UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4861

Fidelity Garrison Street Trust

(Exact name of registrant as specified in charter)

82 Devonshire St., Boston, Massachusetts 02109

(Address of principal executive offices) (Zip code)

Scott C. Goebel, Secretary

82 Devonshire St.

Boston, Massachusetts 02109

(Name and address of agent for service)

Registrant's telephone number, including area code: 617-563-7000

Date of fiscal year end: | December 31 |

|

|

Date of reporting period: | December 31, 2011 |

Item 1. Reports to Stockholders

Fidelity® VIP

Investment Grade Central Fund

Annual Report

December 31, 2011

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov. You may also call 1-800-544-8544 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Forms N-Q are available on the SEC's web site at http://www.sec.gov. A fund's Forms N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

VIGC-ANN-0212 1.831202.105

Performance: The Bottom Line

Average annual total return reflects the change in the value of an investment, assuming reinvestment of the fund's distributions from dividend income and capital gains (the profits earned upon the sale of securities that have grown in value, if any) and assuming a constant rate of performance each year. During periods of reimbursement by Fidelity, a fund's total return will be greater than it would be had the reimbursement not occurred. Performance numbers are net of all underlying fund operating expenses, but do not include any insurance charges imposed by your insurance company's separate account. If performance information included the effect of these additional charges, the total returns would have been lower. How a fund did yesterday is no guarantee of how it will do tomorrow.

Average Annual Total Returns

Periods ended December 31, 2011 | Past 1 | Past 5 | Life of |

Fidelity® VIP Investment Grade Central Fund | 7.96% | 6.73% | 7.19% |

A From June 23, 2006

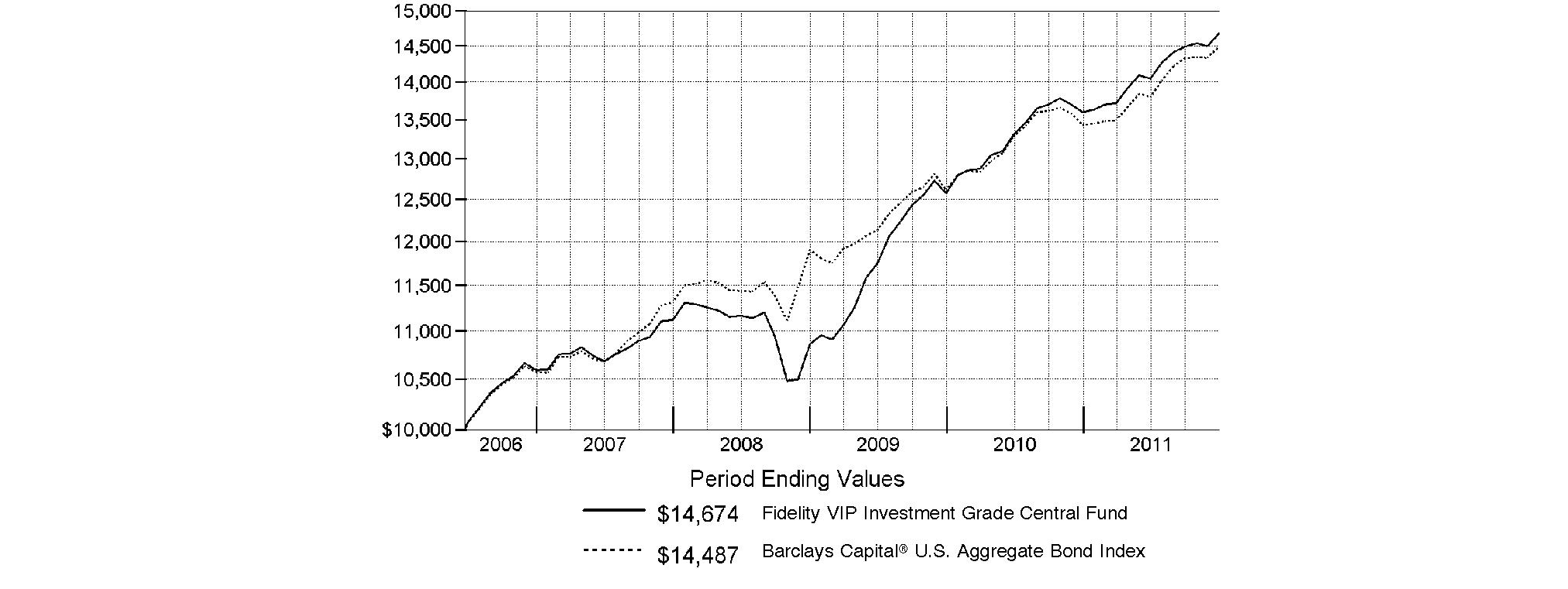

$10,000 Over Life of Fund

Let's say hypothetically that $10,000 was invested in Fidelity® VIP Investment Grade Central Fund on June 23, 2006, when the fund started. The chart shows how the value of your investment would have changed, and also shows how the Barclays Capital® U.S. Aggregate Bond Index performed over the same period.

Annual Report

Management's Discussion of Fund Performance

Market Recap: Against the backdrop of ultra-low interest rates, acute market volatility and a global flight to quality, U.S. taxable investment-grade bonds generated solid gains for the year ending December 31, 2011, as evidenced by the 7.84% return of the Barclays Capital® U.S. Aggregate Bond Index. Among the major sectors that comprise the index, U.S. Treasury bonds fared best, rising 9.81%. Treasuries benefited from robust investor demand for high-quality assets when the global economy weakened, inflation expectations fell, sovereign debt woes in Europe worsened, Congress wrangled over raising the federal debt ceiling and Standard & Poor's downgraded the U.S. long-term sovereign credit rating. Investment-grade corporate bonds gained 8.35%, bolstered by demand for higher-yielding bonds amid improved corporate profitability. Government-agency-issued residential mortgage-backed securities (MBS) rose 6.23%, receiving a boost from slower-than-expected prepayments and the Federal Reserve's program to reinvest payments from its holdings of agency debentures into the MBS sector, although the positive impact was somewhat offset by concerns that the bondholders would be negatively affected should the government modify homeowner refinancing programs. Slightly more muted returns were seen elsewhere in the market, with commercial mortgage-backed securities (CMBS), asset-backed securities (ABS) and government agency securities gaining 6.02%, 5.14% and 4.82%, respectively.

Comments from Ford O'Neil, Portfolio Manager of VIP Investment Grade Central Fund: For the year, the fund returned 7.96%, modestly outpacing the Barclays Capital index. Positioning among U.S. Treasury securities, an overweighting in corporate bonds and an underweighting in U.S. government agency securities bolstered relative performance, more than offsetting some disadvantageous sector weightings elsewhere and security selection among corporates. Although the fund gave up some ground due to an underweighting in Treasuries since they were among the U.S. fixed income market's best performers, overall yield-curve positioning within the sector was a plus. Specifically, overweighting 10- to 30-year bonds proved beneficial, as they significantly outpaced the index during the period. A corresponding underweighting in shorter-term Treasury issues also was advantageous, as this group showed more-subdued gains. An out-of-benchmark stake in Treasury Inflation-Protected Securities (TIPS), with a focus on intermediate- and long-maturity bonds, further contributed. Conversely, an emphasis on lagging financials curbed our upside within corporates, while overweightings in asset-backed and commercial-backed mortgage securities also detracted.

The views expressed above reflect those of the portfolio manager(s) only through the end of the period as stated on the cover of this report and do not necessarily represent the views of Fidelity or any other person in the Fidelity organization. Any such views are subject to change at any time based upon market or other conditions and Fidelity disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Fidelity fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Fidelity fund.

Annual Report

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2011 to December 31, 2011).

Actual Expenses

The first line of the accompanying table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the accompanying table provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| Annualized | Beginning | Ending | Expenses Paid |

Actual | .0020% | $ 1,000.00 | $ 1,045.10 | $ .01 |

Hypothetical (5% return per year before expenses) |

| $ 1,000.00 | $ 1,025.20 | $ .01 |

* Expenses are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

Annual Report

Investment Changes (Unaudited)

Quality Diversification (% of fund's net assets) | |||||||

As of December 31, 2011 | As of June 30, 2011 | ||||||

| U.S. Government and |

| | U.S. Government and |

| ||

| AAA 7.4% |

| | AAA 7.9% |

| ||

| AA 2.7% |

| | AA 2.7% |

| ||

| A 7.7% |

| | A 8.3% |

| ||

| BBB 14.5% |

| | BBB 13.1% |

| ||

| BB and Below 2.9% |

| | BB and Below 3.4% |

| ||

| Not Rated† 0.0% |

| | Not Rated† 0.0% |

| ||

| Short-Term |

| | Short-Term |

| ||

We have used ratings from Moody's Investors Service, Inc. Where Moody's® ratings are not available, we have used S&P® ratings. All ratings are as of the date indicated and do not reflect subsequent changes. Securities rated BB or below were rated investment grade at the time of acquisition. |

Weighted Average Maturity as of December 31, 2011 | ||

|

| 6 months ago |

Years | 6.4 | 6.2 |

This is a weighted average of all the maturities of the securities held in a fund. Weighted Average Maturity (WAM) can be used as a measure of sensitivity to interest rate changes and market changes. Generally, the longer the maturity, the greater the sensitivity to such changes. WAM is based on the dollar-weighted average length of time until principal payments must be paid. Depending on the types of securities held in a fund, certain maturity shortening devices (e.g., demand features, interest rate resets, and call options) may be taken into account when calculating the WAM. |

Duration as of December 31, 2011 | ||

|

| 6 months ago |

Years | 4.8 | 5.0 |

Duration estimates how much a bond fund's price will change with a change in comparable interest rates. If rates rise 1%, for example, a fund with a 5-year duration is likely to lose about 5% of its value. Other factors also can influence a bond fund's performance and share price. Accordingly, a bond fund's actual performance may differ from this example. Duration takes into account any call or put option embedded in the bonds. |

