (the "Index") was up 12.18% during the fourth quarter and was down 7.98% for the full year. In terms of market capitalizations, small-cap value stocks, as represented by the Russell 2000® Value Index, declined 14.48% for the year. The Russell Midcap® Value Index declined by 12.03% for the full year, while large-cap value stocks, as represented by the Russell 1000® Value Index, posted an annual decline of 7.54%.

Looking ahead, many investors are not only wondering just how restrictive monetary policy will become, but also how healthy the economy really is. Of course, nobody can answer these questions with absolute certainty, but we can definitively say that the current investment landscape continues to be polarizing, and we would not be surprised to see further bouts of elevated volatility in 2023.

14

Victory RS Investors Fund

Managers' Commentary (continued)

How did Victory RS Investors Fund (the "Fund") perform during the reporting period?

The Fund returned -2.01% (Class A at net asset value) for the fiscal year ended December 31, 2022, outperforming the Index, which returned -7.98% for the reporting period.

What strategies did you employ during the reporting period?

The Fund outperformed the Index primarily through stock selection in the Financials and Industrials sectors. Our focus on businesses that have the potential for long-term value creation while limiting our downside paid off during 2022. For the year, the stocks that provided positive contribution tended to be undergoing a unique structural change, but also holding a competitive advantage. Within the Financials sector, White Mountains Insurance Group and The Progressive Corp. were significant positive contributors to performance. The Industrials sector provided other holdings that benefitted the portfolio. Fluor Corp. and Meritor, Inc. led performance. Where we struggled was in a couple of our holdings in the Technology sector. NCR Corp. saw its share price fall as supply chain issues, coupled with uncertainty surrounding the company's strategic review, pressured the shares. Euronet Worldwide, Inc. continued to experience pressure on the travel segment of its ATM business, which impacted the share price. At the end of the day, we managed to outperform the Index in 2022 and we remain confident in our process and feel it will provide us with the discipline which leads to longer-term performance which will benefit our investors over time.

We continue to believe that the current environment is creating potential pockets of opportunity for astute, long-term investors. Our experience has taught us that any tumultuous market backdrop (and the subsequent short-term price dislocations) can be an advantage for active managers. Our team continues to seek and identify companies that share two vital traits: a trend of improving their ROIC (return on invested capital), and stock prices trading at what we perceive as a deep discount to intrinsic value. We believe that allocating to these types of companies is a means to generate attractive risk-adjusted returns over longer time periods, and this continues to be a primary focus for us.

15

Victory RS Investors Fund

Investment Overview

(Unaudited)

Average Annual Total Return

Year Ended December 31, 2022

Class A | Class C | Class R | Class Y | ||||||||||||||||||||||||||||

INCEPTION DATE | 11/15/05 | 7/24/07 | 1/3/07 | 5/1/07 | |||||||||||||||||||||||||||

| Net Asset Value | Maximum Offering Price | Net Asset Value | Contingent Deferred Charges | Net Asset Value | Net Asset Value | Russell 3000® Value Index1 | |||||||||||||||||||||||||

One Year | –2.01 | % | –7.66 | % | –2.69 | % | –3.62 | % | –2.63 | % | –1.73 | % | –7.98 | % | |||||||||||||||||

Five Year | 7.05 | % | 5.78 | % | 6.25 | % | 6.25 | % | 6.39 | % | 7.35 | % | 6.50 | % | |||||||||||||||||

Ten Year | 10.14 | % | 9.48 | % | 9.48 | % | 9.48 | % | 9.52 | % | 10.45 | % | 10.16 | % | |||||||||||||||||

The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month's end, please visit vcm.com.

The maximum offering price figures reflect a maximum sales charge of 5.75% for Class A. Class C is not subject to an initial sales charge, but is subject to a deferred sales charge of 1.00% on shares redeemed within one year of purchase. Net Asset Value does not reflect sales charges. Total return measures the price change in a share assuming the reinvestment of all net investment income and realized capital gain distributions, if any. The total returns quoted do not reflect adjustments made to the enclosed financial statements in accordance with U.S. Generally Accepted Accounting Principles or the deduction of taxes that a shareholder would pay on net investment income and realized capital gain distributions, including reinvested distributions, or redemptions of shares. The total return figures set forth above include all waivers of fees. Without such fee waivers, the total returns would have been lower.

Victory RS Investors Fund — Growth of $10,000

1The Russell 3000® Value Index measures the performance of those Russell 3000® Index companies with lower price-to-book ratios and lower forecasted growth values. The stocks in this index are also members of either the Russell 1000® Value or the Russell 2000® Value indexes. Index results assume the reinvestment of dividends paid on the stocks constituting the index. This index does not include the effect of sales charges, commissions, expenses, or taxes, is not representative of the Fund and it is not possible to invest directly in an index.

The graph reflects investment of growth of a hypothetical $10,000 investment in the Fund.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares.

Past performance is not indicative of future results.

16

Victory Global Energy Transition Fund

Managers' Commentary

(Unaudited)

What were the market conditions during the reporting period?

After a prolonged period of subdued inflation and low interest rates, inflation spiked in 2022, prompting a series of rate hikes by the U.S. Federal Reserve. Commodity prices continued to recover from COVID-19-related fears of a demand shock, reflecting tight inventories and limited spare capacity. In addition, improved capital discipline by producers resulted in market-leading free-cash flow yields for natural resource stocks. As a result, natural resource equities led the market for the second year in a row. Investors who had pared back or eliminated inflation hedges or inflation-sensitive exposure in their portfolio were left with little protection as equity and bond markets sold off in tandem while commodity prices spiked.

How did Victory Global Energy Transition Fund (the "Fund") perform during the reporting period?

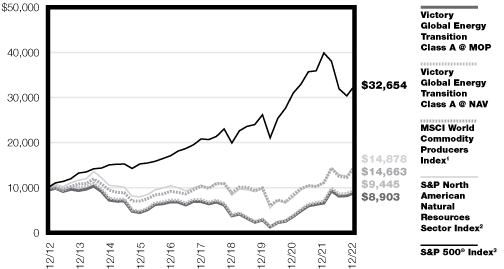

The Fund returned 35.01% (Class A at net asset value) for the fiscal year ended December 31, 2022, outperforming the MSCI World Commodity Producers Index, which returned 32.13% for the reporting period.

What strategies did you employ during the reporting period?

We stuck to our longstanding process during the reporting period. We seek to identify companies that, over a market cycle for commodity prices, have the potential to provide favorable long-term investment performance in any of the natural resources industries that we believe will be required for the Energy Transition, which refers to efforts designed to develop energy systems with zero carbon emissions and expand access to affordable, sustainable energy services around the world. We seek exposure to "advantaged producers" of those natural resources who are favorably positioned on the supply cost curve and can generate an intrinsic rate of return in excess of raw commodity beta. We underwrite our investment universe at the asset level based on proved reserves and conservative commodity price assumptions. We seek to own securities trading at a discount to our underwriting of net asset value. We view this underwriting process and the intrinsic return generated by structurally advantaged producers as the primary driver of returns for our portfolio. While we believe decarbonization efforts are adding inflationary pressures to many supply-constrained commodities, we do not attempt to forecast commodity price or demand increases and view these catalysts as additional upside potential for the investors in our strategy. Consistent with this approach, the majority of our absolute and relative returns versus different indices were a function of stock selection as opposed to commodity mix, a fact reinforced by strong performance in oil and oil-related stocks and our general lack of ownership in that space.

17

Victory Global Energy Transition Fund

Investment Overview

(Unaudited)

Average Annual Total Return

Year Ended December 31, 2022

Class A | Class C | Class R | Class Y | ||||||||||||||||||||||||||||||||||||

INCEPTION DATE | 11/15/95 | 5/1/07 | 12/4/06 | 5/1/07 | |||||||||||||||||||||||||||||||||||

| Net Asset Value | Maximum Offering Price | Net Asset Value | Contingent Deferred Charges | Net Asset Value | Net Asset Value | MSCI World Commodity Producers Index1 | S&P North American Natural Resources Sector Index2 | S&P 500® Index3 | |||||||||||||||||||||||||||||||

One Year | 35.01 | % | 27.24 | % | 33.94 | % | 32.94 | % | 34.44 | % | 35.46 | % | 32.13 | % | 34.07 | % | –18.11 | % | |||||||||||||||||||||

Five Year | 5.18 | % | 3.94 | % | 4.34 | % | 4.34 | % | 4.79 | % | 5.52 | % | 7.28 | % | 7.13 | % | 9.42 | % | |||||||||||||||||||||

Ten Year | –0.57 | % | –1.16 | % | –1.20 | % | –1.20 | % | –0.93 | % | –0.24 | % | 3.90 | % | 4.05 | % | 12.56 | % | |||||||||||||||||||||

The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month's end, please visit vcm.com.

The maximum offering price figures reflect a maximum sales charge of 5.75% for Class A. Class C is not subject to an initial sales charge, but is subject to a deferred sales charge of 1.00% on shares redeemed within one year of purchase. Net Asset Value does not reflect sales charges. Total return measures the price change in a share assuming the reinvestment of all net investment income and realized capital gain distributions, if any. The total returns quoted do not reflect adjustments made to the enclosed financial statements in accordance with U.S. Generally Accepted Accounting Principles or the deduction of taxes that a shareholder would pay on net investment income and realized capital gain distributions, including reinvested distributions, or redemptions of shares. The total return figures set forth above include all waivers of fees. Without such fee waivers, the total returns would have been lower.

Victory Global Energy Transition Fund — Growth of $10,000

1The MSCI World Commodity Producers Index is an equity-based index designed to reflect the performance related to stocks of commodity producers. The index is a free float-adjusted market-capitalization-weighted index composed of commodity producer companies based on the Global Industry Classification Standard (GICS). The index reflects the reinvestment of dividends paid on the stocks constituting the index, net of withholding taxes. This index does not include the effect of sales charges, commissions, expenses, or taxes, is not representative of the Fund, and it is not possible to invest directly in an index.

2The S&P North American Natural Resources Sector Index is a modified capitalization-weighted index designed as a benchmark for U.S.-traded securities in the natural resources sector. The index includes companies involved in the following categories: extractive industries, energy companies, owners and operations or timber tracts, forestry services, producers of pulp and paper, and owners of plantations. Index results assume the reinvestment of dividends paid on the stocks constituting the index. This index does not include the effect of sales charges, commissions, expenses, or taxes, is not representative of the Fund, and it is not possible to invest directly in an index.

3The S&P 500® Index is an unmanaged index comprised of 500 domestically traded common stocks, is weighted according to the market value of each common stock in the index, and includes reinvestment of dividends. This index does not include the effect of sales charges, commissions, expenses, or taxes, is not representative of the Fund, and it is not possible to invest directly in an index.

The graph reflects investment of growth of a hypothetical $10,000 investment in the Fund.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares.

Past performance is not indicative of future results.

18

| Victory Portfolios Victory RS Partners Fund | December 31, 2022 | ||||||

(Unaudited)

Investment Objective and Portfolio Holdings:

The Fund seeks to provide long-term capital appreciation.