Asset Allocation (% of fund's net assets) | |||||||

As of December 31, 2011* | As of June 30, 2011** | ||||||

| Corporate Bonds 25.0% |

| | Corporate Bonds 24.3% |

| ||

| U.S. Government and |

| | U.S. Government and |

| ||

| Asset-Backed |

| | Asset-Backed |

| ||

| CMOs and Other |

| | CMOs and Other |

| ||

| Municipal Bonds 0.3% |

| | Municipal Bonds 0.4% |

| ||

| Other Investments 0.4% |

| | Other Investments 0.1% |

| ||

| Short-Term |

| | Short-Term |

| ||

* Foreign investments | 4.1% |

| ** Foreign investments | 3.3% |

| ||

* Futures and Swaps | 2.2% |

| ** Futures and Swaps | 2.2% |

| ||

*** Short-Term Investments and Net Other Assets are not included in the pie chart. |

† Amount represents less than 0.1% |

Annual Report

Investments December 31, 2011

Showing Percentage of Net Assets

Nonconvertible Bonds - 25.0% | ||||

| Principal Amount | Value | ||

CONSUMER DISCRETIONARY - 1.8% | ||||

Media - 1.8% | ||||

AOL Time Warner, Inc. 7.625% 4/15/31 | $ 1,625,000 | $ 2,094,636 | ||

Comcast Corp.: | ||||

4.95% 6/15/16 | 2,975,000 | 3,295,402 | ||

5.7% 5/15/18 | 2,400,000 | 2,761,073 | ||

6.4% 3/1/40 | 2,884,000 | 3,578,248 | ||

6.45% 3/15/37 | 1,410,000 | 1,706,255 | ||

COX Communications, Inc. 4.625% 6/1/13 | 3,475,000 | 3,663,623 | ||

Discovery Communications LLC: | ||||

3.7% 6/1/15 | 2,648,000 | 2,785,458 | ||

6.35% 6/1/40 | 2,421,000 | 2,910,877 | ||

NBCUniversal Media LLC: | ||||

3.65% 4/30/15 | 1,200,000 | 1,266,761 | ||

5.15% 4/30/20 | 3,234,000 | 3,599,423 | ||

6.4% 4/30/40 | 3,340,000 | 4,098,471 | ||

News America Holdings, Inc. 7.75% 12/1/45 | 2,067,000 | 2,526,289 | ||

News America, Inc.: | ||||

6.15% 3/1/37 | 2,331,000 | 2,543,657 | ||

6.15% 2/15/41 | 2,132,000 | 2,452,698 | ||

Time Warner Cable, Inc.: | ||||

5.85% 5/1/17 | 2,467,000 | 2,810,140 | ||

6.2% 7/1/13 | 7,000,000 | 7,512,323 | ||

6.75% 7/1/18 | 4,425,000 | 5,254,223 | ||

Time Warner, Inc.: | ||||

5.375% 10/15/41 | 1,021,000 | 1,103,733 | ||

5.875% 11/15/16 | 5,514,000 | 6,365,764 | ||

6.5% 11/15/36 | 2,337,000 | 2,814,786 | ||

Viacom, Inc.: | ||||

3.5% 4/1/17 | 1,312,000 | 1,367,317 | ||

6.75% 10/5/37 | 935,000 | 1,158,292 | ||

| 67,669,449 | |||

CONSUMER STAPLES - 1.2% | ||||

Beverages - 0.3% | ||||

Diageo Capital PLC 5.2% 1/30/13 | 1,705,000 | 1,785,626 | ||

FBG Finance Ltd. 5.125% 6/15/15 (c) | 2,185,000 | 2,378,340 | ||

Fortune Brands, Inc.: | ||||

5.375% 1/15/16 | 471,000 | 517,239 | ||

5.875% 1/15/36 | 6,267,000 | 6,554,994 | ||

| 11,236,199 | |||

Food Products - 0.5% | ||||

General Mills, Inc. 5.2% 3/17/15 | 3,528,000 | 3,930,753 | ||

Kraft Foods, Inc.: | ||||

5.375% 2/10/20 | 4,086,000 | 4,713,062 | ||

6.125% 2/1/18 | 3,684,000 | 4,317,132 | ||

6.5% 8/11/17 | 3,514,000 | 4,181,136 | ||

| 17,142,083 | |||

| ||||

| Principal Amount | Value | ||

Tobacco - 0.4% | ||||

Altria Group, Inc. 9.7% 11/10/18 | $ 4,450,000 | $ 5,985,495 | ||

Philip Morris International, Inc.: | ||||

4.875% 5/16/13 | 2,904,000 | 3,064,789 | ||

5.65% 5/16/18 | 2,751,000 | 3,253,060 | ||

Reynolds American, Inc. 7.25% 6/15/37 | 2,962,000 | 3,430,260 | ||

| 15,733,604 | |||

TOTAL CONSUMER STAPLES | 44,111,886 | |||

ENERGY - 3.6% | ||||

Energy Equipment & Services - 0.5% | ||||

DCP Midstream LLC: | ||||

4.75% 9/30/21 (c) | 3,739,000 | 3,863,019 | ||

5.35% 3/15/20 (c) | 3,724,000 | 3,984,047 | ||

El Paso Pipeline Partners Operating Co. LLC: | ||||

4.1% 11/15/15 | 3,902,000 | 3,995,297 | ||

5% 10/1/21 | 1,517,000 | 1,560,718 | ||

Transocean, Inc.: | ||||

5.05% 12/15/16 | 2,488,000 | 2,540,984 | ||

6.375% 12/15/21 | 3,286,000 | 3,491,342 | ||

| 19,435,407 | |||

Oil, Gas & Consumable Fuels - 3.1% | ||||

Anadarko Petroleum Corp. 6.375% 9/15/17 | 6,869,000 | 7,964,029 | ||

Canadian Natural Resources Ltd. 5.7% 5/15/17 | 5,685,000 | 6,723,303 | ||

ConocoPhillips 5.75% 2/1/19 | 3,900,000 | 4,698,100 | ||

Duke Capital LLC 6.25% 2/15/13 | 855,000 | 896,431 | ||

Duke Energy Field Services 6.45% 11/3/36 (c) | 2,477,000 | 2,820,141 | ||

El Paso Natural Gas Co. 5.95% 4/15/17 | 3,330,000 | 3,740,003 | ||

Enbridge Energy Partners LP 4.2% 9/15/21 | 4,399,000 | 4,591,980 | ||

EnCana Holdings Finance Corp. 5.8% 5/1/14 | 320,000 | 347,579 | ||

EQT Corp. 4.875% 11/15/21 | 1,669,000 | 1,684,106 | ||

Kaneb Pipe Line Operations Participation LP 7.75% 2/15/12 | 4,200,000 | 4,228,228 | ||

Marathon Petroleum Corp. 5.125% 3/1/21 | 2,187,000 | 2,283,862 | ||

Motiva Enterprises LLC 5.75% 1/15/20 (c) | 1,496,000 | 1,738,038 | ||

Nakilat, Inc. 6.067% 12/31/33 (c) | 1,808,000 | 1,925,520 | ||

Nexen, Inc.: | ||||

5.875% 3/10/35 | 5,405,000 | 5,506,436 | ||

6.4% 5/15/37 | 710,000 | 750,821 | ||

NGPL PipeCo LLC 6.514% 12/15/12 (c) | 2,360,000 | 2,384,114 | ||

Pemex Project Funding Master Trust 1.1272% 12/3/12 (c)(i) | 410,000 | 407,130 | ||