Top 10 Holdings*:

December 31, 2022

(% of Net Assets)

Globe Life, Inc. | 3.7 | % | |||||

Primerica, Inc. | 3.4 | % | |||||

Federated Hermes, Inc. | 3.3 | % | |||||

Kemper Corp. | 3.2 | % | |||||

White Mountains Insurance Group Ltd. | 2.8 | % | |||||

Graphic Packaging Holding Co. | 2.6 | % | |||||

Verint Systems, Inc. | 2.5 | % | |||||

Equity Commonwealth | 2.5 | % | |||||

Four Corners Property Trust, Inc. | 2.4 | % | |||||

U.S. Foods Holding Corp. | 2.4 | % | |||||

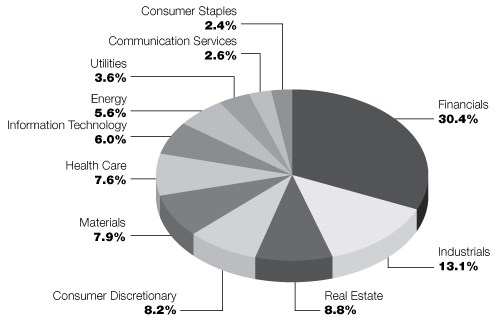

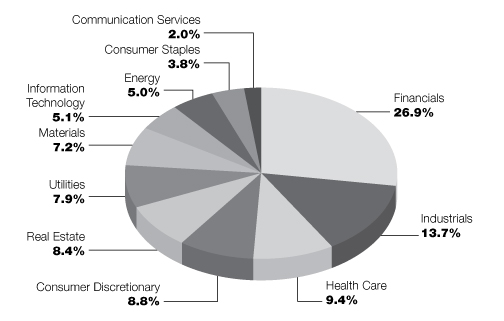

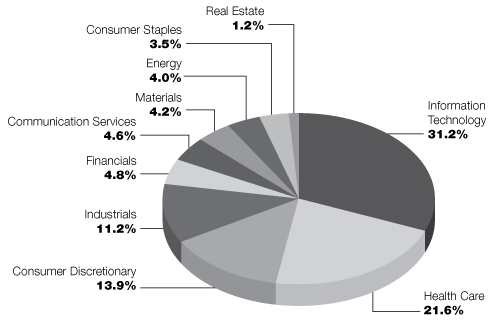

Sector Allocation*:

December 31, 2022

(% of Net Assets)

* Does not include futures contracts, money market instruments, and short-term investments purchased with cash collateral from securities loaned.

Percentages are of the net assets of the Fund and may not equal 100%.

Refer to the Schedule of Portfolio Investments for a complete list of securities.

19

| Victory Portfolios Victory RS Value Fund | December 31, 2022 | ||||||

(Unaudited)

Investment Objective and Portfolio Holdings:

The Fund seeks to provide long-term capital appreciation.

Top 10 Holdings*:

December 31, 2022

(% of Net Assets)

Fairfax Financial Holdings Ltd. | 4.0 | % | |||||

Vistra Corp. | 3.4 | % | |||||

Globe Life, Inc. | 3.3 | % | |||||

Markel Corp. | 3.1 | % | |||||

Federated Hermes, Inc. | 2.9 | % | |||||

The Progressive Corp. | 2.8 | % | |||||

Brown & Brown, Inc. | 2.6 | % | |||||

Graphic Packaging Holding Co. | 2.6 | % | |||||

Fiserv, Inc. | 2.5 | % | |||||

Humana, Inc. | 2.5 | % | |||||

Sector Allocation*:

December 31, 2022

(% of Net Assets)

* Does not include futures contracts, money market instruments, and short-term investments purchased with cash collateral from securities loaned.

Percentages are of the net assets of the Fund and may not equal 100%.

Refer to the Schedule of Portfolio Investments for a complete list of securities.

20

| Victory Portfolios Victory RS Large Cap Alpha Fund | December 31, 2022 | ||||||

(Unaudited)

Investment Objective and Portfolio Holdings:

The Fund seeks to provide long-term capital appreciation.

Top 10 Holdings*:

December 31, 2022

(% of Net Assets)

Fairfax Financial Holdings Ltd. | 5.4 | % | |||||

Markel Corp. | 4.6 | % | |||||

The Progressive Corp. | 3.7 | % | |||||

Vistra Corp. | 3.7 | % | |||||

Merck & Co., Inc. | 3.2 | % | |||||

Cboe Global Markets, Inc. | 3.1 | % | |||||

Brown & Brown, Inc. | 3.1 | % | |||||

AbbVie, Inc. | 2.9 | % | |||||

Fidelity National Information Services, Inc. | 2.8 | % | |||||

UnitedHealth Group, Inc. | 2.6 | % | |||||

Sector Allocation*:

December 31, 2022

(% of Net Assets)

* Does not include futures contracts, money market instruments, and short-term investments purchased with cash collateral from securities loaned.

Percentages are of the net assets of the Fund and may not equal 100%.

Refer to the Schedule of Portfolio Investments for a complete list of securities.

21

| Victory Portfolios Victory RS Investors Fund | December 31, 2022 | ||||||

(Unaudited)

Investment Objective and Portfolio Holdings:

The Fund seeks to provide long-term capital appreciation.

Top 10 Holdings*:

December 31, 2022

(% of Net Assets)

Markel Corp. | 4.8 | % | |||||

Fairfax Financial Holdings Ltd. | 4.7 | % | |||||

Vistra Corp. | 4.5 | % | |||||

Brown & Brown, Inc. | 4.4 | % | |||||

Cboe Global Markets, Inc. | 4.1 | % | |||||

Federated Hermes, Inc. | 4.0 | % | |||||

The Progressive Corp. | 4.0 | % | |||||

White Mountains Insurance Group Ltd. | 3.9 | % | |||||

Willis Towers Watson PLC | 3.6 | % | |||||

Verint Systems, Inc. | 3.5 | % | |||||

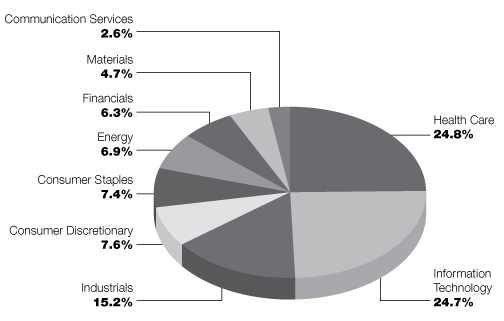

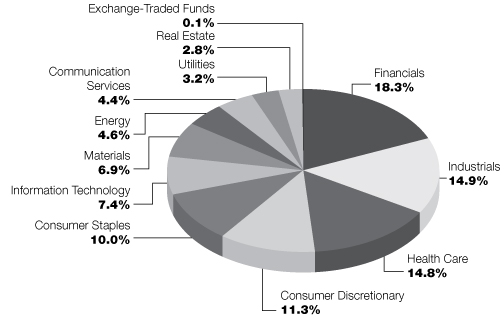

Sector Allocation*:

December 31, 2022

(% of Net Assets)

* Does not include futures contracts, money market instruments, and short-term investments purchased with cash collateral from securities loaned.

Percentages are of the net assets of the Fund and may not equal 100%.

Refer to the Schedule of Portfolio Investments for a complete list of securities.

22

| Victory Portfolios Victory Global Energy Transition Fund | December 31, 2022 | ||||||

(Unaudited)

Investment Objective and Portfolio Holdings:

The Fund seeks to provide long-term capital appreciation.

Top 10 Holdings*:

December 31, 2022

(% of Net Assets)

Whitecap Resources, Inc. | 14.5 | % | |||||

First Quantum Minerals Ltd. | 9.2 | % | |||||

Cameco Corp. | 8.0 | % | |||||

Ivanhoe | 5.1 | % | |||||

Newmont Corp. | 5.0 | % | |||||

Linde PLC | 4.7 | % | |||||

NextEra Energy, Inc. | 4.6 | % | |||||

Iluka Resources Ltd. | 4.6 | % | |||||

Enterprise Products Partners LP | 4.3 | % | |||||

Norsk Hydro ASA | 4.3 | % | |||||

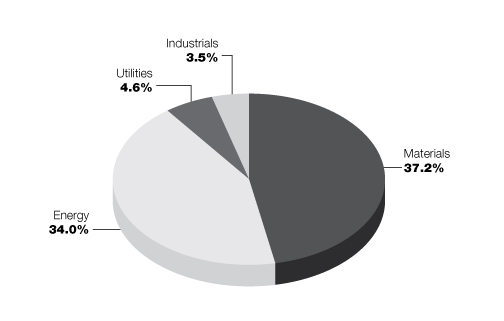

Sector Allocation*:

December 31, 2022

(% of Net Assets)

* Does not include futures contracts, money market instruments, and short-term investments purchased with cash collateral from securities loaned.

Percentages are of the net assets of the Fund and may not equal 100%.

Refer to the Schedule of Portfolio Investments for a complete list of securities.

23

| Victory Portfolios Victory RS Partners Fund | Schedule of Portfolio Investments December 31, 2022 | ||||||