Nonconvertible Bonds - continued | ||||

| Principal Amount | Value | ||

ENERGY - continued | ||||

Oil, Gas & Consumable Fuels - continued | ||||

Petro-Canada: | ||||

6.05% 5/15/18 | $ 1,480,000 | $ 1,741,742 | ||

6.8% 5/15/38 | 3,485,000 | 4,491,660 | ||

Petrobras International Finance Co. Ltd.: | ||||

3.875% 1/27/16 | 3,612,000 | 3,721,819 | ||

5.75% 1/20/20 | 5,908,000 | 6,322,269 | ||

7.875% 3/15/19 | 4,277,000 | 5,105,442 | ||

Petroleos Mexicanos: | ||||

5.5% 1/21/21 | 3,601,000 | 3,916,088 | ||

6.5% 6/2/41 (c) | 4,805,000 | 5,381,600 | ||

Plains All American Pipeline LP/PAA Finance Corp.: | ||||

3.95% 9/15/15 | 2,158,000 | 2,285,581 | ||

5% 2/1/21 | 1,784,000 | 1,964,527 | ||

6.125% 1/15/17 | 1,250,000 | 1,413,484 | ||

Ras Laffan Liquefied Natural Gas Co. Ltd. III: | ||||

4.5% 9/30/12 (c) | 2,009,000 | 2,040,140 | ||

5.5% 9/30/14 (c) | 2,808,000 | 3,004,560 | ||

5.832% 9/30/16 (c) | 1,842,525 | 1,971,502 | ||

6.332% 9/30/27 (c) | 2,415,000 | 2,624,791 | ||

6.75% 9/30/19 (c) | 1,838,000 | 2,176,192 | ||

Schlumberger Investment SA 3.3% 9/14/21 (c) | 2,428,000 | 2,493,345 | ||

Spectra Energy Partners, LP: | ||||

2.95% 6/15/16 | 668,000 | 672,630 | ||

4.6% 6/15/21 | 873,000 | 911,897 | ||

Suncor Energy, Inc. 6.1% 6/1/18 | 4,665,000 | 5,520,766 | ||

Transcontinental Gas Pipe Line Corp. 6.4% 4/15/16 | 615,000 | 712,225 | ||

Western Gas Partners LP 5.375% 6/1/21 | 3,820,000 | 4,049,849 | ||

| 115,211,930 | |||

TOTAL ENERGY | 134,647,337 | |||

FINANCIALS - 12.1% | ||||

Capital Markets - 1.8% | ||||

Bear Stearns Companies, Inc. 5.3% 10/30/15 | 2,079,000 | 2,236,123 | ||

BlackRock, Inc. 4.25% 5/24/21 | 1,183,000 | 1,236,275 | ||

Goldman Sachs Group, Inc.: | ||||

3.7% 8/1/15 | 5,186,000 | 5,081,585 | ||

5.25% 7/27/21 | 1,823,000 | 1,777,751 | ||

5.625% 1/15/17 | 3,000,000 | 2,942,412 | ||

5.95% 1/18/18 | 755,000 | 773,093 | ||

6.15% 4/1/18 | 5,954,000 | 6,143,474 | ||

6.75% 10/1/37 | 3,421,000 | 3,178,465 | ||

| ||||

| Principal Amount | Value | ||

JPMorgan Chase Capital XX 6.55% 9/29/36 | $ 3,090,000 | $ 3,090,000 | ||

JPMorgan Chase Capital XXV 6.8% 10/1/37 | 6,975,000 | 7,001,156 | ||

Lazard Group LLC: | ||||

6.85% 6/15/17 | 3,241,000 | 3,400,483 | ||

7.125% 5/15/15 | 5,585,000 | 5,997,994 | ||

Merrill Lynch & Co., Inc.: | ||||

5.45% 2/5/13 | 1,820,000 | 1,833,384 | ||

6.11% 1/29/37 | 1,572,000 | 1,210,163 | ||

6.4% 8/28/17 | 1,989,000 | 1,926,404 | ||

Morgan Stanley: | ||||

4.75% 4/1/14 | 2,554,000 | 2,516,178 | ||

5.5% 7/28/21 | 8,558,000 | 7,910,159 | ||

6.625% 4/1/18 | 10,165,000 | 10,034,837 | ||

| 68,289,936 | |||

Commercial Banks - 2.4% | ||||

Bank of America NA 5.3% 3/15/17 | 6,480,000 | 5,845,673 | ||

Credit Suisse New York Branch 6% 2/15/18 | 6,110,000 | 6,024,350 | ||

Discover Bank: | ||||

7% 4/15/20 | 2,796,000 | 2,924,448 | ||

8.7% 11/18/19 | 6,339,000 | 7,225,528 | ||

Export-Import Bank of Korea 5.5% 10/17/12 | 6,570,000 | 6,722,575 | ||

Fifth Third Bancorp: | ||||

4.5% 6/1/18 | 1,179,000 | 1,181,690 | ||

8.25% 3/1/38 | 4,319,000 | 5,277,524 | ||

Fifth Third Bank 4.75% 2/1/15 | 487,000 | 504,546 | ||

Fifth Third Capital Trust IV 6.5% 4/15/67 (i) | 2,412,000 | 2,363,760 | ||

HBOS PLC 6.75% 5/21/18 (c) | 2,600,000 | 2,084,152 | ||

Huntington Bancshares, Inc. 7% 12/15/20 | 1,004,000 | 1,137,480 | ||

JPMorgan Chase & Co. 5.4% 1/6/42 | 4,270,000 | 4,447,380 | ||

KeyBank NA: | ||||

5.45% 3/3/16 | 1,618,000 | 1,741,601 | ||

5.8% 7/1/14 | 2,049,000 | 2,187,935 | ||

6.95% 2/1/28 | 800,000 | 885,794 | ||

KeyCorp. 5.1% 3/24/21 | 1,855,000 | 1,925,635 | ||

Korea Development Bank 5.3% 1/17/13 | 3,805,000 | 3,908,542 | ||

Marshall & Ilsley Bank: | ||||

4.85% 6/16/15 | 1,796,000 | 1,896,070 | ||

5% 1/17/17 | 4,625,000 | 4,878,663 | ||

5.25% 9/4/12 | 1,200,000 | 1,233,034 | ||

Regions Bank: | ||||

6.45% 6/26/37 | 3,952,000 | 3,270,280 | ||

7.5% 5/15/18 | 2,383,000 | 2,359,170 | ||

Nonconvertible Bonds - continued | ||||

| Principal Amount | Value | ||

FINANCIALS - continued | ||||

Commercial Banks - continued | ||||

Regions Financial Corp.: | ||||

5.75% 6/15/15 | $ 814,000 | $ 777,370 | ||

7.75% 11/10/14 | 2,367,000 | 2,378,835 | ||

SouthTrust Corp. 5.8% 6/15/14 | 1,440,000 | 1,535,057 | ||

SunTrust Banks, Inc. 3.6% 4/15/16 | 3,163,000 | 3,221,636 | ||

Wachovia Bank NA 4.875% 2/1/15 | 4,405,000 | 4,668,014 | ||

Wachovia Corp. 4.875% 2/15/14 | 785,000 | 818,892 | ||

Wells Fargo & Co.: | ||||

3.625% 4/15/15 | 2,350,000 | 2,460,466 | ||

3.676% 6/15/16 | 1,714,000 | 1,791,493 | ||

3.75% 10/1/14 | 3,750,000 | 3,959,453 | ||

| 91,637,046 | |||

Consumer Finance - 0.5% | ||||

General Electric Capital Corp.: | ||||

2.25% 11/9/15 | 2,597,000 | 2,609,089 | ||

2.95% 5/9/16 | 774,000 | 796,208 | ||

3.5% 6/29/15 | 799,000 | 837,925 | ||

5.625% 5/1/18 | 9,700,000 | 10,861,100 | ||

6.375% 11/15/67 (i) | 4,000,000 | 3,940,000 | ||

| 19,044,322 | |||

Diversified Financial Services - 2.0% | ||||

Bank of America Corp. 5.75% 12/1/17 | 12,290,000 | 11,611,002 | ||

BP Capital Markets PLC: | ||||

3.125% 10/1/15 | 3,694,000 | 3,869,868 | ||

4.742% 3/11/21 | 3,000,000 | 3,396,681 | ||

Capital One Capital V 10.25% 8/15/39 | 1,378,000 | 1,429,675 | ||

Citigroup, Inc.: | ||||

3.953% 6/15/16 | 3,838,000 | 3,825,542 | ||

4.75% 5/19/15 | 10,152,000 | 10,283,113 | ||

5.5% 4/11/13 | 1,390,000 | 1,419,222 | ||

6.125% 5/15/18 | 2,692,000 | 2,864,495 | ||

6.5% 8/19/13 | 8,073,000 | 8,404,736 | ||

JPMorgan Chase & Co.: | ||||

3.15% 7/5/16 | 4,200,000 | 4,220,534 | ||

4.35% 8/15/21 | 4,371,000 | 4,412,581 | ||

6.3% 4/23/19 | 3,920,000 | 4,438,616 | ||

Prime Property Funding, Inc.: | ||||

5.125% 6/1/15 (c) | 3,844,000 | 3,908,891 | ||

5.35% 4/15/12 (c) | 1,700,000 | 1,706,273 | ||

5.5% 1/15/14 (c) | 2,405,000 | 2,457,831 | ||

TECO Finance, Inc.: | ||||

4% 3/15/16 | 1,075,000 | 1,130,812 | ||

5.15% 3/15/20 | 1,545,000 | 1,716,152 | ||

ZFS Finance USA Trust II 6.45% 12/15/65 (c)(i) | 3,716,000 | 3,381,560 | ||

| ||||

| Principal Amount | Value | ||

ZFS Finance USA Trust IV 5.875% 5/9/62 (c)(i) | $ 500,000 | $ 470,000 | ||

ZFS Finance USA Trust V 6.5% 5/9/67 (c)(i) | 1,016,000 | 914,400 | ||

| 75,861,984 | |||

Insurance - 2.1% | ||||

Allstate Corp. 6.2% 5/16/14 | 2,709,000 | 3,021,578 | ||

American International Group, Inc. 4.875% 9/15/16 | 4,224,000 | 3,998,033 | ||

Aon Corp.: | ||||

3.125% 5/27/16 | 3,681,000 | 3,723,556 | ||

3.5% 9/30/15 | 1,538,000 | 1,578,508 | ||

5% 9/30/20 | 1,402,000 | 1,545,983 | ||

6.25% 9/30/40 | 1,150,000 | 1,413,187 | ||

Axis Capital Holdings Ltd. 5.75% 12/1/14 | 420,000 | 441,659 | ||

Liberty Mutual Group, Inc. 5% 6/1/21 (c) | 4,093,000 | 4,009,274 | ||

Lincoln National Corp. 7% 5/17/66 (i) | 4,799,000 | 4,331,098 | ||

Marsh & McLennan Companies, Inc. 4.8% 7/15/21 | 2,278,000 | 2,492,483 | ||

MetLife, Inc.: | ||||

4.75% 2/8/21 | 1,477,000 | 1,597,215 | ||

5.875% 2/6/41 | 1,577,000 | 1,842,056 | ||

6.75% 6/1/16 | 3,234,000 | 3,726,412 | ||

Metropolitan Life Global Funding I 5.125% 6/10/14 (c) | 2,884,000 | 3,105,855 | ||

New York Life Global Funding 4.65% 5/9/13 (c) | 6,045,000 | 6,338,370 | ||

New York Life Insurance Co. 6.75% 11/15/39 (c) | 1,348,000 | 1,718,155 | ||

Northwestern Mutual Life Insurance Co. 6.063% 3/30/40 (c) | 2,214,000 | 2,652,682 | ||

Pacific Life Insurance Co. 9.25% 6/15/39 (c) | 2,297,000 | 3,054,123 | ||

Pacific LifeCorp 6% 2/10/20 (c) | 2,514,000 | 2,674,800 | ||

Prudential Financial, Inc.: | ||||

4.5% 11/16/21 | 2,700,000 | 2,726,036 | ||

5.8% 11/16/41 | 2,824,000 | 2,853,104 | ||

6.2% 11/15/40 | 1,297,000 | 1,354,775 | ||

7.375% 6/15/19 | 1,250,000 | 1,477,140 | ||

8.875% 6/15/38 (i) | 4,682,000 | 5,360,890 | ||

Symetra Financial Corp. 6.125% 4/1/16 (c) | 6,355,000 | 6,423,151 | ||

The Chubb Corp. 5.75% 5/15/18 | 1,895,000 | 2,226,204 | ||

Unum Group 5.625% 9/15/20 | 2,099,000 | 2,160,541 | ||

| 77,846,868 | |||

Real Estate Investment Trusts - 0.7% | ||||

AvalonBay Communities, Inc. 5.5% 1/15/12 | 508,000 | 508,593 | ||

Camden Property Trust 5.375% 12/15/13 | 2,985,000 | 3,120,203 | ||

Developers Diversified Realty Corp.: | ||||

4.75% 4/15/18 | 2,883,000 | 2,757,739 | ||

Nonconvertible Bonds - continued | ||||

| Principal Amount | Value | ||

FINANCIALS - continued | ||||

Real Estate Investment Trusts - continued | ||||

Developers Diversified Realty Corp.: - continued | ||||

5.375% 10/15/12 | $ 1,764,000 | $ 1,780,560 | ||

7.5% 4/1/17 | 1,944,000 | 2,099,108 | ||

Duke Realty LP 4.625% 5/15/13 | 1,047,000 | 1,070,764 | ||

Equity One, Inc.: | ||||

5.375% 10/15/15 | 455,000 | 468,938 | ||

6% 9/15/17 | 2,405,000 | 2,506,662 | ||

Federal Realty Investment Trust: | ||||

5.4% 12/1/13 | 1,401,000 | 1,476,945 | ||

5.9% 4/1/20 | 1,046,000 | 1,131,755 | ||

HRPT Properties Trust: | ||||

5.75% 11/1/15 | 1,155,000 | 1,205,834 | ||

6.25% 6/15/17 | 4,455,000 | 4,686,553 | ||

UDR, Inc. 5.5% 4/1/14 | 3,685,000 | 3,891,891 | ||

United Dominion Realty Trust, Inc. 5.25% 1/15/15 | 904,000 | 961,661 | ||

| 27,667,206 | |||

Real Estate Management & Development - 2.4% | ||||

AMB Property LP 5.9% 8/15/13 | 2,575,000 | 2,669,276 | ||

BioMed Realty LP: | ||||

3.85% 4/15/16 | 3,700,000 | 3,650,561 | ||

6.125% 4/15/20 | 1,392,000 | 1,460,616 | ||

Brandywine Operating Partnership LP: | ||||

5.7% 5/1/17 | 5,000,000 | 5,177,290 | ||

5.75% 4/1/12 | 1,376,000 | 1,384,795 | ||

Colonial Properties Trust 5.5% 10/1/15 | 6,290,000 | 6,422,895 | ||

Digital Realty Trust LP: | ||||

4.5% 7/15/15 | 1,829,000 | 1,865,876 | ||

5.25% 3/15/21 | 1,953,000 | 1,955,947 | ||

Duke Realty LP: | ||||

5.4% 8/15/14 | 2,242,000 | 2,347,605 | ||

5.5% 3/1/16 | 1,270,000 | 1,335,632 | ||

5.95% 2/15/17 | 928,000 | 997,936 | ||

6.25% 5/15/13 | 2,913,000 | 3,046,724 | ||

6.5% 1/15/18 | 2,445,000 | 2,701,094 | ||

ERP Operating LP: | ||||

4.625% 12/15/21 | 7,498,000 | 7,643,146 | ||

4.75% 7/15/20 | 2,827,000 | 2,931,769 | ||

5.375% 8/1/16 | 1,066,000 | 1,159,990 | ||

5.5% 10/1/12 | 3,560,000 | 3,650,616 | ||

5.75% 6/15/17 | 5,343,000 | 5,925,382 | ||

Liberty Property LP: | ||||

4.75% 10/1/20 | 4,185,000 | 4,251,182 | ||

5.5% 12/15/16 | 2,290,000 | 2,476,571 | ||

6.625% 10/1/17 | 2,673,000 | 3,023,281 | ||

| ||||

| Principal Amount | Value | ||

Post Apartment Homes LP 6.3% 6/1/13 | $ 2,679,000 | $ 2,800,198 | ||

Reckson Operating Partnership LP 6% 3/31/16 | 3,099,000 | 3,215,941 | ||

Regency Centers LP: | ||||

5.875% 6/15/17 | 1,827,000 | 1,990,062 | ||

6.75% 1/15/12 | 2,035,000 | 2,038,103 | ||

Simon Property Group LP: | ||||

2.8% 1/30/17 | 857,000 | 875,574 | ||

4.125% 12/1/21 | 2,399,000 | 2,507,540 | ||

4.2% 2/1/15 | 1,523,000 | 1,615,260 | ||

5.1% 6/15/15 | 2,220,000 | 2,426,156 | ||

Tanger Properties LP: | ||||

6.125% 6/1/20 | 4,625,000 | 5,188,057 | ||

6.15% 11/15/15 | 349,000 | 386,352 | ||

| 89,121,427 | |||

Thrifts & Mortgage Finance - 0.2% | ||||

Bank of America Corp.: | ||||

3.75% 7/12/16 | 1,850,000 | 1,713,298 | ||

6.5% 8/1/16 | 3,000,000 | 3,021,801 | ||

First Niagara Financial Group, Inc. 6.75% 3/19/20 | 3,095,000 | 3,258,107 | ||

| 7,993,206 | |||

TOTAL FINANCIALS | 457,461,995 | |||

HEALTH CARE - 0.5% | ||||

Biotechnology - 0.1% | ||||

Amgen, Inc. 5.15% 11/15/41 | 4,000,000 | 4,138,428 | ||

Health Care Providers & Services - 0.4% | ||||

Aristotle Holding, Inc. 4.75% 11/15/21 (c) | 3,953,000 | 4,088,845 | ||

Express Scripts, Inc.: | ||||

3.125% 5/15/16 | 3,450,000 | 3,469,827 | ||

5.25% 6/15/12 | 3,016,000 | 3,073,129 | ||

6.25% 6/15/14 | 1,108,000 | 1,207,870 | ||

Medco Health Solutions, Inc. 4.125% 9/15/20 | 2,723,000 | 2,712,427 | ||

| 14,552,098 | |||

TOTAL HEALTH CARE | 18,690,526 | |||

INDUSTRIALS - 0.5% | ||||

Airlines - 0.3% | ||||

Continental Airlines, Inc.: | ||||

6.648% 3/15/19 | 1,356,055 | 1,384,804 | ||

6.795% 2/2/20 | 2,140,621 | 2,046,861 | ||

Northwest Airlines, Inc. pass-thru trust certificates 7.027% 11/1/19 | 2,770,388 | 2,822,195 | ||

Nonconvertible Bonds - continued | ||||

| Principal Amount | Value | ||

INDUSTRIALS - continued | ||||

Airlines - continued | ||||

U.S. Airways pass-thru trust certificates: | ||||

6.85% 1/30/18 | $ 1,028,020 | $ 997,046 | ||

8.36% 1/20/19 | 4,052,222 | 4,011,700 | ||

| 11,262,606 | |||

Industrial Conglomerates - 0.2% | ||||

General Electric Co. 5.25% 12/6/17 | 7,130,000 | 8,185,654 | ||

TOTAL INDUSTRIALS | 19,448,260 | |||

INFORMATION TECHNOLOGY - 0.0% | ||||

Office Electronics - 0.0% | ||||

Xerox Corp. 4.5% 5/15/21 | 1,347,000 | 1,364,617 | ||

MATERIALS - 0.9% | ||||

Chemicals - 0.5% | ||||

Dow Chemical Co.: | ||||

4.125% 11/15/21 | 3,587,000 | 3,677,805 | ||

4.25% 11/15/20 | 1,931,000 | 2,006,417 | ||

4.85% 8/15/12 | 3,520,000 | 3,601,316 | ||

5.25% 11/15/41 | 1,786,000 | 1,874,927 | ||

7.6% 5/15/14 | 7,213,000 | 8,157,492 | ||

| 19,317,957 | |||

Metals & Mining - 0.4% | ||||

Anglo American Capital PLC 9.375% 4/8/14 (c) | 2,675,000 | 3,053,938 | ||

ArcelorMittal SA 3.75% 3/1/16 | 996,000 | 945,669 | ||

Corporacion Nacional del Cobre de Chile (Codelco) 3.875% 11/3/21 (c) | 3,750,000 | 3,792,188 | ||

Rio Tinto Finance Ltd. (United States) 3.75% 9/20/21 | 2,525,000 | 2,644,776 | ||