Security Description | Shares | Value | |||||||||

Common Stocks (96.0%) | |||||||||||

Banks (11.0%): | |||||||||||

Banner Corp. | 51,620 | $ | 3,262,384 | ||||||||

Eastern Bankshares, Inc. | 437,770 | 7,551,532 | |||||||||

First Bancorp/Puerto Rico | 395,710 | 5,033,431 | |||||||||

SouthState Corp. | 90,270 | 6,893,017 | |||||||||

Synovus Financial Corp. | 93,980 | 3,528,949 | |||||||||

The Bank of NT Butterfield & Son Ltd. | 262,760 | 7,832,876 | |||||||||

UMB Financial Corp. | 53,182 | 4,441,761 | |||||||||

38,543,950 | |||||||||||

Capital Markets (5.1%): | |||||||||||

Federated Hermes, Inc. | 319,930 | 11,616,658 | |||||||||

PJT Partners, Inc., Class A | 84,260 | 6,209,120 | |||||||||

17,825,778 | |||||||||||

Communication Services (2.6%): | |||||||||||

Madison Square Garden Sports Corp. | 42,980 | 7,879,523 | |||||||||

World Wrestling Entertainment, Inc., Class A | 17,976 | 1,231,716 | |||||||||

9,111,239 | |||||||||||

Consumer Discretionary (8.2%): | |||||||||||

Bloomin' Brands, Inc. | 168,910 | 3,398,469 | |||||||||

Carter's, Inc. | 56,370 | 4,205,766 | |||||||||

Columbia Sportswear Co. | 49,220 | 4,310,688 | |||||||||

Light & Wonder, Inc. (a) | 62,490 | 3,661,914 | |||||||||

Taylor Morrison Home Corp. (a) | 145,520 | 4,416,532 | |||||||||

The Wendy's Co. | 168,070 | 3,803,424 | |||||||||

Under Armour, Inc., Class C (a) | 540,350 | 4,819,922 | |||||||||

28,616,715 | |||||||||||

Consumer Staples (2.4%): | |||||||||||

U.S. Foods Holding Corp. (a) | 245,120 | 8,338,982 | |||||||||

Energy (5.6%): | |||||||||||

California Resources Corp. | 90,060 | 3,918,511 | |||||||||

Comstock Resources, Inc. | 102,000 | 1,398,420 | |||||||||

Northern Oil and Gas, Inc. | 179,980 | 5,546,983 | |||||||||

PDC Energy, Inc. | 53,060 | 3,368,249 | |||||||||

Plains GP Holdings, LP, Class A | 434,550 | 5,405,802 | |||||||||

19,637,965 | |||||||||||

Health Care (7.4%): | |||||||||||

Encompass Health Corp. | 127,350 | 7,616,804 | |||||||||

Halozyme Therapeutics, Inc. (a) | 139,360 | 7,929,584 | |||||||||

The Ensign Group, Inc. | 77,790 | 7,359,712 | |||||||||

Zimvie, Inc. (a) | 302,880 | 2,828,899 | |||||||||

25,734,999 | |||||||||||

Industrials (13.1%): | |||||||||||

Applied Industrial Technologies, Inc. | 44,500 | 5,608,335 | |||||||||

Atkore, Inc. (a) | 35,250 | 3,998,055 | |||||||||

See notes to financial statements.

24

| Victory Portfolios Victory RS Partners Fund | Schedule of Portfolio Investments — continued December 31, 2022 | ||||||

Security Description | Shares | Value | |||||||||

Finning International, Inc. | 161,540 | $ | 4,016,425 | ||||||||

Fluor Corp. (a) | 157,420 | 5,456,177 | |||||||||

Granite Construction, Inc. | 114,880 | 4,028,842 | |||||||||

H&E Equipment Services, Inc. | 107,060 | 4,860,524 | |||||||||

IAA, Inc. (a) | 42,320 | 1,692,800 | |||||||||

ICF International, Inc. | 40,130 | 3,974,876 | |||||||||

McGrath RentCorp | 22,440 | 2,215,726 | |||||||||

Mueller Water Products, Inc., Class A | 320,980 | 3,453,745 | |||||||||

The Timken Co. | 54,870 | 3,877,663 | |||||||||

Triton International Ltd. | 34,950 | 2,403,861 | |||||||||

45,587,029 | |||||||||||

Information Technology (6.0%): | |||||||||||

ACI Worldwide, Inc. (a) | 292,720 | 6,732,560 | |||||||||

Belden, Inc. | 34,490 | 2,479,831 | |||||||||

Verint Systems, Inc. (a) | 236,990 | 8,597,997 | |||||||||

Verra Mobility Corp. (a) | 237,430 | 3,283,657 | |||||||||

21,094,045 | |||||||||||

Insurance (14.3%): | |||||||||||

Globe Life, Inc. | 106,470 | 12,834,958 | |||||||||

Kemper Corp. | 228,060 | 11,220,552 | |||||||||

Primerica, Inc. | 84,103 | 11,927,487 | |||||||||

Safety Insurance Group, Inc. | 25,210 | 2,124,195 | |||||||||

Selective Insurance Group, Inc. | 23,130 | 2,049,549 | |||||||||

White Mountains Insurance Group Ltd. | 6,820 | 9,645,731 | |||||||||

49,802,472 | |||||||||||

Materials (7.9%): | |||||||||||

Axalta Coating Systems Ltd. (a) | 148,970 | 3,794,266 | |||||||||

Constellium SE (a) | 300,220 | 3,551,603 | |||||||||

Graphic Packaging Holding Co. | 406,230 | 9,038,617 | |||||||||

Olin Corp. | 130,320 | 6,899,141 | |||||||||

Summit Materials, Inc., Class A (a) | 151,662 | 4,305,684 | |||||||||

27,589,311 | |||||||||||

Real Estate (8.8%): | |||||||||||

Corporate Office Properties Trust | 265,310 | 6,882,141 | |||||||||

Equity Commonwealth | 341,680 | 8,531,750 | |||||||||

Four Corners Property Trust, Inc. | 323,360 | 8,384,725 | |||||||||

Kennedy-Wilson Holdings, Inc. | 222,760 | 3,504,015 | |||||||||

The Howard Hughes Corp. (a) | 42,260 | 3,229,509 | |||||||||

30,532,140 | |||||||||||

Utilities (3.6%): | |||||||||||

ALLETE, Inc. | 27,040 | 1,744,350 | |||||||||

Black Hills Corp. | 78,655 | 5,532,593 | |||||||||

ONE Gas, Inc. | 69,120 | 5,233,766 | |||||||||

12,510,709 | |||||||||||

Total Common Stocks (Cost $285,644,090) | 334,925,334 | ||||||||||

See notes to financial statements.

25

| Victory Portfolios Victory RS Partners Fund | Schedule of Portfolio Investments — continued December 31, 2022 | ||||||

Security Description | Shares | Value | |||||||||

Preferred Stocks (0.2%) | |||||||||||

Health Care (0.2%): | |||||||||||

WellDoc, Inc. Series B (b) (c) | 1,587,483 | $ | 587,369 | ||||||||

Total Preferred Stocks (Cost $1,942,920) | 587,369 | ||||||||||

Total Investments (Cost $287,587,010) — 96.2% | 335,512,703 | ||||||||||

Other assets in excess of liabilities — 3.8% | 13,199,774 | ||||||||||

NET ASSETS — 100.00% | $ | 348,712,477 | |||||||||

(a) Non-income producing security.

(b) The Fund's Adviser has deemed this security to be illiquid based upon procedures approved by the Board of Trustees. As of December 31, 2022, illiquid securities were 0.2% of net assets.

(c) Security was fair valued based upon procedures approved by the Board of Trustees and represents 0.2% of net assets as of December 31, 2022. This security is classified as Level 3 within the fair value hierarchy. (See Note 2 in the Notes to Financial Statements)

LP — Limited Partnership

See notes to financial statements.