Vale Overseas Ltd. 6.25% 1/23/17 | 3,115,000 | 3,511,113 | ||

| 13,947,684 | |||

TOTAL MATERIALS | 33,265,641 | |||

TELECOMMUNICATION SERVICES - 1.4% | ||||

Diversified Telecommunication Services - 0.9% | ||||

AT&T, Inc.: | ||||

6.3% 1/15/38 | 364,000 | 446,083 | ||

6.8% 5/15/36 | 10,939,000 | 13,826,229 | ||

CenturyLink, Inc.: | ||||

6.15% 9/15/19 | 1,562,000 | 1,568,660 | ||

6.45% 6/15/21 | 4,979,000 | 4,986,429 | ||

7.6% 9/15/39 | 488,000 | 478,151 | ||

Embarq Corp. 7.995% 6/1/36 | 1,808,000 | 1,870,779 | ||

Telefonica Emisiones SAU: | ||||

5.462% 2/16/21 | 2,456,000 | 2,342,855 | ||

5.855% 2/4/13 | 1,438,000 | 1,462,232 | ||

| ||||

| Principal Amount | Value | ||

Verizon Communications, Inc.: | ||||

6.1% 4/15/18 | $ 2,190,000 | $ 2,630,286 | ||

6.25% 4/1/37 | 1,380,000 | 1,699,517 | ||

6.9% 4/15/38 | 2,420,000 | 3,228,708 | ||

| 34,539,929 | |||

Wireless Telecommunication Services - 0.5% | ||||

America Movil SAB de CV 2.375% 9/8/16 | 5,411,000 | 5,397,115 | ||

DIRECTV Holdings LLC/DIRECTV Financing, Inc.: | ||||

4.75% 10/1/14 | 3,759,000 | 4,060,867 | ||

5.875% 10/1/19 | 4,711,000 | 5,301,128 | ||

6.35% 3/15/40 | 1,471,000 | 1,670,406 | ||

Vodafone Group PLC 5% 12/16/13 | 2,775,000 | 2,978,013 | ||

| 19,407,529 | |||

TOTAL TELECOMMUNICATION SERVICES | 53,947,458 | |||

UTILITIES - 3.0% | ||||

Electric Utilities - 1.6% | ||||

Alabama Power Co. 3.375% 10/1/20 | 2,167,000 | 2,292,636 | ||

Ameren Illinois Co. 6.125% 11/15/17 | 1,465,000 | 1,715,185 | ||

AmerenUE 6.4% 6/15/17 | 3,819,000 | 4,565,943 | ||

Commonwealth Edison Co. 1.625% 1/15/14 | 4,011,000 | 4,040,497 | ||

Duke Energy Carolinas LLC 4.25% 12/15/41 | 1,749,000 | 1,825,806 | ||

Duquesne Light Holdings, Inc.: | ||||

5.9% 12/1/21 (c) | 2,580,000 | 2,662,250 | ||

6.4% 9/15/20 (c) | 6,054,000 | 6,435,493 | ||

Edison International 3.75% 9/15/17 | 2,401,000 | 2,471,340 | ||

EDP Finance BV: | ||||

4.9% 10/1/19 (c) | 1,100,000 | 839,080 | ||

6% 2/2/18 (c) | 1,864,000 | 1,567,585 | ||

FirstEnergy Corp. 7.375% 11/15/31 | 4,457,000 | 5,473,058 | ||

FirstEnergy Solutions Corp.: | ||||

4.8% 2/15/15 | 990,000 | 1,056,769 | ||

6.05% 8/15/21 | 3,642,000 | 4,040,016 | ||

LG&E and KU Energy LLC: | ||||

2.125% 11/15/15 | 2,670,000 | 2,630,108 | ||

3.75% 11/15/20 | 525,000 | 529,801 | ||

Nevada Power Co. 6.5% 5/15/18 | 3,165,000 | 3,796,588 | ||

Pacific Gas & Electric Co. 3.25% 9/15/21 | 585,000 | 593,363 | ||

Pennsylvania Electric Co. 6.05% 9/1/17 | 2,905,000 | 3,324,921 | ||

Pepco Holdings, Inc. 2.7% 10/1/15 | 2,535,000 | 2,568,100 | ||

Nonconvertible Bonds - continued | ||||

| Principal Amount | Value | ||

UTILITIES - continued | ||||

Electric Utilities - continued | ||||

Progress Energy, Inc.: | ||||

4.4% 1/15/21 | $ 4,274,000 | $ 4,709,397 | ||

5.625% 1/15/16 | 2,000,000 | 2,284,980 | ||

Wisconsin Electric Power Co. 2.95% 9/15/21 | 679,000 | 691,751 | ||

| 60,114,667 | |||

Gas Utilities - 0.0% | ||||

Southern Natural Gas Co. / Southern Natural Issuing Corp. 4.4% 6/15/21 | 1,182,000 | 1,215,538 | ||

Independent Power Producers & Energy Traders - 0.3% | ||||

Exelon Generation Co. LLC 6.2% 10/1/17 | 6,685,000 | 7,678,632 | ||

PPL Energy Supply LLC: | ||||

6.2% 5/15/16 | 1,229,000 | 1,370,946 | ||

6.5% 5/1/18 | 2,640,000 | 3,001,009 | ||

PSEG Power LLC 2.75% 9/15/16 | 919,000 | 923,703 | ||

| 12,974,290 | |||

Multi-Utilities - 1.1% | ||||

Consolidated Edison Co. of New York, Inc. 5.7% 6/15/40 | 1,395,000 | 1,746,681 | ||

Dominion Resources, Inc.: | ||||

2.8793% 9/30/66 (i) | 9,626,000 | 8,089,402 | ||

6.25% 6/30/12 | 1,938,000 | 1,989,014 | ||

MidAmerican Energy Holdings, Co.: | ||||

5.875% 10/1/12 | 2,880,000 | 2,981,477 | ||

6.5% 9/15/37 | 1,334,000 | 1,672,002 | ||

National Grid PLC 6.3% 8/1/16 | 4,181,000 | 4,798,785 | ||

NiSource Finance Corp.: | ||||

4.45% 12/1/21 | 1,622,000 | 1,656,748 | ||

5.4% 7/15/14 | 3,885,000 | 4,215,656 | ||

5.45% 9/15/20 | 613,000 | 678,757 | ||

5.8% 2/1/42 | 2,085,000 | 2,176,859 | ||

5.95% 6/15/41 | 3,834,000 | 4,107,334 | ||

6.25% 12/15/40 | 837,000 | 911,044 | ||

6.4% 3/15/18 | 2,760,000 | 3,172,769 | ||

San Diego Gas & Electric Co. 3% 8/15/21 | 992,000 | 1,019,749 | ||

Wisconsin Energy Corp. 6.25% 5/15/67 (i) | 1,426,000 | 1,426,713 | ||

| 40,642,990 | |||

TOTAL UTILITIES | 114,947,485 | |||

TOTAL NONCONVERTIBLE BONDS (Cost $884,240,171) |

| |||

U.S. Government and Government Agency Obligations - 28.4% | ||||

| Principal | Value | ||

U.S. Government Agency Obligations - 1.1% | ||||

Fannie Mae Guaranteed Mortgage pass-thru certificates: | ||||

0.625% 10/30/14 | $ 619,000 | $ 619,761 | ||

0.75% 12/19/14 | 195,000 | 195,605 | ||

0.875% 8/28/14 | 2,750,000 | 2,772,484 | ||

Freddie Mac: | ||||

0.375% 11/27/13 | 30,614,000 | 30,570,344 | ||

0.625% 12/29/14 | 97,000 | 96,929 | ||

1% 7/30/14 | 1,456,000 | 1,471,924 | ||

1% 8/27/14 | 1,511,000 | 1,525,979 | ||

Tennessee Valley Authority 5.375% 4/1/56 | 2,375,000 | 3,207,058 | ||

U.S. Department of Housing and Urban Development Government guaranteed participation certificates Series 1996-A, 7.63% 8/1/14 | 200,000 | 201,140 | ||