26

| Victory Portfolios Victory RS Value Fund | Schedule of Portfolio Investments December 31, 2022 | ||||||

Security Description | Shares | Value | |||||||||

Common Stocks (98.2%) | |||||||||||

Banks (0.8%): | |||||||||||

KeyCorp | 129,920 | $ | 2,263,206 | ||||||||

Capital Markets (8.3%): | |||||||||||

Cboe Global Markets, Inc. | 51,090 | 6,410,262 | |||||||||

Federated Hermes, Inc. | 237,840 | 8,635,970 | |||||||||

Interactive Brokers Group, Inc. | 86,330 | 6,245,976 | |||||||||

State Street Corp. | 40,530 | 3,143,912 | |||||||||

24,436,120 | |||||||||||

Communication Services (2.0%): | |||||||||||

Liberty Media Corp.-Liberty SiriusXM, Class C (a) | 129,780 | 5,078,292 | |||||||||

World Wrestling Entertainment, Inc., Class A | 13,160 | 901,723 | |||||||||

5,980,015 | |||||||||||

Consumer Discretionary (8.8%): | |||||||||||

Carter's, Inc. | 44,100 | 3,290,301 | |||||||||

Columbia Sportswear Co. | 19,920 | 1,744,594 | |||||||||

Darden Restaurants, Inc. | 29,800 | 4,122,234 | |||||||||

LKQ Corp. | 85,620 | 4,572,964 | |||||||||

Mattel, Inc. (a) | 254,730 | 4,544,383 | |||||||||

The Wendy's Co. | 234,570 | 5,308,319 | |||||||||

Toll Brothers, Inc. | 49,220 | 2,457,062 | |||||||||

26,039,857 | |||||||||||

Consumer Staples (3.8%): | |||||||||||

Keurig Dr Pepper, Inc. | 131,755 | 4,698,383 | |||||||||

U.S. Foods Holding Corp. (a) | 195,230 | 6,641,725 | |||||||||

11,340,108 | |||||||||||

Energy (5.0%): | |||||||||||

Baker Hughes Co. | 108,320 | 3,198,690 | |||||||||

Chesapeake Energy Corp. | 24,020 | 2,266,767 | |||||||||

Marathon Oil Corp. | 160,980 | 4,357,729 | |||||||||

Ovintiv, Inc. | 59,410 | 3,012,681 | |||||||||

The Williams Cos., Inc. | 62,250 | 2,048,025 | |||||||||

14,883,892 | |||||||||||

Health Care (9.4%): | |||||||||||

Charles River Laboratories International, Inc. (a) | 14,950 | 3,257,605 | |||||||||

Encompass Health Corp. | 106,830 | 6,389,502 | |||||||||

Halozyme Therapeutics, Inc. (a) | 78,940 | 4,491,686 | |||||||||

Humana, Inc. | 14,190 | 7,267,976 | |||||||||

Zimmer Biomet Holdings, Inc. | 48,500 | 6,183,750 | |||||||||

27,590,519 | |||||||||||

Industrials (13.7%): | |||||||||||

AGCO Corp. | 38,070 | 5,279,928 | |||||||||

Crane Holdings Co. | 33,310 | 3,345,990 | |||||||||

Curtiss-Wright Corp. | 17,530 | 2,927,335 | |||||||||

Fluor Corp. (a) | 131,760 | 4,566,802 | |||||||||

IAA, Inc. (a) | 27,900 | 1,116,000 | |||||||||

L3Harris Technologies, Inc. | 7,340 | 1,528,261 | |||||||||

See notes to financial statements.

27

| Victory Portfolios Victory RS Value Fund | Schedule of Portfolio Investments — continued December 31, 2022 | ||||||