TOTAL U.S. GOVERNMENT AGENCY OBLIGATIONS | 40,661,224 | |||

U.S. Treasury Inflation Protected Obligations - 2.7% | ||||

U.S. Treasury Inflation-Indexed Bonds: | ||||

2.125% 2/15/40 (f) | 27,385,310 | 36,736,584 | ||

2.125% 2/15/41 | 6,710,660 | 9,069,246 | ||

2.5% 1/15/29 | 8,437,280 | 11,255,092 | ||

U.S. Treasury Inflation-Indexed Notes: | ||||

1.125% 1/15/21 | 39,940,105 | 44,543,017 | ||

1.375% 1/15/20 | 5,236 | 5,960 | ||

TOTAL U.S. TREASURY INFLATION PROTECTED OBLIGATIONS | 101,609,899 | |||

U.S. Treasury Obligations - 24.6% | ||||

U.S. Treasury Bonds 4.375% 5/15/41 | 131,844,000 | 171,397,200 | ||

U.S. Treasury Notes: | ||||

0.5% 8/15/14 | 20,970,000 | 21,068,307 | ||

0.875% 11/30/16 | 42,223,000 | 42,358,240 | ||

1% 9/30/16 | 9,736,000 | 9,839,445 | ||

2% 11/15/21 | 29,650,000 | 29,974,312 | ||

2.125% 8/15/21 | 17,270,000 | 17,704,444 | ||

2.375% 8/31/14 | 115,000,000 | 121,154,340 | ||

2.375% 2/28/15 | 41,183,000 | 43,705,459 | ||

2.625% 7/31/14 (f) | 245,000,000 | 259,393,726 | ||

U.S. Government and Government Agency Obligations - continued | ||||

| Principal Amount | Value | ||

U.S. Treasury Obligations - continued | ||||

U.S. Treasury Notes: - continued | ||||

2.625% 12/31/14 | $ 55,045,000 | $ 58,713,254 | ||

3.125% 5/15/21 | 143,205,000 | 159,819,071 | ||

TOTAL U.S. TREASURY OBLIGATIONS | 935,127,798 | |||

TOTAL U.S. GOVERNMENT AND GOVERNMENT AGENCY OBLIGATIONS (Cost $988,545,627) |

| |||

U.S. Government Agency - Mortgage Securities - 38.4% | ||||

| ||||

Fannie Mae Guaranteed Mortgage pass-thru certificates - 24.6% | ||||

1.67% 9/1/33 (i) | 710,809 | 736,546 | ||

1.807% 5/1/34 (i) | 1,222,299 | 1,261,003 | ||

1.946% 7/1/35 (i) | 45,796 | 48,100 | ||

1.96% 10/1/33 (i) | 48,339 | 50,451 | ||

2.05% 3/1/35 (i) | 19,527 | 20,615 | ||

2.11% 10/1/33 (i) | 1,046,769 | 1,088,555 | ||

2.301% 7/1/34 (i) | 57,800 | 61,231 | ||

2.303% 6/1/36 (i) | 101,216 | 107,298 | ||

2.424% 10/1/33 (i) | 91,062 | 96,162 | ||

2.457% 3/1/35 (i) | 63,743 | 67,106 | ||

2.474% 11/1/36 (i) | 1,319,802 | 1,405,589 | ||

2.478% 8/1/36 (i) | 1,776,301 | 1,867,453 | ||

2.5% 7/1/35 (i) | 118,450 | 125,814 | ||

2.537% 2/1/36 (i) | 1,122,101 | 1,172,553 | ||

2.623% 5/1/36 (i) | 400,730 | 419,662 | ||

2.635% 7/1/37 (i) | 231,692 | 246,752 | ||

2.654% 5/1/35 (i) | 232,880 | 245,621 | ||

2.695% 12/1/35 (i) | 525,216 | 558,213 | ||

2.702% 9/1/36 (i) | 1,126,250 | 1,199,456 | ||

3% 1/1/27 (e) | 9,000,000 | 9,295,118 | ||

3.5% 1/1/26 to 3/1/41 | 13,993,407 | 14,733,546 | ||

3.5% 1/1/27 (e) | 16,400,000 | 17,149,121 | ||

3.5% 1/1/27 (e) | 16,400,000 | 17,149,121 | ||

3.791% 6/1/40 (i) | 1,655,684 | 1,726,746 | ||

4% 11/1/26 to 11/1/41 | 134,830,973 | 142,033,195 | ||

4% 9/1/41 | 265,492 | 279,363 | ||

4% 10/1/41 | 7,495,660 | 7,900,151 | ||

4% 10/1/41 | 249,229 | 262,679 | ||

4% 1/1/42 (e) | 35,400,000 | 37,185,852 | ||

4% 1/1/42 (e) | 37,000,000 | 38,866,569 | ||

| ||||

| Principal | Value | ||

4.5% 4/1/18 to 11/1/41 | $ 207,069,697 | $ 221,376,725 | ||

4.5% 1/1/27 (e) | 9,600,000 | 10,232,331 | ||

4.5% 1/1/42 (e) | 33,600,000 | 35,762,308 | ||

5% 2/1/18 to 6/1/40 | 88,921,077 | 96,168,712 | ||

5.5% 11/1/17 to 3/1/39 | 111,001,841 | 120,888,839 | ||

5.5% 1/1/42 (e) | 13,000,000 | 14,155,890 | ||

6% 6/1/14 to 11/1/39 | 117,210,821 | 128,901,939 | ||

6.5% 6/1/13 to 2/1/36 | 4,816,058 | 5,244,894 | ||

7% 3/1/15 to 8/1/32 | 1,692,442 | 1,924,724 | ||

7.5% 7/1/16 to 11/1/31 | 1,414,926 | 1,656,045 | ||

8% 1/1/30 to 5/1/30 | 46,659 | 55,621 | ||

8.5% 3/1/25 to 6/1/25 | 797 | 955 | ||

TOTAL FANNIE MAE GUARANTEED MORTGAGE PASS-THRU CERTIFICATES | 933,728,624 | |||

Freddie Mac - 6.9% | ||||

2.081% 4/1/35 (i) | 862,606 | 912,457 | ||

2.125% 3/1/36 (i) | 182,234 | 191,980 | ||

2.499% 1/1/35 (i) | 193,529 | 199,835 | ||

2.906% 3/1/33 (i) | 17,706 | 18,857 | ||

2.91% 11/1/35 (i) | 382,060 | 406,622 | ||

3.135% 10/1/35 (i) | 144,193 | 153,588 | ||

4% 12/1/40 to 10/1/41 | 7,970,220 | 8,404,791 | ||

4% 9/1/41 | 946,925 | 997,617 | ||

4% 1/1/42 (e) | 37,500,000 | 39,327,341 | ||

4.5% 7/1/25 to 10/1/41 | 79,040,195 | 84,009,732 | ||

4.5% 1/1/42 (e) | 14,000,000 | 14,841,898 | ||

5% 7/1/35 to 9/1/40 | 32,544,777 | 35,167,744 | ||

5.5% 1/1/38 to 1/1/40 | 51,362,744 | 55,625,322 | ||

5.5% 1/1/42 (e) | 13,700,000 | 14,856,053 | ||

6% 4/1/32 to 8/1/37 | 5,762,179 | 6,366,327 | ||

7.5% 5/1/17 to 11/1/31 | 142,603 | 165,429 | ||

8% 7/1/17 to 5/1/27 | 9,327 | 10,665 | ||

8.5% 3/1/20 to 1/1/28 | 127,586 | 150,476 | ||

TOTAL FREDDIE MAC | 261,806,734 | |||

Ginnie Mae - 6.9% | ||||

3.5% 1/15/41 to 2/15/41 | 1,717,366 | 1,797,004 | ||

3.5% 1/1/42 (e) | 12,000,000 | 12,534,901 | ||

4% 1/15/25 to 12/15/41 (e) | 52,739,344 | 56,691,106 | ||

4% 1/1/42 (e) | 24,000,000 | 25,745,122 | ||

4% 1/1/42 (e) | 400,000 | 429,085 | ||

4.5% 5/15/39 to 4/20/41 | 63,176,035 | 69,049,768 | ||

4.5% 1/1/42 (e) | 2,800,000 | 3,051,505 | ||

5% 3/15/39 to 8/15/41 (e) | 54,053,331 | 60,019,423 | ||

5% 9/15/41 (e) | 897,543 | 994,379 | ||

5% 1/1/42 (e) | 15,100,000 | 16,728,295 | ||

5% 1/1/42 (e) | 1,700,000 | 1,883,318 | ||

6% 3/15/29 to 11/15/34 | 6,004,460 | 6,811,239 | ||

U.S. Government Agency - Mortgage Securities - continued | ||||

| Principal Amount | Value | ||

Ginnie Mae - continued | ||||

6.5% 10/15/34 to 11/15/35 | $ 402,980 | $ 462,375 | ||

7% 1/15/28 to 7/15/32 | 2,858,268 | 3,276,123 | ||

7.5% 4/15/22 to 10/15/28 | 711,717 | 821,413 | ||

8% 2/15/17 to 9/15/30 | 57,771 | 67,035 | ||

8.5% 12/15/16 to 3/15/30 | 11,780 | 13,463 | ||

TOTAL GINNIE MAE | 260,375,554 | |||

TOTAL U.S. GOVERNMENT AGENCY - MORTGAGE SECURITIES (Cost $1,432,875,930) |

| |||

Asset-Backed Securities - 2.3% | ||||

| ||||

Accredited Mortgage Loan Trust Series 2005-1 Class M1, 0.7636% 4/25/35 (i) | 451,680 | 246,481 | ||

ACE Securities Corp. Home Equity Loan Trust Series 2005-HE2 Class M2, 0.7436% 4/25/35 (i) | 40,770 | 39,537 | ||

Advanta Business Card Master Trust Series 2006-C1 Class C1, 0.6758% 10/20/14 (i) | 169,000 | 1,690 | ||

Airspeed Ltd. Series 2007-1A Class C1, 2.7783% 6/15/32 (c)(i) | 2,643,255 | 1,361,277 | ||

Ally Auto Receivables Trust: | ||||

Series 2009-A: | ||||

Class A3, 2.33% 6/17/13 (c) | 750,851 | 754,273 | ||

Class A4, 3% 10/15/15 (c) | 1,600,000 | 1,630,343 | ||

Series 2010-5 Class A4, 1.75% 3/15/16 | 1,430,000 | 1,447,664 | ||

Series 2011-1 Class A4, 2.23% 3/15/16 | 6,420,000 | 6,578,167 | ||

Ally Master Owner Trust: | ||||

Series 2010-3 Class A, 2.88% 4/15/15 (c) | 3,400,000 | 3,456,098 | ||

Series 2011-1 Class A2, 2.15% 1/15/16 | 3,150,000 | 3,183,851 | ||

Series 2011-3 Class A2, 1.81% 5/15/16 | 2,760,000 | 2,773,072 | ||

AmeriCredit Automobile Receivables Trust Series 2011-1 Class A3, 1.39% 9/8/15 | 2,660,000 | 2,671,039 | ||

Ameriquest Mortgage Securities, Inc. pass-thru certificates: | ||||

Series 2003-10 Class M1, 0.9936% 12/25/33 (i) | 29,859 | 23,355 | ||

Series 2004-R2 Class M3, 0.8436% 4/25/34 (i) | 47,022 | 14,847 | ||

Series 2005-R2 Class M1, 0.7436% 4/25/35 (i) | 727,000 | 643,946 | ||

| ||||

| Principal Amount | Value | ||

Argent Securities, Inc. pass-thru certificates: | ||||

Series 2003-W7 Class A2, 1.0372% 3/25/34 (i) | $ 16,878 | $ 11,273 | ||

Series 2004-W11 Class M2, 0.9936% 11/25/34 (i) | 198,000 | 137,831 | ||

Series 2004-W7 Class M1, 0.8436% 5/25/34 (i) | 209,000 | 149,783 | ||

Series 2006-W4 Class A2C, 0.4536% 5/25/36 (i) | 474,181 | 122,330 | ||

Asset Backed Securities Corp. Home Equity Loan Trust Series 2004-HE2 Class M1, 1.1186% 4/25/34 (i) | 902,083 | 613,577 | ||

Bank of America Auto Trust Series 2009-1A Class A4, 3.52% 6/15/16 (c) | 3,100,000 | 3,154,498 | ||

BMW Vehicle Lease Trust Series 2010-1 Class A3, 0.82% 4/15/13 | 5,250,000 | 5,249,069 | ||

Brazos Higher Education Authority, Inc. Series 2006-2 Class A9, 0.5838% 12/25/24 (i) | 493,407 | 434,198 | ||

Carmax Auto Owner Trust Series 2011-1 Class A3, 1.29% 9/15/15 | 2,760,000 | 2,774,199 | ||

Carrington Mortgage Loan Trust: | ||||

Series 2006-FRE1 Class M1, 0.5936% 7/25/36 (i) | 402,000 | 14,786 | ||

Series 2007-RFC1 Class A3, 0.4336% 12/25/36 (i) | 635,000 | 196,780 | ||

Chrysler Financial Auto Securitization Trust Series 2010-A Class A3, 0.91% 8/8/13 | 6,300,000 | 6,301,721 | ||

Citibank Credit Card Issuance Trust Series 2009-A5 Class A5, 2.25% 12/23/14 | 12,500,000 | 12,684,690 | ||

Countrywide Home Loans, Inc.: | ||||

Series 2003-BC1 Class B1, 5.4035% 3/25/32 (MGIC Investment Corp. Insured) (i) | 40,946 | 3,088 | ||

Series 2004-3 Class M4, 1.2636% 4/25/34 (i) | 56,336 | 27,234 | ||

Series 2004-4 Class M2, 1.0886% 6/25/34 (i) | 207,174 | 93,106 | ||

Series 2005-3 Class MV1, 0.7136% 8/25/35 (i) | 129,199 | 126,373 | ||

Series 2005-AB1 Class A2, 0.5036% 8/25/35 (i) | 3,230 | 3,224 | ||

Fannie Mae subordinate REMIC pass-thru certificates Series 2004-T5 Class AB3, 0.7513% 5/28/35 (i) | 13,702 | 8,735 | ||

Fieldstone Mortgage Investment Corp. Series 2004-3 Class M5, 2.4686% 8/25/34 (i) | 102,000 | 59,562 | ||

First Franklin Mortgage Loan Trust Series 2004-FF2 Class M3, 1.1186% 3/25/34 (i) | 5,606 | 687 | ||

Asset-Backed Securities - continued | ||||

| Principal Amount | Value | ||

Ford Credit Auto Lease Trust Series 2010-B Class A3, 0.91% 7/15/13 (c) | $ 5,190,000 | $ 5,191,778 | ||

Ford Credit Auto Owner Trust: | ||||

Series 2009-D: | ||||

Class A3, 2.17% 10/15/13 | 734,023 | 737,774 | ||

Class A4, 2.98% 8/15/14 | 1,800,000 | 1,839,452 | ||

Series 2010-B Class A3, 0.98% 10/15/14 | 3,356,069 | 3,361,786 | ||

Ford Credit Floorplan Master Owner Trust Series 2010-5 Class A1, 1.5% 9/15/15 | 3,580,000 | 3,585,844 | ||

Fremont Home Loan Trust Series 2005-A: | ||||

Class M3, 0.7836% 1/25/35 (i) | 334,000 | 99,705 | ||

Class M4, 0.9736% 1/25/35 (i) | 128,000 | 29,336 | ||

GCO Education Loan Funding Master Trust II Series 2007-1A Class C1L, 0.8861% 2/25/47 (c)(i) | 829,000 | 414,500 | ||

GE Business Loan Trust Series 2003-1 Class A, 0.7083% 4/15/31 (c)(i) | 80,277 | 76,389 | ||

GSAMP Trust: | ||||

Series 2004-AR1: | ||||

Class B4, 4.8751% 6/25/34 (c)(i) | 140,338 | 40,015 | ||

Class M1, 0.9436% 6/25/34 (i) | 772,000 | 476,478 | ||

Series 2007-HE1 Class M1, 0.5436% 3/25/47 (i) | 289,000 | 11,060 | ||

Guggenheim Structured Real Estate Funding Ltd. Series 2006-3 Class C, 0.8436% 9/25/46 (c)(i) | 538,000 | 70,908 | ||

Home Equity Asset Trust: | ||||

Series 2003-3 Class M1, 1.5836% 8/25/33 (i) | 248,220 | 194,766 | ||

Series 2003-5 Class A2, 0.9936% 12/25/33 (i) | 11,595 | 7,955 | ||

Series 2005-5 Class 2A2, 0.5436% 11/25/35 (i) | 7,010 | 6,970 | ||

Series 2006-1 Class 2A3, 0.5186% 4/25/36 (i) | 154,916 | 153,170 | ||

HSBC Home Equity Loan Trust Series 2006-2 Class M2, 0.5749% 3/20/36 (i) | 220,749 | 178,905 | ||

HSI Asset Securitization Corp. Trust Series 2007-HE1 Class 2A3, 0.4836% 1/25/37 (i) | 436,000 | 144,643 | ||

Hyundai Auto Receivables Trust Series 2009-A Class A3, 2.03% 8/15/13 | 815,069 | 818,285 | ||

JPMorgan Mortgage Acquisition Trust Series 2007-CH1: | ||||

Class AV4, 0.4236% 11/25/36 (i) | 438,000 | 365,669 | ||

Class MV1, 0.5236% 11/25/36 (i) | 356,000 | 173,532 | ||

| ||||

| Principal Amount | Value | ||

Keycorp Student Loan Trust Series 1999-A Class A2, 0.9038% 12/27/29 (i) | $ 209,085 | $ 182,963 | ||

Long Beach Mortgage Loan Trust Series 2004-2 Class M2, 1.3736% 6/25/34 (i) | 30,272 | 19,005 | ||

MASTR Asset Backed Securities Trust: | ||||

Series 2006-AM3 Class M1, 0.5536% 10/25/36 (i) | 158,000 | 4,359 | ||

Series 2007-HE1 Class M1, 0.5936% 5/25/37 (i) | 249,000 | 6,087 | ||

Merrill Lynch Mortgage Investors Trust: | ||||

Series 2003-OPT1 Class M1, 1.2686% 7/25/34 (i) | 30,884 | 20,866 | ||

Series 2006-FM1 Class A2B, 0.4036% 4/25/37 (i) | 497,020 | 359,253 | ||

Series 2006-OPT1 Class A1A, 0.5536% 6/25/35 (i) | 516,281 | 368,015 | ||

Morgan Stanley ABS Capital I Trust: | ||||

Series 2004-HE6 Class A2, 0.6336% 8/25/34 (i) | 20,187 | 14,709 | ||

Series 2004-NC8 Class M6, 1.5436% 9/25/34 (i) | 100,003 | 56,961 | ||

Series 2005-NC1 Class M1, 0.7336% 1/25/35 (i) | 141,000 | 89,004 | ||

New Century Home Equity Loan Trust: | ||||

Series 2005-4 Class M2, 0.8036% 9/25/35 (i) | 503,000 | 217,110 | ||

Series 2005-D Class M2, 0.7636% 2/25/36 (i) | 105,000 | 9,826 | ||

Nissan Auto Receivables Owner Trust Series 2010-A Class A4, 1.31% 9/15/16 | 2,140,000 | 2,153,964 | ||

Ocala Funding LLC Series 2006-1A Class A, 1.6849% 3/20/11 (b)(c)(i) | 414,000 | 0 | ||

Park Place Securities, Inc.: | ||||

Series 2004-WCW1: | ||||

Class M3, 1.5436% 9/25/34 (i) | 188,000 | 64,733 | ||

Class M4, 1.7436% 9/25/34 (i) | 241,000 | 54,083 | ||

Series 2005-WCH1: | ||||

Class M2, 0.8136% 1/25/36 (i) | 1,972,000 | 1,693,847 | ||

Class M3, 0.8536% 1/25/36 (i) | 168,000 | 104,532 | ||

Class M4, 1.1236% 1/25/36 (i) | 520,000 | 192,007 | ||

Series 2005-WHQ2 Class M7, 1.5436% 5/25/35 (i) | 736,833 | 4,780 | ||

Salomon Brothers Mortgage Securities VII, Inc. Series 2003-HE1 Class A, 1.0936% 4/25/33 (i) | 1,796 | 1,454 | ||

Asset-Backed Securities - continued | ||||

| Principal Amount | Value | ||

Saxon Asset Securities Trust Series 2004-1 Class M1, 1.0886% 3/25/35 (i) | $ 481,647 | $ 299,405 | ||

Sierra Receivables Funding Co. Series 2007-1A Class A2, 0.4048% 3/20/19 (FGIC Insured) (c)(i) | 164,772 | 157,716 | ||

SLM Private Credit Student Loan Trust Series 2004-A Class C, 1.4963% 6/15/33 (i) | 448,000 | 215,954 | ||

Structured Asset Investment Loan Trust Series 2004-8 Class M5, 2.0186% 9/25/34 (i) | 23,321 | 9,003 | ||

Terwin Mortgage Trust Series 2003-4HE Class A1, 1.1536% 9/25/34 (i) | 10,148 | 7,220 | ||

Volkswagen Auto Lease Trust Series 2010-A Class A3, 0.99% 11/20/13 | 5,630,000 | 5,638,092 | ||

Whinstone Capital Management Ltd. Series 1A Class B3, 2.2183% 10/25/44 (c)(i) | 630,180 | 277,279 | ||

TOTAL ASSET-BACKED SECURITIES (Cost $91,083,708) |

| |||

Collateralized Mortgage Obligations - 1.1% | ||||

| ||||

Private Sponsor - 0.9% | ||||

Banc of America Mortgage Securities, Inc.: | ||||

Series 2004-B Class 1A1, 2.7465% 3/25/34 (i) | 19,735 | 16,388 | ||

Series 2005-E Class 2A7, 2.8416% 6/25/35 (i) | 2,680,000 | 1,718,651 | ||

Bear Stearns ALT-A Trust floater Series 2005-1 Class A1, 0.8536% 1/25/35 (i) | 687,769 | 485,652 | ||

Chase Mortgage Finance Trust: | ||||

Series 2007-A1 Class 1A5, 2.7533% 2/25/37 (i) | 350,631 | 312,058 | ||

Series 2007-A2 Class 2A1, 2.7671% 7/25/37 (i) | 187,958 | 184,925 | ||

Citigroup Mortgage Loan Trust Series 2004-UST1 Class A4, 2.2695% 8/25/34 (i) | 2,069,311 | 2,031,674 | ||

Credit Suisse First Boston Mortgage Securities Corp. floater Series 2007-AR7 Class 2A1, 2.7759% 11/25/34 (i) | 692,952 | 590,972 | ||

Granite Master Issuer PLC floater: | ||||

Series 2006-1A Class C2, 1.4849% 12/20/54 (c)(i) | 2,117,000 | 1,084,963 | ||

Series 2006-2 Class C1, 1.2249% 12/20/54 (i) | 1,885,000 | 966,063 | ||

Series 2006-3 Class C2, 0.7849% 12/20/54 (i) | 396,000 | 202,950 | ||

| ||||

| Principal Amount | Value | ||

Series 2006-4: | ||||

Class B1, 0.4649% 12/20/54 (i) | $ 1,059,000 | $ 868,380 | ||

Class C1, 1.0449% 12/20/54 (i) | 647,000 | 331,588 | ||

Class M1, 0.6249% 12/20/54 (i) | 279,000 | 202,275 | ||

Series 2007-1: | ||||

Class 1C1, 0.8849% 12/20/54 (i) | 654,000 | 335,175 | ||

Class 1M1, 0.5849% 12/20/54 (i) | 425,000 | 308,125 | ||

Class 2C1, 1.2449% 12/20/54 (i) | 298,000 | 152,725 | ||

Class 2M1, 0.7849% 12/20/54 (i) | 546,000 | 395,850 | ||

Series 2007-2 Class 2C1, 0.7146% 12/17/54 (i) | 757,000 | 387,963 | ||

Granite Mortgages PLC floater Series 2003-3 Class 1C, 2.8592% 1/20/44 (i) | 151,584 | 97,105 | ||

JPMorgan Chase Commercial Mortgage Securities Trust Series 2007-CB18 Class A3, 5.447% 6/12/47 (i) | 6,099,246 | 6,407,167 | ||

JPMorgan Mortgage Trust: | ||||

Series 2004-A5 Class 2A1, 2.3733% 12/25/34 (i) | 632,979 | 555,477 | ||

Series 2006-A2 Class 5A1, 2.6481% 11/25/33 (i) | 775,425 | 691,159 | ||

Series 2007-A1 Class 1A1, 2.8092% 7/25/35 (i) | 1,926,149 | 1,637,354 | ||

MASTR Adjustable Rate Mortgages Trust Series 2007-3 Class 22A2, 0.5036% 5/25/47 (i) | 299,074 | 184,604 | ||

Merrill Lynch Alternative Note Asset Trust floater Series 2007-OAR1 Class A1, 0.4636% 2/25/37 (i) | 444,647 | 290,037 | ||

Merrill Lynch Floating Trust floater Series 2006-1: | ||||

Class C, 0.468% 6/15/22 (c)(i) | 449,000 | 438,898 | ||

Class D, 0.478% 6/15/22 (c)(i) | 173,000 | 168,675 | ||

Class E, 0.488% 6/15/22 (c)(i) | 276,000 | 268,410 | ||

Class F, 0.518% 6/15/22 (c)(i) | 498,000 | 483,060 | ||

Class G, 0.588% 6/15/22 (c)(i) | 103,000 | 99,653 | ||

Class H, 0.608% 6/15/22 (c)(i) | 207,000 | 199,755 | ||

Class J, 0.648% 6/15/22 (c)(i) | 242,000 | 232,925 | ||

Opteum Mortgage Acceptance Corp. floater Series 2005-3 Class APT, 0.5836% 7/25/35 (i) | 717,264 | 542,379 | ||

Option One Mortgage Loan Trust floater Series 2007-CP1 Class M1, 0.5936% 3/25/37 (i) | 861,000 | 33,064 | ||

Provident Funding Mortgage Loan Trust Series 2005-2 Class 3A, 2.6531% 10/25/35 (i) | 1,395,452 | 1,029,802 | ||

Collateralized Mortgage Obligations - continued | ||||

| Principal Amount | Value | ||

Private Sponsor - continued | ||||

RESI Finance LP/RESI Finance DE Corp. floater Series 2003-B Class B5, 2.6263% 7/10/35 (c)(i) | $ 239,380 | $ 154,664 | ||

Residential Asset Mortgage Products, Inc. sequential payer Series 2003-SL1 Class A31, 7.125% 4/25/31 | 47,660 | 50,490 | ||

Residential Funding Securities Corp. floater Series 2003-RP2 Class A1, 0.7436% 6/25/33 (c)(i) | 63,908 | 58,966 | ||

Sequoia Mortgage Trust floater Series 2004-6 Class A3B, 1.275% 7/20/34 (i) | 12,620 | 8,401 | ||

TBW Mortgage-Backed pass-thru certificates floater Series 2006-4 Class A3, 0.4572% 9/25/36 (i) | 1,153,000 | 854,259 | ||

Wells Fargo Mortgage Backed Securities Trust: | ||||

Series 2004-H Class A1, 2.7436% 6/25/34 (i) | 557,916 | 518,230 | ||

Series 2005-AR10 Class 2A2, 2.703% 6/25/35 (i) | 2,340,823 | 2,050,893 | ||

Series 2005-AR12: | ||||

Class 2A5, 2.705% 7/25/35 (i) | 3,269,322 | 2,823,907 | ||

Class 2A6, 2.705% 7/25/35 (i) | 3,063,115 | 2,611,048 | ||

Series 2005-AR3 Class 2A1, 2.6974% 3/25/35 (i) | 632,268 | 535,613 | ||

TOTAL PRIVATE SPONSOR | 33,602,372 | |||

U.S. Government Agency - 0.2% | ||||

Fannie Mae Guaranteed Mortgage pass-thru certificates planned amortization class: | ||||

Series 1999-54 Class PH, 6.5% 11/18/29 | 1,417,148 | 1,559,138 | ||

Series 1999-57 Class PH, 6.5% 12/25/29 | 1,047,268 | 1,169,405 | ||

Fannie Mae subordinate REMIC pass-thru certificates: | ||||

planned amortization class Series 2002-9 Class PC, 6% 3/25/17 | 139,075 | 149,825 | ||

sequential payer Series 2004-86 Class KC, 4.5% 5/25/19 | 253,109 | 262,351 | ||

| ||||

| Principal Amount | Value | ||

Freddie Mac Multi-class participation certificates guaranteed planned amortization class Series 2500 Class TE, 5.5% 9/15/17 | $ 3,376,173 | $ 3,615,772 | ||

Ginnie Mae guaranteed REMIC pass-thru certificates Series 2007-35 Class SC, 38.5047% 6/16/37 (i)(k) | 124,008 | 240,020 | ||