Security Description | Shares | Value | |||||||||

Leidos Holdings, Inc. | 48,450 | $ | 5,096,455 | ||||||||

nVent Electric PLC | 81,280 | 3,126,842 | |||||||||

Parker-Hannifin Corp. | 12,130 | 3,529,830 | |||||||||

Sensata Technologies Holding PLC | 125,240 | 5,057,191 | |||||||||

The Timken Co. | 69,510 | 4,912,272 | |||||||||

40,486,906 | |||||||||||

Information Technology (5.1%): | |||||||||||

Fiserv, Inc. (a) | 72,430 | 7,320,500 | |||||||||

Global Payments, Inc. | 15,760 | 1,565,283 | |||||||||

Verint Systems, Inc. (a) | 171,730 | 6,230,365 | |||||||||

15,116,148 | |||||||||||

Insurance (17.8%): | |||||||||||

Brown & Brown, Inc. | 136,450 | 7,773,557 | |||||||||

Fairfax Financial Holdings Ltd. | 19,780 | 11,718,824 | |||||||||

Globe Life, Inc. | 80,180 | 9,665,699 | |||||||||

Markel Corp. (a) | 6,810 | 8,972,107 | |||||||||

The Progressive Corp. | 64,470 | 8,362,404 | |||||||||

White Mountains Insurance Group Ltd. | 4,210 | 5,954,329 | |||||||||

52,446,920 | |||||||||||

Materials (7.2%): | |||||||||||

Graphic Packaging Holding Co. | 343,630 | 7,645,768 | |||||||||

Olin Corp. | 87,910 | 4,653,955 | |||||||||

Sealed Air Corp. | 124,040 | 6,187,115 | |||||||||

Summit Materials, Inc., Class A (a) | 95,943 | 2,723,822 | |||||||||

21,210,660 | |||||||||||

Real Estate (8.4%): | |||||||||||

Alexandria Real Estate Equities, Inc. | 43,530 | 6,341,015 | |||||||||

Equity Commonwealth | 232,530 | 5,806,274 | |||||||||

Equity LifeStyle Properties, Inc. | 45,480 | 2,938,008 | |||||||||

Invitation Homes, Inc. | 115,360 | 3,419,270 | |||||||||

National Retail Properties, Inc. | 135,430 | 6,197,277 | |||||||||

24,701,844 | |||||||||||

Utilities (7.9%): | |||||||||||

Constellation Energy Corp. | 17,690 | 1,525,055 | |||||||||

Evergy, Inc. | 54,480 | 3,428,426 | |||||||||

FirstEnergy Corp. | 65,580 | 2,750,425 | |||||||||

The AES Corp. | 189,110 | 5,438,804 | |||||||||

Vistra Corp. | 432,160 | 10,026,112 | |||||||||

23,168,822 | |||||||||||

Total Common Stocks (Cost $243,501,097) | 289,665,017 | ||||||||||

Total Investments (Cost $243,501,097) — 98.2% | 289,665,017 | ||||||||||

Other assets in excess of liabilities — 1.8% | 5,254,059 | ||||||||||

NET ASSETS — 100.00% | $ | 294,919,076 | |||||||||

(a) Non-income producing security.

PLC — Public Limited Company

See notes to financial statements.

28

| Victory Portfolios Victory RS Large Cap Alpha Fund | Schedule of Portfolio Investments December 31, 2022 | ||||||

Security Description | Shares | Value | |||||||||

Common Stocks (97.2%) | |||||||||||

Banks (1.5%): | |||||||||||

JPMorgan Chase & Co. | 52,680 | $ | 7,064,388 | ||||||||

Capital Markets (7.3%): | |||||||||||

Cboe Global Markets, Inc. | 117,500 | 14,742,725 | |||||||||

Interactive Brokers Group, Inc. | 159,690 | 11,553,572 | |||||||||

State Street Corp. | 103,260 | 8,009,878 | |||||||||

34,306,175 | |||||||||||

Communication Services (1.7%): | |||||||||||

Alphabet, Inc., Class A (a) | 92,630 | 8,172,745 | |||||||||

Consumer Discretionary (3.9%): | |||||||||||

Darden Restaurants, Inc. | 39,420 | 5,452,968 | |||||||||

LKQ Corp. | 157,790 | 8,427,564 | |||||||||

Mattel, Inc. (a) | 248,320 | 4,430,029 | |||||||||

18,310,561 | |||||||||||

Consumer Staples (7.6%): | |||||||||||

Keurig Dr Pepper, Inc. | 265,360 | 9,462,738 | |||||||||

Lamb Weston Holdings, Inc. | 60,620 | 5,417,003 | |||||||||

Mondelez International, Inc., Class A | 175,300 | 11,683,745 | |||||||||

U.S. Foods Holding Corp. (a) | 271,130 | 9,223,842 | |||||||||

35,787,328 | |||||||||||

Energy (8.1%): | |||||||||||

Enterprise Products Partners LP | 402,790 | 9,715,295 | |||||||||

Hess Corp. | 63,370 | 8,987,133 | |||||||||

Marathon Oil Corp. | 394,330 | 10,674,513 | |||||||||

Ovintiv, Inc. | 167,430 | 8,490,375 | |||||||||

37,867,316 | |||||||||||

Health Care (19.0%): | |||||||||||

AbbVie, Inc. | 82,650 | 13,357,066 | |||||||||

Cigna Corp. | 33,690 | 11,162,845 | |||||||||

Humana, Inc. | 23,120 | 11,841,833 | |||||||||

Johnson & Johnson | 47,780 | 8,440,337 | |||||||||

McKesson Corp. | 14,040 | 5,266,685 | |||||||||

Medtronic PLC | 151,930 | 11,807,999 | |||||||||

Merck & Co., Inc. | 132,680 | 14,720,846 | |||||||||

UnitedHealth Group, Inc. | 23,155 | 12,276,318 | |||||||||

88,873,929 | |||||||||||

Industrials (11.9%): | |||||||||||

Eaton Corp. PLC | 37,260 | 5,847,957 | |||||||||

FedEx Corp. | 24,360 | 4,219,152 | |||||||||

Johnson Controls International PLC | 140,860 | 9,015,040 | |||||||||

L3Harris Technologies, Inc. | 24,040 | 5,005,369 | |||||||||

Leidos Holdings, Inc. | 84,170 | 8,853,842 | |||||||||

PACCAR, Inc. | 38,650 | 3,825,191 | |||||||||

Raytheon Technologies Corp. | 59,462 | 6,000,905 | |||||||||

See notes to financial statements.

29

| Victory Portfolios Victory RS Large Cap Alpha Fund | Schedule of Portfolio Investments — continued December 31, 2022 | ||||||

Security Description | Shares | Value | |||||||||

Sensata Technologies Holding PLC | 204,940 | $ | 8,275,477 | ||||||||

Union Pacific Corp. | 21,560 | 4,464,429 | |||||||||

55,507,362 | |||||||||||

Information Technology (4.5%): | |||||||||||

Fidelity National Information Services, Inc. | 188,780 | 12,808,723 | |||||||||

FleetCor Technologies, Inc. (a) | 30,080 | 5,525,094 | |||||||||

Global Payments, Inc. | 25,130 | 2,495,912 | |||||||||

20,829,729 | |||||||||||

Insurance (16.8%): | |||||||||||

Brown & Brown, Inc. | 258,240 | 14,711,933 | |||||||||

Fairfax Financial Holdings Ltd. | 42,320 | 25,072,834 | |||||||||

Markel Corp. (a) | 16,310 | 21,488,262 | |||||||||

The Progressive Corp. | 133,420 | 17,305,908 | |||||||||

78,578,937 | |||||||||||

Materials (3.9%): | |||||||||||

PPG Industries, Inc. | 64,690 | 8,134,121 | |||||||||

Sealed Air Corp. | 206,982 | 10,324,262 | |||||||||

18,458,383 | |||||||||||

Real Estate (4.4%): | |||||||||||

Alexandria Real Estate Equities, Inc. | 62,510 | 9,105,832 | |||||||||

Equity LifeStyle Properties, Inc. | 73,120 | 4,723,552 | |||||||||

Invitation Homes, Inc. | 229,660 | 6,807,122 | |||||||||

20,636,506 | |||||||||||

Utilities (6.6%): | |||||||||||

Constellation Energy Corp. | 57,463 | 4,953,885 | |||||||||

Exelon Corp. | 199,280 | 8,614,875 | |||||||||

Vistra Corp. | 741,030 | 17,191,896 | |||||||||

30,760,656 | |||||||||||

Total Common Stocks (Cost $385,954,723) | 455,154,015 | ||||||||||

Total Investments (Cost $385,954,723) — 97.2% | 455,154,015 | ||||||||||

Other assets in excess of liabilities — 2.8% | 13,130,483 | ||||||||||

NET ASSETS — 100.00% | $ | 468,284,498 | |||||||||

(a) Non-income producing security.

LP — Limited Partnership

PLC — Public Limited Company

See notes to financial statements.

30

| Victory Portfolios Victory RS Investors Fund | Schedule of Portfolio Investments December 31, 2022 | ||||||

Security Description | Shares | Value | |||||||||

Common Stocks (95.2%) | |||||||||||

Banks (3.2%): | |||||||||||

Comerica, Inc. | 7,830 | $ | 523,436 | ||||||||

The Bank of NT Butterfield & Son Ltd. | 30,940 | 922,321 | |||||||||

1,445,757 | |||||||||||

Capital Markets (8.1%): | |||||||||||

Cboe Global Markets, Inc. | 14,680 | 1,841,900 | |||||||||

Federated Hermes, Inc. | 49,510 | 1,797,708 | |||||||||

3,639,608 | |||||||||||

Communication Services (2.1%): | |||||||||||

Alphabet, Inc., Class A (a) | 10,590 | 934,356 | |||||||||

Consumer Discretionary (2.5%): | |||||||||||

LKQ Corp. | 21,020 | 1,122,678 | |||||||||

Consumer Staples (6.8%): | |||||||||||

Keurig Dr Pepper, Inc. | 41,730 | 1,488,092 | |||||||||

U.S. Foods Holding Corp. (a) | 45,950 | 1,563,219 | |||||||||

3,051,311 | |||||||||||

Energy (5.1%): | |||||||||||

Northern Oil and Gas, Inc. | 40,060 | 1,234,649 | |||||||||

PDC Energy, Inc. | 16,860 | 1,070,273 | |||||||||

2,304,922 | |||||||||||

Health Care (14.4%): | |||||||||||

Encompass Health Corp. | 24,180 | 1,446,206 | |||||||||

Humana, Inc. | 2,560 | 1,311,206 | |||||||||

Medtronic PLC | 13,450 | 1,045,334 | |||||||||

Merck & Co., Inc. | 12,830 | 1,423,488 | |||||||||

Zimmer Biomet Holdings, Inc. | 10,160 | 1,295,400 | |||||||||

6,521,634 | |||||||||||

Industrials (4.9%): | |||||||||||

Fluor Corp. (a) | 33,020 | 1,144,473 | |||||||||

Sensata Technologies Holding PLC | 26,750 | 1,080,165 | |||||||||

2,224,638 | |||||||||||

Information Technology (6.6%): | |||||||||||

Fidelity National Information Services, Inc. | 20,910 | 1,418,744 | |||||||||

Verint Systems, Inc. (a) | 43,630 | 1,582,896 | |||||||||

3,001,640 | |||||||||||

Insurance (25.4%): | |||||||||||

Brown & Brown, Inc. | 34,830 | 1,984,265 | |||||||||

Fairfax Financial Holdings Ltd. | 3,620 | 2,144,699 | |||||||||

Markel Corp. (a) | 1,630 | 2,147,509 | |||||||||

The Progressive Corp. | 13,790 | 1,788,701 | |||||||||

White Mountains Insurance Group Ltd. | 1,250 | 1,767,912 | |||||||||

Willis Towers Watson PLC | 6,720 | 1,643,578 | |||||||||

11,476,664 | |||||||||||

See notes to financial statements.

31

| Victory Portfolios Victory RS Investors Fund | Schedule of Portfolio Investments — continued December 31, 2022 | ||||||

Security Description | Shares | Value | |||||||||

Materials (9.2%): | |||||||||||

Graphic Packaging Holding Co. | 64,710 | $ | 1,439,797 | ||||||||

Olin Corp. | 26,490 | 1,402,381 | |||||||||

Sealed Air Corp. | 25,930 | 1,293,388 | |||||||||

4,135,566 | |||||||||||

Real Estate (2.4%): | |||||||||||

Four Corners Property Trust, Inc. | 41,730 | 1,082,059 | |||||||||

Utilities (4.5%): | |||||||||||

Vistra Corp. | 87,780 | 2,036,496 | |||||||||

Total Common Stocks (Cost $38,983,266) | 42,977,329 | ||||||||||

Total Investments (Cost $38,983,266) — 95.2% | 42,977,329 | ||||||||||

Other assets in excess of liabilities — 4.8% | 2,166,096 | ||||||||||

NET ASSETS — 100.00% | $ | 45,143,425 | |||||||||

(a) Non-income producing security.

PLC — Public Limited Company

See notes to financial statements.

32