TOTAL U.S. GOVERNMENT AGENCY | 6,996,511 | |||

TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS (Cost $42,805,544) |

| |||

Commercial Mortgage Securities - 6.3% | ||||

| ||||

Asset Securitization Corp. Series 1997-D5: | ||||

Class A2, 7.08% 2/14/43 (i) | 1,435,000 | 1,461,027 | ||

Class A3, 7.13% 2/14/43 (i) | 1,545,000 | 1,581,749 | ||

Banc of America Commercial Mortgage Trust: | ||||

sequential payer: | ||||

Series 2006-2 Class AAB, 5.9029% 5/10/45 (i) | 1,839,138 | 1,948,097 | ||

Series 2006-5: | ||||

Class A2, 5.317% 9/10/47 | 7,446,514 | 7,526,229 | ||

Class A3, 5.39% 9/10/47 | 1,985,000 | 2,075,161 | ||

Series 2007-2: | ||||

Class B, 5.6425% 4/10/49 (i) | 485,000 | 130,913 | ||

Class C, 5.8173% 4/10/49 (i) | 1,290,000 | 301,888 | ||

Class D, 5.8173% 4/10/49 (i) | 650,000 | 117,033 | ||

Series 2007-3 Class A3, 5.8009% 6/10/49 (i) | 6,100,000 | 6,361,251 | ||

Banc of America Commercial Mortgage, Inc.: | ||||

sequential payer: | ||||

Series 2005-1 Class A3, 4.877% 11/10/42 | 579,891 | 579,495 | ||

Series 2007-1 Class A2, 5.381% 1/15/49 | 739,242 | 738,299 | ||

Series 2001-3 Class H, 6.562% 4/11/37 (c) | 4,889,139 | 4,887,183 | ||

Banc of America Large Loan, Inc. floater: | ||||

Series 2005-MIB1: | ||||

Class F, 0.7483% 3/15/22 (c)(i) | 217,000 | 206,150 | ||

Class G, 0.8083% 3/15/22 (c)(i) | 141,000 | 131,130 | ||

Series 2006-BIX1: | ||||

Class F, 0.5883% 10/15/19 (c)(i) | 558,000 | 518,940 | ||

Class G, 0.6083% 10/15/19 (c)(i) | 380,000 | 336,300 | ||

Commercial Mortgage Securities - continued | ||||

| Principal Amount | Value | ||

Bayview Commercial Asset Trust: | ||||

floater: | ||||

Series 2004-1: | ||||

Class A, 0.6536% 4/25/34 (c)(i) | $ 440,694 | $ 342,134 | ||

Class B, 2.1936% 4/25/34 (c)(i) | 34,632 | 19,796 | ||

Class M1, 0.8536% 4/25/34 (c)(i) | 28,219 | 20,037 | ||

Class M2, 1.4936% 4/25/34 (c)(i) | 25,287 | 17,504 | ||

Series 2004-2: | ||||

Class A, 0.7236% 8/25/34 (c)(i) | 344,887 | 267,927 | ||

Class M1, 0.8736% 8/25/34 (c)(i) | 55,701 | 40,534 | ||

Series 2004-3: | ||||

Class A1, 0.6636% 1/25/35 (c)(i) | 700,939 | 526,847 | ||

Class A2, 0.7136% 1/25/35 (c)(i) | 91,240 | 64,005 | ||

Class M1, 0.7936% 1/25/35 (c)(i) | 93,387 | 62,078 | ||

Class M2, 1.2936% 1/25/35 (c)(i) | 60,379 | 36,184 | ||

Series 2005-2A: | ||||

Class A1, 0.6036% 8/25/35 (c)(i) | 389,654 | 298,094 | ||

Class M1, 0.7236% 8/25/35 (c)(i) | 28,891 | 16,671 | ||

Class M2, 0.7736% 8/25/35 (c)(i) | 47,519 | 25,541 | ||

Class M3, 0.7936% 8/25/35 (c)(i) | 26,230 | 13,901 | ||

Series 2005-3A: | ||||

Class A1, 0.6136% 11/25/35 (c)(i) | 215,488 | 161,256 | ||

Class A2, 0.6936% 11/25/35 (c)(i) | 139,629 | 105,023 | ||

Series 2005-4A: | ||||

Class A2, 0.6836% 1/25/36 (c)(i) | 746,466 | 515,252 | ||

Class M1, 0.7436% 1/25/36 (c)(i) | 156,186 | 87,278 | ||

Class M2, 0.7636% 1/25/36 (c)(i) | 47,118 | 24,162 | ||

Class M3, 0.7936% 1/25/36 (c)(i) | 68,495 | 32,335 | ||

Series 2006-1 Class A2, 0.6536% 4/25/36 (c)(i) | 74,942 | 54,883 | ||

Series 2006-2A: | ||||

Class A1, 0.5236% 7/25/36 (c)(i) | 730,432 | 538,727 | ||

Class A2, 0.5736% 7/25/36 (c)(i) | 65,932 | 42,550 | ||

Class M1, 0.6036% 7/25/36 (c)(i) | 69,229 | 39,110 | ||

| ||||

| Principal Amount | Value | ||

Class M2, 0.6236% 7/25/36 (c)(i) | $ 48,978 | $ 25,269 | ||

Class M6, 0.8336% 7/25/36 (c)(i) | 49,920 | 15,163 | ||

Series 2006-3A: | ||||

Class M5, 0.7736% 10/25/36 (c)(i) | 64,655 | 6,789 | ||

Class M6, 0.8536% 10/25/36 (c)(i) | 126,260 | 9,469 | ||

Series 2006-4A: | ||||

Class A1, 0.5236% 12/25/36 (c)(i) | 461,734 | 281,658 | ||

Class A2, 0.5636% 12/25/36 (c)(i) | 1,029,059 | 607,145 | ||

Class M1, 0.5836% 12/25/36 (c)(i) | 74,570 | 30,596 | ||

Series 2007-1: | ||||

Class A2, 0.5636% 3/25/37 (c)(i) | 198,139 | 85,200 | ||

Class B3, 3.6436% 3/25/37 (c)(i) | 22,055 | 441 | ||

Series 2007-2A: | ||||

Class A1, 0.5636% 7/25/37 (c)(i) | 186,365 | 106,469 | ||

Class A2, 0.6136% 7/25/37 (c)(i) | 174,438 | 68,127 | ||

Class B1, 1.8936% 7/25/37 (c)(i) | 164,001 | 7,471 | ||

Class B2, 2.5436% 7/25/37 (c)(i) | 97,204 | 3,195 | ||

Class M2, 0.7036% 7/25/37 (c)(i) | 96,910 | 12,231 | ||

Class M3, 0.7836% 7/25/37 (c)(i) | 96,910 | 10,247 | ||

Class M4, 0.9436% 7/25/37 (c)(i) | 205,001 | 18,107 | ||

Class M5, 1.0436% 7/25/37 (c)(i) | 182,638 | 13,656 | ||

Class M6, 1.2936% 7/25/37 (c)(i) | 227,365 | 13,791 | ||

Series 2007-3: | ||||

Class A2, 0.5836% 7/25/37 (c)(i) | 286,301 | 99,722 | ||

Class B1, 1.2436% 7/25/37 (c)(i) | 132,324 | 12,783 | ||

Class B2, 1.8936% 7/25/37 (c)(i) | 462,532 | 31,421 | ||

Class B3, 4.2936% 7/25/37 (c)(i) | 90,466 | 3,000 | ||

Class M1, 0.6036% 7/25/37 (c)(i) | 117,287 | 35,171 | ||

Class M2, 0.6336% 7/25/37 (c)(i) | 123,302 | 31,385 | ||

Class M3, 0.6636% 7/25/37 (c)(i) | 269,459 | 58,767 | ||

Class M4, 0.7936% 7/25/37 (c)(i) | 425,842 | 79,113 | ||

Commercial Mortgage Securities - continued | ||||

| Principal Amount | Value | ||

Bayview Commercial Asset Trust: - continued | ||||

floater: | ||||

Series 2007-3: | ||||

Class M5, 0.8936% 7/25/37 (c)(i) | $ 159,390 | $ 25,882 | ||

Class M6, 1.0936% 7/25/37 (c)(i) | 120,294 | 14,658 | ||

Series 2007-4A: | ||||

Class B1, 2.8436% 9/25/37 (c)(i) | 233,022 | 3,495 | ||

Class B2, 3.7436% 9/25/37 (c)(i) | 24,948 | 249 | ||

Class M4, 1.8936% 9/25/37 (c)(i) | 750,491 | 30,020 | ||

Class M5, 2.0436% 9/25/37 (c)(i) | 750,491 | 22,515 | ||

Class M6, 2.2436% 9/25/37 (c)(i) | 750,491 | 15,010 | ||

Series 2004-1, Class IO, 1.25% 4/25/34 (c)(j) | 1,258,218 | 44,667 | ||

Bear Stearns Commercial Mortgage Securities Trust: | ||||

floater: | ||||

Series 2006-BBA7: | ||||

Class H, 0.9283% 3/15/19 (c)(i) | 148,890 | 142,357 | ||

Class J, 1.1283% 3/15/19 (c)(i) | 143,000 | 122,396 | ||

Series 2007-BBA8: | ||||

Class D, 0.5283% 3/15/22 (c)(i) | 147,000 | 133,266 | ||

Class E, 0.5783% 3/15/22 (c)(i) | 763,000 | 686,374 | ||

Class F, 0.6283% 3/15/22 (c)(i) | 468,000 | 412,108 | ||

Class G, 0.6783% 3/15/22 (c)(i) | 120,000 | 104,313 | ||

Class H, 0.8283% 3/15/22 (c)(i) | 147,000 | 124,843 | ||

Class J, 0.9783% 3/15/22 (c)(i) | 147,000 | 114,553 | ||

Series 2006-PW13 Class A3, 5.518% 9/11/41 | 2,010,000 | 2,108,798 | ||

Series 2007-PW16: | ||||

Class B, 5.9043% 6/11/40 (c)(i) | 1,405,000 | 665,849 | ||

Class C, 5.9043% 6/11/40 (c)(i) | 1,170,000 | 413,009 | ||

Class D, 5.9043% 6/11/40 (c)(i) | 1,170,000 | 321,942 | ||

C-BASS Trust floater Series 2006-SC1 Class A, 0.5636% 5/25/36 (c)(i) | 268,604 | 212,261 | ||

| ||||

| Principal Amount | Value | ||

Citigroup Commercial Mortgage Trust: | ||||

floater Series 2006-FL2: | ||||

Class G, 0.6063% 8/15/21 (c)(i) | $ 156,000 | $ 151,224 | ||

Class H, 0.6463% 8/15/21 (c)(i) | 125,000 | 115,406 | ||

sequential payer Series 2006-C5 Class A4, 5.431% 10/15/49 | 3,810,000 | 4,231,893 | ||

Series 2007-C6 Class A1, 5.622% 12/10/49 (i) | 3,050,935 | 3,050,069 | ||

Series 2007-FL3A Class A2, 0.4183% 4/15/22 (c)(i) | 2,595,000 | 2,445,393 | ||

Series 2008-C7 Class A2B, 6.2744% 12/10/49 (i) | 6,933,340 | 7,167,347 | ||

Citigroup/Deutsche Bank Commercial Mortgage Trust: | ||||

sequential payer Series 2007-CD4 Class A4, 5.322% 12/11/49 | 2,960,000 | 3,139,533 | ||

Series 2007-CD4 Class A3, 5.293% 12/11/49 | 6,065,000 | 6,451,025 | ||

COMM pass-thru certificates: | ||||

floater: | ||||

Series 2005-F10A: | ||||

Class G, 0.8283% 4/15/17 (c)(i) | 28,059 | 25,552 | ||

Class H, 0.8983% 4/15/17 (c)(i) | 60,000 | 50,439 | ||

Class J, 1.1283% 4/15/17 (c)(i) | 46,000 | 33,120 | ||

Series 2005-FL11: | ||||

Class F, 0.7283% 11/15/17 (c)(i) | 65,513 | 57,652 | ||

Class G, 0.7783% 11/15/17 (c)(i) | 45,227 | 39,348 | ||

sequential payer Series 2006-CN2A: | ||||

Class A2FX, 5.449% 2/5/19 (c) | 2,775,000 | 2,694,758 | ||

Class AJFX, 5.478% 2/5/19 (c) | 2,110,000 | 2,094,076 | ||

Credit Suisse Commercial Mortgage Trust: | ||||

sequential payer: | ||||

Series 2007-C2 Class A2, 5.448% 1/15/49 (i) | 3,784,098 | 3,820,648 | ||

Series 2007-C3 Class A4, 5.9037% 6/15/39 (i) | 3,750,000 | 3,936,825 | ||

Series 2006-C4 Class AAB, 5.439% 9/15/39 | 3,385,979 | 3,468,620 | ||

Series 2007-C5 Class A4, 5.695% 9/15/40 (i) | 2,750,000 | 2,869,177 | ||

Commercial Mortgage Securities - continued | ||||

| Principal Amount | Value | ||

Credit Suisse First Boston Mortgage Securities Corp.: | ||||

sequential payer Series 2004-C1: | ||||

Class A3, 4.321% 1/15/37 | $ 291,128 | $ 292,546 | ||

Class A4, 4.75% 1/15/37 | 3,035,000 | 3,179,257 | ||

Series 2001-CKN5 Class AX, 1.9234% 9/15/34 (c)(i)(j) | 4,518,716 | 6,615 | ||

Series 2002-CP3 Class G, 6.639% 7/15/35 (c) | 250,000 | 244,560 | ||

Series 2006-C1 Class A3, 5.5807% 2/15/39 (i) | 2,735,265 | 2,892,947 | ||

Credit Suisse Mortgage Capital Certificates floater Series 2007-TFL1: | ||||

Class B, 0.4283% 2/15/22 (c)(i) | 3,470,000 | 3,018,900 | ||

Class C: | ||||

0.4483% 2/15/22 (c)(i) | 657,000 | 565,020 | ||

0.5483% 2/15/22 (c)(i) | 234,000 | 198,900 | ||

Class F, 0.5983% 2/15/22 (c)(i) | 469,000 | 393,960 | ||

GE Capital Commercial Mortgage Corp. sequential payer Series 2007-C1 Class A4, 5.543% 12/10/49 | 4,470,000 | 4,704,903 | ||

Greenwich Capital Commercial Funding Corp.: | ||||

floater Series 2006-FL4 Class B, 0.4614% 11/5/21 (c)(i) | 3,490,000 | 3,363,557 | ||

sequential payer Series 2007-GG11 Class A2, 5.597% 12/10/49 | 13,805,000 | 14,163,695 | ||

Series 2006-GG7 Class A3, 6.0734% 7/10/38 (i) | 3,460,000 | 3,458,588 | ||

GS Mortgage Securities Corp. II: | ||||

floater: | ||||

Series 2006-FL8A: | ||||

Class E, 0.6403% 6/6/20 (c)(i) | 1,821,615 | 1,717,570 | ||

Class F, 0.7103% 6/6/20 (c)(i) | 294,000 | 274,356 | ||

Series 2007-EOP: | ||||

Class C, 2.1455% 3/6/20 (c)(i) | 1,335,000 | 1,293,235 | ||

Class D, 2.3636% 3/6/20 (c)(i) | 400,000 | 385,486 | ||

Class E, 2.6688% 3/6/20 (c)(i) | 670,000 | 649,039 | ||

Class F, 2.8433% 3/6/20 (c)(i) | 335,000 | 322,845 | ||

Class G, 3.0177% 3/6/20 (c)(i) | 165,000 | 159,029 | ||

Class H, 3.5846% 3/6/20 (c)(i) | 275,000 | 266,424 | ||

Class J, 4.4568% 3/6/20 (c)(i) | 395,000 | 385,644 | ||

| ||||

| Principal Amount | Value | ||

sequential payer Series 2004-GG2 Class A4, 4.964% 8/10/38 | $ 2,251,930 | $ 2,271,362 | ||

Series 2006-GG6 Class A2, 5.506% 4/10/38 | 1,649,479 | 1,660,382 | ||

GS Mortgage Securities Trust sequential payer Series 2007-GG10 Class A2, 5.778% 8/10/45 | 4,824,843 | 4,904,077 | ||

JPMorgan Chase Commercial Mortgage Securities Trust: | ||||

floater Series 2006-FLA2: | ||||

Class E, 0.5583% 11/15/18 (c)(i) | 75,668 | 65,074 | ||

Class F, 0.6083% 11/15/18 (c)(i) | 113,502 | 96,477 | ||

Class G, 0.6383% 11/15/18 (c)(i) | 98,884 | 81,085 | ||

Class H, 0.7783% 11/15/18 (c)(i) | 75,685 | 59,034 | ||

sequential payer: | ||||

Series 2006-CB14 Class A3B, 5.6772% 12/12/44 (i) | 3,821,435 | 3,918,258 | ||

Series 2006-LDP9 Class A2, 5.134% 5/15/47 (i) | 4,188,269 | 4,319,939 | ||

Series 2007-LDPX Class A3, 5.42% 1/15/49 | 3,796,000 | 4,103,670 | ||

Series 2005-LDP3 Class A3, 4.959% 8/15/42 | 3,832,500 | 3,929,623 | ||

Series 2007-CB19: | ||||

Class B, 5.9313% 2/12/49 (i) | 755,000 | 257,127 | ||

Class C, 5.9313% 2/12/49 (i) | 1,971,000 | 572,534 | ||

Class D, 5.9313% 2/12/49 (i) | 2,075,000 | 449,267 | ||

Series 2007-LDP10: | ||||

Class BS, 5.437% 1/15/49 (i) | 1,725,000 | 345,582 | ||

Class CS, 5.466% 1/15/49 (i) | 745,000 | 89,786 | ||

Class ES, 5.7317% 1/15/49 (c)(i) | 4,663,000 | 244,168 | ||

LB Commercial Conduit Mortgage Trust sequential payer Series 2007-C3 Class A4, 6.1415% 7/15/44 (i) | 3,733,000 | 4,063,091 | ||

LB-UBS Commercial Mortgage Trust: | ||||

sequential payer: | ||||

Series 2006-C1 Class A2, 5.084% 2/15/31 | 422,321 | 426,678 | ||

Series 2006-C6 Class A2, 5.262% 9/15/39 (i) | 238,446 | 238,623 | ||

Series 2007-C1: | ||||

Class A3, 5.398% 2/15/40 | 5,000,000 | 5,173,090 | ||

Class A4, 5.424% 2/15/40 | 8,620,000 | 9,392,447 | ||

Series 2007-C2 Class A3, 5.43% 2/15/40 | 1,165,000 | 1,242,658 | ||

Series 2001-C3 Class B, 6.512% 6/15/36 | 191,287 | 192,505 | ||

Commercial Mortgage Securities - continued | ||||

| Principal Amount | Value | ||

Lehman Brothers Floating Rate Commercial Mortgage Trust floater Series 2006-LLFA: | ||||

Class F, 0.6183% 9/15/21 (c)(i) | $ 402,971 | $ 333,523 | ||

Class G, 0.6383% 9/15/21 (c)(i) | 795,609 | 634,627 | ||

Class H, 0.6783% 9/15/21 (c)(i) | 204,773 | 155,149 | ||

Merrill Lynch Mortgage Trust: | ||||

sequential payer: | ||||

Series 2004-KEY2 Class A2, 4.166% 8/12/39 | 72,224 | 72,489 | ||

Series 2005-MCP1 Class A2, 4.556% 6/12/43 | 461,492 | 464,988 | ||

Series 2007-C1 Class A4, 6.0234% 6/12/50 (i) | 3,796,000 | 4,092,935 | ||

Merrill Lynch-CFC Commercial Mortgage Trust: | ||||

sequential payer: | ||||

Series 2007-5 Class A3, 5.364% 8/12/48 | 4,298,000 | 4,449,393 | ||

Series 2007-6 Class A4, 5.485% 3/12/51 (i) | 3,875,000 | 4,075,741 | ||

Series 2007-9 Class A4, 5.7% 9/12/49 | 5,500,000 | 5,853,788 | ||

Series 2006-3 Class ASB, 5.382% 7/12/46 (i) | 4,333,801 | 4,555,449 | ||

Series 2007-7 Class B, 5.9332% 6/12/50 (i) | 770,000 | 108,801 | ||

Morgan Stanley Capital I Trust: | ||||

floater: | ||||

Series 2006-XLF Class C, 1.479% 7/15/19 (c)(i) | 113,478 | 66,952 | ||

Series 2007-XCLA Class A1, 0.479% 7/17/17 (c)(i) | 95,579 | 88,171 | ||

Series 2007-XLFA: | ||||

Class D, 0.469% 10/15/20 (c)(i) | 235,000 | 213,539 | ||

Class E, 0.529% 10/15/20 (c)(i) | 294,000 | 249,510 | ||

Class F, 0.579% 10/15/20 (c)(i) | 176,000 | 133,527 | ||

Class G, 0.619% 10/15/20 (c)(i) | 218,000 | 158,851 | ||

Class H, 0.709% 10/15/20 (c)(i) | 137,000 | 79,278 | ||

Class J, 0.859% 10/15/20 (c)(i) | 80,460 | 33,116 | ||

Class NHRO, 1.169% 10/15/20 (c)(i) | 87,905 | 71,203 | ||

sequential payer: | ||||

Series 2007-HQ11 Class A31, 5.439% 2/12/44 (i) | 4,785,000 | 4,985,482 | ||

Series 2007-IQ13 Class A1, 5.05% 3/15/44 | 93,564 | 93,442 | ||

Series 2005-IQ9 Class X2, 1.21% 7/15/56 (c)(i)(j) | 14,513,936 | 14,180 | ||

| ||||

| Principal Amount | Value | ||

Series 2007-HQ12 Class A2, 5.783% 4/12/49 (i) | $ 4,450,211 | $ 4,544,974 | ||

Series 2007-IQ14 Class B, 5.9066% 4/15/49 (i) | 2,175,000 | 564,413 | ||

Providence Place Group Ltd. Partnership Series 2000-C1 Class A2, 7.75% 7/20/28 (c) | 3,235,944 | 3,355,351 | ||

Wachovia Bank Commercial Mortgage Trust: | ||||

floater: | ||||

Series 2006-WL7A: | ||||

Class E, 0.5626% 9/15/21 (c)(i) | 491,000 | 378,416 | ||

Class F, 0.6226% 9/15/21 (c)(i) | 661,000 | 489,605 | ||

Class G, 0.6426% 9/15/21 (c)(i) | 626,000 | 444,901 | ||

Class J, 0.8826% 9/15/21 (c)(i) | 139,000 | 61,258 | ||

Series 2007-WHL8: | ||||

Class AP2, 1.0783% 6/15/20 (c)(i) | 53,945 | 47,472 | ||

Class F, 0.7583% 6/15/20 (c)(i) | 1,046,000 | 679,900 | ||

sequential payer: | ||||

Series 2003-C7 Class A1, 4.241% 10/15/35 (c) | 424,082 | 426,735 | ||

Series 2007-C30: | ||||

Class A3, 5.246% 12/15/43 | 5,940,000 | 6,003,261 | ||

Class A4, 5.305% 12/15/43 | 3,240,000 | 3,384,579 | ||

Class A5, 5.342% 12/15/43 | 3,796,000 | 4,001,504 | ||

Series 2007-C31 Class A4, 5.509% 4/15/47 | 2,332,000 | 2,458,796 | ||

Series 2007-C32 Class A2, 5.9259% 6/15/49 (i) | 1,093,400 | 1,119,359 | ||

Series 2006-C23 Class A5, 5.416% 1/15/45 (i) | 3,010,000 | 3,297,572 | ||

Series 2007-C30 Class E, 5.553% 12/15/43 (i) | 6,257,000 | 1,028,651 | ||

Series 2007-C31 Class C, 5.8744% 4/15/47 (i) | 2,455,000 | 447,780 | ||

TOTAL COMMERCIAL MORTGAGE SECURITIES (Cost $255,070,566) |

| |||

Municipal Securities - 0.3% | ||||

| ||||

Beaver County Indl. Dev. Auth. Poll. Cont. Rev. Bonds (FirstEnergy Nuclear Generation Corp. Proj.) Series 2005 A, 3.375%, tender 7/1/15 (i) | 1,200,000 | 1,227,192 | ||

California Gen. Oblig. 7.5% 4/1/34 | 2,095,000 | 2,513,686 | ||

Illinois Gen. Oblig.: | ||||

Series 2010, 4.421% 1/1/15 | 2,850,000 | 2,950,064 | ||

Municipal Securities - continued | ||||

| Principal | Value | ||

Illinois Gen. Oblig.: - continued | ||||

Series 2011: | ||||

5.665% 3/1/18 | $ 1,885,000 | $ 2,006,168 | ||

5.877% 3/1/19 | 1,755,000 | 1,889,556 | ||

TOTAL MUNICIPAL SECURITIES (Cost $9,770,647) |

| |||

Foreign Government and Government Agency Obligations - 0.3% | ||||

| ||||

Brazilian Federative Republic 5.625% 1/7/41 | 1,920,000 | 2,232,000 | ||

Chilean Republic 3.25% 9/14/21 | 4,140,000 | 4,233,150 | ||

United Mexican States: | ||||

5.875% 1/15/14 | 1,665,000 | 1,798,200 | ||

6.05% 1/11/40 | 2,660,000 | 3,251,850 | ||

TOTAL FOREIGN GOVERNMENT AND GOVERNMENT AGENCY OBLIGATIONS (Cost $10,645,322) |

| |||

Supranational Obligations - 0.0% | ||||

| ||||

Corporacion Andina de Fomento 5.2% 5/21/13 | 350,000 |

| ||

Preferred Securities - 0.1% | |||

| |||

FINANCIALS - 0.1% | |||

Commercial Banks - 0.1% | |||

Credit Suisse Ltd. (Guernsey) 5.86% (d)(i) | 4,785,000 |

| |

Money Market Funds - 6.0% | |||

Shares |

| ||

Fidelity Cash Central Fund, 0.11% (a) | 227,061,250 |

| |

TOTAL INVESTMENT PORTFOLIO - 108.2% (Cost $3,947,332,007) | 4,099,341,451 | ||

NET OTHER ASSETS (LIABILITIES) - (8.2)% | (308,960,335) | ||

NET ASSETS - 100% | $ 3,790,381,116 | ||

TBA Sale Commitments | |||

| Principal | Value | |

Fannie Mae Guaranteed Mortgage pass-thru certificates | |||

3.5% 1/1/27 | $ (23,400,000) | $ (24,468,867) | |

3.5% 1/1/27 | (16,400,000) | (17,149,121) | |

4.5% 1/1/42 | (9,000,000) | (9,579,190) | |

5% 1/1/42 | (4,900,000) | (5,294,403) | |

5.5% 1/1/42 | (200,000) | (217,783) | |

TOTAL FANNIE MAE GUARANTEED MORTGAGE PASS-THRU CERTIFICATES | (56,709,364) | ||

Freddie Mac | |||

5.5% 1/1/42 | (13,700,000) | (14,856,053) | |

5.5% 1/1/42 | (13,700,000) | (14,856,053) | |

TOTAL FREDDIE MAC | (29,712,106) | ||

Ginnie Mae | |||

4% 1/1/42 | (400,000) | (429,085) | |

4% 1/1/42 | (400,000) | (429,085) | |

4% 1/1/42 | (4,000,000) | (4,290,854) | |

4.5% 1/1/42 | (100,000) | (108,982) | |

4.5% 1/1/42 | (2,500,000) | (2,724,558) | |

5% 1/1/42 | (1,700,000) | (1,883,318) | |

5% 1/1/42 | (1,700,000) | (1,883,318) | |

5% 1/1/42 | (7,600,000) | (8,419,539) | |

5% 1/1/42 | (1,000,000) | (1,107,834) | |

TOTAL GINNIE MAE | (21,276,573) | ||

TOTAL TBA SALE COMMITMENTS (Proceeds $107,292,492) | $ (107,698,043) | ||

Swap Agreements | |||||

| Expiration Date | Notional |

| ||

Credit Default Swaps | |||||

Receive monthly a fixed rate of .15% multiplied by the notional amount and pay to Credit Suisse First Boston upon each credit event of one of the issues of ABX AA 07-01 Index, par value of the proportional notional amount (Rating-C) (Upfront Premium Received/(Paid) $360,000) (h) | Sept. 2037 | $ 1,722,753 | (1,627,498) | ||

Swap Agreements - continued | |||||

| Expiration Date | Notional | Value | ||

Credit Default Swaps - continued | |||||